Embed Size (px)

Citation preview

Language FTR and Earnings Management: International Evidence

Marco Fasan Department of Management

Ca Foscari University of Venice [email protected]

Giorgio Gotti

College of Business University of Texas at El Paso

Tony Kang DeGroote School of Business

McMaster University [email protected]

Yi Liu

DeGroote School of Business McMaster University [email protected]

Abstract

We study whether a particular aspect of language structure, the future-time reference (FTR) of a language, explains variation in corporate earnings management behaviors around the world. Based on the Sapir-Whorf hypothesis (Whorf 1956), we predict that grammatically referencing the future, which induces humans to perceive the future more sharply distinct from the present, induces myopic management behavior. In support of this idea, we find that firms headquartered in strong-FTR language countries are more likely to engage in accrual and real activities earnings management to meet short-term earning benchmarks. Keywords: Accrual-based Earnings Management, Real Earnings Management,

Future-Time-Reference, Language, Myopia, Short-Termism Acknowledgements: We thank seminar participants at Syracuse University, Ca’ Foscari University

of Venice, and AAA-International Accounting Section 2016 Midyear meeting for helpful comments.

1

1. Introduction

The Sapir-Whorf hypothesis (Whorf 1956) posits that the structure of a language systematically

shapes the ways its speakers conceptualize the world, affecting their thoughts and behaviors.

Consistent with this idea, Wittgenstein (1922) argues that language is the means by which people

picture and reason about reality. In contrast, others claim that all human languages are constrained

by a “universal grammar” (Chomsky 1957) and that there is no compelling evidence that languages

dramatically shape their speakers’ way of thinking (Pinker 1994). To date, this remains an

unresolved issue in humanities and social science, and evidence in the context of economic decision

making is even more limited, with the exception of Chen (2013). Not surprisingly, the issue is

severely understudied in corporate settings. To fill this void in the literature and to enhance our

understanding on this issue, we study whether the dominant business language in a society explains

an important corporate decision, i.e., corporate earnings management behavior.

One major difference in language structure is the future-time reference (FTR), i.e., the way of

grammatically encoding the future events (Dahl 1985). If a language requires its speakers to

explicitly use future tense to mark prospective events, then the language is regarded as having

strong-FTR. If it does not have such a requirement, it is said to be a weak-FTR language. In this

paper, we investigate the effects of future-time reference (FTR) of language on corporate earnings

management. The motivation of our paper is twofold. First, prior economics and finance literature

has found that language FTR affects the economic behaviors across individual (e.g., individual

savings, Chen 2013), as well as firm behaviors, e.g., corporate social responsibility, (Liang et al.

2

2014) and corporate cash holdings (Chen et al. 2015). However, there is little evidence on whether

the language feature explains corporate financial reporting behavior. Second, international evidence

on earnings management shows that corporate earnings management varies with country-level legal,

economic and cultural institutions (e.g., Leuz et al. 2003; Han et al. 2010). Despite the potential

pervasive effect on human behavior and various institutions (Whorf et al. 1956; Liang et al. 2014),

however, there is no direct evidence that links the structure of the dominant business language in the

economy to the prevailing corporate reporting behavior.

We address this issue by testing whether firms headquartered in strong-FTR language countries,

where the economic agents have been shown to demonstrate more myopic behavior, manage

earnings more. Earnings management through accounting accruals or real operations to meet

short-term capital market benchmarks is often characterized as being myopic, as the decision tends

to reverse in the future (Healy and Wahlen 1999). If, as linguistics and economics theories predict,

strong-FTR language, by requiring grammatically separating the future from the present, leads its

speakers to feel less pressure from the future and, thus, fosters short-term oriented behavior,

managers in jurisdictions where the dominant business language is more future oriented are more

likely to engage in earnings management.

Next, we examine how language FTR interacts with investor protection in affecting earnings

management. A priori, the interaction between language FTR and investor protection is not obvious.

On the one hand, given that public accounting information is more extensively used in managerial

3

contracting in strong investor protection countries (Han et al. 2010), it is possible that myopic

strong-FTR managers are more incentivized to engage in earnings manipulation in countries with

strong investor protection to meet short-term capital market benchmarks. On the other hand,

however, since investor protection limits the ability of managers to acquire private control benefits

and mask firm performance (Leuz et al. 2003), the tendency for managers to engage in earnings

management harbored by strong language FTR should be curbed.

We empirically examine the above predictions about the effects of language FTR on earnings

management across 37 countries during the period 1994-2013. Following Liang et al. (2014) and

Chen et al. (2015), we categorize the FTR of the official language (strong versus weak) in each

country based on the classification of Chen (2013). We examine three types of earnings management

behaviors: accrual-based earnings management, earnings management through real economic

decisions (real earnings management) and earnings benchmark meeting/beating. We document a

significantly positive association between strong language FTR and earnings management (both

accrual-based and real activities) after accounting for firm, industry, country level controls.

Furthermore, this association decreases with the strength of investor protection, consistent with

investor protection acting as a governance mechanism in mitigating earnings manipulation.

This study makes important contributions to several strands of literature. First, it extends the

accounting, finance, and international business literature that documents institutional influence on

corporate earnings management behavior. Specifically, we identify language as a relevant human

4

institution that explains such behavior, in addition to legal and cultural institutions (e.g., Leuz et al.

2003; Han et al. 2010). Second, this study contributes to corporate finance literature on managerial

myopia by identifying strong-FTR languages as a driver of such behavior in corporate decisions.

Third, it contributes to the broader economics literature by providing evidence in support of the

Sapir-Whorf hypothesis (1956). Our findings complement recent studies that provided support to

this hypothesis using individual and household data (Chen 2013) by documenting evidence from

corporate behavior.

The remainder of this article is organized as follows. In section 2, we review related literature, and

develop our hypotheses. In section 3, we describe our key variables and model specifications. In

section 4, we present and interpret the main results. In section 5, we perform sensitivity analyses and

robustness checks. And finally in section 6, we make our conclusions.

2. Literature Review and Hypothesis Development

2.1 Linguistic relativity, Future-Time Reference of Language and Economic Behavior

One stream of research in linguistics, known as linguistic relativity (or Sapir-Whorf hypothesis),

argues that the structure of a language systematically shapes the ways its speakers conceptualize the

world, affects their thoughts and behaviors, and even influences their cognitive processes and

national culture (Sapir 1951; Whorf et al. 1956; Chen 2013). For instance, Slobin (1987) posits that

language affects thoughts because speakers are required to grammatically attend to and encode

various aspects of situations when they speak. Cognitive science research lends support to this

5

argument by showing that variation in grammatical systems influences speakers’ cognitive

representation of the reality (e.g., Evans and Levinson 2009).

Recent studies in economics and finance have started to link heterogeneity in language structure

with differences in both individual and corporate economic behaviors.

In particular, these studies relies on a stream of linguistics literature showing that languages differ

widely in terms of grammatically marking the future time of events (e.g., Dahl 1985). In some

languages (i.e., strong-FTR languages), e.g., English, the use of grammaticalized future-time

reference is “explicitly required in (main clause) prediction-based contexts” (Dahl 2000), whereas in

other languages (i.e., weak-FTR languages), e.g., Mandarin, the future tense is not required. To

illustrate, when talking about the future, English forces its speaker to put constructs such as “will”,

“shall”, or “be going to” in the sentence to refer to the future. However, since Mandarin does not

differentiate between the future and the present tenses, a Mandarin speaker tends to omit any

equivalent of “will” in English. Below is an example of how an English speaker and a Mandarin

speaker describe what they are going to do for tomorrow:

English: I will go to school.

Mandarin (original): Wo qu shangxue.

Mandarin (translated): I go to school.

As can be seen from the example, a future tense (or “will” in this case) is mandated in English, but

not in Mandarin. Linguistics literature has documented that this grammatical difference is

6

widespread among languages across countries.

By building on this notion, Chen (2013) finds that weak-FTR language speakers tend to have more

savings, consistent with weak-FTR leading to more future-oriented human behaviors. Tested at the

corporate level, weak-FTR language is found to be associated with greater firm future-oriented

activities, such as higher precautionary cash holdings (Chen et al. 2015), and more corporate social

responsibility (CSR) (Liang et al. 2014).

2.2 Earnings Management

Earnings management is defined as occurring when managers use judgment in financial reporting

and in structuring transactions to alter financial reports to either mislead some stakeholders about the

underlying economic performance of the company, or to influence contractual outcomes that depend

on reported accounting numbers (see Healy and Wahlen 1999).

Previous studies found the existence of two main types of earnings management: accrual-based

earnings management and management of real economic activities. For accruals management,

managers “borrow” earnings from past or future periods to improve earnings reported in the current

period (see Healy and Whalen 1999). For real activities management, managers time revenues or

adjust discretionary expenses to meet current earnings targets (see Bushee 1998; Roychowdhury

2006). While earnings management is usually seen in the light of the Agency Theory, where

managers with more information can achieve benefits at the expenses of the shareholders, Brochet et

al (2014) suggest that it is a short-term oriented practice, as firms are often found to manipulate

7

earnings in order to meet short-term capital market benchmarks.

2.3 Linguistic Hypotheses in Earnings Management

Based on the linguistic relativity literature and prior evidence on the connection between language

FTR and economic behaviors, we focus on one type of corporate behavior – earnings management,

which is to a large extent influenced by managerial short termism and thus very likely to be affected

by such a language structure difference.

Linguistic relativity posits that language influences people’s decision-making process through its

grammatical future-time reference. More specifically, Chen (2013) identifies two mechanisms

(perception of future distance and timing uncertainty) connecting language FTR to short termism.

First (perception of future distance), weak-FTR language speakers, who refer to future events as

they were happening now, should perceive future events as less distant. Therefore, they are more

long-term oriented than strong-FTR language speakers.

Second (timing uncertainty), to repeatedly refer to the future should lead to a sharper distinction

between the present and the future and to a clearer classification of future as a different category.

This lower (higher) timing uncertainty leads strong (weak) FTR language speakers being more short

(long) term oriented (see Chen, 2013).

Hence, strong-FTR language speakers would feel less pressure from the future, and their behaviors

tend to be more short-term oriented (Liang et al. 2014). Prior theories and evidence in accounting

indicate that managers placing a greater weight on the short term are more likely to manipulate

8

current-period earnings (either through accounting choices or real actions) in order to obtain the

benefits of short-term positive earnings surprises or to avoid adverse equity market consequences,

probably at the expense of future earnings and long-term value creation (Stein 1989; Brochet et al.

2014). Based on the above arguments, we hypothesize that strong-FTR language induces managers

to be more short-term oriented. And such managerial myopia increases the likelihood for managers

to engage in earnings management to meet short-term earnings benchmarks.

H1: Managers in strong-FTR language countries manage earnings more

In addition, we examine the interaction between language FTR and investor protection in affecting

earnings management. On the one hand, legal institutions such as investor protection may reinforce

the effect of language FTR on earnings management. For example, Han et al. (2010) argue that

public accounting information is more extensively used in managerial contracting in strong investor

protection countries than in weak investor protection countries. Supporting this argument, DeFond et

al. (2007) find that earnings are more highly correlated with stock prices in strong investor

protection countries. If this is the case, we would expect short-term oriented strong-FTR managers

to have more incentives to engage in earnings management to meet short-term earnings benchmarks

in strong investor protection environments. On the other hand, investor protection may mitigate the

effect of language FTR on earnings management. This is premised on the idea that strong investor

protection limits the ability of the managers to acquire private control benefits, reducing their

incentives to mask corporate performance (Leuz et al. 2003). Thus, investor protection may act as a

governance mechanism to curb myopic managers that are exposed to the influences of strong-FTR

language environments from indulging themselves in earnings manipulation. Taken together, a

9

priori, it is unclear how language FTR and investor protection interact with each other to affect

earnings management. Therefore, our second hypothesis, stated in null form, is:

H2: The interaction between language FTR and investor protection in affecting earnings

management is undeterminable.

3. Research Design and Sample

3.1 Measure of Future-Time Reference of Language

To categorize the FTR of the official language (strong versus weak) in each country, we use the

three measures in Chen (2013) and one aggregate measure developed using the principal component

analysis (PCA) . The first measure is 𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!", a dummy variable that takes the value of one

for firms headquartered in strong-FTR language countries, and zero otherwise. This categorization

mirrors Thieroff’s (2000) classification of neutral language for “futureless” language. The second

measure is 𝑆𝑅!" , which calculates the proportion of sentences containing a grammatical

future-marker when referring to the future in a language, while the third is 𝑉𝑅!" measuring the ratio

of the number of grammatically future-marked verbs to the total number of future-referring verb in a

language. These two measures are continuous variables and capture the frequency of a language

grammatically marking the future time. Finally, to capture the common dimension in the three

individual measures, we employ the PCA to construct an overall summary measure of the intensity

of the use of language FTR (𝑝𝑐𝐹𝑇𝑅!") for each country.

3.2 Measures of Earnings Management

The accounting literature generally documents two types of earnings management strategies:

10

accrual-based earnings management and real activities manipulation. Following Kothari et al. (2005),

we proxy for accrual-based earnings management (𝐴𝑀!") by performance-matched discretionary

accruals. In the first step, we use the modified Jones (1991) model to obtain discretionary accruals,

which are computed as the difference between firms’ actual accruals and normal accruals, estimated

for each country-industry-year using Equation (1). We require at least 8 observations to run each

regression. We then subtract from the modified Jones model discretionary accruals of firm i [i.e., the

residuals from Equation (1)] those of another firm in the same country-industry-year with the closest

ROA, and the difference is the performance-matched discretionary accruals for firm i.

∆!""#$%&'!"!""#$"!"!!

= 𝛽! + 𝛽!!

!""#$"!"!!+ 𝛽!

∆!"#$%!" ! ∆!"#!"!""#$"!"!!

+ 𝛽!!!"!"

!""#$"!"!!+ 𝜀!" (1)

where ∆𝐴𝑐𝑐𝑟𝑢𝑎𝑙𝑠!" is the earnings before extraordinary items and discontinued operations minus

operating cash flows in year t (Zang 2012); 𝐴𝑠𝑠𝑒𝑡𝑠!"!! is the total assets beginning in year

t; ∆𝑆𝑎𝑙𝑒𝑠!" is the change in sales from year t-1 to year t; ∆𝑅𝑒𝑐!" is the change in net receivables

from year t-1 to year t; and 𝑃𝑃𝐸!" is the gross property, plant, and equipment in year t.

Following Roychowdhury (2006) and Cohen and Zarowin (2010), we use the abnormal level of

production cost ( 𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙𝑃𝑅𝑂𝐷!" ), the abnormal level of cash flow from operations

(𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙𝐶𝐹𝑂!"), and the abnormal level of discretionary expenses (𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙𝐷𝐼𝑆𝑋!") to capture

the extent of real activities manipulation. They are calculated as the differences between actual

values and the fitted values predicted by equations (2), (3) and (4). Like previously, the models are

11

estimated for each country-industry-year, and at least 8 observations are needed to run each

regression.

!"#$!"!""#$"!"!!

= 𝛽! + 𝛽!!

!!!"#!!"!!+ 𝛽!

!"#$%!"!""#$"!"!!

+ 𝛽!∆!"#$%!"!""#$"!"!!

+ 𝛽!∆!"#$%!"!!!""#$"!"!!

+ 𝜀!" (2)

!"#!"!""#$"!"!!

= 𝛽! + 𝛽!!

!""#$"!"!!+ 𝛽!

!"#$%!"!""#$"!"!!

+ 𝛽!∆!"#$%!"!""#$"!"!!

+ 𝜀!" (3)

!"#$!"!""#$"!"!!

= 𝛽! + 𝛽!!

!""#$"!"!!+ 𝛽!

!"#$%!"!!!""#$"!"!!

+ 𝜀!" (4)

where 𝑃𝑅𝑂𝐷!" is the production cost, defined as the sum of costs of goods sold in year t and

change in inventories from t-1 to t; 𝐶𝐹𝑂!" is the cash flow from operations appearing in the

statement of cash flows in year t; 𝐷𝐼𝑆𝑋!" is the discretionary expenses defined as the sum of R&D,

advertising, and selling, general, and administrative (SG&A) expenditures in year t; and 𝑆𝑎𝑙𝑒𝑠!" is

the sales in year t. Similar to Cohen and Zarowin (2010) and Zang (2012), we multiply

𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙𝐶𝐹𝑂!" and 𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙𝐷𝐼𝑆𝑋!" by -1 so that greater amounts indicate that firms are more

likely to increase reported earnings. We then combine the three individual measures into one

aggregate measure as the real earnings management proxy, 𝑅𝑀!", by taking their sum.

In addition to the accrual-based and real earnings management strategies, prior research shows that

firms manipulate earnings to report positive profits, and to meet analysts’ expectations (Degeorge et

al. 1999). Therefore, we also use loss avoidance (𝐿𝐴!") and small positive earnings surprises (𝑆𝑃𝐸𝑆!")

12

to proxy for corporate earnings management. We define 𝐿𝐴!" as a dummy variable that equals one

if a firm reports 0 to 0.01 earnings per share (𝐸𝑃𝑆!"), and zero otherwise. 𝑆𝑃𝐸𝑆!" is defined as a

dummy variable that equals one if a firm reports actual 𝐸𝑃𝑆!" 0 to 0.01 higher than consensus

earnings forecast, and zero otherwise1.

3.3 Model Specifications

3.3.1 Test of Hypothesis 1

To test Hypothesis 1 on the relationship between language FTR and earnings management, we

estimate the following multivariate models, where Equation (5) is estimated using OLS regression

and Equation (6) using Logit regression.

|𝐴𝑀!"|(𝑜𝑟 |𝑅𝑀!"|) = 𝛼! + 𝛼!𝐹𝑇𝑅!" + 𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠!" + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝐹𝐸 + 𝑌𝑒𝑎𝑟𝐹𝐸 + 𝜀! (5)

𝑃𝑟 𝐿𝐴!" [𝑜𝑟 𝑃𝑟 𝑆𝑃𝐸𝑆!" ] = 𝛽! + 𝛽!𝐹𝑇𝑅!" + 𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠!" + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝐹𝐸 + 𝑌𝑒𝑎𝑟𝐹𝐸 + 𝜀! (6)

where |𝐴𝑀!"| and |𝑅𝑀!"| are the absolute values of accrual-based (𝐴𝑀!") and real (𝑅𝑀!") earnings

management, respectively. 𝐹𝑇𝑅!" represents the four measures of language FTR (𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!",

𝑆𝑅!", 𝑉𝑅!", or 𝑝𝑐𝐹𝑇𝑅!"). 𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠!" is an array of firm- and country-level control variables that

are expected to be associated with earnings management. The first set of variables included in

𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠!" are country-level variables: Hofstede’s (2001) cultural dimensions including power

1 Consensus earnings forecast is the arithmetic average of I/B/E/S estimates for a company for the fiscal period indicated.

13

distance (𝑃𝐷!"), individualism (𝐼𝑁𝐷𝐼𝑉!"), masculinity (𝑀𝐴!"), uncertainty avoidance (𝑈𝐴!"), and

long-term orientation (𝐿𝑇𝑂!"), and indulgence (𝐼𝑁𝐷𝑈𝐿!"); investor protection score (𝐼𝑁𝑉𝑃𝑅𝑂!")

based on anti-director index from Djankov et al. (2008); annual GDP growth rate per country

(𝐺𝐺𝑅𝑂𝑊𝑇𝐻!"). One thing to mention on cultural values (e.g., Hofstede’s cultural dimensions) is

that prior literature has shown that language intertwines with culture and even shapes culture. Thus,

inclusion of these cultural variables may subsume the relationship between language FTR and

earnings management. But any documented significance of 𝐹𝑇𝑅!" would enhance the confidence in

the effect of language FTR on earnings management.

The second set of controls are firm-level variables: firm size (𝐿𝑁𝑆𝐼𝑍𝐸!"); book-to-market ratio

(𝐵𝑇𝑀!"); leverage ratio (𝐿𝐸𝑉!"); return on assets (𝑅𝑂𝐴!"); an indicator variable for equity issuance

(𝐼𝑆𝑆𝑈𝐸!"); an indicator variable for loss firms (𝐿𝑂𝑆𝑆!"); an indicator variable for meeting or beating

analyst earnings forecast (𝑀𝐸𝐸𝑇!"). 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝐹𝐸 and 𝑌𝑒𝑎𝑟𝐹𝐸 are indicator variables controlling

for industry (based on 3-digit SIC codes) and year fixed effects, with standard errors clustered at the

firm level. Based on Hypothesis 1, strong-FTR language is predicted to be associated with greater

earnings management and, thus, we expect both 𝛼! and 𝛽! to be positive.

3.3.2 Test of Hypothesis 2

To test Hypothesis 2 on the interaction between language FTR and investor protection, we extend

the previous regression models by adding a variable that interacts 𝐹𝑇𝑅!" with 𝐼𝑁𝑉𝑃𝑅𝑂!". The

models estimated are as follows:

14

𝐴𝑀!" 𝑜𝑟 𝑅𝑀!" = 𝛼! + 𝛼!𝐹𝑇𝑅!" + 𝛼!𝐹𝑇𝑅!" ∗ 𝐼𝑁𝑉𝑃𝑅𝑂!" + 𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠!" + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝐹𝐸 +

𝑌𝑒𝑎𝑟𝐹𝐸 + 𝜀! (7)

𝑃𝑟 𝐿𝐴!" 𝑜𝑟 𝑃𝑟 𝑆𝑃𝐸𝑆!" =

𝛽! + 𝛽!𝐹𝑇𝑅!" + 𝛽!𝐹𝑇𝑅!" ∗ 𝐼𝑁𝑉𝑃𝑅𝑂!" + 𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠!" + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝐹𝐸 + 𝑌𝑒𝑎𝑟𝐹𝐸 + 𝜀!

(8)

Based on Hypothesis 2, the signs of 𝛼! or 𝛽! are indeterminable.

3.4 Sample Selection

We test our hypothesis using a global panel data set of publicly listed companies during the period

1994-2013. Financial companies (SIC codes 6000-6999) and firms that lack relevant accounting

information data to construct variables are excluded from the sample. Our primary data source for

firms’ financial performance is Compustat North America and Compustat Global. All continuous

financial variables are winsorized at the 1% and 99% of the distributions to reduce the influence of

outliers. Data related with analyst forecast are obtained from I/B/E/S. We then identify official

language FTR available from Chen (2013) to match the country-level FTR measures with firm-level

financial variables. Other country-level legal and cultural indices are hand-collected from the

relevant previous papers and relevant website, as discussed in Section 3. Detailed description of all

variables is provided in the Appendix. Following the above procedures, we finally obtain 74606

15

firm-year observations (with 15248 distinct firms) in 37 countries.

4. Results

4.1 Descriptive Statistics

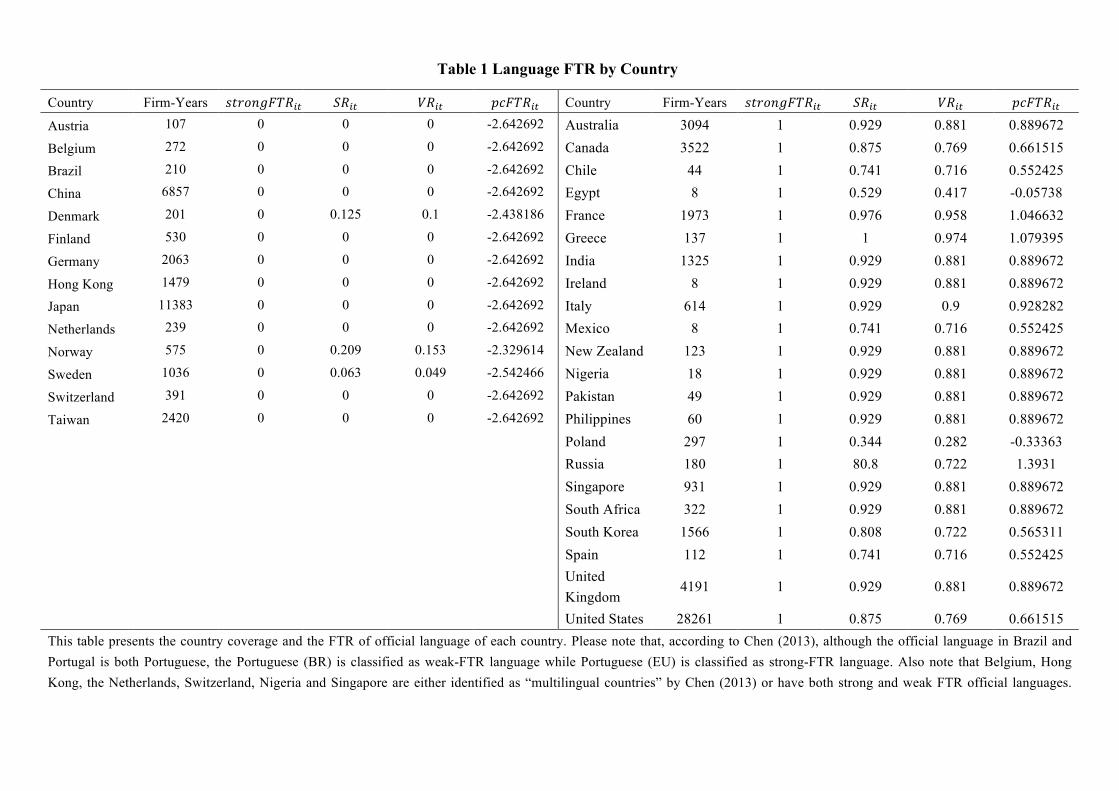

Table 1 reports the country coverage and the FTR measures of the official languages for each

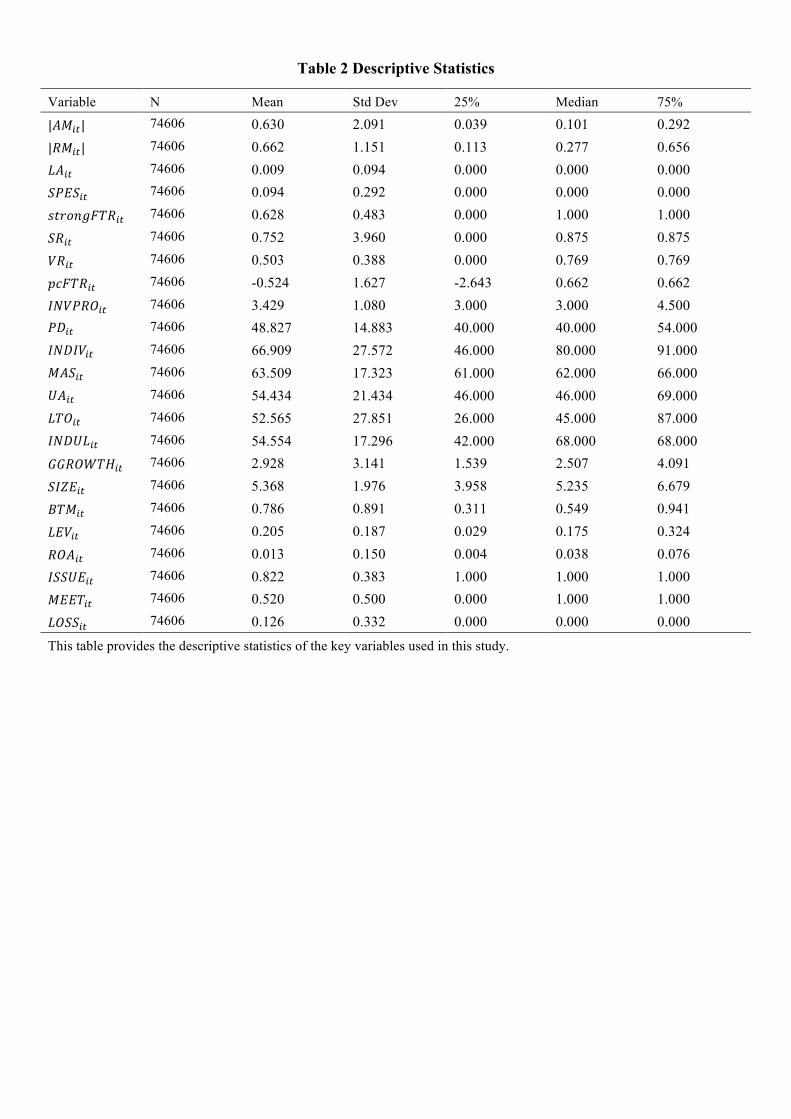

country. Among the 37 countries, U.S. constitutes the largest number of observations. Table 2

provides the descriptive statistics on our main regression variables. The mean (median) values for

|𝐴𝑀!"| and |𝑅𝑀!"| are 0.630 (0.101) and 0.662 (0.277), while the mean (median) for 𝐿𝐴!" and

𝑆𝑃𝐸𝑆!" are 0.009 (0) and 0.094 (0), respectively. 𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" is right skewed with mean (median)

of 0.628 (1), consistent with Table 1 that there are more firm-year observations for strong-FTR

language countries than for weak-FTR language countries.

[Insert Table 1 and 2 Here]

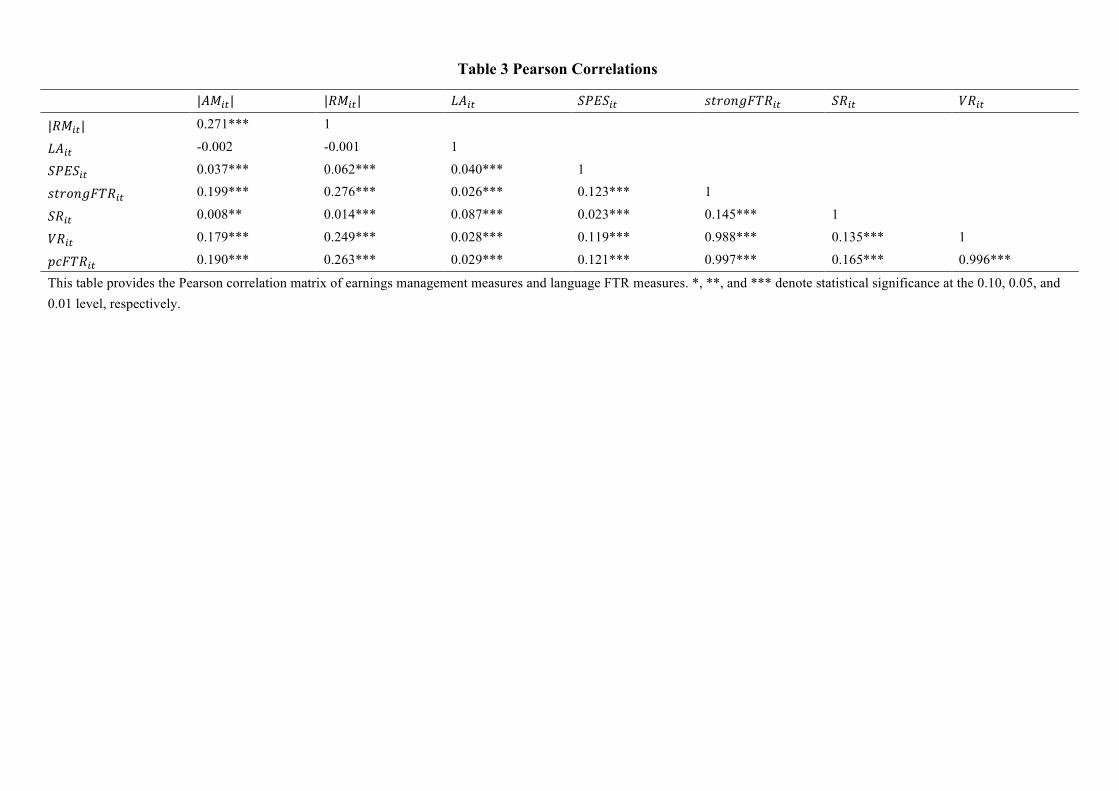

Table 3 presents the pairwise correlations between the four language FTR measures and various

measures of earnings management. Generally, there is a significant and positive association between

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" , 𝑆𝑅!" , 𝑉𝑅!" , or 𝑝𝑐𝐹𝑇𝑅!" and |𝐴𝑀!"|, |𝑅𝑀!"|, 𝐿𝐴!" or 𝑆𝑃𝐸𝑆!" . In other words,

firms in strong-FTR countries have a higher level of both accrual-based and real earnings

management on average, and display a greater propensity to avoid losses and negative earnings

surprises. All correlations are statistically significant at 0.01 or 0.05 level.

[Insert Table 3 Here]

16

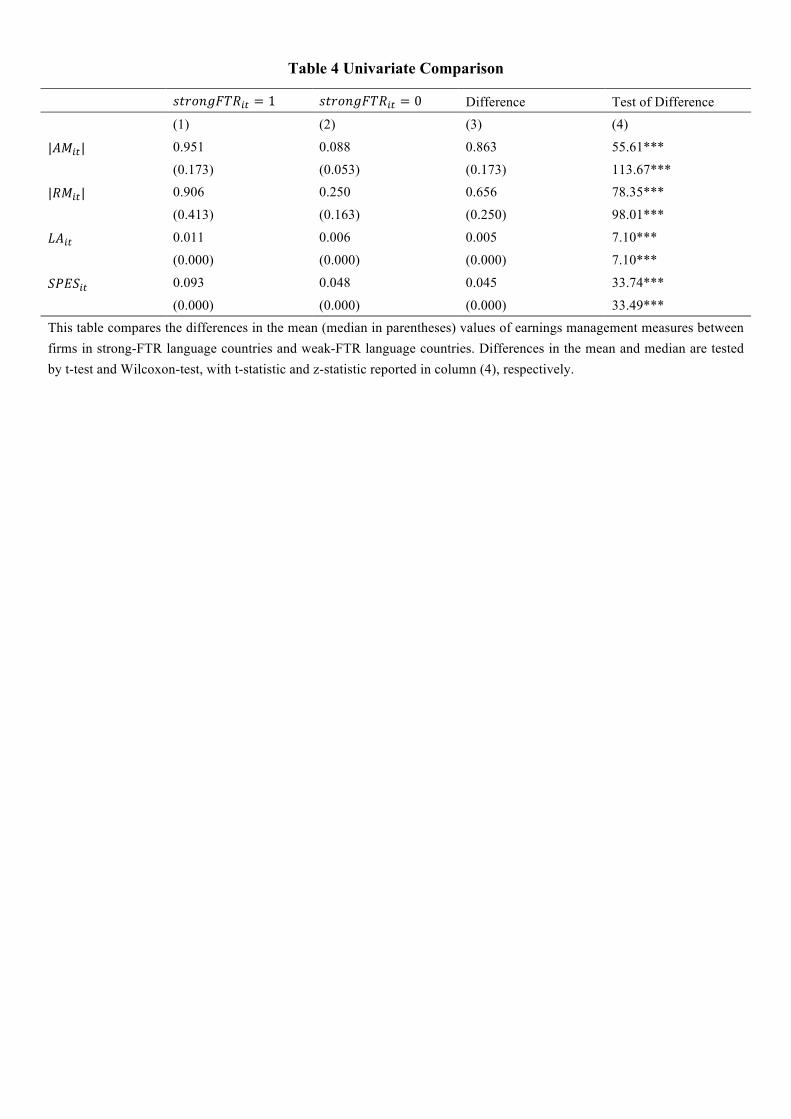

4.2 Univariate Comparison

Table 4 compares the mean (median) values of each earnings management measure between firms in

strong-FTR language countries (𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" = 1) and those in weak-FTR language countries

(𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" = 0). The magnitudes of all earnings management measures are greater for firms

headquartered in strong-FTR countries, and the differences between the two types of earnings

management are consistently significant, indicating that strong-FTR firms are more likely to engage

in earnings manipulation. But, given the above comparison is univariate, we shall turn to

multivariate regressions

[Insert Table 4 Here]

4.3 Multivariate Regressions

4.3.1 Test of Hypothesis 1

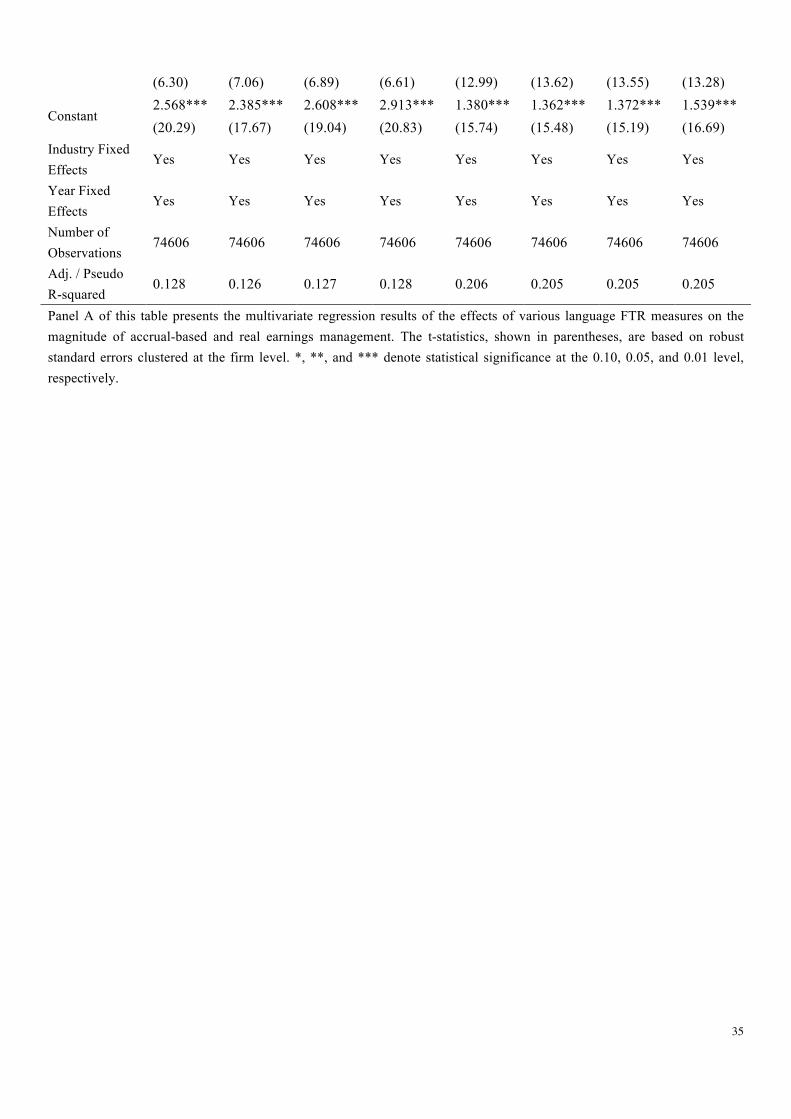

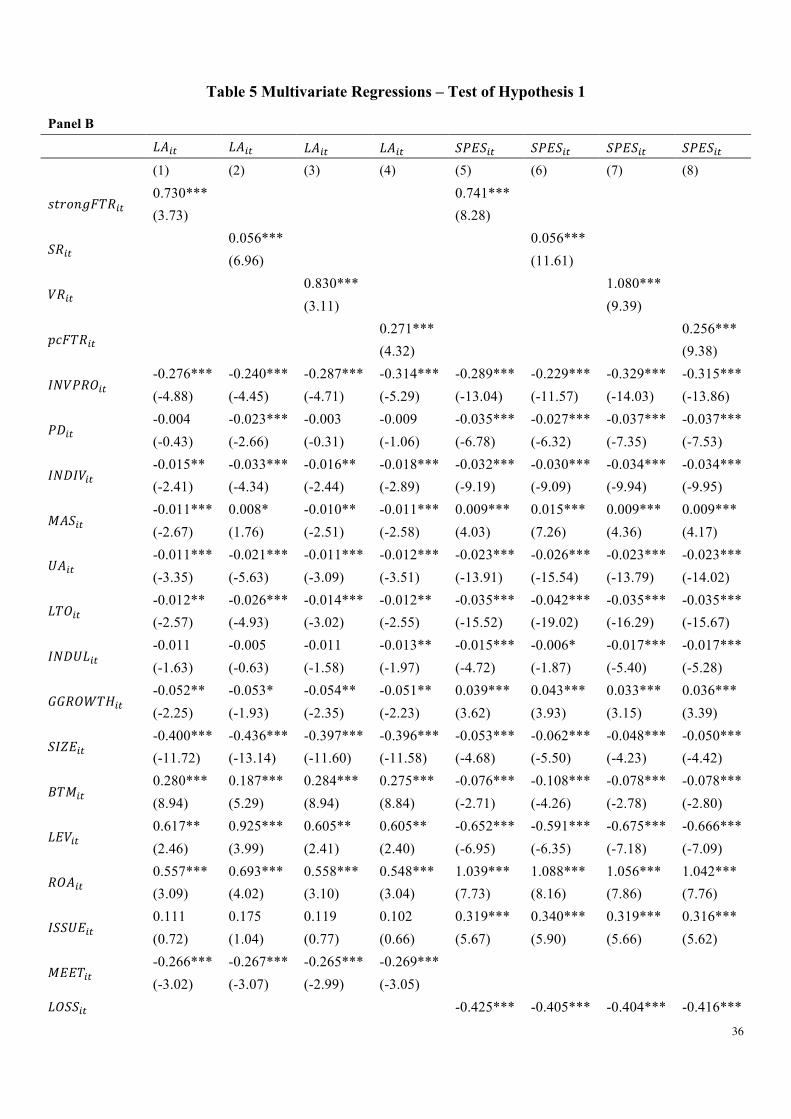

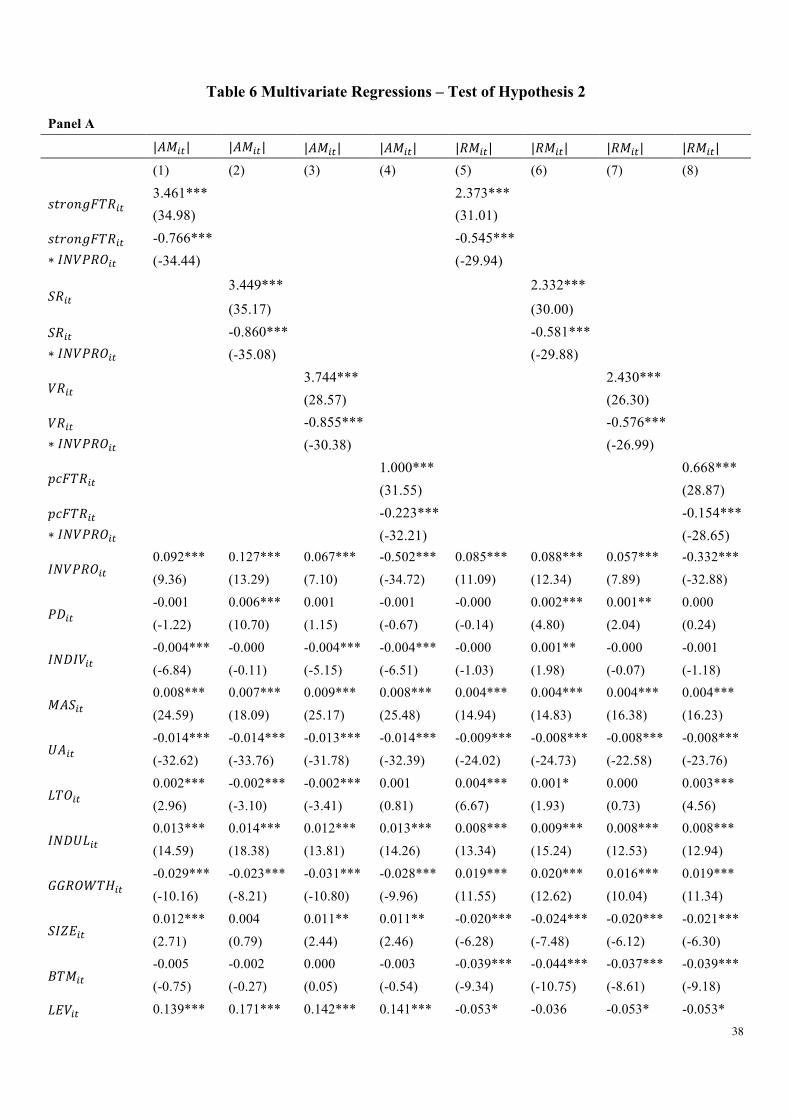

Table 5 reports the regression results for the hypothesis on the relationship between language FTR

and the absolute magnitudes of accrual-based and real earnings management as well as the

likelihood of reporting small positive income and earnings surprises. All columns include industry

and year fixed effects to control for the heterogeneity in earnings management of firms in different

industries and different years. And Panel A shows that 𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!", 𝑆𝑅!", 𝑉𝑅!", and 𝑝𝑐𝐹𝑇𝑅!"

are significantly positively associated with |𝐴𝑀!"| and 𝑅𝑀!" all at the 0.01 level. These results

indicate that firms headquartered in a strong-FTR country, on average, report 0.424 more

accrual-based and 0.210 more real earnings management than their counterparts in a weak-FTR

country. This effect is economically sizable, given that the mean values of absolute discretionary

17

accruals and real activities manipulation are 0.630 and 0.662. Inspection of Panel B suggests that the

odds of firms avoiding reporting losses, and of meeting analysts’ earnings forecasts in a strong-FTR

language country are 2.075 (𝑒!.!"#) and 2.098 (𝑒!.!"#) times the odds of firms in a weak-FTR

language country2. These results are consistent with strong-FTR language inducing managers to

behave myopically to meet short-term benchmarks. Note that all the significance is after controlling

for cultural traits. Thus, it seems that language FTR is a fundamental source of managerial myopia

and, hence, corporate earnings management, and its influence is above and beyond conventionally

recognized cultural proxies. Indeed, Liang et al. (2014) argue that language is a key determinant

because it acts as a “specific underlying mechanism that carries culture”.

[Insert Table 5 Here]

Turning our attention to control variables, we find that 𝐼𝑁𝑉𝑃𝑅𝑂!" is significantly negatively

associated with |𝐴𝑀!"| , |𝑅𝑀!"| , 𝐿𝐴!" and 𝑆𝑃𝐸𝑆!" (at the 0.01 level), indicating that the

effectiveness of legal protection can reduce firms’ earnings management. 𝐼𝑁𝐷𝐼𝑉!" and 𝐿𝑇𝑂!" are

also generally negatively associated with these earnings management measures consistent with prior

research that managers in cultures with low levels of individualism are less likely to manipulate

earnings since they intend to protect the collective welfare of corporate stakeholders, and that

long-term oriented societies are less inclined to manipulate earnings due to its long-run perspective

(Doupnik 2008). On the contrary, 𝑀𝐴𝑆!" is generally positively associated with earnings

management, supporting the view that managers are more motivated to manage earnings to achieve

2 These results are robust to all the additional analyses discussed in Section 5.

18

financial goals in masculine societies.

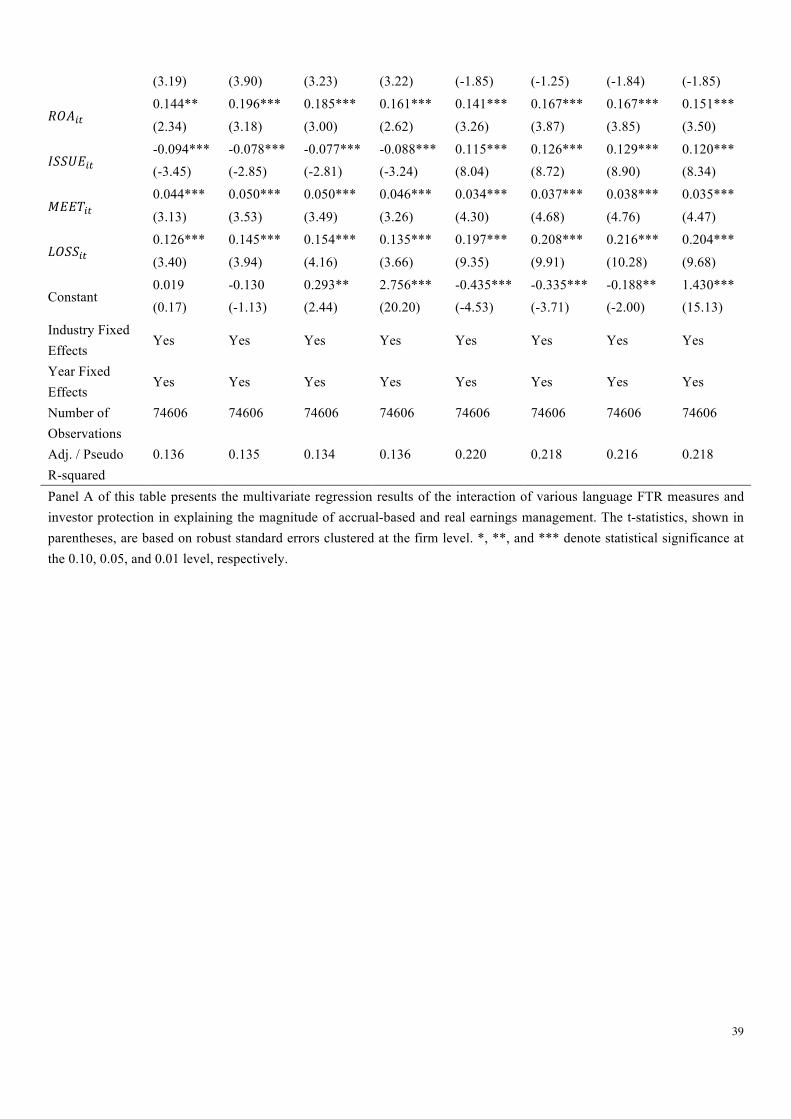

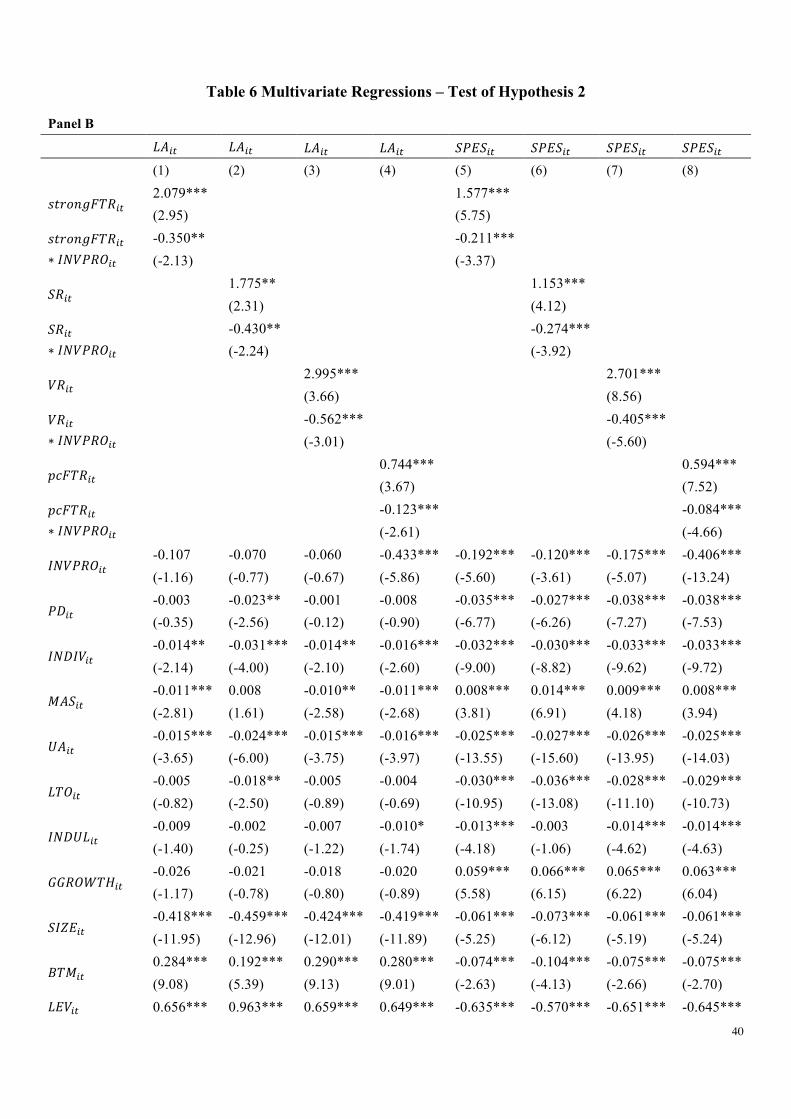

4.3.2 Test of Hypothesis 2

Hypothesis 2 suggests that investor protection may influence the effects of language FTR on firms’

earnings manipulation pattern. The multivariate regression results of test of the second hypothesis

are provided in Table 6. Specifically, the estimated coefficients on the four interaction terms are

generally negatively significantly related with the four earnings management measures, suggesting

that the formal institution of investor protection acts as a governance mechanism in mitigating

earnings manipulation.

[Insert Table 6 Here]

Overall, our findings generally support the correlation between language FTR and earnings

management as predicted. This is consistent with the hypotheses that strong language FTR affects

managerial decision making process, and formal legal institution such as investor protection may

have an impact on such a process.

5. Additional Analyses

5.1 Additional Controls

Prior literature shows that religiosity is negatively associated with incidences of financial reporting

irregularities (McGuire et al. 2012). To the extent that religiosity is an integrated measure of cultural

19

values, one may be worried that our results are driven by differences in religiosities across countries.

To mitigate this concern, we include the variable 𝑅𝐸𝐿𝐼𝐺𝐶!", which measures the percentage of

Christianity (Protestant plus Catholic) religious beliefs in the country. Besides, recent emerging

evidence suggests that social trust increases investors’ demand for corporate information and

induces firms’ information production, thereby increasing financial reporting transparency (Nanda

and Wysocki 2013). We measure the level of social trust (𝑇𝑅𝑈𝑆𝑇!") in a country based on the

response of the World Values Survey to the question “Generally speaking, would you say that most

people can be trusted or that you can't be too careful in dealing with people?” In addition, we further

include an alternative measure of investor protection, i.e., the public enforcement index (𝑃𝐸𝑁𝐹!")

documented by Djankov et al. (2008). Untabulated results show that, after adding these additional

variables, all our main regression results hold.

These results are particularly important because they exclude the possibility that language FTR is

not causing earnings management but it is rather simply reflecting legal, regulatory or cultural

differences. Chen (2013) shows, both theoretically and empirically, that language and culture are

two different constructs. Our analysis extends this notion to companies, showing that the effect of

language FTR is not subsumed by any additional legal, regulatory and cultural institutions.

5.2 Dropping observations

Given that U.S. constitutes the largest number of observations (both in the general sample and in the

strong-FTR subsample), we repeat the tests after dropping the U.S. firms to assess the sensitivity of

the results to the U.S. exclusion. All earnings management measures continue to have a similar

20

association with language FTR as in the reported main results, except that 𝑝𝑐𝐹𝑇𝑅!" is now

insignificant for |𝑅𝑀!"|. Hence, other than this single real activities manipulation measure, the

inferences on the impact of language FTR on earnings management are not heavily affected by U.S.

firms. We also rerun the analysis by removing Japanese and Chinese firms, as they represent 55% of

the weak-FTR language subsample. The main results relative to both Hypothesis 1 and 2 hold, and

this allows us ruling out the possibility that results are driven by omitted country-level effects.

In addition, some countries have both strong and weak FTR populations. Belgium, Switzerland,

Hong Kong, Singapore, Nigeria and the Netherlands are either identified as “multilingual countries”

by Chen (2013) or have both strong FTR and weak FTR official languages. In order to get a cleaner

setting to test our hypotheses, we drop these six countries to check where our main findings still

hold. In untabulated results, the coefficients of language FTR are comparable to those reported using

the full dataset for Hypothesis 1, but not for Hypothesis 2.

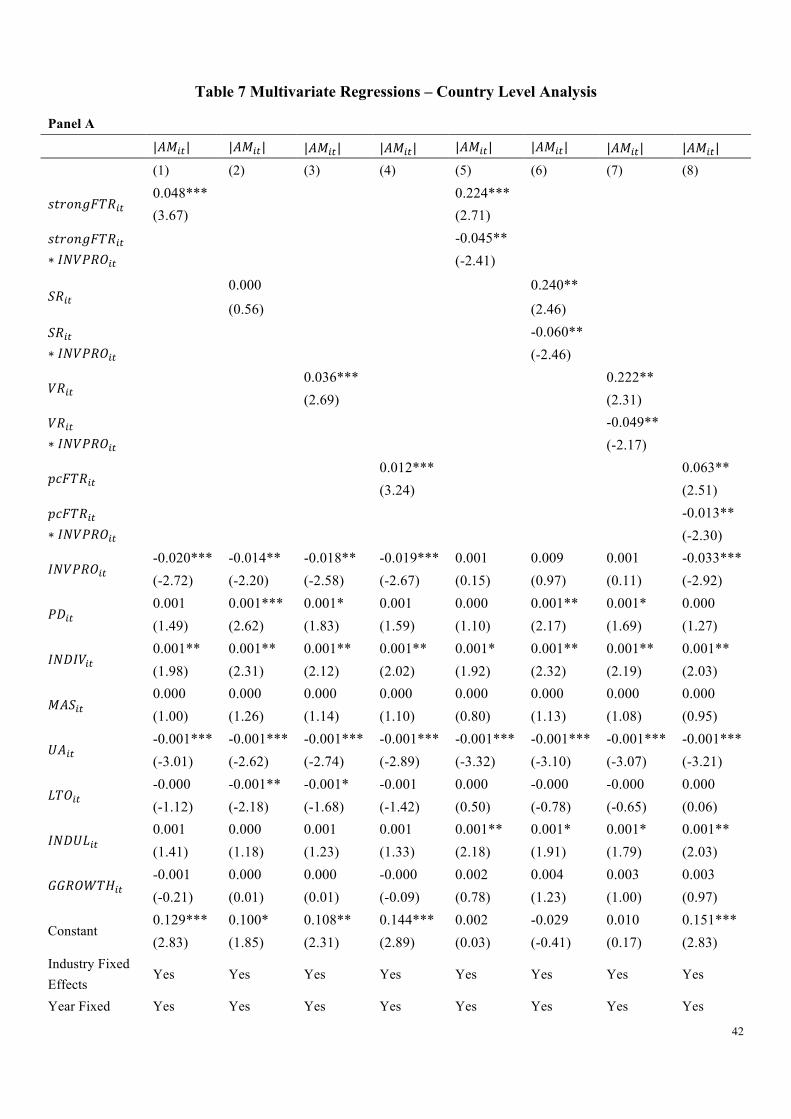

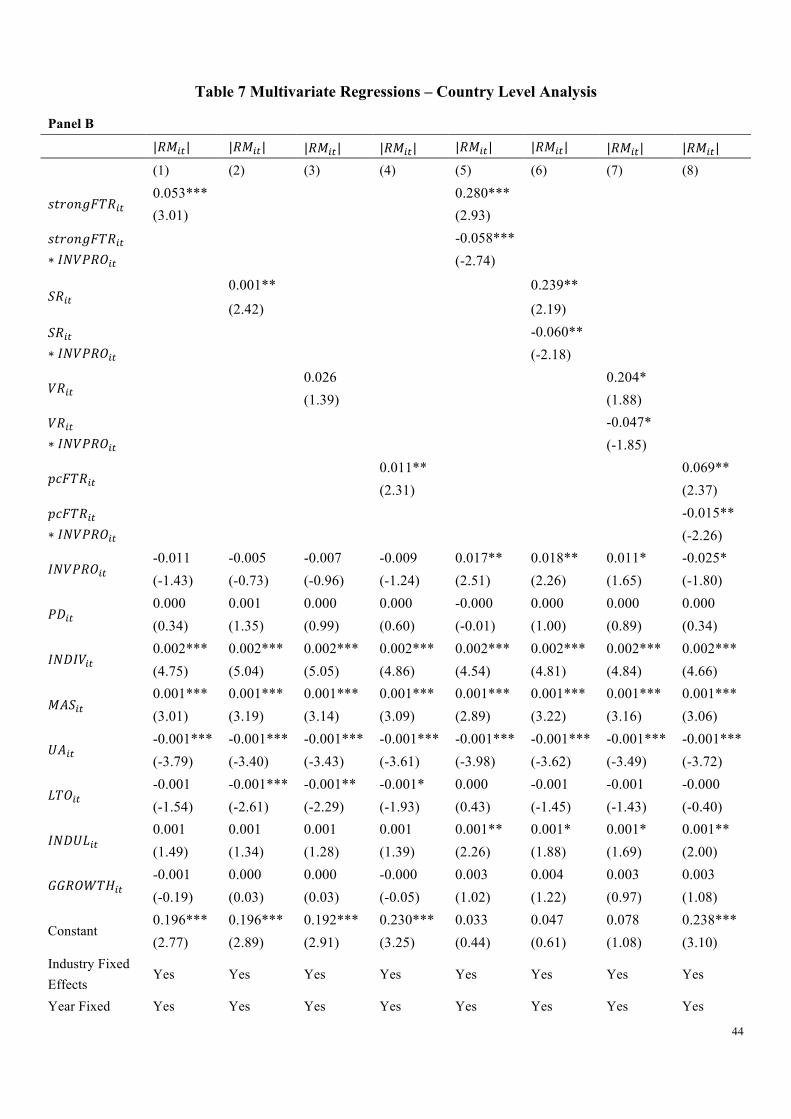

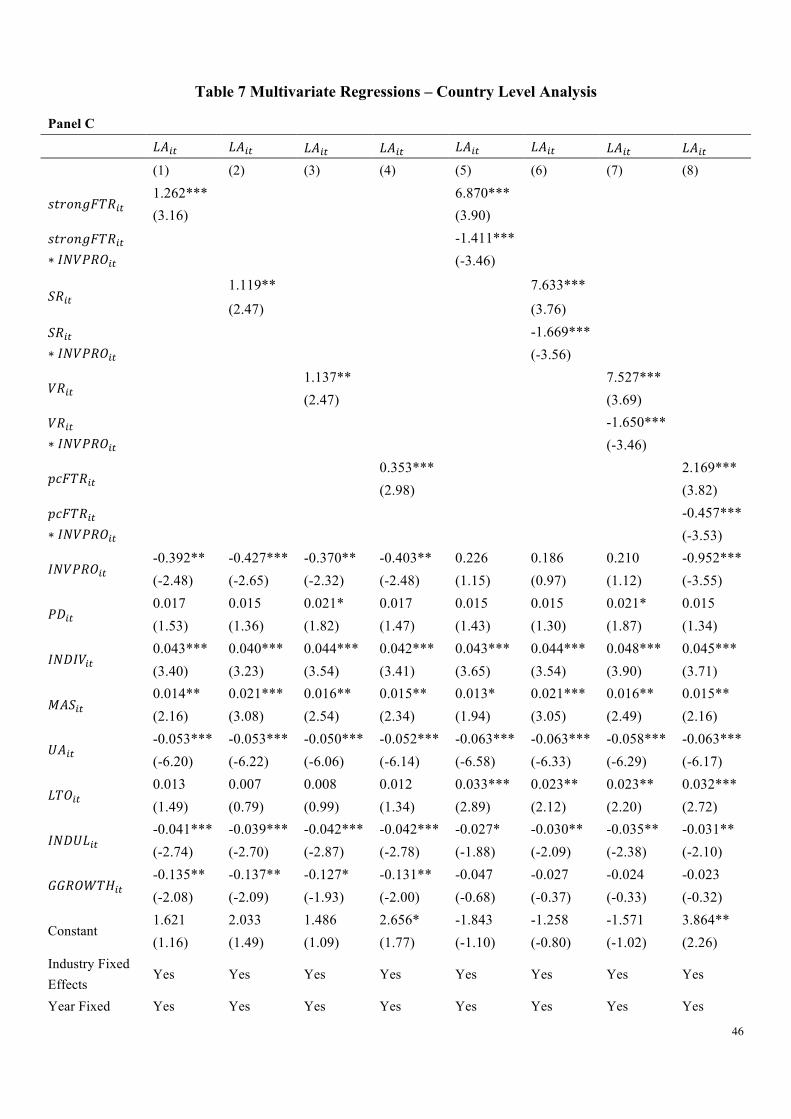

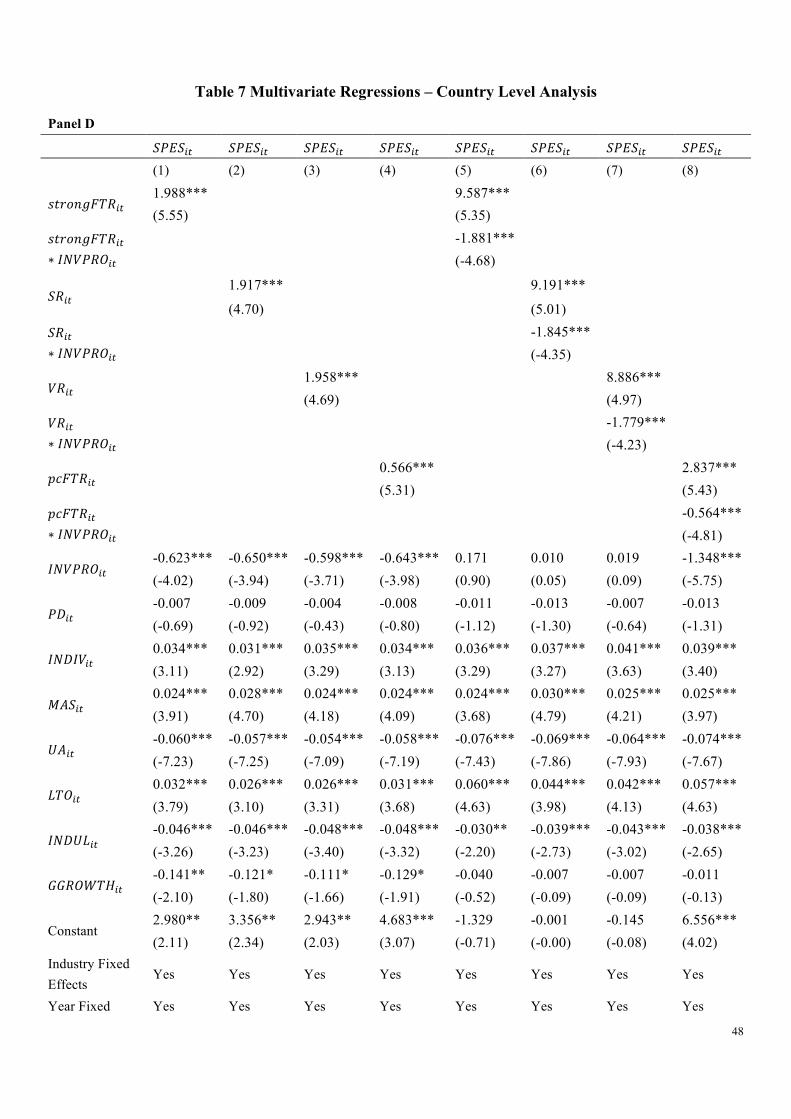

5.3 Country-Level Analysis

To mitigate the concern that the dependent earnings management variables are measured at the firm

level while the independent language FTR variables do not vary across firms in a country, we

perform a country-level analysis where |𝐴𝑀!"| and |𝑅𝑀!"| are calculated at their medians for each

country-year, and 𝐿𝐴!" and 𝑆𝑃𝐸𝑆!" are dummy variables that take one if a country has the above

median number of loss avoidance firms and small positive earnings surprises firms in a given year

and zero otherwise. We then regress them on different measures of 𝐹𝑇𝑅!", the interaction terms of

21

𝐹𝑇𝑅!" ∗ 𝐼𝑁𝑉𝑃𝑅𝑂!", and country-level legal, cultural and economic institutions, while controlling for

year fixed effects. This approach alleviates the concern of the regression results being influence by

uneven number of observations across countries, while controlling for any time-series variation in

the earnings management proxies driven by the other firm- and country-level factors. The evidence

for the new country-year observation sample is consistent with (though weaker than) the firm-year

observation sample, as almost all 𝐹𝑇𝑅!" measures and the interaction terms of 𝐹𝑇𝑅!" ∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

load significantly for most of the equations and all with the predicted signs.

[Insert Table 7 Here]

In general, results in this section support the hypothesis on the important role that the official

language FTR plays in shaping corporate earnings management. It turns out that language FTR is a

statistically and economically significant determinant of earnings management, beyond the

conventionally recognized cultural proxies. The results are robust to additional country-level

controls, different sample compositions, and a country-level regression.

6. Conclusion

In this paper, we investigate the effect of variation in an important linguistic feature, i.e., the future

time reference of a language, on international differences in earnings management. We identify

grammatical FTR as an key determinant of managerial myopia. Repeatedly encoding the future time

period induces strong-FTR language speakers to unconsciously separate the future from the present,

and induces more short-term oriented behaviors. Controlling for firm-, industry- and country-level

22

determinants of earnings management, we document a significantly positive association between

strong language FTR and the tendency (and intensity) to engage in real and accrual-based earnings

manipulation to meet short-term earnings benchmarks. Furthermore, this association decreases with

the strength of investor protection. These results are also robust to using multiple proxies for

earnings management, additional controls and different potential research design issues. Overall, our

results highlight the important role of a salient language feature in shaping corporate decision

making.

23

References

Brochet, F., Loumioti, M., Serafeim, G., 2014. Short-termism, investor clientele, and corporate

performance. Working Paper, Harvard University.

Bushee, B., 1998. The influence of institutional investors in myopic R&D investment behavior. The

Accounting Review 73(3), 305-334.

Chen, M. K., 2013. The effect of language on economic behavior: Evidence from savings rates,

health behaviors, and retirement assets. American Economic Review 103 (2), 690–731.

Chen, S., Cronqvist, H., Ni, S., Zhang, F., 2015. Languages and corporate cash holdings:

International Evidence. Working paper, China Europe International Business School.

Chomsky, N., 1957. Syntactic Structures. Paris: Mouton and Co.

Cohen, D., Zarowin, P., 2010. Accrual-based and real earnings management activities around

seasoned equity offerings. Journal of Accounting and Economics 50 (1), 2–19.

Dahl, O., 1985. Tense and Aspect Systems. Blackwell Publishers, Oxford, U.K.

Dahl, O., 2000. The grammar of future time reference in European languages. Tense and Aspect in

the Languages of Europe (6), 309–328.

DeFond, M., Hung, M., Trezevant, R., 2007. Investor protection and the information content of

annual earnings announcements: International evidence. Journal of Accounting and Economics 43

(1), 37-67.

24

Dechow, P. M., Sloan, R. G., Sweeny., A. P., 1995. Detecting earnings management. The

Accounting Review 70 (2), 193–225.

Degeorge, F., Patel, J., Zeckhauser, R., 1999. Earnings management to exceed thresholds. Journal of

Business 72 (1), 1–33.

Doupnik, T. S., 2008. Influence of culture on earnings management: A note. Abacus 44 (3), 317–

340.

Djankov, S., La Porta, R., Lopez-de-Silanes, F., Shleifer, A., 2008. The law and economics of

self-dealing. Journal of Financial Economics 88 (3), 430–465.

Evans, N., Levinson, S. C., 2009. The myth of language universals: Language diversity and its

importance for cognitive science. Behavioral and Brain Sciences 32 (5), 429–448.

Han, S., Kang, T., Salter, S., Yoo, Y. K., 2010. A cross-country study on the effects of national

culture on earnings management. Journal of International Business Studies 41 (1), 123–141.

Healy, P. M., Wahlen, J. M., 1999. A review of the earnings management literature and its

implications for standard setting. Accounting Horizons 13 (4), 365-383.

Hofstede, G. 2001 Culture’s Consequences, Comparing Values, Behaviors, Institutions, and

Organizations Across Nations. Sage, Thousand Oaks, CA.

Jones, J.J., 1991. Earnings management during import relief investigations. Journal of Accounting

Research 29 (2), 193–228

Kothari, S., Leone, A., Wasley, C., 2005. Performance matched discretionary accrual measures.

25

Journal of Accounting and Economics 39 (1), 163–197.

Leuz, C., Nanda, D., Wysocki, P. D., 2003. Earnings management and investor protection: An

international comparison. Journal of Financial Economics 69 (3), 505–527.

Liang, H., Marquis, C., Renneboog, L., Sun, S. L., 2014. Speaking of corporate social responsibility.

Working Paper, Harvard Business School.

McGuire, S. T., Omer, T. C., Sharp, N. Y., 2012. The impact of religion on financial reporting

irregularities. The Accounting Review 87 (2), 645–673.

Nanda, D., Wysocki, P., 2013. Trust, external capital and financial transparency. Working Paper,

University of Miami.

Pinker, S., 1994. The Language Instinct: How the Mind Creates Language. New York: William

Morrow and Company.

Roychowdhury, S., 2006. Earnings management through real activities manipulation. Journal of

Accounting and Economics 42 (3), 335–370.

Sapir, E., 1951. The Status of Linguistics as a Science. In Selected Writings. David Mandelbaum, ed.

Berkeley: University of California Press. Orig. pub. in Language 5, 207–214.

Slobin, D. I., 1987. Thinking for speaking. In: Proceedings of the Berkeley Linguistics Society. 3,

435–445.

Stein, J. C., 1989. Efficient capital markets, inefficient firms: A model of myopic corporate behavior.

Quarterly Journal of Economics 104 (4), 655–669.

26

Stulz, R., Williamson, R., 2003. Culture, openness, and finance. Journal of Financial Economics 70

(3), 261–300.

Thieroff, R., 2000. On the areal distribution of tense-aspect categories in Europe. Empirical

Approaches to Language Typology (6), 265–308.

Whorf, B. L., Carroll, J. B., Chase, S., 1956. Language, Thought and Reality: Selected Writings of

Benjamin Lee Whorf. MIT Press, Cambridge.

Wittgenstein, L. 1922. Tractatus Logico-Philosophicus. London: Routledge.

Zang, A., 2012. Evidence on the trade-off between real activities manipulation and accrual-based

earnings management. The Accounting Review 87 (2), 675–670.

27

Appendix: Variable Definition

Dependent Variables:

|𝐴𝑀!"|

Absolute value of accrual-based earnings management, i.e., the absolute value of the difference between the residuals estimated from Equation (1) for firm i and for its performance-matched firm (with the closest ROA and in the same country-industry-year), based on Kothari et al. (2005)

|𝑅𝑀!"| Absolute value of real earnings management, i.e., absolute value of the sum of the residuals estimated from Equation (2), negative residuals estimated from Equation (3) and negative residuals estimated from Equation (4)

𝐿𝐴!" A dummy variable that takes 1 for firm-year observations with annual EPS between 0 and 0.005, and 0 otherwise

𝑆𝑃𝐸𝑆!" A dummy variable that takes 1 for firm-year observations with the difference between actual annual EPS and consensus earnings forecast between 0 and 0.005, and 0 otherwise

Main Variables of Interest:

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" A dummy variable that takes 1 for firm-year observations from countries where the official languages are classified as having strong FTR by Chen (2013), and 0 otherwise

𝑆𝑅!" Sentence ratio calculated as the proportion of sentences containing a grammatical future-marker when referring to the future, as in Chen (2013)

𝑉𝑅!" Verb ratio calculated as the ratio of the number of grammatically future-marked verbs to the total number of future-referring verb, as in Chen (2013)

𝑝𝑐𝐹𝑇𝑅!" Aggregate measure of language FTR developed using the principal component analysis (PCA) based on 𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!", 𝑆𝑅!", and 𝑉𝑅!".

Country-level Controls:

𝐼𝑁𝑉𝑃𝑅𝑂!" Investor protection score based on anti-director index from Djankov et al. (2008)

𝑃𝐷!" Power distance index score based on Hofstede (2001) (data source: http://geert-hofstede.com/countries.html)

𝐼𝑁𝐷𝐼𝑉!" Individualism/collectivism index score based on Hofstede (2001) (data source: http://geert-hofstede.com/countries.html)

28

𝑀𝐴𝑆!" Masculinity/femininity index score based on Hofstede (2001) (data source: http://geert-hofstede.com/countries.html)

𝑈𝐴!" Uncertainty avoidance index score based on Hofstede (2001) (data source: http://geert-hofstede.com/countries.html)

𝐿𝑇𝑂!" Long-/short-term orientation index score based on Hofstede (2001) (data source: http://geert-hofstede.com/countries.html)

𝐺𝐺𝑅𝑂𝑊𝑇𝐻!" Country GDP growth rate (data source: http://data.worldbank.org/indicator)

𝑅𝐸𝐿𝐼𝐺𝐶!"

Christianity religious index score calculated as the ratio of [% Protestant + % (Roman) Catholic] based on the responses from the World Values Survey to the question “Do you belong to a religion or religious denomination? If yes, which one?”

𝑇𝑅𝑈𝑆𝑇!"

Social trust index score calculated as the ratio of (% Most people can be trusted) / (% Most people can be trusted + % Need to be careful) based on the responses from the World Values Survey to the question “Generally speaking, would you say that most people can be trusted or that you need to be very careful in dealing with people?”

𝑃𝐸𝑁𝐹!" Public enforcement index score from Djankov et al. (2008)

Firm-level Controls:

𝑆𝐼𝑍𝐸!" Natural log of total assets adjusted for inflation rate

𝐵𝑇𝑀!" Book value of common equity divided by market value of equity

𝐿𝐸𝑉!" Short- and long-term debt divided by total assets

𝑅𝑂𝐴!" Income before extraordinary items divided by total assets

𝐼𝑆𝑆𝑈𝐸!" Dummy variable that takes one for firm-year observations with equity issuance, zero otherwise

𝐿𝑂𝑆𝑆!" Dummy variable that takes one for firm-year observations with negative income before extraordinary items, zero other wise

𝑀𝐸𝐸𝑇!" Dummy variable that takes one for firm-year observations with actual annual EPS greater than or equal to consensus analyst earnings forecast, zero otherwise

Table 1 Language FTR by Country

Country Firm-Years 𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 𝑆𝑅!" 𝑉𝑅!" 𝑝𝑐𝐹𝑇𝑅!" Country Firm-Years 𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 𝑆𝑅!" 𝑉𝑅!" 𝑝𝑐𝐹𝑇𝑅!"

Austria 107 0 0 0 -2.642692 Australia 3094 1 0.929 0.881 0.889672

Belgium 272 0 0 0 -2.642692 Canada 3522 1 0.875 0.769 0.661515

Brazil 210 0 0 0 -2.642692 Chile 44 1 0.741 0.716 0.552425

China 6857 0 0 0 -2.642692 Egypt 8 1 0.529 0.417 -0.05738

Denmark 201 0 0.125 0.1 -2.438186 France 1973 1 0.976 0.958 1.046632

Finland 530 0 0 0 -2.642692 Greece 137 1 1 0.974 1.079395

Germany 2063 0 0 0 -2.642692 India 1325 1 0.929 0.881 0.889672

Hong Kong 1479 0 0 0 -2.642692 Ireland 8 1 0.929 0.881 0.889672

Japan 11383 0 0 0 -2.642692 Italy 614 1 0.929 0.9 0.928282

Netherlands 239 0 0 0 -2.642692 Mexico 8 1 0.741 0.716 0.552425

Norway 575 0 0.209 0.153 -2.329614 New Zealand 123 1 0.929 0.881 0.889672

Sweden 1036 0 0.063 0.049 -2.542466 Nigeria 18 1 0.929 0.881 0.889672

Switzerland 391 0 0 0 -2.642692 Pakistan 49 1 0.929 0.881 0.889672

Taiwan 2420 0 0 0 -2.642692 Philippines 60 1 0.929 0.881 0.889672

Poland 297 1 0.344 0.282 -0.33363

Russia 180 1 80.8 0.722 1.3931

Singapore 931 1 0.929 0.881 0.889672

South Africa 322 1 0.929 0.881 0.889672

South Korea 1566 1 0.808 0.722 0.565311

Spain 112 1 0.741 0.716 0.552425

United

Kingdom 4191 1 0.929 0.881 0.889672

United States 28261 1 0.875 0.769 0.661515 This table presents the country coverage and the FTR of official language of each country. Please note that, according to Chen (2013), although the official language in Brazil and Portugal is both Portuguese, the Portuguese (BR) is classified as weak-FTR language while Portuguese (EU) is classified as strong-FTR language. Also note that Belgium, Hong Kong, the Netherlands, Switzerland, Nigeria and Singapore are either identified as “multilingual countries” by Chen (2013) or have both strong and weak FTR official languages.

30

Based on Stulz and Williamson (2003) and Chen et al. (2015), we categorize Belgium, Hong Kong, the Netherlands and Switzerland’s FTR as weak, and Nigeria and Singapore’s FTR as strong. In an additional analysis, we drop these countries to test whether the results hold under a cleaner setting.

Table 2 Descriptive Statistics

Variable N Mean Std Dev 25% Median 75%

|𝐴𝑀!"| 74606 0.630 2.091 0.039 0.101 0.292

|𝑅𝑀!"| 74606 0.662 1.151 0.113 0.277 0.656

𝐿𝐴!" 74606 0.009 0.094 0.000 0.000 0.000

𝑆𝑃𝐸𝑆!" 74606 0.094 0.292 0.000 0.000 0.000

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 74606 0.628 0.483 0.000 1.000 1.000

𝑆𝑅!" 74606 0.752 3.960 0.000 0.875 0.875

𝑉𝑅!" 74606 0.503 0.388 0.000 0.769 0.769

𝑝𝑐𝐹𝑇𝑅!" 74606 -0.524 1.627 -2.643 0.662 0.662

𝐼𝑁𝑉𝑃𝑅𝑂!" 74606 3.429 1.080 3.000 3.000 4.500 𝑃𝐷!" 74606 48.827 14.883 40.000 40.000 54.000 𝐼𝑁𝐷𝐼𝑉!" 74606 66.909 27.572 46.000 80.000 91.000 𝑀𝐴𝑆!" 74606 63.509 17.323 61.000 62.000 66.000 𝑈𝐴!" 74606 54.434 21.434 46.000 46.000 69.000 𝐿𝑇𝑂!" 74606 52.565 27.851 26.000 45.000 87.000 𝐼𝑁𝐷𝑈𝐿!" 74606 54.554 17.296 42.000 68.000 68.000

𝐺𝐺𝑅𝑂𝑊𝑇𝐻!" 74606 2.928 3.141 1.539 2.507 4.091

𝑆𝐼𝑍𝐸!" 74606 5.368 1.976 3.958 5.235 6.679

𝐵𝑇𝑀!" 74606 0.786 0.891 0.311 0.549 0.941

𝐿𝐸𝑉!" 74606 0.205 0.187 0.029 0.175 0.324

𝑅𝑂𝐴!" 74606 0.013 0.150 0.004 0.038 0.076

𝐼𝑆𝑆𝑈𝐸!" 74606 0.822 0.383 1.000 1.000 1.000

𝑀𝐸𝐸𝑇!" 74606 0.520 0.500 0.000 1.000 1.000

𝐿𝑂𝑆𝑆!" 74606 0.126 0.332 0.000 0.000 0.000

This table provides the descriptive statistics of the key variables used in this study.

Table 3 Pearson Correlations

|𝐴𝑀!"| |𝑅𝑀!"| 𝐿𝐴!" 𝑆𝑃𝐸𝑆!" 𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 𝑆𝑅!" 𝑉𝑅!"

|𝑅𝑀!"| 0.271*** 1

𝐿𝐴!" -0.002 -0.001 1

𝑆𝑃𝐸𝑆!" 0.037*** 0.062*** 0.040*** 1

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 0.199*** 0.276*** 0.026*** 0.123*** 1

𝑆𝑅!" 0.008** 0.014*** 0.087*** 0.023*** 0.145*** 1

𝑉𝑅!" 0.179*** 0.249*** 0.028*** 0.119*** 0.988*** 0.135*** 1

𝑝𝑐𝐹𝑇𝑅!" 0.190*** 0.263*** 0.029*** 0.121*** 0.997*** 0.165*** 0.996***

This table provides the Pearson correlation matrix of earnings management measures and language FTR measures. *, **, and *** denote statistical significance at the 0.10, 0.05, and 0.01 level, respectively.

Table 4 Univariate Comparison

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" = 1 𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" = 0 Difference Test of Difference (1) (2) (3) (4)

|𝐴𝑀!"| 0.951 0.088 0.863 55.61***

(0.173) (0.053) (0.173) 113.67***

|𝑅𝑀!"| 0.906 0.250 0.656 78.35***

(0.413) (0.163) (0.250) 98.01***

𝐿𝐴!" 0.011 0.006 0.005 7.10***

(0.000) (0.000) (0.000) 7.10***

𝑆𝑃𝐸𝑆!" 0.093 0.048 0.045 33.74***

(0.000) (0.000) (0.000) 33.49*** This table compares the differences in the mean (median in parentheses) values of earnings management measures between firms in strong-FTR language countries and weak-FTR language countries. Differences in the mean and median are tested by t-test and Wilcoxon-test, with t-statistic and z-statistic reported in column (4), respectively.

34

Table 5 Multivariate Regressions – Test of Hypothesis 1

Panel A

|𝐴𝑀!"| |𝐴𝑀!"| |𝐴𝑀!"| |𝐴𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| (1) (2) (3) (4) (5) (6) (7) (8)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 0.424***

0.210***

(19.66)

(14.29)

𝑆𝑅!" 0.007*** 0.010***

(11.88) (12.73)

𝑉𝑅!" 0.342*** 0.138***

(11.05) (6.79)

𝑝𝑐𝐹𝑇𝑅!" 0.108*** 0.051*** (15.59) (11.11)

𝐼𝑁𝑉𝑃𝑅𝑂!" -0.264*** -0.224*** -0.257*** -0.263*** -0.167*** -0.149*** -0.161*** -0.166***

(-31.63) (-30.46) (-29.95) (-30.96) (-30.51) (-30.05) (-28.95) (-29.94)

𝑃𝐷!" -0.004*** 0.003*** -0.002* -0.003*** -0.002*** 0.001 -0.001 -0.002***

(-4.51) (4.61) (-1.79) (-3.56) (-3.60) (1.01) (-0.87) (-2.76)

𝐼𝑁𝐷𝐼𝑉!" -0.008*** -0.003*** -0.007*** -0.008*** -0.003*** -0.001*** -0.002*** -0.003*** (-11.94) (-5.59) (-9.42) (-11.07) (-6.70) (-3.14) (-4.33) (-6.03)

𝑀𝐴𝑆!" 0.010*** 0.009*** 0.010*** 0.010*** 0.005*** 0.005*** 0.005*** 0.005***

(30.47) (21.34) (27.76) (29.62) (21.48) (18.37) (19.46) (20.97)

𝑈𝐴!" -0.004*** -0.004*** -0.004*** -0.004*** -0.002*** -0.002*** -0.002*** -0.002***

(-12.45) (-11.71) (-11.37) (-11.99) (-6.93) (-7.49) (-6.31) (-6.63)

𝐿𝑇𝑂!" -0.015*** -0.018*** -0.017*** -0.016*** -0.009*** -0.010*** -0.010*** -0.009*** (-27.22) (-33.36) (-30.19) (-28.63) (-21.43) (-26.69) (-24.30) (-22.77)

𝐼𝑁𝐷𝑈𝐿!" 0.005*** 0.007*** 0.005*** 0.005*** 0.002*** 0.004*** 0.003*** 0.003***

(5.98) (10.02) (6.62) (6.16) (4.56) (7.21) (5.39) (4.80)

𝐺𝐺𝑅𝑂𝑊𝑇𝐻!" -0.079*** -0.074*** -0.077*** -0.078*** -0.016*** -0.014*** -0.015*** -0.016***

(-24.62) (-22.92) (-23.88) (-24.24) (-9.87) (-8.43) (-9.26) (-9.61)

𝑆𝐼𝑍𝐸!" 0.038*** 0.032*** 0.037*** 0.038*** -0.002 -0.005 -0.003 -0.002 (8.51) (7.09) (8.08) (8.36) (-0.53) (-1.60) (-0.88) (-0.64)

𝐵𝑇𝑀!" -0.012** -0.010 -0.008 -0.011* -0.045*** -0.050*** -0.042*** -0.044***

(-1.98) (-1.49) (-1.26) (-1.83) (-10.53) (-11.83) (-9.82) (-10.38)

𝐿𝐸𝑉!" 0.083* 0.117*** 0.091** 0.086* -0.093*** -0.072** -0.087*** -0.091***

(1.87) (2.64) (2.05) (1.95) (-3.19) (-2.46) (-2.98) (-3.11)

𝑅𝑂𝐴!" 0.195*** 0.242*** 0.223*** 0.208*** 0.177*** 0.198*** 0.192*** 0.184*** (3.13) (3.90) (3.58) (3.35) (4.01) (4.51) (4.36) (4.18)

𝐼𝑆𝑆𝑈𝐸!" -0.022 -0.006 -0.013 -0.017 0.167*** 0.174*** 0.172*** 0.169***

(-0.80) (-0.22) (-0.47) (-0.63) (11.19) (11.65) (11.50) (11.34)

𝑀𝐸𝐸𝑇!" 0.056*** 0.062*** 0.059*** 0.057*** 0.042*** 0.045*** 0.044*** 0.043***

(3.92) (4.31) (4.12) (4.01) (5.28) (5.59) (5.49) (5.37) 𝐿𝑂𝑆𝑆!" 0.232*** 0.258*** 0.252*** 0.242*** 0.272*** 0.284*** 0.283*** 0.278***

35

(6.30) (7.06) (6.89) (6.61) (12.99) (13.62) (13.55) (13.28)

Constant 2.568*** 2.385*** 2.608*** 2.913*** 1.380*** 1.362*** 1.372*** 1.539***

(20.29) (17.67) (19.04) (20.83) (15.74) (15.48) (15.19) (16.69) Industry Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Year Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Number of Observations

74606 74606 74606 74606 74606 74606 74606 74606

Adj. / Pseudo R-squared

0.128 0.126 0.127 0.128 0.206 0.205 0.205 0.205

Panel A of this table presents the multivariate regression results of the effects of various language FTR measures on the magnitude of accrual-based and real earnings management. The t-statistics, shown in parentheses, are based on robust standard errors clustered at the firm level. *, **, and *** denote statistical significance at the 0.10, 0.05, and 0.01 level, respectively.

36

Table 5 Multivariate Regressions – Test of Hypothesis 1

Panel B

𝐿𝐴!" 𝐿𝐴!" 𝐿𝐴!" 𝐿𝐴!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" (1) (2) (3) (4) (5) (6) (7) (8)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 0.730***

0.741***

(3.73)

(8.28)

𝑆𝑅!" 0.056*** 0.056***

(6.96) (11.61)

𝑉𝑅!" 0.830*** 1.080***

(3.11) (9.39)

𝑝𝑐𝐹𝑇𝑅!" 0.271*** 0.256*** (4.32) (9.38)

𝐼𝑁𝑉𝑃𝑅𝑂!" -0.276*** -0.240*** -0.287*** -0.314*** -0.289*** -0.229*** -0.329*** -0.315***

(-4.88) (-4.45) (-4.71) (-5.29) (-13.04) (-11.57) (-14.03) (-13.86)

𝑃𝐷!" -0.004 -0.023*** -0.003 -0.009 -0.035*** -0.027*** -0.037*** -0.037***

(-0.43) (-2.66) (-0.31) (-1.06) (-6.78) (-6.32) (-7.35) (-7.53)

𝐼𝑁𝐷𝐼𝑉!" -0.015** -0.033*** -0.016** -0.018*** -0.032*** -0.030*** -0.034*** -0.034*** (-2.41) (-4.34) (-2.44) (-2.89) (-9.19) (-9.09) (-9.94) (-9.95)

𝑀𝐴𝑆!" -0.011*** 0.008* -0.010** -0.011*** 0.009*** 0.015*** 0.009*** 0.009***

(-2.67) (1.76) (-2.51) (-2.58) (4.03) (7.26) (4.36) (4.17)

𝑈𝐴!" -0.011*** -0.021*** -0.011*** -0.012*** -0.023*** -0.026*** -0.023*** -0.023***

(-3.35) (-5.63) (-3.09) (-3.51) (-13.91) (-15.54) (-13.79) (-14.02)

𝐿𝑇𝑂!" -0.012** -0.026*** -0.014*** -0.012** -0.035*** -0.042*** -0.035*** -0.035*** (-2.57) (-4.93) (-3.02) (-2.55) (-15.52) (-19.02) (-16.29) (-15.67)

𝐼𝑁𝐷𝑈𝐿!" -0.011 -0.005 -0.011 -0.013** -0.015*** -0.006* -0.017*** -0.017***

(-1.63) (-0.63) (-1.58) (-1.97) (-4.72) (-1.87) (-5.40) (-5.28)

𝐺𝐺𝑅𝑂𝑊𝑇𝐻!" -0.052** -0.053* -0.054** -0.051** 0.039*** 0.043*** 0.033*** 0.036***

(-2.25) (-1.93) (-2.35) (-2.23) (3.62) (3.93) (3.15) (3.39)

𝑆𝐼𝑍𝐸!" -0.400*** -0.436*** -0.397*** -0.396*** -0.053*** -0.062*** -0.048*** -0.050*** (-11.72) (-13.14) (-11.60) (-11.58) (-4.68) (-5.50) (-4.23) (-4.42)

𝐵𝑇𝑀!" 0.280*** 0.187*** 0.284*** 0.275*** -0.076*** -0.108*** -0.078*** -0.078***

(8.94) (5.29) (8.94) (8.84) (-2.71) (-4.26) (-2.78) (-2.80)

𝐿𝐸𝑉!" 0.617** 0.925*** 0.605** 0.605** -0.652*** -0.591*** -0.675*** -0.666***

(2.46) (3.99) (2.41) (2.40) (-6.95) (-6.35) (-7.18) (-7.09)

𝑅𝑂𝐴!" 0.557*** 0.693*** 0.558*** 0.548*** 1.039*** 1.088*** 1.056*** 1.042*** (3.09) (4.02) (3.10) (3.04) (7.73) (8.16) (7.86) (7.76)

𝐼𝑆𝑆𝑈𝐸!" 0.111 0.175 0.119 0.102 0.319*** 0.340*** 0.319*** 0.316***

(0.72) (1.04) (0.77) (0.66) (5.67) (5.90) (5.66) (5.62)

𝑀𝐸𝐸𝑇!" -0.266*** -0.267*** -0.265*** -0.269***

(-3.02) (-3.07) (-2.99) (-3.05)

𝐿𝑂𝑆𝑆!" -0.425*** -0.405*** -0.404*** -0.416***

37

(-8.03) (-7.64) (-7.64) (-7.88)

Constant 1.558 3.730*** 1.549 2.793** 5.158*** 4.505*** 5.541*** 6.165***

(1.33) (3.19) (1.28) (2.37) (8.71) (8.69) (9.31) (10.01) Industry Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Year Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Number of Observations

74375 74375 74375 74375 74559 74559 74559 74559

Adj. / Pseudo R-squared

0.093 0.103 0.092 0.094 0.094 0.096 0.095 0.095

Panel B of this table presents the multivariate regression results of the effects of various language FTR measures on the propensity of loss avoidance and reporting small positive earnings surprises. The t-statistics, shown in parentheses, are based on robust standard errors clustered at the firm level. *, **, and *** denote statistical significance at the 0.10, 0.05, and 0.01 level, respectively.

38

Table 6 Multivariate Regressions – Test of Hypothesis 2

Panel A

|𝐴𝑀!"| |𝐴𝑀!"| |𝐴𝑀!"| |𝐴𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| (1) (2) (3) (4) (5) (6) (7) (8)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 3.461***

2.373***

(34.98)

(31.01)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.766*** -0.545***

(-34.44) (-29.94)

𝑆𝑅!" 3.449*** 2.332***

(35.17) (30.00)

𝑆𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.860*** -0.581***

(-35.08) (-29.88)

𝑉𝑅!" 3.744*** 2.430***

(28.57) (26.30)

𝑉𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.855*** -0.576***

(-30.38) (-26.99)

𝑝𝑐𝐹𝑇𝑅!" 1.000*** 0.668*** (31.55) (28.87)

𝑝𝑐𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.223*** -0.154*** (-32.21) (-28.65)

𝐼𝑁𝑉𝑃𝑅𝑂!" 0.092*** 0.127*** 0.067*** -0.502*** 0.085*** 0.088*** 0.057*** -0.332***

(9.36) (13.29) (7.10) (-34.72) (11.09) (12.34) (7.89) (-32.88)

𝑃𝐷!" -0.001 0.006*** 0.001 -0.001 -0.000 0.002*** 0.001** 0.000

(-1.22) (10.70) (1.15) (-0.67) (-0.14) (4.80) (2.04) (0.24)

𝐼𝑁𝐷𝐼𝑉!" -0.004*** -0.000 -0.004*** -0.004*** -0.000 0.001** -0.000 -0.001

(-6.84) (-0.11) (-5.15) (-6.51) (-1.03) (1.98) (-0.07) (-1.18)

𝑀𝐴𝑆!" 0.008*** 0.007*** 0.009*** 0.008*** 0.004*** 0.004*** 0.004*** 0.004***

(24.59) (18.09) (25.17) (25.48) (14.94) (14.83) (16.38) (16.23)

𝑈𝐴!" -0.014*** -0.014*** -0.013*** -0.014*** -0.009*** -0.008*** -0.008*** -0.008***

(-32.62) (-33.76) (-31.78) (-32.39) (-24.02) (-24.73) (-22.58) (-23.76)

𝐿𝑇𝑂!" 0.002*** -0.002*** -0.002*** 0.001 0.004*** 0.001* 0.000 0.003***

(2.96) (-3.10) (-3.41) (0.81) (6.67) (1.93) (0.73) (4.56)

𝐼𝑁𝐷𝑈𝐿!" 0.013*** 0.014*** 0.012*** 0.013*** 0.008*** 0.009*** 0.008*** 0.008***

(14.59) (18.38) (13.81) (14.26) (13.34) (15.24) (12.53) (12.94)

𝐺𝐺𝑅𝑂𝑊𝑇𝐻!" -0.029*** -0.023*** -0.031*** -0.028*** 0.019*** 0.020*** 0.016*** 0.019***

(-10.16) (-8.21) (-10.80) (-9.96) (11.55) (12.62) (10.04) (11.34)

𝑆𝐼𝑍𝐸!" 0.012*** 0.004 0.011** 0.011** -0.020*** -0.024*** -0.020*** -0.021***

(2.71) (0.79) (2.44) (2.46) (-6.28) (-7.48) (-6.12) (-6.30)

𝐵𝑇𝑀!" -0.005 -0.002 0.000 -0.003 -0.039*** -0.044*** -0.037*** -0.039***

(-0.75) (-0.27) (0.05) (-0.54) (-9.34) (-10.75) (-8.61) (-9.18)

𝐿𝐸𝑉!" 0.139*** 0.171*** 0.142*** 0.141*** -0.053* -0.036 -0.053* -0.053*

39

(3.19) (3.90) (3.23) (3.22) (-1.85) (-1.25) (-1.84) (-1.85)

𝑅𝑂𝐴!" 0.144** 0.196*** 0.185*** 0.161*** 0.141*** 0.167*** 0.167*** 0.151***

(2.34) (3.18) (3.00) (2.62) (3.26) (3.87) (3.85) (3.50)

𝐼𝑆𝑆𝑈𝐸!" -0.094*** -0.078*** -0.077*** -0.088*** 0.115*** 0.126*** 0.129*** 0.120*** (-3.45) (-2.85) (-2.81) (-3.24) (8.04) (8.72) (8.90) (8.34)

𝑀𝐸𝐸𝑇!" 0.044*** 0.050*** 0.050*** 0.046*** 0.034*** 0.037*** 0.038*** 0.035***

(3.13) (3.53) (3.49) (3.26) (4.30) (4.68) (4.76) (4.47)

𝐿𝑂𝑆𝑆!" 0.126*** 0.145*** 0.154*** 0.135*** 0.197*** 0.208*** 0.216*** 0.204***

(3.40) (3.94) (4.16) (3.66) (9.35) (9.91) (10.28) (9.68)

Constant 0.019 -0.130 0.293** 2.756*** -0.435*** -0.335*** -0.188** 1.430*** (0.17) (-1.13) (2.44) (20.20) (-4.53) (-3.71) (-2.00) (15.13)

Industry Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Year Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Number of Observations

74606 74606 74606 74606 74606 74606 74606 74606

Adj. / Pseudo R-squared

0.136 0.135 0.134 0.136 0.220 0.218 0.216 0.218

Panel A of this table presents the multivariate regression results of the interaction of various language FTR measures and investor protection in explaining the magnitude of accrual-based and real earnings management. The t-statistics, shown in parentheses, are based on robust standard errors clustered at the firm level. *, **, and *** denote statistical significance at the 0.10, 0.05, and 0.01 level, respectively.

40

Table 6 Multivariate Regressions – Test of Hypothesis 2

Panel B

𝐿𝐴!" 𝐿𝐴!" 𝐿𝐴!" 𝐿𝐴!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" (1) (2) (3) (4) (5) (6) (7) (8)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 2.079***

1.577***

(2.95)

(5.75)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.350** -0.211***

(-2.13) (-3.37)

𝑆𝑅!" 1.775** 1.153***

(2.31) (4.12)

𝑆𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.430** -0.274*** (-2.24) (-3.92)

𝑉𝑅!" 2.995*** 2.701***

(3.66) (8.56)

𝑉𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.562*** -0.405***

(-3.01) (-5.60)

𝑝𝑐𝐹𝑇𝑅!" 0.744*** 0.594*** (3.67) (7.52)

𝑝𝑐𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.123*** -0.084*** (-2.61) (-4.66)

𝐼𝑁𝑉𝑃𝑅𝑂!" -0.107 -0.070 -0.060 -0.433*** -0.192*** -0.120*** -0.175*** -0.406***

(-1.16) (-0.77) (-0.67) (-5.86) (-5.60) (-3.61) (-5.07) (-13.24)

𝑃𝐷!" -0.003 -0.023** -0.001 -0.008 -0.035*** -0.027*** -0.038*** -0.038*** (-0.35) (-2.56) (-0.12) (-0.90) (-6.77) (-6.26) (-7.27) (-7.53)

𝐼𝑁𝐷𝐼𝑉!" -0.014** -0.031*** -0.014** -0.016*** -0.032*** -0.030*** -0.033*** -0.033***

(-2.14) (-4.00) (-2.10) (-2.60) (-9.00) (-8.82) (-9.62) (-9.72)

𝑀𝐴𝑆!" -0.011*** 0.008 -0.010** -0.011*** 0.008*** 0.014*** 0.009*** 0.008***

(-2.81) (1.61) (-2.58) (-2.68) (3.81) (6.91) (4.18) (3.94)

𝑈𝐴!" -0.015*** -0.024*** -0.015*** -0.016*** -0.025*** -0.027*** -0.026*** -0.025*** (-3.65) (-6.00) (-3.75) (-3.97) (-13.55) (-15.60) (-13.95) (-14.03)

𝐿𝑇𝑂!" -0.005 -0.018** -0.005 -0.004 -0.030*** -0.036*** -0.028*** -0.029***

(-0.82) (-2.50) (-0.89) (-0.69) (-10.95) (-13.08) (-11.10) (-10.73)

𝐼𝑁𝐷𝑈𝐿!" -0.009 -0.002 -0.007 -0.010* -0.013*** -0.003 -0.014*** -0.014***

(-1.40) (-0.25) (-1.22) (-1.74) (-4.18) (-1.06) (-4.62) (-4.63)

𝐺𝐺𝑅𝑂𝑊𝑇𝐻!" -0.026 -0.021 -0.018 -0.020 0.059*** 0.066*** 0.065*** 0.063*** (-1.17) (-0.78) (-0.80) (-0.89) (5.58) (6.15) (6.22) (6.04)

𝑆𝐼𝑍𝐸!" -0.418*** -0.459*** -0.424*** -0.419*** -0.061*** -0.073*** -0.061*** -0.061***

(-11.95) (-12.96) (-12.01) (-11.89) (-5.25) (-6.12) (-5.19) (-5.24)

𝐵𝑇𝑀!" 0.284*** 0.192*** 0.290*** 0.280*** -0.074*** -0.104*** -0.075*** -0.075***

(9.08) (5.39) (9.13) (9.01) (-2.63) (-4.13) (-2.66) (-2.70) 𝐿𝐸𝑉!" 0.656*** 0.963*** 0.659*** 0.649*** -0.635*** -0.570*** -0.651*** -0.645***

41

(2.63) (4.15) (2.66) (2.61) (-6.77) (-6.12) (-6.94) (-6.87)

𝑅𝑂𝐴!" 0.593*** 0.747*** 0.617*** 0.597*** 1.025*** 1.073*** 1.038*** 1.023***

(3.28) (4.25) (3.40) (3.29) (7.63) (8.06) (7.74) (7.63)

𝐼𝑆𝑆𝑈𝐸!" 0.063 0.129 0.061 0.047 0.293*** 0.313*** 0.279*** 0.282***

(0.42) (0.80) (0.40) (0.31) (5.26) (5.52) (5.02) (5.07)

𝑀𝐸𝐸𝑇!" -0.270*** -0.271*** -0.269*** -0.273***

(-3.05) (-3.12) (-3.04) (-3.09)

𝐿𝑂𝑆𝑆!" -0.447*** -0.433*** -0.438*** -0.447***

(-8.41) (-8.11) (-8.25) (-8.41)

Constant 0.557 2.594** 0.179 2.843** 4.532*** 3.747*** 4.532*** 6.208***

(0.46) (1.98) (0.14) (2.39) (7.47) (6.70) (7.44) (10.15) Industry Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Year Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Number of Observations

74375 74375 74375 74375 74559 74559 74559 74559

Adj. / Pseudo R-squared

0.093 0.104 0.094 0.095 0.094 0.096 0.096 0.095

Panel B of this table presents the multivariate regression results of the interaction of various language FTR measures and investor protection in explaining the propensity of loss avoidance and reporting small positive earnings surprises. The t-statistics, shown in parentheses, are based on robust standard errors clustered at the firm level. *, **, and *** denote statistical significance at the 0.10, 0.05, and 0.01 level, respectively.

42

Table 7 Multivariate Regressions – Country Level Analysis

Panel A

|𝐴𝑀!"| |𝐴𝑀!"| |𝐴𝑀!"| |𝐴𝑀!"| |𝐴𝑀!"| |𝐴𝑀!"| |𝐴𝑀!"| |𝐴𝑀!"| (1) (2) (3) (4) (5) (6) (7) (8)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 0.048***

0.224***

(3.67)

(2.71)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.045**

(-2.41)

𝑆𝑅!" 0.000 0.240**

(0.56) (2.46)

𝑆𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.060**

(-2.46)

𝑉𝑅!" 0.036*** 0.222**

(2.69) (2.31)

𝑉𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.049**

(-2.17)

𝑝𝑐𝐹𝑇𝑅!" 0.012*** 0.063** (3.24) (2.51)

𝑝𝑐𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.013** (-2.30)

𝐼𝑁𝑉𝑃𝑅𝑂!" -0.020*** -0.014** -0.018** -0.019*** 0.001 0.009 0.001 -0.033***

(-2.72) (-2.20) (-2.58) (-2.67) (0.15) (0.97) (0.11) (-2.92)

𝑃𝐷!" 0.001 0.001*** 0.001* 0.001 0.000 0.001** 0.001* 0.000

(1.49) (2.62) (1.83) (1.59) (1.10) (2.17) (1.69) (1.27)

𝐼𝑁𝐷𝐼𝑉!" 0.001** 0.001** 0.001** 0.001** 0.001* 0.001** 0.001** 0.001**

(1.98) (2.31) (2.12) (2.02) (1.92) (2.32) (2.19) (2.03)

𝑀𝐴𝑆!" 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000

(1.00) (1.26) (1.14) (1.10) (0.80) (1.13) (1.08) (0.95)

𝑈𝐴!" -0.001*** -0.001*** -0.001*** -0.001*** -0.001*** -0.001*** -0.001*** -0.001***

(-3.01) (-2.62) (-2.74) (-2.89) (-3.32) (-3.10) (-3.07) (-3.21)

𝐿𝑇𝑂!" -0.000 -0.001** -0.001* -0.001 0.000 -0.000 -0.000 0.000

(-1.12) (-2.18) (-1.68) (-1.42) (0.50) (-0.78) (-0.65) (0.06)

𝐼𝑁𝐷𝑈𝐿!" 0.001 0.000 0.001 0.001 0.001** 0.001* 0.001* 0.001**

(1.41) (1.18) (1.23) (1.33) (2.18) (1.91) (1.79) (2.03)

𝐺𝐺𝑅𝑂𝑊𝑇𝐻!" -0.001 0.000 0.000 -0.000 0.002 0.004 0.003 0.003

(-0.21) (0.01) (0.01) (-0.09) (0.78) (1.23) (1.00) (0.97)

Constant 0.129*** 0.100* 0.108** 0.144*** 0.002 -0.029 0.010 0.151***

(2.83) (1.85) (2.31) (2.89) (0.03) (-0.41) (0.17) (2.83) Industry Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Year Fixed Yes Yes Yes Yes Yes Yes Yes Yes

43

Effects

Number of Observations

364 364 364 364 364 364 364 364

Adj. / Pseudo R-squared

0.071 0.053 0.060 0.065 0.084 0.073 0.071 0.078

Panel A of this table presents the multivariate regression results on accrual-based earnings management at the country-year level. The t-statistics, shown in parentheses, are based on White (1980) robust standard errors. *, **, and *** denote statistical significance at the 0.10, 0.05, and 0.01 level, respectively.

44

Table 7 Multivariate Regressions – Country Level Analysis

Panel B

|𝑅𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| |𝑅𝑀!"| (1) (2) (3) (4) (5) (6) (7) (8)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 0.053***

0.280***

(3.01)

(2.93)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.058***

(-2.74)

𝑆𝑅!" 0.001** 0.239**

(2.42) (2.19)

𝑆𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.060**

(-2.18)

𝑉𝑅!" 0.026 0.204*

(1.39) (1.88)

𝑉𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.047*

(-1.85)

𝑝𝑐𝐹𝑇𝑅!" 0.011** 0.069** (2.31) (2.37)

𝑝𝑐𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.015** (-2.26)

𝐼𝑁𝑉𝑃𝑅𝑂!" -0.011 -0.005 -0.007 -0.009 0.017** 0.018** 0.011* -0.025*

(-1.43) (-0.73) (-0.96) (-1.24) (2.51) (2.26) (1.65) (-1.80)

𝑃𝐷!" 0.000 0.001 0.000 0.000 -0.000 0.000 0.000 0.000

(0.34) (1.35) (0.99) (0.60) (-0.01) (1.00) (0.89) (0.34)

𝐼𝑁𝐷𝐼𝑉!" 0.002*** 0.002*** 0.002*** 0.002*** 0.002*** 0.002*** 0.002*** 0.002***

(4.75) (5.04) (5.05) (4.86) (4.54) (4.81) (4.84) (4.66)

𝑀𝐴𝑆!" 0.001*** 0.001*** 0.001*** 0.001*** 0.001*** 0.001*** 0.001*** 0.001***

(3.01) (3.19) (3.14) (3.09) (2.89) (3.22) (3.16) (3.06)

𝑈𝐴!" -0.001*** -0.001*** -0.001*** -0.001*** -0.001*** -0.001*** -0.001*** -0.001***

(-3.79) (-3.40) (-3.43) (-3.61) (-3.98) (-3.62) (-3.49) (-3.72)

𝐿𝑇𝑂!" -0.001 -0.001*** -0.001** -0.001* 0.000 -0.001 -0.001 -0.000

(-1.54) (-2.61) (-2.29) (-1.93) (0.43) (-1.45) (-1.43) (-0.40)

𝐼𝑁𝐷𝑈𝐿!" 0.001 0.001 0.001 0.001 0.001** 0.001* 0.001* 0.001**

(1.49) (1.34) (1.28) (1.39) (2.26) (1.88) (1.69) (2.00)

𝐺𝐺𝑅𝑂𝑊𝑇𝐻!" -0.001 0.000 0.000 -0.000 0.003 0.004 0.003 0.003

(-0.19) (0.03) (0.03) (-0.05) (1.02) (1.22) (0.97) (1.08)

Constant 0.196*** 0.196*** 0.192*** 0.230*** 0.033 0.047 0.078 0.238***

(2.77) (2.89) (2.91) (3.25) (0.44) (0.61) (1.08) (3.10) Industry Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Year Fixed Yes Yes Yes Yes Yes Yes Yes Yes

45

Effects

Number of Observations

364 364 364 364 364 364 364 364

Adj. / Pseudo R-squared

0.186 0.172 0.173 0.179 0.202 0.186 0.179 0.190

Panel B of this table presents the multivariate regression results on real earnings management at the country-year level. The t-statistics, shown in parentheses, are based on White (1980) robust standard errors. *, **, and *** denote statistical significance at the 0.10, 0.05, and 0.01 level, respectively.

46

Table 7 Multivariate Regressions – Country Level Analysis

Panel C

𝐿𝐴!" 𝐿𝐴!" 𝐿𝐴!" 𝐿𝐴!" 𝐿𝐴!" 𝐿𝐴!" 𝐿𝐴!" 𝐿𝐴!" (1) (2) (3) (4) (5) (6) (7) (8)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 1.262***

6.870***

(3.16)

(3.90)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-1.411***

(-3.46)

𝑆𝑅!" 1.119** 7.633***

(2.47) (3.76)

𝑆𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-1.669***

(-3.56)

𝑉𝑅!" 1.137** 7.527***

(2.47) (3.69)

𝑉𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-1.650***

(-3.46)

𝑝𝑐𝐹𝑇𝑅!" 0.353*** 2.169*** (2.98) (3.82)

𝑝𝑐𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.457*** (-3.53)

𝐼𝑁𝑉𝑃𝑅𝑂!" -0.392** -0.427*** -0.370** -0.403** 0.226 0.186 0.210 -0.952***

(-2.48) (-2.65) (-2.32) (-2.48) (1.15) (0.97) (1.12) (-3.55)

𝑃𝐷!" 0.017 0.015 0.021* 0.017 0.015 0.015 0.021* 0.015

(1.53) (1.36) (1.82) (1.47) (1.43) (1.30) (1.87) (1.34)

𝐼𝑁𝐷𝐼𝑉!" 0.043*** 0.040*** 0.044*** 0.042*** 0.043*** 0.044*** 0.048*** 0.045***

(3.40) (3.23) (3.54) (3.41) (3.65) (3.54) (3.90) (3.71)

𝑀𝐴𝑆!" 0.014** 0.021*** 0.016** 0.015** 0.013* 0.021*** 0.016** 0.015**

(2.16) (3.08) (2.54) (2.34) (1.94) (3.05) (2.49) (2.16)

𝑈𝐴!" -0.053*** -0.053*** -0.050*** -0.052*** -0.063*** -0.063*** -0.058*** -0.063***

(-6.20) (-6.22) (-6.06) (-6.14) (-6.58) (-6.33) (-6.29) (-6.17)

𝐿𝑇𝑂!" 0.013 0.007 0.008 0.012 0.033*** 0.023** 0.023** 0.032***

(1.49) (0.79) (0.99) (1.34) (2.89) (2.12) (2.20) (2.72)

𝐼𝑁𝐷𝑈𝐿!" -0.041*** -0.039*** -0.042*** -0.042*** -0.027* -0.030** -0.035** -0.031**

(-2.74) (-2.70) (-2.87) (-2.78) (-1.88) (-2.09) (-2.38) (-2.10)

𝐺𝐺𝑅𝑂𝑊𝑇𝐻!" -0.135** -0.137** -0.127* -0.131** -0.047 -0.027 -0.024 -0.023

(-2.08) (-2.09) (-1.93) (-2.00) (-0.68) (-0.37) (-0.33) (-0.32)

Constant 1.621 2.033 1.486 2.656* -1.843 -1.258 -1.571 3.864**

(1.16) (1.49) (1.09) (1.77) (-1.10) (-0.80) (-1.02) (2.26) Industry Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Year Fixed Yes Yes Yes Yes Yes Yes Yes Yes

47

Effects

Number of Observations

357 357 357 357 357 357 357 357

Adj. / Pseudo R-squared

0.238 0.251 0.229 0.237 0.267 0.283 0.258 0.270

Panel C of this table presents the multivariate regression results on the propensity of loss avoidance at the country-year level. The t-statistics, shown in parentheses, are based on White (1980) robust standard errors. *, **, and *** denote statistical significance at the 0.10, 0.05, and 0.01 level, respectively.

48

Table 7 Multivariate Regressions – Country Level Analysis

Panel D

𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" 𝑆𝑃𝐸𝑆!" (1) (2) (3) (4) (5) (6) (7) (8)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!" 1.988***

9.587***

(5.55)

(5.35)

𝑠𝑡𝑟𝑜𝑛𝑔𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-1.881***

(-4.68)

𝑆𝑅!" 1.917*** 9.191***

(4.70) (5.01)

𝑆𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-1.845***

(-4.35)

𝑉𝑅!" 1.958*** 8.886***

(4.69) (4.97)

𝑉𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-1.779***

(-4.23)

𝑝𝑐𝐹𝑇𝑅!" 0.566*** 2.837*** (5.31) (5.43)

𝑝𝑐𝐹𝑇𝑅!"∗ 𝐼𝑁𝑉𝑃𝑅𝑂!"

-0.564*** (-4.81)

𝐼𝑁𝑉𝑃𝑅𝑂!" -0.623*** -0.650*** -0.598*** -0.643*** 0.171 0.010 0.019 -1.348***

(-4.02) (-3.94) (-3.71) (-3.98) (0.90) (0.05) (0.09) (-5.75)

𝑃𝐷!" -0.007 -0.009 -0.004 -0.008 -0.011 -0.013 -0.007 -0.013

(-0.69) (-0.92) (-0.43) (-0.80) (-1.12) (-1.30) (-0.64) (-1.31)

𝐼𝑁𝐷𝐼𝑉!" 0.034*** 0.031*** 0.035*** 0.034*** 0.036*** 0.037*** 0.041*** 0.039***

(3.11) (2.92) (3.29) (3.13) (3.29) (3.27) (3.63) (3.40)

𝑀𝐴𝑆!" 0.024*** 0.028*** 0.024*** 0.024*** 0.024*** 0.030*** 0.025*** 0.025***

(3.91) (4.70) (4.18) (4.09) (3.68) (4.79) (4.21) (3.97)

𝑈𝐴!" -0.060*** -0.057*** -0.054*** -0.058*** -0.076*** -0.069*** -0.064*** -0.074***

(-7.23) (-7.25) (-7.09) (-7.19) (-7.43) (-7.86) (-7.93) (-7.67)

𝐿𝑇𝑂!" 0.032*** 0.026*** 0.026*** 0.031*** 0.060*** 0.044*** 0.042*** 0.057***

(3.79) (3.10) (3.31) (3.68) (4.63) (3.98) (4.13) (4.63)

𝐼𝑁𝐷𝑈𝐿!" -0.046*** -0.046*** -0.048*** -0.048*** -0.030** -0.039*** -0.043*** -0.038***

(-3.26) (-3.23) (-3.40) (-3.32) (-2.20) (-2.73) (-3.02) (-2.65)

𝐺𝐺𝑅𝑂𝑊𝑇𝐻!" -0.141** -0.121* -0.111* -0.129* -0.040 -0.007 -0.007 -0.011

(-2.10) (-1.80) (-1.66) (-1.91) (-0.52) (-0.09) (-0.09) (-0.13)

Constant 2.980** 3.356** 2.943** 4.683*** -1.329 -0.001 -0.145 6.556***

(2.11) (2.34) (2.03) (3.07) (-0.71) (-0.00) (-0.08) (4.02) Industry Fixed Effects

Yes Yes Yes Yes Yes Yes Yes Yes

Year Fixed Yes Yes Yes Yes Yes Yes Yes Yes

49

Effects

Number of Observations

362 362 362 362 362 362 362 362

Adj. / Pseudo R-squared

0.249 0.255 0.232 0.246 0.294 0.291 0.264 0.292

Panel D of this table presents the multivariate regression results on the propensity of reporting small positive earnings surprises at the country-year level. The t-statistics, shown in parentheses, are based on White (1980) robust standard errors. *, **, and *** denote statistical significance at the 0.10, 0.05, and 0.01 level, respectively.