Embed Size (px)

Citation preview

LAN

D BA

NK of TA

IWA

N A

nnual Report 2011

Website:http://newmops.tse.com.tw

The Bank Website:http://www.landbank.com.tw

Time of Publication︰June 2012

Stock code:5857ISSN:1997-9053(Print) ISSN:1997-9061 (Online)

LAND BANK of TAIWAN Annual Report

Spokesman:Mr. Chen,Toong-Ming

Title : Executive Vice PresidentTel : (886)2-2348-3678

E-mail:[email protected]

First Substitute spokesman:Mr. Huang,Chung-Min

Title : Executive Vice PresidentTel : (886)2-2348-3366

E-mail:[email protected]

Second Substitute spokesman:Mr.Kao,Ming-HsienTitle : Executive Vice PresidentTel : (886)2-2348-3566E-mail:[email protected]

Address & Tel of the Bank's Head Office and Branches (Please refer to "Directory of LBOT's offices")

Credit rating agencies

Name : Moody's Investors ServiceAddress : 24/F One Pacific Place 88 Queensway

Admiralty, Hong KongTel : (852)37581330 Fax : (852)37581631

Web Site:http://www.moodys.com

Name:Standard & Poor's Corp.Address:The landmark, Edinburgh Tower 15 Queens

Road Central,Suite 3003, Hong KongTel:(852)25333500 Fax:(852)25333566

Web Site:http://www.standardandpoors.com

Name:Taiwan Ratings CorporationAddress:49Fl., No.7, Sec. 5, Xinyi Rd., Xinyi Dist.,

Taipei City 11049, Taiwan (R.O.C.)Tel:(886)2-8722-5800 Fax:(886)2-8722-5879

Web Site:http://www.taiwanratings.com

Stock transfer agencyName:Secretariat, Land Bank of Taiwan Co., Ltd.Address:3F., No.53, Huaining St., Zhongzheng Dist.,

Taipei City 10046, Taiwan (R.O.C.)Tel:(886)2-2348-3456 Fax:(886)2-2375-7023Web Site:http://www.landbank.com.tw

Certified Public Accountants of financial statements for the past year

Name of attesting CPAs:Andrew Fuh ,Daniel HsuName of Accounting Firm :Ernst & YoungAddress:9F., No.333, Sec. 1, Keelung Rd., Xinyi Dist.,

Taipei City 11012, Taiwan (R.O.C.)Tel : (886)2-2720-4000 Fax:(886)2-2757-6050Web Site:http://www.ey.com/taiwan

The Bank's Website:http://www.landbank.com.tw

Published by : Land Bank of Taiwan Co., Ltd

Time of Publication : June 2012

Land Bank of Taiwan Annual Report 2011Publisher : Land Bank of Taiwan Co., Ltd.

Address : No.46, Guanqian Rd., Taipei City

10047, Taiwan (R.O.C.)

Tel : (886) 2-2348-3456

Website : http://www.landbank.com.tw

Time of publication : June 2012

Time of first publication : June 1964

E-publication : This Annual Report is available

on the Bank website

Price:NT $600

GPN:2005300018

ISSN:1997-9053(Print)

1997-9061(Online)

Upon Taiwan’s centennial, we put on heart and soul,

With a perfect lineup, offering integrated banking service in full scale.

Upholding “abundance, harmony, sincerity, innovation” as core principles,

We stand in Taiwan, deploy over Asia, and aim for the World.

Land Bank deserves your upmost approval!

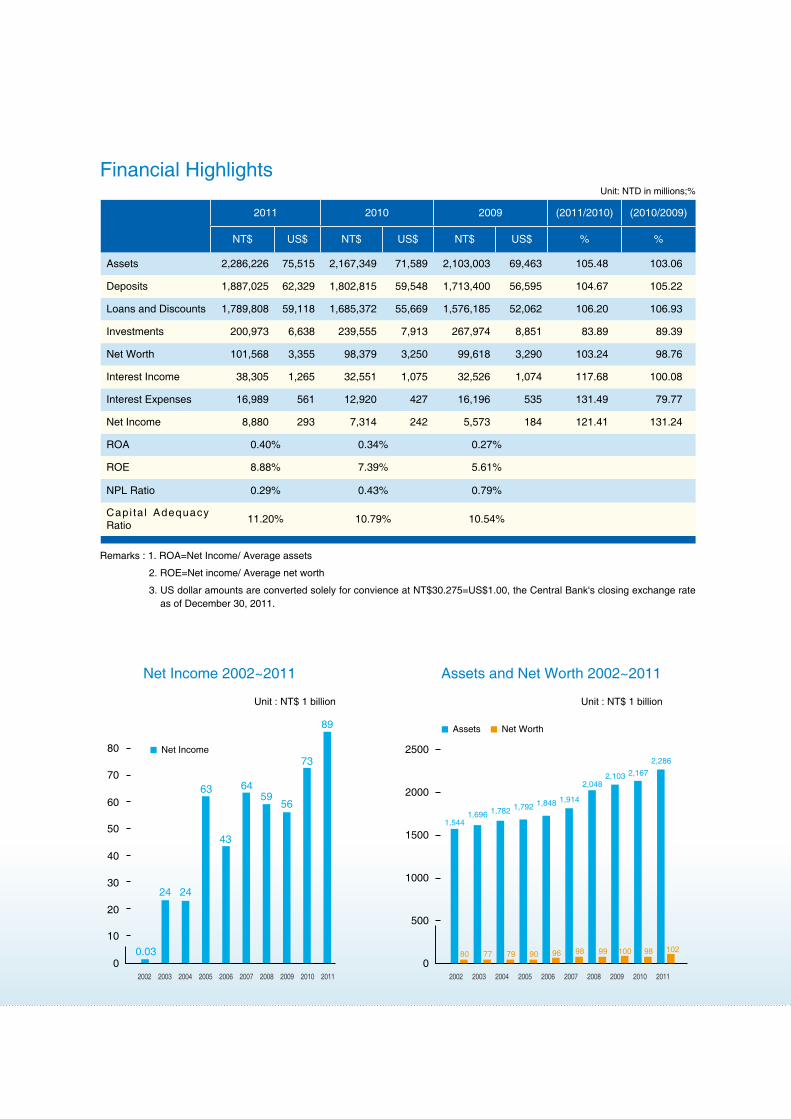

FINANCIAL HIGHLIGHTS

BUSINESS REPORTS

BANK PROFILE

DIRECTORS, SUPERVISORS AND OFFICERS

STATUS OF CORPORATE GOVERNANCE PRACTICE

OPERATING OVERVIE

FINANCIAL STATUS AND RISK MANAGEMENT

FINANCIAL STATEMENTS

DIRECTORY OF LBOT’S OFFICES

5

10

18

21

24

34

40

56

64

Contents

70

80

60

50

40

30

20

10

0

Unit : NT$ 1 billion

Net Income

0.03

24

63

24

43

6459

56

73

89

Financial Highlights

Assets and Net Worth 2002~2011Net Income 2002~2011

Unit : NT$ 1 billion

500

1000

1500

2000

2500

0

Net WorthAssets

1,544

80 77 79 90 96 98 99 100 98 102

1,696 1,782 1,792 1,848 1,914

2,0482,103 2,167

2,286

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Unit: NTD in millions;%

2011 2010 2009 (2011/2010) (2010/2009)

NT$ US$ NT$ US$ NT$ US$ % %

Assets 2,286,226 75,515 2,167,349 71,589 2,103,003 69,463 105.48 103.06

Deposits 1,887,025 62,329 1,802,815 59,548 1,713,400 56,595 104.67 105.22

Loans and Discounts 1,789,808 59,118 1,685,372 55,669 1,576,185 52,062 106.20 106.93

Investments 200,973 6,638 239,555 7,913 267,974 8,851 83.89 89.39

Net Worth 101,568 3,355 98,379 3,250 99,618 3,290 103.24 98.76

Interest Income 38,305 1,265 32,551 1,075 32,526 1,074 117.68 100.08

Interest Expenses 16,989 561 12,920 427 16,196 535 131.49 79.77

Net Income 8,880 293 7,314 242 5,573 184 121.41 131.24

ROA 0.40% 0.34% 0.27%

ROE 8.88% 7.39% 5.61%

NPL Ratio 0.29% 0.43% 0.79%

Capi ta l Adequacy Ratio 11.20% 10.79% 10.54%

Remarks : 1. ROA=Net Income/ Average assets

2. ROE=Net income/ Average net worth

3. US dollar amounts are converted solely for convience at NT$30.275=US$1.00, the Central Bank's closing exchange rate as of December 30, 2011.

Soar on WingsAdvance to Excellence

Business ReportsBusiness Review for 2011

Brief Business Plan for 2012

Future Development Strategies

Credit Ratings

1010

14

15

15

A sophisticated professional.Perfect presentation.

Applying specialty niches, cultivating core businesses, Land Bank performs entrepreneurial spirit.

During 2011, in the second quarter the 311 Japan Earthquake and the European Sovereign Debt Crisis

occurred in a row, in July the U.S. national debt problem surfaced, and in August the U.S. credit rating

was downgraded, which all led to lagging global stock markets. Moreover, emerging market countries

gradually tighten money supply to ease the inflationary pressure, making economic expansion slow down,

and the European Debt Crisis encounters unsolvable fundamental problems, so the international economic

situation has actually entered a pattern of short-term adjustment, or even business cycle contraction.

Because major economies and emerging market economies have yet seen the first light of morning in the

short term, the overall economic forecast for 2012 tends to be conservative.

In recent years Taiwan's house prices kept skyrocketing and loans of financial institutions concentrated

on real estate financing, which led to increasing operating risk of banks. The government continuously

promoted measures of house price stabilization and credit risk control, including levying luxury tax and

advancing actual price registration for real estate transactions, so the growth in housing and construction

loans undertaken by banks gradually slowed down. As a real estate loan specialty bank, the Bank

certainly sustained impacts on related loan business, while the crisis was also an opportunity for the Bank

to disperse the risk and diversify business development.

Thanks to excellent leadership of its management team and dedicated efforts made by its staff, the

Bank was able to respond to the market situation, flexibly adjust its operating strategies, and sustain

steady growth in sales volume. Its business review for 2011 and business plan for 2012 can be outlined

below:

I. Business Review for 20111. Domestic and Overseas Economic and Financial Landscape

(1) Economic situation

During the first half of 2011, the 311 Japan Earthquake impacted the global production and supply

Business Reports10

chain; since the second half of 2011, business demand has been weak along with the worsening

European/American debt problem, fiscal restraint, and delaying improvement in the employment

situation; earlier on emerging countries gradually contracted money supply to cope with the

inflationary pressure, making economic expansion worldwide slow down substantially. Based on

data provided by Global Insight Inc., the global economic growth rate for 2011 was 3.0%, while

the projected rate for 2012 will decline to 2.7%.

Taiwan's economy was affected by the global business cycle, where export demand withered,

capacity utilization rates of companies went down, and corporate investment tended to be more

conservative; moreover, given an unstable financial market and the no-pay leave implemented by

certain companies, people´s wealth and consumer confidence were accordingly affected, which

led to weaker overall economic growth dynamics. According to statistics from the Directorate-

General of Budget, Accounting and Statistics of the Executive Yuan, the full-year economic growth

rate for 2011 was 4.04%, and the projected economic growth rate for 2012 is 3.85%.

(2) Financial situation

The European Debt Crisis seriously hit financial markets worldwide, where the alarm has yet

been solved. Earlier on nations gradually contracted money supply to cope with the inflationary

pressure, but because in the third quarter the prices of international raw materials fell from the

period high and price inflation pressure was eased, currency policies of certain countries turned to

be looser. The domestic financial industry benefited by the Central Bank's prior and continuous

interest raise, for its effects have gradually surfaced. Interest rate margins of local banks reached

a new three-year high, loan and wealth management businesses continued to grow, and interest

income and administrative fee income obviously picked up, along with steady asset quality and

consequential growth in profits, so that at year end 2011 the overall return on equity (ROE) of

Taiwan banks reached 9.33%.

Wang, Yao-ShingChairperson of the Board

11

Business R

eports

2. Organizational Change of the Bank

(1) The Bank opened its New York Branch On January 11, 2011, to expand its operating

scale in foreign exchange and deepen its overseas deployment.

(2) The Bank strengthened horizontal and vertical communication among departments of the

head office, and actively integrated marketing operations in light of characteristics of its

channels and customer groups, to advance the operating performance.

(3) With the broadened cross-business operations of banking, securities, insurance, and

investment trust, the Bank has been actively planning to set up the state-run “Land Bank

Urban Renewal Investment Trust Co., Ltd." and “Land Bank Insurance Brokerage

Co., Ltd.," and adapted to the fittest organization development style to fully exercise

organizational efficiency.

3. Practice Achievements of Business Plan and Operating Strategies

Su, Ler- MingPersident

12

Unit: NTD in millions; USD in millions (foreign exchange); %

YearMajor Operation Category

2011 2010 Growth Rate Compared to Preceding Year

Deposits 1,935,018 1,860,418 +4.01

Loans 1,732,242 1,624,973 +6.60

Foreign Exchange 41,197 38,287 +7.60

Scale of Trust Property 290,316 282,001 +2.95

Guaranty 62,858 56,815 +10.64

Securities Brokerage 164,309 193,220 (Note)-14.96

Note: Influenced by a slowing international business cycle, investors in the local securities market turned conservative in their dealings, and the composite trading volume was reduced, so that the volume of securities operations decreased compared to the preceding year.

4. Status of Budget Execution

In the year of 2011, the total accumulated average deposit amounted to NT$1,935 billion,

reaching 115.18% of the budget goal; the accumulated average loan outstanding amounted to

NT$1,732.2 billion, reaching 120.71% of the budget goal; the accumulated volume of foreign

exchange transactions undertaken amounted to US$41.197 billion, reaching 164.79% of the

budget goal; and the before-tax net income amounted to NT$10.533 billion, reaching 131.66% of

the budget goal.

13

Business R

eports

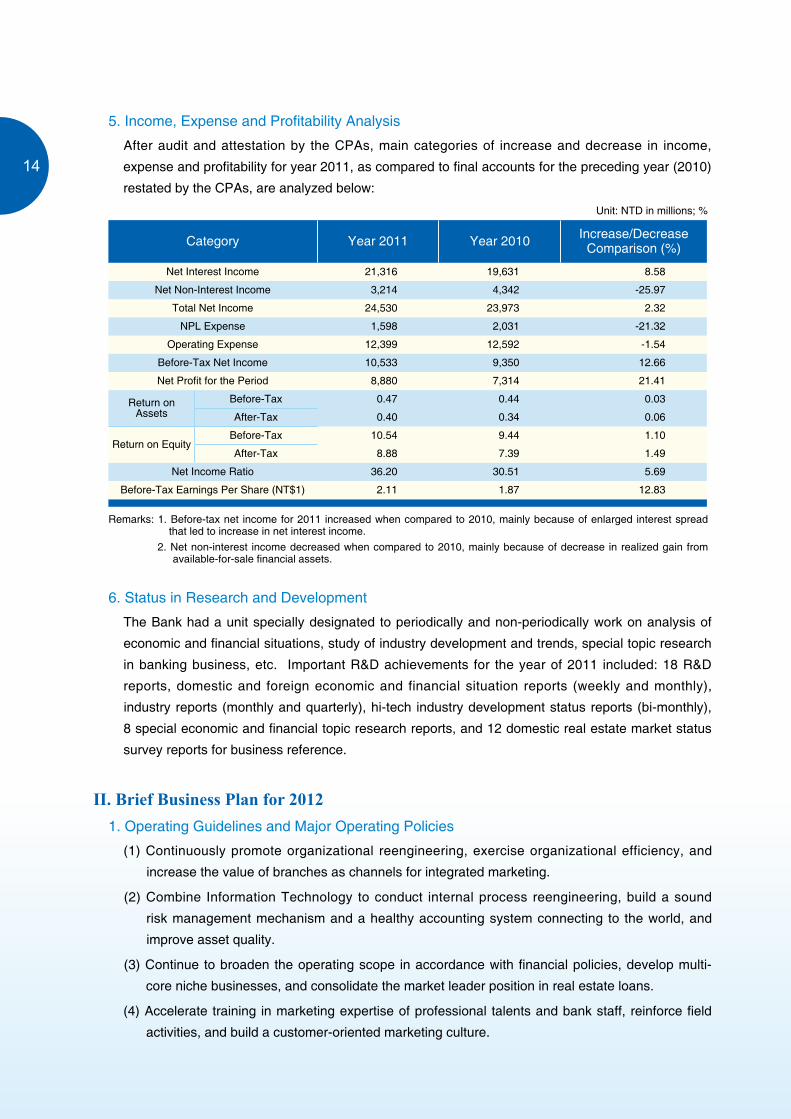

Unit: NTD in millions; %

Category Year 2011 Year 2010 Increase/Decrease Comparison (%)

Net Interest Income 21,316 19,631 8.58

Net Non-Interest Income 3,214 4,342 -25.97

Total Net Income 24,530 23,973 2.32

NPL Expense 1,598 2,031 -21.32

Operating Expense 12,399 12,592 -1.54

Before-Tax Net Income 10,533 9,350 12.66

Net Profit for the Period 8,880 7,314 21.41

Return on Assets

Before-Tax 0.47 0.44 0.03

After-Tax 0.40 0.34 0.06

Return on EquityBefore-Tax 10.54 9.44 1.10

After-Tax 8.88 7.39 1.49

Net Income Ratio 36.20 30.51 5.69

Before-Tax Earnings Per Share (NT$1) 2.11 1.87 12.83

Remarks: 1. Before-tax net income for 2011 increased when compared to 2010, mainly because of enlarged interest spread that led to increase in net interest income.

2. Net non-interest income decreased when compared to 2010, mainly because of decrease in realized gain from available-for-sale financial assets.

5. Income, Expense and Profitability Analysis

After audit and attestation by the CPAs, main categories of increase and decrease in income,

expense and profitability for year 2011, as compared to final accounts for the preceding year (2010)

restated by the CPAs, are analyzed below:

6. Status in Research and Development

The Bank had a unit specially designated to periodically and non-periodically work on analysis of

economic and financial situations, study of industry development and trends, special topic research

in banking business, etc. Important R&D achievements for the year of 2011 included: 18 R&D

reports, domestic and foreign economic and financial situation reports (weekly and monthly),

industry reports (monthly and quarterly), hi-tech industry development status reports (bi-monthly),

8 special economic and financial topic research reports, and 12 domestic real estate market status

survey reports for business reference.

II. Brief Business Plan for 20121. Operating Guidelines and Major Operating Policies

(1) Continuously promote organizational reengineering, exercise organizational efficiency, and

increase the value of branches as channels for integrated marketing.

(2) Combine Information Technology to conduct internal process reengineering, build a sound

risk management mechanism and a healthy accounting system connecting to the world, and

improve asset quality.

(3) Continue to broaden the operating scope in accordance with financial policies, develop multi-

core niche businesses, and consolidate the market leader position in real estate loans.

(4) Accelerate training in marketing expertise of professional talents and bank staff, reinforce field

activities, and build a customer-oriented marketing culture.

14

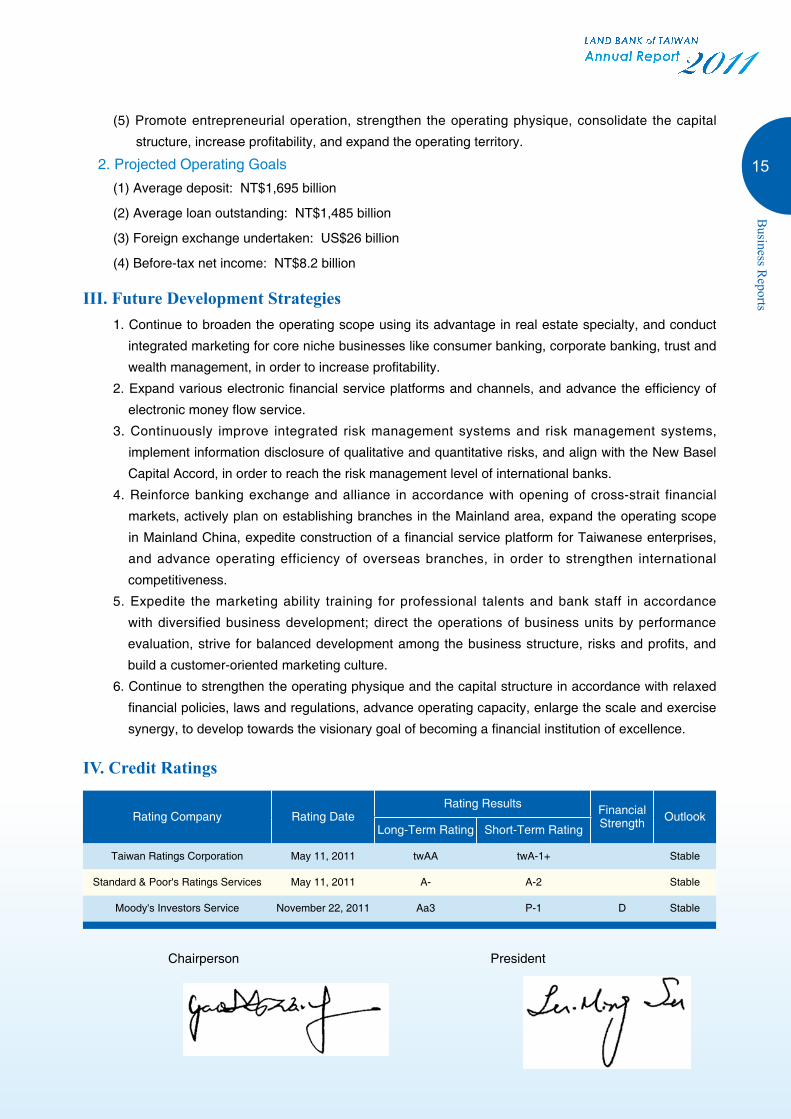

Chairperson President

Rating Company Rating DateRating Results Financial

Strength OutlookLong-Term Rating Short-Term Rating

Taiwan Ratings Corporation May 11, 2011 twAA twA-1+ Stable

Standard & Poor's Ratings Services May 11, 2011 A- A-2 Stable

Moody's Investors Service November 22, 2011 Aa3 P-1 D Stable

(5) Promote entrepreneurial operation, strengthen the operating physique, consolidate the capital

structure, increase profitability, and expand the operating territory.

2. Projected Operating Goals

(1) Average deposit: NT$1,695 billion

(2) Average loan outstanding: NT$1,485 billion

(3) Foreign exchange undertaken: US$26 billion

(4) Before-tax net income: NT$8.2 billion

III. Future Development Strategies1. Continue to broaden the operating scope using its advantage in real estate specialty, and conduct

integrated marketing for core niche businesses like consumer banking, corporate banking, trust and

wealth management, in order to increase profitability.

2. Expand various electronic financial service platforms and channels, and advance the efficiency of

electronic money flow service.

3. Continuously improve integrated risk management systems and risk management systems,

implement information disclosure of qualitative and quantitative risks, and align with the New Basel

Capital Accord, in order to reach the risk management level of international banks.

4. Reinforce banking exchange and alliance in accordance with opening of cross-strait financial

markets, actively plan on establishing branches in the Mainland area, expand the operating scope

in Mainland China, expedite construction of a financial service platform for Taiwanese enterprises,

and advance operating efficiency of overseas branches, in order to strengthen international

competitiveness.

5. Expedite the marketing ability training for professional talents and bank staff in accordance

with diversified business development; direct the operations of business units by performance

evaluation, strive for balanced development among the business structure, risks and profits, and

build a customer-oriented marketing culture.

6. Continue to strengthen the operating physique and the capital structure in accordance with relaxed

financial policies, laws and regulations, advance operating capacity, enlarge the scale and exercise

synergy, to develop towards the visionary goal of becoming a financial institution of excellence.

IV. Credit Ratings

15

Business R

eports

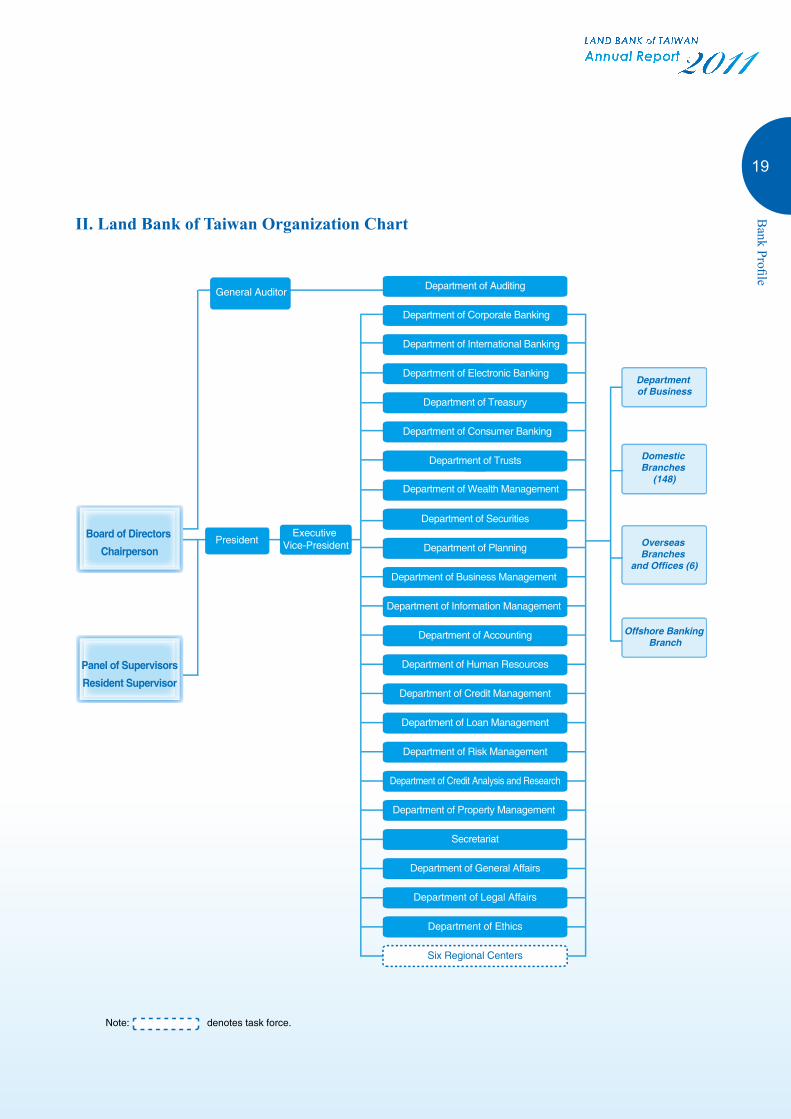

Bank ProfileHistory

Land Bank of Taiwan Organization Chart

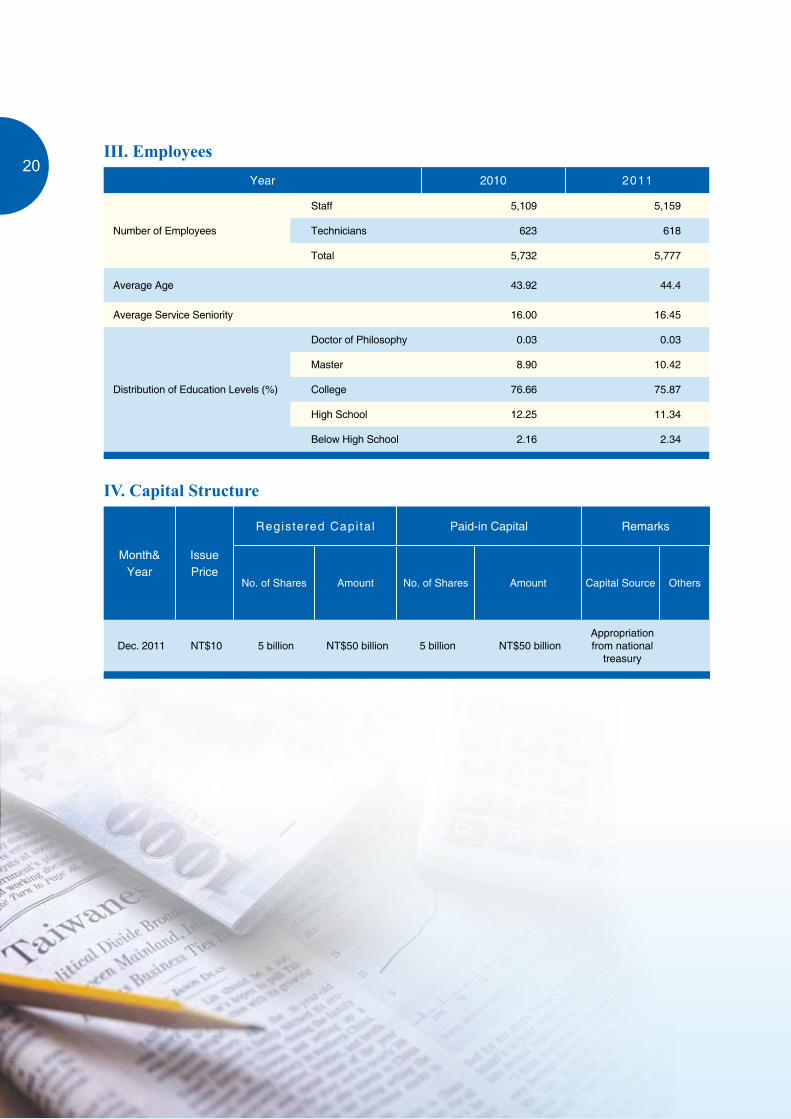

Employees

Capital Structure

Directors, Supervisors and OfficersDirectors and Supervisors

Officers

Status of Corporate Governance PracticeStatus of the Bank's Corporate Governance Practice, Its Deviations from the Corporate Governance Best-Practice Principles for Banks, and Respective Reasons

Status of Social Responsibility Performance

18

21

20

20

21

21

19

A state-run brand. Stable and reliable.

Enhancing the capital structure, integrating banking service, Land Bank earns diverse competitiveness.

18

24

28

24

I. History

The history of the Land Bank of Taiwan dates from 1945, when the government decided to

promote land policies such as land-rights equalization and the land-to-the-tiller program in Taiwan,

and thus the national treasury appropriated 60 million dollars as capital to establish the “Land

Bank of Taiwan" pursuant to R.O.C. law on 1st September, 1946 utilizing the five branches

of the Nippon Kangyo Bank which had been set up in Taipei, Hsinchu, Taichung, Tainan, and

Kaohsiung during the Japanese occupation. In May, 1985, the Land Bank of Taiwan became

qualified as a juristic person pursuant to Article 52 of the Banking Act; on 21st December, 1998,

it became a state-run business organization upon implementation of the Province Simplification

Statute; on 1st July, 2003, it was re-organized as the “Land Bank of Taiwan Co., Ltd.;" further

on 21st May, 2004, it was transformed into a public company.

Bank Profile18

Board of Directors Chairperson

Panel of SupervisorsResident Supervisor

PresidentExecutive

Vice-President

General Auditor Department of Auditing

Department of Corporate Banking

Department of International Banking

Department of Electronic BankingDepartment of Business

Domestic Branches

(148)

Overseas Branches

and Offices (6)

Offshore Banking Branch

Department of Treasury

Department of Consumer Banking

Department of Trusts

Department of Wealth Management

Department of Securities

Department of Planning

Department of Business Management

Department of Information Management

Department of Accounting

Department of Human Resources

Department of Credit Management

Department of Loan Management

Department of Risk Management

Department of Credit Analysis and Research

Department of Property Management

Secretariat

Department of General Affairs

Department of Legal Affairs

Department of Ethics

Six Regional Centers

II. Land Bank of Taiwan Organization Chart

Note: denotes task force.

19

Bank Profile

III. EmployeesYear 2010 2011

Number of Employees

Staff 5,109 5,159

Technicians 623 618

Total 5,732 5,777

Average Age 43.92 44.4

Average Service Seniority 16.00 16.45

Distribution of Education Levels (%)

Doctor of Philosophy 0.03 0.03

Master 8.90 10.42

College 76.66 75.87

High School 12.25 11.34

Below High School 2.16 2.34

Month& Year

Issue Price

Registered Capital Paid-in Capital Remarks

No. of Shares Amount No. of Shares Amount Capital Source Others

Dec. 2011 NT$10 5 billion NT$50 billion 5 billion NT$50 billionAppropriation from national

treasury

IV. Capital Structure

20

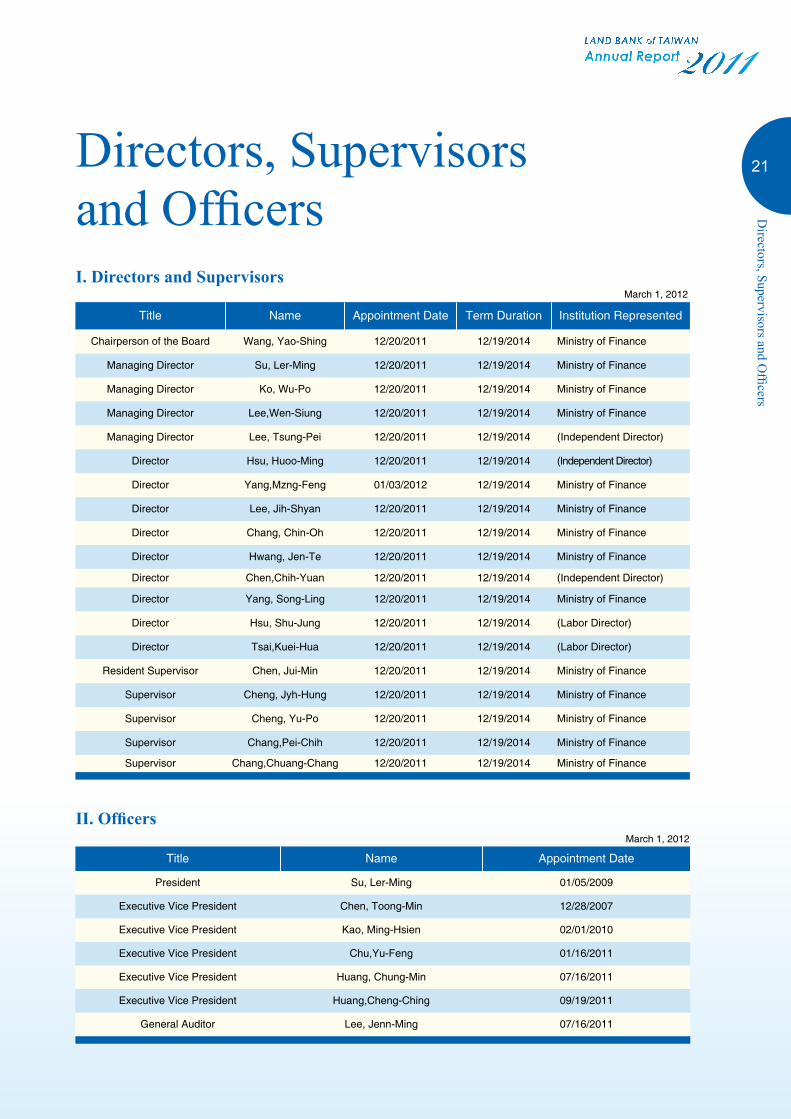

I. Directors and Supervisors

II. Officers

Directors, Supervisors and Officers

Title Name Appointment Date Term Duration Institution Represented

Chairperson of the Board Wang, Yao-Shing 12/20/2011 12/19/2014 Ministry of Finance

Managing Director Su, Ler-Ming 12/20/2011 12/19/2014 Ministry of Finance

Managing Director Ko, Wu-Po 12/20/2011 12/19/2014 Ministry of Finance

Managing Director Lee,Wen-Siung 12/20/2011 12/19/2014 Ministry of Finance

Managing Director Lee, Tsung-Pei 12/20/2011 12/19/2014 (Independent Director)

Director Hsu, Huoo-Ming 12/20/2011 12/19/2014 (Independent Director)

Director Yang,Mzng-Feng 01/03/2012 12/19/2014 Ministry of Finance

Director Lee, Jih-Shyan 12/20/2011 12/19/2014 Ministry of Finance

Director Chang, Chin-Oh 12/20/2011 12/19/2014 Ministry of Finance

Director Hwang, Jen-Te 12/20/2011 12/19/2014 Ministry of Finance

Director Chen,Chih-Yuan 12/20/2011 12/19/2014 (Independent Director)

Director Yang, Song-Ling 12/20/2011 12/19/2014 Ministry of Finance

Director Hsu, Shu-Jung 12/20/2011 12/19/2014 (Labor Director)

Director Tsai,Kuei-Hua 12/20/2011 12/19/2014 (Labor Director)

Resident Supervisor Chen, Jui-Min 12/20/2011 12/19/2014 Ministry of Finance

Supervisor Cheng, Jyh-Hung 12/20/2011 12/19/2014 Ministry of Finance

Supervisor Cheng, Yu-Po 12/20/2011 12/19/2014 Ministry of Finance

Supervisor Chang,Pei-Chih 12/20/2011 12/19/2014 Ministry of Finance

Supervisor Chang,Chuang-Chang 12/20/2011 12/19/2014 Ministry of Finance

Title Name Appointment Date

President Su, Ler-Ming 01/05/2009

Executive Vice President Chen, Toong-Min 12/28/2007

Executive Vice President Kao, Ming-Hsien 02/01/2010

Executive Vice President Chu,Yu-Feng 01/16/2011

Executive Vice President Huang, Chung-Min 07/16/2011

Executive Vice President Huang,Cheng-Ching 09/19/2011

General Auditor Lee, Jenn-Ming 07/16/2011

March 1, 2012

March 1, 2012

21

Directors, Supervisors and O

fficers

Directors and Supervisors

1. Resident Supervisor / Chen, Jui-Min

2. Managing Director / Lee, Tsung-Pei

3. Managing Director / Ko, Wu-Po

4. Managing Director / Lee,Wen-Siung

13 42

22

Management Team

1. Chairperson of the Board / Wang, Yao-Shing

2. President / Su, Ler-Ming

3. Executive Vice President / Chen, Toong-Min

4. Executive Vice President / Kao, Ming-Hsien

5. Executive Vice President / Chu,Yu-Feng�

6. Executive Vice President / Huang, Chung-Min

7. Executive Vice President / Huang,Cheng-Ching

8. General Auditor / Lee, Jenn-Ming

常駐監察人 / 陳瑞敏14 3 6 857 2

23

Directors, Supervisors and O

fficers

I. Status of the Bank’s Corporate Governance Practice, Its Deviations from the Corporate Governance Best-Practice Principles for Banks, and Respective Reasons

Status of Corporate Governance Practice

Category Status of Practice

Deviations from the Corporate Governance Best-Practice Principles for Banks

and Respective Reasons

1. Bank ownership structure and shareholders' equity

(1) Way of the Bank handling shareholder suggestions or disputes

(1) There was spec i f ica l ly -ass igned personne l hand l ing s tock a f fa i rs , keeping the channel for communication unhindered.

No deviation.

(2) Status of the Bank being fully informed of the major shareholders that actually control the Bank, and their ultimate controllers

(2) The ROC Government was the sole shareholder of the Bank, and the Bank specifically assigned personnel to handle stock affairs, so it was actually informed of its major shareholder and its ultimate controller.

No deviation.

(3) Status of the Bank building the risk control mechanism and firewall with affiliated enterprises

(3) To reinforce control over its subsidiaries, t h e B a n k h a s e s t a b l i s h e d t h e “Land Bank of Taiwan Subsidiaries Management Guideline" and the “Land Bank of Taiwan Management Guideline for Appointing Personnel to Serve as Directors and Supervisors of Reinvested B u s i n e s s e s a n d S u b s i d i a r i e s ," to imp lement i t s superv is ion and management mechanism.

No deviation.

2. Composition and duties of the Board of Directors(1) Status of the Bank retaining

Independent Directors(1) The Bank has established the “Rules

Governing the Scope of Dut ies of Independent Directors," and retained 3 Independent Directors at the time.

No deviation.

(2) Status of periodically reviewing the attesting CPA's independence

(2) The Bank retained its attesting CPA in accordance with the Government Procurement Act, and has reached with the accounting firm provisions regarding annual review, contract termination and contract cancellation.

No deviation.

3. Status of establishing communication channels with stakeholders

The Bank established a toll-free customer complaint hot l ine, and had executive mailbox, customer complaint and e-mail box on the opinion exchange section of the Bank's website, where specifically-assigned personnel handled suggestions or disputes of customers and stakeholders.

No deviation.

24

Category Status of Practice

Deviations from the Corporate Governance Best-Practice Principles for Banks

and Respective Reasons

4. Information disclosure

(1) Status of the Bank setting up a website to disclose information about finance, business, and the Bank's corporate governance

(1) The Bank has set up a website and disclosed information like important f inancial and business affairs and corporate governance every quarter in accordance with pertinent regulations.

No deviation.

(2) Other means adopted by the Bank to disclose information (such as setting up an English website, specifically assigning personnel to collect and disclose bank information, implementing the spokesperson mechanism, and posting taped investor conferences on the Bank website)

(2) The Bank has set up an English website and specifically assigned personnel to periodically collect important financial and business information, and disclosed related information on the website. To implement the spokesperson mechanism, the Bank established the “Notice for News Release and Contact," where the President appointed one Executive Vice-President as the news spokesperson, and separately appointed another Executive Vice-President as the deputy spokesperson, to exclusively make public comments on major policies and business measures adopted by the Bank. On the other hand, the Secretariat's Public Relations Section was in charge of collection of related information and news release; i t also posted taped investor conferences on the Bank website, although the Ministry of Finance as an institution was the sole investor of the Bank, of which the stock was not yet publicly listed.

No deviation.

5. Operating status of the Bank establishing the Nomination Committee, the Remuneration Committee or other functional committees

Not yet established. All shares of the Bank were held by the ROC Government, and all Directors were approved and appointed by the Ministry of Finance, where major decisions of the Bank were submitted to the Board of Directors for discussion and approval, further monitored by the Supervisors.

6. Status of the Bank's corporate governance practice and its deviations from the “Corporate Governance Best-Practice Principles for Banks" and respective reasons: See the above columns for details.

7. Other important information that enhances understanding of the Bank's corporate governance practice (such as Directors and Supervisors continuing education, status of Directors' attending and Supervisors' observing the Board of Directors meeting, status of executing risk management policies and risk measurement standards, status of executing the consumer protection or customer policy, status of executing Directors' avoiding proposals with conflict of interests, duties of managers, status of the Bank purchasing liability insurance for Directors and Supervisors, etc.):

(1) Directors and Supervisors continuing education: All the Bank's Directors and Supervisor took training courses on administrative neutrality and corporate governance according to pertinent regulations, and on December 20, 2011 the Bank held the “(Independent) Directors and Supervisors Advanced Practice Seminar" to discuss the Personal Information Protection Act.

(2) Status of Directors' attending and Supervisors'observing the Board of Directors meeting: Details for holding Board meetings of the Bank were all included in the Bank's Articles of Incorporation and Board of Directors Meeting Rules, where Supervisors were invited to the meetings for observance.

25

公司治理報告

Status of Corporate G

overnance Practice

(3) Status of executing risk management policies and risk measurement standards:

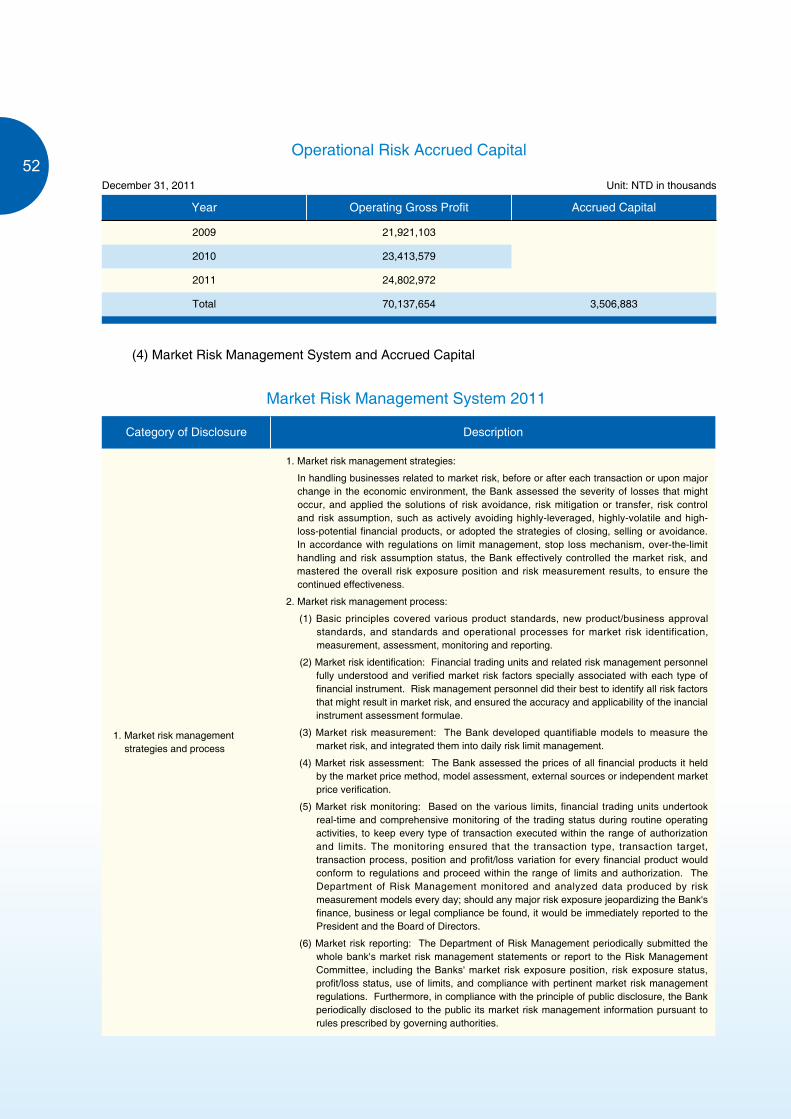

a. The Bank's “Risk Management Committee" convened 6 meetings during the year, reviewed the whole bank's risk monitoring reports and risk control proposals, and continued to have the Department of Risk Management handle measuring, monitoring and reporting of the whole bank's credit, market, operational and other risks.

b. On February 24, 2011 and July 7, 2011 the Bank consecutively issued letters to revise the “Land Bank of Taiwan Table of Limits for the Market Value-at-Risk," to consolidate market risk management of the Bank.

c. On May 19, 2011 the Bank issued a letter to announce Land Bank of Taiwan's “Liquidity Risk Management Guideline" and “Interest Rate Risk Management Guideline."

d. On June 30, 2011 the Bank submitted to the Financial Supervisory Commission the “Land Bank of Taiwan Operating Plan for 2011," the “Land Bank of Taiwan Capital Adequacy Assessment Result for 2010" and the “Land Bank of Taiwan Statement of Self-Assessment on Various Risk Indicators for 2010."

e. To work with the Financial Examination Bureau of the Financial Supervisory Commission on regular business examination on the Bank, on June 7, 2011 the Bank completed and submitted the examination form for the operating status of its management of overall risk, credit risk, market risk, operational risk, liquidity risk and banking book interest rate risk.

(4) Status of executing the consumer protection or customer policy:

a. To protect consumer rights and interests, on January 10, 2011 the Bank issued a letter to every operating unit, reinstating that each unit shall fully abide by pertinent regulations in handling businesses related to Article 12-1 of the Banking Act.

b. To protect consumer rights and interests as well as maintain fair market competition, on March 25, 2011 the Bank sent a copy of its “Fee Schedule for Credit Card Related Services," asking each unit to post it on an obvious place of the lobby.

c. On March 31, 2011 the Bank wrote to ask every operating unit to claim the poster of “Never Borrow Via An Agent" to be posted on obvious places at its operating premises (including the automated equipment service area), to help inform the public of the correct financial consumption concept.

d. To protect consumer rights and interests, on April 22, 2011 the Bank issued a letter to every operating unit, reinstating that each unit shall proceed fully in accordance with Article 7 of the “Directions for Members of the Bankers Association of the Republic of China Executing Article 12-1 of the Banking Act" established by the Bankers Association of the Republic of China with respect to collateralizing guaranteed loans.

e. On May 9, 2011 the Bank forwarded a letter relayed by the Bankers Association for the Financial Supervisory Commission, stating that “to prevent loan application in another person's name and affecting financial order, all financial institutions shall fully implement credit analysis and credit extension review, and financial examination will reinforce the inspection on borrower credit analysis, use of fund and source of repayment," and the Bank required its operating units to proceed accordingly pursuant to pertinent regulations of the Bank regarding credit analysis and extension.

f. On June 3, 2011 the Bank forwarded a letter relayed by the Bankers Association for the Financial Supervisory Commission regarding the Legislator's suggestion that financial institutions shall not incur the unreasonable situation of “age discrimination" when handling the loan against collateral.

g. On July 18, 2011 the Bank issued a letter to every operating unit, mandating that, when handling credit extension, each unit shall initiate explanation with the borrower about ways of searching repayment details, and that the unit shall not reject the borrower's request for repayment details, in order to protect the borrower's rights and interests and avoid disputes.

h. On August 2, 2011 the Bank forwarded a reply letter relayed by the Bankers Association for the Financial Supervisory Commission, mandating full implementation of the rule that “the figure of a debtor's total unsecured debt balance (including credit card, debit card and credit loan) at all financial institutions divided by his/her average monthly income should not exceed 22."

i. To build excellent customer relations management for subsequent business transactions and convenient operations, on August 22, 2011 the Bank issued a letter to every operating unit, mandating that each unit shall favorably consider a credit card application should the applicant's domicile, mailing address or working location indicate community relation with the handling unit.

j. To protect consumer data, rights and interests, on October 21, 2011 the Bank issued a letter to every operating unit, reinstating that when a customer rejected telephone or e-mail marketing from a sales representative of the Bank, the representative could ask the customer to call the customer service center, where the service personnel would first confirm customer identification and then proceed with online computer registration, connecting to the “Customer Relations Management (CRM)" database to make a note on its “customer marketing list management" section.

k. On November 3, 2011 the Bank forwarded a letter relayed by the Bankers Association for the Financial Supervisory Commission regarding pertinent regulations on handling the vehicle loan business, and thus the Bank updated its car loan related forms; besides, to protect customer rights and interests, customer data retrieved from the Joint Credit Information Center were used for the Bank's internal credit analysis only, not for use of car dealers.

l. To improve the Bank's housing loan series products, and provide consumers with more diverse financial services, on November 16, 2011 the Bank issued a letter to every operating unit to introduce the “Land Bank of Taiwan Measures for the Happy Life Special Housing Loan Program."

26

m. To consolidate bank operations and protect people's rights and interests, on November 22, 2011 the Bank forwarded a letter of the Financial Supervisory Commission, mandating that each unit, when requesting guarantors and related data in the lending process, shall meet pertinent regulations like the Civil Code, the Credit Analysis and Extension Guideline, and the Implementation Rules of Internal Audit and Internal Control System of Financial Holding Companies and Banking Industries, and thus fully implement the credit extension and identity verification procedure and conduct review, to preclude dummy guarantors or improperly requesting minors to act as guarantors.

n. To implement amended (supplemental) provisions of Article 12-1 and Article 12-2 of the Banking Act, and to avoid disputes upon actual execution, the Bank organized each operating unit's questions and answers to execution of the amendment (supplement), and on November 30, 2011 issued a letter to every operating unit stating “The Bank's Guideline for Observing Articles 20-1 and 20-2 of the Banking Act in Consumer Loan Credit Extension" for the reference of practice.

o. On December 28, 2011 the Bank relayed the “Directions for Members of the Bankers Association of the Republic of China Handling Deferred Principal Payment and Extended Repayment Deadline for Residential Housing Loans of Involuntarily-Unemployed Laborers" established by the Bankers Association, as well as related operating rules and matters to be accordingly handled.

(5) Status of implementing Directors' avoiding proposals with conflict of interests: Pursuant to the Bank's Articles of Incorporation and Board of Directors Meeting Rules, Directors shall immediately avoid proposals with conflict of interests.

(6) Duties of managers: As provided by Article 35 and Article 36 of Chapter 7 (Managers) of the Bank's Articles of Incorporation.

(7) Status of the Bank purchasing liability insurance for Directors and Supervisors: No liability insurance policy was made at the time.

8. Where there is a corporate governance self-assessment report or a corporate governance assessment report made by another contracting professional institution, please clearly state the results of the self-assessment (or contracting assessment), the major defects (or suggestions), and the status of improvement:

(1) In 2011 the Bank retained a professional institution, Feng Chia University Corporate Governance Research Center, to conduct corporate governance assessment, for which the general opinions are summarized below:

a. The Company promptly announced related information on its annual report and website according to law, and established facebook and blog platforms for complete disclosure of public issues, indicating great information transparency.

b. The management practiced good legal compliance, fully implemented business risk management, and engaged in normal business conduct.

c. All Directors and Supervisors followed pertinent corporate ethics rules, and the Labor Director actually participated in making major decisions of the Company.

d. The Company coordinated with each stakeholder, worked with the corporate labor union to periodically hold the Labor-Management Meeting, and set up an employee section in its internal network as the labor-management communication channel, which further indicated the Company's well-functioning personnel management. Besides, the Company conducted public interest activities to fulfill social responsibility, and worked with the government to conduct various policy-oriented loans.

e. Suggestions to the Bank: During the ROC Centennial, the Company gave an excellent operating performance. However, facing the economic environment after the European Debt Crisis and signing of cross-strait MOU and ECFA, the Company is advised to further strengthen its innovation and marketing management strategies, to advance competitiveness and profitability.

(2) Review and improvement:

It has been an inevitable trend for financial institutions to develop towards business professionalization and operation internationalization, and future competition is going to turn white-hot. To improve operating efficiency, the Bank actively adopted the following measures:

a. Utilize the “creative reform proposal" measure to encourage responsible operating units of the head office to continuously weed through the old to bring forth the new in products and services.

b. Actively collect market updates and information about fellow financial institutions promoting business, for the reference of product design and marketing.

c. Expand diverse electronic channels like online and mobile banking, and increase administrative fee income sources, in order to generate more revenues.

d. Conduct integrated marketing for multi-core niche businesses, consolidate the core niches of consumer banking, corporate banking, trust and wealth management, strengthen electronic money flow channels and service, expand the operating scale for banking, securities, insurance and investment trust, nurture cross-industry professional talents and techniques, broaden the business scope and reinforce overseas deployment, to continuously increase competitiveness.

27

公司治理報告

Status of Corporate G

overnance Practice

II. Status of Social Responsibility Performance

Category Status of Practice

1. Implementing promotion of corporate governance

(1) Status of the Bank establishing the corporate social responsibility policy or system and reviewing implementation achievements.

The Bank is a state-run enterprise 100% owned by the government, and for years the Bank followed the government policy to conduct various special loans and promoted national economic development; under the idea of “What is taken from society is used on society," the Bank spared no efforts to sponsor community care, environment protection and underrepresented groups, and did not separately establish a corporate social responsibility policy or system.

(2) Operating status of the Bank establishing a specially-set (adjunct) unit to promote corporate social responsibility.

The Bank did not establish any specially-set (adjunct) unit to promote corporate social responsibility.

(3) Status of the Bank periodically holding corporate ethics training sessions and promotion campaignsfor Directors, Supervisors and employees, and combining it with the employee performance evaluation system to establish a clear and effective reward and punishment mechanism.

a. The Bank's Directors and Supervisor all took training courses on administrative neutrality and corporate governance according to pertinent regulations, and the Bank unperiodically arranged promotion courses like Introduction to the Civil Servants Service Act or the Personal Information Protection Act, to build up a consensus on civil service.

b. In the year the Bank arranged various professional and orientation training programs to offer corporate ethics education courses, promoted related laws like civil servants anti-corruption ethics regulations and professional responsibility, and drafted related advertising materials, delivering the idea of knowing the law and obeying the law.

c. Pursuant to the “Directions for General Evaluation of Civil Servants of the Executive Yuan and Affiliated Agencies" and the “Directions for Evaluation of Personnel of State-Run Financial and Insurance Business Organizations Under the Ministry of Finance," the Bank included employee work competency, service attitude, character, integrity, organizational goal fulfillment, and implementation of customer orientation as the items for employee general evaluation and annual evaluation, where proper rewards (punishments) would be issued for superior (inferior) performances.

2. Developing a sustainable environment(1) Status of the Bank striving for

improving usage efficiency of various resources, as well as using recycled materials of low environment load and impact.

a. To celebrate the ROC Centennial, promote healthful exercises, and advocate the idea of environment protection, on September 25, 2011 the Bank held “Finance Cup United Fun Athletic Meeting" and “Cherish Land Charity Fair" at the NTU Sports Center, before which during the preparation period the Bank launched a resource recycling campaign, raising totally 1,820 kilograms of recyclable resources like scrap batteries, CDs and cell phones to be given to Yu-Cheng Social Welfare Foundation after the competition; besides, the Bank offered 300 osmanthus saplings and 1,500 small pot plants for participants' adoption, building the concept of environmental sustainability in everyone's heart.

b. Every year the Bank conducted 4 hours of environment education sessions, in order to advance employee environmental ethics and responsibilities, maintain ecological balance, uphold respect for life, and fulfill sustainable development.

c. The Bank promoted using both sides of copy paper, and procured recycled paper; it also advanced green procurement, purchasing much more environment-friendly products with Energy Label, Water Saving Label, and Green Building Label.

(2) Status of the Bank establishing a proper environment management system according to characteristics of its sector.

The Bank periodically cleaned and waxed its working premises, cleared up waste , renewed flowers, trees and pot plants, beautified the working environment, and regularly sent patrol personnel to reinforce environment management.

(3) Status of the Bank establishing the specially-designated environment management unit or personnel for environment preservation.

The Bank had the Labor Safety Section under the Department of General Affairs, which was responsible for promoting environment education, maintaining a clean environment, etc.

28

Category Status of Practice

(4) Status of the Bank paying attention to influence of climate change on operating activities, as well as setting up its policy on energy saving, carbon reduction and greenhouse gas emission reduction.

a. The Bank set an annual goal of saving more than 2% of water, electricity and fuel expenditure, and every year replaced 10% of high electricity-consuming appliances with energy-saving equipment.

b. The Bank continued to implement garbage sorting, garbage reduction, and resource recycling.

3. Safeguarding social interest

(1) Status of the Bank observing pertinent labor laws and regulations, protecting legal rights and interests of employees, and establishing proper management manners and procedures.

a. In accordance with the business nature and Article 70 of the Labor Standards Act, the Bank established work rules on the following matters, and reported to the governing authority, Department of Labor of the Taipei City Government, for reference before they were publicly announced:

(a) Work hours, time off, leave of absence, national holidays, special leave of absence, and methods for arranging shifts for doing continuous work.

(b) Wage rates, calculation method and pay days.

(c) Overtime work.

(d) Allowances and bonuses.

(e) Disciplinary policy.

( f ) Attendance, leave taking, commending or demerits, and promotion and transfer.

(g) Recruitment, discharge, separation, withdrawal of service, and retirement.

(h) Compensation and pension for injury or disease caused by occupational accidents.

( i ) Welfare measures.

( j ) Safety and health regulations to be observed by the laborers and the employer.

(k) Methods for promoting communication and cooperation between the laborers and the employer.

( l ) Others.

b. The Bank held the “Labor-Management Meeting" in accordance with Article 83 of the Labor Standards Act and the Labor-Management Meeting Implementation Regulations:

(a) The Bank held at least one periodical Labor-Management Meeting every three months.

(b) Besides the aforesaid periodical meeting, the Bank also held the Interim Labor-Management Meeting when necessary.

(c) The Bank's Executive Vice-President in charge of human resources and the labor union's Chairperson took turns serving as the chair of the Labor-Management Meeting, to maintain equity and impartiality of the meeting.

(d) The Bank sent the meeting notice 7 days before the Labor-Management Meeting was held; when there was a proposal, the meeting staff delivered it to Labor-Management Meeting representatives 3 days before the meeting was held; and then the Labor-Management Meeting was held at the time and location stated on the meeting notice.

(e) More than one half of the representatives from each side of the laborers and the management had to attend the meeting, and a resolution was adopted after a consensus had been reached by negotiation; if a consensus could not be reached by negotiation, a resolution would be adopted by consent of at least three fourths of present representatives.

( f ) The essence of a meeting resolution lies on its execution, so both sides actively participated in execution and promotion of every resolution, did the best to coordinate with related units, and had items under the resolution timely completed.

29

公司治理報告

Status of Corporate G

overnance Practice

Category Status of Practice

(2) Status of the Bank offering employees with a safe and healthful work environment, and periodically providing employees with safety and health education.

a. The Bank established the “Working Directions for Labor Safety and Health" pursuant to Article 25 of the Labor Safety and Health Act, which shall be strictly followed by all employees, to jointly prevent various incidents from happening.

b. The Bank established the “Labor Safety and Health Management Notice" pursuant to Article 12-1 of the Labor Safety and Health Organization Management and Automatic Inspection Regulations, to fully implement which the Bank further established the “Labor Safety and Health Management Plan," to increase the sense of safety and health of all employees, and safeguard their safety and health.

c. Every 3 years the Bank held a 3-hour on-job safety and health training session for employees.

(3) Status of the Bank establishing and announcing its consumer rights policy, as well as providing a transparent and effective consumer complaint procedure for its products and service.

a. When the Bank reached pertinent contracts with customers, clauses or words relating to the review period and personal information protection were always included, and the complaint hotline, fax and website also provided.

b. Every quarter the customer service center produced the Statistical Table by Category and the Detailed List of Cases Processed of phone calls and complaints received, for perusal of the management, as well as for continuous follow-up till improvement.

c. On its website the Bank set up the three channels of executive mailbox, customer complaint and e-mail to communicate with the public, where customer requirements and suggestions would be timely processed by responsible units according to their functions and duties.

(4) Status of the Bank working with suppliers to jointly strive for advancing corporate social responsibility.

On May 29, 2011 the Bank, Franklin Templeton Investments and National Taiwan Museum jointly held the fair of “Colorful LOHAS and Public Charity-Land Bank doubles your love," where the Bank's honorable guests and the general public, totaling 1,000 people, were invited to participate. The event received very positive feedback and great advertising results.

(5) Status of the Bank participating in activities of community development and public charity groups via commercial events, commoditydonation, corporate volunteer service or other free professional services.

a. On January 24, 2011 the Bank and Chinese Calligraphy Association jointly held the Chinese New Year writing and rewarding event of “Culture in Every House, Good Year for Everyone" at the doorway of the Department of Business.

b. During the year the Bank supported and promoted sports activities to help take deeper roots, separately held teenager badminton and tennis summer camps in central Taiwan and northern Taiwan, and sponsored school sports teams competing abroad, which have earned great compliments of society.

c. The Bank continued to care for underrepresented groups and actively returned favor of society by actual practice, such as responding to the 2011 “United Way One-Day Donation Campaign" held by United Way of Taiwan, raising over NT$1,400,000 in total; the Bank also participated in the event of “22nd Year-End Party for the Homeless and Elderly Living Alone" held by Genesis Social Welfare Foundation in 2011, where the Bank was the first to donate NT$300,000 and called for response of kind people; to fulfill the spirit of “all for one, one for all," the Bank donated NT$1,000,000 to the Social Welfare Department of the New Taipei City Government to support underrepresented families that incurred emergency, which greatly presented the Bank's public-spirited image.

d. To celebrate the ROC Centennial, given a vision of greeting the bright future hand in hand, on November 5 at South North Square in front of the Office of the President, the Bank held the event of “Glorious 100: ROC Centennial Finance Carnival," where it transferred all cash and Uniform Invoices donated by people to 6 public interest groups like Genesis Social Welfare Foundation.

e. The Bank granted totally NT$2,090,000 in scholarship to sponsor students of 27 public and privates schools.

30

Category Status of Practice

f. The Bank retained Small and Medium Enterprises Joint Consultation Center to produce the Tax Health Check DIY CD for companies, and helped small and medium enterprises understand management problems and promptly adopt responsive measures, reaching the goal of win-win between the Bank and borrowers.

g. Financial consultants of the Bank were invited to serve as lecturers for the 2011 “Walk in Campus and Community: Financial Knowledge Promotion Campaign" sponsored by the Financial Supervisory Commission of the Executive Yuan, assisting the government in making financial education popular and take deeper roots, as well as promoting sound consumption and financial planning concepts.

4. Enhancing information disclosure

(1) Way of the Bank disclosing relevant and reliable corporate social responsibility information.

Information of the Bank relating to corporate social responsibility was disclosed on “Corporate Governance Section" of the Bank website.

(2) Status of the Bank drafting the corporate social responsibility report and disclosing promotion of corporate social responsibility.

None.

5. If the Bank establishes its own corporate social responsibility guideline pursuant to the “Corporate Social Responsibility Best-Practice Principles for Listed Companies," the Bank is to clearly state any operating deviation from the guideline: None.

6. Other important information that enhances understanding of the Bank's corporate social responsibility practice (such as the system and measures adopted by the Bank and their performance status for environment protection, community participation, social contribution, social service, public interest, consumer rights and interests, human rights, safety and health, and other social responsibility activities):

The ROC Government was the sole shareholder of the Bank, and the Bank not only followed the government policy to promote various special and relief loans, but also paid attention to fulfillment of its social responsibility as a corporate citizen; under the idea of “What is taken from society is used on society," the Bank spared no efforts to continuously sponsor, encourage and support care for community environment protection, public interest activities, academics and culture, underrepresented groups, and the others, with actual operations detailed as the above-mentioned points.

7. Where the Bank's product or corporate social responsibility report passes a related examination institution's inspection standards, it shall be clearly stated: None.

31

公司治理報告

Status of Corporate G

overnance Practice

Operating OverviewDeposits

Loans

Trusts

Wealth Management

Foreign Exchange and International Banking

Electronic Banking

Financial Planning and Investment

Securities

34

34

36

36

36

37

34

A humble friend. Faithful and kind.

Listening carefully, serving with heart, Land Bank wins public praise.

37

37

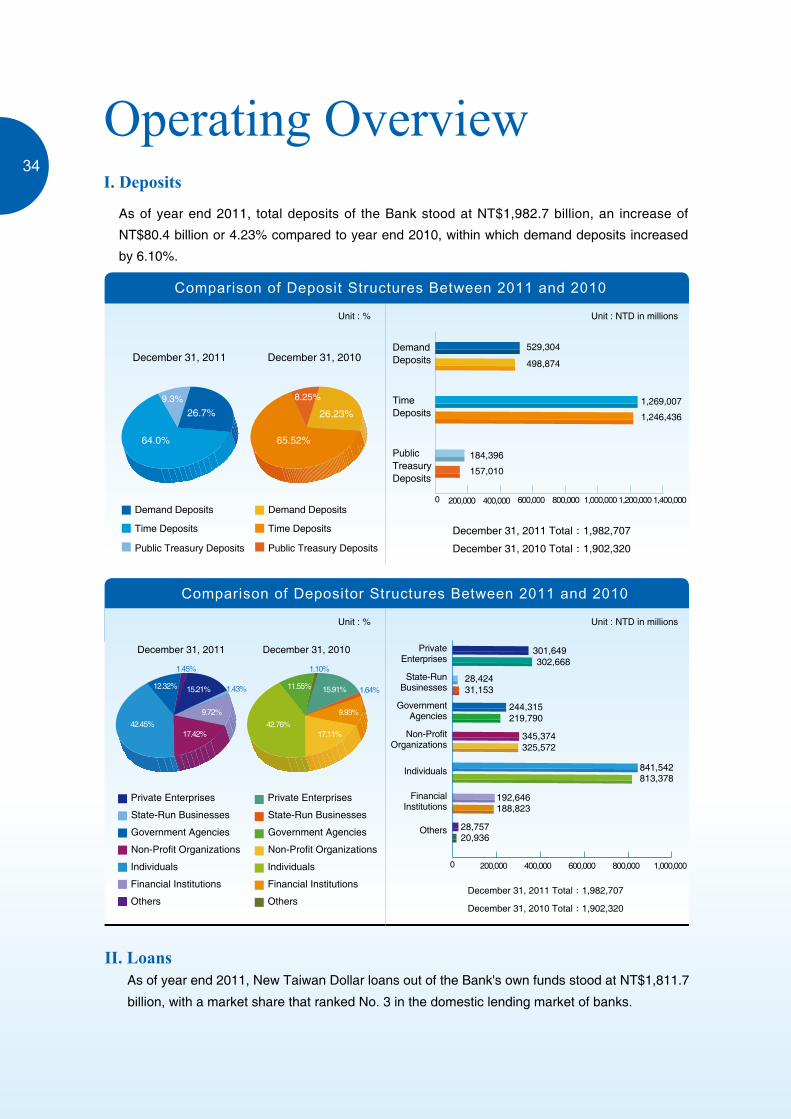

Operating OverviewI. Deposits

As of year end 2011, total deposits of the Bank stood at NT$1,982.7 billion, an increase of

NT$80.4 billion or 4.23% compared to year end 2010, within which demand deposits increased

by 6.10%.

II. LoansAs of year end 2011, New Taiwan Dollar loans out of the Bank's own funds stood at NT$1,811.7

billion, with a market share that ranked No. 3 in the domestic lending market of banks.

Demand Deposits

Demand DepositsDecember 31, 2011

December 31, 2011 Total:1,982,707

December 31, 2010 Total:1,902,320

December 31, 2010

9.3% 8.25%

64.0% 65.52%

26.7% 26.23%

Unit : % Unit : NTD in millions

Demand Deposits

Time Deposits

Time Deposits

Time Deposits

Public Treasury Deposits

Public Treasury Deposits

0 200,000

529,304

184,396

1,269,007

1,246,436

498,874

157,010

400,000 600,000 800,000 1,000,000 1,200,000 1,400,000

Public Treasury Deposits

Comparison of Deposit Structures Between 2011 and 2010

December 31, 2011

December 31, 2011 Total:1,982,707

December 31, 2010 Total:1,902,320

December 31, 2010

Unit : % Unit : NTD in millions

State-Run Businesses

Private Enterprises

Individuals

Government Agencies

Financial Institutions

Non-Profit Organizations

Others

State-Run Businesses

Private Enterprises

Individuals

Government Agencies

Financial Institutions

Non-Profit Organizations

Others

0 200,000

301,649

28,424

244,315

345,374

841,542

192,646

28,757

813,378

188,823

20,936

302,668

31,153

219,790

325,572

400,000 600,000 800,000 1,000,000

Comparison of Depositor Structures Between 2011 and 2010

15.21% 15.91%

9.72% 9.93%42.45% 42.76%

12.32% 11.55%

17.42% 17.11%

1.43% 1.64%

1.45% 1.10%State-Run

Businesses

Private Enterprises

Individuals

Government Agencies

Financial Institutions

Non-Profit Organizations

Others

34

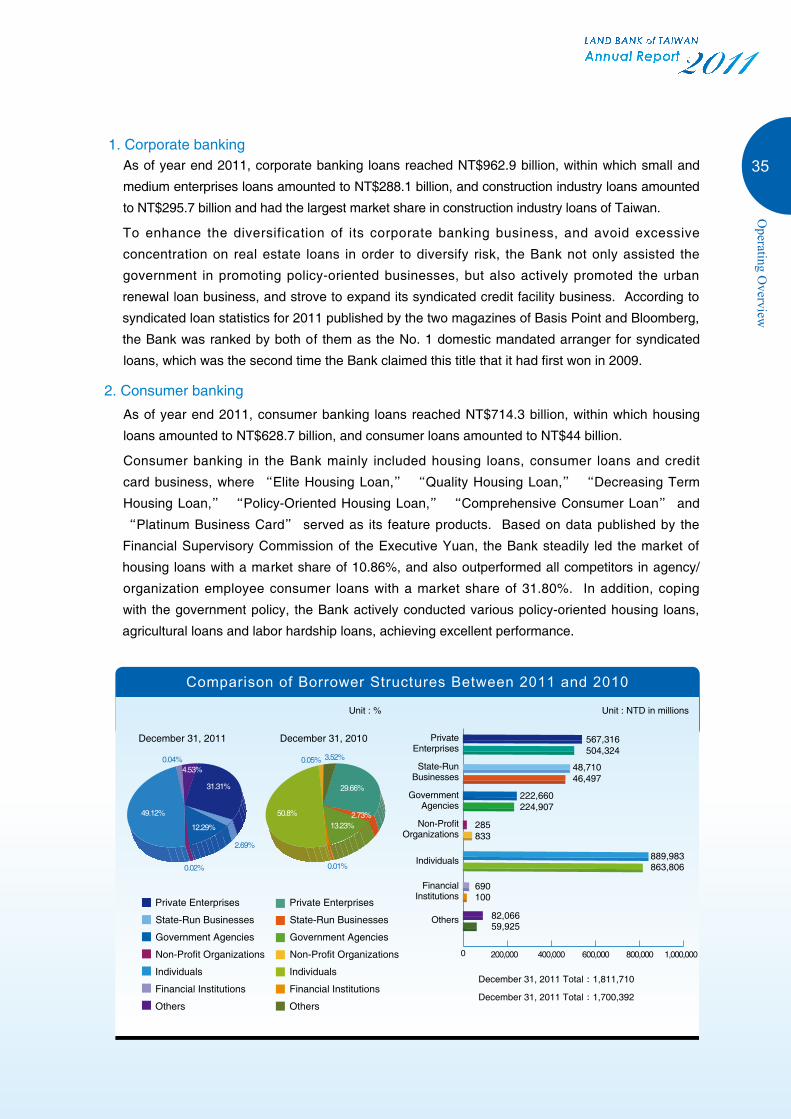

1. Corporate bankingAs of year end 2011, corporate banking loans reached NT$962.9 billion, within which small and

medium enterprises loans amounted to NT$288.1 billion, and construction industry loans amounted

to NT$295.7 billion and had the largest market share in construction industry loans of Taiwan.

To enhance the diversification of its corporate banking business, and avoid excessive

concentration on real estate loans in order to diversify risk, the Bank not only assisted the

government in promoting policy-oriented businesses, but also actively promoted the urban

renewal loan business, and strove to expand its syndicated credit facility business. According to

syndicated loan statistics for 2011 published by the two magazines of Basis Point and Bloomberg,

the Bank was ranked by both of them as the No. 1 domestic mandated arranger for syndicated

loans, which was the second time the Bank claimed this title that it had first won in 2009.

2. Consumer banking

As of year end 2011, consumer banking loans reached NT$714.3 billion, within which housing

loans amounted to NT$628.7 billion, and consumer loans amounted to NT$44 billion.

Consumer banking in the Bank mainly included housing loans, consumer loans and credit

card business, where “Elite Housing Loan," “Quality Housing Loan," “Decreasing Term

Housing Loan," “Policy-Oriented Housing Loan," “Comprehensive Consumer Loan" and

“Platinum Business Card" served as its feature products. Based on data published by the

Financial Supervisory Commission of the Executive Yuan, the Bank steadily led the market of

housing loans with a market share of 10.86%, and also outperformed all competitors in agency/

organization employee consumer loans with a market share of 31.80%. In addition, coping

with the government policy, the Bank actively conducted various policy-oriented housing loans,

agricultural loans and labor hardship loans, achieving excellent performance.

December 31, 2011

December 31, 2011 Total:1,811,710

December 31, 2011 Total:1,700,392

December 31, 2010

Unit : % Unit : NTD in millions

0 200,000

567,316

48,710

222,660

285

889,983

690

82,066

863,806

100

59,925

504,324

46,497

224,907

833

400,000 600,000 800,000 1,000,000

Comparison of Borrower Structures Between 2011 and 2010

31.31%

2.73%49.12% 50.8%

4.53%

29.66%

12.29% 13.23%

0.04%

0.02%

2.69%

3.52%0.05%

0.01%

State-Run Businesses

Private Enterprises

Individuals

Government Agencies

Financial Institutions

Non-Profit Organizations

Others

State-Run Businesses

Private Enterprises

Individuals

Government Agencies

Financial Institutions

Non-Profit Organizations

Others

State-Run Businesses

Private Enterprises

Individuals

Government Agencies

Financial Institutions

Non-Profit Organizations

Others

35

Operating O

verview

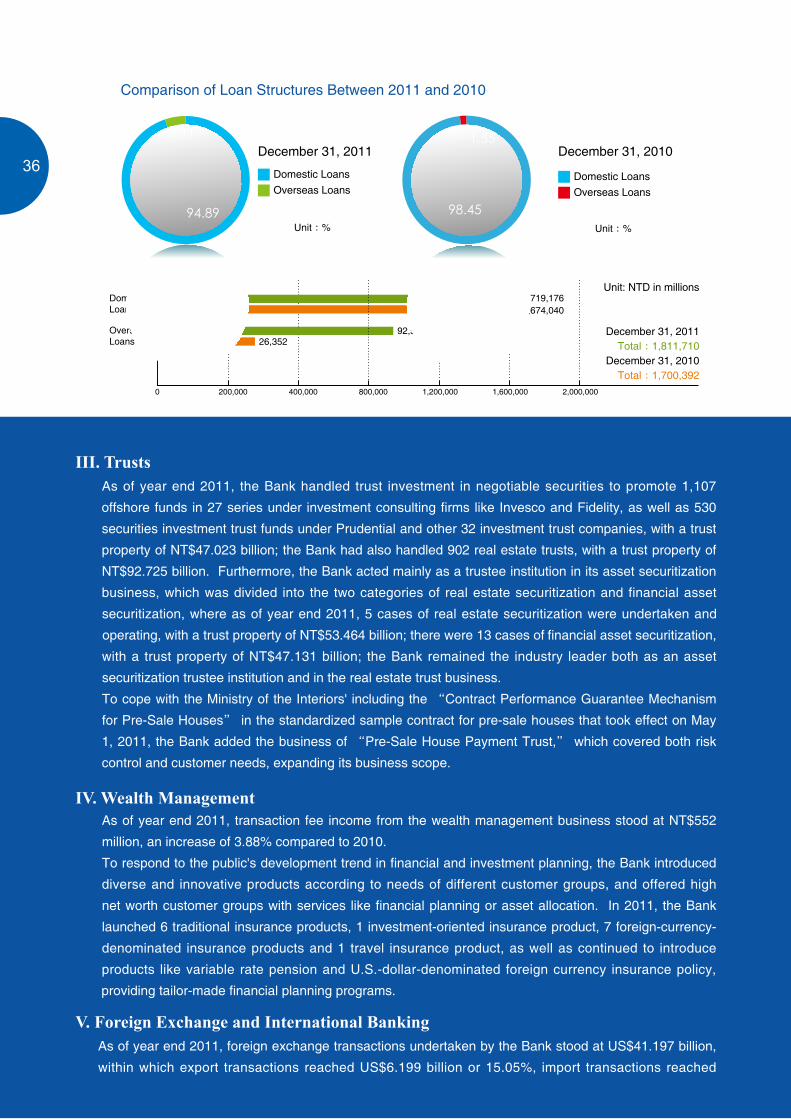

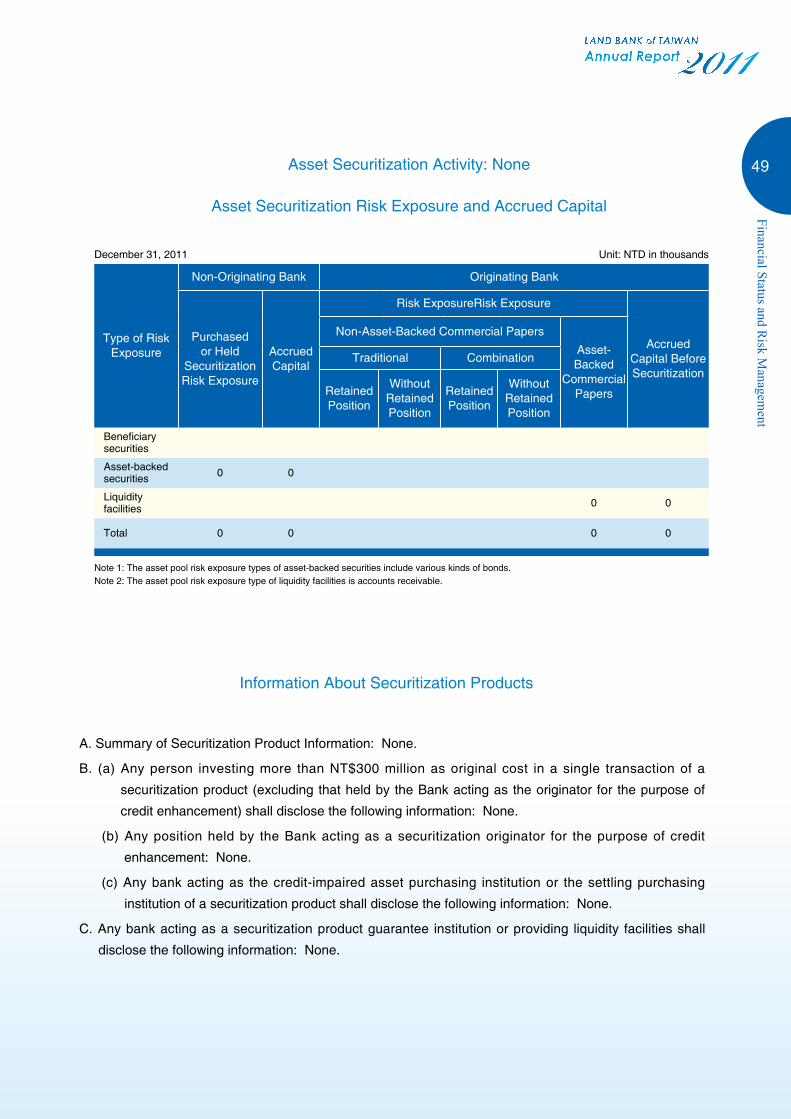

III. TrustsAs of year end 2011, the Bank handled trust investment in negotiable securities to promote 1,107

offshore funds in 27 series under investment consulting firms like Invesco and Fidelity, as well as 530

securities investment trust funds under Prudential and other 32 investment trust companies, with a trust

property of NT$47.023 billion; the Bank had also handled 902 real estate trusts, with a trust property of

NT$92.725 billion. Furthermore, the Bank acted mainly as a trustee institution in its asset securitization

business, which was divided into the two categories of real estate securitization and financial asset

securitization, where as of year end 2011, 5 cases of real estate securitization were undertaken and

operating, with a trust property of NT$53.464 billion; there were 13 cases of financial asset securitization,

with a trust property of NT$47.131 billion; the Bank remained the industry leader both as an asset

securitization trustee institution and in the real estate trust business.

To cope with the Ministry of the Interiors' including the “Contract Performance Guarantee Mechanism

for Pre-Sale Houses" in the standardized sample contract for pre-sale houses that took effect on May

1, 2011, the Bank added the business of “Pre-Sale House Payment Trust," which covered both risk

control and customer needs, expanding its business scope.

IV. Wealth ManagementAs of year end 2011, transaction fee income from the wealth management business stood at NT$552

million, an increase of 3.88% compared to 2010.

To respond to the public's development trend in financial and investment planning, the Bank introduced

diverse and innovative products according to needs of different customer groups, and offered high

net worth customer groups with services like financial planning or asset allocation. In 2011, the Bank

launched 6 traditional insurance products, 1 investment-oriented insurance product, 7 foreign-currency-

denominated insurance products and 1 travel insurance product, as well as continued to introduce

products like variable rate pension and U.S.-dollar-denominated foreign currency insurance policy,

providing tailor-made financial planning programs.

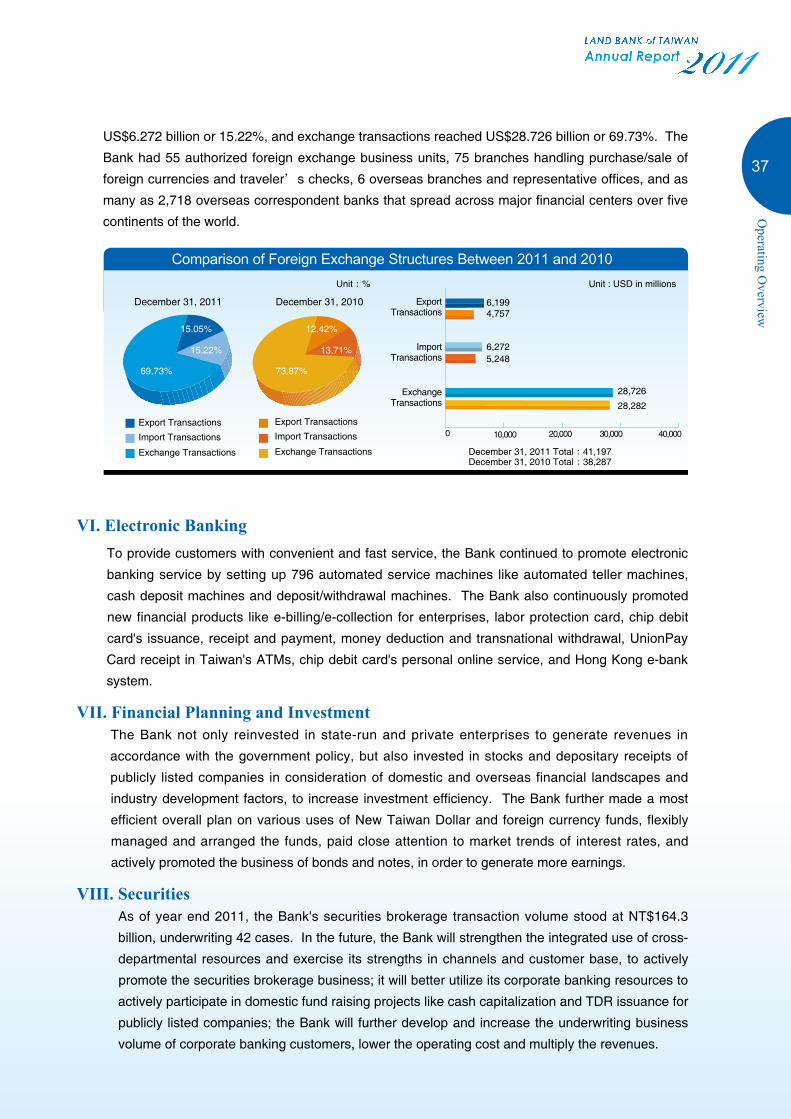

V. Foreign Exchange and International BankingAs of year end 2011, foreign exchange transactions undertaken by the Bank stood at US$41.197 billion,

within which export transactions reached US$6.199 billion or 15.05%, import transactions reached

Unit: NTD in millions

December 31, 2011 Total:1,811,710

December 31, 2010 Total:1,700,392

1,600,0001,200,000800,000400,000200,0000

Domestic Loans

1,719,1761,674,040

92,53426,352

Overseas Loans

2,000,000

Unit:%

December 31, 2011

Domestic LoansOverseas Loans

Comparison of Loan Structures Between 2011 and 2010

94.89

5.11December 31, 2010

Domestic LoansOverseas Loans

98.45

1.55

Unit:%

36

US$6.272 billion or 15.22%, and exchange transactions reached US$28.726 billion or 69.73%. The

Bank had 55 authorized foreign exchange business units, 75 branches handling purchase/sale of

foreign currencies and traveler´s checks, 6 overseas branches and representative offices, and as

many as 2,718 overseas correspondent banks that spread across major financial centers over five

continents of the world.

VI. Electronic BankingTo provide customers with convenient and fast service, the Bank continued to promote electronic

banking service by setting up 796 automated service machines like automated teller machines,

cash deposit machines and deposit/withdrawal machines. The Bank also continuously promoted

new financial products like e-billing/e-collection for enterprises, labor protection card, chip debit

card's issuance, receipt and payment, money deduction and transnational withdrawal, UnionPay

Card receipt in Taiwan's ATMs, chip debit card's personal online service, and Hong Kong e-bank

system.

VII. Financial Planning and InvestmentThe Bank not only reinvested in state-run and private enterprises to generate revenues in

accordance with the government policy, but also invested in stocks and depositary receipts of

publicly listed companies in consideration of domestic and overseas financial landscapes and

industry development factors, to increase investment efficiency. The Bank further made a most

efficient overall plan on various uses of New Taiwan Dollar and foreign currency funds, flexibly

managed and arranged the funds, paid close attention to market trends of interest rates, and

actively promoted the business of bonds and notes, in order to generate more earnings.

VIII. SecuritiesAs of year end 2011, the Bank's securities brokerage transaction volume stood at NT$164.3

billion, underwriting 42 cases. In the future, the Bank will strengthen the integrated use of cross-

departmental resources and exercise its strengths in channels and customer base, to actively

promote the securities brokerage business; it will better utilize its corporate banking resources to

actively participate in domestic fund raising projects like cash capitalization and TDR issuance for

publicly listed companies; the Bank will further develop and increase the underwriting business

volume of corporate banking customers, lower the operating cost and multiply the revenues.

Export Transactions

Import Transactions

Exchange Transactions

Export Transactions

Export Transactions

December 31, 2011 Total:41,197December 31, 2010 Total:38,287

15.05% 12.42%

69.73% 73.87%

15.22% 13.71%

Unit:% Unit : USD in millions

Import Transactions

Import Transactions

Exchange Transactions

Exchange Transactions

0

6,199

6,272

28,726

28,282

4,757

5,248

10,000 20,000 30,000 40,000

Comparison of Foreign Exchange Structures Between 2011 and 2010

Export Transactions

Import Transactions

Exchange Transactions

December 31, 2011 December 31, 2010

37

Operating O

verview

Financial Status and Risk ManagementCondensed Consolidated Balance Sheets and Income Statements for the Last Five Years

Financial Analysis for the Last Five Years

Risk Management

Financial Statements

40

56

41

45

40

An active planner. Precise execution.Pushing organizational reengineering, building a culture of marketing, Land Bank fulfills its social responsibility.

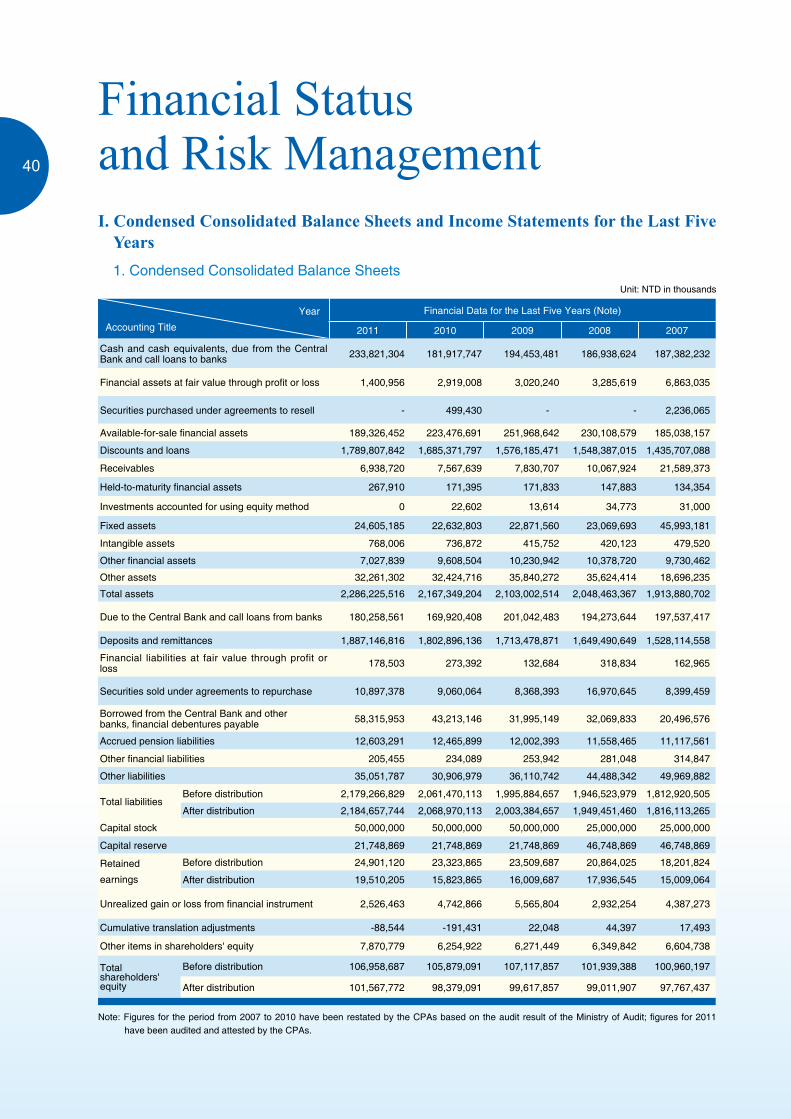

I. Condensed Consolidated Balance Sheets and Income Statements for the Last Five Years1. Condensed Consolidated Balance Sheets

Unit: NTD in thousands

Year

Accounting Title

Financial Data for the Last Five Years (Note)

2011 2010 2009 2008 2007

Cash and cash equivalents, due from the Central Bank and call loans to banks 233,821,304 181,917,747 194,453,481 186,938,624 187,382,232

Financial assets at fair value through profit or loss 1,400,956 2,919,008 3,020,240 3,285,619 6,863,035

Securities purchased under agreements to resell - 499,430 - - 2,236,065

Available-for-sale financial assets 189,326,452 223,476,691 251,968,642 230,108,579 185,038,157

Discounts and loans 1,789,807,842 1,685,371,797 1,576,185,471 1,548,387,015 1,435,707,088

Receivables 6,938,720 7,567,639 7,830,707 10,067,924 21,589,373

Held-to-maturity financial assets 267,910 171,395 171,833 147,883 134,354

Investments accounted for using equity method 0 22,602 13,614 34,773 31,000

Fixed assets 24,605,185 22,632,803 22,871,560 23,069,693 45,993,181

Intangible assets 768,006 736,872 415,752 420,123 479,520

Other financial assets 7,027,839 9,608,504 10,230,942 10,378,720 9,730,462

Other assets 32,261,302 32,424,716 35,840,272 35,624,414 18,696,235

Total assets 2,286,225,516 2,167,349,204 2,103,002,514 2,048,463,367 1,913,880,702

Due to the Central Bank and call loans from banks 180,258,561 169,920,408 201,042,483 194,273,644 197,537,417

Deposits and remittances 1,887,146,816 1,802,896,136 1,713,478,871 1,649,490,649 1,528,114,558

Financial liabilities at fair value through profit or loss 178,503 273,392 132,684 318,834 162,965

Securities sold under agreements to repurchase 10,897,378 9,060,064 8,368,393 16,970,645 8,399,459

Borrowed from the Central Bank and other banks, financial debentures payable 58,315,953 43,213,146 31,995,149 32,069,833 20,496,576

Accrued pension liabilities 12,603,291 12,465,899 12,002,393 11,558,465 11,117,561

Other financial liabilities 205,455 234,089 253,942 281,048 314,847

Other liabilities 35,051,787 30,906,979 36,110,742 44,488,342 49,969,882

Total liabilitiesBefore distribution 2,179,266,829 2,061,470,113 1,995,884,657 1,946,523,979 1,812,920,505

After distribution 2,184,657,744 2,068,970,113 2,003,384,657 1,949,451,460 1,816,113,265

Capital stock 50,000,000 50,000,000 50,000,000 25,000,000 25,000,000

Capital reserve 21,748,869 21,748,869 21,748,869 46,748,869 46,748,869

Retained

earnings

Before distribution 24,901,120 23,323,865 23,509,687 20,864,025 18,201,824

After distribution 19,510,205 15,823,865 16,009,687 17,936,545 15,009,064

Unrealized gain or loss from financial instrument 2,526,463 4,742,866 5,565,804 2,932,254 4,387,273

Cumulative translation adjustments -88,544 -191,431 22,048 44,397 17,493

Other items in shareholders' equity 7,870,779 6,254,922 6,271,449 6,349,842 6,604,738

Total shareholders' equity

Before distribution 106,958,687 105,879,091 107,117,857 101,939,388 100,960,197

After distribution 101,567,772 98,379,091 99,617,857 99,011,907 97,767,437

Note: Figures for the period from 2007 to 2010 have been restated by the CPAs based on the audit result of the Ministry of Audit; figures for 2011 have been audited and attested by the CPAs.

Financial Status and Risk Management40

2. Condensed Consolidated Income StatementsUnit: NTD in thousands

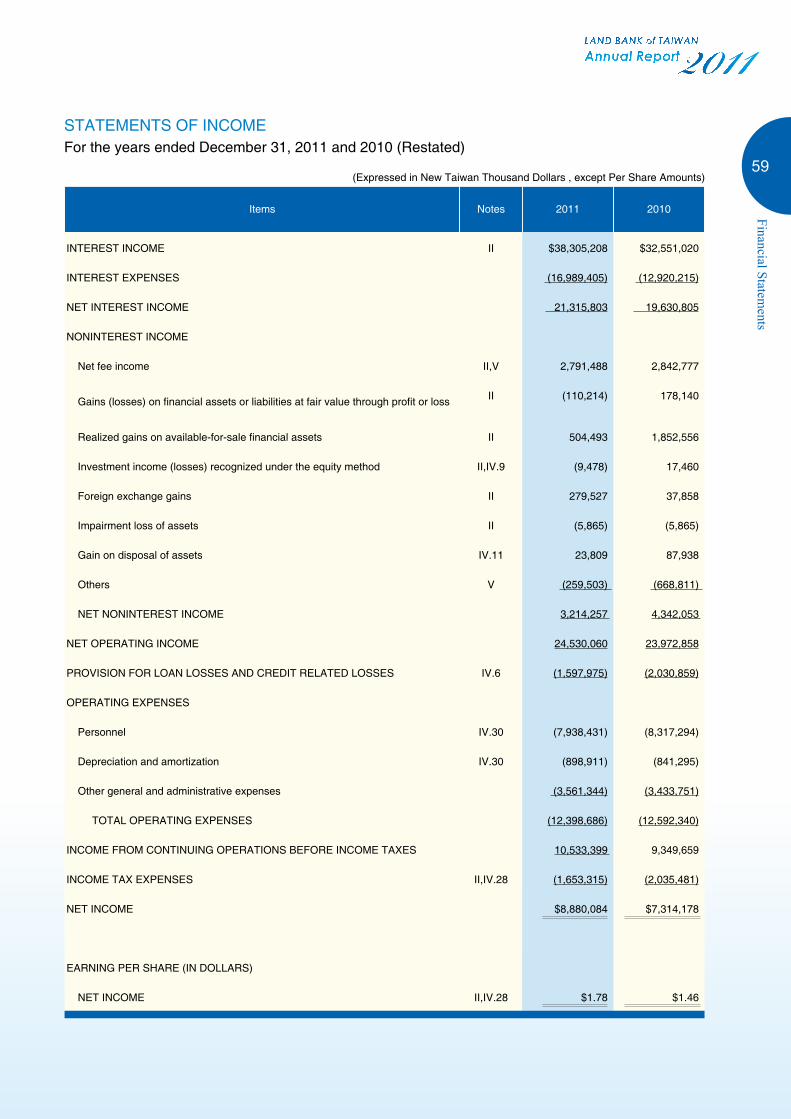

Year Accounting Title

Financial Data for the Last Five Years (Notes)

2011 2010 2009 2008 2007

Net interest income 21,315,803 19,630,805 16,329,911 18,708,307 17,006,876

Net non-interest income 3,214,257 4,342,053 5,676,611 5,655,608 7,947,092

Net operating income 24,530,060 23,972,858 22,006,522 24,363,915 24,953,968

Provision for loan losses 1,597,975 2,030,859 1,665,363 3,822,472 4,181,626

Operating expenses 12,398,686 12,592,340 12,167,781 13,001,123 13,119,186

Income before income tax 10,533,399 9,349,659 8,173,378 7,540,320 7,653,156

Income tax expense (or benefit) 1,653,315 2,035,481 2,600,236 1,685,359 1,267,636

Net income 8,880,084 7,314,178 5,573,142 5,854,961 6,385,520

Earnings per share 1.78 1.46 1.11 1.17 1.28

Notes: 1. Figures for the period from 2007 to 2010 have been restated by the CPAs based on the audit result of the Ministry of Audit; figures for 2011 have been audited and attested by the CPAs.

2. No interest capitalization occurred in the above years.

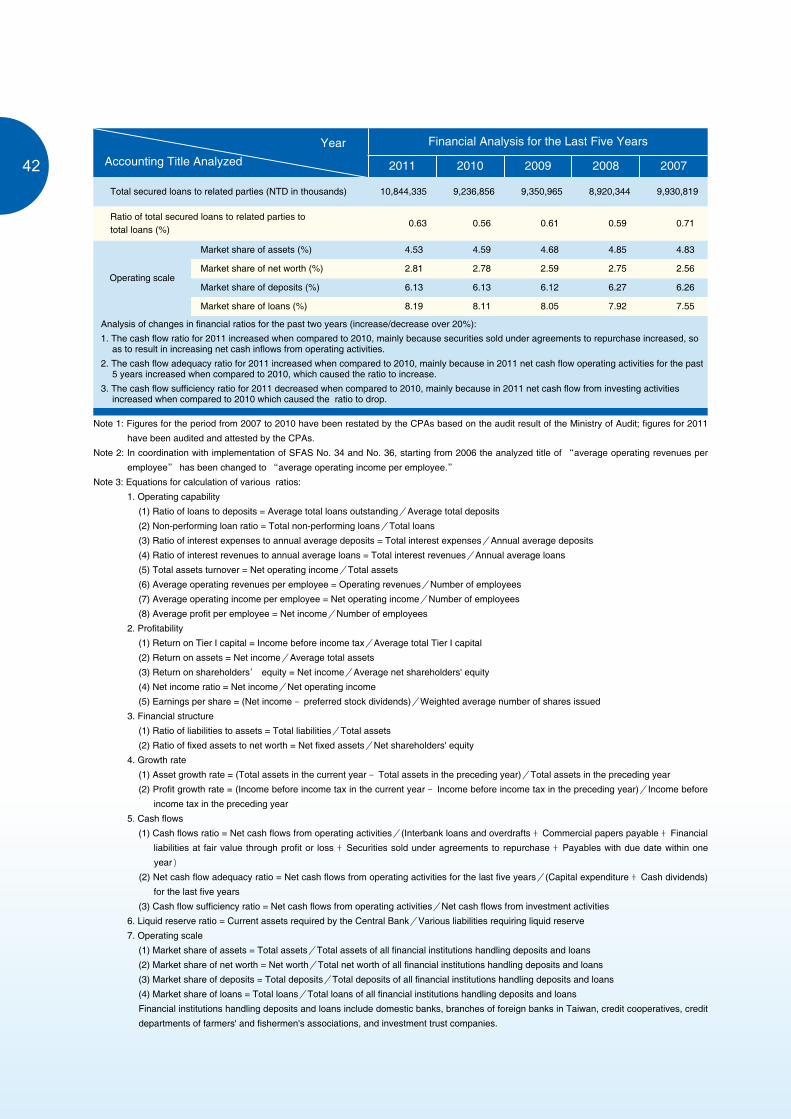

II. Financial Analysis for the Last Five YearsUnit: NTD in thousands;%

YearAccounting Title Analyzed

Financial Analysis for the Last Five Years

2011 2010 2009 2008 2007

Operating capability

Ratio of deposits to loans (%) 96.25 94.68 93.01 94.82 94.87

Non-performing loan ratio (%) 0.29 0.43 0.79 1.00 1.15

Ratio of interest expenses to annual average deposits (%) -0.88 -0.69 0.90 2.16 2.05

Ratio of interest revenues to annual average loans (%) 2.21 2.00 2.12 3.71 3.66

Total assets turnover (times) 0.01 0.01 0.01 0.01 0.01

Average operating income per

employee (NTD in thousands)4,246.16 4,182.29 3,694.23 4,191.28 4,315.80

Average profit per employee (NTD in

thousands)1,537.14 1,276.03 935.56 1,007.22 1,104.38

Profitability

Return on Tier I capital (%) 12.31 11.11 9.61 8.95 9.12

Return on assets (%) 0.40 0.34 0.27 0.30 0.34

Return on shareholders´ equity (%) 8.88 7.39 5.61 5.95 6.58

Net income ratio (%) 36.20 30.51 25.32 24.03 25.59

Earnings per share (NTD) 1.78 1.46 1.11 2.34 2.55

Financial structureRatio of liabilities to assets (%) 95.56 95.46 95.26 95.17 94.89

Ratio of fixed assets to shareholders´ equity (%) 24.23 23.01 22.96 23.30 23.47

Growth rateAsset growth rate (%) 5.48 3.06 2.66 7.03 3.56

Profit growth rate (%) 12.66 14.39 8.40 -1.47 65.18

Cash flows

Cash flow ratio (%) 21.87 13.46 -8.11 44.00 -2.18

Cash flow adequacy ratio (%) 179.14 147.74 363.42 954.53 1,323.31

Cash flow sufficiency ratio (%) -16.57 -13.88 10.80 -17.07 3.11

Liquid reserve ratio (%) 15.33 16.87 18.33 15.50 16.72

41

Financial Status and Risk M

anagement

YearAccounting Title Analyzed

Financial Analysis for the Last Five Years

2011 2010 2009 2008 2007

Total secured loans to related parties (NTD in thousands) 10,844,335 9,236,856 9,350,965 8,920,344 9,930,819

Ratio of total secured loans to related parties to total loans (%)

0.63 0.56 0.61 0.59 0.71

Operating scale

Market share of assets (%) 4.53 4.59 4.68 4.85 4.83

Market share of net worth (%) 2.81 2.78 2.59 2.75 2.56

Market share of deposits (%) 6.13 6.13 6.12 6.27 6.26

Market share of loans (%) 8.19 8.11 8.05 7.92 7.55

Analysis of changes in financial ratios for the past two years (increase/decrease over 20%):

1. The cash flow ratio for 2011 increased when compared to 2010, mainly because securities sold under agreements to repurchase increased, so as to result in increasing net cash inflows from operating activities.

2. The cash flow adequacy ratio for 2011 increased when compared to 2010, mainly because in 2011 net cash flow operating activities for the past 5 years increased when compared to 2010, which caused the ratio to increase.

3. The cash flow sufficiency ratio for 2011 decreased when compared to 2010, mainly because in 2011 net cash flow from investing activities increased when compared to 2010 which caused the ratio to drop.

Note 1: Figures for the period from 2007 to 2010 have been restated by the CPAs based on the audit result of the Ministry of Audit; figures for 2011

have been audited and attested by the CPAs.

Note 2: In coordination with implementation of SFAS No. 34 and No. 36, starting from 2006 the analyzed title of “average operating revenues per

employee" has been changed to “average operating income per employee."

Note 3: Equations for calculation of various ratios:

1. Operating capability

(1) Ratio of loans to deposits = Average total loans outstanding/Average total deposits

(2) Non-performing loan ratio = Total non-performing loans/Total loans

(3) Ratio of interest expenses to annual average deposits = Total interest expenses/Annual average deposits

(4) Ratio of interest revenues to annual average loans = Total interest revenues/Annual average loans

(5) Total assets turnover = Net operating income/Total assets

(6) Average operating revenues per employee = Operating revenues/Number of employees

(7) Average operating income per employee = Net operating income/Number of employees

(8) Average profit per employee = Net income/Number of employees

2. Profitability

(1) Return on Tier I capital = Income before income tax/Average total Tier I capital

(2) Return on assets = Net income/Average total assets

(3) Return on shareholders´ equity = Net income/Average net shareholders' equity

(4) Net income ratio = Net income/Net operating income

(5) Earnings per share = (Net income ﹣preferred stock dividends)/Weighted average number of shares issued

3. Financial structure

(1) Ratio of liabilities to assets = Total liabilities/Total assets

(2) Ratio of fixed assets to net worth = Net fixed assets/Net shareholders' equity

4. Growth rate

(1) Asset growth rate = (Total assets in the current year ﹣Total assets in the preceding year)/Total assets in the preceding year

(2) Profit growth rate = (Income before income tax in the current year ﹣Income before income tax in the preceding year)/Income before

income tax in the preceding year

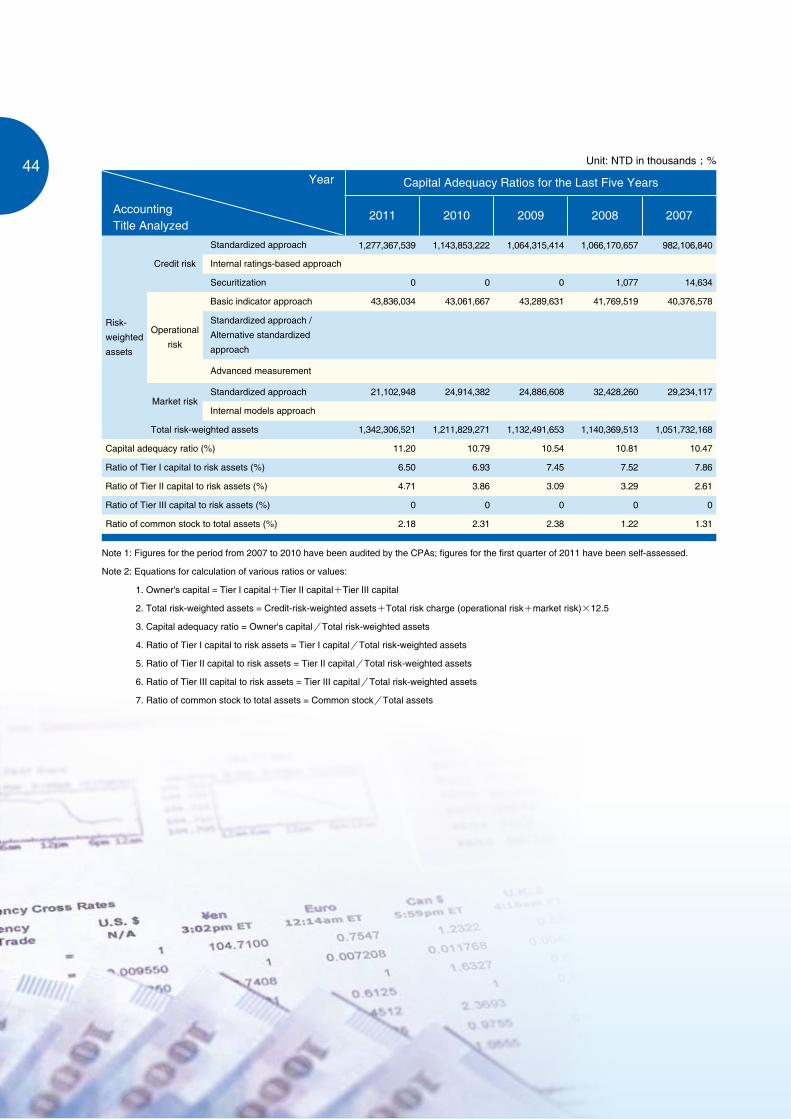

5. Cash flows