Embed Size (px)

Citation preview

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

A Company and Industry Analysis October 2010

CONTENTS

Current Environment

• Sector Overview

• Sector Performance

• Leading Companies

• Mergers and Acquisitions

Industry Profile

• Industry Size and Value - Fixed-line Broadband Market

- Mobile Broadband Market

- Fixed-line Market

• Sector Investment

• Policy and Regulatory

Environment

Market Trends and Outlook

• The Rise of Mobile Broadband

in Latin America

• Mobile Virtual Network

Operator Market Set to Take

Off

• WiMAX Gains Ground in

Latin America

• Market Outlook

Country Profiles

• Argentina

• Brazil

• Chile

• Mexico

• Peru

Currency Conversion Table

The Scope of this Report

Key References

Comparative Data

Reports Coverage

Current Environment — Key Points

• The Latin American telecommunications market showed strong growth over the past six months

despite the global economic slowdown still affecting several other world markets.

• Improved business conditions, the region’s large geographical size and strong levels of consumer

consumption spurred demand for mobile telephony, particularly in Brazil.

• The share prices of the top six leading companies dropped slightly by 1.22% on the NSYE over

the March-September period, but all stocks had rebounded by late September due to sustained

consumer spending and a recovery in investment.

• The level of merger and acquisition activity picked up in the region over the last six months, as

international telecoms companies looked to the region to target new opportunities, as other world

markets remained lackluster.

Industry Profile — Key Points

• Mexican and Brazilian telecoms companies dominate the Latin American telecommunications

industry.

• After the Asia Pacific, the region is home to the fastest growing telecoms markets in the world.

• The Latin American fixed-line broadband market lags behind most other regions of the world,

largely due to the costs of broadband for consumers and a lack of competition.

• Mobile broadband has grown in popularity in recent years due to the shift from fixed lines to

mobile phones. Geographical constraints on infrastructure have also boosted the mobile markets.

• Nevertheless, fixed-line services retain some market share, particularly in urban areas with good

infrastructure, where fixed-line costs challenge mobile services costs.

Market Trends and Outlook — Key Points

• Mobile broadband has become important to broadband services throughout Latin America driven by

an increase in 3G network deployments and upgrades to HSPA high-speed mobile data networks.

• With mobile penetration rates already above 100% in Argentina, Chile, Uruguay and Venezuela,

the mobile virtual network operator (MVNO) market is set to expand in Latin America.

• WiMAX is gaining ground in some markets, as there are many people in the region with no fixed

connectivity.

• Most Latin American telecoms markets are expected to show strong growth in 2011. The wireless

services markets throughout the region are particularly expected to grow robustly, thanks to the

accelerating deployment of high-speed internet access networks.

• Even so, the high cost of logistics and advertising and customer acquisition costs will limit the

number of players entering the market.

1

Latin America

Telecommunications Sectors

Adding Value to Information Since 1900

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

2

Copyright Statement

Copyright 2010 by Mergent, Inc. All Information contained herein is

copyrighted in the name of Mergent, Inc. and none of such information may be

copied or otherwise reproduced, repackaged, further transmitted, transferred,

disseminated, redistributed or resold, or stored for subsequent use for any

such purpose, in whole or in part, in any form or matter or by any means

whatsoever, by any person without prior written consent from Mergent.

http://www.mergent.com

Disclaimer

All information contained herein is obtained by Mergent, from sources believed

by it to be accurate and reliable. Because of the possibility of human and

mechanical error as well as other factors, however, such information is

provided “as is” without warranty of any kind. NO WARRANTY, EXPRESS

OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS,

MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF

ANY INFORMATION IS GIVEN OR MADE BY MERGENT IN ANY FORM OR

MANNER WHATSOEVER. Under no circumstances shall MERGENT have

any liability to any person or entity for (a) any loss or damage in whole or

in part caused by, resulting from, or relating to, any error (negligent or otherwise)

or other circumstance involved in procuring, collecting, compiling, interpreting,

analyzing, editing, transcribing, transmitting, communicating or delivering any

such information, or (b) any direct, indirect, special, consequential or incidental

damages whatsoever, even if Mergent is advised in advance of the possibility

of such damages, resulting from the use of, or inability to use, any such

information.

The Latin America Industry Reports are

published by Mergent, Inc., headquartered in

Fort Mill, South Carolina, USA. Each

industry sector report is updated every six

months. Mergent, Inc., a leading provider of

global business and financial information on

publicly traded companies, operates sales

offices in key North American cities as well as

London, Tokyo and Melbourne.

Publisher

Jonathan Worrall

Director

John Pedernales

Managing Editor

Peter O’Shea

Research Analyst

Kelly Ong Sheau Chi

Website:

http://webreports.mergent.com

Customer Service:

1800 342 5647 or 704 559 7601

email: [email protected]

Sales Enquiries:

Fred Jenkins - Executive Vice President, Sales

704 559 6897

email: [email protected]

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

3

Current Environment

The Latin American telecommunications sector showed

signs of recovery over the last six months with growing

demand for services and higher revenues reported by

leading companies. Improved economic conditions and

a strong rebound in consumer consumption spurred

significant demand for mobile telephony, particularly in

Brazil, with 174 million lines, a 15.5% growth in 2009,

making the country the world’s fifth largest mobile

telephony market by users, according to the National

Agency of Telecommunications (ANATEL).

The total value of spending on information technology

products and services in Brazil represented more than

20% of the Latin American market. This was driven by

fierce competition among operators, while tax cuts led

to a 3.9% increase in household consumption and more

flexible terms of payment. The growth was also aided

by plans announced by the Government in May plans to

invest R$3.2 billion (US$1.88 billion) to offer broadband

services for R$35 (US$20.60) per month through its state-

run telecoms company Telecomunicacoes Brasileiras SA

(Telebras). Industry experts forecast this will help boost the

number of the internet users steadily in months to come,

aided by government projects aimed at improving points of

access throughout the country.

In Mexico, mobile customer growth experienced a

considerable slowdown in the first quarter, a 37.8%

decrease from the previous corresponding period of 2009 to

1.75 million mobile users, due largely to a tough economic

climate, according to the Federal Telecommunications

Commission (COFETEL). Many rural parts of the country

remain under-served by mobile network infrastructure,

with operators having been generally slow to expand their

business presence there. In September fixed-line telephone

giant Teléfonos de Mexico SAB de CV (Telmex) (NYSE:

TMX) announced plans to invest approximately US$765

million in optical fiber networks in some parts of Mexico to

enhance the download speed by four times to 20 megabits

a second.

Chile meanwhile continued to be a highly developed

telecoms market in the region, spurred by a combination of

rising incomes, growing personal computer (affordability,

and favorable demographics. According to the Chilean

Telecoms Regulator (SUBTEL), mobile phones sales

increased by 9.71% from the first half of 2009 to

CLP$29.08 million (US$600,516) in the first six months of

this year. Additionally, in an attempt to boost competition

in both the Chilean mobile telecommunications and digital

TV markets, Chile’s Government announced in August it

would create a telecommunications infrastructure provider

to concentrate solely on service provision by renting out

its infrastructure to third parties. The purpose of the plan is

to encourage companies that enter the market to have the

necessary resources to provide their best service quality to

their customers.

After Peru opened its market to private operators in the

early 1990s, along with other market-oriented economic

reforms, Peru’s telecommunications penetration has

risen. It had around 22.9 million mobile subscribers in

June this year, with a mobile penetration of 79.3 lines per

100 inhabitants, according to data from the Ministry of

Transports and Communications (MTC). It had nearly

772,000 internet subscribers, a 3.3% increase from 747,235

internet subscribers in June, thanks to government efforts

to boost competition and encourage fixed-line investment.

In August, the Peruvian telecom regulator (OSIPTEL)

approved a 15% reduction in mobile phone termination

rates (MTRs) — a measure that could cut the retail price

for mobile services and could result in a 30% rise in mobile

traffic over the near term.

Further south, driven by high demand in mobile broadband

services and the large number of pre-paid subscribers in

the market, the Argentine telecommunications market

remained healthy. According to the National Institute of

Statistics and Census (INDEC), Argentina’s telecoms

market remained one of the most advanced in the region.

The total spending on information technology products

and services amounted to US$3 billion in 2009, while

industry experts forecast it could reach US$4 billion by

2012. About 92% of all internet users were broadband

subscribers, with broadband charges cheaper in Argentina

than in most other Latin American countries. As a result,

industry experts estimate broadband subscribers are likely

to grow this year even in the wake of the global economic

slowdown, albeit at a much slower rate than previous

years.

Sector Overview

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

4

Current Environment

Sector Performance

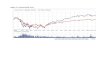

For the period from March 22 to September 20, the stock

prices of the top six leading companies by revenues as

tracked by Mergent dropped slightly by 1.22% on the New

York Stock Exchange (NSYE). Most stock prices were hit

hard in May when investors became more concerned about

the potential for fund withdrawals by foreigners from Latin

America and Europe as the sovereign debt problems in

Europe took their toll on markets.

Weaker-than-expected US data also weighed on stocks

and investor sentiment leading to a global sell-off on

fears of a waning economic recovery. As such, out of the

six companies, three Latin American telecoms company

stocks examined by Mergent lost an average of 12.15%

over the March-September period on the NYSE. These

were Tele Norte Leste Participações SA (NYSE: TNE),

Vivo Participações SA (NYSE: VIV) and Teléfonos de

Mexico SAB de CV.

After Brazil’s largest fixed-line phone company Tele Norte

Leste Participações SA, also known as Oi, announced it

would sell R$12 billion (US$6.78 billion) in stock to

existing shareholders as part of the Portugal Telecom

SGPS SA (NYSE: PT) agreement to buy a stake in Telemar

(BVSPA: TMAR5) in July, shares of Oi tumbled more than

17%. They fell to US$14.97 on July 16, the most since

December 2008 on the NYSE. Oi’s mobile-phone share

fell 19.74% in August, from 19.93% in the previous month,

after posting the smallest rise in new subscribers among its

closest rivals. Overall, its stock prices dropped US$4.06, or

14.07%, to US$14.07 on the NYSE on September 20.

Shares of the largest wireless carrier in Brazil, Vivo

Participações SA, also fell (by 7.89%) over the period to

US$25.92 on June 30, compared with US$28.14 on March

22 on the NYSE as the takeover battle between Spain’s

Telefónica SA (NYSE: TEF) and Portugal Telecom SGPS

SA raised uncertainty surrounding the future of Vivo. But

its share price rebounded and rose 13% from US$23.60 on

August 17 to US$26.67 on September 20 on the NYSE,

after Telefónica SA and Telecom SA reached an agreement

under which Telefónica bought Portugal Telecom’s stake

in Vivo for US$10 billion. Its plans involved combining

Vivo with its Sao Paulo-based fixed-line operator

Telecomunicacoes de Sao Paulo (NYSE: TSP).

The share prices of the biggest fixed-line telephone

company in Mexico, Teléfonos de Mexico SAB de CV,

remained insipid on the NYSE, closing at US$14.88 on

September 20, compared with US$16.53 on April 23,

after posting weak quarterly results as clients switched

to mobile services or cable providers’ voice plans. As of

Table 1: Leading Companies’ Share Price Movements on the New York Stock Exchange

Source: Mergent analysis, 2010

10%

-10%

0%

-20%

5%

-15%

-5%

-25%

2010 April May June July August

Telecomunicacoes de Sao Paulo

TIM Participações SA

Vivo Participações SA

Tele Norte Leste Participações SA

September

América Mõvil SAB de CV

Teléfonos de Mexico SAB de CV

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

5

Current Environment

late September, all leading Latin American telecom stocks

appeared to have recovered and were on the rise again. The

share prices of these companies were boosted by a rebound

in consumer spending and investment, after reassuring

comments from the US Federal Reserve Chief that seemed

to allay fears about the pace of economic recovery in the

US.

Leading Companies

Mexican and Brazilian telecoms companies continued to

dominate the Latin American telecommunications industry.

A Mergent analysis shows that the top seven companies,

as defined by total revenues in 2009, generated US$89.39

billion, a 34% increase from prior-year levels due largely

to the still low penetration rate and government support for

improving rural connectivity.

In 2009, all of the companies coped better with the global

economic downturn and continued to report solid growth

in revenues, except Brazil’s biggest fixed-line telephone

company, Tele Norte Leste Participações SA (BVSPA:

TNL3), also known as Oi. The company posted a net loss of

US$744.89 million in 2009, partly due to higher marketing

expenses, mostly linked to the campaigns to launch the Oi

fixed and Oi broadband portfolios nationwide. Nevertheless,

its net revenues more than double to US$17.13 billion in

2009, from US$8.04 billion a year earlier, due largely to the

expansion of its mobile user base and broadband internet

user base. The user base for fixed broadband in 2009 grew

to 4.21 million, up from 3.82 million in 2008. The addition

of its 3G broadband service added 64,000 new customers

in 2009. As a result, the number of broadband subscribers

to mobile and fixed-line services rose 18.8% to 741,000

in 2009.

Industry leader América Móvil SAB de CV (BMV: AMX)

reported total revenues up by 20.86%, from US$24.95 billion

in 2008 to US$30.15 billion in 2008. This was driven by a

faster increase of post-paid subscribers, strong demand for

wireless data services, following better coverage, quality

of service and an improved technological platform. The

company reported 36.79% year-on-year higher net income

to US$30.15 billion for the 2009 full year.

Despite the presence of large companies with a diversified

range of businesses locally and internationally, another

leading wireless operator in Brazil Vivo Participações SA

(Vivo) saw its net revenues jump 41.37% from US$6.64

billion in 2008 to US$9.38 billion in 2009. This was due

primarily to the growing substitution of fixed by mobile

traffic as a result of the penetration of mobile telephone

coverage in Brazil. The rise in its customer base in the last

quarters, improvements in its post-paid customer mix and

further activity in the pre-paid segment resulted in higher

sales. Vivo reported its net profit rose nearly twofold from

the previous year to US$491.54 million in 2009.

Mexico’s top provider of fixed-line telecommunications

services Teléfonos de Mexico SAB de CV (Telmex) saw its

net profit grow 7.37% from year-earlier levels to US$1.56

billion in the 2009 full year, thanks to lower financing

cost charges and income tax costs. However, Telmex’s

revenues improved slightly for the year, up 1.57% from

year-earlier levels to US$9.1 billion as demand fixed lines

weakened quite markedly. Demand for local and outgoing

Table 2: Leading Companies’ Share Price Movements on the New York Stock Exchange

Company Name Country TickerShare Price on Rise/Fall

(%)March 22 Sept 20

América Móvil SAB de CV Mexico AMX US$49.19 US$51.12 +3.92

Tele Norte Leste Participações SA Brazil TNE US$18.13 US$14.07 -22.39

Vivo Participações SA Brazil VIV US$28.14 US$26.67 -8.78

Teléfonos de Mexico SAB de CV Mexico TMX US$15.71 US$14.88 -5.28

Telecomunicacoes de Sao Paulo Brazil Telesp US$21.89 US$24.24 +10.74

TIM Participações SA Brazil TSU US$27.97 US$32.02 +14.48

Average Rise/Fall (%) -1.22

Source: Mergent analysis, 2010

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

6

Current Environment

international long distance calls picked up considerably

in 2009. Its total operating costs and expenses were

MEX$34.159 billion (US$2.71 billion) — 5% higher

than the prior year levels — after the company boosted its

marketing and advertising expenses to improve product

visibility and expand its market share.

In Brazil, fixed-line carriers Telecomunicacoes de Sao

Paulo SA (Telesp) and wireless carrier TIM Participações

SA showed positive financial results, with double digit sales

growth in 2009. Buoyed by strong demand for broadband

internet services, higher access lines and installation fees,

the Brazilian subsidiary of Spanish telecom giant Telefonica

SA, Telesp’s net profit rose by 20% in 2009 compared with

the previous year to US$1.04 billion. TIM Participações

SA reported its net profit grew by more than 59% from

US$77.27 million in 2008 to US$123.18 million in 2009.

This was largely due to higher sign-up fees in its post-paid

segment and continued demand for wireless broadband

with 41.1 million clients, a 12.9% year-on-year growth for

the 2009 full-year.

With multi-service package offerings that include several

telecommunications services with substantial discounts

(of up to 42%), Mexican-based telecommunications group

Telmex Internacional SAB de CV reported net revenues up

28.86% from US$5.49 billion in 2008 to US$7.07 billion

in 2009. Its net profit also surged 79.7% year-on-year to

US$730.46 million in 2009, driven by higher demand for

broadband services and other voice services. In an attempt

to capture more of Mexico’s broadband growth, Telmex

has sold almost two million computers on installment over

the last ten years.

Mergers and Acquisitions

Mergers and acquisitions continued to be the key means of

growing market share or entering a new market particularly

in Brazil. Many international telecoms companies

increasingly eyed this new and growing market niche

and continued to expand their presence in Latin America

to take advantage of the large and increasingly affluent

population. One of the most noteworthy deals in the

industry involved Telefónica SA, a Spanish-based telecom

company that signed an agreement with Portuguese-based

telecom company Telecom SGPS SA to buy its shares

in Brazilian mobile operator Vivo Participações SA at a

value of !7.5 billion (US$9.75 billion) on July 28. The

move complemented its faltering position in Brazil, with

the company planning to integrate its fixed-line operator

Telesp with Vivo and take a converged offering to the

lucrative enterprise market. This would make it one of the

leading telecommunications operators in Brazil.

In July, the largest telecommunications service provider

in Portugal, Portugal Telecom (NYSE: PT), paid up to

R$3.73 billion (US$2.20 billion) for a 22.4% stake in

Brazilian phone giant Oi operating unit Telemar Norte

Leste and R$4.24 billion (US$2.50 billion) for shares of

Telemar Participações, as part of a broader plan to expand

in Latin America. The move allowed Portugal Telecom to

gain a presence in Brazil, develop new technologies, gain

Table 3: Selected Financial Results of Leading Telecommunications Companies in Latin America (in US$)

CompanyDecember 31, 2009 December 31, 2008

Total Revenue Net Income Total Revenue Net Income

América Móvil SAB de CV 30,149,963,646 5,881,473,499 24,946,291,677 4,299,621,157

Tele Norte Leste Participações SA 17,128,690,937 (249,928,357) 8,036,028,119 494,960,314

Vivo Participações SA 9,379,872,017 491,536,852 6,635,069,113 167,138,319

Teléfonos de Mexico SAB de CV 9,097,458,090 1,563,521,272 8,956,810,157 1,456,189,672

Telecomunicacoes de Sao Paulo 9,054,614,909 1,245,613,699 6,853,521,177 1,037,945,933

TIM Participações SA 7,512,717,448 123,183,153 5,638,934,030 77,268,709

Telmex Internacional SAB de CV 7,068,665,453 730,460,268 5,485,345,048 406,390,215

Total 89,391,982,500 9,785,860,386 66,551,999,321 7,939,514,319

Source: Mergent analysis, 2010

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

7

Current Environment

scale in the growing Brazilian market and expand both

internationally and local operations.

With an aim to expand its market position in the fiercely

competitive Mexican wireless sector, Mexican telecoms

giant America Móvil SA de CV acquired 92.27% of the

shares in fixed-line carrier Telmex Internacional SAB de

CV in a cash and stock transaction valued at approximately

MEX$1.9 billion (US$150.76 million) in June.

Simultaneously, American Movil also acquired a 99.4%

stake in Carso Global Telecom SAB de CV, an investment

holding company operating in the telecommunications

industry. The acquisition not only made America Móvil a

full-service provider to offer converged wireless, wireline

voice, broadband and video services to over 250 million

subscribers, but also created a telecom powerhouse better

placed to take on rivals like Spanish-based Telefonica SA.

Nevertheless, some analysts warned that the tie-up would

be a drag on America Movil as shares of Telmex were

the worst performing stock in Mexico’s benchmark IPC

index last year and had lost value since mid-2008. Despite

uncertainty and concerns, the consolidation will dilute

America Movil’s value. Some analysts say the company has

strong growth potential and its shares will keep expanding

quickly over the next several years in Latin America as

Telmex plans to upgrade its wireline broadband network

with up to 20 Mbps speed capabilities.

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

8

Industry Profile

The overall Latin American telecoms market is still

relatively small as a regional service market, accounting

for about 10% of total global revenues in 2009, according

to the International Telecommunication Union (ITU).

Nevertheless, the region has become the fastest growing

telecoms market in the world, after the Asia-Pacific. A

combination of large geographical size and population,

rising disposable incomes and sustained investment in

mobile networks in recent decades has driven significant

growth in the region’s telecoms markets in recent years.

Brazilian telecoms companies dominate the market and

accounted for 52.48% of total telecom revenue in 2009.

A Mergent analysis shows that the top eight companies

by 2009 revenues posted combined revenues of US$95.63

billion, while Mexican telecoms companies — America

Móvil SAB de CV, Telefonos de Mexico SAB de CV and

Telmex Internacional SAB de CV — stood at US$45.44

billion in 2009.

Fixed-line Broadband Market

Given the average fixed-line broadband penetration in

the region is less than 10%, Latin America lags behind

many other regions of the world. According to a study

from the ITU, the total number of broadband internet

users in Latin America jumped by 38.2% from year-earlier

levels to 27.7 million in 2008. Apart from Caribbean

islands, almost one third of the region’s internet users

were in Brazil, while the highest user penetration rates

were found in Argentina and Chile. A report from the

OECD shows that the northern band comprising the US

and Canada enjoyed 73% internet user penetration, while

South America stood at about 34% last year. This was due

largely to the costs for broadband in the region and a lack

of competition.

For instance, the lowest monthly subscription rate for

broadband in the OECD countries averages US$19 in

purchasing power parity (PPP), while such services cost

US$29 and US$35 in Mexico and Chile, respectively, in

2009. The average connection speed in those countries

is normally 17 megabits per second (Mbps), while in

the most advanced countries in Latin America and the

Caribbean; however, it is no higher than 2 Mbps.

Mobile Broadband Market

In Latin America, mobile broadband has started to become

increasingly popular as people use their mobile phones

more often. Mobile service provider 3G Americas reports

that mobility serves more than half a billion users in Latin

America, with the average wireless penetration exceeding

86% in 2009, thanks to a hefty price drop, competitive

pricing and a saturated mobile voice market. Many mobile

operators offer very competitive capped data packages. As

such, the mobile telephony market in the region performed

strongly in 2009, with mobile subscriptions totaling 88.2%

of the region’s total population, compared with 55.2% in

the Asia-Pacific and 90.4% in North America, according

to ALACEL.

The global system for mobile communications and high-

speed packet access — GSM-HSPA — continues to be

the overwhelming mobile wireless technology leader for

mobile broadband deployments. The explosion of third

generation partnership project (3GPP) mobile broadband

subscriptions has highlighted the growing interest of mobile

use of advanced 3G technology services and applications,

and the growing proliferation of smartphones. The total

number of GSM-HSPA subscriptions in Latin America

comprises 91% market share in Latin America with more

than 464 million connections in 2009, of which 9.4 million

were 3G connections in 2009.

Fixed-line Market

Latin America’s largest fixed-line operator in terms of lines

in service is Telmex Internacional SAB de CV, controlled

by Mexican billionaire Carlos Slim. In terms of revenue,

Brazil’s Oi (Telemar) is in the lead, having overtaken

Telmex in 2007. The performance of Latin America’s fixed-

lines services was hit hard by cheap deals for mobiles and

mobile internet, the shift from fixed-lines to mobile phones

and geographical constraints on infrastructure expansion

particularly the remote Andean or rainforest regions. A

2009 study from ITU shows Latin America’s fixed-line

penetration comprised only 18.6% of the total population

and the fixed-line market grew by an average of 2.5% per

year in Latin America between 2004 and 2009, well below

Industry Size and Value

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

9

Industry Profile

growth rates for mobile subscriptions. Nevertheless, fixed-

line services will retain some market share, particularly

in urban areas with good infrastructure, where fixed-line

costs can challenge mobile services.

Sector Investment

There are increasing numbers of foreign investors who

are keen to invest in Latin America due to their large

populations and the demand for high-speed mobile services.

There is also a greater proportion of capital flowing within

Latin American markets, with the deregulation of most

countries’ markets in recent years. Last September, French

entertainment and telecoms group Vivendi SA (PAR: VIV)

announced plans to invest US$2.9 billion in a leading

alternative telecom operator in Brazil, GVT (BVSPA:

GVTT3). The aim was to seek growth in emerging markets

like Brazil. The friendly all-cash offer for GVT was for

approximately !2 billion (US$2.72 billion). The deal will

not only give GVT much greater scope to expand, but could

also accelerate the growth of its fixed-line telephone and

internet services into cities dominated by the competition.

In November 2009, Vivendi purchased around 37% of

GVT shares and had signed a deal to buy a further 19%

stake via irrevocable options with third parties.

Other firms are also continuing their push into emerging

markets, with some like Spanish telecom giant Telefonica

last December announcing plans to invest R$1.14 billion

(US$671.38 million) in Brazil by end of this year.

Telefonica has been facing a fall in revenue from its fixed-

line business in Spain. To address this Telefonica plans

to offer more competitively internet access plans. It also

announced it could acquire 21% of a pay television business,

Digital+, for !470 million (US$639.45 million) to develop

audiovisual and other businesses in Spain to strengthen the

content offering of its pay-TV service Imagenio.

Policy and Regulatory Environment

In May, the Brazilian Government launched R$11 billion

(US$6.48 billion) broadband program to improve access

to broadband internet services to low-income households.

The national broadband plan (PNBL) not only aims to

revive Telebras, the former state telecom monopoly, but

also aims to quadruple the number of municipalities with

internet broadband access by 2014, or the equivalent to 40

million households. A national fund for telecommunications

investments, known as Funntel, will finance additional

R$1.75 billion (US$1.03 billion) in research and

development to kick off the program.

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

10

Market Trends & Outlook

Mobile broadband has become important to broadband

services throughout Latin America driven by an increase

in 3G network deployments and upgrades to HSPA

high-speed mobile data networks. According to a study

by a wireless industry trade association, 3G Americas,

the Latin American and Caribbean regions continued

to see a dramatic increase in market share for 3GPP

technologies, rising to 92% at the end of the first quarter

of 2010. 3GPP technologies added a total of 68.6 new

connections, including 12.6 million Universal Mobile

Telecommunications System-High Speed Packet Access

(UMTS-HSPA) subscriptions, with a number of 486

million subscribers in the first quarter of 2010. This was

due largely to the rise of flat rate mobile data pricing,

further smartphone shipments and the greater availability

of high-speed mobile broadband.

The continuous effort of wireless operators in Latin America

to invest in mobile broadband infrastructure, devices and

innovative services, has produced a healthy jump in the

data contribution to service revenues reaching 19% in the

first half of 2010. The success of Apple’s iPhone and other

smartphones that offer downloadable applications through

their stores and allow customers to use thread-party VoIP

clients over WiFi and cellular broadband networks is

fueling the trend. Mobile broadband is a huge opportunity

for the telecommunications industry throughout the region.

Analysys Mason, a UK-based analyst firm, forecasts that

Latin America’s wireless network traffic is likely to reach

a 86% in compound annual growth rate (CAGR) over the

next five years.

Mobile Virtual Network Operator Market Set to Take

Off

With mobile penetration rates already above 100% in

Argentina, Chile, Uruguay and Venezuela, the mobile

virtual network operator (MVNO) market is set to expand

in Latin America. As of May 31, 2010, Latin America

represented a small share of the world’s 104 million

MVNO subscriptions, with the MVNO market only

having around 20 active MVNOs in the region, out of 550

MVNOs or resellers worldwide, according to ALACEL.

As such, MVNOs could play a bigger role going forward.

Mobile network operators now see MVNOs as a good

opportunity to grow their subscriptions and revenues by

offering mobile services.

For instance, Telecom Argentina (NYSE: TEO) negotiated

an MVNO agreement in August with Uruguay’s state-

owned telecoms company, Antel, to offer mobile telephony

in Uruguay’s mobile market. In Mexico, cable TV operator

Megacable recently unveiled plans to launch an MVNO

operation in Mexico in partnership with Telefonica SAB de

CV. Megacable has over 1.7 million cable TV subscribers in

more than 200 local markets, and is one of Mexico’s largest

triple play providers. Through the partnership, Megacable

became the first firm in Mexico to offer quad-play offering

of mobile, fixed-line phone, internet and TV. According to

figures released by Informa Telecoms & Media, MVNO

subscriptions in Latin America could grow at a CAGR of

28% to 6.6 million by 2013.

WiMAX Gains Ground in Latin America

WiMAX is gaining ground in some Latin American

markets, as there are many people in the region with no

fixed connectivity. WiMAX plays well in environments

in which the business model is developing from being an

alternative to wired broadband access into a means for

strengthening operator offers through service bundling.

Additionally, WiMAX is also used to penetrate markets

where operators still do not have a fixed-line network.

With relatively little construction and infrastructure in

rural areas, it is easy to install a tower and power an area

reaching up to 30 miles with high-speed internet. Major

urban centers like Sao Paulo, Buenos Aires, and Mexico

City won’t be the only ones to benefit; eventually remote

communities that currently have no broadband internet

services will be able to access such wireless features.

According to research from market intelligence company

ABI Research, the number of WiMAX subscribers in the

region will increase eightfold from 500,000 in 2009 to

approximately 4.5 million at the end of 2015.

Market Outlook

Most Latin American telecoms markets are expected to

show strong growth in 2011. The wireless services markets

The Rise of Mobile Broadband in Latin America

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

11

Market Trends & Outlook

throughout the region are particularly expected to grow

robustly, thanks to the accelerating deployment of high-

speed internet access networks, the implementation of

mobile broadband along with packages targeted at low-

income and higher-income consumers. All these factors are

likely to drive the regional equipment market. Meanwhile,

mobile data revenues in the region are projected to grow

rapidly, due largely to the acceleration in deployment

of advanced technologies, an increasingly competitive

market, and growing consumer demand for mobile data

services driven by popular data-optimized devices such as

Apple’s iPhone.

According to the ITU, the mobile penetration rate in Latin

America is well ahead of the world average, reaching 93%

in mid-2010 compared to a global rate of around 73%.

Given that mobile growth is slowing in Latin America and

that there is intense competition over bundled services,

the MVNO market should grow further, with many fixed-

line operators opting for an MVNO model to add mobile

services to their current service portfolio of telephony,

internet and in some cases pay TV.

Nevertheless, the high cost of logistics and advertising and

customer acquisition costs will limit the number of players

entering the market. As a result, the Brazilian telecoms

regulator ANATEL plans to launch new MVNO regulations

this year, in order to attract more foreign operators into the

market. The Mexican telecoms regulator COFETEL is also

planning to work on a new rule to bring more competition

to the industry, including the auction of wireless spectrums

early next year. Looking forward, competition looks set to

intensify as additional 3G spectrums are released and more

MVNOs enter the market. Rural coverage will remain a

major focus over the near term, while wireless technologies

are likely to remain a popular choice for encouraging the

continued expansion of telecoms services into remote

areas. Broadband growth will be from investment in both

fixed and wireless technologies, allowing remote towns

and cities to get online.

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

12

Country ProfileArgentina

Argentina’s telecommunications industry remained strong

in 2009, with two of its top telecoms companies recording

year-on-year increases in revenues fueled by improving

confidence in the employment market. According to

INDEC, Argentina has the largest mobile market in the

region with many mobile users signed up for multiple

mobile accounts. Its mobile telephony market has saw

steady growth of 25.5% over the past two years, with 50.4

million mobile lines in service and a penetration rate of

120.6% at the end of 2009. Altogether, wireless telephony

traffic reached 4.74 billion calls in December 2009,

representing an increase of 24.7% compared to the same

months in 2008, according to INDEC.

Nevertheless, the number of fixed-line telephone subscribers

showed tepid growth by just 0.2% in 2009, from 9.74

million in 2008 to 9.76 million in 2009, according to data

from INDEC. The number of public phones nationwide

dropped 8.5% year-on-year to reach 142,800 in 2009.

This was because the Government fixed the telephone

rate after a sharp devaluation of the Argentine currency.

Many telecoms companies aggressively moved into

internet access and mobile phone services where prices

are unregulated by the Government. INDEC data shows

the average annual rate of mobile broadband enjoyed the

highest growth rate of 24% in 2009, followed by mobile

telephony.

Leading Companies

Telefónica de Argentina

Spanish-owned Telefónica de Argentina is the largest

mobile operator in terms of revenue in Argentina. It

provides broadband, local and long distance telephone

services nationwide. In the first half of 2010, the company

generated revenues of !1.44 billion (US$1.96 billion), up

8.2% over the same period in 2009. This was mainly due

to higher sales from mobile and fixed-line sectors, which

grew 17.4% to !920 million (US$1.25 billion) and 10.5%

Sector Overview

Table 4: Key Telecoms Statistics, 2007 — 2009

Category 2007 2008 2009

Fixed Line

Total Subscribers 9,430,000 9,740,000 9,760,000

Penetration Rate (%) 24.0 24.5 24.3

Annual Growth (%) -0.3 3.4 0.2

Mobile Telephony

Total Subscribers 38,560,000 43,700,000 48,400,000

Penetration Rate (%) 98.0 110.0 120.6

Annual Growth (%) 28.0 13.0 11.0

Internet

Total Users 16,000,000 20,000,000 23,000,000

Penetration Rate (%) 40.7 50.3 57.3

Annual Growth (%) 23.0 25.0 15.0

Broadband

Total Subscribers 2,560,000 3,470,000 4,300,000

Penetration Rate (%) 6.5 8.7 10.7

Annual Growth (%) 61.0 35.0 24.0

Source: National Institute of Statistics & Census

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

13

Country Profile - Argentina

to !566 million (US$770.06 million), respectively, in the

first half of 2010. As such, with strong growth in wireless

accesses, the sharp rise in fixed broadband customers and

stable fixed-line telephony accesses, the company reported

a total of 22.4 million accesses at the end of June, up 6.8%

over the same period the previous year.

Telecom Argentina SA (BUE: TECO2)

Buenos Aires-based Telecom Argentina SA is one of the

leading telecommunications companies in the country,

offering voice, data transmission, internet, telephone

services and other wireless telecommunication services.

In the first quarter of 2010, it saw its consolidated net

revenues amount to ARS$3.25 billion (US$820.19 million)

in the first quarter ended March 31, a 15% increase from

the corresponding period of 2009. This was due primarily

to higher mobile service revenues, with further demand

for smartphones, new applications and social networks

services. Telecom Argentina SA saw its net income rise

by 17% from ARS$341.13 million (US$86.09 million) in

the same period of 2009 to ARS$411 million (US$103.72

million), due to a bigger subscriber base and strong growth

in mobile services. Nevertheless, administrative and selling

expenses for the quarter were up nearly 15% from the same

period of last year to ARS$2.49 million (US$0.63 million)

as a result of inflationary effects on the cost structure and

greater expenses related to competition in mobile and

internet businesses.

Market Outlook

There should be further growth in the number of mobile

telephony subscriptions for the remainder of this

year. Wireless broadband access services will become

increasingly popular over the next 12 months due to a

shortage of fixed broadband accesses outside urban areas,

the expansion of 3G networks and the freeze on fixed-line

telephony rates. Argentine telecoms operators estimate that

broadband business may outstrip the income of their fixed-

line services, with internet business forecast to grow by

15% this year. However, the Government shut down Grupo

Clarin SA’s (BUE: GCLA) internet service — Fibertel

SA — on August 19 after the company was accused of

operating illegally in the telecoms and broadband industry.

Industry experts estimate that the elimination of Fibertel

will start the virtual monopolies on broadband service and

choking off competing internet service providers.

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

14

Country ProfileBrazil

Brazil remained the largest telecommunication market

in Latin America in terms of the number of subscribers

in 2009, due to the country’s growing fixed-line and

mobile telephony base. The country had 227.1 million

subscribers in 2009, a 12.5% increase in 12 months,

according to ANATEL. The number of mobile subscribers

in Brazil rose from 174 million to 185 million between

January and June 2010, accounting for 90.6% of the total

population. However, Brazil had only 41.7 million fixed-

line subscribers, a 1.3% increase over the previous year,

with demand for mobile telephony overtaking that for

fixed-line. According to ANATEL, Brazil was the world’s

third fastest growing market for wireless users, after China

and India, attracting both domestic and international firms

to invest in the wireless segment.

Industry Size and Value

As of December 31, 2009, the Brazilian telecoms market,

including fixed and mobile phone segments, had four

major players. They were Oi, also known as Tele Norte

Leste Participações (BVSPA: TNL3), Vivo Participações

SA (BVSPA: VIVO3), Telecomunicacoes de Sao Paulo

SA (BVSPA: TLPP) and TIM Participações SA (BVSPA:

TCSL4). A booming mobile phone market and growth

in fixed-phone and broadband segments helped Brazil’s

largest mobile network operator, Oi to expand its client

base from 59.72 million in the previous year to 62.6 million

in the second quarter of 2010. TIM Participações SA also

announced its mobile subscriber base grew 17.4% year-

on-year to 44.4 million lines in June this year. With the

country’s economic recovery underway and the spending

power of Brazilian consumers on the rise, demand should

remain strong for telecom services over the next 12 months,

particularly broadband and mobile telephony segments.

Leading Companies

Tele Norte Leste Participações SA

(BVSPA: TNLP3, TNLP4)

Tele Norte Leste Participações SA (TNL) is the largest

telecoms operator in Brazil, offering services in the fixed

and mobile segments, data transmission, broadband

internet access, internet provider and other services. As

of December 2009, its wireless segment had about 36.11

million users while its traditional fixed-line telephone

service had more than 21 million subscribers.

During the second quarter, TNL saw its consolidated gross

revenue rise by 1.3% from the previous corresponding

period of 2009 to R$7.39 billion (US$4.35 billion), driven

by the rapid expansion of mobile broadband services. Its

consolidated EBITDA reached R$2.67 billion (US$1.57

billion) in the second quarter, with a 9.2% increase from the

previous year. The increase followed higher profitability

from customers in its mobile segment, better operating

performances and cost reduction initiatives in the process

of integrating management. TNL posted net earnings of

R$444 million (US$261.48 million) in the second quarter

of 2010, from a net loss of R$146 million (US$85.98

million) in the previous year.

Vivo Participações SA (BVSPA: VIVO3)

Vivo Participações SA (Vivo) is the joint venture of the

wireless operations owned by Portugal Telecom and Spain’s

Telefónic with a market share of around 30% in Brazil.

Vivo provides mobile telecommunication services, cellular

phone data transmission, mobile internet services, voice

and ancillary services and wireless application protocol

services. In the second quarter of 2010, Vivo saw its total

revenue grow 9.9% from the previous corresponding

period of 2009 to R$4.4 billion (US$2.59 billion), thanks

to a higher number of mobile internet users. Vivo’s wireless

data service revenues grew by 10.7% over the previous

corresponding period of 2009 to R$4.13 billion (US$2.43

billion) in the second quarter of 2010. Its EBITDA for the

second quarter also rose, by 10.6%, from the same quarter

of the previous year to R$1.34 billion (US$0.79 billion).

However, the company recorded higher total operating

costs from R$3.6 billion (US$2.12 billion) in the previous

corresponding period of 2009 to R$3.9 billion (US$2.30

billion) in the second quarter due to a jump in advertising

expenses, third party services as well as an increase in

expenses arising from higher service revenues.

Market Outlook

Brazil’s telecommunications market is expected to grow

this year, with wireless services remaining the main driver

of industry growth. The Brazilian Government’s R$11

Sector Overview

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

15

Country Profile - Brazil

billion (US$6.48 billion) in broadband funding will also

boost the market. The Government is also planning to

distribute free mobile handsets to low-income groups to

boost mobile penetration levels, while it’s plan auction

off frequencies for WiMAX and 3G services should also

provide a boost to the market. The plan not only will

reach 30 million fixed broadband accesses and 60 million

mobile broadband potential subscribers, but should

shake up telecoms operators and drive them to improve

customer services. Nevertheless, a shortage of fixed-line

infrastructure and expensive broadband prices may inhibit

the growth of broadband to some degree.

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

16

Country ProfileChile

The Chilean telecommunications market remained one

of the most technologically advanced in Latin America

over the last year. According to SUBTEL, it was the first

country in the region to roll out services such as mobile

WiMAX, IPTV, wireless TVoIP, triple play, EDGE, and

mobile voice-to-text. As of December 31, 2009, Chile had

become the first country in Latin America and the fifth in

the world after Sweden, Norway, Japan, and the US, to test

Long Term Evolution (LTE) technology.

After the Chilean Government approved the introduction

of mobile number portability and enabled new players to

focus solely on rolling out services, the sector experienced

aggressive competition with affordable and attractive

pricing packages that include flat-rate or bundled cellular

services. The demand for wireless mobile broadband

connections was strong over the last year. A 2009 survey

by SUBTEL found that Chile had 15.74 million mobile

subscribers in March 2010, with a household penetration

rate of 92.5%, up significantly from 87.8% in the same

period of 2009. The number of 3G mobile users grew more

than threefold from 190,825 subscribers in the same period

of 2009 to 894,682 in March of 2010.

Leading Companies

Movistar Chile

Movistar Chile, formerly known as Telefónica Chile SA, is

a subsidiary of Spanish broadband and telecommunications

provider Telefónica SA (NYSE: TEF). It is the largest

mobile operator in Chile engaged in data transmission,

broadband, WiFi, public telephones, terminal equipment

sales, leasing and other value-added services. In fiscal 2009,

Movistar Chile posted a net profit of CLP$43.5 billion

(US$89.83 million) in 2009, a 9.3% drop from CLP$48

billion (US$99.12 million) in 2008. Its total revenues also

fell by 5% from the prior-year levels to CLP$711 billion

(US$1.47 billion) in 2009, thanks to a drop in the fixed

mobile interconnection charges introduced in January

2009. With a 4% increase in broadband revenues and a

9% increase in broadband subscribers to 774,656 in 2009,

Movistar Chile estimates that market share of fixed-lines

in service will decline over the next five years to reach

approximately 40.8% in 2014. The company allocated

US$600 million in both cellular and fixed networks sectors

to build faster fiber-optic broadband networks nationwide.

Empresa Nacional de Telecomunicaciones SA

(BSAN: ENTEL)

With a 39% share of the mobile market in Chile, Empresa

Nacional de Telecomunicaciones SA is the second largest

mobile operator in the country. The company also provides

wireline services such as data networks, local telephony,

internet access, long distance, IT services network rentals

and wholesale traffic services. In 2009, Entel’s customer

base grew by 8% from year earlier levels to 6,457,335

subscribers due to the reduction in access charges, the roll

out of new mobile broadband access solutions and other

value-added services such as mobile internet and email

access. ENTEL posted a 26% jump in EBITDA from

CLP$71.04 billion (US$146.70 million) in 2008 to CLP$96

billion (US$198.24 million) in 2009. Its total revenue also

rose by 7% from year earlier levels to CLP$285 billion

(US$589.53 million) in 2009, driven largely by demand

for Apple’s iPhone 3GS and other smartphones.

Market Outlook

The Chilean telecoms sector is set to see growth in the

mobile and broadband markets for the next two years, with

a highly developed infrastructure, growing incomes and a

well-functioning financial market. Subtel plans to launch

an auction for spectrum in the 2.6GHz band intended for

4G services at the end of this year, to be awarded mid-2011.

This will not only coincide with the introduction of number

portability, but also boost competition by strengthening

other smaller network operators’ positions against top

players in the market.

Sector Overview

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

17

The Mexican telecommunications industry enjoyed healthy

growth of 12.9% during the first quarter of 2010, according

to COFETEL. In the first quarter of 2010, COFETEL data

shows the total amount of fixed-lines dropped 5.4% during

the first quarter of 2010 to 19.34 million after low-cost

access to mobile telephony allowed lower income groups

to boost their use of mobile phones. The total number of

mobile telephone users was up 17.7% year-on-year to 85.3

million in the first quarter.

With the expansion of new services and attractive

promotional plans, the TV industry also saw growth.

According to COFETEL, the number of cable TV subscribers

grew by 5.8% year-on-year to 5.15 million users in the

first quarter of 2010. The satellite TV segment registered

a 78.9% surge in the number of subscribers, making it the

fastest growing segment in the telecoms industry during

the first quarter of 2010. Microwave TV (MMDS), on the

other hand registered its worst performance ever, down

35.8% from previous-year levels to 439,000 users in the

first quarter of 2010 due to the popularity of satellite TV

channel options.

Nevertheless, a lack of competition in telecoms held

back growth to some extent. America Movil SAB de CV

dominated Mexico’s telecoms industry, with a 72% market

share as of February 2010, while its subsidiary Telefonos de

Mexico SAB de CV, known as Telmex (BMV: TELMEX),

controlled about 80% of the fixed-line market. In an attempt

to end the monopoly over the country’s telecom market

the Government in May 2010 started a tender process to

auction off wireless airwaves. The auction will include

90 megahertz of spectrum in the 1.7 gigahertz band and

30 megahertz in the 1.9 gigahertz band, airwaves suitable

for third-generation wireless services such as high-speed

internet access.

Leading Companies

América Móvil SAB de CV (BMV: AMX)

América Móvil SAB de CV is the largest mobile network

operator in Latin America in terms of revenues. With most

Latin American economies expanding throughout the

second quarter of 2010, América Móvil saw its consolidated

revenues jump by 11.9% from the previous corresponding

period of 2009 to MEX$100.9 billion (US$8.01 billion)

in the second quarter of 2010 due to strong growth in

wireless data service revenue. The share of data in service

revenues continued to climb in the second quarter, up

10.8% from MEX$80.14 billion (US$6.36 billion) in the

second quarter of 2009 to MEX$88.77 billion (US$7.04

billion). The quarter’s EBITDA also rose, by 9.4% from

year earlier levels to MEX$42 billion US$3.33 billion).

The company added 4.9 million wireless subscribers in

the second quarter — 30.7% more than in the same period

of last year. Nevertheless, its second quarter net profit fell

17.9% to MEX$18.7 million (US$1.48 million) due to

depreciation costs.

Telefonos de Mexico SAB de CV (BMV: TELMEX)

Telefonos de Mexico SAB de CV, known as Telmex, is

a Mexican-based telecoms operator that has nearly 80%

share of Mexico’s fixed-line market. The company’s

service coverage comprises the operation of local and

long distance networks. In the second quarter 2010, the

company saw its net revenues fall 4.6% from MEX$27.09

billion (US$2.15 billion) in the second quarter of 2009 to

MEX$28.4 billion (US$2.25 billion) due to lower average

realized selling prices. The company posted a 37.5% drop

in its second quarter net profit from MEX$2.25 billion

(US$178.53 million) in the same period of last year to

MEX$3.6 billion (US$285.65 million) after it continued to

lose clients to wireless operators and other competitors. As

a result, Telmex proposed building its internet business to

make up for a decline in its fixed-line and long-distance

telephone revenues.

Market Outlook

The Mexican telecommunications industry is expected

to grow throughout the rest of 2010. The auctioning of

access to the national fiber network and additional mobile

spectrums is expected to boost the market and competition,

which should help pull down prices for consumers. The

move may also facilitate the entry of new competition in

the industry, with the expansion of new services. Some

Country ProfileMexico

Sector Overview

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

18

Country Profile - Mexico

industry experts forecast broadband will remain the driver

of growth for most fixed services providers. Fixed-line

customers will likely migrate to wireless alternatives as

they begin to rely on mobile only communication access,

in part spurred by their need to reduce household costs.

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

19

After Peru opened its telecommunications market to private

players in the early 1990s, the Peruvian telecommunications

sector has seen tremendous growth, with the rapid

expansion of telephony and mobile telephony services.

According to the MTC, the total fixed-line subscriber

base increased by 3.57% from 2.88 million subscribers in

2008 to 2.98 million in 2009. The total number of wireless

mobile subscribers also rose by 12.07% from year earlier

levels to 23.48 million in 2009, according to the MTC.

Nevertheless, the average telephone density in Peru

remained the lowest in Latin America, with only 10.2

lines per 100 inhabitants in 2009 due to expensive calling

rates. The local telephony market is mainly dominated by

Telefónica del Perú SAA (Telefonica) with a 97% market

share of the Peruvian fixed-line market, followed by

Movistar, which is also owned by Spanish-based telecoms

giant Telefónica SA.

The Peruvian Government opened up its market to

attract more mobile operators to improve competition in

the country. In an attempt to maintain its market share,

Peru’s largest telecommunications company Telefónica

del Perú announced early this year it would invest US$1.5

billion between 2010 and 2013 to develop a core fiber

optic communications network to improve the speed and

coverage of broadband internet nationwide.

Leading Companies

Telefónica Del Perú SAA

Telefónica del Perú SAA (Telefonica) is a subsidiary of the

Spanish telecommunication service provider Telefonica

SA and offers various services including fixed and mobile

telephony services, domestic and international long-

distance calls, public telephony, internet access, facsimile

transmission services, electronic voice messaging and

cable television services. In the first quarter of 2010, the

company saw its total revenues drop 3.8% from the same

period of last year to S/.938 million (US$336.3 million),

due to lower revenues in local telephony, long distance

and interconnection services. Local telephony and long

distance revenues fell 6.8% and 12.8% from the previous

corresponding period of 2009 to S/.311 million (US$111.49

million) and S/.66 million (US$23.67 million) in the first

quarter of 2010, respectively. This was due largely to a

decline in fix-lined demand, lower use of pre-paid cards

and the shift of fixed-line minutes to the mobile network.

As such, its net income declined 20.2% from the same

period of last year to S/.155 million (US$55.57 million).

Nextel Del Perú SA

Nextel Del Peru SA is one of the subsidiaries of Boston-

based mobile operator NII Holdings Inc (NESDAQ:

NIHD). Nextel del Peru offers a fully integrated wireless

communications tool nationwide with a digital two-way

radio feature, digital telephone interconnection, text and

numeric paging and wireless internet access. In the first

half of 2010, the company saw its net revenue increase

13.55% from US$149.2 million in the first half of 2009

to US$268.4 million as the results of improving growth

trend in the wireless business and stabilizing growth in

wireline business continued to drive the company’s sales

upward. The company added 60,400 net subscribers to

its network, bringing its subscriber base to 965,900 in the

first half of the year, a 29.1% increase from the first half

of 2009. Nevertheless, the company suffered a net loss

of US$22.8 million in the first half of 2010, from a net

profit of US$400,000 in the first half of 2009 due to pricing

pressure on mobile services, lower handset sales and a rise

in expenditure.

Market Outlook

With intensifying competition in the telecommunications

sector, MTC forecasts broadband prices in Peru could fall

in 2011. The Peruvian Government announced in February

it would invest S/.260 million (US$93.2 million) via the

Telecommunications Investment Fund (Fitel) over the next

five years to expand coverage in Peru’s Andean highlands.

The installation of telephone lines in isolated villages

may help reduce agricultural costs and increase farmers’

income. FITEL announced in August that some US$400

million would be allocated to finance the deployment of a

fiber optic transport network in areas that are not currently

covered by private operators. This should help boost the

Peruvian telecoms sector for several years to come.

Country ProfilePeru

Sector Overview

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

20

Currency Conversion Table

Source: Federal Reserve Bank of New York

Note: Base currency is US Dollar (US$)

Currency exchange rates as of September 30, 2010

Currency Unit Units per US$ US$ per unit

US Dollar (US$) 1 1

Argentine Peso (ARS$) 3.9625 0.25237

Brazilian Real (R$) 1.6980 0.58893

Chilean Peso (CLP$) 484.250 0.002065

Mexican Peso (MEX$) 12.6029 0.07935

Peruvian Nuevos Sole (S/.) 2.78950 0.358487

EMU Euro (!) 0.735005 1.36054

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

21

The Scope Of This Report

This report examines the telecommunications sectors in Latin America, with special focus on Argentina, Brazil, Chile,

Mexico and Peru. The report aims to give a general picture of the current environment as well as global and regional affairs

that influence the development of the various segments of the industry, using available data. As part of these industries, a

number of industry segments are examined, namely: voice and data, wireless services and equipment makers.

Research analysts draw on a range of credible industry and company data sources as well as news and information services

to research and analyze the current trading environment, industry landscape and market trends and outlook for a particular

sector. Primary sources are used, unless otherwise indicated, and include company data, e.g. annual reports and company

financial results: macroeconomic and trade data; data information from global and country regulatory, industry and trade

bodies; government data; and reports; and reports from industry organizations and private research organizations.

The following SIC codes are relevant to the industry. For the services side: 4812 (Radiotelephone Communications); 4813

(Telephone Communications, excl. Radio); 4822 (Telegraph and Other Communications) and 4899 (Communications

Services). For the manufacturing segment: 3661 (Telephone and Telegraph Apparatus); 3663 (Radio and TV

Communications Equipment) and; 3669 (Communications Equipment).

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

22

Key References

Global and Regional

Analysys Mason

Analysys Mason is an adviser on telecoms, technology and media.

http://www.analysysmason.com

The Economic Commission for Latin America and the Caribbean (ECLAC)

Established in 1948, the ECLAC aims to contribute to the economic development of Latin America, coordinate efforts,

and reinforce economic relationships among countries. Headquartered in Santiago, Chile, it is one of five regional

commissions of the United Nations.

http://www.eclac.org

International Telecommunication Union (ITU)

ITU is an agency of the United Nations and regulates information and communication technology issues.

http://itu.int/

New York Stock Exchange (NYSE)

The NYSE is a stock exchange based in New York City. It is the largest stock exchange in the world by dollar volume.

http://www.nyse.com

Organisation for Economic Cooperation Development (OECD)

The OECD is a group of 30 member countries that share a commitment to democratic government and the market economy.

The OECD plays a prominent role in fostering good governance in the public service and in corporate activity.

http://www.oecd.org

Argentina

Buenos Aires Stock Exchange (BCBA)

Established in 1854, it is the principal stock exchange in Argentina.

http://www.cei.gov.ar

Fibertel (FIBERTEL)

Fibertel is an Argentine internet service provider.

http://www.fibertel.com.ar/

National Institute of Statistics and Census (INDEC)

This bureau is responsible for the coordination and supervision of all public statistical activities in Argentina.

http://www.indec.gov.ar

Brazil

National Agency of Telecommunication (ANATEL)

Anatel is the Brazilian telecommunications regulator and promotes the development of telecommunications in the

country.

http://www.anatel.gov/br/

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

23

The São Paulo Stock Exchange (BOVESPA)

BOVESPA is the only stock trade center in Brazil and Latin America’s largest stock exchange.

http://bovespa.com.br

The Brazilian Institute of Geography and Statistics (IBGE)

Brazil’s Census Bureau provides information and data about the country’s economy, geography and population.

http://www.ibge.gov.br

Chile

Ministry of Telecommunications (SUBTEL)

Subtel is a unit of the Ministry of Transport and Telecommunications and helps promote the development of the

telecommunication sector in Chile.

http://www.subtel.cl/

Mexico

Federal Telecommunications Commission (COFETEL)

Mexico’s telecoms regulator is an independent administrative body operating under the country’s transport and

communications ministry.

Instituto Nacional de Estadística Geografía e Informática (INEGI)

The National Institute of Statistics, Geography and Information is a unit of the Secretariat of Property and Public Credit,

and provides statistical and information on the country’s demographics, pollution and the economy.

http://www.inegi.gob.mx/

Peru

Ministry of Transport and Communications (MTC)

The ministry is responsible for administering the country’s transport and communications services.

http://www.mtc.gob.pe/

Supervisory Board for Private Investment in Telecommunications (OSIPTEL)

OSIPTEL is responsible for the development and modernization of telecommunication services in Peru.

http://osiptel.gob.pe/

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

24

Notes to Comparative Data

- All figures are in United States dollars.

- All figures are as reported by the company.

- N/A = Data Not Available.

- N/L = Not Listed.

- Companies ranked by total revenue for the full year most recently reported.

Definitions

- Total Revenue = All revenues, including net sales, operating revenues, interest income, royalties, excise taxes etc.

- EBITDA = Earnings before interest, taxes, depreciation and amortization.

- EPS Cont Operations = Earnings Per Share as reported by company excluding extraordinary items.

- Total Current Assets = All assets expected to be realized within the next year, includes cash, accounts receivable and inventories.

- Long Term Debt = Debt due to be paid at a date more than one year in the future.

- Return on Equity = The company’s earnings divided by its equity (book value).

- Profit Margin = The company’s net income as a percent of revenues.

Comparative Company Data | LATIN AMERICA

Company Country Ticker Exchange Primary SIC Other SICs

America Movil SAB de CV Mexico AMX BMV 4812 4813

Tele Norte Leste Participaco Brazil TNL3 BVSPA 4813 6719

Vivo Participacoes SA Brazil VIVO3 BVSPA 4812 6719

Telefonos de Mexico SAB de CV Mexico TELMEX BMV 4813 4812

Telecomunicacoes de Sao Paulo Brazil TLPP BVSPA 4813 6719

TIM Participacoes SA Brazil TCSL3, TCSL4 BVSPA 4812 6719

Telmex Internacional SAB de CV Mexico TELINT BMV 4813 4899 4841

Brasil Telecom SA Brazil BRTP3, BRTP4 BVSPA 4813

Telecom Argentina SA Argentina TECO2 BUE 4813 4812

Empresa Nacional de Telecomunicaciones SA Chile ENTEL BSAN 4813 4899

Company Total Revenue - FYE - 1 Total Revenue - FYE - 2 Total Revenue - FYE - 3 EBITDA - FYE - 1 EBITDA - FYE - 2 EBITDA - FYE - 3

America Movil SAB de CV $30,149,963,646 $24,946,291,677 $28,567,005,921 N/A N/A N/A

Tele Norte Leste Participaco $17,128,690,937 $8,036,028,119 $9,864,796,634 $2,843,221,681 $2,027,021,183 $3,408,134,642

Vivo Participacoes SA $9,379,872,017 $6,635,069,113 $7,008,411,781 $2,712,011,013 $1,666,751,837 $1,486,207,013

Telefonos de Mexico SAB de CV $9,097,458,090 $8,956,810,157 $11,989,356,458 N/A N/A N/A

Telecomunicacoes de Sao Paulo $9,054,614,909 $6,853,521,177 $8,262,306,872 $3,248,928,778 $2,692,382,952 $3,388,256,942

TIM Participacoes SA $7,512,717,448 $5,638,934,030 $7,003,523,142 $1,606,888,006 $1,082,754,853 $1,435,519,776

Telmex Internacional SAB de CV $7,068,665,453 $5,485,345,048 $6,212,551,142 $2,046,523,711 $1,161,989,201 $1,700,222,519

Brasil Telecom SA $6,235,920,027 $4,967,266,450 $6,292,217,672 $245,537,414 $1,563,576,631 $1,979,695,933

Telecom Argentina SA $3,205,978,821 $3,052,419,749 $2,879,930,895 N/A N/A N/A

Empresa Nacional de Telecomunicaciones SA $1,649,532,990 $1,975,030,263 $1,633,715,764 N/A N/A N/A

Company Net Income - FYE - 1 Net Income - FYE - 2 Net Income - FYE - 3 EPS - FYE - 1 EPS - FYE - 2 EPS - FYE - 3

America Movil SAB de CV $5,881,473,499 $4,299,621,157 $5,381,630,208 $0.18 $0.13 $0.15

Tele Norte Leste Participaco -$249,928,357 $494,960,314 $1,300,420,757 -$0.65 $1.30 $3.41

Vivo Participacoes SA $491,536,852 $167,138,319 -$56,005,610 $1.23 $0.45 -$0.04

Telefonos de Mexico SAB de CV $1,563,521,272 $1,456,189,672 $3,305,717,534 $0.17 $0.15 $0.33

Telecomunicacoes de Sao Paulo $1,245,613,699 $1,037,945,933 $1,325,643,759 $2.46 $2.05 $2.62

TIM Participacoes SA $123,183,153 $77,268,709 $38,318,093 $0.05 $0.03 $0.02

Telmex Internacional SAB de CV $730,460,268 $406,390,215 $643,044,913 $0.04 $0.02 $0.03

Brasil Telecom SA -$655,023,818 $441,696,751 $448,836,466 -$1.11 $0.81 $0.82

Telecom Argentina SA $368,427,960 $276,524,828 $280,566,334 $0.37 $0.28 $0.29

Empresa Nacional de Telecomunicaciones SA $237,342,493 $286,719,470 $202,239,637 $0.00 $0.00 $0.00

CompanyTotal Current Assets -

FYE - 1Total Current Assets -

FYE - 2Total Current Assets -

FYE - 3Long-Term Debt -

FYE - 1Long-Term Debt -

FYE - 2Long-Term Debt -

FYE - 3

America Movil SAB de CV $8,257,079,794 $8,190,399,654 $7,397,047,768 $7,771,491,573 $8,426,342,393 $7,774,790,736

Tele Norte Leste Participaco $10,538,836,815 $7,639,287,832 $7,138,378,682 $12,247,635,975 $6,986,060,312 $4,138,008,415

Vivo Participacoes SA $3,911,125,426 $3,828,973,961 $3,831,455,259 $2,465,611,460 $2,136,512,495 $1,347,629,173

Telefonos de Mexico SAB de CV $3,959,516,301 $3,761,428,993 $2,843,343,623 $6,348,002,007 $6,074,810,658 $7,259,558,014

Telecomunicacoes de Sao Paulo $4,040,284,503 $2,784,299,742 $2,932,782,609 $1,004,529,710 $1,379,949,356 $1,404,223,843

TIM Participacoes SA $3,878,774,035 $2,502,617,569 $2,966,513,885 $1,572,138,219 $886,345,250 $745,019,355

Telmex Internacional SAB de CV $2,916,704,188 $2,507,702,470 $3,539,245,697 $1,627,795,425 $786,276,823 $1,033,212,219

Brasil Telecom SA $3,252,439,813 $2,619,541,435 $2,592,426,367 $2,047,925,572 $1,712,716,237 N/A

Telecom Argentina SA $771,732,019 $748,142,095 $756,640,429 $21,502,557 $205,739,076 $547,167,827

Empresa Nacional de Telecomunicaciones SA $621,715,793 $688,228,660 $781,822,633 $650,435,631 $772,396,856 $776,134,655

Company Return on Equity (Most Recent Yr) Profit Margin (Most Recent Yr) Date FYE - 1 Date FYE - 2 Date FYE - 3

America Movil SAB de CV 43.46 19.51 31-Dec-2009 31-Dec-2008 31-Dec-2007

Tele Norte Leste Participaco -5.45 -1.46 31-Dec-2009 31-Dec-2008 31-Dec-2007

Vivo Participacoes SA 8.41 5.24 31-Dec-2009 31-Dec-2008 31-Dec-2007

Telefonos de Mexico SAB de CV 53.41 17.19 31-Dec-2009 31-Dec-2008 31-Dec-2007

Telecomunicacoes de Sao Paulo 21.61 13.76 31-Dec-2009 31-Dec-2008 31-Dec-2007

TIM Participacoes SA 2.58 1.64 31-Dec-2009 31-Dec-2008 31-Dec-2007

Telmex Internacional SAB de CV 9.61 10.33 31-Dec-2009 31-Dec-2008 31-Dec-2007

Brasil Telecom SA -10.30 -10.50 31-Dec-2009 31-Dec-2008 31-Dec-2007

Telecom Argentina SA 25.85 11.49 31-Dec-2009 31-Dec-2008 31-Dec-2007

Empresa Nacional de Telecomunicaciones SA 21.05 14.39 31-Dec-2008 31-Dec-2007 31-Dec-2006

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

25

Notes

http://webreports.mergent.com

Industry Report - Telecommunications - October 2010

303434

Industry Reports Coverage 2010

Regional Reports

www.mergent.com