Embed Size (px)

Citation preview

kghfhfhf

Bertelsmann AG Presentation

March 2002

Bertelsmann’s Strategic Positioning IN THE MEDIA & ENTERTAINMENT INDUSTRY

University of Illinois Executive MBA

kghfhfhf

Bertelsmann AG Presentation

Donna AcklinJay BartlettDan Becker

Brad ComincioliAnne Jennings

Christine MajersRadha Nandkumar

Paulo OliveiraTroy Scott

Vanisha TaylorFaculty Advisor: Professor Joe Mahoney

Bertelsmann’s Strategic Positioning IN THE MEDIA & ENTERTAINMENT INDUSTRY

kghfhfhf

Bertelsmann AG Presentation

Defining the Business: The Starting Point of Strategy

For the purposes of our presentation, we define the

Media & Entertainment Industry as encompassing

companies dedicated to the creation and/or

aggregation and/or distribution of intellectual property

aimed at providing leisure to users, through any

available media outlet.

kghfhfhf

Bertelsmann AG Presentation

Key Industry Participants

AOL Time Warner

Bertelsmann

News Corporation / Fox

Walt Disney

Viacom

Vivendi Universal

kghfhfhf

Bertelsmann AG Presentation

What are the key strategic factors shaping the

Media & Entertainment industry?

What strategies will enhance Bertelsmann’s

future positioning within the industry?

Strategic Focus of the Presentation

kghfhfhf

Bertelsmann AG Presentation

Bertelsmann’s Strategic Positioning in the Media & Entertainment Industry

Industry Analysis

Value Chain Analysis

Recommendations

….……….….Jay Bartlett

…… Anne Jennings

….……. Paulo Oliveira

kghfhfhf

Bertelsmann AG Presentation

Industry Analysis

Jay Bartlett

kghfhfhf

Bertelsmann AG Presentation

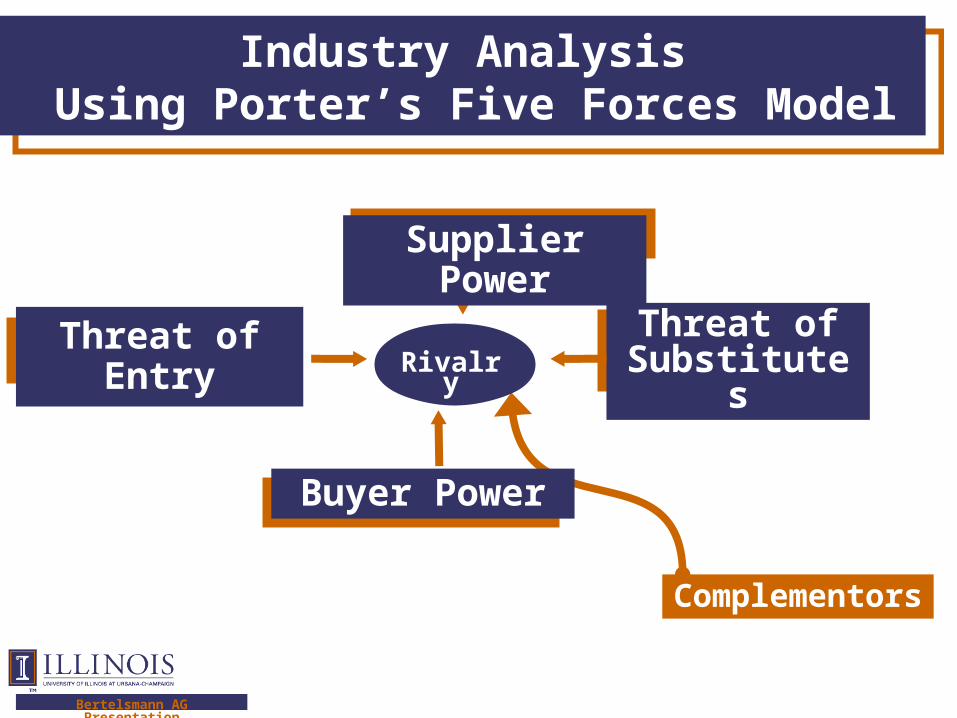

Industry Analysis Using Porter’s Five Forces Model

Buyer Power

RivalryThreat of

SubstitutesThreat of Entry

Supplier Power

Complementors

kghfhfhf

Bertelsmann AG Presentation

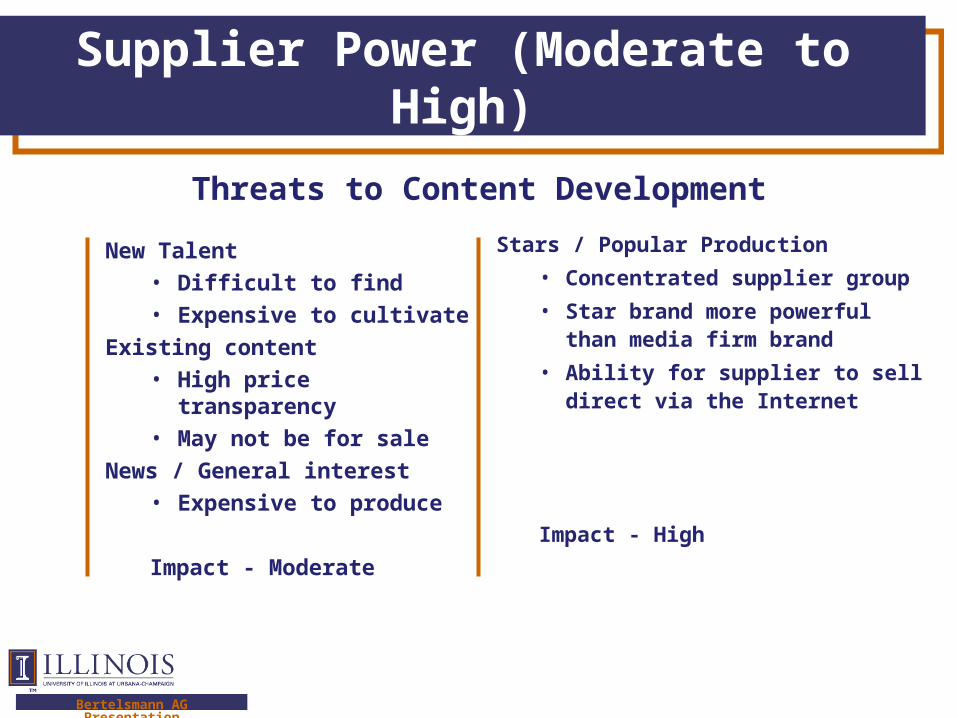

Supplier Power (Moderate to High)

New Talent

• Difficult to find

• Expensive to cultivate

Existing content

• High price transparency

• May not be for sale

News / General interest

• Expensive to produce

Impact - Moderate

Stars / Popular Production

• Concentrated supplier group

• Star brand more powerful than media firm brand

• Ability for supplier to sell direct via the Internet

Impact - High

Threats to Content Development

kghfhfhf

Bertelsmann AG Presentation

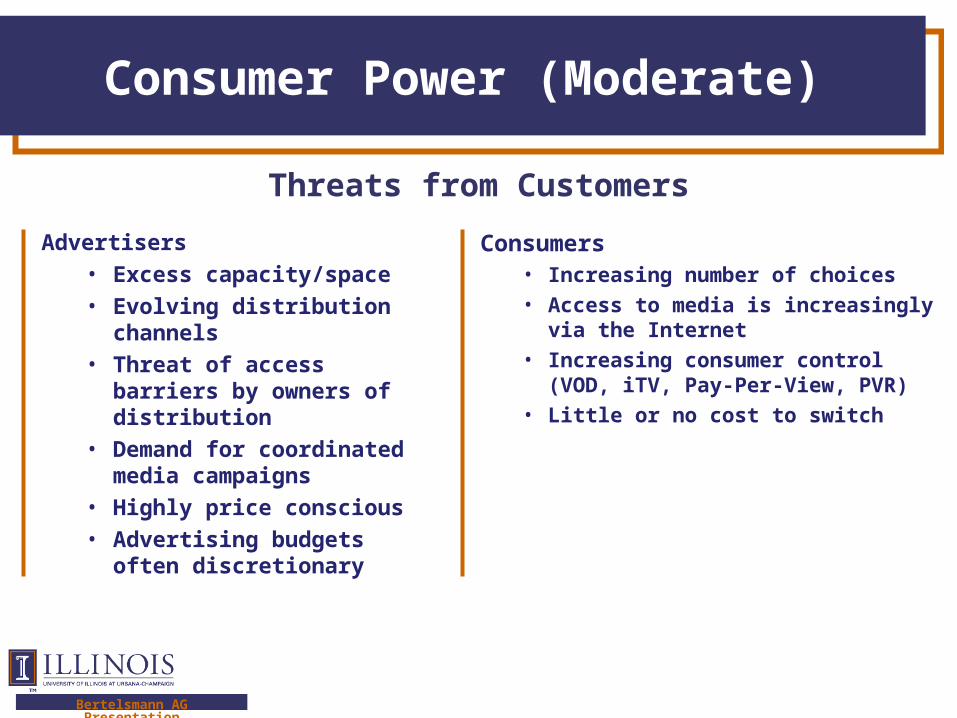

Consumer Power (Moderate)

Advertisers

• Excess capacity/space

• Evolving distribution channels

• Threat of access barriers by owners of distribution

• Demand for coordinated media campaigns

• Highly price conscious

• Advertising budgets often discretionary

Consumers• Increasing number of choices

• Access to media is increasingly via the Internet

• Increasing consumer control (VOD, iTV, Pay-Per-View, PVR)

• Little or no cost to switch

Threats from Customers

kghfhfhf

Bertelsmann AG Presentation

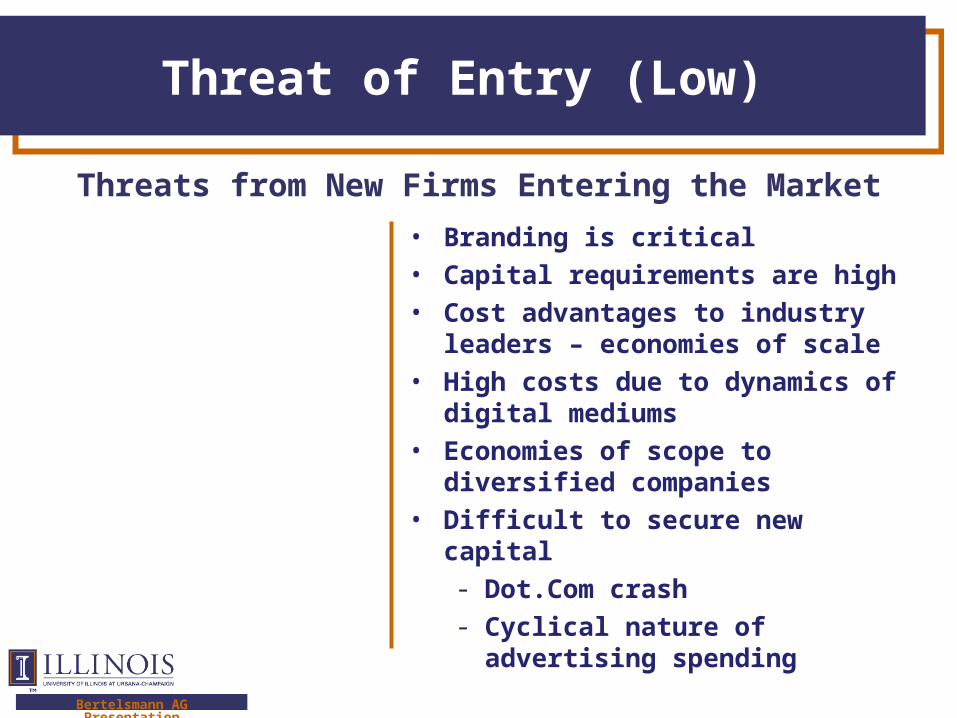

Threat of Entry (Low)

• Branding is critical• Capital requirements are high• Cost advantages to industry

leaders – economies of scale• High costs due to dynamics of

digital mediums • Economies of scope to diversified

companies• Difficult to secure new capital

- Dot.Com crash- Cyclical nature of advertising

spending

Threats from New Firms Entering the Market

kghfhfhf

Bertelsmann AG Presentation

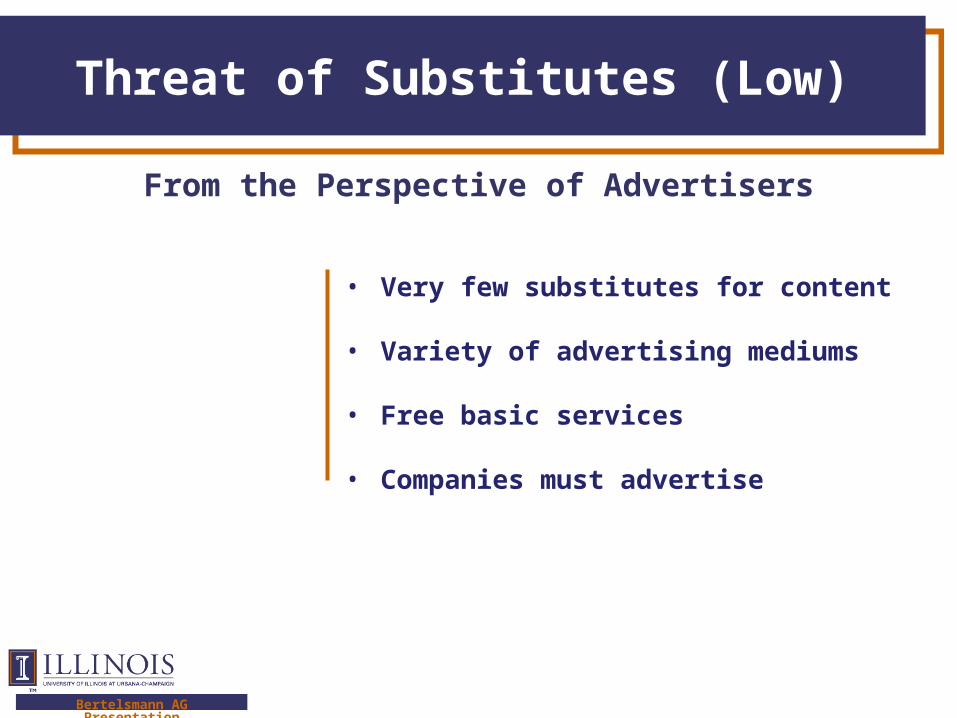

Threat of Substitutes (Low)

• Very few substitutes for content

• Variety of advertising mediums

• Free basic services

• Companies must advertise

From the Perspective of Advertisers

kghfhfhf

Bertelsmann AG Presentation

Rivalry (High)

• Evolving industry• High fixed costs• Excess advertising capacity• Short product life cycles• High entry and exit costs• Large number of competitors

Propensity for Strong Price-based Competition

kghfhfhf

Bertelsmann AG Presentation

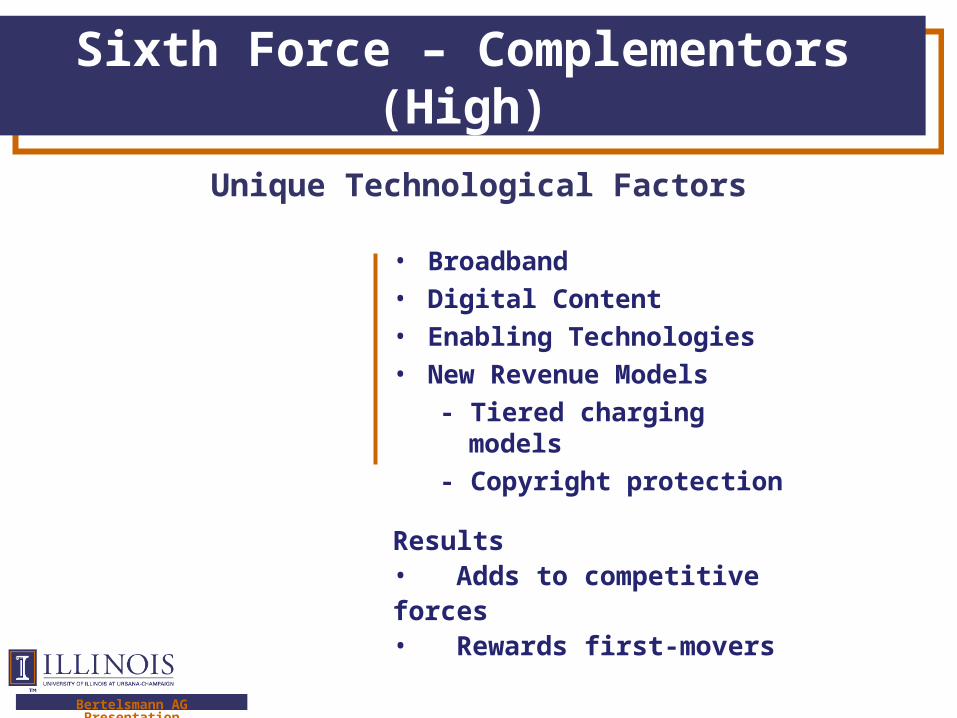

Sixth Force – Complementors (High)

• Broadband• Digital Content• Enabling Technologies• New Revenue Models

- Tiered charging models

- Copyright protection

Unique Technological Factors

Results • Adds to competitive forces • Rewards first-movers

kghfhfhf

Bertelsmann AG Presentation

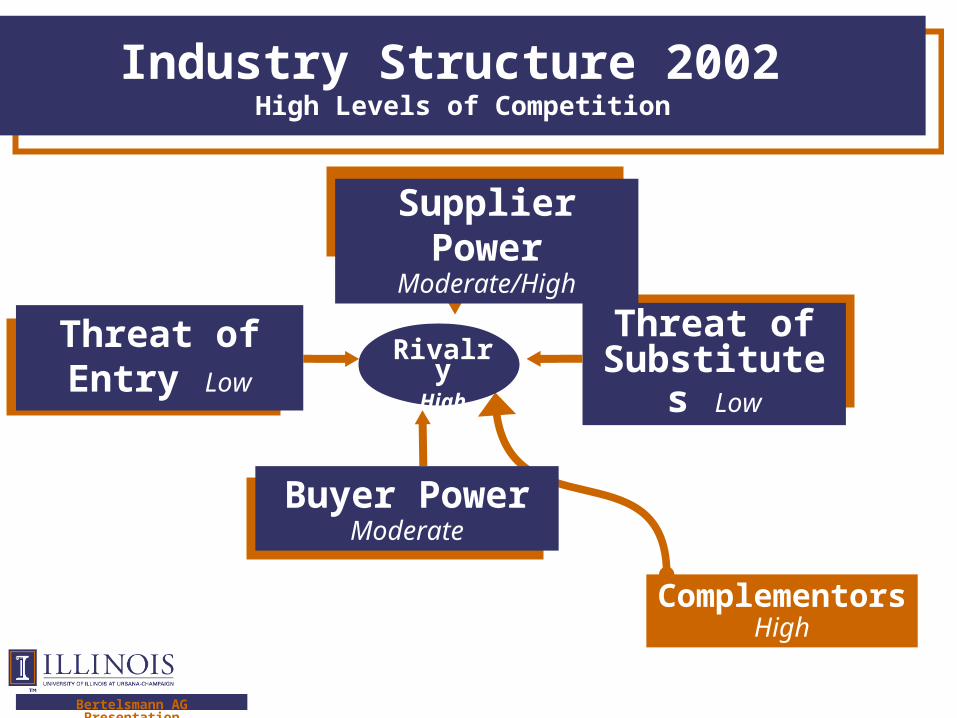

Industry Structure 2002 High Levels of Competition

Buyer Power Moderate

RivalryHigh

Threat of Substitutes

Low

Threat of Entry Low

Supplier Power Moderate/High

ComplementorsHigh

kghfhfhf

Bertelsmann AG Presentation

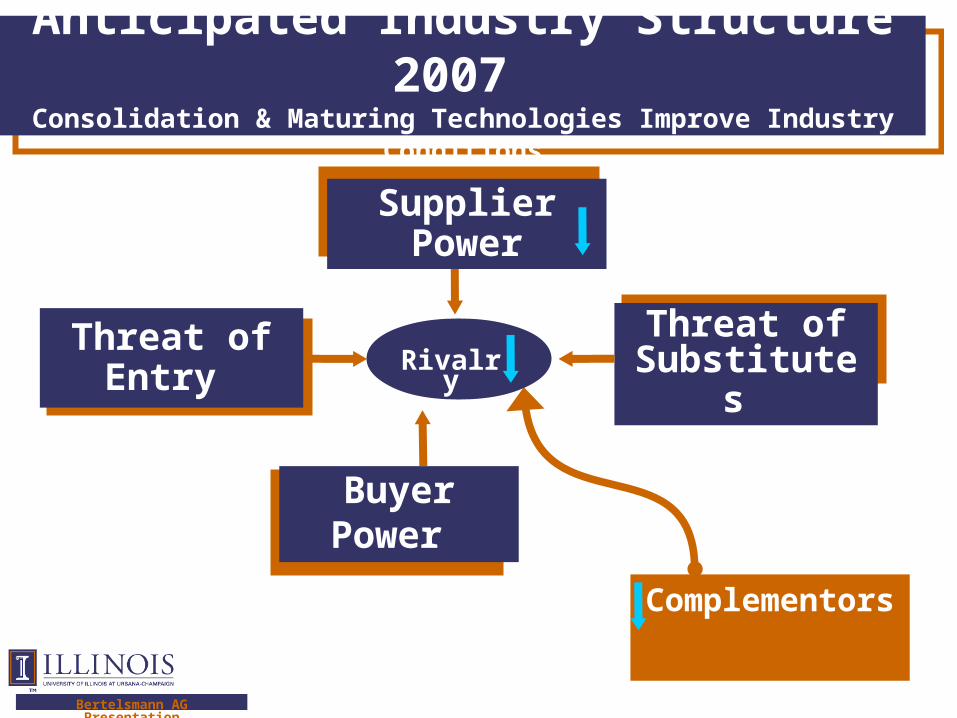

Anticipated Industry Structure 2007 Consolidation & Maturing Technologies Improve Industry Conditions

Buyer Power

RivalryThreat of

Substitutes Threat of

Entry

Supplier Power

Complementors

kghfhfhf

Bertelsmann AG Presentation

Value Chain Analysis

Anne Jennings

kghfhfhf

Bertelsmann AG Presentation

Vertical Coordination

From the industry analysis we conclude that a key element to improving industry conditions is vertical integration.

• Cost reduction

• Distribution channel risks

• Wide-scope advertising campaigns

Therefore, we turn our focus towards the firm using the tool value-chain analysis.

kghfhfhf

Bertelsmann AG Presentation

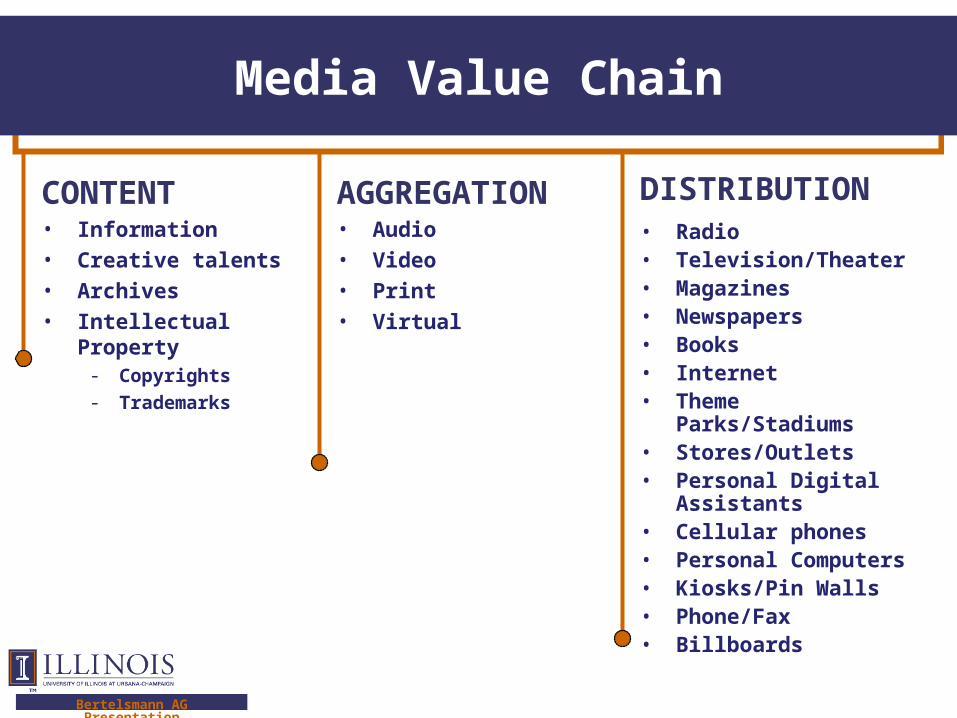

Media Value Chain

DISTRIBUTION• Radio• Television/Theater• Magazines• Newspapers• Books• Internet• Theme Parks/Stadiums• Stores/Outlets• Personal Digital

Assistants• Cellular phones• Personal Computers• Kiosks/Pin Walls• Phone/Fax• Billboards

CONTENT• Information• Creative talents• Archives• Intellectual Property

- Copyrights- Trademarks

AGGREGATION• Audio• Video• Print• Virtual

kghfhfhf

Bertelsmann AG Presentation

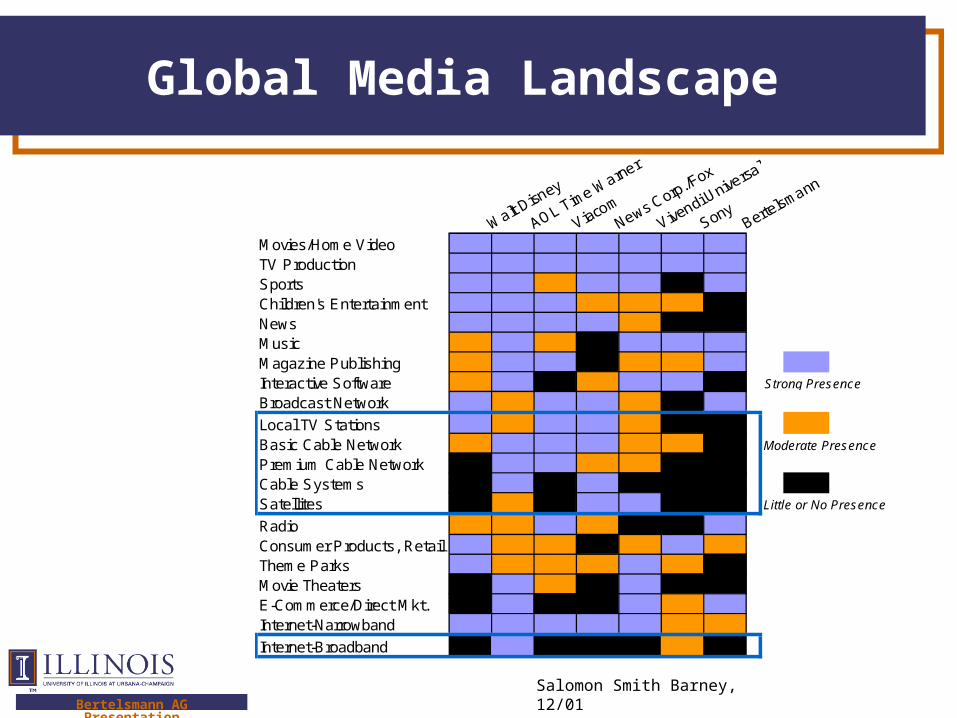

Global Media Landscape

Movies/Home VideoTV ProductionSportsChildren's EntertainmentNewsMusicMagazine PublishingInteractive SoftwareBroadcast Network

Local TV StationsBasic Cable Network Moderate Presence

Premium Cable NetworkCable SystemsSatellites Little or No Presence

RadioConsumer Products, RetailTheme ParksMovie TheatersE-Commerce/Direct Mkt.Internet-Narrowband

Internet-Broadband

Strong Presence

Salomon Smith Barney, 12/01

kghfhfhf

Bertelsmann AG Presentation

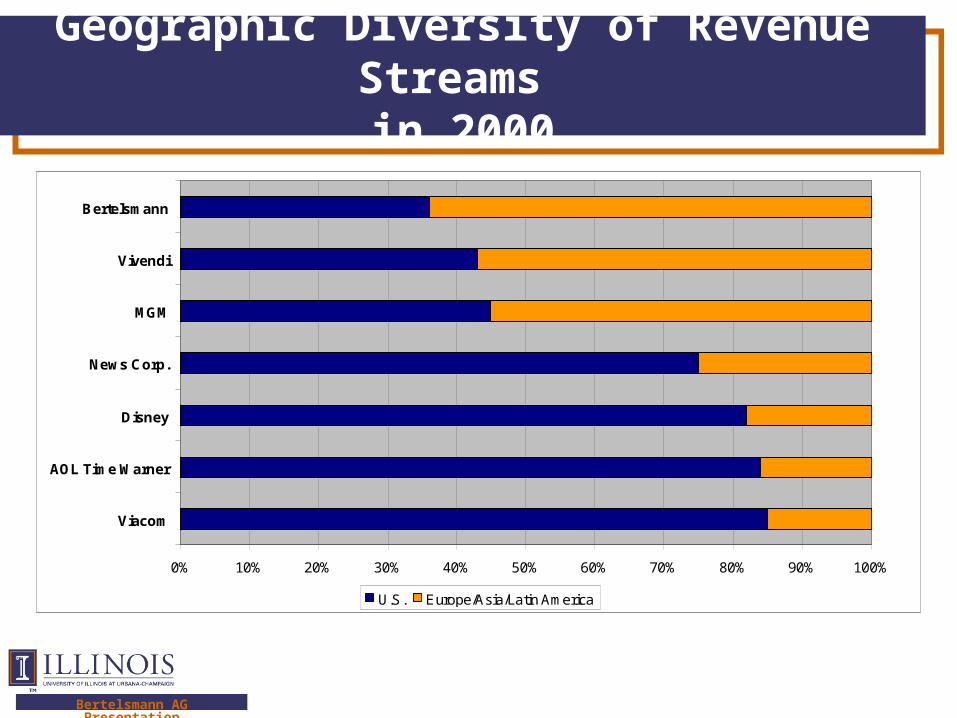

Geographic Diversity of Revenue Streams in 2000

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Viacom

AOL Time Warner

Disney

News Corp.

MGM

Vivendi

Bertelsmann

U.S. Europe/Asia/Latin America

kghfhfhf

Bertelsmann AG Presentation

Conclusions & Recommendations

Paulo Oliveira

kghfhfhf

Bertelsmann AG Presentation

What are the key strategic factors shaping the Media & Entertainment Industry?

• Convergence of technologies

• Consolidation of creators, aggregators and distributors

• Governmental regulations

kghfhfhf

Bertelsmann AG Presentation

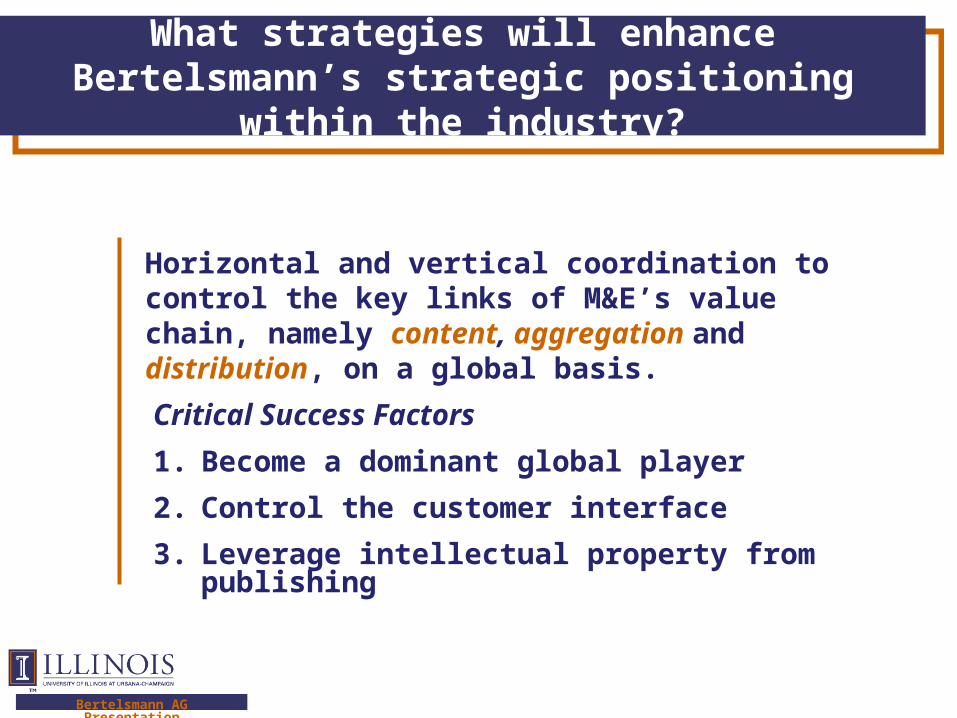

What strategies will enhance Bertelsmann’s strategic positioning within the industry?

Critical Success Factors

1. Become a dominant global player

2. Control the customer interface

3. Leverage intellectual property from publishing

Horizontal and vertical coordination to control the key links of M&E’s value chain, namely content, aggregation and distribution, on a global basis.

kghfhfhf

Bertelsmann AG Presentation

Recommendations

1. Become a dominant global player • Be a catalyst for non-integrated companies• Utilize M&A, Co-opetition, JV’s, strategic alliances

2. Control the customer interface • Expand electronic distribution capability • Explore unique position in the U.S.A.

3. Leverage intellectual property from publishing • Expand into filmed entertainment production• Lead e-book development

kghfhfhf

Bertelsmann AG Presentation

Possible Scenarios: Integrating Complementary Businesses

“Lone stars” in the U.S.A.

• MGM

• NBC

• AT&T Comcast

kghfhfhf

Bertelsmann AG Presentation

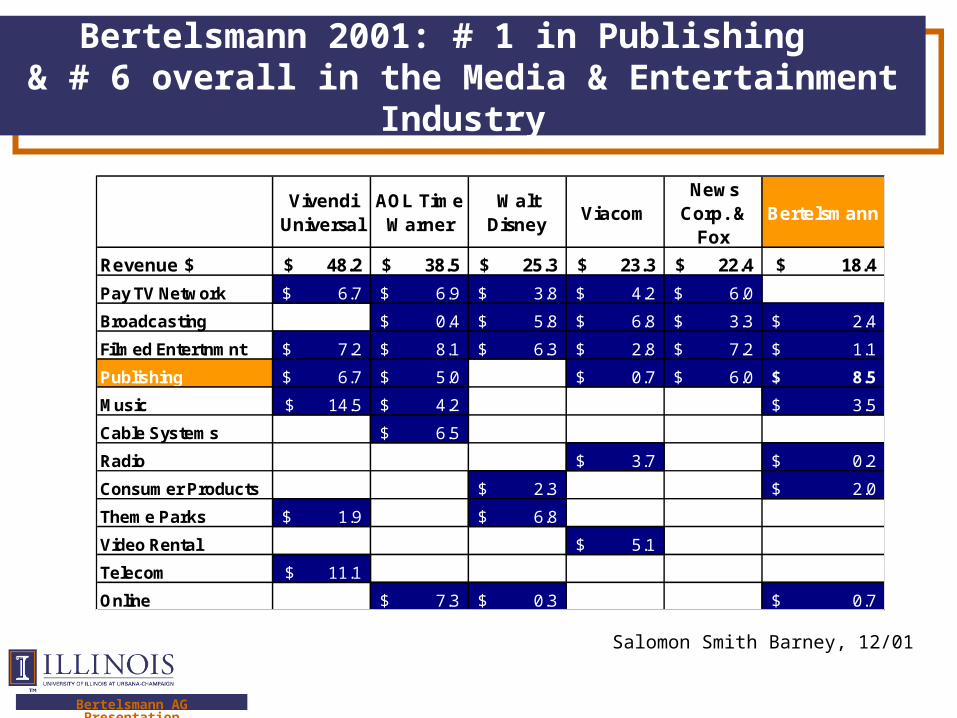

Bertelsmann 2001: # 1 in Publishing & # 6 overall in the Media & Entertainment Industry

Vivendi Universal

AOL Time Warner

Walt Disney

Viacom News

Corp. & Fox

Bertelsmann

Revenue $ 48.2$ 38.5$ 25.3$ 23.3$ 22.4$ 18.4$

Pay TV Network 6.7$ 6.9$ 3.8$ 4.2$ 6.0$

Broadcasting 0.4$ 5.8$ 6.8$ 3.3$ 2.4$

Filmed Entertnmnt 7.2$ 8.1$ 6.3$ 2.8$ 7.2$ 1.1$

Publishing 6.7$ 5.0$ 0.7$ 6.0$ 8.5$

Music 14.5$ 4.2$ 3.5$

Cable Systems 6.5$

Radio 3.7$ 0.2$

Consumer Products 2.3$ 2.0$

Theme Parks 1.9$ 6.8$

Video Rental 5.1$

Telecom 11.1$

Online 7.3$ 0.3$ 0.7$

Salomon Smith Barney, 12/01

kghfhfhf

Bertelsmann AG Presentation

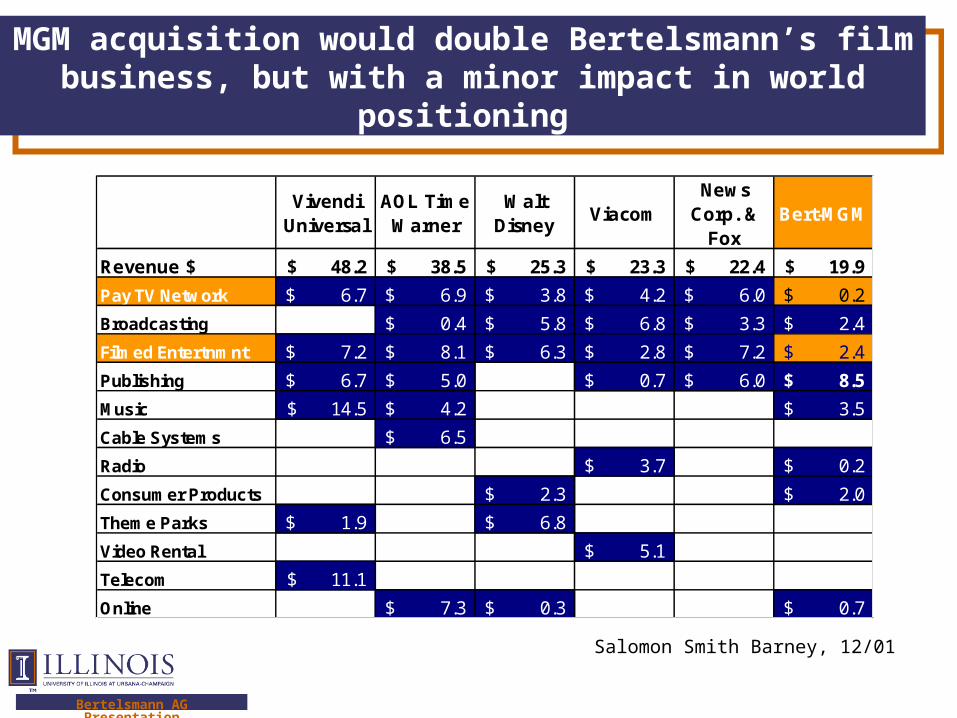

MGM acquisition would double Bertelsmann’s film business, but with a minor impact in world positioning

Vivendi Universal

AOL Time Warner

Walt Disney

Viacom News

Corp. & Fox

Bert-MGM

Revenue $ 48.2$ 38.5$ 25.3$ 23.3$ 22.4$ 19.9$

Pay TV Network 6.7$ 6.9$ 3.8$ 4.2$ 6.0$ 0.2$

Broadcasting 0.4$ 5.8$ 6.8$ 3.3$ 2.4$

Filmed Entertnmnt 7.2$ 8.1$ 6.3$ 2.8$ 7.2$ 2.4$

Publishing 6.7$ 5.0$ 0.7$ 6.0$ 8.5$

Music 14.5$ 4.2$ 3.5$

Cable Systems 6.5$

Radio 3.7$ 0.2$

Consumer Products 2.3$ 2.0$

Theme Parks 1.9$ 6.8$

Video Rental 5.1$

Telecom 11.1$

Online 7.3$ 0.3$ 0.7$

Salomon Smith Barney, 12/01

kghfhfhf

Bertelsmann AG Presentation

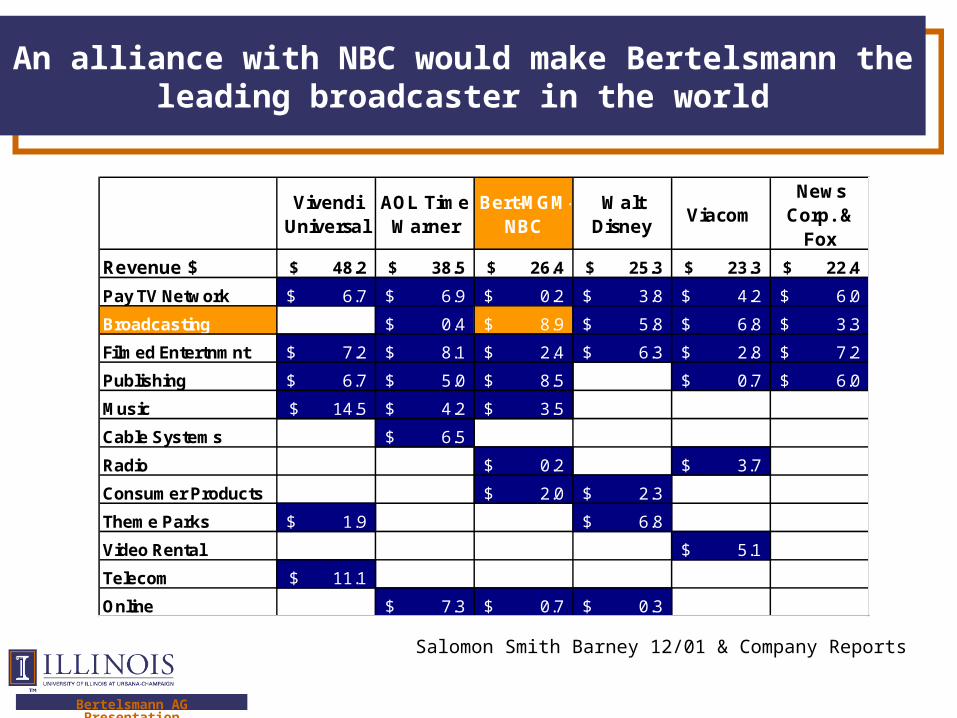

An alliance with NBC would make Bertelsmann the leading broadcaster in the world

Vivendi Universal

AOL Time Warner

Bert-MGM-NBC

Walt Disney

Viacom News

Corp. & Fox

Revenue $ 48.2$ 38.5$ 26.4$ 25.3$ 23.3$ 22.4$

Pay TV Network 6.7$ 6.9$ 0.2$ 3.8$ 4.2$ 6.0$

Broadcasting 0.4$ 8.9$ 5.8$ 6.8$ 3.3$

Filmed Entertnmnt 7.2$ 8.1$ 2.4$ 6.3$ 2.8$ 7.2$

Publishing 6.7$ 5.0$ 8.5$ 0.7$ 6.0$

Music 14.5$ 4.2$ 3.5$

Cable Systems 6.5$

Radio 0.2$ 3.7$

Consumer Products 2.0$ 2.3$

Theme Parks 1.9$ 6.8$

Video Rental 5.1$

Telecom 11.1$

Online 7.3$ 0.7$ 0.3$

Salomon Smith Barney 12/01 & Company Reports

kghfhfhf

Bertelsmann AG Presentation

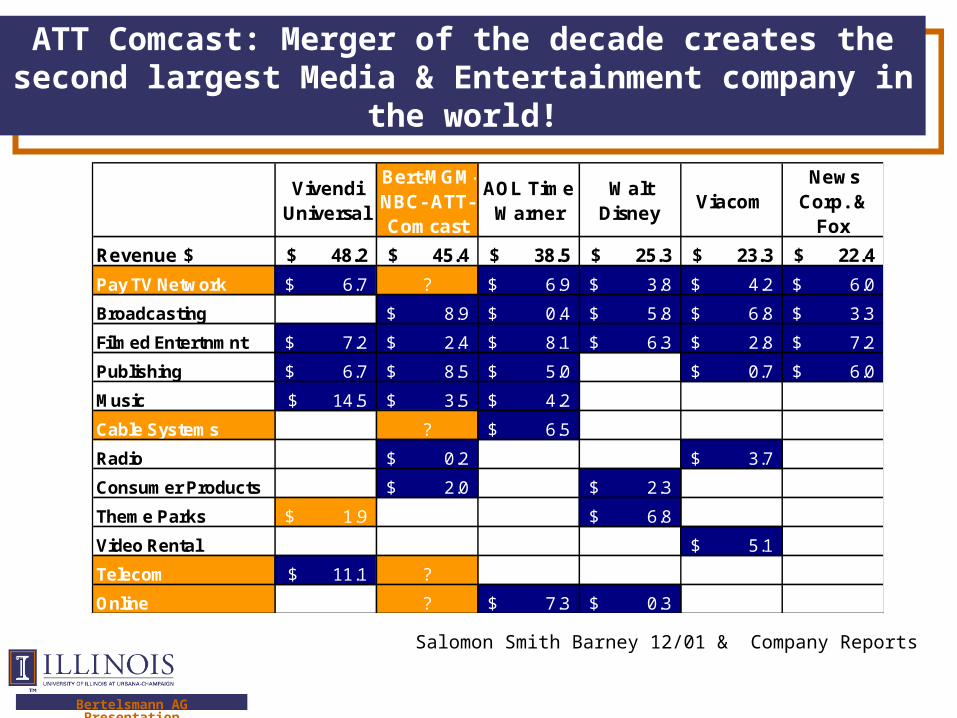

ATT Comcast: Merger of the decade creates the second largest Media & Entertainment company in the world!

Vivendi Universal

Bert-MGM-NBC- ATT-Comcast

AOL Time Warner

Walt Disney

Viacom News

Corp. & Fox

Revenue $ 48.2$ 45.4$ 38.5$ 25.3$ 23.3$ 22.4$

Pay TV Network 6.7$ ? 6.9$ 3.8$ 4.2$ 6.0$

Broadcasting 8.9$ 0.4$ 5.8$ 6.8$ 3.3$

Filmed Entertnmnt 7.2$ 2.4$ 8.1$ 6.3$ 2.8$ 7.2$

Publishing 6.7$ 8.5$ 5.0$ 0.7$ 6.0$

Music 14.5$ 3.5$ 4.2$

Cable Systems ? 6.5$

Radio 0.2$ 3.7$

Consumer Products 2.0$ 2.3$

Theme Parks 1.9$ 6.8$

Video Rental 5.1$

Telecom 11.1$ ?

Online ? 7.3$ 0.3$

Salomon Smith Barney 12/01 & Company Reports

kghfhfhf

Bertelsmann AG Presentation

Thank you!