Embed Size (px)

Citation preview

Siddharth Rajeev, B.Tech, MBA, CFA Analyst

May 5, 2016

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Laguna Blends Inc. (CSE: LAG / FWB: LB6A / OTC: LAGBF): Network Marketing Company with an

Initial Focus on Hemp - Initiating Coverage

Sector/Industry: Multi-Level Marketing www.lagunablendsinc.com

Market Data (as of May 5, 2016)

Current Price C$0.12

Fair Value C$0.45

Rating* BUY

Risk* 4 (Speculative)

52 Week Range N/A

Shares O/S 20.36 mm

Market Cap C$2.44 mm

Current Yield N/A

P/E (forward) N/A

P/B N/A

YoY Return N/A

YoY TSXV -6.2% *See back of report for rating and risk definitions

Investment Highlights � Laguna Blends Inc. (“Laguna, “company”) is a brand new network marketing

(multi-level marketing / MLM) company with an initial focus on functional beverage products containing hemp and other efficacious ingredients.

� Hemp is a good source of protein, omega 3, 6 and 9 fatty acids, magnesium, zinc, iron, dietary fibre, etc., and therefore, has been receiving increasing focus on its potential use in health foods and functional foods.

� The company, formed in 2014, went public through the reverse takeover (“RTO”) of a Canadian Stock Exchange (“CSE”) listed company in September 2015. CEO, Stuart Gray, and his spouse, own 18.5% of the outstanding shares.

� The company has launched two products to date - the first one is a hemp protein coffee called Caffé, and the second one is a hemp protein functional beverage called Pro369. Laguna does not manufacture its own products, but partners with researchers, manufacturers and suppliers to produce white label products under the brand name Laguna Blends.

� Laguna launched sales on March 7, 2016, with 135 direct independent sellers (affiliates) in the U.S. and Canada. As of April 4, 2016, the count increased to over 700.

� We are initiating coverage on Laguna with a BUY rating and a fair value estimate of $0.45 per share.

Risks � Laguna is a startup and has yet to report revenues. � The company’s ability to attract affiliates is vital for its long-term success. � Although hemp focused beverages are relatively new, the functional food and

beverage industry is dominated by large players. � As with any direct selling company, the company is also susceptible to

negative changes to regulatory laws. � Critical technologies are currently licensed from third-parties. � Although MLM is a large market and there are thousands of companies

operating in the space, MLM companies are viewed with scepticism by a certain segment of the market.

Key Financial Data

(in C$); YE - Mar 31 2015 (9M) 2015E 2016E

Revenues - - 747,983

EBITDA (1,878,903) (2,231,738) (903,888)

Net Income (8,007,694) (8,360,529) (903,888)

EPS (basic) (0.73) (0.41) (0.04)

Total Assets 304,412 270,616 547,048

Page 2

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Multi-Level

Marketing

Direct selling is the act of marketing and selling a product directly to consumers instead of through retail outlets. Direct selling is broadly classified into single-level marketing and multi-level marketing (“MLM”). In the case of single-level marketing, a seller (also referred to as an independent sales representative, consultant, distributor, etc.) makes money by purchasing products at the wholesale price from the parent company and selling them directly to customers at retail prices. As for multi-level marketing (also referred to as network marketing), sellers are compensated not only from the sale of products to customers, but also from the sales made by other sellers (also referred to as a seller’s downline) whom they recruit / sponsor. According to the World Federation of Direct Selling Associations (“WFDSA”), there were approximately 99.7 million direct sellers in the world in 2014 (up from 84.6 million in 2011), and they generated retail sales of US$182.8 billion (up from US$151.3 billion in 2011). From 2011 to 2014, global direct sales grew at a compounded annual growth

rate (“CAGR”) of 6.5%. The U.S. is the largest market and accounted for 19% of global sales, followed by China (17%) and Japan (9%) in 2014.

Global Direct Sales by Region (2014)

Source: WFSDA

In the U.S., direct selling accounted for US$34.5 billion in sales from 18.2 million

sellers (across 1,400 companies) in 2014. Canada accounted for US$1.83 billion from 779,688 direct sellers in the same year. The following chart shows the growth in sales and the number of direct sellers since 2006 in the U.S.

Page 3

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Source: DSA

The following table shows the average annual sales per direct seller. The average sales in the U.S. were $1,894 in 2014, in line with the global average of $1,834.

2014 Canada U.S. Global Average

Total Sales $1,825,000,000 $34,470,000,000 $182,800,000,000

Direct Sellers 779,688 18,200,000 99,700,000

Average Annual Sales $2,341 $1,894 $1,834

Average Monthly Sales $195 $158 $153

Source: DSA and other sources

Direct sellers are typically able to purchase products at a 30% discount to the retail price.

Therefore, based on average annual sales of approximately $2,000, a typical direct

seller typically makes 30% of the sales, or $600 per year. However, industry sources state that a very small percentage of the direct sellers generate US$100,000+ in income. Their income comes not only from product sales but by also through commissions from sales generated by their downline. Most people choose to get involved in direct selling due to its potential to provide additional income with flexible work schedules. Another key reason is that they can buy exclusive products and services at a discount from the parent company. Direct selling is also a very low risk business as it does not involve any significant capital investment.

According to the DSA, approximately 14.9% of the households in the U.S. had

someone involved in direct selling in 2014 (versus 13.8% in 2013).

Page 4

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Approximately 94% of the direct sellers have full-time jobs and work part-time (typically 10 hours a week) as direct sellers.

Direct Sellers by Time Worked

Source: DSA

The industry is dominated by women, but that dynamic is changing as the percentage of men has been increased from 12.1% in 2007, to 25.6% by 2014.

Direct Sellers by Gender in the U.S.

Source: DSA

The mean age of direct sellers was 46.3 years in 2014, with 48% of the total in the 35 to 54 year age group.

Page 5

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Direct Sellers by Age

Source: DSA

Negative sentiment towards direct selling: MLM companies have historically been subject to criticisms and lawsuits primarily because consumers confuse them with illegal pyramid and ponzi schemes. In a pyramid scheme, new recruits are required to make a significant upfront payment in return for a share of money received from every new member they recruit. On the other hand, legitimate MLM companies offer real

products / services to consumers and members make most of their income from

product sales rather than hiring new members. Also, legitimate MLM companies typically charge a nominal fee upfront for a starter kit ($50 - $100), which includes items such as samples, catalogs, order forms and other tools that help the seller to sell. The following table shows a list of the major players in the space. The largest MLM company is Amway, which generated US$9.5 billion in revenues and had approximately 3 million direct sellers in 2015, in more than 100 countries.

Company Name2015 (US$,

billions)Salespeople

Average

Annual Sales

per Salesperson

Amway $9.50 3,000,000 $3,167

Avon Products (NYSE: AVP) $6.16 6,000,000+ $1,027

Herbalife (NYSE: HLF) $4.46 4,000,000 $1,115

Vorwerk $4.00 592,000 $6,757

Infinitus $3.88

Mary Kay $3.70 3,500,000 $1,057

Natura (BOVESPA: NATU3) $2.41 1,700,000 $1,418

Tupperware (NYSE: TUP) $2.28 2,600,000 $878

Nu Skin Enterprises (NYSE: NUS) $2.25 1,208,000 $1,860

Most of these players sell a wide array of products including cosmetics, personal care, food and beverage, kitchenware and appliances, home care, wellness, electronics, etc. The

Page 6

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

following chart shows the key segments in the U.S. – the number one segment is

“wellness”, which are basically products (such as weight-loss products and dietary supplements) that promote good physical and mental health. Laguna`s initial focus is on this segment. With increasing concerns for health and appearance, this segment has enjoyed significant growth in the past decade.

Source: DSA

In Canada, the mix is slightly different, with personal care products being the largest segment, followed by home and family care products and wellness products.

Although direct sales only account for less than 1% of the total retail sales in the U.S. (see chart below), they account for 30.1% in wellness product sales, clearly indicating Laguna’s reason to enter the market through this segment. Unique and niche products

tend to do well with direct sales, as they require person-to person product education

and higher levels of customer service.

Page 7

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Total Direct Sales as a Percentage of Total Retail Sales

Source: DSA

Direct Selling vs Industry Retail Sales

Source: DSA

According to IBISWorld, the industry’s EBIT (earning before interest and taxes) margin is estimated to have been approximately 5.3% in 2015. These margins are similar to companies operating in the retail sector because their lower rent and utilities costs are offset by higher wage costs.

Page 8

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Costs as a percentage of Revenues

The following chart shows the margins of the key players in the space. As shown, net margins ranged between 4% and 8% for most companies in 2015.

Company NameGross

Margin

EBITDA

Margin

Net Income

Margin

Debt /

Capital

EV /

Revenues

EV /

EBITDAP / E

Avon Products (NYSE: AVP) 60.50% 7.20% -18.60% 191.20% 0.60 8.40 N/A

Herbalife (NYSE: HLF) 52.80% 15.30% 7.60% 103.40% 1.40 9.20 15.00

Natura (BOVESPA: NATU3) 69.40% 17.70% 6.50% 83.70% 2.00 11.20 25.10

Tupperware (NYSE: TUP) 67.40% 16.60% 8.10% 82.70% 1.60 9.90 16.40

Nu Skin Enterprises (NYSE: NUS) 78.20% 14.10% 5.90% 23.20% 1.00 6.80 17.40

Immunotec Inc. (TSXV:IMM) 25.70% 6.80% 4.80% 16.10% 0.20 3.80 7.20

Average 59.00% 12.95% 2.38% 83.38% 1.13 8.22 16.22 The following table shows a summary of Immunotec Inc.’s (TSXV: IMM) performance. The table serves two purposes – 1) shows the growth potential of companies in the space, and 2) gives an understanding on the various operating costs of the business. Immunotec, headquartered in Quebec, Canada, primarily offers nutritional products through its network of independent consultants. Mexico is their largest market with approximately 49% of the total revenues in the quarter ended January 31, 2016. The U.S. and Canada accounted for 48%.

Page 9

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Immunotec Inc. (TSXV:IMM) - C$ 2013 2014 2015

Revenues $54,771,074 $80,790,470 $84,758,161

Cost of Sales $13,499,239 $18,694,307 $20,350,042

Field Incentives $25,785,581 $42,074,019 $42,595,855

Selling, general and administrative $12,614,723 $15,003,825 $15,733,134

Net Profit $1,377,274 -$2,692,559 $4,042,216

% of Revenues 2013 2014 2015

Cost of Sales 24.65% 23.14% 24.01%

Field Incentives 47.08% 52.08% 50.26%

Selling, general and administrative 23.03% 18.57% 18.56%

Net Profit 2.5% -3.3% 4.8% Immunotec generated C$85 million in revenues in 2015, up from $54.77 million in 2013, reflecting a CAGR of 24%. Their cost of sales averaged 24% of the revenues, field incentives (bonus / commissions paid to sellers) averaged 50% of the revenues, and selling, general and administrative expenses averaged 20% of the revenues. Note that field incentives are paid to a very small percentage of the total number of direct sellers – explained by the highly skewed income distribution of direct sellers. MLM companies compete with department stores, mass merchandisers and e-commerce retailers. The emergence of e-commerce, providing convenience and competitive prices to consumers, has resulted in a significant drop in industry wide margins. MLM companies also face stiff competition from other companies in the space primarily because of the industry’s low barriers to entry and low start-up costs or licensing requirements for new members. As with retail sales, the demand for direct sellers’ products are also dependent on macroeconomic factors such as the gross domestic product (“GDP”) growth, unemployment rate, disposable income, consumer confidence, etc. The following chart shows the strong correlation between direct sales and U.S. GDP growth.

Source: DSA

Page 10

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Overview of

Laguna

Blends

The industry has a high turnover rate among direct sellers; therefore, businesses

have to consistently attract and recruit new members to grow sales. According to the DSA, the dropout rate was 33.5% in the U.S. in 2014, but the industry attracted 40.7% new recruits in the same year. They key to retain members for a long duration is for businesses to not only offer high-quality and unique products, but also attractive earning opportunities (known as “field incentives”) to its members.

Laguna Blends was founded by Stuart Gray, who has a strong background in the network marketing business. The company was originally incorporated in Nevada, U.S., in June 2014, under the name Bonzy Marketing Corp. Subsequently, in September 2014, the name was changed to Laguna Blends Inc. The company went public through the reverse

takeover (“RTO”) of Canadian Stock Exchange (“CSE”) listed Grenadier Resource

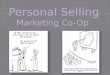

Corp. in September 2015. In January 2016, the company completed a 2.5:1 share consolidation and reduced the number of outstanding shares from 45.65 million to 18.53 million. Management believes that traditional network companies have not kept up-to-date with technology, and therefore, decided to build the business backed by innovative and new technologies. The backbone of Laguna’s infrastructure is a virtual 3D technology

platform (called Laguna World - http://www.lagunaworld.com/) that allows its

members (affiliates) to recruit, train, and generate sales. The primary objective of the platform is to enable affiliates to build their business from their own home, or while travelling, replacing the need for physical meetings. The platform also allows affiliates to record and tracks their sales, and the company to track the performance of all of its independent consultants, and the various incentives earned. According to Laguna, they are the only network company that utilizes such a technology, and believes this technology is a game changer in the industry. We were provided a virtual tour of Laguna World and

witnessed the platform’s features, which we found to be very impressive. Images of Laguna World are shown below:

Page 11

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Source: Company

The company currently licenses the cloud technology from an unrelated private

company.

Laguna charges a start-up fee of $39.97 to its new members, which includes a Laguna online business kit, replicated website (personalized page) and back end office and access to Laguna World. The company also charges a nominal annual renewal fee of $25.

As mentioned earlier, the primary difference between MLM companies and illegal pyramid schemes is the affiliates’ compensation structure. Therefore, Laguna decided to replicate the compensation structure of proven and established MLM companies in order to avoid any potential scrutiny from consumers, investors or regulatory agencies. The various types of compensation plans offered by Laguna to its affiliates are listed below. The list is presented only for illustrative purposes, and the definitions are beyond the scope of this report.

� Retail Profit

� Builder/Retailing Pack Bonus

� Fast Start Bonus

� Binary Bonus – 1/3 – 2/3 Cycling

� Four Level Matching Bonus

� Lifestyle Bonus

� Rank Achievement Bonus

Page 12

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Hemp

Industry

� Binary Re-Entry Opportunity

Laguna does not manufacture its own products, instead partners with researchers, manufacturers and suppliers to produce white label products under the brand name Laguna Blends. Management decided to enter the business with functional beverage products containing hemp and other efficacious ingredients. The company has so far launched two products. The first one is a hemp protein coffee called Caffe, and the second one is single serving hemp protein pouches, called Pro369. The company has partnered with different companies for the first two products. Details of each product and their partners are discussed later in the report. Hemp is a variety of the Cannabis plant. It is a high growing plant typically cultivated for industrial and commercial (non-drug) use. Hemp is refined into a wide range of products, including hemp seed foods, oil, resin, wax, cloth, rope, pulp, paper, etc. Hemp is not to be confused with the recreational drug, cannabis / marijuana, which is also a variety of the cannabis plant, but does not have the same active ingredients. A 60-year ban on hemp production was lifted in Canada in 1998. In the case of U.S., the ban was lifted in 28 states in 2015, but products made with hemp can be sold legally in the entire country.

Hemp is a good source of protein, omega 3, 6 and 9 fatty acids, magnesium, zinc,

iron, dietary fibre, etc., and therefore, has been receiving increasing focus on its

potential use in health foods and functional foods.

According to a report by the Congressional Research Service, the global market for hemp consists of over 25,000 products. The Hemp Industries Association estimates that the total retail sales of hemp food, supplements, and body care products in the U.S. is approximately US$200 million. The total value of all hemp related products is estimated at US$620 million a year. Canadian sales are estimated to be approximately US$20 - US$40 million. Large retailers such as Costco (Nasdaq: COST), Superstore (TSX: L), Walmart (NYSE: WMT), etc. now carry a variety of hemp products, including hemp hearts (raw shelled hemp seeds), hemp seed oil, hemp beverages, hemp granola and cereal. The majority of these products are manufactured and sold by privately held Canadian companies such as Nature’s Path Foods and Manitoba Harvest Hemp Foods. Hemp protein is becoming an increasingly popular substitute in the functional beverage market. Numerous health and nutrition companies such as Vega (acquired by WhiteWave Foods Company, [NYSE: WWAV], in 2015 for US$550 million) are producing hemp protein products targeting health conscious consumers. While most hemp proteins contain fewer grams of protein relative to generic whey protein, the abundance of omega 3, 6 and 9 fatty acids, fiber, vitamins and minerals make it an appealing product. Canadian

Page 13

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Functional

Food and

Beverage

Industry

companies account for the majority of producers in the hemp protein market.

Laguna believes that network marketing is the most effective way to distribute hemp-

based products because it allows person-to-person product education and higher

levels of customer service, which are not as readily available through other

distribution channels.

Growing health concerns, consumer awareness, and general convenience are expected to drive demand for functional food and beverages. Functional food and beverages are basically products that have potentially positive effects on health beyond basic nutrition. The industry has been experiencing rapid growth over the last decade. According to Leatherhead Research, a food research company, the global market for functional foods is expected to grow from US$43.21 billion in 2013, to US$54 billion by

2017, 25% growth from 2013 levels. The industry was at US$34.2 billion in 2009. The market for functional drinks in the U.S. grew from $19 billion in 2009, to $27 billion by 2013, reflecting a CAGR of 8.7%. The market is forecasted to rise to US$38.5 billion by 2017.

Market for Functional Drinks

Source: Trifecta Research 2015

While protein drinks only accounted for a 1.4% share of the functional category last year, the segment is experiencing the strongest growth of any sub-segment. Euromonitor International states that the U.S. market for sports nutrition plus energy/nutrition bars and sports drink is set to hit US$20 billion by 2020, up from the current US$16 billion, which includes sport nutrition (US$6.7 billion, of which sports protein powders make up US$4.7billion), US$6.9 billion sports drink, and US$2.5 billion in energy and nutrition bars.

Page 14

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Source: Euromonitor International

Laguna’s focus is on daily consumable products and their strategy is to develop

modified versions of such products by adding unique features and selling points. The following section presents details of Laguna’s first two products:

Caffé – launched in March 2016, this is an instant coffee beverage that is infused with whey protein, hemp protein, and natural flavors. Each box consists of 30 sachets. Each 6.4g sachet contains 2g of protein.

Page 15

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Although several companies produce coffee flavored protein and coffee drinks with added protein, management believes that Caffé is the only product that combines coffee, hemp and whey protein. Starbucks (Nasdaq: SBUX) offers protein coffee, but they are ready to serve cold protein coffee in a can. Several companies, including (Kellogg’s / NYSE: K), offer coffee flavored protein beverages. Caffé is unique and differs from these products as it is an instant black coffee with the addition of hemp and whey protein. While most coffee flavored protein beverages target athletes or avid gym-goers, Caffé is marketed towards coffee-drinkers looking for the nutritional benefit of hemp and whey protein. A box consisting of 30 sachets is offered by Laguna to its affiliates at a wholesale price of US$44.95 (C$54.97). Laguna suggests that affiliates market their products at a 15+% premium to end-consumers. This implies a single serving price of US$1.50 (C$1.83) for affiliates, and US$1.72 (C$2.10) for end-consumers. Being distinct due to its hemp and whey content, Caffé is marketed as a premium product and commands a higher price when compared with most instant coffee (US$0.10 – US$0.20 per serving). According to US News, the average American pays US$2.70 for a standard cup of coffee.

Product development: In September 2014, Laguna entered into a research and development and supply agreement wherein Laguna appointed Walking Tree as a researcher, developer and supplier of products for an initial term of two years. As per the agreement, Laguna retains all of the intellectual property and rights on the products developed by Walking Tree. Laguna spent approximately $100k for a year of expenses in connection with research and development of the Caffé. Manufacturing: Contract manufacturer of nutraceutical and pharmaceutical products, PNP Pharmaceuticals Inc. (“PNP”) of Burnaby, B.C. manufactures Caffé. Commercial production commenced in January 2016, and 500,000 sachets have been produced to date.

Page 16

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Laguna’s

Products

According to Laguna, PNP was an ideal choice as the contract manufacturer because PNP manufactures pharmaceuticals, in addition to nutritional products, so they are required to meet quality standards that other manufacturers do not. Founded in 1999, PNP operates a 75,000 square foot manufacturing facility in Burnaby, BC. Packaged products are shipped from Expeditors’ (Nasdaq: EXPD – a global logistics and freight forwarding company) distribution centre in Richmond, B.C. Expeditors arranges the delivery of the product to consumers on behalf of Laguna. Pro369 – launched in April 2016, this is a single serving 30g “on the go” hemp protein drink. Consumers can directly mix the product in water, milk, shakes, smoothies, almond milk, sprinkle it over cereal, etc. It currently comes in four flavours:

� Vanilla caramel

� Tropical fruit

� Mixed berry

� Chocolate banana

Pro369’s main ingredients are hemp, ginseng, and stevia. Each packet of Pro369 includes 13g of protein, 2.9g of omega 3, 6 and 9, and 50mg of ginseng. Typical protein shakes offer 25g of protein; however, the addition of omegas and ginseng make Pro369 a convenient “all-in-one” nutritional source. Pro369’s omega content is comparable with most omega 3-6-9 supplements and provides the daily adequate intake. The product has been approved by Health Canada as a Natural Product, with the following approved health claims:

� A source of protein that helps build and repair body tissues.

Page 17

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

� Source of amino acids involved in muscle protein synthesis.

� Assists in the building of lean muscle.

� An adaptogen to help maintain a healthy immune system.

� Supportive therapy for the promotion of healthy glucose levels.

Our research indicates that very few protein supplements in the market have Health Canada approval. Laguna offers Pro369 to its affiliates at a wholesale price of US$44.95 (C$54.97) per box (12 servings). Affiliates market the product at a 15+% premium to consumers. The single serving price is US$3.75 (C$4.58) for affiliates, implying a consumer price of US$4.31 (C$5.27). While the price of whey protein products varies, we find that the average cost per serving is between US$0.50 and US$1 (C$0.64 – C$1.29). Laguna markets Pro369 as a premium protein due its unique features mentioned above and the five approved health claims from Health Canada.

We were provided samples of both products and we found both of them to be

convenient and of good taste.

Product development: In April 2015, Laguna entered into an agreement with Naturally Splendid Enterprises Ltd. (“NSE”) (TSX-V: NSP) to jointly develop and market products, primarily focused on hemp protein formulations developed by NSP. As per the agreement, NSP will contribute to the research and development, and Laguna will be responsible for marketing and sales. Naturally Splendid, headquartered in Vancouver, BC, is a biotechnology company that is focused on the development, commercialization, and licensing of plant based products with a special focus on hemp and hemp derivatives. The following chart summarizes its various divisions and operations.

Page 18

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Relevant

Comparables

As per the agreement, NSP will grant to Laguna:

• a worldwide exclusive and a non-transferrable and royalty-free license to market, sell and distribute the developed products under the Laguna brand name as a white label product, dependent on Laguna achieving the following sales targets: $1.60 million in the first year of the agreement, and $4.50 million in the second year.

• if Laguna does not achieve the sales targets, the license will turn into a non-exclusive license.

All of the research and development was completed at NSE’s expense.

NSP is currently contracting out the production of Pro369 to a third-party manufacturer. The manufactured products are delivered to Expeditors’ facility in Richmond, BC and Los Angeles, CA for distribution to affiliates in the U.S. and Canada.

We identified two companies that provide a benchmark for Laguna’s operations:

Organo Gold: Established in 2008 in Richmond, BC, Canada, Organo Gold has been successful so far as a MLM company. Organo Gold currently operates in 35 countries and offers a variety of coffees, teas, health & wellness products, and bath & beauty products. Organo Gold is a private company and details pertaining to its financial performance are unknown. However, sources indicate that they generated $270+ million in revenues, and had 600,000+ members in 2012.

Page 19

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Future

Products

Building a

Network of

Affiliates

Management

Rocky Mountain High Brands, Inc. (OTCPK: RMHB): Dallas-based Rocky Mountain Brands was established in July 2014. Specializing in the development, manufacturing, and distribution of hemp-infused food and beverage products, RMHB began producing its first line of products in February 2015. They currently have five hemp-infused beverages, hemp-infused edibles (protein bar, energy bar and chia crisp bar), hemp-infused 2 oz. energy shots and 2.5 oz. coffee shots. The company uses a network of brokers and distributors to market its products. In the six months ended December 31, 2015, the company generated US$0.59 million in revenues, US$0.27 million in gross profit, and an operating loss of US$0.81 million.

Laguna intends to expand its product line to include other hemp-based nutritional products. In April 2016, the company announced that it entered into an agreement with Robert Lamberton Consulting for the development of a “Limitless, Healthy Brain and Memory

Coffee” product. As per the agreement, Robert Lamberton Consulting will bear all the costs associated with the development of the product, while Laguna will own the intellectual property and world wide marketing rights for the product. Robert Lamberton is a Clinical Nutritionist, Functional Medicine Consultant. He provides consulting services to help companies develop and market nutritional products.

Laguna will pay Mr. Lamberton a royalty of 3% on sales for the first eight years, which will drop to 2% thereafter.

As mentioned earlier, larger MLM companies offer a wide range of products through their affiliates. Currently, Laguna is considering future product offerings in the functional beverage category, such as hemp teas and additional coffee products. They are also considering adding new product categories. The company launched sales on March 7, 2016, with 135 affiliates in the U.S. and Canada. As of April 4, 2016, the count increased to over 700, of which, approximately 70% are in the U.S. and 30% in Canada. Management indicated to us that approximately 150 – 175 affiliates are currently active. The company has yet to disclose any sales data, but announced that they intend to post financial sales data in early May of 2016. We believe it is a very promising sign that the company has been able to expand its network of affiliates at a rapid pace in a short time period.

Management has extensive experience in the network marketing business. CEO, Stuart Gray, and his spouse, own 18.5% of the outstanding shares. The high equity interest is very encouraging for investors as it shows management’s positive outlook on the company, and aligns management and investors’ interests. The company has four directors – Rhys Williams, Stuart Gray, Negar Adam and Martin Carleton, of which, two are independent. Brief biographies of the management team and

Page 20

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

board members, as provided by the company, follows:

Stuart Gray – CEO and Director

Mr. Gray’s responsibilities with Laguna consist of managing the day to day operations of Laguna, being responsible for business development, management and financial reporting, and such other responsibilities typically ascribed to a CEO and CFO. Mr. Gray was introduced to business and sales through network marketing at 19 years of age. He achieved early MLM success achieving the second highest level in the Company’s pay plan in 18 months. Stuart built a team of leaders in several countries and had one of the largest volume groups in the company for the Silver Executive level. Mr. Gray went on to educate himself in business and marketing. Mr. Gray first attended the Okanagan College for business and marketing and then trained at the Vancouver Film School where he graduated as a Producer/Director in 1995. He founded NewTrends Film and Video Productions (“NewTrends”) in 1996 and served as President of NewTrends from 1996 to 2006. During his tenure, NewTrends was recognized for profitability, innovation and technology and won several awards in these categories. Mr. Gray has in excess of 18 years of experience in business and marketing. As a Producer and Director by background, Stuart has founded several media- and promotional- related companies and has provided consulting to over 120 public and private companies in the U.S. and Canada. Mr. Gray has assisted in taking several companies public through reverse takeovers and assisting in fundraising.

Stuart Kei Kawasaki – President Laguna Blends USA

Mr. Kawasaki has been involved in the multilevel marketing industry since 1988, with extensive hands-on experience in all aspects of corporate and business development, event management, product and field development as well as overall financial and operational responsibility. His corporate experience has ranged from ground-up startups to billion dollar companies and has initiated and grown operations in 19 countries around the world. Currently the principal at BeeCubed, a business and management consultancy that assists companies in all phases of starting up, building, reorganization and crisis management. Industry niches include direct sales/network marketing, retail/wholesale and services-oriented companies. Mr. Kawasaki earned a Bachelor of Science degree from Santa Clara University. Selected achievements: successful ground-up launch of internationally based MLM company in the North American/global market, implemented and/or reorganized operations to be compliant in international markets for client companies, established and launched operations in China, Indonesia, Singapore, Malaysia, Thailand, Philippines, Australia, Israel, the United States and Canada; oversaw operations with full profit and loss responsibility for up to 20 staff and 15,000 independent distributors.

Ray W. Grimm, Jr. – President Laguna Blends Inc.

Mr. Grimm is a veteran entrepreneur with more than a quarter century of experience building some of the top nutritional and weight loss companies in direct sales history. Mr. Grimm has what many consider to be the Midas touch in building multimillion dollar companies, three of which exceeded $50 million in sales within their first five years. In

Page 21

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

2011, Mr. Grimm also created and co-founded one of the fastest growing weight loss brands ever developed producing $10 million in sales in its first year. His vision, leadership and expertise in nutrition, weight loss and direct sales are unmatched and so is his unique formula for success all of which have benefited the physical and financial health of thousands. Ray has extensive experience in managing operations, sales, training and marketing of fast growing companies. He is a proud member of the DSA (Direct Selling Association) and founding member and current member of the MLMIA (Multilevel Marketing International Association).

Dennis Compo - Executive Director of Marketing

Dennis Compo has consulted in the Music, Entertainment, Sales and Marketing Industries for 35 years. He has held the following positions: � GanoLife Canada Inc, Vice President - June 2013 – July 31, 2014 � Legends Of Rock-N-Roll , Vice President - August 2005 – Present (9 years) � Gano Excel Canada, Vice-President and General Manager - July 2008 – October 2012

Martin Carleton - Head Technical Development

Mr. Carleton’s responsibilities with Laguna consist of acting as member of the board of directors of Laguna and participating in the governance of the company. Mr. Carleton has 8 years of experience in the Internet Technology sector where he has worked both as a web developer and project manager. Most notably, Martin has led a team of developers in creating a prize winning metering system for Skype that garnered the “Skype API Developer Award” in 2005 and in 2006 as part of his San Francisco based internet start-up. Since then Martin has undertaken numerous projects developing commercial websites as a developer and more recently overseeing the construction of an internet/TV fiber optic network intended to serve an 800-room temporary logging facility in the Oil fields of North Dakota. Originally from Ottawa, Canada, Martin obtained his B. Eng in Communications Engineering from Carleton University.

Rhys Williams - Director

Mr. Williams has been involved in the business of manufacturing since 1993, when he served as a Final Quality Inspector for Western Star Trucks. In 2002, while attending University College of the Fraser Valley, Mr. Williams co-founded BC Northern Lights Ltd., a private indoor greenhouse appliance company that has received recognition and rewards for its innovative product line. Mr. Williams was also involved in the early development of the Urban Cultivator product which was featured on CBC’s Dragons’ Den in 2011. The Urban Cultivator is an award winning kitchen appliance that grows fresh herbs and is distributed worldwide.

Negar Adam - Director

Ms. Adam earned a Bachelor of Commerce from the University of British Columbia and has a corporate finance background. Mrs. Adam has been a director and officer of numerous Canadian public companies over the last 15 years. Ms. Adam has been the

Page 22

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Financials

President and Secretary of Makena Resources Inc. since June 19, 2007 and serves as its Chief Executive Officer. In addition to previously sitting on the board of several companies listed on the TSX Venture Exchange, Ms. Adam is self-employed as a consultant who offers consulting services to public companies since 1999.

Charles Carleton – Head of Laguna Tech

Mr. Charles Carleton has 20 years’ experience in Technology and Entrepreneurship. He has worked both for large corporations and small start-ups and is at ease in both worlds. A solid technical and analytical background coupled with good overall business acumen has enabled him to effectively work across all departments which compose a successful business. Originally from Ottawa, Canada, Mr. Charles Carleton obtained his BSC cum lade in Experimental Physics from York University in Toronto. He headed west and spent the next 15 years in the tech industry out in California between Silicon Valley, San Francisco and San Diego as an employee for Microsoft, Allied Signal and Honeywell. He also started some of his own software companies during that time. One of which was partnered with Skype in their very early existence (when they were only seven guys working out of an office over a bar in Estonia) and contributed in designing and building their original Platform and API.

The following chart shows a summary of the company’s operating performance.

STATEMENTS OF OPERATIONS

(in C$) - YE Mar 31st 2015 (9M)

Revenues

COGS

Gross Profit -

EXPENSES

General and administrative 855,841

Stock based compensation 158,506

Buiness development 864,556

EBITDA (1,878,903)

Amortization

EBIT (1,878,903)

Other income

Interest expense

EBT (1,878,903)

Unusual items (6,128,791)

Taxes

Net Profit (Loss) (8,007,694)

EPS -0.73

Page 23

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Cash Flows

Balance

Sheet

In the nine month period ended December 31, 2015, the company reported $1.88 million in operating losses. General and administrative (“G&A”) expenses were $0.42 million, and consulting / business development expenses were $1.30 million (of which approximately $0.78 million were related fees paid in shares). Management expects G&A and business development expenses to be approximately $0.75 million in 2016. The company reported public company listing and acquisition fees of $6.07 million in the nine month period. This was a non-cash event. Our revenue forecasts for FY2016, and FY2017, are $0.75 million, and $3.08 million, respectively. Our net loss forecast for 2016 is $0.90 million (EPS: -$0.04) and for

FY2017 is $0.37 million (EPS: -$0.02). The following table shows a summary of the company’s cash flows:

Summary of Cash Flows

($, mm) 2015 (9M)

Operating -$0.88

Investing -$0.16

Financing $1.04

Effects of Exchange Rate $0.00

Net $0.00

Free Cash Flows to Firm (FCF) -$1.04 Free cash flows (“FCF”) were -$1.04 million in the nine month period ended December 31, 2015.

The company had $0.08 million in cash, with a working capital of -$0.70 million at the end of December 31, 2015. The following table shows the company’s cash and liquidity position.

Liquidity & Capital Structure Q3-2015

Cash 76,005

Working Capital (702,878)

Current Ratio 0.3

LT Debt -

Total Debt 689,231

LT Debt / Capital 0.0%

Laguna currently has $0.81 million in debt, of which, $0.70 million is held by the CEO’s

Page 24

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Stock Options

and Warrants

Valuation

and Rating

spouse. Terms and conditions of the debt are shown in the table below.

Amount Interest (p.a.) Maturity Lender

$250,000 10% 16-Jul-16 Spouse of the CEO

$150,000 10% 12-Nov-16 Spouse of the CEO

$100,000 10% 11-Dec-16 Spouse of the CEO

$200,000 10% 20-Jan-17 Spouse of the CEO

$50,000 10% 31-Jul-16 Unrelated party

$25,000 10% 12-Nov-16 Unrelated party

$20,000 10% 20-Jan-17 Unrelated party

$10,000 10% 28-Jan-17 Unrelated party

$805,000 10% Equity financing – In March 2016, the company announced its plans to pursue a $0.21 million private placement by issuing 1.86 million units at a unit price of $0.11. Each unit consist of a common share and share purchase warrant (exercise price - $0.15 per share for one year). The company currently has 40,000 options (weighted average exercise price – $0.70), and 2.30 million warrants (weighted average exercise price - $0.85) outstanding. All the options and warrants are currently out of the money. The following table shows the revenue forecasts based on the company achieving 24,000 active affiliates by the end of 2020. Note that our forecasts are based on the assumption that Laguna will continue to introduce new products to its portfolio. Future revenues will primarily depend on Laguna’s ability to attract affiliates.

2016E 2017E 2018E 2019E 2020E

# of Active Affiliates (year-end) - company est. 2,000 5,750

# of Active Affiliates (year-end) 1,000 3,000 6,000 12,000 24,000

Average Sales per Year / Affiliate 2,000 2,000 2,000 2,000 2,000

Total Sales 1,150,000 4,000,000 9,000,000 18,000,000 36,000,000

Annual Affiliate Fee ($39.97 per year) 22,983 79,940 179,865 359,730 719,460

Cost of Sales (20% of Sales) 230,000 800,000 1,800,000 3,600,000 7,200,000

Compensation plan (50% of Sales) 575,000 2,000,000 4,500,000 9,000,000 18,000,000 Our base-case forecasts are shown below:

Page 25

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

STATEMENTS OF OPERATIONS

(in C$) - YE Mar 31st 2016E 2017E 2018E 2019E 2020E

Revenues 747,983 3,079,940 7,679,865 15,359,730 30,719,460

COGS 543,750 2,250,000 5,625,000 11,250,000 22,500,000

Gross Profit 204,233 829,940 2,054,865 4,109,730 8,219,460

EXPENSES

General and administrative 625,645 688,209 959,983 1,919,966 3,839,933

Stock based compensation 232,475 255,723 281,295 309,425 340,367

Consulting & Buiness development 250,000 246,395 307,195 614,389 1,228,778

EBITDA (903,888) (360,387) 506,392 1,265,950 2,810,382

Amortization 5,000 9,750 14,263 18,549

EBIT (903,888) (365,387) 496,642 1,251,687 2,791,832

Interest expense

EBT (903,888) (365,387) 496,642 1,251,687 2,791,832

Unusual items

Taxes - - 173,825 438,091 977,141

Net Profit (Loss) (903,888) (365,387) 322,817 813,597 1,814,691

EPS -0.04 -0.02 0.02 0.04 0.09 We estimate the average expected return on equity for companies in the Vitamins and Nutritional Supplements industry, Household and Personal Products industries is approximately 10.2%. Adding a micro-cap premium and a premium to account for the early stage nature of Laguna’s operations, we used a discount rate of 13.5% for our Discounted Cash Flow (“DCF”) model. As shown below, our DCF valuation on Laguna’s shares is currently at $0.40 per share.

Page 26

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

DCF Valuation (C$) 2016E 2017E 2018E 2019E 2020E

Funds Flow from Operations -$671,412 -$104,664 $613,863 $1,137,284 $2,173,608

-increase in w/c -$287,998 -$261,657 -$276,373 -$461,544 -$923,087

Cash Flows from Operations -$959,410 -$366,322 $337,489 $675,740 $1,250,520

-capex -$100,000 -$100,000 -$100,000 -$100,000 -$100,000

Free Cash Flows -$1,059,410 -$466,322 $237,489 $575,740 $1,150,520

Present Value -$933,401 -$361,988 $162,426 $346,931 $610,822

Discount Rate 13.5%

Terminal Growth 3%

Present Value $10,616,587

Cash - Debt -$613,226

Fair Value $10,003,361

Shares O/S (treasury stock method)*

24,904,681

Value per share (C$) $0.40

*Assuming a $0.50M equity financing this year The following chart shows the sensitivity of our fair value estimate to the expected number of active affiliates by the end of 2020. As shown in the chart, the valuation increases to $1.06 per share if our models assume 100,000 active members by the end of 2020. The valuation drops to $0.30 per share if our models assume only 12,000 members by the end of 2020.

Page 27

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Risks

The following table shows the valuation based on our expected EBITDA estimate in 2020 and the average EV / EBITDA multiple of 8.2x of selected MLM companies (presented earlier in the report). The estimated value was discounted back to the present using a 13.5% discount rate.

2020 Forecast (EBITDA) 2,810,382

Average EV/ EBITDA 8.22

Expected EV ($) $23,091,970

Value per Share ($) $0.48

Comparables Valuation

Based on our valuation models, we are initiating coverage on Laguna with a BUY

rating and a fair value estimate of $0.45 per share. The company is expected to start

reporting sales figures shortly. We believe the value proposition and market

absorption of the initial set of products will play a key role in the company’s ability to

attract affiliates.

The following risks may cause our estimates to differ from actual results (not exhaustive): � Laguna is a start-up and has yet to report revenues. � The networking marketing industry is highly competitive. � The company’s ability to attract affiliates is vital for its long-term success. � Although hemp focused beverages are relatively new, the functional food and

beverage industry is dominated by large players. � The demand for the company’s products is dependent on macroeconomic factors,

such as GDP growth, unemployment rate, disposable income, consumer confidence, etc.

� As with any direct selling company, the company is also susceptible to negative changes to regulatory laws.

� Critical technologies are currently licensed from third-parties. � Although MLM is a large market and there are thousands of companies operating in

the space, MLM companies are viewed with scepticism by a certain segment of the market.

� As a manufacturer of nutritional beverages, Laguna may be exposed to product liability claims, regulatory action and litigation.

Page 28

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Appendix

STATEMENTS OF OPERATIONS

(in C$) - YE Mar 31st 2015E 2016E 2017E

Revenues - 747,983 3,079,940

COGS - 543,750 2,250,000

Gross Profit - 204,233 829,940

EXPENSES

General and administrative 568,768 625,645 688,209

Stock based compensation 211,341 232,475 255,723

Consulting & Buiness development 1,451,629 250,000 246,395

EBITDA (2,231,738) (903,888) (360,387)

Amortization 5,000

EBIT (2,231,738) (903,888) (365,387)

Interest expense

EBT (2,231,738) (903,888) (365,387)

Unusual items (6,128,791)

Taxes - -

Net Profit (Loss) (8,360,529) (903,888) (365,387)

EPS -0.41 -0.04 -0.02

Page 29

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

BALANCE SHEETS

(in C$) - YE Mar 31st 2015E 2016E 2017E

ASSETS

CURRENT

Cash and cash equiv. 30,788 221,378 5,057

A/R 37,955 36,784 151,466

Inventory 164,597 173,926 359,846

Prepaid 37,275 14,960 61,599

Total Current Assets 270,616 447,048 577,967

Fixed assets 100,000 195,000

Total Assets 270,616 547,048 772,967

LIABILITIES

CURRENT

A/P 604,312 302,156 387,740

Loans payable 825,000 1,575,000 1,575,000

Due to related party 114,231 114,231 114,231

Total Current Liabilities 1,543,543 1,991,387 2,076,971

SHAREHOLDERS EQUITY

Share capital 7,607,988 8,107,988 8,357,988

Reserves 609,806 842,281 1,098,004

Deficit -9,490,721 -10,394,609 -10,759,996

Total shareholders’ equity (deficiency) (1,272,927) (1,444,339) (1,304,004)

Total Liabilities and Shareholders Equity 270,616 547,048 772,967

Page 30

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

STATEMENTS OF CASH FLOWS

(in C$) - YE Mar 31st 2015E 2016E 2017E

OPERATING ACTIVITIES

Net profit for the year -8,360,529 -903,888 -365,387

Adjusted for items not involving cash:

Depreciation 5,000

Stock compensation / option expense 779,506 232,475 255,723

Unusual items 6,130,316

Funds From Operations -1,450,707 -671,412 -104,664

Change in working capital

A/R -32,026 1,171 -114,681

Inventory -164,597 -9,329 -185,920

Prepaid 20,644 22,315 -46,639

A/P 508,226 -302,156 85,584

NET CASH USED IN OPERATING ACTIVITIES -1,118,461 -959,410 -366,322

INVESTING ACTIVITIES

PP&E -156,759 -100,000 -100,000

NET CASH USED IN INVESTING ACTIVITIES -156,759 -100,000 -100,000

FINANCING ACTIVITIES

Equity 251,448 500,000 250,000

Debt 1,040,000 750,000

NET CASH FROM FINANCING ACTIVITIES 1,291,448 1,250,000 250,000

Foreign Exchange / Others

INCREASE IN CASH FOR THE YEAR 16,228 190,590 -216,322

CASH, BEGINNING OF THE YEAR 14,560 30,788 221,378

CASH, END OF THE YEAR 30,788 221,378 5,057

Page 31

2016 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Fundamental Research Corp. Equity Rating Scale:

Buy – Annual expected rate of return exceeds 12% or the expected return is commensurate with risk Hold – Annual expected rate of return is between 5% and 12% Sell – Annual expected rate of return is below 5% or the expected return is not commensurate with risk Suspended or Rating N/A— Coverage and ratings suspended until more information can be obtained from the company regarding recent events.

Fundamental Research Corp. Risk Rating Scale:

1 (Low Risk) - The company operates in an industry where it has a strong position (for example a monopoly, high market share etc.) or operates in a regulated industry. The future outlook is stable or positive for the industry. The company generates positive free cash flow and has a history of profitability. The capital structure is conservative with little or no debt. 2 (Below Average Risk) - The company operates in an industry where the fundamentals and outlook are positive. The industry and company are relatively less sensitive to systematic risk than companies with a Risk Rating of 3. The company has a history of profitability and has demonstrated its ability to generate positive free cash flows (though current free cash flow may be negative due to capital investment). The company’s capital structure is conservative with little to modest use of debt. 3 (Average Risk) - The company operates in an industry that has average sensitivity to systematic risk. The industry may be cyclical. Profits and cash flow are sensitive to economic factors although the company has demonstrated its ability to generate positive earnings and cash flow. Debt use is in line with industry averages, and coverage ratios are sufficient. 4 (Speculative) - The company has little or no history of generating earnings or cash flow. Debt use is higher. These companies may be in start-up mode or in a turnaround situation. These companies should be considered speculative. 5 (Highly Speculative) - The company has no history of generating earnings or cash flow. They may operate in a new industry with new, and unproven products. Products may be at the development stage, testing, or seeking regulatory approval. These companies may run into liquidity issues, and may rely on external funding. These stocks are considered highly speculative.

Disclaimers and Disclosure The opinions expressed in this report are the true opinions of the analyst about this company and industry. Any “forward looking statements” are our best estimates and opinions based upon information that is publicly available and that we believe to be correct, but we have not independently verified with respect to truth or correctness. There is no guarantee that our forecasts will materialize. Actual results will likely vary. The analyst and Fundamental Research Corp. “FRC” does not own any shares of the subject company, does not make a market or offer shares for sale of the subject company, and does not have any investment banking business with the subject company. Fees were paid by Laguna to FRC. The purpose of the fee is to subsidize the high costs of research and monitoring. FRC takes steps to ensure independence including setting fees in advance and utilizing analysts who must abide by CFA Institute Code of Ethics and Standards of Professional Conduct. Additionally, analysts may not trade in any security under coverage. Our full editorial control of all research, timing of release of the reports, and release of liability for negative reports are protected contractually. To further ensure independence, Laguna has agreed to a minimum coverage term including four updates. Coverage can not be unilaterally terminated. Distribution procedure: our reports are distributed first to our web-based subscribers on the date shown on this report then made available to delayed access users through various other channels for a limited time. The performance of FRC’s research is ranked by Investars. Full rankings and are available at www.investars.com. The distribution of FRC’s ratings are as follows: BUY (69%), HOLD (8%), SELL (5%), SUSPEND (19%). To subscribe for real-time access to research, visit http://www.researchfrc.com/subscription.htm for subscription options. This report contains "forward looking" statements. Forward-looking statements regarding the Company and/or stock’s performance inherently involve risks and uncertainties that could cause actual results to differ from such forward-looking statements. Factors that would cause or contribute to such differences include, but are not limited to, continued acceptance of the Company's products/services in the marketplace; acceptance in the marketplace of the Company's new product lines/services; competitive factors; new product/service introductions by others; technological changes; dependence on suppliers; systematic market risks and other risks discussed in the Company's periodic report filings, including interim reports, annual reports, and annual information forms filed with the various securities regulators. By making these forward looking statements, Fundamental Research Corp. and the analyst/author of this report undertakes no obligation to update these statements for revisions or changes after the date of this report. A report initiating coverage will most often be updated quarterly while a report issuing a rating may have no further or less frequent updates because the subject company is likely to be in earlier stages where nothing material may occur quarter to quarter. Fundamental Research Corp DOES NOT MAKE ANY WARRANTIES, EXPRESSED OR IMPLIED, AS TO RESULTS TO BE OBTAINED FROM USING THIS INFORMATION AND MAKES NO EXPRESS OR IMPLIED WARRANTIES OR FITNESS FOR A PARTICULAR USE. ANYONE USING THIS REPORT ASSUMES FULL RESPONSIBILITY FOR WHATEVER RESULTS THEY OBTAIN FROM WHATEVER USE THE INFORMATION WAS PUT TO. ALWAYS TALK TO YOUR FINANCIAL ADVISOR BEFORE YOU INVEST. WHETHER A STOCK SHOULD BE INCLUDED IN A PORTFOLIO DEPENDS ON ONE’S RISK TOLERANCE, OBJECTIVES, SITUATION, RETURN ON OTHER ASSETS, ETC. ONLY YOUR INVESTMENT ADVISOR WHO KNOWS YOUR UNIQUE CIRCUMSTANCES CAN MAKE A PROPER RECOMMENDATION AS TO THE MERIT OF ANY PARTICULAR SECURITY FOR INCLUSION IN YOUR PORTFOLIO. This REPORT is solely for informative purposes and is not a solicitation or an offer to buy or sell any security. It is not intended as being a complete description of the company, industry, securities or developments referred to in the material. Any forecasts contained in this report were independently prepared unless otherwise stated, and HAVE NOT BEEN endorsed by the Management of the company which is the subject of this report. Additional information is available upon request. THIS REPORT IS COPYRIGHT. YOU MAY NOT REDISTRIBUTE THIS REPORT WITHOUT OUR PERMISSION. Please give proper credit, including citing Fundamental Research Corp and/or the analyst, when quoting information from this report. The information contained in this report is intended to be viewed only in jurisdictions where it may be legally viewed and is not intended for use by any person or entity in any jurisdiction where such use would be contrary to local regulations or which would require any registration requirement within such jurisdiction.