Embed Size (px)

Citation preview

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17

PART VM-22: Maximum Statutory Valuation Interest Rates For Income Annuities

Guidance Note: Over time, the NAIC intends for VM-22 to contain the valuation requirements for all annuity products not covered by VM-21. For now, the purpose of VM-22 is limited to prescribing the valuation interest rates, but not the valuation methodology, to be used for some, but not all, of the products that are within the intended scope of VM-22. All reserve requirements for non-variable annuities that are not within the defined scope of VM-22 (I. A and I. B below) are contained in Appendices VM-A and VM-C. These reserve requirements are not intended to change the reserve requirements for annuities in the accumulation phase. The valuation interest rates for the products in the defined scope of VM-22 (I.A and I. B below) supersede those described in Appendices VM-A and VM-C, but they do not otherwise change how those Appendices are to be interpreted. VM-C IX.B provided guidance on valuation interest rates and is therefore superseded by these requirements for products in scope. Any interest rate references in VM-C IX-C are also superseded by these requirements.

Table of ContentsSection 1. Background

Section 2. Purpose and Scope

Section 2. Definitions

Section 3. Determination Selection of the Statutory Maximum Valuation Interest Rate

Appendix 1: Re-determination of Weights

Appendix 2: Re-determination of Default Costs

Appendix 3: Re-determination of Spreads

Appendix 4: Re-determination of Reference Rates

Appendix 5: Re-determination of Daily and Average Daily Corporate Rates

Appendix 6: Calculation of Statutory Maximum Valuation Interest Rates

Section 1: BackgroundGuidance Note:

Over time, the NAIC intends for VM-22 to contain the valuation requirements for all annuity productcontracts not covered by VM-21. For now, the purpose of VM-22 is limited to prescribing the valuation interest rates, but not the valuation methodology, to be used for some, but not all, of the productcontracts that are within the intended scope of VM-22. All reserve requirements for non-variable annuities that are not within the defined scope of VM-22 (Section I2. A and I. B below) are contained in Appendices VM-A and VM-C. These reserve requirements of this Part are not intended to changeaffect the reserve requirements for deferred annuities in the accumulation phase, except as provided in Section 2.C. The valuation interest rates for the products in the defined scope of VM-22 (I.A and I. B below) supersede those described in Appendices VM-A and VM-C, but they do not otherwise change how those Appendices are to be interpreted. VM-C IX.B provided guidance on valuation interest rates and is therefore superseded by these requirements for products in scope. Any interest rate references in VM-C IX-C are also superseded by these requirements.

© 2017 National Association of Insurance Commissioners 1

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17

The VM-22 statutory maximum valuation interest rates are published by the NAIC. The process of calculating the rates involves a set of spreads, a set of weights, a set of default costs, a set of corporate bond rates and a set of average US Treasury rates. The process of selecting the appropriate rate from the published rates is described in Section 3. The processes for re-determining the weights, default costs, spreads, reference rates and daily corporate rates are described and sample calculations illustrated, in Appendices 1, 2, 3, 4 and 5, respectively. The process of calculating the statutory maximum valuation interest rates is described in Appendix 6.

Information that is downloaded, published or illustrated must of necessity be rounded. Users who wish to perform the calculations illustrated herein should note that, when calculating a daily or quarterly valuation rate, no rounding should occur before the final step.

Section 12. Purpose and Scope

[A.] These requirements form part of the Commissioner’s Annuity Reserve Valuation Method (CARVM), (and, for certain contracts, the Commissioner’s Reserve Valuation Method (CRVM) for certain contracts1), for single premium immediate annuity contracts and other similar contracts, certificates and contract features, or supplementary contracts, and define, for such policies, contracts, certificates and contract features, or supplementary contracts issued after December 31, 2017, the statutory maximum valuation interest rate determined as of the Premium Determination Date that complies with the Standard Valuation Law (SVL)Model #820.

[B.] The following categories of annuities contracts, certificates andor contract features, whether group or individual, including both life contingent and term term-certain certain-only contracts, directly written or assumed through reinsurance, are covered by this Section Part of the Valuation Manual:1. Immediate annuity contracts issued after December 31, 2017;2. Deferred income annuity contracts issued after December 31, 2017;3. Structured settlements in payout or deferred status, issued after December 31, 2017; [4.] Fixed pPayout annuities resulting from the exercise of settlement options or annuitizations after

December 31, 2017, from other contracts regardless of the issue date of the host contract, and regardless of whether a new contract is issued;

[5.] Supplementary contracts issued after December 31, 2017, regardless of the issue date of the host contract; and

[6.] Contracts containing other similar fFixed income payment streams, including those attributable to contingent deferred annuities issued after December 31, 2017 and guaranteed lifetime income benefits , once the underlying contract funds are exhausted. ;

4. Fixed income payment streams attributable to guaranteed lifetime income benefits associated with deferred annuity contracts issued after December 31, 2017, once the contract funds are exhausted; and

11 SVL Model #820 Section 5.C.(2): Group annuity and pure endowment contracts purchased under a retirement plan or plan of deferred compensation, established or maintained by an employer (including a partnership or sole proprietorship) or by an employee organization, or by both, other than a plan providing individual retirement accounts or individual retirement annuities under Section 408 of the Internal Revenue Code, as now or hereafter amended.© 2017 National Association of Insurance Commissioners 2

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/175. G roup annuity and pure endowment contracts specified in Model #820, Section 5.C.2, purchased for

the purpose of providing certificate holders benefits upon their retirement, issued after December 31, 2017.

Guidance Note: Note that for Sections 2.B.4 and 2.B.5 above, there is no restriction on the type of contract that may give rise to the benefit.

Guidance Note: In general, in respect of the categories in this Section 2.B, the intent is to select a valuation interest rate that is aligned with the company’s investment strategy pertaining to the timing of the investment of assets required to provide the benefits. However, this Part does not impose any requirements on the company’s investment policy.

Guidance Note: Pertaining to Section 2.B.8 above, certificates purchased after December 31, 2017 in contracts issued on or before December 31, 2017, are excluded from these provisions.

C. Exemptions:1. With the permission of the domiciliary commissioner, when a deferred annuity contract is being valued in accordance with Actuarial Guideline XXXIII, Actuarial Guideline XVIII or Part VM-21, the company may select the valuation interest rate for the annuitization stream as of the issue date of the contract in accordance with applicable guidance and may use the same valuation interest rate upon actual annuitization (Section 2.B.4 or 2.B.5, whichever is applicable), rather than the statutory maximum valuation interest rate prescribed in this Part. In order to obtain such permission, the company must demonstrate that its investment policy and practices are consistent with this approach.

2. With the permission of the domiciliary commissioner, when a deferred annuity contract is being valued in accordance with Actuarial Guideline XXXIII, Actuarial Guideline XVIII or Part VM-21, the company may select the valuation interest rate for the projected fixed payment stream that arises once the account value is exhausted as of the issue date of the contract in accordance with the applicable guidance and may use the same valuation interest rate for the actual fixed payment stream that arises once the account value is exhausted (Section 2.B.7), rather than the statutory maximum valuation interest rate prescribed in this Part. In order to obtain such permission, the company must demonstrate that its investment policy and practices are consistent with this approach.

D. The valuation interest rates for the contracts, certificates and contract features within the scope of this Part supersede those described in Appendices VM-A and VM-C of the Valuation Manual, but they do not otherwise change how those Appendices are to be interpreted. In particular, Actuarial Guideline IX-B (see VM-C) provides guidance on valuation interest rates and is therefore superseded by these requirements for contracts, certificates and contract features in scope. Likewise, any valuation interest rate references in Actuarial Guideline IX-C (see VM-C) are also superseded by these requirements.

© 2017 National Association of Insurance Commissioners 3

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17

Section 2. Definitions

[A.] Portfolio Credit Quality Distribution – This term means the prescribed asset credit rating distribution as follows:

5% Treasuries 15% Aa bonds (5% Aa1, 5% Aa2, 5% Aa3) 40% A bonds (13.33% A1, 13.33% A2, 13.33% A3) 40% Baa bonds (13.33% Baa1, 13.33% Baa2, 13.33% Baa3)

Guidance Note: The credit quality designations above have the same meaning as in VM-20, subsection 9.F.3.

[B.] Daily Treasury Rate – This term means the Daily Treasury Yield Curve Rate for a given maturity as published by the U.S. Department of the Treasury.

Guidance Note: The source for these rates is: https://www.treasury.gov

[C.] Expected Default Cost – This term means a vector of annual default costs by weighted average life calculated as a weighted average of the VM-20 prescribed annual default costs (Table A) in effect for the quarter prior to the Premium Determination Date for the Portfolio Credit Quality Distribution, as published on the Life Actuarial Task Force (LATF) website of the NAIC.

[D.] Reference Period - This term means the length of time, rounded to the nearest year, from the Premium Determination Date to the date of the last non-life-contingent payment under the individual contract or group certificate, as applicable.

Guidance Note: The definition of Reference Period assumes a series of material, substantially similar payments and materiality is relative to the life-contingent payments. If the payments are not substantially similar, the actuary should apply prudent judgment and select the Valuation Rate Bucket with Macaulay duration that is a best fit to the Macaulay duration of the payments in question.

[E.] Jumbo Contract – This term means a contract with an initial consideration equal to or greater than $250,000,000. Considerations for contracts issued to the same party within 90 days shall be combined for purposes of determining whether a contract meets this threshold.

[F.] Non-jumbo Contract – This term means a contract that does not meet the definition of the Jumbo Contract.

[G.] Expected Spread – This term means a vector of spreads by weighted average life, calculated as a weighted average of the VM-20 prescribed spreads (Table F) for the quarter prior to the Premium Determination Date for the Portfolio Credit Quality Distribution, as published on the Life Actuarial Task Force (LATF) website of the NAIC.

[H.] Quarterly Treasury Rate – This term means the average of the Daily Treasury Rates defined in Subsection 2B above for a given maturity over the calendar quarter prior to the Premium Determination Date.

© 2017 National Association of Insurance Commissioners 4

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17[I.] Premium Determination Date – This term means the date upon which the premium is determined by the

insurance company and is committed to by the client. This term is generally defined as the issue date. For supplementary contracts and annuitizations, this would normally be the date of election of the supplementary contracts and the annuitizations, but a company may use the valuation rate basis in effect when the original contract was issued with domestic commissioner approval.

Guidance Note: The Premium Determination Date is intended to be a date proximate to the date of the investment of the assets that support the contract. As examples,

for a group annuity for which the company locks in investment yields at the time of a quote, but the contract is issued subsequently, that “lock-in-date” should be used by the company on a consistent basis;

for a single-premium immediate annuity contract, this would normally be the issue date; for a supplementary contract, however, this date would normally be the date of annuitization. The

definition permits, subject to the domestic commissioner’s approval, the use of some other date. An example of such a situation includes using the issue date of the original deferred annuity contract for annuitizations. Approval would normally be granted when the domestic commissioner has been provided satisfactory demonstration that the company employs an appropriate asset/liability matching strategy.

[J.] Initial Age – Age as of the last birthday as of the Premium Determination Date. For joint life contracts or certificates, the Initial Age means the Initial Age of the younger annuitant. For contracts with impaired lives being valued using a rated age, Initial Age means the rated age. For contracts with impaired lives being valued using a substandard mortality table, Initial Age is based on an equivalent rated age.

© 2017 National Association of Insurance Commissioners 5

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Section 3. Determination Selection of the Statutory Maximum Valuation Interest Rate

A. Valuation Rate Buckets[1.] For the purpose of the calculation ofselecting the statutory maximum valuation interest rate, each

contract or certificatethe contract, certificate or contract feature being valued must is to be assigned to one of four Valuation Rate Bucketvaluation rate buckets labeled A through D.

[2.] For contracts or certificates withoutIf the contract, certificate or contract feature has no life contingencies, the Valuation Rate Bucketvaluation rate buckets are is assigned based on the length of the Reference reference Period period (RP), as follows:

Table 3-1 : Assignment to Valuation Rate Bucket by Reference Period Only

RP ≤ 5Years 5Y < RP ≤ 10Y

10Y < RP ≤ 15Y

RP > 15Y

A B C D

[3.] For contracts or certificates withIf the contract, certificate or contract feature has life contingencies, the Valuation Rate Bucketvaluation rate buckets are is assigned based on the length of the Reference reference Period period (RP) and the Initial initial Age age of the annuitant, as follows:

Table 3-2: Assignment to Valuation Rate Bucket by Reference Period and Initial Age

Initial Age RP ≤ 5Y 5Y < RP ≤ 10Y 10Y < RP ≤ 15Y

RP > 15Y

90+ A B C D

80-89 B B C D

70-79 C C C D

<70 D D D D

.

[4.] Except as provided in Subsection 3A.5 below, for group annuity contracts, the statutory maximum valuation rate shall be determined separately for each certificate holder, based on their Initial Age and the certificate Reference Period.

[5.] For group annuity contracts purchased under a retirement or deferred compensation plan with multiple annuity form options available to the certificate holder, the statutory maximum valuation rate shall be based on the normal form of payout as defined in the contract or as is evidenced by the underlying pension plan documents or census file. If the normal form of payout cannot be determined, the statutory maximum valuation rate shall be based on the most conservative annuity form available to the certificate holder.

© 2017 National Association of Insurance Commissioners 6

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17

© 2017 National Association of Insurance Commissioners 7

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17B. Premium Determination Dates

1. The following table specifies the decision rules for setting the premium determination date for each of the contracts, certificates and contract features listed in Section 2:

Table 3-3: Premium Determination Date

Item # in Section 2 Item Description Premium determination date

2.B.1 Immediate annuity Date consideration determined and committed to by contract holder

2.B.2 Deferred income annuity Date consideration determined and committed to by contract holder

2.B.3 Structured settlements Date consideration determined and committed to by contract holder

2.B.4 Payout annuities resulting from settlement options or annuitizations from other contracts

Benefit commencement date

2.B.5 Supplementary contracts Date of issue of supplementary contract

2.B.6 Fixed income payment streams from contingent deferred annuities, AV=0

Payment stream commencement date

2.B.7 Fixed income payment streams from guaranteed living benefits, AV=0

Payment stream commencement date

2.B.8 Group annuity, and related certificates Date consideration determined and committed to by contract holder

2. Immaterial Change in Consideration

If the premium determination date is based on the consideration, and if the consideration changes by an immaterial amount subsequent to the original premium determination date, such as due to a data correction, then the original premium determination date shall be retained.

C. Statutory Maximum Valuation Interest Rate

1. For a given contract, certificate or contract feature ,Tthe statutory maximum valuation interest rate is determined selected from the published rates based on itsthe assigned Valuation Rate Bucketvaluation rate bucket defined in (Section 3.A), its premium determination date (Section 3.B) and whether the contract associated with it is a jumbo contract or a non-jumbo contract.Subsection 3A and the Premium Determination Date of the contract or certificate

© 2017 National Association of Insurance Commissioners 8

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/172. Statutory maximum valuation interest rates for jumbo contracts are published daily. For a given premium determination date, the statutory maximum valuation interest rate is the daily maximum statutory maximum valuation interest rate published for that premium determination date.

3. Statutory maximum valuation interest rates for non-jumbo contracts are published quarterly, by the third business day of the quarter. For a given premium determination date, the statutory maximum valuation interest rate is the quarterly statutory maximum valuation interest rate published for the quarter in which the premium determination date falls.

D. Group Annuity Contracts

For a group annuity or pure endowment contract purchased under a retirement or deferred compensation plan (Section 2.B.8), the following apply:

1. The statutory maximum valuation interest rate shall be determined separately for each certificate, considering its premium determination date, the certificate holder’s initial age, the reference period corresponding to its form of payout and whether the contract is a jumbo contract or a non-jumbo contract.

Guidance Note: Under some group annuity contracts, certificates may be purchased on different dates.

2. In the case of a certificate whose form of payout has not been elected by the beneficiary at its premium determination date, the statutory maximum valuation interest rate shall be based on the reference period corresponding to the normal form of payout as defined in the contract or as is evidenced by the underlying pension plan documents or census file. If the normal form of payout cannot be determined, the maximum valuation interest rate shall be based on the reference period corresponding to the most conservative annuity form available to the certificate holder.

Guidance Note: The statutory maximum valuation interest rate will not change when the form of payout is elected.

E. Non-level Payment Streams The definition of reference period assumes a series of material, substantially similar payments and

materiality is relative to the life-contingent payments. If the payments are not substantially similar, the company shall select the valuation rate bucket using a reference period equal to the Macaulay duration of the payment stream being valued.

© 2017 National Association of Insurance Commissioners 9

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Appendix 1: Re-determination of Weights

Section A1-1: Steps in Calculating Weights

The system for calculating the statutory maximum valuation interest rates relies on a set of four tables of weights. A given set of weight tables is applicable to the calculations for every day of the calendar year.

In the fourth quarter of each calendar year, the weights used within each valuation rate bucket for determining the applicable valuation interest rates for the following calendar year will be updated using the following process:

1. Each valuation rate bucket has a set of representative annuity forms. These annuity forms are as follows:a. Bucket A:

i. Single Life Annuity age 91 with 0 and 5-year certain periodsii. 5-year certain only

b. Bucket B:i. Single Life Annuity age 80 and 85 with 0, 5, and 10-year certain periods

ii. 10-year certain onlyc. Bucket C:

i. Single Life Annuity age 70 with 0 and 15-year certain periodsii. Single Life Annuity age 75 with 0, 10 and 15-year certain periods

iii. 15-year certain onlyd. Bucket D:

i. Single Life Annuity age 55, 60, and 65 with 0 and 15-year certain periodsii. 25-year certain only

2. Annual cash flows are projected assuming annuity payments are made at the end of each year. These cash flows are averaged for each valuation rate bucket across the annuity forms for that bucket using the valuation mortality table in effect for the following calendar year for individual annuities for males.

3. The average of the daily rates in the third quarter for the 2-yr, 5-yr, 10-yr and 30-yr US Treasuries are downloaded from https://fred.stlouisfed.org as input to calculate the present values in Step 4.

4. The average cash flows are summed into four time period groups: years 1-3, years 4-7, years 8-15 and years 16-30. (Note: the present value of cash flows beyond year 30 is included in the years 16-30 bucket. This present value is based on the lower of 3% and the 30-year Treasury rate input in Step 3.)

5. The present value of each summed cash flow group in Step 4 is then calculated by using the Step 3 US Treasury rates for the mid-point of that group (and using the linearly interpolated US Treasury rate when necessary).

6. The duration-weighted present value of the cash flows is determined by multiplying the present value of the cash flow groups by the midpoint of the time period for each applicable group.

© 2017 National Association of Insurance Commissioners 10

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/177. Weights for each cash flow time period group within a valuation rate bucket are calculated by dividing the duration-weighted present value of the cash flow by the sum of the duration-weighted present value of cash flow for each valuation rate bucket.

Guidance Note: The weights, which are illustrated in Tables A1-1, A1-2, A1-3 and A1-4, are based on duration and asset-liability-cash-flow-matching analysis for representative annuities within each valuation rate bucket, as described above.

© 2017 National Association of Insurance Commissioners 11

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Section A1-2: Sample Calculation of Table A1-1 Weights for Bucket B

The example below shows the calculation of 2018 Table A1-1 weights for valuation rate bucket B, following the steps in Appendix 1, Section A1-1.

1. Bucket B products defined in Appendix 1.1.b as follows: Bucket B:

i. Single Life Annuity age 80 and 85 with 0, 5, and 10-year certain periodsii. 10-year certain only

Note: The following cash flows are based on a $5,000 payment and 2012 IAR Mortality Table Male for a person age x in year 2018.

2. Annual cash flows are projected assuming annuity payments are made at the end of each year. These cash flows are averaged for each valuation rate bucket across the annuity forms for that bucket using the statutory valuation mortality table in effect for the following calendar year for individual annuities for males.

Note: Color bars show time period groups used in subsequent steps.

Table A1-5: Bucket B Annuity Calculation

© 2017 National Association of Insurance Commissioners 12

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17

Iss Age Att Age SLA SL w 5 yr certain SL w 10 yr certain Iss Age Att Age SLA SL w 5 yr certain SL w 10 yr certain 10 -Year Certain Average80 80 4,848.24 5,000.00 5,000.00 85 85 4,719.94 5,000.00 5,000.00 5,000.00 4938.3180 81 4,683.37 5,000.00 5,000.00 85 86 4,422.93 5,000.00 5,000.00 5,000.00 4872.3380 82 4,505.11 5,000.00 5,000.00 85 87 4,108.84 5,000.00 5,000.00 5,000.00 4801.9980 83 4,315.13 5,000.00 5,000.00 85 88 3,781.62 5,000.00 5,000.00 5,000.00 4728.1180 84 4,111.55 5,000.00 5,000.00 85 89 3,440.90 5,000.00 5,000.00 5,000.00 4650.3580 85 3,893.64 3,893.64 5,000.00 85 90 3,090.57 3,090.57 5,000.00 5,000.00 4138.3580 86 3,660.64 3,660.64 5,000.00 85 91 2,740.82 2,740.82 5,000.00 5,000.00 3971.8580 87 3,412.17 3,412.17 5,000.00 85 92 2,393.16 2,393.16 5,000.00 5,000.00 3801.5280 88 3,152.44 3,152.44 5,000.00 85 93 2,053.67 2,053.67 5,000.00 5,000.00 3630.3280 89 2,879.59 2,879.59 5,000.00 85 94 1,733.27 1,733.27 5,000.00 5,000.00 3460.8280 90 2,596.53 2,596.53 2,596.53 85 95 1,432.11 1,432.11 1,432.11 - 1726.5680 91 2,312.83 2,312.83 2,312.83 85 96 1,168.14 1,168.14 1,168.14 - 1491.8480 92 2,028.16 2,028.16 2,028.16 85 97 930.49 930.49 930.49 - 1267.9980 93 1,747.57 1,747.57 1,747.57 85 98 726.15 726.15 726.15 - 1060.1680 94 1,481.67 1,481.67 1,481.67 85 99 551.46 551.46 551.46 - 871.3480 95 1,229.34 1,229.34 1,229.34 85 100 409.43 409.43 409.43 - 702.3380 96 1,007.24 1,007.24 1,007.24 85 101 295.81 295.81 295.81 - 558.4580 97 805.37 805.37 805.37 85 102 205.66 205.66 205.66 - 433.3080 98 631.15 631.15 631.15 85 103 138.61 138.61 138.61 - 329.8980 99 480.82 480.82 480.82 85 104 89.23 89.23 89.23 - 244.3180 100 358.22 358.22 358.22 85 105 55.32 55.32 55.32 - 177.2380 101 259.80 259.80 259.80 85 106 33.19 33.19 33.19 - 125.5780 102 181.02 181.02 181.02 85 107 19.92 19.92 19.92 - 86.1280 103 122.29 122.29 122.29 85 108 11.95 11.95 11.95 - 57.5380 104 78.73 78.73 78.73 85 109 7.17 7.17 7.17 - 36.8280 105 48.81 48.81 48.81 85 110 4.30 4.30 4.30 - 22.7680 106 29.29 29.29 29.29 85 111 2.58 2.58 2.58 - 13.6680 107 17.57 17.57 17.57 85 112 1.55 1.55 1.55 - 8.2080 108 10.54 10.54 10.54 85 113 0.93 0.93 0.93 - 4.9280 109 6.33 6.33 6.33 85 114 0.56 0.56 0.56 - 2.9580 110 3.80 3.80 3.80 85 115 0.33 0.33 0.33 - 1.7780 111 2.28 2.28 2.28 85 116 0.20 0.20 0.20 - 1.0680 112 1.37 1.37 1.37 85 117 0.12 0.12 0.12 - 0.6480 113 0.82 0.82 0.82 85 118 0.07 0.07 0.07 - 0.3880 114 0.49 0.49 0.49 85 119 0.04 0.04 0.04 - 0.2380 115 0.30 0.30 0.30 85 120 - - - - 0.1380 116 0.18 0.18 0.18 - - - - 0.0880 117 0.11 0.11 0.11 - - - - 0.0580 118 0.06 0.06 0.06 - - - - 0.0380 119 0.04 0.04 0.04 - - - - 0.0280 120 - - - - - - - 0.00

Bucket B Calculation

3. The average of the daily rates in the third quarter for the 2-yr, 5-yr, 10-yr and 30-yr US Treasuries are downloaded from https://fred.stlouisfed.org as input to calculate the present values in Step 4.

Table A1-6: Previous Year 3Q Average Treasury (%)2 Year 5 Year 10 Year 30 Year1.36 1.81 2.24 2.82

4. The average cash flows are summed into four time period groups: years 1-3, years 4-7, years 8-15 and years 16-30. (Note: the present value of cash flows beyond year 30 is included in the years 16-30 bucket. This present value is based on the lower of 3% and the 30-year Treasury rate input in Step 3.)

Table A1-7: Summing Cash Flows

© 2017 National Association of Insurance Commissioners 13

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Duration Sum of Average Cash Flows

1 - 3 Sum of Rows 1–3 from Table 1-5 = 14,612.63

4 - 7 Sum of Rows 4–7 from Table 1-5 = 17,488.65

8 - 15 Sum of Rows 8–15 from Table 1-5 = 17,310.56

16 - 30 Sum of Rows 16–30 from Table 1-5 = 2,804.03

31 Net Present Value of Rows 31+ us ing Interest Rate of 2.82% = 4.09

5. The present value of each summed cash flow group in Step 4 is then calculated by using the Step 3 US Treasury rates for the mid-point of that group (and using the linearly interpolated US Treasury rate when necessary).

Table A1-8: Interpolated Average Treasury RatesTime Period

Group1-3 4 - 7 8 - 15 16 - 30 31 +

Mid-Point 2 5.5 11.5 23 31 +

Linear Interpolated Treasuries (%)1.36 1.85 2.28 2.62 2.82

© 2017 National Association of Insurance Commissioners 14

Attachment FourteenLife Actuarial (A) Task Force

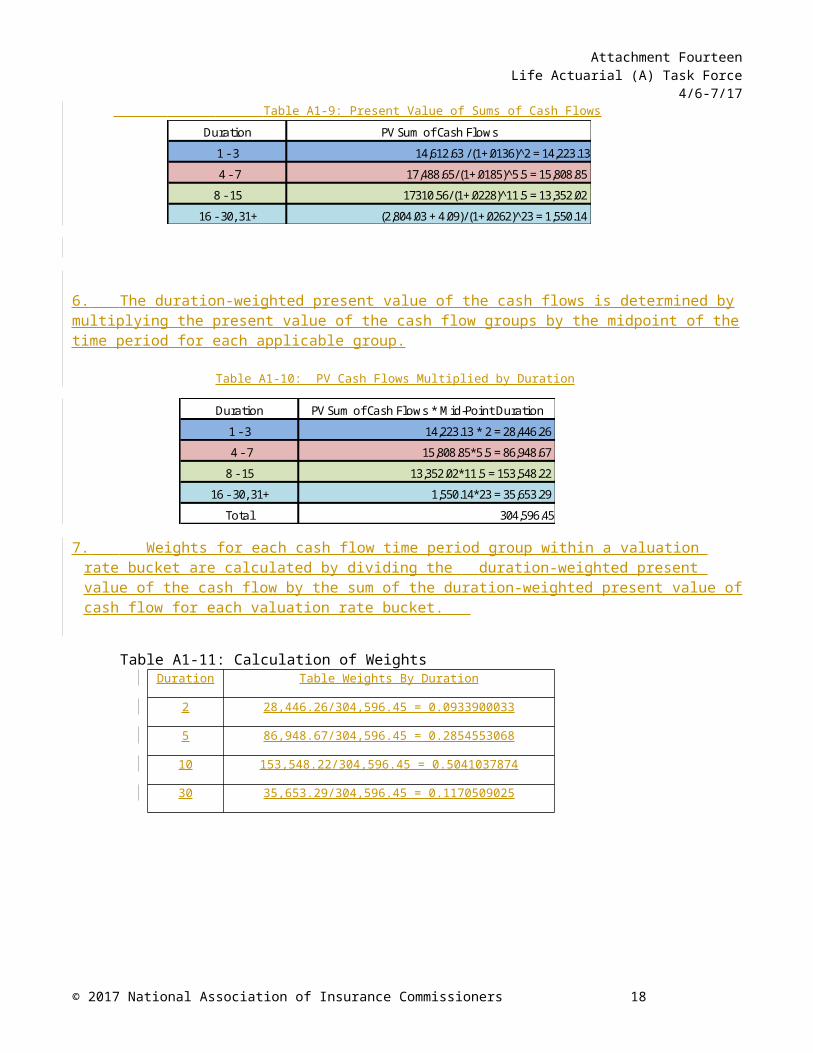

4/6-7/17 Table A1-9: Present Value of Sums of Cash Flows

Duration PV Sum of Cash Flows

1 - 3 14,612.63 /(1+.0136)^2 = 14,223.13

4 - 7 17,488.65/(1+.0185)^5.5 = 15,808.85

8 - 15 17310.56/(1+.0228)^11.5 = 13,352.02

16 - 30, 31+ (2,804.03 + 4.09)/(1+.0262)^23 = 1,550.14

6. The duration-weighted present value of the cash flows is determined by multiplying the present value of the cash flow groups by the midpoint of the time period for each applicable group.

Table A1-10: PV Cash Flows Multiplied by Duration

Duration PV Sum of Cash Flows * Mid-Poi nt Duration

1 - 3 14,223.13 * 2 = 28,446.26

4 - 7 15,808.85*5.5 = 86,948.67

8 - 15 13,352.02*11.5 = 153,548.22

16 - 30, 31+ 1,550.14*23 = 35,653.29

Tota l 304,596.45

7. Weights for each cash flow time period group within a valuation rate bucket are calculated by dividing the duration-weighted present value of the cash flow by the sum of the duration-weighted present value of cash flow for each valuation rate bucket.

Table A1-11: Calculation of Weights

© 2017 National Association of Insurance Commissioners 15

Duration Table Weights By Duration

2 28,446.26/304,596.45 = 0.0933900033

5 86,948.67/304,596.45 = 0.2854553068

10 153,548.22/304,596.45 = 0.5041037874

30 35,653.29/304,596.45 = 0.1170509025

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Section A1-3: Sample Calculation of Weights: Determination of Other Weight Tables

Starting with Table A1-1 as illustrated in Section A1-2:

Weights Table A1-1Bucket 2 Year 5 Year 10 Year 30 Year

A 26.19582562% 50.86877631% 21.89565925% 1.03973882%B 9.33900033% 28.54553068% 50.41037874% 11.70509025%C 4.42359018% 14.74706367% 47.59367021% 33.23567594%D 2.23031779% 7.52527717% 26.26320289% 63.98120215%

1. Table A1-2 is identical to Table A1-1.

Weights Table A1-2Bucket 2 Year 5 Year 10 Year 30 Year

A 26.19582562% 50.86877631% 21.89565925% 1.03973882%B 9.33900033% 28.54553068% 50.41037874% 11.70509025%C 4.42359018% 14.74706367% 47.59367021% 33.23567594%D 2.23031779% 7.52527717% 26.26320289% 63.98120215%

2. Table A1-3 is based on the same set of underlying weights as Table A1-1, but the 10 year and 30 year columns are combined since VM-20 default rates are only published for maturities of up to 10 years.

Weights Table A1-3Bucket 2 Year 5 Year 10 Year

A 26.19582562% 50.86877631% 22.93539807%B 9.33900033% 28.54553068% 62.11546899%C 4.42359018% 14.74706367% 80.82934615%D 2.23031779% 7.52527717% 90.24440504%

3. Table A1-4 is derived from Table A1-1 as follows:

a. Column 1 of Table A1-4 is identical to column 1 of Table A1-1.b. Column 2 of Table A1-4 is 50% of column 2 of Table A1-1.c. Column 3 of Table A1-4 is identical to column 2 of Table A1-4.d. Column 4 of Table A1-4 is 50% of column 3 of Table A1-1.e. Column 5 of Table A1-4 is identical to column 4 of Table A1-4.f. Column 6 of Table A1-4 is identical to column 4 of Table A1-1.

Bucket 1Y - 3Y 3Y - 5Y 5Y - 7Y 7Y - 10Y 10Y - 15Y +15YA 26.19582562% 25.43438815% 25.43438815% 10.94782963% 10.94782963% 1.03973882%B 9.33900033% 14.27276534% 14.27276534% 25.20518937% 25.20518937% 11.70509025%C 4.42359018% 7.37353184% 7.37353184% 23.79683510% 23.79683510% 33.23567594%

D 2.23031779% 3.76263858% 3.76263858% 13.13160144% 13.13160144% 63.98120217%

Weights Table A1-4

4. In every table, the weights in a given row (valuation rate bucket) must add to exactly 100%.

© 2017 National Association of Insurance Commissioners 16

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17

Appendix 2: Re-determination of Default Costs

Section A2-1: Frequency

Default costs used in VM-22 calculations for each valuation rate bucket are calculated and updated annually during the second quarter as described below. This calculation depends on VM-20 Table A data. Since the annual default cost raw data used to construct Table A is released late in the first quarter of the year, Table A updates are expected to be made and published to the NAIC website in the second quarter.

Section A2-2: Calculation of Default Cost Rates

1. From the NAIC website, download the VM-20 prescribed annual default cost table (Table A) in effect for the prior quarter.

2. For WALs 2, 5 and 10 years only, select the VM-20 Table A prescribed annual default costs for PBR Credit Ratings 2 through 10.

3. For WALs 2, 5 and 10 years only, calculate the expected default cost, which is a weighted average of the Table A prescribed annual default costs, using the following prescribed portfolio credit quality distribution as weights:

5% Treasuries 15% Aa bonds (5% PBR2, 5% PBR3, 5% PBR4) 40% A bonds (13.33% PBR5, 13.33% PBR6, 13.33% PBR7) 40% Baa bonds (13.33% PBR8, 13.33% PBR9, 13.33% PBR10)

4. Calculate Expected Default Costs by WAL

Table A2-1: Calculation of Expected Default Costs by WAL

WAL(Weighted

Average Life)

Investment Grade PBR Credit Rating1 2 3 4 5 6 7 8 9 10 Expected

Default CostAaa/AAA Aa1/AA+ Aa2/AA Aa3/AA- A1/A+ A2/A A3/A- Baa1/BBB+ Baa2/

BBB Baa3/BBB-

Portfolio Credit

Quality Dist0.00% 5.00% 5.00% 5.00% 13.33% 13.33

% 13.33% 13.33% 13.33% 13.33%

2 0.02 0.32 0.84 2.01 3.91 7.40 9.96 18.61 32.46 75.42 19.86

5 0.09 0.97 2.13 4.45 8.19 14.69 18.71 28.28 42.35 85.89 26.79

10 0.15 1.49 2.98 5.97 10.48 18.08 23.09 33.63 48.84 88.11 30.15

5. Calculate the default cost for each valuation rate bucket, which is a weighted average of the expected default costs for WALs 2, 5, and 10, using Table A1-3 for the current calendar year as weights.

© 2017 National Association of Insurance Commissioners 17

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17

Table A2-2: Calculation of Expected Default Costs by Valuation Bucket:

Table A1-3 Val Rate Bucket 2 Year 5 Year 10 Year Default Cost A 0.261958 0.508688 0.229354 25.75B 0.093390 0.285455 0.621155 28.23C 0.044236 0.147471 0.808293 29.20D 0.022303 0.075253 0.902444 29.67

Example – Bucket A: 19.86 x 26.1958% + 26.79 x 50.8688% + 30.15 x 22.9354% = 25.75

© 2017 National Association of Insurance Commissioners 18

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Appendix 3: Re-determination of Spreads

Section A3-1: Frequency

VM-22 spreads for each valuation rate bucket are calculated and updated by the 5 th business day following the end of each quarter as described below. This calculation depends on VM-22 Table X spreads, which are published on the NAIC website by the 5th business day following the end of each quarter.

Section A3-2: Calculation of Spreads

1. From the NAIC website, download the VM-22 prescribed spread table (Table X) in effect for the prior quarter.

2. For WALs 2, 5, 10 and 30 years only, select the VM-22 quarterly average Table X prescribed spreads for PBR Credit Ratings 1 through 10.

3. For WALs 2, 5, 10 and 30 years only, calculate the expected spread, which is a weighted average of the Table X spreads, using the following prescribed portfolio credit quality distribution as weights:

5% Treasuries 15% Aa bonds (5% PBR2, 5% PBR3, 5% PBR4) 40% A bonds (13.33% PBR5, 13.33% PBR6, 13.33% PBR7) 40% Baa bonds (13.33% PBR8, 13.33% PBR9, 13.33% PBR10)

4. Calculate Expected Spreads by WAL.Table A3-1: Calculation of Expected Spreads by WAL

WAL(Weighted

Average Life)

Investment Grade PBR Credit Rating1 2 3 4 5 6 7 8 9 10 Expected

SpreadsAaa/AAA Aa1/AA+ Aa2/AA Aa3/AA- A1/A+ A2/A A3/A- Baa1/BBB+ Baa2/BBB Baa3/

BBB-Portfolio Credit

Quality Dist0.00% 5.00% 5.00% 5.00% 13.33% 13.33% 13.33% 13.33% 13.33% 13.33%

2 20.75 28.58 36.40 40.31 44.22 48.13 56.03 63.94 71.85 122.03 19.86

5 33.82 39.26 44.71 51.48 58.25 65.02 78.99 92.97 106.94 139.57 26.79

10 50.90 58.79 66.68 74.67 82.66 90.65106.95 123.26 139.56 155.88

30.15

30 88.60 97.79 106.99 115.09 123.19 131.29157.60 183.92 210.23 191.22

148.99

5. Calculate the Spread for each valuation rate bucket, which is a weighted average of the Expected Spread for WALs 2, 5, 10, and 30 using Table A1-2 for the current calendar year as weights.

Table A3-2: Calculation of Expected Spreads by Valuation Rate BucketVal Rate Bucket Table A1-2 Spread 2 Year 5 Year 10 Year 30 Year A 0.26196 0.50869 0.21896 0.0104 26.98B 0.09339 0.28546 0.5041 0.11705 42.14C 0.04424 0.14747 0.47594 0.33236 68.70

© 2017 National Association of Insurance Commissioners 19

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17D 0.0223 0.07525 0.26263 0.63981 105.70

Example – Bucket A: (19.86 x .26196) + (26.79 x .50869) + (30.15 x .21896) + (148.99 x .0104) = 26.98

Appendix 4: Re-determination of Reference Rates

Section A4-1: Frequency

Reference rates are updated quarterly.

Section A4-2: Calculation of Reference Rates

1. Download the average of the daily rates for the prior quarter for the 2-yr, 5-yr, 10-yr and 30-yr US Treasuries from https://fred.stlouisfed.org

Table A4-1: Average Quarterly US Treasury RatesQuarterly US Treasury Rates from Federal Reserve Economic Database (FRED)

Series Name DGS2 DGS5 DGS10 DGS30Constant Maturity 2-Yr Treasury 5-Yr Treasury 10-Yr Treasury 30-Yr Treasury

2017 Q4 1.69 2.07 2.37 2.82

2. Using weight Table A1-1, calculate a reference rate for each valuation rate bucket.

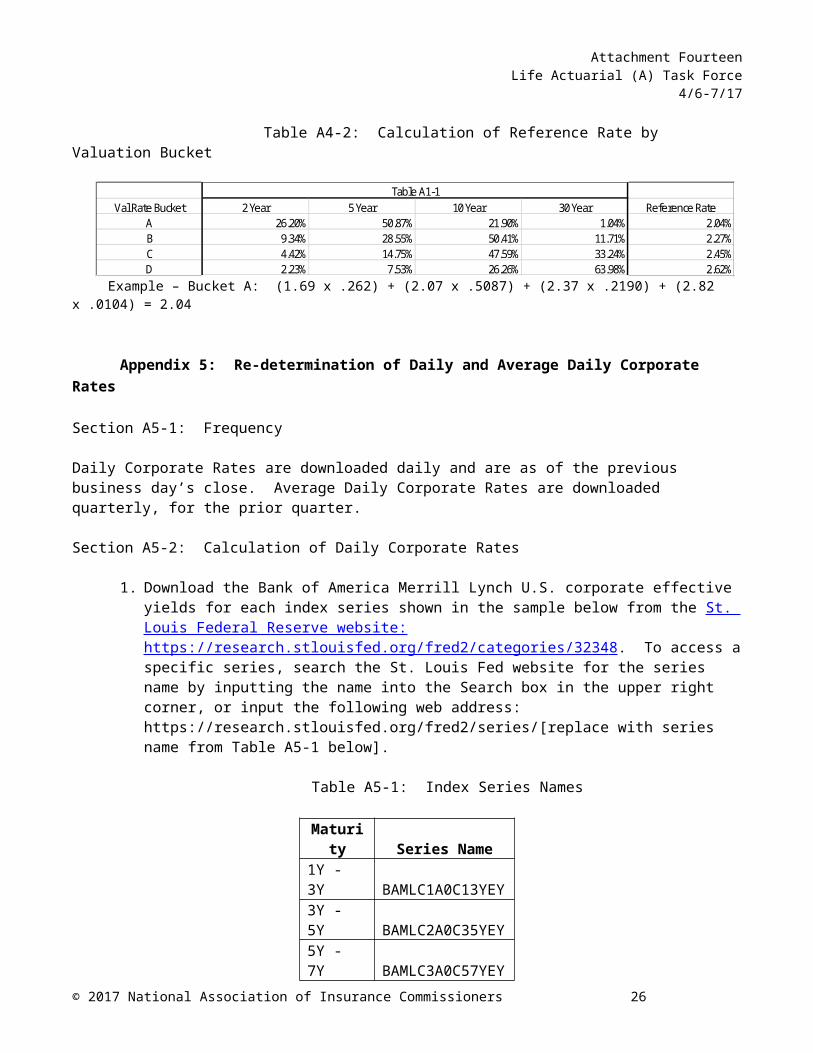

Table A4-2: Calculation of Reference Rate by Valuation Bucket

Val Rate Bucket 2 Year 5 Year 10 Year 30 Year Reference RateA 26.20% 50.87% 21.90% 1.04% 2.04%B 9.34% 28.55% 50.41% 11.71% 2.27%C 4.42% 14.75% 47.59% 33.24% 2.45%D 2.23% 7.53% 26.26% 63.98% 2.62%

Table A1-1

Example – Bucket A: (1.69 x .262) + (2.07 x .5087) + (2.37 x .2190) + (2.82 x .0104) = 2.04

Appendix 5: Re-determination of Daily and Average Daily Corporate Rates

Section A5-1: Frequency

Daily Corporate Rates are downloaded daily and are as of the previous business day’s close. Average Daily Corporate Rates are downloaded quarterly, for the prior quarter.

Section A5-2: Calculation of Daily Corporate Rates

1. Download the Bank of America Merrill Lynch U.S. corporate effective yields for each index series shown in the sample below from the St. Louis Federal Reserve website: https://research.stlouisfed.org/fred2/categories/3234 8 . To access a specific series, search the St. Louis Fed website for the series name by inputting the name into the Search box in the upper right corner, or input the following web address: https://research.stlouisfed.org/fred2/series/[replace with series name from Table A5-1 below].

© 2017 National Association of Insurance Commissioners 20

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Table A5-1: Index Series Names

Maturity Series Name1Y - 3Y BAMLC1A0C13YEY3Y - 5Y BAMLC2A0C35YEY

5Y - 7Y BAMLC3A0C57YEY7Y - 10Y BAMLC4A0C710YEY10Y - 15Y BAMLC7A0C1015YEY15Y+ BAMLC8A0C15PYEY

Sample for Business Day 1/10/2018, Downloaded on 1/11/2018:

Table A5-2: Downloaded Daily Corporate Rates

Index Series Name BAMLC1A0C13YEY BAMLC2A0C35YEY BAMLC3A0C57YEY BAMLC4A0C710YEY BAMLC7A0C1015YEY BAMLC8A0C15PYEYMaturity 1Y – 3Y 3Y – 5Y 5Y – 7Y 7Y – 10Y 10Y – 15Y 15Y+

Rate 2.45 2.88 3.26 3.55 4.00 4.20

2. Calculate the daily corporate rate for each valuation rate bucket, which is a weighted average of the Bank of America Merrill Lynch U.S. corporate effective yields, using Table A1-4 for the current calendar year as weights.

Sample calculation for Business Day 1/10/2018:

Table A5-3: Calculation of Daily Corporate Rates by Valuation Bucket

1Y - 3Y 3Y - 5Y 5Y - 7Y 7Y - 10Y 10Y - 15Y +15YA 26.20% 25.40% 25.40% 10.90% 10.90% 1.00% 3.07*B 9.30% 14.30% 14.30% 25.20% 25.20% 11.70% 3.50C 4.40% 7.40% 7.40% 23.80% 23.80% 33.20% 3.75D 2.20% 3.80% 3.80% 13.10% 13.10% 64.00% 3.96

BucketTable A1-4: Weights for Daily Corporate Rates (Sample)

Daily Corp

Rate (%)

*Note: Weighted Average of Bucket A: (2.45 x .262) + (2.88 x .254) + (3.26 x .254) + (3.55 x .109) + (4.00 x .109) + (4.20 x .01) = 3.07

Section A5-3: Calculation of Average Daily Corporate Rates1. Calculate the quarterly average Bank of America Merrill Lynch U.S. corporate effective yields for

each index series shown in the sample below from the St. Louis Federal Reserve website: https://research.stlouisfed.org/fred2/categories/3234 8 . To access a specific series, search the St. Louis Fed website for the series name by inputting the name into the Search box in the upper right corner, or input the following web address: https://research.stlouisfed.org/fred2/series/[replace with series name from below].

© 2017 National Association of Insurance Commissioners 21

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Table A5-4: Downloaded Average Daily Corporate Rates

Index Series Name BAMLC1A0C13YEY BAMLC2A0C35YEY BAMLC3A0C57YEY BAMLC4A0C710YEY BAMLC7A0C1015YEY BAMLC8A0C15PYEYMaturity 1Y – 3Y 3Y – 5Y 5Y – 7Y 7Y – 10Y 10Y – 15Y 15Y+

Rate 1.99 2.48 2.97 3.40 3.98 4.272. Calculate the average daily corporate rate for each valuation rate bucket, which is a weighted

average of the quarterly average Bank of America Merrill Lynch U.S. corporate effective yields, using Table A1-4 for the current calendar year as weights.

Sample calculation for period 07/01/2017 thru 9/30/2017:

Table A5-5: Calculation of Average Daily Corporate Rates by Valuation BucketTable A5-5: Calculation of Average Daily Corporate Rates by Valuation Bucket (period 07/01/2017 thru 9/30/2017)

Table A1-4: Weights for Daily Corporate Rates (Sample)Bucket 1Y - 3Y 3Y - 5Y 5Y - 7Y 7Y - 10Y 10Y - 15Y +15Y Avg. Corp Rate (%)

A 25.5% 25.4% 25.4% 11.3% 11.3% 1.1% 2.772*B 8.9% 13.9% 13.9% 25.4% 25.4% 12.4% 3.342C 4.1% 7.0% 7.0% 23.6% 23.6% 34.6% 3.685D 2.0% 3.5% 3.5% 12.7% 12.7% 65.6% 3.968*Weighted Average of Bucket A: (1.99 x .255) + (2.48 x .254) + (2.97 x .254) + (3.40 x .113) + (3.98 x .113) + (4.27 x .011) = 2.772

© 2017 National Association of Insurance Commissioners 22

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Appendix 6: Calculation of Maximum Valuation Interest Rates

Section A6-1: Calculation of Quarterly Valuation Rate1. For each valuation rate bucket, calculate the Quarterly Valuation Rate as follows:

Iq = R + S – D – E

where:

a. R is the reference rate for that valuation rate bucket (see Appendix 4);b. S is the spread for that valuation rate bucket (see Appendix 3);c. D is the default cost for that valuation rate bucket (see Appendix 2); andd. E is the spread deduction defined as 0.25%.

For non-jumbo contracts, the statutory maximum valuation interest rate is the Quarterly Valuation Rate (Iq) rounded to the nearest one-fourth of one percent (1/4 of 1%).

Sample Calculation for based on 1st Quarter 2018:

Table A6-1: Calculation of Quarterly Statutory Maximum Valuation Interest RateIq Rounded to .25% Iq = R + S – D – E R S D E

Bucket Statutory Maximum Valuation Rate Quarterly Valuation Rate Reference Rate Spread Default Cost Expense ProvisionA 2.25% 2.34% 2.04% 0.80% 0.26% 0.25%B 2.75% 2.72% 2.27% 0.98% 0.28% 0.25%C 3.00% 3.03% 2.45% 1.13% 0.29% 0.25%D 3.25% 3.37% 2.62% 1.30% 0.30% 0.25%

Section A6-2: For each valuation rate bucket, calculate the Daily Valuation Rate for a given date as follows:

Id = Iq + Cd-1 – Cq

where:a. Iq is the Quarterly Valuation Rate for the calendar quarter preceding the business day immediately preceding the given date;b. Cd-1 is the Daily Corporate Rate (see Appendix 5) for the business day immediately preceding the given date; andc. Cq is the Average Daily Corporate Rate (see Appendix 5) corresponding to the same period for which Iq is applicable.

For jumbo contracts, the statutory maximum valuation interest rate is the Daily Valuation Rate rounded to the nearest one-hundredth of one percent (1/100 of 1%).

© 2017 National Association of Insurance Commissioners 23

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Example for the Daily Valuation Rate Calculation for 01/11/2018:

I (01/11/2018) = I(4) (based on data from 07/01/2017 thru 09/30/2017) + C(01/10/2018)

- C(4) (based on data from 07/01/2017 thru 09/30/2017)

where:a. I(4) is the Quarterly Valuation Rate for the calendar quarter preceding the business day

(01/10/2018) immediately preceding the given date (01/11/2018);b. C (01/10/18) is the Daily Corporate Rate (see Appendix 5) for the business day (01/10/2018)

immediately preceding the given date (01/11/2018); andc. C(4) is the Average Daily Corporate Rate (see Appendix 5) corresponding to the period

(07/01/2017 – 09/30/2017) used to develop I(4).

Table A6-2: Calculation of Daily Statutory Maximum Valuation Interest Rate

Id rounded to .01% Id = 01/11/2018

Bucket Stat Maximum Valuation Rate = Iq + Cd-1 - Cq

A 2.50% 2.495% 2.195% 3.07% 2.77%B 2.83% 2.830% 2.674% 3.50% 3.34%C 3.14% 3.140% 3.067% 3.75% 3.68%D 3.48% 3.480% 3.481% 3.96% 3.97%

Iq = 4 Cd-1 = 01/10/2018 Cq = 4

© 2017 National Association of Insurance Commissioners 24

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Section A6-3: Timing of Data Downloads

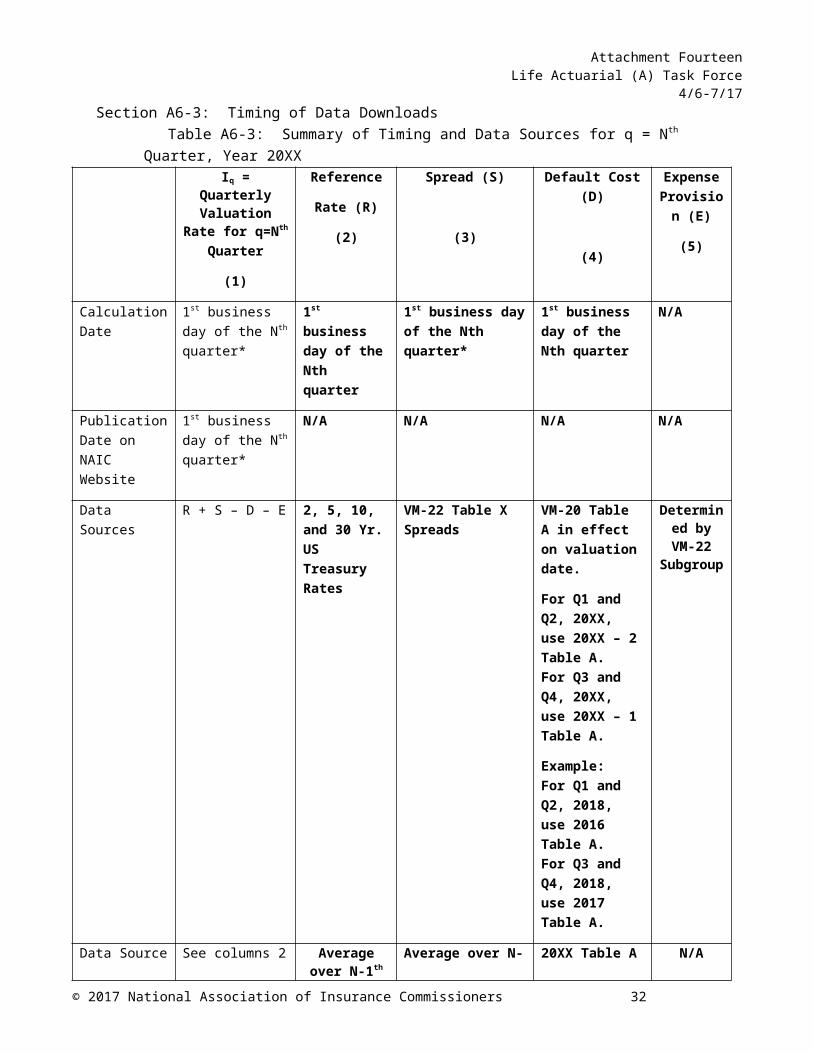

Table A6-3: Summary of Timing and Data Sources for q = Nth Quarter, Year 20XXIq = Quarterly

ValuationRate for q=Nth

Quarter

(1)

Reference

Rate (R)

(2)

Spread (S)

(3)

Default Cost (D)

(4)

Expense Provision

(E)

(5)

Calculation Date

1st business day of the Nth quarter*

1st business day of the Nth quarter

1st business day of the Nth quarter*

1st business day of the Nth quarter

N/A

Publication Date on NAIC Website

1st business day of the Nth quarter*

N/A N/A N/A N/A

Data Sources R + S – D – E 2, 5, 10, and 30 Yr. US Treasury Rates

VM-22 Table X Spreads

VM-20 Table A in effect on valuation date.

For Q1 and Q2, 20XX, use 20XX – 2 Table A. For Q3 and Q4, 20XX, use 20XX – 1 Table A.

Example: For Q1 and Q2, 2018, use 2016 Table A. For Q3 and Q4, 2018, use 2017 Table A.

Determined by VM-22 Subgroup

Data Source Time Period

See columns 2 - 5 Average over N-1th quarter

Average over N-1th quarter

20XX Table A is based on default cost data updated through 20XX - 1

N/A

Data Source Calculation Date

See columns 2 - 5 1st business day of Nth quarter

1st business day of Nth quarter*

VM-20 Table A is updated annually during the 2nd quarter

N/A. Held constant at

25 basis points

Data Source Publication Date on NAIC Website

See columns 2 - 5 N/A Not currently published, but could be on the 1st business day of Nth quarter

Annually during the 2nd quarter

N/A

Weight Table Used for Year 20XX, effective 1st business day of 20XX)

See columns 2 - 5 Table A1-1 Table A1-2 Table A1-3 N/A

© 2017 National Association of Insurance Commissioners 25

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17

Quarterly Valuation Rate is defined as follows:Iq = R + S – D – E Where:e. R is the Reference Rate defined in Subsection 3C;f. S is the Spread defined in Subsection 3D;g. D is the Default Cost defined in Subsection 3E; andE is the spread deduction defined as 0.25%.Daily Valuation Rate is defined as follows:Id = Iq + Cd – Cq

Where:d. Iq is the Quarterly Valuation Rate for the calendar quarter preceding the business day

immediately preceding the contract’s Premium Determination Date;e. Cd is the Daily Corporate Rate defined in Subsection 3F for the business day immediately

preceding the contract’s Premium Determination Date; andf. Cq is the Average Daily Corporate Rate defined in Subsection 3F corresponding to the period

used to develop Iq , which is the calendar quarter preceding the calendar quarter during which Iq is the Quarterly Valuation Rate.Guidance Note: As an example, for a contract with an 8/17/17 Premium Determination Date, the dates associated with the variables for the Daily Valuation Rate would be as follows:

Iq: 6/30/17

Cd: 8/16/17

Cq = the average Daily Corporate Rate over the period 1/1/17 to 3/31/17.

For Jumbo Contracts, the statutory maximum valuation interest rate is the Daily Valuation Rate rounded to the nearest one-hundredth of one percent (1/100 of 1%).

For Non-jumbo Contracts, the statutory maximum valuation interest rate is the Quarterly Valuation Rate rounded to the nearest one-fourth of one percent (1/4 of 1%).

Reference RateThe Reference Rate is the weighted average of the Quarterly Treasury Rates calculated using the following weights based on the contract’s Valuation Rate Bucket:

Table 3

Weights

Bucket

2 Year

5 Year

10 Year

30 Year

A 26.8%

51.6%

20.7%

0.9%

B 10. 30. 50. 9.6

© 2017 National Association of Insurance Commissioners 26

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/171% 3% 0% %

C 4.7%

15.8%

50.2%

29.2%

D 2.5%

8.3%

28.8%

60.5%

Guidance Note: Unrounded weights are used in the calculation. Appendix 1 explains how the weights are developed.

D. SpreadThe spread is the weighted average of the Expected Spreads calculated using the following weights based on the contract’s Valuation Rate Bucket:

Table 4

Weights

Bucket

2 Year

5 Year

10 Year

30 Year

A 26.8%

51.6%

20.7%

0.9%

B 10.1%

30.3%

50.0%

9.6%

C 4.7%

15.8%

50.2%

29.2%

D 2.5%

8.3%

28.8%

60.5%

E. Default CostThe Default Cost is the weighted average of the Expected Default Costs calculated using the following weights based on the contract’s Valuation Rate Bucket:Table 5

Weights

Bucket 2 Year

5 Year

10 Year

A 26.8% 51.6% 21.6%

© 2017 National Association of Insurance Commissioners 27

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17B 10.1

% 30.3% 59.6%

C 4.7% 15.8% 79.4%

D 2.5% 8.3% 89.3%

Guidance Note: These weights are based on duration and asset liability cash flow matching analysis for representative annuities within each Valuation Rate Bucket. Tables 3 to 5 are identical, except that for Table 5, the 10 year and 30 year columns are combined since VM-20 default rates are only published for maturities of up to 10 years.

F. Daily Corporate RateThe Daily Corporate Rate is the weighted average of the Bank of America Merrill Lynch U.S. corporate effective yields calculated using the following weights based on the contract’s Valuation Rate Bucket:

Table 6

Weights

Bucket

1Y – 3Y

3Y- 5Y

5Y – 7Y

7Y – 10Y

10Y – 15Y

+15Y

A 26.8%

25.8%

25.8%

10.3%

10.3%

0.9%

B 10.1%

15.2%

15.2%

25.0%

25.0%

9.6%

C4.7%

7.9%

7.9%

25.1%

25.1%

29.2%

D2.5%

4.1%

4.1%

14.4%

14.4%

60.5%

The Average Daily Corporate Rate means the average of the Daily Corporate Rates over a given calendar quarter.Guidance Note: The columns correspond to the groupings that Bank of America Merrill Lynch publishes. The source for these rates is the St. Louis Federal Reserve website:

© 2017 National Association of Insurance Commissioners 28

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17To access a specific series, search the St. Louis Fed website for the series name by inputting the name into the Search box in the upper right corner, or input the following web address: https://research.stlouisfed.org/fred2/series/[replace with series name from below].Index Series Names:

Maturity

Series Name

1Y - 3Y

BAMLC1A0C13YEY

3Y - 5Y

BAMLC2A0C35YEY

5Y - 7Y

BAMLC3A0C57YEY

7Y - 10Y

BAMLC

© 2017 National Association of Insurance Commissioners 29

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/174A0C710YEY

10Y - 15Y

BAMLC7A0C1015YEY

15Y+

BAMLC8A0C15PYEY

Guidance Note: LATF intends to review the weights in the above tables 3-6, and when necessary, update them to better reflect changes in the shape of the yield curve and/or the level of market interest rates. A brief description of the weight calculation methodology is provided in Attachment A.

G. Multiple Premiums

The prescribed methodology applies to single premium contracts providing fixed benefits. For contracts involving multiple premium payments, the benefits purchased by each premium shall be valued using the valuation interest rate in effect at the time the premium was determined and committed to by the purchaser.

© 2017 National Association of Insurance Commissioners 30

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17H. Except as provided in Subsection 3A.5 below, for group annuity contracts, the statutory maximum valuation rate shall be determined separately for each certificate holder, based on their Initial Age and the certificate Reference Period.

For group annuity contracts purchased under a retirement or deferred compensation plan with multiple annuity form options available to the certificate holder, the statutory maximum valuation rate shall be based on the normal form of payout as defined in the contract or as is evidenced by the underlying pension plan documents or census file. If the normal form of payout cannot be determined, the statutory maximum valuation rate shall be based on the most conservative annuity form available to the certificate holder.

Immaterial Premium Change

If the premium changes by an immaterial amount subsequent to the original Premium Determination Date, such as due to a data correction, the original Premium Determination Date shall be used.

Appendix 1

In the fourth quarter of each calendar year, the weightings used within each Valuation Rate Bucket for determining the applicable valuation interest rates for the following calendar year will be updated using the following process:

8.[1.] Each Valuation Rate Bucket has a set of representative annuity forms. These annuity forms are as follows:

© 2017 National Association of Insurance Commissioners 31

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17a. Bucket A:

i. Single Life Annuity age 91 with 0 and 5-year certain periodsii. 5-year certain only

b. Bucket B:i. Single Life Annuity age 80 and 85 with 0, 5, and 10-year certain periods

ii. 10-year certain onlyc. Bucket C:

i. Single Life Annuity age 70 with 0 and 15-year certain periodsii. Single Life Annuity age 75 with 0, 10 and 15-year certain periods

iii. 15-year certain onlyd. Bucket D:

i. Single Life Annuity age 55, 60, and 65 with 0 and 15-year certain periodsii. 25-year certain only

9.[2.] Annual cash flows are projected assuming annuity payments are made at the end of each year. These cash flows are averaged for each Valuation Rate Bucket across the annuity forms for that Bucket using the statutory valuation mortality table effective for the following calendar year for individual annuities for males.

10.[3.] The average daily rates in the third quarter for the 2-yr, 5-yr, 10-yr and 30-yr US Treasuries are calculated as input to calculate the present values in step 4.

11.[4.] The average cash flows are summed into four time period groups: years 1-3, years 4-7, years 8-15 and years 16-30. (Note, the present value of cash flows beyond year 30 is included in the years 16-30 Bucket. This present value is based on the lower of 3% and the 30-year Treasury rate input in Step3.)

12.[5.] The present value of each summed cash flow group in Step 4 is then calculated by using the Step 3 US Treasury rates for the mid-point of that group (and using the linearly interpolated US Treasury rate when necessary).

13.[6.] The duration weighted present value of the cash flows is determined by multiplying the present value of the cash flow groups by the midpoint of the time period for each applicable group.

14.[7.] Weightings for each cash flow time period group within a Valuation Rate Bucket are calculated by dividing the duration weighted present value of the cash flow by the sum of the duration weighted present value of cash flow for each Valuation Rate Bucket. Note, unrounded weights are used to calculate the single valuation rate for each Valuation Rate Bucket.

/tt/file_convert/5b29e5217f8b9ad8298b4f29/document.docxSection 2. Definitions

Portfolio Credit Quality Distribution – This term means the prescribed asset credit rating distribution as follows:

5% Treasuries 15% Aa bonds (5% Aa1, 5% Aa2, 5% Aa3) 40% A bonds (13.33% A1, 13.33% A2, 13.33% A3) 40% Baa bonds (13.33% Baa1, 13.33% Baa2, 13.33% Baa3)

© 2017 National Association of Insurance Commissioners 32

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17Guidance Note: The credit quality designations above have the same meaning as in VM-20, subsection 9.F.3.

Daily Treasury Rate – This term means the Daily Treasury Yield Curve Rate for a given maturity as published by the U.S. Department of the Treasury.

Guidance Note: The source for these rates is: https://www.treasury.gov

Expected Default Cost – This term means a vector of annual default costs by weighted average life calculated as a weighted average of the VM-20 prescribed annual default costs (Table A) in effect for the quarter prior to the Premium Determination Date for the Portfolio Credit Quality Distribution, as published on the Life Actuarial Task Force (LATF) website of the NAIC.Definitions – to be moved to VM-01:

1. The term “Rreference Pperiod” - This term means the length of time, rounded to the nearest year, from the Ppremium Ddetermination Ddate to the earlier of

(a) the date of the last non-life-contingent payment under the individual contract, or group certificate or contract feature, as applicable; and.

(b) the date of the first life-contingent payment under the contract, certificate or contract feature.

Guidance Note: The definition of Reference Period assumes a series of material, substantially similar payments and materiality is relative to the life-contingent payments. If the payments are not substantially similar, the actuary should apply prudent judgment and select the Valuation Rate Bucket with Macaulay duration that is a best fit to the Macaulay duration of the payments in question.

2. The term “Jjumbo Ccontract” – This term means a contract with an initial consideration equal to or greater than $250,000,000. Considerations for contractscontracts issued by an insurer to the same partycontract holder within 90 days shall be combined for purposes of determining whether athe contractcontracts meets this threshold.

Guidance Note: If multiple contracts meet this criterion in aggregate, then each contract is a jumbo contract.

3. The term “Nnon-jumbo Ccontract” – This term means a contract that does not meet the definition of thea Jumbo Contractjumbo contract.

B.[K.] Expected Spread – This term means a vector of spreads by weighted average life, calculated as a weighted average of the VM-20 prescribed spreads (Table F) for the quarter prior to the Premium Determination Date for the Portfolio Credit Quality Distribution, as published on the Life Actuarial Task Force (LATF) website of the NAIC.

© 2017 National Association of Insurance Commissioners 33

Attachment FourteenLife Actuarial (A) Task Force

4/6-7/17C.[L.] Quarterly Treasury Rate – This term means the average of the Daily Treasury Rates defined in

Subsection 2B above for a given maturity over the calendar quarter prior to the Premium Determination Date.

4. The term “Ppremium Ddetermination Ddate” – This term means the date uponas of which the valuation interest rate for the contract, certificate or contract feature being valued is selected.

premium is determined by the insurance company and is committed to by the client. This term is generally defined as the issue date. For supplementary contracts and annuitizations, this would normally be the date of election of the supplementary contracts and the annuitizations, but a company may use the valuation rate basis in effect when the original contract was issued with domestic commissioner approval.

Guidance Note: The Premium Determination Date is intended to be a date proximate to the date of the investment of the assets that support the contract. As examples,

for a group annuity for which the company locks in investment yields at the time of a quote, but the contract is issued subsequently, that “lock-in-date” should be used by the company on a consistent basis;

for a single-premium immediate annuity contract, this would normally be the issue date; for a supplementary contract, however, this date would normally be the date of annuitization. The

definition permits, subject to the domestic commissioner’s approval, the use of some other date. An example of such a situation includes using the issue date of the original deferred annuity contract for annuitizations. Approval would normally be granted when the domestic commissioner has been provided satisfactory demonstration that the company employs an appropriate asset/liability matching strategy.

5. The term “Iinitial Aage” means the age of the contract holder or certificate holder as of his or her – Age as of most recent the last birthday relative to as of the Ppremium Ddetermination Ddate. For joint life contracts, or certificates or contract features, the Iinitial Aage means the Iinitial Aage of the younger annuitant. ForIf a contract, certificate or contract feature is being valued on a standard mortality table contracts has an annuitant who is with impaired lives being valued using a rated age, I “initial Aage” means the rated age. If a contract, certificate or contract feature is being valued on a substandard mortalityFor contracts with impaired lives being valued using a substandard mortality table, I “initial Aage” is based onmeans an equivalent rated age.

© 2017 National Association of Insurance Commissioners 34

![sharing-economy.jp...¬ª»¾®¯Àµ² e S ¤¡ ¤ O j ¸½5 j Vm ¤9A ¯Àµ² I; ¤ = £0 ¤ ¬ª»¾®¯Àµ² X ~'( 9A¿¯Àµ² Vm ] ¤ Vm ¤9A L ¡ ¤ E` Vm ¤9A L 5 '( Vm 9A¿¯Àµ²](https://img.pdfslide.us/doc/110x75/5f067c9d7e708231d4183c06/sharing-e-s-o-j-5-j-vm-9a-i-.jpg)