Embed Size (px)

Citation preview

1

© 2010 Lane Powell PC1838741 1

ESTATE PLANNING IN 2010 - 2011

Maneuvering Through the Years of Uncertainty

Harold E. Snow, Jr.Filmore E. RoseLane Powell, PC

[email protected]@lanepowell.com

KING COUNTY BAR ASSOCIATIONSeattle, Washington

October 6, 2010

1420 Fifth Avenue, Suite 4100Seattle, Washington 98101-2338

206.223.7000

© 2010 Lane Powell PC1838741 2

Estate Tax Repeal Update

What We Will Discuss Today

A. How We Got to Where We Are Today

B. Attempts to Deal With EGTRRA’s Estate Tax Repeal

1. Events in 2009

2. 2010 Possibilities

C. Issues Surrounding the Retroactive Application of the Estate Tax Legislation

D. Where We Are Today: The 2010 IRC § 1022 Carry-Over Basis Rules

1. The New Federal Tax Regime

E. Planning Opportunities

1. Review Will Provisions

2. Other Impacts

3. Planning

© 2010 Lane Powell PC1838741 3

Estate Tax Law Under the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA)

A. HOW WE GOT TO WHERE WE ARE

TODAY

2

© 2010 Lane Powell PC1838741 4

Generation Skipping Tax Under the Economic and Tax Relief Reconciliation Act

of 2001 (EGTRRA)

© 2010 Lane Powell PC1838741 5

NO FEDERAL ESTATE TAX OR GST TAX

AS OF JANUARY 1, 2010

● There is a Gift Tax

� $1,000,000 Exemption

� 35% Top Rate

© 2010 Lane Powell PC1838741 6

● The estate and GST tax situation is the result

of the Economic Growth and Tax Relief

Reconciliation Act of 2001, commonly known

as “EGTRRA.”

3

© 2010 Lane Powell PC1838741 7

● EGTRRA was enacted in 2001 by a

Republican-controlled Congress.

● Budget surpluses of several trillion dollars

were forecast for the coming decade.

● EGTRRA sought to return some of the $1.3

trillion in surpluses in the form of tax cuts to

the taxpayer.

© 2010 Lane Powell PC1838741 8

● EGTRRA tax changes expire on 12/31/2010 and the tax law “shall be applied . . . as if the provisions and amendments (of EGTRRA) had not been enacted.”

● Expiration required by the “Byrd Rule” within the Congressional Budget Act which prevents the reduction in tax receipts beyond the period provided in the Congressional Budget Resolution.

● Byrd Rule could have been waived by 60 votes. The 60 votes were not available.

● The end of estate tax repeal in 2010 was the result of the Byrd Rule and a politically balanced Senate in 2001.

● No intent to create the 2010-2011 estate tax dilemma we now face.

© 2010 Lane Powell PC1838741 9

B. Attempts to Deal with EGTRRA’s Estate Tax Repeal1. Events In 2009

Proposed Estate Tax Legislation

4

© 2010 Lane Powell PC1838741 10

2. 2010 POSSIBILITIES

● February 11, 2010: Senators Baucus (D-MT) and

Grassley (R-IA) proposed jobs bill would have

permitted the introduction of several estate tax

legislative proposals.

● February 11, 2010: Senate Majority Leader Harry

Reid (D-NV) jobs bill introduced and passed

February 23. This scuttled the chance for the Baucus-

Grassley jobs bill and estate tax compromise.

© 2010 Lane Powell PC1838741 11

ADMINISTRATION PROPOSALS

2011 TREASURY GREENBOOK(pages 122-126)

● Restrictions on Scope of Valuation Discounts

� Modify IRC § 2704(b) to create a series of

restrictions that would be ignored for valuation

purposes.

●Minimum 10-year term for GRATs.

� Remainder interest must have a value greater than

zero. No more “zeroed-out” GRATs.

© 2010 Lane Powell PC1838741 12

H.R. 4849 SMALL BUSINESS AND

INFRASTRUCTURE JOBS ACT OF 2010

● H.R. 4849 introduced by Rep. Sander Levin (D-MI) acting Chair of the House Ways & Means Committee, which would amend IRC § 2702 and require:� A 10-year minimum term for a GRAT and

� A remainder value greater than zero.� Passed House committed, March 17, 2010

� Amends IRC § 2702

● Rep. Sander Levin (D-MI) comments on March 16, 2010 that the House Ways & Means Committee favors a retroactive reinstatement of the 2009 estate tax regime.

● On September 16, 2010, the Senate version of the Bill was adopted without the GRAT limitation. It was signed into law by the President.

5

© 2010 Lane Powell PC1838741 13

C. ISSUES SURROUNDING THE

RETROACTIVE APPLICATION OF THE ESTATE TAX LEGISLATION

● Senator Baucus (D-MI) and Rep. Levin (D-MI), the Chairs of the two primary committees that would deal with estate tax legislation want retroactivity.

● Fifth Amendment Due Process Argument. See United States v. Carlton, 512 U.S. 26, 30-31 (1994) finding that taxpayers have a substantive economic right that may be violated if the retroactivity is not a “rational means” of furthering a “legitimate legislative purpose.” See also PBGC v. R.A. Gray & Co., 467 U.S. 717, 729-730 (1984) which upheld a more than 12-month retroactive application of an amendment to estate tax legislation regarding ESOPs.

© 2010 Lane Powell PC1838741 14

POSSIBLE DISTINCTION

● Retroactive changes to existing legislation

versus a “wholly new tax.” See Untermeyer v.

Anderson, 276 U.S. 440 (1928); Quartz v.

United States, 170 F.3d 961 (9th Cir. 1999).

● No estate tax in 2010. Does the retroactive

allocation of estate tax legislation in 2010

amount to a “wholly new tax”?

© 2010 Lane Powell PC1838741 15

D. WHERE WE ARE TODAY:

THE 2010 IRC § 1022 CARRY-OVER

BASIS RULES

6

© 2010 Lane Powell PC1838741 16

THE NEW FEDERAL TAXING REGIMEIRC § 1022(a) CARRY-OVER BASIS RULES

● Basis of Property Acquired from a Decedent:

The lesser of the decedent’s adjusted basis in

the property or the fair market value of the

property on the decedent’s death. IRC

§1022(a)(2)

● Determining basis will be tough.

© 2010 Lane Powell PC1838741 17

EXCEPTION TO CARRY-OVER BASIS

1. Executor can allocate up to $1,300,000 (only $60,000 for non-resident aliens) (increased by Net Operating Losses and Loss Carryovers) to increase the basis of assets. IRC § 1022(b)(2).

2. Executor can allocate $3,000,000 to increase the basis of assets passing to a surviving spouse (Spousal Property Basis Increase) either outright or pursuant to a Q-TIP. IRC §1022(c).

• IMPACT – Possibly affects 70,000 estates – vs – 6,000 if the 2009

Estate Tax Law was in place.

• Estates without surviving spouses negatively impacted.

• Non-resident aliens are not entitled to the Spousal Property Basis

Increase.

© 2010 Lane Powell PC1838741 18

CHARACTER OF PROPERTY CARRIES

OVER TO THE HEIRS

● Not only will the tax basis of the decedent in

the property generally carry over to the heirs,

but the character of the property, as ordinary

income or capital gains property, will also

carry over to the heirs.

● Will impact capital gains or ordinary income

treatment.

7

© 2010 Lane Powell PC1838741 19

PROPERTY MUST BE

“ACQUIRED FROM THE DECEDENT”

● Property acquired (IRC § 1022(d))

� By Gift

� Joint tenancy

� Community property

� Revocable trusts

� IRC § 1022(d)(1)(B)(iii) property over which the decedent holds a power of appointment (from a third party) will not be treated as owned by the decedent.

© 2010 Lane Powell PC1838741 20

EXCEPTION TO THE CARRY-OVER

BASIS RULE

IRC § 1022(b)(2) Aggregate Basis Increase: $1,300,000 general increase in tax basis which permits every decedent to increase the basis of assets to eliminate $1,300,000 of taxable appreciation.

Example: Rental Property: FMV: 600,000Basis: 300,000Basis Allocation: 300,000

Portfolio: FMV: 2,500,000Basis 1,500,000Basis Allocation: 1,000,000

© 2010 Lane Powell PC1838741 21

BASIS INCREASE DOES NOT APPLY TO

ALL PROPERTY (IRC § 1022(d)(1)(C-D))

● Property acquired by the decedent by gift within three years of death.

● Property acquired by decedent within one year of death and bequeathed back to donor.

● Foreign personal holding company stock sales.

● Stock of a domestic international sales corporation.

● Stock of a foreign investment company.

● Stock in a passive foreign investment company.

● Income in respect of a decedent property.

8

© 2010 Lane Powell PC1838741 22

§ 1022(c) $3,000,000 Spousal Property Basis Increase:

● In addition to the $1,300,000 Aggregate Basis Increase

� Qualified Spousal Property IRC § 1022(c)(3)

� Outright Transfers

� Qualified Terminable Interest Property (“QTIP”). The

interest passing to the surviving spouse must not lapse upon

the occurrence of an event or a contingency. IRC § 1022(c)(5)

� Upon the death of the surviving spouse, property in the

QTIP is probably not eligible for the $1,300,000 basis

adjustment since it is not “acquired from” the decedent life

interest holder.

© 2010 Lane Powell PC1838741 23

QTIP ISSUES

● No provision in IRC § 1022 for a partial QTIP

election as there now is within the IRC § 2056

QTIP, and no ability to split the QTIP into two

trusts. Disclaimed property might not be

“acquired from the decedent.”

� A provision for two marital trusts should be set

forth within the will from the beginning so as to

be “acquired from” the decedent.

© 2010 Lane Powell PC1838741 24

MISCELLANEOUS

● Inflation Adjustment § 1022(d)(4). The inflation increases will be based upon the cost of living adjustment for a particular calendar year, using 2009 as the base year.

● Community Property § 1022(d)(1)(B)(iv). A surviving spouse’s one-half share of community property assets will be treated as “acquired from” the decedent and subject to the carryover basis rules if one-half of the interest is treated under local law as owned by the decedent.

9

© 2010 Lane Powell PC1838741 25

MISCELLANEOUS (cont’d)

● 3-Year Rule § 1022(d)(1)(C): No basis step-up

available for property acquired by gift within

three years of death. To prevent the shifting of

assets between high and low income tax

brackets to obtain basis step-up.

© 2010 Lane Powell PC1838741 26

ALLOCATION OF THE BASIS

● Basis is to be allocated by the executor, IRC §1022(d)(3).

● Increase reporting and filing requirements for estates

● How should the basis adjustment be allocated.� Pro rata based upon the fair market value of the assets?

� Equally amongst the heirs?

● Independent Basis Allocation Executor: Include strong exoneration language in the will.

● Can the executor allocate basis to non-probate assets?

© 2010 Lane Powell PC1838741 27

FACTORS AFFECTING THE CHOICE OF

BASIS ALLOCATION

● Ordinary income versus capital gains property (e.g., for farms with zero basis calves or crops and IRC §1245 depreciation recapture).

● Prospective holding period of the inherited property.

● Difficulty in determining basis.

● Other available gain exclusion (e.g., IRC § 121 personal residence exclusion).

● Income tax situation of the beneficiary (no basis allocation to a charity).

10

© 2010 Lane Powell PC1838741 28

E. PLANNING OPPORTUNITIESWill Drafting in Light of the Estate Tax Exemption

Gap Between State and Federal Law

© 2010 Lane Powell PC1838741 29

1. REVIEW WILL PROVISIONS

● Applicable Exclusion Trust – “I give, devise and

bequeath the pecuniary sum which is the largest

dollar amount that will not create a state or federal

estate tax upon my death, to the Trustee of my Family

Trust (Applicable Exclusion Trust).”

● QTIP Trust – “I give, devise and bequeath the

pecuniary sum which is necessary to avoid the

creation of a state or federal estate tax on my death to

the Trustee of my Marital Trust.”

© 2010 Lane Powell PC1838741 30

GST CLAUSE

● The term “GST Exempt Amount” shall mean an amount equal to my unused generation-skipping transfer tax exemption (as defined in Code Section 2631) remaining after all allocations of such exemption before or after my death. It is my intention that my Executor maximize the use of my generation skipping transfer tax exemption. If any of my issue survive me, my Executor shall pay the GST Exempt Amount, as defined above, in accordance with the provision below entitled “Distribution for Grandchildren.” If none of my issue survive me, this bequest shall lapse.

11

© 2010 Lane Powell PC1838741 31

2. Other Impacts

● GST Exemption: $1,000,000 indexed for inflation.

● Estate and Gift Tax Exemption: $1,000,000.

● Top Tax Rate: 55%

● § 2031(c) conservation easement exclusion eliminated.

� Up to $500,000 in value.

● § 2057 QF0BI deduction returns.

● § 6166 amendments eliminated and ‘closely held’ reverts to 15 owners from 45.

● GST severance rules eliminated.

© 2010 Lane Powell PC1838741 32

3. Planning

● GST Gifts. Use a formula clause in the documents

creating the gift which provides that any amount that

is greater than your GST exemption (retroactively

reinstated) available at the date of the gift will be

allocated to a sub-trust for the children.

� Estate of Petter v. Commissioner, T.C. Memo 2009-280.

� Grandchildren’s and children’s trusts created within the

document.

� Taxable gift 35% tax rate.

© 2010 Lane Powell PC1838741 33

● Petter v. Commission, T.C. Memo 2009-280 and

Formula Claims. The decedent made gifts of LLC

units to an intentionally defective irrevocable grantor

trust (IDGT) and to two public charities. A dollar

amount of LLC units was gifted to the IDGT. If the

value of the LLC units was increased upon audit by

the IRS, as a condition of gift, the IDGT had to gift

LLC units reflecting such increased value to the

charities.

� No taxable gift was possible with the formula.

12

© 2010 Lane Powell PC1838741 34

IRC § 2653(a) “Drop Down” Rule Might Not Apply

● Normally, a transfer in trust for the benefit of grandchildren would be a GST transfer and the “drop down” rule would treat the trust as if the transferor were one generation above the generation of the trust’s beneficiaries. The trust would be treated as though a child of the grantor were the transferor.

● No GST tax in 2010, so no “direct skip” upon funding the trust. In 2011, the provisions of EGTRRA (including the 2010 suspension of the GST tax) are treated as if they never were enacted.

● “As if they never were enacted” might mean that the transfer to the trust is treated as a direct skip in 2011 not to impose a tax but to trigger the drop down rules in 2011 for purposes of defining taxable distributions.

● Gift into trust in 2010 might result in an inclusion ration other than zero.

© 2010 Lane Powell PC1838741 35

GST GIFTING IN 2011

● Direct transfers to grandchildren in 2010.

● Utilize a Family Limited Partnership (FLP) or

Family Limited Liability Company (FLLC) as

the gifting vehicle in order to retain control?

● Grandchild may then place the gifted interest

within a trust for further asset protection.

© 2010 Lane Powell PC1838741 36

WASHINGTON “PATCH” STATUS(11.108.0001-0002)

11.108.0001. Federal Estate and Generation-Skipping Transfer Tax Laws.

A will or a trust of a decedent who dies after December31, 2009, and before

January 1, 2011, is deemed to refer to the federal estate and generation-

skipping transfer tax laws as they applies with respect to estates of decedents

dying on December 31, 2009, if the will or trust contains a formula that: . . .

11.108.0002. Federal Estate and Generation-Skipping Transfer Tax Laws

– Proceedings Relating to Applicability.

The personal representative, trustee, or any affected beneficiary under a will or

trust may bring a proceeding under the trust and estate dispute resolution act in

Chapter 11.96 RCW, to determine whether the decedent intended . . .

13

© 2010 Lane Powell PC1838741 37

WILLS

● New Intent Paragraph.

� Provide for spouse and children.

� Minimize income, estate, gift and GST taxes.

● Three-tier trust system.

● Independent Executor to allocate basis

increase.

© 2010 Lane Powell PC1838741 38

WILLS (cont’d)

● State with no estate tax: Bequeath the maximum

amount to a marital trust that qualified for the

$3,000,000 Spousal Property Basis Increase and the

remainder to a bypass/credit shelter trust.

● State with an estate tax: Entire estate to the marital

trust except for an amount not in excess of the state’s

estate tax exclusion amount bequeathed to the bypass

trust.

© 2010 Lane Powell PC1838741 39

WILLS (cont’d)

Three Tier Trust System

1. Assets with $1,300,000 in appreciation to the Family Trust.● Draft for flexibility if the 2001 $1,000,000 federal estate

tax exemption returns.

2. $3,000,000 of appreciated assets to the QTIP and qualify as a QSP.

3. Balance.● If insufficient basis increase to go around, then allocate the

$1,300,000 in proportion to the appreciation in value received.

14

© 2010 Lane Powell PC1838741 40

GRATS

● GRATs have never been a vehicle for

transferring wealth to skip persons because the

GST exemption cannot be allocated until the

end of the GRAT term as a result of the estate

tax exclusion period rules (“ETIP”).

© 2010 Lane Powell PC1838741 41

TESTAMENTARY TRUSTS CREATED IN 2010

● IRC § 2652(a) defines the transferor for purposes of the GST tax as a decedent with respect to whom the property transferred is subject to estate or gift tax.

● If no estate tax applies, it appears there is no transferor for GST purposes.

● Should be no skip-person because no one is two or more generations below a transferor.

● Not cured in 2011 when GST tax returns because the assets within the trust were never subject to estate tax.

© 2010 Lane Powell PC1838741 42

IRREVOCABLE LIFE INSURANCE TRUSTS

(ILITS)

● Issue arises for ILITs that are intended to be permanently in place for multiple generations and to which the GST exemption is allocated on the annual contributions into trust.

● No GST tax in 2010. No GST exemption to allocate in 2010.

● In subsequent years, the exclusion ratio might be other than zero.

● Make a loan to the trust in 2010 for the premium payment in order to preserve the exclusion ratio.

15

© 2010 Lane Powell PC1838741 43

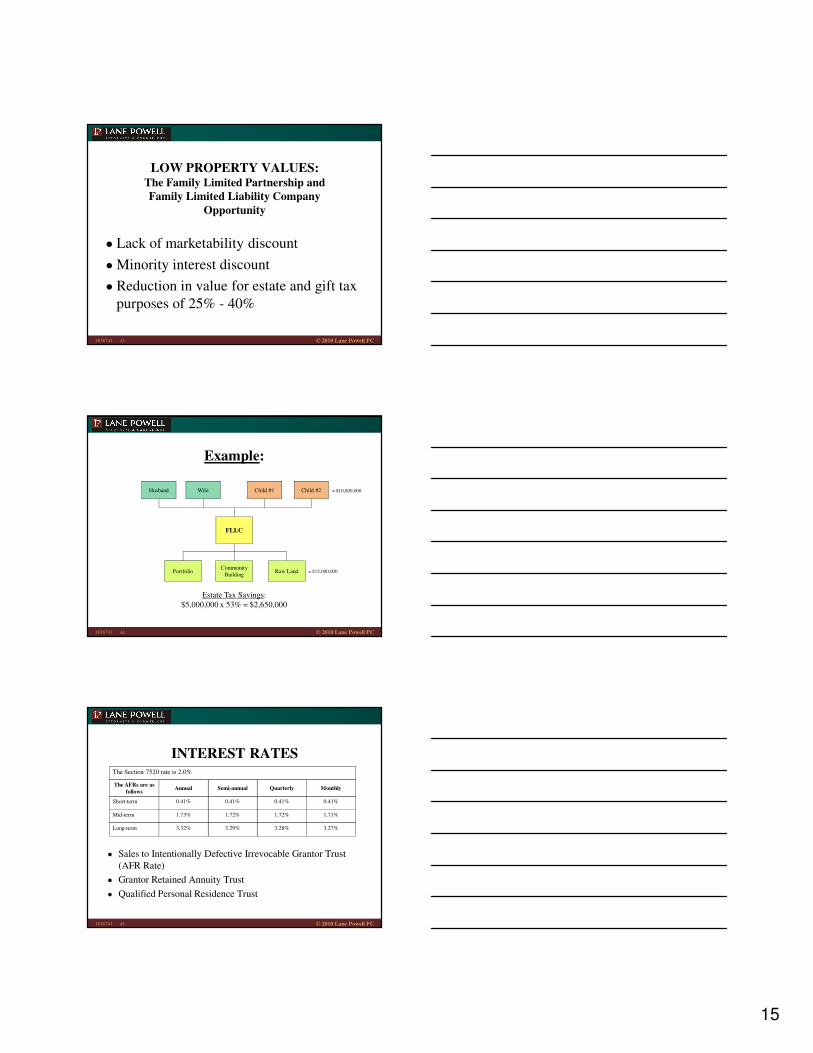

LOW PROPERTY VALUES:The Family Limited Partnership andFamily Limited Liability Company

Opportunity

● Lack of marketability discount

● Minority interest discount

● Reduction in value for estate and gift tax

purposes of 25% - 40%

© 2010 Lane Powell PC1838741 44

Example:

Estate Tax Savings:

$5,000,000 x 53% = $2,650,000

Husband Wife Child #1 Child #2

FLLC

PortfolioCommunity

BuildingRaw Land

= $10,000,000

= $15,000,000

© 2010 Lane Powell PC1838741 45

INTEREST RATES

● Sales to Intentionally Defective Irrevocable Grantor Trust

(AFR Rate)

● Grantor Retained Annuity Trust

● Qualified Personal Residence Trust

The Section 7520 rate is 2.0%

The AFRs are as follows

Annual Semi-annual Quarterly Monthly

Short-term 0.41% 0.41% 0.41% 0.41%

Mid-term 1.73% 1.72% 1.72% 1.71%

Long-term 3.32% 3.29% 3.28% 3.27%

16

© 2010 Lane Powell PC1838741 46

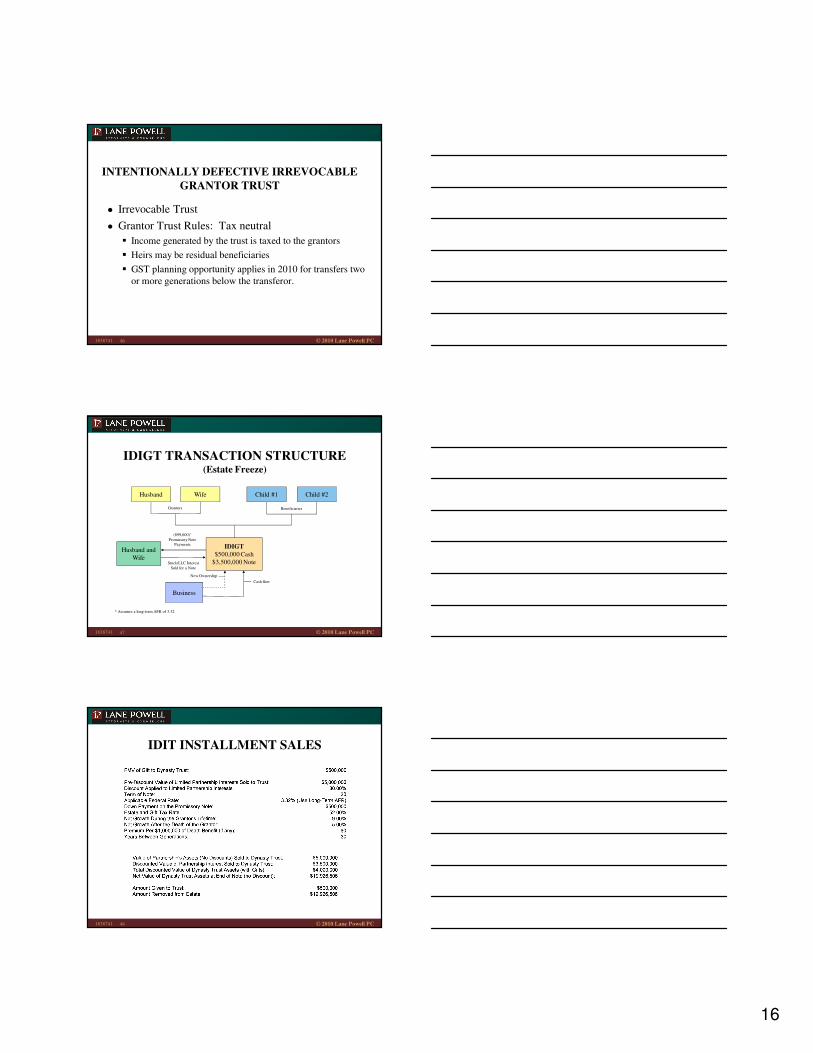

INTENTIONALLY DEFECTIVE IRREVOCABLE

GRANTOR TRUST

● Irrevocable Trust

● Grantor Trust Rules: Tax neutral

� Income generated by the trust is taxed to the grantors

� Heirs may be residual beneficiaries

� GST planning opportunity applies in 2010 for transfers two

or more generations below the transferor.

© 2010 Lane Powell PC1838741 47

Beneficiaries

IDIGT TRANSACTION STRUCTURE(Estate Freeze)

IDIGT

$500,000 Cash

$3,500,000 Note

Husband and

Wife

Business

Wife Child #2Child #1

($99,600)*

Promissory NotePayments

Stock/LLC Interest

Sold for a Note

Husband

Grantors

* Assumes a long-term AFR of 3.32.

Cash flow

New Ownership

© 2010 Lane Powell PC1838741 48

IDIT INSTALLMENT SALES

17

© 2010 Lane Powell PC1838741 49

EQUITY BUILD-UP WITHIN THE TRUST

© 2010 Lane Powell PC1838741 50

GRANTOR RETAINED ANNUITY TRUST

(GRAT)

● Irrevocable Grantor Trust

● Grantor transfers assets to trust in return for an

annuity

● Annuity is for a term of years

● End of annuity term, Trust assets pass to trust

remainder beneficiaries outright or in trust

● Taxable Gift = Present value of the remainder interest

© 2010 Lane Powell PC1838741 51

GRAT TRANSACTION STRUCTURE

Child #2Child #1

GRATHusband and

Wife

$2,575,200

(51.504%)

$5,000,000 (stock)

Remainder Beneficiaries

18

© 2010 Lane Powell PC1838741 52

HOW DOES A GRAT WORK?

● The GRAT can be structured so that the amount of the gift is minimal or zero.

● If the GRAT assets do not appreciate at a rate greater than the § 7520 rate, all the trust property is returned to the grantor in the form of annuity payments.

● If grantor dies during the GRAT term, all or most of the trust property will be included in the grantor’s gross estate and be subject to estate tax.

● If grantor survives the GRAT term and the assets appreciate at a rate greater than the § 7520 rate, the excess value passes to the remainder beneficiaries free of transfer tax.

© 2010 Lane Powell PC1838741 53

ADVANTAGES OF A GRAT

● Valuation – the annuity payments may be defined as a percentage of the contributed assets as finally determined for federal tax purposes.

● No trust income tax burden – GRATs are generally “grantor trusts” for income tax purposes.

● Substitution of assets – Grantor may retain power to substitute assets.

● High leverage – annuity may approximate value of assets contributed to trust; no additional equity required as compared to sale to a grantor trust.

● Preserves gift tax exemption – little or no gift tax exemption used up.

© 2010 Lane Powell PC1838741 54

CASE STUDY

● Grantor transfers 1,000,000 share of XYZ, Inc. stock to a 2-year GRAT. XYZ, Inc. is publicly traded and has a value of $5 per share. Grantor believes its value will appreciate at the rate of 50% per year over the next two years. Grantor wants to shift value to his children without any gift or estate tax. This is an opportune time to establish a GRAT due to the following factors:� The interest rate to calculate the value of the retained annuity is

extraordinarily low: 2%.

� The value of the asset is low and is expected to appreciate substantially over a relatively short period of time.

� Congress is likely to enact legislation in the near future that will reduce the desirability and effectiveness of GRATs.

● You prepare the following illustration.

19

© 2010 Lane Powell PC1838741 55

GRANTOR RETAINED ANNUITY TRUST

© 2010 Lane Powell PC1838741 56

GRANTOR RETAINED ANNUITY TRUST

© 2010 Lane Powell PC1838741 57

POTENTIAL DISADVANTAGES OF A GRAT

● § 7520 rate is higher than AFR, compare to sale.

● Decline in value of assets may cause GRAT to fail.

● Death of grantor during GRAT term may cause the GRAT to fail.

● Improper administration may cause the GRAT to fail.� Untimely payment of the annuity.

� Inadvertently making more than one contribution to the GRAT.

� Underpayment of the annuity due to valuation issues or otherwise.

� Acceleration or commutation of the amounts owned to grantor.

● Grantor’s GST exemption cannot be allocated during the GRAT term.

● What if the GRAT is too successful? The result may be inconsistent with grantor’s plans for his descendants.

20

© 2010 Lane Powell PC1838741 58

PROPOSED GRAT LEGISLATION

● The President has proposed restrictions on GRATs and a bill

approved by the House of Representatives earlier this year,

H.R. 4849, incorporated the following additional requirements

to be imposed on GRATs:

� A GRAT must have a minimum term of 10 years.

� The remainder interest must have a value greater than zero; and

� The annuity payments may not decrease during the term of the GRAT.

● H.R. 4849 provides that these restrictions will be effective for

transfers made after date of enactment. The bill has not been

passed by the Senate, but its passage is likely.

© 2010 Lane Powell PC1838741 59

QUALIFIED PERSONAL RESIDENCE TRUST

(QPRT)

● Convey home into an Irrevocable Trust

● Retain right to live in home for a term of years

● At end of term, home passes to trust beneficiaries outright or continues in trust

● Grantors may retain right to lease from trust at end of term

● Grantors may buy and sell home

● Grantors may repair and improve home

● Use two or four QPRTs: Fractional interest discount reduces Gift Tax Cost

● Low interest rates = higher remainder interest value (larger gift but property worth less)

© 2010 Lane Powell PC1838741 60

QUALIFIED PERSONAL RESIDENCE TRUST(No Fractional Interest Discount)

21

© 2010 Lane Powell PC1838741 61

QUALIFIED PERSONAL RESIDENCE TRUST(With 30% Fractional Interest Discount)

© 2010 Lane Powell PC1838741 62

QUALIFIED PERSONAL RESIDENCE TRUST(With Fractional Interest Discount)

© 2010 Lane Powell PC1838741 63

CHARITABLE LEAD ANNUITY TRUST (CLAT)

● You create a CLAT by transferring cash or other assets to an irrevocable trust. A charity receives fixed annuity (principal and interest) payments from the trust for the number of years you specify. At the end of that term, assets in the trust are transferred to the non-charitable remainder person (or persons) you specified when you set up the trust. Usually, this person is a child or grandchild but can be anyone, even someone who is not related to you. The transfer to the remainder person can be either outright or in trust.

● You can set up a CLAT during your lifetime or at your death.

● You can set up a CLAT so that you will receive an immediate and sizeable income tax deduction. In the second and following years, you must report the income earned by the trust even though it is actually paid to the charity in the form of an annuity. The advantage of the CLAT is that you can obtain an accelerated up front deduction and can spread out the income over a number of years.

(Continued)

22

© 2010 Lane Powell PC1838741 64

CHARITABLE LEAD ANNUITY TRUST

(CLAT)

● Another advantage of the CLAT is that it allows a “discounted” gift to family members. The value of a gift is determined at the time the gift is made. The family member remainderman must wait for the charity’s term to expire; therefore, the value of that remainderman’s interest is discounted for the “time cost” of waiting. In other words, the cost of making a gift is lowered because the value of the gift is decreased by the value of the annuity interest donated to charity.

● When the assets in the trust are transferred to the remainderman, any appreciation on the value of the assets is free of either gift or estate taxation in your estate.

© 2010 Lane Powell PC1838741 65

CHARITABLE LEAD ANNUITY TRUST

© 2010 Lane Powell PC1838741 66

CHARITABLE LEAD ANNUITY TRUST

23

© 2010 Lane Powell PC1838741 67

MISCELLANEOUS

Review IRA Beneficiary Designations

● Recent court cases make it unclear whether

non-spouse beneficiaries interest in an IRA

will be exempt from creditors’ claims

� In re Nessa (2010 Bankr. Ct. MN), 105 AFTR 2d

1020-609, 01/11/2010

� In re Chilton (Bankr. Ct. TX), 105 AFTR 2d 2010-

575, 03/03/2010

© 2010 Lane Powell PC1838741 68

Review IRA Beneficiary Designations(cont’d)

● Solution – The client should designate an irrevocable trust as the remainder beneficiary for the IRA account when the beneficiary is not a surviving spouse. Sub-trusts can be established within the trust for each child. Assets within the trust will be protected from the claims of the beneficiaries’ creditors. Otherwise, the debtor-beneficiary will have to hope that the state bankruptcy exemption statute protects the inherited IRA account.

© 2010 Lane Powell PC1838741 69

IRS Continues Attack to Prevent Gifts of Family LLCInterest from Qualifying for the § 2503(b) Annual Exclusion

● Two recent cases, Fisher and Price, have followed the reasoning of the 2003 Hackl decision to deny the grantors the $13,000 present interest gift tax exclusion under § 2503(b) when the grantors gifted LLC interests to their children.� Fisher v. United States, No. 1:08-V-00908

� Price v. Commissioner, T.C. Memo 2010-2 (January 4, 2010)

� Hackl v. Commissioner, 188 T.C. 279 (2002); affirmed, 335 F.3d 664 (7th Cir. 2003).

24

© 2010 Lane Powell PC1838741 70

● Both courts held that the gift of a present interest

requires the transfer of a right to a substantial present

economic benefit.

● Notwithstanding the regs talk about the “… present,

use, possession, enjoyment of the property transferred

…” Treas. Reg. § 25-2503-3(b)

● LLC Operating Agreements

� Very restrictive transfer rights

� No right to current distributions of “Distributable Cash”

© 2010 Lane Powell PC1838741 71

Solutions to the Present Interest Dilemma

● Operating Agreement Provisions

� Grant each donee a 30-day “put” option to convey

the gifted interest to the LLC for cash

� Require the distribution of Distributable Cash on a

yearly basis

© 2010 Lane Powell PC1838741 72

Seattle Portland

Olympia Anchorage

Tacoma London

www.lanepowell.com

Please be advised that this communication does not constitute federal tax advice and cannot be used for the

purpose of avoiding tax penalties unless you have expressly engaged us in advance and in writing to provide

written advice in a form that satisfies IRS standards for “covered opinions” or we have informed you in writing

that those standards do not apply to this communication

![AMERICAN BAR ASSOCIATION & INTERNATIONAL BAR … · [AMERICAN BAR ASSOCIATION & INTERNATIONAL BAR ASSOCIATION] AFFIDAVIT OF OBLIGATION INTERNATIONAL COMMERCIAL LIEN (This is a verified](https://img.pdfslide.us/doc/110x75/5f15d353e4731c257a32dad2/american-bar-association-international-bar-american-bar-association-.jpg)

![AMERICAN BAR ASSOCIATION & INTERNATIONAL …...[AMERICAN BAR ASSOCIATION & INTERNATIONAL BAR ASSOCIATION] AFFIDAVIT OF OBLIGATION INTERNATIONAL COMMERCIAL LIEN (This is a verified](https://img.pdfslide.us/doc/110x75/5f15d35de4731c257a32db06/american-bar-association-international-american-bar-association-.jpg)