Embed Size (px)

Citation preview

CLASSIFICATION SHEET

This document relates to the following request:

June 11, 2008

References: VAST-L23a08001M-GPI

Lehman Brothers Real Estate Fund

LBP Luxco S.a r .1. - Fiscal number: 2006 2437 456

I. Ke to ics: PPL ------------ - J 2. Name of the advisor : PwC -------3. Corporate group.'._s name or fu_nd sponsor: Lehman Brothers Real Estate Fun~ _________ J

4. Name of the project:

S. Amount intended to be invested: 33 million ----------------------~

6. Date of receipt:

- 2 JUIL. 2008

For the attention of Mr Marius Kohl

Administration des Contributions Dircctcs Bureau d'Imposition Societes VI 18, Rue du Fort Wedell L-2982 Luxembourg

11 June 2008

References: VAST/ L23a08001M-GPI

Lehman Brothers Real Estate Fund JI

LBP Luxco S.a r.I. - Fiscal number: 2006 2437 456

Dear Mr Kohl,

Prlrewalerhous.Cooprrs

Sorlet~ A rcsponsabilito! llmll&!

Ro!vlscur d'cotrcpri>cs

4()(), IOUIC d'Esch

B.P. 1443

L·1014 Lu~cmbour¥

Telephone 1352 494R48- 1

Facsimile + 352 494848-2900

www.pwc.conv'lu [email protected]

At the request of our client above, we are pleased to submit for your review and approval the Luxembourg tax treatment of the following structure. Alternatively, we would be pleased to receive your written comments on this structure.

The current financing structure involving the company LBP Luxco S.a r.I. was described to you in a previous agreement prepared by A TOZ S.A. and dated 18111 January 2007 and 301

h August 2007. Some modifications will be made to this structure in order to comply with the new Gennan interest capping rules.

The new structure will include a profit participating loan arrangement that will flow through the Luxembourg structure to ultimately finance real estate investments in Gennany.

The issues we are seeking your approval for, concern the tax treatment of this profit participating loan agreement, the margins applicable to the back-to-back financing arrangements and other issues related to this structure.

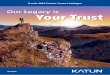

Please find enclosed to this letter a chart showing the holding structure in a diagrammatic form (Appendix 2).

R.C.S. Luxembourg B 65 477 - TVA I Ul7564447

A Facts and Background

A.l Holding structure

LBREP II Lion S.a r.l. (hereinafter "LBREP II") entered into a Joint Venture with CAST Partner S.a r.l. (hereinafter CAST Partner). The Joint Venture parties own shares in a holding company in Luxembourg, LBP Luxco S.a r.l. ("LuxTopco") that serves as the Luxembourg holding vehicle for several indirect real estate investments in Gennany. Approx. 87% of the shares in LuxTopco are held by LBREP II while the remaining 13% are owned by CAST Partner S.a r.l..

2 LuxTopCo has set up in turn two Luxembourg holding companies, LBP Lion Holdings S.a r.l. and LBC Goodwater Holdings S.a r.I. (hereinafter collectively "LuxHoldco"), which are each the sole indirect shareholder of 8 real property companies (S.a r.I. & Co KGs, hereinafter "Property KGs"). Property KGs own real estate in Germany.

A.2 Financing structure

A.2.1 General

3 The Luxembourg group entities, LuxTopco and the intermediate project holding LuxHoldco arc financed with a mix of equity, preferred equity certificates (PECs) and convertible preferred equity certificate (CPECs).

4 LuxTopco is financed with ca. 1 % equity and 99% PECs instruments.

5 Further to the modifications of the Gennan interest capping rules, the current financing of the LuxTopco with a PECs is to be replaced with a Profit Participation Loan (hereinafter "PPL") between LuxTopco and LBREP II. Please find attached in Appendix 3 the sample draft version of a PPL - Agreement.

(2)

A.2.2 Characteristics oft/re PPL

LBREP II Lion S.a r.l. to LuxTopco

Amount Approx. 72 million

Currency EUR

Interest rate - I % fixed interest rate

- variable interest in the amount of the share in the adjusted accounting profits1 of LuxTopco, to the extent the profits derive from the underlying investments minus an annual margin of 0.25% computed on the principal amount of the PPL

Payment On a date falling no later than 120 days following the date of approval of the annual accounts of the LuxTopco each year

Maturity date Not exceeding 8 years

Voting rights The lender is not entitled to any voting rights in the borrower

Risk's level Limited recourse

1 before deduction of any Variable Interest which has accrued on the outstanding principal during !he relevant accounting pcnod and after deduction of losses brought forward and an amount oqual to the fixed interest during the relevant accounung pcnod.

(3)

fJR/cEWA1£RHousE[roPERS I

B Tax treatment of the Profit Participating Loan

B.1. Qualification of Profit Participating Loan

6 ln order to be qualified as equity under German tax law, PPLs will provide that the Borrower has an option between (i) the redemption of the PPL advance by allocation of newly issued shares and (ii) the redemption of the PPL advance by payment in cash, i.e. an amount equal to the greater of the advance plus a fixed amount of EUR 10 000, and the fair market value of the shares the Lender would have received on such date.

7 Even if the PPL provides for a the possible payment of a "premium" of EUR 10 000 maximum at repayment, the PPL should stilh be treated as debt for Luxembourg income and net wealth tax purposes, given that all the characteristics that are regarded as relevant for detennining the tax treatment of the PPL as debt in Luxembourg remain unchanged, i.e.:

• Maturity date of 8 years (subject to a possible extension); • Fixed Interest of 1 %; • Ranking superior to equity; • No voting rights.

8 The PPLs interest will qualify as interest rather than dividend.

9 No withholding tax (in the meaning of either article 146 ( 1) 2 LITL or of article 146 (1) 3 LITL) will be due on interest paid under any of the PPLs.

10 Due to the qualification of the PP Ls as debt instrument and the qualification of the remuneration due to the PPL holder as interest, 100% of all interest accrued on the PPL payables will in principle be tax deductible in accordance with article 45 (1) LITL, unless a specific provision is applicable.

11 See our technical analysis on the tax regime applicable to PPL in Appendix 4.

(4)

B.2 Debt-to-equity ratio

12 The investments made by LuxTopco using funds deriving from the PPL consist of loans (PEC) granted to its subsidiaries LBC Goodwater Holding Sari and LBP Lion Holding Sarl, as well as shares in those subsidiaries.

13 It should be noted that since LuxCo will be deemed to be in an economic back-to-back funding position with respect to all investments financed by the PPL, this activity will fall outside the calculation of the 85: 15 debt-to-equity ratio (see our techn ical analysis in Appendix 4).

14 In this context, none of the interest paid by LuxTopco will be re-characterised into deemed dividend. As a result all the interest paid by LuxTopco will be fully deductible for income taxes purposes and will not be subject to any withholding tax.

8.3 Taxable spread

15 In the current financing structure, LuxTopco earns a 0.25% margin per annum on the aggregate outstanding amount of the PEC.

16 After replacement of the PEC by the PPL, LuxTopco will still earn this 0.25% spread.

B.4 Absence of silent partnership

17 Interest payment under the PPL will not be subject to withholding tax by virtue of articles 97(1)-2 and 146 (1)-2 LITL (i.e. "Stille Gesellschaft'', "bailleur de fonds" or "silent partnership"). Indeed, there is no intention to create such partnership in the case at hand as there is no "affectio societatis" by the PPL holder and no intention to establish a company in the sense of article 1832 of the civil Law Code.

(5)

We respectfully request that you confirm the tax treatment of the situation described above or that you provide us with your remarks, if any.

We remain at your disposal should you need any further infonnation and would like to thank you for the attention that you will give to our request.

Yours sincerely,

PfCJlr_ Geraldine Piat Partner

Appendices:

I Background information 2 Holding structure 3 Draft PPL-Agreement 4 Technical tax analysis

For app, oval

Le prepose f ~ b11rea11 d'impositio11 Societes 6

711is tax agreem<•nt is based on the facts as presented to Price ·aterho11seCoopers Sari as at the date the advice was given. 771e

agreement Is dependent on specific facts and circumstances and 111 !Y not be appropriate to another party than the one for which II was

prepared. 711is tax agreement was prepared with only the interests\ PrlcewaterhouscCoopers ·Client LBP Lu.>.co S.a r.I., in mind, and

was not planned or carried out in contemplation of any use by any ~~1er party. PricewaterhouseCoopers Sari. its parmers. employees

and or agents. neither owe nor accept any duty of care or any respon\/'l?ility to any other party. whether in contract or in lort (including

without limiwtion. negligence or breach of stalutory duly) howe11er a'Asing. and .~hall not be liable in respect of any loss. damage or

exprm1• of wl10tel'er nat11re which is caused lo any other parly.

(6)

Appendix I

A Background information

Lehman Brothers' Real Estate Private Equity group is a full-service real estate merchant banking business which operates two opportunistic equity funds, aggregating $4.0 billion of equity capital and one mezzanine investment fund aggregating $1.1 billion of equity capital. The Funds are invested and managed by a team of over 80 professionals in North America, Europe and Asia-Pacific.

Lehman Brothers' inaugural real estate private equity fund, Lehman Brothers Real Estate Partners (LBREP I), closed in 2001 with over $ 1.6 billion in aggregate in commitments and is now fully invested. Lehman Brothers Real Estate Partners II (LBREP II), a $2.4 billion fund closed in 2005, makes direct private equity investments in properties, real estate companies and service businesses ancillary to the real estate industry in North America, Europe and Asia-Pacific.

(7)

[JRJcEWAifRHousF[roPERS I

LUX

DE

Ban It

U.S.

BER

. I

I I

• PPL

• .. ,,, ........ ..

Holding Structure

........ \

- PEC I CPEC Financing-.----=- ----. :

LBREP II Europe Holdings s.a r.I.

.... PEC I CPEC Financing

.----~--..., . .-----------.,

.. ........

.... CAST Partner S.a r.I.

-87% -13%

LBP LuxCo S.a r.I.

PE'C I CPE~. F 1nancing

· .......

........ ........

Shareholder Loan . . . - \~ .....---~-----..

Bank Loan

LBC Goodwaler Holdings S.a r.I .

Appendix 2

Equity

SH Loan (tbc)

···--··---· PEC I CPEC (tbc)

----------· Bank Loan

----------·

(8)

BSS LBP - Lion I Profit Participating Facility (Draft 1) For discussion purpose only 080611_BSS-Vcrsion von FA 9.ll_PwC Comments 13.00

Dated [ •] June 2008

between

(1) LBP Luxco S.a r.l. as Recipient

and

(2) LBREP II Lion S.a r.l. as Investor

PROFIT PARTICIPATlNG FACILITY AGREEMENT

relating to a up to € [ •] facility

BONN SCt-MTT STEICHEN AVOCA T S -- -

44, RUE DE LA VALLtE L-2661 LUXEMBOURG BP 522 L-2015 LUXEMUOURG

Tu: (+352) -l5 58 58 FAx: (+352) 45 58 59 E-MAIL: [email protected] www.bsslaw.net

TABLE OF CONTENTS

l. INTERPRETATION ......... .............. .... .. ...... ................................. ... ..... ............ .... ... .................. 3

2. THE FACILITY .......... .. ......................................................................... ................. .................. 5

3. CONDITIONS OF UTILISATION ............................................................. ........... .................. 6

4. INTEREST ....... ................. ........... ... ............... .. .... ..... ................................... ............................. 6

5. REPAYMENT ................................................................................ ........................ .................. 7

6. PAYMENT ............. ....................... ................ .............................................. ............................. 8

7. REPRESENTATIONS AND WARRANTlES ............... ..... ....... .......... .......... ..... ... ................ 10

8. DEFAULT ...................................................... .................. .... ........... ..... ........ ........ ... .......... ... ... 10

9. SUCCESSOR AND ASSIGNMENT ........................................................... ... ........ ................ 12

10. INVALIDITY OF PROVISION ...... ........... ... ........... ...... ..... ............................... ..... ............... 12

11. GOVERNING LAW AND JURISDICTION ......................................................................... .12

12. GENERAL ......... ......... .. ........ .... ..... ............................................................... .......... ................ 12

2

BETWEEN

(A) LBREP II Lion S.a r.I., a company duly incorporated and ex1stmg under the laws of Luxembourg, having its registered office at 2, avenue Charles de Gaulle, L-1653 Luxembourg, and registered with the Luxembourg trade and companies register under number B 120098, hereby represented by David Beardsell and ... ......... in their capacity as Managers,

hereinafter referred to as the "Investor";

AND

(B) LBP LuxCo S.a r.I., a company duly incorporated and ex1stmg under the laws of Luxembourg, having its registered office at 2, avenue Charles de Gaulle, L-1653 Luxembourg, and registered with the Luxembourg trade and companies register under number B 120195, hereby represented by David Beardsell and Francesco Abbruzzese in their capacity as Managers,

hereinafter referred to as the "Recipient".

BACKGROUND:

This Agreement sets out the terms on, and subject to which, the Investor has agreed to make available a facility of up to € [ •] ([ •]) to the Recipient for the latter to grant loan facilities in the form of PECs and to finance the shares in its direct and/or indirect subsidiaries for the acquisition and holding of real estate properties located in Germany (the "Investment").

IT IS HEREBY AGREED

1. INTERPETATION

1.1. Definitions

In this Agreement:

"Advance" means the advance to be made to the Recipient by the lnvestor under the Facility or, as the case may be, the principal amount borrowed and not repaid of such advance.

"Adjusted Profits" has the meaning described in Clause 4.1.2.

"Advance Interest Payments" has the meaning described in Clause 4.2.2.

"Auditor" means the duly appointed auditor of the Recipient.

"Availability Period" means the period from the Facility Date until the Maturity Date.

"Business Day" means a day (other than a Saturday or Sunday) on which banks are open for general business in Luxembourg and [ ·].

3

"Cash Flow Available for Payment" means, with respect to any relevant period, all cash revenues and proceeds received by the Recipient during such period, from whatever source deriving exclusively, but whether directly or indirectly, from the Investments, following deduction of any amount equal to the sum of (i) any Tax payable on the Profit Margin, and (ii) the aggregate amount of all the Recipient expenses, as determined for such period by the Board of Managers at least ten ( 10) Business Days prior to the relevant date of payment.

"Orawdown" means the draw down of the Facility.

"Euro" means the single currency introduced in the member states of the European Community which adopted the single currency in accordance with the Treaty of Rome of 25 March 1957, as amended by, inter alia, the Single European Act 1986 and the Treaty of European Union of7 February 1992, establishing the European Union.

"Event of Default" has the meaning described in Clause 8.

"Facility" means the Euro [ •] principal amount provided on and subject to the terms of this Agreement.

"Facility Commitment" bas the meaning described in Clause 2.

"Facility Date" means [ •] 2008.

"Fixed Interest" has the meaning described in Clause 4.1 .1.

"Funding Date" in relation to a Drawdown means the date of that Drawdown or such other date as may be agreed between the Recipient and the Investor.

"Maturity Date" means [•] 2016.

"Other Similar Agreements" means any agreement generally in the same terms and conditions to this Agreement entered into by the Recipient with its other investors.

"Party" means a party to this Agreement.

"Percentage" means the share of the Investor in the total amount of funds received by the Recipient (i) under this Agreement, (ii) as equity from shareholders or (iii) from Investors under Other Similar Agreements computed as a percentage.

"Profit Margin" means with respect to any relevant period, an annual margin of 0.25% computed on the average Outstanding Advance which corresponds to the minimum required taxable margin of the Recipient.

"Redemption Date" has the meaning described in Clause 6.1 .1 .

"Rolled Over Profit Margin" means the amount of the Profit Margin computed on an annual basis with respect to any pervious accounting years and which was not accounted and reflected as profit of such given year in the accounts of the Recipient prepared under Luxembourg GAAP.

"Shares" means class [ •] shares in the capital of the Recipient.

4

"Subsidiary" means an entity from time to time of which a person has direct or indirect control or owns directly or indirectly more than fifty per cent. (50%) of the share capital or similar right of ownership. All together referred to as "Subsidiaries".

"Variable Interest" has the meaning described in Clause 4.1.1.

1.2. Interpretation of Certain References

Unless a contrary intention is stated:

1.2.1 . references to Clauses are to Clauses of this Agreement. References to paragraphs arc to paragraphs in the same sub-clause. References to sub-paragraphs are to sub-paragraphs in the same paragraph;

1.2.2. references to the "Investor" shall be construed so as to include its respective successors and permitted assignees;

1.2.3. references to "person" are to any person, firm, company, corporation, government, state or agency of a state or any association or partnership (whether or not having separate legal personality) of two or more of the foregoing;

1.2.4. references to other documents include those documents as they may be amended, modified, varied, supplemented or novated;

1.2.5. references to time are (except as otherwise provided in this Agreement) to Luxembourg time;

1.2.6. references to assets are to present and future assets and include revenues. References to assets of the Recipient are to assets which the Recipient administers and which were entrusted to it at its establishment or which arc acquired by it during the operation of its business.

1.3. Headings

All headings and titles are inserted for convenience only. They are to be ignored in the interpretation of this Agreement.

2. THE FACILITY

Amount and nature

The Facility shall be for a maximum amount of Euro [ ·] (the "'Facility Commitment") which can be drawn in one or several Advances during the Availability Period.

Purpose

2.2.1 . The Recipient agrees to use the proceeds of the Facility towards financing the Investment.

2.2.2. Without prejudice to the obligations of the Recipient under paragraph 2.2.1. above, the Investor shall not be obliged to concern itself with the application of amounts to be used or raised by the Recipient under this Agreement.

5

Availability of the Facility

2.3.1. This Agreement has become effective between the Investor and the Recipient as of the Facility Date and shall remain in full force and effect until the Maturity Date, unless it is tenninated prior the Maturity Date by mutual consent of the Parties.

2.3.2. The Facility shall be available until the Availability Period expires.

3. CONDITIONS OF UTILISATION

The Recipient may from time to time, within the limits of the Facility Commitment, request the making of an Advance by delivering to the Investor a duly completed request of Drawdown prior to the expiration of the Availability Period not less than twelve (12) Business Days before the proposed Funding Date.

4. INTEREST

Interest Rate

4.1 . l. As interest on the Facility, the Investor shall receive:

(i) an amount equal to 1 % per annum (365/366 days basis) computed on the outstanding principal amount of the Advances (the "Fixed Interest"); and

(ii) an amount equal to the Percentage of the Adjusted Profits of the Recipient (the "Variable Interest").

4.1.2. The "Adjusted Profits" shall mean the positive amount resulting from the sum of all income and gains (including foreign exchange gains) resulting from the Investments for the relevant accrual period to the extent they have been reflected in the accounts of the Recipient prepared under Luxembourg GAAP,

(-) the direct and indirect costs of the Investments as accounted for by the Recipient under Luxembourg GAAP, excluding any Fixed or Variable 1nterest,

(-)Fixed Interest,

(-)losses and losses carried forward derived from the Investments as accounted for by the Recipient under Luxembourg GAAP,

(-) the Profit Margin and any Rolled Over Profit Margin.

Income and gains shall always include, to the extent they have been accounted for by the company, all foreign exchange gains or losses realized or unrealized, including such gains or losses arising in connection with this Agreement or its full or partial repayment .

4.1.3. Following the closing of each accounting year or period and preparation of statutory account statements, the Recipient shall calculate the interest charge. At the Investor's request, the Recipient shall provide copies of the calculations and supporting documentation to the Investor. Such calculations shall be final subject lo changes in the financial statements of the Recipient made or required to be made in connection with obtaining approval of shareholders at the general meeting, in which case

6

appropriate changes shall be made to the calculation of the interest rate.

4.2. Interest Payment Dates

4.2.1 . All Fixed Interest payable under tlus Agreement shall accrue from day to day and will be paid of each calendar quarter from, and including, the Business Day which is three (3) calendar months following the Funding Date to, and including, the Maturity Date. The first Fixed Interest payment date shall be [•] 2008. Accrued Fixed Interest on a given Advance may be payable at the end of each calendar quarter which is a Business Day; provided, however, that, upon the request of the Recipient, interest may continue to accrue and not be so paid so long as no such accrual of interest shall extend beyond the Maturity Date or the Redemption Date of such Advance.

4.2.2. Variable Interest will be paid at the end of each calendar quarter ("Advance Interest Payment") from, and including, the Business Day which is three (3) calendar months following the Funding Date to, and including, the Maturity Date, on the basis of the projection of the Adjusted Profits of the Recipient. The first Variable Interest payment date shall be [ •] 2008.

The final Variable Interest due for each year shall be determined no more than one hundred and twenty ( 120) days after the end of each fiscal year on the basis of the approved draft annual statutory accounts of the Recipient.

4.3. Adjustment of Interest Payments

The difference between the sum of all Advance Interest Payments made during the relevant fiscal year and the final Variable Interest shall be paid by the Recipient to the Investor within fi Ileen (15) calendar days after the approval of the annual statutory accounts of the Recipient by its managers.

If the sum of all Advance Interest Payments made during the relevant fiscal year is superior to the final Variable Interest, the difference shall be reimbursed by the Investor to the Recipient within fifteen (15) calendar days ailer the approval of the annual statutory accounts of the Recipient.

4.4. Default interest

Any interest, which accrues but is unpaid when due will be added to the sum owed by the Recipient and will itself bear interest.

5. REPAYMENT

5.1. Repayment date

Subject to paragraphs 5.2 and 5.3 of this Clause 5, the Facility shall be repaid on the Maturity Date together with accrued interest thereon. The Investor and the Recipient may decide in common agreement to repay partly or wholly the Facility prior to the Maturity Date.

5.2. Limited Recourse

Payment of the Variable Interest or the accrued Fixed Interest as well as the reimbursement of the Advances is subject to the condition that the Cash Flow Available for Payment enable the Recipient to make the relevant payment.

7

5.3. Extension

5.3.1. The Investor may extend the redemption of the Facility to maximum one (l) year.

5.3.2. The Recipient may postpone, with a five (5) Business Days written notice to the Investor, the payment of any interest due on any Advance, until it has sufficient liquidities to make payment.

5.4. Pre-payment

Subject to clause 5.2, the Investor may require pre-payment of all but not part of the Facility upon occurrence of any of the following events:

5.4.1. the Recipient or any affiliate of the Recipient ceasing to carry on its business or a substantial part of its business except as a result of a winding up pursuant to a scheme previously approved by the Investor;

5.4.2. the Recipient or any Affiliate of the Recipient:

(i) being adjudicated to be insolvent;

(ii) entering into a composition or other arrangement for the benefit of its creditors generally (other than by a scheme resolved by shareholders of the Recipient;

5.4.3. an encumbrance taking possession or a receiver or administrative receiver or manager or scquestrator being appointed of the whole or any substantial part of the undertaking or assets of the Recipients or any Affiliate of the Recipient;

5.4.4. an administration order being made in relation to the Recipient or any Affiliate of the Recipient; or

5.4.5. it becomes unlawful for the Investor to maintain the Facility.

In such case the Investor shall give written notice to the Recipient specifying the date on which the Facility shall be repaid (together with all interest accrued until (but excluding) such date and which remains unpaid).

6. PAYMENT

6.1. Redemption by allocation of shares

6.1 .1. The Recipient shall be entitled, at any time and at its election, to redeem any or all Advances on a ce1tain date (the "Redemption Date") specified in a notice of redemption by allocating Shares to the Investor.

6.1.2. The Investor shall accept the allocation of Shares.

6.1.3. All Shares issued under this Agreement will be issued credited as fully paid-up and from the date of allotment rank pari passu in all respects and fo1m one class with the Shares in issue on that date, except that they will not rank for any interim or final dividend to be declared in respect of any period up to and including the relevant Redemption Date.

6.1.4. Auditors will (acting as experts and not as arbitrators) determine the number of Shares to be allocated and/or cash to be paid upon redemption. The determination of the

8

Auditors shall (except in case of manifest error) be binding upon all parties and their cost shall be borne as the Auditors may direct.

6.2. Redemption by payment

6.2.1. Redemption by partial allocation of shares and partial payment shall be allowed.

6.2.2. Alternatively the Recipient shall be entitled, at any time and at its sole discretion, to redeem the Advances by cash payment of an amount equal to the greater of:

(i) the Advance plus an amount o f€ I 0,000.-; and

(ii) the fair market value of the Shares (as determined by the Recipient in good faith);

the Investor would have received on such date.

6.2.3. Payment shall be effected in freely transferable and immediately same day funds into the account of the Investor in accordance with the Investor's instructions.

6.2.4. Payment shall be made in Euro. All payments in respect of costs, losses, expenses and liabilities payable hereunder shall be made in the currency in which they were incurred.

6.2.5. Any repayment on the Facility shall be made before any payment shall be made or any assets distributed to the holders of any subordinated securities but after payment (or providing reasonable reserves for the future payment) of all other obligations of the Company to prior ranking ordinary or subordinated creditors whether privileged, secured or unsecured.

6.3. Payment in full

6.3.1. AJI payments to be made by the Recipient to the Investor hereunder shall be made free and clear of and without deduction for or on account of any tax or withholding of any nature whatsoever unless the Recipient is required by Jaw to make such a payment subject to the deduction or withholding of tax, in which case the sum payable by the Recipient in respect of which such deduction or withholding is required to be made, shall be increased to the extent necessary to ensure that, after the making of such deduction or withholding the Investor receives and retains (free from any liability in respect of any such deduction or withholding) a net sum equal to the sum which it would have received and so retained had no such deduction or withholding been made or required to be made.

6.3.2. If the Recipient makes any payment hereunder in respect of which it is required by law to make such deduction or withholding, it shall pay the full amount to be deducted or withheld to the relevant taxation or other authority within the time allowed for such payment under applicable law and shall deliver to the Investor, within thirty days after it has made such payment to the applicable authority, a declaration by the Recipient in a form acceptable to the Lnvcstor evidencing the payment to such authority of all amounts so required to be deducted or withheld, together with such other documentation as the Investor may reasonably require.

9

7. REPRESENT A TIO NS AND WARRANTIES

The Recipient, acknowledging that the Investor has entered into this Agreement also in reliance on the following representations and warranties, hereby represents and warrants that:

(a) it is a company duly established and validly existing under the laws of the Grand Duchy of Luxembourg and has the corporate power and authority to own its properties and assets and carry on its business as it is now being conducted;

(b) the making, performance and delivery of this Agreement, have been authorized by all proper proceedings and do not contravene any law or any contractual restrictions binding on the Recipient;

(c} this Agreement have been duly executed and delivered by the Recipient and constitutes legal, valid and binding obligations of the Recipient enforceable in accordance with their terms;

( d) the signing and perfonnance of this Agreement do not violate any contract to which the Recipient is a party or any undertaking of the Recipient which is binding upon the Recipient or its assets or revenues;

(e) as at the date of this A!,7Ieement the Recipient did not have any significant liability (contingent or otherwise) which is not disclosed; and

(f) the Recipient is not in default with respect to any material obligation under any agreement to which it may be a party, and there is not presently pending or, to the knowledge of the Recipient, threatened any action, suit or proceeding before any court, board or arbitration or administrative body or commission against it or its property or assets which, if adversely detennined, might reasonably be expected to affect materially the capability of repayment of the Facility by the Recipient in accordance with the clauses of this Agreement.

The foregoing representations and warranties shall survive the signfog of this Agreement and shall be deemed to be repeated on a continuous basis by the Recipient during the entire life of this Agreement.

8. DEFAULT

8.1. Events of Default

Each of the events set out below is an "Event of Default", whether or not caused by any reason outside of the Recipient's control:

8.1. l. the Recipient fails to pay any sum due under this Agreement on its due date for payment; or

8.1.2. the Recipient fails to pay the interest due pursuant to Clause 4 above, upon the Investor having requested the Recipient to pay any outstanding interest in writing at least [five (5)] days prior thereto; or

10

8.1.3. any statement delivered or made, or any representation made proves to be incorrect, inaccurate or misleading in any material respect;

8.1.4. any obligation of the Recipient is defaulted upon;

8.1 .5. a material distress or other execution is levied upon, or against any part of the property of the Recipient;

8.1.6. the Recipient is unable or admits in writing his ability to pay his lawful debts as they mature, or makes a general assignment lo the benefit of his creditors;

8.1. 7. if the Recipient enters into composition proceedings, bankruptcy, insolvency or similar proceedings or any order shall be made by any competent court or resolution passed by the Recipient for the appointment of a receiver or similar authority;

8.1.7. the Recipient ceases or threatens to cease to carry its business or disposes or threatens to dispose of a material part of its business;

8.1.8. any licence, consent, permission or approval required in connection with the implementation, maintenance and performance of this Agreement is revoked, terminated or modified in a manner found unacceptable to the Investor;

8.1.9. in the opinion of the Investor, a material adverse change which may affect the ability of the Recipient to carry out its obligations under this Agreement occurs;

8.1. l 0. a transfer or disposal of all or a substantial part of the Recipient 's assets whether by one or a series of transactions, related or not, except for fair value and in ordinary course of business occurs;

8.1.1 l. the Recipient is dissolved or liquidated; or

8.1.12. it becomes unlawful for the Recipient to perform all or any of its obligation under the Agreement.

8.2. Payments following an Event of Default

Upon the occurrence of any Event of Default, and at any time while the same is continuing, the Investor may by written notice to the Recipient declare the Facility and applicable interest immediately due and payable.

8.3. Indemnity

The Recipient agrees to reimburse the Investor for the amount of any reasonable and documented expenses incurred by the Investor in protecting, preserving or enforcing its rights under this Agreement.

9. SUCCESSOR AND ASSIGNMENT

9.1. Successor

This Agreement will be binding upon and inure to the benefit of each party and their respective successors and assigns except as set forth below, and references in this Agreement

11

lo any of them shall be construed accordingly.

9.2. Assignment by the Investor

The Investor will be entitled at any time to assign and transfer, in whole or in pait, its rights and obligations under this Agreement or their perfom1ance. Except with the prior written consent of the Investor, the Recipient may not assign or transfer all or any of its rights and obligations under this Agreement.

10. INVALIDITY OF PROVISION

ln case any or more of the provisions contained in this Agreement should be or become fully or in part invalid, illegal or unenforceable in any respect under any applicable law, the validity, legality and enforceability of the remaining provisions contained in this Agreement shall not in any way be affected or impaired thereby. Provisions that are fully or in part invalid, illegal or unenforceable shall be implemented according to the spirit and purpose of this Agreement. Modifications and amendments to this Agreement shall be made in writing and signed by the contracting parties.

11. GOVERNING LAW AND JURISDICTION

11.1. Governing law

This Agreement will be interpreted in accordance with and governed in all respects by the laws of Luxembourg.

11.2. Jurisdiction

For the benefit of the Investor, the Recipient irrevocably agrees that the courts of the city of Luxembourg are to have jurisdiction to settle disputes which arise out of, or in connection with, this Agreement.

This provision will not lllnit the rights of the Investor to take proceedings in any other jurisdiction.

12. GENERAL

12.1. Entire agreement

This Agreement embodies the entire agreement between the parties and supersedes all previous statements, representations and agreements between the parties relating to the subject matter of this Agreement.

12.2. Reliance

No party shall be able to rely on any change in any provision of th.is Agreement unless the change has been effected in writing and executed by duly authorized representatives of each of the parties.

12.3. Counterparts

This Agreement may be executed in any number of counterparts and by different parties on separate counterparts, each of which when executed and delivered, shall together constitute but one of the same instrument.

12

IN WITNESS WIIEREOF the Investor and the Recipient have caused this Agreement in two original counterparts to be executed by their duly authorized representatives as of [ •] 2008, each party acknowledging receipt of one executed original counterparts.

The Recipient The Investor

LBP Luxco S.a r.l. LBREP II Lion S.a r.l.

Represented by: David Beardsell I A Manager Represented by: David Bcardsell

Francesco Abbruzzese I B Manager

13

Appendix 4

Techni.cal Tax Analysis

A Tax residency of the Luxembourg entity

LuxTopco as fully taxable Luxembourg capital company is tax resident in Luxembourg within the meaning of the tax treaties concluded by Luxembourg and within the meaning of article 159 of the Luxembourg lncome Tax Law ("LITL"), provided that its shareholders' meetings and board meetings take place in Luxembourg and their accounting and archives arc kept in Luxembourg.

2 Furthermore from a Luxembourg tax point of view, LuxTopco does not constitute pcnnanent establishments of any other non-resident group companies.

B Tax qualification of the PPL

B.J Characterisatio11 as debt

3 According to the commentaries to the income tax law (commentaries included in "Projet de Loi N° 571 (1955)") on the former article 114 LITL (now article 97 LITL) on income from participation, where a profit participating loan bears a minimum fixed interest rate, payable even when the company is in a loss position, and provided the principal amount of the loan is repayable before the reimbursement of the company's share capital, the profit participating loan should continue to be treated as a debt for Luxembourg tax purposes.

4 Ln the case at hand, the fixed interest will accrue without taking into consideration if the company is in a profit or loss position.

5 Consequently, the PPL will be qualified as debt for both net wealth tax purposes and income taxes purposes, and interest thereon will be deductible under the same conditions as apply to fixed interest debt.

B.2 Characterisation of PPL interest payments

6 Authors have examined the possibility that the definition of "dividends" given by the Luxembourg income tax law could include payments qualified as interest. According to their analysis, the key criteria to qualify a payment as a dividend, rather than interest2 are:

• Entitlement to ongoing profit (including profit reserves); and • Entitlement to the liquidation proceeds.

2 A. Steichen, "Pr6ci~ de droit fiscal de l'cntrcprisc," Editions Saint-Paul, 2004, Section 702 and following, p. 462.

(9)

7 Under this interpretation, the payment of an amount not relating to the profit of the borrower, or to its liquidation proceeds may not be considered as a dividend.

8 In the case at hand, since the PPL variable interest will be dependent on the profits realised after deduction of losses brought forward, and before Luxembourg taxes and interest charges, it will consequently be qualified as interest rather than dividend.

9 In addition 100% of all interest paid on the PPL will be tax deductible in accordance with article 45(1) LITL, unless article 45(2) LITL or 166 (5) is applicable (interest expense in relation to exempt income).

B.3 Withholding tax treatment on PPL interest payments

10 Article 146(1 )-3 LITL provides for the application of a dividend withholding tax upon payment of interest arising from participating bonds or other similar securities. Interest payments arc only subject to a 15% dividend withholding tax in Luxembourg if the following conditions are satisfied:

• The loan is structured in the fonn of bonds or other similar securities; and

• As well as the fixed interest, supplementary interest varying according to the amount of profits otherwise distributed is paid, unless the said supplementary interest is stipulated simultaneously with a momentary decrease of the fixed interest.

11 In the present case, the debt owed by LuxTopco is structured as PPL facility and the participating interest does not depend on distributed profit. Therefore, interest on the PPL paid by LuxTopco will not be subject to any dividend withholding tax.

12 Furthennore, interest payment under the PPL will not be subject to withholding tax by virtue of articles 97(1)-2 and 146 (1)-2 LITL (i.e. "Stille Gesellschaft", "bailleur de fonds" or "silent partnership"). Indeed, there is no intention to create such partnership in the case at hand as there is no "affectio societatis" by the PPL holder and no intention to establish a company in the sense of article 1832 of the civil Law Code.

13 Therefore, no withholding tax in the meaning of article 146(1 )-2 or 146( 1)-3 LITL will apply on PPLs interest payment.

(10)

C Profit participating loan

C.J Debt to equity ratio

14 Generally, according to Luxembourg practice, a debt to equity ratio of 85:15 needs to be respected by a company investing in participations. Any interest paid in excess of the applicable ratio should be qualified as dividends and subject to a 15% withholding tax for the purposes of article 146 LITL. However, back-to-back arrangements are not required to comply with the aforementioned thin-capitalisation requirements.

15 In the case at hand, PPL granted to LuxTopco is used to finance economically linked investments (equity injected in and interest-bearing loans granted to subsidiaries). This is economically speaking clearly the case: if the investments made by LuxTopco do well, LuxTopco pays out a very significant element of its income as variable interest on the PPL, and if the investments do badly, only fixed interest has to be paid on the PPL to the extent that the identical cash proceeds will be made available at the level of LuxTopeo. Furthermore, the PPL granted provide for limited recourse by the lender against the assets financed by the PPL. The principal amount of the PPL outstanding will also be (partially) reimbursed in case of (a partial) exit from or of the investments financed. LuxTopco will therefore from an economic point of view be in a back-to-back position between the PPL and the investments (both equity and debt) financed by the PPL. The economic linkage will be respected for the purposes of consideration of the debt-to-equity ratio.

16 Since LuxTopco will be deemed to be in a connected position with respect to all investments financed by the PPL, its financing activity will fall outside the calculation of the 85: 15 debt-to-equity ratio. Hence none of the interest paid by LuxTopco on the PPL will be re-characterized as a deemed dividend. As a result all the interest paid by LuxTopco on the PPL will be fully deductible for income tax purpose and will not be subject to any withholding tax.

C.2 Margin subject to taxation

17 Taking into account the fact that LuxTopco does not bear material risk and that the amounts lent by LBREP II and invested in the LuxHoldco match, the overall remuneration earned by the company will be considered as being at arm's length and the interest paid tax deductible, as long as a margin of 0.25% per annum of the whole PPL amount flowing from the LuxHoldco to LuxTopco will be subject to income taxes in Luxembourg.

( 11 )