Embed Size (px)

Citation preview

Presented by:

Lauren Freedman: President, the e-tailing group

W. Sean Ford: COO & CMO, Zmags

Lauren Freedman

President

the e-tailing group

W. Sean Ford

COO & CMO

Zmags

About Our Speakers

2

16 years e-commerce consulting

Fortune 500 client projects ranging

from strategic planning, customer

experience with an emphasis on

merchandising to technology

marketing and lead generation

Proprietary research studies on

mystery shopping, merchandising,

mobile and consumer behavior

Author, It’s Just Shopping

50+ years traditional retail and

catalog experience

The Voice of Cross-Channel Merchandising Straight talk from “in-the-trenches” online merchandising experts

3

Helps thousands of the

world’s most progressive

retailers and brands design

brilliant and consistent

marketing and

merchandising campaigns

across touchpoints

Drive product discovery and

inspire purchase

Among the fastest growing

technology companies in

North America, ranking #70 on

the Deloitte 2011 Technology

Fast 500

Offices in Boston, London,

and Copenhagen

Zmags: Discover Shopping Inspiration

4

Holiday headlines merit attention

• “US Online Holiday Shopping Season reaches record $37.2

Billion for Nov/Dec period up 15% vs. year ago” (comscore)

• “Sales from smartphones and tablets account for 11% of total

online sales in Dec ‘11 up from 5.5% in Dec ’10” (IBM)

• “2011-mcommerce will be at least $10B” (Internet Retailer)

• “More than 60% of 25-34 year olds own a smartphone and

29% of smartphone owners use their phone for shopping-

related activities” (Nielsen)

• “14.6% all online retailer sessions were initiated from mobile

devices more than double 2010 at 5.6%” (IBM)

• “10% of total web sales were made on smartphones and

tablets the week leading up to Valentine’s Day triple 2011”

(IBM)

• “800 million people connected via Facebook and more than ¾

of consumers are active Facebook users” (Zmags)

5

More devices, more touchpoints= MORE ACCESS

6

Merchant food-for-thought

• Am I best leveraging my content investments?

• Have I effectively curated content for my customers?

• Do we deliver an experience for our shoppers or merely foster simple search and find shopping?

• Does my business warrant an app? Will anyone use?

• How much traffic are we seeing from tablets?

• Is conversion from the tablet significantly higher than from smartphones?

• Have we explored how our site renders on all devices?

• Have we seized the day on Facebook and shared the best of our content via social networks?

7

1-800 Flowers Clinique Golfsmith Neiman Marcus Shop NBC

ABT Coach Green Mountain Net-A-Porter Shop PBS

Altrec Crate & Barrel Gymboree Newegg Staples

Amazon.com Crutchfield Harry & David Nike Sundance

American Eagle Outfitters Dell Hayneedle Nordstrom Sunglass Hut

American Girl Dick’s Sporting Goods Home Depot Office Depot Target

Ann Taylor Discovery Channel HP Home and Home Office Orvis The Men’s Wearhouse

Apple Disney.com HSN Overstock Things Remembered

Athleta DSW Shoes J. Crew Patagonia Tiffany & Co.

Aveda eBags.com JCPenney Petco Title 9

Ballard Designs EBGames Jonathan Adler PetSmart Tory Burch

Barnes & Noble Finish Line King Arthur Flour Pottery Barn Toys ‘R Us

Bath & Body Works Foot Locker Kohls QVC Tumi

Belk Free People L.L. Bean Ralph Lauren Victoria’s Secret

Benefit Frontgate Lands’ End Redenvelope Walgreen’s

Best Buy Gap Lane Bryant REI Wal-Mart

Blue Nile Garnet Hill Lego Road Runner Sports Waterford

Brookstone Giggle Lowe's Room And Board Williams-Sonoma

Cabela’s GNC Macy's Sears Wine.com

Chicos Godiva Moosejaw Sephora Zappos

2011 e-tailing group Mystery Shopping EG100

8

Mobile and social presences are felt by shoppers

9

e-tailing 100

4Q11

e-tailing 100

4Q10

% Penetration % Penetration

Mobile Commerce 78% 44%

Link to Mobile Commerce on Ecommerce Site 50% (78 sites) N/A

Mobile Apps 66% N/A

Link to Mobile Apps on Ecommerce Site 65% (66 sites) N/A

SMS Sign-Up 31% 29%

Link To Social Networking (“Follow Us On

Twitter!”)

95% 83%

Facebook 93% (95 sites) 96% (83 sites)

Twitter 89% (95 sites) 87% (83 sites)

You Tube 55% (95 sites) 43% (83 sites)

"Like" Button 71% 36%

Share 71% 75%

Google + 30% N/A

e-tailing group 4Q11 Mystery Shopping Study

How does the consumer feel about

shopping via these devices?

Devices mean happy, excited and productive customers

Zmags; 2012

10

12

Q33-34

Traffic growth from mobile significant where

revenues are following suit

None 2% < 1

11%

1 - 1.9% 10%

2 - 4.9% 26%

5 - 9.9% 27%

10% + 16%

Don't know

8%

What percent of your traffic comes via mobile browsers or mobile applications?

None 4%

< 1% 23%

1 - 2.9% 27%

3 - 4.9% 11%

5 - 9.9% 18%

10% + 6%

Don't know 11%

What percent of your revenue comes via mobile browsers or mobile applications?

Tablet conversion is already powerful for retailers

13

e-tailing group Annual Merchant Survey, 2012

10%

4%

22%

11%

6%

20%

56%

16%

23%

23%

74%

35%

Mobile web

Stand-alone native apps

Tablets

What conversion rates are you seeing from mobile?

Significantly/Somewhat More Than Website

About the Same as Website

Significantly/Somewhat Less Than Website

N/A

2012: The Year of the Tablet

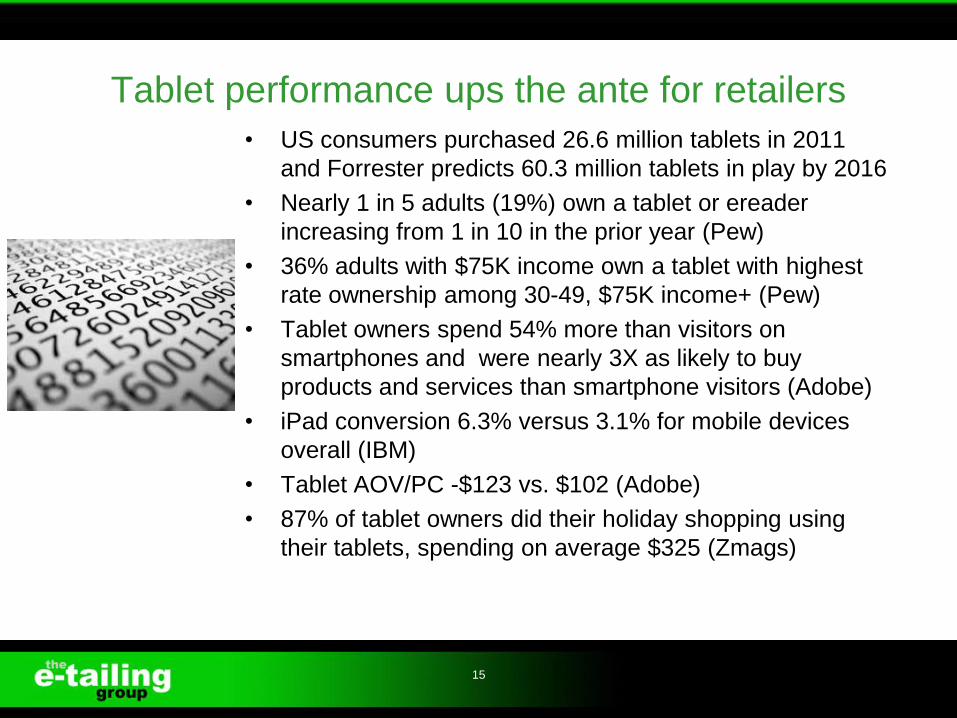

Tablet performance ups the ante for retailers

• US consumers purchased 26.6 million tablets in 2011

and Forrester predicts 60.3 million tablets in play by 2016

• Nearly 1 in 5 adults (19%) own a tablet or ereader

increasing from 1 in 10 in the prior year (Pew)

• 36% adults with $75K income own a tablet with highest

rate ownership among 30-49, $75K income+ (Pew)

• Tablet owners spend 54% more than visitors on

smartphones and were nearly 3X as likely to buy

products and services than smartphone visitors (Adobe)

• iPad conversion 6.3% versus 3.1% for mobile devices

overall (IBM)

• Tablet AOV/PC -$123 vs. $102 (Adobe)

• 87% of tablet owners did their holiday shopping using

their tablets, spending on average $325 (Zmags)

15

When you shop via a tablet

what is your most frequent

motivation?

Convenience creates “couch consumers”

Zmags; 2012

16

Tablet devices are the new multi-purpose tool for

researching, browsing, and buying

17

Q30 Source: e-tailing group/Oracle Connected Customer Survey; 2011

61%

56%

55%

54%

36%

I use my tablet device to research products prior to a store visit

My tablet device is an ideal tool for browsing products from my favorite catalogs and retailers

I use my tablet device to research products and then purchase them right on the device

I use my tablet device to research products then purchase them online via my computer

I use my tablet device to research products during a store visit

Please indicate your agreement with the following statements regarding browsing or buying products via your tablet device.

(Top-2 Strongly/Somewhat Agree)

Tablet owners appear to use these devices to browse

and buy online more frequently than smartphone owners

18

Q7/15 – 400S/417T

6%

16%

17%

11%

10%

15%

25%

10%

19%

19%

12%

7%

9%

24%

Daily

Weekly

Several times per month

Once a month

4 or more times per year

Less than 4 times per year

Never

How frequently do you browse or buy products and services online?

Smartphone Tablet

e-tailing group/CoffeeTable The Shopping Mindset of a Mobile Consumer Survey; 2011

Tablet owners purchased Books/Magazines,

Clothing/Accessories, Digital Books, Consumer Electronics,

Computer Hardware & Software

19

Q18 – 324

45% 37%

30% 28%

27% 24%

21% 20%

19% 18%

17% 13%

12% 12%

10% 10% 10%

8% 6%

1% 1% 1%

Books/Magazines

Clothing and accessories (men’s, women’s, kid’s)

Digital books

Consumer electronics

Computer hardware and software

Music/DVD/Videos

Movies

Gifts and collectibles/Flowers

Gift Card/Certificates

Tickets (movies, concerts, theatre)

Toys/Video games

Furniture/Home and garden

Crafts/Hobbies

Food

Pet supplies

Sporting goods

Health and beauty items

Jewelry/Watches

Luxury items

Travel

Don't know/unsure

Other, please specify

In which categories did you purchase products or services via your iPad or Tablet? Select all that apply.

e-tailing group/CoffeeTable The

Shopping Mindset of a Mobile

Consumer Survey; 2011

Shopping via a tablet delivers a more satisfactory experience

than shopping via a smartphone

20

Q10/19– 400/324

32%

41%

24%

3%

0%

50%

38%

9%

3%

0%

Very satisfactory

Somewhat satisfactory

Mixed bag (sometimes satisfactory/sometimes not satisfactory)

Somewhat unsatisfactory

Very unsatisfactory

Thinking about your most recent shopping experiences, what level of satisfaction would you report?

Smartphone Tablet

e-tailing group/CoffeeTable The Shopping Mindset of a Mobile Consumer Survey; 2011

69% of tablet owners report that their most recent shopping experiences

via these devices was significantly to somewhat better than shopping

with their smartphones

21

Q19 – 324

39%

30%

17%

2%

1%

6%

5%

Significantly better

Somewhat better

About the same

Somewhat worse

Significantly worse

Don't shop on both devices

Don’t own both devices

How would you rate the shopping experience on the iPad or Tablet versus your mobile phone?

e-tailing group/CoffeeTable The Shopping Mindset of a Mobile Consumer Survey; 2011

Thinking ahead a year, how do

you expect your digital

purchasing behavior to change

compared to this holiday

season

The future looks bright for mobile

Zmags; 2012

22

Then and Now

23

2012 2000 1% 7%

Retail Unprepared for Tablets

24

FEWER THAN ONE-THIRD OF RETAILERS HAVE OPTIMIZED,

OR EVEN ADJUSTED, THEIR SITES FOR TABLETS.

Innovation?

25

Owning Inspiration

26

DIRECTED

PURCHASE DISCOVERY

SHOPPING

Discover

Shopping

Inspiration

2000+

SELL ME

2008+

SURPRISE ME

2010+

INSPIRE ME

Shopper Discovery Curating Experiences for Customers

Shopper Discovery: why it matters

• Search only takes shopping so far

• Experiences truly engage shoppers with the brand

• Edited experiences facilitate shopping

• Discovery is multi-dimensional and starts with brand

engagement informing shoppers prior to purchase

• Tactics evolve where merchant utilization fosters

consumer adoption

• Marketing potential across channels and devices

expands reach for retailers

28

Imagery sets the standard for engaging shopping

29

ESSENTIAL (>50%) MERCHANT CHOICE (33-49%) SOCIAL (<33%)

Quality of the image (74%) Product guides (49%) Email-a-friend (18%)

Ability to see selected product in color

of choice (69%)View product on a model (46%) Like button (18%)

Alternative views of selected item (64%) Live help (40%) Share button (16%)

Zoom (63%) Product demonstrations (39%)

Peer ratings and reviews (53%) Video of the product in use (37%)

Product comparisons (51%) Product recommendations (35%)

Q/A (34%)

View product in a room setting

(33%)

Source: e-tailing group/Oracle Connected Consumer Survey

When viewing a merchant’s product page online, how important is the

following information when selecting and ultimately purchasing a

product? (Top-2 Critical/Very Important)

Savvy sellers have always invested in experiences

and evolved with the times

30

e-tailing 100

4Q11

e-tailing 100

4Q10

% Penetration % Penetration

EVERGREEN

Themed Areas 64% 39%

Brand Boutiques 89% (83 sites) 76% (79 sites)

Quality/Content (1-5 5=Excellent) 2.6 (83 sites) 3.16 (60 sites)

Shop the Catalog 35% 32%

Ad Campaigns 21% 25%

EVOLVERS

Home Page Slide Show Of Featured Items

and/or Promotions On Home Page

53% 57%

Look Book 24% (71 sites) N/A

Shoppable 59% (17 sites) N/A

Videos 83% 88%

31

Catalogers took the early lead

• The famous Christmas Book has

evolved into an extraordinary

virtual brand experience,

complete with video content

• Integrated with website to enable

online purchase

MAKING THE BRAND

EXPERIENCE COME

ALIVE ONLINE

32

Traditional advertising is now reinterpreted online

33

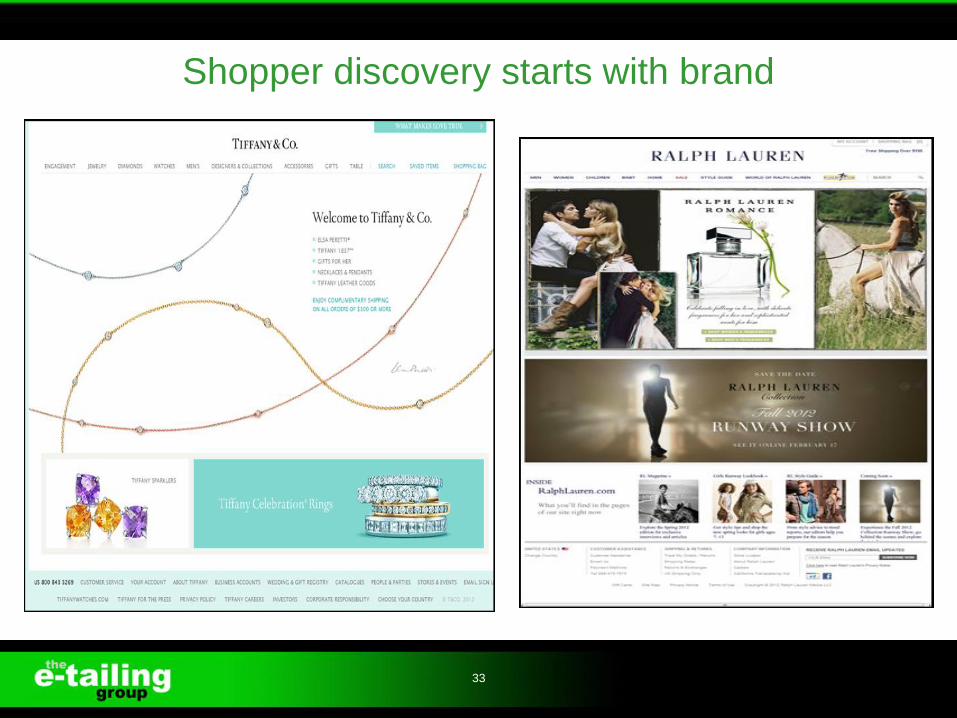

Shopper discovery starts with brand

Consistency is core to smart branding

34

35

Brands look to control experiences across partners From syndication to retail-controlled efforts standout performance is a differentiator

2011 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001

Brand showcase 89% 76% 87% 85% 81% 86% 85% 83% 75% 85% 68%

Quality/Content 1-5 5 = excellent 2.6 3.16 2.69 2.62 2.55 2.76 2.18 NA NA NA NA

36

Exploring what’s new excites shoppers

37

Educating and informing shoppers pre-purchase is

a value-add

Decision-making through experiences are facilitated

across channels

38

Customers will be interacting with ipads at retail on their

own and with associates further fueling interest

39

Within next 24 months; 56.2%

of 130 retailers put ipads in

hands of store associates

(Aruba Networks)

“It allows retailers to take

advantage of rich media

and larger images for

both the customer

experience as well as

employee training.”

Lookbooks take on New Meaning

40

Multi-dimensional merchandising

• New modern approach to themed areas where trends and new

product takes center stage

• Regardless of the merchandise category, lookbooks tell stories by

grouping merchandise meaningfully and providing supportive

content

• Apparel retailers put “fashion” savvy in play to better connect their

customers/prospects to the brand while department stores and mass

merchants follow suit in similar categories

• Brands with broad fashion appeal and reach (Tiffany & Co) or who

target younger, hipper demographic embrace lookbooks (American

Eagle Outfitters, Free People, Net-A-Porter, Zappos)

• Porting to Facebook adds new dimension

41

24% EG100 deployed with 59% shoppable

2011 e-tailing group Mystery Shopping

Establishing “point-of-view” essential in a crowded

marketplace

42 42

Collection entrée with scrolling access for

assortment exposure optimal

43

Editorial meets merchandising

44 44

45

Showcasing “must haves” puts seasonal shopping

wheels in motion

46

Shoppable lookbooks impact the bottom-line

Home market opportunities beginning to take shape

47

Cross-channel visibility and broad customer appeal best

serves shopper

48 48

Guiding Connected Consumers

• Evaluate current position from a “discovery” point-of-view

• Explore opportunities to better showcase your brand

testing discovery models onsite

• Be consistent across channels for greatest marketing

impact

• Deploy across mobile to capture your fair share of couch

commerce

• Expand reach via Facebook and other social channels

• Establish a series of metrics that gauge customer

interest

49

Retailer Takeaways

50

Create a World Class Experience

51

• Rich, immersive brand

experience, consistent

across all touchpoints

• Design to take advantage of

tablet functionality as well

as smartphones, PCs or

laptops

• Advance online

merchandising and

commerce from traditional

search-and-purchase to a

discovery and inspiration

• Buy off the page for an

uninterrupted experience

51

Drive Engagement Wherever Customers Interact

52

Treat Every Channel Like a Storefront Re-create the intimacy of the in-store shopping experience online

53 53

Social Media is an Untapped Opportunity

54

• 8.3 million page views

• 18,100 hours spent looking at

the catalog

• 60% lower bounce rate than

the web site

• 27 pages viewed per visit

• 3 million pieces of stoneware

sold in last 3 years

First Mover Advantages Abound

55

UP TO

2X LIFT IN CONVERSION

RATES

INCREASE IN AVERAGE

ORDER VALUES 40%+ INCREASE IN PAGE VIEWS 5X

Retailer Takeaways

• Create a world class experience

• Drive engagement wherever customers interact with

your brand

• Treat every channel like a storefront

• Social media is an untapped opportunity

• First mover advantages abound

56

Contact Info

Lauren Freedman

773-975-7280

www.e-tailing.com

57

W. Sean Ford

617-963-8051

www.zmags.com

Q&A

58

Please submit your questions now.