Embed Size (px)

Citation preview

Understanding the

Safe Harbor®-Directed IraTM

What is Lasaii?

Lasaii offers an alternative method for using your IRA funds to support the purchase of real estate. The key difference between our program and other IRA real estate investment programs is that with the Lasaii program you can occupy your property. You can apply your SAfe HARboR®-Directed IRA™ (SHIRA™) to any real estate asset—a primary residence, a second home, a vacation rental, or an investment property. You can even use it to support existing mortgage payments for the home you occupy now.

Today’s financial landscape is challenging. What if you could start enjoying the benefits of your accumulated retirement savings now and still

have IRA money for income when you retire? Are you tired of investing in the same old thing? Have you been dreaming of buying a second home? This document will explain how Lasaii’s program can help you meet your real estate and financial goals.

Sometimes it’s easier to understand what a program is if you also understand what it is not. Lasaii’s program is not for everyone. A key component of our program is that your retirement funds work in tandem with a mortgage. If you cannot or do not have a mortgage, Lasaii is not the answer for you. If you want your retirement funds to be invested solely in the stock market, this program is not compatible with your financial needs, either.

2

The Solution for Using Your IRA to Support the Purchase of Real Estate You Can Occupy

© C

opyr

ight

201

3 La

saii®

LLC

Lasaii’s program is also not a risky short-term invest-ment. Through our IRS-reviewed SAfe HARboR®-Directed IRA™ your retirement funds are invested in a principal protected vehicle, shielding them from fluctuations in the stock market. The struc-ture is designed to facilitate a 30-year mortgage, but you may use any other mortgage that best suits your needs. This is not a program designed for short-term real estate investments, such as buying a house one year and selling it the next. our program does not support “flipping” houses.

The majority of our clients pay no out of pocket fees to establish the SAfe HARboR®-Directed IRA™ account, though the fee structure depends on the client’s choice of custodian. Some custodians agree to pay compensation directly to Lasaii, which results in no out of pocket cost to the client. other custodians do not pay compensation, and therefore

Lasaii will require a one-time out of pocket fee based on the rollover amount. There is also a small annual maintenance fee payable to Lasaii.

finally, our program is not new. Since 1992, Lasaii has assisted people in structuring IRAs, 401(k) rollovers, and other types of retirement plans to support the purchase of real estate. The Lasaii IRA real estate investing program was not designed in response to today’s economic crises. We have been engaged in this work for a long time. We have hundreds of clients across 36 states and five countries. The Lasaii IRA real estate investing program was reviewed by the IRS in 2005. Lasaii’s proprietary approach was found to be compliant relative to all 29 IRS tax codes governing tax avoidance, qualified plans, and/or real estate transactions. You can be fully confident that your investments are safe and legal.

3 © C

opyr

ight

201

3 La

saii®

LLC

Americans hold 4.7 trillion dollars in IRAs, more than any other type of tax-deferred savings account, and that number continues to grow. In addition to IRAs, employer-sponsored retirement plans and an-nuities also play important roles in the US retire-ment system. Total US retirement assets reach over $17 trillion.1

The terms “Check book IRA LLC,” “Self Directed IRA,” and “SAfe HARboR®-Directed IRA™” are legally no different from any other IRA. These terms are not technical or legal terms; they are

rather descriptive terms that reveal how the IRA is managed. You will not find any of these terms in the IRS tax code, but you will find that the tax code allows you to structure these plans in legal ways. Although most brokerage houses and banks are able to offer these IRAs to their clients, they tend to limit the range of alternatives available to clients based on the scope of the firms’ own investment products. Therefore, specialized companies or consultants are the primary avenues for establishing any of the three types of IRAs mentioned above. (The basic differences are explained on page 5.)

4

Alternative Ways You Can Use Your IRA

© C

opyr

ight

201

3 La

saii®

LLC

1Sources: Investment Company Institute, federal Reserve board, National Association of Government Defined Contribution Administrators, American Council of Life Insurers, and Internal Revenue Service Statistics of Income Division. See “The U.S. Retirement Market, fourth Quarter 2010.” other plans include private-sector Db plans; federal, state, and local pension plans; and all fixed and variable annuity reserves at life insurance companies less annuities held by IRAs, 403(b) plans, 457 plans, and private pension funds. federal pension plans include U.S. Treasury security holdings of the civil service retirement and disability fund, the military retirement fund, the judicial retirement funds, the Railroad Retirement board, and the foreign service retirement and disability fund. These plans also include securities held in the National Railroad Retirement Investment Trust and federal employees Retirement System (feRS) Thrift Savings Plan (TSP).

The CbIRA offers more flexibil-ity than the SDIRA. It grants its owner checkbook-writing privi-leges, or “checkbook control.” It gives the IRA account holder complete freedom to decide how, when, and where to invest, as long as the SDIRA rules are followed. This type of IRA is owned by an LLC, which offers significant ben-efits, such as limited liability and asset protection (exceptions and limitations may vary from state to state, so be sure to check with a real estate lawyer). However, the same SDIRA occupancy restric-tions apply to the CbIRA. It is prohibited for the CbIRA owner or any family members to occupy the real estate. The CbIRA is not a good option if you wish to in-vest in your “dream home” or oc-cupy the property.

Violation of the IRS’s rules for CBIRAs would cause the entire value of the real estate investment to be taxable as additional income during the same year as the prohibited transaction. You would also incur early withdrawal penalties during the same year the violation occurred if you are under 59.5 years of age.

Check Book IRA LLC (CBIRA)

Self Directed IRA (SDIRA)

5

The term self-directed simply indicates that you, the client, choose what you want your IRA to be invested in, including real estate. There are, however, prohibited transactions about which one must be aware. for instance, it is prohibited for the SDIRA owner or any of the owner’s ascending/descending family members to occupy the real estate. These restrictions eliminate your ability to use your IRA to invest in a vacation home or second home because you are not allowed to live in the property for any amount of time.

Violation of the IRS’s rules for SDIRAs would cause the entire value of the SDIRA real estate investment to be taxable as additional income during the same year as the prohibited transaction. You would also incur early withdrawal penalties during the same year the violation occurred if you are under 59.5 years of age.

SAfe HARBoR®-Directed IRA™ (SHIRA™)

The SAfe HARboR®-Directed IRA™ invests the owner’s funds in a principal protected account in compliance with IRS tax shelter inspectors to allow for some upside potential while buffering from downside risk. Those assets, in coordination with non-IRA funds, can be structured to support existing or new mortgage payments. You or any family member can occupy the property because the title is held in your name rather than being held by the IRA. In essence, you own two investments—one is your SHIRA™ and the other is the real estate.

Payments generated from the SHIRA™ are taxable as additional income in the year withdrawn. If you qualify, all tax offsets can be applied against your normal income and your SHIRA™ tax liability. For instance, if you’ve made monthly mortgage payments of $1500 from your SHIRA™, your annual taxable income will equal $18,000. But any tax liability will be eliminated or minimized by normal real estate tax write offs.

© C

opyr

ight

201

3 La

saii®

LLC

6

Many self-directed IRA companies and related books are advertising a “retirement dream home approach,” a method for using your IRA to fund the purchase of real estate in which you’d someday like to retire. In a volatile financial market, these programs are appealing, especially because most people who use their IRAs to purchase real estate do indeed plan to retire in those homes. However, most people don’t know that these traditional self-directed IRA programs carry costs that can turn dream homes into nightmares.

Let’s look at a case study to find out more:

CAse study:

Brother Can Buy Sister’s RetirementDream Home For Less Than She Can!

A couple, Janet and Tom, travel to Panama on vaca-tion and fall in love with the country. They dream about retiring there and living in a house on the beach. They learn about traditional self-directed IRA programs that promise to make their dream a reality. Janet and Tom discover they can use their IRAs to fund a real estate investment in Panama in which they can live when they retire. Janet used a 401(k) rollover from a previous employer to establish a traditional self-directed IRA to buy the property outright.

Janet and Tom travel to Panama to look for their dream home, and they soon find it! They are de-lighted to be back in Panama, and they are ecstatic that they found a place they both love on the beach. Their dream beachfront home costs $300,000. Since Janet already set up a traditional self-directed IRA, she completes a buy Direction Letter to instruct the firm holding her traditional self-directed IRA to purchase the property with her IRA. Her IRA will take title once the transaction is complete. The IRA

custodian will work with Panamanian attorneys and the title company to make sure the IRA has owner-ship and that all income and expenses are properly credited and debited to her IRA.

Sounds great, right? A beautiful home in Panama on the beach! but guess what? During the time the property is owned by her IRA, Janet and Tom can’t live in their dream home. They can’t even stay in it for a few days. Their parents can’t stay in it. Their children can’t stay in it. Their children’s spouses can’t stay in it. Their grandchildren can’t stay in it. They are all disqualified to occupy the property.

So what happens to Janet and Tom’s dream home? Janet and Tom have to hire a property manager to maintain the property. And if they choose to rent the property to tourists—after all someone should be able to enjoy the house!—the rental income will go back into her IRA. All maintenance expenses, property taxes, and annual fees will be taken from the IRA’s rental income, performed by third par-

© C

opyr

ight

201

3 La

saii®

LLC

7

ties to prevent any prohibited transactions. Janet and Tom can check on their dream home to see if it needs renovations or upgrades while their IRA owns it, but they cannot spend the night there or do any manual work themselves. Any improvements must be done by a third party, and all costs must be paid by IRA monies. further, there are no normally allowed real estate tax write offs available because the IRA purchased the home outright.

one assumes Janet and Tom will want to visit Pan-ama while their property is owned by her IRA, but where will they stay? They can’t stay in their dream house, so they’ll have to find somewhere else to stay—a motel or a hotel or a house they rent down the road from their dream house. And one day they’ll be strolling along the beach, and Janet and Tom will look up at their dream house, and they’ll have the painful experience of seeing someone else enjoying the spectacular view from their balcony!

finally, six years have passed, and Janet and Tom

are ready to retire to their dream home in Panama. first, Janet will need to take a complete distribution of the property owned by her IRA. This will become a taxable event for US tax purposes. In other words, the fair market value of the house will be taxable income, all at once.

Let’s run some numbers:

• Janet bought their retirement dream home outright for $300,000 by using her traditional self-directed IRA.

• Six years later when they are ready to retire to their dream home, the house is appraised at $325,000.

• She will have to pay taxes on this total appraised amount ($325,000), which will place them in the 30% (approximate) tax bracket.

• 30% of $325,000 is $97,500—a veritable “tax explosion,” money they will have to come up with on their own.

© C

opyr

ight

201

3 La

saii®

LLC

• If Janet is under 59.5 years of age, she can also be subject to a 10% penalty for early withdrawal, or $32,500.

• Assuming no penalty, they will have paid $422,500 for their dream house ($325,000 + $97,500 in tax liability), which only should have cost them the original price of $300,000. And that’s not even including the money her IRA paid to their property manager, or the fees to the custodian/trustee, or the money they paid to rent a hotel room when they visited and weren’t allowed to stay in their dream house. (even though they earned rental income from the property, a good chunk of those funds was needed for the expense of maintaining the home.)

So what should Janet and Tom have done differ-ently? How can they avoid the “tax explosion” when they’re ready to retire? How can they make sure they don’t pay more for their home than it’s worth? How can they enjoy their dream home as soon as possible?

Here are several possible options, and you will soon see that only one of them makes any financial sense at all (Hint: it’s number 4!):

(1) one of the three biggest self-directed IRA facili-tators offers this solution to the “tax explosion” prob-lem: They suggest Janet and Tom cross their fingers and hope they’ll be in a lower tax bracket when the time comes to retire and finally occupy their retire-ment dream home. That doesn’t sound like a sensible solution to us, especially given the reality that even if Janet and Tom aren’t making any income at all when they retire, they will still be taxed on the entire appraised value of the home. for Janet and Tom in this example, their tax liability would be $97,500 just on the home in Panama alone.

(2) Another self-directed IRA custodian/trustee company has a different suggestion: Instead of waiting until Janet retires to take a complete distribution of the property owned by her IRA, she can take smaller distributions annually. To mitigate the tax hit of a full distribution Janet can gradually distribute the house over a period of years by reassigning a portion or percentage of the grant deed through an “assignment.” for example, she can own 10% of the house the first year, 20% of the house the following year, 30% the following year, and so on until she eventually owns 100% of the home. This is performed by the title company and the custodian until the full ownership is distributed “in-kind” to Janet. each distribution will be subject to the appropriate income tax rates. In essence, this approach is only spreading out the tax hit over multiple years versus taking it all at once as suggested in option #1. for example, Janet’s first ownership transfer of 10% means she will have a distribution equal to $30,000 which counts as additional income over and above her regular income, and she will have to pay income tax on that amount. further, if she is under the age of 59.5 that distribution will be subject to a 10% penalty ($3,000). but what if the house increases in value? Assuming the house appreciates, the tax liability will increase as well. This partial distribution process could be expensive and take years to complete, and while they wait, Janet and Tom are further delayed from living in their retirement dream home.

8© C

opyr

ight

201

3 La

saii®

LLC

9

(3) Here’s another solution: Janet can complete a Sell Direction Letter to instruct the firm holding her traditional self-directed IRA to sell their dream home to Janet’s brother. Janet’s brother can buy Ja-net and Tom’s dream home for the appraised value of $325,000 without having to pay any taxes on it. That’s $97,500 less than Janet and Tom would have to pay. Janet’s brother owes Janet a lot of favors, so maybe he’ll be kind enough to let Janet and Tom live in the dream house he bought right out from under them.

(4) finally, here’s a solution that makes sense—Lasaii’s SAfe HARboR®-Directed IRA™. Lasaii offers an alternative method for using your IRA funds to support the purchase of real estate. Here’s how our program works:

• Through Lasaii’s program, your SAfe HARboR®-Directed IRA™ invests your IRA funds in a principal protected account in compliance with IRS tax shelter inspectors that allows for some upside potential while buffering from downside risk. Those assets, in coordination with non-IRA funds, can be structured to support existing or new mortgage payments.

• In essence, you own two investments: the SAfe HARboR®-Directed IRA™ and the real estate. That means you—or any of your family members—can occupy your property immediately because the title is held in your name. You don’t have to wait. You can use it as a primary residence or as a vacation home or as a rental property or a combination of these. It’s up to you.

• There will be no “tax explosion.” Payments generated from the SAfe HARboR®- Directed IRA™ are taxable as additional income in the year withdrawn. All qualifying real estate tax offsets can be applied against your personal and SHIRA™ tax liability.

With Lasaii’s SAfe HARboR®-Directed IRA™, you can avoid the potential nightmare situations previously outlined and support a real estate investment you and your family can occupy immediately.

We invite you to join hundreds of our clients around the world already enjoying the benefits of their IRS reviewed SAfe HARboR®-Directed IRA™. The team at Lasaii looks forward to helping you meet your retirement and real estate goals.

you – or any of your family

members – can occupy your

property immediately because

the title is held in your name.

© C

opyr

ight

201

3 La

saii®

LLC

10

What Are the Benefits of the SAFE HARBOR®-Directed IRA™ Alternative?

ChoiCesWith a SAfe HARboR®-Directed IRA™, you can buy a primary residence, a second home, a vacation/rental/investment property, commercial sites, or land on which to build. You can also use the SHIRA™ to fund payments for an existing mortgage.

FlexibilityIf you sell one property supported by your SAfe HARboR®-Directed IRA™, you can restructure your SHIRA™ to fund a new property. You can buy in the US and/or overseas if you qualify. You can mix SHIRA™ and non-SHIRA™ funds to buy property or properties. You can buy real estate as an individual or with partners.

immediate oCCupanCy & enjoymentThe real estate is titled in your name—not in the name of your IRA—so you and your family can occupy and enjoy your home immediately. You can use the property as a primary residence, a vacation home, a rental property, or simply keep it as an investment. The choice is yours.

appreCiationIf you subscribe to the theory of “buy low; sell high,” then this is an excellent time to purchase real estate and allow it to appreciate over time. If you choose to support the purchase of real estate with a SAfe HARboR®-Directed IRA™, then you will be allowed to occupy and enjoy the property while it increases in value.

© C

opyr

ight

201

3 La

saii®

LLC

11

tax savingsIf you qualify, you can enjoy all the tax benefits associated with real estate ownership. Like all IRAs, your SAfe HARboR®-Directed IRA™ will continue to grow, tax deferred.

rental inComeAny net rental income goes directly to the individual and not to the IRA. It is yours to use as you wish.

step up in basisThe real estate you purchase through a SAfe HARboR®-Directed IRA™ can be passed to your heirs with a “step up in basis.” This means there will be tax savings on any appreciation accumulated. SHIRAs™ offer additional inheritance benefits as well.

© C

opyr

ight

201

3 La

saii®

LLC

STep Up In baSIS

Tax

SavIngS

renTal IncoMe

appr

ecIa

TIo

n

IMMeDIaTe

occUpancy

& enjoyMenT

flexIbIlITy

cHo

IceS

12

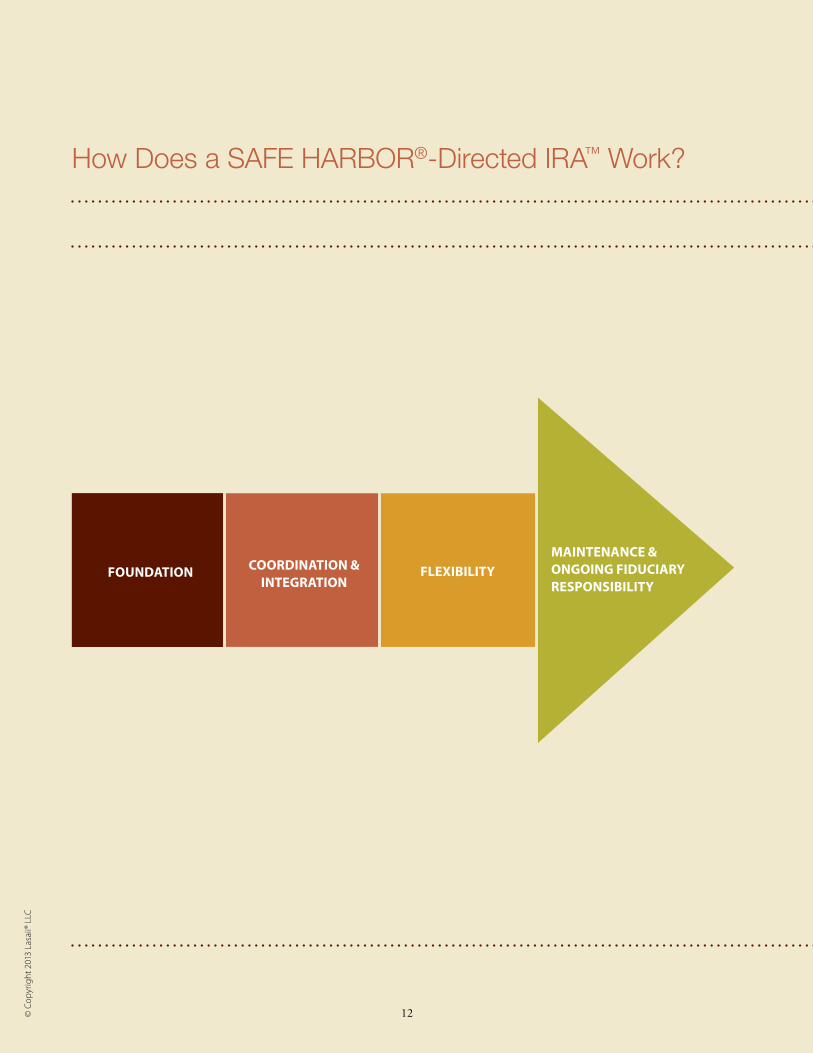

How Does a SAFE HARBOR®-Directed IRA™ Work?

© C

opyr

ight

201

3 La

saii®

LLC

maintenanCe & ongoing FiduCiary responsibility

FlexibilityCoordination & integration

Foundation

13

FlexibilityCoordination& integrationFoundation

maintenanCe &ongoing FiduCiary

responsibility

1-2 weeks 2-4 weeks always ongoing

Lasaii has 20 years of experience working with clients to coordinate IRA real estate plans. You can rest assured your account will be properly structured and maintained in accordance with all IRS retirement plan rules and real estate legislation.

Lasaii’s program combines a selection of 29 IRS real estate tax codes governing tax avoidance, qualified plans, and/or real estate transactions (depending on a client’s individual plan). We carefully monitor all updates to these tax codes, as well as any legislative changes. We also continually review the custodian’s IRA investment vehicles to ensure they meet all requirements mandated by IRS tax shelter inspectors.

As stewards of your SHIRA™, we keep all records in our database and in hard files for complete transparency.

In the initial consulta-tion, we will discuss your financial goals and person-al circumstances to help you decide if the SAfe HARboR®-Directed IRA™ is right for you–and to determine if you qualify for the program. If so, our consultants will help guide you in structuring a customized IRA real estate plan, personalized to meet your needs and goals.

Clients can then choose from a variety of IRS approved custodians for their SHIRA™. The custodians we offer for the SHIRA™ account provide vehicles that protect the principal from market downturns and allow for growth at the same time.

Next, the SHIRA™ account is opened by rolling over or transferring funds from existing qualified retirement plans to the SHIRA™ without any tax consequences.

A lender of your choice is engaged to establish your mortgage or prepare to refinance your current mortgage. You will open a real estate checking account at the bank of your choice, to receive monthly direct deposits from your SAfe HARboR®-Directed IRA™ earmarked to make mortgage payments. (The checking account and other back office documents are necessary to remain compliant with IRS tracking requirements.) When structured properly, your plan can also offer tax benefits associated with real estate ownership.

The greatest benefit is FLEXIBILITY. What if you move, sell, or buy additional real estate? Your SAfe HARboR®-Directed IRA™ can be structured to support the mortgage you wish to service most.

When unanticipated events occur (divorce, death, illness, etc.), adjustments can be made to the structure of your plan to accommodate your new situation.

Depending on the choice of custodian, clients can reallocate their funds within the account annually.

Real estate purchases can be made in the US or overseas and can be made by an individual or with partners.

© C

opyr

ight

201

3 La

saii®

LLC

Q: How long has Lasaii beenassisting clients in structuringSAFE HARBOR®-Directed IRAs™?

A: Since 1992. We have hundreds of satisfied clients across 36 states and five countries.

Q: How much does Lasaii’s program cost?

A: The majority of our clients pay no fees at all out of pocket to establish the SHIRA™, though whether or not you pay fees out of pocket depends on your choice of custodian. There is a small annual maintenance fee.

Q: Which of my retirement accounts will qualify for Lasaii’s program?

A: Most IRAs, 401(k)s, and employer sponsored retirement plans are eligible for rollover or for reallocation to a SAfe HARboR®-Directed IRA™. The particulars of the plan, your age, and your employment status will determine eligibility. Roth IRAs, however, do not qualify. Q: What is the minimum funding requirement to establish a SAFE HARBOR®-Directed IRA™?

A: $100,000. but allowances will be made on an individual basis. for example, we work with homeowners who are struggling to make their monthly mortgage payments due to job loss or other challenging economic situations. Your SHIRA™ can be structured to provide additional monthly income to apply to an existing mortgage payment and property taxes to tide you over during this transition time.

Q: Can my family and I occupy the real estate we purchase with your program?

A: Yes. our program is flexible, and we can assist you in designing a structure that allows you to occupy the property either as a vacation home, a primary residence, or rental property.

Q: What if I have already purchased avacation home? Can Lasaii put my retirement monies to work to pay for it?

A: Yes. Any existing mortgage you have is eligible for a SAfe HARboR®-Directed IRA™,including the mortgage for the home you live in now.

Q: Can I buy real estate in a country other than the United States? A: Yes, provided you are legally allowed to buy real estate in that country, you file US tax returns, and you can obtain a mortgage for the purchase.

frequently Asked Questions

14© C

opyr

ight

201

3 La

saii®

LLC

Q: Do I need to have my real estate identified and ready to purchase when I start working with Lasaii? A: No. The first step is to transfer your IRA funds to a SAfe HARboR®-Directed IRA™ account where the principal is protected against a potential decline in the stock market. You may take as long as you’d like to choose your real estate.

Q: What restrictions apply to the type of real estate I can buy?

A: You may purchase or build a primary residence, a second (or vacation) home, investment real estate (residential or commercial), or undeveloped land.

Q: What happens if I need to sellreal estate purchased using my SAFE HARBOR®-Directed IRA™?

A: Just as you may purchase your real estate at any time, you are also free to sell it at any time. The flexibility of the program allows you to redirect the SAfe HARboR® proceeds to support the mortgage payments for a different property you choose to buy, or you can use it to support an existing mortgage. You can also choose to leave your SHIRA™ with the same custodian and use the proceeds for retirement income.

frequently Asked Questions

15 © C

opyr

ight

201

3 La

saii®

LLC

Lasaii’s clients enjoy results like these:

• A house to fit their growing family

• A family home saved from foreclosure

• A ranch

• A retirement condominium

• A beach house

• A mountain hideaway

• An investment property

Can your IRA do this?Ours CAN!

Call us at 1-800-208-5857 to learn more.

675 Sun Valley Road, Suite J PO Box 9290, Ketchum, ID 83340Office 1-208-726-8625 Toll Free 1-800-208-5857 Fax 1-208-726-7208

www.lasaii.com

© C

opyr

ight

201

3 La

saii®

LLC