Embed Size (px)

Citation preview

Schlumberger-Private

Paal KibsgaardChairman and CEO

2018 Barclays CEO Energy-Power Conference

New York, September 4, 2018

Schlumberger-Private

2

This presentation contains “forward-looking statements” within the meaning of the federal securities laws — that is, statements about the future, not about

past events. Such statements often contain words such as “expect,” “may,” “believe,” “plan,” “estimate,” “intend,” “anticipate,” “should,” “could,” “will,” “see,”

“likely,” and other similar words. Forward-looking statements address matters that are, to varying degrees, uncertain, such as statements about our financial

and performance targets and other forecasts or expectations regarding, or dependent on, our business outlook; growth for Schlumberger as a whole and for

each of our product lines (and for specified products or geographic areas within each product line); oil and natural gas demand and production growth; oil and

natural gas prices; rig activity, pricing; access to sand; improvements in operating procedures and technology, including our transformation program; our stock

repurchase program and dividend strategy; capital expenditures by Schlumberger and the oil and gas industry; the business strategies of Schlumberger’s

customers; the success of Schlumberger’s SPM projects; the success of Schlumberger’s acquisitions, joint ventures and alliances; future global economic

conditions; and future results of operations. These statements are subject to risks and uncertainties, including, but not limited to, global economic conditions;

changes in exploration and production spending by Schlumberger’s customers and changes in the level of oil and natural gas exploration and development;

general economic, political and business conditions in key regions of the world; foreign currency risk; pricing pressure; weather and seasonal factors; the

inability to procure or produce sand; our inability to meet our financial and performance targets and other forecasts or expectations, such as revenue and free

cash flow conversion; operational modifications, delays or cancellations; production declines; the inability close pending transactions; changes in government

regulations and regulatory requirements, including those related to offshore oil and gas exploration, radioactive sources, explosives, chemicals, hydraulic

fracturing services and climate-related initiatives; the inability of technology to meet new challenges in exploration; and other risks and uncertainties detailed

in our most recent Forms 10-K, 10-Q, and 8-K filed with or furnished to the U.S. Securities and Exchange Commission. If one or more of these or other risks

or uncertainties materialize (or the consequences of such a development changes), or should underlying assumptions prove incorrect, actual outcomes may

vary materially from those reflected in our forward-looking statements. The forward-looking statements speak only as of the date of this presentation, and

Schlumberger disclaims any intention or obligation to update publicly or revise such statements, whether as a result of new information, future events or

otherwise.

Safe Harbor

Schlumberger-Private

3

Key Questions

Why the need

for increased

E&P investment?

Why will Schlumberger

generate the best returns

in the coming upcycle?

Why is Schlumberger

best positioned to

capture the growth?

Schlumberger-Private

Why the need for increased E&P investment?

4

Schlumberger-Private

0

200

400

600

800

1,000

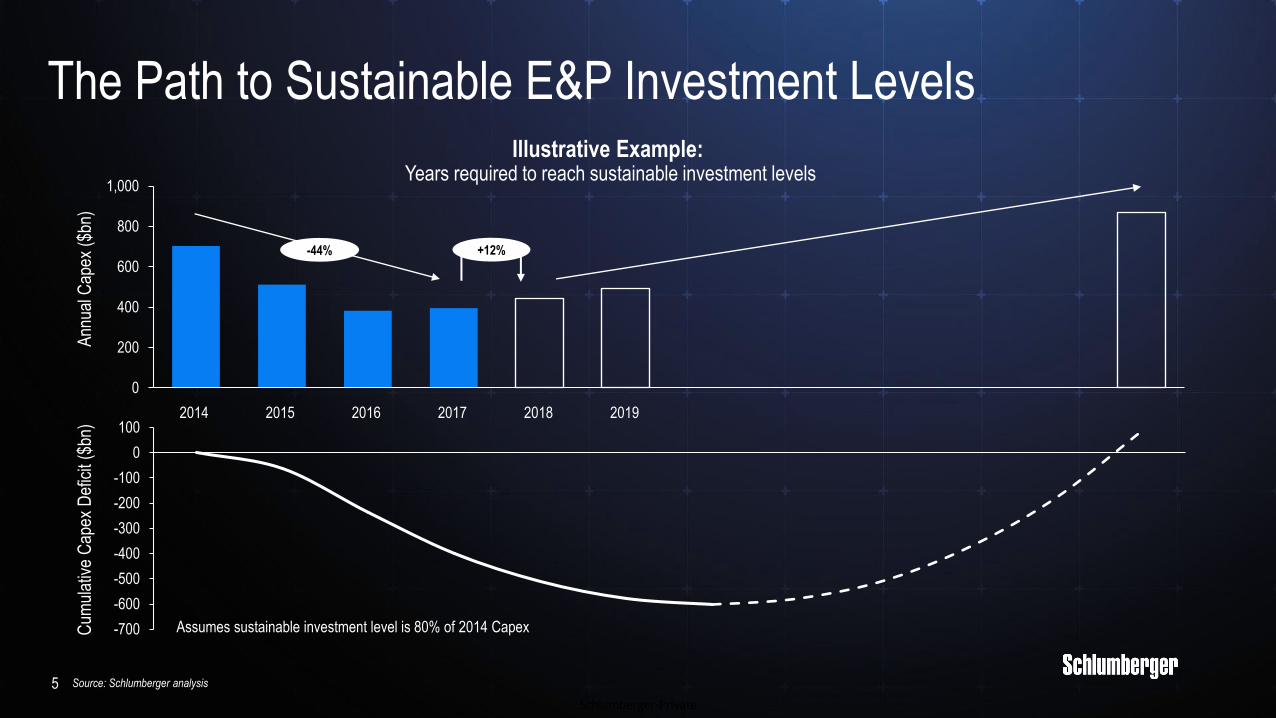

The Path to Sustainable E&P Investment Levels

5

-700

-600

-500

-400

-300

-200

-100

0

100

Illustrative Example: Years required to reach sustainable investment levels

-44%

20162014 2015 20192017 2018

+12%

Ann

ual C

apex

($b

n)C

umul

ativ

e C

apex

Def

icit

($bn

)

Assumes sustainable investment level is 80% of 2014 Capex

Source: Schlumberger analysis

Schlumberger-Private

0

10

20

30

40

50

6

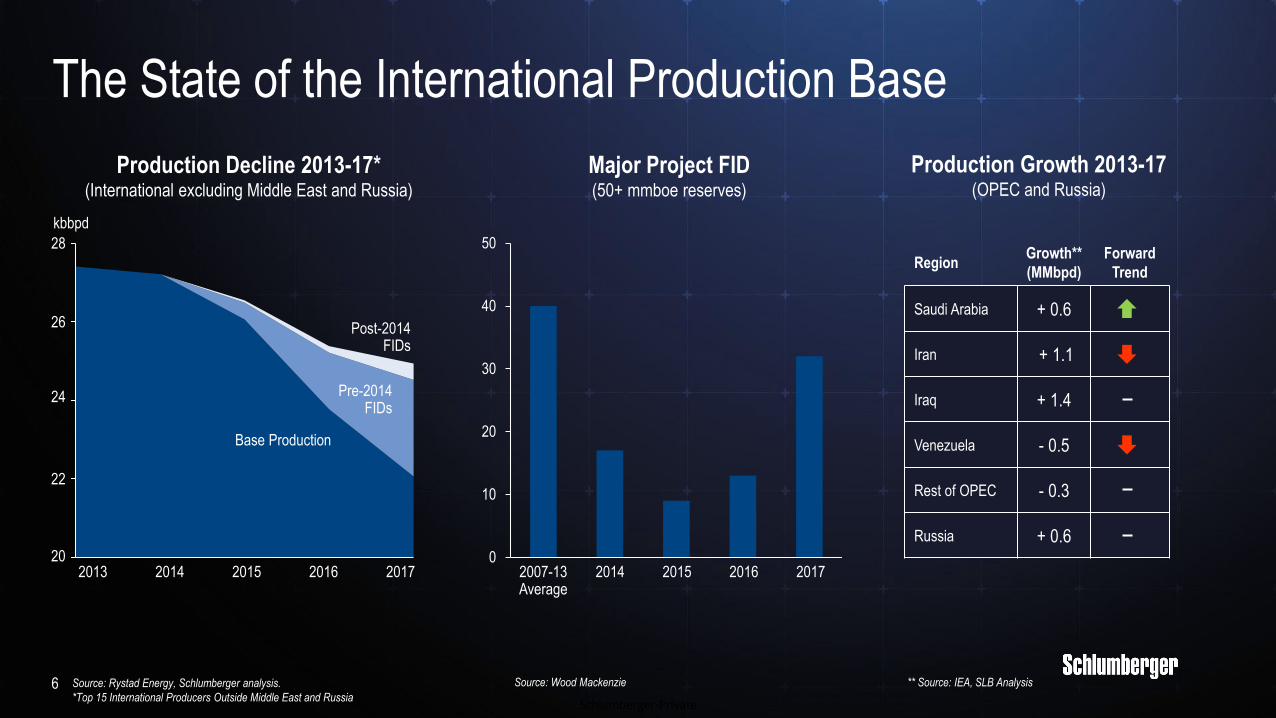

24

20

28

kbbpd

2014 2016 2017

Base Production

Pre-2014FIDs

The State of the International Production Base

Production Decline 2013-17*(International excluding Middle East and Russia)

Major Project FID(50+ mmboe reserves)

Production Growth 2013-17(OPEC and Russia)

2007-13Average

20162014 2015 20172013 2015

Post-2014FIDs

RegionGrowth**

(MMbpd)

Forward

Trend

Saudi Arabia + 0.6

Iran + 1.1

Iraq + 1.4

Venezuela - 0.5

Rest of OPEC - 0.3

Russia + 0.6

26

22

Source: Rystad Energy, Schlumberger analysis.

*Top 15 International Producers Outside Middle East and Russia

Source: Wood Mackenzie ** Source: IEA, SLB Analysis

Schlumberger-Private

7

0

2

4

6

8

10

12

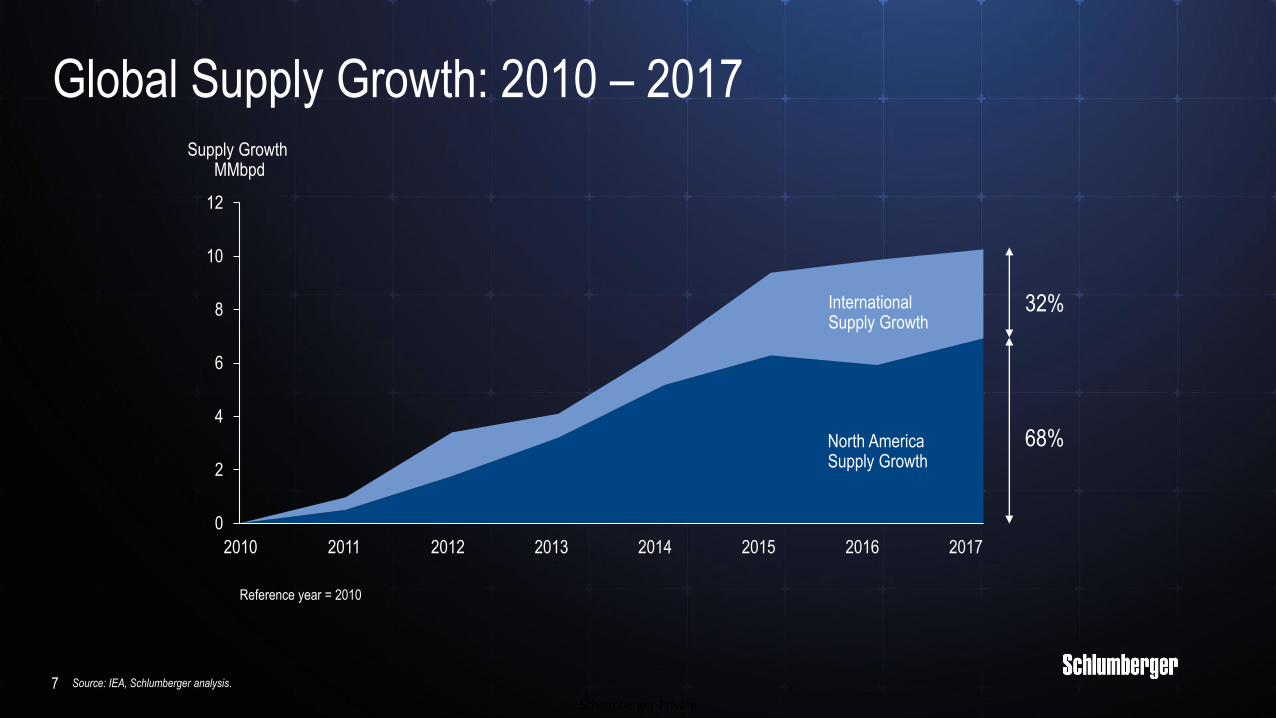

2010 2013 201620122011 2014 2015 2017

North AmericaSupply Growth

Global Supply Growth: 2010 – 2017

Reference year = 2010

InternationalSupply Growth

Source: IEA, Schlumberger analysis.

Supply Growth MMbpd

68%

32%

Schlumberger-Private

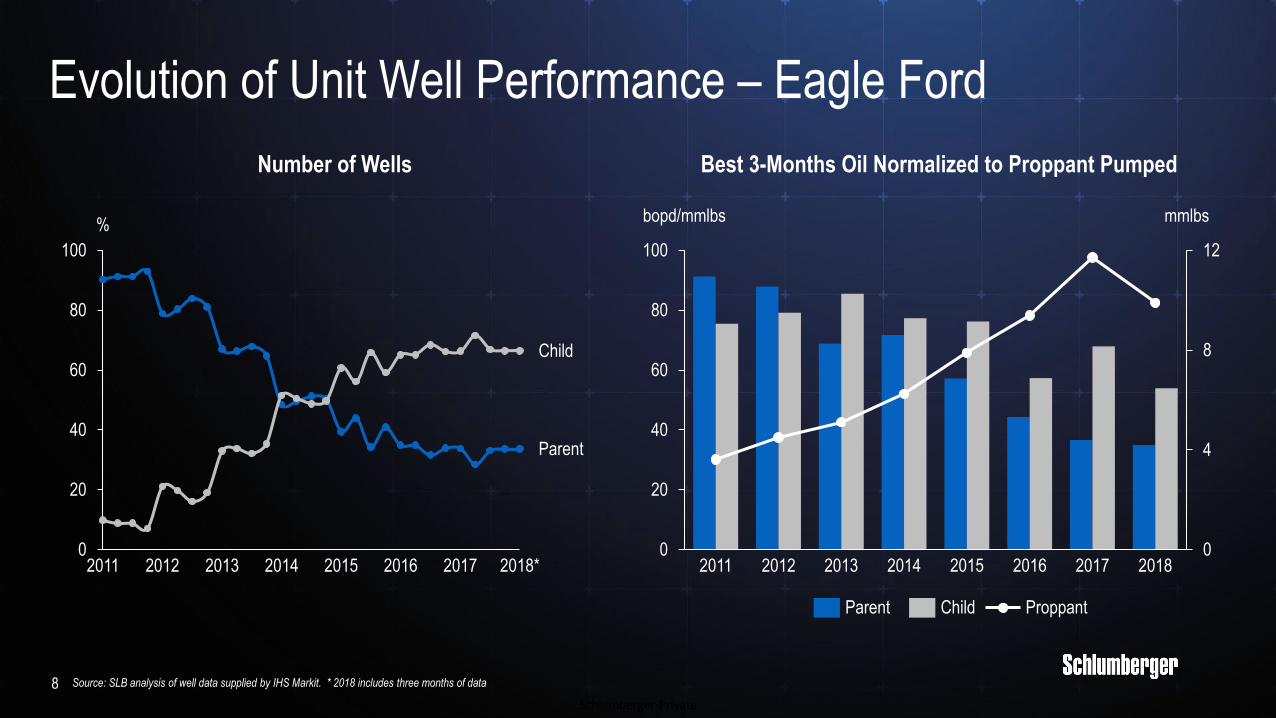

Evolution of Unit Well Performance – Eagle Ford

0

20

40

60

80

100

2014

%

20122011 20162013 2015 2017 2018*

Parent

Child

0

4

8

12

0

20

40

60

80

100

2014

mmlbs

20132011 2012 2015 2016 2017 2018

bopd/mmlbs

ChildParent Proppant

Best 3-Months Oil Normalized to Proppant PumpedNumber of Wells

Source: SLB analysis of well data supplied by IHS Markit. * 2018 includes three months of data8

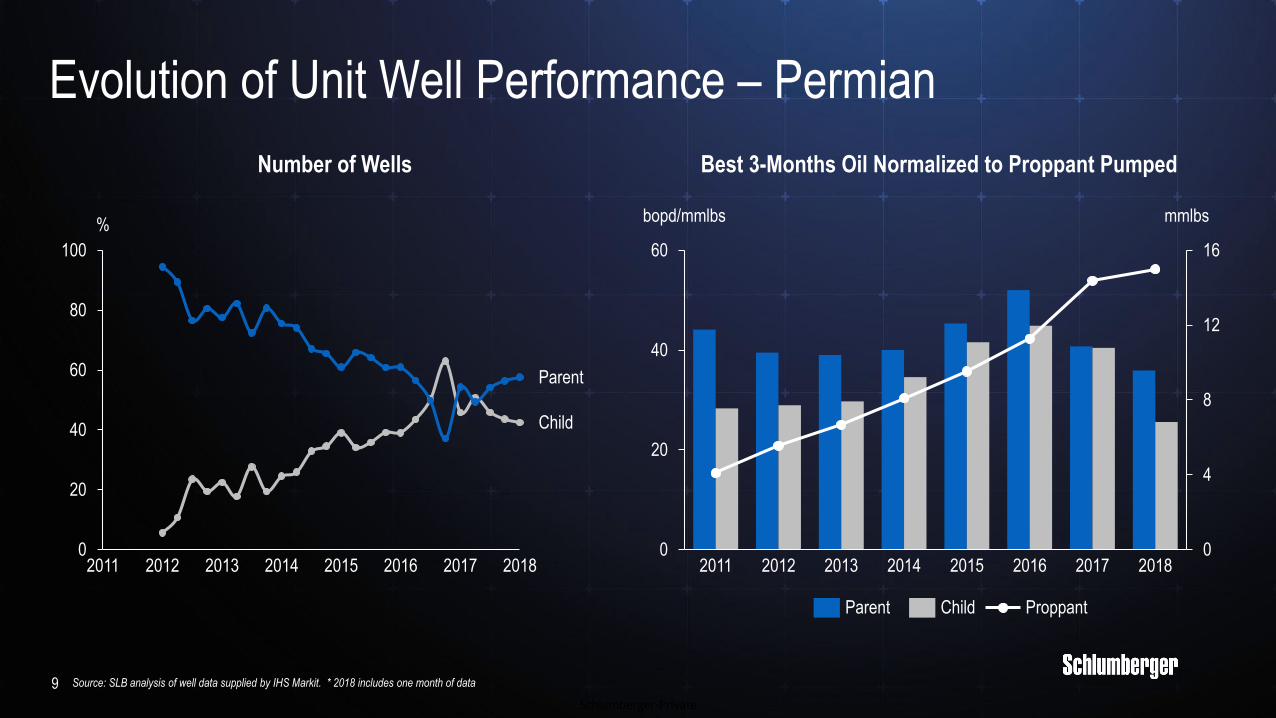

Schlumberger-Private

0

20

40

60

80

100

%

20152011 20172012 201620142013 2018

Child

Parent

0

4

8

12

16

0

20

40

60

mmlbs

20182015

bopd/mmlbs

20162011 2012 2013 2014 2017

ProppantParent Child

Best 3-Months Oil Normalized to Proppant PumpedNumber of Wells

Source: SLB analysis of well data supplied by IHS Markit. * 2018 includes one month of data9

Evolution of Unit Well Performance – Permian

Schlumberger-Private

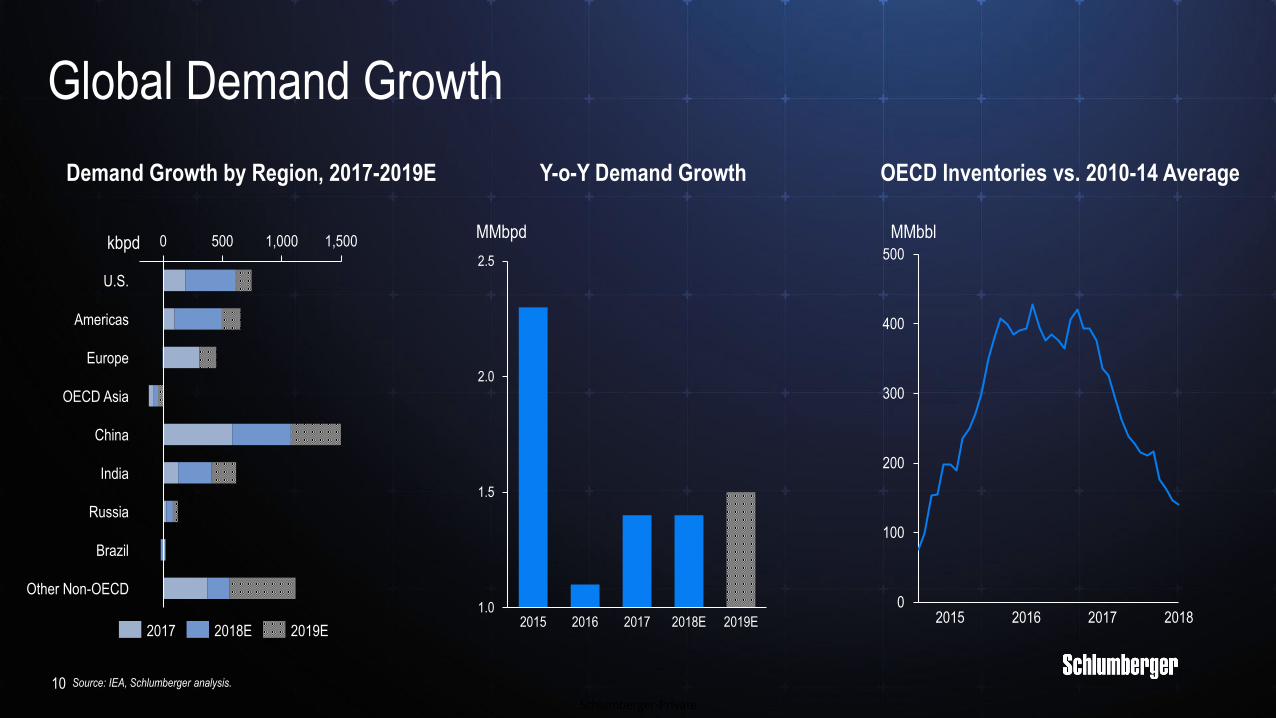

Global Demand Growth

10

1,5005000 1,000

U.S.

Americas

Europe

OECD Asia

China

India

Russia

Brazil

Other Non-OECD

2017 2019E2018E

Demand Growth by Region, 2017-2019E

0

100

200

300

400

500

20172015 2016 2018

OECD Inventories vs. 2010-14 Average

1.0

1.5

2.0

2.5

2018E20172015 2016 2019E

Y-o-Y Demand Growth

kbpdMMbpd MMbbl

Source: IEA, Schlumberger analysis.

Schlumberger-Private

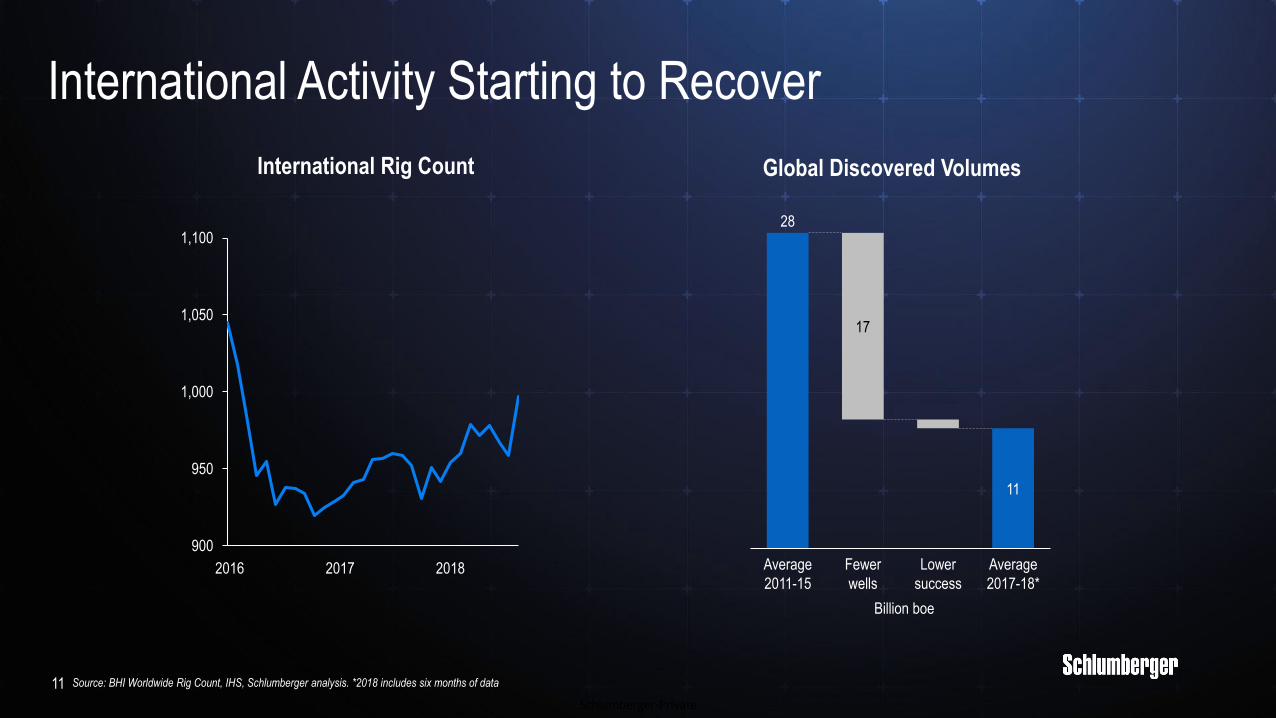

International Activity Starting to Recover

11

Global Discovered Volumes

900

950

1,000

1,050

1,100

2016 2017 2018

International Rig Count

Billion boe

Source: BHI Worldwide Rig Count, IHS, Schlumberger analysis. *2018 includes six months of data

Average

2011-15

17

Fewer

wells

Lower

success

Average

2017-18*

11

28

Schlumberger-Private

12

Why is Schlumberger best positioned to capture the growth?

Schlumberger-Private

Unmatched Global Footprint

13

100,000 Employees

120 Countries

140+ Nationalities

90 Technology & Mfg centers

1,900 Facilities

Global Stewardship

Schlumberger-Private

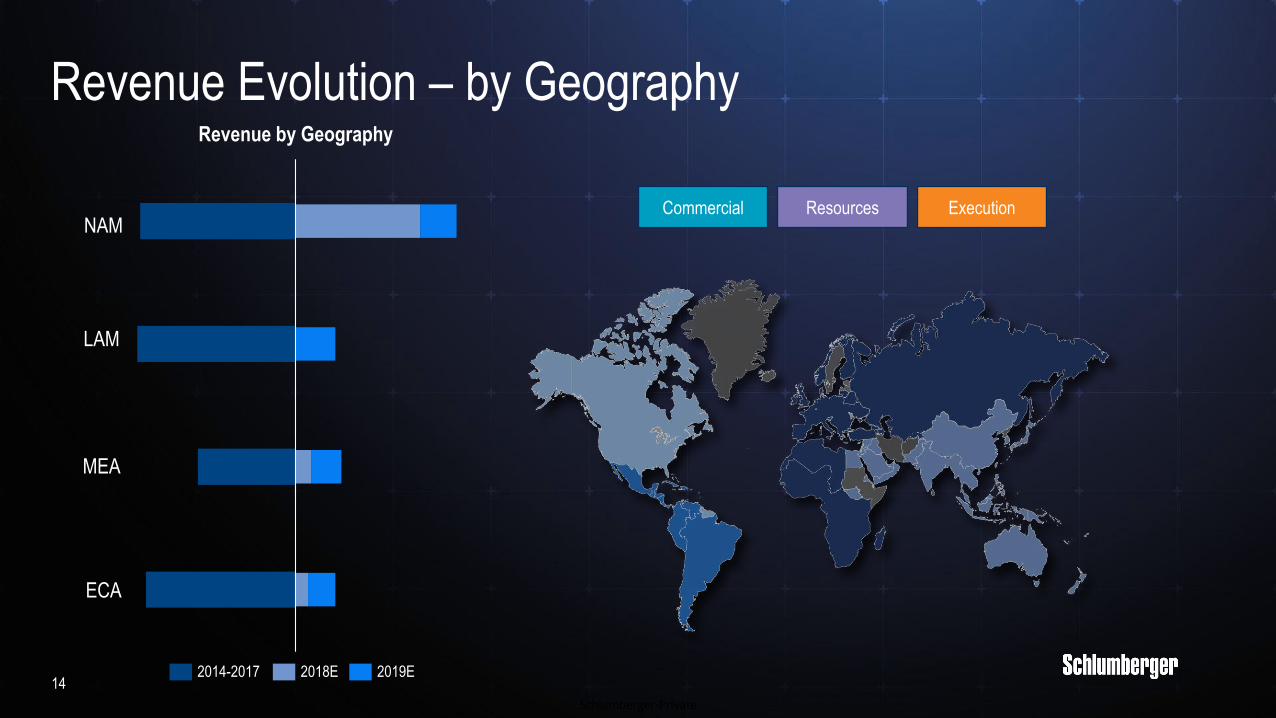

Revenue Evolution – by Geography

14

Revenue by Geography

NAM

LAM

MEA

ECA

2018E 2019E2014-2017

Commercial Resources Execution

Schlumberger-Private

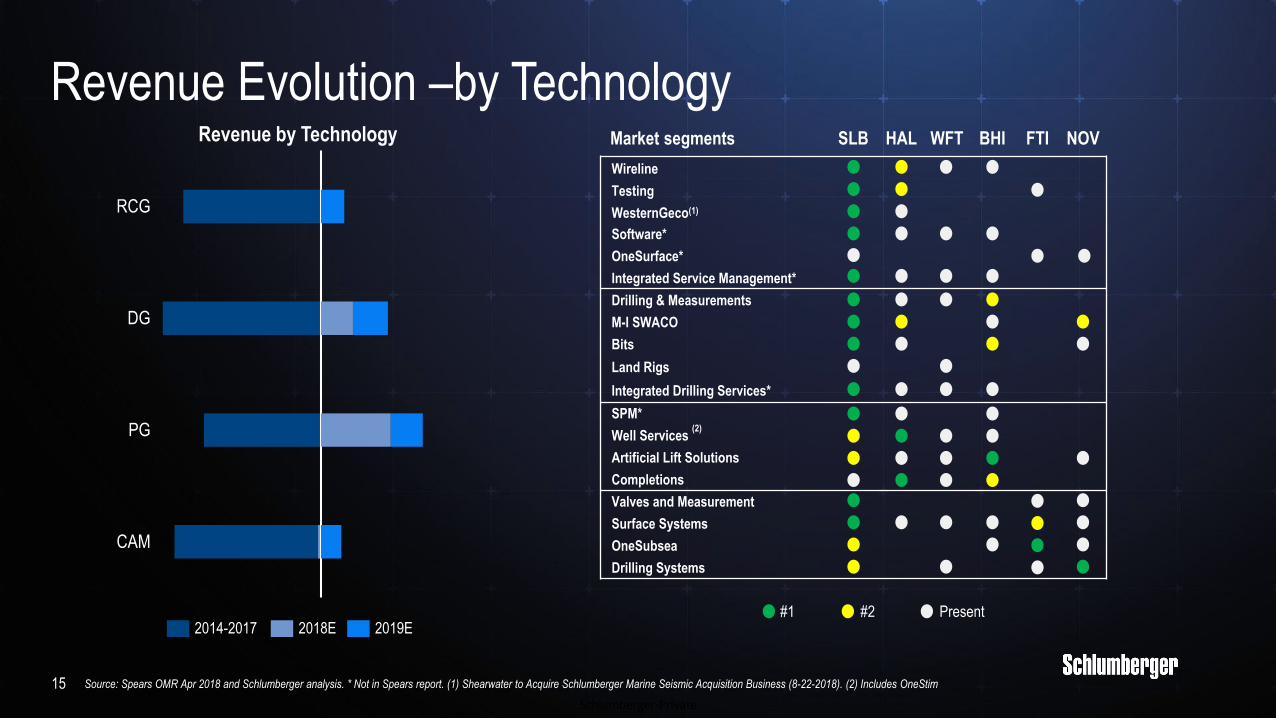

Revenue Evolution –by Technology

Source: Spears OMR Apr 2018 and Schlumberger analysis. * Not in Spears report. (1) Shearwater to Acquire Schlumberger Marine Seismic Acquisition Business (8-22-2018). (2) Includes OneStim15

#1 #2 Present

Market segments SLB HAL WFT BHI FTI NOV

Wireline

Testing

WesternGeco(1)

Software*

OneSurface*

Integrated Service Management*

Drilling & Measurements

M-I SWACO

Bits

Land Rigs

Integrated Drilling Services*

SPM*

Well Services (2)

Artificial Lift Solutions

Completions

Valves and Measurement

Surface Systems

OneSubsea

Drilling Systems

PG

RCG

DG

CAM

2014-2017 2019E2018E

Revenue by Technology

Schlumberger-Private

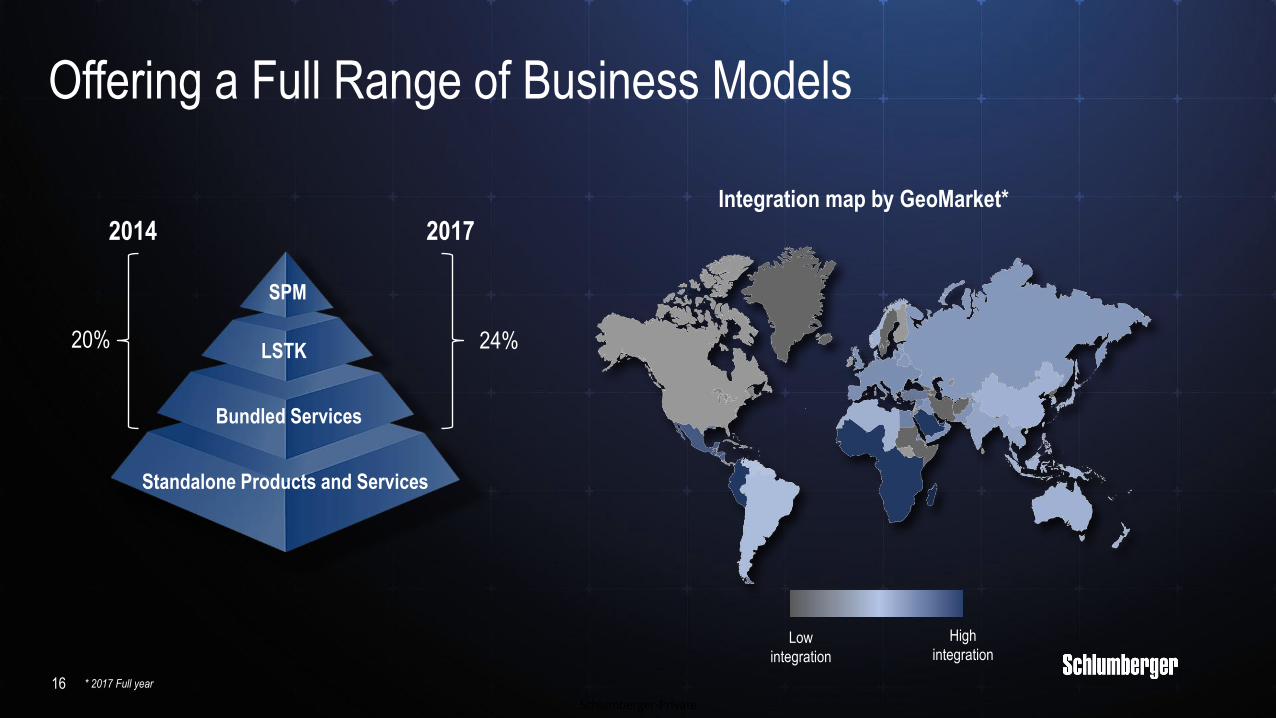

Offering a Full Range of Business Models

2014 2017

20% 24%

SPM

LSTK

Bundled Services

16

High

integrationLow

integration

Standalone Products and Services

Integration map by GeoMarket*

* 2017 Full year

Schlumberger-Private

17

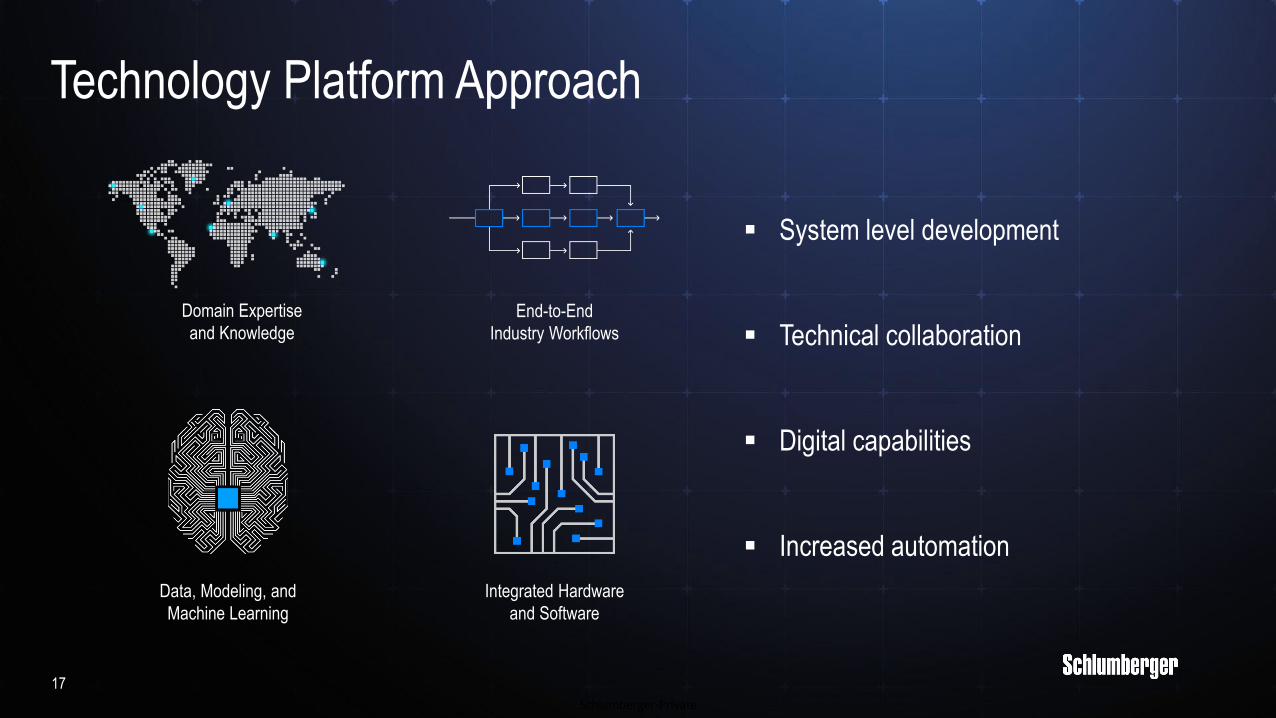

Technology Platform Approach

End-to-End

Industry Workflows

Domain Expertise

and Knowledge

Integrated Hardware

and Software

Data, Modeling, and

Machine Learning

▪ System level development

▪ Technical collaboration

▪ Digital capabilities

▪ Increased automation

Schlumberger-Private

18

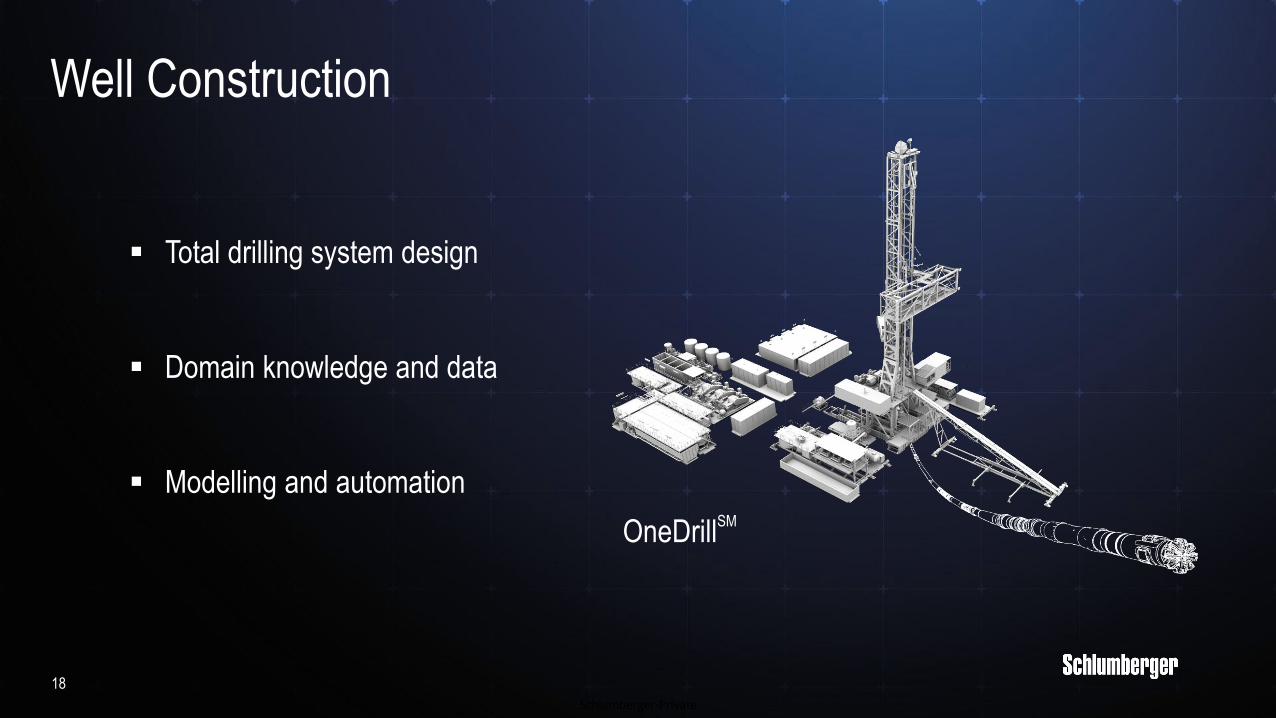

Well Construction

▪ Total drilling system design

▪ Domain knowledge and data

▪ Modelling and automation

OneDrillSM

Schlumberger-Private

19

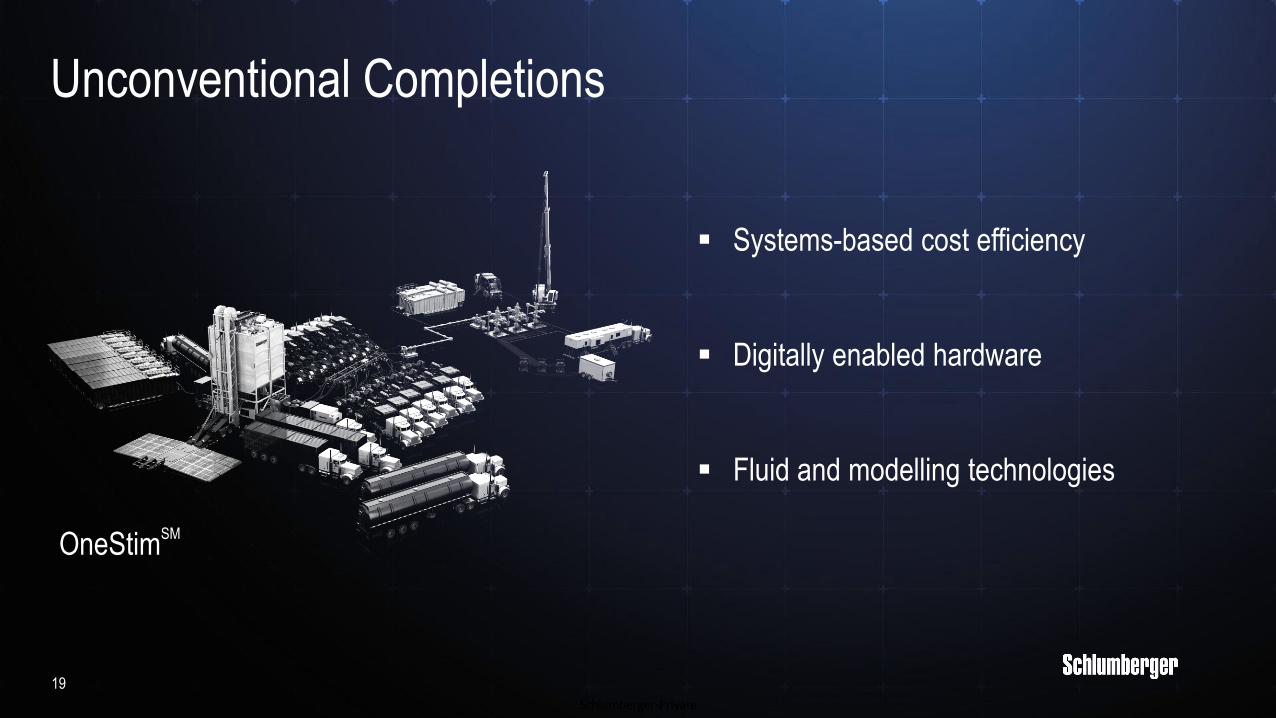

Unconventional Completions

▪ Systems-based cost efficiency

▪ Digitally enabled hardware

▪ Fluid and modelling technologies

OneStimSM

Schlumberger-Private

20

Why will Schlumberger generate the best

returns in the coming upcycle?

Schlumberger-Private

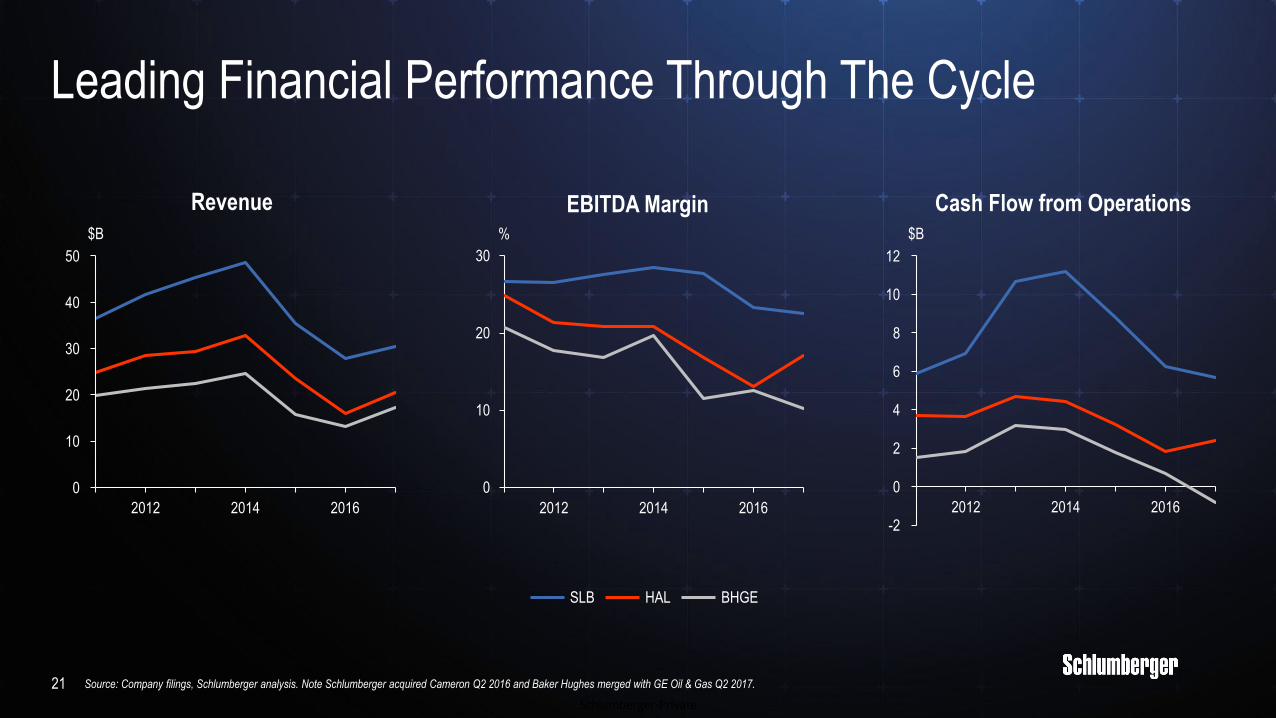

Leading Financial Performance Through The Cycle

21 Source: Company filings, Schlumberger analysis. Note Schlumberger acquired Cameron Q2 2016 and Baker Hughes merged with GE Oil & Gas Q2 2017.

Revenue EBITDA Margin Cash Flow from Operations

0

20142012 2016

20

10

30

40

50

$B

0

10

20

30

20142012 2016

%

2012 20162014

2

-2

0

4

6

12

8

10

$B

SLB HAL BHGE

Schlumberger-Private

22

Perfecting Our Modernized Way of Working

Streamlined Internal Workflows Digital Capabilities

Professionalized Functions Millennials Workplace

Schlumberger-Private

Top Line Outgrow

Incremental Margins >65%

Cashflow Conversion >75%

Excess Cash Return to Shareholders

23

Our Goals