Embed Size (px)

Citation preview

LARGE CITIESRETAIL MARKETS IN 2014STATE OF AFFAIRS

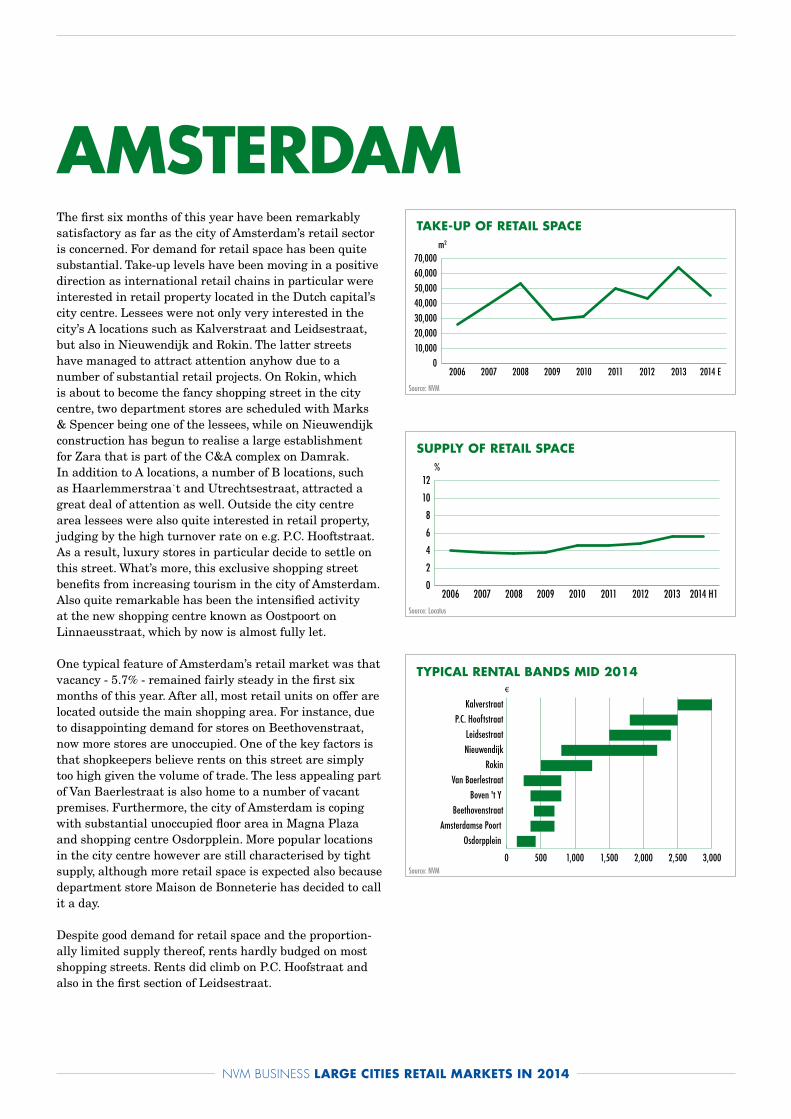

The first six months of this year have been remarkably satisfactory as far as the city of Amsterdam’s retail sector is concerned. For demand for retail space has been quite substantial. Take-up levels have been moving in a positive direction as international retail chains in particular were interested in retail property located in the Dutch capital’s city centre. Lessees were not only very interested in the city’s A locations such as Kalverstraat and Leidsestraat, but also in Nieuwendijk and Rokin. The latter streets have managed to attract attention anyhow due to a number of substantial retail projects. On Rokin, which is about to become the fancy shopping street in the city centre, two department stores are scheduled with Marks & Spencer being one of the lessees, while on Nieuwendijk construction has begun to realise a large establishment for Zara that is part of the C&A complex on Damrak. In addition to A locations, a number of B locations, such as Haarlemmerstraa˙t and Utrechtsestraat, attracted a great deal of attention as well. Outside the city centre area lessees were also quite interested in retail property, judging by the high turnover rate on e.g. P.C. Hooftstraat. As a result, luxury stores in particular decide to settle on this street. What’s more, this exclusive shopping street benefits from increasing tourism in the city of Amsterdam. Also quite remarkable has been the intensified activity at the new shopping centre known as Oostpoort on Linnaeusstraat, which by now is almost fully let.

One typical feature of Amsterdam’s retail market was that vacancy - 5.7% - remained fairly steady in the first six months of this year. After all, most retail units on offer are located outside the main shopping area. For instance, due to disappointing demand for stores on Beethovenstraat, now more stores are unoccupied. One of the key factors is that shopkeepers believe rents on this street are simply too high given the volume of trade. The less appealing part of Van Baerlestraat is also home to a number of vacant premises. Furthermore, the city of Amsterdam is coping with substantial unoccupied floor area in Magna Plaza and shopping centre Osdorpplein. More popular locations in the city centre however are still characterised by tight supply, although more retail space is expected also because department store Maison de Bonneterie has decided to call it a day.

Despite good demand for retail space and the proportion-ally limited supply thereof, rents hardly budged on most shopping streets. Rents did climb on P.C. Hoofstraat and also in the first section of Leidsestraat.

AMSTERDAM

0 500 1,000 1,500 2,000 2,500 3,000

Osdorpplein Amsterdamse Poort

BeethovenstraatBoven 't Y

Van BaerlestraatRokin

NieuwendijkLeidsestraat

P.C. HooftstraatKalverstraat

€

TYPICAL RENTAL BANDS MID 2014

Source: NVM

010,00020,00030,00040,00050,00060,00070,000

2014 E20132012201120102009200820072006

m2

TAKE-UP OF RETAIL SPACE

Source: NVM

0

2

4

6

8

10

12

2014 H120132012201120102009200820072006

%

SUPPLY OF RETAIL SPACE

Source: Locatus

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

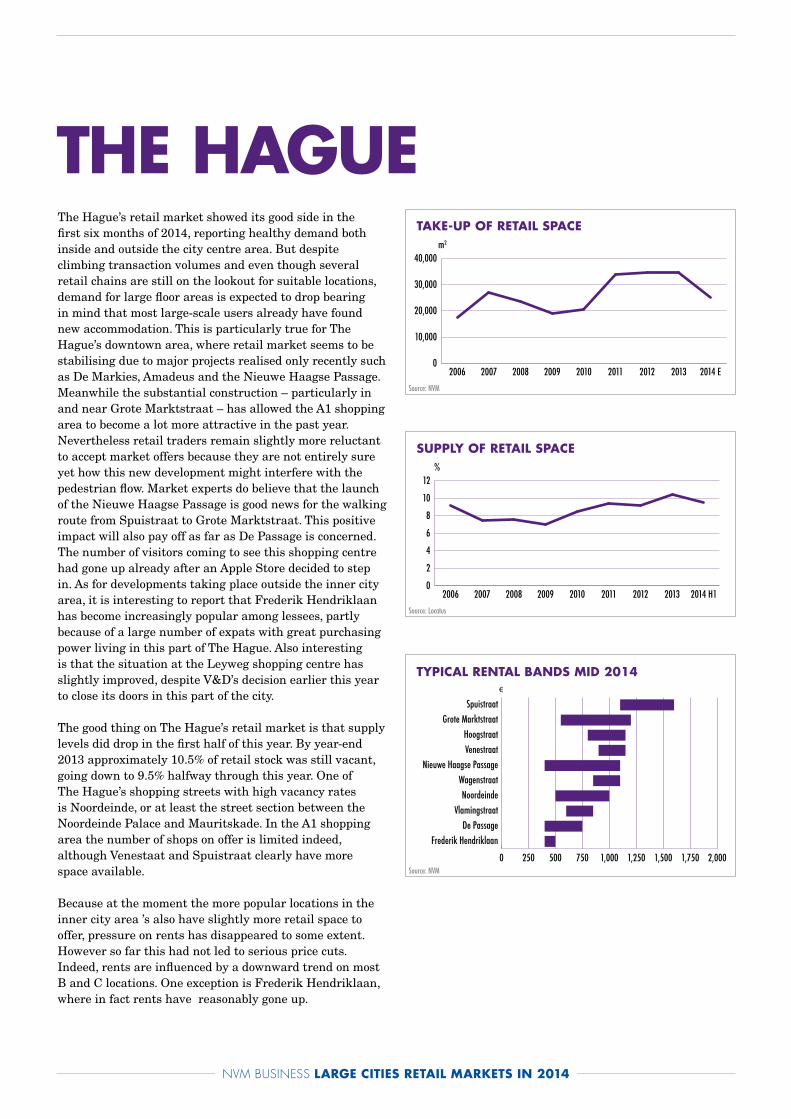

The Hague’s retail market showed its good side in the first six months of 2014, reporting healthy demand both inside and outside the city centre area. But despite climbing transaction volumes and even though several retail chains are still on the lookout for suitable locations, demand for large floor areas is expected to drop bearing in mind that most large-scale users already have found new accommodation. This is particularly true for The Hague’s downtown area, where retail market seems to be stabilising due to major projects realised only recently such as De Markies, Amadeus and the Nieuwe Haagse Passage. Meanwhile the substantial construction – particularly in and near Grote Marktstraat – has allowed the A1 shopping area to become a lot more attractive in the past year. Nevertheless retail traders remain slightly more reluctant to accept market offers because they are not entirely sure yet how this new development might interfere with the pedestrian flow. Market experts do believe that the launch of the Nieuwe Haagse Passage is good news for the walking route from Spuistraat to Grote Marktstraat. This positive impact will also pay off as far as De Passage is concerned. The number of visitors coming to see this shopping centre had gone up already after an Apple Store decided to step in. As for developments taking place outside the inner city area, it is interesting to report that Frederik Hendriklaan has become increasingly popular among lessees, partly because of a large number of expats with great purchasing power living in this part of The Hague. Also interesting is that the situation at the Leyweg shopping centre has slightly improved, despite V&D’s decision earlier this year to close its doors in this part of the city.

The good thing on The Hague’s retail market is that supply levels did drop in the first half of this year. By year-end 2013 approximately 10.5% of retail stock was still vacant, going down to 9.5% halfway through this year. One of The Hague’s shopping streets with high vacancy rates is Noordeinde, or at least the street section between the Noordeinde Palace and Mauritskade. In the A1 shopping area the number of shops on offer is limited indeed, although Venestaat and Spuistraat clearly have more space available.

Because at the moment the more popular locations in the inner city area ’s also have slightly more retail space to offer, pressure on rents has disappeared to some extent. However so far this had not led to serious price cuts. Indeed, rents are influenced by a downward trend on most B and C locations. One exception is Frederik Hendriklaan, where in fact rents have reasonably gone up.

THE HAGUE

0 250 500 750 1,000 1,250 1,500 1,750 2,000

Frederik HendriklaanDe Passage

VlamingstraatNoordeinde

WagenstraatNieuwe Haagse Passage

VenestraatHoogstraat

Grote MarktstraatSpuistraat

€

TYPICAL RENTAL BANDS MID 2014

0

10,000

20,000

30,000

40,000

2014 E20132012201120102009200820072006

m2

TAKE-UP OF RETAIL SPACE

0

2

4

6

8

10

12

2014 H120132012201120102009200820072006

%

SUPPLY OF RETAIL SPACE

Source: NVM

Source: NVM

Source: Locatus

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

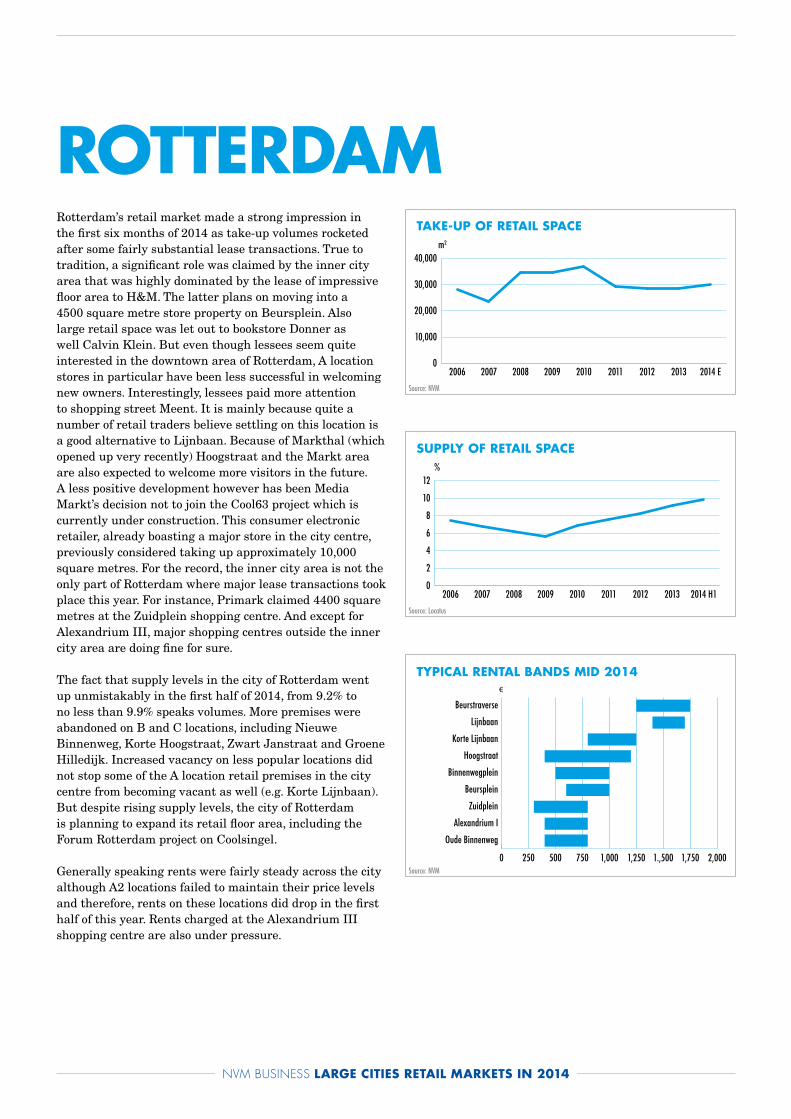

ROTTERDAMRotterdam’s retail market made a strong impression in the first six months of 2014 as take-up volumes rocketed after some fairly substantial lease transactions. True to tradition, a significant role was claimed by the inner city area that was highly dominated by the lease of impressive floor area to H&M. The latter plans on moving into a 4500 square metre store property on Beursplein. Also large retail space was let out to bookstore Donner as well Calvin Klein. But even though lessees seem quite interested in the downtown area of Rotterdam, A location stores in particular have been less successful in welcoming new owners. Interestingly, lessees paid more attention to shopping street Meent. It is mainly because quite a number of retail traders believe settling on this location is a good alternative to Lijnbaan. Because of Markthal (which opened up very recently) Hoogstraat and the Markt area are also expected to welcome more visitors in the future. A less positive development however has been Media Markt’s decision not to join the Cool63 project which is currently under construction. This consumer electronic retailer, already boasting a major store in the city centre, previously considered taking up approximately 10,000 square metres. For the record, the inner city area is not the only part of Rotterdam where major lease transactions took place this year. For instance, Primark claimed 4400 square metres at the Zuidplein shopping centre. And except for Alexandrium III, major shopping centres outside the inner city area are doing fine for sure.

The fact that supply levels in the city of Rotterdam went up unmistakably in the first half of 2014, from 9.2% to no less than 9.9% speaks volumes. More premises were abandoned on B and C locations, including Nieuwe Binnenweg, Korte Hoogstraat, Zwart Janstraat and Groene Hilledijk. Increased vacancy on less popular locations did not stop some of the A location retail premises in the city centre from becoming vacant as well (e.g. Korte Lijnbaan). But despite rising supply levels, the city of Rotterdam is planning to expand its retail floor area, including the Forum Rotterdam project on Coolsingel.

Generally speaking rents were fairly steady across the city although A2 locations failed to maintain their price levels and therefore, rents on these locations did drop in the first half of this year. Rents charged at the Alexandrium III shopping centre are also under pressure.

0 250 500 750 1,000 1,250 1.,500 1,750 2,000

Oude Binnenweg

Alexandrium I

Zuidplein

Beursplein

Binnenwegplein

Hoogstraat

Korte Lijnbaan

Lijnbaan

Beurstraverse

€

TYPICAL RENTAL BANDS MID 2014

0

10,000

20,000

30,000

40,000

2014 E20132012201120102009200820072006

m2

TAKE-UP OF RETAIL SPACE

0

2

4

6

8

10

12

2014 H120132012201120102009200820072006

%

SUPPLY OF RETAIL SPACE

Source: NVM

Source: Locatus

Source: NVM

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

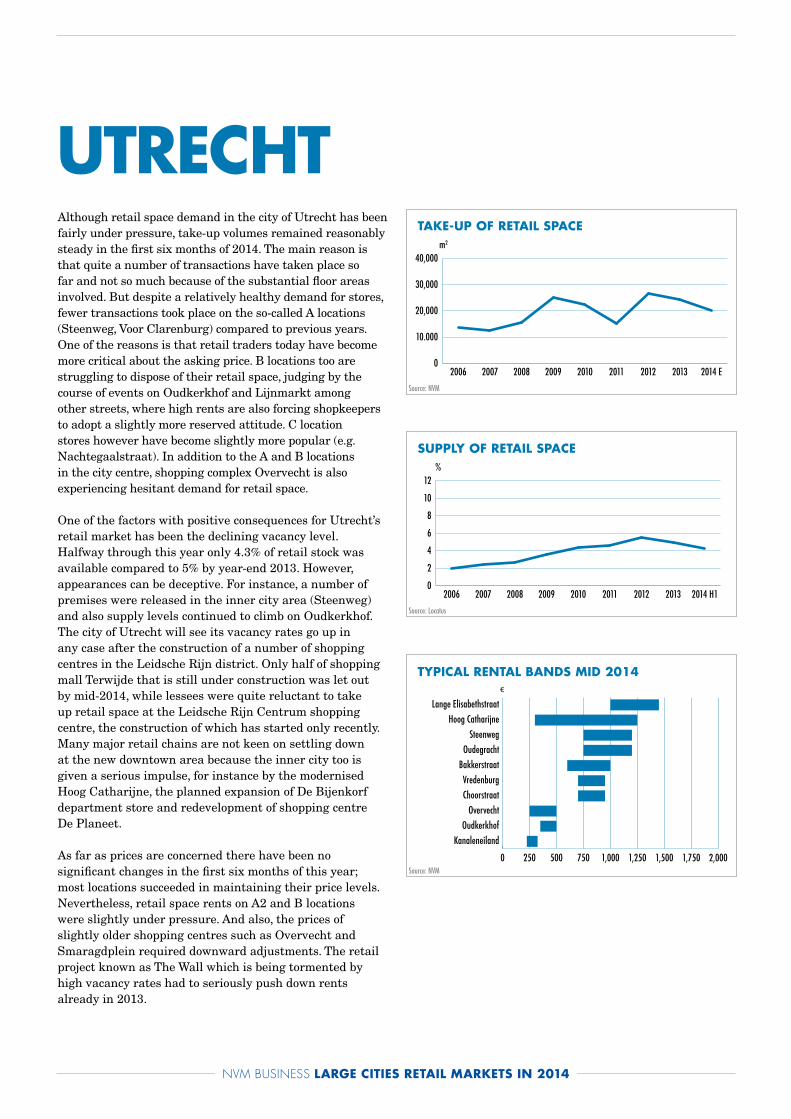

Although retail space demand in the city of Utrecht has been fairly under pressure, take-up volumes remained reasonably steady in the first six months of 2014. The main reason is that quite a number of transactions have taken place so far and not so much because of the substantial floor areas involved. But despite a relatively healthy demand for stores, fewer transactions took place on the so-called A locations (Steenweg, Voor Clarenburg) compared to previous years. One of the reasons is that retail traders today have become more critical about the asking price. B locations too are struggling to dispose of their retail space, judging by the course of events on Oudkerkhof and Lijnmarkt among other streets, where high rents are also forcing shopkeepers to adopt a slightly more reserved attitude. C location stores however have become slightly more popular (e.g. Nachtegaalstraat). In addition to the A and B locations in the city centre, shopping complex Overvecht is also experiencing hesitant demand for retail space.

One of the factors with positive consequences for Utrecht’s retail market has been the declining vacancy level. Halfway through this year only 4.3% of retail stock was available compared to 5% by year-end 2013. However, appearances can be deceptive. For instance, a number of premises were released in the inner city area (Steenweg) and also supply levels continued to climb on Oudkerkhof. The city of Utrecht will see its vacancy rates go up in any case after the construction of a number of shopping centres in the Leidsche Rijn district. Only half of shopping mall Terwijde that is still under construction was let out by mid-2014, while lessees were quite reluctant to take up retail space at the Leidsche Rijn Centrum shopping centre, the construction of which has started only recently. Many major retail chains are not keen on settling down at the new downtown area because the inner city too is given a serious impulse, for instance by the modernised Hoog Catharijne, the planned expansion of De Bijenkorf department store and redevelopment of shopping centre De Planeet.

As far as prices are concerned there have been no significant changes in the first six months of this year; most locations succeeded in maintaining their price levels. Nevertheless, retail space rents on A2 and B locations were slightly under pressure. And also, the prices of slightly older shopping centres such as Overvecht and Smaragdplein required downward adjustments. The retail project known as The Wall which is being tormented by high vacancy rates had to seriously push down rents already in 2013.

UTRECHT

0 250 500 750 1,000 1,250 1,500 1,750 2,000

KanaleneilandOudkerkhof

OvervechtChoorstraatVredenburg

BakkerstraatOudegracht

SteenwegHoog Catharijne

Lange Elisabethstraat€

TYPICAL RENTAL BANDS MID 2014

0

10.000

20,000

30,000

40,000

2014 E20132012201120102009200820072006

m2

TAKE-UP OF RETAIL SPACE

0

2

4

6

8

10

12

2014 H120132012201120102009200820072006

%

SUPPLY OF RETAIL SPACE

Source: NVM

Source: Locatus

Source: NVM

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

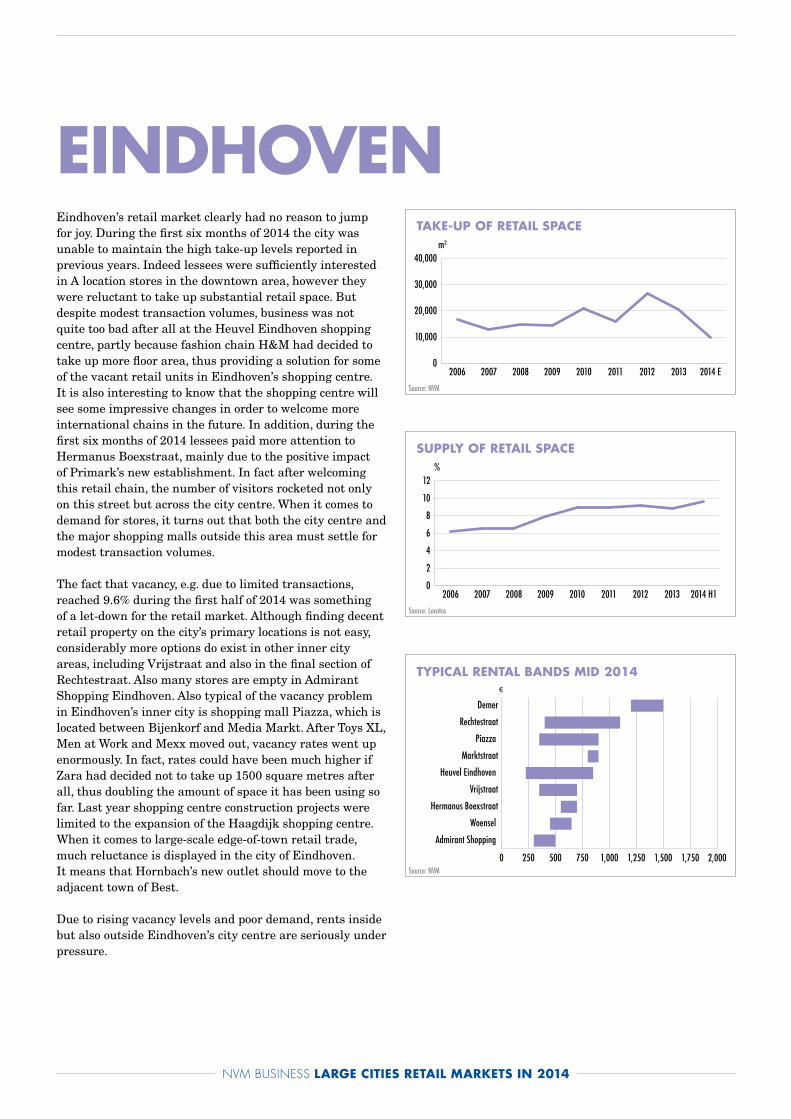

EINDHOVENEindhoven’s retail market clearly had no reason to jump for joy. During the first six months of 2014 the city was unable to maintain the high take-up levels reported in previous years. Indeed lessees were sufficiently interested in A location stores in the downtown area, however they were reluctant to take up substantial retail space. But despite modest transaction volumes, business was not quite too bad after all at the Heuvel Eindhoven shopping centre, partly because fashion chain H&M had decided to take up more floor area, thus providing a solution for some of the vacant retail units in Eindhoven’s shopping centre. It is also interesting to know that the shopping centre will see some impressive changes in order to welcome more international chains in the future. In addition, during the first six months of 2014 lessees paid more attention to Hermanus Boexstraat, mainly due to the positive impact of Primark’s new establishment. In fact after welcoming this retail chain, the number of visitors rocketed not only on this street but across the city centre. When it comes to demand for stores, it turns out that both the city centre and the major shopping malls outside this area must settle for modest transaction volumes.

The fact that vacancy, e.g. due to limited transactions, reached 9.6% during the first half of 2014 was something of a let-down for the retail market. Although finding decent retail property on the city’s primary locations is not easy, considerably more options do exist in other inner city areas, including Vrijstraat and also in the final section of Rechtestraat. Also many stores are empty in Admirant Shopping Eindhoven. Also typical of the vacancy problem in Eindhoven’s inner city is shopping mall Piazza, which is located between Bijenkorf and Media Markt. After Toys XL, Men at Work and Mexx moved out, vacancy rates went up enormously. In fact, rates could have been much higher if Zara had decided not to take up 1500 square metres after all, thus doubling the amount of space it has been using so far. Last year shopping centre construction projects were limited to the expansion of the Haagdijk shopping centre. When it comes to large-scale edge-of-town retail trade, much reluctance is displayed in the city of Eindhoven. It means that Hornbach’s new outlet should move to the adjacent town of Best.

Due to rising vacancy levels and poor demand, rents inside but also outside Eindhoven’s city centre are seriously under pressure.

0 250 500 750 1,000 1,250 1,500 1,750 2,000

Admirant Shopping

Woensel

Hermanus Boexstraat

Vrijstraat

Heuvel Eindhoven

Marktstraat

Piazza

Rechtestraat

Demer

€

TYPICAL RENTAL BANDS MID 2014

0

10,000

20,000

30,000

40,000

2014 E20132012201120102009200820072006

m2

TAKE-UP OF RETAIL SPACE

0

2

4

6

8

10

12

2014 H120132012201120102009200820072006

%

SUPPLY OF RETAIL SPACE

Source: NVM

Source: Locatus

Source: NVM

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

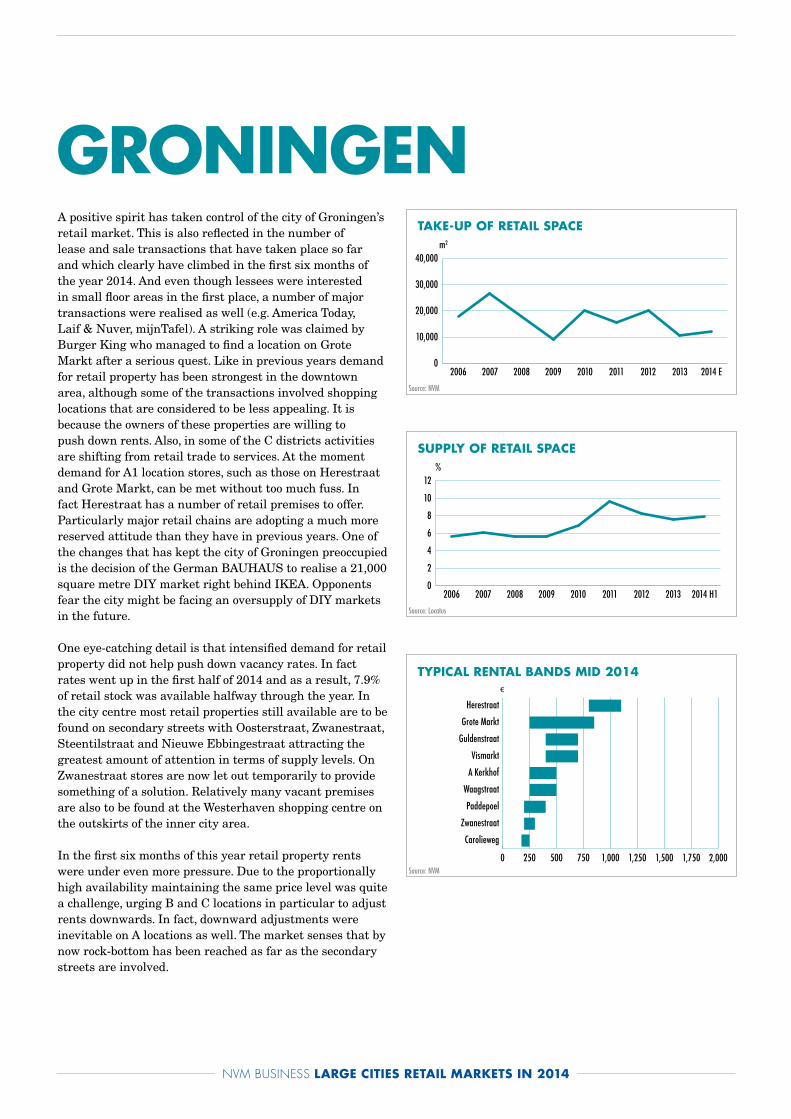

A positive spirit has taken control of the city of Groningen’s retail market. This is also reflected in the number of lease and sale transactions that have taken place so far and which clearly have climbed in the first six months of the year 2014. And even though lessees were interested in small floor areas in the first place, a number of major transactions were realised as well (e.g. America Today, Laif & Nuver, mijnTafel). A striking role was claimed by Burger King who managed to find a location on Grote Markt after a serious quest. Like in previous years demand for retail property has been strongest in the downtown area, although some of the transactions involved shopping locations that are considered to be less appealing. It is because the owners of these properties are willing to push down rents. Also, in some of the C districts activities are shifting from retail trade to services. At the moment demand for A1 location stores, such as those on Herestraat and Grote Markt, can be met without too much fuss. In fact Herestraat has a number of retail premises to offer. Particularly major retail chains are adopting a much more reserved attitude than they have in previous years. One of the changes that has kept the city of Groningen preoccupied is the decision of the German BAUHAUS to realise a 21,000 square metre DIY market right behind IKEA. Opponents fear the city might be facing an oversupply of DIY markets in the future.

One eye-catching detail is that intensified demand for retail property did not help push down vacancy rates. In fact rates went up in the first half of 2014 and as a result, 7.9% of retail stock was available halfway through the year. In the city centre most retail properties still available are to be found on secondary streets with Oosterstraat, Zwanestraat, Steentilstraat and Nieuwe Ebbingestraat attracting the greatest amount of attention in terms of supply levels. On Zwanestraat stores are now let out temporarily to provide something of a solution. Relatively many vacant premises are also to be found at the Westerhaven shopping centre on the outskirts of the inner city area.

In the first six months of this year retail property rents were under even more pressure. Due to the proportionally high availability maintaining the same price level was quite a challenge, urging B and C locations in particular to adjust rents downwards. In fact, downward adjustments were inevitable on A locations as well. The market senses that by now rock-bottom has been reached as far as the secondary streets are involved.

GRONINGEN

0 250 500 750 1,000 1,250 1,500 1,750 2,000

Carolieweg

Zwanestraat

Paddepoel

Waagstraat

A Kerkhof

Vismarkt

Guldenstraat

Grote Markt

Herestraat

€

TYPICAL RENTAL BANDS MID 2014

0

10,000

20,000

30,000

40,000

2014 E20132012201120102009200820072006

m2

TAKE-UP OF RETAIL SPACE

0

2

4

6

8

10

12

2014 H120132012201120102009200820072006

%

SUPPLY OF RETAIL SPACE

Source: NVM

Source: Locatus

Source: NVM

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

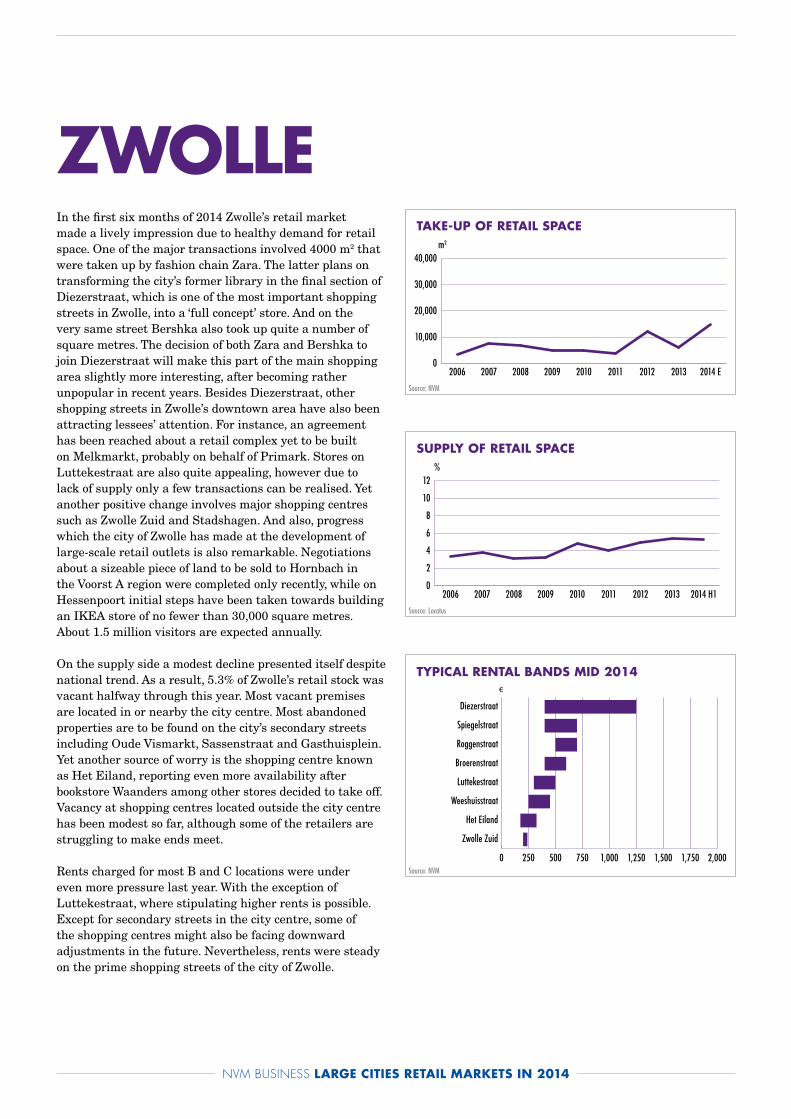

In the first six months of 2014 Zwolle’s retail market made a lively impression due to healthy demand for retail space. One of the major transactions involved 4000 m2 that were taken up by fashion chain Zara. The latter plans on transforming the city’s former library in the final section of Diezerstraat, which is one of the most important shopping streets in Zwolle, into a ‘full concept’ store. And on the very same street Bershka also took up quite a number of square metres. The decision of both Zara and Bershka to join Diezerstraat will make this part of the main shopping area slightly more interesting, after becoming rather unpopular in recent years. Besides Diezerstraat, other shopping streets in Zwolle’s downtown area have also been attracting lessees’ attention. For instance, an agreement has been reached about a retail complex yet to be built on Melkmarkt, probably on behalf of Primark. Stores on Luttekestraat are also quite appealing, however due to lack of supply only a few transactions can be realised. Yet another positive change involves major shopping centres such as Zwolle Zuid and Stadshagen. And also, progress which the city of Zwolle has made at the development of large-scale retail outlets is also remarkable. Negotiations about a sizeable piece of land to be sold to Hornbach in the Voorst A region were completed only recently, while on Hessenpoort initial steps have been taken towards building an IKEA store of no fewer than 30,000 square metres. About 1.5 million visitors are expected annually.

On the supply side a modest decline presented itself despite national trend. As a result, 5.3% of Zwolle’s retail stock was vacant halfway through this year. Most vacant premises are located in or nearby the city centre. Most abandoned properties are to be found on the city’s secondary streets including Oude Vismarkt, Sassenstraat and Gasthuisplein. Yet another source of worry is the shopping centre known as Het Eiland, reporting even more availability after bookstore Waanders among other stores decided to take off. Vacancy at shopping centres located outside the city centre has been modest so far, although some of the retailers are struggling to make ends meet.

Rents charged for most B and C locations were under even more pressure last year. With the exception of Luttekestraat, where stipulating higher rents is possible. Except for secondary streets in the city centre, some of the shopping centres might also be facing downward adjustments in the future. Nevertheless, rents were steady on the prime shopping streets of the city of Zwolle.

ZWOLLE

0 250 500 750 1,000 1,250 1,500 1,750 2,000

Zwolle Zuid

Het Eiland

Weeshuisstraat

Luttekestraat

Broerenstraat

Roggenstraat

Spiegelstraat

Diezerstraat

€

TYPICAL RENTAL BANDS MID 2014

0

10,000

20,000

30,000

40,000

2014 E20132012201120102009200820072006

m2

TAKE-UP OF RETAIL SPACE

0

2

4

6

8

10

12

2014 H120132012201120102009200820072006

%

SUPPLY OF RETAIL SPACE

Source: NVM

Source: Locatus

Source: NVM

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

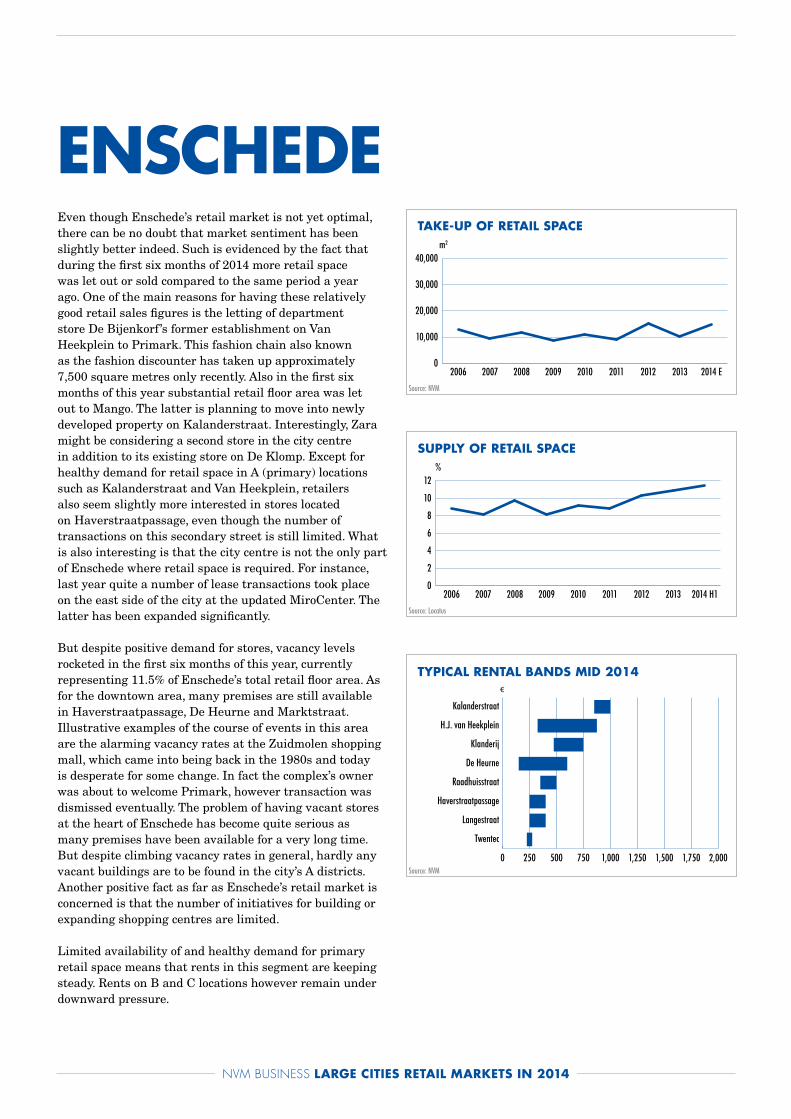

Even though Enschede’s retail market is not yet optimal, there can be no doubt that market sentiment has been slightly better indeed. Such is evidenced by the fact that during the first six months of 2014 more retail space was let out or sold compared to the same period a year ago. One of the main reasons for having these relatively good retail sales figures is the letting of department store De Bijenkorf ’s former establishment on Van Heekplein to Primark. This fashion chain also known as the fashion discounter has taken up approximately 7,500 square metres only recently. Also in the first six months of this year substantial retail floor area was let out to Mango. The latter is planning to move into newly developed property on Kalanderstraat. Interestingly, Zara might be considering a second store in the city centre in addition to its existing store on De Klomp. Except for healthy demand for retail space in A (primary) locations such as Kalanderstraat and Van Heekplein, retailers also seem slightly more interested in stores located on Haverstraatpassage, even though the number of transactions on this secondary street is still limited. What is also interesting is that the city centre is not the only part of Enschede where retail space is required. For instance, last year quite a number of lease transactions took place on the east side of the city at the updated MiroCenter. The latter has been expanded significantly.

But despite positive demand for stores, vacancy levels rocketed in the first six months of this year, currently representing 11.5% of Enschede’s total retail floor area. As for the downtown area, many premises are still available in Haverstraatpassage, De Heurne and Marktstraat. Illustrative examples of the course of events in this area are the alarming vacancy rates at the Zuidmolen shopping mall, which came into being back in the 1980s and today is desperate for some change. In fact the complex’s owner was about to welcome Primark, however transaction was dismissed eventually. The problem of having vacant stores at the heart of Enschede has become quite serious as many premises have been available for a very long time. But despite climbing vacancy rates in general, hardly any vacant buildings are to be found in the city’s A districts. Another positive fact as far as Enschede’s retail market is concerned is that the number of initiatives for building or expanding shopping centres are limited.

Limited availability of and healthy demand for primary retail space means that rents in this segment are keeping steady. Rents on B and C locations however remain under downward pressure.

ENSCHEDE

0 250 500 750 1,000 1,250 1,500 1,750 2,000

Twentec

Langestraat

Haverstraatpassage

Raadhuisstraat

De Heurne

Klanderij

H.J. van Heekplein

Kalanderstraat

€

TYPICAL RENTAL BANDS MID 2014

0

10,000

20,000

30,000

40,000

2014 E20132012201120102009200820072006

m2

TAKE-UP OF RETAIL SPACE

0

2

4

6

8

10

12

2014 H120132012201120102009200820072006

%

SUPPLY OF RETAIL SPACE

Source: NVM

Source: Locatus

Source: NVM

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

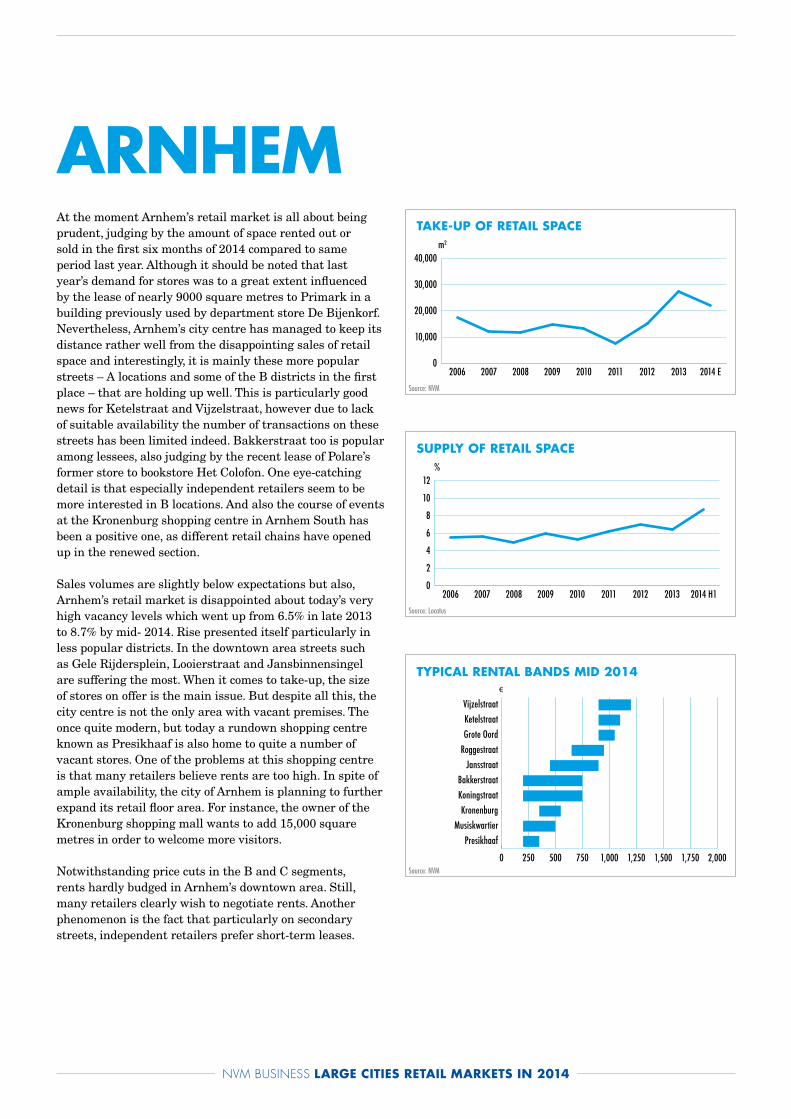

At the moment Arnhem’s retail market is all about being prudent, judging by the amount of space rented out or sold in the first six months of 2014 compared to same period last year. Although it should be noted that last year’s demand for stores was to a great extent influenced by the lease of nearly 9000 square metres to Primark in a building previously used by department store De Bijenkorf. Nevertheless, Arnhem’s city centre has managed to keep its distance rather well from the disappointing sales of retail space and interestingly, it is mainly these more popular streets – A locations and some of the B districts in the first place – that are holding up well. This is particularly good news for Ketelstraat and Vijzelstraat, however due to lack of suitable availability the number of transactions on these streets has been limited indeed. Bakkerstraat too is popular among lessees, also judging by the recent lease of Polare’s former store to bookstore Het Colofon. One eye-catching detail is that especially independent retailers seem to be more interested in B locations. And also the course of events at the Kronenburg shopping centre in Arnhem South has been a positive one, as different retail chains have opened up in the renewed section.

Sales volumes are slightly below expectations but also, Arnhem’s retail market is disappointed about today’s very high vacancy levels which went up from 6.5% in late 2013 to 8.7% by mid- 2014. Rise presented itself particularly in less popular districts. In the downtown area streets such as Gele Rijdersplein, Looierstraat and Jansbinnensingel are suffering the most. When it comes to take-up, the size of stores on offer is the main issue. But despite all this, the city centre is not the only area with vacant premises. The once quite modern, but today a rundown shopping centre known as Presikhaaf is also home to quite a number of vacant stores. One of the problems at this shopping centre is that many retailers believe rents are too high. In spite of ample availability, the city of Arnhem is planning to further expand its retail floor area. For instance, the owner of the Kronenburg shopping mall wants to add 15,000 square metres in order to welcome more visitors.

Notwithstanding price cuts in the B and C segments, rents hardly budged in Arnhem’s downtown area. Still, many retailers clearly wish to negotiate rents. Another phenomenon is the fact that particularly on secondary streets, independent retailers prefer short-term leases.

ARNHEM

0 250 500 750 1,000 1,250 1,500 1,750 2,000

PresikhaafMusiskwartier

KronenburgKoningstraatBakkerstraat

JansstraatRoggestraatGrote OordKetelstraatVijzelstraat

€

TYPICAL RENTAL BANDS MID 2014

0

10,000

20,000

30,000

40,000

2014 E20132012201120102009200820072006

m2

TAKE-UP OF RETAIL SPACE

0

2

4

6

8

10

12

2014 H120132012201120102009200820072006

%

SUPPLY OF RETAIL SPACE

Source: NVM

Source: Locatus

Source: NVM

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

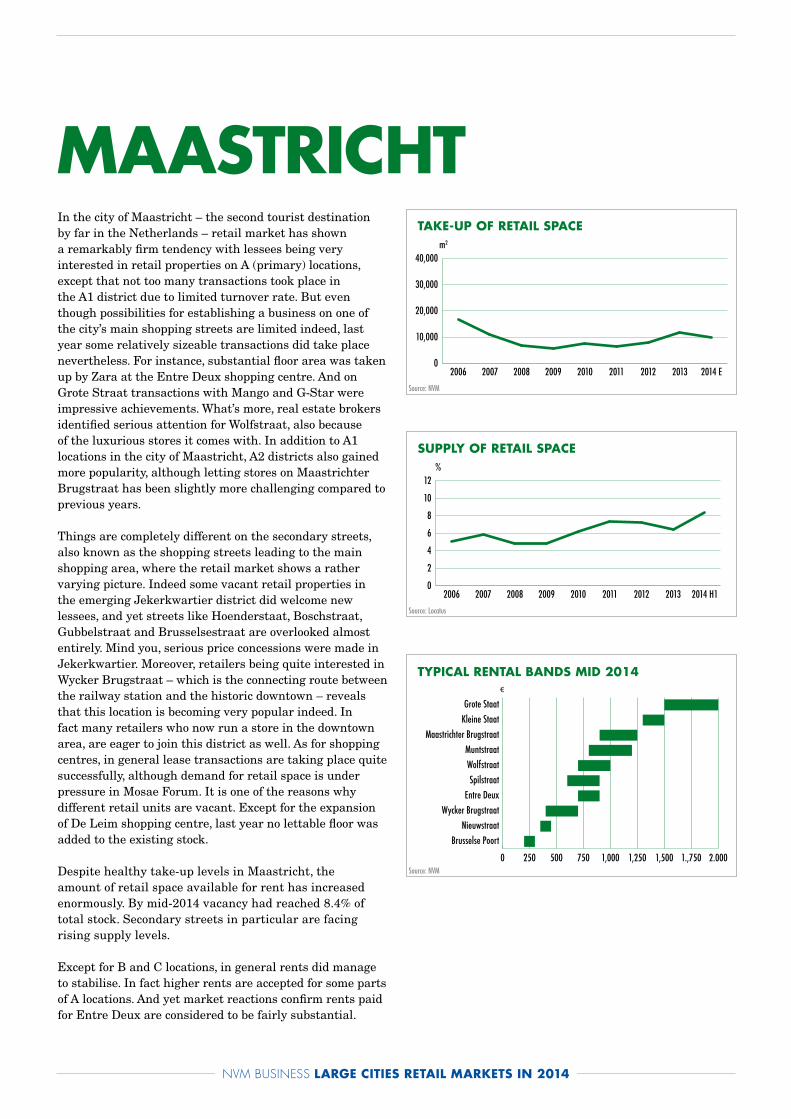

In the city of Maastricht – the second tourist destination by far in the Netherlands – retail market has shown a remarkably firm tendency with lessees being very interested in retail properties on A (primary) locations, except that not too many transactions took place in the A1 district due to limited turnover rate. But even though possibilities for establishing a business on one of the city’s main shopping streets are limited indeed, last year some relatively sizeable transactions did take place nevertheless. For instance, substantial floor area was taken up by Zara at the Entre Deux shopping centre. And on Grote Straat transactions with Mango and G-Star were impressive achievements. What’s more, real estate brokers identified serious attention for Wolfstraat, also because of the luxurious stores it comes with. In addition to A1 locations in the city of Maastricht, A2 districts also gained more popularity, although letting stores on Maastrichter Brugstraat has been slightly more challenging compared to previous years.

Things are completely different on the secondary streets, also known as the shopping streets leading to the main shopping area, where the retail market shows a rather varying picture. Indeed some vacant retail properties in the emerging Jekerkwartier district did welcome new lessees, and yet streets like Hoenderstaat, Boschstraat, Gubbelstraat and Brusselsestraat are overlooked almost entirely. Mind you, serious price concessions were made in Jekerkwartier. Moreover, retailers being quite interested in Wycker Brugstraat – which is the connecting route between the railway station and the historic downtown – reveals that this location is becoming very popular indeed. In fact many retailers who now run a store in the downtown area, are eager to join this district as well. As for shopping centres, in general lease transactions are taking place quite successfully, although demand for retail space is under pressure in Mosae Forum. It is one of the reasons why different retail units are vacant. Except for the expansion of De Leim shopping centre, last year no lettable floor was added to the existing stock.

Despite healthy take-up levels in Maastricht, the amount of retail space available for rent has increased enormously. By mid-2014 vacancy had reached 8.4% of total stock. Secondary streets in particular are facing rising supply levels.

Except for B and C locations, in general rents did manage to stabilise. In fact higher rents are accepted for some parts of A locations. And yet market reactions confirm rents paid for Entre Deux are considered to be fairly substantial.

MAASTRICHT

0 250 500 750 1,000 1,250 1,500 1.,750 2.000

Brusselse PoortNieuwstraat

Wycker BrugstraatEntre Deux

SpilstraatWolfstraatMuntstraat

Maastrichter BrugstraatKleine StaatGrote Staat

€

TYPICAL RENTAL BANDS MID 2014

0

10,000

20,000

30,000

40,000

2014 E20132012201120102009200820072006

m2

TAKE-UP OF RETAIL SPACE

0

2

4

6

8

10

12

2014 H120132012201120102009200820072006

%

SUPPLY OF RETAIL SPACE

Source: NVM

Source: Locatus

Source: NVM

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

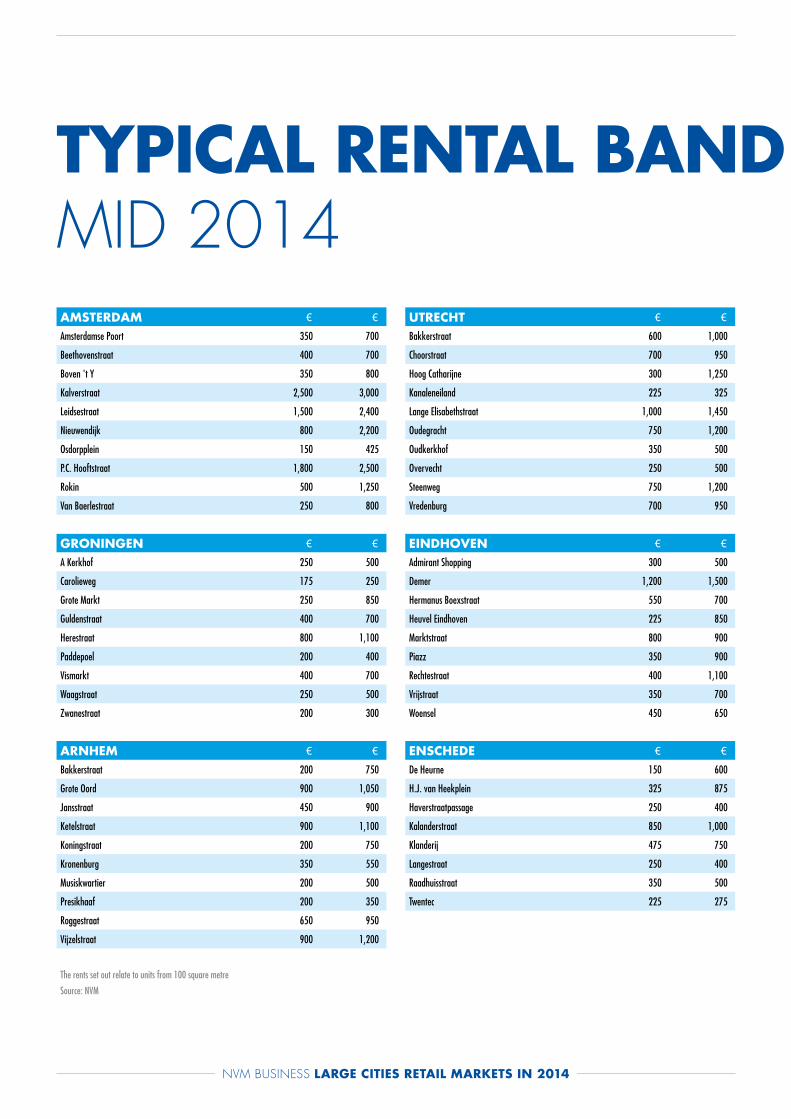

TYPICAL RENTAL BAND S MID 2014

The rents set out relate to units from 100 square metre

Source: NVM

AMSTERDAM 2 2

Amsterdamse Poort 350 700

Beethovenstraat 400 700

Boven 't Y 350 800

Kalverstraat 2,500 3,000

Leidsestraat 1,500 2,400

Nieuwendijk 800 2,200

Osdorpplein 150 425

P.C. Hooftstraat 1,800 2,500

Rokin 500 1,250

Van Baerlestraat 250 800

GRONINGEN 2 2

A Kerkhof 250 500

Carolieweg 175 250

Grote Markt 250 850

Guldenstraat 400 700

Herestraat 800 1,100

Paddepoel 200 400

Vismarkt 400 700

Waagstraat 250 500

Zwanestraat 200 300

ARNHEM 2 2

Bakkerstraat 200 750

Grote Oord 900 1,050

Jansstraat 450 900

Ketelstraat 900 1,100

Koningstraat 200 750

Kronenburg 350 550

Musiskwartier 200 500

Presikhaaf 200 350

Roggestraat 650 950

Vijzelstraat 900 1,200

UTRECHT 2 2

Bakkerstraat 600 1,000

Choorstraat 700 950

Hoog Catharijne 300 1,250

Kanaleneiland 225 325

Lange Elisabethstraat 1,000 1,450

Oudegracht 750 1,200

Oudkerkhof 350 500

Overvecht 250 500

Steenweg 750 1,200

Vredenburg 700 950

EINDHOVEN 2 2

Admirant Shopping 300 500

Demer 1,200 1,500

Hermanus Boexstraat 550 700

Heuvel Eindhoven 225 850

Marktstraat 800 900

Piazz 350 900

Rechtestraat 400 1,100

Vrijstraat 350 700

Woensel 450 650

ENSCHEDE 2 2

De Heurne 150 600

H.J. van Heekplein 325 875

Haverstraatpassage 250 400

Kalanderstraat 850 1,000

Klanderij 475 750

Langestraat 250 400

Raadhuisstraat 350 500

Twentec 225 275

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

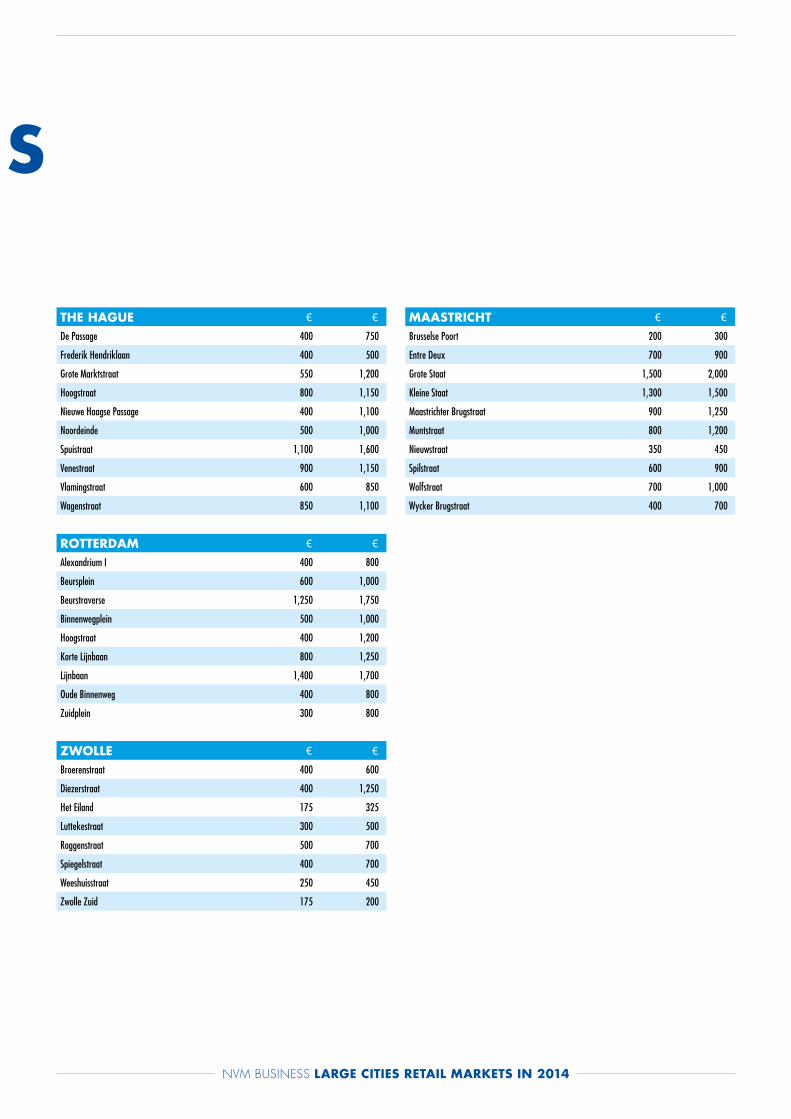

TYPICAL RENTAL BAND S MID 2014

THE HAGUE 2 2

De Passage 400 750

Frederik Hendriklaan 400 500

Grote Marktstraat 550 1,200

Hoogstraat 800 1,150

Nieuwe Haagse Passage 400 1,100

Noordeinde 500 1,000

Spuistraat 1,100 1,600

Venestraat 900 1,150

Vlamingstraat 600 850

Wagenstraat 850 1,100

ROTTERDAM 2 2

Alexandrium I 400 800

Beursplein 600 1,000

Beurstraverse 1,250 1,750

Binnenwegplein 500 1,000

Hoogstraat 400 1,200

Korte Lijnbaan 800 1,250

Lijnbaan 1,400 1,700

Oude Binnenweg 400 800

Zuidplein 300 800

ZWOLLE 2 2

Broerenstraat 400 600

Diezerstraat 400 1,250

Het Eiland 175 325

Luttekestraat 300 500

Roggenstraat 500 700

Spiegelstraat 400 700

Weeshuisstraat 250 450

Zwolle Zuid 175 200

MAASTRICHT 2 2

Brusselse Poort 200 300

Entre Deux 700 900

Grote Staat 1,500 2,000

Kleine Staat 1,300 1,500

Maastrichter Brugstraat 900 1,250

Muntstraat 800 1,200

Nieuwstraat 350 450

Spilstraat 600 900

Wolfstraat 700 1,000

Wycker Brugstraat 400 700

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

ANALYSING SECONDARY LOCATIONSIn quite a number of cities the purpose of shopping streets leading to the main shopping area – usually these are B and C districts of the main shopping area – has been under pressure due to consumers’ ever-changing purchasing behaviour. This leads to vacant buildings and lower rents. And yet, secondary streets do have a key function as far as the main shopping areas are concerned. Being home to specialist shops and catering establishments, means they do add a particular colour to the character of a city.

Secondary streets must continue to make investments in order to remain attractive. However, it depends on local circumstances and therefore, maintaining all secondary streets is not a realistic thing to do. There are promising streets but also disadvantaged ones. Disadvantaged streets also qualify for a different purpose in life, e.g. provision of services and housing.

At least some aspects need to exist in order to have promising and future-proof secondary streets. These aspects are mentioned in NVM Business’ report called Aanloopstraten in beeld. Locational aspects such as the proximity of a shopping centre or direct connection to a primary district, are pivotal. Adjustment to certain aspects might be required in order to strengthen the secondary streets in the years to come.

Collaboration is key, for strengthening those streets is a common interest of shopkeepers and entrepreneurs alike as well as property owners, financiers, municipalities and real estate agents. All parties involved must ensure optimal accessibility at all times, a balanced distribution of the number of parking spaces and a clean and safe shopping area. Also one might consider changing the secondary street concept for the better, increasing pedestrian flow by organising interesting events, improving property and the public spaces.

In proceeding together one should also take specific (temporary and structural) measures in order to fight against vacancy. Temporary measures include pop-up stores or disguising vacant property by means of (three-dimensional) photo prints. Structural steps include the acquisition of premises through a special fund and the introduction of turnover rent. It is best to opt for strong locations and powerful concepts in order to tackle secondary street vacancies.

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

DEFINITIONS A locations Retail locations in the main shopping areas are categorised as A, B or C. This is also referred to as classification based on pedestrian flow or quality of the location. The busiest part of any shopping area, which is the area with most passers-by, is known as A1. Other locations within a shopping area are categorised according to how the number of passers-by compares to the maximum number of passers-by on the A1 location (see table below). The table below represents the bandwidth of the number of passers-by for each type of location compared to the most crowded part of the shopping area in question.

A1 locations 75 - 100% A2 locations 50 - 75%B1 locations 25 - 50%B2 locations 10 - 25%C locations 5 - 10%

Rent Basic rent realised per square metre of lettable floor area, exclusive of VAT.

Retail space A spatial and independent unit accessible to the public, used primarily by end consumers in order to display and offer items that are not consumed on the spot. Hence a retail trade purpose must be involved.

Secondary location B or C location in the main shopping area.

Supply Retail space immediately available for rent or sale. Supply does not include stores at the preparatory stage and which are yet to be constructed. Supply does include vacant stores and stores under construction as well as spaces that are still being used but which will be released in the near future.

Take-up Lease and sales transactions taking place on the open market. Take-up does not include users who provide for their own accommodation (‘owner-occupier development’). The same applies to sale-and-leaseback agreements and extensions of contracts.

Vacancy The total amount of physically vacant retail premises. Usually vacancy is less than supply.

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014

This publication has been produced with the assistance of: Berk & Levert Makelaardij (Amsterdam), Blok Makelaardij (Rotterdam), Boek & Offermans Makelaars (Maastricht), Boers & Lem (Enschede), Colliers International (Amsterdam), De Graaf van Vilsteren Garantiemakelaars (Zwolle), Frisia Makelaars (Den Haag), GNM Makelaardij (Maastricht), Jansen Nadorp Weatherall (Den Haag), Kolsteren Bedrijfshuisvesting (Eindhoven), KroesePaternotte (Amsterdam), KroeseTempert Bedrijfsmakelaars (Zwolle), Molenbeek Makelaars (Utrecht), MVGM (Arnhem), Ooms Makelaars Bedrijfshuisvesting (Rotterdam), Overduin & Casander Bedrijfsmakelaars (Groningen), Rodenburg Bedrijfsmakelaars (Zwolle), RSP Makelaars (Eindhoven), Ruijters Groep (Maastricht), Snelder Zijlstra Bedrijfsmakelaars (Enschede), Strijbosch Thunnissen Makelaars (Arnhem), Van Rossum Makelaars Bedrijfshuisvesting (Utrecht), Vos Hoving Bedrijfsmakelaars (Groningen), Waltmann Bedrijfshuisvesting (Utrecht)

Colophon

Composition Drs. R.L. Bak and drs. G. RavenData source NVM Data & Research, Locatus, LMBS Retail, Strijbosch Thunnissen Makelaars Design Proof Studio, AmsterdamPhotography Hugo Thomassen/3W New Development

September 2014

NVM BusinessFakkelstede 13431 HZ Nieuwegein Telephone: (030) 608 51 85

NVM BUSINESS LARGE CITIES RETAIL MARKETS IN 2014