Embed Size (px)

Citation preview

1

LAGOS STATE PUBLIC FINANCIAL MANAGEMENT WORK PLAN AND MATRICES

Priority 1: BUDGETING Strategy Budgeting is a key process in translating government policies, programmes and activities into real services to the citizens. A sound budgeting process will ensure that activities funded under the budget are linked to achieving the objectives stated in the state’s policies, and that they are budgeted for with due consideration of the funding capability and limitations of the state. In other words, the budget should be policy‐based, credible, predictable, comprehensive and transparent. The budget data should be captured and accounted for in the State financial management system – which the Oracle Financials has the capacity to do. 2010 Improving budget discipline and value for money are desirable goals of any sound budgeting system. It requires political will and commitment, and systems, processes and procedures that assure high integrity in financial management. Proper implementation of the State MTSS/MTEF (budget process to commence with political office holders giving directives on priority areas in accordance with the MTSS/MTEF) is desirable; and building capacity of political office holders and technocrats on budget preparation and implementation. The systems of budget coding and accounts classification need reviewing to conform to GFS/COFOG to enhance proper financial data capture and reporting. MDAS need to introduce realistic activities into the annual budget that tie with state policy priorities. MDAs also have to render accurate and timely returns to the MEPB and STO to ensure proper monitoring and reporting on the budget. Besides, there should be emphasis on training and professionalizing the planning and budget cadre in the state to enhance efficiency. State website to provide constantly updated information on budget process, budget estimates, audited accounts, projects, govt contracts, etc. MEPB to ensure strict adherence to budget calendars which must be circulated to all stakeholders and also published on the website.The current Process Reform has recognised the need for re‐introduction of Budget Ceilings through the use of MTEF. Henceforth, adherence to the budget calendars will ensure that the House of Assembly receives and considers the budget before the end of a current year. Every stakeholder in the budget process should be trained in the understanding and interpretation of a budget speech that incorporates all the micro, macro and factors that will impact on the ability to drive a successful budget. Adopt International Public Sector Accounting Standards (IPSAS) standards on disclosure requirement

2012 At this stage of the programme implementation it is expected that structures, laws and guidelines introduced by 2010 would be fully in place and functional. The set of activities at this level will establish the platforms and systems for improving the process of budgeting in the state towards a more credible and comprehensive budgeting system. The activities will be aimed at operationalisation of a well functioning budgeting system that is capable of enhancing budget data gathering and generation of required budget reports and reporting requirements.

Key Priority Milestones Budgets are made more realistic by adopting simple and practical forecasting methods to estimate revenue and expenditure; At least 80% of the original budget is implemented as passed by the State House of Assembly.

2

Targets & Outputs Activities Responsible Agency

09 2010 2011 2012

4 1 2 3 4 1 2 3 4 1 2 3 4

Change Matrix Outcome 1 Immediate end 2010: Budget is more realistic and service delivery outcomes are in line with policy priorities. Change Matrix Outcome 2 Immediate end 2010: Improved ease and timeliness of access of the annual budget to the general public

1. Annual budget profiled by MDAs (MDA annual budget should indicate monthly and quarterly funding requirements.)

Budget profiling & execution model created. MDA staff trained in the use of budget profiling. MDAs prepare budget using new profiling model. Consolidate MDA profiled budgets.

Ministry of Economic Planning and Budgets (MEPB).

X

2. New Call Circular developed Develop new instructions for MDA’s preparation of their budget submissions. Revise budget calendar to allow for sufficient time for MDA submissions and negotiations

MEPB

(NOTE – COMBINED WITH “CALL CIRCULAR FORMATS” BELOW)

X

3. IGR Revenue forecasting model built Identify source(s) of revenue data. Identify drivers for the forecast. Build IGR revenue forecasting model. Test IGR forecasting model. MEPB staff training in use

MEPB, State Treasury Office (STO), and Lagos Internal Revenue Service (LIRS). (COMBINED WITH MACRO ECONOMIC MODEL BELOW)

X

A basic macro economic “model” is designed and used based on realistic projections/ notifications of federal releases, IGR budget, and debt financing costs for the 2011 budget

Identify and collect relevant State and national economic and financial data. Develop a fiscal strategy paper (FSP) for 2011‐2013. Get Exco approval of FSP. Use FSP as a basis for 2011 budget.

MEPB, STO (COMBINED WITH REVENUE FORECASTING MODEL 3 ABOVE)

X

4. Clear rules for budget reallocation are defined and complied with.

Revise and update guidelines for budget reallocation. MDAs sensitised on the requirements for budget reallocation

MEPB. X

5. Budget and Policy Retreats held annually for political leadership and SHA to engender budget discipline

Conduct budget preparation and policy retreat for Exco and SHA members, Perm Secs, Heads of MDAs. Hold half‐yearly budget

MEPB. X

3

Targets & Outputs Activities Responsible 09 2010 2011 2012

implementation reviews with Exco and SHA members, PSs, Heads of MDAs.

6. Costed MTSS are prepared for selected pilot Sectors based on politically approved sector envelopes derived from LSG ceilings determined by a realistic macro‐economic model.

Drafting of MTSS for selected MDAs. Stakeholder workshop on the draft MTSS. Exco approval of MTSS.

MEPB, Pilot MDAs (X‐CHECK WITH P&S)

X

7. Chart of Accounts reviewed and upgraded; staff of MDAs trained in use.

Review and upgrading of chart of accounts. Training of MDA staff on new chart of accounts and budget classification

MEPB, STO (IMPLICATION FOR MTSS COSTING ETC)

X

8. 2010 budget made available to the public by 2 months after approval, through the bookshop and website.

Publication of approved budget within 2 months of approval in State websites, Government Printer, public libraries.

MEPB. X

Call circulars are prepared in a standard format and sets out a clear and achievable budget calendars and incorporate clear frameworks and responsibilities for budget coordination.

Adoption of a timely Budget Calendar. Issuance of Budget Call Circular (for recurrent and capital estimates) by July

MEPB.

(NOTE – COMBINED WITH “NEW CALL CIRCULAR DEVELOPED” 2 ABOVE)

X

9. Increased information is provided to the SHA to support budget scrutiny and approval including macroeconomic assumptions and details of fiscal deficits and financing.

Development of formats for reporting and presenting budget information to SHA based on the PEFA requirement. Information including macroeconomic assumptions, fiscal deficit, deficit financing, debt stock, financial assets, prior year budget outturn, current years budget outturn, summarised budget data (for recurrent and capital expenditure), explanation of budget implications of new policy initiatives. Submission of budget information and documentation to SHA at least 2 months to the beginning of the next fiscal year.

MEPB.

(X‐CHECK WITH SAVI)

X

Implementation Notes: The state government will require commitment of funds and political will to implement these activities. SPARC should support with technical assistance. The state will be required to provide the required funding and logistics for these organisations, while SPARC could support technically with resources (consultants) for studies, workshops and training where necessary.

4

Targets & Outputs Activities Responsible 09 2010 2011 2012

Change Matrix Outcome 1 Intermediate end 2012: Annual budget linked to policy priorities. 1. Revised Budget Code and Chart of Accounts

(BC&CoA) Workshop to review and propose amendment to the requirements & structure of new BC&CoA. Finalise detailed BC&CoA

MEPB, STO

2. MTSS’s for all MDA’s/ sectors are costed and consistent with sector envelopes

Sector envelopes are agreed. MDA’s are trained to prioritise and cost capital projects. MDA’s are trained to prioritise and cost recurrent expenditure. MDA’s prepare prioritised and costed capital projects

MEPB

3. Multi‐year database of capital projects built and populated

Investigation of current information sources on capital projects. Agree content and location/responsibility for database. MDA’s supported to prepare information on Capital Projects for inclusion on database

MEPB, MDAs

4. Improved in‐year budget reporting and analysis Ongoing improvements to timeliness and format of budget reporting response to government needs. Train MEPB, MDA and SHA (Appropriation/PAC members and support staff) to analyse budget reports.

MEPB, STO

5. The Macro‐economic model is refined and used to determine within +/‐ 15% accuracy, the funds available for next budget year and forward 2 years for the period 2012‐1014

Review of the 2011‐2013 Fiscal Strategy Paper to 2012‐2014. FSP used for 2012 budget.

MEBP, MoF, STO

6. Costed MTSS are prepared by 8 Sectors based on politically approved sector envelopes

Preparation of MTSS for selected eight priority sectors. Stakeholder workshop on the draft MTSS. Exco approval of MTSS.

MEBP

7. Financial systems are updated/ configured to support the operational and refined BC&COA and able to support an agreed budgeting policy methodology (programme, activity based, etc).

Development or reconfiguration of IT systems software for the state PFM system integrating the updated BC&COA. Development & adoption of

MEPB, STO

5

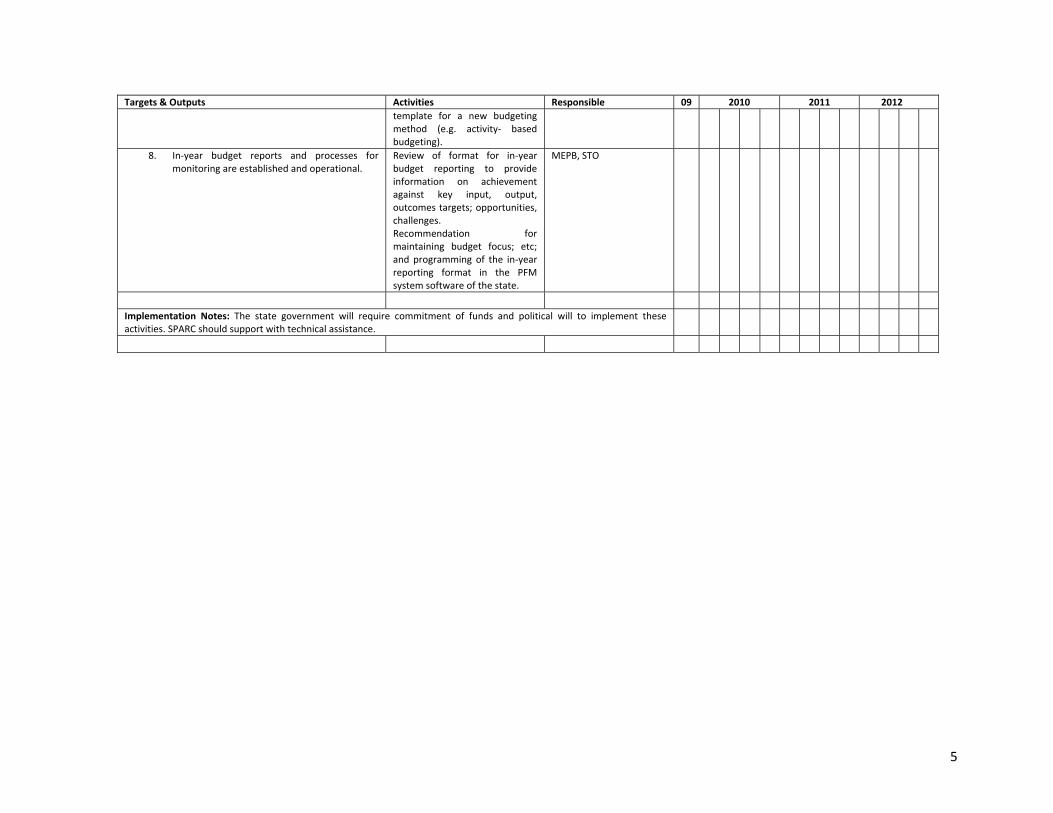

Targets & Outputs Activities Responsible 09 2010 2011 2012

template for a new budgeting method (e.g. activity‐ based budgeting).

8. In‐year budget reports and processes for monitoring are established and operational.

Review of format for in‐year budget reporting to provide information on achievement against key input, output, outcomes targets; opportunities, challenges. Recommendation for maintaining budget focus; etc; and programming of the in‐year reporting format in the PFM system software of the state.

MEPB, STO

Implementation Notes: The state government will require commitment of funds and political will to implement these activities. SPARC should support with technical assistance.

6

Priority 2: ACCOUNTING (Recording and reporting systems)

Strategy The accounting function is at the heart of the PFM system implementation. It generates and records data, as well as ensures the integrity of the PFM system. The accounting system should be such that ensures accurate and timely information for the management of the state finances. The accounting function should be closely linked to the budgeting system to ensure effective funding, implementation and reporting of the budget. An IT enabled accounting system will ensure efficiency, timeliness and accuracy of accounting information; as well as reduce the incidence of fraud. The Oracle Financials deployed by the State has interlinked applications that can produce and deliver accounting and financial reports timely and accurately as long as the data input is accurate, relevant and timely. 2010/2012 The State has already a robust financial accounting software – the Oracle Financials. Attention should be paid to accurate data capture, and effective deployment of the capabilities to enhance the accounting recording and reporting systems of the State. To this end, the capacity of STO staff and MDA accountants should be enhanced to understand and use the Oracle applications in various aspects of their work. Effort will be devoted to ensuring that MDAs get cash releases on time and in a predictable manner to enable them make payment commitments towards implementing their activities and programmes. The financial risks of parastatals and public enterprises will be better managed if their accounts are consolidated in a state‐wide public sector accounts and financial statement. This also will provide a clearer picture of the size of the Lagos State public sector balance sheet.

Key Priority Milestones The State Accounting information system is strengthened for timely routine recording, accounting and reporting of government transactions: State final accounts are produced and published from the State Accounting System within six months of end of financial year.

7

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

4 1 2 3 4 1 2 3 4 1 2 3 4 Change Matrix Outcome 1 Immediate end 2010:18 month rolling cash forecast monthly produced and used.

1. Excel based Cash Forecasting model created.

Build cash forecasting model. Train Treasury staff in use. Data capture from all sources. Progressive model improvement. Prepare notes for users on model

STO

X

2. Revised work‐plan to be used and submitted in accordance with agreed timetable in 2/3 pilot sectors to reflect profiled and seasonal resource needs.

Production and issuance of a guideline and timetable for the submission of capital expenditure workplans to reflect seasonal resource needs. Format discussed and agreed with MDAs.

MEPB, STO X X X

AG prepares cash forecasts based on profiled work‐plans.

Development of cash forecast that match profiled work‐plans STO (NOTE – COMBINED WITH WORK PLANS ‐ 2 ABOVE)

X X

3. Quarterly revenue and expenditure returns are maintained.

Preparation of format for quarterly revenue and expenditure returns. Circular issued to ensure compliance. Training of MDA accountants on the use of the returns format

STO X X X X

4. Procedures established to require parastatals, PEs and AGAs to submit annual accounts, financial budgets and activities to MEPB and MoF.

Proposal and approval of Exco directive to enforce the requirement for parastatals and public enterprises to render timely financial statements and other fiscal information to the STO & Auditor General

STO, AuG X

5. Details of parastatal, PE and AGA revenue and expenditure is recorded in the SG budget.

State PFM Law to provide for the consolidation of PE and AGA revenue and expenditure in SG budget and accounts

STO, SHA X

6. Procedures for controlling the operation of suspense accounts are established and implemented. These include limits to, and controls over suspense accounts, including approval, operation , reconciliation and retirement procedures.

Effective monitoring of MDAs’ compliance with retirement of advances by the Monitoring and Investigation Unit of the STO

STO X X

Implementation Notes: The Accountant General will be on the driving seat of these activities with SPARC providing some measure of technical assistance.

Change Matrix Outcome 1 Intermediate end 2012: New budget/cash release system implemented and working.

1. Excel based Cash Forecasting model improved.

Upgrade model to include forecast drivers. Capture source of drivers.

STO

8

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

Create a performance feed‐back loop to improve model.

2. Redesigned budget/cash release system.

Review existing procedures & processes for budget/cash releases. Hold a workshop on problems & potential solutions. Create new procedures & processes. Train stakeholders in new procedures & processes. Pilot & then implement new procedures & processes.

STO X

3. Cash flow projection and cash planning is implemented to enable timely cash releases to MDAs

Development and implementation of a software that enables routine cash‐flow planning that matches MDA spending needs.

STO, MEPB

4. Resources sent to the MDAs and primary service delivery units are published

Publication of funds released to MDAs and PSDUs on State website, newspapers and other publicly accessible media

STO, MEPB

5. Any agency that receives funding from any international body are mandated to report both budgeted and actual expenditure to the MEPB and MOF respectively for inclusion in the SG budget and accounts

Produce guidelines for reporting donor grants including receipts and expenditures to MEBP, MoF, STO. Exco directive enforcing this requirement

MEPB, STO, MoF

Implementation Notes: The STO will be leading most of the activities in collaboration with MEPB, and Tenders Board as appropriate; while SPARC provides technical support where necessary.

9

Priority 3: ACCOUNTING (Payroll Controls)

Strategy

Payroll constitutes a large portion of the government’s recurrent budget in Nigeria; sometimes the recurrent budget is more than 50% of the total government expenditure and unfortunately is prone to abuse and fraud. The integrity of the payroll system is key to the integrity of the overall PFM system and thus requires very close attention in PFM reforms. The payroll system should be reviewed and strengthened, and linked to the personnel management system and the Lagos State Oracle Financial System. 2010 The State Payroll and personnel data base is linked in Oracle Financial System. However, there is need for timely and regular updating and reconciliation of both the payroll and personnel data base at least every quarter to maintain the integrity of the system. 2012 The State Payroll system will be reviewed in great details to ensure it is functioning as intended; and recommendations for improvement made and implemented in order to keep pace with the operations of the State Financial management systems; as well as to maintain the integrity of the system.

Key Priority Milestones Payroll system and controls ensure the accuracy, timeliness and integrity in both payroll and personnel administrations, such that only bona‐fide staff of the State Service are maintained on the payroll database, in accordance with approved establishment positions and personnel records, and are paid correctly in accordance with corresponding guidelines.

10

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

4 1 2 3 4 1 2 3 4 1 2 3 4

Change Matrix Outcome 1 Immediate end 2010: Strengthened integrity of the State payroll system.

1. Quarterly Personnel and payroll data base reconciliation reports produced.

Conduct four quarterly personnel and payroll reconciliation exercises

Central Payroll Office (CPO), Office of Head of Service (OHoS). (X‐CHECK WITH PSM)

X X X X

Implementation Notes: The process should be coordinated jointly by the OHoS and CPO in the STO, with SPARC providing technical support

Change Matrix Outcome 2 Intermediate end 2012: Sustained operational functionality and integrity of the State payroll system

2. Comprehensive review of the State Payroll system implemented

Conduct a comprehensive review of the Lagos State payroll system. Produce recommendations for improvement.

CPO; STO. (X‐CHECK WITH PSM)

X X

3. Recommendations from State Payroll review implemented

Implement recommendations from payroll system review

CPO; STO.(X‐CHECK WITH PSM)

X

Implementation Notes: The CPO in conjunction with the OHoS will coordinate the activities in this dimension. SPARC could support with relevant technical resources.

11

Priority 4: ACCOUNTING (Internal Controls) Strategy Internal controls consists of systems, procedures, processes, and structures put in place to promote checks and balances, prevent fraud and ensure overall system integrity. The Lagos State PFM internal control measure is maintained by the Central Internal Audit (CIA) Department in the Ministry of Finance. The system of internal controls is to be reviewed and strengthened, and regularly checked for compliance; and there should be increasing utilisation of the Oracle Financial to enhance the internal control system of the State 2010 Emphasis here is to effectively deploy the Oracle Relational Database Management System to enhance the internal control systems of the State financial management system. 2012 A mid‐term review of the internal control reforms is envisaged by 2012 to determine the effectiveness or otherwise of the reforms introduced in 2010. Implementation of recommendations coming out of the review will help further strengthen the internal control systems of the State with more effective utilisation of the Oracle Financials.

Key Priority Milestones Internal Control measures are strengthened to prevent fraud and ensure the integrity of the State financial and accounting system: Qualified and experience accounting and internal audit staff are deployed to MDAs with adequate resources to enable the application of adequate checks and balances in financial and accounting transactions and recording.

12

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

4 1 2 3 4 1 2 3 4 1 2 3 4 Change Matrix Outcome 1 Immediate end 2010: Effective usage of the Oracle Financials to enhance the State’s internal control system.

1. Strengthening the Central Internal Audit (CIA) Department in the State.

Needs analysis of the CIA Department. Upgrading the CIA department to an office. Capacity building for the staff and Office of the Internal Auditor – training on the Oracle Financials (Note This is treated as part of Internal Audit)

Central Internal Audit Department, STO

2. Strengthening the Monitoring and Investigation Directorate of STO

Capacity building for the Monitoring and Investigation Directorate in the STO ‐ training on the Oracle Financials with emphasis on the Systems Audit

Central Internal Audit Department, STO

X X

3. Audit Committees Establishing of Internal Audit Committees in the MDAs

(Note This is treated as part of Internal Audit)) Central Internal Audit Department, MDAs

Implementation Notes: The CIA Department and STO will lead in all the activities here, while SPARC will support with training and other technical assistance.

Change Matrix Outcome 1 Intermediate end 2012: Strengthened internal controls system by full deployment of the Oracle Financials

4. Reviewed Internal Control System and a set of recommendations on further reforms by 2014.

Conduct a review of the Internal Control Functions and Systems to ascertain the effectiveness of the reforms introduced

Central Internal Audit Department, STO

X X

Implementation Notes: The Central Internal Audit Department and the Monitoring and Investigation Unit in the STO will coordinate activities with possible SPARC technical support.

13

Priority 5: REVENUE ADMINISTRATION

Strategy Internal revenue generation for most states in Nigeria is weak because of overdependence on revenues from the centre. However, Lagos State Government has recently taken measures to reform and improve its internal revenue generation which has resulted in tremendous improvements in the State’s IGR. These efforts need to be strengthened – backed by relevant legislations, funding and political support to succeed. The reform in revenue generation though driven by the LIRS should be comprehensive and seen as State‐wide effort – with all MDAs playing their appropriate roles; and revenue generation, collection and reconciliation properly linked to treasury operations of the State. 2010 The State already has an advanced internal revenue generating system, but a robust taxpayer data base that is computerised and interlinked among the revenue generating agencies and State Treasury Office should be created to enhance and fully realise the revenue potentials of the state. Besides, there should be legislations to institutionalise taxpayers’ complaints mechanism. And the Board of Internal Revenue with relevant membership constituted and given a full governance mandate over the State revenue generation and collection system. 2012 Given that legislation over compulsory registration of tax payers is not possible at the State level, persuasion, improved service delivery, joined up collaboration among all the revenue generating MDAs to harness data of service users and potential tax payers in the State should be the strategy. The focus should be to adopt measures that increase voluntary compliance by tax paying adults to register and present themselves for tax assessment.

Key Dimension Milestones Measures are in place to fully realise the revenue generation potentials of the State, State revenues are collected and accounted for in a transparent manner: Tax payers are made aware of their liabilities and the collection is fraud free.

14

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

4 1 2 3 4 1 2 3 4 1 2 3 4 Change Matrix Outcome 1 Immediate end 2010: Data base and structures for enhanced revenue administration in place.

1. A computerised and robust taxpayer database is implemented.

Establish a robust data interface mechanism linking all the revenue collecting agencies and the LIRS.

LIRS, STO, MEPB X X

2. Board of Internal Revenue Constituted and functional

Set up the State Board of Internal Revenue that has membership from other revenue generating MDAs of the State.

Office of the Governor, MoF X X X

3. Revised edict for Body of Appeal Commission to institute a permanent and functional Revenue Complaints and Information Mechanism.

Amend the State Revenue Law to institutionalise the Revenue Complaints and Information Unit.

LIRS, MoJ, MoF

X X X

Implementation Notes: The LIRS will be driving the implementation of these activities in collaboration with the STO and other relevant MDAs (MoJ, MoF, MEPB). SPARC resources will go to support technical work such as studies, training and designing of technical proposals Change Matrix Outcome 1 Intermediate end 2012: A taxpaying and voluntary compliance culture instituted in the State

4. A system is in place to encourage taxpayer registration from 18 years and above

LIRS to work with the Ministry of Science and Technology, and Lagos Bureau of Statistics (Central Statistics Department) in MEPB to compile tax payer data.

LIRS, MoST, Central Statistics Department.

X X X

5. Ongoing Tax Compliance and registration

Continuation and deepening voluntary compliance through political advocacy, institute income generating policies, taxpayer enlightenment

EXCO, LIRS

X X X

Implementation Notes: The LIRS will lead on mobilising taxpayer data base, and in conducting tax payer enlightenment programmes; while the EXCO will ensure that government institutes income generating policies and programmes that will enhance the tax base of the State.

15

Priority 6: DEBT MANAGEMENT

Strategy The debt management function is important in the risk asset management of the state – in determining the stock, classification, maturity and sustainability of the state’s debt profile and ability to advise the government properly on debt and funding decisions. The Public Finance and Debt Management Office (PFDMO) requires capacity to fully perform its functions. Its activities should dovetail into the state treasury operations and interfaced with the Federal Debt Management Office (DMO), with deep debt market knowledge 2010 There is in place a strong PFDMO but it requires major capacity building with respect to processes, systems and staff. The debt recording, reporting and management functions of the office needs support and strengthening with relevant software and hardware deployment to enable the office to fully carry out its mandate as contained in State Debt Management and PFM legislations. A systems capacity needs assessment should be carried out for the PFDMO’s to identify its material, systems, staffing and funding needs. The required working materials and capability should be procured and deployed. The State’s Debt Management Law and the PFM Law as it concerns debt management should be implemented through the production and use of appropriate regulations and procedure manuals 2012 Sustaining timely debt data capture and reconciliation will ensure the integrity of the debt management system. Therefore, standard templates will be developed for data capture; necessary equipment will be installed; and requisite staff and skills deployed to operate the system.

Key Priority Milestones There is a comprehensive and up‐to‐date record of the State external and internal debts; Debt contracting is sustainable and undertaken in line with an approved State debt policy and procedures.

16

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

4 1 2 3 4 1 2 3 4 1 2 3 4 Change Matrix Outcome 1 Immediate end 2010: Records of internal and external debt held by LSG are reliable and clearly show receipts, service payments, repayments and liabilities

1. Support to Debt recording & Management

X X X X X X

a. Process of verifying debt commitment of MDAs to be established.

Capacity of the PFDMO built to monitor MDAs commitment encumbrances through the Oracle Financials.

PFDMO X X X X X X

b Debt Sustainability analysis implemented

Capacity of the DMO built to carry out debt sustainability analysis and debt management functions.

PFDMO X X X X X X

c. Reliable quarterly reconciliations between PFDMO and FDMO spreadsheet records to be established

Design of reconciliation statement between records of PFDMO and FDMO for external debt through acquisition of appropriate software, and training of staff.

PFDMO X X X X X X

d. PFDMO staff trained in concepts of debt recording and reporting; and software for debt recording to acquired and installed.

Design training module on debt recording and reporting for relevant staff of the PFDMO. Procure debt recording software; install and operationalise debt recording software.

PFDMO X X X X X X

e. Policy to define arrears, rollovers and liabilities to be in place

Produce policy and procedure (for negotiating, approving, executing and recording) for loans, arrears, rollovers, guarantees and contingent liabilities.

PFDMO X X X X X X

f. External and internal debt as submitted by the relevant Agencies such as FDMO, STO etc are properly recorded, reported and managed

Debt recording template to include informal debt to be created. Staff trained in the new template. Recording and preparing debt using the new template. Consolidate relationship between all relevant MDAs. Use excel to calculate the debt profile

PFDMO X X X X X X

2. The debt management function is fully computerised; and data base supported by IT capability.

Conduct systems’ needs analysis. Procure recommended computer software and hardware. Deploy software and hardware to debt management functions. Train staff on software use.

PFDMO X X X

3. Contractor payment and reporting procedures are reviewed and streamlined.

Carry out review of contractor payment and reporting procedures.Produce recommendations for streamlining procedures among MDAs. Implement recommendations

PFDMO, STO X X

4. A comprehensive debt management manual is introduced which clearly identifies responsibilities, internal controls and procedures relating to approvals and reporting, based on Debt Management legislation

Review Debt Management Law and PFM Law. Produce a Debt Management Manual based on the Laws identifying responsibilities, internal controls, approvals, reporting, and other relevant procedures

PFDMO, STO X X

17

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

Implementation Notes: PFDMO will lead on all the activities in this dimension in collaboration with relevant agencies. SPARC will support with necessary technical support.

Change Matrix Outcome 1 Intermediate end 2012: Records of LSG external and internal debt and contingent liabilities are reliable. The FDMO is able to report on all loans according to criteria in PFDMO template

Spreadsheet and system for recording internal debt, external debt and contingent liabilities created.

Design spreadsheet for recording internal, external debt, and contingent liabilities. Train staff on use and population of spreadsheet.

PFDMO

Reliable monthly reconciliation of all PFDMO debt records with FDMO records / LSG accounting records

Conduct monthly reconciliation of PFDMO debt records, FDMO records, and the State accounting records (including MDAs commitments to contractors, staff salary arrears, pension arrears, unpaid bills, judgement debts, and other contingent liabilities).

PFDMO, STO

Capacity in fiscal risk evaluations built. Produce a module on fiscal risk evaluation. Training for staff of DMO on fiscal risk evaluation.

PFDMO

5. Fiscal Risk of parastatals reviewed and monitored

Review of loan commitments of parastatals.

DMD puts in place procedure to monitor parastatals’ fiscal risk.

DMO conducts monthly monitoring.

PFDMO, STO X X

The PFDMO is fully equipped and staffed.

Conduct Equipment and staffing needs assessment for PFDMO. Procure recommended required equipment. Hire or deploy required staff.

PFDMO, OHoS

Implementation Notes: PFDMO will lead on all the activities in this dimension in collaboration with relevant agencies. SPARC will support with necessary technical support

18

Priority 7: PROCUREMENT

Strategy Procurement, a major means of implementing the capital budget has been subject of abuse, and mismanagement of public funds. It is should form a critical plank of the LSG PFM reform plan. Institutional structures that support good procurement management should be strengthened such the Ministerial and State Tenders Boards. Also, the enabling legislations (the Public Procurement Law, and The Fiscal Responsibility Laws) should be enacted in the State to guide procurement practices. The Oracle Financials procurement management capabilities should be activated and utilised to facilitate the process, and accounting for procurements. 2010 A legal backing is necessary for the well functioning of State procurement system, and the already existing procurement bodies. The law will legitimise the functions of the various procurement agencies and units in the State to be set up, including the establishment of the regulatory body for procurement in the state i.e. the State Procurement Council. Procurement units need to be well staffed and staff trained. The implementation of the activities, and achievement of the targets and outputs will require the collaboration of high level agencies such as the Office of the Governor, EXCO, Ministry of Justice and the Office of the Head of Service. 2012 Having the Procurement Law in place will pave the way for the introduction of Procurement regulations and guidelines. Mechanism for the settlement of procurement disputes will be introduced. And the system of procurement in the State strengthened by adequate equipment, staffing and training of procurement staff.

Key Priority Milestones The State enacts a procurement law, Procurement practices are made in accordance with the law and procedures: State procurement is undertaken in an open and competitive manner.

19

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

4 1 2 3 4 1 2 3 4 1 2 3 4

Change Matrix Outcome 1 Immediate end 2010: . Institutions and capacity for efficient and transparent procurement system in place.

1. Legislation ‐ A new procurement law is enacted.

Finalise the draft LSG Public Procurement Bill. Hold stakeholders’ workshop for input to the Bill. Presentation to Exco for approval. Presentation to SHA for passage.

MoF, MoJ, State Tenders Board

X

2. Support to Structures a). A well constituted procurement council is established

Constitution and inauguration of State Procurement Council. EXCO, MoF X X X

b) A Procurement Regulatory Authority is established

Set up a procurement regulatory authority. Staff and equip the authority.

EXCO X X X

C) A procurement unit/department established in MDA’S

Set up procurement units in MDAs. Staff MDA procurement units. Equip MDA procurement units. Provide guidance manual for staff.

MoF, OHoS, State Tenders Board

X X X

3. Capacity of procurement officers enhanced.

Conduct training needs assessment for procurement staff. Training of staff.

. OHoS, State Tenders Board. X

Implementation Notes: Activities on procurement reforms should be championed by the State Tenders Board in collaboration with other relevant agencies including EXCO, MoJ, Office of the Head of Service (HoS). SPARC support will be required in the conduct of needs assessment for the equipment, staffing and training needs of the Procurement Agency and Units.

Change Matrix Outcome 1 Intermediate end 2012: More efficient and transparent procurement system operational in the State.

New procurement regulations and guidelines are introduced and administered by PRA.

Drafting of new Lagos State Procurement Regulations. Stakeholders’ meeting on the draft regulation. EXCO approval of Procurement Regulations. Drafting of Procurement Guidelines. EXCO approval of Procurement Guidelines.

MoF, State Tenders Board, MoJ

X

Procurement complains mechanism is established

Constitution and inauguration of State Procurement mediation committee comprising government and non‐state members

MoF, EXCO, MoJ

X X X

MDA capacity to manage transparent procurement processes is established.

Needs assessment of MDA procurement units. Equipping of units. Staffing of units. And training of staff.

MoF, State Tenders Board

X X

Review of the implementation of the procurement reforms.

Conduct of a review of the procurement reforms so far introduced. Produce recommendations. Implement recommendations.

MoF, State Tenders Board

X X

Implementation Notes: Activities on procurement reforms should be championed by the State Tenders Board in collaboration with other relevant agencies including EXCO, MoJ, and Office of the Head of Service (HoS). MoF will coordinate the constitution and inauguration of the State and Ministerial Tenders Boards, while the HoS will deploy staff to the Board’s secretariats. SPARC will support needs assessment for the equipment, staffing and training needs of the Procurement Agency and Units.

20

Priority 8: EXTERNAL AUDIT

Strategy External audit provides the scrutiny over the financial activities of the government; and is important to ensure that the accounting, recording and reporting of the state’s financial activities follow laid down laws, rules, regulations and procedures. The State’s supreme audit institution – the Office of the Auditor General is responsible for this function. In Lagos State, the ability of the Auditor General to carry out its functions is impaired by capacity constraints. The PFM reforms contemplated for the State should as a necessity seek to adequately equip, staff and fund the Auditor General’s Office. Besides, the Office should be knowledgeable about the reforms in all the aspects of the state’s PFM in order to provide effective financial oversight. 2010 The level of sophistication in the Lagos State financial management system (the Oracle Financials) requires that the Supreme Audit Institution of the State – The Office of the Auditor General should possess the requisite knowledge, skills and capacity to provide effective audit function over the State financial systems. These will include capacity to carry out systems audit, computer based audits, and forensic audits. The introduction of Audit Committees at the various MDAs will strengthen the ability of the MDAs to respond timely to audit queries. 2012 In the mid‐term, a review of the effectiveness of the measures introduced in the immediate term will carried out to ensure that structures, systems and institutional capacities are adequate and functioning. Where necessary, improvements and upgrades will be implemented.

Key Priority Milestones The Office of the Auditor General is made independent: A new law establishing the independence of the Office of the Auditor General for Lagos State is enacted and implemented.

21

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

4 1 2 3 4 1 2 3 4 1 2 3 4

Change Matrix Outcome 1 Immediate end 2010: Strengthened capacity for more effective external audit function. 1. Capacity Building and Training X X X X X

a) Programme to strengthen Capacity to plan and undertake systems based audit, computer audit techniques is established to enable the audit of Oracle Applications.

Carry out needs analysis for systems‐based audit, and computer audit techniques to determine capacity requirements. Design capacity building programme. Implement recommendations.

Office of the State Auditor General

X X X

b) Audit committee operational process reviewed and recommendations for implementation made..

Carry out a study to determine the operational processes of the Audit Committees towards introduction of Audit Committees in Lagos State. Develop recommendations. Implement recommendations. Note: Audit Committees are not relevant to External Audit.

Office of State Auditor General, Central Internal Audit Department.

c) Increased capacity of existing auditors through training on the use of relevant audit software achieved.

Conduct capacity needs assessment on the use of relevant audit software’s in the State. Develop a training plan. Train auditors on the use of software’s.

Office of the State Auditor General

X X X

2. Relevant local/ internationally accepted auditing standards adopted.

Review and identify relevant generally acceptable auditing standard for the State. Make recommendation to EXCO/PAC for approval.

Office of the State Auditor General

X X X

3. Perimeter and forensic auditing introduced Conduct an assessment of requirements for introducing perimeter and forensic auditing in the State. Propose and recommend to EXCO/PAC. Develop a programme of implementation. Implement introduction of forensic audit.

Office of the State Auditor General

X

Implementation Notes: The Auditor General will lead these activities. SPARC will assist with technical resources where necessary.Change Matrix Outcome 1 Intermediate end 2012: More efficient and effective systems of external audit in place. Audit Committee system in place and operating Review performance of Audit Committees.

Recommend improvement measures. Implement measures. Note: Audit Committees are not relevant to External Audit.

Office of the State Auditor General

Audit queries and recommendations following SHA scrutiny are followed up and addressed in a timely manner.

Develop a follow up and tracking measures for the implementation of audit queries. Implement and review measure periodically (quarterly)

Office of the State Auditor General

X

Audit scope widened beyond revenue and Identify financial activities outside the AuG’s Office of the State X

22

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

expenditure systems and performance audit to include all government financial activities.

audit programme. Obtain EXCO/PAC approval to include these activities. Amend audit programme to include all SG financial activities. Implement programme.

Auditor General

Strict adherence to the provisions of local/ international auditing standards

Review compliance with chosen generally acceptable auditing standards.

Office of the State Auditor General

The use of advance forensic audit established Review and upgrade forensic audit capability Office of the State Auditor General

Computer audit of Oracle applications, database, infrastructure and network undertaken

Develop an audit programme for Oracle applications, database, infrastructure and network. Implement programme. Develop recommendations for improvement of observed weaknesses.

Office of the State Auditor General

Implementation Notes: The state government should have responsibility for equipping and staffing the Office of the Auditor General. The AuG should ensure that funding needs are articulated and included in the relevant State budgets. SPARC could support the needs assessment of the Auditor General’s Office, and training of the staff.

23

Priority 9: INTERNAL AUDIT Strategy The internal audit function is meant to assist the chief executive or chief accounting officer of the MDA to maintain compliance of the internal controls, and laid down accounting procedures for the MDA. The internal auditors, who are staff of the Central Internal Audit Department in the MoF, are in an awkward position as they are meant to be responsible to the chief accounting officer of the MDA they work in. More often than not the internal auditors are incapable of standing up to the chief accounting officer on issues that contravene proper procedures because they are usually junior officers. For the internal audit function to be effective the internal auditors must be seen to be independent; and their functions should compliment those of the Auditor General of the State 2010 The internal audit function is part of the responsibility of the Central Internal Audit Department in Lagos State. The Department selects and posts internal auditors to MDAs. The internal audit function can be made to function better by introducing measures for improvement. There is need to create a professional cadre of internal auditors, who are trained and supported by the CIAD to function properly. To guide their work, internal audit regulations, manual and guidelines will be introduced. While audit committees are proposed to review and take action on the reports and queries of the internal auditor at the MDA level. 2012 The internal audit staff be well trained, and posted to the MDAs. The training curriculum will be designed by the Central Internal Audit Department with technical support from SPARC. Also, SPARC could support the training of the internal audit staff. The training of the internal auditors should result in their certification after completion of a certain level of training and examination.

Key Priority Milestones The internal audit function is strengthened with a new professional cadre of internal auditors, The function will be managed by a professional head, Deployed within MDAs and report regularly to an Audit Committee.

24

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

4 1 2 3 4 1 2 3 4 1 2 3 4

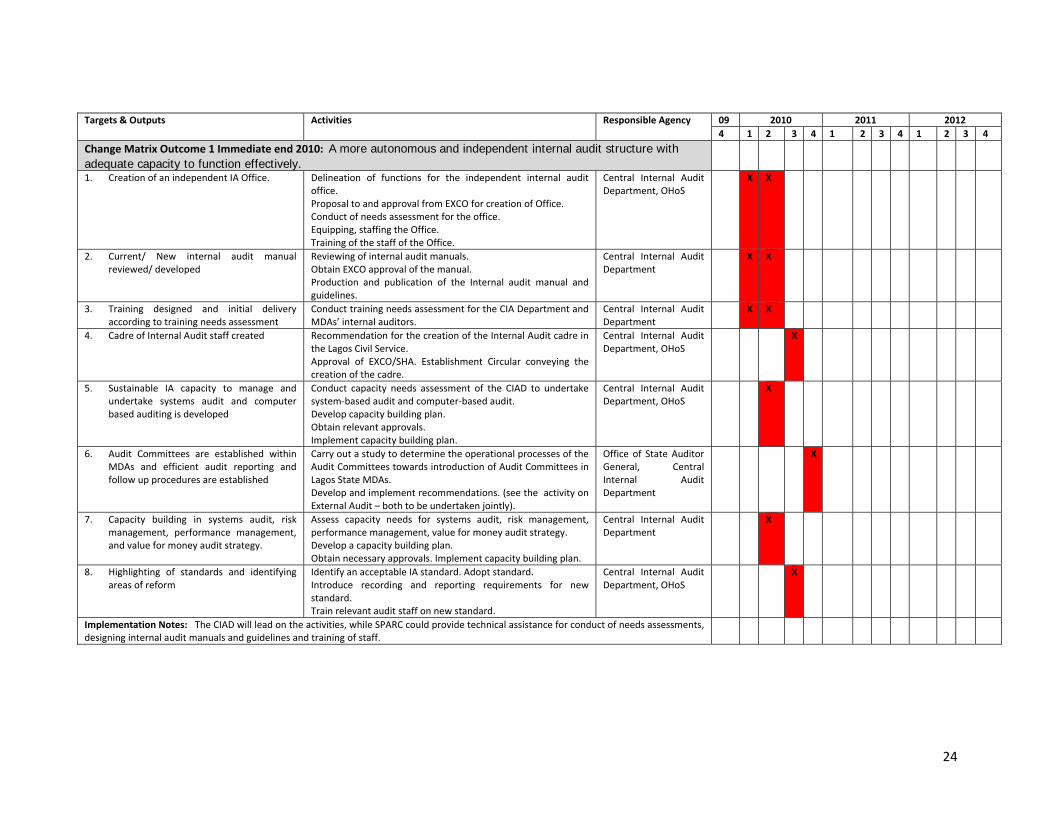

Change Matrix Outcome 1 Immediate end 2010: A more autonomous and independent internal audit structure with adequate capacity to function effectively.

1. Creation of an independent IA Office. Delineation of functions for the independent internal audit office. Proposal to and approval from EXCO for creation of Office. Conduct of needs assessment for the office. Equipping, staffing the Office. Training of the staff of the Office.

Central Internal Audit Department, OHoS

X X

2. Current/ New internal audit manual reviewed/ developed

Reviewing of internal audit manuals. Obtain EXCO approval of the manual. Production and publication of the Internal audit manual and guidelines.

Central Internal Audit Department

X X

3. Training designed and initial delivery according to training needs assessment

Conduct training needs assessment for the CIA Department and MDAs’ internal auditors.

Central Internal Audit Department

X X

4. Cadre of Internal Audit staff created Recommendation for the creation of the Internal Audit cadre in the Lagos Civil Service. Approval of EXCO/SHA. Establishment Circular conveying the creation of the cadre.

Central Internal Audit Department, OHoS

X

5. Sustainable IA capacity to manage and undertake systems audit and computer based auditing is developed

Conduct capacity needs assessment of the CIAD to undertake system‐based audit and computer‐based audit. Develop capacity building plan. Obtain relevant approvals. Implement capacity building plan.

Central Internal Audit Department, OHoS

X

6. Audit Committees are established within MDAs and efficient audit reporting and follow up procedures are established

Carry out a study to determine the operational processes of the Audit Committees towards introduction of Audit Committees in Lagos State MDAs. Develop and implement recommendations. (see the activity on External Audit – both to be undertaken jointly).

Office of State Auditor General, Central Internal Audit Department

X

7. Capacity building in systems audit, risk management, performance management, and value for money audit strategy.

Assess capacity needs for systems audit, risk management, performance management, value for money audit strategy. Develop a capacity building plan. Obtain necessary approvals. Implement capacity building plan.

Central Internal Audit Department

X

8. Highlighting of standards and identifying areas of reform

Identify an acceptable IA standard. Adopt standard. Introduce recording and reporting requirements for new standard. Train relevant audit staff on new standard.

Central Internal Audit Department, OHoS

X

Implementation Notes: The CIAD will lead on the activities, while SPARC could provide technical assistance for conduct of needs assessments, designing internal audit manuals and guidelines and training of staff.

25

Change Matrix Outcome 1 Intermediate end 2012: More proficient and effective internal audit staff.

Training in internal audit delivered Develop a training programme on Oracle Financials (or any other financial management software adopted by the STO) for internal auditors. Implement training programme. Certify trained staff

1. CIAD, STO, OHoS

Implementation Notes: The Central Internal Audit Department will lead and collaborate with the STO and HoS to implement the activities. SPARC can assist with the training of internal auditors on the Oracle Financials

26

Priority 10 : INTERGOVERNMENTAL FISCAL RELATIONS

Strategy Inter‐governmental fiscal relations between the state and local governments have been a contentious issue since the return of democratic rule in 1999. The 1999 Constitution created an ambiguity in the control of local government by the state. The state has been accused of meddling with the politics, functions and funding of the local governments thereby weakening the growth of that level of government in the country. Besides, the fiscal risks of the local governments are not fully comprehended by the state as the financial activities of the local governments are not properly reported and consolidated in the state‐wide financial accounts. For truly effective governance reform (especially PFM) to succeed in the state, there is a need to properly define the roles and relationships between the two tiers of the sub‐national government. 2010 Fiscal relations between the state and local governments should be clearly defined in law and regulations that acceptable to both tiers of government to overcome the conflict in revenue collection mandates and administration. State Agencies that have carry out local government function should sit with the LGs to draw out an MOU for the administration of revenue from such activities such as signage, and refuse and waste management. To promote possible consolidation and comparison of both LG and SG budgets, a uniform reporting format based on the COFOG should be implemented. 2012 Resolving the intergovernmental fiscal relations between the state and local governments require a clear constitutional and legal provisioning; and sincere and committed dialogue between the relevant stakeholders. The political and fiscal status of the local government should be resolved to make it either fully autonomous or independent or merged fully with the state. In the meantime, the fiscal relations between the LASG and the LGs should be strengthened by reviewing the local government laws to clearly spell out and/or implement the criteria for distributing the funds meant for LGs in the JAAC pool. Also such legislations should state reporting requirement from the LGs to the state authorities – Accountant General, Auditor General and Ministry of Local Government to enable the state provide proper fiscal risk oversight and to determine the size of the state’s economy.

Key Priority Milestones Fiscal risk oversight of local governments is strengthened by making local government submit their financial statements timely (at least three months from the end of the financial year) for audit; LGs’ annual accounts are consolidated by the state Local Government Auditor General.

27

Targets & Outputs Activities Responsible Agency 09 2010 2011 2012

4 1 2 3 4 1 2 3 4 1 2 3 4 Change Matrix Outcome 1 Immediate end 2010: More transparent fiscal relations between the State and LGs. 1. .a). Clear guidelines are developed and

agreed, based on legislation, which clearly define responsibilities and delineate revenue jurisdictions between the State and LGs.

Drafting or amending of existing legislation on IGR which spells out the jurisdictional boundaries for both the state and local government revenue collection. Stakeholder consideration of the draft bill. EXCO approval and presentation to the SHA. House consideration and passage into law.

Ministry of Local Government. STO. ALGON. X‐REF TO PSM MANDATES

X X

1. .b) Bye‐laws on revenue administration are enacted by LG legislators

Finance Departments, Treasurer and Finance Supervisor draft and introduce bills for bye‐laws on Local Government Revenue Administration. Finance and General Purpose Committee approves bill. Bill presented to the LG Council for consideration and passage. Regulations on Local Government Revenue Administration introduced.

Individual LGs X‐REF TO PSM MANDATES

X X

2. Memorandum of understanding signed between LG and boards who undertake LG functions (LASAA, LAWMA). Land Use Charge, PIE etc should be made public.

Consultations with LASAA and LAWMA. Negotiate terms of revenue sharing and responsibilities. Agree and draft and execute MOU. Publish Land use charges, PIE, etc periodically to reflect any changes in tariff.

Individual LGs, ALGON, LAWMA, LASAA. X‐REF TO PSM MANDATES

X X

3. Harmonisation of state government and LG reporting and budgeting system in line with COFOG format

Review LG and State Budget reporting systems. Make recommendations on harmonisation and adoption of COFOG format for State and LG budget reporting. Implement recommendation

MEPB, MoLG, ALGON, LGs.

X X

Implementation Notes: The State Government through the relevant MDAs will lead on the implementation of the activities both in terms of funding and logistics. Also the LG s and their representatives should be involved in the implementation. SPARC assistance will be channelled towards providing technical resources to support the implementation of the activities.

Change Matrix Outcome 1 Intermediate end 2012: More transparent fiscal relation between the State and LGs

4. JAAC criteria for allocating funds to LGs are made clear and public

Implement the criteria for the allocation of funds to LGs as provided in the State Local Government Law.

State Executive Council. JAAC

X X

5. Monthly allocations to LGs are published. Publication of monthly allocation from the JAAC in local state media

JAAC

X

6. All state deductions from LG made public and justified

LG Chairmen and councillors consulted and their approval sought to agree deductions from LG accounts. Deduction published in state‐wide media

Ministry of Local Governments, JAAC, and representatives of local governments.

Implementation Notes: The State Government through the relevant MDAs will lead on the implementation of the activities both in terms of funding and logistics. Also the LG s and their representatives should be involved in the implementation. SPARC assistance will be channelled towards providing technical resources to support the implementation of the activities.