Embed Size (px)

Citation preview

Kraken Investment Case Study

1

TABLE OF CONTENTS INTRODUCTION ....................................................................................................................................... 2

Objectives................................................................................................................................................. 2

ANALYSIS .................................................................................................................................................. 4

Technical Differences .......................................................................................................................... 4

Project Governance............................................................................................................................. 5

Community Value ............................................................................................................................... 8

Risks ................................................................................................................................................... 10

Our Answer ....................................................................................................................................... 12

Investment Portfolio ............................................................................................................................. 13

Probability Pricing Model ................................................................................................................ 14

Final Results ...................................................................................................................................... 17

Investment Recommendation........................................................................................................... 18

CONCLUSION ......................................................................................................................................... 19

APPENDICES ........................................................................................................................................... 20

Appendix A – Appreciation Rate for Probability Pricing Model ..................................................... 20

Appendix B – Depreciation Rate for Probability Pricing Model ...................................................... 21

Appendix B – Depreciation Rate for Probability Pricing Model ...................................................... 22

Appendix C – The Legality of Bitcoin in different countries ............................................................ 23

REFERENCE ............................................................................................................................................ 25

Kraken Investment Case Study

2

INTRODUCTION

“…to boldly go where no man has gone before…” – Star Trek

It was not too long ago when people used commodity money (gold and silver) or representative

money (a claim on a commodity) as units of exchange. Today, we use currencies that are fiat

money (by Government regulation or law). Imagine a world just 10-15 years later, when today’s

kids and teens start to buy things and enter into transactions. What will they use as a unit of

exchange? Will it be similar to what we use now or something straight out of Star Trek? We

already see glimpses of the future – examples include social media, 3-D printing, Holograms.

Cryptocurrencies or digital assets are examples of future of exchange and contracts. The future is

already knocking at our doors and it is up to us to embrace it and “go boldly where no man has

gone before…”

Bitcoin and Ethereum are two main players in the field of cryptocurrencies. They are used as an

internet-based currency allowing for instantaneously completed transactions across the globe.

Bitcoin is the type of digital currency in which encryption techniques are used to regulate the

generation of units of exchange and verify the transfer of funds, operating independently of a

centralized bank. Ethereum, on the other hand, is a public blockchain-based distributed

computing platform, featuring smart contract functionality. It can execute peer-to-peer contracts

using a cryptocurrency called ether.

Objectives

We have only one objective. Decide how to invest $1 million in bitcoin, ethereum, or both that

will maximize profit with minimal risk. The caveat? We cannot touch our investment for 5 years.

Kraken Investment Case Study

3

To address such an objective, we must, first, answer the question “Which is the digital asset of

the future?”

After a crash course in digital assets, Green Eagle Investments has arrived at a unique investment

strategy using our own price model with best and worst case scenarios. The future holds

unknown risks. To minimize these risks, we considered a litany of perspectives: technical

differences, project governance, community value, risks, supply and demand, and government

regulations (Appendix C).

Kraken Investment Case Study

4

ANALYSIS

Technical Differences

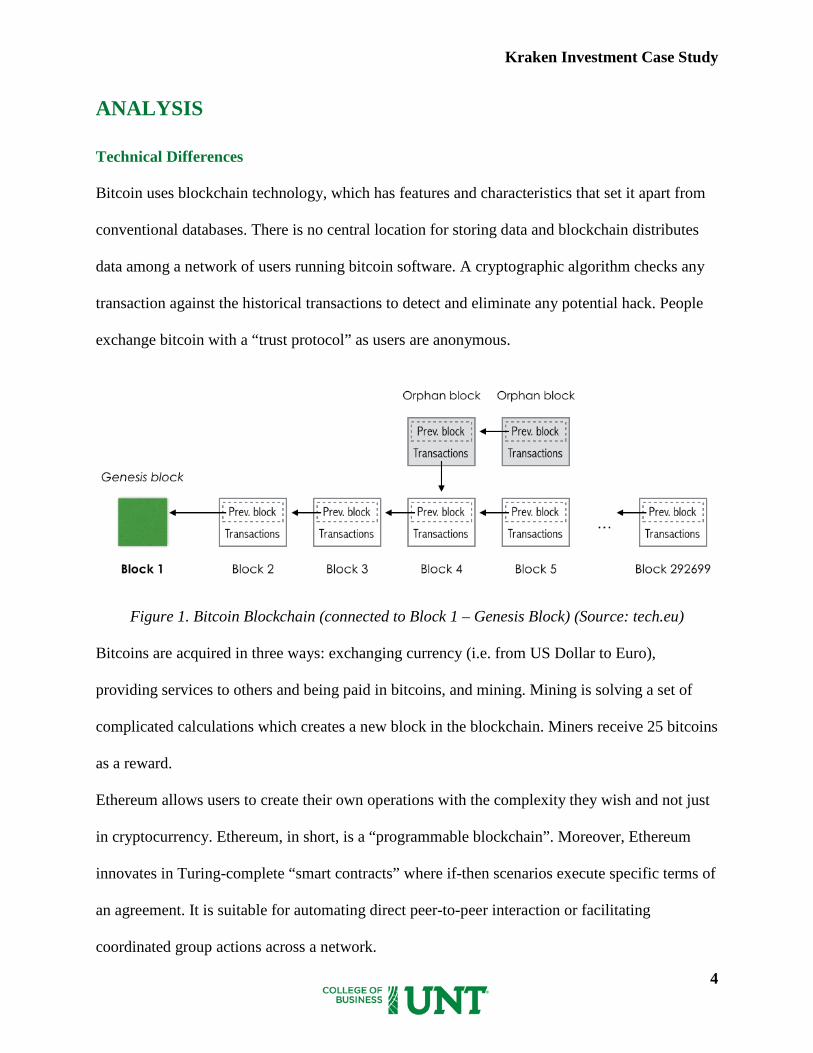

Bitcoin uses blockchain technology, which has features and characteristics that set it apart from

conventional databases. There is no central location for storing data and blockchain distributes

data among a network of users running bitcoin software. A cryptographic algorithm checks any

transaction against the historical transactions to detect and eliminate any potential hack. People

exchange bitcoin with a “trust protocol” as users are anonymous.

Figure 1. Bitcoin Blockchain (connected to Block 1 – Genesis Block) (Source: tech.eu)

Bitcoins are acquired in three ways: exchanging currency (i.e. from US Dollar to Euro),

providing services to others and being paid in bitcoins, and mining. Mining is solving a set of

complicated calculations which creates a new block in the blockchain. Miners receive 25 bitcoins

as a reward.

Ethereum allows users to create their own operations with the complexity they wish and not just

in cryptocurrency. Ethereum, in short, is a “programmable blockchain”. Moreover, Ethereum

innovates in Turing-complete “smart contracts” where if-then scenarios execute specific terms of

an agreement. It is suitable for automating direct peer-to-peer interaction or facilitating

coordinated group actions across a network.

Kraken Investment Case Study

5

Figure 2. Ethereum Smart Contract example (Source: ethereum.org)

Ethereum uses a “ghost protocol” where the block time is 14 to 15 seconds compared to 10

minutes for Bitcoin, which gives it faster transactional power. Ethereum does have a more

complex way to calculate transaction costs. In Bitcoin, it is simpler where transactions compete

equally with each other.

Project Governance

Project governance comes down to who makes the decision. Bitcoin and Ethereum highlight

decentralization as the “game changer” in digital currency. In theory, each will eliminate the

need for financial intermediaries, which will speed up transactions and minimize fees. Each will

rely on network and platform users to maintain the integrity of the system. In reality, each has

experienced challenges in keeping a true decentralized format. In the end, who makes the

decision? Is it the network users? Is it the platform developers? More importantly, what are the

foreseeable impacts?

Kraken Investment Case Study

6

In a decentralized environment, a simple decision is like climbing a mountain. 100% unity of

users is needed 100% of the time. Imagine the amount of energy needed to sustain that.

Illustrating the conundrum, let’s review the reaction to one security breach each has experienced.

As recently as August 2016, hackers stole $65 million from Bitcoin which made Bitcoin’s value

drop 15% before recovering to its pre-hack value (Nakamura & Chen, 2016).

Figure 3. Bitcoin’s plunge after being hacked in August 2016

(Source: coindesk.com)

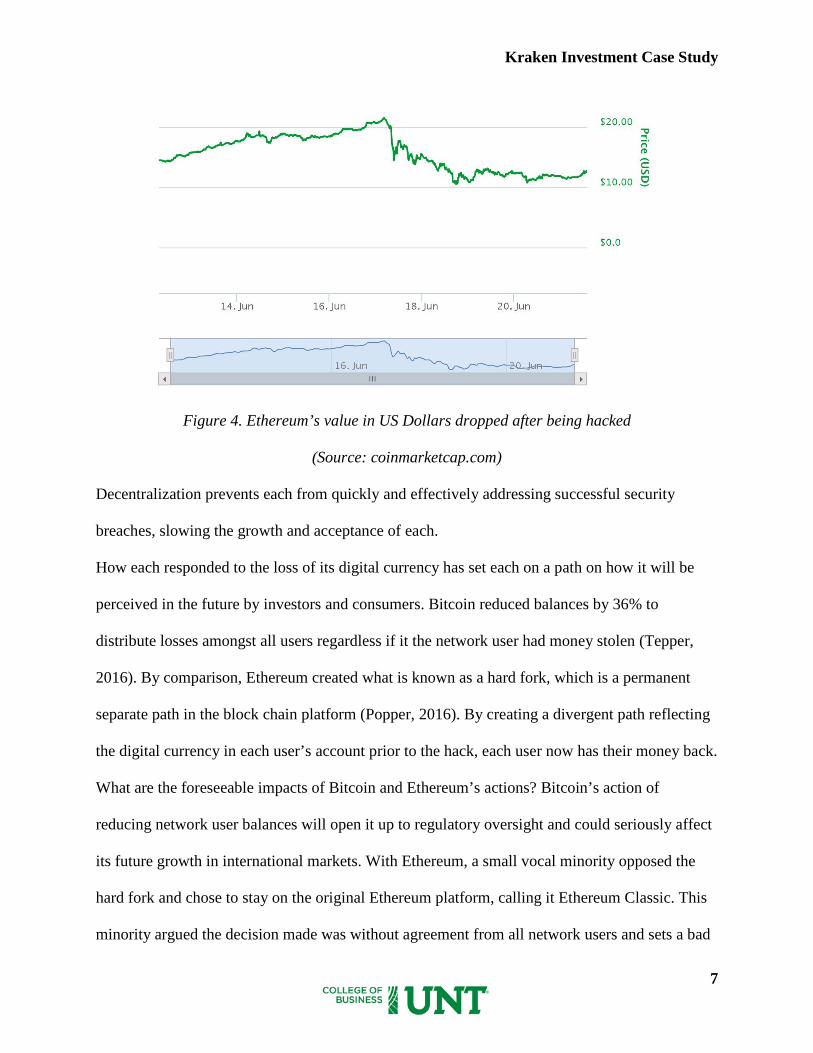

In June 2016, hackers stole $50 million from Ethereum. The impact on Ethereum’s value was

just as severe (Price, 2016).

Kraken Investment Case Study

7

Figure 4. Ethereum’s value in US Dollars dropped after being hacked

(Source: coinmarketcap.com)

Decentralization prevents each from quickly and effectively addressing successful security

breaches, slowing the growth and acceptance of each.

How each responded to the loss of its digital currency has set each on a path on how it will be

perceived in the future by investors and consumers. Bitcoin reduced balances by 36% to

distribute losses amongst all users regardless if it the network user had money stolen (Tepper,

2016). By comparison, Ethereum created what is known as a hard fork, which is a permanent

separate path in the block chain platform (Popper, 2016). By creating a divergent path reflecting

the digital currency in each user’s account prior to the hack, each user now has their money back.

What are the foreseeable impacts of Bitcoin and Ethereum’s actions? Bitcoin’s action of

reducing network user balances will open it up to regulatory oversight and could seriously affect

its future growth in international markets. With Ethereum, a small vocal minority opposed the

hard fork and chose to stay on the original Ethereum platform, calling it Ethereum Classic. This

minority argued the decision made was without agreement from all network users and sets a bad

Kraken Investment Case Study

8

precedent that could lead to further centralization. If you have a vocal minority opposing such

benevolent attempts, you have the potential to create instability in digital currency trading.

Community Value

Bitcoin and Ethereum have differences when bringing value to the community but there are some

things in common. The primary value of Bitcoin is the protection for users’ money and identity.

Each transaction is recorded with an anonymous Bitcoin address that changes every time. The

transaction cost when using bitcoins is minor or zero, both domestically and internationally,

however, users have to deal with irreversible transactions. If bitcoins go to the wrong address,

users are likely to lose their money if the receiver does not want to send it back. No liability

protection is in place. In case a user’s wallet gets hacked, that user will suffer the loss.

In addition, Bitcoin value does fluctuate (this also applies to Ethereum), and the volatility can

discourage individual users from using bitcoins. For instance, Bitcoin value went from,

approximately, $1,100 to $600 in less than a month in 2013.

Figure 5. Bitcoin’s volatility in December 2013

(Source: coindesk.com)

Businesses can minimize the risks of volatility by converting Bitcoin payments to cash.

Businesses can, also, benefit by reducing the costs of building pricey Point-of-Sale (POS)

Kraken Investment Case Study

9

systems and hardware. In addition, fraud is limited thanks to the public blockchain. Therefore, in

2015, more than 100,000 merchants accept Bitcoin. Bitcoin is, also, active in international

markets of Europe and Asia, showing its worldwide market strength. One concern for Bitcoin is

how easy users can buy illegal products online with no repercussions.

What value does Ethereum add? Ethereum, indeed, has more usages than Bitcoin. It is used as a

means of exchange or payment. This is the primary reason Ethereum is known as Bitcoin’s rival.

Ethereum is now attracting the attention of big banks and major corporations. According to the

Wall Street Journal, “…banks remain enamored with the idea of using the new technologies to

cut costs and make a whole host of processes simpler and more efficient” (Demos, 2016). The

article, specifically, highlighted JPMorgan Chase’s Quorum project (Demos, 2016). In another

article in the Huffington Post, “UBS was nearing a formal announcement of its acceptance of

Ethereum”. (Seaman, 2016). What we found quite interesting is UBS is going to use to transmit

“financial data around the world” (Seaman, 2016). This has the potential to reduce settlement

times and improve redemption flow for a variety of financial products. Crowdfunding is another

example. You can use Ethereum’s smart contract to raise money for a start-up and not be

charged fees such as the DAO.

Decentralized applications built on Ethereum are getting noticed. ‘Vevue’, described as “bring

Google Street View to life”, enables users to take shorts clips of where they eat, shop, stay and

share with others around the globe. ‘Etheria’ is an app that builds a Minecraft-like virtual world.

‘KYC-Chain’ creates a better tool to manage identity.

Most importantly, major organizations are finding ways to use Ethereum as an advanced version

of Bitcoin. Founder and CEO of Gatecoin, a bitcoin and ether trading platform, Aurélien Menant

Kraken Investment Case Study

10

believes decentralized apps developed on Ethereum “are the next disruptors, and we are

expecting to see the next Facebook, Uber or Airbnb, being fully decentralized, relying on

blockchain technology, and probably built on Ethereum” (Brown, 2016).

Risks

Security Risks

With money and asset, security is the top priority, especially when “real money” is transferred to

“virtual money”. Blockchain creators are aware of this, therefore transactions are checked with

historical data. Although each has constant updates to its systems, Ethereum’s Casper for

example, there are always chances that hackers find tiny holes in the system to get through and

get their jobs done.

Liquidation Risks

The security and legality of Bitcoin and Ethereum are key roles that will determine the

cryptocurrencies cycle life, which directly affect their liquidation. In fact, not many countries

consider cryptocurrencies as legal method for payment due to illegal transactions and money

laundering.

Structural/Political Risks

China is the best place to mine bitcoin and other cryptocurrencies due to its cost efficiency. From

our calculations from blockchain.info, China mining pools accounted for 73% of new Bitcoin

created in 2016. Moreover, China is the most active Bitcoin market with a significant number of

transactions (Popper, 2016). Technically, the majority will dominate minority in making

decisions over all transactions in Bitcoin system. Beginning in 2013, many Chinese digital

currency pools are now investing mining for ether. China will become the biggest producer of

ether in the future. Knowing this, it leads us to believe that there will be structural or political

Kraken Investment Case Study

11

risk for Bitcoin and Ethereum in China. The decentralized system would become more

centralized when decisions are based on majority.

Figure 6. Bitcoin Mining Share (Source: blockchain.info)

73%

24%

3%

Marketshare of Bitcoin Mining (Hashrate Distribution)

China Global Unknown

Kraken Investment Case Study

12

Our Answer

After Satoshi Nakamoto raised a global interest in Bitcoin, debates about virtual currency exist.

People talk potential, breakthrough, and risks. Bitcoin is the most-known cryptocurrency with

the largest market value among its type. Ethereum has rapidly emerged as a superstar in the

world of digital currencies. They draw similarities, but to us, mostly they are effective in

different ways.

In our analysis, each’s strengths outweigh the other in certain areas. We cannot judge them like a

boxing match, who wins the most rounds; instead, we judge the whole world of virtual

currencies. Despite subject to manipulation, Bitcoin, Ethereum, and other digital currencies are

bringing a technological advancement to the financial world. Winklevoss Twins, founders of

Gemini, affirmed that Bitcoin would fragment the role of gold in future, while Ether would

change the world of contract law (Maras, 2016).

At the moment, it is premature to conclude which one is better. Our final answer is

cryptocurrency, not a single kind of coin, is the asset of the future.

Kraken Investment Case Study

13

Investment Portfolio

Taking into account our research, we decided to invest in Bitcoin and Ethereum in order to

maximize our wealth in the next five years.

Bitcoin is the “safer” asset, while Ethereum is riskier since it is in its infancy. At the time of

research, Bitcoin volatile index with USD is 0.89% and 1.07% for 30-day and 60-day estimate,

respectively. Ether’s price changes, approximately, 2% a month and 7% for 60-day. Bitcoin has

constantly updated its performance after being hacked multiple times. In contrast, Ethereum

needs more experience testing its platform to better run efficiently and confidentially.

In 2017, Ethereum will introduce a GHOST protocol called Casper to increases the security

process of producing blocks. Therefore, a portfolio with 60% of Bitcoin (XBT) and 40% of

Ethereum (ETH) in five years will meet our investment goals.

Table 1. Outlook of Investment Portfolio

Source: Kraken Bitcoin Exchange on October 16, 2016

Investment budget: $1,000,000

% Bitcoin in Portfolio 60% % Ethereum in Portfolio 40% Value in portfolio $600,000 Value in portfolio $400,000 Bitcoin Price $642.56 Ethereum Price $11.96 # Bitcoin 933.76 # Ether 33,444.82

Kraken Investment Case Study

14

Probability Pricing Model We built the following model incorporating the probabilities of events (risks) that happen in the

next five years.

Figure 7. Probability Pricing Model for Bitcoin and Ether

U

D

U2

UD

D2

U3

D3

UDU

UDD

U4

UDUU

UDUD

UDDD

D4

U5

D5

UDUUU

UDUDU

UDUDD

UDDDD

2016 2017 2018 2019 2020 2021

50%

50%

33.33%

33.34%

33.33%

15%

15%

35%

35%

10%

10%

25%

25%

5%

5%

35%

10%

35%

10%

30%

Kraken Investment Case Study

15

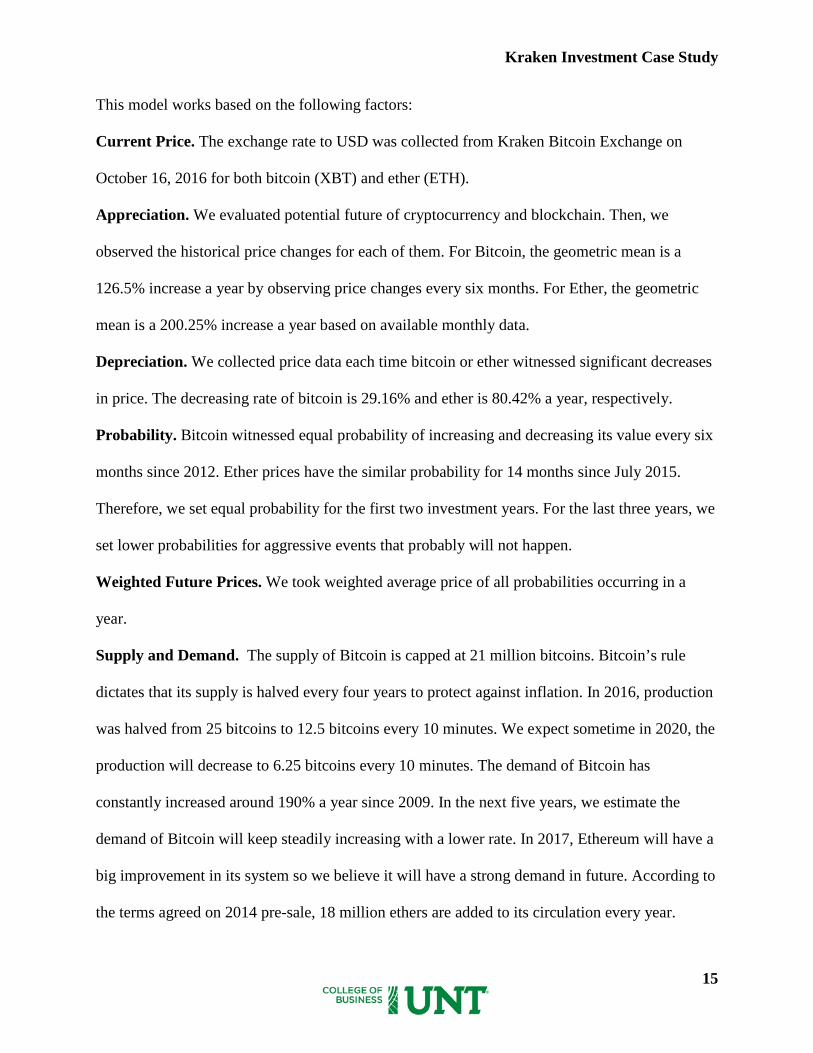

This model works based on the following factors:

Current Price. The exchange rate to USD was collected from Kraken Bitcoin Exchange on

October 16, 2016 for both bitcoin (XBT) and ether (ETH).

Appreciation. We evaluated potential future of cryptocurrency and blockchain. Then, we

observed the historical price changes for each of them. For Bitcoin, the geometric mean is a

126.5% increase a year by observing price changes every six months. For Ether, the geometric

mean is a 200.25% increase a year based on available monthly data.

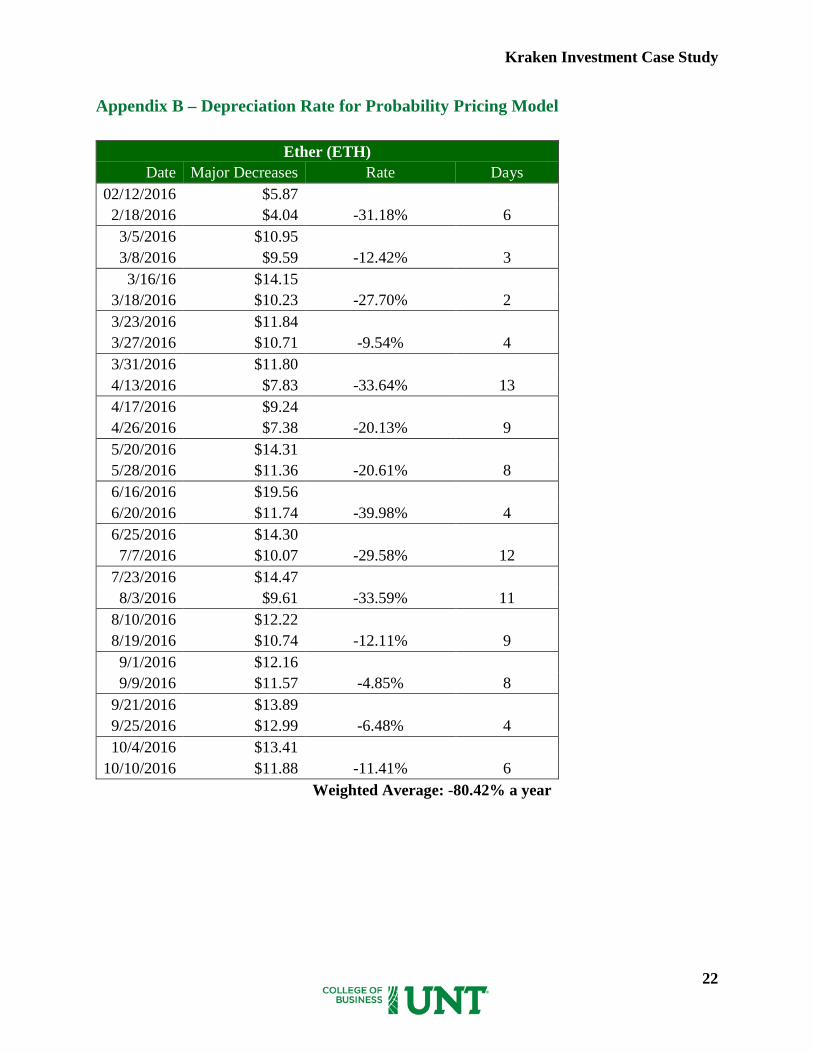

Depreciation. We collected price data each time bitcoin or ether witnessed significant decreases

in price. The decreasing rate of bitcoin is 29.16% and ether is 80.42% a year, respectively.

Probability. Bitcoin witnessed equal probability of increasing and decreasing its value every six

months since 2012. Ether prices have the similar probability for 14 months since July 2015.

Therefore, we set equal probability for the first two investment years. For the last three years, we

set lower probabilities for aggressive events that probably will not happen.

Weighted Future Prices. We took weighted average price of all probabilities occurring in a

year.

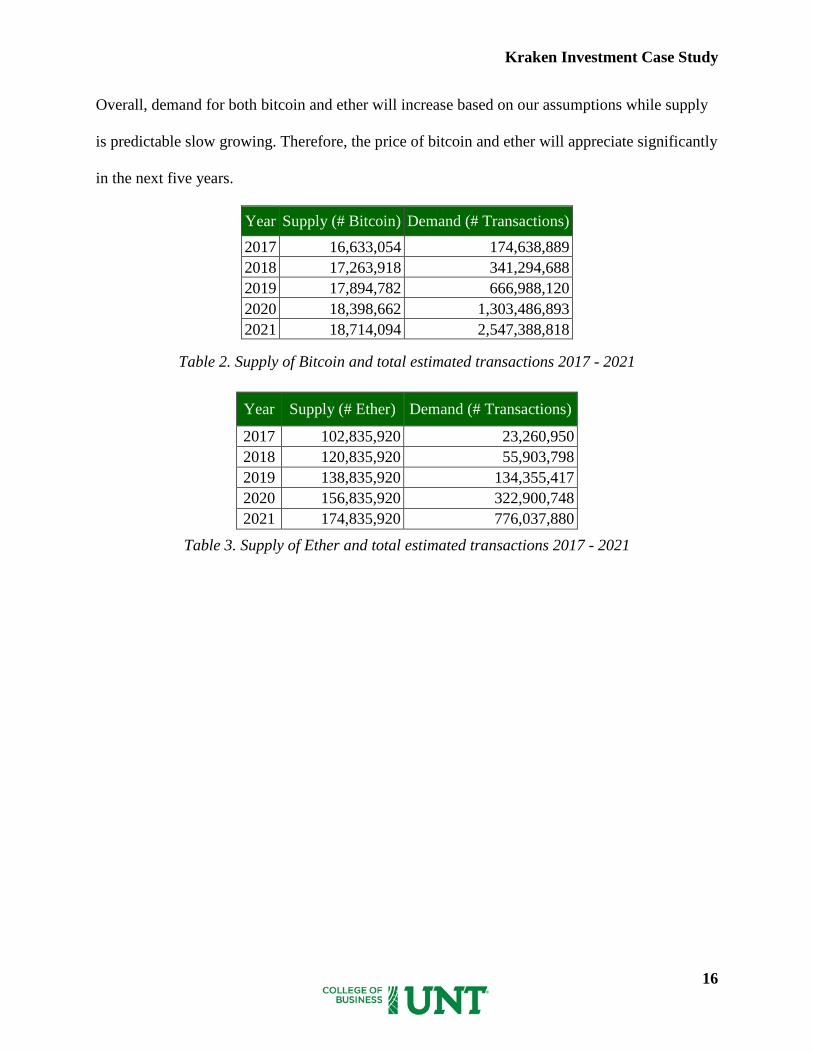

Supply and Demand. The supply of Bitcoin is capped at 21 million bitcoins. Bitcoin’s rule

dictates that its supply is halved every four years to protect against inflation. In 2016, production

was halved from 25 bitcoins to 12.5 bitcoins every 10 minutes. We expect sometime in 2020, the

production will decrease to 6.25 bitcoins every 10 minutes. The demand of Bitcoin has

constantly increased around 190% a year since 2009. In the next five years, we estimate the

demand of Bitcoin will keep steadily increasing with a lower rate. In 2017, Ethereum will have a

big improvement in its system so we believe it will have a strong demand in future. According to

the terms agreed on 2014 pre-sale, 18 million ethers are added to its circulation every year.

Kraken Investment Case Study

16

Overall, demand for both bitcoin and ether will increase based on our assumptions while supply

is predictable slow growing. Therefore, the price of bitcoin and ether will appreciate significantly

in the next five years.

Table 2. Supply of Bitcoin and total estimated transactions 2017 - 2021

Table 3. Supply of Ether and total estimated transactions 2017 - 2021

Year Supply (# Bitcoin) Demand (# Transactions) 2017 16,633,054 174,638,889 2018 17,263,918 341,294,688 2019 17,894,782 666,988,120 2020 18,398,662 1,303,486,893 2021 18,714,094 2,547,388,818

Year Supply (# Ether) Demand (# Transactions)

2017 102,835,920 23,260,950 2018 120,835,920 55,903,798 2019 138,835,920 134,355,417 2020 156,835,920 322,900,748 2021 174,835,920 776,037,880

Kraken Investment Case Study

17

Final Results

2016 2017 2018 2019 2020 2021 $38,304.93 $16,911.67 $7,466.52 $11,980.23 $3,296.48 $5,289.28 $1,455.40 $2,335.22 $3,746.93

$642.56 $1,031.00 $1,654.27 $455.19 $730.36 $1,171.89 $322.46 $517.39 $228.43 $366.52 $161.82 $114.63

Future Price $955.29 $1,549.98 $2,227.20 $3,655.30 $4,877.24 Table 4. Bitcoin’s Prices in the next five years by Probability Pricing Model

2016 2017 2018 2019 2020 2021 $2,922.79 $973.16 $324.02 $190.54 $107.88 $63.44 $35.92 $21.12 $12.42

$11.96 $7.03 $14.96 $2.34 $1.38 $0.81 $0.46 $0.27 $0.09 $0.05 $0.02 $0.00

Future Price $19.13 $38.46 $56.49 $117.74 $169.83 Table 5. Ether’s Prices in the next five years by Probability Pricing Model

The results above show that the price of a Bitcoin in 2021 would be approximately $4,877.27

and Ether could worth somewhere around $170. Using those figures to calculate Net Present

Value of the investment portfolio with various discount rates:

Kraken Investment Case Study

18

Discount rate PV of Bitcoin PV of Ether NPV

IBitcoin: $600,000 IEther: $400,000

10% $2,827,796.29 $3,526,800.10 $5,354,596.40 20% $1,830,228.51 $2,282,643.24 $3,112,871.75 30% $1,226,576.91 $1,529,774.82 $1,756,351.73 40% $846,781.51 $1,056,097.69 $902,879.20 50% $599,729.28 $747,976.54 $347,705.82 60% $434,321.80 $541,681.94 -$23,996.25 70% $320,750.20 $400,036.54 -$279,213.26

Table 6. NPV of the Portfolio in 2021

This table shows that with the discount rate from 10% to 50%, the portfolio will have positive

NPV. If the discount rate goes beyond 50%, the investment will receive losses in 2021.

Investment Recommendation

Our pricing model based on probabilities of future events predicted an appreciated price for both

bitcoin and ether in the next five years. A portfolio combining bitcoin and ether will maximize

our wealth and satisfy our risk tolerance. Investing $1,000,000 over five-years, we recommend

investing 60% in Bitcoin and 40% in Ethereum. Using a discount rate of 40%, the portfolio gains

$902,879, approximately, a 90% return on investment 2021.

Kraken Investment Case Study

19

CONCLUSION

Despite the debates about who will win the battle, it is too soon to conclude which is the asset of

the future. What is more important is to look at the future of cryptocurrency as a whole.

Investment-wise, within the next five years, Bitcoin will be more stable and Ethereum may have

more significant growths. After a crash course in digital assets, we are excited about where we

will “boldly go” in the future.

Kraken Investment Case Study

20

APPENDICES

Appendix A – Appreciation Rate for Probability Pricing Model

Bitcoin

Date Price % Change Nov 2012 $12.25 June 2013 $94.26 669.47% Dec 2013 $764.27 710.81% June 2014 $620.34 -18.83% Dec 2014 $315.46 -49.15% June 2015 $263.33 -16.53% Dec 2015 $429.91 63.26% Jul 2016 $652.14 51.69% Oct 2016 $618.00 -5.24%

Geometric Mean: 126.5% a year

Ether

Date Price % Change Jul 2015 $1.36

Aug 2015 $0.67 -50.74% Sep 2015 $0.97 44.78% Oct 2015 $0.87 -10.31% Nov 2015 $0.94 8.05% Dec 2015 $2.39 154.26% Jan 2016 $6.40 167.78% Feb 2016 $11.80 84.38% Mar 2016 $8.21 -30.42% Apr 2016 $13.20 60.78% May 2016 $12.50 -5.30% Jun 2016 $12.19 -2.48% Jul 2016 $11.34 -6.97%

Aug 2016 $13.21 16.49% Sep 2016 $11.80 -10.67%

Geometric Mean: 200.25% a year

Kraken Investment Case Study

21

Appendix B – Depreciation Rate for Probability Pricing Model

Bitcoin (XBT) Date Major Decreases Rate Days

06/08/2011 $32 11/18/2011 $2 -92.81% 163 04/08/2013 $238 07/03/2013 $80 -66.39% 86 12/03/2013 $1,151 12/20/2013 $613 -46.74% 17 01/04/2014 $896 02/04/2014 $528 -41.07% 31 03/03/2014 $678 04/12/2014 $405 -40.27% 40 06/02/2014 $674 01/17/2015 $211 -68.69% 229 03/09/2014 $294 04/13/2014 $216 -26.53% 35 07/11/2015 $309 08/23/2015 $213 -31.07% 43 11/02/2015 $409 11/10/2015 $310 -24.21% 8 12/14/2015 $459 02/04/2016 $386 -15.90% 52 06/15/2016 $762 08/01/2016 $515 -32.41% 47

Weighted Average: -29.16% a year

Kraken Investment Case Study

22

Appendix B – Depreciation Rate for Probability Pricing Model

Ether (ETH) Date Major Decreases Rate Days

02/12/2016 $5.87 2/18/2016 $4.04 -31.18% 6 3/5/2016 $10.95 3/8/2016 $9.59 -12.42% 3 3/16/16 $14.15

3/18/2016 $10.23 -27.70% 2 3/23/2016 $11.84 3/27/2016 $10.71 -9.54% 4 3/31/2016 $11.80 4/13/2016 $7.83 -33.64% 13 4/17/2016 $9.24 4/26/2016 $7.38 -20.13% 9 5/20/2016 $14.31 5/28/2016 $11.36 -20.61% 8 6/16/2016 $19.56 6/20/2016 $11.74 -39.98% 4 6/25/2016 $14.30 7/7/2016 $10.07 -29.58% 12

7/23/2016 $14.47 8/3/2016 $9.61 -33.59% 11

8/10/2016 $12.22 8/19/2016 $10.74 -12.11% 9 9/1/2016 $12.16 9/9/2016 $11.57 -4.85% 8

9/21/2016 $13.89 9/25/2016 $12.99 -6.48% 4 10/4/2016 $13.41

10/10/2016 $11.88 -11.41% 6 Weighted Average: -80.42% a year

Kraken Investment Case Study

23

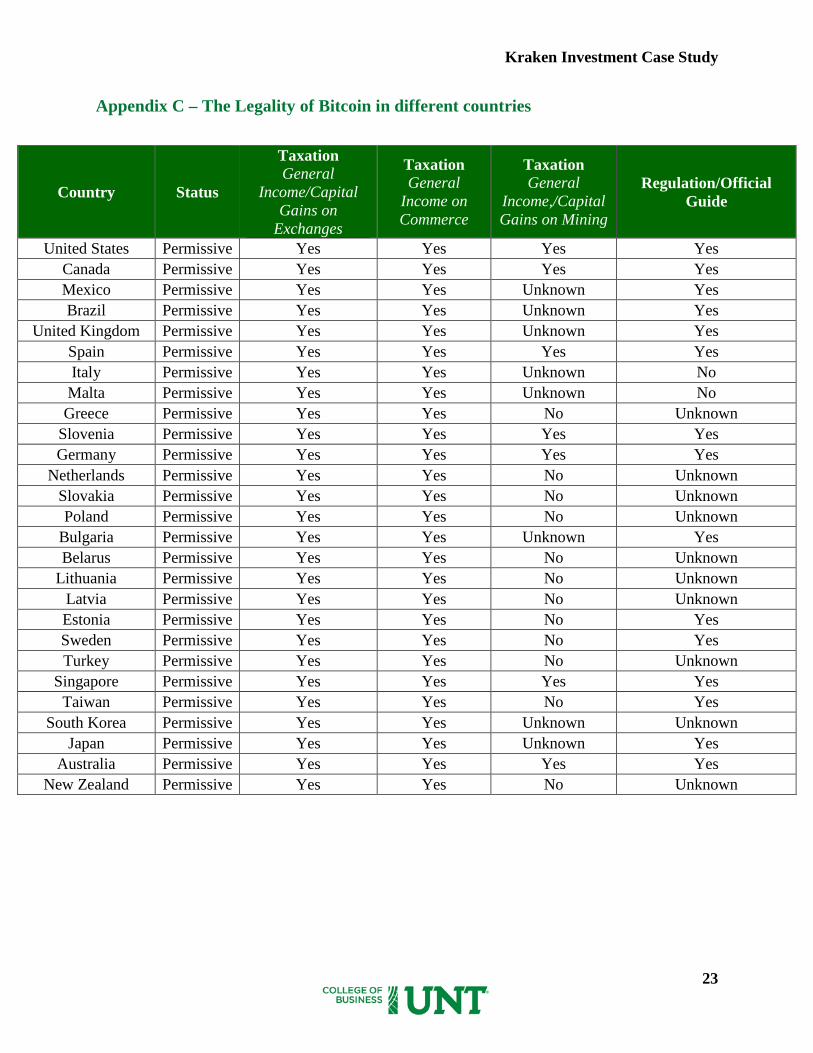

Appendix C – The Legality of Bitcoin in different countries

Country Status

Taxation General

Income/Capital Gains on

Exchanges

Taxation General

Income on Commerce

Taxation General

Income,/Capital Gains on Mining

Regulation/Official Guide

United States Permissive Yes Yes Yes Yes Canada Permissive Yes Yes Yes Yes Mexico Permissive Yes Yes Unknown Yes Brazil Permissive Yes Yes Unknown Yes

United Kingdom Permissive Yes Yes Unknown Yes Spain Permissive Yes Yes Yes Yes Italy Permissive Yes Yes Unknown No Malta Permissive Yes Yes Unknown No Greece Permissive Yes Yes No Unknown

Slovenia Permissive Yes Yes Yes Yes Germany Permissive Yes Yes Yes Yes

Netherlands Permissive Yes Yes No Unknown Slovakia Permissive Yes Yes No Unknown Poland Permissive Yes Yes No Unknown

Bulgaria Permissive Yes Yes Unknown Yes Belarus Permissive Yes Yes No Unknown

Lithuania Permissive Yes Yes No Unknown Latvia Permissive Yes Yes No Unknown Estonia Permissive Yes Yes No Yes Sweden Permissive Yes Yes No Yes Turkey Permissive Yes Yes No Unknown

Singapore Permissive Yes Yes Yes Yes Taiwan Permissive Yes Yes No Yes

South Korea Permissive Yes Yes Unknown Unknown Japan Permissive Yes Yes Unknown Yes

Australia Permissive Yes Yes Yes Yes New Zealand Permissive Yes Yes No Unknown

Kraken Investment Case Study

24

Appendix C – The Legality of Bitcoin in different countries

(Source: bitlegal.io)

Countries banned Bitcoin or other digital currencies: Russia, Iceland, Dominican

Republic, Ecuador, and Bolivia.

Countries that still debate about the legality of Bitcoin: China, Vietnam, Thailand,

India, Jordan, and Kazakhstan.

Country Status

Taxation General

Income/Capital Gains on

Exchanges

Taxation General

Income on Commerce

Taxation General

Income,/Capital Gains on Mining

Regulation/Official Guide

Argentina Permissive Unknown Unknown Unknown Unknown Columbia Permissive Unknown Unknown Unknown Unknown

France Permissive Unknown Unknown Unknown Yes Portugal Permissive Unknown Unknown Unknown Unknown

Luxembourg Permissive Unknown Unknown Unknown Yes Austria Permissive Unknown Unknown Unknown Unknown Croatia Permissive Unknown Unknown Unknown Unknown

Hungary Permissive Unknown Unknown Unknown Unknown Belgium Permissive Unknown Unknown Unknown Unknown

Czech Republic Permissive Unknown Unknown Unknown Unknown Ukraine Permissive Unknown Unknown Unknown Yes Israel Permissive Unknown Unknown Unknown Unknown

Lebanon Permissive Unknown Unknown Unknown Unknown Iran Permissive Unknown Unknown Unknown Unknown

South Africa Permissive Unknown Unknown Unknown No Indonesia Permissive Unknown Unknown Unknown Yes

Philippines Permissive Unknown Unknown Unknown Unknown Switzerland Permissive No Yes No Yes

Liechtenstein Permissive No Yes No No Denmark Permissive No No No No Finland Permissive No No Yes No Norway Permissive No No No Yes Cyprus Permissive No Yes No Unknown

Malaysia Permissive No Yes No Unknown Hong Kong Permissive No Yes No Yes

Kraken Investment Case Study

25

REFERENCE

Brown, C. (2016). How Companies Are Using Ethereum as an Advanced Version of Bitcoin.

Retrieved from https://due.com/blog/ethereum-advanced-version-bitcoin/

Demos, T. (2016). J.P. Morgan Has a New Twist on Blockchain. Retrieved from

http://www.wsj.com/articles/j-p-morgan-has-a-new-twist-on-blockchain-1475537138

Maras, E. (2016) Winklevoss Brothers: Bitcoin Will Disrupt Gold As Crypto Holds The Future.

Retrieved from https://www.cryptocoinsnews.com/winklevoss-brothers-bitcoin-will-

disrupt-gold-as-crypto-holds-the-future/

Nakamura, Y. & Chen, L. U. (2016). Bitcoin Plunges, Rebounds After Hackers Steal $65 Million.

Bloomberg. Retrieved from https://www.bloomberg.com/news/articles/2016-08-

03/bitcoin-plunges-after-hackers-breach-h-k-exchange-steal-coins

Popper, N. (2016). A Hacking of More Than $50 Million Dashes Hopes in the World of Virtual

Currency. Retrieved from

http://www.nytimes.com/2016/06/18/business/dealbook/hacker-may-have-removed-

more-than-50-million-from-experimental-cybercurrency-project.html?_r=0

Popper, N. (2016) How China Took Center Stage in Bitcoin’s Civil War. Retrieved from

http://www.nytimes.com/2016/07/03/business/dealbook/bitcoin-china.html

Price, R. (2016). Digital currency Ethereum is cratering because of a $50 million hack. Retrieved

from http://www.businessinsider.com/dao-hacked-ethereum-crashing-in-value-tens-of-

millions-allegedly-stolen-2016-6

Kraken Investment Case Study

26

Seaman, D. (2016). Ethereum: Here Come The Big Banks. Retrieved from

http://www.huffingtonpost.com/david-seaman/ethereum-here-come-the-

bi_b_11439206.html

Tepper, F. (2016). Hacked Bitcoin exchange Bitfinex will reduce balances by 36% to distribute

losses amongst all users. Retrieved from https://techcrunch.com/2016/08/08/hacked-

bitcoin-exchange-bitfinex-will-reduce-balances-by-36-to-distribute-losses-amongst-all-

users

Quenston, A. (2016). The Biggest Bitcoin Hacks and Thefts of All Time. Retrieved from

https://hacked.com/biggest-bitcoin-hacks-thefts-time/