Embed Size (px)

Citation preview

BAB.5025.0001.0102

>l RURAL BANK

BOARD CREDIT COMMITTEE

MEETING

Tuesday 12th March 2013 at 8:00AM (ACST)

Board Credit Committee

March 2013 2

AGENDA Present / Apologies

Declarations of Pecuniary / Conflict of Interest

1 Opening Items 4

1.1 Minutes of Meeting Dated 6th February 2013 5

1.2 Matters Arising Schedule 10

1.3 Committee Program 11

2 Executive Summary 12

3 Portfolio Performance 18

3.1 Portfolio Balance and Utilisation 19

3.2 Loan Performance – Total Portfolio by Dollars 21

3.3 Loan Summaries 24

3.4 Asset Composition 25

3.5 CRR Movements 26

3.6 CRR Migration - National 27

3.7 Clients with Exposure ≥ 5% of Bank Capital 28

3.8 Clients with Exposure ≥ $5 Million 29

3.9 Geographic Concentration 31

3.10 Industry Concentration (By Cash Flow Income Source) 32

4 New Lending 33

4.1 Loan Approval Summaries 34

4.2 Approval Categories 38

4.3 Summary of Loan Approvals by Managing Director & Management Credit

Committee 39

4.4 Summary of Loan Approvals by Board Credit Committee 41

4.5 Summary of Loan Approvals for Board Notification 43

4.6 Summary of Business Banking Loan Approvals 43

BAB.5025.0001.0103

BAB.5025.0001 .0104

>l RURAL BANK Board Credit Committee

5

6

7

8

Credit Quality

5.1 Credit Qual ity Report

5.2 Loan Book Performance

5.3 Over Limit and Arrears > 90 Days

5.4 Over Limit and Arrears> 30 Days

5.5 Impaired Assets

5.6 Provisioning

5.7 Large Exposures Over Limit

5.8 AMIS Accounts Overdue

Compliance

6.1 Related Party Exposures

6.2 Counterparty Limits - Exposures

6.3 Preferred Underwriting Standards

6.4 Reviews Outstanding

6.5 Internal Control Program

Management Reports

7.1 Transfer of Elders Ltd Security Documentation

7.2 Confidential

7.3 Rural Portfolio Feb 13 Quarterly Stress Test Update

44 45

45

46

47

49

54

56

78

79

80

81

82

84

85

86

87

89

92

7.4 Credit Framework and Operations Review ("CFOR'') Project 101

7.5 Credit policy and process manuals - valuation of security 104

7.6 Credit Policy and process - LSR for broad acre land 137

7.7 Credit Policy and Process - LSR Non Broad Acre 141

7.8 Write Offs 143

7.9 New Provisions Agricultural Managed Investment Scheme Loans 150

7.10 Confidential

7:11 Elders Limited

Reference Material

8.1 Local Conditions

8.2 Delegated Lending Authorities

8.3 Credit Risk Grading System

8.4 Rural Bank Limited Board and Committee Meeting Schedule

153

155

159

160

163

165

168

Next Meeting: 24 April 2013 3:30PM (ACST)

March 2013 3

Board Credit Committee

March 2013 4

1 Opening Items

1.1 Minutes of Meeting Dated 6th February 2013 5

1.2 Matters Arising Schedule 10

1.3 Committee Program 11

BAB.5025.0001.0105

BAB.5025.0001.0106

>l RURAL BANK Board Credit Committee

I 1.1 MINUTES OF MEETING DATED 5 tR FEBRUARY 2013

PRESENT:

ATTENDEES:

Minutes of a meeting of the RURAL BANK LIMITED

BOARD CREDIT COMMITTEE Held at the Rural Bank Board Room

Bendigo Bank Board Room On Wednesday 6 February 2013 at 8,0oam (ACST)

Mr J P Patton - Chairman Mr J T Hazel - Director Mr RE Pinney - Director Mr PG Hutchinson - Managing Director Mr T Piper - Bendigo and Adelaide Bank Mr S Gorman - Bendigo and Adelaide Bank

Mr B Speirs- Chief Financial Officer Mr M G Ormsby - General Manager Credit Mrs V V Duncan - General Manager Risk Mr P B Corolis - General Manager Operations Mr B F Debenham - General Manager Business Capability Mr S M Moore - General Manager Sales Mr J Marshall - General Manager Marketing Mr A B Wilkinson - Head of Asset Management Mr AG G Waddington - Senior Manager Head Office Mr M W Davidson - Senior Manager Credit Risk

DECLARATIONS OF PECUNIARY/CONFLICT OF INTEREST

1. OPENING ITEMS

1.1 The Minutes from the previous meeting held on 14 December 2012 were approved by the Committee.

1.2 The Committee noted and agreed the Matters Arising Schedule.

1.3 The Committee noted the Board Credit Committee Program.

1.4 The Chairman welcomed and congratulated Mrs Duncan on her appointment as General Manager Risk and thanked Mr Davidson for his assistance over the past 18 months.

2. EXECUTIVE SUMMARY

The Committee noted the Executive Summary Report.

Matters discussed were: -

• •

• •

March 2013

Initial damage reports frotn clients impacted by the Queensland floods have not been significant; There have been a number of approvals for significant amounts over the past few months, however hav~et to progress to draw down; Facilities torGGMP® l>H.9M and 1•$9@ $29.4M are now in order; and General Manager Credit is attending a finance sector briefing with the Victorian Minister for Agriculture later in the week re issues affecting the dairy industry.

5

BAB.5025.0001.0107

>t RURAL BANK Board Credit Committee

3. PORTFOLIO PERFORMANCE

The Committee noted the Portfolio Performance Reports.

Specific items were discussed were as follows:

3.1 O Exposures > 5% of Bank Capital (Quarterly Reporting)

liml~l®t Mr Hutchinson advised the development of an Agri Trust was being progressed for consF&i1on y the Board. Mr Hutchinson advised if the Agri Trust proceeded, m1would likely be the first client included.

application to be re-submitted to the Committee to cover changes to

••*W® Head ot AMU visiting client later in the week to complete review, updated valuations being finalised.

4. NEW LENDING

The Committee noted the New Lending Reports.

5. CREDIT QUALITY

The Committee noted the Credit Quality Reports.

Specific items were discussed were as follows:

5.5 Impaired Assets

~- delayed settlement should be completed later today, additional provision of $300k will be -;eqrn;ecr-Conl1denltal - offer received for $2M with $1.5M on settlement, balance to be received over the following 6 months with a possible write back of $400k.

Confidential - property now settled, additional provision required of $30k.

deposit cheque for the sale o•mm®•was dishonoured, however selling a.gent did not notify the Bank or Receiver.

--offer received for $1.45M, subject to finance.

Conf1de11t1al - • 1d"*has sold property to neighbour for $1.4M who will allowMHPlfl"to remain in the house, settlement expected in 30 days. Action to commence againstllllshortly.

Confidential $4.65M unconditional contract received, no further provision required.

lfiiG®®• contracts issued for $1 .1 M, additional provision of $250 required.

~farming property settled earlier this week, bush block remains unsold.

Conl1dent1al - updated valuation received for $1 .2M.

Mr Hazel noted that it appeared at times the recovery process was being delayed by varying actions instigated by some clients.

Mr Wilkinson advised at times, clients were seeking to delay or cease the recovery process by engaging provisions under the Financial Ombudsman Service (FOS). Although it may eventually be determined the

March 2013 6

BAB.5025.0001.0108

>t RURAL BANK Board Credit Committee

client's circumstances had always fallen outside of the FOS jurisdiction, the Bank is required to undertake the due process of the FOS scheme.

Mr Wilkinson noted that due to FOS interaction or Farm Debt Mediation requirements, it was imperative that a discrete recovery process was investigated as soon as accounts entered a default position as regularisation or recovery was taking at least 12 months to achieve in many instances.

5. 7 Large Exposures Over Limit

Confidential -facilities now in order.

Confidential refinancing attempts are still progressing.

Confidential - exe~ution of O.eed of forbearance is still being progressed with client and legal representatives.

6. COMPLIANCE

The Committee noted the Compliance Reports.

7. MANAGEMENT REPORTS

The Committee noted the Management Reports.

Specific items discussed were as follows:

7.1 Transfer ot Elders Limited Security Documentation

The Committee noted the report.

7.2 Southern Finance Limited (SFU

Mr Waddington advised due diligence had been completed covering 237 clients totalling $103M.

A desktop Credit Risk Rating (CAR) tor the portfolio was calculated for CAR 1. to 5 of $78M (215 clients) and CRR 6 to 9 of $25M (22 clients). Of these, 17 clients or $21 M would be assumed by AMU.

Two olients were identified as each requiring a $1 OOk provision (exposures of $3.SM and $355k).

Mr Hazel enquired if sufficient provisioning has been allocated to this portfolio.

Mr Gorman advised a bulk amount had been allocated to the enti re transaction, not just the Rural Bank portion. Individual facilities would be assigned to Rural Bank Balance Sheet at face value less any applicable provision.

Mr Hazel requested that Mr Pinney reviews and approves the valuation of the portfolio being assigned to Rural Bank.

Mr Waddington advised the Bank had been engaged by BEN to participate in a Stage 1 tender due diligence process on a Banksia Securities portfolio of 121 clients for $46M.

7.3 Geographic Concentration - District W2

The Committee noted the report.

7.4 Panel Valuers

The Committee noted the report.

March 2013 7

BAB.5025. 0001. 0109

>t RURAL BANK Board Credit Committee

7.5 Credit Framework and Operations Review

The Committee noted the report and requested General Manager Risk and General Manager Business Capability to keep the Committee informed on how the Risk Appetite Statement will be engrained within the Bank's operations.

Mr Pinney enquired how changes can be made to ensure the Credit Risk Rating is updated on a timely basis.

Mr Debenham advised the proposed Credit Risk Rating (CAR) system changes to ABS will assist with reviewing and amending a client's CRR each time a Banker or Credit & Lending staff materially interact with a client's Credit File I loan facilities.

7.6 Agribusiness Sector Guidelines (ASG)

The Committee noted the ASGs.

Mr Gorman noted as Rural Bank referred new Business Banking leads to BEN, a protocol should be established to facilitate the referral process and contact points to ensure a positive customer experience and result

7.7 Credit Policy and Procedures Manual

The Committee approved the review of the manuals.

7.8 Elders Limited

I

The Committee noted the paper.

OTHER BUSINESS

Review of Delegated Lending Authorities

Mr Ormsby confirmed he was undertaking a review of the Delegated Lending Authorities (DLA) which included liaising with various stakeholders.

Matters under consideration included: -

• Reducing DLA matrices from 4 to 2; • Increasing DLA levels; • Temporary Limtt approval criteria and amount; • Additional lending without going to a higher DLA; • DLAs for Relationship Managers (RBL personnel); • Expansion of Management Credit Committee (MCC) activities; and • Changes to the Post Decision Overview (PDO) process to incorporate above.

The Committee acknowledged the work being undertaken and requested the above matters be advanced along with the development of training and accreditation of DLA holders, MCC responsibilities and PDO process with Mr Gorman and General Manager Risk and re-submit to the Committee.

Confidential

The Committee was advised the Bank is currently in negotiations and I or progressing on the following matters: -

• Confirmation the CEO of the District Council of the Copper Coast will be appointed to act on behalt of the Council;

March 2013 8

Board Credit Committee

March 2013 9

• The Council has expressed an interest in the golf course on the basis it will be gifted to them plus seed funds supplied for three years;

• Outstanding Stamp Duty issues with the State Government; • Greg Norman is supportive of attempts to maintain the golf course; and • Kevin McGuiness will be engaged on a retainer and assume management of the development.

Mr Patton noted further capital expenditure was on hold pending approval of budgets. Mr Gorman requested care be taken to ensure the resultant facilities are recorded correctly on the Balance Sheet.

The meeting closed at 9.50am.

Next meeting: Tuesday 12 March 2013 at 8.00am (CST) in Adelaide.

Minutes confirmed……………………………… (Chairman)

BAB.5025.0001.0110

Board Credit Committee

March 2013 10

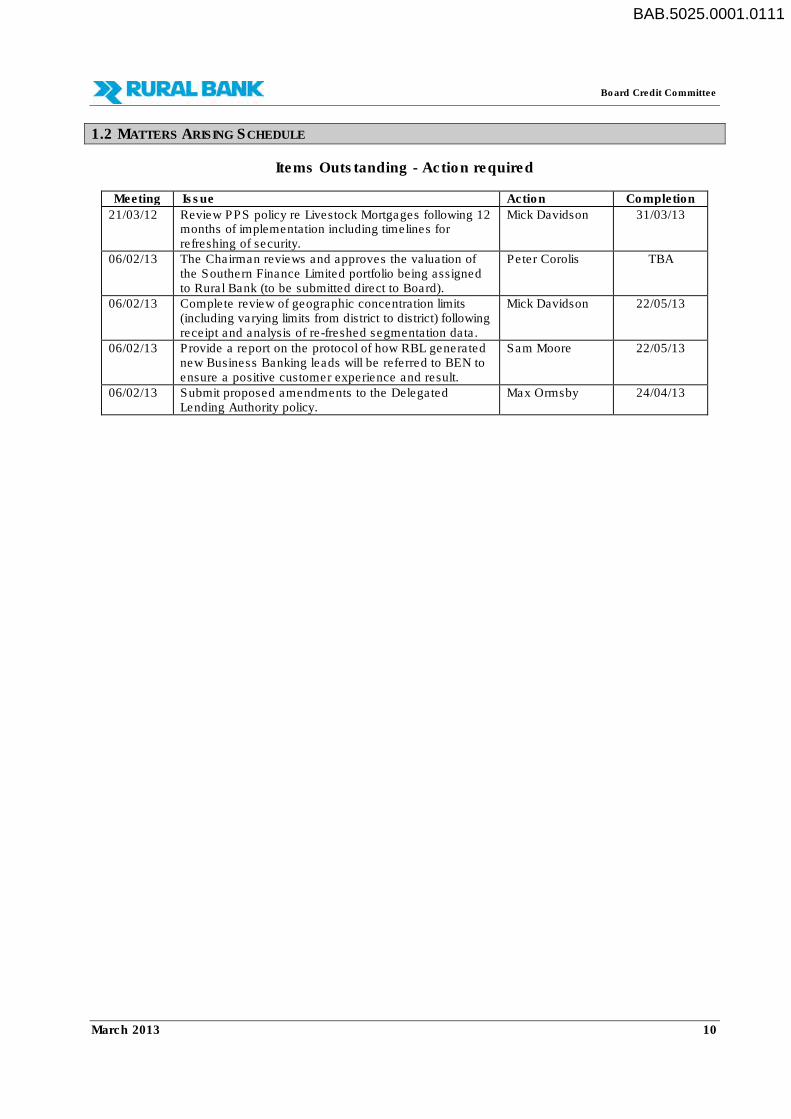

1.2 MATTERS ARISING SCHEDULE

Items Outstanding - Action required

Meeting Issue Action Completion

21/03/12 Review PPS policy re Livestock Mortgages following 12 months of implementation including timelines for refreshing of security.

Mick Davidson 31/03/13

06/02/13 The Chairman reviews and approves the valuation of the Southern Finance Limited portfolio being assigned to Rural Bank (to be submitted direct to Board).

Peter Corolis TBA

06/02/13 Complete review of geographic concentration limits (including varying limits from district to district) following receipt and analysis of re-freshed segmentation data.

Mick Davidson 22/05/13

06/02/13 Provide a report on the protocol of how RBL generated new Business Banking leads will be referred to BEN to ensure a positive customer experience and result.

Sam Moore 22/05/13

06/02/13 Submit proposed amendments to the Delegated Lending Authority policy.

Max Ormsby

24/04/13

BAB.5025.0001.0111

Board Credit Committee

March 2013 11

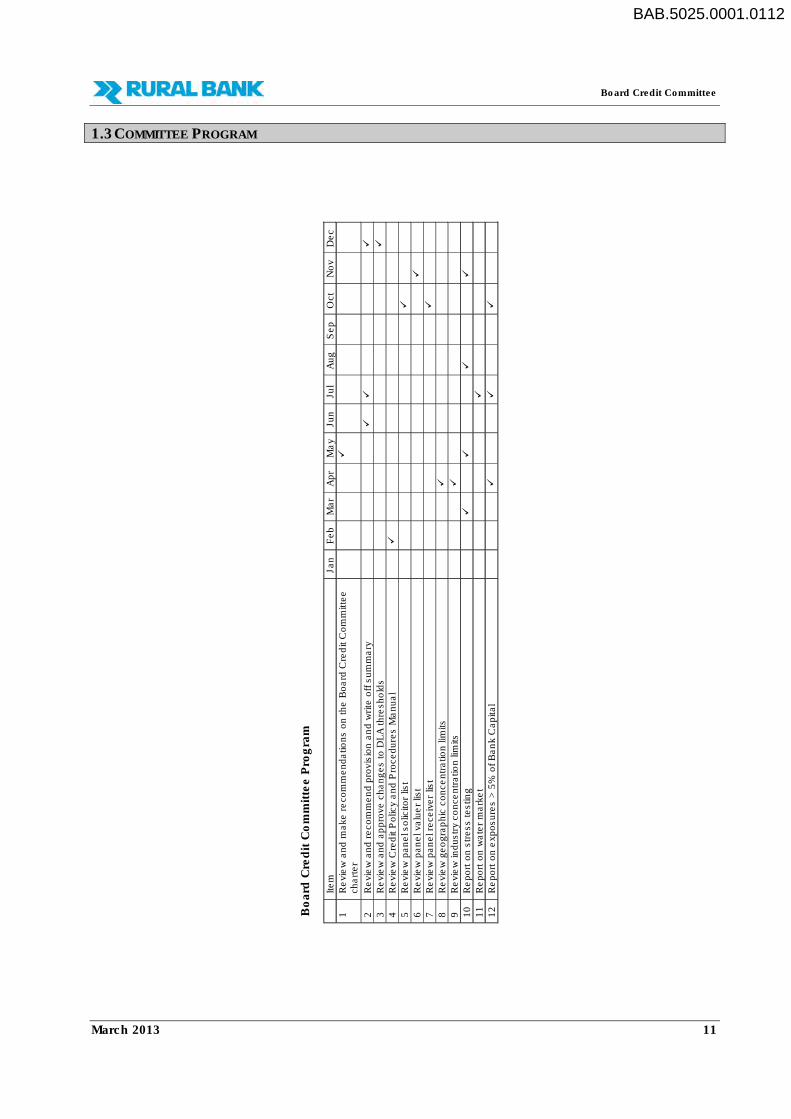

1.3 COMMITTEE PROGRAM

B

oard

Cre

dit

Co

mm

itte

e P

rog

ram

Item

Jan

F

eb

M

ar

Apr

Ma

y Ju

n

Jul

Aug

Sep

O

ct

No

v D

ec

1

Re

vie

w a

nd

make r

eco

mm

enda

tions o

n t

he B

oa

rd C

red

it C

om

mitte

e

cha

rter

�

2

Re

vie

w a

nd

recom

men

d p

rovis

ion

an

d w

rite

off

sum

ma

ry

�

�

�

3

Re

vie

w a

nd

ap

pro

ve c

ha

ng

es to D

LA

thre

sho

lds

�

4

Re

vie

w C

red

it P

olic

y a

nd P

rocedure

s M

anua

l

�

5

Re

vie

w p

an

el s

olic

itor

list

�

6

Re

vie

w p

an

el va

lue

r lis

t

�

7

Re

vie

w p

an

el r

eceiv

er

list

�

8

Re

vie

w g

eo

gra

phic

conce

ntr

atio

n li

mits

�

9

Re

vie

w in

dustr

y co

nce

ntr

atio

n li

mits

�

10

R

eport

on s

tress testin

g

�

�

�

�

11

R

eport

on w

ate

r m

ark

et

�

12

R

eport

on e

xposure

s >

5%

of B

an

k C

apital

�

�

�

BAB.5025.0001.0112

Board Credit Committee

March 2013 104

7.5 CREDIT POLICY AND PROCESS MANUALS - VALUATION OF SECURITY

Management Report TYPE OF MEETING: Board Credit Committee (“BCC”) DATE OF MEETING: 12 March 2013 SUBJECT: Review of credit policy and credit process manuals in respect of the valuation

of security

Purpose

Based on feedback received from staff within Credit and Lending/the Asset Management Unit and RBLs distribution partners, RBL has undertaken a comprehensive review of its policies and processes in respect of the valuation of its security.

Discussion RBL sought feedback from a number of bankers and credit and lending staff to assess what changes should be considered to be made to the valuations policy and process. The feedback received indicates that the narrative within the current Credit Policy and Credit Process Manuals is either duplicated, out of date, difficult to understand/interpret and/or misleading. The relevant sections in respect of properties, valuations, real estate market appraisals, etc within the Credit Policy Manual and the Credit Process Manual have been reviewed and re-written taking into account the above feedback and recent recommendations that have been submitted to the BCC. In addition to the above, we note that BEN has established specific policy in respect of Property Construction, Development and Land Subdivision (“Property Development”). The RBL Credit Policy manual makes specific reference to the BEN credit policy and guides all RBL staff and RBL distribution partners to the BEN Credit policy in respect of Property Development. This has been done to ensure that the RBL approach, methodology and credit assessment of such transactions is absolutely consistent with that of BEN. The re-written sections of the Credit Policy Manual and the Credit Process Manual in respect of the Valuations of Security are attached as Annexure A and Annexure B respectively. As previously advised to the BCC, RBL will be providing REMA and FCV training to RBL, BEN and ERS staff which is expected to be delivered in late April/early May 2013. The roll-out of this training will also include sessions which will focus on: � Communication of the credit policy and process (in particular the recent changes that have been made

approved by the BCC); and � Understanding and Application – users of the credit policy will be provided with training to ensure that it

is properly understood and applied by all staff involved in the credit assessment process. Recommendation It is recommended that the sections within the Credit Policy Manual and the Credit Process Manual in respect of the Valuations of Security are approved by the BCC.

BAB.5025.0001.0113

Board Credit Committee

March 2013 105

Written and recommended by Bruce Debenham General Manager, Business Capability Supported by Max Ormsby General Manager, Credit Supported by Veronica Duncan General Manager, Risk Supported by Paul Hutchinson, Managing Director

BAB.5025.0001.0114

>~RURAL BANK ANNEXURE A- Valuations of Security - Policy

VALUATION OF SECURITIES - POLICY

GLOSSARY OF TERMS

ALFA AMU API BEN DLA ERS FCV ICP LLV LSR LVR RBL REIA REMA RHOC RWR SA-V ZBM

PURPOSE

Australian Livestock & Property Agents Association Asset Management Unit Australian Property Institute Bendigo and Adelaide Bank Delegated Lending Authortty Elders Rural Seivices Full Certified Valuation Internal Control Program Loan to Lending Value Ratio Loan to Securtty Ratio Loan to Value Ratio Rural Bank Limited Real Estate Institute of Australia Real Estate Market Appraisal Regional Head of Credit Ray White Rural Seivice Agreements - Valuations Zone Banking Manager

BAB.5025.0001 .0115

Board Credit Commi ttee

The purpose of this policy is to establish standard tenninology and processes to identify and value assets charged to RBL as securtty. These processes will only be applied where RBL securtty documentation and legal requirements have been fully satisfied.

This document addresses the valuation policy and procedures to be applied to:

• Real Property; • Property Improvements; • Specialised Improvements; • Livestock; • Crops; • Water Entitlements; • Other Assets; • Guarantee From an ADI; and • First Charge Over a RBL Tenn Deposit

LENDING AND SECURITY RATIOS EXPLAINED

Overview

The valuation policy takes, as a starting point, the detennination of market value which is the estimated amount for which an asset should exchange on the date of valuation:

• in an ann's length transaction; • between a willing buyer and willing seller; • after proper marketing; and • wherein the parties had each acted knowledgeably, prudently and without compulsion.

March 2013 106

Board Credit Committee

March 2013 107

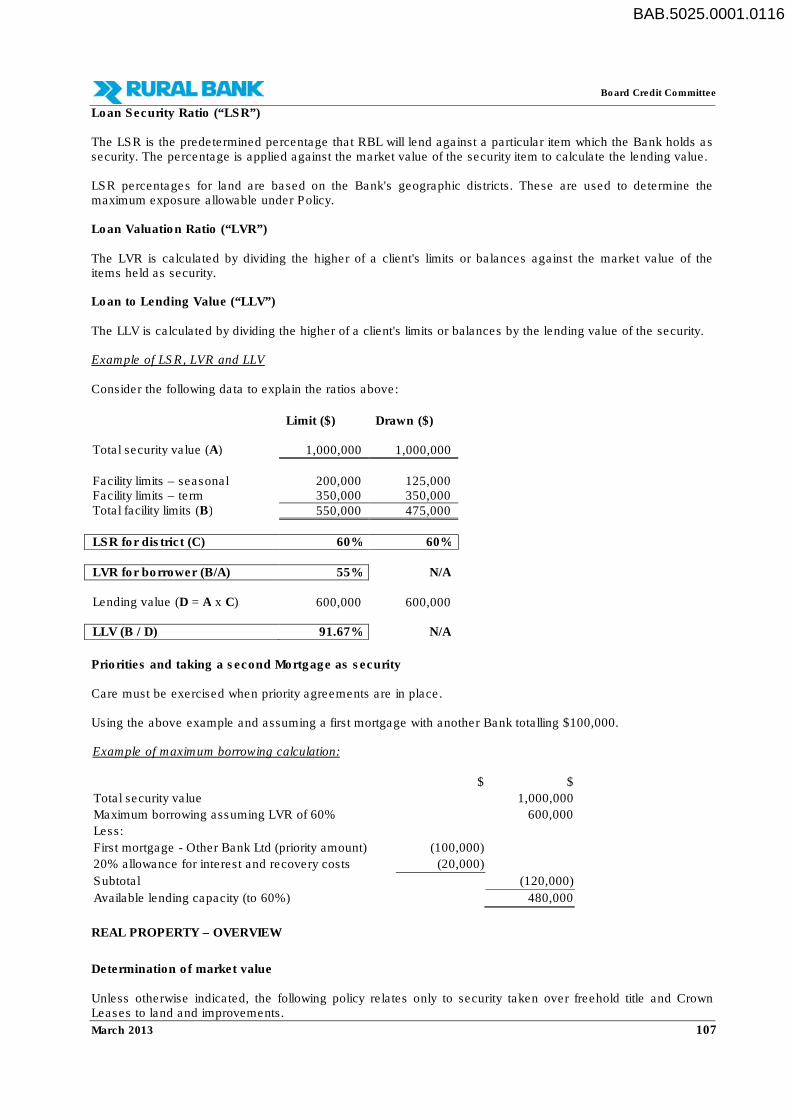

Loan Security Ratio (“LSR”) The LSR is the predetermined percentage that RBL will lend against a particular item which the Bank holds as security. The percentage is applied against the market value of the security item to calculate the lending value. LSR percentages for land are based on the Bank's geographic districts. These are used to determine the maximum exposure allowable under Policy. Loan Valuation Ratio (“LVR”) The LVR is calculated by dividing the higher of a client's limits or balances against the market value of the items held as security. Loan to Lending Value (“LLV”) The LLV is calculated by dividing the higher of a client's limits or balances by the lending value of the security. Example of LSR, LVR and LLV Consider the following data to explain the ratios above:

Limit ($) Drawn ($) Total security value (A) 1,000,000 1,000,000

Facility limits – seasonal 200,000 125,000 Facility limits – term 350,000 350,000 Total facility limits (B) 550,000 475,000

LSR for district (C) 60% 60% LVR for borrower (B/A) 55% N/A Lending value (D = A x C) 600,000 600,000 LLV (B / D) 91.67% N/A

Priorities and taking a second Mortgage as security Care must be exercised when priority agreements are in place. Using the above example and assuming a first mortgage with another Bank totalling $100,000. Example of maximum borrowing calculation:

$ $

Total security value 1,000,000

Maximum borrowing assuming LVR of 60% 600,000

Less:

First mortgage - Other Bank Ltd (priority amount) (100,000)

20% allowance for interest and recovery costs (20,000)

Subtotal (120,000)

Available lending capacity (to 60%) 480,000

REAL PROPERTY – OVERVIEW

Determination of market value Unless otherwise indicated, the following policy relates only to security taken over freehold title and Crown Leases to land and improvements.

BAB.5025.0001.0116

BAB.5025.0001 .0117

>~RURAL BANK Board Credit Commi ttee

Generally valuations and appraisals will be based on market value, with the major consideration being the sales of comparable nearby property and the relevant factors Impacting on value as determined by the completing officer.

Sales evidence should be no more than 12 months old. If no recent sales are evident then matter should be referred to the State Credit and Lending Manager and/or the DLA holder for their direction.

OTHER MATTERS

Provisioning requirements

An amount equal to at least 5% of the market value will be used as a discount In the calculation of specific provisioning requirements. This percentage amount is to cover legal and selling costs associated with the security property.

Industry limits

From time to time individual industries may experience Internal and external issues which can affect the viability of the industry. During these times, the General Manager Rlsk may temporarily amend the LSR for specific industries and/or districts.

Legal forms of possession

The following are legal forms of possession:

• Freehold: the absolute right to land and/or buildings (Improvements). • Leasehold: the right to use and hav e exclusive possession (but not ownership) of real estate for a specified

period and subject to the fulfilment of certain conditions as recorded In a lease agreement. Examples of leasehold are western lands and Crown Lands.

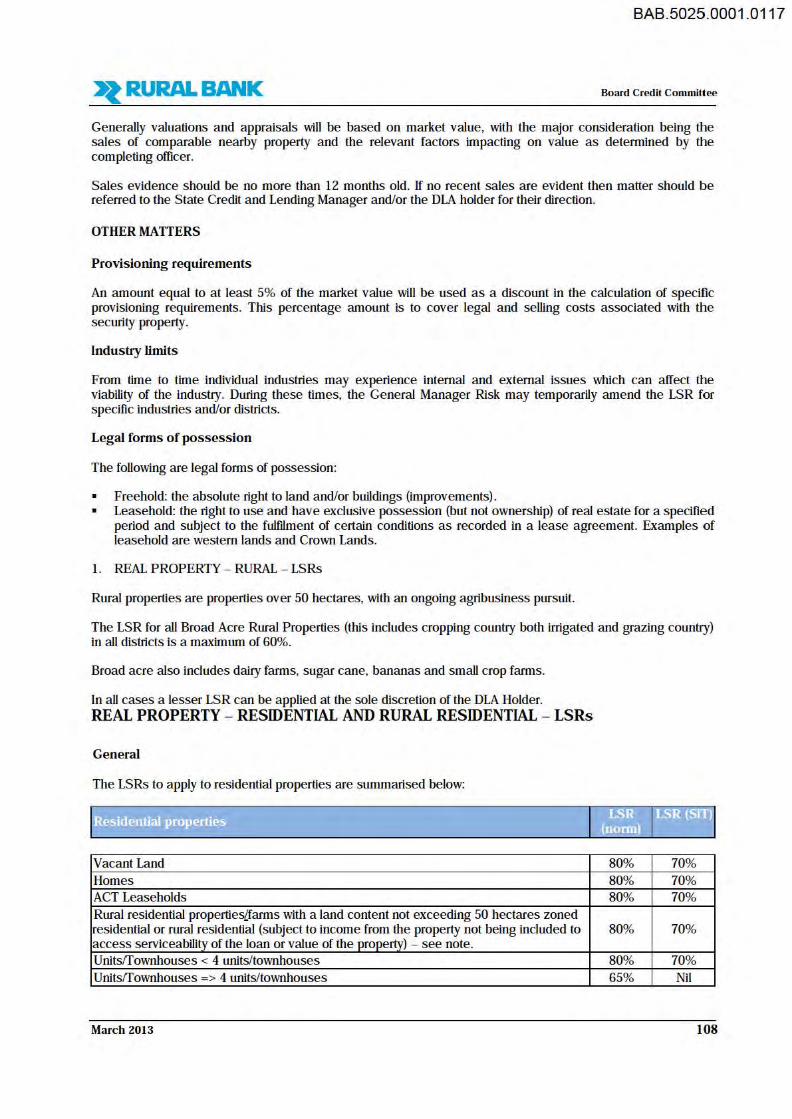

1. REAL PROPERTY - RURAL - LSRs

Rural properties are properties over 50 hectares, with an ongoing agribusiness pursuit.

The LSR for all Broad Acre Rural Properties (this includes cropping country both Irrigated and grazing country) in all districts is a maximum of 60%.

Broad acre also includes dairy farms, sugar cane, bananas and small crop farms.

In all cases a lesser LSR can be applied at the sole discretion of the DLA Holder. REAL PROPERTY - RESIDENTIAL AND RURAL RESIDENTIAL - LSRs

General

The LSRs to apply to residential properties are summarised below:

Vacant Land 80% 70%

Homes 80% 70% ACT Leaseholds 80% 70%

Rural residential propertiesLfarms with a land content not exceeding 50 hectares zoned residential or rural residential (subject to Income from the property not being included to 80% 70% access serviceability of the loan or value of the property) - see note. Units!fownhouses < 4 units/ townhouses 80% 70%

Units!fownhouses => 4 units/ townhouses 65% Nil

March 2013 108

BAB.5025.0001.01 18

>~RURAL BANK Board Credit Committee

Note:

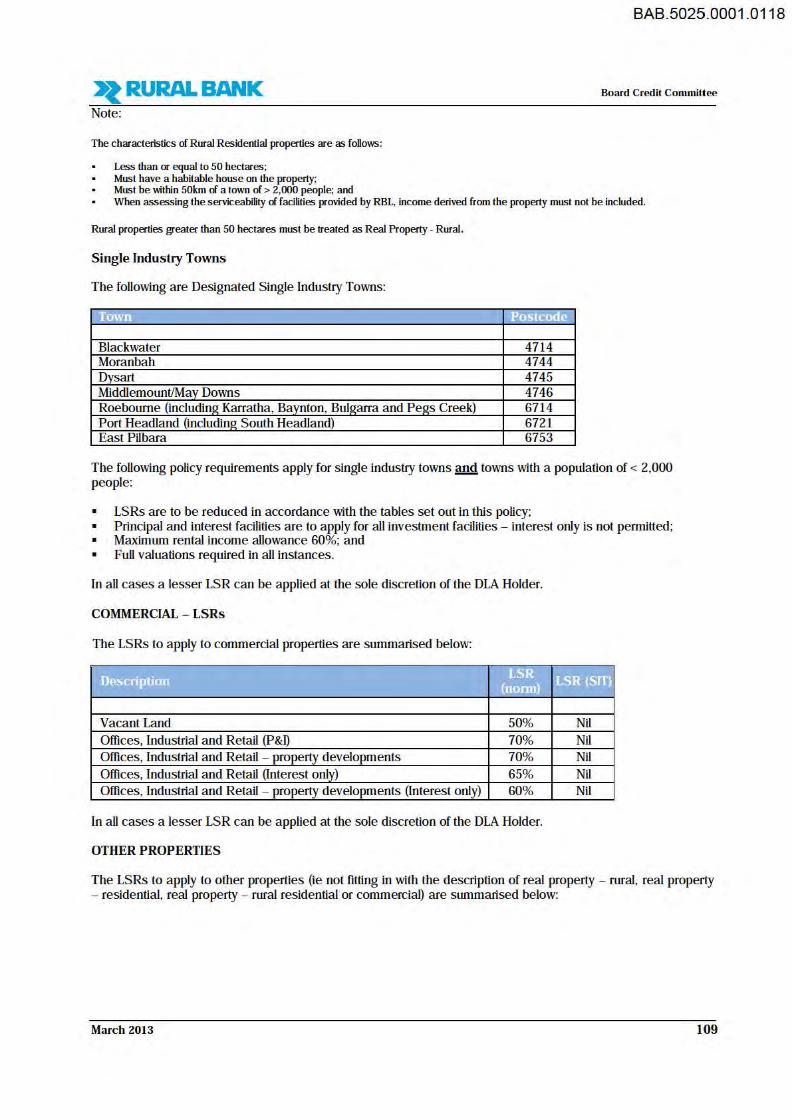

The characteristics of Rural Residential properties are as follows:

Less than or equal to 50 hectares; Must have a habitable house on the property; Must be within 50km cl a town cl> 2,000 people; and When assessing the serviceability cl facilities provided by RBL, income derived from the property must not be included.

Rural properties greater than 50 hecta-es must be treated as Real Property- Rural.

Single Industry Towns

The following are Designated Single Industry Towns:

"ll'iWlil 1!.r11..." 1•• em

Blackwater 4714 Moran bah 4744 Dysart 4745 Mlddlemount/May Downs 4746 Roebourne (including Karratha, Baynton, Bulgarra and Pegs Creek) 6714 Port Headland (includinu: South Headland) 6721 East Pilbara 6753

The following policy requirements apply for single industry towns and towns with a population of < 2,000 people:

• LSRs are to be reduced in accordance with the tables set out in this policy; • Principal and interest facilities are to apply for all investment facilities - interest only is not permitted; • Maximum rental income allowance 60%; and • Full valuations required in all instances.

In all cases a lesser LSR can be applied at the sole discretion of the DLA Holder.

COMMERCIAL - LSRs

The LSRs to apply to commercial properties are summarised below:

- - .)Ifill_ IJ£fill [{fili JI. I !l.ll!lll .. I 1• 111

Vacant Land 50% Nil Offices, Industrial and Retail (P&l) 70% Nil Offices, Industrial and Retail - property developments 70% Nil Offices, Industrial and Retail (Interest only) 65% Nil Offices, Industrial and Retail - property developments (Interest only) 60% Nil

In all cases a lesser LSR can be applied at the sole discretion of the DLA Holder.

OTHER PROPERTIES

The LSRs to apply to other properties (le not fitting in with the description of real property - rural, real property - residential, real property - rural residential or commercial) are summarised below:

March 2013 109

BAB.5025.0001 .0119

>~RURAL BANK Board Credit Commi ttee

- - ~- IJ£fill [{fili JI. I !l.ll!lll .. I 1• 111

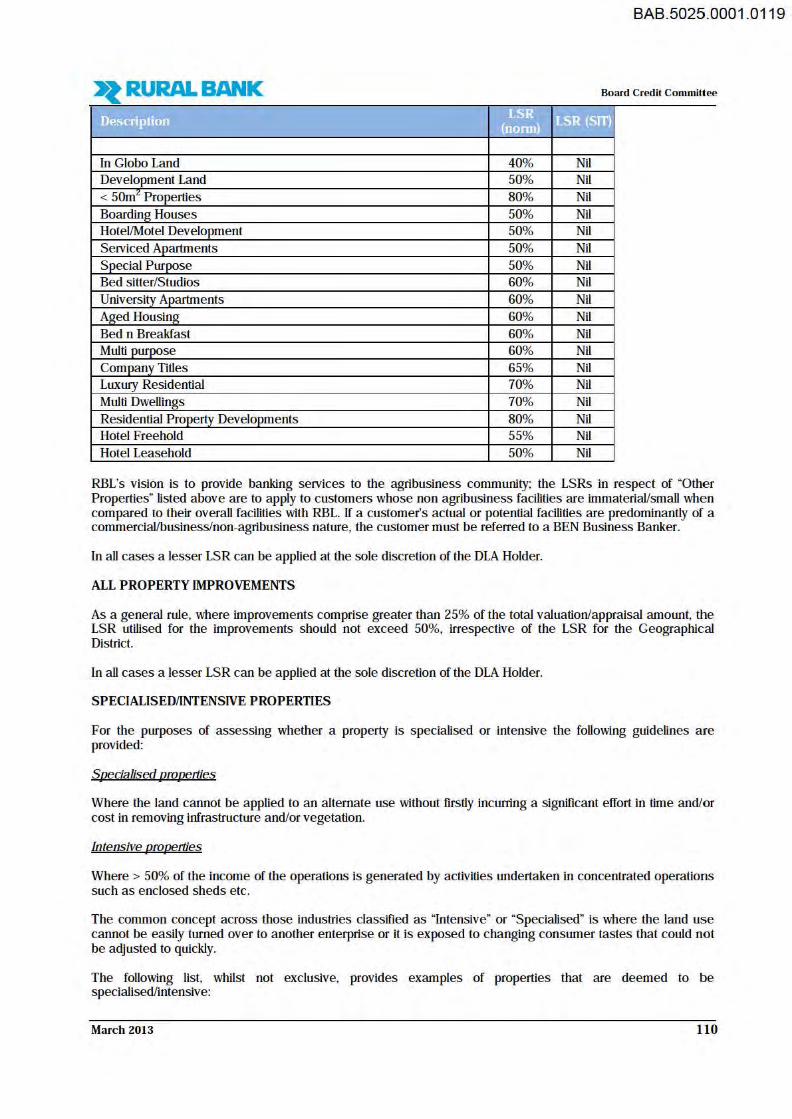

In Globo Land 40% Nil Development Land 50% Nil < 50mG Properties 80% Nil Boarding Houses 50% Nil Hotel/Motel Development 50% Nil Serviced Apartments 50% Nil Special Puroose 50% Nil Bed sitter/Studios 60% Nil University Apartments 60% Nil Aged Housing 60% Nil Bed n Breakfast 60% Nil Multi purpose 60% Nil Company Titles 65% Nil Luxury Residential 70% Nil Multi Dwellings 70% Nil Residential Property Developments 80% Nil Hotel Freehold 55% Nil Hotel Leasehold 50% Nil

RBL's vision is to provide banking services to the agribusiness community; the LSRs In respect of "Other Properties" listed above are to apply to customers whose non agribusiness facilities are Immaterial/small when compared to their overall facilities with RBL. If a customer's actual or potential facilities are predominantly of a commercial/business/non-agribusiness nature, the customer must be referred to a BEN Business Banker.

In all cases a lesser LSR can be applied at the sole discretion of the DLA Holder.

ALL PROPERTY IMPROVEMENTS

As a general rule, where Improvements comprise greater than 25% of the total valuation/appraisal amount, the LSR utilised for the Improvements should not exceed 50%, Irrespective of the LSR for the Geographical District.

In all cases a lesser LSR can be applied at the sole discretion of the DLA Holder.

SPECIALISED/INTENSIVE PROPERTIES

For the purposes of assessing whether a property Is specialised or Intensive the following guidelines a!l'e provided:

Soecialised prooerties

Where the land cannot be applied to an alternate use without firstly incurring a significant effort In time and/or cost In removing Infrastructure and/or vegetation.

Intensive prooerties

Where > 50% of the income of the operations Is generated by activities undertaken In concentrated operations such as enclosed sheds etc.

The common concept across those Industries classified as "Intensive" or "Specialised" Is where the land use cannot be easily turned over to another enterprise or it Is exposed to changing consumer tastes that could not be adjusted to quickly.

The following list, whilst not exclusive, provides examples of properties that are deemed to be specialised/intensive:

March 2013 110

Board Credit Committee

March 2013 111

� Feedlots � Intensive piggeries � Commercial cool stores and/or packing sheds � Woodlots � Wineries � Vineyards � Orchards of exotic fruits � Intensive horticulture (eg glass houses) � Broilers � Poultry sheds � Hot houses or covered farming � A property subject to an MIS or a lease to third party for more than 50% of the net farm area � Specialised improvements (eg a cheese factory on a dairy property) � Non permanent improvements (eg greenhouses) In all cases the LSR utilised for the specialised and intensive properties must not exceed 50%, irrespective of the Geographical District's LSR applied for the land only component. In all cases a lesser LSR can be applied at the sole discretion of the DLA Holder. PROPERTY CONSTRUCTION, DEVELOPMENT AND LAND SUBDIVISION Property development finance (which includes property construction and land subdivisions) usually involves special risk to RBL due to one or more of the following factors: � security is usually property under development and failure by the developer to complete it to a marketable

standard may impair RBL’s security position; � the potential for project cost overruns, or other increases, caused by construction delays, insolvency of the

builder, inaccurate original costings, variations to original design, or other factors; and/or � speculative nature of development where no ‘guaranteed’ take out exists. In view of the above, for all transactions that are deemed to be property construction, property development and/or property land subdivisions referral must be made to the BEN credit policy for “Property Construction, Development and Land Subdivision”. Please liaise with staff from the State and/or Head Office Credit and Lending department for further guidance. LIVESTOCK RBL will accept livestock which are secured by a livestock mortgage as security. Livestock LSR The LSR for livestock is 50% and is only applicable for beef and sheep. Should an existing stock mortgage secure livestock other than beef and/or sheep and an LSR of 50% has been applied against this livestock, the existing LSR may be honoured at the discretion of the DLA holder. For a new or existing client, a livestock mortgage may be taken over livestock other than beef and/or sheep, however no lending value will be applied. Stud stock If a herd/flock comprises stud stock and the value of the stud component of the overall value of the herd/flock is ≤ 10%, the value assigned to the stud stock maybe utilised. If a herd/flock comprises stud stock and the value of the stud component of the overall value of the herd/flock is > 10%, the value assigned to the stud stock must be a commercial/trade value. Stock numbers Livestock numbers are assessed by:

BAB.5025.0001.0120

Board Credit Committee

March 2013 112

� reviewing historical shearing/crutching documentation and forecast numbers supplied by the borrower in the loan application and

� confirming these numbers with a combination of a: � physical count; � review of the borrower's financial statements (balance sheets); and � consultation with the client's selling agent.

The livestock numbers may be adjusted (with supporting reasons/rationale) if deemed necessary by DLA holder. Warnings in respect of Pastoral Leases: � Care needs to be taken where stock numbers are generally an estimate only as the Relationship

Manager/ERS representative/external representative cannot complete a full physical count. � Livestock values should take into consideration the costs of mustering and transport to markets, which can

significantly lessen the security value of the livestock. Livestock insurance Insurance is only required for livestock when: � stud stock is taken as security (required only for stud stock component); or � the approving DLA holder has identified circumstances they determine necessitate the requirement of

insurance and have included such as an approval condition (this is expected to occur by exception). In all cases a lesser LSR can be applied at the sole discretion of the DLA Holder. CROPS The LSR for crops is 50%. RBL set crop values every season. The crop policy security values are available in the Crop policy calculator. Crop policy security values represent 100% of the estimated commodity value, less a deduction for costs. It is the responsibility of the Relationship Manager and the DLA holder to ensure the appropriate freight/storage/levies etc are deducted to obtain the farm gate return. Risk Management determine the appropriate value for each grain at the commencement of each calendar year Minimum four-year farm average A four-year farm average is used to determine crop yield for facilities secured by crop liens. If a four-year farm average cannot be obtained due to: � inadequate records being maintained or � the farm or farmers being new an Elders or suitably qualified external Agronomist with knowledge of the farm and/or farmer must be used to validate the yields (ie sign off). Formula The following formula is used to calculate the market value of crops for security assessment purposes. [(Four Year Farm Average or District Average Yield x Area Sown) x Crop Policy Security Value] An LSR of 50% for crops is applied to calculate the LLV.

BAB.5025.0001.0121

Board Credit Committee

March 2013 113

In all cases a lesser LSR can be applied at the sole discretion of the DLA Holder. WATER ENTITLEMENTS Overview � Where a water entitlement forms part of the Bank’s security, it must be valued separately in the

REMA/FCV. � The value of the water entitlement must be input separately into the ABS irrespective if the land

component also has an LSR of 50%. � Comparable water sales over the past 24 months must be included in REMAs/FCVs. � The lowest sale price must be used in ABS for security calculations. � In determining the lowest sale price, transactions for zero or of a non-commercial amount, must be

excluded in determining the lowest sale price. Government and Local Water Authority data � In instances where a Government instrumentality or water authority provides data on the median price per

mega litre for water sold and there is an actively traded market, this data may be utilised in valuing water. � In these instances, 90% of the average sale price over the previous 24 months maybe utilised to determine

the value of water. Ground water � In instances where the Bank's security is over ground water and comparative sale information is limited, the

REMA/FCV must comment on how the value was calculated. High security water schemes � A number of small, private water schemes have been established which have developed supply

infrastructure and entered into long term contracts for the provision of treated water for irrigation purposes. � The industries involved have included horticulture/viticulture and have allowed growers to remain at full

production. � Due to the high security water available to these schemes, the Bank may increase the LSR to 60% for both

the water security and land component of horticulture/viticulture industries within the scheme. � Outside these schemes the LSR for horticulture/viticulture must remain at 50%. � For an LSR of 60% to be approved for a particular scheme, approval is required by the General Manager

Credit. � At a minimum, the following factors will be considered in assessing any application:

� Scheme structure and size/membership conditions; � Condition of infrastructure; � Saleability of water entitlement; � Contract with water supply authority; � Specific security requirements; and � RBL's rights and obligations.

In all cases a lesser LSR can be applied at the sole discretion of the DLA Holder. OTHER ASSETS Other assets include plant and equipment, debtors and stock. Plant and equipment, debtors and stock can be taken as security under Specific Security Agreement or General Security Agreement where required. This form of security is generally seen as supporting security only, therefore no lending value is attributed.

BAB.5025.0001.0122

Board Credit Committee

March 2013 114

FIRST CHARGE OVER A RBL TERM DEPOSIT A Term Deposit held with RBL can be taken as security utilising an appropriate security document. Charge must be noted on the Term Deposit and funds not released without the debt the being repaid in full, or sufficient alternative security held. Any release of the charge must be approved by Credit and Lending, within DLA. The LSR for a RBL Term Deposit is 100%. GUARANTEE FROM AN ADI A Guarantee from an ADI with a minimum rating of BBB (Standard and Poors rating) can be taken as security. The Guarantee document must not have an expiry date. It must also be deemed appropriate and acceptable by the Bank’s Panel Solicitors. The Guarantee must not be released without the debt being repaid in full, or sufficient alternative security held. Any release of the Guarantee must be approved by Credit and Lending within DLA. The LSR for a guarantee from an ADI is 100%.

BAB.5025.0001.0123

BAB.5025.0001 .0124

>~RURAL BANK Board Credit Commi ttee

ANNEXURE B - Valuations of Security - Process

VALUATION OF SECURITIES - PROCESS

REAL EST ATE MARKET APPRAISALS - PROCESS

Overview

The REMA record details, amongst other things, the property, description of the country, production history, Irrigation, Improvements, comparable sales and basis of REMA. It Is mandatory that all sections are completed.

Overview

A REMA can be completed In the following circumstances:

I ®1!.Miii·~i«l16!1!.l.J1IW~'®®h!Ul''I!§~ s $3m 1 to 9 All other FCV

Timing and frequency of REMA

• REMAs are deemed to be valid and up to date If they are less than 2 years old at the time of the review. • REMAs which are considered to be out of date cannot be used. • Accredited Relationship Managers can undertake REMAs based on the total level of exposure. • For any accounts where the facility Is transferred to the control of Credit and Lending and/or AMU or the

facility becomes non-accrual (Impaired) , an updated REMA may be required. • The following table Indicates when a new REMA Is required:

No prior REMAs com leted

> 2 years

Note:

New REMA required

Not applicable

Not applicable

New REMA not required (see notes)

Not applicable

New REMA required

1. At the discretion of the DLA holder a new REMA may be requested for any facility. 2. Where a new REMA is not required, the Relationship Manager is required to provide commentary to

support that the current security values In ABS can still be relied upon.

Reduction in value

Where a reduction In value (for property where RBL has relied on an REMA) exceeds 10% over a 2 year period, the person who previously prepared the REMA may be requested to provide RBL with a written explanation as to the factors leading to a material reduction In value and addressing any other concerns raised by RBL.

Comparable sales greater than 12 months old

If all comparable sales are greater than twelve months old the Relationship Manager must seek guidance from the DLA holder as to how the appralsal/valuation Is to be addressed.

Who can complete REMAs?

Accredited Relationship Managers can complete REMAs. • At least one of the persons signing the REMA must undertake a comprehensive physical and on-site

inspection of the property. • The approving DLA holder can Insist on applying a higher authority level as and when deemed necessary

based on the assessment of credit risk.

March 2013 115

BAB.5025.0001 .0125

>~RURAL BANK Board Credit Commi tt ee

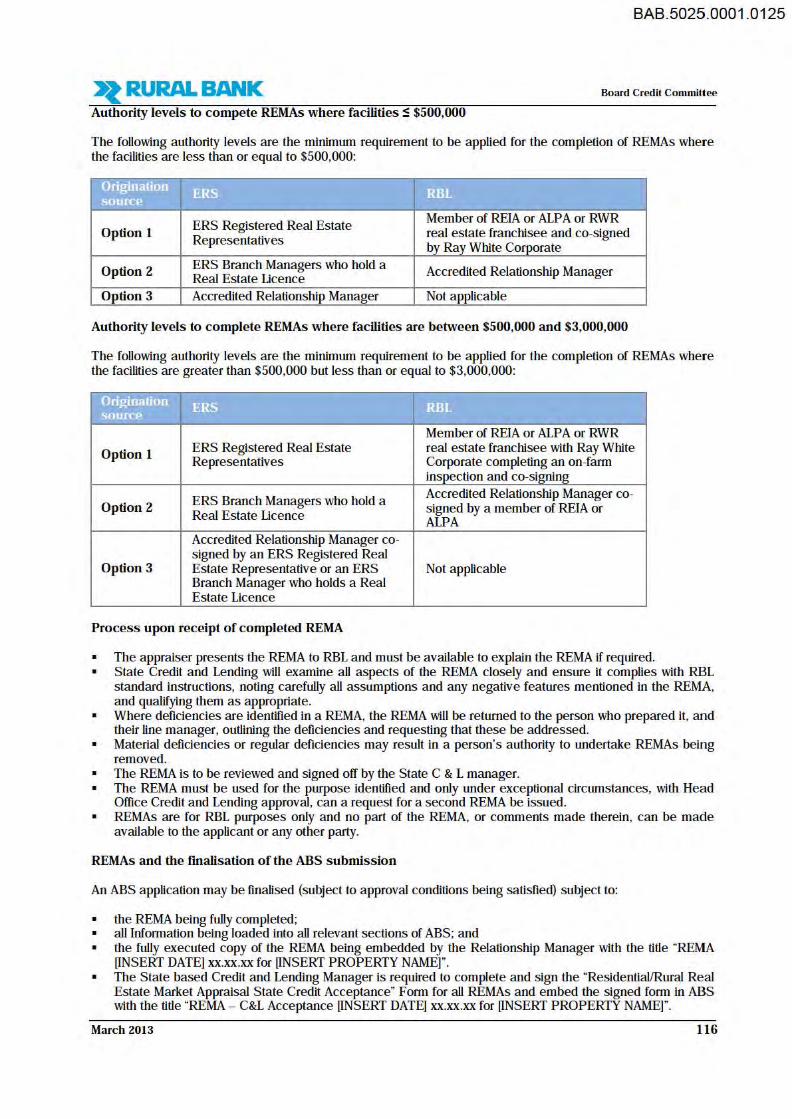

Authority levels to compete REMAs where facilities :S $500,000

The following authority levels are the minimum requirement to be applied for the completion of REMAs where the facilities are less than or equal to $500,000:

Origination source

ERS RBL

ERS Registered Real Estate Member of REIA or ALPA or RWR

Option 1 real estate franchisee and co-signed Representatives by Ray White Corporate

Option 2 ERS Branch Managers who hold a Accredited Relationship Manager Real Estate Licence

Option 3 Accredited Relationship Manager Not applicable

Authority levels to complete REMAs where facilities are between $500,000 and $3,000,000

The following authority levels are the minimum requirement to be applied for the completion of REMAs where the facilities are greater than $500,000 but less than or equal to $3,000,000:

Origination source ERS RBL

Member of REIA or ALPA or RWR

Option 1 ERS Registered Real Estate real estate franchisee with Ray White Representatives Corporate completing an on-farm

inspection and co-signing

ERS Branch Managers who hold a Accredited Relationship Manager co-

Option 2 signed by a member of REIA or Real Estate Licence ALPA Accredited Relationship Manager co-signed by an ERS Registered Real

Option 3 Estate Representative or an ERS Not applicable Branch Manager who holds a Real Estate Licence

Process upon receipt of completed REMA

• The appraiser presents the REMA to RBL and must be available to explain the REMA if required. • State Credit and Lending will examine all aspects of the REMA closely and ensure it compiles with RBL

standard instructions, noting carefully all assumptions and any negative features mentioned in the REMA, and qualifying them as appropriate.

• Where deficiencies are identified in a REMA, the REMA wlll be returned to the person who prepared it, and their line manager, outlining the deficiencies and requesting that these be addressed.

• Material deficiencies or regular deficiencies may result in a person's authority to undertake REMAs being removed.

• The REMA is to be reviewed and signed off by the State C & L manager. • The REMA must be used for the purpose identified and only under exceptional circumstances, with Head

Office Credit and Lending approval, can a request for a second REMA be issued. • REMAs are for RBL purposes only and no part of the REMA, or comments made therein, can be made

available to the applicant or any other party.

REMAs and the finalisation of the ABS submission

An ABS application may be finalised (subject to approval conditions being satisfied) subject to:

• the REMA being fully completed; • all Information being loaded into all relevant sections of ABS; and • the fully executed copy of the REMA being embedded by the Relationship Manager with the title "REMA

CTNSERT DATE] xx.xx.xx for CTNSERT PROPERTY NAME]". • The State based Credit and Lending Manager ls required to complete and sign the "Residential/Rural Real

Estate Market Appraisal State Credit Acceptance" Form for all REMAs and embed the signed form in ABS with the title "REMA - C&L Acceptance CTNSERT DATE] xx.xx.xx for CTNSERT PROPERTY NAME)".

March 2013 116

Board Credit Committee

March 2013 117

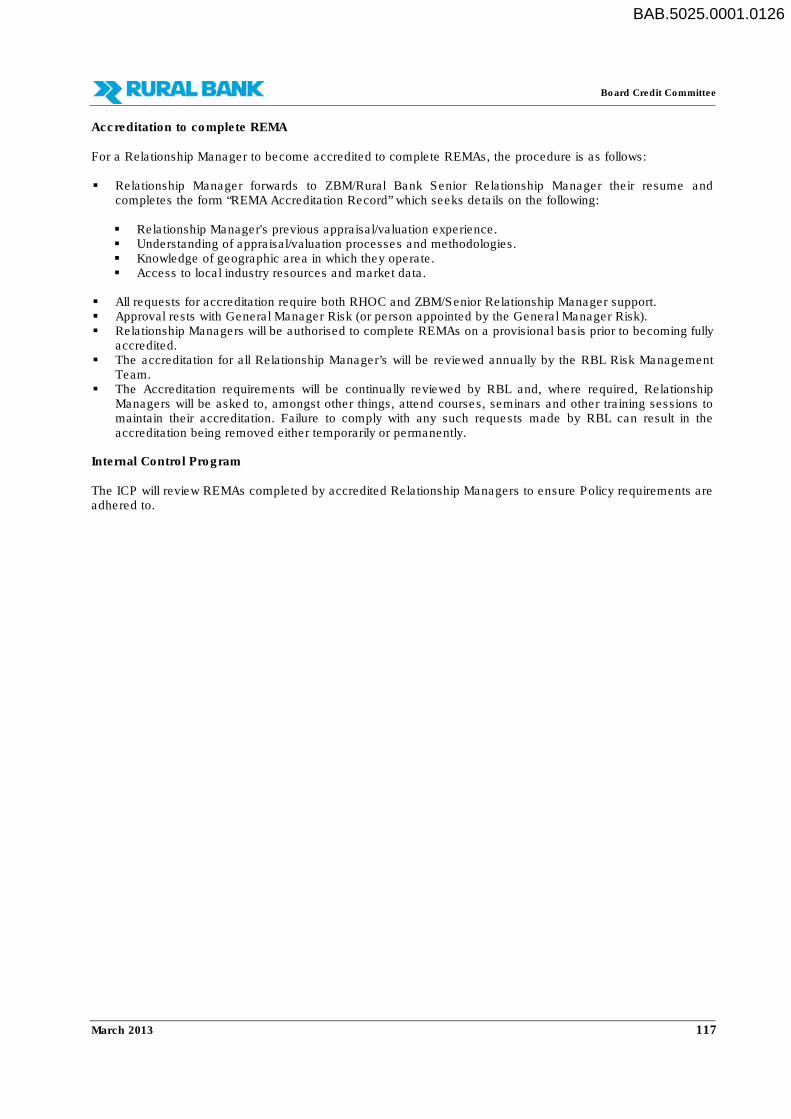

Accreditation to complete REMA For a Relationship Manager to become accredited to complete REMAs, the procedure is as follows: � Relationship Manager forwards to ZBM/Rural Bank Senior Relationship Manager their resume and

completes the form “REMA Accreditation Record” which seeks details on the following: � Relationship Manager's previous appraisal/valuation experience. � Understanding of appraisal/valuation processes and methodologies. � Knowledge of geographic area in which they operate. � Access to local industry resources and market data.

� All requests for accreditation require both RHOC and ZBM/Senior Relationship Manager support. � Approval rests with General Manager Risk (or person appointed by the General Manager Risk). � Relationship Managers will be authorised to complete REMAs on a provisional basis prior to becoming fully

accredited. � The accreditation for all Relationship Manager’s will be reviewed annually by the RBL Risk Management

Team. � The Accreditation requirements will be continually reviewed by RBL and, where required, Relationship

Managers will be asked to, amongst other things, attend courses, seminars and other training sessions to maintain their accreditation. Failure to comply with any such requests made by RBL can result in the accreditation being removed either temporarily or permanently.

Internal Control Program The ICP will review REMAs completed by accredited Relationship Managers to ensure Policy requirements are adhered to.

BAB.5025.0001.0126

BAB.5025.0001.0127

>~RURAL BANK Board Credit Committee

FULL CERTIFIED VALUATION - PROCESS

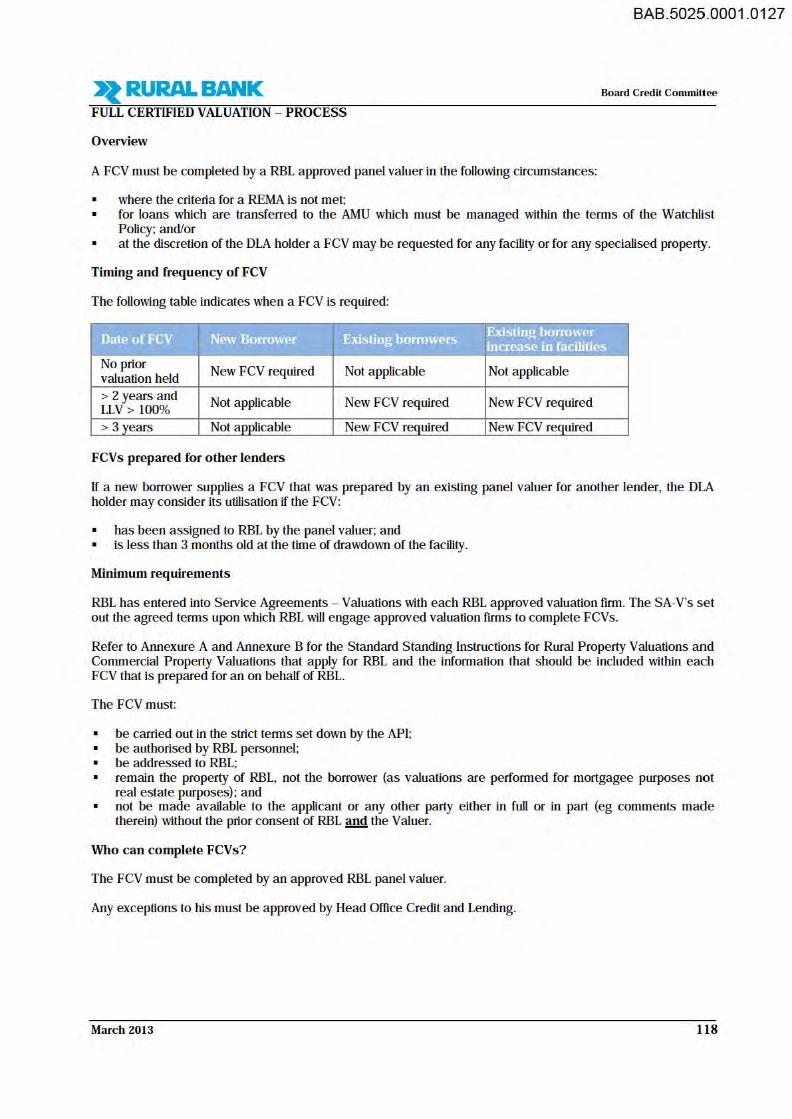

Overview

A FCV must be completed by a RBL approved panel valuer in the following circumstances:

• where the criteria for a REMA is not met; • for loans which are transferred to the AMU which must be managed within the tenns of the Watch!Est

Policy; and/or • at the dlscretion of the DLA holder a FCV may be requested for any facility or for any specialised property.

Timing and frequency of FCV

The following table indicates when a FCV is required:

Date ofFCV New Borrower Existing borrowers Existing borrower increase in facilities

No prior New FCV required Not applicable Not applicable valuation held

> 2 years and Not applicable New FCV required New FCV required LLV > 100% > 3 years Not aoolicable New FCV required New FCV required

FCVs prepared for other lenders

If a new borrower supplies a FCV that was prepared by an existing panel valuer for another lender, the DLA holder may consider its utilisation if the FCV:

• has been assigned to RBL by the panel valuer; and • is less than 3 months old at the time of drawdown of the facility.

Minimum requirements

RBL has entered into Service Agreements - Valuations with each RBL approved valuation finn. The SA-V's S€t out the agreed tenns upon which RBL will engage approved valuation finns to complete FCVs.

Refer to Annexure A and Annexure B for the Standard Standing Instructions for Rural Property Valuations and Commercial Property Valuations that apply for RBL and the infonnation that should be included within each FCV that is prepared for an on behalf of RBL.

The FCV must:

• be carried out in the strict terms set down by the API; • be authorised by RBL personnel; • be addressed to RBL; • remain the property of RBL, not the borrower (as valuations are performed for mortgagee purposes not

real estate purposes); and • not be made available to the applicant or any other party either in full or in part (eg comments made

therein) without the prior consent of RBL and the Valuer.

Who can complete FCVs?

The FCV must be completed by an approved RBL panel valuer.

Any exceptions to his must be approved by Head Office Credlt and Lendlng.

March 2013 118

BAB.5025.0001.0128

>~RURAL BANK Board Credit Commi ttee

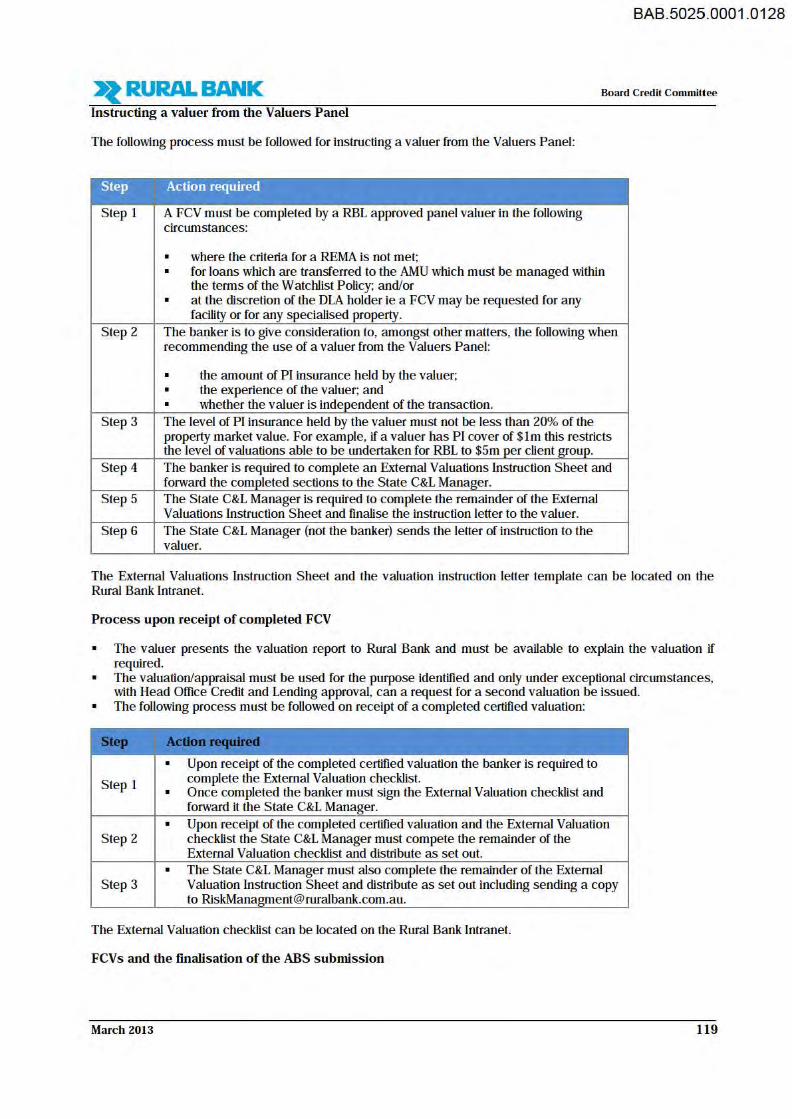

Instructing a valuer from the Valuers Panel

The following process must be followed for instructing a valuer from the Valuers Panel:

Step Action required

Step 1 A FCV must be completed by a RBL approved panel valuer in the following circumstances:

• where the crlterta for a REMA Is not met; • for loans which are transferred to the AMU which must be managed within

the terms of the W atchlist Polley; and/or • at the dlscretion of the DLA holder le a FCV may be requested for any

facility or for any specialised property. Step 2 The banker is to give consideration to, amongst other matters, the following when

recommendlng the use of a valuer from the Valuers Panel:

• the amount of PI Insurance held by the valuer; • the experience of the valuer; and • whether the valuer is independent of the transaction .

Step 3 The level of PI insurance held by the valuer must not be less than 20% of the property market value. For example, if a valuer has PI cover of $l m this restrtcts the level of valuations able to be undertaken for RBL to $5m per client group.

Step 4 The banker is required to complete an External Valuations Instruction Sheet and forward the completed sections to the State C&L Manager.

Step 5 The State C&L Manager is required to complete the remainder of the External Valuations Instruction Sheet and finalise the Instruction letter to the valuer.

Step 6 The State C&L Manager (not the banker) sends the letter of instruction to the valuer.

The External Valuations Instruction Sheet and the valuation instruction letter template can be located on the Rural Bank Intranet.

Process upon receipt of completed FCV

• The valuer presents the valuation report to Rural Bank and must be available to explain the valuation if required.

• The valuation/appraisal must be used for the purpose identified and only under exceptional circumstances, with Head Office Credit and Lending approval, can a request for a second valuation be Issued.

• The following process must be followed on receipt of a completed certified valuation:

Step .Adonmqalred

• Upon receipt of the completed certified valuation the banker is required to

Step 1 complete the External Valuation checklist. • Once completed the banker must sign the External Valuation checklist and

forward It the State C&L Manager.

• Upon receipt of the completed certified valuation and the External Valuation Step 2 checklist the State C&L Manager must compete the remainder of the

External Valuation checklist and distrtbute as set out.

• The State C&L Manager must also complete the remainder of the External Step 3 Valuation Instruction Sheet and dlstrlbute as set out includlng sending a copy

The External Valuation checklist can be located on the Rural Bank Intranet.

FCVs and the finalisation of the ABS submission

March 2013 119

BAB.5025.0001 .0129

>~RURAL BANK Board Credit Committ ee

An ABS application may be finalised (subject to approval conditions being satisfied) subject to:

• the External Valuation Instruction Sheet being fully completed; • the External Valuation checklist being fully completed; • all infonnation being loaded into all relevant sections of ABS; • a copy of the FCV and checklist is being embedded, unless system capacity prohibits this; and • where the system capacity prohibits a copy of the FCV being embedded, the original copy of the FCV must

be kept by Credit and Lending for inclusion in the Credit File.

Who can recommend a valuer to add to the Valuers Panel?

The need to appoint an external valuer (the "prospect valuer") to the Valuers Panel in a particular region may be nominated by:

• the Relationship Manager or ZBM; • a member of staff from the C&L team; and/or • a member of staff from the AMU team.

(the "nominating party")

The RHOC in each State will investigate the prospect valuer in the region, paying special attention to the:

• prospect valuer's capacity to handle the expected volume of transactions from RBL; • geographical spread of the prospect valuer; • quality, cost and standard of service the prospect valuer can provide; • experience of the prospect valuer to meet RBL's requirements particularly with specialised property in the

Agribusiness sector; and • ability of the prospect valuer to meet deadlines.

Process for adding valuers to the Valuers Panel

The following process must be followed for recommending and then adding valuers to the Valuers Panel:

Step .Adonmqalred

The nominating party should discuss the need to add a particular valuer to the Step 1 Valuers Panel with the RHOC prior to undertaking any further work or

discussions with the prospect valuer. Through discussions with the prospect valuer the nominating party should

Step 2 identify the services the prospect valuer is proposing to provide to RBL eg specialised agricultural properties, business banking proposals, commercial properties, residential properties, etc. Assuming that the RHOC supports progressing the nomination further, the prospect valuer is to provide the following: • a copy of their up to date Professional Indemnity ("PI") insurance; • a curriculum vitae for each valuer who will be providing valuation services to

Step 3 RBL;

• details of any financial institutions, government bodies or other relevant parties they currently act for and, if available, summary details of the work undertaken for each party and references; and

• any other infonnation that is relevant to the request by the prospect valuer to be added to the Valuers Panel.

The RHOC will review the infonnation provided by the prospect valuer and any supporting rationale provided by the nominating party. If the prospect valuer is

Step 4 deemed to meet RBL's requirements and the nomination is supported by the RHOC, the RHOC will recommend their appointment to the General Manager Credit. The General Manager Credit will assess the nomination. The General Manager Credit will review and consider the following as part of the overall assessment:

Step 5 • professional qualifications held by the valuer; • relevant experience of the valuer; • appropriate insurances held by the valuer; and • the number of existing valuers on the Valuers Panel in the area/region (le to

March 2013 120

BAB.5025.0001.0130

>~RURAL BANK Board Credit Committ ee

Step .Adon mqalred

avoid any concentration risks) .

If satisfied that the prospect valuer meets RBL's requirements and that there is a need for the prospect valuer to be added to the Valuers Panel (for whatever

Step 6 reason) the General Manager Credit will add the valuer to the Valuers Panel. As part of the assessment process the General Manager Credit will consult with the Head of AMU who will only provide comments on an exception basis only.

Step 7 The General Manager Credit will advise the Risk Department of the valuers name so that the Valuers Panel can be updated on the Intranet.

Process for removing valuers from the Valuers Panel

The following process must be followed for recommending removal of a valuer from the Valuers Panel:

Step .Adonmqalred

Step 1 At any point in time a nominating party may request the removal of a valuer from the Valuers Panel to the General Manager Credit.

Step 2 The request must detail the reason and rationale with supporting evidence as to why a particular valuer should be removed from the Valuers Panel.

The RHOC will review the information provided by the nominating party seeking

Step 3 removal of a valuer from the Valuers Panel. If the reason and rationale provided supports the need to remove the valuer from the Valuers Panel the RHOC will recommend the removal of the valuer to the General Manager Credit. The General Manager Credit will assess the request to remove a valuer from the Valuers Panel.

Step 4 As part of the assessment process the General Manager Credit will consult with the Head of AMU on the prospect valuer on an exception basis only. If satisfied that the valuer should be removed, the General Manager Credit will advise all RHOCs and the General Manager Risk via email.

Step 5 The General Manager Credit will advise the Risk Department of the valuers name so that the Valuers Panel can be updated on the Intranet.

Step 6 The RHOCs will advise their respective teams within 24 hours of the name of the valuer that has been removed from the Valuers Panel.

Immediately upon removing the valuer from the Valuers Panel where removal is

Step 7 for performances reasons, the General Manager Credit will commission a review of 20% of the certified valuations completed for RBL by the removed valuer over the course of the last 12 months. The reviews will be completed by the Risk Department, Head Office C&L , AMU

Step 8 and/or RBL's internal auditor. The reviews will be completed within 60 days of the valuer being removed from the Valuers Panel. The reviewers will review the valuations to ensure compliance with RBLs requirements. The reviewers will also specifically address the reasons why the

Step 9 valuer was removed from the Valuers Panel and how these reason may impact the valuations being reviewed. Each reviewer is to recommend whether or not a fresh valuation is required and each recommendation is to be supported with reason and rationale. The General Manager Credit will review the reviews completed in Step 9 to

Step 10 assess whether or not fresh valuations are required paying particular attention to the time before the next valuation is required to be updated and the overall risk profile of the client.

• The BCC, Managing Director, General Manager Risk, General Manager Credit or Head d AMU have absolute discretion to remove a valuer from the panel and are not required to fdlow steps 1 to 5 above. Ongoing review and monitoring of the Valuers Panel

March 2013 121

Board Credit Committee

March 2013 122

� The General Manager Risk (or person appointed by the General Manager Risk) will review the Valuers

Panel at least annually, to assess whether any valuers should be added to a particular region and/or if a valuer should be removed from the Valuers Panel.

� As part of this review, up to date certificates of PI insurance will be requested from each valuer on the Valuers Panel.

� The level of business each valuer undertakes for RBL will be monitored and reported as part of the annual review. This will assist in determining if there are any undue concentration risks that are evident (eg by the repeated use of a minimal number of valuers).

Notification to BCC for changes to the Valuers Panel At least annually, the General Manager Risk (or person appointed by the General Manager Risk) will provide the BCC with an update of movements onto and off of the Valuers Panel. LIVESTOCK APPRAISALS – PROCESS Overview In all cases where a livestock mortgage is held as security a Livestock Appraisal form, which fully details all of the livestock taken as security, must be completed. Timing and frequency of Livestock Appraisal � An up to date Livestock Appraisal is mandatory when livestock security is taken. � A Livestock Appraisal must be updated when additional funds are borrowed and/or when a review is

undertaken. Livestock Appraisal form The Livestock Appraisal form offers three options in validating livestock values for security purposes: 1. Physical inspection of the livestock – mandatory for new business. 2. Physical inspection of a portion of the livestock and balance appraised from a general description supplied

by the owner. 3. From a general description supplied by the owner with no physical inspection having been undertaken –

only available to Credit Risk Rating 1 to 4. Either option 1 or 2 must be completed at least every two years. The approving DLA holder can insist on applying option 1 or option 2 in lieu of option 3 and option 1 in lieu of option 2 based on their assessment of the credit risk. Process for new clients New to bank clients who seek facilities secured solely by livestock are to display the following attributes: � Credit Risk Rating 1 – 4; and � The Livestock to be held as security should be de-pastured on property owned by the borrower and/or their

guarantor. Who can complete Livestock Appraisals? � Accredited Relationship Managers can complete Livestock Appraisals. � The approving DLA holder can insist on applying a higher authority level as and when deemed necessary

based on the assessment of credit risk. Authority levels to compete Livestock Appraisals where facilities ≤ $500,000 The following authority levels are the minimum requirement to be applied for the completion of Livestock Appraisals where the facilities are less than or equal to $500,000:

BAB.5025.0001.0131

BAB.5025.0001.0132

>~RURAL BANK Board Credit Committee

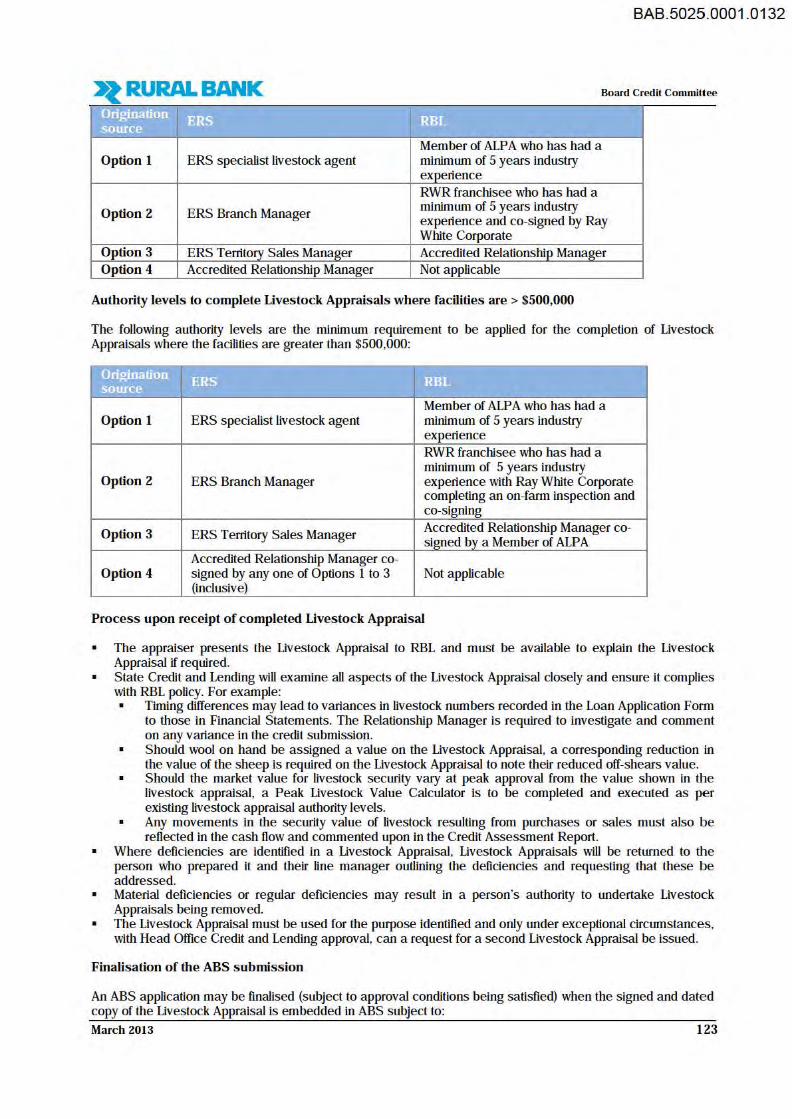

WiIB '~ .... I I o

I ....... Member of ALPA who has had a

Option 1 ERS specialist livestock agent minimum of 5 years industry expertence RWR franchisee who has had a

Option 2 ERS Branch Manager minimum of 5 years industry expertence and co-signed by Ray White Corporate

Option 3 ERS Terrttory Sales Manager Accredited Relationship Manager Option 4 Accredited Relationship Manager Not applicable

Authority levels to complete Livestock Appraisals where facilities are > $500,000

The following authority levels are the minimum requirement to be applied for the completion of Livestock Appraisals where the facilities are greater than $500,000:

Origination ERS RBL source

Member of ALPA who has had a Option 1 ERS specialist livestock agent minimum of 5 years industry

experience RWR franchisee who has had a minimum of 5 years industry

Option 2 ERS Branch Manager experience with Ray White Corporate completing an on-farm inspection and co-signing

Option 3 ERS Terrttory Sales Manager Accredited Relationship Manager co-signed by a Member of ALPA

Accredited Relationship Manager co-Option 4 signed by any one of Options 1 to 3 Not applicable

(inclusive)

Process upon receipt of completed Livestock Appraisal

• The appraiser presents the Livestock Appraisal to RBL and must be available to explain the Livestock Appraisal if required.

• State Credit and Lending will examine all aspects of the Livestock Appraisal closely and ensure it complies with RBL policy. For example: • Timing differences may lead to variances in livestock numbers recorded in the Loan Application Form

to those in Financial Statements. The Relationship Manager is required to investigate and comment on any variance in the credit submission. Should wool on hand be assigned a value on the Livestock Appraisal, a corresponding reduction in the value of the sheep is required on the Livestock Appraisal to note their reduced off-shears value. Should the market value for livestock securtty vary at peak approval from the value shown in the livestock appraisal, a Peak Livestock Value Calculator is to be completed and executed as per existing livestock appraisal authority levels. Any movements in the securtty value of livestock resulting from purchases or sales must also be reflected in the cash flow and commented upon in the Credit Assessment Report.

• Where deficiencies are identified in a Livestock Appraisal , Livestock Appraisals will be returned to the person who prepared it and their line manager outlining the deficiencies and requesting that these be addressed.

• Material deficiencies or regular deficiencies may result in a person's authority to undertake Liv estock Appraisals being removed.

• The Livestock Appraisal must be used for the purpose identified and only under exceptional circumstances, with Head Office Credit and Lending approval, can a request for a second Livestock Appraisal be issued.

Finalisation of the ABS submission

An ABS application may be finalised (subject to approval conditions being satisfied) when the signed and dated copy of the Livestock Appraisal is embedded in ABS subject to:

March 2013 123

Board Credit Committee

March 2013 124

� The livestock appraisal being fully completed (and Peak Livestock Value Calculator if required); � Information must be loaded into all relevant sections of ABS; � The fully executed copy of the Livestock Appraisal is to be embedded by the Relationship Manager with

title “LIVESTOCK APPRAISAL [INSERT DATE] xx.xx.xx for [INSERT PROPERTY NAME”; and � Livestock Appraisals being for RBL purposes only and no part of the Livestock Appraisal, or comments

made therein, can be made available to the applicant or any other party. Accreditation to complete Livestock Appraisals For a Relationship Manager to become accredited to complete Livestock Appraisals, the procedure is as follows: � Relationship Manager forwards to ZBM/Senior Manager Agribusiness their resume and details on:

� Relationship Manager's previous appraisal/valuation experience. � Understanding of appraisal/valuation processes and methodologies. � Knowledge of livestock industries and geographic area in which they operate. � Access to local industry resources and market data.

� All requests for accreditation require both RHOC and ZBM/Rural Bank Senior Relationship Manager support.

� Approval rest with General Manager Risk (or person appointed by the General Manager Risk). � Relationship Managers will be authorised to complete Livestock Appraisals on a provisional basis prior to

becoming fully accredited. � The accreditation for all Relationship Manager’s will be reviewed annually by the RBL Risk Management

Team. Internal Control Program � The ICP will review Livestock Appraisals completed by accredited Relationship Managers to ensure Policy

requirements are adhered to.

BAB.5025.0001.0133

Board Credit Committee

March 2013 125

ANNEXURE A: Standard Standing Instructions for Rural

Property Valuations for RBL

1. General

These instructions apply to the preparation of Valuation Reports for rural properties undertaken by the Service Provider. The requirements set out in this Schedule must be applied, where they are applicable, to the rural property for which the Valuation Report is being undertaken by the Service Provider.

Each Valuation Report must:

(a) include a summary page near the front of the Valuation Report, which gives the valuation figure and, subject to clause 2.3 below, notes any conditions or provisos which are detailed in the body of the Valuation Report;

(b) subject to clause 2.3 below, include all details, assumptions, conditions and/or provisos upon which the valuation is predicated;

(c) include details all other matters that may affect the value, leasing or sale of the property or affect its value to RBL as security; and

(d) be net of GST with all GST assumptions are to be clearly noted; and

(e) include the Letter of Instruction in the appendices.

2. Instructions

2.1 Use These Instructions for Rural Property are to be used for the purpose of undertaking a Valuation Service and preparing a Valuation Report for rural property only and must:-

(a) note that the Valuation is prepared under instructions from RBL; and

(b) be addressed to RBL.

2.2 Assessment

The valuation is to be assessed on the following basis:

(a) an arms length transaction;

(b) between a willing buyer and willing seller;

(c) after proper marketing; and

(d) wherein the parties each act knowledgeably, prudently and without compulsion.

2.3 Physical Inspection The Bank requires the Service Provider to undertake a sufficiently detailed physical inspection of the property so as to be able to accurately provide the information set out in this Schedule.

2.4 Disclaimers, exclusion or limitation of liability clauses Otherwise than set out in this agreement, RBL will not accept any Valuation Report that contains any term or condition having (or purporting to have) the effect of limiting, excluding or otherwise disclaiming the liability (or any other term having, or purporting to have similar legal effect) of the Service Provider in relation to the Valuation Service undertaken or Valuation Report provided.

3. Contents of Valuation Report

3.1 Purpose of Valuation Each Valuation Report must:

BAB.5025.0001.0134

Board Credit Committee

March 2013 126

(a) state that it is suitable for mortgage security purposes;

(b) indicate whether the property is a suitable security against which the bank should advance funds;

(c) include a definition of market value;

(d) be completed on “as is” basis subject to any development approvals, consents, caveats, etc;

(e) be completed on vacant possession basis;

(f) show the split between the “walk-in-walk-out” values (if appropriate) for “Land & Buildings” and “Business” components;

(g) where it is determined that the “highest and best” use of the property is for redevelopment, an assessment assuming continued use;

(h) explain the reason for any variation (higher or lower) between the recorded purchase price and the current valuation or assessment of value;

(i) include the name of the instructing Bank officer;

(j) include the date of inspection; and

(k) describe the type of agricultural or livestock enterprise.

3.2 Legal Description For each Valuation Report:

(a) a current title search of the property must be undertaken and included;

(b) Deposited Plans, strata plans etc should also be included where appropriate;

(c) Filed/Deposited Plan References; and

(d) the legal description of the subject property must include the following:

(i) Certificate of Title Reference and date searched;

(ii) Allotment, Section and Part Section numbers;

(iii) Hundred Name, Filed/Deposited Plan References;

(iv) Registered Proprietor;

(v) Type of ownership and, in particular, the nature of the estate held by the Registered Proprietor in respect of the subject property; and

(vi) Fully identify and describe all title encumbrances such as easements, covenants, rights of carriageway, liens, caveats, leases, mortgages, any statutory charges and the like together with commentary concerning any affect on the value of the property;

3.3 Land Description Each Valuation Report must include:

(a) the full address of the property, as well as comments on the size, dimensions, shape, topography and soil types of the land concerned;

(b) the physical characteristics of the land;

(c) statutory assessments; including the valuation assessment number, date applicable, site and capital values;

(d) details of services which are connected or available to the site;

(e) a description of the major soil types and areas found on the property and the general topography;

(f) a review and commentary on the actual area of pasture (annual or perennial) and description of quality (bush or swamp etc);

(g) comments on the water supplies and indicate whether or not they are adequate for requirements. This is to also include commentary on adequacy of drainage, vulnerability to flood, erosion, etc and highlight positive and negative features including details of any problem e.g. presence of salt in irrigation areas. a general description of standard and condition of fencing and the number of paddocks;

(h) comments where the property has an entitlement to use of water for irrigation purposes including the following summary details:

BAB.5025.0001.0135

Board Credit Committee

March 2013 127

(i) entitlement holder name;

(ii) type of Entitlement;

(iii) supply authority;

(iv) licensee;

(v) agreement number;

(vi) term; and

(vii) volume.

(i) a general description of the standard and condition of fencing and the number of paddocks;

(j) a listing of current stock, production achieved, carrying capacity in an average season including details in respect of any leased land or agistment used; and

(k) a description of the building(s) and improvements and main structural features.

3.4 Location Factors Each Valuation Report must include, describe and/or note:

(a) a location map identifying the subject property;

(b) photographs of the subject property;

(c) the location including the direction and distance from the Central Business District/Town Centre, etc;

(d) a discussion of the access and egress characteristics of the site. (For example, is the site subject to existing or potential road widening proposals, controlled road access? Can vehicles access the site from both directions? Are there any other road constraints, which may inhibit vehicular access?);

(e) particular features of this locality, including demographic and socio-economic profiles, recent developments, major attractions and/or detractions, surrounding land uses, general building ages, architectural styles, condition etc. Commentary should be provided on any general trends within the surrounding area i.e. decaying profile, population growth, traffic flows, transport adequacy, etc;

(f) proximity to local facilities, services, transport, schools, shops, recreational facilities, etc including commentary on the services which are connected or available to the site;

(g) current use of the land and its appropriateness in this specific location; and

(h) commentary on the highest and best use for the land.

3.5 Environmental Each Valuation Report must:

(a) fully address any site contamination and environmental issues and identify previous uses of the land;

(b) include commentary on any obvious site contamination and is to identify any current or prior activities, which may lead to soil contamination on this or adjoining land;

(c) include commentary as to whether an environmental assessment and/or audit report should be obtained, and whether any contamination may impact on market value; and

(d) clearly identify and discuss all assumptions.

3.6 Town Planning Each Valuation Report must:

(a) identify the current zoning of the land and summarise the principles of development within this zone;

(b) include comments on existing and potential uses for the property and its surroundings; advise if the current or proposed use of the land has appropriate approvals, and whether it is a permitted, consent or prohibited use under current and/or proposed zones;

(c) have zoning and land use confirmed at council to identify if there are any Planning Amendment Reports, current or proposed, which may impact on the subject property;

BAB.5025.0001.0136

Board Credit Committee

March 2013 128

(d) include an assessment as to whether current uses comply with consent conditions. A copy of certificates should be supplied; and

(e) in the event of a proposed development, include advice whether the proposed works have appropriate approvals and whether the conditions attaching thereto are consistent with the type of development proposed and not of an onerous nature. A copy of the Approvals should be supplied.

3.7 Property Improvements Each Valuation Report must include:

(a) a description of the physical improvements such as the size and shape of the buildings, the architectural style, description of building systems, materials used and quality of finish, the floor plan, the gross area and net lettable floor dimensions, age and condition of the improvements (deterioration, etc) and the suitability of the present/proposed usage. Where the property specialised in nature, note on the flexibility of the buildings and site for alternate uses;

(b) comment on the nature of any impact such listing may have on the subject where the property Heritage Listed;

(c) an opinion of the cost of any essential repairs;

(d) an opinion as to whether the existing improvements provide the development with functional utility or otherwise;

(e) comments on any existing or likely orders being imposed;

(f) comments on the services connected or available to the property and the adequacy of supply;

(g) advice on possible alternative uses and the cost estimates of conversion to add value to the security;

(h) comments on any adverse features of the property; and

(i) advise whether the building improvements are erected within the title boundaries of the site. Identify if there are any known or potential encroachments on or by the subject land.

3.8 Native Title For each Valuation Report:

(a) a search of the relevant National and State Registers is required to determine if the property, or any portion of it, is subject to any notified Native Title claim. The Valuation Report is to include any pertinent information in the Native Title section of the report; and

(b) the Service Provider is to specifically enquire of the Borrower whether they have been notified of any such claims.

3.9 Asbestos Register For each Valuation Report:

(a) the issue of asbestos materials being present within the building must be fully addressed; and

(b) a definitive statement should be made regarding whether or not an asbestos register has been prepared. If so, the Valuation Report should be succinctly summarised and the implications of the presence of this material should be detailed.

3.10 Marketability Each Valuation Report must include:

(a) an overview of market conditions in relation to the property, including the effect of seasonal conditions such as rainfall, livestock markets, grain markets, etc;

(b) comments on the existing investment and leasing market and the possible future demand for the subject property. For example, how long would it take to let up and/or sell the property? What category of tenant and/or buyer would be interested?

(c) advice on the level of current and future competition in the market for the letting and sale of the property;

(d) details of the purchase price and date of any transaction(s) on the property; and

BAB.5025.0001.0137

Board Credit Committee

March 2013 129

(e) details of all relevant market evidence used in the valuation/appraisal with reference to sales, rentals, dates, land use, property description, etc.