Embed Size (px)

Citation preview

L7: International Capital Budgeting

15.1 Adjusted NPV:

Discounted CF of all equity firm (incremental, after tax CF in same currency)

Value of fin side effects (costs issue securities, tax implications financing, costs fin distress, subsidies from gov

Value of growth options

Adjusted NPV = NPV + NPVF + GO 15.2 Deriving NPV of Free Cash flow

Incremental profits = from project

Revenues: forecasets depend on future eco enviro

Costs= costs good sold

Dep = legal tax shield, subtracted before taxes calc

Cap expenses: spend on PPE

Net Working Capital= inc and cash on hand

1. Revenue – costs = EBIT 2. EBIT – Taxes on EBIT = Net

operating Profit less adjusted taxes (NOPLAT)

3. NOPLAT + accounting depreciation = Gross Cash Flow GCF

4. GCF - ∆NWC – CAPEX = Free Cash flow

15.3 Financial Side Effects

Costs issuing sec: monetary fee, underwriting disc (spread of what firm receives from issuing and what public pays EOS as money raised inc)

Tax shields for sec: - Interest Tax shield = value of ability to

deduct interest expense for tax purposes Proper Discount rate = reflect riskiness cash flows

Costs fin distress: - If no costs, use 100% debt in cap structure - Direct costs = legal, consulting, account, 3% - Indirect costs = loss value due to expected failure (lost sales, creditors not extending credit, cant attract labour)

Equilibrium debt: MARGINAL BENEFIT TAX SHIELD = MARGINAL COST of FIN DISTRESS Subsidised financing:

Interest subsidies: value benefit of reduction in cost capital separately, then add to project value

Discount rate is mkt required rate return on debt because firm is as likely to default on subsidized loan Tax Holidays:

Local gov give tax rates to foreign firms investing PROJECT VALUE INCREASE with reduced taxes - Value cost of tax subsidy separately, add to project value

Blocked funds:

Gov hold portion of funds, don’t allow repatriation for some time. Project value reduced (time value money if OC keeping aborad) - Value project without blocked funds, then value costs of blocked funds. (or value with new timeline of cash flows)

Negative Value Project tie ins

Gov want firm to invest in neg value projects ie local development and infra project value decreased - Value cost of tie in separately, then deduct from project value

15.4 Growth Options:

Growht option = firm undertake project and obtain option to do another project in future (included as real option)

Problem Discount CF approach vs ANPV: - Ignore real options (eg enter another foreign markets) (price changes, real ex rate,t iming,

competition) 15.5: Parent Vs Subsidiary CF

ANPV parent v subsidd is different. (forex controls, royalties, licensing, overheads, profits differ)

3 Step Approach: 1. NPV CF analysis of foreign subsid as if independent 2. CF from parents perspective (after withholding tax dif, after tax value of royalty/licensing/sale intermediate, impact cannibalization export 3. Adjust project value for NPV of financing side effects and possible growth options

Intl Cap Budgeting: When project not Domestic?

1. Project perspective: value in foreign currency, then convert to parent domestic currency

2. Parent perspective: convert CF to parent currency, value using domestic disc rates

IF IR parity, difference? SEE 15.6 CASE INTERNATIONAL WOOD PRODUCTS for example

EBIT: Pretax operating income without debt NOPLAT = EBIT – taxes GCF = NPLAT + depreciation CAPX is cap expenditures (large initially, investment later when repairs costly)

L8: Additional Topics in Intl Capital Budgeting

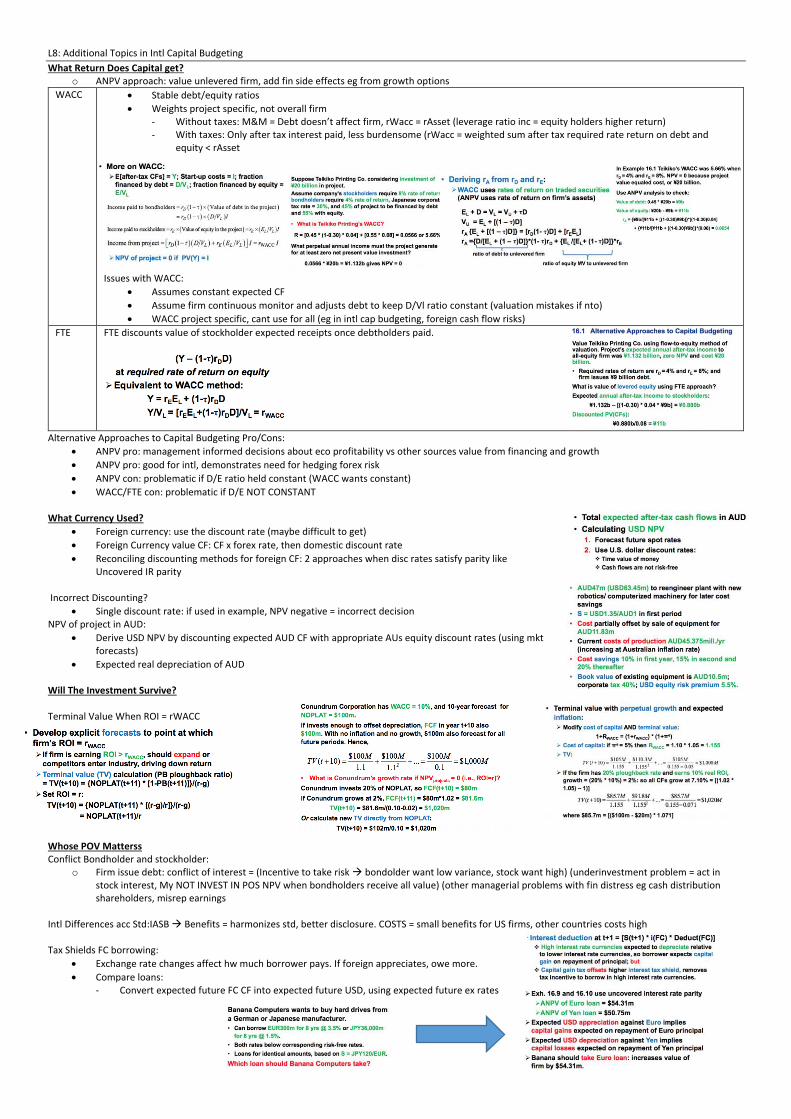

What Return Does Capital get? o ANPV approach: value unlevered firm, add fin side effects eg from growth options

WACC Stable debt/equity ratios

Weights project specific, not overall firm - Without taxes: M&M = Debt doesn’t affect firm, rWacc = rAsset (leverage ratio inc = equity holders higher return) - With taxes: Only after tax interest paid, less burdensome (rWacc = weighted sum after tax required rate return on debt and

equity < rAsset

Issues with WACC:

Assumes constant expected CF

Assume firm continuous monitor and adjusts debt to keep D/Vl ratio constant (valuation mistakes if nto)

WACC project specific, cant use for all (eg in intl cap budgeting, foreign cash flow risks)

FTE FTE discounts value of stockholder expected receipts once debtholders paid.

Alternative Approaches to Capital Budgeting Pro/Cons:

ANPV pro: management informed decisions about eco profitability vs other sources value from financing and growth

ANPV pro: good for intl, demonstrates need for hedging forex risk

ANPV con: problematic if D/E ratio held constant (WACC wants constant)

WACC/FTE con: problematic if D/E NOT CONSTANT What Currency Used?

Foreign currency: use the discount rate (maybe difficult to get)

Foreign Currency value CF: CF x forex rate, then domestic discount rate

Reconciling discounting methods for foreign CF: 2 approaches when disc rates satisfy parity like Uncovered IR parity

Incorrect Discounting?

Single discount rate: if used in example, NPV negative = incorrect decision NPV of project in AUD:

Derive USD NPV by discounting expected AUD CF with appropriate AUs equity discount rates (using mkt forecasts)

Expected real depreciation of AUD Will The Investment Survive? Terminal Value When ROI = rWACC

Whose POV Matterss Conflict Bondholder and stockholder:

o Firm issue debt: conflict of interest = (Incentive to take risk bondolder want low variance, stock want high) (underinvestment problem = act in stock interest, My NOT INVEST IN POS NPV when bondholders receive all value) (other managerial problems with fin distress eg cash distribution shareholders, misrep earnings

Intl Differences acc Std:IASB Benefits = harmonizes std, better disclosure. COSTS = small benefits for US firms, other countries costs high Tax Shields FC borrowing:

Exchange rate changes affect hw much borrower pays. If foreign appreciates, owe more.

Compare loans: - Convert expected future FC CF into expected future USD, using expected future ex rates

Lecture 9: Purchasing Power Parity & Real Exchange Rates

PPP

Exchange rate determination:simple model ex rate determination, fundamental role in location plants, pricing products, hedging - Assess cost living decisions

Nominal Price & Real Value

o Flat money: difference between nominal & real value - Nominal: price real goods in monetary - Real value: price of real goods in other real goods

nominal value increases while real value is fixed inflation Price Level

Nominal price level of country’s basket of goods Price Index & Inflation/Deflation

Price Index = Ratio of Price levels - Inflation (price level/index rising) - Deflation (price level/index falling)

Calculating Inflation

o Annual: o Cumulative:

Purchasing Power:

o Internal = amount g/s purchased with $1 in US. o External = amt g/s/ purchased with $1 outside US

Absolute Purchasing Power Parity: Exchange rates adjust to equalize internal and external purchasing powers of currency.

o Note SPPP is hypothetical XR, not real XR o IF Absolute PPP doesn’t work arbitrage. o Is arbitrage feasible?

- Shipping costs, labour costs, perishables?

Law of One Price:

o Perfect market = identical goods cost same once converted o LOOP = no arbitrage. If violated, then arbitrage o WHY LAW OF ONE PRICE VIOLATED?

- Tariff & Quota - Transac costs - Small mkt - Noncompetitive market - Sticky prices (menu costs)

Currency Over/Undervaluation:

o Overvalued: External PP>Internal PP (can buy more abroad) IMPORT CAD o Undervalued: Internal > External (buy more local) EXPORT CAS

Overvaluation one currency = undervaluation of other PREDICTIONS:

o OVERVALUED CURRENCY DEPRECIATE, UNDERVALUED APPRECIATE. Market & PPP XR:

o IF S> SPPP currency in numerator undervalued, denom overvalued

o If S< SPPP, numerator overvalued, denom undervalued. PPP Deviations & BOP

o Absolute PPP doesn’t always work (takes time for market XR to converge to PPP XR) - Currency overvalued = external PP greater, import more, Current account weaken, currency depreciate.

Relative PPP

Consider mkt imperfections

Over/undervaluations last for a while, due to a reason eg China weakened RMB Real XR (exchange between consumptions of 2 countries) Mkt XR: exchange between 2 currencies PPP XR: hypothetical nominal XR, real XR=1