Embed Size (px)

Citation preview

Klépierre2013 Investors Days

June 7, 2013

DISCLAIMER

This document has been prepared by Klépierre (the “Company”) solely for use at the presentation of June 7, 2013. This document is not to be reproduced nordistributed, in whole or in part, by any person other than the Company. The Company takes no responsibility for the use of these materials by any person.

The information contained in this document has not been subject to independent verification and no representation, warranty or undertaking, express orimplied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions containedherein. None of the Company, its shareholders, its advisors or representatives nor any other person shall have any liability whatsoever for any loss arisingfrom any use of this document or its contents or otherwise arising in connection with this document.

This document does not constitute an offer to sell or an invitation or solicitation of an offer to subscribe for or purchase any securities, and this shall not formthe basis for or be used for any such offer or invitation or other contract or engagement in any jurisdiction.

Participants are invited to read the registration document (“document de référence”) of the Company filed with the AMF on March 18, 2013 and the risk factorsdescribed in the Risk Factors section from page 89 to 96 of the registration document. The registration document is made available free of charge at theheadquarters of the Company (Klépierre), on the Internet site of the AMF (http://www.amf-france.org) and on the website of the Company(http://www.klepierre.com).

Certain statements included in the registration document contain forward-looking statements with respect to future events, trends, plans or objectives. Theinformation, assumptions and estimates that were used to determine these objectives are subject to change or modification due to economic, financial andcompetitive uncertainties. Furthermore, it is possible that some of the risks described in the aforementioned section of the registration document could havean impact on the Company’s ability to achieve these objectives. Accordingly, the Company cannot give any assurance as to whether it will achieve theobjectives described, and makes no commitment or undertaking to update or otherwise revise this information.

No assurance is given as to the fairness, accuracy, completeness or correctness of the information or opinions contained in this document. In case of anydiscrepancies between the information contained in this document and the registration document, the latter will prevail.

Klépierre 2013 Investors Days - 06/07/20132 -

TABLE OF CONTENTS

3 -

1 I E-COMMERCE: KEY FACTS/FRAMINGTHE DEBATE

2 I A TARGETED ASSET ALLOCATION STRATEGY

3 I COST OPTIMIZATION POTENTIAL

4 I OPERATIONAL EXCELLENCE AND PARTNERSHIP WITH RETAILERS

Klépierre 2013 Investors Days - 06/07/2013

Table of Contents

1 I E-COMMERCE: KEY FACTS/FRAMING THE DEBATE

4 - Klépierre 2013 Investors Days - 06/07/2013

5 -

+21.1%

WORLD GDP

WORLD E-COMMERCE SALES

2012 GROWTH (vs. 2011)

+3.2%71.8

1.1

in $ trillion

EUROPE

NORTH AMERICA

ASIA

OTHER

35%

6%

26%

33%

2012 E-COMMERCE SALES BY REGION

WORLD E-COMMERCE: KEY FIGURES

Europe accounts for more than one third of e-commer ce sales

E-commerce growth is 10 times higher than global tr ade growth

+19.0%EUROPE E-COMMERCE SALES 0.4

Source: Ecommerce Europe association

May 23, 2013

Klépierre 2013 Investors Days - 06/07/2013

E-COMMERCE IN FRANCE: 2020 PROJECTIONS

2010 2012 2015e 2020e

115

3%4%

7%

10%

72

45

31

FRENCH E-COMMERCE SALES PROJECTIONS(in Bn €)Share of e-commerce in

total consumption

By 2020, e-commerce is expected to account for 10% of total consumption in France

Source: Casas & Associés

Methodology used: Consumption growth +0.0% 2013, +0.5% 2014 and 1.5% thereafter

E-commerce sales growth +18% 2013, +17% 2014, +15% 2015 and +10% thereafter

6 -

E-COMMERCE SALES IN FRANCE (in Bn€)2007 2009 2010 2011 2012

16 25 31 38 45

Klépierre 2013 Investors Days - 06/07/2013

THE EXPANSION OF E-COMMERCE

7 -

5 80015 200

36 900

64 100

100 400

117 500621 k€

383 k€

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

0

100

200

300

400

500

600

700

2003 2005 2007 2009 2011 2012

Number of e-commerce merchant websites

Average turnover per website

E-COMMERCE MERCHANT WEBSITES AND AVERAGE SALES REVENUE (1)

� Europe’s main e-commerce countries: the UK,

Germany and France

� In 10 years, the number of e-commerce

merchant websites has increased 20-fold in

France

� Average sales revenue has dropped significantly

over same period

� Growth broadly driven by all sectors, with the

exception of food sales

� E-commerce sales growth mainly driven by the

increase in number of e-shoppers(2) and

purchasing frequency

(in k€)

1. Data for France

2. Around 250 million e-shoppers in Europe (source: European Commerce Report – May 2013) and around 32 million in France

Klépierre 2013 Investors Days - 06/07/2013

E-COMMERCE AND PHYSICAL COMMERCE ARE INTERTWINED AND COMPLEMENTARY

Omni-channel prevails and the frontier between physical store and e-commerce is disappearing

All channels are interdependent and mutually reinforce one another

ROPO (Research Online – Purchase Offline) is a well-established phenomenon

Purchasing behavior is similar for both on-line and off-line distribution

The key is to get the customer’s attention by providing the best service with impulse buying

International retailer development strategy is base d on physical stores and e-stores

The most successful e-retailers worldwide - with few exceptions -enjoy a large physical footprint and are pursuing their development in both channels

The use of digital tools is part of the shopper’s experience

8 -

88%

66%do both

69%

of shoppersresearch online before

buying offline

visit the store before buying online

Source: Digitas Research – Statistics for France

of smartphone users use them at physical

point of sale

76%

Klépierre 2013 Investors Days - 06/07/2013

Shoppers like the physical experience of shopping

73% of the French prefer physical shopping. Physical shopping attributes are ”vivid” and ”human”. This preference is cross-generational.

78% of the French say they need to touch and possibly try out/on products before purchasing(1)

Transformation rates are higher in shopping malls than online

40.6%(2) in shopping malls vs. 2.15% online(3)

For personal products, the transformation rate is event higher: 55%(4)

Shoppers compare online but the majority still buy in store(5)

ASPIRATIONAL EXPERIENCE COUNTS AND IS MORE EFFICIENT

9 -

(1) IPSOS survey on a representative sample of French people aged 16+(2) French National Association of Shopping Centers, Capgemini(3) Fevad (French Federation of E-Commerce) [check translation](4) Journal du Textile(5) Source: OTO Research 2012

Exclusively in stores

Both in stores and online

Exclusively online

83% 10% 7%

BUYINGACT

Klépierre 2013 Investors Days - 06/07/2013

1. E-commerce pure players (Amazon, Asos, Cdiscoun t, Price Minister, Vente Privée, Yoox, Leboncoin.fr, etc.)

Successful e-retailer business model is usually based on the concept of marketplace

They gather a diversity of products from various brands, which allows the customer to comparison shop

10 -

+40%

+41%

+27%

0%

5%

10%

15%

20%

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

2010 2011 2012

AMAZON (US)in M$

TURNOVER EBITDA MARGIN

TWO MODELS OF SUCCESSFUL RETAILERS INE-COMMERCE (1)

EBITDA multiple(1)

� 2013E: 28.8x� 2014E: 22.0x

(1) As of 28/05/2013 estimates, source Thomsom Reuters

+52%

+46%

+35%

0%

5%

10%

15%

20%

0

200

400

600

800

1 000

1 200

2010 2011 2012

ASOS (UK)in M£

EBITDA multiple(1)

� 2013E: 44.6x� 2014E: 34.5x

YOOX (IT)in M€

+41%

+36%

+29%

0%

5%

10%

15%

20%

0

100

200

300

400

500

2010 2011 2012

EBITDA multiple(1)

� 2013E: 21.2x� 2014E: 15.3x

⇒ Revenue growth remains high but EBITDA margin is flat or declining

⇒ Trading at high EBITDA multiples

⇒ Major challenges: low margin and significant delivery costs. Only a few pure players and a handful of niche players will

surviveKlépierre 2013 Investors Days - 06/07/2013

TWO MODELS OF SUCCESSFUL RETAILERS INE-COMMERCE (2)

2. Traditional retailers are expanding in e-commerc e…

Some retailers have demonstrated the sustainability of their business model in “physical” commerce

Their success is based on a integrated model: from production to distribution

E-shops were launched in the mid/late 2000’s and their appeal is based on an extensive physical footprint that supports strong brand awareness

… but also increasing their traffic-generating retai l locations

Continued reliance on their physical presence around the world to deliver profitable growth: H&M, Zara, Sephora, Mango, Castorama, etc.

Retail real estate with a portfolio of dominant and leading shopping centers in their catchment area are best positioned to respond to these demands

11 -

E-shop launch First e-shop launched in 2009 (H&M Home) in Scandinavia, Netherlands, Germany and Austria

First e-shop in 2007 (Zara Home)

StrategyRecent acceleration in e-commercePriority given to physical stores: new locations include Europe & USA

Recent and aggressive development in e-commerceRate of new physical store openings high around the world

E-commerce weight €214 M, i.e., 3.3% of total revenues in 2011 (1) €350 M (est.) i.e. 2% of total revenues in 2012

Online buyingIn-store delivery is not possibleHome delivery entails extra costs

Free in-store deliveryHome delivery entails extra costs

Number of store openings planned for 2013

325 (out of 2,776 stores as of 31/12/12)(2) Between 440 and 480 (out of 6,009 stores as of 31/12/12)(3)

(1) Source: Internet Retailer (2) Source: H&M 2012 Annual Report (3) Source: INDITEX 2012 Annual report

Klépierre 2013 Investors Days - 06/07/2013

MULTICHANNEL PLAYERS ARE BLAZING THE TRAIL IN E-COMMERCE

Ranking in attractiveness for e-commerce websites

12 -

Source: OC&C survey, May 2011

Retailers alsodistributing goods in stores

1 Amazon Amazon Amazon

2 Yves Rocher eBay Netflix

3 Vente-Privee Douglas iTunes

4 Fnac.com Tchibo Victoria’s Secret

5 Decathlon Esprit eBay

6 iTunes Rossmann Costco

7 Darty S. Oliver Barnes & Noble

8 Créateurs de Beauté Otto LL Bean

9 eBay Deichmann Bestbuy

10 Price Minister H&M Macys

11 La Redoute Conrad Elektronic Wal-Mart

12 Sephora Bonprix Target

13 Cdiscount Dawanda JC Penney

14 Pixmania C&A Home Depot

15 Marionnaud Kaufhof GAP

#

Retailer presentin Klepierre malls

Despite having started their online development later, traditional retailers’ e-shops rank among the most attractive. Online success partly due to on an extensive network of physical stores

Klépierre 2013 Investors Days - 06/07/2013

CHALLENGES AND OPPORTUNITIES FOR KLEPIERRE

Adapting the business model and developing its comp lementarity to this new and still evolving way of shopping

⇒ Customers are increasingly mobile but the answer is not only digital

⇒ Accelerate re-tenanting and adapt sizes

⇒ Shopping centers should more than ever appeal to retailers as the ideal place to be, providing them with the highest purchase transformation rates

⇒ Shopping centers should answer aspirational customer needs:� create vibrant marketplaces

� adopt a hospitality attitude

� socialize more, entertain more, surprise more

� more rewards for loyalty

13 - Klépierre 2013 Investors Days - 06/07/2013

Table of Contents

2 I A TARGETED ASSET ALLOCATION STRATEGY

14 - Klépierre 2013 Investors Days - 06/07/2013

KLEPIERRE: A DOMINANT PLAYER IN KEY EUROPEAN REGIONS

15 -

La Gavia, Madrid

Créteil Soleil, Créteil

Val d’Europe, Marne-la-Vallée

Le Millénaire, Aubervilliers

Arcades, Noisy-le-Grand

St. Lazare Paris, Paris

Les Sentiers de Claye-Souilly

Les Passages, Boulogne-Billancourt

Southern ScandinaviaGreater Paris Area

Southwest FranceBlagnac, Toulouse

Grand Portet, Toulouse

Bègles, Bordeaux

Saint-Orens, Toulouse

Odysseum, Montpellier

Aqua Portimão, Portimão

Parque Nascente, Porto

Northern Italy

Metropoli, Milan

Brianza, Milan

Le Corti Venete, Verona

Milanofiori, Milan

Acquario center, Vignate (Milan)

Il Leone di Lonato, Lonato

Il Destriero, Vittuone

Fields’, Copenhagen

Allum, Partille

Emporia, Malmö

Sollentuna, Sollentuna

Kupolen, Borlänge

Bruun's Galleri, Aarhus

Marieberg, Örebro

Novỳ Smíchov, Prague L’esplanade, Louvain-la-Neuve

Belle Epine, Thiais

Meridiano, Santa Cruz de Tenerife

Klépierre 2013 Investors Days - 06/07/2013

STRONG FOCUS ON STRATEGIC REGIONS

16 -

Demographics and high purchasing power are key criteria

Priority given to countries with high entry barriers

Capitalizing on a strong historical and local footprint with dedicated teams

+ Additional spots in capital cities and popular tourist destinations: Madrid, Tenerife, Porto, Algarve, Warsaw, BudapestSource: Eurostat, 2010 data / GDP per capita in purchasing power standards

Population GDP per capita Demo. growth by 2030

Greater Paris Area 11.8 M 49 800 € +10.7%

Southwest France 8.7 M 25 133 € +16.7%

Greater Lyon Area 7.5 M 28 700 € +10.7%

Southern France 4.9 M 28 300 € +12.5%

Scandinavia 19.6 M 41 415 € +10.0%

Northern Italy 19.1 M 29 133 € +5.7%

Greater Brussels Area 2.5 M 41 039 € +12.2%

Prague Greater Area 2.4 M 29 700 € +10.1%

Europe 500 M 24 500 € +4.1%

Regions enjoying better demographic outlook

Klépierre 2013 Investors Days - 06/07/2013

DELIVERY OF PROJECTS IN THE PAST 5 YEARS AND GOING FORWARD WILL REINFORCE KLEPIERRE’S POSITION

17 -17 -

Southern ScandinaviaGreater Paris Area

Southwest France

Northern Italy

2007-2012■ Le Millénaire

■ St.Lazare Paris

■ Claye-Souilly

2007-2012■ Saint –Orens

■ Blagnac

■ Odysseum

■ Roques

2007-2012■ Il Leone di Lonato

■ Le Corti Venete

■ Il Destriero

■ Metropoli

2007-2012■ Steen & Strøm

■ Sollentuna

■ Gulskogen

■ Metro

■ Emporia

2007 2008 2009 2010 2011 2012 2017

Central Europe

Iberia

Italy

Scandinavia

France-Belgium

+ 2.7Bn€*

9.5Bn€12.7Bn€ 13.0Bn€

13.9Bn€ 15.0Bn€15.5Bn€

2017

13.7%

58.6%

11.5%

45.9%

26.9%

Shopping center portfolio valuation (total share, ex cl. duties)* Total pipeline estimated cost as of 12/31/2012

+ €641 M

+ €820 M

+ €4,176 M

+ €296 M

10.9%

46.3%

27.8%

Klépierre 2013 Investors Days - 06/07/2013

Project GLA (sq.m.)Estimated cost

(M€)*Expected initial

yield*Targeteddelivery

FR

AN

CE

Greater Paris Area

Val d’Europeextension

17,000 94 7.1% Q3 2016

Montparnassetrain station

Klépierre participating in the beauty contest

Southwest FranceGrand Portet

extension8,000 51 9.9% Q3 2016

Lyons Greater AreaClermont Jaude

extension16,000 101 7.2% Q3 2013

Southeast France Marseille Bourse 2,660 17 6.4% Q4 2014

SC

AN

DIN

AV

IA NorwayVinterbro extension 7,600 33 7.6% 13 June 2013

Åsane 52,000 111 8.4% Q4 2017

SwedenKristianstad 28,500 128 7.2% Q4 2014

Allum extension 14,500 58 8.4% 2015

Denmark Viva 48,500 223 6.4% Q4 2015

NORTHERN ITALYRomagna Center

extension8,000 26 7.8% Q1 2014

GREATER BRUSSELS AREA

L’esplanadeextension

26,000 130 7.6% 2016-2017

Neo project Klépierre participating in the beauty con test

DEVELOPMENT PIPELINE TARGETING SPECIFIC REGIONS

18 -

*Data as of December 31, 2012

Klépierre 2013 Investors Days - 06/07/2013

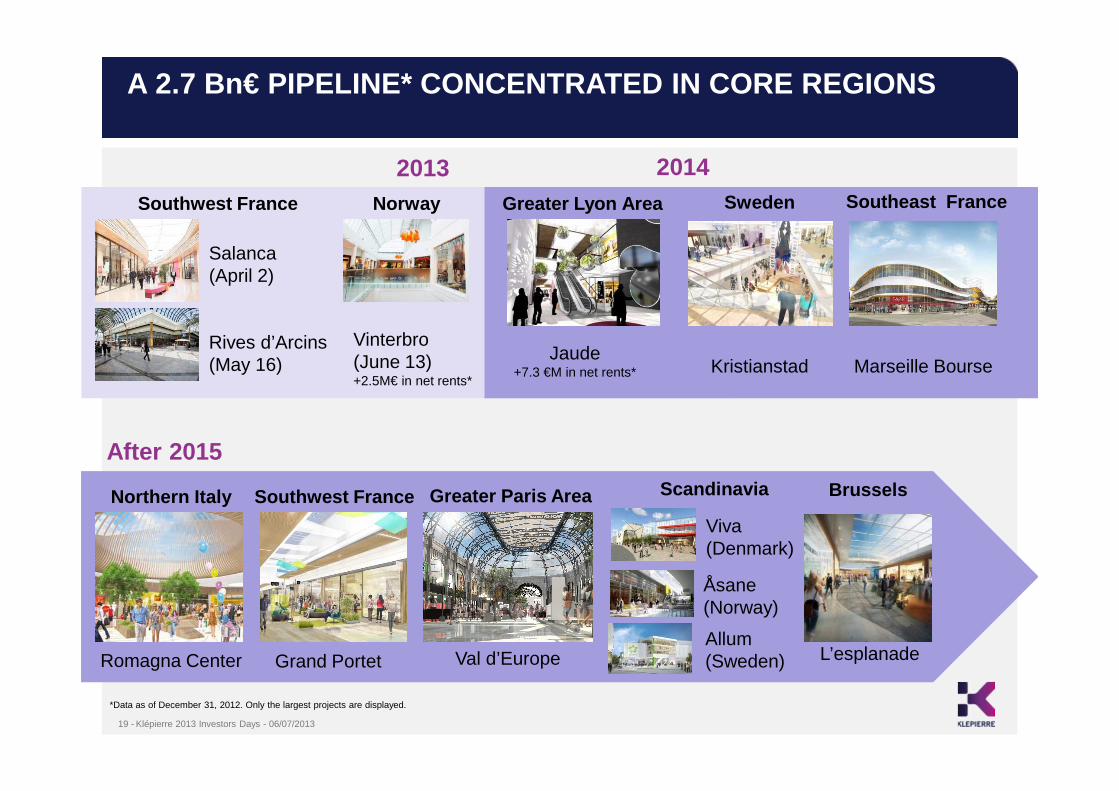

A 2.7 Bn€ PIPELINE* CONCENTRATED IN CORE REGIONS

19 -

Southwest France Norway

Salanca(April 2)

Rives d’Arcins(May 16)

Vinterbro(June 13) +2.5M€ in net rents*

Greater Lyon Area

Jaude+7.3 €M in net rents*

2013 2014Sweden

Kristianstad

*Data as of December 31, 2012. Only the largest projects are displayed.

Greater Paris Area

Val d’Europe

Brussels

L’esplanade

After 2015

Southeast France

Marseille Bourse

Scandinavia

Åsane(Norway)

Viva(Denmark)

Allum(Sweden)

Southwest FranceNorthern Italy

Romagna Center Grand Portet

Klépierre 2013 Investors Days - 06/07/2013

Table of Contents

3 I COST OPTIMIZATION POTENTIAL

20 - Klépierre 2013 Investors Days - 06/07/2013

COST OPTIMIZATION POTENTIAL

Cost-based Analysis

21 - Klépierre 2013 Investors Days - 06/07/2013

2012 Klépierre’s cost base is €166.5 M for manageme nt of a €20 Bn portfolio

22 -

- €120.5 M

72% - €46.0 M

28%

BREAKDOWN IN ASSETS UNDER MANAGEMENT

Klépierre assetsManagement

100%

In €M Total share Group share Third parties

Asset value (excl. duties)

16 445 12 779 3 393

Gross rents 983 782 234

Net rents 918 728 218

COSTS: KLEPIERRE BEST IN CLASS BUT SEEKS TO FURTHER OPTIMISE

PAYROLL GENERAL EXPENSES

Costs 2012 -€166.5 M

� 100% third-party fees +€17.5 M

� JV partners, property & development fees +€72.8 M

Net Costs 2012 -€76.2 M

Net Costs = 9.7% of gross rents

COST BREAKDOWN €166.5 M

Klépierre 2013 Investors Days - 06/07/2013

COST STRUCTURE LARGELY DOMINATED BY FRANCE AND SCANDINAVIA

23 -

GEOGRAPHIC BREAKDOWN IN COSTS2012 (-€166.5 M)

IBERIA(-€12.0 M)

ITALY(-€8.8 M)

CENTRAL EUROPE(-€5.6 M)

58%26%

7%5% 3%

SCANDINAVIA(-€43.4 M)

FRANCE(-€96.3 M)

BREAKDOWN IN RENTS UNDER MANAGEMENT 2012

(INCL. THIRD PARTIES - € 1 217.1 M)

47%

25%

12%

11%6%

IBERIA€140.5 M

ITALY€127.8 M

CENTRAL EUROPE€78.4 M

SCANDINAVIA€298.3 M

FRANCE€566.5 M

2010 2011 2012

1508 1492 1473 1467*

2012 2010 2011 2012

121 119 116 107*

2012

HEADCOUNT (AVERAGE)

Group Spain

* End of period

No. of employees WORKFORCE

FRANCE 576

SCANDINAVIA 405

IBERIA 152

ITALY 130

CENTRAL EUROPE 201

⇒ Not all countries are comparable: in-house facility management in Scandinavia and Central Europe

Klépierre 2013 Investors Days - 06/07/2013

Operational projectsover SAP system

COST REDUCTION DRIVEN BY NEW IT SYSTEM

⇒ Clipper development aims to improve Klépierre’s organization by reinforcing business units and downsizing support functions

General expenses expected to be positively impacted in the short term with implementation of the final steps of the new d ata processing system (SAP Clipper project)

2014 - 2015

Fast implementation of SAP in all countries (invoicing, accounting, reporting)

Central Europe

France Spain

Italy S&S

2010 2011 2012 2013

24 - Klépierre 2013 Investors Days - 06/07/2013

FOCUS ON CLIPPER PROJECT

Asset management

Rental and property management

Better control of net rents and cash flows

Full availability and transparency of data enabling investment strategy adjustments

Financial reporting Immediate availability of business information

Group organization Shared service centers for accounting, reporting and IT. Automation of closing tasks

• Global view of 13 000 contracts representing net rent of €920 M

• Annual expenses of €250 M

• ONE shared master data set

• Immediate availability of all cross-country information on demand

• Consolidated accounts available on D+5

• Group indicators available on D+7

• Significant reduction in back office

• Industrialized IT production

• Traceability

New support for ongoing and

upcoming strategic projects

� Standardized dashboards for retailer sales revenue and shopping center sales performance analysis

� Harmonization of rental forecast process

� Electronic invoicing

� Treasury integration

� CRM

� Facilitated potential integration of new countries

Material efficiency gains expected across business areas

25 - Klépierre 2013 Investors Days - 06/07/2013

ADDITIONAL SAVINGS ON GENERAL EXPENSES

Actions in progress:

⇒ Streamlining all expenses

⇒ Renegotiation with suppliers

⇒ Paris HQ: Relocation planned mid-2014/mid-2015 = A single location

Expected outcome ≈ 10% savings over 3 years

Missions & external fees(-€11.8 M / 26%)

Insurance, Communication, Special events, etc.

(-€10.1 M / 22%)Head offices

(-€9.7 M / 21%)

Operating costs(-€5.1 M / 11%)

IT(-€4.5 M / 10%)

Taxes(-€2.4 M / 5%)

R & D (-€2.4 M / 5%)

€46 M in general expenses where substantial savings are expected

26 - Klépierre 2013 Investors Days - 06/07/2013

Focus on financial structure and costs

27 -

COST OPTIMIZATION POTENTIAL

Klépierre 2013 Investors Days - 06/07/2013

STEADY IMPROVEMENT IN COST OF DEBT

28 -

Klépierre’s cost of debt is the result of:

- Long- and short-term financing

- Debt denominated in Euros & Scandinavian currencies

- A sound interest rate risk management policy

Klépierre has succeeded in lowering its cost of deb t thanks to active

management of both financing resources and interest rate hedging portfolio:

▲Private placements, taps and new issues in order to price several maturities

in Klépierre’s credit curve

▲Swaps unwinding

▲Liquidity position improved from €500 M to € 2 Bn =>

4,45% 4,47%4,17%

3,95%

3,50%

2009 2010 2011 2012 Q1 2013

COST OF DEBT(PUBLISHED DATA)

Higher cost of liquidity.

EUR 68%NOK 14%

SEK 12%

DKK 7%

KLÉPIERRE GROUP'S FINANCING BREAKDOWN BY CURRENCY - UTILIZATIONS

Commercial Paper10% Financial

leases2% Bilateral

facilities2%

Syndicated loans13%

Mortgage loans30%

Bonds43%

KLÉPIERRE GROUP'S FINANCING BREAKDOWN BY TYPE OF RESOURCE - UTILIZATIONS

Data as of June 3, 2013Klépierre 2013 Investors Days - 06/07/2013

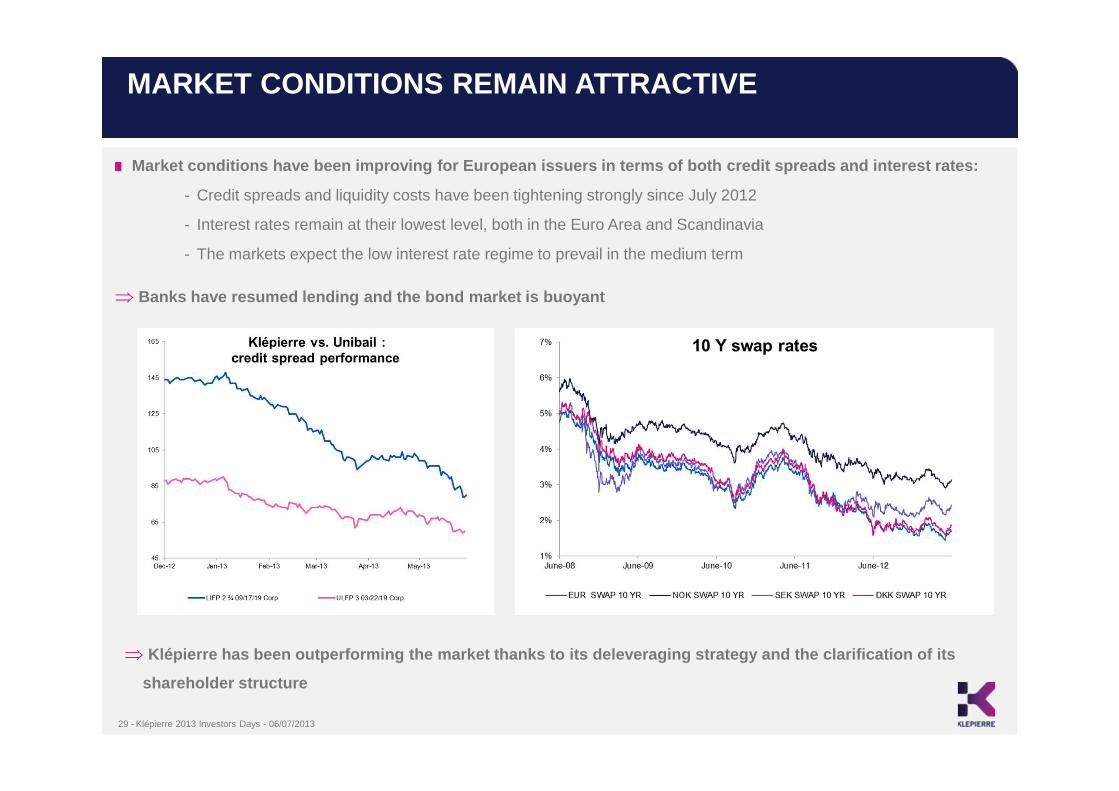

MARKET CONDITIONS REMAIN ATTRACTIVE

29 -

Market conditions have been improving for European issuers in terms of both credit spreads and interes t rates:

- Credit spreads and liquidity costs have been tightening strongly since July 2012

- Interest rates remain at their lowest level, both in the Euro Area and Scandinavia

- The markets expect the low interest rate regime to prevail in the medium term

⇒ Banks have resumed lending and the bond market is b uoyant

⇒ Klépierre has been outperforming the market thanks to its deleveraging strategy and the clarification of its

shareholder structure

Klépierre 2013 Investors Days - 06/07/2013

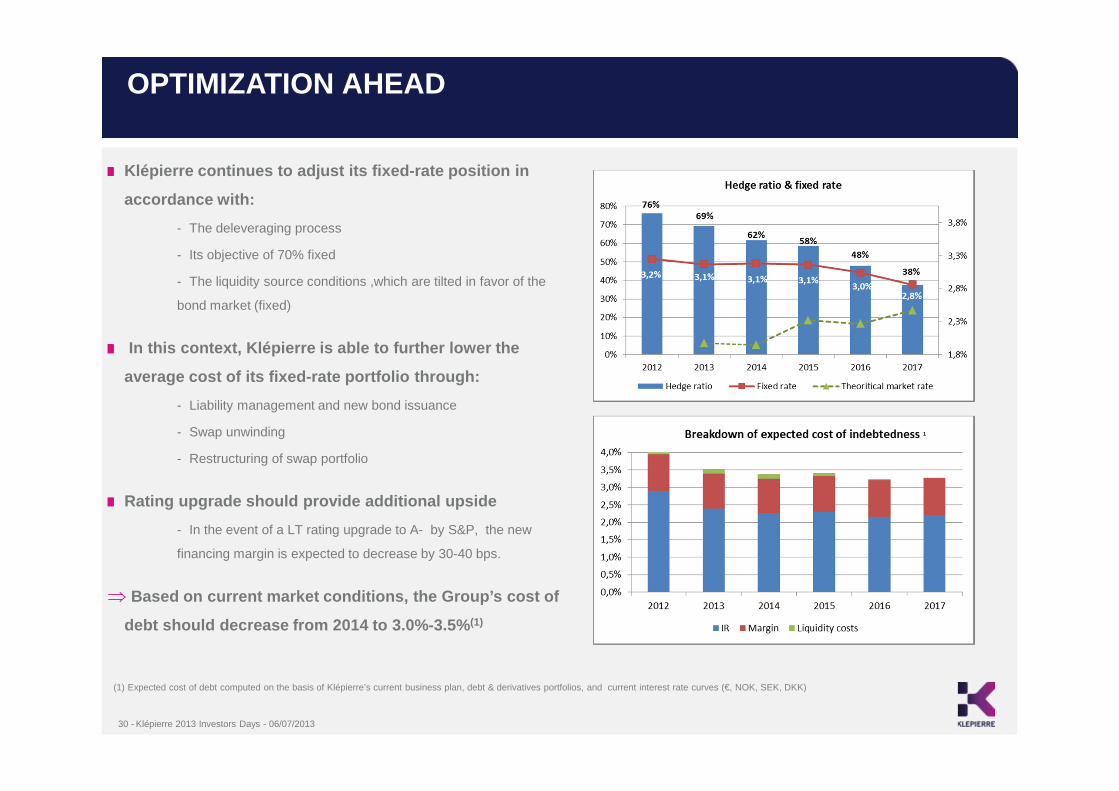

OPTIMIZATION AHEAD

30 -

Klépierre continues to adjust its fixed-rate positi on in

accordance with:

- The deleveraging process

- Its objective of 70% fixed

- The liquidity source conditions ,which are tilted in favor of the

bond market (fixed)

In this context, Klépierre is able to further lower the

average cost of its fixed-rate portfolio through:

- Liability management and new bond issuance

- Swap unwinding

- Restructuring of swap portfolio

Rating upgrade should provide additional upside

- In the event of a LT rating upgrade to A- by S&P, the new

financing margin is expected to decrease by 30-40 bps.

⇒ Based on current market conditions, the Group’s cos t of

debt should decrease from 2014 to 3.0%-3.5% (1)

(1) Expected cost of debt computed on the basis of Klépierre’s current business plan, debt & derivatives portfolios, and current interest rate curves (€, NOK, SEK, DKK)

Klépierre 2013 Investors Days - 06/07/2013

A NEW €750 M REVOLVING CREDIT FACILITY

31 -

On June 3, 2012 Klépierre signed a new € 750 M syndi cated RCFs (16 banks)

This line partially replaces 2 former BNP Paribas u ndrawn RCFs maturing 2016 and 2018

This transaction enables Klépierre to:

- Reduce its liquidity cost, with expected full-year savings of €3.3 M

- Diversify its sources of financing in terms of counterparty: BNP Paribas’ share in total authorization ≈ 22%

- Lengthen the average remaining maturity of its liquidity: + 1 year (≈ 4 years)

- Smoothen the debt maturity profile

Participation of prominent global banks underscores Klépierre’s credit attractiveness and financial syn ergies with

SPG

0

200

400

600

800

1000

1200

1400

1600

1800

2013 2014 2015 2016 2017 2018 2019 2020 2021 ≥ 2022

DEBT MATURITY SCHEDULE

Authorized debt Authorized debt with new syndicated loan (750€M)

RCFS: BREAKDOWN BY COUNTERPARTS' RATING

Klépierre 2013 Investors Days - 06/07/2013

Table of Contents

4 I OPERATIONAL EXCELLENCE AND PARTNERSHIP WITH RETAILERS

32 - Klépierre 2013 Investors Days - 06/07/2013

Retail industry challenges

Sustained economic slowdown across Europe is affecting purchasing power

Changes in e-commerce and consumption habits: customers are more complex

Retailers being online and offline may require different premises

Customer flows need to be more proactively addressed

Increasing time spent in shopping malls to increase purchase rate

Shopping centers: greater need to differentiate from competition

CHALLENGES OF AN EVOLVING RETAIL ENVIRONMENT REQUIRE OPERATIONAL EXCELLENCE

33 -

Klépierre initiatives

Operational Excellence

From Klépierre management and teams

From and towards our tenants/retailers

In welcoming shoppers

Renewed Mix Merchandising

Adapted to specific catchment areas

Adapted to what clients expect and trends

High quality of the retail mix

Customer-centric Shopping Centers

Focus on customer services, welcome and cultivating a zero-defect culture

Klépierre 2013 Investors Days - 06/07/2013

34 -

Must have 70 – 80%

Differientiate 10 – 15%

Exclusive 10 – 15%

RETAILERSTARGET MIX

For each and every asset: there is an ambition and a definition of the leasing action plan

• By sector • Local vs. international brands• Diversity in store size• Synergies between brands

(competition vs. complementarity)

RESPECT FOR RETAIL MIX BALANCE IN THE AREA

• Renewals• Renewal with latest concepts• Re-tenanting before leases

expire

• Coherence with primary and secondary catchment area

• Marketing analysis based: client expectations, satisfaction level

• Development of the area• Shopping center competition –

current and future

• KPIs: Est. Rental Value, OCR• Sales growth, etc. • Latest concept of the retailer? • Adapted size?

ANALYSISBY TENANT

CUSTOMERPROFILE

LEASING

MERCHANDISING MIX OF A REGIONAL SHOPPING CENTER

A STRUCTURED APPROACH TO LEASING ANDRE-TENANTING

Klépierre 2013 Investors Days - 06/07/2013

CHANGING THE MERCHANDISING MIX IN A FEW WORDS

Re-tenanting: time is of the essence!

Part of a global and consistent plan for the shopping center: - not an isolated decision for a specific retailer within a mall

- not one standard mix applicable everywhere

The result of a multi-criteria approach

The decision to re-tenant before the lease expires is made after a thorough financial analysis

A one- to three-year timetable for execution

As some traditional anchor stores reduce store size or close, Klépierre has an opportunity to work on value-creative reconfigurations and extract rental uplift

35 - Klépierre 2013 Investors Days - 06/07/2013

EXAMPLE OF RETENANTING PLAN – NOVY SMICHOV

Ambition ���� Be the best shopping center in the city with differ entiating and upscale brands in all sectors

36 -

How is the review structured?

1. Center analysis: key strengths and weaknesses

- Footfall analysis, revenueperformances, yields, OCR, rents benchmark, KPIs by tenants, etc.)

2. Mix merchandising and offer structure

3. Competition Analysis

4. Structured leasing action plan with timetable:

- By area, re-lettings, new brands, etc.

- Actions since 2011, additional objectives:

5. Marketing plan: achievements, ambitions, objectives

6. Financial plan: ERVs and 5-year cash flowprojections

Klépierre 2013 Investors Days - 06/07/2013

NOVY SMICHOV – NEW OPENINGS 2013

Revitalizing the retail mix with differentiating bra nds

37 -

Tommy HilfigerOpened 28/03

Swarovski Opened 15/02

Armani JeansOpened 04/03

Carwash ExpressOpened 01/03

MACOpened 01/05

Brioche DoréeOpened 28/03

Klépierre 2013 Investors Days - 06/07/2013

RELATIONSHIPS WITH RETAILERS - PROMISE: KLEPIERREIS A PARTNER TO RETAILERS

38 -

This promise demands operational excellence from bo th parties

An approach by key account complements the “asset by asset” approach

Review of each retailer’s portfolio at regional, domestic and international levels

The country and regional managers, the Group Head of Leasing and CEO/COO -when appropriate - lead account reviews:

- Bi-annual meetings with each retailer to review:

- Recent openings, new projects, new concepts to implement with Klépierre

- Financial performance

- Overall relationship

- Retailer’s strategic and development plan across the regions

Klépierre 2013 Investors Days - 06/07/2013

RELATIONSHIPS WITH RETAILERS – EXAMPLES

39 -

Expanding Italian Group – 3,000 stores globally -developing the Calzedonia, the Intimissimi, Tezenisand Falcoreni brands

Already 31 Calzedonia stores, 30 Intimissi stores and 15 Tezenis stores in Europe with Klépierre

Increased brand awareness in France and expansion plan: 5 stores opened in 2012 with Klépierre in France

MORE CALZEDONIA STORES IN KLEPIERRE SHOPPING CENTERS

Klépierre supports the development of expanding ret ailers

CELIO’S FIRST OPENING IN POLAND WITH KLEPIERRE IN THE SADYBA SHOPPING CENTER

Celio, the leading men’s clothing retailer in France has developed a strong global presence: 1,000 retail outlets in more than 60 countries.

65 Celio outlets, of which 53 in France and 12 in Europe, with Klépierre

The arrival of Celio in Poland: a major strategic challenge for the brand, and an illustration of the successful European partnership with Klépierre

Klépierre 2013 Investors Days - 06/07/2013

KEEP RETAIL MOVING FORWARD

40 -

An “R&D” team in charge of systematic, regular review of promising new retailers

Established retailers in a shopping center are very demanding towards Klépierre to regularly renew the retail mix with selected differentiating retailer/new concepts

Objective: Identify new brands and winning concepts and bring them to Klepierre malls

Successful new large retailers expanding in Europe (e.g., Primark, Hollister, J.Crew, Uniqlo, etc.)

Local brands targeting international development

Exclusive brands or exceptional designs

A methodical approach by industry: Fashion, Health & Beauty, Food & Beverage

Klépierre 2013 Investors Days - 06/07/2013

INNOVATION - KLEPIERRE AND CINEMA CITY OPEN THE FIRST 4-DX CINEMA

41 -

MAY 2013: Klépierre and Cinema City, the leading operator of multiplex cinemas in Central Europe, open the first cinema equipped with the 4-DX technology in NovýSmíchov (Prague)

This significant innovation and investment reinforce the center’s attractiveness for retailers

Klepierre already counts 19 Cinema City movie theaters in its Central Europe shopping centers and some 6.5 million people visited them in 2012

Klépierre’s goal is to constantly innovate by propo sing unique and novel concepts that amaze customers and increase their loy alty

Klépierre 2013 Investors Days - 06/07/2013

KEEP RETAIL MOVING FORWARD - FASHION

42 -

Unexpected discovery of new brands and concept stor es

Klépierre 2013 Investors Days - 06/07/2013

KEEP RETAIL MOVING FORWARD – HEALTH AND BEAUTY

43 -

Fantastic shop designs and customer invitations to try out products

Klépierre 2013 Investors Days - 06/07/2013

KEEP RETAIL MOVING FORWARD – FOOD & BEVERAGE

44 -

A great and ever-changing selection of food and bev erages from around the world

Klépierre 2013 Investors Days - 06/07/2013

45 -

OPERATIONAL EXCELLENCE IN SUSTAINABLE DEVELOPMENT

Klépierre’s 2010-2015 action plan is reviewed annua lly and adapted in accordance with changes in Group activities and reg ulations

ENVIRONMENTAL

SOCIAL

SOCIETAL

PERFORMANCE Risks whose

improvements are measurable

EXEMPLARITYMust-have social and

working conditions

INNOVATIONRisks identified as key for

the future

OBJECTIVES

ACTION PLAN

TIMETABLE

THE MOST SIGNIFICANT AND MATERIAL FOR KLÉPIERRE AND STAKEHOLDERS :

A detailed mapping of key topics

Topics belong to the 3 types of traditional risks

Topics divided into 3 expected performance targets level

For each, definition of

Klépierre 2013 Investors Days - 06/07/2013

46 -

REDUCE ENERGY CONSUMPTION

IMPROVE WASTE RECYCLING

As of 31/12/2012, 39% of waste in Klépierre’s malls was recycled

Objective: Reach 50% by 2016

ACCESSIBILITY OFSHOPPING MALLS

Objective: Increase shopping center access options to decrease carbon footprint of our shopping centers

Action plan: Development of zones dedicated to green transportation, communication on various ways to access shopping centers, etc.

SUSTAINABLE DEVELOPMENT: SELECTED EXAMPLES

PERFORMANCE PERFORMANCE INNOVATIONTarget level

Topics

Action plan

Klépierre 2013 Investors Days - 06/07/2013

Between 2010 and 2012, 33 million kWh were saved, a 10% reduction (constant scope basis)

Objective: Reduce energy consumption by 25% (kWh/visit by 2020)

THANK YOU

Klépierre 2013 Investors Days - 06/07/201347 -