Embed Size (px)

Citation preview

KITZ CORPORATION AND SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED MARCH 31, 2014

The accompanying notes are an integral part of these financial statements.

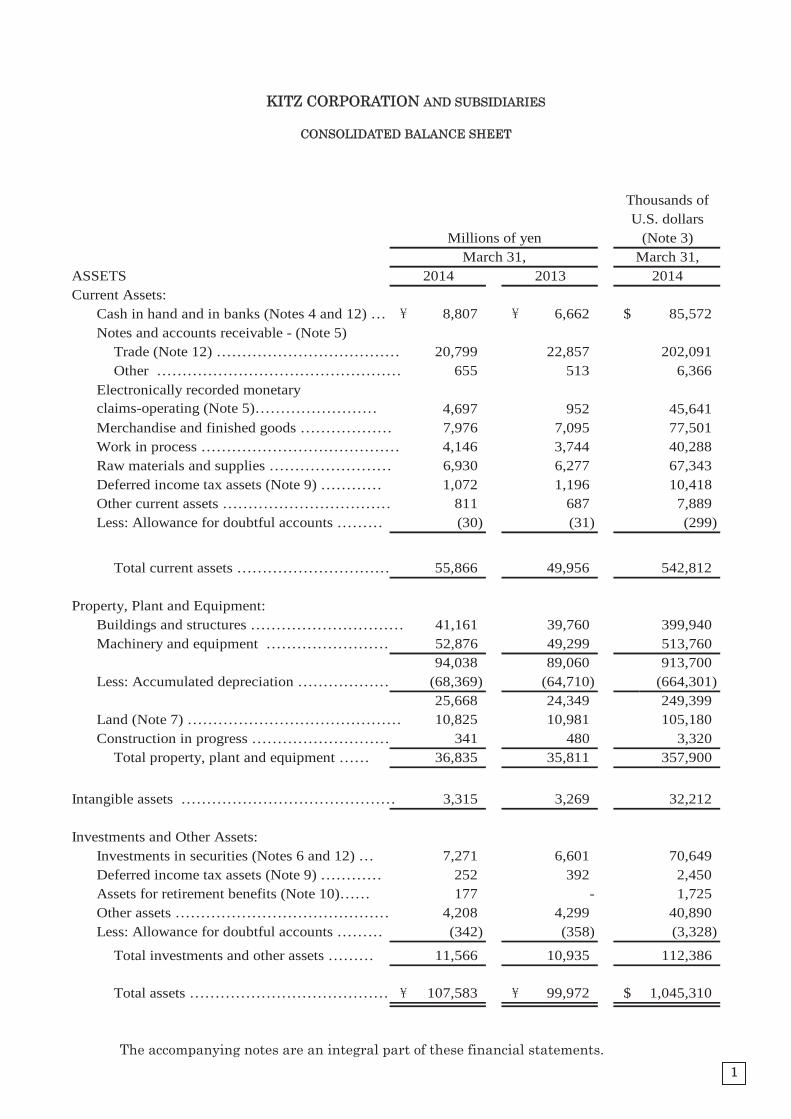

KITZ CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEET

March 31, March 31,ASSETSCurrent Assets:

Cash in hand and in banks (Notes 4 and 12) … 8,807 6,662 $ 85,572Notes and accounts receivable - (Note 5)

Trade (Note 12) ……………………………… 20,799 22,857 202,091Other ………………………………………… 655 513 6,366

4,697 952 45,641Merchandise and finished goods ……………… 7,976 7,095 77,501Work in process ………………………………… 4,146 3,744 40,288Raw materials and supplies …………………… 6,930 6,277 67,343Deferred income tax assets (Note 9) ………… 1,072 1,196 10,418Other current assets …………………………… 811 687 7,889Less: Allowance for doubtful accounts ……… (30) (31) (299)

Total current assets ………………………… 55,866 49,956 542,812

Property, Plant and Equipment:Buildings and structures ………………………… 41,161 39,760 399,940Machinery and equipment …………………… 52,876 49,299 513,760

94,038 89,060 913,700Less: Accumulated depreciation ……………… (68,369) (64,710) (664,301)

25,668 24,349 249,399Land (Note 7) …………………………………… 10,825 10,981 105,180Construction in progress ……………………… 341 480 3,320

Total property, plant and equipment …… 36,835 35,811 357,900

Intangible assets …………………………………… 3,315 3,269 32,212

Investments and Other Assets:Investments in securities (Notes 6 and 12) … 7,271 6,601 70,649Deferred income tax assets (Note 9) ………… 252 392 2,450Assets for retirement benefits (Note 10)…… 177 - 1,725Other assets …………………………………… 4,208 4,299 40,890Less: Allowance for doubtful accounts ……… (342) (358) (3,328)

Total investments and other assets ……… 11,566 10,935 112,386

Total assets ………………………………… 107,583 99,972 $ 1,045,310

Electronically recorded monetaryclaims-operating (Note 5)……………………

2014 2013 2014

Thousands ofU.S. dollars

Millions of yen (Note 3)

1

The accompanying notes are an integral part of these financial statements.

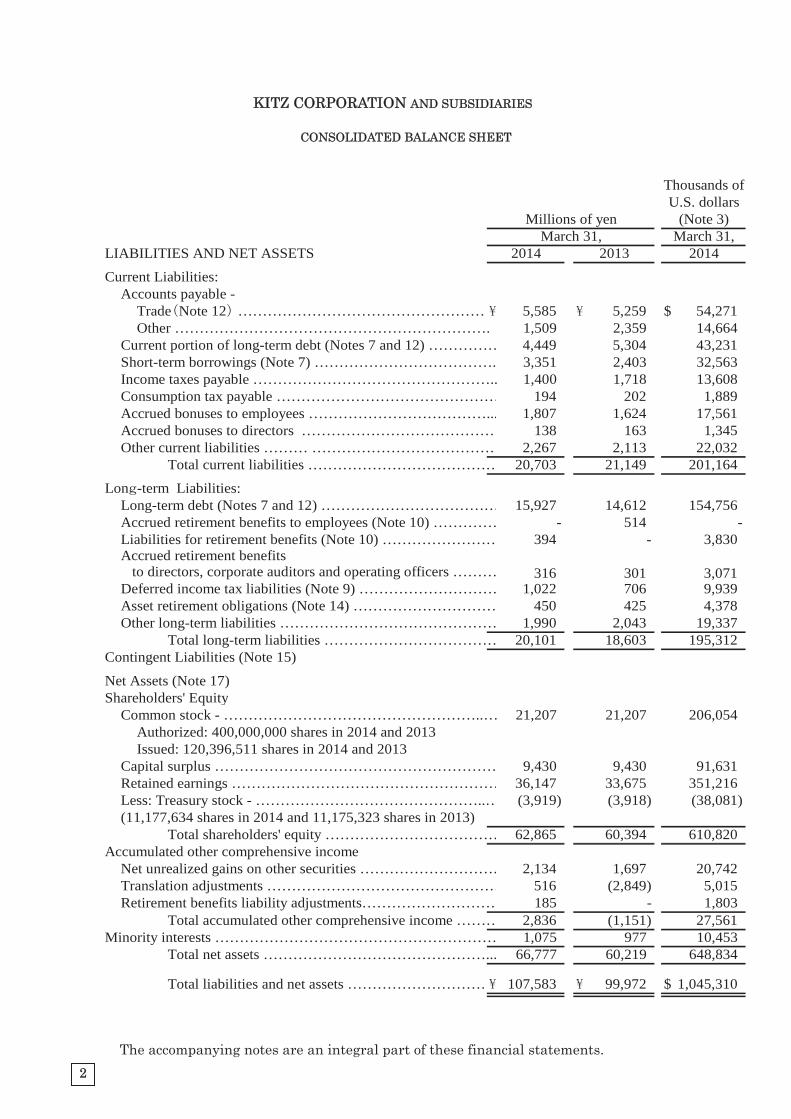

KITZ CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEET

March 31, March 31,LIABILITIES AND NET ASSETS

Current Liabilities:Accounts payable -

Trade Note 12 …………………………………………… 5,585 5,259 $ 54,271Other ………………………………………………………. 1,509 2,359 14,664

Current portion of long-term debt (Notes 7 and 12) …………… 4,449 5,304 43,231Short-term borrowings (Note 7) ………………………………. 3,351 2,403 32,563Income taxes payable ………………………………………….. 1,400 1,718 13,608Consumption tax payable ……………………………………… 194 202 1,889Accrued bonuses to employees ………………………………... 1,807 1,624 17,561Accrued bonuses to directors ………………………………… 138 163 1,345Other current liabilities ……… ………………………………… 2,267 2,113 22,032

Total current liabilities ………………………………… 20,703 21,149 201,164

Lon -term Liabilities:Long-term debt (Notes 7 and 12) ……………………………… 15,927 14,612 154,756Accrued retirement benefits to employees (Note 10) …………… - 514 -Liabilities for retirement benefits (Note 10) …………………… 394 - 3,830Accrued retirement benefits to directors, corporate auditors and operating officers ……… 316 301 3,071Deferred income tax liabilities (Note 9) ………………………… 1,022 706 9,939Asset retirement obligations (Note 14) ………………………… 450 425 4,378Other long-term liabilities ……………………………………… 1,990 2,043 19,337

Total long-term liabilities ……………………………… 20,101 18,603 195,312Contingent Liabilities (Note 15)

Net Assets (Note 17)Shareholders' Equity

Common stock - ……………………………………………..… 21,207 21,207 206,054Authorized: 400,000,000 shares in 2014 and 2013Issued: 120,396,511 shares in 2014 and 2013

Capital surplus ………………………………………………… 9,430 9,430 91,631Retained earnings ……………………………………………… 36,147 33,675 351,216Less: Treasury stock - ………………………………………..… (3,919) (3,918) (38,081)(11,177,634 shares in 2014 and 11,175,323 shares in 2013)

Total shareholders' equity ……………………………… 62,865 60,394 610,820Accumulated other comprehensive income

Net unrealized gains on other securities ………………………… 2,134 1,697 20,742Translation adjustments ………………………………………… 516 (2,849) 5,015Retirement benefits liability adjustments……………………… 185 - 1,803

Total accumulated other comprehensive income ……… 2,836 (1,151) 27,561Minority interests ………………………………………………… 1,075 977 10,453

Total net assets ………………………………………... 66,777 60,219 648,834

Total liabilities and net assets ………………………… 107,583 99,972 $ 1,045,310

2014 2013 2014

Thousands ofU.S. dollars

Millions of yen (Note 3)

2

The accompanying notes are an integral part of these financial statements.

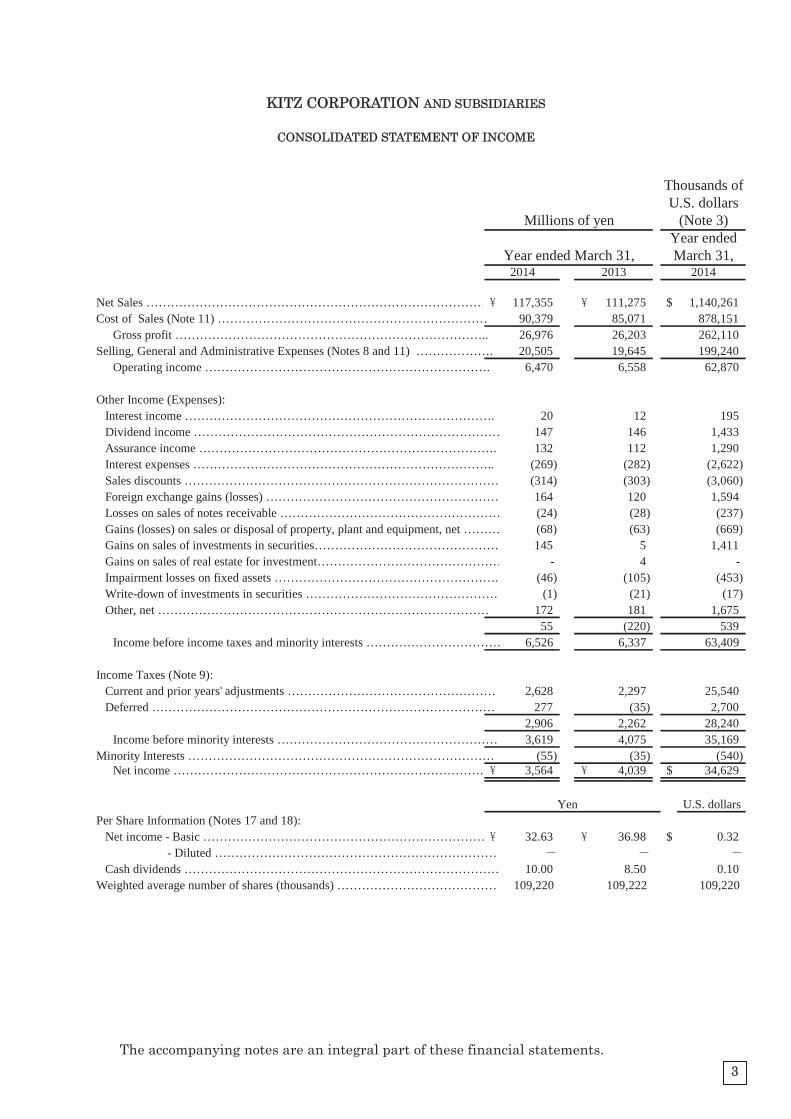

KITZ CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF INCOME

Year endedYear ended March 31, March 31,

Net Sales ………………………………………………………………………… 117,355 111,275 $ 1,140,261Cost of Sales (Note 11) ………………………………………………………… 90,379 85,071 878,151

Gross profit ………………………………………………………………….. 26,976 26,203 262,110Selling, General and Administrative Expenses (Notes 8 and 11) ………………. 20,505 19,645 199,240

Operating income ……………………………………………………………. 6,470 6,558 62,870

Other Income (Expenses):Interest income …………………………………………………………………. 20 12 195Dividend income ………………………………………………………………… 147 146 1,433Assurance income ………………………………………………………………. 132 112 1,290Interest expenses ……………………………………………………………….. (269) (282) (2,622)Sales discounts …………………………………………………………………… (314) (303) (3,060)Foreign exchange gains (losses) ………………………………………………… 164 120 1,594Losses on sales of notes receivable ……………………………………………… (24) (28) (237)Gains (losses) on sales or disposal of property, plant and equipment, net ……… (68) (63) (669)Gains on sales of investments in securities……………………………………… 145 5 1,411Gains on sales of real estate for investment……………………………………… - 4 - Impairment losses on fixed assets ……………………………………………….. (46) (105) (453)Write-down of investments in securities ………………………………………… (1) (21) (17)Other, net ……………………………………………………………………… 172 181 1,675

55 (220) 539Income before income taxes and minority interests …………………………… 6,526 6,337 63,409

Income Taxes (Note 9):Current and prior years' adjustments …………………………………………… 2,628 2,297 25,540Deferred ………………………………………………………………………… 277 (35) 2,700

2,906 2,262 28,240Income before minority interests ……………………………………………… 3,619 4,075 35,169

Minority Interests ………………………………………………………………… (55) (35) (540)Net income …………………………………………………………………… 3,564 4,039 $ 34,629

Yen U.S. dollarsPer Share Information (Notes 17 and 18):

Net income - Basic …………………………………………………………… 32.63 36.98 $ 0.32 - Diluted ……………………………………………………………Cash dividends …………………………………………………………………… 10.00 8.50 0.10

Weighted average number of shares (thousands) ………………………………… 109,220 109,222 109,220

2014 2013 2014

Thousands ofU.S. dollars

Millions of yen (Note 3)

3

The accompanying notes are an integral part of these financial statements.

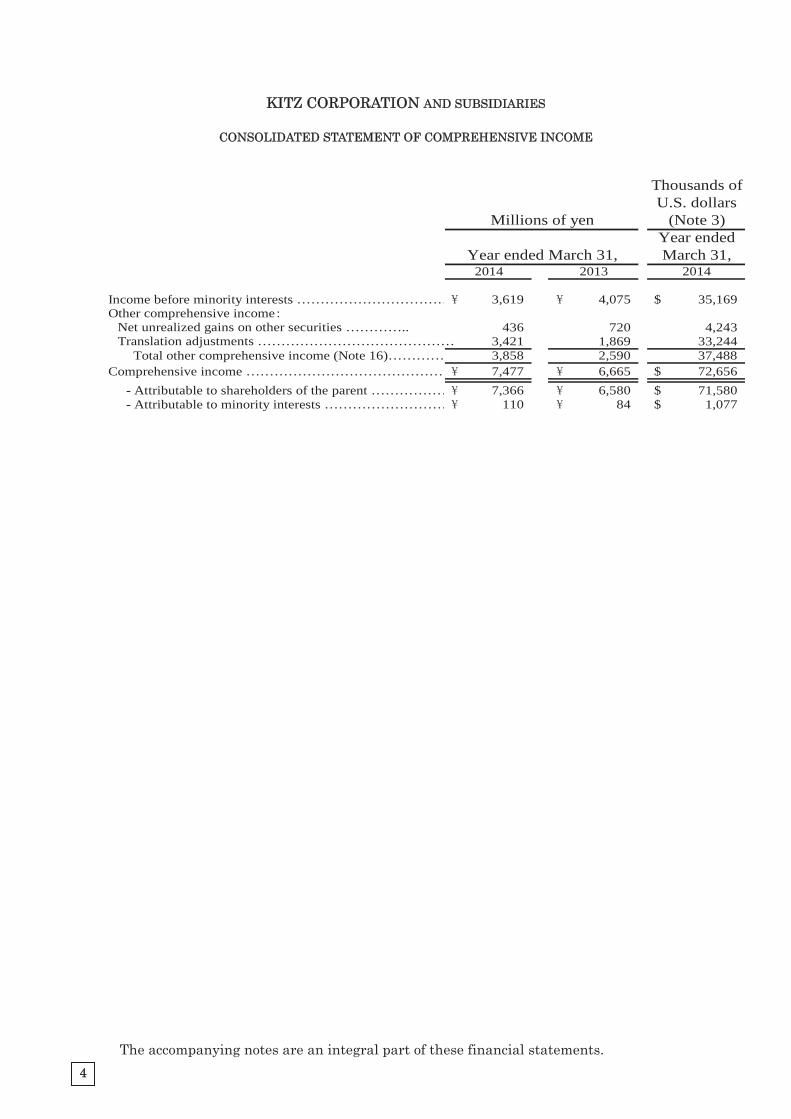

KITZ CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

Year endedYear ended March 31, March 31,

Income before minority interests …………………………… 3,619 4,075 $ 35,169Other comprehensive income

Net unrealized gains on other securities ………….. 436 720 4,243Translation adjustments …………………………………… 3,421 1,869 33,244

Total other comprehensive income (Note 16)………… 3,858 2,590 37,488Comprehensive income …………………………………… 7,477 6,665 $ 72,656 - Attributable to shareholders of the parent ……………… 7,366 6,580 $ 71,580 - Attributable to minority interests ……………………… 110 84 $ 1,077

2014 2013 2014

Thousands ofU.S. dollars

Millions of yen (Note 3)

4

The accompanying notes are an integral part of these financial statements.

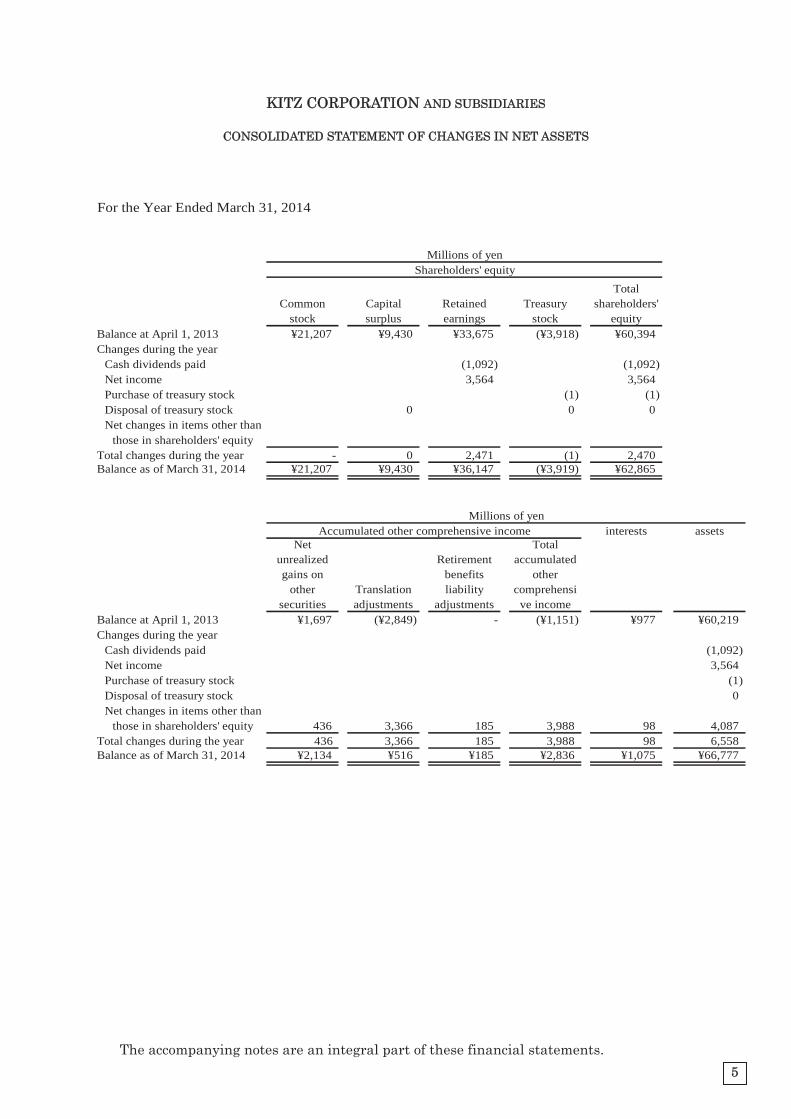

KITZ CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN NET ASSETS

For the Year Ended March 31, 2014

Commonstock

Capitalsurplus

Retainedearnings

Treasurystock

Totalshareholders'

equityBalance at April 1, 2013 ¥21,207 ¥9,430 ¥33,675 (¥3,918) ¥60,394Changes during the year

Cash dividends paid (1,092) (1,092)Net income 3,564 3,564Purchase of treasury stock (1) (1)Disposal of treasury stock 0 0 0Net changes in items other than

those in shareholders' equityTotal changes during the year - 0 2,471 (1) 2,470Balance as of March 31, 2014 ¥21,207 ¥9,430 ¥36,147 (¥3,919) ¥62,865

interests assetsNet

unrealizedgains on

othersecurities

Translationadjustments

Retirementbenefitsliability

adjustments

Totalaccumulated

othercomprehensi

ve incomeBalance at April 1, 2013 ¥1,697 (¥2,849) - (¥1,151) ¥977 ¥60,219Changes during the year

Cash dividends paid (1,092)Net income 3,564Purchase of treasury stock (1)Disposal of treasury stock 0Net changes in items other than

those in shareholders' equity 436 3,366 185 3,988 98 4,087Total changes during the year 436 3,366 185 3,988 98 6,558Balance as of March 31, 2014 ¥2,134 ¥516 ¥185 ¥2,836 ¥1,075 ¥66,777

Millions of yen

Shareholders' equityMillions of yen

Accumulated other comprehensive income

5

The accompanying notes are an integral part of these financial statements.

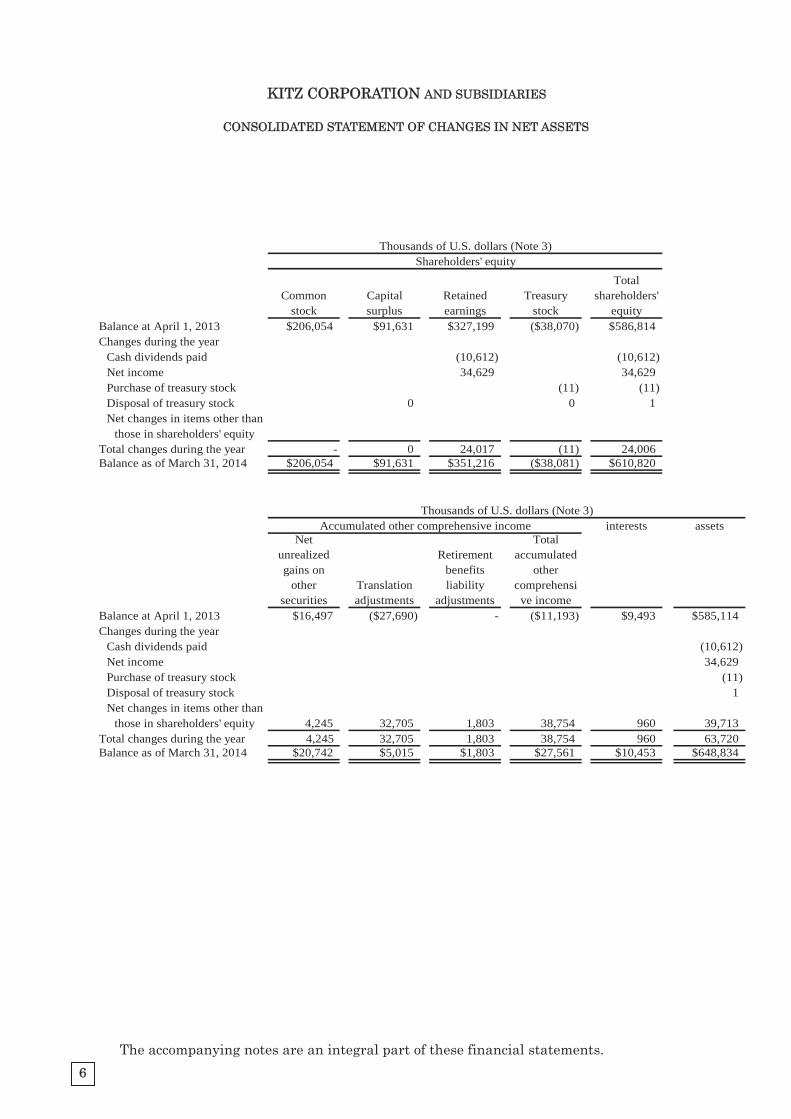

KITZ CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN NET ASSETS

Commonstock

Capitalsurplus

Retainedearnings

Treasurystock

Totalshareholders'

equityBalance at April 1, 2013 $206,054 $91,631 $327,199 ($38,070) $586,814Changes during the year

Cash dividends paid (10,612) (10,612)Net income 34,629 34,629Purchase of treasury stock (11) (11)Disposal of treasury stock 0 0 1Net changes in items other than

those in shareholders' equityTotal changes during the year - 0 24,017 (11) 24,006Balance as of March 31, 2014 $206,054 $91,631 $351,216 ($38,081) $610,820

interests assetsNet

unrealizedgains on

othersecurities

Translationadjustments

Retirementbenefitsliability

adjustments

Totalaccumulated

othercomprehensi

ve incomeBalance at April 1, 2013 $16,497 ($27,690) - ($11,193) $9,493 $585,114Changes during the year

Cash dividends paid (10,612)Net income 34,629Purchase of treasury stock (11)Disposal of treasury stock 1Net changes in items other than

those in shareholders' equity 4,245 32,705 1,803 38,754 960 39,713Total changes during the year 4,245 32,705 1,803 38,754 960 63,720Balance as of March 31, 2014 $20,742 $5,015 $1,803 $27,561 $10,453 $648,834

Thousands of U.S. dollars (Note 3)Accumulated other comprehensive income

Thousands of U.S. dollars (Note 3)Shareholders' equity

6

The accompanying notes are an integral part of these financial statements.

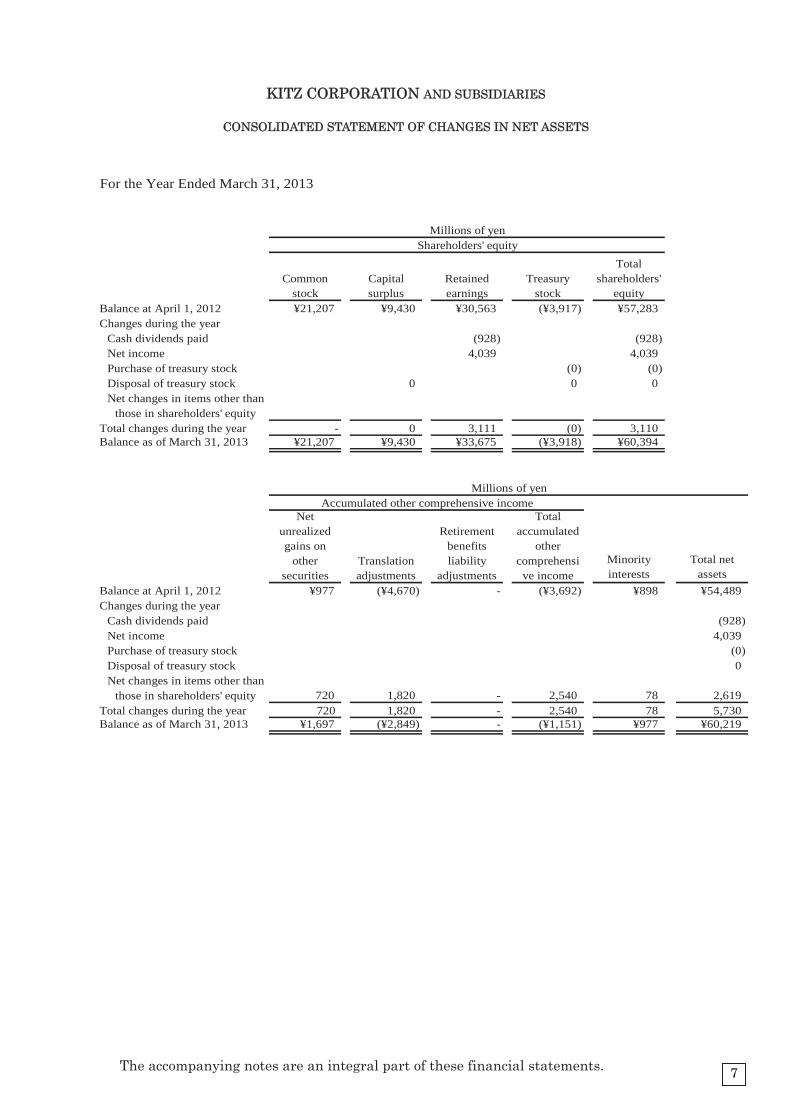

KITZ CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN NET ASSETS

For the Year Ended March 31, 2013

Commonstock

Capitalsurplus

Retainedearnings

Treasurystock

Totalshareholders'

equityBalance at April 1, 2012 ¥21,207 ¥9,430 ¥30,563 (¥3,917) ¥57,283Changes during the year

Cash dividends paid (928) (928)Net income 4,039 4,039Purchase of treasury stock (0) (0)Disposal of treasury stock 0 0 0Net changes in items other than

those in shareholders' equityTotal changes during the year - 0 3,111 (0) 3,110Balance as of March 31, 2013 ¥21,207 ¥9,430 ¥33,675 (¥3,918) ¥60,394

Netunrealizedgains on

othersecurities

Translationadjustments

Retirementbenefitsliability

adjustments

Totalaccumulated

othercomprehensi

ve incomeBalance at April 1, 2012 ¥977 (¥4,670) - (¥3,692) ¥898 ¥54,489Changes during the year

Cash dividends paid (928)Net income 4,039Purchase of treasury stock (0)Disposal of treasury stock 0Net changes in items other than

those in shareholders' equityTotal changes during the year 720 1,820 - 2,540 78 5,730Balance as of March 31, 2013 ¥1,697 (¥2,849) - (¥1,151) ¥977 ¥60,219

720 1,820 - 2,540 78 2,619

Total netassets

Millions of yen

Shareholders' equityMillions of yen

Accumulated other comprehensive income

Minorityinterests

7

The accompanying notes are an integral part of these financial statements.

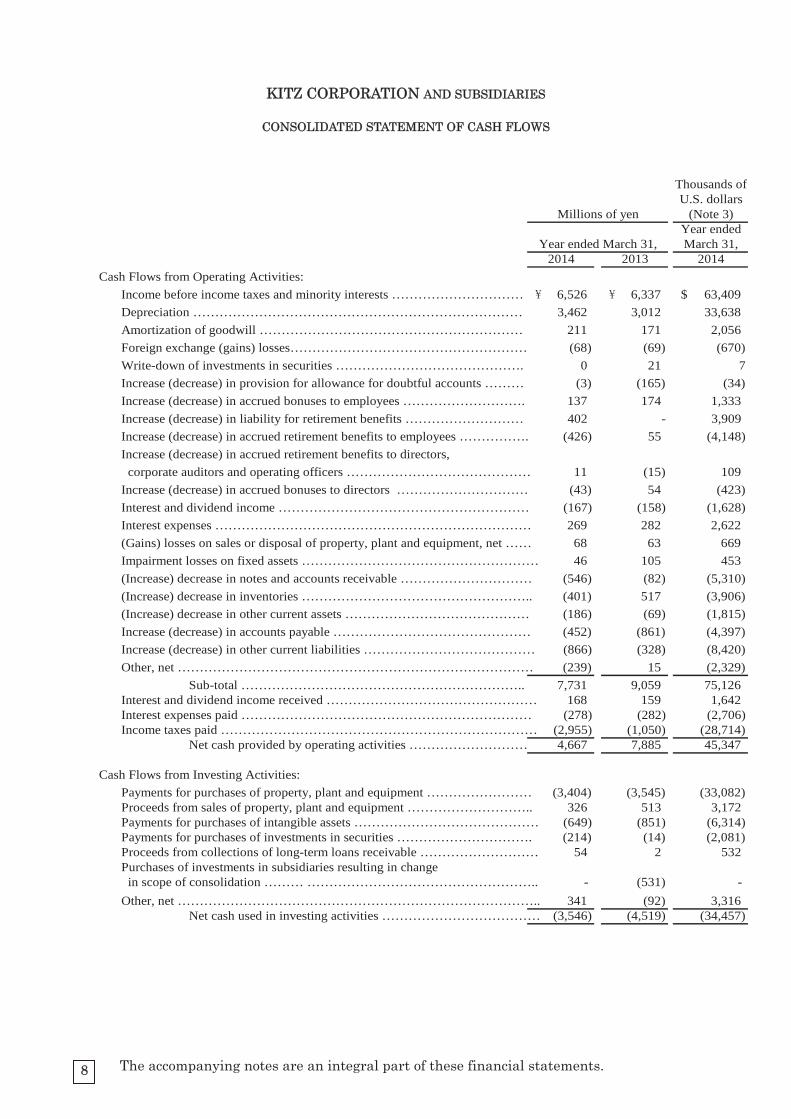

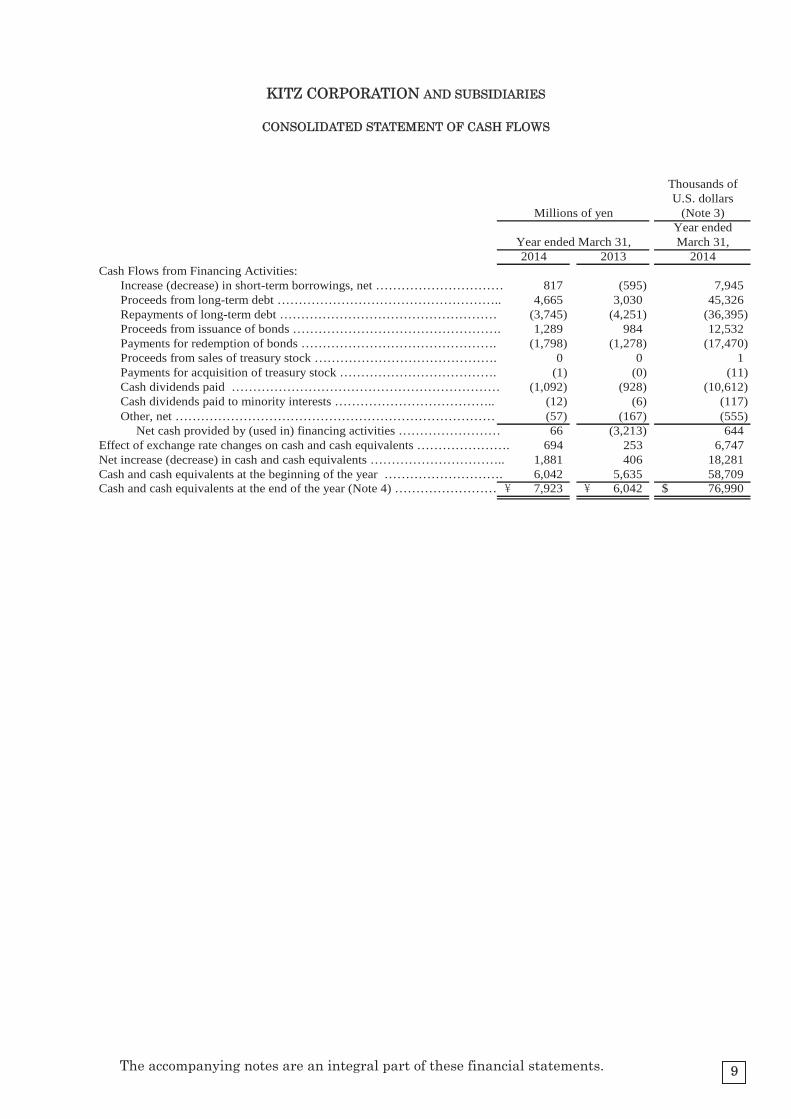

KITZ CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CASH FLOWS

Year endedYear ended March 31, March 31,

Cash Flows from Operating Activities:Income before income taxes and minority interests ………………………… 6,526 6,337 $ 63,409Depreciation ………………………………………………………………… 3,462 3,012 33,638Amortization of goodwill …………………………………………………… 211 171 2,056Foreign exchange (gains) losses……………………………………………… (68) (69) (670)Write-down of investments in securities ……………………………………. 0 21 7Increase (decrease) in provision for allowance for doubtful accounts ……… (3) (165) (34)Increase (decrease) in accrued bonuses to employees ………………………. 137 174 1,333Increase (decrease) in liability for retirement benefits ……………………… 402 - 3,909Increase (decrease) in accrued retirement benefits to employees ……………. (426) 55 (4,148)Increase (decrease) in accrued retirement benefits to directors, corporate auditors and operating officers …………………………………… 11 (15) 109Increase (decrease) in accrued bonuses to directors ………………………… (43) 54 (423)Interest and dividend income ………………………………………………… (167) (158) (1,628)Interest expenses ……………………………………………………………… 269 282 2,622(Gains) losses on sales or disposal of property, plant and equipment, net …… 68 63 669Impairment losses on fixed assets ……………………………………………… 46 105 453(Increase) decrease in notes and accounts receivable ………………………… (546) (82) (5,310)(Increase) decrease in inventories …………………………………………….. (401) 517 (3,906)(Increase) decrease in other current assets …………………………………… (186) (69) (1,815)Increase (decrease) in accounts payable ……………………………………… (452) (861) (4,397)Increase (decrease) in other current liabilities ………………………………… (866) (328) (8,420)Other, net ……………………………………………………………………… (239) 15 (2,329)

Sub-total ……………………………………………………….. 7,731 9,059 75,126Interest and dividend income received ………………………………………… 168 159 1,642Interest expenses paid ………………………………………………………… (278) (282) (2,706)Income taxes paid ……………………………………………………………… (2,955) (1,050) (28,714)

Net cash provided by operating activities ……………………… 4,667 7,885 45,347

Cash Flows from Investing Activities:Payments for purchases of property, plant and equipment …………………… (3,404) (3,545) (33,082)Proceeds from sales of property, plant and equipment ……………………….. 326 513 3,172Payments for purchases of intangible assets …………………………………… (649) (851) (6,314)Payments for purchases of investments in securities …………………………. (214) (14) (2,081)Proceeds from collections of long-term loans receivable ……………………… 54 2 532Purchases of investments in subsidiaries resulting in change in scope of consolidation ……… …………………………………………….. - (531) - Other, net ……………………………………………………………………….. 341 (92) 3,316

Net cash used in investing activities ……………………………… (3,546) (4,519) (34,457)

2014 2013 2014

Thousands ofU.S. dollars

Millions of yen (Note 3)

8

The accompanying notes are an integral part of these financial statements.

KITZ CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CASH FLOWS

Year endedYear ended March 31, March 31,

Cash Flows from Financing Activities:Increase (decrease) in short-term borrowings, net ………………………… 817 (595) 7,945Proceeds from long-term debt …………………………………………….. 4,665 3,030 45,326Repayments of long-term debt …………………………………………… (3,745) (4,251) (36,395)Proceeds from issuance of bonds …………………………………………. 1,289 984 12,532Payments for redemption of bonds ………………………………………. (1,798) (1,278) (17,470)Proceeds from sales of treasury stock ……………………………………. 0 0 1Payments for acquisition of treasury stock ………………………………. (1) (0) (11)Cash dividends paid ……………………………………………………… (1,092) (928) (10,612)Cash dividends paid to minority interests ……………………………….. (12) (6) (117)Other, net ………………………………………………………………… (57) (167) (555)

Net cash provided by (used in) financing activities …………………… 66 (3,213) 644Effect of exchange rate changes on cash and cash equivalents …………………. 694 253 6,747Net increase (decrease) in cash and cash equivalents ………………………….. 1,881 406 18,281Cash and cash equivalents at the beginning of the year ………………………. 6,042 5,635 58,709Cash and cash equivalents at the end of the year (Note 4) …………………… 7,923 6,042 $ 76,990

2014 2013 2014

Thousands ofU.S. dollars

Millions of yen (Note 3)

9

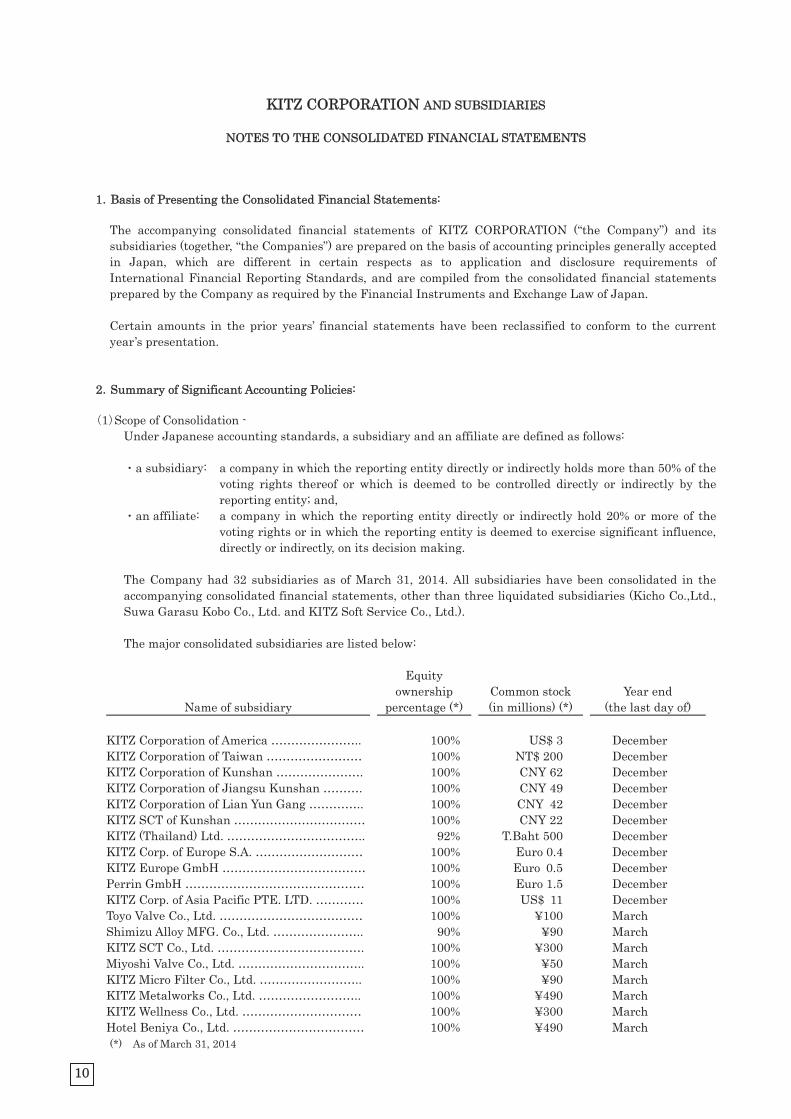

KITZ CORPORATION AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

1 Basis of Presenting the Consolidated Financial Statements:

The accompanying consolidated financial statements of KITZ CORPORATION (“the Company”) and its subsidiaries (together, “the Companies”) are prepared on the basis of accounting principles generally accepted in Japan, which are different in certain respects as to application and disclosure requirements of International Financial Reporting Standards, and are compiled from the consolidated financial statements prepared by the Company as required by the Financial Instruments and Exchange Law of Japan. Certain amounts in the prior years’ financial statements have been reclassified to conform to the current year’s presentation.

2 Summary of Significant Accounting Policies:

1 Scope of Consolidation - Under Japanese accounting standards, a subsidiary and an affiliate are defined as follows:

a subsidiary: a company in which the reporting entity directly or indirectly holds more than 50% of the

voting rights thereof or which is deemed to be controlled directly or indirectly by the reporting entity; and,

an affiliate: a company in which the reporting entity directly or indirectly hold 20% or more of the voting rights or in which the reporting entity is deemed to exercise significant influence, directly or indirectly, on its decision making.

The Company had 32 subsidiaries as of March 31, 2014. All subsidiaries have been consolidated in the accompanying consolidated financial statements, other than three liquidated subsidiaries (Kicho Co.,Ltd., Suwa Garasu Kobo Co., Ltd. and KITZ Soft Service Co., Ltd.).

The major consolidated subsidiaries are listed below:

Name of subsidiary

Equity ownership

percentage (*)Common stock (in millions) (*)

Year end (the last day of)

KITZ Corporation of America ………………….. 100% US$ 3 December KITZ Corporation of Taiwan …………………… 100% NT$ 200 December KITZ Corporation of Kunshan …………………. 100% CNY 62 December KITZ Corporation of Jiangsu Kunshan ………. 100% CNY 49 December KITZ Corporation of Lian Yun Gang ………….. 100% CNY 42 December KITZ SCT of Kunshan …………………………… 100% CNY 22 December KITZ (Thailand) Ltd. …………………………….. 92% T.Baht 500 December KITZ Corp. of Europe S.A. ……………………… 100% Euro 0.4 December KITZ Europe GmbH ……………………………… 100% Euro 0.5 December Perrin GmbH ……………………………………… 100% Euro 1.5 December KITZ Corp. of Asia Pacific PTE. LTD. ………… 100% US$ 11 December Toyo Valve Co., Ltd. ……………………………… 100% ¥100 March Shimizu Alloy MFG. Co., Ltd. ………………….. 90% ¥90 March KITZ SCT Co., Ltd. ………………………………. 100% ¥300 March Miyoshi Valve Co., Ltd. ………………………….. 100% ¥50 March KITZ Micro Filter Co., Ltd. …………………….. 100% ¥90 March KITZ Metalworks Co., Ltd. …………………….. 100% ¥490 March KITZ Wellness Co., Ltd. ………………………… 100% ¥300 March Hotel Beniya Co., Ltd. …………………………… 100% ¥490 March (*) As of March 31, 2014

10

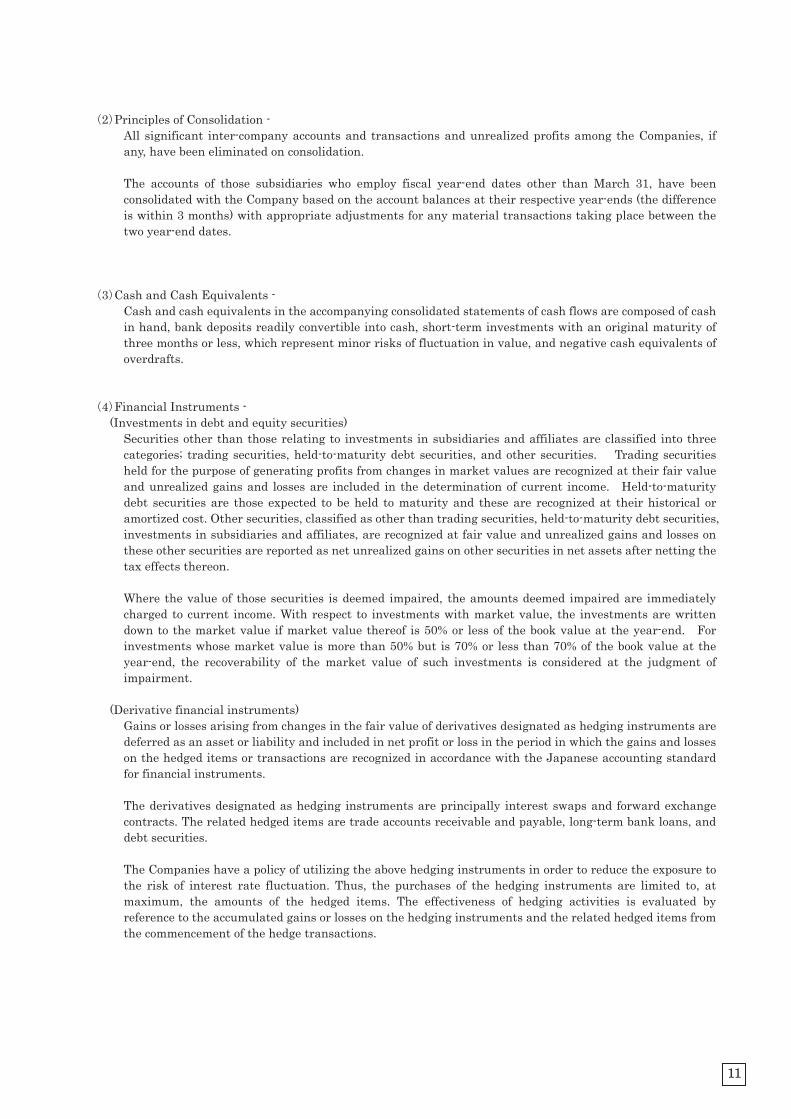

2 Principles of Consolidation -

All significant inter-company accounts and transactions and unrealized profits among the Companies, if any, have been eliminated on consolidation. The accounts of those subsidiaries who employ fiscal year-end dates other than March 31, have been consolidated with the Company based on the account balances at their respective year-ends (the difference is within 3 months) with appropriate adjustments for any material transactions taking place between the two year-end dates.

3 Cash and Cash Equivalents -

Cash and cash equivalents in the accompanying consolidated statements of cash flows are composed of cash in hand, bank deposits readily convertible into cash, short-term investments with an original maturity of three months or less, which represent minor risks of fluctuation in value, and negative cash equivalents of overdrafts.

4 Financial Instruments -

(Investments in debt and equity securities) Securities other than those relating to investments in subsidiaries and affiliates are classified into three categories; trading securities, held-to-maturity debt securities, and other securities. Trading securities held for the purpose of generating profits from changes in market values are recognized at their fair value and unrealized gains and losses are included in the determination of current income. Held-to-maturity debt securities are those expected to be held to maturity and these are recognized at their historical or amortized cost. Other securities, classified as other than trading securities, held-to-maturity debt securities, investments in subsidiaries and affiliates, are recognized at fair value and unrealized gains and losses on these other securities are reported as net unrealized gains on other securities in net assets after netting the tax effects thereon. Where the value of those securities is deemed impaired, the amounts deemed impaired are immediately charged to current income. With respect to investments with market value, the investments are written down to the market value if market value thereof is 50% or less of the book value at the year-end. For investments whose market value is more than 50% but is 70% or less than 70% of the book value at the year-end, the recoverability of the market value of such investments is considered at the judgment of impairment.

(Derivative financial instruments)

Gains or losses arising from changes in the fair value of derivatives designated as hedging instruments are deferred as an asset or liability and included in net profit or loss in the period in which the gains and losses on the hedged items or transactions are recognized in accordance with the Japanese accounting standard for financial instruments. The derivatives designated as hedging instruments are principally interest swaps and forward exchange contracts. The related hedged items are trade accounts receivable and payable, long-term bank loans, and debt securities. The Companies have a policy of utilizing the above hedging instruments in order to reduce the exposure to the risk of interest rate fluctuation. Thus, the purchases of the hedging instruments are limited to, at maximum, the amounts of the hedged items. The effectiveness of hedging activities is evaluated by reference to the accumulated gains or losses on the hedging instruments and the related hedged items from the commencement of the hedge transactions.

11

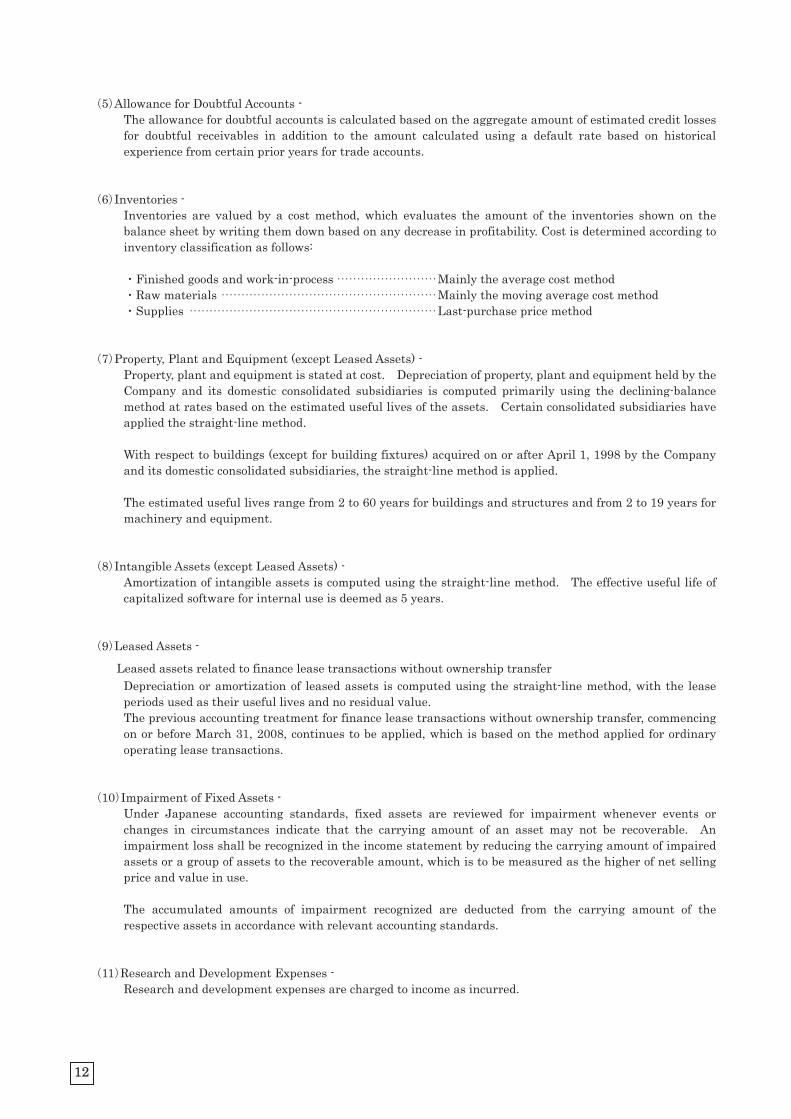

5 Allowance for Doubtful Accounts - The allowance for doubtful accounts is calculated based on the aggregate amount of estimated credit losses for doubtful receivables in addition to the amount calculated using a default rate based on historical experience from certain prior years for trade accounts.

6 Inventories -

Inventories are valued by a cost method, which evaluates the amount of the inventories shown on the balance sheet by writing them down based on any decrease in profitability. Cost is determined according to inventory classification as follows:

Finished goods and work-in-process ························· Mainly the average cost method Raw materials ······················································ Mainly the moving average cost method Supplies ······························································ Last-purchase price method

7 Property, Plant and Equipment (except Leased Assets) -

Property, plant and equipment is stated at cost. Depreciation of property, plant and equipment held by the Company and its domestic consolidated subsidiaries is computed primarily using the declining-balance method at rates based on the estimated useful lives of the assets. Certain consolidated subsidiaries have applied the straight-line method. With respect to buildings (except for building fixtures) acquired on or after April 1, 1998 by the Company and its domestic consolidated subsidiaries, the straight-line method is applied. The estimated useful lives range from 2 to 60 years for buildings and structures and from 2 to 19 years for machinery and equipment.

8 Intangible Assets (except Leased Assets) -

Amortization of intangible assets is computed using the straight-line method. The effective useful life of capitalized software for internal use is deemed as 5 years.

9 Leased Assets -

Leased assets related to finance lease transactions without ownership transfer Depreciation or amortization of leased assets is computed using the straight-line method, with the lease periods used as their useful lives and no residual value. The previous accounting treatment for finance lease transactions without ownership transfer, commencing on or before March 31, 2008, continues to be applied, which is based on the method applied for ordinary operating lease transactions.

10 Impairment of Fixed Assets -

Under Japanese accounting standards, fixed assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. An impairment loss shall be recognized in the income statement by reducing the carrying amount of impaired assets or a group of assets to the recoverable amount, which is to be measured as the higher of net selling price and value in use. The accumulated amounts of impairment recognized are deducted from the carrying amount of the respective assets in accordance with relevant accounting standards.

11 Research and Development Expenses - Research and development expenses are charged to income as incurred.

12

12 Deferred Charges - Bond issuance expenses are charged to income as incurred.

13 Income Taxes -

Income taxes of the Company and its domestic subsidiaries and affiliates mainly consist of corporate income taxes, municipal inhabitants’ taxes and enterprise taxes. Income taxes are determined using the asset and liability approach, whereby deferred tax assets and liabilities are recognized in respect of temporary differences between the tax basis of assets and liabilities and those as reported in the financial statements as well as losses carried forward for the tax purposes. The Company files a consolidated tax return for corporate income taxes. All 100% owned domestic subsidiaries are included in the consolidated tax return and those subsidiaries other than 100% owned domestic subsidiaries file their tax returns separately.

14 Accrued Bonuses to Employees -

Accrued bonuses to employees are provided for the amount attributable to each fiscal year calculated based on the estimated bonus payments.

15 Accrued Bonuses to Directors -

Accrued bonuses to directors are provided for the estimated bonus payments based on operating results for fiscal year.

16 Accrued Retirement Benefits to Directors, Corporate Auditors and Operating Officers -

In Japan, directors and corporate auditors are customarily paid a lump-sum upon their retirement which is subject to the prior approval of shareholders at the annual general meeting. For the proper calculation of the profit for the period, an accounting policy of recognizing such retirement benefits on an accrual basis has been employed as general practice in Japan provided that approved internal rules have been established.

17 Accounting Method of Retirement Benefits

Accrued retirement and prepaid pension cost for employees have been recorded mainly at the amount calculated based on the retirement benefit obligation and the fair value of the pension plan assets as of the balance sheet date. The retirement benefit obligation for employees is attributed to each period by the straight-line method over the estimated years of service of the eligible employees. Actuarial gain or loss is amortized in the year following the year in which the gain or loss is recognized primarily by the straight-line method over periods (5 years), which are shorter than the average remaining years of service of the employees. Certain foreign consolidated subsidiaries have adopted the corridor approach for the amortization of actuarial gain and loss. Prior service cost is being amortized as incurred by the straight-line method over periods (5 years), which are shorter than the average remaining years of service of the employees. Unrecognized actuarial differences and unrecognized prior service cost are recorded as retirement benefit liability adjustments in accumulated other comprehensive income within net assets after adjusting for tax effects. Certain consolidated subsidiaries have adopted the simplified method of calculating the retirement benefit obligation and costs.

18 Consumption Taxes -

Transactions subject to consumption taxes are recorded at amounts excluding consumption taxes.

13

19 Amortization of Goodwill - Goodwill is amortized on a straight-line basis over its estimated useful life. Amortization is calculated mainly over 10 years.

20 Other - (Changes in Accounting Policies) (Adoption of Accounting Standard for Retirement Benefits) The Company adopted “Accounting Standard for Retirement Benefits” (ASBJ Statement No.26, May 17, 2012) and “Guidance on Accounting Standard for Retirement Benefits” (ASBJ Guidance No.25, May 17, 2012) (except the provisions of the main clause of section 35 of the standard and of the main clause of section 67 of the guidance) as of the end of the year ended March 31, 2014. As a result of this change, an asset and a liability for retirement benefits were recognized in the amounts of ¥177 million ($1,725 thousand) and ¥394 million ($3,830 thousand), respectively, and accumulated other comprehensive income increased by ¥185 million ($1,803 thousand) as of March 31, 2014. The effect on net assets per share is described in Note 18.

(Standards Issued but Not Yet Effective) “Accounting Standard for Retirement Benefits” (ASBJ Statement No.26, May 17, 2012) and “Guidance on Accounting Standard for Retirement Benefits” (ASBJ Guidance No.25, May 17, 2012)

1. Overview

The standard provides guidance for the accounting for unrecognized actuarial differences and unrecognized prior service costs, the calculation methods for the retirement benefit obligation and service costs, and enhancement of disclosures taking into consideration improvements to financial reporting and international trends.

2. Scheduled date for adoption The revised accounting standard and guidance were adopted as of the end of the year ended March 31,

2014. However, revisions to the calculation methods for the retirement benefit obligation and service costs are scheduled to be adopted from the beginning of the year ending March 31, 2015.

3. Effects of the adoption of the accounting standard and guidance The Company is currently evaluating the effect these modifications of the calculation methods for the

retirement benefit obligation and service costs will have on its consolidated results of operations and financial position.

3 U.S. Dollar Amounts:

Amounts in U.S. dollars are included solely for the convenience of readers outside Japan. The rate of ¥102.92= US$1, the approximate rate of exchange prevailing at March 31, 2014 has been used in translation. The inclusion of such amounts is not intended to imply that Japanese yen have been or could be readily converted, realized or settled in U.S. dollars at this rate or any other rates. Japanese yen and U.S. dollars amounts of less than ¥1 million and US$1 thousand in the consolidated financial statements and the accompanying notes are rounded off.

14

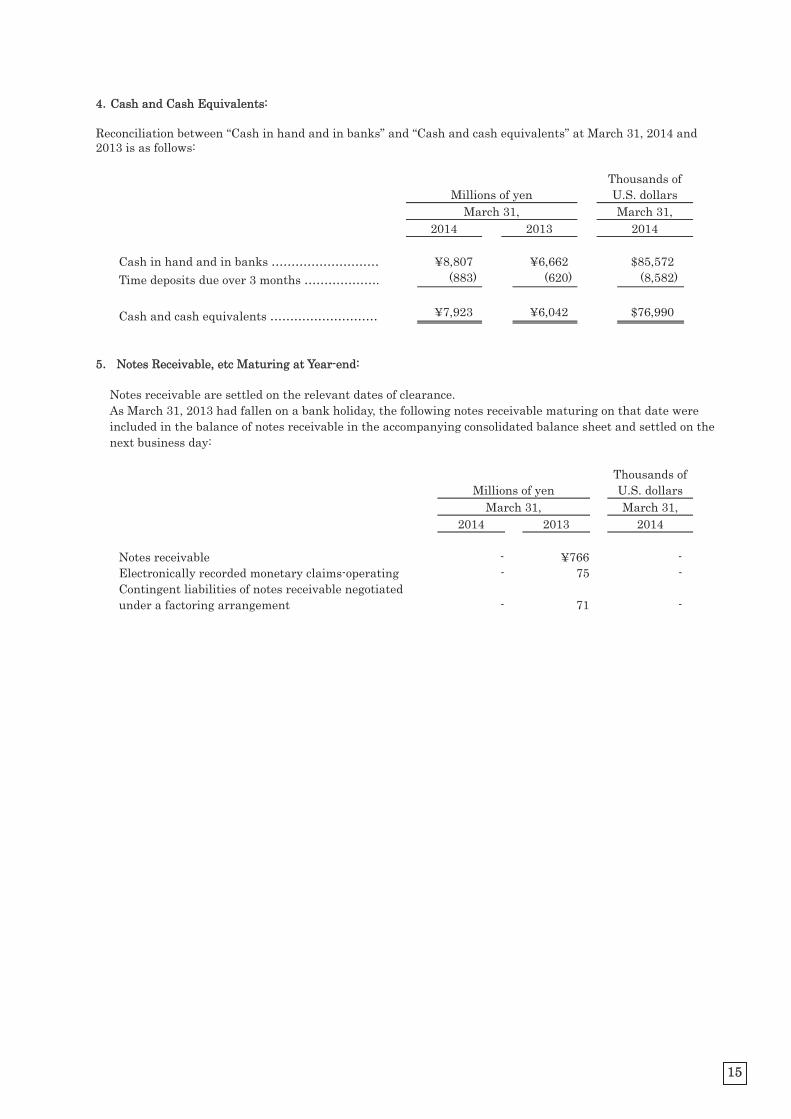

4 Cash and Cash Equivalents:

Reconciliation between “Cash in hand and in banks” and “Cash and cash equivalents” at March 31, 2014 and 2013 is as follows:

Millions of yen Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014

Cash in hand and in banks ……………………… ¥8,807 ¥6,662 $85,572 Time deposits due over 3 months ………………. (883) (620) (8,582) Cash and cash equivalents ……………………… ¥7,923 ¥6,042 $76,990

5 Notes Receivable, etc Maturing at Year-end:

Notes receivable are settled on the relevant dates of clearance. As March 31, 2013 had fallen on a bank holiday, the following notes receivable maturing on that date were included in the balance of notes receivable in the accompanying consolidated balance sheet and settled on the next business day:

Millions of yen Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014

Notes receivable - ¥766 -Electronically recorded monetary claims-operating - 75 -Contingent liabilities of notes receivable negotiated under a factoring arrangement - 71 -

15

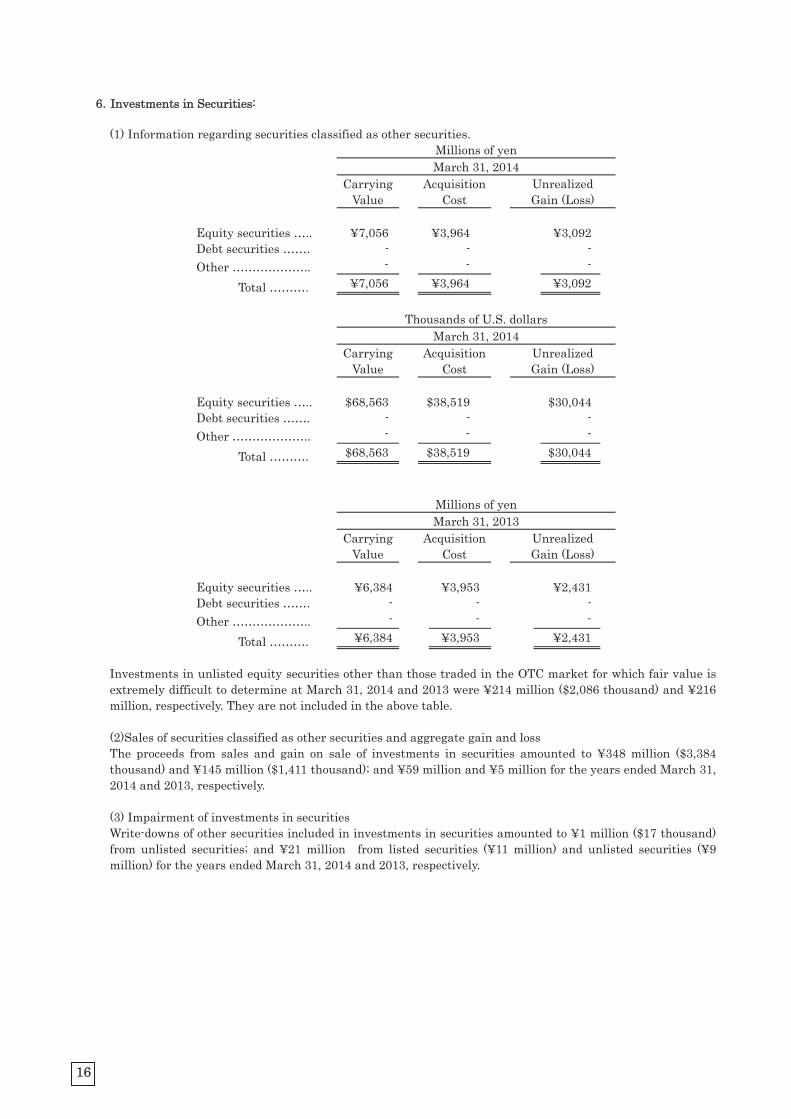

6 Investments in Securities:

(1) Information regarding securities classified as other securities. Millions of yen March 31, 2014

Carrying

Value Acquisition

Cost Unrealized Gain (Loss)

Equity securities ….. ¥7,056 ¥3,964 ¥3,092 Debt securities ……. - - - Other ……………….. - - -

Total ………. ¥7,056 ¥3,964 ¥3,092

Thousands of U.S. dollars March 31, 2014

Carrying

Value Acquisition

Cost Unrealized Gain (Loss)

Equity securities ….. $68,563 $38,519 $30,044 Debt securities ……. - - - Other ……………….. - - -

Total ………. $68,563 $38,519 $30,044

Millions of yen March 31, 2013

Carrying

Value Acquisition

Cost Unrealized Gain (Loss)

Equity securities ….. ¥6,384 ¥3,953 ¥2,431 Debt securities ……. - - - Other ……………….. - - -

Total ………. ¥6,384 ¥3,953 ¥2,431

Investments in unlisted equity securities other than those traded in the OTC market for which fair value is extremely difficult to determine at March 31, 2014 and 2013 were ¥214 million ($2,086 thousand) and ¥216 million, respectively. They are not included in the above table. (2)Sales of securities classified as other securities and aggregate gain and loss The proceeds from sales and gain on sale of investments in securities amounted to ¥348 million ($3,384 thousand) and ¥145 million ($1,411 thousand); and ¥59 million and ¥5 million for the years ended March 31, 2014 and 2013, respectively. (3) Impairment of investments in securities Write-downs of other securities included in investments in securities amounted to ¥1 million ($17 thousand) from unlisted securities; and ¥21 million from listed securities (¥11 million) and unlisted securities (¥9 million) for the years ended March 31, 2014 and 2013, respectively.

16

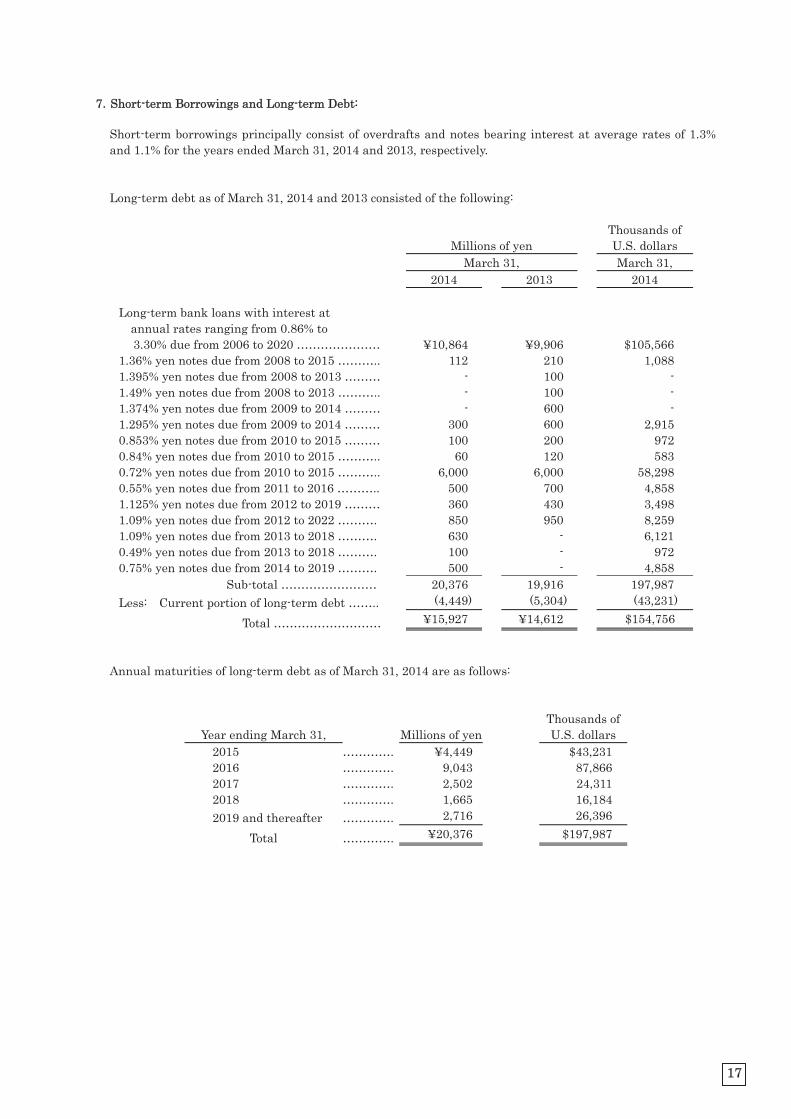

7 Short-term Borrowings and Long-term Debt:

Short-term borrowings principally consist of overdrafts and notes bearing interest at average rates of 1.3% and 1.1% for the years ended March 31, 2014 and 2013, respectively. Long-term debt as of March 31, 2014 and 2013 consisted of the following:

Millions of yen Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014

Long-term bank loans with interest at

annual rates ranging from 0.86% to 3.30% due from 2006 to 2020 ………………… ¥10,864 ¥9,906 $105,566

1.36% yen notes due from 2008 to 2015 ……….. 112 210 1,088 1.395% yen notes due from 2008 to 2013 ……… - 100 - 1.49% yen notes due from 2008 to 2013 ……….. - 100 - 1.374% yen notes due from 2009 to 2014 ……… - 600 - 1.295% yen notes due from 2009 to 2014 ……… 300 600 2,915 0.853% yen notes due from 2010 to 2015 ……… 100 200 972 0.84% yen notes due from 2010 to 2015 ……….. 60 120 583 0.72% yen notes due from 2010 to 2015 ……….. 6,000 6,000 58,298 0.55% yen notes due from 2011 to 2016 ……….. 500 700 4,858 1.125% yen notes due from 2012 to 2019 ……… 360 430 3,498 1.09% yen notes due from 2012 to 2022 ………. 850 950 8,259 1.09% yen notes due from 2013 to 2018 ………. 630 - 6,121 0.49% yen notes due from 2013 to 2018 ………. 100 - 972 0.75% yen notes due from 2014 to 2019 ………. 500 - 4,858

Sub-total …………………… 20,376 19,916 197,987 Less: Current portion of long-term debt …….. (4,449) (5,304) (43,231)

Total ……………………… ¥15,927 ¥14,612 $154,756 Annual maturities of long-term debt as of March 31, 2014 are as follows:

Year ending March 31, Millions of yen Thousands of U.S. dollars

2015 …………. ¥4,449 $43,231 2016 …………. 9,043 87,866 2017 …………. 2,502 24,311 2018 …………. 1,665 16,184 2019 and thereafter …………. 2,716 26,396

Total …………. ¥20,376 $197,987

17

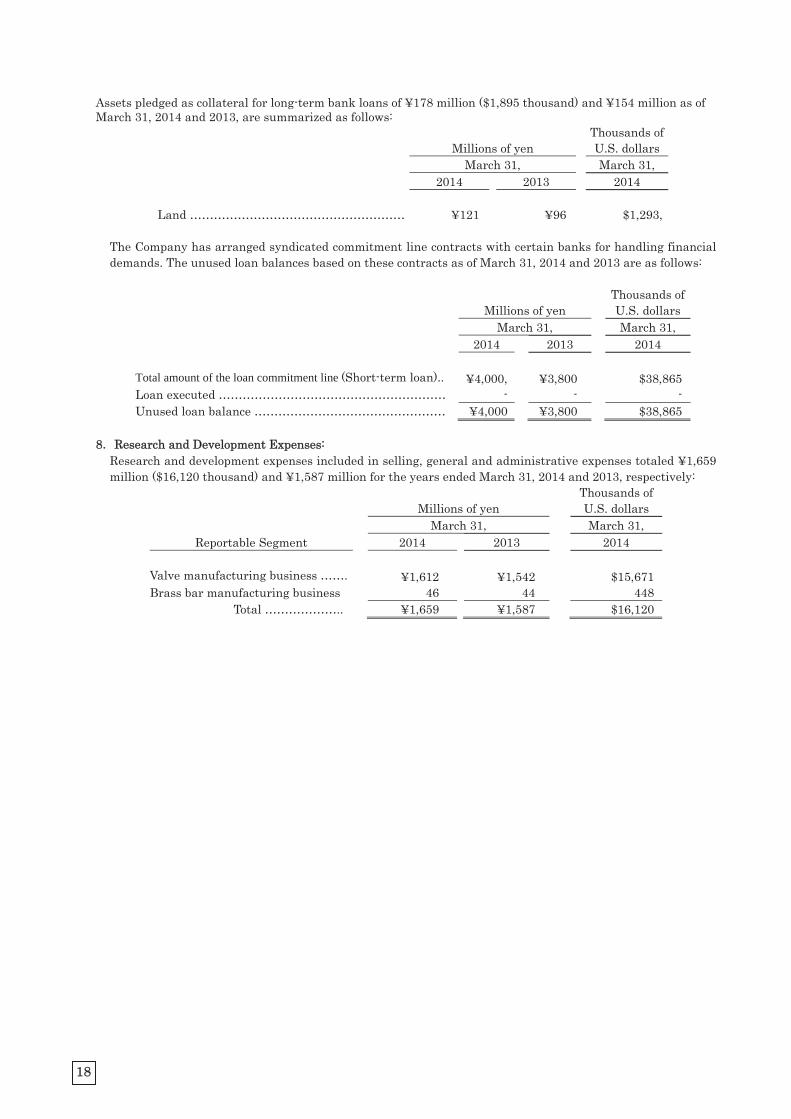

Assets pledged as collateral for long-term bank loans of ¥178 million ($1,895 thousand) and ¥154 million as of March 31, 2014 and 2013, are summarized as follows:

Millions of yen

Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014

Land ……………………………………………… ¥121 ¥96 $1,293, The Company has arranged syndicated commitment line contracts with certain banks for handling financial demands. The unused loan balances based on these contracts as of March 31, 2014 and 2013 are as follows:

Millions of yen Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014

Total amount of the loan commitment line (Short-term loan).. ¥4,000, ¥3,800 $38,865Loan executed ………………………………………………… - - -Unused loan balance ………………………………………… ¥4,000 ¥3,800 $38,865

8 Research and Development Expenses:

Research and development expenses included in selling, general and administrative expenses totaled ¥1,659 million ($16,120 thousand) and ¥1,587 million for the years ended March 31, 2014 and 2013, respectively:

Millions of yen

Thousands of U.S. dollars

March 31, March 31, Reportable Segment 2014 2013 2014

Valve manufacturing business ……. ¥1,612 ¥1,542 $15,671Brass bar manufacturing business 46 44 448

Total ……………….. ¥1,659 ¥1,587 $16,120

18

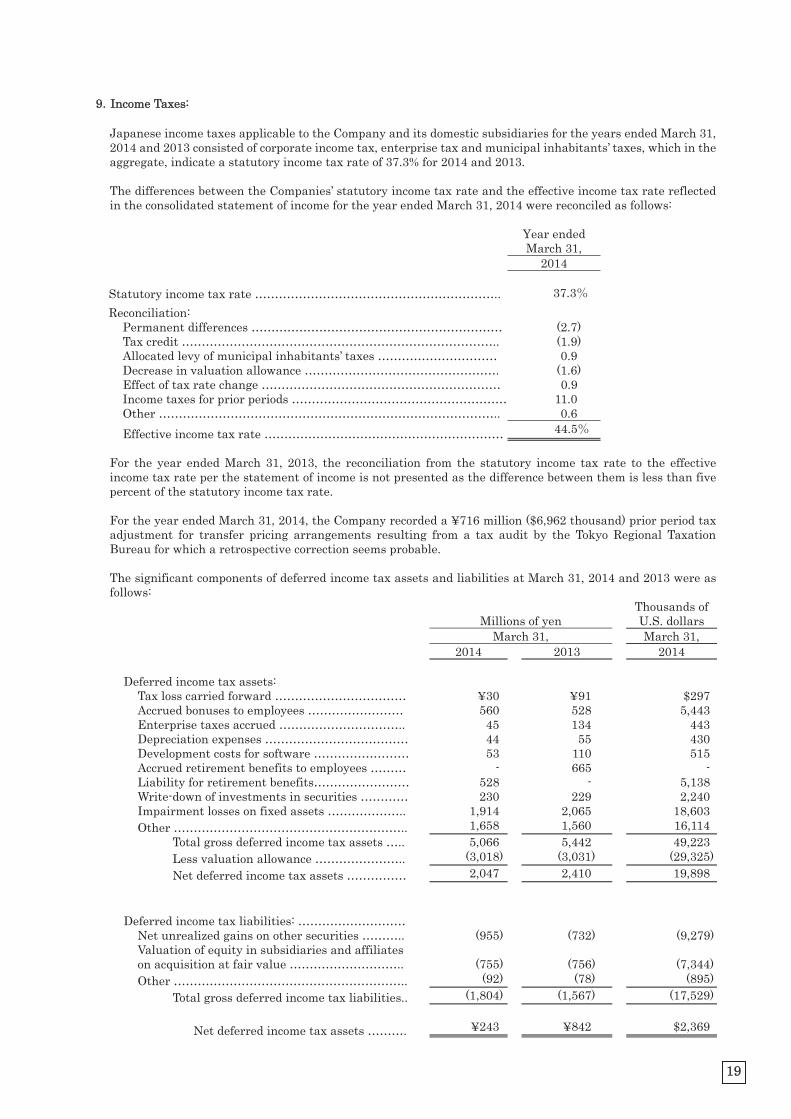

9 Income Taxes:

Japanese income taxes applicable to the Company and its domestic subsidiaries for the years ended March 31, 2014 and 2013 consisted of corporate income tax, enterprise tax and municipal inhabitants’ taxes, which in the aggregate, indicate a statutory income tax rate of 37.3% for 2014 and 2013.

The differences between the Companies’ statutory income tax rate and the effective income tax rate reflected in the consolidated statement of income for the year ended March 31, 2014 were reconciled as follows:

Year ended March 31,

2014

Statutory income tax rate …………………………………………………….. 37.3 Reconciliation:

Permanent differences ……………………………………………………… (2.7) Tax credit …………………………………………………………………….. (1.9) Allocated levy of municipal inhabitants’ taxes ………………………… 0.9 Decrease in valuation allowance …………………………………………. (1.6) Effect of tax rate change …………………………………………………… 0.9 Income taxes for prior periods ……………………………………………… 11.0 Other ………………………………………………………………………….. 0.6 Effective income tax rate …………………………………………………… 44.5

For the year ended March 31, 2013, the reconciliation from the statutory income tax rate to the effective income tax rate per the statement of income is not presented as the difference between them is less than five percent of the statutory income tax rate. For the year ended March 31, 2014, the Company recorded a ¥716 million ($6,962 thousand) prior period tax adjustment for transfer pricing arrangements resulting from a tax audit by the Tokyo Regional Taxation Bureau for which a retrospective correction seems probable. The significant components of deferred income tax assets and liabilities at March 31, 2014 and 2013 were as follows:

Millions of yen Thousands of

U.S. dollars March 31, March 31,

2014 2013 2014 Deferred income tax assets:

Tax loss carried forward …………………………… ¥30 ¥91 $297Accrued bonuses to employees …………………… 560 528 5,443Enterprise taxes accrued ………………………….. 45 134 443Depreciation expenses ……………………………… 44 55 430Development costs for software …………………… 53 110 515Accrued retirement benefits to employees ……… - 665 -Liability for retirement benefits…………………… 528 - 5,138Write-down of investments in securities ………… 230 229 2,240Impairment losses on fixed assets ……………….. 1,914 2,065 18,603Other ………………………………………………….. 1,658 1,560 16,114

Total gross deferred income tax assets ….. 5,066 5,442 49,223Less valuation allowance ………………….. (3,018) (3,031) (29,325)Net deferred income tax assets …………… 2,047 2,410 19,898

Deferred income tax liabilities: ……………………… Net unrealized gains on other securities ……….. (955) (732) (9,279)Valuation of equity in subsidiaries and affiliates on acquisition at fair value ……………………….. (755) (756)

(7,344)

Other ………………………………………………….. (92) (78) (895)Total gross deferred income tax liabilities.. (1,804) (1,567) (17,529)

Net deferred income tax assets ………. ¥243 ¥842 $2,369

19

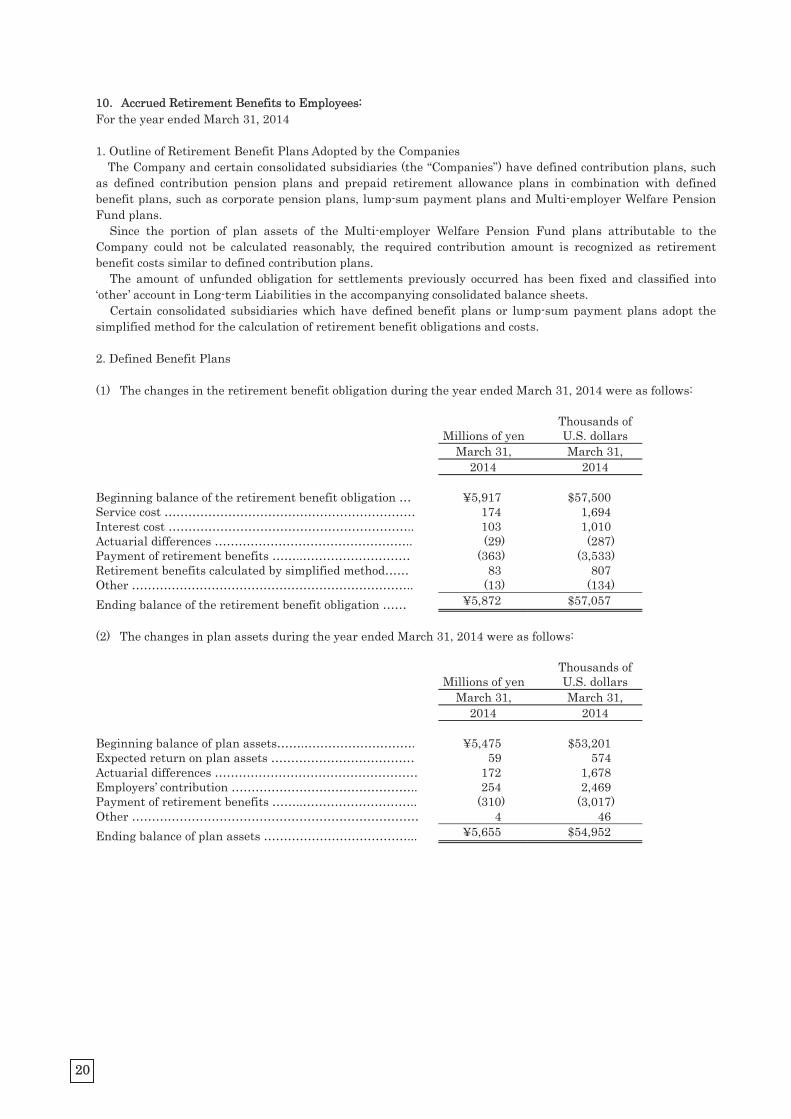

10 Accrued Retirement Benefits to Employees: For the year ended March 31, 2014 1. Outline of Retirement Benefit Plans Adopted by the Companies

The Company and certain consolidated subsidiaries (the “Companies”) have defined contribution plans, such as defined contribution pension plans and prepaid retirement allowance plans in combination with defined benefit plans, such as corporate pension plans, lump-sum payment plans and Multi-employer Welfare Pension Fund plans.

Since the portion of plan assets of the Multi-employer Welfare Pension Fund plans attributable to the Company could not be calculated reasonably, the required contribution amount is recognized as retirement benefit costs similar to defined contribution plans.

The amount of unfunded obligation for settlements previously occurred has been fixed and classified into ‘other’ account in Long-term Liabilities in the accompanying consolidated balance sheets.

Certain consolidated subsidiaries which have defined benefit plans or lump-sum payment plans adopt the simplified method for the calculation of retirement benefit obligations and costs. 2. Defined Benefit Plans (1) The changes in the retirement benefit obligation during the year ended March 31, 2014 were as follows:

Millions of yen Thousands of U.S. dollars

March 31, March 31, 2014 2014

Beginning balance of the retirement benefit obligation … ¥5,917 $57,500 Service cost ……………………………………………………… 174 1,694 Interest cost …………………………………………………….. 103 1,010 Actuarial differences ………………………………………….. (29) (287) Payment of retirement benefits ……..……………………… (363) (3,533) Retirement benefits calculated by simplified method…… 83 807 Other …………………………………………………………….. (13) (134) Ending balance of the retirement benefit obligation …… ¥5,872 $57,057 (2) The changes in plan assets during the year ended March 31, 2014 were as follows:

Millions of yenThousands of U.S. dollars

March 31, March 31, 2014 2014

Beginning balance of plan assets…….………………………. ¥5,475 $53,201 Expected return on plan assets ……………………………… 59 574 Actuarial differences …………………………………………… 172 1,678 Employers’ contribution ……………………………………….. 254 2,469 Payment of retirement benefits ……..……………………….. (310) (3,017) Other ……………………………………………………………… 4 46 Ending balance of plan assets ………………………………... ¥5,655 $54,952

20

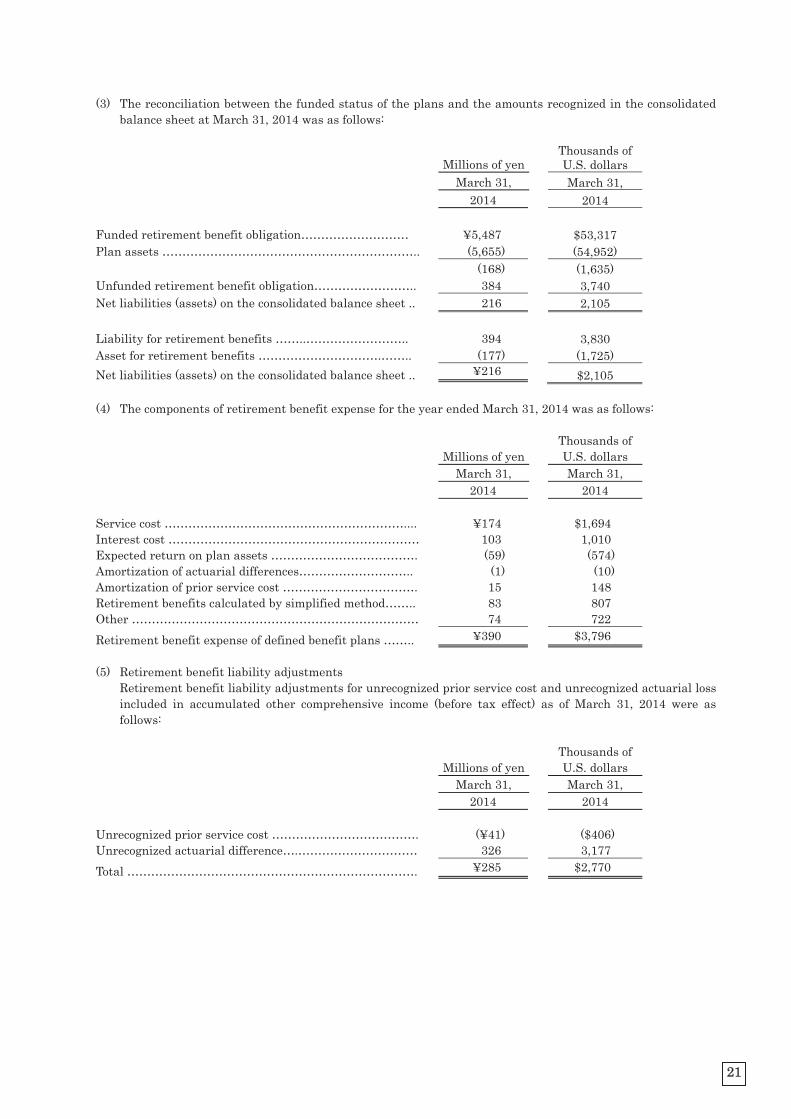

(3) The reconciliation between the funded status of the plans and the amounts recognized in the consolidated balance sheet at March 31, 2014 was as follows:

Millions of yen Thousands of U.S. dollars

March 31, March 31, 2014 2014

Funded retirement benefit obligation……………………… ¥5,487 $53,317 Plan assets ……………………………………………………….. (5,655) (54,952) (168) (1,635) Unfunded retirement benefit obligation…………………….. 384 3,740 Net liabilities (assets) on the consolidated balance sheet .. 216 2,105 Liability for retirement benefits ……..…………………….. 394 3,830 Asset for retirement benefits ………………………….…….. (177) (1,725) Net liabilities (assets) on the consolidated balance sheet .. ¥216 $2,105

(4) The components of retirement benefit expense for the year ended March 31, 2014 was as follows:

Millions of yenThousands of U.S. dollars

March 31, March 31, 2014 2014

Service cost …………………………………………………….... ¥174 $1,694 Interest cost ……………………………………………………… 103 1,010 Expected return on plan assets ………………………………. (59) (574) Amortization of actuarial differences……………………….. (1) (10) Amortization of prior service cost ……………………………. 15 148 Retirement benefits calculated by simplified method…….. 83 807 Other ……………………………………………………………… 74 722 Retirement benefit expense of defined benefit plans …….. ¥390 $3,796

(5) Retirement benefit liability adjustments

Retirement benefit liability adjustments for unrecognized prior service cost and unrecognized actuarial loss included in accumulated other comprehensive income (before tax effect) as of March 31, 2014 were as follows:

Millions of yenThousands of U.S. dollars

March 31, March 31, 2014 2014

Unrecognized prior service cost ………………………………. (¥41) ($406) Unrecognized actuarial difference….………………………… 326 3,177 Total ………………………………………………………………. ¥285 $2,770

21

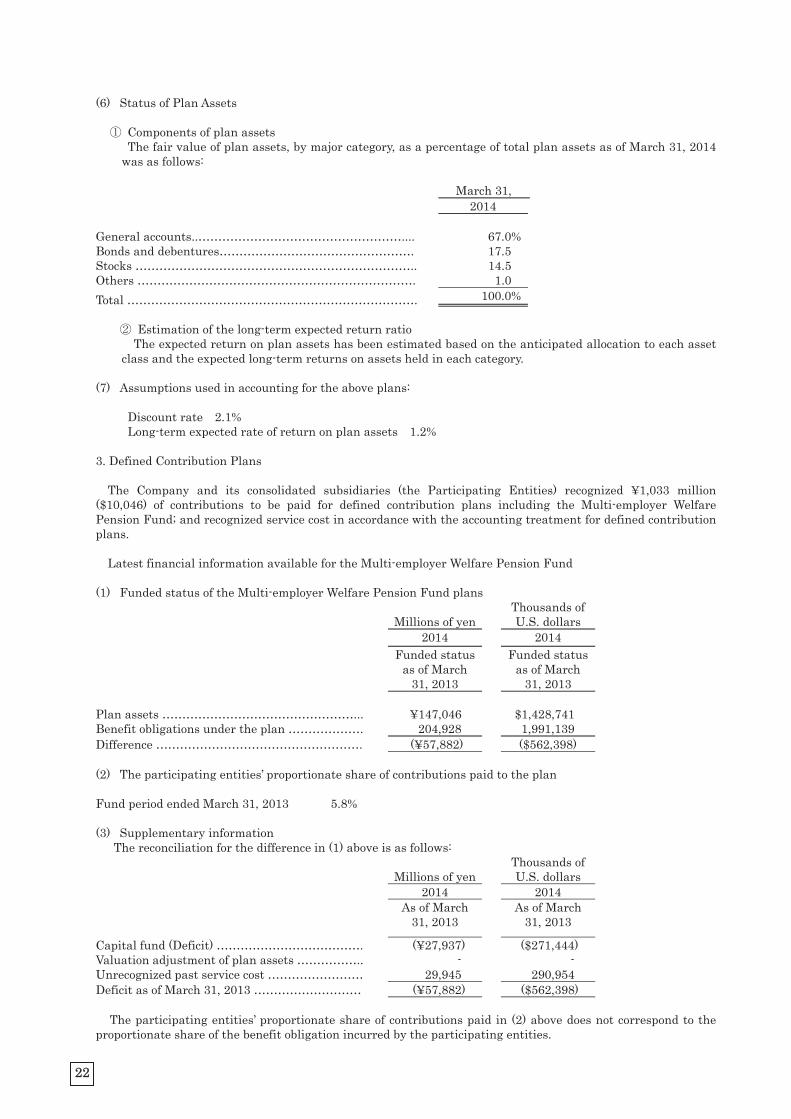

(6) Status of Plan Assets

Components of plan assets The fair value of plan assets, by major category, as a percentage of total plan assets as of March 31, 2014 was as follows:

March 31,

2014 General accounts..…………………………………………….... 67.0%Bonds and debentures…………………………………………. 17.5 Stocks …………………………………………………………….. 14.5 Others ……………………………………………………………. 1.0 Total ………………………………………………………………. 100.0%

Estimation of the long-term expected return ratio The expected return on plan assets has been estimated based on the anticipated allocation to each asset class and the expected long-term returns on assets held in each category.

(7) Assumptions used in accounting for the above plans:

Discount rate 2.1% Long-term expected rate of return on plan assets 1.2%

3. Defined Contribution Plans

The Company and its consolidated subsidiaries (the Participating Entities) recognized ¥1,033 million ($10,046) of contributions to be paid for defined contribution plans including the Multi-employer Welfare Pension Fund; and recognized service cost in accordance with the accounting treatment for defined contribution plans.

Latest financial information available for the Multi-employer Welfare Pension Fund

(1) Funded status of the Multi-employer Welfare Pension Fund plans

Millions of yenThousands of U.S. dollars

2014 2014 Funded status

as of March 31, 2013

Funded status as of March

31, 2013 Plan assets …………………………………………... ¥147,046 $1,428,741 Benefit obligations under the plan ………………. 204,928 1,991,139 Difference ……………………………………………. (¥57,882) ($562,398) (2) The participating entities’ proportionate share of contributions paid to the plan Fund period ended March 31, 2013 5.8% (3) Supplementary information

The reconciliation for the difference in (1) above is as follows:

Millions of yenThousands of U.S. dollars

2014 2014 As of March

31, 2013 As of March

31, 2013

Capital fund (Deficit) ………………………………. (¥27,937) ($271,444) Valuation adjustment of plan assets …………….. - - Unrecognized past service cost …………………… 29,945 290,954 Deficit as of March 31, 2013 ……………………… (¥57,882) ($562,398)

The participating entities’ proportionate share of contributions paid in (2) above does not correspond to the

proportionate share of the benefit obligation incurred by the participating entities.

22

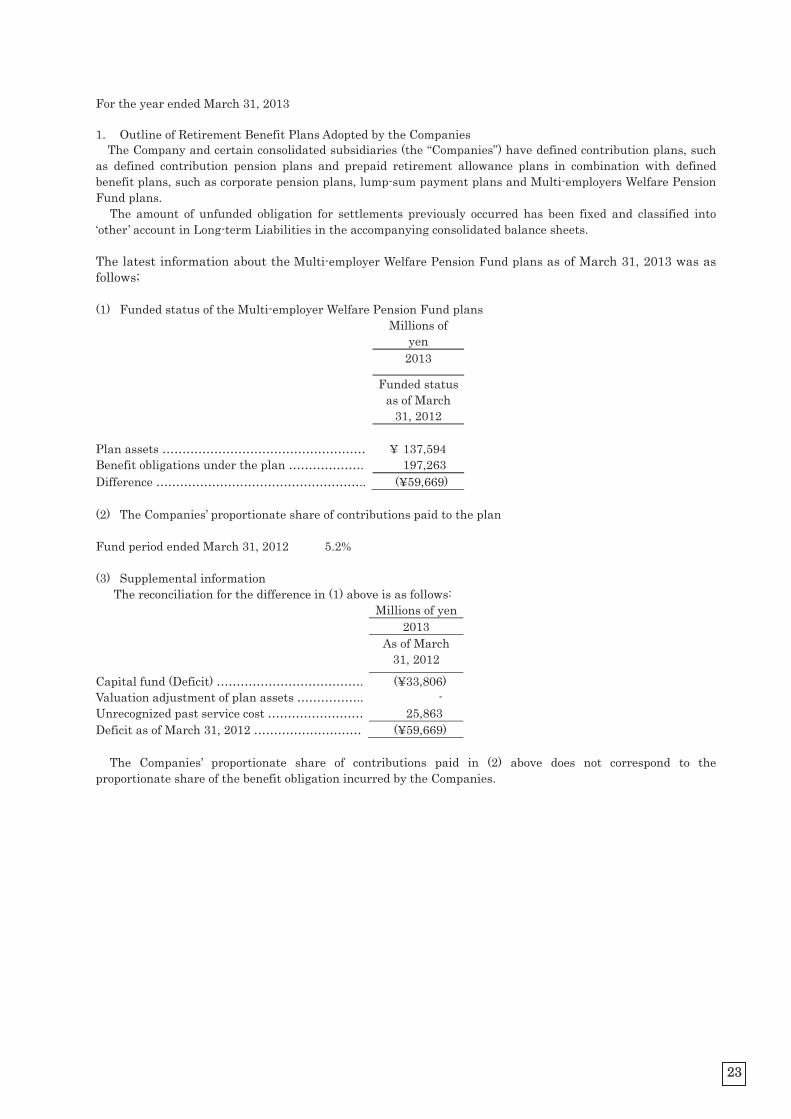

For the year ended March 31, 2013 1. Outline of Retirement Benefit Plans Adopted by the Companies

The Company and certain consolidated subsidiaries (the “Companies”) have defined contribution plans, such as defined contribution pension plans and prepaid retirement allowance plans in combination with defined benefit plans, such as corporate pension plans, lump-sum payment plans and Multi-employers Welfare Pension Fund plans.

The amount of unfunded obligation for settlements previously occurred has been fixed and classified into ‘other’ account in Long-term Liabilities in the accompanying consolidated balance sheets. The latest information about the Multi-employer Welfare Pension Fund plans as of March 31, 2013 was as follows; (1) Funded status of the Multi-employer Welfare Pension Fund plans Millions of

yen 2013

Funded status as of March

31, 2012 Plan assets …………………………………………… ¥ 137,594 Benefit obligations under the plan ………………. 197,263 Difference …………………………………………….. (¥59,669) (2) The Companies’ proportionate share of contributions paid to the plan Fund period ended March 31, 2012 5.2% (3) Supplemental information

The reconciliation for the difference in (1) above is as follows: Millions of yen 2013 As of March

31, 2012

Capital fund (Deficit) ………………………………. (¥33,806) Valuation adjustment of plan assets …………….. - Unrecognized past service cost …………………… 25,863 Deficit as of March 31, 2012 ……………………… (¥59,669)

The Companies’ proportionate share of contributions paid in (2) above does not correspond to the

proportionate share of the benefit obligation incurred by the Companies.

23

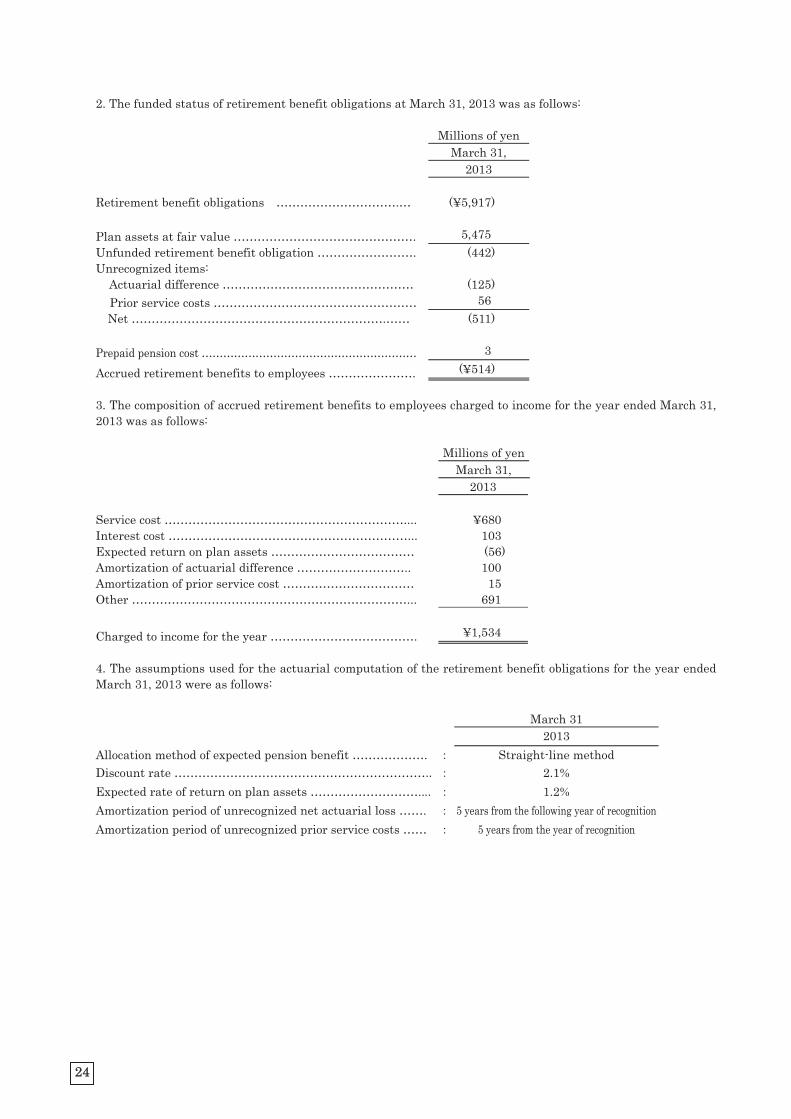

2. The funded status of retirement benefit obligations at March 31, 2013 was as follows: Millions of yen March 31,

2013 Retirement benefit obligations ………………………….… (¥5,917) Plan assets at fair value ………………………………………. 5,475 Unfunded retirement benefit obligation ……………………. (442) Unrecognized items:

Actuarial difference ………………………………………… (125) Prior service costs …………………………………………… 56

Net ……………………………………………………….…… (511) Prepaid pension cost …………………………………………………… 3

Accrued retirement benefits to employees …………………. (¥514)

3. The composition of accrued retirement benefits to employees charged to income for the year ended March 31, 2013 was as follows:

Millions of yen March 31,

2013 Service cost …………………………………………………….... ¥680 Interest cost ……………………………………………………... 103 Expected return on plan assets ……………………………… (56) Amortization of actuarial difference ……………………….. 100 Amortization of prior service cost …………………………… 15 Other ……………………………………………………………... 691 Charged to income for the year ………………………………. ¥1,534 4. The assumptions used for the actuarial computation of the retirement benefit obligations for the year ended March 31, 2013 were as follows:

March 31 2013

Allocation method of expected pension benefit ………………. Straight-line method Discount rate ……………………………………………………….. 2.1% Expected rate of return on plan assets ……………………….... 1.2% Amortization period of unrecognized net actuarial loss ……. 5 years from the following year of recognitionAmortization period of unrecognized prior service costs …… 5 years from the year of recognition

24

11 Lease Transactions -

The lease expenses under finance lease contracts that do not transfer the ownership of the leased property to the lessee for the years ended March 31, 2014 and 2013 amounted to ¥26 million ($258 thousand) and ¥58 million, respectively. As of March 31, 2014 and 2013, summarized information showing estimated acquisition cost, accumulated depreciation and amortization and net book value, which include the portion of interest thereon, of the leased properties under finance leases contracts that do not transfer the ownership of the leased property to the lessee commencing on or before March 31, 2008 was as follows:

Millions of yen Thousands of U.S. dollars March 31, March 31, 2014 2013 2014

Cost

Accumulated depreciation/ amortization

Net book value Cost

Accumulated depreciation/amortization

Net book value Cost

Accumulateddepreciation/amortization

Net book

valueMachinery and

equipment ….. ¥199 ¥164 ¥35 ¥239 ¥177 ¥62 $1,939 $1,594 $346

Total………. ¥199 ¥164 ¥35 ¥239 ¥177 ¥62 $1,939 $1,594 $346 The above amounts include the future interest expense and future lease payments. The scheduled maturities of future lease payments on these lease contracts as of March 31, 2014 and 2013 were as follows:

Millions of yen Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014

Due within one year …………. ¥17 ¥26 $169 Due over one year ……………. 18 35 177

Total ……………. ¥35 ¥62 $346

The above amounts of future lease payments include the future interest expense. Future lease payments for non-cancelable operating leases at March 31, 2014 and 2013 were as follows:

Millions of yen Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014

Due within one year …………. ¥269 ¥354 $2,615 Due over one year ……………. 1,147 1,365 11,151

Total ……………. ¥1,416 ¥1,720 $13,766

25

12 Financial Instruments -

1. Status of financial instruments

(1) Policy regarding financial instruments In light of plans for capital investment, the Companies raise funds mainly by bank borrowings and bond issuance. The Companies manage temporary fund surpluses through financial assets with high liquidity. Further, the Companies raise short-term working capital through bank borrowings. Regarding derivatives policy, the Companies make use of derivatives only to reduce risks as described below and do not enter into speculative transactions.

(2) Details of financial instruments and associated risks

Trade receivables - trade notes and accounts receivable - are exposed to credit risks of customers. Receivables denominated in foreign currencies in the course of business activities abroad are exposed to foreign currency exchange risks. The Companies employ foreign exchange forward contracts to hedge risks relating to foreign currency exchange fluctuations in accordance with internal rules.

Investments in securities are primarily the shares of companies with business relationships with the Company and are exposed to market price fluctuation risks. Trade payables - accounts payable - are settled within almost 3 months. Some payables denominated in foreign currencies are exposed to foreign currency exchange risks. The Companies employs foreign exchange forward contracts to hedge risks relating to foreign currency exchange fluctuations in accordance with internal rules. Long-term debt (Corporate bonds) and long-term debt (Bank loans) are held primarily for fund raising purposes for capital investments. Certain long-term debt, with variable interest rates that is exposed to interest rate fluctuation risk, is hedged by derivative transactions (interest swap transactions). Further information regarding the method of hedge accounting, hedging instruments and hedged items, hedging policy, and the assessment of the effectiveness of hedging activities are provided in Note 2 (4) Financial Instruments (Derivative financial instruments).

(3) Systems for risk management of financial instruments

Credit risk management (the risk that transactions partners may default ) In accordance with the internal regulations regarding credit exposures, the Accounting and Finance Department of the Company periodically monitors principal partners’ credit conditions to manage credit risks of partners by confirming due dates and outstanding account balances for each partner. The Department also actively works on gaining understandings of early stage concerns about recoverability of receivables because of financial difficulties of partner companies and may acquire assets pledged as collateral or credit insurance and so on. Consolidated subsidiaries conduct similar risk management in accordance with the internal regulations of the Company. There is almost no risks regarding derivative instruments realized by the Companies since the Companies arrange such transactions with highly rated financial institutions to minimize credit risks.

Market risk management (the risks arising from fluctuations in exchange rates, interest rates, and other indicators) As for trade receivables and payables denominated in foreign currencies, the Companies hedge the foreign exchange risks by forward foreign exchange contracts in accordance with internal rules. Furthermore, the Company and some of the consolidated subsidiaries arrange the interest rate swap transactions to reduce fluctuation risks of interest payment regarding long-term debt. For investments in securities, the Companies periodically confirm the market value of such financial instruments and the financial position of the issuers (companies having business transactions with the Companies). As for derivative transactions, related departments of the Companies conduct and manage transactions with approvals, based on the internal rules and regulations which describe authorization and trade limitation.

26

Liquidity risk management (the risk that the Companies are unable to settle its payment obligations on due dates) The Administration Department of the Companies appropriately creates and updates cash budget plans, based on the information from other departments and group companies, to control liquidity risks by maintaining sufficient liquid fund for daily operations.

(4) Supplementary explanation of items relating to the market value of financial instruments

The estimated fair value of financial instruments includes prices based on their quoted market prices, or includes prices reasonably estimated if there is no quoted market price. Since the estimations of these prices incorporate fluctuating factors, the prices might be fluctuated due to applying different assumptions. In addition, the contract (notional) amount of derivatives in Note 13 Derivative Transactions is not an indicator of actual risks involved in derivative transactions.

2. Estimated Fair Value and Other Matters Related to Financial Instruments

Carrying value on the consolidated balance sheet, estimated fair value and the difference between them as of March 31, 2014 and 2013 are as follows. The following table does not include financial instruments for which it is extremely difficult to determine the fair value or immaterial items.

Millions of yen Thousands of U.S. dollars March 31, March 31, 2014 2013 2014

Carrying value (*1)

Estimated fair value

(*1)

Difference Carrying value (*1)

Estimated fair value

(*1)

Difference Carrying value (*1)

Estimated fair value

(*1)

Difference

Cash in hand and in banks ………. ¥8,807 ¥8,807 - ¥6,662 ¥6,662 - $85,572 $85,572 -

Notes and accounts receivable -trade ………….. 20,799 20,799 - 22,857 22,857 - 202,091 202,091 -

Investments in securities -Other securities…. 7,056 7,056 - 6,384 6,384 - 68,563 68,563 -Accounts payable -trade …………….. (5,585) (5,585) - (5,259) (5,259) - (54,271) (54,271) -Long-term debt (Corporate bonds)

…. (9,512) (9,621) (¥109) (10,010) (10,154) (¥144) (92,421) (93,483) ($1,062)Long-term debt

(Bank loan) ….. (10,864) (11,057) (192) (9,906) (10,065) (158) (105,566) (107,441) (1,875)

Derivative transactions (*2) … 5 5 - 13 13 - 58 58 - (*1) Liabilities are shown in parentheses. (*2) The assets or liabilities arising from derivatives are shown at net value. Note i : Methods for computing the estimated fair value of financial instruments and items related to

securities and derivative transactions

(Cash in hand and in banks, Notes and accounts receivable-trade, Accounts payable-trade) Since these accounts are settled in a short period of time and their estimated fair values are almost the same as the carrying values, the carrying values are used.

(Investments in securities)

The estimated fair values of these items are as follows: Stocks are measured at quoted market prices of exchange markets. Bonds are measured at trading prices. Classification of investments in securities is presented in Note 6. Investments in Securities.

27

(Long-term debt - Corporate bonds) The fair value of corporate bonds is measured at quoted market price, or at the price computed as the sum of the present value of the principal payment, using a discount rate considering the remaining period and credit risks, if there is no quoted market price.

(Long-term debt - Bank loans)

The fair value of bank loans is computed as the sum of the present value of the principal payment discounted at the assumed market rate of interest applied when a similar new loan is entered into.

(Derivative transactions)

Please refer to Note 13. Derivative Transactions. Note ii: Financial instruments for which it is extremely difficult to determine the fair value

Carrying value

Millions of yen Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014 Unlisted equity securities ……. ¥214 ¥213 $2,086 Others …………………………… - 2 - These items are not included in the above investments in securities – other securities since there are no market values, and estimating their future cash flows is deemed to be extremely difficult.

Note iii: Redemption schedule for cash in banks and notes and accounts receivable-trade within one year after

the year ended March 31, 2014 and 2013:

Within 1 Year Millions of yen Thousands of

U.S. dollars March 31, March 31, 2014 2013 2014 Cash in banks ……………………………... ¥8,745 ¥6,584 $84,971Notes and accounts receivable trade … 20,799 22,857 202,091

Redemption within one year …. ¥29,544 ¥29,441 $287,062

Note iv: Redemption schedule for corporate bonds and bank loans with maturity dates, scheduled after the

year ended March 31, 2014 and 2013:

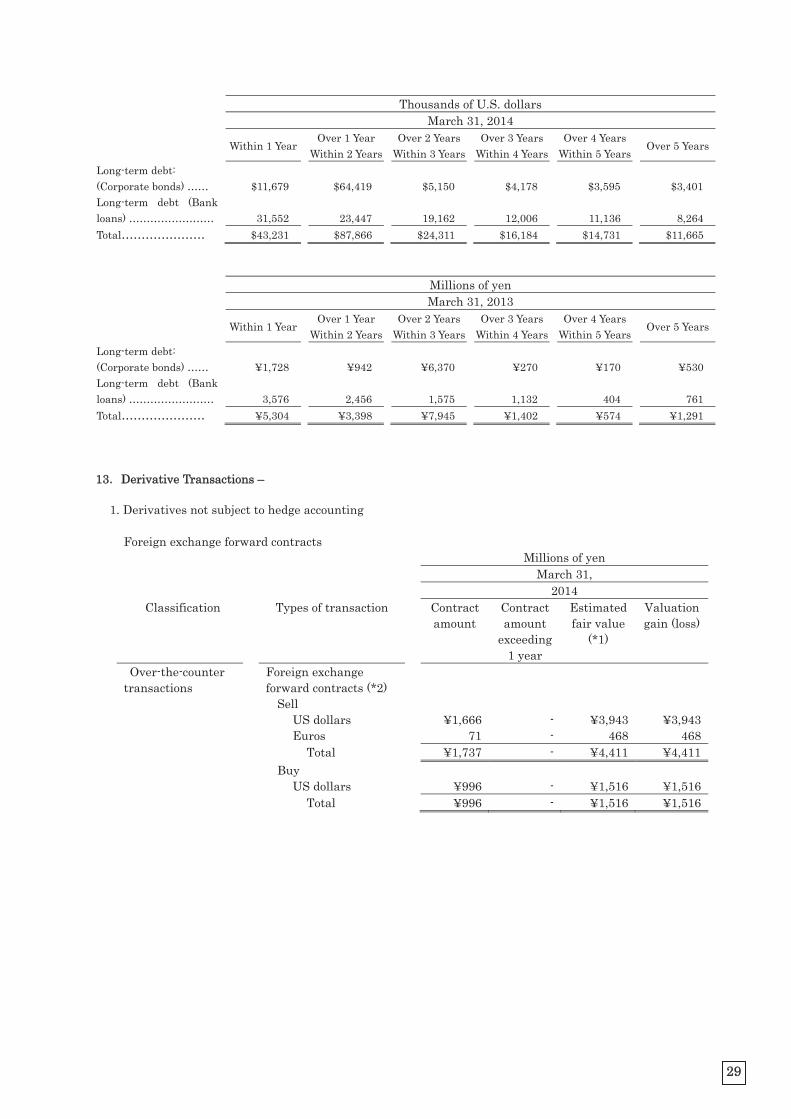

Millions of yen March 31, 2014

Within 1 Year

Over 1 YearWithin 2 Years

Over 2 YearsWithin 3 Years

Over 3 YearsWithin 4 Years

Over 4 Years Within 5 Years

Over 5 Years

Long-term debt: (Corporate bonds) …… ¥1,202 ¥6,630 ¥530 ¥430 ¥370 ¥350 Long-term debt (Bank loans) …………………… 3,247 2,413 1,972 1,235 1,146 850 Total………………… ¥4,449 ¥9,043 ¥2,502 ¥1,665 ¥1,516 ¥1,200

28

Thousands of U.S. dollars March 31, 2014

Within 1 Year

Over 1 YearWithin 2 Years

Over 2 YearsWithin 3 Years

Over 3 YearsWithin 4 Years

Over 4 Years Within 5 Years

Over 5 Years

Long-term debt: (Corporate bonds) …… $11,679 $64,419 $5,150 $4,178 $3,595 $3,401 Long-term debt (Bank loans) …………………… 31,552 23,447 19,162 12,006 11,136 8,264 Total………………… $43,231 $87,866 $24,311 $16,184 $14,731 $11,665

Millions of yen

March 31, 2013

Within 1 Year

Over 1 YearWithin 2 Years

Over 2 YearsWithin 3 Years

Over 3 YearsWithin 4 Years

Over 4 Years Within 5 Years

Over 5 Years

Long-term debt: (Corporate bonds) …… ¥1,728 ¥942 ¥6,370 ¥270 ¥170 ¥530 Long-term debt (Bank loans) …………………… 3,576 2,456 1,575 1,132 404 761 Total………………… ¥5,304 ¥3,398 ¥7,945 ¥1,402 ¥574 ¥1,291

13 Derivative Transactions –

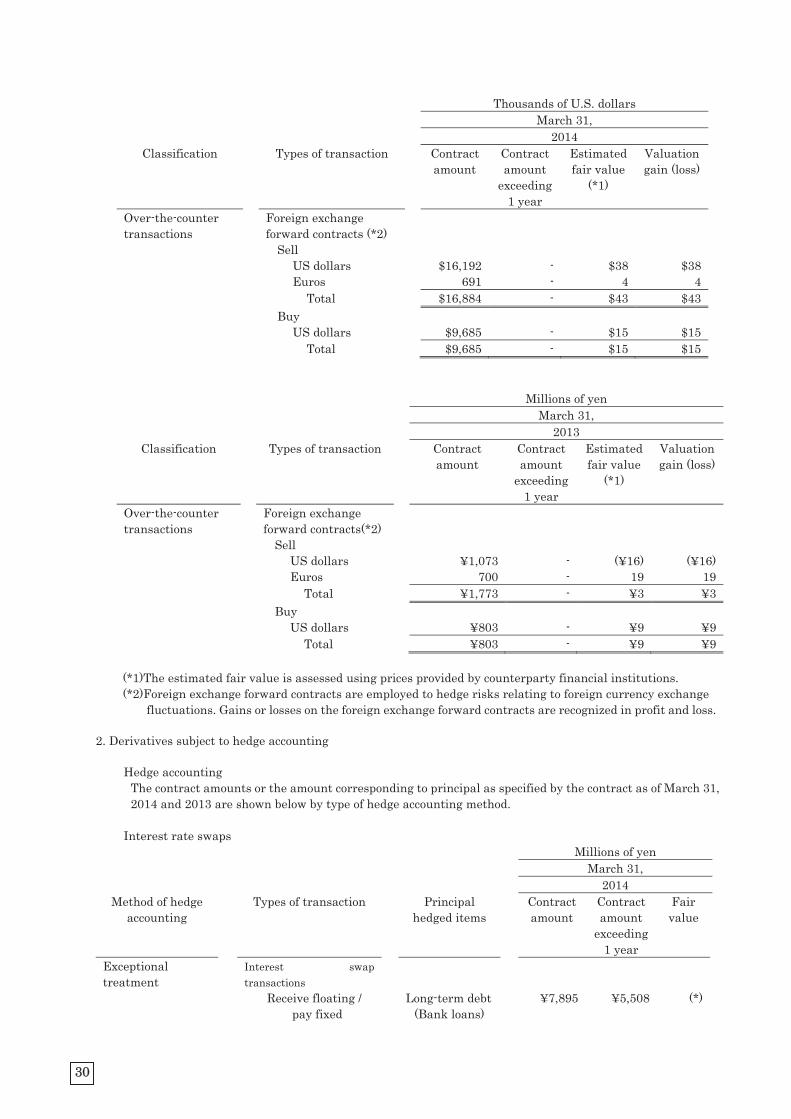

1. Derivatives not subject to hedge accounting Foreign exchange forward contracts

Millions of yen March 31, 2014

Classification Types of transaction Contract amount

Contract amount

exceeding1 year

Estimated fair value

(*1)

Valuation gain (loss)

Over-the-counter transactions

Foreign exchange forward contracts (*2)

Sell US dollars ¥1,666 - ¥3,943 ¥3,943 Euros 71 - 468 468 Total ¥1,737 - ¥4,411 ¥4,411 Buy US dollars ¥996 - ¥1,516 ¥1,516 Total ¥996 - ¥1,516 ¥1,516

29

Thousands of U.S. dollars March 31, 2014

Classification Types of transaction Contract amount

Contract amount

exceeding1 year

Estimated fair value

(*1)

Valuation gain (loss)

Over-the-counter transactions

Foreign exchange forward contracts (*2)

Sell US dollars $16,192 - $38 $38 Euros 691 - 4 4 Total $16,884 - $43 $43 Buy US dollars $9,685 - $15 $15 Total $9,685 - $15 $15

Millions of yen March 31, 2013

Classification Types of transaction

Contract amount

Contract amount

exceeding 1 year

Estimated fair value

(*1)

Valuation gain (loss)

Over-the-counter transactions

Foreign exchange forward contracts(*2)

Sell US dollars ¥1,073 - (¥16) (¥16) Euros 700 - 19 19 Total ¥1,773 - ¥3 ¥3 Buy US dollars ¥803 - ¥9 ¥9 Total ¥803 - ¥9 ¥9

(*1)The estimated fair value is assessed using prices provided by counterparty financial institutions. (*2)Foreign exchange forward contracts are employed to hedge risks relating to foreign currency exchange fluctuations. Gains or losses on the foreign exchange forward contracts are recognized in profit and loss.

2. Derivatives subject to hedge accounting

Hedge accounting

The contract amounts or the amount corresponding to principal as specified by the contract as of March 31, 2014 and 2013 are shown below by type of hedge accounting method.

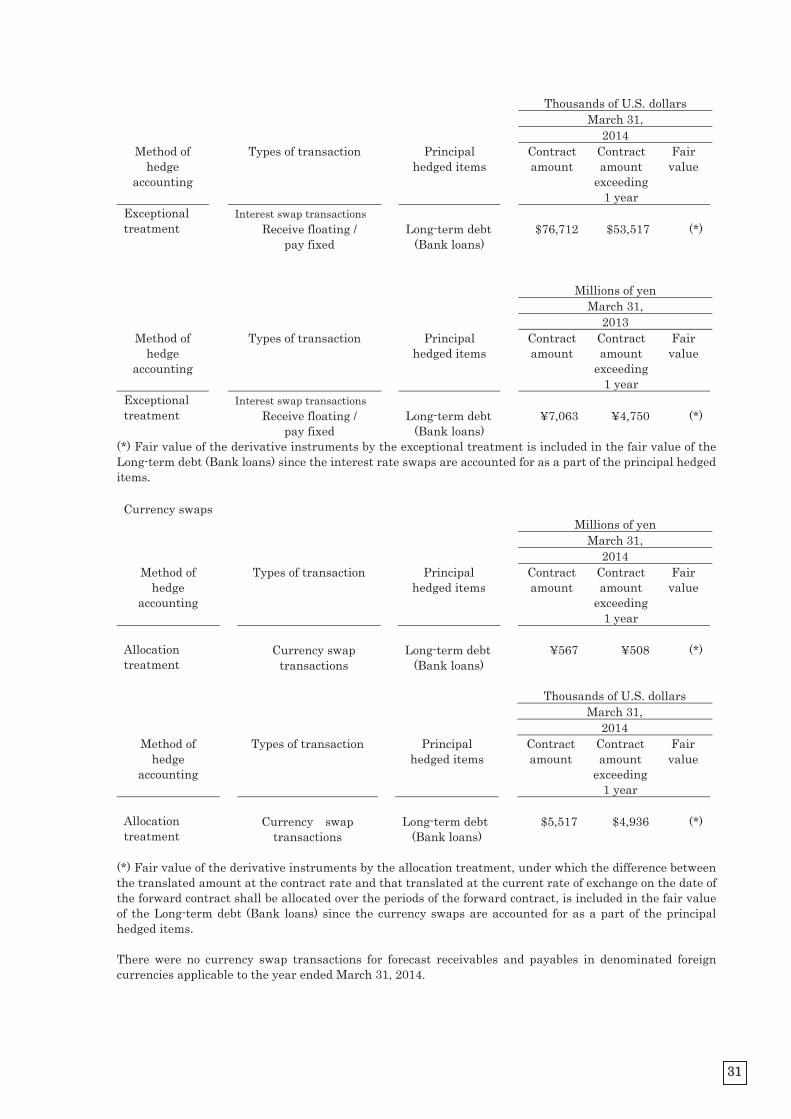

Interest rate swaps

Millions of yen March 31, 2014

Method of hedge accounting

Types of transaction Principal hedged items

Contract amount

Contract amount

exceeding 1 year

Fair value

Exceptional treatment

Interest swap transactions

Receive floating / pay fixed

Long-term debt(Bank loans)

¥7,895 ¥5,508 (*)

30

Thousands of U.S. dollars March 31, 2014

Method of hedge

accounting

Types of transaction Principal hedged items

Contract amount

Contract amount

exceeding 1 year

Fair value

Exceptional treatment

Interest swap transactions Receive floating /

pay fixed Long-term debt

(Bank loans) $76,712 $53,517 (*)

Millions of yen March 31, 2013

Method of hedge

accounting

Types of transaction Principal hedged items

Contract amount

Contract amount

exceeding 1 year

Fair value

Exceptional treatment

Interest swap transactions Receive floating /

pay fixed Long-term debt

(Bank loans) ¥7,063 ¥4,750 (*)

(*) Fair value of the derivative instruments by the exceptional treatment is included in the fair value of the Long-term debt (Bank loans) since the interest rate swaps are accounted for as a part of the principal hedged items.

Currency swaps

Millions of yen March 31, 2014

Method of hedge

accounting

Types of transaction Principal hedged items

Contract amount

Contract amount

exceeding 1 year

Fair value

Allocation treatment

Currency swap

transactions Long-term debt

(Bank loans) ¥567 ¥508 (*)

Thousands of U.S. dollars March 31, 2014

Method of hedge

accounting

Types of transaction Principal hedged items

Contract amount

Contract amount

exceeding 1 year

Fair value

Allocation treatment

Currency swap

transactions Long-term debt

(Bank loans) $5,517 $4,936 (*)

(*) Fair value of the derivative instruments by the allocation treatment, under which the difference between the translated amount at the contract rate and that translated at the current rate of exchange on the date of the forward contract shall be allocated over the periods of the forward contract, is included in the fair value of the Long-term debt (Bank loans) since the currency swaps are accounted for as a part of the principal hedged items. There were no currency swap transactions for forecast receivables and payables in denominated foreign currencies applicable to the year ended March 31, 2014.

31

14 Asset Retirement Obligations: (1)Overview of the asset retirement obligations

The Company records the asset retirement obligations related to the future expenses for removing Asbestos (under the Industrial Safety and Health Law and the Ordinance on Prevention of Asbestos Hazards) on the demolition of buildings, and expenses related to the restoration obligations of store facilities for fitness clubs under real estate lease agreements.

(2) Basis for calculating the asset retirement obligations

Asset retirement obligations are calculated on the assumption of the prospective useful lives of 9 years to 38 years (expenses for removing Asbestos used in buildings), 10 years to 30 years (expenses related to the restoration obligations of store facilities for fitness clubs under real estate lease agreements) and discount rates of 1.245 to 2.520 .

(3) The changes in the asset retirement obligations for the years ended March 31, 2014 and 2013 were as follows:

Millions of yen

Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014

Balance at the beginning of the period …………………………………… ¥425 ¥484 $4,133 Increase due to acquisition of property and equipment ………………… 18 - 178 Accretion expense …………………………………………………………… 7 7 78 Decrease due to settlement …………………………………………………. (3) (65) (36) Other increase (decrease) ………………………………………………….. 2 (1) 27 Balance at the end of the period …………………………………………… ¥450 ¥425 $4,378

15 Contingent Liabilities:

The Companies have the following contingent liabilities as guarantor as of March 31, 2014 and 2013.

Millions of yen Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014 Housing loans borrowed by employees of the Company ………….………….………………….…………….……………. ¥16 ¥23 $159 Leasehold deposits assigned for securitization …………. - 2 - Notes receivable negotiated under a factoring arrangement ………… 148 164 1,439

32

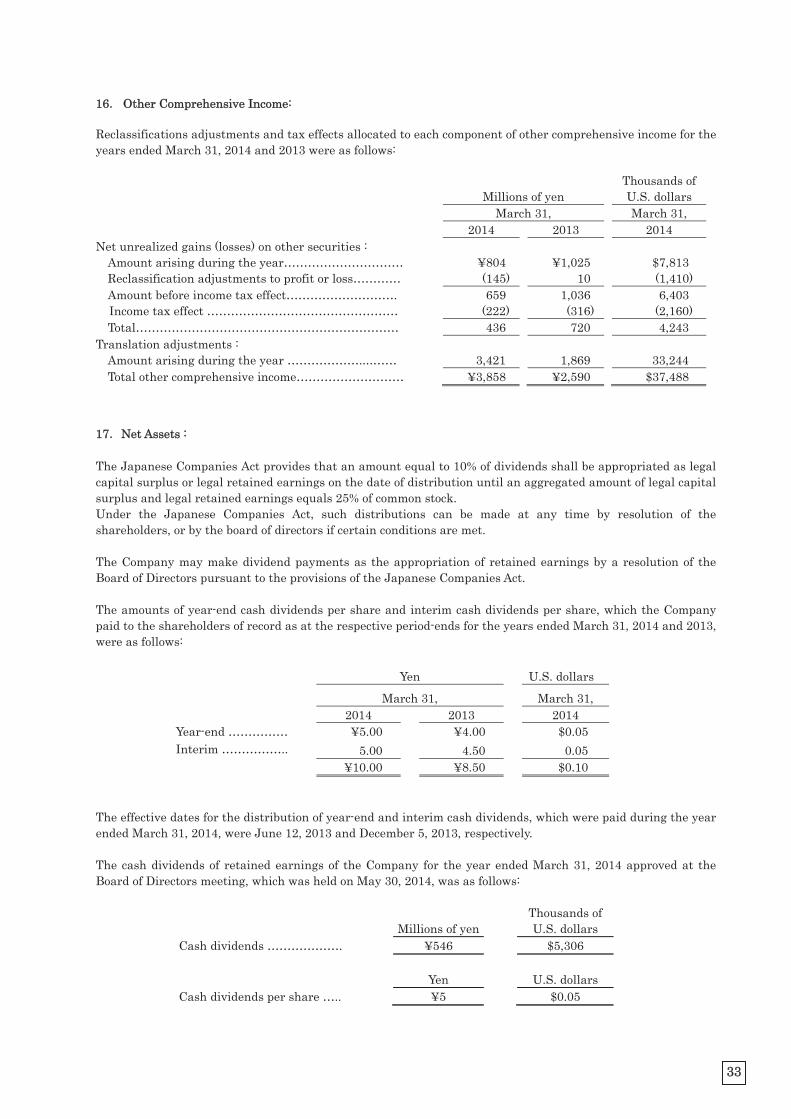

16 Other Comprehensive Income:

Reclassifications adjustments and tax effects allocated to each component of other comprehensive income for the years ended March 31, 2014 and 2013 were as follows:

Millions of yen

Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014

Net unrealized gains (losses) on other securities : Amount arising during the year………………………… ¥804 ¥1,025 $7,813 Reclassification adjustments to profit or loss………… (145) 10 (1,410) Amount before income tax effect………………………. 659 1,036 6,403 Income tax effect ………………………………………… (222) (316) (2,160) Total………………………………………………………… 436 720 4,243

Translation adjustments : Amount arising during the year ……………….……… 3,421 1,869 33,244 Total other comprehensive income……………………… ¥3,858 ¥2,590 $37,488

17 Net Assets : The Japanese Companies Act provides that an amount equal to 10% of dividends shall be appropriated as legal capital surplus or legal retained earnings on the date of distribution until an aggregated amount of legal capital surplus and legal retained earnings equals 25% of common stock. Under the Japanese Companies Act, such distributions can be made at any time by resolution of the shareholders, or by the board of directors if certain conditions are met. The Company may make dividend payments as the appropriation of retained earnings by a resolution of the Board of Directors pursuant to the provisions of the Japanese Companies Act.

The amounts of year-end cash dividends per share and interim cash dividends per share, which the Company paid to the shareholders of record as at the respective period-ends for the years ended March 31, 2014 and 2013, were as follows:

Yen U.S. dollars March 31, March 31, 2014 2013 2014 Year-end …………… ¥5.00 ¥4.00 $0.05 Interim …………….. 5.00 4.50 0.05 ¥10.00 ¥8.50 $0.10

The effective dates for the distribution of year-end and interim cash dividends, which were paid during the year ended March 31, 2014, were June 12, 2013 and December 5, 2013, respectively. The cash dividends of retained earnings of the Company for the year ended March 31, 2014 approved at the Board of Directors meeting, which was held on May 30, 2014, was as follows:

Millions of yen Thousands of U.S. dollars

Cash dividends ………………. ¥546 $5,306 Yen U.S. dollars Cash dividends per share ….. ¥5 $0.05

33

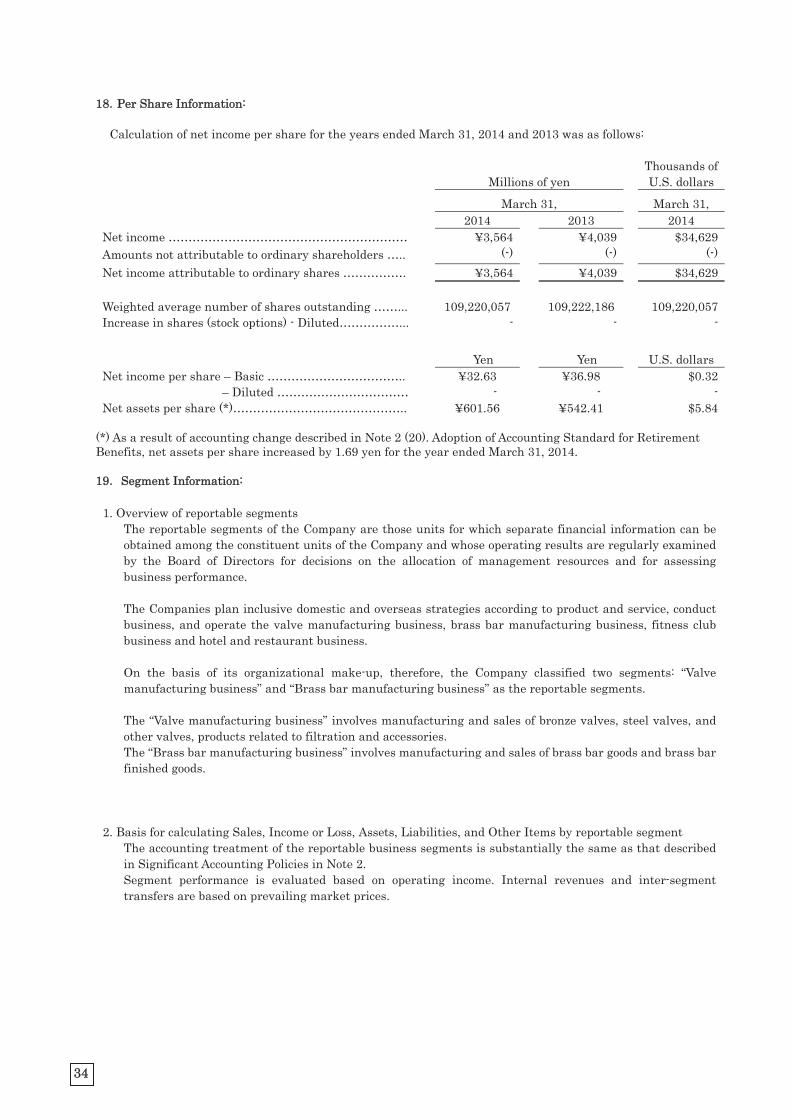

18 Per Share Information:

Calculation of net income per share for the years ended March 31, 2014 and 2013 was as follows:

Millions of yen

Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014 Net income …………………………………………………… ¥3,564 ¥4,039 $34,629Amounts not attributable to ordinary shareholders ….. (-) (-) (-)Net income attributable to ordinary shares ……………. ¥3,564 ¥4,039 $34,629 Weighted average number of shares outstanding ……... 109,220,057 109,222,186 109,220,057Increase in shares (stock options) - Diluted……………... - - - Yen Yen U.S. dollarsNet income per share – Basic …………………………….. ¥32.63 ¥36.98 $0.32 – Diluted …………………………… - - -Net assets per share (*)…………………………………….. ¥601.56 ¥542.41 $5.84

(*) As a result of accounting change described in Note 2 (20). Adoption of Accounting Standard for Retirement Benefits, net assets per share increased by 1.69 yen for the year ended March 31, 2014. 19 Segment Information:

1. Overview of reportable segments

The reportable segments of the Company are those units for which separate financial information can be obtained among the constituent units of the Company and whose operating results are regularly examined by the Board of Directors for decisions on the allocation of management resources and for assessing business performance. The Companies plan inclusive domestic and overseas strategies according to product and service, conduct business, and operate the valve manufacturing business, brass bar manufacturing business, fitness club business and hotel and restaurant business. On the basis of its organizational make-up, therefore, the Company classified two segments: “Valve manufacturing business” and “Brass bar manufacturing business” as the reportable segments. The “Valve manufacturing business” involves manufacturing and sales of bronze valves, steel valves, and other valves, products related to filtration and accessories. The “Brass bar manufacturing business” involves manufacturing and sales of brass bar goods and brass bar finished goods.

2. Basis for calculating Sales, Income or Loss, Assets, Liabilities, and Other Items by reportable segment The accounting treatment of the reportable business segments is substantially the same as that described in Significant Accounting Policies in Note 2. Segment performance is evaluated based on operating income. Internal revenues and inter-segment transfers are based on prevailing market prices.

34

3. Information on sales, income or loss, assets and other items by reportable segment

Sales Sales to outside customers ….. ¥87,888 ¥20,953 ¥8,514 ¥ - ¥117,355 Inter-segment sales/transfers . 240 3,062 35 (3,338) - Total ………………………… 88,128 24,016 8,549 (3,338) 117,355

Segment income …………………. ¥8,597 ¥548 ¥285 (¥2,960) ¥6,470Segment assets (*4) …………….. ¥ - ¥ - ¥ - ¥107,583 ¥107,583Other items ……………………… Depreciation ……………………. ¥2,677 ¥304 ¥218 ¥227 ¥3,428 Amortization of goodwill ……… ¥186 ¥ - ¥24 ¥ - ¥211

Sales Sales to outside customers ….. $853,946 $203,591 $82,725 $ - $1,140,261 Inter-segment sales/transfers . 2,334 29,756 349 (32,438) - Total ………………………… 856,279 233,346 83,073 (32,438) 1,140,261

Segment income …………………. $83,534 $5,327 $2,773 ($28,764) $62,870Segment assets (*4) …………….. $ - $ - $ - $1,045,310 $1,045,310Other items ……………………… Depreciation ……………………. $26,019 $2,954 $2,128 $2,209 $33,310 Amortization of goodwill ……… $1,814 $ - $242 $ - $2,056

Sales Sales to outside customers ….. ¥84,472 ¥17,948 ¥8,855 ¥ - ¥111,275 Inter-segment sales/transfers . 167 2,337 41 (2,546) - Total ………………………… 84,639 20,285 8,896 (2,546) 111,275

Segment income …………………. ¥8,808 ¥441 ¥330 (¥3,022) ¥6,558Segment assets (*4) …………….. ¥ - ¥ - ¥ - ¥99,972 ¥99,972Other items ……………………… Depreciation ……………………. ¥2,168 ¥364 ¥238 ¥220 ¥2,991 Amortization of goodwill ……… ¥146 ¥ - ¥24 ¥ - ¥171

Valvemanufacturing

business

Brass barmanufacturing

businessOther (*1) Adjustments

(*2,4)

Amount recordedin consolidated

financialstatements (*3)

Year ended March 31, 2014

Year ended March 31, 2013

Thousands of U.S. dollars

Millions of yen

Millions of yen

Adjustments(*2,4)

Amount recordedin consolidated

financialstatements (*3)

Valvemanufacturing

business

Brass barmanufacturing

businessOther (*1) Adjustments

(*2,4)

Amount recordedin consolidated

financialstatements (*3)

Year ended March 31, 2014

Reportable segments

Reportable segments

Reportable segments

Valvemanufacturing

business

Brass barmanufacturing

businessOther (*1)

(*1) "Other" included the fitness club business, hotel and restaurant business, and other business which are

not classified into the reportable segments.

35

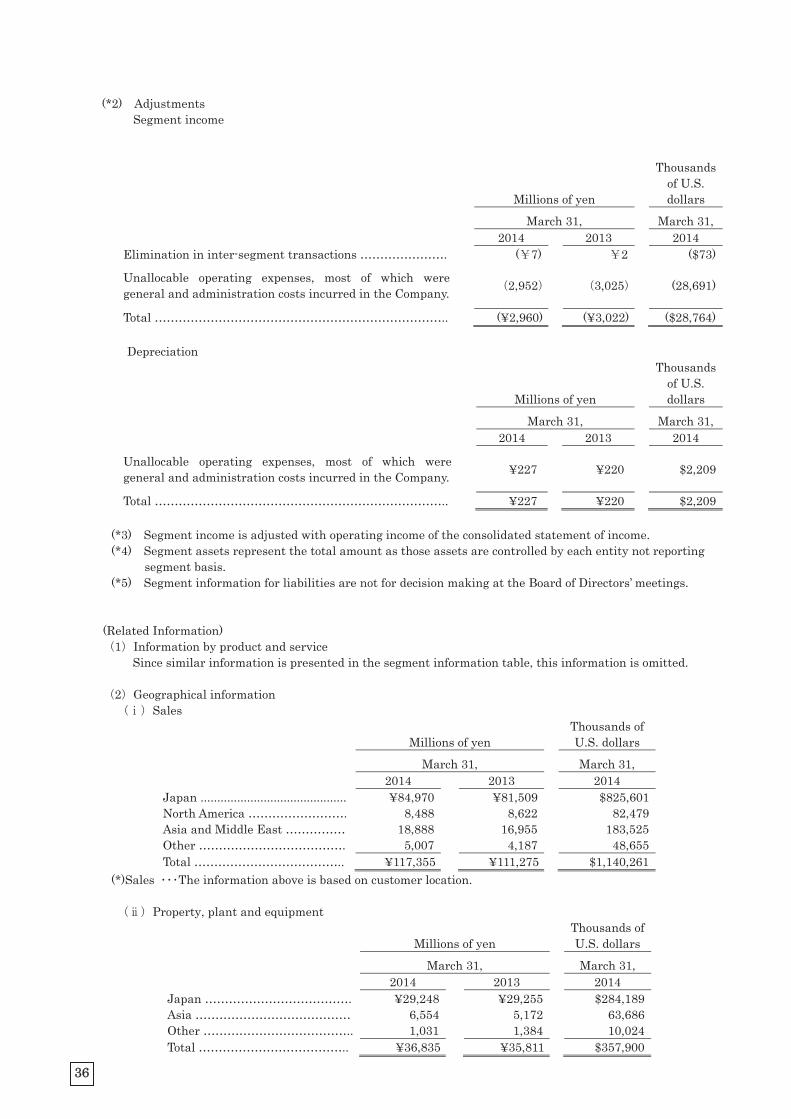

(*2) Adjustments Segment income

Millions of yen

Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014 Elimination in inter-segment transactions …………………. ( 7) 2 ($73)

Unallocable operating expenses, most of which were general and administration costs incurred in the Company. 2,952 3,025 (28,691)

Total ……………………………………………………………….. (¥2,960) (¥3,022) ($28,764) Depreciation

Millions of yen

Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014

Unallocable operating expenses, most of which were general and administration costs incurred in the Company. ¥227 ¥220 $2,209

Total ……………………………………………………………….. ¥227 ¥220 $2,209

(*3) Segment income is adjusted with operating income of the consolidated statement of income. (*4) Segment assets represent the total amount as those assets are controlled by each entity not reporting

segment basis. (*5) Segment information for liabilities are not for decision making at the Board of Directors’ meetings.

(Related Information)

1 Information by product and service Since similar information is presented in the segment information table, this information is omitted.

2 Geographical information Sales

Millions of yen

Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014 Japan ............................................ ¥84,970 ¥81,509 $825,601 North America ……………………. 8,488 8,622 82,479 Asia and Middle East …………… 18,888 16,955 183,525 Other ………………………………. 5,007 4,187 48,655 Total ……………………………….. ¥117,355 ¥111,275 $1,140,261

(*)Sales The information above is based on customer location.

Property, plant and equipment Millions of yen

Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014 Japan ………………………………. ¥29,248 ¥29,255 $284,189 Asia ………………………………… 6,554 5,172 63,686 Other ……………………………….. 1,031 1,384 10,024 Total ……………………………….. ¥36,835 ¥35,811 $357,900

36

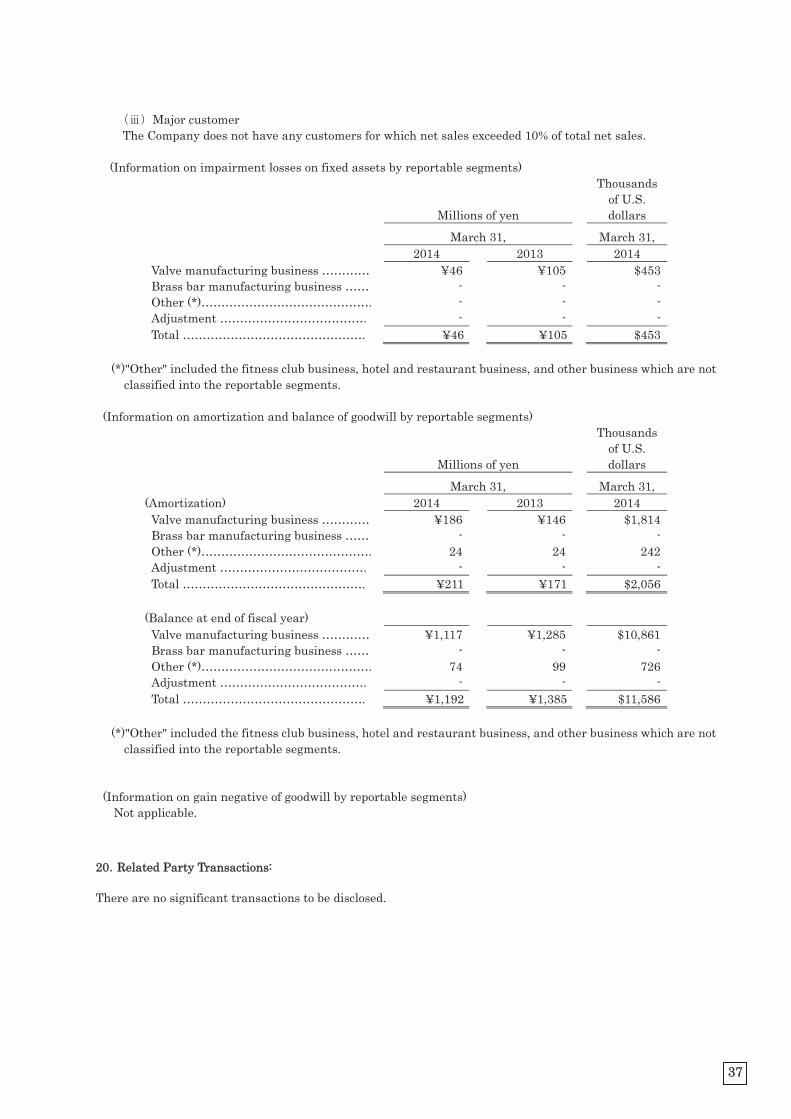

Major customer

The Company does not have any customers for which net sales exceeded 10% of total net sales. (Information on impairment losses on fixed assets by reportable segments)

Millions of yen

Thousands of U.S. dollars

March 31, March 31, 2014 2013 2014 Valve manufacturing business ………… ¥46 ¥105 $453Brass bar manufacturing business …… - - -Other (*)……………………………………. - - -Adjustment ………………………………. - - -Total ………………………………………. ¥46 ¥105 $453

(*)"Other" included the fitness club business, hotel and restaurant business, and other business which are not

classified into the reportable segments.

(Information on amortization and balance of goodwill by reportable segments)

Millions of yen

Thousands of U.S. dollars