Embed Size (px)

DESCRIPTION

The Role and Operational Logistics of the Pharmaceutical Industry in the Great Lakes Megaregion. Research conducted with Anthony Pins. Deliverable for: Landscape Infrastructure Research Seminar [A505] W 2011 with Geoffrey Thün.

Citation preview

1

BIOFUELFLOAT GLASSNICKEL

TIMBERVITICULTUREWASTEWATER

PHARMA:The Role of the Pharmaceutical Industry in the Great Lakes Megaregion

Anthony Pins

Geoffrey Salvatore

3

Ubiquitous advertising and a growing consumer desire for higher quality of life have propelled the pharmaceutical industry into a prominent cultural role. In one regard, these drugs engineer away our way from our biological problems. In another, they are the natural manifestation of our technological advancements.

Amid increasing demand, the pharmaceutical industry utilizes its large financial resources to fund a massive cycles of research and development. This process, necessitated by the regulatory framework that exists, perpetuates a high risk and reward system where in surviving an intensive four to six year series of clinical trials are met with immense payoffs. However, the chances of developing such a

$860B in 2010 worldwide sales$230B in 2010 US sales$21B in pharmaceutical advertising

blockbuster drug are small and the patent protection windows offer minimal security. This situation has created a looming cliff at which time the patents of many major blockbuster drugs are set to expire with no immediate replacements. This will radically reshape the industry as it has relied on its financial windfalls to fund its navigation of the extensive regulatory framework and global expansion.

Beyond its own corporate structures and internal research and development operations, the industry is reliant on a number of networks to fulfill its design and delivery of pharmaceutical drugs. These research, manufacturing and distribution networks exist within the Great Lakes Megaregion. They are in large measure a vestige of the Megaregion’s manufacturing past, but are essential components to an industry implicated in a 21st Century knowledge economy.

Through the analysis of these industrial processes and systems, this investigation seeks to reveal the potential for engaging existing infrastructures at the level of megaregion.

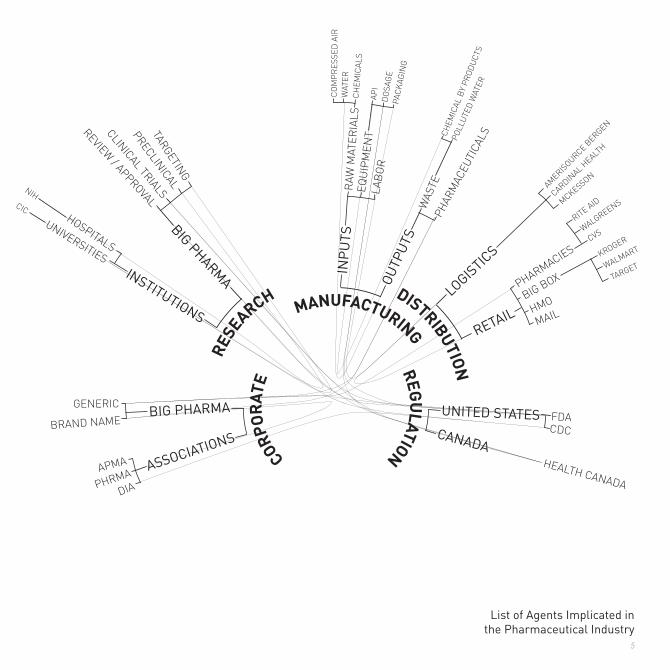

5

RESE

ARCH DISTRIBUTION

MANUFACTURINGCORP

OR

ATE

REGU

LATIONLOGISTIC

S

RETAIL

PHARMACIESCVSWALGREENS

CARDINAL H

EALTH

AMERISOURCE B

ERGEN

MCKESSON

RITE AID

BIG BOX

KROGER

WALMART

TARGET

HMO

INP

UTS

RAW

MAT

ERIA

LSC

HEM

ICAL

S

WAT

ERC

OM

PR

ESSE

D A

IR

EQU

IPM

ENT

API

DO

SAG

EPA

CK

AGIN

G

LAB

OR

OUTP

UTS

WAS

TEPH

ARM

ACEU

TICA

LSPOLL

UTE

D W

ATER

CHEM

ICAL

BY

PROD

UCT

S

UNITED STATES FDACDCCANADA

HEALTH CANADABIG PHARMA

REVIEW / APPROVAL

CLINICAL TRIALS

PRECLINICAL

TARGETING

INSTITUTIONS

UNIVERSITIES

CIC

NIH

HOSPITALS

BIG PHARMABRAND NAME

GENERIC

ASSOCIATIONS

PHRMAAPMA

DIA

List of Agents Implicated in the Pharmaceutical Industry

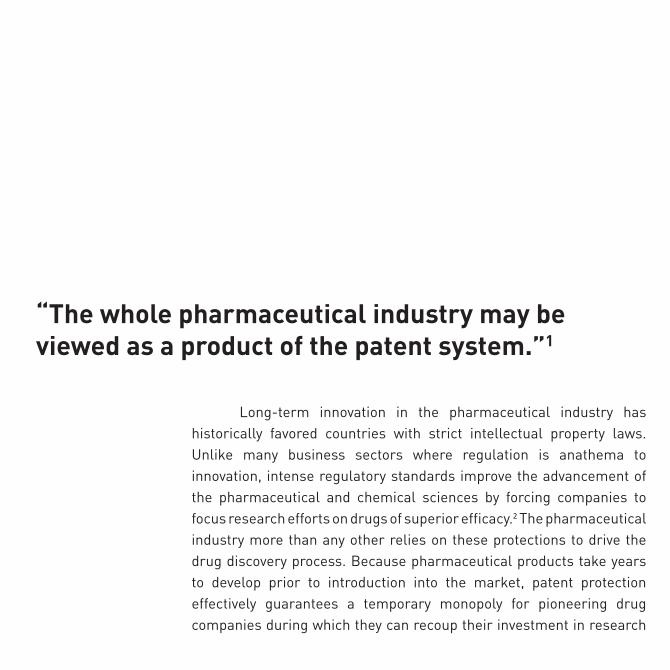

Long-term innovation in the pharmaceutical industry has historically favored countries with strict intellectual property laws. Unlike many business sectors where regulation is anathema to innovation, intense regulatory standards improve the advancement of the pharmaceutical and chemical sciences by forcing companies to focus research efforts on drug s of superior efficacy.2 The pharmaceutical industry more than any other relies on these protections to drive the drug discovery process. Because pharmaceutical products take years to develop prior to introduction into the market, patent protection effectively guarantees a temporary monopoly for pioneering drug companies during which they can recoup their investment in research

“The whole pharmaceutical industry may be viewed as a product of the patent system.”1

7

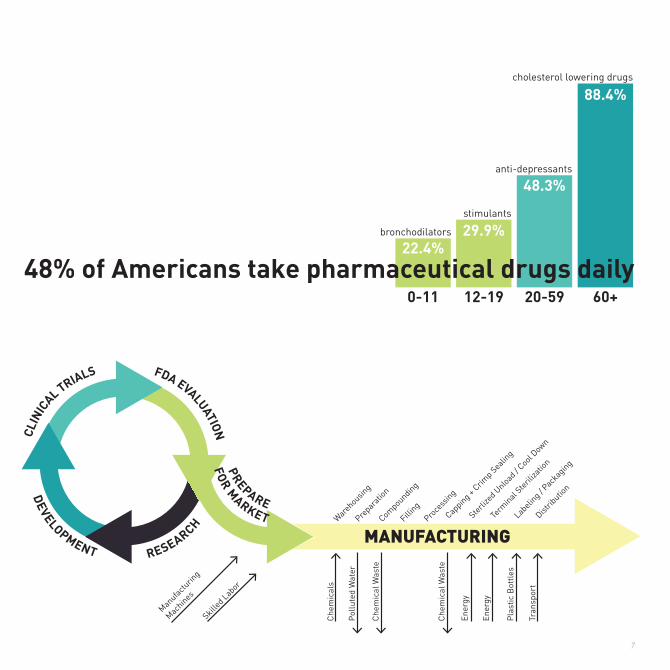

88.4%

48.3%

29.9%22.4%

0-11

bronchodilators

stimulants

anti-depressants

cholesterol lowering drugs

12-19 20-59 60+

48% of Americans take pharmaceutical drugs daily

Warehousin

g

Che

mic

als

Prepar

ation

Compounding

Filling

Proce

ssing

Capping +

Crimp Seali

ng

Sterlize

d Unload

/ Cool D

own

Term

inal Steril

izatio

n

Labelin

g / Pac

kaging

Distrib

ution

Manufac

turin

g

Machines

Skilled Lab

or

Pol

lute

d W

ater

Che

mic

al W

aste

Che

mic

al W

aste

Ener

gy

Ener

gy

Pla

stic

Bot

tles

Tran

spor

t

PREPARE

PHARMACEUTICALDRUG

DEVELOPMENT RESEARCH

CLIN

ICAL TRIALS FDA EVALUATION

FOR M

ARKET

MANUFACTURING

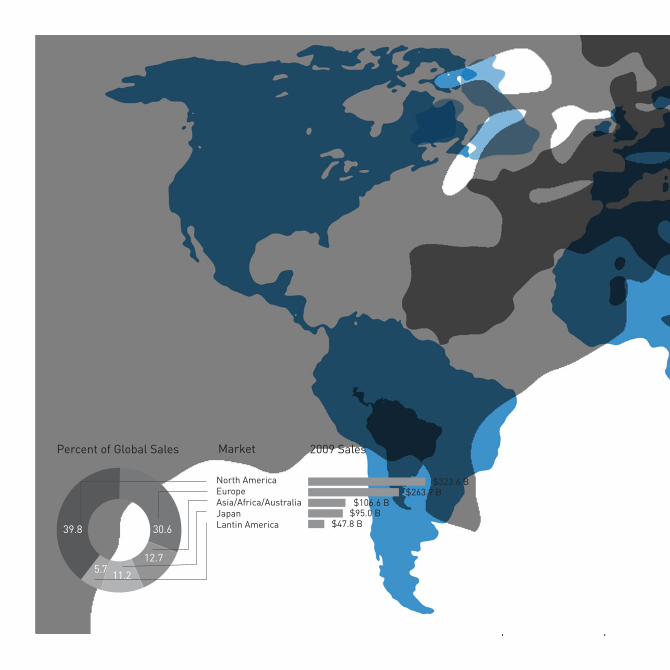

Re-Spatialization of World based on Pharmaceutical Consumption Relative to Population

39.8 30.6

12.7

11.25.7

MarketPercent of Global Sales 2009 Sales

North AmericaEuropeAsia/Africa/AustraliaJapanLantin America

$323.6 B$263.9 B

$106.6 B

$47.8 B$95.0 B

9

39.8 30.6

12.7

11.25.7

MarketPercent of Global Sales 2009 Sales

North AmericaEuropeAsia/Africa/AustraliaJapanLantin America

$323.6 B$263.9 B

$106.6 B

$47.8 B$95.0 B

and development. According to one study of twenty professional sectors, the pharmaceutical industry has the highest sales-weighted propensity to patent product innovations and the second highest propensity to patent process innovations.3

The United States’ favorable patent policies, pro-business climate, and considerable market share have made it home to nearly half of all corporate pharmaceutical activity. To this end, the United States has used its market dominance to become the de facto arbiter of global regulatory issues, holding considerable bargaining power in international trade negotiations. Indeed, the United States was instrumental in initiating discussions linking international trade policy with intellectual property rights prior to the ratification of the North American Free Trade Agreement (NAFTA) and the Agreement on Trade Intellectual Property (TRIPS). Intense lobbying by large intellectual property interests including the pharmaceutical, entertainment, publishing and computer programming industries supported these efforts, gaining access to US trade

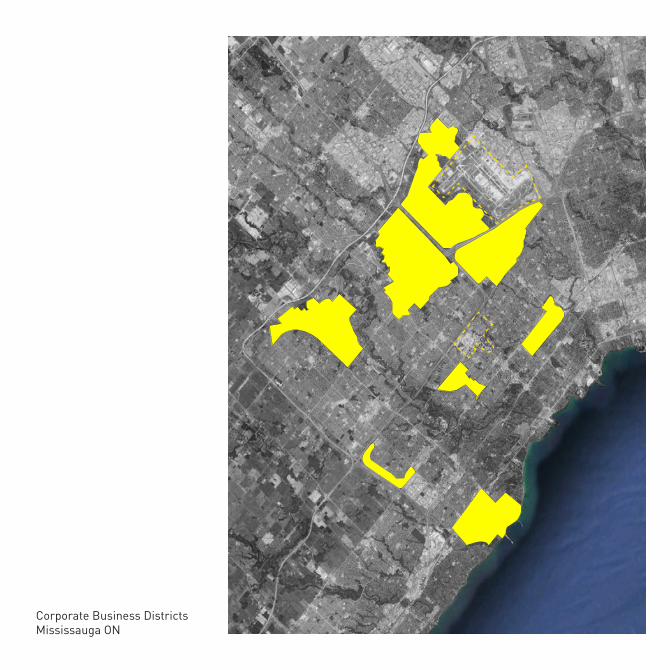

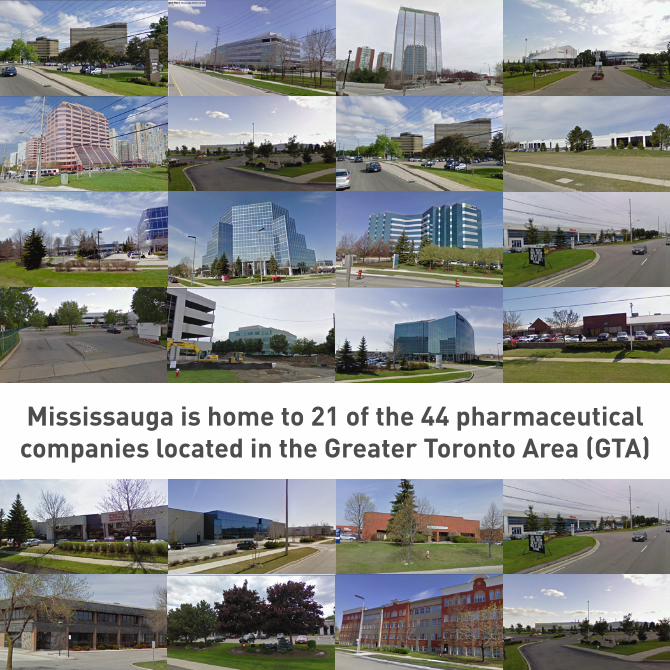

Corporate Business DistrictsMississauga ON

11

policymakers through the Advisory Committee for Trade Negotiation (ACTN). This committee was chaired, not incidentally, by the CEO of the New York-based pharmaceutical giant Pfizer4.

The dissemination of trade and intellectual property standards on a global scale has enlarged the sphere of protection for large pharmaceutical operations, opening new potential in emerging markets and streamlining regulatory limitations previously drawn along political boundaries. Today, the top 20 transnational corporations each have an average of more than 100 foreign affiliates in more than 40 countries, 19 of which are developing nations.5 Despite expansion into markets in Asia and Latin America, over three-quarters of pharmaceutical sales remain in North America, Europe, and Japan6, suggesting that the wider dissemination of pharmaceutical products is still far off. The immediate impact of TRIPS may then be understood to protect and facilitate sales in increasingly competitive existing markets.

This increasingly global pharmaceutical market has spurred a new spatial logic in the distribution of corporate facilities, one not based entirely on proximity to manufacturing and distribution, but rather to political hubs, desirable living, and access to international travel. In Canada, 47 percent of pharmaceutical corporate and research facilities are concentrated in the province of Ontario, with another 42.8 percent located in Quebec, almost exclusively in the areas surrounding Toronto and Montreal, respectively.7 Many of the firms located here are secondary corporate facilities for multinational firms, oriented toward navigating national and provincial regulatory frameworks, taking on the “back-office” functions that require less face-to-face meeting with clients. The convergence of international pharmaceutical companies in Mississauga, Ontario, is instructive in this realm, as nearly half of the major pharmaceutical companies active in the Greater Toronto Area (GTA) are located here.

Mississauga offers a number of strategic advantages to firms’ less-critical corporate functions. Its proximity to both air and ground transportation corridors provide accessibility to downtown Toronto as well as international corporate locations, while co-locating with global logistics carriers around Pearson International Airport (YYZ). Suburban back-office functions also recognize the desired living conditions of the labor force in the Megaregion, providing workers with inexpensive housing (relative to downtown Toronto), access to quality schools as well as

research institutions. Recognizing these advantages, Mississauga has focused job creation in a number of corporate business parks at the fringe of the city limits and heavily marketed itself to corporations seeking to locate there. Among the city’s promotional claims is a dedication to keeping the taxes as low as possible – the city’s current tax rate is about two-thirds that of downtown Toronto – according to an AAA bond rating by Standard and Poor’s and a significant strategic reserve for infrastructure investments.8

13

Mississauga is home to 21 of the 44 pharmaceutical companies located in the Greater Toronto Area (GTA)

In the United States, the largest concentration of pharmaceutical firms remains in northern New Jersey, with additional clusters in the San Francisco Bay Area and North Carolina Research Triangle. Despite the coastal orientation of these firms, the Great Lakes Megaregion maintains significant pharmaceutical presence based largely on its manufacturing legacy and concentration of research institutions. Many of these firms have longstanding ties to their local community, making them integral and often influential civic bodies. However, firms located in the GLM appear to be more vulnerable to corporate restructuring, and most have separate, if not more significant corporate locations in

“Pfizer and Wyeth Merger – Could It Be True (Love)?”10

“Pfizer Cuts Research Operations After Wyeth Deal”11

15

a coastal hub. The maintenance of ties to their local economy results in part from their ability to extract subsidies from local and state governments. Eli Lilly, for example, received over $214 million in state and local tax subsidies in 1999 for pledging to expand its global headquarters and technology center in Indianapolis. Similar tactics have been employed in other jurisdictions, including property tax abatement and access to state research grants.

The waning presence of the region’s manufacturing sector has allowed for the decoupling of co-located corporate and production facilities. Consolidation and outsourcing of the drug manufacturing process to inexpensive labor countries has dissolved the advantages of concentrating business operations in a single location. To this end, Saskia Sassen’s claim of a direct relationship between growth in a megaregion’s dispersed economic activities and

Warner-Lambert

Pfizer

Pfeiffer

Pharmacia

KabiVitrum

Upjohn Phamaceuticals

Monsanto

America Life Sciences

Wyeth

American Home Products

Ayerst

Fort Dodge Serum Co.

AH Robins

American Cynamid

King Pharma

Alpharma

New Jersey Chilcott Laboratories

Pfizer PharmaceuticalsHistorical Diagram of Recent Mergers

1900 1910 1920 1930

1938: Food, Drug and Cosmetic Act

1906: Pure Food and Drug Act (USA)

1920: Food and Drugs Act (CAN)

1909: Patent Medicine Act (CAN)

1952: Patent Act (USA)

1940 1950 1960

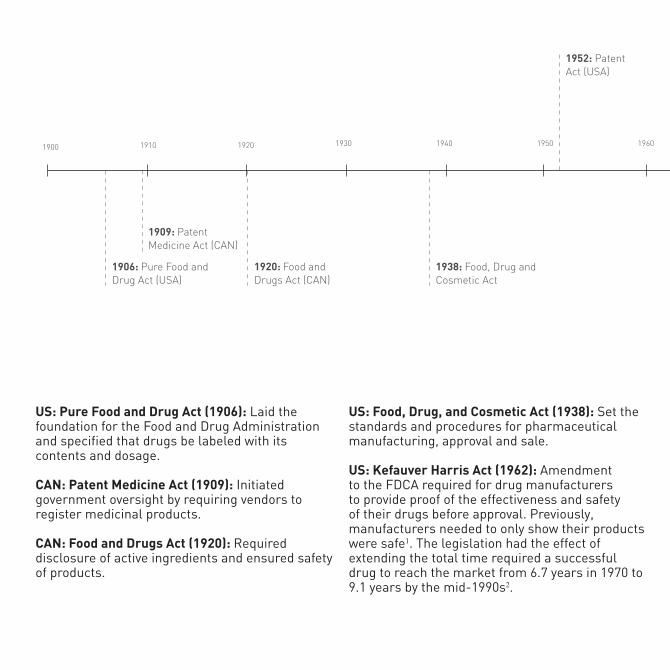

US: Pure Food and Drug Act (1906): Laid the foundation for the Food and Drug Administration and specified that drugs be labeled with its contents and dosage.

CAN: Patent Medicine Act (1909): Initiated government oversight by requiring vendors to register medicinal products.

CAN: Food and Drugs Act (1920): Required disclosure of active ingredients and ensured safety of products.

US: Food, Drug, and Cosmetic Act (1938): Set the standards and procedures for pharmaceutical manufacturing, approval and sale.

US: Kefauver Harris Act (1962): Amendment to the FDCA required for drug manufacturers to provide proof of the effectiveness and safety of their drugs before approval. Previously, manufacturers needed to only show their products were safe1. The legislation had the effect of extending the total time required a successful drug to reach the market from 6.7 years in 1970 to 9.1 years by the mid-1990s2.

17

1952: Patent Act (USA)

1962: Kefauver-Harris Act (USA)

1984: Drug Price Competition and Patent Resotration Act (USA)

1994: Trade-Related Aspects of Intellectual Property (TRIPS) Agreement

1992: Prescription Drug User Fee Act (USA)

1984: Canada Health Act (CAN)

2010: Affordable Care Act

1970 1980 1990 2000 2010 2020

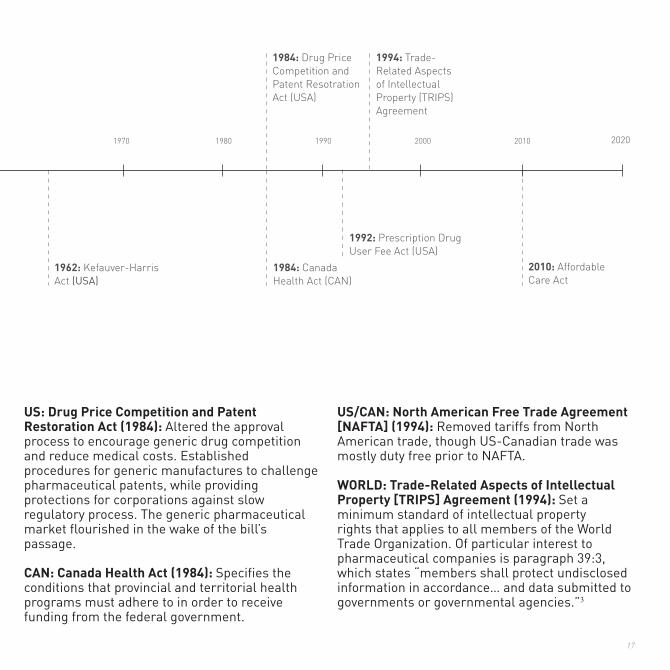

US: Drug Price Competition and Patent Restoration Act (1984): Altered the approval process to encourage generic drug competition and reduce medical costs. Established procedures for generic manufactures to challenge pharmaceutical patents, while providing protections for corporations against slow regulatory process. The generic pharmaceutical market flourished in the wake of the bill’s passage.

CAN: Canada Health Act (1984): Specifies the conditions that provincial and territorial health programs must adhere to in order to receive funding from the federal government.

US/CAN: North American Free Trade Agreement [NAFTA] (1994): Removed tariffs from North American trade, though US-Canadian trade was mostly duty free prior to NAFTA.

WORLD: Trade-Related Aspects of Intellectual Property [TRIPS] Agreement (1994): Set a minimum standard of intellectual property rights that applies to all members of the World Trade Organization. Of particular interest to pharmaceutical companies is paragraph 39:3, which states “members shall protect undisclosed information in accordance… and data submitted to governments or governmental agencies.”3

Lipitor

Pfiz

erSa

nofi-

Aven

tisN

ovar

tisG

laxo

Smith

Klin

eR

oche

Ast

raZe

neca

Mer

ckJo

hnso

n &

Joh

nson

Eli L

illy

Bri

stol

-Mye

rs S

quib

bA

bbot

tB

ayer

Boe

hrin

ger

Inge

lhei

mA

mge

nTa

keda

Teva

Nov

o N

ordi

skA

stel

las

Dai

ichi

San

kyo

Ots

uka

$45.

2 B

$42.

0 B

$38.

4 B

$37.

8 B

$37.

6 B

$32.

8 B

$25.

2 B

$22.

5 B

$21.

2 B

$18.

8 B

$15.

6 B

$15.

0 B

$14.

4 B

$14.

4 B

$14.

2 B

$13.

9 B

$9.8

B$9

.8 B

$8.1

B$7

.9 B

$13.28 B$9.10 B

$8.24 B$8.10 B

$6.01 B$5.86 B

$5.45 B$5.38 B$5.36 B

$5.32 B$5.02 B

$4.57 B$4.67 B$4.68 B

$4.99 B

NexiumSeretideSeroquelEnbrelRemicadeCrestorLipitorZyprexaLipitorHumiraSingulairMabritheraAbilifyLovenox

Cost of Products Sold

Cost of Sales and Marketing

Cost of Research and Development

[Above] Development Costs Associated with Pharmaceutical

[Left] Pharmaceutical Companies and Products by Sales

19

activities subject to high agglomeration economies is troubling for the future of the Great Lakes Megaregion. If, as she claims, “the more the former grow, the more the latter will also grow,”9 the decline of manufacturing would seem to have negative implications for pharmaceutical operations in the region as a whole.

On March 9, 2009, New Jersey-based pharmaceutical giant Merck acquired fellow industry behemoth Schering-Plough in a $41.8 billion merger of the world’s seventh and fifteenth largest pharmaceutical companies. With a combined sales revenue of $36.8 billion in 2008, the merger expanded Merck’s geographic influence and gave it access to Schering-Plough’s developing biologics research, biotechnology drugs derived from living cells that are much harder for generic manufacturers to copy.12 Three days later, Swiss-based Roche Pharmaceuticals bought Genentech, then the nineteenth largest pharmaceutical company, for

0%

1984 2003

10

20

30

40

50

60

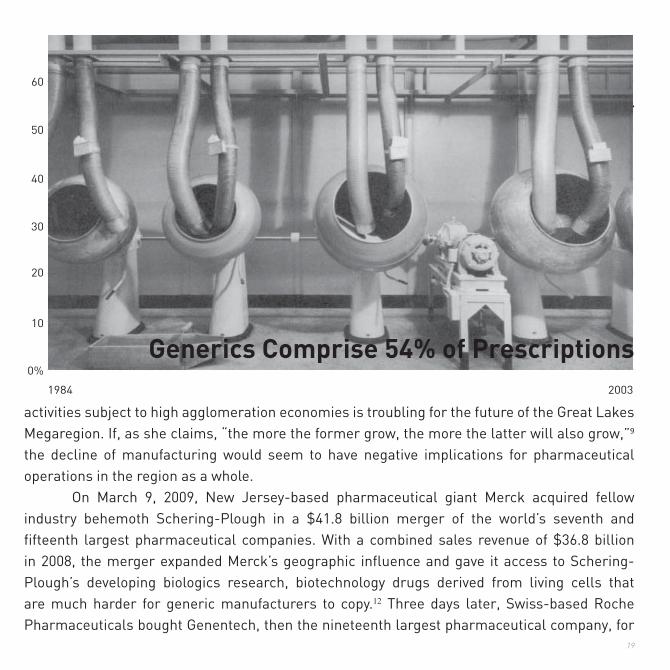

Generics Comprise 54% of Prescriptions

$47 billion. By September 29, 2009, Pfizer, the world’s largest pharmaceutical company, had acquired Wyeth, the world’s tenth largest drug maker, completing perhaps the single largest redistribution of industry power in a single year.

Over the past two decades, a wave of consolidations driven by generic drug competition, strategic alignments for new markets and a desire to reduce overhead costs have reshaped the corporate pharmaceutical landscape. In 1985, the top ten pharmaceutical companies controlled about 20 percent of industry market share. By 2005, the top ten controlled nearly half.13 In addition to the three headline-generating mergers of 2009, 26 other companies merged with or consumed their competitors, consolidating a net worth $126.5 billion. A year prior, 48 mergers occurred, worth $51.1 billion.14

The intensification of consolidation in recent years reflects growing fears that blockbuster drugmakers will be unable to weather the onset of patent expirations threatening their most profitable drugs. First initiated by regulatory changes in the 1980s, generic manufacturers are permitted to develop lower-cost drug equivalents during the patent-life of the original drug. Without development costs associated with clinical trials, chemical research, and safety reviews, generic pharmaceutical companies are able to enter the market with equivalent products almost immediately following patent expiration. In the United States, over half of the prescriptions filled in 2004 were for generic prescriptions. In Canada, generic prescriptions account for over 40 percent of total prescriptions.15

The pharmaceutical industry’s instability stems from its reliance on the success of relatively few drugs to maintain year-to-year profits. In 2010, 34 percent of the pharmaceutical industry’s $860 billion in worldwide sales came from just 133 blockbuster drugs. Of those blockbusters, 13 are set to lose patent protection by 2013. An estimated $250 billion in sales are at risk between now and 2015.16 Pfizer in particular stands vulnerable to the impending wave of patent expirations. Its blockbuster cholesterol drug Lipitor, which accounted for a quarter of the company’s profits in 2010, is set to expire in 2011. Combined with other patent expirations, Pfizer will lose more than 70% of its 2007 revenues by 201517. The company has no equivalent blockbuster drug in production.

21

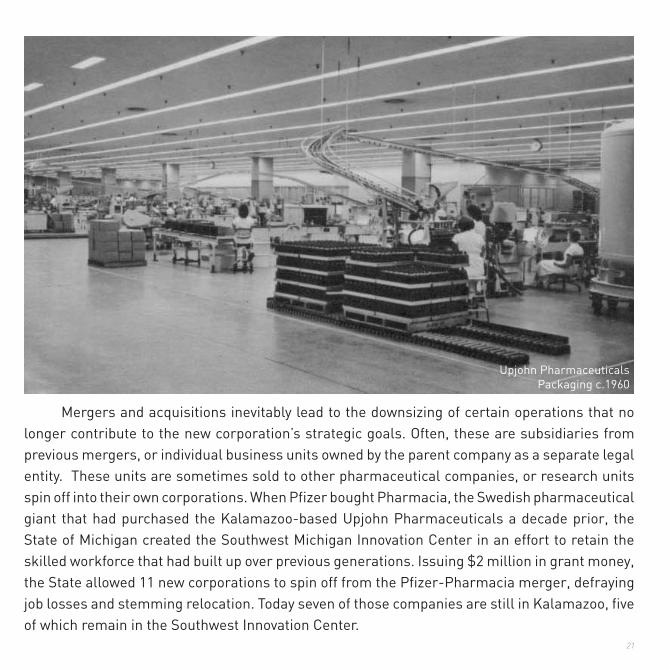

Mergers and acquisitions inevitably lead to the downsizing of certain operations that no longer contribute to the new corporation’s strategic goals. Often, these are subsidiaries from previous mergers, or individual business units owned by the parent company as a separate legal entity. These units are sometimes sold to other pharmaceutical companies, or research units spin off into their own corporations. When Pfizer bought Pharmacia, the Swedish pharmaceutical giant that had purchased the Kalamazoo-based Upjohn Pharmaceuticals a decade prior, the State of Michigan created the Southwest Michigan Innovation Center in an effort to retain the skilled workforce that had built up over previous generations. Issuing $2 million in grant money, the State allowed 11 new corporations to spin off from the Pfizer-Pharmacia merger, defraying job losses and stemming relocation. Today seven of those companies are still in Kalamazoo, five of which remain in the Southwest Innovation Center.

Upjohn PharmaceuticalsPackaging c.1960

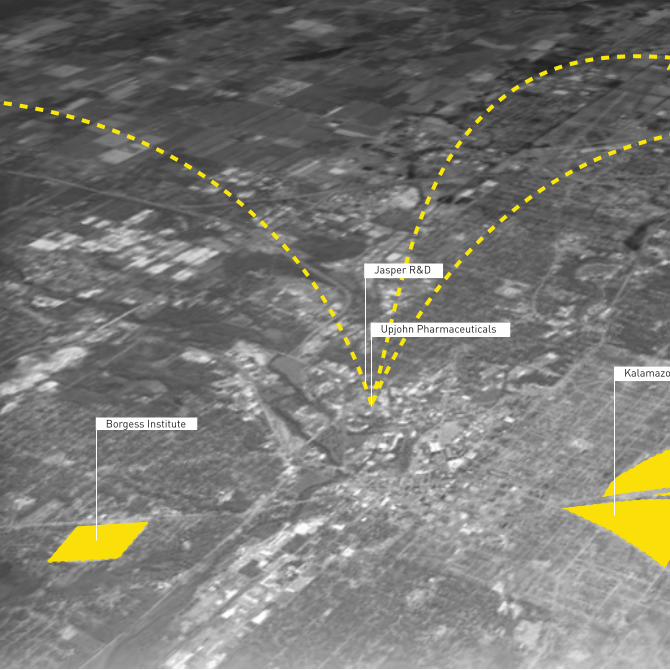

Jasper R&D

Borgess Institute

Upjohn Pharmaceuticals

Kalamazoo College

23

ProteusCeetoxKalexsynAmphibioticsAdmetrx

Pfizer Manufacturing

Western Michigan University

Southwest Innovation Center

Kalamazoo State Hospital

Kalamazoo College

Kalamazoo MI

The trajectory of Kalamazoo is a useful case study in the evolution of the pharmaceutical industry over the past century. Founded by William Upjohn in 1885 following his discovery of the friable pill – the world’s first pill that was easily dissolved in a patient’s stomach – Upjohn Pharmaceuticals grew rapidly throughout the first half of the 20th century, eventually becoming the 6th largest pharmaceutical manufacturing in the world. Despite its growth, Upjohn remained an integral part of the local community in part because the company remained under family control until 1968. Upjohn himself was elected the city’s first mayor after helping incorporate the city, and later established the Upjohn Institute for Employment Research to help train and find employment for the local labor force. To this day, he is known as Kalamazoo’s “first citizen.”

However, the very attributes that led to the company’s favorability with its customers and community proved to be its undoing. Toward the latter half of the 20th century the company suffered a series of blows in the form of diminished market share and legal confrontation. Its inability to remain competitive in a globalizing market eventually led to its merger with Pharmacia in 199518, which was accompanied by massive layoffs and the outsourcing of jobs. From 2000 to 2005, the global outsourcing market for pharmaceutical services compounded annually at an average rate of 8.37%, with an estimated total market size of $60 billion.19 Increased pressure to reduce overhead costs has deployed an army of specialized companies, often spun off from mergers which redistributed operations.

Today, every job at the Pfizer manufacturing plant in Kalamazoo supports an additional 1.6 jobs in the region.20 In 2002, Pharmacia employed 6,200 employees at the plant resulting in a total of 16,120 jobs associated with the company’s presence. Today, there are only 3,400 jobs supporting an additional 5,300 workers in region. This precipitous drop in labor suggests a sagging local economy. However, as home to numerous hospitals and universities, as well as start-up specialty biotechnology firms, Kalamazoo is actually a remarkable example of a niche knowledge economy. Thus, it can be said that Kalamazoo’s knowledge economy exists today because of its manufacturing sector, but also that it’s manufacturing sector remains today because it is closely tied to Kalamazoo’s research institutions.

25

Upjohn PharmaceuticalsAdvertisement c. 1960

While globalization has encouraged the spread of ideas and information democratically, business continues to look toward the networks and relationships it can make through strategic alignments, not only in terms of where it locates research facilities, but also in the partnerships it forms with other organizations. The pharmaceutical industry has a history of pairing with higher education institutions to spark and further research. This occurs in very deliberate ways, including the sharing of clinical data, but also through less tangible structures, such as locating facilities in institution formed intellectually rich areas. These partnerships have helped to produce research about

“Human Creativity is the ultimate economic resource.”21

27

Upjohn PharmaceuticalsManufacturing Line c. 1960

Washington University in St. Louis

Research University

Northwestern University

Cleveland Clinic

Southern Illinois University

Mayo Clinic

University of Illinois at Chicago

University of Wisconsin - Madison

Albany Medical College

Upstate Medical University

Northeastern Ohio Universities

University of McGill

University of Pittsburgh

Ohio State University

University of Minnesota - Twin Cities

Michigan State University

Rush University Medical Center

Rosalind Franklin University

Universite de Montreal

University of Chicago

University of Cincinnati

Saint Louis University

Loyola University - Chicago

Southern Illinois - Carbondale

Queen’s University

$365,408,802

Medical

$0

Pharmacology

$154,467,225 $3,789,023

$77,652,636

$11,312,812

$13,440,114

$2,053,431

$6,609,010

$64,875,000

$1,233,592

$1,072,085

$0

$184,008,362 $0

$84,905,812

$134,897,035 $4,612,350

$21,990,853

$0

$11,330,083

$1,894,240

$952,152

$15,635,000

$0

$0

$332,503,441 $10,784,022

$108,189,681

$140,811,670 $7,351,425

$49,869,302

$4,228,977

$12,875,765

$663,119

$2,463,737

$34,234,000

$2,269,207

$0

$0

$167,774,604 $12,277,655

$91,763,617

$2,770,555

$23,132,283

$2,611,898

$7,998,216

$1,852,037

$325,623,858 $10,861,595

$99,124,848

$141,020,100 $6,781,966

$33,475,539

$2,863,320

$12,941,839

$1,595,150

$1,648,419

$25,852,000

$0

$0

$173,664,346 $0

$88,207,437

$4,186,249

$15,147,315

$554,073

$7,858,974

$149,578,000

$0

$1,726,436

$0

University of Michigan

Indiana University - Purdue University

Case Western Reserve University

Wayne State University

Wright State University

University of Toronto

University of Rochester

Medical College of Wisconsin

University of Toledo

SUNY - Buffalo

University of Illinois Urbana

University of Western Ontario

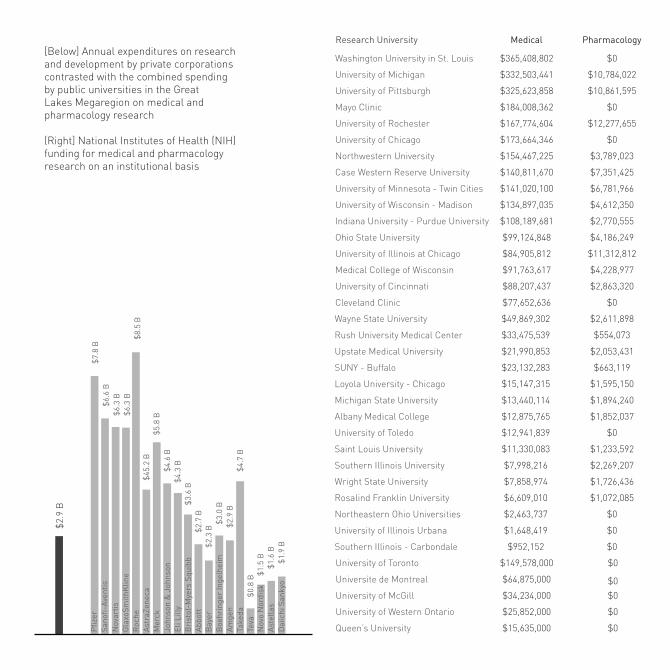

[Below] Annual expenditures on research and development by private corporations contrasted with the combined spending by public universities in the Great Lakes Megaregion on medical and pharmacology research

(Right] National Institutes of Health (NIH) funding for medical and pharmacology research on an institutional basis

Pfiz

erSa

nofi-

Aven

tisN

ovar

tisG

laxo

Smith

Klin

eR

oche

Ast

raZe

neca

Mer

ckJo

hnso

n &

Joh

nson

Eli L

illy

Bri

stol

-Mye

rs S

quib

bA

bbot

tB

ayer

Boe

hrin

ger

Inge

lhei

mA

mge

nTa

keda

Teva

Nov

o N

ordi

skA

stel

las

Dai

ichi

San

kyo

$7.8

B$6

.6 B

$8.5

B

$6.3

B$6

.3 B

$45.

2 B

$5.8

B$4

.6 B

$4.3

B$3

.6 B

$2.7

B$2

.3 B

$3.0

B$2

.9 B

$4.7

B$0

.8 B

$1.5

B$1

.6 B

$1.9

B

$2.9

B

29

pharmacology and how to foster the development of new breakthrough drugs, which the industry is dependent upon financially. The symbiosis of these relationships is what continues to breed such associations. A university desires companies to help it fund its endowment, support its research, and hire its graduates all while advancing the institution’s aim of increasing knowledge for the public benefit. Meanwhile, the corporations desire the intellectual capital that these educational institutions produce in the form of both discoveries and researchers. The Great Lakes Megaregion has long been the home to strong educational institutions. In 1862, the Morrill Act started what we now know as the “land grant” institution with the formation of Michigan State University, the first public research institution of its kind.22 In more recent years, the CIC, or Committee on Institutional Cooperation, formed to promote the cooperation

Upjohn PharmaceuticalsCafeteria c.1960

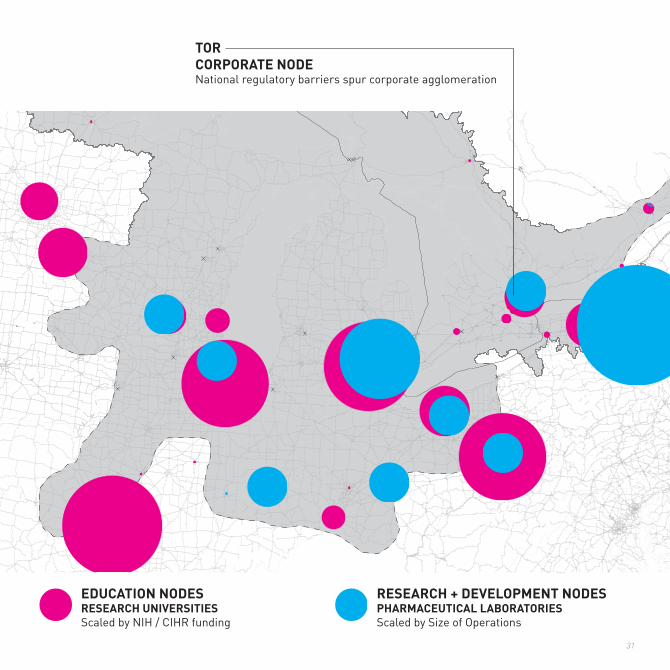

of these research institutions. An organization that mirrors the membership of the Great Lakes’ Big Ten athletics conference with the inclusion of the University of Chicago, the consortium is responsible for over $7 billion in research.23 The University of Michigan alone funds $1.0 billion in research, second in the United States.24 The CIC’s 33,945 faculty members and 98,456 graduate students contribute to the intellectual development within the Megaregion.25 These member organizations are also responsible for a fifth of the nation’s doctoral degrees.26 The power and scale of this consortium helps to evaluate the strength of the research institutions within the region in context to the greater continent. “With 33 percent of the U.S. population, the Great Lakes states produce 38 percent of the country’s bachelor degree holders, 36 percent of all science and engineering degrees, and 37 percent of all advanced science and engineering degrees, far outstripping any other region of the country.”27 The Megaregion and its educational institutions contribute directly to the economic output of the region by generating a large number of educated citizens that are then employed by the pharmaceutical industry. It is not only the sheer quantity of research occurring at these institutions which contributes to the presence of pharmaceutical operations in the region, but also the specificity and strength of the particular programs. The Megaregion is home to the leading recipients of national medical research grants in both Canada and the United States. The University of Michigan, University of Pittsburgh, and Washington University in Saint Louis are all among the top ten recipients of National Institutes of Health funding.28 In Canada, the University of Toronto tops research funding by the Canadian Institutes of Health Research grants to faculties of medicine.29 Furthermore, the Megaregion contains six of the top ten pharmacology programs in the United States.30 This investment in medical research contributes to the pharmaceutical industry’s efforts to produce new drugs. Through the understanding of disease and disorder, which occurs in these programs, pharmaceutical researchers are able to passively outsource work in order to understand these conditions better and thus develop medicines to treat them. Research universities are beneficial to the pharmaceutical drug development pipeline as they help both in the development of drugs and the associated clinical research necessary to understand the effects of these compounds. These particular strengths make the region apt for

31

Distribution

Corporate

Research + Development

Research University Medical Schools

Machinery Manufacturing Plants

Chemical Raw Materials Production

PHARMACEUTICAL INDUSTRY/

Manufacturing

RESEARCH + DEVELOPMENT NODESPHARMACEUTICAL LABORATORIESScaled by Size of Operations

EDUCATION NODESRESEARCH UNIVERSITIESScaled by NIH / CIHR funding

TORCORPORATE NODENational regulatory barriers spur corporate agglomeration

locating research and development facilities in the region. Research within the institutional context is commonly bought, if not shared, and used to help advance pharmacology within the research and development arms of major pharmaceutical corporations. In terms of drug patents, “public research maintains an important role in establishing the grounds for patent applications. Some 50 percent of scientific references in drug and medicine submissions to the patents were to U.S. public science, and 33 percent to foreign science, most of which is also public. Only 17 percent of scientific references were to U.S. drug industry papers.”31 Therefore, research institutions play a large role in the groundwork research that goes into the development of breakthrough drugs. As a result, the private sector is required to pick up where university researchers complete their research. Along these lines, Pfizer’s Investigator-Initiated Research (IIR) seeks public sector research that opens up new avenues for current drugs to continually be refined. This takes research pressure and expense away from the corporation. It also fosters innovation in terms of new uses for existing drugs. Furthermore, smaller inter-University partnerships help to create a more knowledgeable workforce within the region. With higher caliber graduates, the region seeks to remain an attractive location for businesses to grow. Pharmaceutical corporations seek to attract these graduates as the industry is both highly competitive, but also very intelligence intensive, meaning the research and development process requires a large number of highly trained scientists. The collaboration between these schools and the pharmaceutical research that occurs within the Megaregion reinforces the strength of the region. The graduates from these institutions are then more valuable for the aforementioned pharmaceutical corporations. The University Research Corridor, a collaboration between Michigan State University, the University of Michigan, and Wayne State University, seeks to leverage the capacity of these institutions to lure research funding and support.32 The Great Lakes Megaregion is dealing with issues of out-migration as young, educated workers leave for other regions of the continent. As the agricultural and industrial economies continue to downsize, the retention of this demographic becomes increasingly important in reshaping the Megaregion’s economy.33

Another instance of public-private partnership between research institutions occurs through the formation of incubators for innovation startup companies. “Based on the results of

33

a survey of 62 U.S. universities, 19 observe that, at the time they are licensed, most university inventions are little more than a “proof of concept” with unknown commercial potential, and technically so embryonic that additional effort by the inventor is required.”34 Bioscience companies, not only pharmaceutical in focus, work to take the ideas generated at these research institutions and turn them into marketable products. The MaRS [Medical and Related Sciences] Development District adjacent to the campus of the University of Toronto is an example of this type of collaboration. The District intends to be an incubator for science and technology startup companies and aims to foster collaboration between the various biosciences. The only two corporate founders of the partnership are two global pharmaceutical corporations, AstraZeneca and Eli Lilly.35 Both corporations have operations in the Greater Toronto Area and elsewhere in the Megaregion. Not only is their funding crucial to the success of this innovation engine, but their continued support establishes a pipeline from a burgeoning outsourced research farm. Similarly, on the other side of the border, research at the University of Michigan has spawned 93 startup companies in the past ten years.36 This helps to retain and increase the intellectual talent base in the region, strengthening the coordination between pharmaceutical companies and other associated industries in the technology and bioscience fields. This type of consequential impact is what makes the research institution an important ally for pharmaceutical companies. Besides the tangible outcomes of partnerships such as these, pharmaceutical companies also stand to gain brand awareness and respect. In a society where corporate concern about brand loyalty is a necessity, the promotion of public ventures seeks to make these companies good corporate citizens. This creates passive advertising for their brands and the drugs themselves.

Through the complexity of the network and relationships spurred by the pharmaceutical industry, Big Pharma capitalizes on the knowledge economy that has been created by the research institutions of the Great Lakes Megaregion. Research and development jobs are highly coveted for communities in the Megaregion. These jobs typically pay well, are more difficult to outsource, have high opportunity for growth and require large capital investment by the lead corporation. The future for the pharmaceutical industry in the Great Lakes Megaregion will depend on the extent to which pharmaceutical corporations take advantage of the Megaregion’s inherent institutional advantages.

“Most of the time, we live our lives within these invisible systems, blissfully unaware of the artificial life, the intensely designed infrastructures that support them.”37

Information technology and globalization has allowed for the development of just-in-time logistics networks. This has radically changed industrial processes overall, including the pharmaceutical industry. Through the distribution, delivery and consumption of these goods,38 new practices have developed to streamline the manufacturing process of FDA approved drugs following research and development. This highly calculated supply chain reinforces the inherent conditions within the Great Lakes Megaregion that have contributed to the development of the industry. The manufacturing of pharmaceutical drugs provides a lens to view the logistics relationship of the industry

35

McKesson PharmaceuticalDistribution Center c. 2011

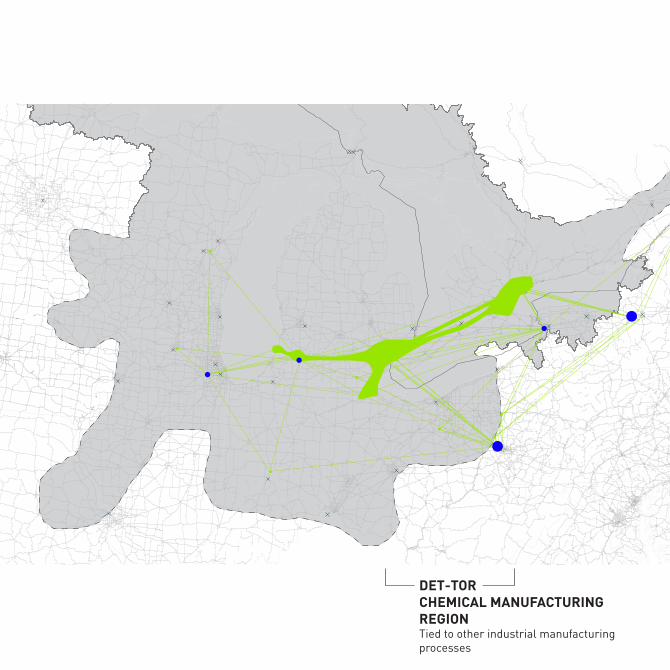

Distribution

Corporate

Research + Development

Research University Medical Schools

Machinery Manufacturing Plants

Chemical Raw Materials Production

PHARMACEUTICAL INDUSTRY/

DET-TORCHEMICAL MANUFACTURING REGIONTied to other industrial manufacturing processes

37

Distribution

Corporate

Research + Development

Research University Medical Schools

Machinery Manufacturing Plants

Chemical Raw Materials Production

PHARMACEUTICAL INDUSTRY/

Manufacturing

MSP-MIL-CHIMANUFACTURING REGIONLarge Scale Stainless Steel Manufacturing EquipmentDeveloped for the agricultural economy in the Megaregion and adapted for the Pharmaceutical Industry

CLE-PITMANUFACTURING REGIONIndustrial Parts / Lab and Safety EquipmentRemnant from the Automobile Industry / Supplier of Research Insitutions

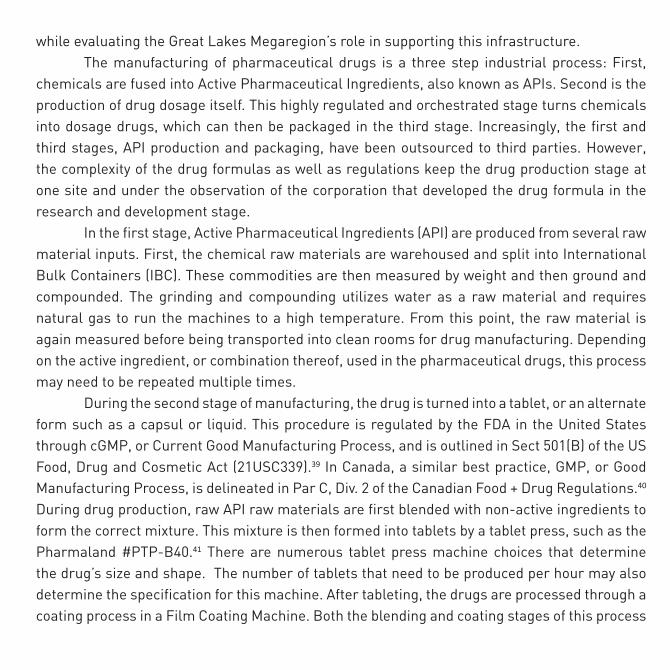

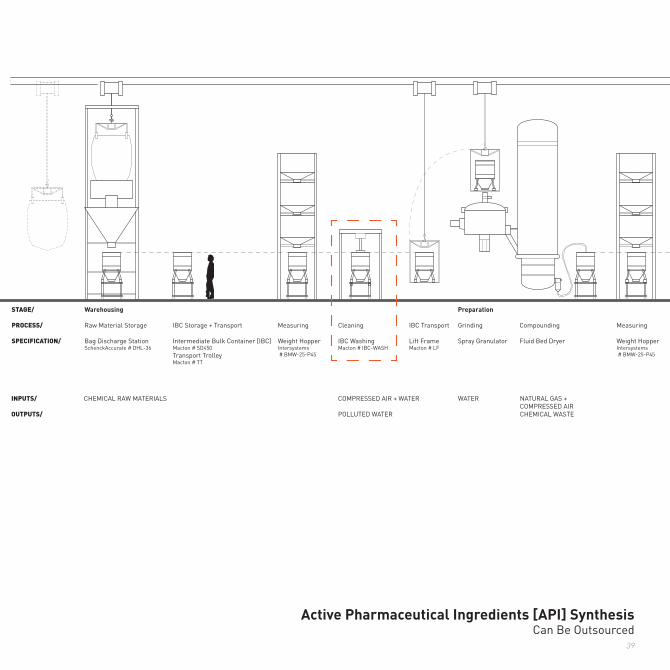

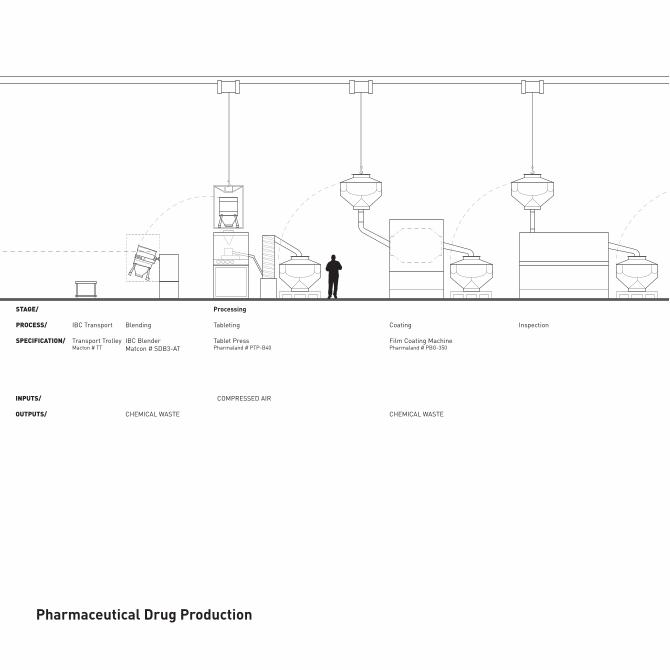

while evaluating the Great Lakes Megaregion’s role in supporting this infrastructure. The manufacturing of pharmaceutical drugs is a three step industrial process: First, chemicals are fused into Active Pharmaceutical Ingredients, also known as APIs. Second is the production of drug dosage itself. This highly regulated and orchestrated stage turns chemicals into dosage drugs, which can then be packaged in the third stage. Increasingly, the first and third stages, API production and packaging, have been outsourced to third parties. However, the complexity of the drug formulas as well as regulations keep the drug production stage at one site and under the observation of the corporation that developed the drug formula in the research and development stage. In the first stage, Active Pharmaceutical Ingredients (API) are produced from several raw material inputs. First, the chemical raw materials are warehoused and split into International Bulk Containers (IBC). These commodities are then measured by weight and then ground and compounded. The grinding and compounding utilizes water as a raw material and requires natural gas to run the machines to a high temperature. From this point, the raw material is again measured before being transported into clean rooms for drug manufacturing. Depending on the active ingredient, or combination thereof, used in the pharmaceutical drugs, this process may need to be repeated multiple times. During the second stage of manufacturing, the drug is turned into a tablet, or an alternate form such as a capsul or liquid. This procedure is regulated by the FDA in the United States through cGMP, or Current Good Manufacturing Process, and is outlined in Sect 501(B) of the US Food, Drug and Cosmetic Act (21USC339).39 In Canada, a similar best practice, GMP, or Good Manufacturing Process, is delineated in Par C, Div. 2 of the Canadian Food + Drug Regulations.40 During drug production, raw API raw materials are first blended with non-active ingredients to form the correct mixture. This mixture is then formed into tablets by a tablet press, such as the Pharmaland #PTP-B40.41 There are numerous tablet press machine choices that determine the drug’s size and shape. The number of tablets that need to be produced per hour may also determine the specification for this machine. After tableting, the drugs are processed through a coating process in a Film Coating Machine. Both the blending and coating stages of this process

39

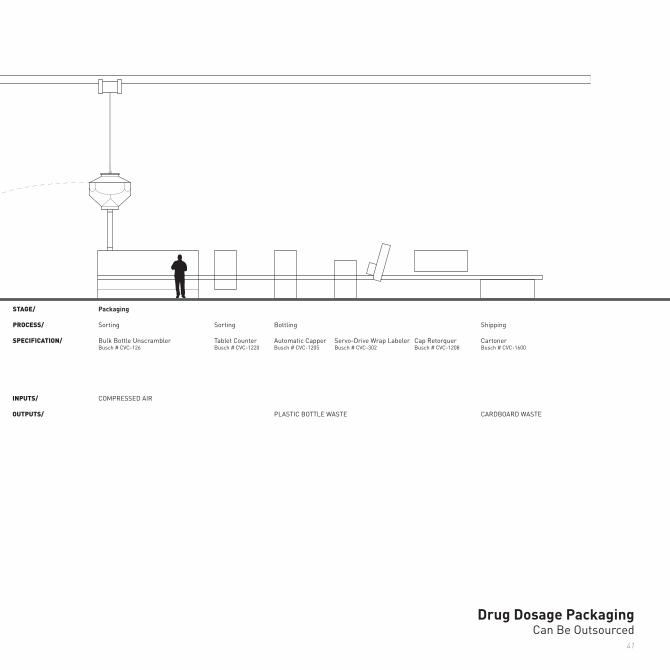

STAGE/

PROCESS/

SPECIFICATION/

Warehousing

Raw Material Storage

Bag Discharge StationSchenckAccurate # DHL-36

IBC Storage + Transport

Intermediate Bulk Container [IBC]Macton # SD450Transport Trolley Macton # TT

IBC Transport

Lift FrameMacton # LF

Measuring

Weight HopperIntersystems # BMW-25-P45

Measuring

Weight HopperIntersystems # BMW-25-P45

Cleaning

IBC WashingMacton # IBC-WASH

Compounding

Fluid Bed Dryer

Preparation

Grinding

Spray Granulator

INPUTS/

OUTPUTS/

COMPRESSED AIR + WATER

POLLUTED WATER

CHEMICAL RAW MATERIALS WATER NATURAL GAS +COMPRESSED AIRCHEMICAL WASTE

Active Pharmaceutical Ingredients [API] SynthesisCan Be Outsourced

STAGE/

PROCESS/

SPECIFICATION/

IBC Transport

Transport Trolley Macton # TT

Blending

IBC BlenderMatcon # SDB3-AT

Processing

Tableting

Tablet PressPharmaland # PTP-B40

Coating

Film Coating MachinePharmaland # PBG-350

Inspection

INPUTS/

OUTPUTS/ CHEMICAL WASTE

CHEMICAL WASTE

COMPRESSED AIR

Pharmaceutical Drug Production

41

Packaging

Sorting

Bulk Bottle UnscramblerBusch # CVC-126

Shipping

CartonerBusch # CVC-1600

Cap RetorquerBusch # CVC-1208

Servo-Drive Wrap LabelerBusch # CVC-302

Sorting

Tablet CounterBusch # CVC-1220

Bottling

Automatic CapperBusch # CVC-1205

STAGE/

PROCESS/

SPECIFICATION/

INPUTS/

OUTPUTS/ PLASTIC BOTTLE WASTE CARDBOARD WASTE

COMPRESSED AIR

Drug Dosage PackagingCan Be Outsourced

Distribution

Corporate

Research + Development

Research University Medical Schools

Machinery Manufacturing Plants

Chemical Raw Materials Production

PHARMACEUTICAL INDUSTRY/

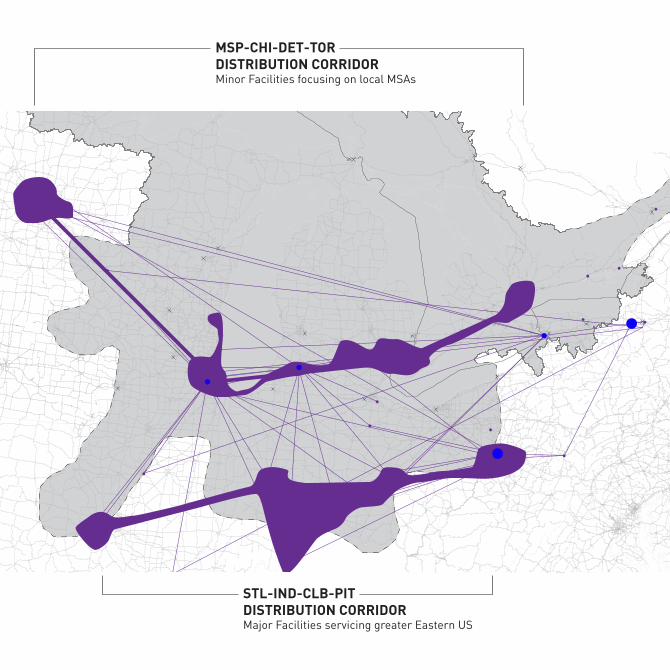

STL-IND-CLB-PITDISTRIBUTION CORRIDORMajor Facilities servicing greater Eastern US

MSP-CHI-DET-TORDISTRIBUTION CORRIDORMinor Facilities focusing on local MSAs

43

produce a chemical waste byproduct. Following inspection of the drug tablets, the tablets are then sorted and bottled. Bottles are then labeled, sealed and packaged for shipping. Like API production, the third stage, the packaging of pharmaceutical drugs, is increasingly occurring off site at consolidated logistics sites as this phase is not governed by the same rules and regulations as the manufacturing of the drugs themselves.

“Information technologies enable firms to disperse a growing range of their operations, whether at the metro, regional, or global level without losing system integration.”42 The logistics landscape of the industry is fully deployed in the distribution system. Three main corporations control this segment of the industry: Cardinal Health, McKesson, and AmerisourceBergen. All three companies have significant operations within the Megaregion, including the Canadian headquarters for all three companies, Cardinal Health’s headquarters and main logistics operations outside Columbus, Ohio, and distribution centers for all three in the low cost warehouse-filled exurbs of the region. These distribution centers are primarily located in the southern reaches of the Great Lakes Megaregion, centered around Columbus, Cincinnati, Louisville, Indianapolis, and Saint Louis. These locations take advantage of greater strategic location on the interstate highway system in order to reach a larger swath of the country. Additionally, they access lower cost labor pools and land area implicated in these operations. “For most of us, design is invisible until it fails.”43These logistical networks are not always precise. The downside of a seamless transportation network such as this are the cases of overlooked contents and deliveries of unintended packages. This was the case in Cascade Township, Michigan in 2007. The freight carrier DHL delivered a persevered body part and a portion of a human head to an unexpecting couple at their home outside of Grand Rapids. The contents, along with 27 other packages were en route from China to an unknown destination. “Most of the time, we live our lives within these invisible systems, blissfully unaware of the artificial life, the intensely designed infrastructures that support them.”44

The distribution corporation’s game is to get drugs through their just-in-time logistics networks to reach the final point of consumer purchase, the ubiquitous pharmacy. As the

number of Americans who take prescription drugs and the quantity of these drugs continues to grow, the pharmacy becomes an increasingly common retail type. The prevalence of the modern chain “corner” drug store has propelled Walgreen’s, CVS, and Rite Aid into the lexicon of American consumer behavior. Seventy-five percent of Americans live within three miles of a CVS pharmacy. Through looking at case study examples in Mississauga, Ontario and Kalamazoo, Michigan, we can observe the ways in which this logistics landscape reinforces the methods by which corporations make decisions to locate various parts of their corporations and derive just-in-time strategies within their supply chains. In Kalamazoo, a research institution and associated public-private business incubator has encouraged pharmaceutical corporations to remain in the area. Various portions of the supply chain, including manufacturing, have chosen to remain there. This is further reinforced by local tax subsidies for these corporations as well as less tangible benefits of developing a local knowledge economy through a program such as the Kalamazoo Promise, which pays for local students to go to college.45 The situation in Mississauga relates directly to the development of agglomeration economies. The dispersal of the logistical networks through the Megaregion forces the concentration of specialized higher tier processes, such as corporate functions. As Toronto has emerged as a global city, it has developed a specialty catering to the pharmaceutical industry apparent in Mississauga’s role as the center of Canadian corporate pharmaceutical operations. All the aforementioned locations in the Great Lakes Megaregion exist within a larger global framework. The region is organized around the Chicago-Detroit-Toronto corridor and the infrastructure that ties these three dominant areas together. Each of these three cities also sits prominently within the wider global aviation infrastructure as major hubs for North American Airlines at ORD, DTW and YYZ. From these three cities combined, nonstop flights are available to most major cities on the five continents.

45

75% of Americans live within

3 miles of a CVS

Pharmacy

Illinois

Walgreens

574

200

224

144

453

251

117

222

CVS Caremark

261

290

243

42

445

313

384

32

Rite Aid

0

10

284

0

640

229

557

0

Walmart

178

119

115

74

111

173

151

96

Kroger

61

144

134

0

0

212

0

0

Indiana

Michigan

Minnesota

New York

Ohio

Pennsylvania

Wisconsin

47

In recent years, the term rust belt has been applied to the Great Lakes Megaregion to characterize the dismantling of formerly rich manufacturing industries. Much speculation has gone into the future of this region economically, particularly as the automotive industry is forced to retool their business model and associated industries downsize in response. This provides for an opportunity for other industries to seize the capacities created by this pre-existing manufacturing infrastructure. Inherently, the downfall of these older industries does not encourage investment in pharmaceutical industry facilities within the region. However, through strategic partnership with existing strong research institutions, acting upon tax subsidies, and being aware of the development of specialization through agglomeration economies, the pharmaceutical industry does not need to retreat, but instead retool as well to take advantage of the opportunities present within the region.

1 Jacobzone, S “Pharmaceutical Policies in OECD Countries: Reconciling Social and Industrial Goals.” Labour Market and Social Policy, Occasional Paper No. 40. (2000) 2 Pazderka, B. and Stegemann, K. “Patent Policy and the Diffusion of Pharmaceutical Innovation.” Queens University. 2005. <http://www.ic.gc.ca/eic/site/ippd-dppi.nsf/vwapj/05%20EN%20V2%20%20Pazderka-Stegeman.pdf/$FILE/05%20EN%20V2%20%20Pazderka-Stegeman.pdf>. 3 Arundel, Anthony, and Isabelle Kabla. “What Percentage of Innovations Are Patented? Empirical Estimates for European Firms.” Research Policy 27, 2 (1998): 127-141. 4 Robert Langton, “Global Patent Rights in Pharmaceuticals: The Impact of the Trips Agreement,” The Global Studies Journal 2:1 (2009): 30. 5 Smith, R., Correa, C., and Oh, C. “Trade, TRIPS and pharmaceuticals.” Trade and Health, Lancet 373 (2009): 684–91. 6 Clinton, P and Mozeson, M. “PharmExec Top 50 2010.” Last modified: May 1, 2010 Accessed April 2, 2011. <http://www.scribd.com/doc/50145456/Pharm-Exec-Top-50-2010>. 7 Needs Citation. 8 City of Mississauga. “Mississauga Taxes and Assessment.” Modfied: Ju;ly 2010. Accessed March 15, 2011. <http://www.mississauga.ca/file/COM/Taxes___Assessment_July_2010.pdf>. 9 Sassen, Saskia S. "Megaregions: Benefits beyond Sharing Trains and Parking Lots?" The Economic Georgraphy of Megaregions (2007): 59-83. Policy Research Institute for the Region at the Woodrow Wilson School of Public and International Affairs, Princeton University and the Regional Plan Association, 2007. <http://wws.princeton.edu/research/prior-publications/conference-books/megaregions.pdf>. 10 Law, Anne. "Pfizer and Wyeth Merger — Could It Be True (love)?" Bizmology.com. 23 Feb. 2009. Web. 13 Apr. 2011. <http://www.bizmology.com/2009/01/23/pfizer-and-wyeth-merger-could-it-be-true-love/>. 11 Pettypiece, Shannon. "Pfizer Cuts Research Operations After Wyeth Deal." Bloomberg - Business & Financial News. 9 Nov. 2009. Web. 13 Apr. 2011. <http://www.bloomberg.com/apps/news?pid=newsarchive>. 12 Singer. N, “Merck to Buy Schering-Plough for $41.1 Billion,” New York Times, March 9, 2009, accessed March 24, 2011, <http://www.nytimes.com/2009/03/10/business/10drug.html>. 13 “Global Pharmaceutical Market.” Last modified 2011. <http://www.checkonomics.com/IndustryOverview.aspx?IID=51&CAT=106CC604&IName=Pharmaceuticals&CatName=Global%20Market>. 14 Clinton, P and Mozeson, M. “PharmExec Top 50 2010.” Last modified: May 1, 2010 Accessed April 2, 2011. <http://www.scribd.com/doc/50145456/Pharm-Exec-Top-50-2010>. 15 Milanese, R. “Overview of North American Generic Market.” Presentation June 19, 2005 Accessed April 3, 2011. <http://www.anapharm.com/site/upload/site/Generateur/RobertMilanese_Overview.pdf>. 16 “Top Selling Brand Drugs Patent Protetions About to Expire” Phillyburb.com March 3 2011. Accessed March 31, 2011. <http://www.phillyburbs.com/blogs/working_my_butt/top-selling-brand-drugs-patent-protections-about-to-expire/article_0b537286-45ae-11e0-abd4-0017a4a78c22.html>. 17 Arnst, C. “Pfizer-Wyeth Merger Isn’t a Cure-All. Bloomberg Businessweek. January 24, 2009. Accessed March 31, 2011. <http://www.businessweek.com/technology/content/jan2009/tc20090123_516076.htm>. 18 Ackerman, L. “Identity is Destiny: Leadership and the Roots of Value Creation.” (San FranciscoL Berrett-Koehler Publishers: 2000) 82-102. 19 “Global Pharmaceutical Market.” Last modified 2011. <http://www.checkonomics.com/IndustryOverview.aspx?IID=51&CAT=106CC604&IName=Pharmaceuticals&CatName=Global%20Market>. 20 Jones. A “Pfizer’s Impact on Southeast Michigan $767.5 million, economic think tank finds.” Kalamazoo Gazette. August 26, 2010. Accessed March 31, 2011. <http://www.mlive.com/business/west-michigan/index.ssf/2010/08/pfizers_impact_on_southwest_mi.html>. 21 Florida, Richard L. The Rise of the Creative Class: and How It's Transforming Work, Leisure, Community and Everyday Life. New York, NY: Basic, 2004. Print. 22 "MSU Facts | Michigan State University." Michigan State University. Est. 1855. East Lansing, Michigan USA. Web. 6 Apr. 2011. <http://www.msu.edu/about/thisismsu/facts.html>.

49

1 Jacobzone, S “Pharmaceutical Policies in OECD Countries: Reconciling Social and Industrial Goals.” Labour Market and Social Policy, Occasional Paper No. 40. (2000) 2 Pazderka, B. and Stegemann, K. “Patent Policy and the Diffusion of Pharmaceutical Innovation.” Queens University. 2005. <http://www.ic.gc.ca/eic/site/ippd-dppi.nsf/vwapj/05%20EN%20V2%20%20Pazderka-Stegeman.pdf/$FILE/05%20EN%20V2%20%20Pazderka-Stegeman.pdf>. 3 Arundel, Anthony, and Isabelle Kabla. “What Percentage of Innovations Are Patented? Empirical Estimates for European Firms.” Research Policy 27, 2 (1998): 127-141. 4 Robert Langton, “Global Patent Rights in Pharmaceuticals: The Impact of the Trips Agreement,” The Global Studies Journal 2:1 (2009): 30. 5 Smith, R., Correa, C., and Oh, C. “Trade, TRIPS and pharmaceuticals.” Trade and Health, Lancet 373 (2009): 684–91. 6 Clinton, P and Mozeson, M. “PharmExec Top 50 2010.” Last modified: May 1, 2010 Accessed April 2, 2011. <http://www.scribd.com/doc/50145456/Pharm-Exec-Top-50-2010>. 7 Needs Citation. 8 City of Mississauga. “Mississauga Taxes and Assessment.” Modfied: Ju;ly 2010. Accessed March 15, 2011. <http://www.mississauga.ca/file/COM/Taxes___Assessment_July_2010.pdf>. 9 Sassen, Saskia S. "Megaregions: Benefits beyond Sharing Trains and Parking Lots?" The Economic Georgraphy of Megaregions (2007): 59-83. Policy Research Institute for the Region at the Woodrow Wilson School of Public and International Affairs, Princeton University and the Regional Plan Association, 2007. <http://wws.princeton.edu/research/prior-publications/conference-books/megaregions.pdf>. 10 Law, Anne. "Pfizer and Wyeth Merger — Could It Be True (love)?" Bizmology.com. 23 Feb. 2009. Web. 13 Apr. 2011. <http://www.bizmology.com/2009/01/23/pfizer-and-wyeth-merger-could-it-be-true-love/>. 11 Pettypiece, Shannon. "Pfizer Cuts Research Operations After Wyeth Deal." Bloomberg - Business & Financial News. 9 Nov. 2009. Web. 13 Apr. 2011. <http://www.bloomberg.com/apps/news?pid=newsarchive>. 12 Singer. N, “Merck to Buy Schering-Plough for $41.1 Billion,” New York Times, March 9, 2009, accessed March 24, 2011, <http://www.nytimes.com/2009/03/10/business/10drug.html>. 13 “Global Pharmaceutical Market.” Last modified 2011. <http://www.checkonomics.com/IndustryOverview.aspx?IID=51&CAT=106CC604&IName=Pharmaceuticals&CatName=Global%20Market>. 14 Clinton, P and Mozeson, M. “PharmExec Top 50 2010.” Last modified: May 1, 2010 Accessed April 2, 2011. <http://www.scribd.com/doc/50145456/Pharm-Exec-Top-50-2010>. 15 Milanese, R. “Overview of North American Generic Market.” Presentation June 19, 2005 Accessed April 3, 2011. <http://www.anapharm.com/site/upload/site/Generateur/RobertMilanese_Overview.pdf>. 16 “Top Selling Brand Drugs Patent Protetions About to Expire” Phillyburb.com March 3 2011. Accessed March 31, 2011. <http://www.phillyburbs.com/blogs/working_my_butt/top-selling-brand-drugs-patent-protections-about-to-expire/article_0b537286-45ae-11e0-abd4-0017a4a78c22.html>. 17 Arnst, C. “Pfizer-Wyeth Merger Isn’t a Cure-All. Bloomberg Businessweek. January 24, 2009. Accessed March 31, 2011. <http://www.businessweek.com/technology/content/jan2009/tc20090123_516076.htm>. 18 Ackerman, L. “Identity is Destiny: Leadership and the Roots of Value Creation.” (San FranciscoL Berrett-Koehler Publishers: 2000) 82-102. 19 “Global Pharmaceutical Market.” Last modified 2011. <http://www.checkonomics.com/IndustryOverview.aspx?IID=51&CAT=106CC604&IName=Pharmaceuticals&CatName=Global%20Market>. 20 Jones. A “Pfizer’s Impact on Southeast Michigan $767.5 million, economic think tank finds.” Kalamazoo Gazette. August 26, 2010. Accessed March 31, 2011. <http://www.mlive.com/business/west-michigan/index.ssf/2010/08/pfizers_impact_on_southwest_mi.html>. 21 Florida, Richard L. The Rise of the Creative Class: and How It's Transforming Work, Leisure, Community and Everyday Life. New York, NY: Basic, 2004. Print. 22 "MSU Facts | Michigan State University." Michigan State University. Est. 1855. East Lansing, Michigan USA. Web. 6 Apr. 2011. <http://www.msu.edu/about/thisismsu/facts.html>.

23 Committee on Institutional Cooperation. Committee on Institutional Cooperation. Annual Report 2009-10. Web. 1 Apr. 2011. <http://www.cic.net/Libraries/Reports/CIC_Annual_Report_2009-10.sflb.ashx>. 24 "Total NIH Awards to Each Medical School in 2010." Chart. Ranking Tables of NIH Funding to US Medical Schools in 2010. Blue Ridge Institute for Medical Research. Web. 23 Feb. 2011. <http://www.brimr.org/NIH_Awards/2010/NIH_Awards_2010.htm>. 25 Committee on Institutional Cooperation. 26 Duderstadt, James J. "A Master Plan for Higher Education in the Midwest: A Roadmap to the Future of the Nation’s Heartland." Heartland Papers (2011): 36. Reforming Higher Education to Compete in a Global Economy. The Chicago Council on Global Affairs, Mar. 2011. Web. 4 Apr. 2011. <http://www.thechicagocouncil.org/files/Event/FY11_Events/03_March_2011/Reforming_Higher_Education_to_Compete_in_the_Global_Economy.aspx>. 27 Duderstadt, 36. 28 "Total NIH Awards to Each Medical School in 2010." 29 "Biomedical and Health Care Research Revenues of Canadian Faculties of Medicine 2008/09." Chart. Association of Faculties of Medicine of Canada Office of Research and Information Services, June 2010. Web. 23 Feb. 2011. <http://www.afmc.ca/pdf/Revenues%202008-09.pdf>. 30 "Best Pharmacy Schools." Chart. Best Graduate Schools: Top Health Schools. US News and World Report, 2008. Web. 6 Apr. 2011. <http://grad-schools.usnews.rankingsandreviews.com/best-graduate-schools/top-health-schools/pharmacy-rankings>. 31 Needs Citation. 32 Simon, Lou Anna K., Mary Sue Coleman, and Irvin D. Reid. "URC Update Letter from the Presidents." Letter. 16 Apr. 2007. University Research Corridor. 16 Apr. 2007. Web. 4 Apr. 2011. <http://urcmich.org/who/update.html>. 33 Duderstadt, 30. 34 Richard Jensen & Jerry Thursby & Marie C. Thursby, 2010. "University-Industry Spillovers, Government Funding, and Industrial Consulting," NBER Working Papers 15732, National Bureau of Economic Research, Inc. 35 "Who Founded MaRS? – MaRS: Building Canada's next Generation of Growth Companies."MaRS Discovery District – MaRS: Building Canada's next Generation of Growth Companies. Web. 12 Apr. 2011. <http://www.marsdd.com/aboutmars/founders/>. 36 "North Campus Research Complex :: University of Michigan." University of Michigan Health System. Web. 5 Apr. 2011. <http://www.med.umich.edu/umrg/>. 37 Leonard, Jennifer, and Bruce Mau. Preface. Massive Change. London: Phaidon, 2004. Print. 38 Waldheim, Charles, and Alan Berger. "Logistics Landscape." Landscape Journal 27 (2008): 219-46. 2008. 39 FDA: Food, Drug and Cosmetic Act, 21USC339 § 501 (B) (2005). 40 Health Canada: Food + Drug Regulations, § Par C, Div. 2. 41 Pharmaceutical Machine Manufacturer: Machine Equipment / Packaging Machinery. Pharmaland. Web. 2 Feb. 2011. <http://pharmaland.ca/product/?lang=en>. 42 Sassen, 61. 43 Leonard and Mau. 44 Leonard and Mau. 45 The Kalamazoo Promise. Kalamazoo Promise. The Kalamazoo Promise: Information for Seniors & Parents. The Kalamazoo Public Schools. Web. 2 Apr. 2011. <https://www.kalamazoopromise.com/uploaded/Promise%20Senior%20Information%20Brochure.pdf>.