Embed Size (px)

Citation preview

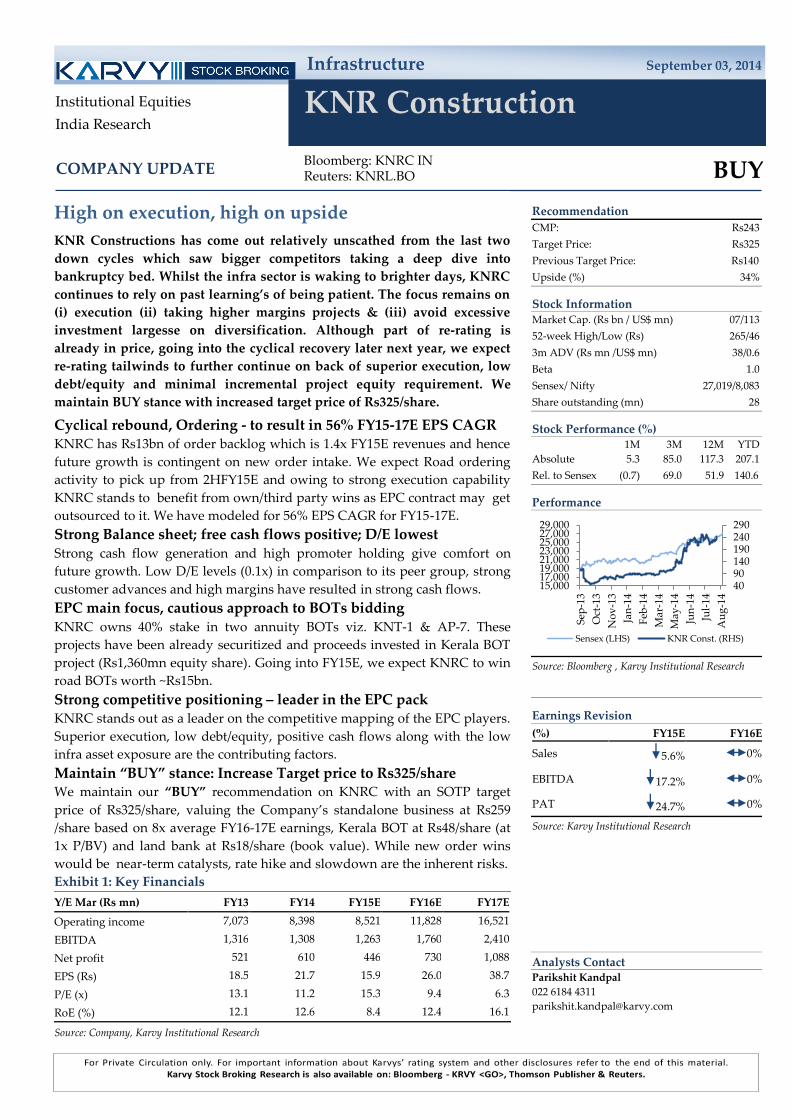

Infrastructure September 03, 2014

KNR Construction

Bloomberg: KNRC IN Reuters: KNRL.BO

BUY

Institutional Equities

India Research

COMPANY UPDATE

Recommendation

CMP: Rs243

Target Price: Rs325

Previous Target Price: Rs140

Upside (%) 34%

Stock Information Market Cap. (Rs bn / US$ mn) 07/113

52-week High/Low (Rs) 265/46

3m ADV (Rs mn /US$ mn) 38/0.6

Beta 1.0

Sensex/ Nifty 27,019/8,083

Share outstanding (mn) 28

Stock Performance (%) 1M 3M 12M YTD

Absolute 5.3 85.0 117.3 207.1

Rel. to Sensex (0.7) 69.0 51.9 140.6

Performance

Source: Bloomberg , Karvy Institutional Research

Click here to enter text.

Earnings Revision

(%) FY15E FY16E

Sales 5.6% 0%

EBITDA 17.2% 0%

PAT 24.7% 0%

Source: Karvy Institutional Research

Analysts Contact Parikshit Kandpal

022 6184 4311

40 90 140 190 240 290

15,000 17,000 19,000 21,000 23,000 25,000 27,000 29,000

Sep

-13

Oct

-13

No

v-1

3

Jan

-14

Feb

-14

Mar

-14

May

-14

Jun

-14

Jul-

14

Au

g-1

4

Sensex (LHS) KNR Const. (RHS)

High on execution, high on upside

KNR Constructions has come out relatively unscathed from the last two

down cycles which saw bigger competitors taking a deep dive into

bankruptcy bed. Whilst the infra sector is waking to brighter days, KNRC

continues to rely on past learning’s of being patient. The focus remains on

(i) execution (ii) taking higher margins projects & (iii) avoid excessive

investment largesse on diversification. Although part of re-rating is

already in price, going into the cyclical recovery later next year, we expect

re-rating tailwinds to further continue on back of superior execution, low

debt/equity and minimal incremental project equity requirement. We

maintain BUY stance with increased target price of Rs325/share.

Cyclical rebound, Ordering - to result in 56% FY15-17E EPS CAGR KNRC has Rs13bn of order backlog which is 1.4x FY15E revenues and hence

future growth is contingent on new order intake. We expect Road ordering

activity to pick up from 2HFY15E and owing to strong execution capability

KNRC stands to benefit from own/third party wins as EPC contract may get

outsourced to it. We have modeled for 56% EPS CAGR for FY15-17E.

Strong Balance sheet; free cash flows positive; D/E lowest Strong cash flow generation and high promoter holding give comfort on

future growth. Low D/E levels (0.1x) in comparison to its peer group, strong

customer advances and high margins have resulted in strong cash flows.

EPC main focus, cautious approach to BOTs bidding KNRC owns 40% stake in two annuity BOTs viz. KNT-1 & AP-7. These

projects have been already securitized and proceeds invested in Kerala BOT

project (Rs1,360mn equity share). Going into FY15E, we expect KNRC to win

road BOTs worth ~Rs15bn.

Strong competitive positioning – leader in the EPC pack KNRC stands out as a leader on the competitive mapping of the EPC players.

Superior execution, low debt/equity, positive cash flows along with the low

infra asset exposure are the contributing factors.

Maintain “BUY” stance: Increase Target price to Rs325/share We maintain our “BUY” recommendation on KNRC with an SOTP target

price of Rs325/share, valuing the Company’s standalone business at Rs259

/share based on 8x average FY16-17E earnings, Kerala BOT at Rs48/share (at

1x P/BV) and land bank at Rs18/share (book value). While new order wins

would be near-term catalysts, rate hike and slowdown are the inherent risks.

Exhibit 1: Key Financials

Y/E Mar (Rs mn) FY13 FY14 FY15E FY16E FY17E

Operating income 7,073 8,398 8,521 11,828 16,521

EBITDA 1,316 1,308 1,263 1,760 2,410

Net profit 521 610 446 730 1,088

EPS (Rs) 18.5 21.7 15.9 26.0 38.7

P/E (x) 13.1 11.2 15.3 9.4 6.3

RoE (%) 12.1 12.6 8.4 12.4 16.1

Source: Company, Karvy Institutional Research

2

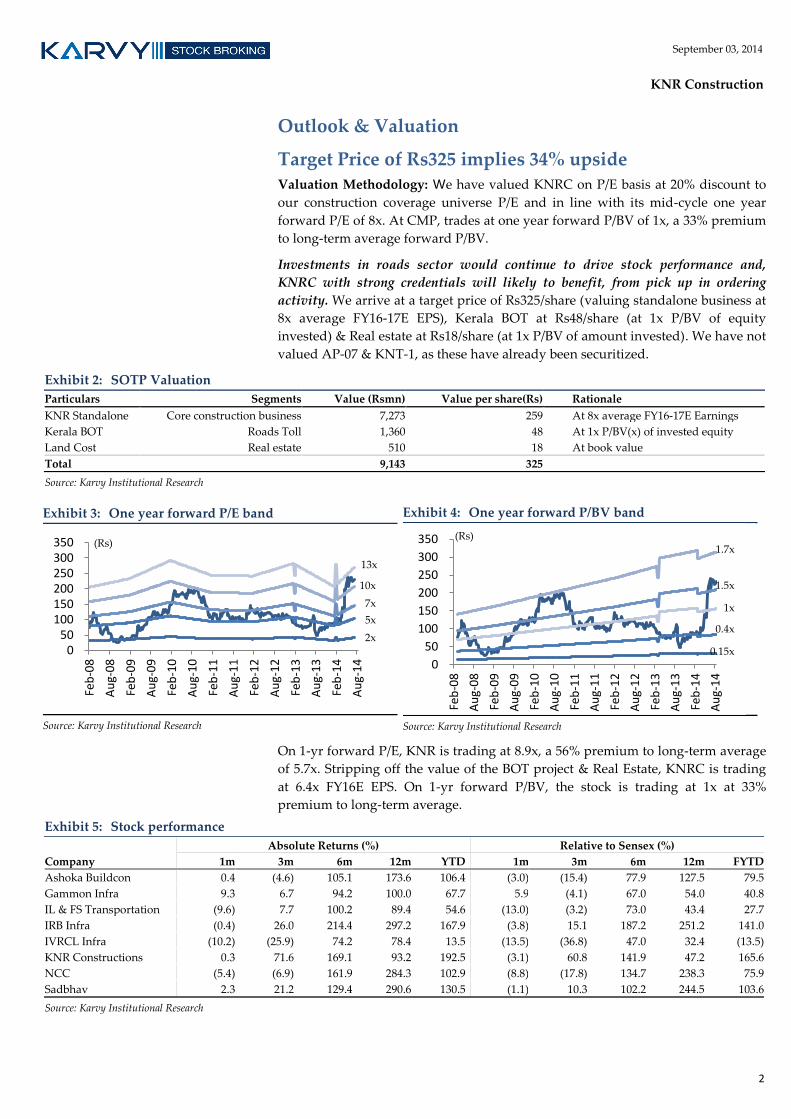

September 03, 2014

KNR Construction

Outlook & Valuation

Target Price of Rs325 implies 34% upside Valuation Methodology: We have valued KNRC on P/E basis at 20% discount to

our construction coverage universe P/E and in line with its mid-cycle one year

forward P/E of 8x. At CMP, trades at one year forward P/BV of 1x, a 33% premium

to long-term average forward P/BV.

Investments in roads sector would continue to drive stock performance and,

KNRC with strong credentials will likely to benefit, from pick up in ordering

activity. We arrive at a target price of Rs325/share (valuing standalone business at

8x average FY16-17E EPS), Kerala BOT at Rs48/share (at 1x P/BV of equity

invested) & Real estate at Rs18/share (at 1x P/BV of amount invested). We have not

valued AP-07 & KNT-1, as these have already been securitized.

Exhibit 2: SOTP Valuation

Particulars Segments Value (Rsmn) Value per share(Rs) Rationale

KNR Standalone Core construction business 7,273 259 At 8x average FY16-17E Earnings

Kerala BOT Roads Toll 1,360 48 At 1x P/BV(x) of invested equity

Land Cost Real estate 510 18 At book value

Total 9,143 325

Source: Karvy Institutional Research

Exhibit 3: One year forward P/E band

Source: Karvy Institutional Research

Exhibit 4: One year forward P/BV band

Source: Karvy Institutional Research

On 1-yr forward P/E, KNR is trading at 8.9x, a 56% premium to long-term average

of 5.7x. Stripping off the value of the BOT project & Real Estate, KNRC is trading

at 6.4x FY16E EPS. On 1-yr forward P/BV, the stock is trading at 1x at 33%

premium to long-term average.

Exhibit 5: Stock performance

Absolute Returns (%) Relative to Sensex (%)

Company 1m 3m 6m 12m YTD 1m 3m 6m 12m FYTD

Ashoka Buildcon 0.4 (4.6) 105.1 173.6 106.4 (3.0) (15.4) 77.9 127.5 79.5

Gammon Infra 9.3 6.7 94.2 100.0 67.7 5.9 (4.1) 67.0 54.0 40.8

IL & FS Transportation (9.6) 7.7 100.2 89.4 54.6 (13.0) (3.2) 73.0 43.4 27.7

IRB Infra (0.4) 26.0 214.4 297.2 167.9 (3.8) 15.1 187.2 251.2 141.0

IVRCL Infra (10.2) (25.9) 74.2 78.4 13.5 (13.5) (36.8) 47.0 32.4 (13.5)

KNR Constructions 0.3 71.6 169.1 93.2 192.5 (3.1) 60.8 141.9 47.2 165.6

NCC (5.4) (6.9) 161.9 284.3 102.9 (8.8) (17.8) 134.7 238.3 75.9

Sadbhav 2.3 21.2 129.4 290.6 130.5 (1.1) 10.3 102.2 244.5 103.6

Source: Karvy Institutional Research

0 50

100 150 200 250 300 350

Feb

-08

Au

g-0

8

Feb

-09

Au

g-0

9

Feb

-10

Au

g-1

0

Feb

-11

Au

g-1

1

Feb

-12

Au

g-1

2

Feb

-13

Au

g-1

3

Feb

-14

Au

g-1

4

(Rs)

2x

5x

7x

10x

13x

0

50

100

150

200

250

300

350

Feb

-08

Au

g-0

8

Feb

-09

Au

g-0

9

Feb

-10

Au

g-1

0

Feb

-11

Au

g-1

1

Feb

-12

Au

g-1

2

Feb

-13

Au

g-1

3

Feb

-14

Au

g-1

4

(Rs)

0.15x

0.4x

1x

1.5x

1.7x

3

September 03, 2014

KNR Construction

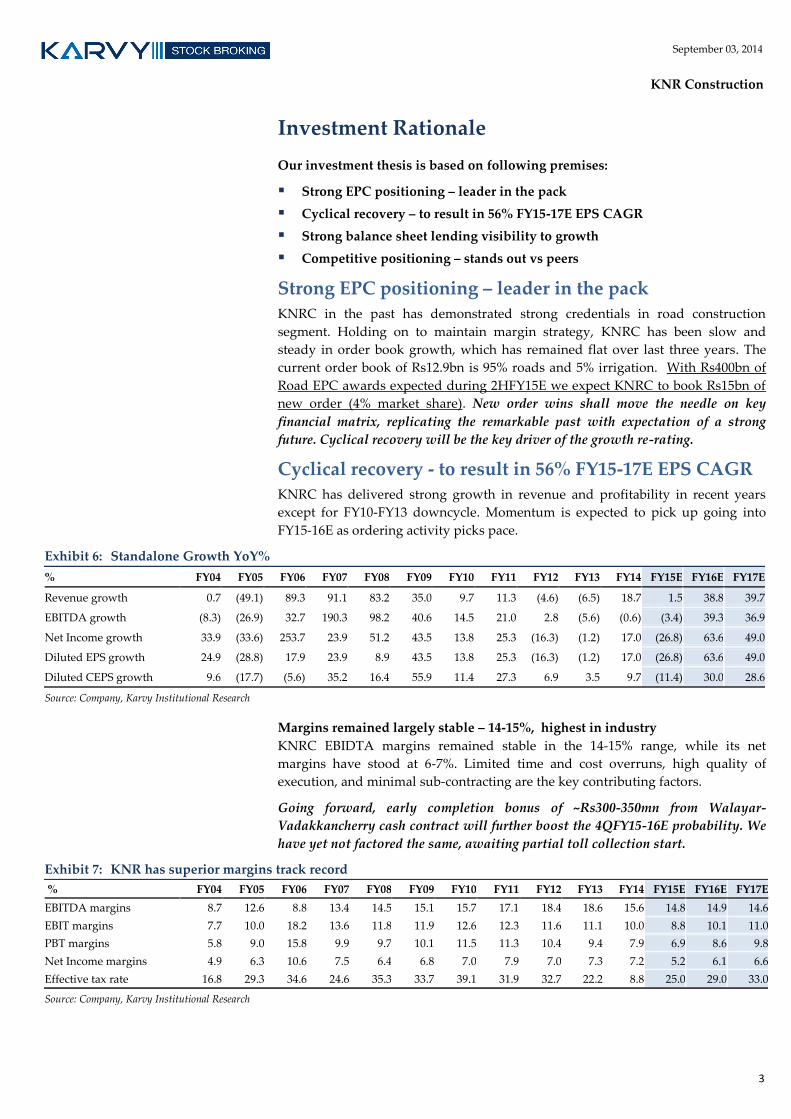

Investment Rationale

Our investment thesis is based on following premises:

Strong EPC positioning – leader in the pack

Cyclical recovery – to result in 56% FY15-17E EPS CAGR

Strong balance sheet lending visibility to growth

Competitive positioning – stands out vs peers

Strong EPC positioning – leader in the pack KNRC in the past has demonstrated strong credentials in road construction

segment. Holding on to maintain margin strategy, KNRC has been slow and

steady in order book growth, which has remained flat over last three years. The

current order book of Rs12.9bn is 95% roads and 5% irrigation. With Rs400bn of

Road EPC awards expected during 2HFY15E we expect KNRC to book Rs15bn of

new order (4% market share). New order wins shall move the needle on key

financial matrix, replicating the remarkable past with expectation of a strong

future. Cyclical recovery will be the key driver of the growth re-rating.

Cyclical recovery - to result in 56% FY15-17E EPS CAGR KNRC has delivered strong growth in revenue and profitability in recent years

except for FY10-FY13 downcycle. Momentum is expected to pick up going into

FY15-16E as ordering activity picks pace.

Exhibit 6: Standalone Growth YoY%

% FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Revenue growth 0.7 (49.1) 89.3 91.1 83.2 35.0 9.7 11.3 (4.6) (6.5) 18.7 1.5 38.8 39.7

EBITDA growth (8.3) (26.9) 32.7 190.3 98.2 40.6 14.5 21.0 2.8 (5.6) (0.6) (3.4) 39.3 36.9

Net Income growth 33.9 (33.6) 253.7 23.9 51.2 43.5 13.8 25.3 (16.3) (1.2) 17.0 (26.8) 63.6 49.0

Diluted EPS growth 24.9 (28.8) 17.9 23.9 8.9 43.5 13.8 25.3 (16.3) (1.2) 17.0 (26.8) 63.6 49.0

Diluted CEPS growth 9.6 (17.7) (5.6) 35.2 16.4 55.9 11.4 27.3 6.9 3.5 9.7 (11.4) 30.0 28.6

Source: Company, Karvy Institutional Research

Margins remained largely stable – 14-15%, highest in industry

KNRC EBIDTA margins remained stable in the 14-15% range, while its net

margins have stood at 6-7%. Limited time and cost overruns, high quality of

execution, and minimal sub-contracting are the key contributing factors.

Going forward, early completion bonus of ~Rs300-350mn from Walayar-

Vadakkancherry cash contract will further boost the 4QFY15-16E probability. We

have yet not factored the same, awaiting partial toll collection start.

Exhibit 7: KNR has superior margins track record

% FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

EBITDA margins 8.7 12.6 8.8 13.4 14.5 15.1 15.7 17.1 18.4 18.6 15.6 14.8 14.9 14.6

EBIT margins 7.7 10.0 18.2 13.6 11.8 11.9 12.6 12.3 11.6 11.1 10.0 8.8 10.1 11.0

PBT margins 5.8 9.0 15.8 9.9 9.7 10.1 11.5 11.3 10.4 9.4 7.9 6.9 8.6 9.8

Net Income margins 4.9 6.3 10.6 7.5 6.4 6.8 7.0 7.9 7.0 7.3 7.2 5.2 6.1 6.6

Effective tax rate 16.8 29.3 34.6 24.6 35.3 33.7 39.1 31.9 32.7 22.2 8.8 25.0 29.0 33.0

Source: Company, Karvy Institutional Research

4

September 03, 2014

KNR Construction

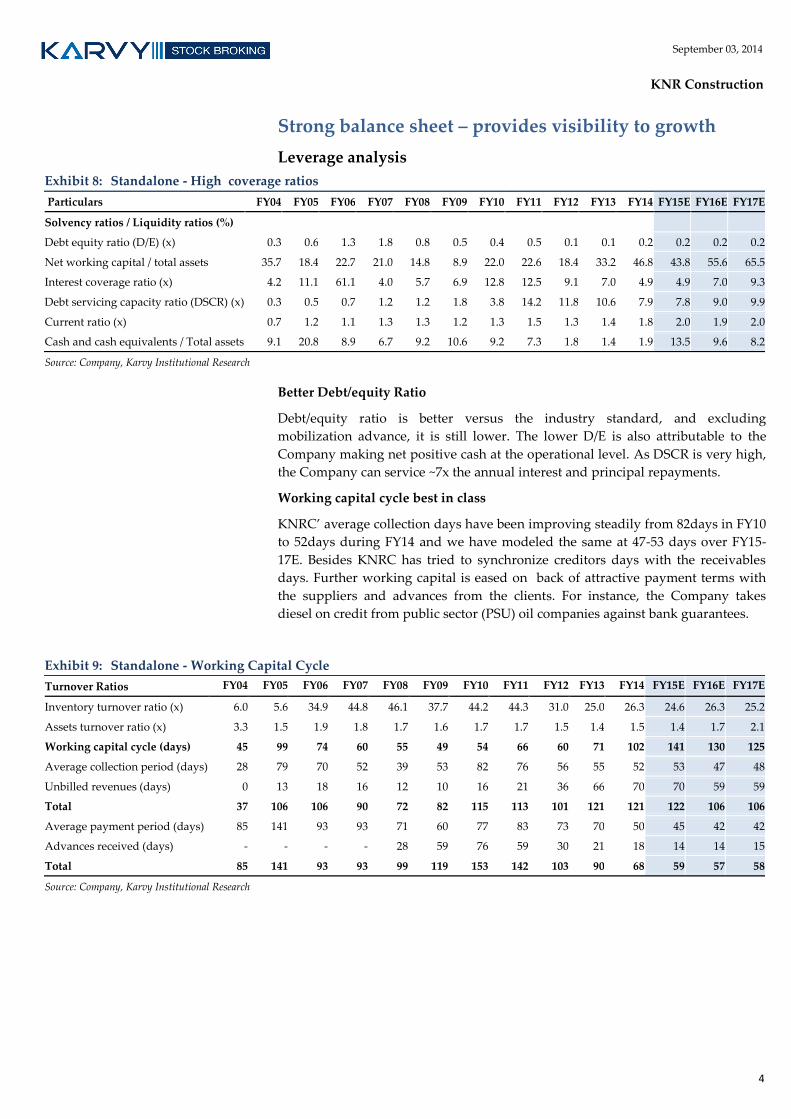

Strong balance sheet – provides visibility to growth

Leverage analysis

Exhibit 8: Standalone - High coverage ratios

Particulars FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Solvency ratios / Liquidity ratios (%)

Debt equity ratio (D/E) (x) 0.3 0.6 1.3 1.8 0.8 0.5 0.4 0.5 0.1 0.1 0.2 0.2 0.2 0.2

Net working capital / total assets 35.7 18.4 22.7 21.0 14.8 8.9 22.0 22.6 18.4 33.2 46.8 43.8 55.6 65.5

Interest coverage ratio (x) 4.2 11.1 61.1 4.0 5.7 6.9 12.8 12.5 9.1 7.0 4.9 4.9 7.0 9.3

Debt servicing capacity ratio (DSCR) (x) 0.3 0.5 0.7 1.2 1.2 1.8 3.8 14.2 11.8 10.6 7.9 7.8 9.0 9.9

Current ratio (x) 0.7 1.2 1.1 1.3 1.3 1.2 1.3 1.5 1.3 1.4 1.8 2.0 1.9 2.0

Cash and cash equivalents / Total assets 9.1 20.8 8.9 6.7 9.2 10.6 9.2 7.3 1.8 1.4 1.9 13.5 9.6 8.2

Source: Company, Karvy Institutional Research

Better Debt/equity Ratio

Debt/equity ratio is better versus the industry standard, and excluding

mobilization advance, it is still lower. The lower D/E is also attributable to the

Company making net positive cash at the operational level. As DSCR is very high,

the Company can service ~7x the annual interest and principal repayments.

Working capital cycle best in class

KNRC’ average collection days have been improving steadily from 82days in FY10

to 52days during FY14 and we have modeled the same at 47-53 days over FY15-

17E. Besides KNRC has tried to synchronize creditors days with the receivables

days. Further working capital is eased on back of attractive payment terms with

the suppliers and advances from the clients. For instance, the Company takes

diesel on credit from public sector (PSU) oil companies against bank guarantees.

Exhibit 9: Standalone - Working Capital Cycle

Turnover Ratios FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Inventory turnover ratio (x) 6.0 5.6 34.9 44.8 46.1 37.7 44.2 44.3 31.0 25.0 26.3 24.6 26.3 25.2

Assets turnover ratio (x) 3.3 1.5 1.9 1.8 1.7 1.6 1.7 1.7 1.5 1.4 1.5 1.4 1.7 2.1

Working capital cycle (days) 45 99 74 60 55 49 54 66 60 71 102 141 130 125

Average collection period (days) 28 79 70 52 39 53 82 76 56 55 52 53 47 48

Unbilled revenues (days) 0 13 18 16 12 10 16 21 36 66 70 70 59 59

Total 37 106 106 90 72 82 115 113 101 121 121 122 106 106

Average payment period (days) 85 141 93 93 71 60 77 83 73 70 50 45 42 42

Advances received (days) - - - - 28 59 76 59 30 21 18 14 14 15

Total 85 141 93 93 99 119 153 142 103 90 68 59 57 58

Source: Company, Karvy Institutional Research

5

September 03, 2014

KNR Construction

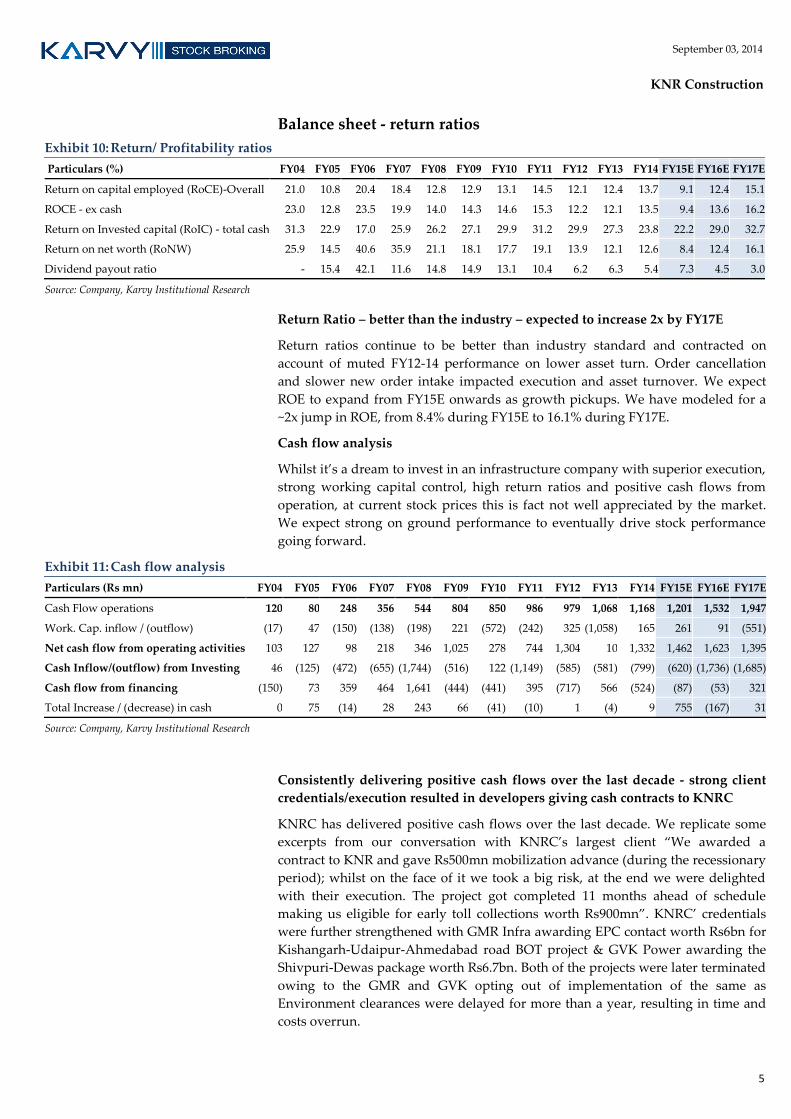

Balance sheet - return ratios

Exhibit 10: Return/ Profitability ratios

Particulars (%) FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Return on capital employed (RoCE)-Overall 21.0 10.8 20.4 18.4 12.8 12.9 13.1 14.5 12.1 12.4 13.7 9.1 12.4 15.1

ROCE - ex cash 23.0 12.8 23.5 19.9 14.0 14.3 14.6 15.3 12.2 12.1 13.5 9.4 13.6 16.2

Return on Invested capital (RoIC) - total cash 31.3 22.9 17.0 25.9 26.2 27.1 29.9 31.2 29.9 27.3 23.8 22.2 29.0 32.7

Return on net worth (RoNW) 25.9 14.5 40.6 35.9 21.1 18.1 17.7 19.1 13.9 12.1 12.6 8.4 12.4 16.1

Dividend payout ratio - 15.4 42.1 11.6 14.8 14.9 13.1 10.4 6.2 6.3 5.4 7.3 4.5 3.0

Source: Company, Karvy Institutional Research

Return Ratio – better than the industry – expected to increase 2x by FY17E

Return ratios continue to be better than industry standard and contracted on

account of muted FY12-14 performance on lower asset turn. Order cancellation

and slower new order intake impacted execution and asset turnover. We expect

ROE to expand from FY15E onwards as growth pickups. We have modeled for a

~2x jump in ROE, from 8.4% during FY15E to 16.1% during FY17E.

Cash flow analysis

Whilst it’s a dream to invest in an infrastructure company with superior execution,

strong working capital control, high return ratios and positive cash flows from

operation, at current stock prices this is fact not well appreciated by the market.

We expect strong on ground performance to eventually drive stock performance

going forward.

Exhibit 11: Cash flow analysis

Particulars (Rs mn) FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Cash Flow operations 120 80 248 356 544 804 850 986 979 1,068 1,168 1,201 1,532 1,947

Work. Cap. inflow / (outflow) (17) 47 (150) (138) (198) 221 (572) (242) 325 (1,058) 165 261 91 (551)

Net cash flow from operating activities 103 127 98 218 346 1,025 278 744 1,304 10 1,332 1,462 1,623 1,395

Cash Inflow/(outflow) from Investing 46 (125) (472) (655) (1,744) (516) 122 (1,149) (585) (581) (799) (620) (1,736) (1,685)

Cash flow from financing (150) 73 359 464 1,641 (444) (441) 395 (717) 566 (524) (87) (53) 321

Total Increase / (decrease) in cash 0 75 (14) 28 243 66 (41) (10) 1 (4) 9 755 (167) 31

Source: Company, Karvy Institutional Research

Consistently delivering positive cash flows over the last decade - strong client

credentials/execution resulted in developers giving cash contracts to KNRC

KNRC has delivered positive cash flows over the last decade. We replicate some

excerpts from our conversation with KNRC’s largest client “We awarded a

contract to KNR and gave Rs500mn mobilization advance (during the recessionary

period); whilst on the face of it we took a big risk, at the end we were delighted

with their execution. The project got completed 11 months ahead of schedule

making us eligible for early toll collections worth Rs900mn”. KNRC’ credentials

were further strengthened with GMR Infra awarding EPC contact worth Rs6bn for

Kishangarh-Udaipur-Ahmedabad road BOT project & GVK Power awarding the

Shivpuri-Dewas package worth Rs6.7bn. Both of the projects were later terminated

owing to the GMR and GVK opting out of implementation of the same as

Environment clearances were delayed for more than a year, resulting in time and

costs overrun.

6

September 03, 2014

KNR Construction

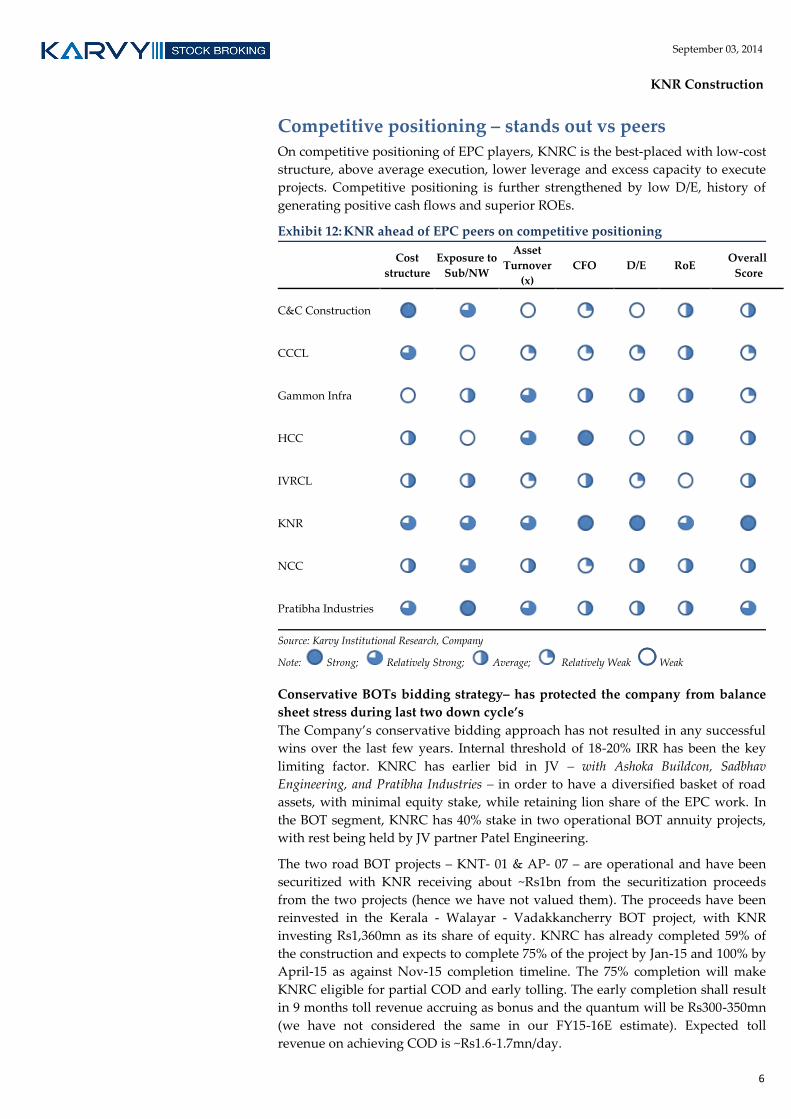

Competitive positioning – stands out vs peers

On competitive positioning of EPC players, KNRC is the best-placed with low-cost

structure, above average execution, lower leverage and excess capacity to execute

projects. Competitive positioning is further strengthened by low D/E, history of

generating positive cash flows and superior ROEs.

Exhibit 12: KNR ahead of EPC peers on competitive positioning

Cost

structure

Exposure to

Sub/NW

Asset

Turnover

(x)

CFO D/E RoE Overall

Score

C&C Construction

CCCL

Gammon Infra

HCC

IVRCL

KNR

NCC

Pratibha Industries

Source: Karvy Institutional Research, Company

Note: Strong; Relatively Strong; Average; Relatively Weak Weak

Conservative BOTs bidding strategy– has protected the company from balance

sheet stress during last two down cycle’s

The Company’s conservative bidding approach has not resulted in any successful

wins over the last few years. Internal threshold of 18-20% IRR has been the key

limiting factor. KNRC has earlier bid in JV – with Ashoka Buildcon, Sadbhav

Engineering, and Pratibha Industries – in order to have a diversified basket of road

assets, with minimal equity stake, while retaining lion share of the EPC work. In

the BOT segment, KNRC has 40% stake in two operational BOT annuity projects,

with rest being held by JV partner Patel Engineering.

The two road BOT projects – KNT- 01 & AP- 07 – are operational and have been

securitized with KNR receiving about ~Rs1bn from the securitization proceeds

from the two projects (hence we have not valued them). The proceeds have been

reinvested in the Kerala - Walayar - Vadakkancherry BOT project, with KNR

investing Rs1,360mn as its share of equity. KNRC has already completed 59% of

the construction and expects to complete 75% of the project by Jan-15 and 100% by

April-15 as against Nov-15 completion timeline. The 75% completion will make

KNRC eligible for partial COD and early tolling. The early completion shall result

in 9 months toll revenue accruing as bonus and the quantum will be Rs300-350mn

(we have not considered the same in our FY15-16E estimate). Expected toll

revenue on achieving COD is ~Rs1.6-1.7mn/day.

7

September 03, 2014

KNR Construction

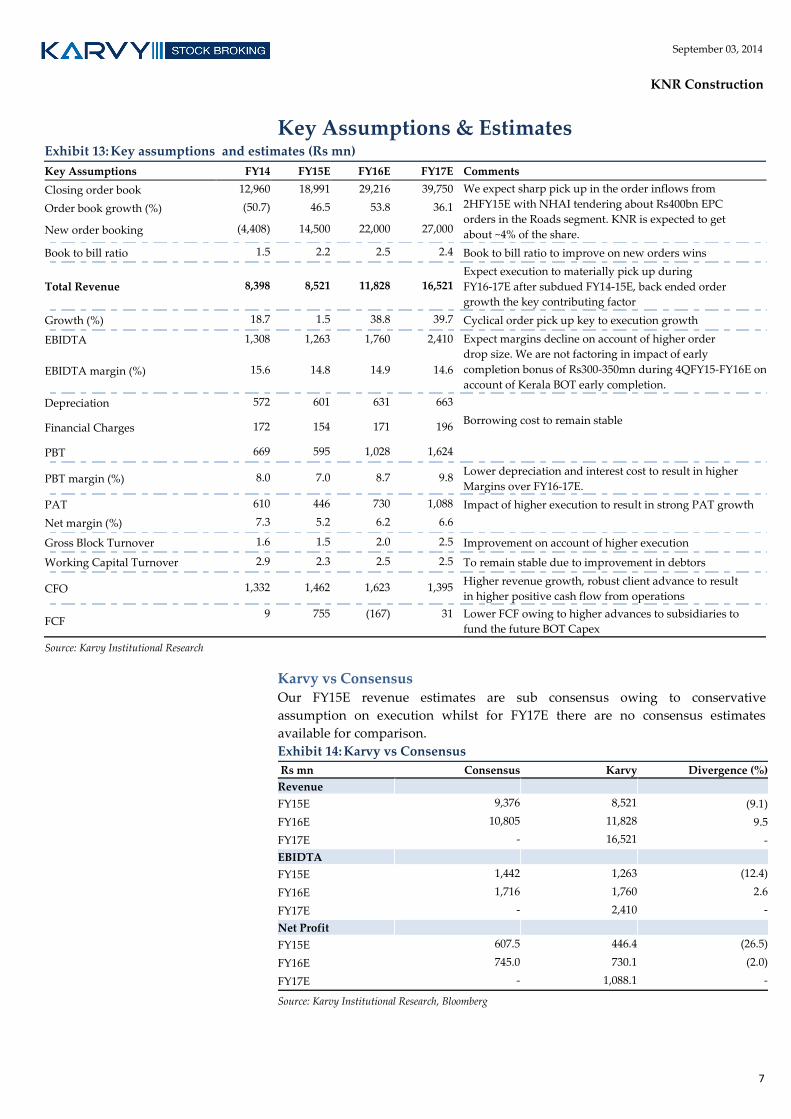

Key Assumptions & Estimates Exhibit 13: Key assumptions and estimates (Rs mn)

Key Assumptions FY14 FY15E FY16E FY17E Comments

Closing order book 12,960 18,991 29,216 39,750 We expect sharp pick up in the order inflows from

2HFY15E with NHAI tendering about Rs400bn EPC

orders in the Roads segment. KNR is expected to get

about ~4% of the share.

Order book growth (%) (50.7) 46.5 53.8 36.1

New order booking (4,408) 14,500 22,000 27,000

Book to bill ratio 1.5 2.2 2.5 2.4 Book to bill ratio to improve on new orders wins

Total Revenue 8,398 8,521 11,828 16,521 Expect execution to materially pick up during

FY16-17E after subdued FY14-15E, back ended order

growth the key contributing factor

Growth (%) 18.7 1.5 38.8 39.7 Cyclical order pick up key to execution growth

EBIDTA 1,308 1,263 1,760 2,410 Expect margins decline on account of higher order

drop size. We are not factoring in impact of early

completion bonus of Rs300-350mn during 4QFY15-FY16E on

account of Kerala BOT early completion. EBIDTA margin (%) 15.6 14.8 14.9 14.6

Depreciation 572 601 631 663

Financial Charges 172 154 171 196 Borrowing cost to remain stable

PBT 669 595 1,028 1,624

PBT margin (%) 8.0 7.0 8.7 9.8 Lower depreciation and interest cost to result in higher

Margins over FY16-17E.

PAT 610 446 730 1,088 Impact of higher execution to result in strong PAT growth

Net margin (%) 7.3 5.2 6.2 6.6

Gross Block Turnover 1.6 1.5 2.0 2.5 Improvement on account of higher execution

Working Capital Turnover 2.9 2.3 2.5 2.5 To remain stable due to improvement in debtors

CFO 1,332 1,462 1,623 1,395 Higher revenue growth, robust client advance to result

in higher positive cash flow from operations

FCF 9 755 (167) 31 Lower FCF owing to higher advances to subsidiaries to

fund the future BOT Capex

Source: Karvy Institutional Research

Karvy vs Consensus Our FY15E revenue estimates are sub consensus owing to conservative

assumption on execution whilst for FY17E there are no consensus estimates

available for comparison.

Exhibit 14: Karvy vs Consensus

Rs mn Consensus Karvy Divergence (%)

Revenue

FY15E 9,376 8,521 (9.1)

FY16E 10,805 11,828 9.5

FY17E - 16,521 -

EBIDTA

FY15E 1,442 1,263 (12.4)

FY16E 1,716 1,760 2.6

FY17E - 2,410 -

Net Profit

FY15E 607.5 446.4 (26.5)

FY16E 745.0 730.1 (2.0)

FY17E - 1,088.1 -

Source: Karvy Institutional Research, Bloomberg

8

September 03, 2014

KNR Construction

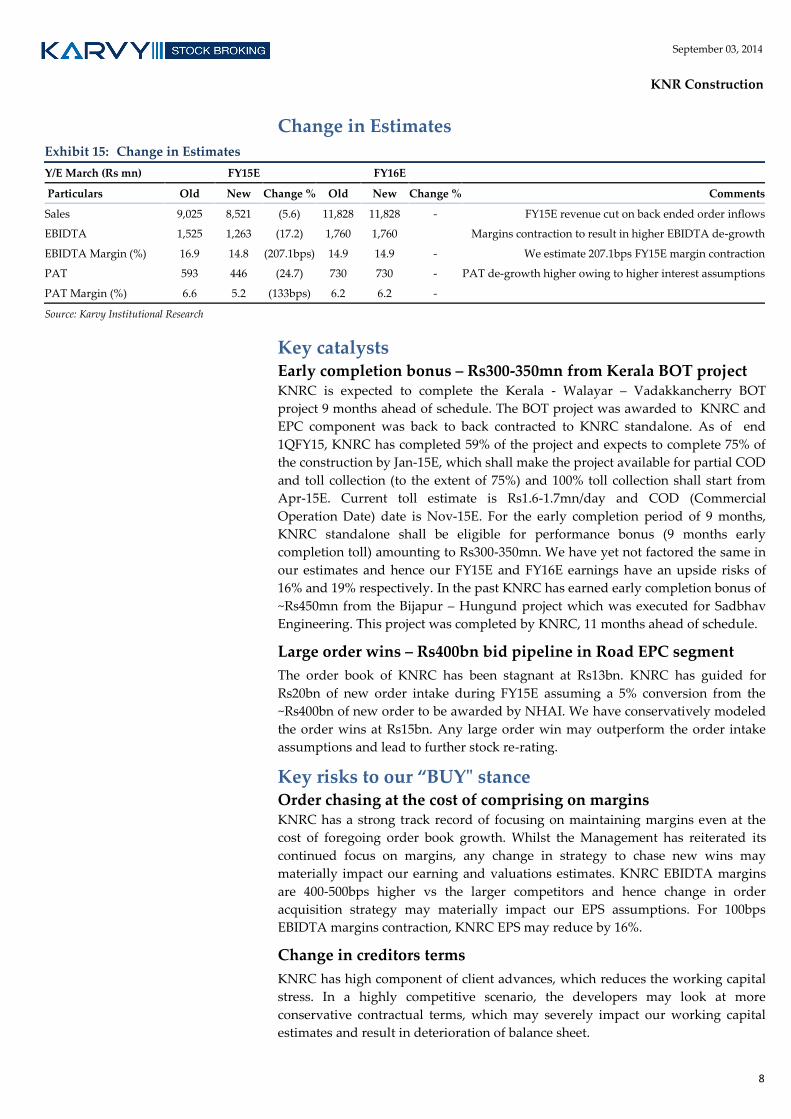

Change in Estimates

Exhibit 15: Change in Estimates

Y/E March (Rs mn)

FY15E FY16E

Particulars Old New Change % Old New Change % Comments

Sales 9,025 8,521 (5.6) 11,828 11,828 - FY15E revenue cut on back ended order inflows

EBIDTA 1,525 1,263 (17.2) 1,760 1,760

Margins contraction to result in higher EBIDTA de-growth

EBIDTA Margin (%) 16.9 14.8 (207.1bps) 14.9 14.9 - We estimate 207.1bps FY15E margin contraction

PAT 593 446 (24.7) 730 730 - PAT de-growth higher owing to higher interest assumptions

PAT Margin (%) 6.6 5.2 (133bps) 6.2 6.2 -

Source: Karvy Institutional Research

Key catalysts Early completion bonus – Rs300-350mn from Kerala BOT project KNRC is expected to complete the Kerala - Walayar – Vadakkancherry BOT

project 9 months ahead of schedule. The BOT project was awarded to KNRC and

EPC component was back to back contracted to KNRC standalone. As of end

1QFY15, KNRC has completed 59% of the project and expects to complete 75% of

the construction by Jan-15E, which shall make the project available for partial COD

and toll collection (to the extent of 75%) and 100% toll collection shall start from

Apr-15E. Current toll estimate is Rs1.6-1.7mn/day and COD (Commercial

Operation Date) date is Nov-15E. For the early completion period of 9 months,

KNRC standalone shall be eligible for performance bonus (9 months early

completion toll) amounting to Rs300-350mn. We have yet not factored the same in

our estimates and hence our FY15E and FY16E earnings have an upside risks of

16% and 19% respectively. In the past KNRC has earned early completion bonus of

~Rs450mn from the Bijapur – Hungund project which was executed for Sadbhav

Engineering. This project was completed by KNRC, 11 months ahead of schedule.

Large order wins – Rs400bn bid pipeline in Road EPC segment

The order book of KNRC has been stagnant at Rs13bn. KNRC has guided for

Rs20bn of new order intake during FY15E assuming a 5% conversion from the

~Rs400bn of new order to be awarded by NHAI. We have conservatively modeled

the order wins at Rs15bn. Any large order win may outperform the order intake

assumptions and lead to further stock re-rating.

Key risks to our “BUY" stance Order chasing at the cost of comprising on margins KNRC has a strong track record of focusing on maintaining margins even at the

cost of foregoing order book growth. Whilst the Management has reiterated its

continued focus on margins, any change in strategy to chase new wins may

materially impact our earning and valuations estimates. KNRC EBIDTA margins

are 400-500bps higher vs the larger competitors and hence change in order

acquisition strategy may materially impact our EPS assumptions. For 100bps

EBIDTA margins contraction, KNRC EPS may reduce by 16%.

Change in creditors terms

KNRC has high component of client advances, which reduces the working capital

stress. In a highly competitive scenario, the developers may look at more

conservative contractual terms, which may severely impact our working capital

estimates and result in deterioration of balance sheet.

9

September 03, 2014

KNR Construction

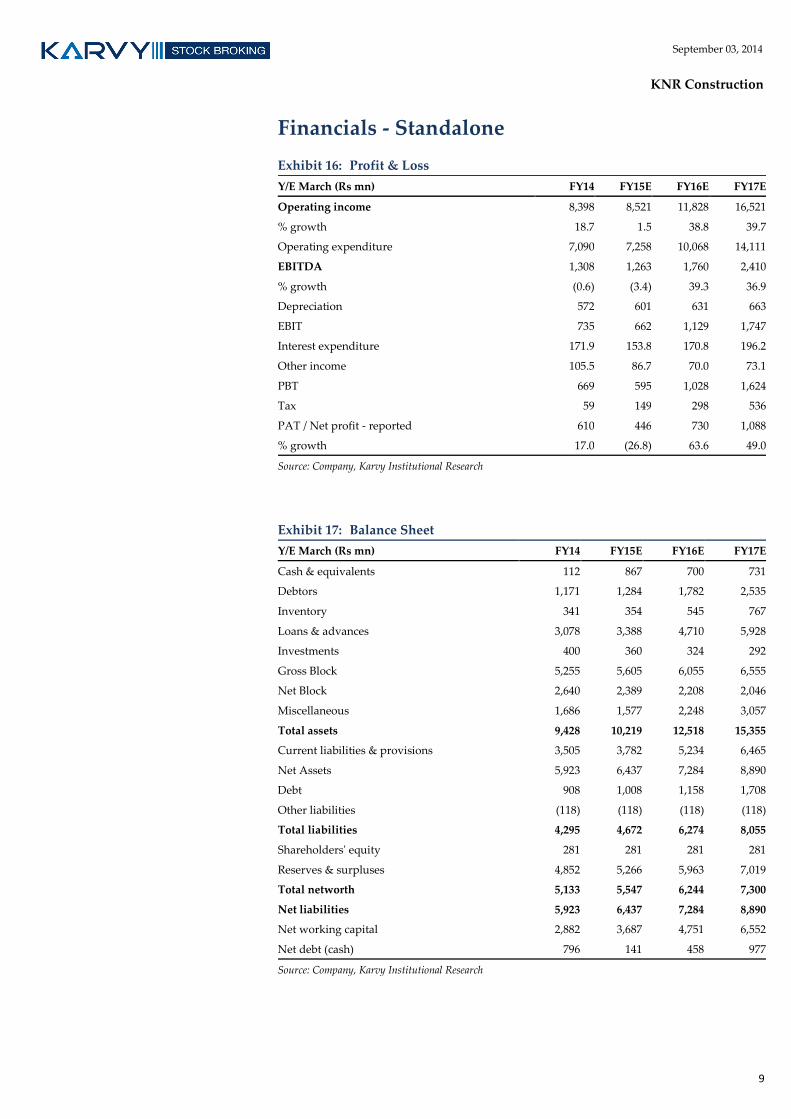

Financials - Standalone

Exhibit 16: Profit & Loss

Y/E March (Rs mn) FY14 FY15E FY16E FY17E

Operating income 8,398 8,521 11,828 16,521

% growth 18.7 1.5 38.8 39.7

Operating expenditure 7,090 7,258 10,068 14,111

EBITDA 1,308 1,263 1,760 2,410

% growth (0.6) (3.4) 39.3 36.9

Depreciation 572 601 631 663

EBIT 735 662 1,129 1,747

Interest expenditure 171.9 153.8 170.8 196.2

Other income 105.5 86.7 70.0 73.1

PBT 669 595 1,028 1,624

Tax 59 149 298 536

PAT / Net profit - reported 610 446 730 1,088

% growth 17.0 (26.8) 63.6 49.0

Source: Company, Karvy Institutional Research

Exhibit 17: Balance Sheet

Y/E March (Rs mn) FY14 FY15E FY16E FY17E

Cash & equivalents 112 867 700 731

Debtors 1,171 1,284 1,782 2,535

Inventory 341 354 545 767

Loans & advances 3,078 3,388 4,710 5,928

Investments 400 360 324 292

Gross Block 5,255 5,605 6,055 6,555

Net Block 2,640 2,389 2,208 2,046

Miscellaneous 1,686 1,577 2,248 3,057

Total assets 9,428 10,219 12,518 15,355

Current liabilities & provisions 3,505 3,782 5,234 6,465

Net Assets 5,923 6,437 7,284 8,890

Debt 908 1,008 1,158 1,708

Other liabilities (118) (118) (118) (118)

Total liabilities 4,295 4,672 6,274 8,055

Shareholders' equity 281 281 281 281

Reserves & surpluses 4,852 5,266 5,963 7,019

Total networth 5,133 5,547 6,244 7,300

Net liabilities 5,923 6,437 7,284 8,890

Net working capital 2,882 3,687 4,751 6,552

Net debt (cash) 796 141 458 977

Source: Company, Karvy Institutional Research

10

September 03, 2014

KNR Construction

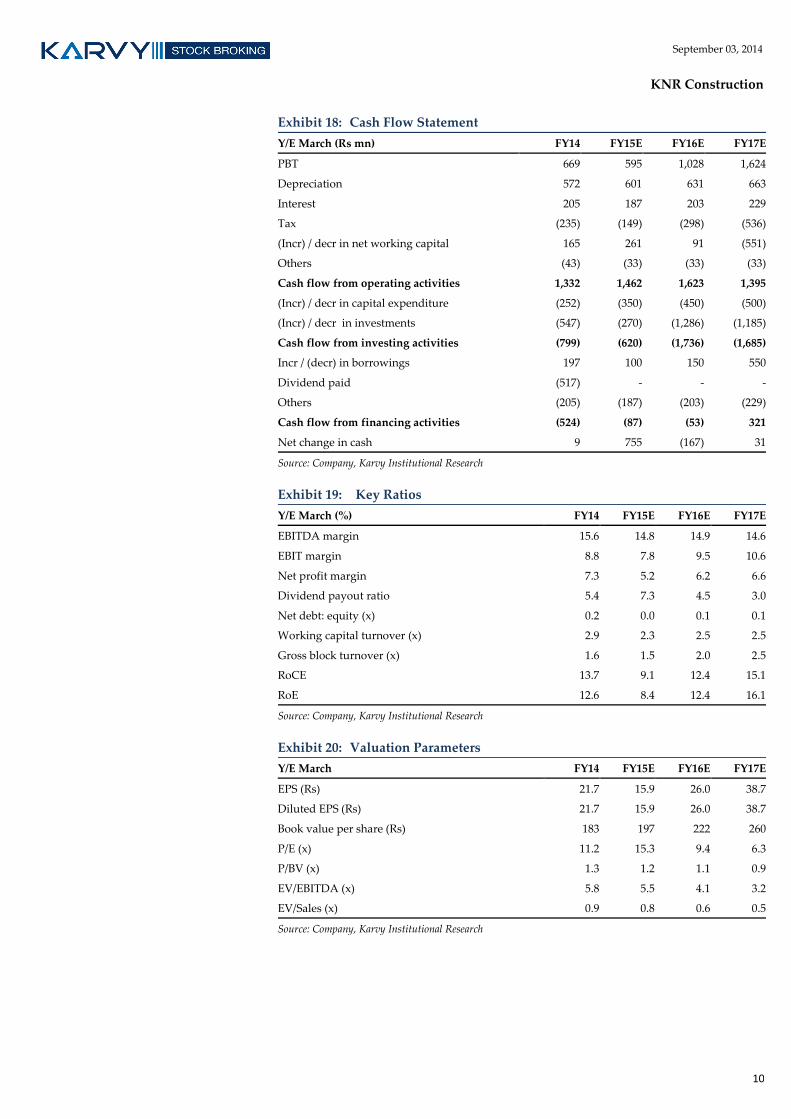

Exhibit 18: Cash Flow Statement

Y/E March (Rs mn) FY14 FY15E FY16E FY17E

PBT 669 595 1,028 1,624

Depreciation 572 601 631 663

Interest 205 187 203 229

Tax (235) (149) (298) (536)

(Incr) / decr in net working capital 165 261 91 (551)

Others (43) (33) (33) (33)

Cash flow from operating activities 1,332 1,462 1,623 1,395

(Incr) / decr in capital expenditure (252) (350) (450) (500)

(Incr) / decr in investments (547) (270) (1,286) (1,185)

Cash flow from investing activities (799) (620) (1,736) (1,685)

Incr / (decr) in borrowings 197 100 150 550

Dividend paid (517) - - -

Others (205) (187) (203) (229)

Cash flow from financing activities (524) (87) (53) 321

Net change in cash 9 755 (167) 31

Source: Company, Karvy Institutional Research

Exhibit 19: Key Ratios

Y/E March (%) FY14 FY15E FY16E FY17E

EBITDA margin 15.6 14.8 14.9 14.6

EBIT margin 8.8 7.8 9.5 10.6

Net profit margin 7.3 5.2 6.2 6.6

Dividend payout ratio 5.4 7.3 4.5 3.0

Net debt: equity (x) 0.2 0.0 0.1 0.1

Working capital turnover (x) 2.9 2.3 2.5 2.5

Gross block turnover (x) 1.6 1.5 2.0 2.5

RoCE 13.7 9.1 12.4 15.1

RoE 12.6 8.4 12.4 16.1

Source: Company, Karvy Institutional Research

Exhibit 20: Valuation Parameters

Y/E March FY14 FY15E FY16E FY17E

EPS (Rs) 21.7 15.9 26.0 38.7

Diluted EPS (Rs) 21.7 15.9 26.0 38.7

Book value per share (Rs) 183 197 222 260

P/E (x) 11.2 15.3 9.4 6.3

P/BV (x) 1.3 1.2 1.1 0.9

EV/EBITDA (x) 5.8 5.5 4.1 3.2

EV/Sales (x) 0.9 0.8 0.6 0.5

Source: Company, Karvy Institutional Research

11

September 03, 2014

KNR Construction

Institutional Equities Team Rahul Sharma

Head – Institutional Equities /

Research / Pharma +91-22 61844310/01 [email protected]

Gurdarshan Singh Kharbanda Head - Sales-Trading +91-22 61844368/69 [email protected]

INSTITUTIONAL RESEARCH

Analysts Industry / Sector Desk Phone Email ID

Mitul Shah Automobiles/Auto Ancillary +91-22 61844312 [email protected]

Parikshit Kandpal Infra / Real Estate / Strategy/Consumer +91-22 61844311 [email protected]

Rajesh Kumar Ravi Cement/ Logistics/ Paints +91-22 61844313 [email protected]

Rupesh Sankhe Power/Capital Goods +91-22 61844315 [email protected]

Asutosh Mishra Banking & Finance +91-22-61844329 [email protected]

Vinesh Vala Research Associate +91 22 61844325 [email protected]

Rajesh Mudaliar Research Associate +91 22 61844322 [email protected]

INSTITUTIONAL SALES

Celine Dsouza Sales +91 22 61844341 [email protected]

Edelbert Dcosta Sales +91 22 61844344 [email protected]

INSTITUTIONAL SALES TRADING & DEALING

Aashish Parekh Institutional Sales/Trading/ Dealing +91-22 61844361 [email protected]

Prashant Oza Institutional Sales/Trading/ Dealing +91-22 61844370 /71 [email protected]

Pratik Sanghvi Institutional Dealing +91-22 61844366 /67 [email protected]

12

September 03, 2014

KNR Construction

For further enquiries please contact:

Tel: +91-22-6184 4300

Disclosures Appendix

Analyst certification

The following analyst(s), who is (are) primarily responsible for this report, certify (ies) that the views expressed herein accurately reflect

his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of his (their) compensation was, is or will be

directly or indirectly related to the specific recommendation(s) or views contained in this research report.

Disclaimer

The information and views presented in this report are prepared by Karvy Stock Broking Limited. The information contained herein is

based on our analysis and upon sources that we consider reliable. We, however, do not vouch for the accuracy or the completeness

thereof. This material is for personal information and we are not responsible for any loss incurred based upon it. The investments

discussed or recommended in this report may not be suitable for all investors. Investors must make their own investment decisions

based on their specific investment objectives and financial position and using such independent advice, as they believe necessary.

While acting upon any information or analysis mentioned in this report, investors may please note that neither Karvy nor Karvy Stock

Broking nor any person connected with any associate companies of Karvy accepts any liability arising from the use of this information

and views mentioned in this document.

The author, directors and other employees of Karvy and its affiliates may hold long or short positions in the above mentioned

companies from time to time. Every employee of Karvy and its associate companies are required to disclose their individual stock

holdings and details of trades, if any, that they undertake. The team rendering corporate analysis and investment recommendations are

restricted in purchasing/selling of shares or other securities till such a time this recommendation has either been displayed or has been

forwarded to clients of Karvy. All employees are further restricted to place orders only through Karvy Stock Broking Ltd. This report is

intended for a restricted audience and we are not soliciting any action based on it. Neither the information nor any opinion expressed

herein constitutes an offer or an invitation to make an offer, to buy or sell any securities, or any options, futures nor other derivatives

related to such securities.

Karvy Stock Broking Limited Institutional Equities

Office No. 701, 7th Floor, Hallmark Business Plaza, Opp.-Gurunanak Hospital, Mumbai 400 051 Regd Off : 46, Road No 4, Street No 1, Banjara Hills, Hyderabad – 500 034.

Karvy Stock Broking Research is also available on: Bloomberg - KRVY <GO>, Thomson Publisher & Reuters.

Stock Ratings Absolute Returns Buy : > 15% Hold : 5 - 15% Sell : < 5%