Embed Size (px)

Citation preview

Leader in industrial pow

er outsourcing market

Leader in industrial pow

er outsourcing market

and in green energy generation

and in green energy generation

IPO Presentation

IPO Presentation

April, 2005

April, 2005

2

�Key investment highlights

�Market and competition

�Business model and strategy

�Financial standing

�New

projects

�IPO details

Agenda

Agenda

Key investment highlights

Key investment highlights

4

�PEP is the leader in industrial power outsourcing market and in generation

& supply of green energy from

biomass

�PEP’smarket segm

ents are fast grow

ing, especially renew

able energy

�Proven track record places PEP ahead of competition

�PEP business model provides shareholders with growing and predictable cash

flow

sKey investment highlights

Key investment highlights

Market and com

petition

Market and com

petition

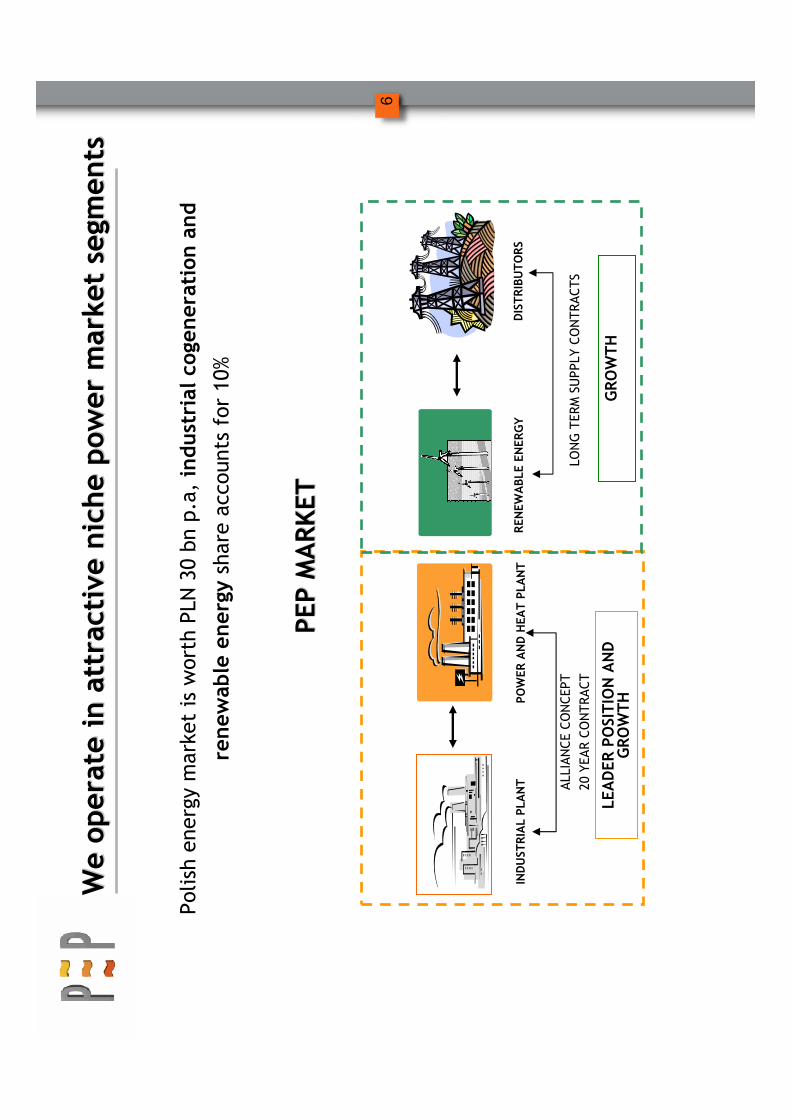

6

We operate in attractive niche pow

er market segm

ents

We operate in attractive niche pow

er market segm

ents

Polish energy market is worth PLN 30bn

p.a, industrial cogeneration and

renewable energyshare accounts for 10%

PEP MARKET

PEP MARKET

POWER AND HEAT PLANT

REN

EWABLE ENERGY

GROWTH

LEADER POSITION AND

GROWTH

INDUSTRIAL PLANT ALLIANCE CONCEPT

20 YEAR CONTRACT

LONG TERM SUPPLY CONTRACTS

DISTRIBUTORS

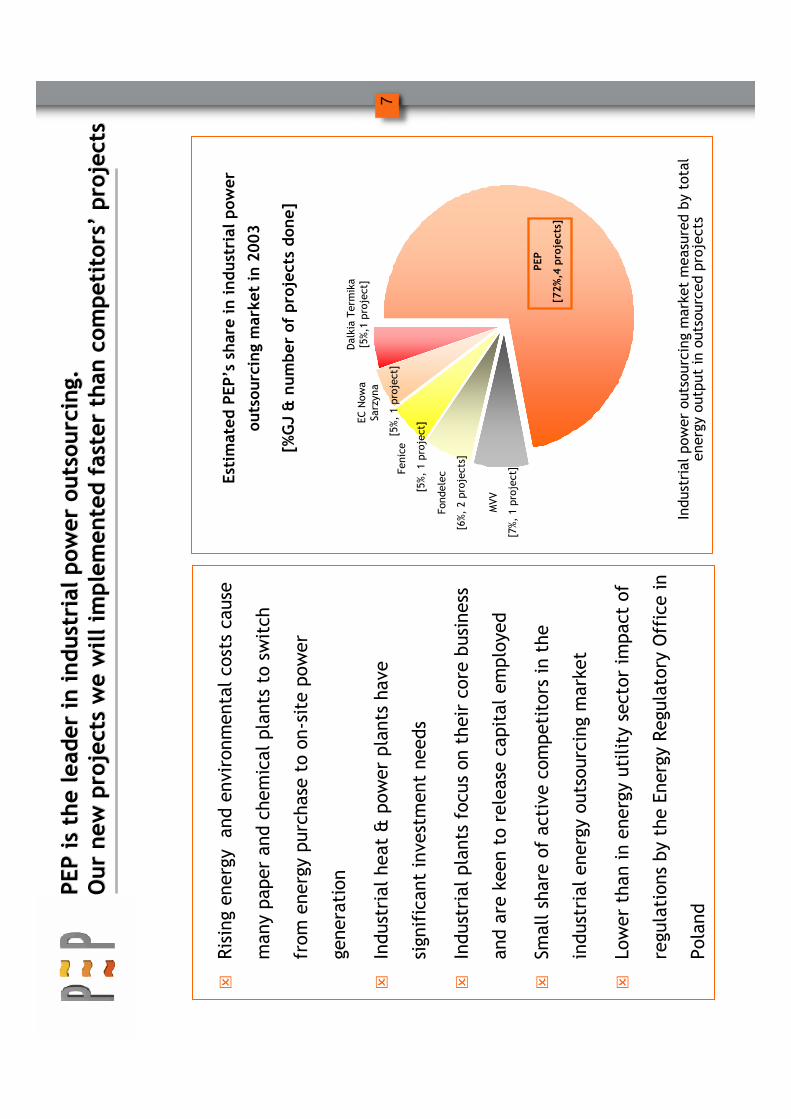

7

PEP is the leader in industrial pow

er outsourcing.

PEP is the leader in industrial pow

er outsourcing.

Our new projects we will implemented faster than com

petitors

Our new projects we will implemented faster than com

petitors’’projects

projects

�Rising energy and environm

ental costs cause

many paper and chem

ical plants to switch

from

energy purchase to on-site power

generation

�Industrial heat & pow

er plants have

significant investment needs

�Industrial plants focus on their core business

and are keen to release capital em

ployed

�Sm

all share of active competitors in the

industrial energy outsourcing market

�Lower than in energy utility sector impact of

regulations by the Energy Regulatory Office in

Poland

EstimatedPEP’sshare in industrial pow

er

outsourcing market in 2003

[%GJ & number of projects done]

PEP

[72%,4 projects]

Fondelec

[6%, 2 projects]

Fenice

[5%, 1 project]

ECNow

a Sarzyna

[5%, 1 project]

Dalkia Termika

[5%,1 project]

MVV

[7%, 1 project]

Industrial pow

er outsourcing market measured by total

energy output in outsourced projects

8

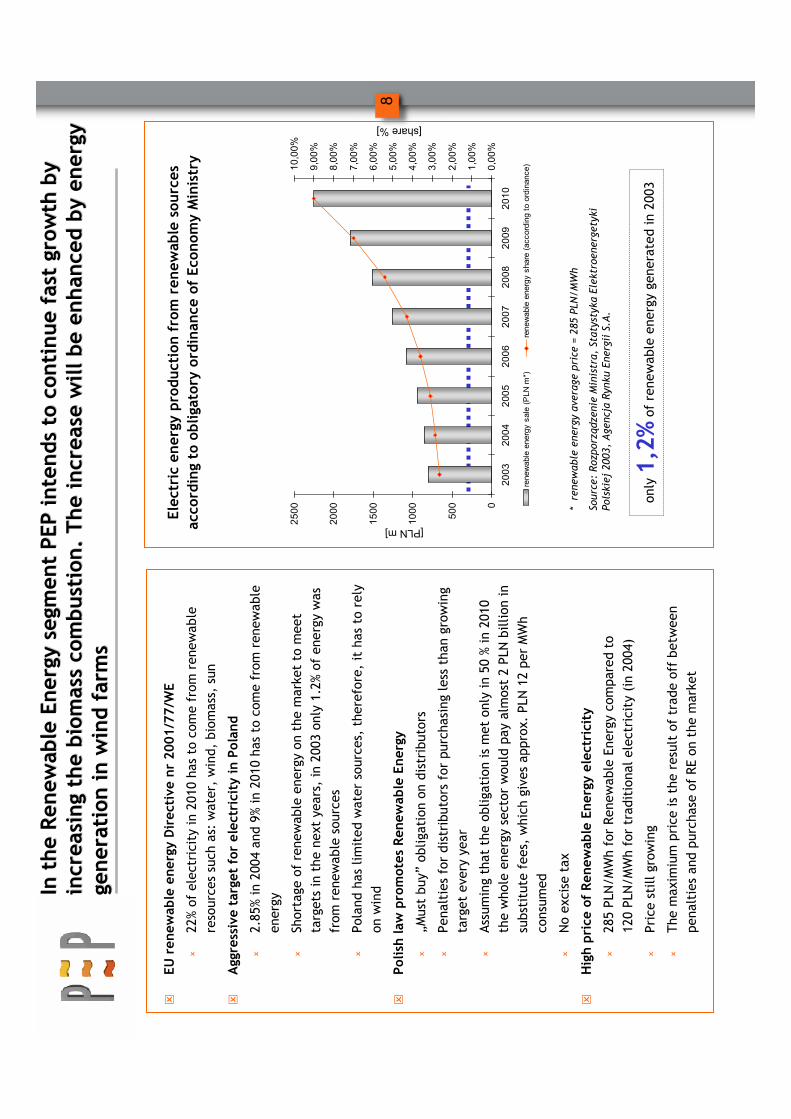

�EU

renewable energy Directive nr 2001/77/W

E

�22% of electricity in 2010 has to com

e from

renew

able

resources such as: water, wind, biomass, sun

�Aggressive target for electricity in Poland

�2.85% in 2004 and 9% in 2010 has to come from

renew

able

energy

�Shortage of renewable energy on the market to meet

targets in the next years, in 2003 only 1.2% of energy was

from

renew

able sources

�Poland has limited water sources, therefore, it has to rely

on wind

�Polish law

promotes Renewable Energy

�„Must buy”

obligation on distributors

�Penalties for distributors for purchasing less than growing

target every year

�Assum

ing that the obligation is met only in 50 % in 2010

the whole energy sector would pay almost 2 PLN billion in

substitute fees, which gives approx. PLN 12 perMWh

consum

ed

�No excise tax

�High price of Renewable Energy electricity

�285 PLN/MWhfor Renew

able Energy compared to

120 PLN/MWhfor traditional electricity (in 2004)

�Price still growing

�The

maximiumprice is the result of trade off between

penalties and purchase of RE on the market

In the Renewable Energy segm

ent PEP intends to continue fast gro

In the Renewable Energy segm

ent PEP intends to continue fast growth by

wth by

increasing the biomass combustion. The increase will be enhanced

increasing the biomass combustion. The increase will be enhancedby energy

by energy

generation in wind farms

generation in wind farms

Electric energy production from renewable sources

according to obligatory ordinance of Economy Ministry

0

500

1000

1500

2000

2500

2003

2004

2005

2006

2007

2008

2009

2010

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

10,00%

renewable energy sale (PLN m

*)renewable energy share (according to ordinance)

[PLN m]

[share %]

* renewable energy average price

= 285 PLN/MWh

Source:Rozporządzenie M

inistra,Sta

tystyka Elektroenergetyki

Polskiej2003,Agencja Rynku EnergiiS.A

.

only 1,2%

ofrenewable energy generated in 2003

Business model and strategy

Business model and strategy

10

Nov 1998PEP is successfully managing five facilities and is the leader i

PEP is successfully managing five facilities and is the leader i n industrial pow

er

n industrial pow

er

outsourcing and generation of renewable energy from

biomass

outsourcing and generation of renewable energy from

biomass

Jan 2001

June 2001

May 2002March 2004

July 2004

July 2004March 2005

Wind pow

er development j.v.with EPA

Start of CFB Boiler in Saturn

Contract withWałbrzych

Coke Mill

Mercury (Wałbrzych) in operation

CHP Saturn in operation

New

investor-PolenergyInvestments B.V. CHPJeziornain operation

CHPZakrzówin operation

Oct 2000 CHPWizówin operation

Contract withWizów

chem

ical plant

Establishing PEP; first investor-Enterprise Investors

Contract with Polar

July 1999

Nov 2000

Contract withMetsaTissue

April 2002

Contract withMondiPackaging PaperŚw

iecie

July 1998

July 1997

June 2005

CHPJeziornaoperation extension

11

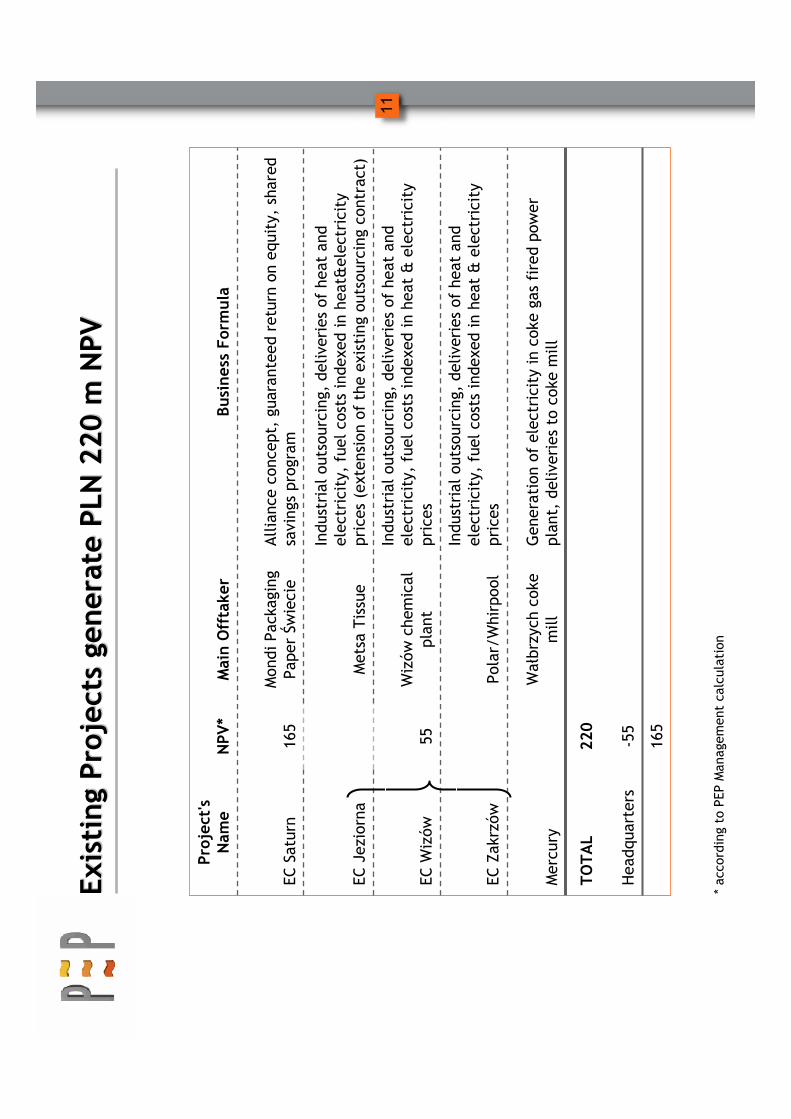

Existing Projects generate PLN 220 m NPV

Existing Projects generate PLN 220 m NPV

Industrial outsourcing, deliveries of heat and

electricity, fuel costs indexed in heat&electricity

prices (extension of the existing outsourcing contract)

MetsaTissue

EC Jeziorna

165

-55

Headquarters

220

TOTAL

Generation of electricity in coke gas fired pow

er

plant, deliveries to coke mill

Wałbrzych

coke

mill

Mercury

Industrial outsourcing, deliveries of heat and

electricity, fuel costs indexed in heat & electricity

prices

Polar/Whirpool

ECZakrzów

Industrial outsourcing, deliveries of heat and

electricity, fuel costs indexed in heat & electricity

prices

Wizów

chem

ical

plant

55EC

Wizów

Alliance concept, guaranteed return on equity, shared

savings program

MondiPackaging

PaperŚwiecie

165

EC Saturn

Business Formula

MainOfftaker

NPV*

Project's

Nam

e

* according to PEP Managem

ent calculation

12

In 2002

In 2002PEP took over the MPP

PEP took over the MPP ŚŚwiecie

wiecieheat and pow

er plant

heat and pow

er plant

�MondiPackaging PaperŚwiecieS.A. (formerFrantschach ŚwiecieS.A.), in order to

reduce the energy cost in the total manufacturing costs, had to build a boiler

combusting biom

ass coming from

the paper production process. The

planned

investment was supposed to amount to app. EUR 45 million.

�Simultaneously, MPP

Świeciewas implem

enting an investment program within its

core business, i.e. paper production, totaling EUR 180 million

�In the light of considerable investments in the core business, the com

pany could

not and did not want to make such important investments in the heat and pow

er

plant

13

�In order to implem

ent the necessary investments and reduce energy costs, the

Board of Directors made a decision on outsourcing the combined heat and pow

er

plant

�One of the essential tender terms was to come up with a co-operation model in

which MPP

Świecieretains the strategic control over the separated heat and power

plant, implem

entation of the investment program and cost reduction

�PEP proposed the so called Alliance Concept, a co-operation model which met all

the requirem

ents offering the best technical solutions and cost reduction

In 2002, PEP took over the MPP

In 2002, PEP took over the MPP ŚŚwiecie

wiecieheat and pow

er plant

heat and pow

er plant

14

�20 year contract

�PEP to implem

ent a jointly agreed investment program

�Continuous reduction of heat and electricity costs

�System

of mutual settlements based on the “open-book”principles and incurring by the

custom

er the macro risks, including FX rate risk related to debtservice and purchase of raw

materials

�For PEP, the safe and predictable IRR in long term, at the minimum level of 16% depends on:

�capital invested,

�quality of operating services,

�cost reduction level and

�ROCE of MPP

Świecie

and does not depend on the energy sales volum

e

�The benefits from

the mutual savings program are to be split between PEP and MPP

Świecie

The Alliance Concept with MPP

The Alliance Concept with MPP ŚŚwiecie

wiecieassumes:

assumes:

15

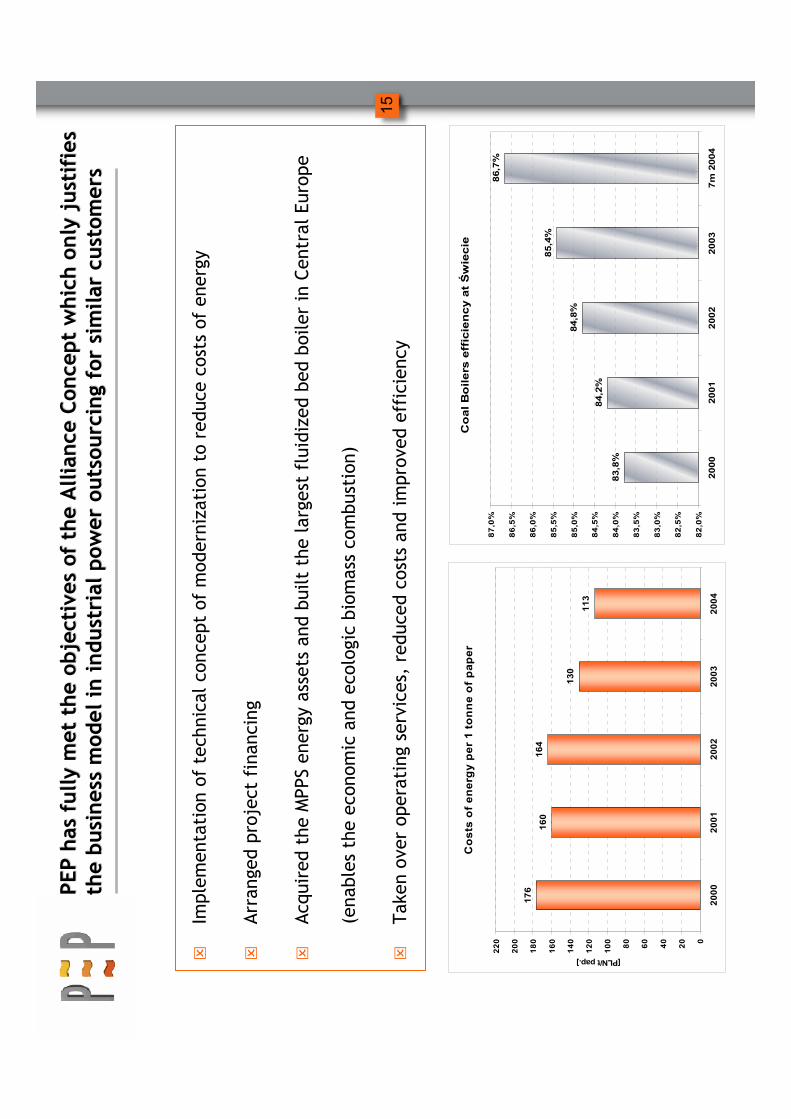

�Implem

entation of technical concept of modernization to reduce costs of energy

�Arranged project financing

�Acquired the MPPS energy assets and built the largest fluidized bed boiler in Central Europe

(enables the economic and ecologic biom

ass combustion)

�Taken overoperatingservices, reduced costs and improved efficiency

Costs of energy per 1 tonne of paper

176

160

164

130

113

0

20

40

60

80

100

120

140

160

180

200

220

2000

2001

2002

2003

2004

[PLN/t pap.]

Coal Boilers efficiency at Świecie

83,8%

84,2%

84,8%

85,4%

86,7%

82,0%

82,5%

83,0%

83,5%

84,0%

84,5%

85,0%

85,5%

86,0%

86,5%

87,0%

2000

2001

2002

2003

7m 2004

PEP has fully met the objectives of the Alliance Concept which o

PEP has fully met the objectives of the Alliance Concept which only justifies

nly justifies

the business model in industrial pow

er outsourcing for similar c

the business model in industrial pow

er outsourcing for similar custom

ers

ustom

ers

16

�Better use of new CFB, increased use of biomass by 50% and increased electricity

generation

–PLN 2 m pa, as forecast for 2005

�Higher efficiency, better autom

ation, low

er costs of central purchasing, lower

environm

ental fees, head count reduction at other PEP sites. Potential saving

for PEP (average from 2004 –2008): PLN 1.0 –1.3 m pa

�CO2em

ission trading

In addition there are

In addition there are

futher

futheropportunities to reduce costs and

opportunities to reduce costs and

increase profits from sharing ten benefits

increase profits from sharing ten benefits

17

Alliance Concept allows to reduce som

e risks

Alliance Concept allows to reduce som

e risks

XCost of credit

XService and

Modernizations

XEnvironm

ental

costs

XCustomer financial

standing

XEquipm

ent

efficiency

XChange in Law and

Regulations

XFuel price

increase

Custom

er

Pow

er

plant

Typical risk Profile

PEP risk Profile

XX

Cost of credit and

debt risk

XService and

Modernizations

XEnvironm

ental

costs

XCustomer

financial standing

XEquipm

ent

efficiency

XChange in Law

and Regulations

XFuel price

increase

Custom

er

PEP

Who bears the risks?

18

�Our contracts with key clients are for 20 years

�Our clients are healthy local com

panies

with good financial outlook, mainly

operating in paper, chem

ical and petrochem

ical industry

�Our business structure transfers the macroeconom

ic risk (e.g. changes in fuel price)

to the customers through agreed „pass through”mechanism or indexation formula

�Our business structure assures good return on invested equity through leverage and

contract formulas

�Our know-how

assures excellent operational results –lower energy costs for our

clientsAlliance Concept allows to generate stable and predictable cash

Alliance Concept allows to generate stable and predictable cash

flow

sflow

s

19

�Add two new projects in the industrial outsourcing in Poland

�Increase biomass renewable energy generation from 187,000

MWhto 258,000

MWhin Poland

�Operate 22 MW wind farms and start the construction of the additional 50 MW

�Win two industrial outsourcing projects in the Central and Eastern European

markets

Strategic milestones for 2005

Strategic milestones for 2005-- 2006 will further create value

2006 will further create value

Strategic goals

Financial standing

Financial standing

21

Key financial inform

ation

Key financial inform

ation

64 764

52 926

65 584

65 195

34 226

Operational revenue

with interests from

leased assets

40 325

26 449

8 627

2004

144 747

40 954

9 012

2005

Forecast

108 332

126 000

2 088

Capital expenditure

25 704

18 126

-3 718

Adjusted cash flow

from

operations*

6 766

14 249

-11 044

Net profit

2003

2002

2001

[‘000 PLN]

* NOTE: Cash

flow fro

m operations pre

sente

d w

ith equity and debt servicepayments disclosed

in oth

er investment in flows section of CFnet off investment VAT rece

ivables

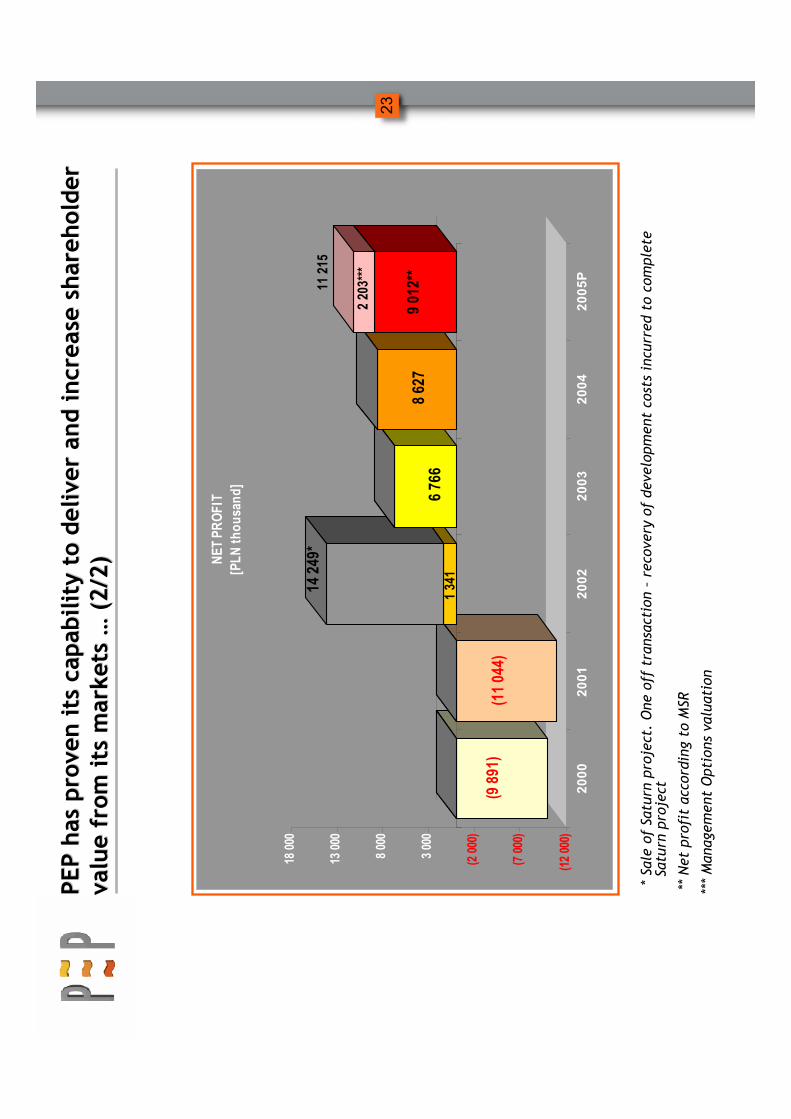

22

PEP has proven its capability to deliver and increase shareholde

PEP has proven its capability to deliver and increase shareholder r

value from its markets

value from its markets……(1/2)

(1/2)

NOTE: Cash

flow fro

m operations pre

sente

d w

ith equity and debt servicepayments disclosed

in oth

er investment in flows section of CFand net off investment VAT rece

ivables

(5 6

41)

(3 7

18)

18 1

26

25 7

04

26 4

49

40 9

54

(6 00

0)(1

000)

4 000

9 000

14 00

019

000

24 00

029

000

34 00

039

000

44 00

0

2000

2001

2002

2003

2004

2005P

AD

JUS

TED

CA

SH

FLO

W F

RO

M O

PER

ATIO

NS

[PLN

thousa

nd]

23

PEP has proven its capability to deliver and increase shareholde

PEP has proven its capability to deliver and increase shareholder r

value from its markets

value from its markets……(2/2)

(2/2)

*Sale

of Satu

rn pro

ject. One off transaction –

reco

very of development co

sts incu

rred to complete

Satu

rn pro

ject

** Net pro

fit accord

ing to M

SR

*** Management Options valuation

3 00

0

8 00

0

13 0

00

18 0

00

NE

T P

RO

FIT

(9 8

91)

(11 0

44)

14

249*

6 7

668

627

9 01

2**

2 20

3***

(12

000)

(7 0

00)

(2 0

00)

3 00

0

8 00

0

13 0

00

18 0

00

2000

2001

2002

2003

2004

2005P

NET

PR

OFIT

[PLN

thousa

nd]

1 34

1

11 2

15

24

Net margine

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

18,0%

EC Bed

zin

Kogen

eracja

MPEC W

rocław

Praterm

PEP

2003

2004

Source: WSE, PEP

Return on equity

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

8,0%

9,0%

10,0%

EC Bedzin

Kogeneracja

MPEC W

rocław

Praterm

PEP

2003

2004

We have better than average profitability and higher return on e

We have better than average profitability and higher return on equity

quity

25

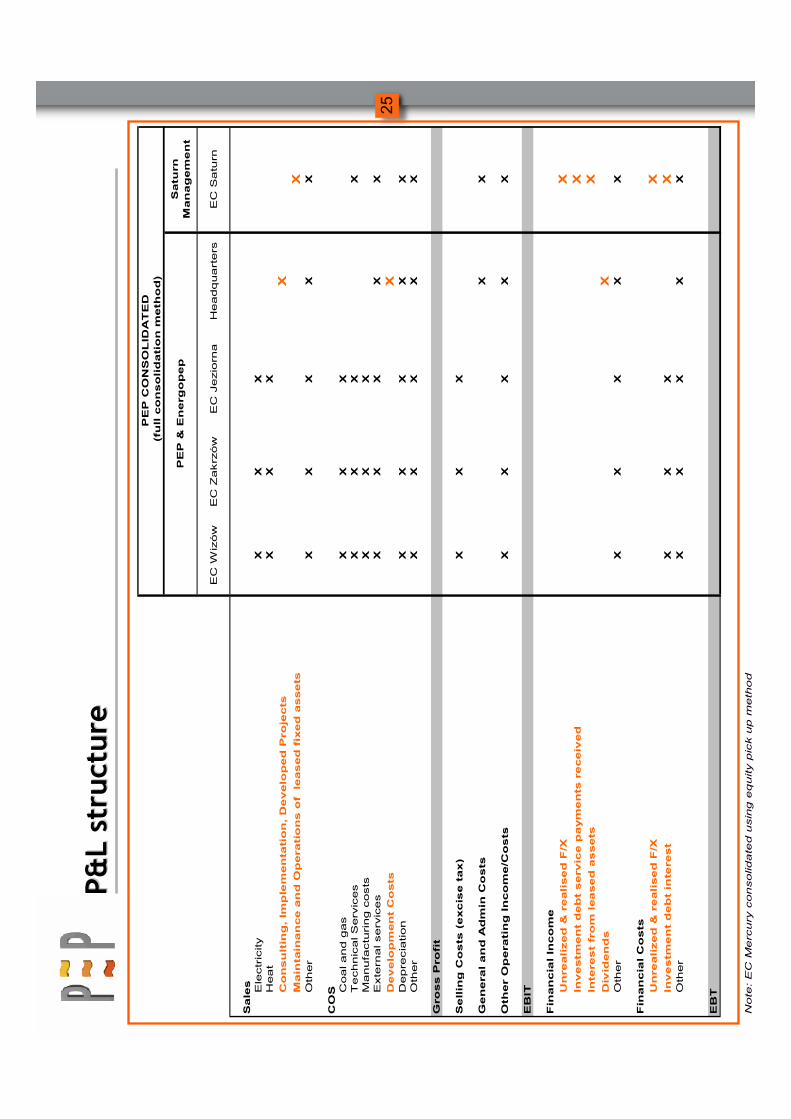

P&L structure

P&L structure

Saturn

Management

EC W

izów

EC Zakrzów

EC Jeziorna

Headquarters

EC Saturn

SalesElectricity

XX

XHeat

XX

X

Consulting, Im

plementation, Developed Projects

XMaintainance and Operations of leased fixed assets

XOther

XX

XX

X

COS Coal and gas

XX

XTechnical Services

XX

XX

Manufacturing costs

XX

XExternal services

XX

XX

X

Development Costs

XDepreciation

XX

XX

XOther

XX

XX

X

Gross Profit

Selling Costs (excise tax)

XX

X

General and Admin Costs

XX

Other Operating Income/Costs

XX

XX

X

EBIT

Financial Income

Unrealized & realised F/X

XInvestm

ent debt service payments received

XInterest from leased assets

XDividends

XOther

XX

XX

X

Financial Costs

Unrealized & realised F/X

XInvestm

ent debt interest

XX

XX

Other

XX

XX

X

EBT

Note: EC Mercury consolidated using equity pick up method

PEP & Energopep

PEP CONSOLIDATED

(full consolidation m

ethod)

New projects

New projects

27

Recently acquired projects will be financed from own cash flows

Recently acquired projects will be financed from own cash flows

and will generate additional NPV of PLN 57 m

and will generate additional NPV of PLN 57 m

Development services, no capital invested

Arctic Paper

Kostrzyń

3APK

57TOTAL

Production of green electricity based on

long term pow

er purchase agreem

ent

with indexed electricity price

Electricity

Distributors

28Wind Farm

Alliance concept, guaranteed return on

equity,shared savings program

MondiPackaging Paper

Świecie

25EC Jupiter

(Saturn

extension)

Business Formula

MainOfftaker

NPV*

Project's

Nam

e

* according to PEP Managem

ent calculation

28

Puck wind farm

Puck wind farm --project rationale

project rationale

�Planned 22 MW wind farm will be situated in potentially one of the best places

in Poland

�Wind farms generally contribute average IRR of 16%-20%

�High wind productivity, low grid connection costs and growing green energy

prices in Puck wind farm place the expected IRR in the higher end of the bracket

Planned location

of Puck wind farm

29

Puck wind farm

Puck wind farm ––project progress against key milestones

project progress against key milestones

�Wind resources assessment

and electricity generation

forecast (confirmation in

progress)

�Changes in spatial planning

plan

�Environm

ental impact

assessment report

�Lease agreem

ents

�Grid connection agreement

�Technical design

�Building permit

�Prom

issorylicencefor energy

generation

DEVELO

PMEN

T

IMPLEMEN

TATION

DEVELO

PMEN

T

ACTIONS COMPLETED

IN PROGRESS

SEPTEM

BER 2005

�Power purchase agreem

ent –

April 2005 (LOI signed in

March 2005)

�EPC contract –June 2005

�Financial closure –June

2005

�Com

mencement of

construction of wind

farm

30

�The essence of the project is to invest in a new turbine which will allow the

CHPoptimalisation(low

er cost of energy generation) and increase the

renewable energy production (additional revenues from

green energy sales)

�PEP’sbenefits will come mainly from

equity service paym

ents and additional

green energy generation

Jupiter

Jupiter ––project rationale

project rationale

31

Jupiter

Jupiter ––project progress against key milestones

project progress against key milestones

�Tendering process –presentation

of short list –1st week of April

2005

�Approval of the project by MPPS –

3rd week of April 2005

DEVELO

PMEN

T

IMPLEMEN

TATION

DEVELO

PMENT

ACTIONS COMPLETED

IN PROGRESS

July2005

�Negotiations with banks

�Financing agreem

ents signed –

May 2005

�Negotiations with turbine

manufacturers

�Key contracts signed –

1st week of June 2005

�Estimated start-up of

new turbine

construction

32

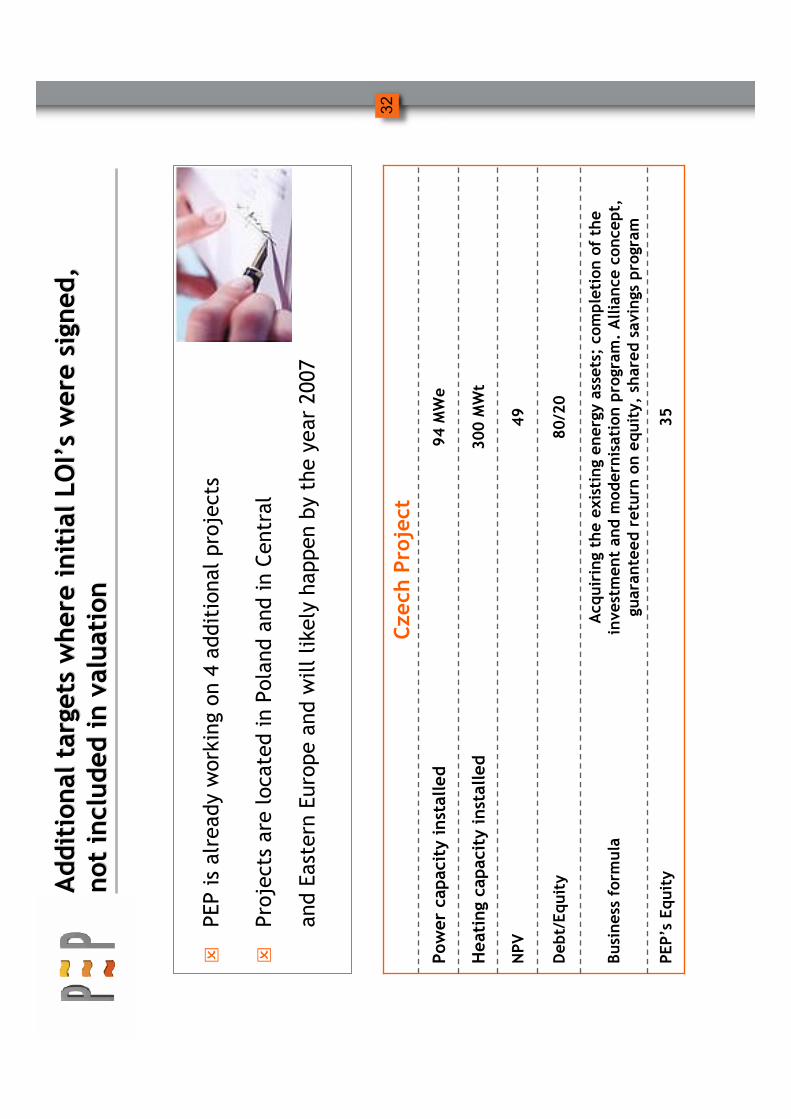

�PEP is already working on 4 additional projects

�Projects are located in Poland

and in Central

and Eastern Europe and will likely happen by the year 2007

Additional targets where initial

Additional targets where initialLO

ILO

I ’’sswere signed,

were signed,

not included in valuation

not included in valuation

94MWe

Pow

er capacity installed

300MWt

Heating capacity installed

35

PEP’sEquity

Acquiring the existing energy assets; completion of the

investment andmodernisationprogram

. Alliance concept,

guaranteed return on equity, shared savings program

Business formula

80/20

Debt/Equity

49

NPV

Czech Project

33

�PEP is the leader in industrial power outsourcing market and in generation

& supply of green energy from

biomass

�PEP’smarket segm

ents are fast grow

ing, especially renew

able energy

�Proven track record places PEP ahead of competition

�PEP business model provides shareholders with growing and predictable cash

flow

sKey investment highlights

Key investment highlights

IPO details

IPO details

35

�Public Offering: 10 651 440 shares offered byPEP’sshareholders:

�PolenergyInvestments B.V –6 151 440 shares (all shares owned)

�Polish Enterprise Fund, L.P.* –4 500 000 shares (from

10 605 768 ow

ned)

�Tranches:

�InstitutionalTranche: 80% public offering –8 521 152 shares

�RetailTranche: 20% public offering –2 130 288 shares

Offering

Offering

* Polish Enterprise Fund, L.P. is represented by Enterprise Investors Sp. z o. o.

36

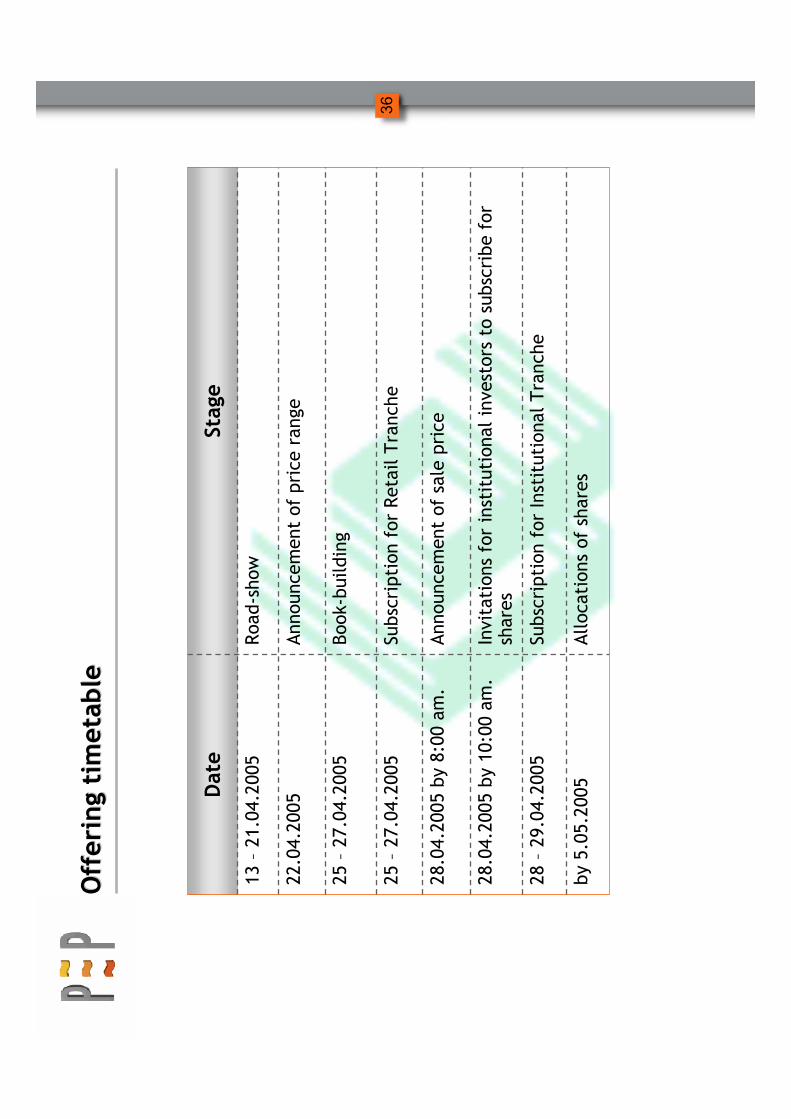

Offering timetable

Offering timetable

Allocations of shares

by 5.05.2005

Subscription for InstitutionalTranche

28 –29.04.2005

Invitations for institutional investors to subscribe for

shares

28.04.2005 by 10:00 am

.

Announcem

ent of sale price

28.04.2005 by 8:00 am.

Subscription for RetailTranche

25 –27.04.2005

Book-building

25 –27.04.2005

Announcem

ent of price range

22.04.2005

Road-show

13 –21.04.2005

Stage

Date

37

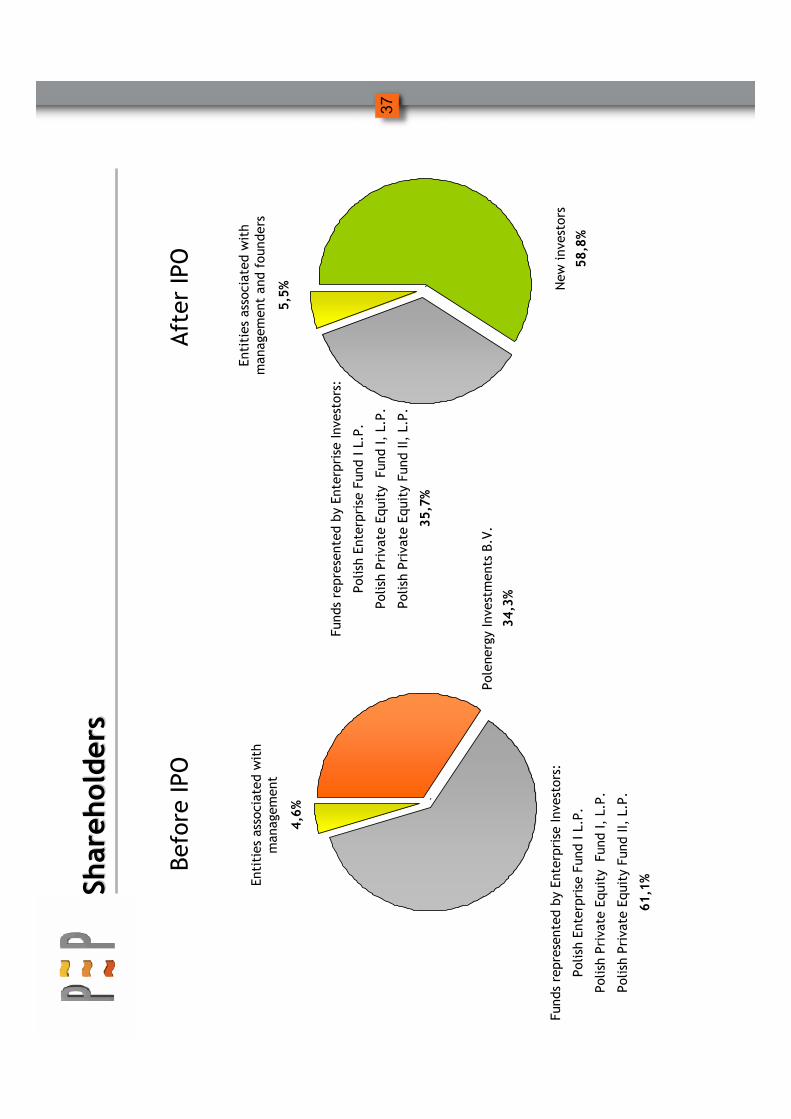

Shareholders

Shareholders

`

PolenergyInvestments B.V.

34,3%

Before IPO

After IPO

` New

investors

58,8%

Funds represented by Enterprise Investors:

Polish Enterprise Fund I L.P.

Polish Private Equity Fund I, L.P.

Polish Private Equity Fund II, L.P.

61,1%Entities associated with

managem

ent

4,6%

Funds represented by Enterprise Investors:

Polish Enterprise Fund I L.P.

Polish Private Equity Fund I, L.P.

Polish Private Equity Fund II, L.P.

35,7%

Entities associated with

managem

ent and founders

5,5%

38

Appendix

39

Quick Response by Leaders to rising energy costs and Green Electricity opportunity

Other recent projects in Industry (announced project only in Janand Feb 2005)

Replace

oil

Biom

ass

+Oil

145 MW

Includes

installatio

n of back

pressure

turbines

115

Mills areGruvon,

KarlsborgandSkarblacka

Billerud

A.B.

Bark wood

waste

Boiler

ArkhangelskPulp and

Paper Mill, Russia **

Replace

gas + oil

Biom

ass

Boiler

Stam

bolijski, Bulgaria *

PFS

Contract

with grid

Biofuels

sludge

20 MW

85 MW

Boiler +

turbine

75Chapelle Darblay, France

UPM

Varo, Sweden

Biofuels

sludge

81 MW

Turbines

50Monsteras, Sweden

Sodra

Replaced

coal fired

boiler

Bark peat

Forest

residue

sludge

107 MW

Increase

steam and

electricity

BFR

20Rauma, Finland

UPM

Remarks

Fuel

Capacity

Project

Investment

Location

Co

* sells carbon credits toNetherlandEm

ission Reduction Co up found

** expects Emission Trading to EU and generating 22 to EURO 25 million

Industry is reacting to rising energy costs

Industry is reacting to rising energy costs

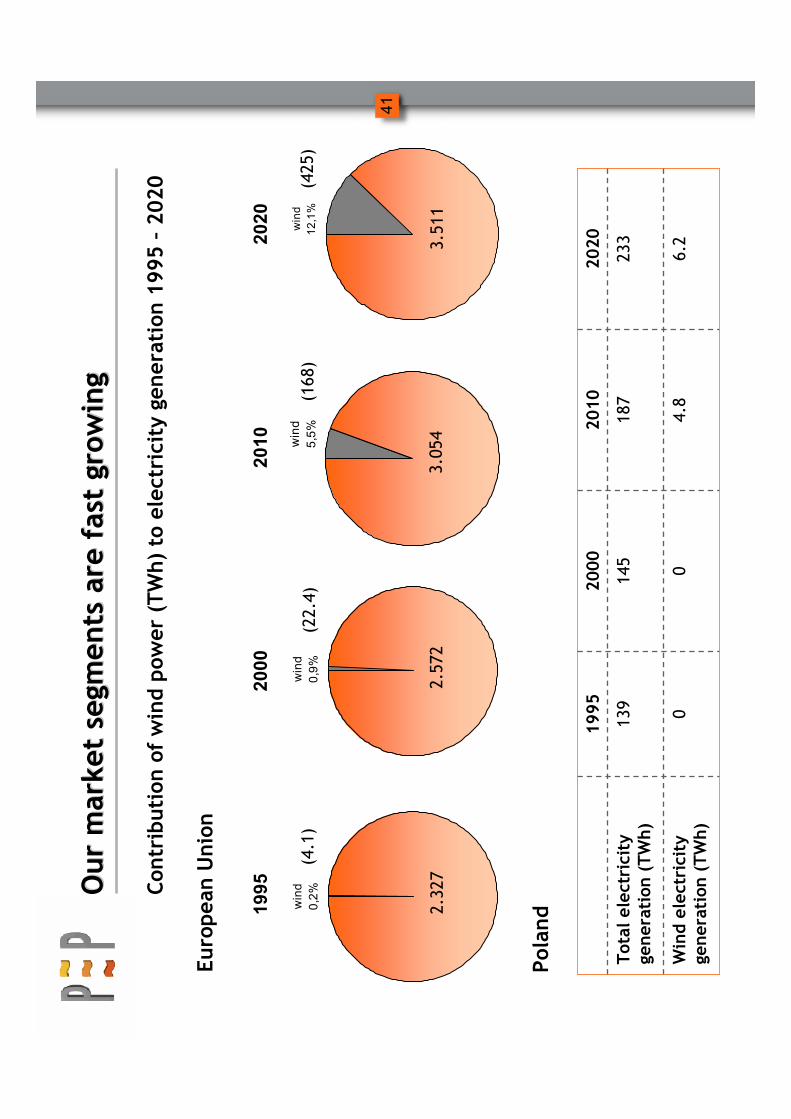

40

wind

12,1%

wind

0,2%

wind

0,9%

wind

5,5%

1995

2000

2010

2020

2.327

2.572

3.054

3.511

(4.1)

(22.4)

(168)

(425)

European Union

Poland wind

0,0%

139

(0.0)

wind

0,0%

145

(0.0)

wind

2,6%

187

(4.8)

wind

2,7%

233

(6.2)

Our market segm

ents are fast grow

ing

Our market segm

ents are fast grow

ing

Contribution of wind pow

er (TWh) to electricity generation 1995 –2020

41

Our market segm

ents are fast grow

ing

Our market segm

ents are fast grow

ing

4.8

187

2010

6.2

00

Wind electricity

generation (TWh)

233

145

139

Total electricity

generation (TWh)

2020

2000

1995

Contribution of wind pow

er (TWh) to electricity generation 1995 –2020

Polandw

ind

0,2%

wind

0,9%

wind

5,5%

wind

12,1%

1995

2000

2010

2020

2.327

2.572

3.054

3.511

(4.1)

(22.4)

(168)

(425)

European Union

42

EUR 2.9 m*

Financing arranged by PEP

EUR 0.8 m*

Equity contributed

20 years

Length of contract

PGNiG

Fuel supplier

Wizów

SAOfftaker

Gas-fired CHP

plant,

cogeneration

Technology

42MWt

Heating capacity installed

4Mwe

Power capacity installed

1999

Operation beginning

Key data

Com

pleted projects

Com

pleted projects

ECWizów

1999

1 EUR=4.1318 PLN (NBP average exch

ange rate

,

15.04.2005)

43

EUR 3.3 m*

Financing arranged by PEP

EUR 1.5 m*

Equity contributed

20 years

Length of contract

PGNiG

Fuel supplier

Polar S.A.

(Whirlpool Group)

Offtaker

Gas-fired CHP

plant,

cogeneration

Technology

36MWt

Heating capacity installed

3Mwe

Power capacity installed

2000

Operation beginning

Key data

ECZakrzów2000

Com

pleted projects

Com

pleted projects

*1 EUR=4.1318 PLN (NBP average exch

ange rate

,

15.04.2005)

44

n/a**

(debt financing

EUR 1.1 m* in

2005)

Financing arranged by PEP

EUR 0.5 m*

(additional equity

EUR 0.8 m in 2005)

Equity contributed

5 years

(extended in 2005

for the next 11

years)

Length of contract

Dom

estic coal

mines

Fuel supplier

MetsaTissue

Offtaker

Coal-fired CHP

plant,

cogeneration

Technology

95MWt

Heating capacity installed

6Mwe

Power capacity installed

2001

Operation beginning

Key data

* *lease agre

ement

ECJeziorna2001

Com

pleted projects

Com

pleted projects

*1 EUR=4.1318 PLN (NBP average exch

ange rate

,

15.04.2005)

45

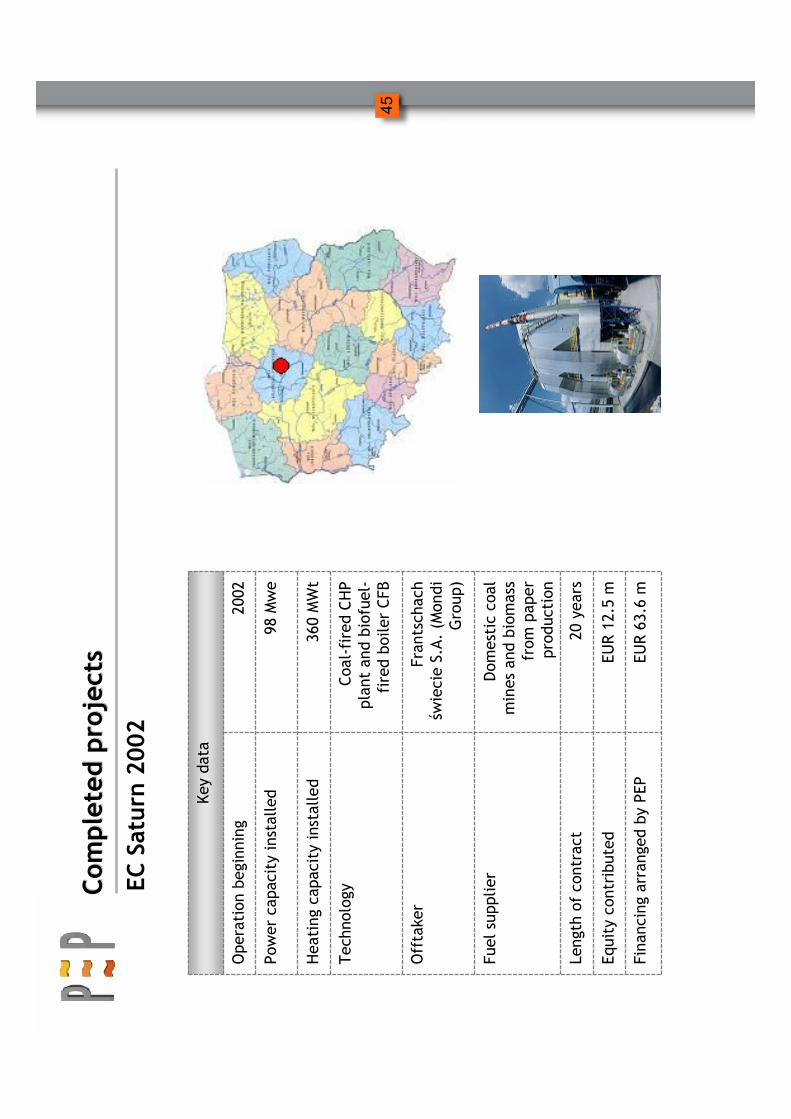

EUR 63.6 m

Financing arranged by PEP

EUR 12.5 m

Equity contributed

20 years

Length of contract

Dom

estic coal

mines and biomass

from

paper

production

Fuel supplier

Frantschach

świecieS.A. (Mondi

Group)

Offtaker

Coal-fired CHP

plant andbiofuel-

fired boiler CFB

Technology

360MWt

Heating capacity installed

98Mwe

Power capacity installed

2002

Operation beginning

Key data

EC Saturn 2002

Com

pleted projects

Com

pleted projects

46

�EPA –leading developer of wind farms in Poland

�Negotiations started in 2003, concluded in 2004

�3-year agreement, providing for sharing costs and

profits from

wind farm development

�PEP granted the right of first refusal for all farms

developed on the basis of the agreem

ent

�PEP plans to acquire and build at least 100 MW

over the next 5 years

�Both parties plan to renew

the agreement after the

first 3-year period

Wind project development j.v.with EPA 2004

Projects in progress

Projects in progress

47

EUR 2.2 m*

Financing arranged by PEP

EUR 0.8 m*

Equity contributed

6+4 years

Length of contract

Zakłady

Koksownicze

Wałbrzych

S.A.

(Coke Plant

Walbrzych)

Fuel supplier

Zakłady

Koksownicze

Wałbrzych

S.A.

(Coke Plant

Walbrzych)

Offtaker

Coke gas-fired

Power Plant

Technology

0MWt

Heating capacity installed

8.3Mwe

Power capacity installed

2005

Operation beginning

Key data

Mercury 2004

Projects in progress

Projects in progress

*1 EUR=4.1318 PLN (NBP average exch

ange rate

,

15.04.2005)

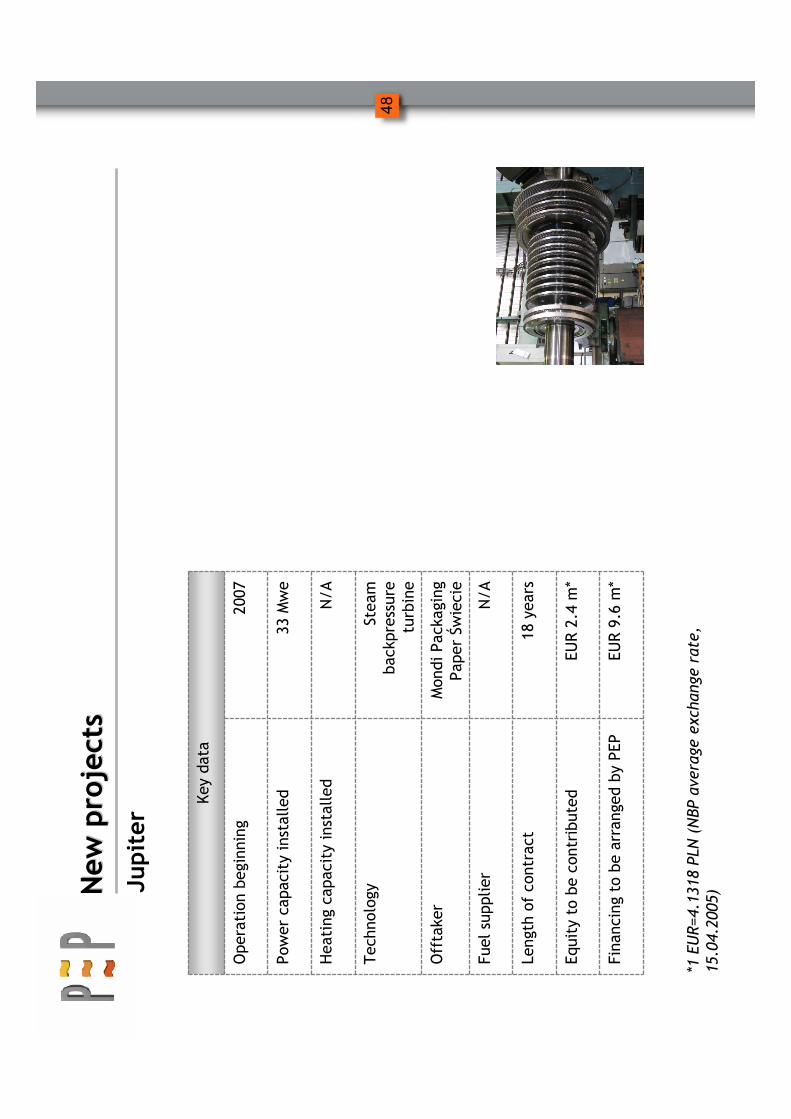

48

EUR 9.6 m*

Financing to be arranged by PEP

EUR 2.4 m*

Equity to be contributed

18 years

Length of contract

N/A

Fuel supplier

MondiPackaging

PaperŚwiecie

Offtaker

Steam

backpressure

turbine

Technology

N/A

Heating capacity installed

33Mwe

Power capacity installed

2007

Operation beginning

Key data

Jupiter

New projects

New projects

*1 EUR=4.1318 PLN (NBP average exch

ange rate

,

15.04.2005)

49

New projects

New projects

EUR 19.0 m*

Financing to be arranged by

PEP

EUR 5.7 m*

Equity to be contributed

20 years

Length of contract

N/A

Fuel supplier

Electricity

distributors

Offtaker

Wind turbines

Technology

N/A

Heating capacity installed

22Mwe

Power capacity installed

2006

Operation beginning

Key data

Wind Farm #1

*1 EUR=4.1318 PLN (NBP average exch

ange rate

,

15.04.2005)

50

Selected

Selectedfinancial inform

ation

financial inform

ation

2002

2003

2004

Key operational data

Production of heat

['000 GJ]

4 870

6 330

7 530

Production of electricity

['000 MWh]

449,9

474,7

520,6

Profit & loss

Revenues

['000 PLN]

63 353

60 665

50 103

Revenues growth

--4,2%

-17,4%

Gross profit

['000 PLN]

21 866

21 674

18 869

Gross profit growth

--0,9%

-12,9%

EBITDA

['000 PLN]

14 275

1 681

18 803

EBITDA growth

--88,2%

1018,6%

EBITDA m

argin

22,5%

2,8%

37,5%

Depreciation

['000 PLN]

2 663

2 841

2 191

EBIT

['000 PLN]

11 612

1 160

-

16 612

EBIT growth

--110,0%

-1532,1%

EBIT m

argin

18,3%

-1,9%

33,2%

EBT

10 294

10 317

11 003

EBT growth

-0,2%

6,6%

EBT m

argin

16,2%

17,0%

22,0%

Net profit

['000 PLN]

14 249

6 766

8 627

Net profit m

argin

22,5%

11,2%

17,2%

Earnings per share

PLN

0,82

0,39

0,50

EPS growth

--52,5%

27,5%

Balance sheet

Total assets

['000 PLN]

200 702

352 688

341 274

Receivables

['000 PLN]

122 551

255 207

243 651

Total debt

['000 PLN]

95 708

219 985

210 905

Total Debt Recovered

['000 PLN]

75 833

201 162

194 325

Net debt

['000 PLN]

77 453

186 667

174 302

Shareholders' equity

['000 PLN]

86 632

93 398

102 025

Cash flow

Cash flow from operations

['000 PLN]

12 169

7 115

17 506

Adjusted cash flow from operations

['000 PLN]

18 126

25 704

26 449

Cash flow from investment

['000 PLN]

121 583

-

93 768

-

25 162

-

Cash flow from financing

['000 PLN]

123 122

101 716

10 941

51

�Com

pletion of critical initiatives

�Com

pletionof projects developm

ent

�Em

mission

trading benefits

�Energy trading com

petence

�Benchm

arking, synergies and further cost reductions for operating plants

�Improvem

ent of development efficiency and reduction of its time span

�Succesfullyentryinto the Central Europe Markets

�Continuous improvem

ent program realization

in all sites

Our objectives for next 12 months

Our objectives for next 12 months