Embed Size (px)

Citation preview

Our Approach to Finance Home Loans to Low

Income Segment

Tokyo - Oct, 2012

Aadhar Housing

Finance Pvt. Ltd.

(A DHFL Group Company)

About Us

Aadhar is supported by DHFL, DHFL Vysya and

International Finance Corporation (IFC)

DHFL has 27 years of strong expertise in providing housing

loans to low and middle income segments at fair terms.

Aadhar is registered as a Housing Finance Company and

Regulated by the National Housing Bank

2

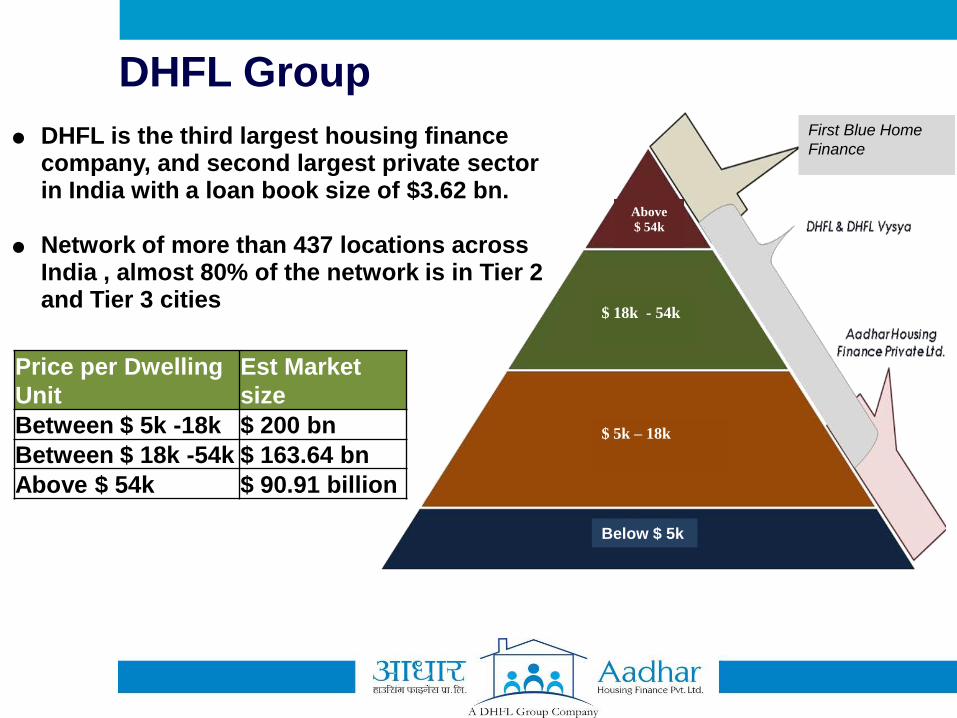

● DHFL is the third largest housing finance company, and second largest private sector in India with a loan book size of $3.62 bn.

● Network of more than 437 locations across

India , almost 80% of the network is in Tier 2 and Tier 3 cities

Price per Dwelling

Unit

Est Market

size

Between $ 5k -18k $ 200 bn

Between $ 18k -54k $ 163.64 bn

Above $ 54k $ 90.91 billion

First Blue Home

Finance

DHFL Group

Above

$ 54k

$ 18k - 54k

$ 5k – 18k

Below $ 5k

Industry

• Estimated housing shortage of 24.7 million units in urban and

rural India.

• Of the total shortage, 98% constitutes demand from low-

income households.

• Total housing loan market in India is estimated at $110 bn.

• Low Mortgage to GDP ratio for India provides huge opportunity

for growth on sustainable basis for years to come

• Low-cost housing units of 200–350 sq ft. priced between

$3,000- 6,000 would be affordable without subsidies to 23–28

million Indian households. Those households already pay

rents comparable to the mortgage EMIs they would pay.

4

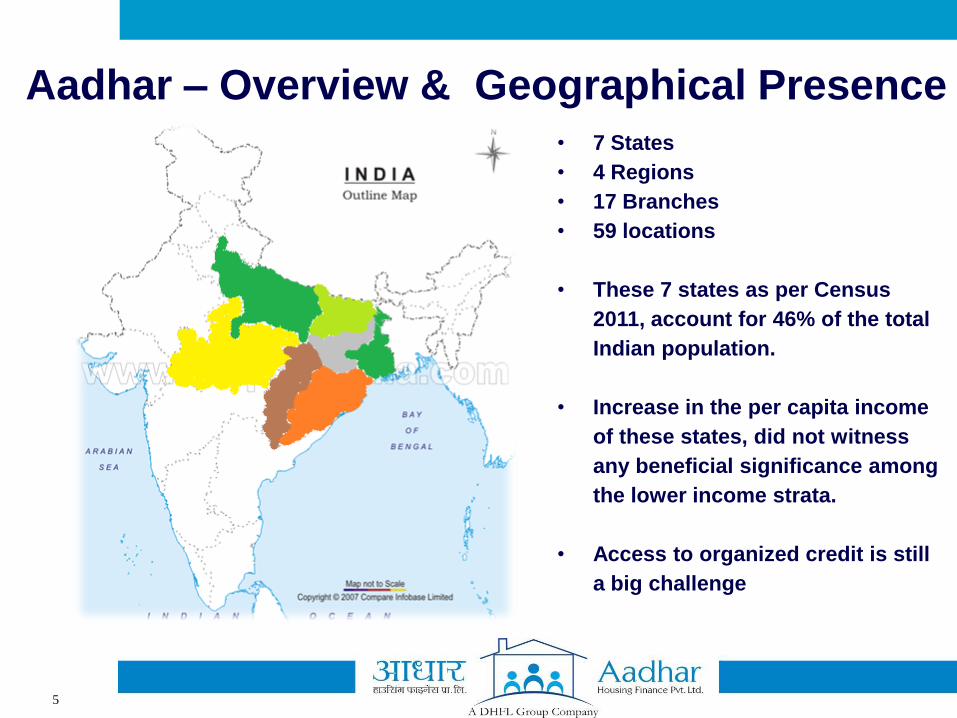

Aadhar – Overview & Geographical Presence

• 7 States

• 4 Regions

• 17 Branches

• 59 locations

• These 7 states as per Census

2011, account for 46% of the total

Indian population.

• Increase in the per capita income

of these states, did not witness

any beneficial significance among

the lower income strata.

• Access to organized credit is still

a big challenge

5

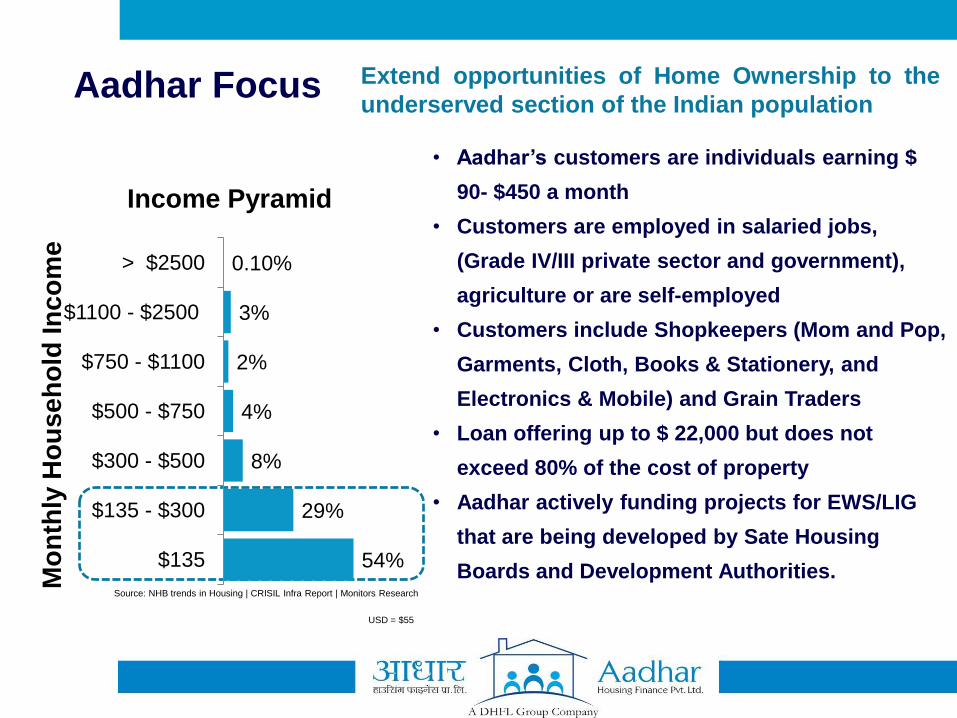

Aadhar Focus M

on

thly

Ho

us

eh

old

In

co

me

Source: NHB trends in Housing | CRISIL Infra Report | Monitors Research

USD = $55

0.10%

3%

2%

4%

8%

29%

54%

> $2500

$1100 - $2500

$750 - $1100

$500 - $750

$300 - $500

$135 - $300

$135

Income Pyramid

• Aadhar’s customers are individuals earning $

90- $450 a month

• Customers are employed in salaried jobs,

(Grade IV/III private sector and government),

agriculture or are self-employed

• Customers include Shopkeepers (Mom and Pop,

Garments, Cloth, Books & Stationery, and

Electronics & Mobile) and Grain Traders

• Loan offering up to $ 22,000 but does not

exceed 80% of the cost of property

• Aadhar actively funding projects for EWS/LIG

that are being developed by Sate Housing

Boards and Development Authorities.

Extend opportunities of Home Ownership to the

underserved section of the Indian population

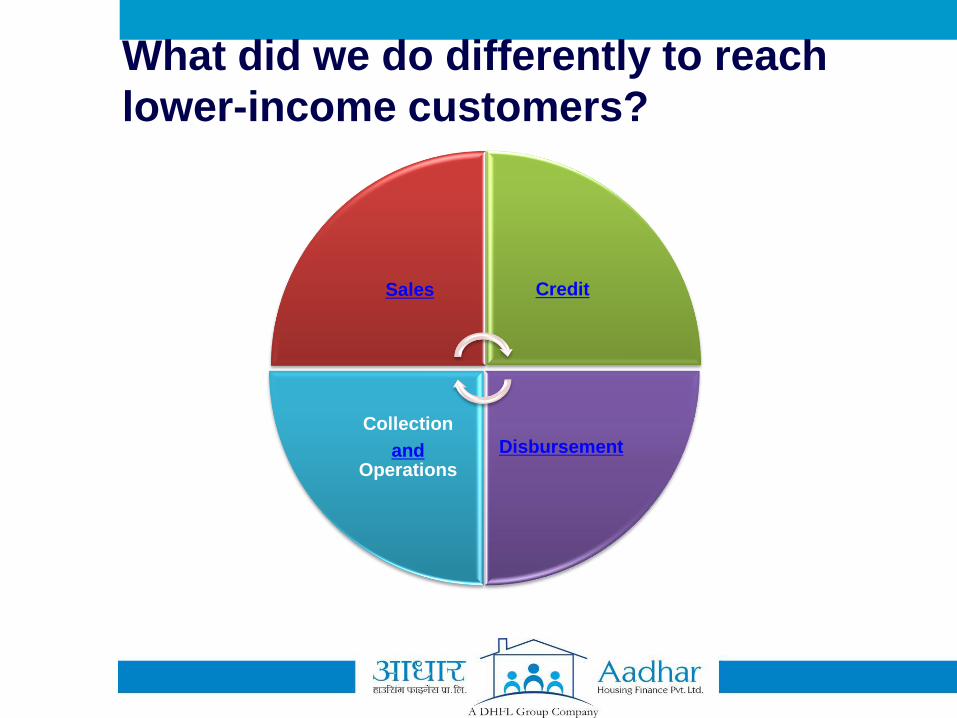

What did we do differently to reach

lower-income customers?

Sales Credit

Disbursement

Collection

and Operations

Sales – Overcoming challenges

Challenges

● Under penetrated markets

● Attracting talent

● Distribution

● Limited supply of housing in this segment

Overcoming Challenges

● Hub and Spoke model adopted for maximum reach

● Outsourced sales through a mix of variable and fixed payouts .

● Set up channels comprising sales agents

● Focused on resale transactions through brokers. About 50 % of

business come from brokers.

Credit – Overcoming challenges

Challenges

● Insufficient KYC

● Informal Segment

● Cash flow assessment

● Poor financial awareness

Overcoming Challenges

● Policy providing other options in accordance with regulators

● Credit policy and process tailor made for Informal Segment

● KYC / Loan availability awareness through events

Disbursement – Overcoming challenges

Challenges

● Legal - Chain documents insufficient / unavailable

● Property valuation – actual and documented valuation

● Technical

● Subdivision of plots , Identification of property address

● Plot not demarcated with boundary wall

● Vertical deviations

Overcoming Challenges

● Adapted region specific policy guidelines for legal and technical

guidelines

● Market value funding

Collection & Operations – Overcoming

Challenges

Challenges

● Banking / Repayment awareness

● Prompt collection

● Cost of collection

Overcoming Challenges

● Welcome Kit issued to customers which is a handy

information on their loan

● Reminders through SMS for EMI repayments

● Maximized collection through electronic modes –

ECS

● Local collections set up

● Facility for cash repayment at branches

Outcome

• Strong customer base of 2425 and growing.

• 79% of customers earn below $ 550/month

• 30% of customers are self-employed.

• 23% of loans are disbursed in rural areas.

• 40% of total customers pay through ECS

• 93% of customers are ECS enabled.

• Average ticket size of $ 9800.

• 29% of customers prefer self construction.

• 84% of customers prefer individual units as against

flats.

12

achieved through….

Operations in 7 states of India with 15 branches and servicing 45 locations.

Managing healthy profile mix

Salaried 69%

Self employed 31%

Through Product Mix –

Purchase of flat/dwelling unit 50%

Self construction 30%

Plot 3%

Mortgage (Loan Against Property ) 13 %

Home Extension/ Improvement 4 %

Repayment of 1010 loans through Electronic Clearance. Balance all cases

through Post Dated Cheques

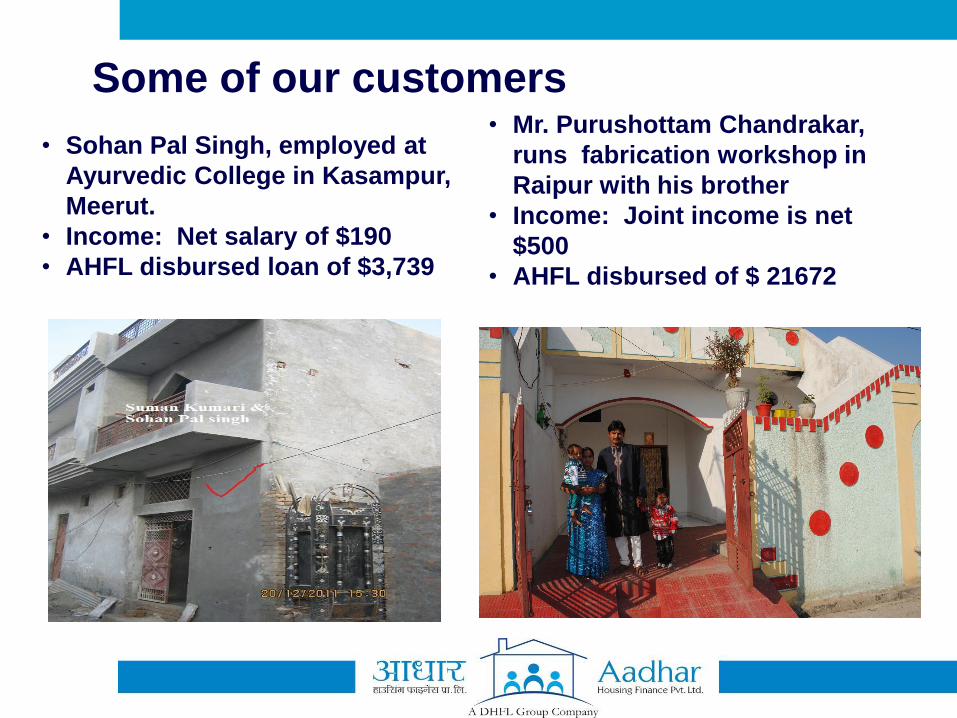

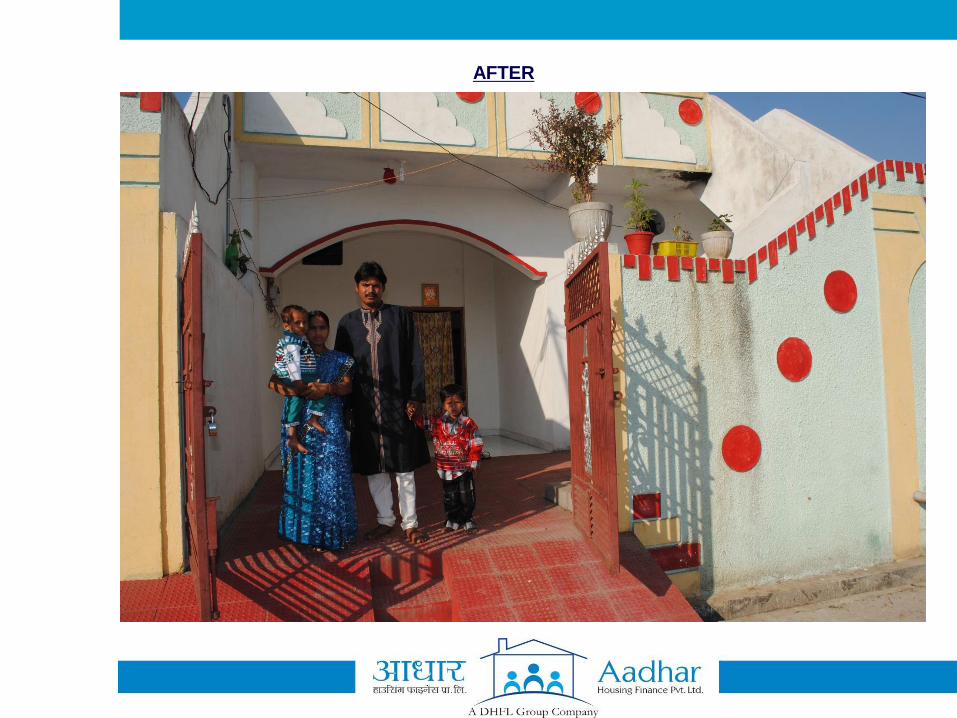

BEFORE Some of our customers

• Sohan Pal Singh, employed at

Ayurvedic College in Kasampur,

Meerut.

• Income: Net salary of $190

• AHFL disbursed loan of $3,739

• Mr. Purushottam Chandrakar,

runs fabrication workshop in

Raipur with his brother

• Income: Joint income is net

$500

• AHFL disbursed of $ 21672

Challenges for Expansion

• Low developer/DA/ activity impacts housing availability in many of

the Tier 3, 4 markets.

• Availability of proper legal chain documents is a constant challenge,

and technical deviations in the property is common in these

locations, as the borrowers(purchasers) are unaware of the legal and

technical norms.

• The field investigation, legal and technical evaluation charges are

much higher in smaller locations as economies of scale are low and

vendors are hard to find.

• High cost of borrowings further impacts the cost of operations.

15

16

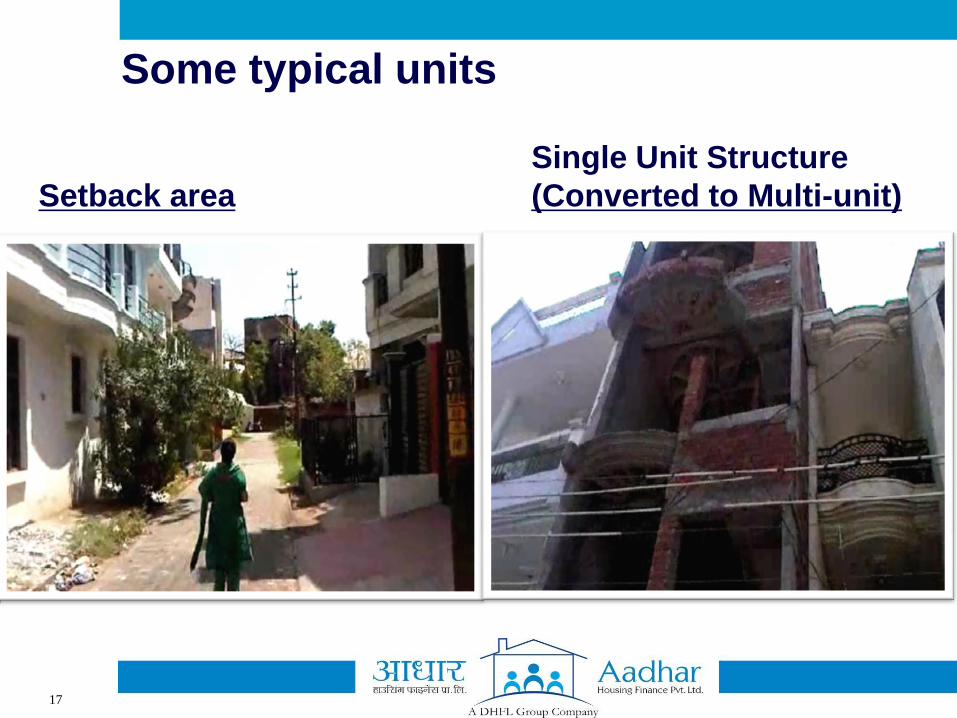

Some typical units

Setback area

Single Unit Structure

(Converted to Multi-unit)

17

Some of our Customers

Customer-

Applicant – Mr. Sohan Pal Singh a Bareilly resident is employed as a Peon with

Ayurvedic College in Kasampur , Meerut.

Income : Net salary of $ 190. His elder brother is a General Physician &

younger brother has a cable TV repair business.

Current Property-

The customer wanted to demolish his existing house & build a G+1 unit.

Customer has maintains average balance in his savings account & also has

timely salary credits.

AHFL has disbursed a loan of $ 3739 to Mr. Sohan Pal Singh to reconstruct his

dream home.

BEFORE AFTER

Some of our Customers

Customer-

Applicant - Mr.Purushottam Chandrakar along with his brother runs a

fabrication workshop in Raipur for last 5 years

Income - Joint income of applicant & his brother is net $ 500.

Current Property-

The customer resides in his two room parental house with his parents,

brother, wife & two children . His dream is to continue staying in a joint

family and have their own house where his children would grow up and

have a bright future. They identified a property but had hesitation due to

high interest rates in the market.

When he got to know about the loan structure at Aadhar Housing

Finance Limited he saw a ray of hope and felt Confident. Aadhar

disbursed a loan of $ 21672 and he now sees his dream turning

into reality .

BEFORE AFTER

![KNOW YOUR CUSTOMER [KYC] & ANTI MONEY LAUNDEERING … · UNITED PETRO FINANCE LIMITED 1 | P a g e KNOW YOUR CUSTOMER [KYC] & ANTI MONEY LAUNDEERING ... nature as defined in Annexure](https://img.pdfslide.us/doc/110x75/613000f71ecc51586943d0b2/know-your-customer-kyc-anti-money-laundeering-united-petro-finance-limited.jpg)