Embed Size (px)

Citation preview

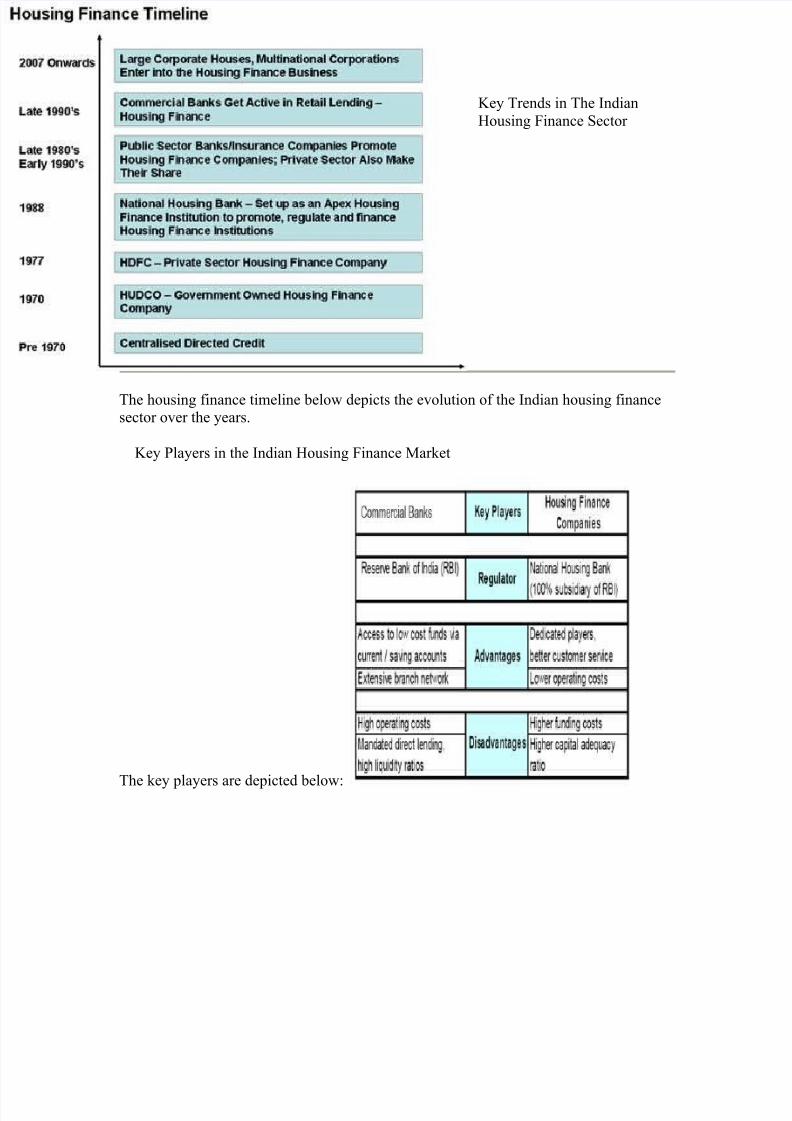

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 1/13

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 2/13

Key Funding Sources The ey funding sources for the Indian housing finance maret

include!• "ans

o Savings and current accounts

o #oan assignment through Inter "an Participation $etificates

o

%efinance from &H"• Housing Finance $ompanies

o $ommercial bans

o "onds and 'ebentures

o International(multilateral funding

o %efinance from &H"

o Term 'eposits )HF$s not allowed to have Term and Savings account*

o #oan assignment

o Mortgage "aced Securitisation

+ther trends in the housing loan maret include!

• Changing Profile of Borrowers: Traditionally, late -s and early /s was theage profile of borrowers for procuring a housing loan, but liberali0ation, risingincomes, and easily accessible and attractive loan options, have propelled the

younger generation, typically in their -s, to borrow for their house purchases.

1ccording to 21 Study of %esidential Housing 'emand in India2, conducted by

the &ational Institute of "an Management )&I"M* in 1pril 34 for &ationalHousing "an )&H"*!

o Though most of the borrowers are in the age group of /56, a significant

367 are below -6 years of age. It is also found that there is a falling trendin the average age profile of the housing finance.

o The demand for house5si0e is found to be inversely related with the age of

the borrowers. 1lso, more the number of dependents in a family, less isthe affordability and hence the si0e of the house.

The changing age profile has resulted in!

o #ong5term #oans! The distinct shift in the age profile of the borrowers

allows Housing Finance $ompanies to structure loans for longer terms.

Till a few years ago, the ma8imum tenure was 9 years. Today, most

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 3/13

lenders offer 35year loans, although the 965year tenure is the most

popular.

o Innovative #oan Products! The changing age profile is spurring the

Housing Finance $ompanies and bans to go beyond the vanilla loan

products and offer more innovative products to attract young people.

:oung borrowers are offered loans in which the ;MI is initiallylow but increases with the years when the borrower<s income

would also rise.

1nother favourite is the loan with a floating rate of interest, whichmeans the ;MI will vary with changes in interest rates.

To mae it easier for borrowers to choose between a fi8ed or

floating rate loan, blended options are being offered wherein thecustomer can hedge part of the interest rate ris by opting for a

combination of fi8ed and floating rates.

#enders are introducing various schemes such as free home

insurance, refinance, etc.

$ross5selling of products and services is rather popular. Thus, a person looing for a housing loan is also offered life insurance,

home protection insurance, and other privileges or baningfacilities.

Method of computation of interest is different for various housing

finance institutions. $orporate loans are offered by financiers to corporate bodies for

the construction or purchase of new residential housing for the use

of their employees anywhere in India. #oans to $orporates for

non5residential premises are also readily available. Some financiers provide loans against rent receivables.

The larger housing finance players offer 'eveloper #oans toapproved developers for the construction of housing pro=ects whichare secured on rent receivables from their tenants. 'eveloper loans

are typically for a term of one to two years. Financiers generally

re>uire security by way of mortgage over the property, including a personal guarantee in respect of the amounts due under the loan.

• Flexible Repayment Options: Most players offer fle8ible repayment options,

catering to the individual<s needs. For instance, there are various repaymentoptions such as!

o Step Up Repayment Facility where the repayment schedule is lined to the

customers< e8pected growth in income and repayment is accelerated proportionately with the assumed increase in income.

o Flexible Loan Installment Plan where an initial higher installment

followed by a lower installment for the balance term.

o PrePayment Facility where repayment is made from a financial

investment, such as an insurance policy or bond, which is assigned as

security for the loan.

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 4/13

• Higher Loan to Value (LV! Ratio: Initially, the bans and HF$s were

e8tending only about ?67 of the value of the house proposed to be purchased."ut with competition among the housing finance lenders becoming very hot in

late nineties, borrowers could raise up to 97 or 997 of the value of property

from lenders. @ith the recent downward trend in property prices as well as the prescription of lower ris weights for housing loans with lower #TA ratio by the

%eserve "an of India and &ational Housing "an, the #TA ratio has fallen to

B7.

• "efault Rate: 1ccording to the $%ISI#, the leading credit rating agency in India,

Indians are least liely to default on a housing loan among all their liabilities. Thelevel of non5performing assets in the housing loan segment was close to /7 in

3?. 1lthough paying rent for a house is far more affordable than the ;MIs,

paying the ;MIs helps to generate an asset, which leads to higher comfort levelsand hence controls housing loan delin>uencies. 1ccording to the findings of 21

Study of %esidential Housing 'emand in India2, conducted by the &ational

Institute of "an Management )&I"M* in 1pril 34 for &ational Housing "an)&H"*!

o "igger the si0e of house )in s>uare meter*, lower is the ris of default.

o Higher the monthly income, lower the chance of default because of higher

ability to pay.

o Creater the value of asset, lesser the ris of default because of greater

affordability due to wealth effect.

o Higher the security margin available to the ban, lower is the chance of

default in housing loan.o 'ecrease in #TA increases the odds of default.

o Increase in ;MI to Income ratio increases the lielihood of default.

o The lielihood of default in housing loan decreases significantly with the

presence of additional collateral. The presence of more number of co5 borrowers reduces the ris of default. Interestingly, higher the co5

borrower<s monthly income, lesser is the chance of default because of

availability of second line of source of income.

o 1s number of dependents increases, probability of default also

significantly rises because of higher financial burden.

o %ural and semi urban people are risier than the urban borrowers.

However, borrowers located in big cities are risier than medium andsmaller cities. This may be because of easy access to finance which maes

borrowers prone to overstretching their financial commitments, and this

conse>uently increases possibility of housing loan default.

o 1n increase in C'P growth rate reduces the lielihood of default.

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 5/13

• ax Benefits: The Covernment of India offers various ta8 incentives to housing

loan borrowers to promote home ownership. 1s per the provisions of the Income

Ta8 1ct, 9DB9, borrowers can claim ta8 benefits on both the principal )underSection 4$* and interest components Eunder Section 3/)b* of the housing loan.

These deductions are available to borrowers who have taen a loan to either buy

or build a house. The principal payment up to %s. +ne lah is eligible for ta8e8emption under Section 4$ of the IT 1ct. Further, Section 3/ of the Income

Ta8 1ct, pertaining to income from house property, allows individuals an interest

deduction of up to %s 96, on housing loans. These ta8 benefits haveconsiderably reduced the effective rate of interest on a loan, to the e8tent that it is

beneficial to borrow from a ban or an HF$ rather than use one<s own funds.

)%ead @hat ta8 benefits can you avail on a home loanG)To be lined to the phase9 article**

Sources

http!((www.ficci.com

$%ISI# %eports

http!((www.hdfc.com(pdf(H'F$5IHF/.pdf

http!((www.ta8guru.in(income5ta8(all5about5deduction5under5section54c5and5ta85

planning.html

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 6/13

$omparative Study of "ans 1nd HF$S

The housing finance sector witnessed an enormous growth since the early 9DDs. Totalhome loan disbursements by bans and housing finance companies rose considerably.

"ans, despite being late entrants in the field of Housing Finance have taen overHousing Finance $ompanies in the home loan maret.

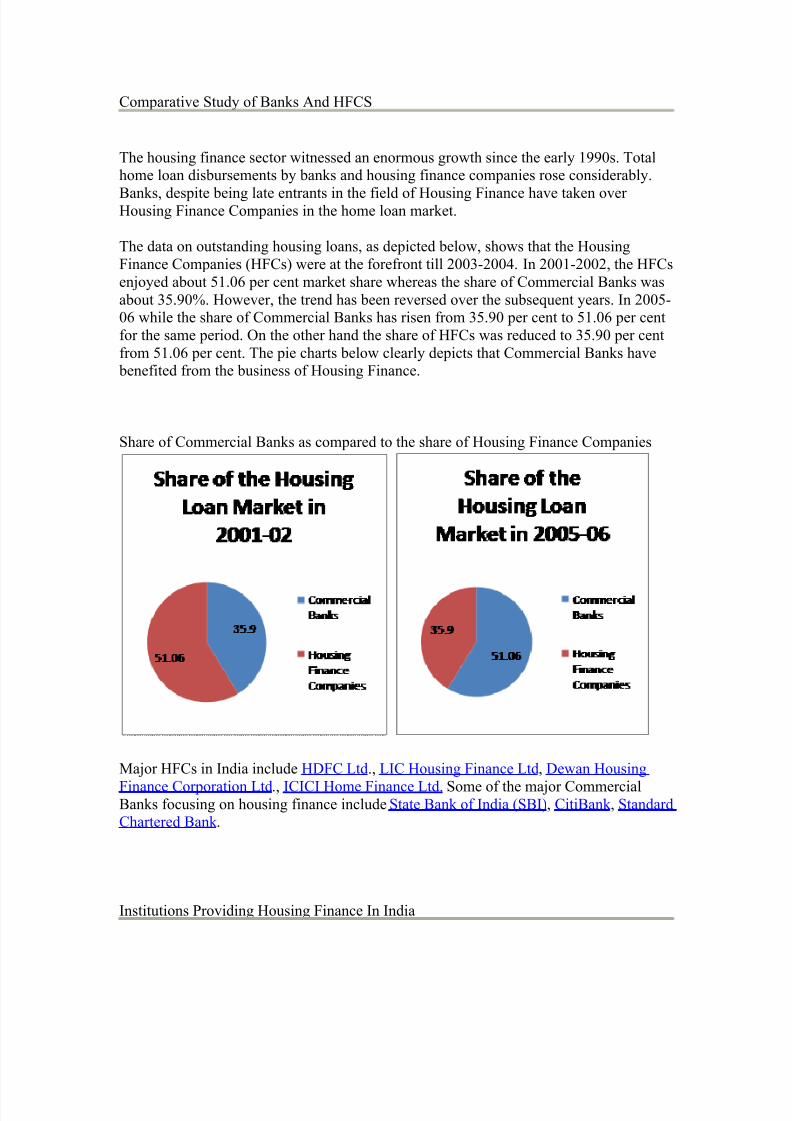

The data on outstanding housing loans, as depicted below, shows that the Housing

Finance $ompanies )HF$s* were at the forefront till 3-53/. In 39533, the HF$s

en=oyed about 69.B per cent maret share whereas the share of $ommercial "ans was

about -6.D7. However, the trend has been reversed over the subse>uent years. In 365B while the share of $ommercial "ans has risen from -6.D per cent to 69.B per cent

for the same period. +n the other hand the share of HF$s was reduced to -6.D per cent

from 69.B per cent. The pie charts below clearly depicts that $ommercial "ans have benefited from the business of Housing Finance.

Share of $ommercial "ans as compared to the share of Housing Finance $ompanies

Ma=or HF$s in India include H'F$ #td., #I$ Housing Finance #td, 'ewan Housing

Finance $orporation #td., I$I$I Home Finance #td. Some of the ma=or $ommercial"ans focusing on housing finance include State "an of India )S"I*, $iti"an , Standard$hartered "an .

Institutions Providing Housing Finance In India

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 7/13

"efore the advent of $ommercial "ans that e8tended Home #oans, borrowers depended

on local lenders, family and friends to undertae house buying decisions.

The Housing Finance providers in India can be divided into two categories!• Formal Mechanism

• Informal Mechanism

Formal Mechanism

The setting up of Housing and rban 'evelopment $orporation #td. )H'$+* in 9D?

for providing Housing #oans to #ow Income Croups, and to finance urban infrastructureactivities furthered the cause of Formal Housing Finance in India. Housing 'evelopment

Finance $orporation #td. )H'F$* in 9D?? was Indias first private sector enterprise set

up to provide financial assistance to individuals, groups, cooperative societies and

companies for staff housing.

The main Institutions providing formal long5term Housing Finance in India include!

• Commer#ial Ban$s: +ver years the share of $ommercial "ans in the home loan

maret has overtaen that of Housing Finance $ompanies )HF$s* who are facingsevere competition from the former in view of their competitive rates and reach.

Today, the $ommercial "ans in India are also re>uired by %"I to earmar a

minimum of -7 of their incremental deposits for e8tending housing loans.

• %tate Cooperati&e Ban$s an' Regional Rural Ban$s: These "ans are

State(%egional5level credit institutions. @hile these "ans are allowed to provide

Housing Finance, they have not been very active in the field.

•

gri#ultural an' Rural "e&elopment Ban$s (R"Bs!: They are term lendinginstitutions operating e8clusively in the rural sector. 1t present there are various

1%'"s in India operating through their own branches or through branches of

primary $ooperative 1griculture and %ural 'evelopment "ans.

• Housing Finan#e Companies: They are &on "aning Financial $ompanies,

whose principal ob=ect is to provide Housing Finance.

• Cooperati&e Housing Finan#e %o#ieties: They have a two5tier structure

comprising 1pe8 $ooperative Housing Finance societies at the State level and thePrimary $ooperative Housing Finance societies at the retail level.

• )i#rofinan#e *nstitutions ()F*s!: There are a number of MFIs in India such as

S;@1. 'H1&, and SH1%;, providing finance for housing to low income group

of their members.

&ational Housing "an

1lthough &H" does not e8tend Housing Finance directly, it plays a very significant role

in the development of Housing Finance maret by e8tending financial support to the

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 8/13

primary lending institutions. The refinance products of &H" are for different maturities

and they are also e8tended on fi8ed or floating rate basis, depending on the re>uirements

of Primary #ending Institutions. &H" has also formulated schemes to support most of theHousing Finance providers catering to the ;@S(%ural Segments at concessional terms so

as to cater to the housing needs of the society at large.

Please visit http!((www.nhb.org.in(Financial(&ewJSchemes.PHP for the role of &H" andthe products offered by them to Housing Finance providers.

1lso %ead! http!((www.rbi.org.in(scripts(banlins.asp8 Informal Mechanism

The Informal Financial sources generally include funds available from family sources or

local money lenders. The local money lenders charge e8orbitant interest rates, generally

ranging from -B7 to B7, due to their monopoly in the absence of any other source ofcredit.

However, recogni0ing the need of many in the Informal Financial Sector, several

organi0ations provide assistance through fle8ible repayment schemes, lower rates ofinterest, etc. The e8perience of these informal intermediaries shows that although the

savings of group members are small in nature and do not attract high returns, it is still a preferred choice due to security reasons and for availing loans at lower rates compared to

those available from money lenders.

%ead Housing Finance $lassification

1lso %ead! #ist of "ans and HF$s India

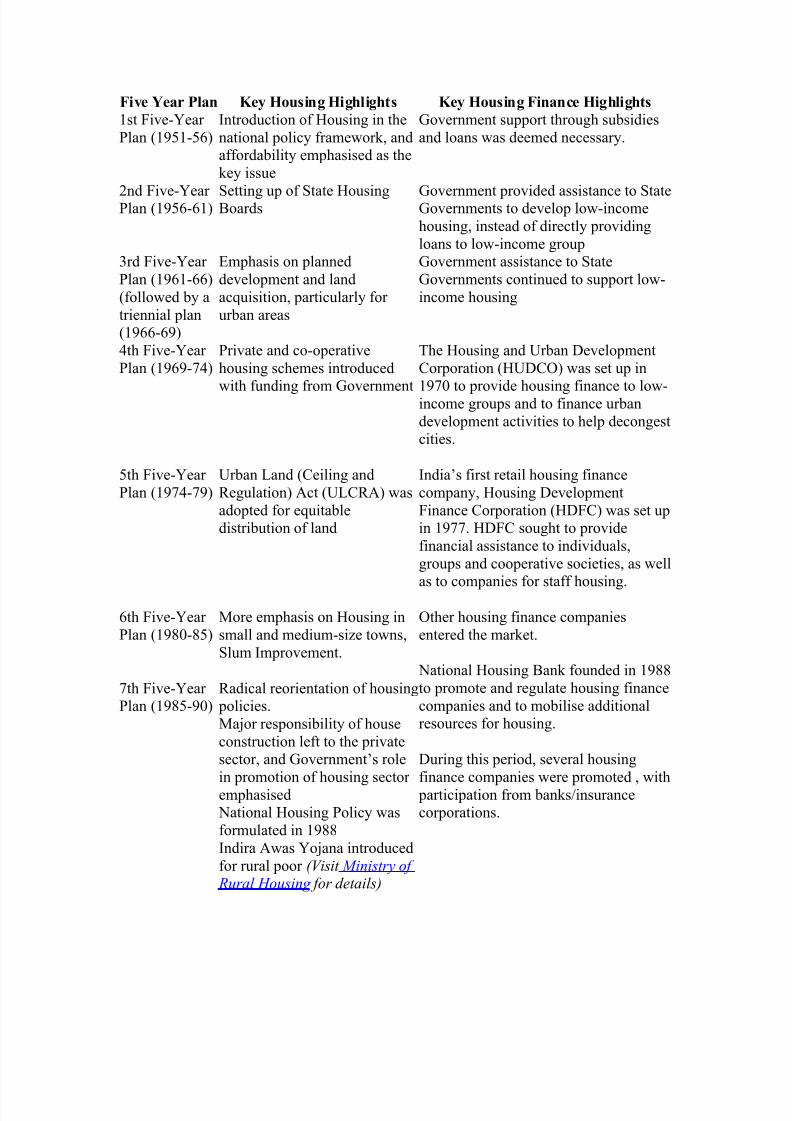

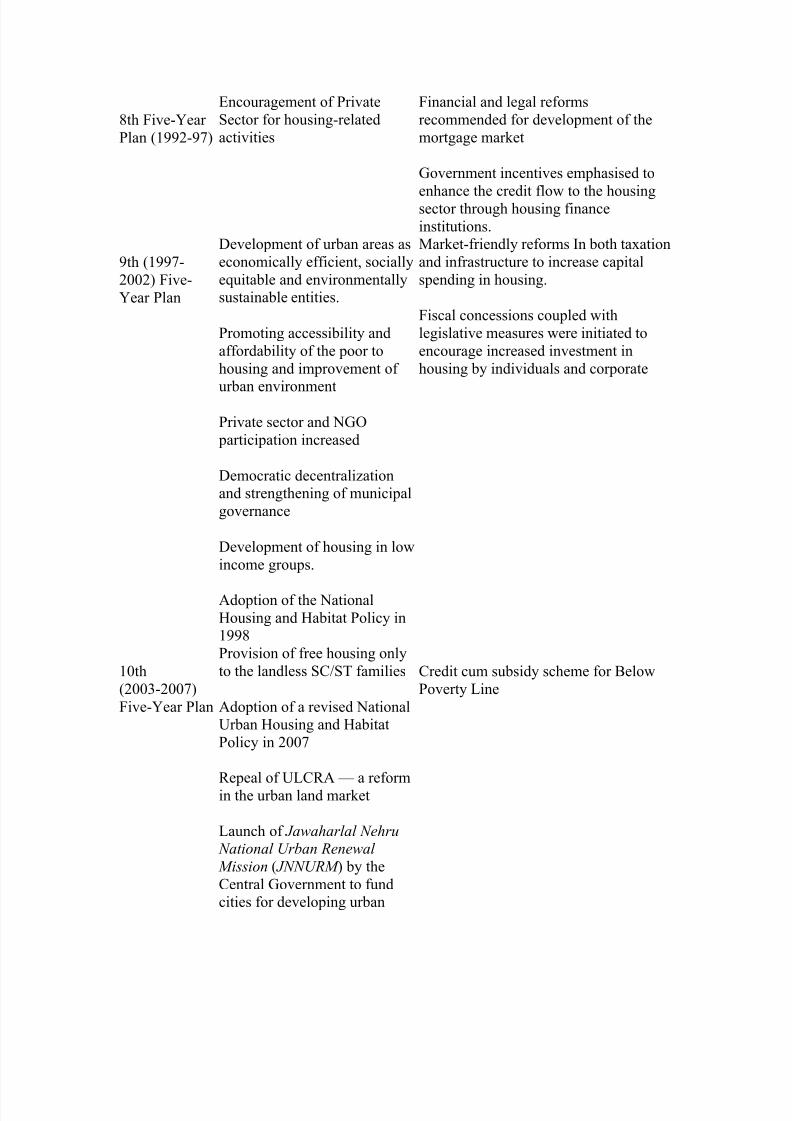

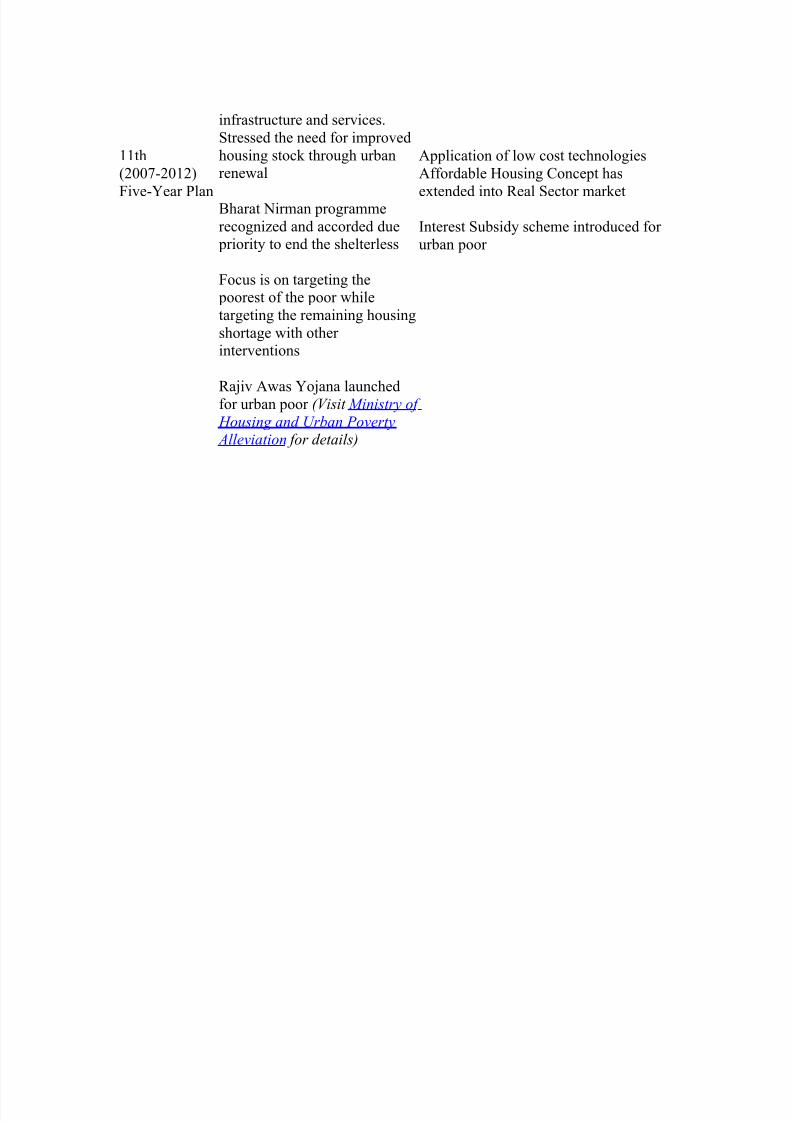

Crowth of Housing Finance Through The Five :ear Plans

Housing and housing finance have grown hand in hand in India. The table below tracesthe evolution of both sectors through the five year plans.

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 9/13

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 10/13

4th Five5:ear

Plan )9DD35D?*

;ncouragement of Private

Sector for housing5related

activities

Financial and legal reforms

recommended for development of the

mortgage maret

Covernment incentives emphasised to

enhance the credit flow to the housingsector through housing finance

institutions.

Dth )9DD?5

33* Five5

:ear Plan

'evelopment of urban areas as

economically efficient, socially

e>uitable and environmentallysustainable entities.

Promoting accessibility and

affordability of the poor to

housing and improvement of

urban environment

Private sector and &C+

participation increased

'emocratic decentrali0ationand strengthening of municipal

governance

'evelopment of housing in low

income groups.

1doption of the &ational

Housing and Habitat Policy in9DD4

Maret5friendly reforms In both ta8ation

and infrastructure to increase capital

spending in housing.

Fiscal concessions coupled with

legislative measures were initiated to

encourage increased investment in

housing by individuals and corporate

9th

)3-53?*

Five5:ear Plan

Provision of free housing only

to the landless S$(ST families

1doption of a revised &ationalrban Housing and Habitat

Policy in 3?

%epeal of #$%1 a reformin the urban land maret

#aunch of !a"a#arlal $e#ru $ational Urban Rene"al

Mission ) !$$URM * by the

$entral Covernment to fundcities for developing urban

$redit cum subsidy scheme for "elow

Poverty #ine

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 11/13

infrastructure and services.

99th

)3?5393*

Five5:ear Plan

Stressed the need for improved

housing stoc through urbanrenewal

"harat &irman programme

recogni0ed and accorded due priority to end the shelterless

Focus is on targeting the poorest of the poor while

targeting the remaining housing

shortage with otherinterventions

%a=iv 1was :o=ana launchedfor urban poor (Visit Ministry of

Housing and Urban Po%erty &lle%iation for details

1pplication of low cost technologies

1ffordable Housing $oncept has

e8tended into %eal Sector maret

Interest Subsidy scheme introduced for

urban poor

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 12/13

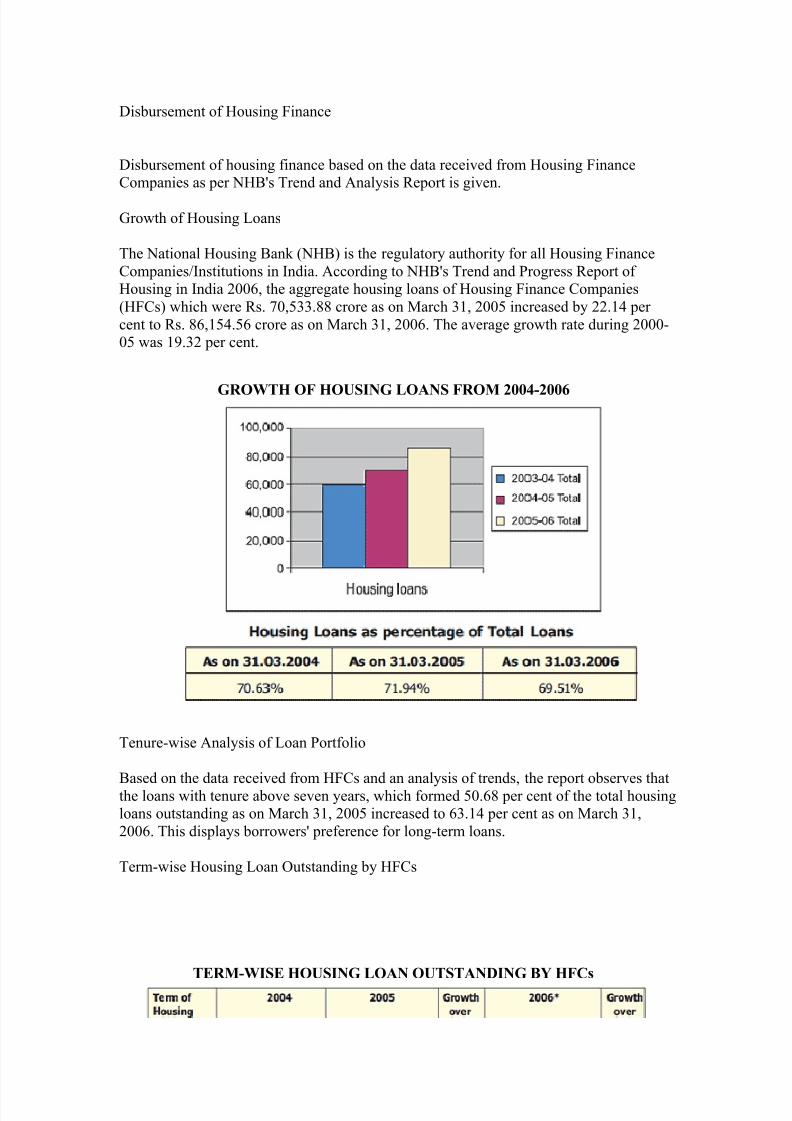

'isbursement of Housing Finance

'isbursement of housing finance based on the data received from Housing Finance$ompanies as per &H"<s Trend and 1nalysis %eport is given.

Crowth of Housing #oans

The &ational Housing "an )&H"* is the regulatory authority for all Housing Finance

$ompanies(Institutions in India. 1ccording to &H"<s Trend and Progress %eport ofHousing in India 3B, the aggregate housing loans of Housing Finance $ompanies

)HF$s* which were %s. ?,6--.44 crore as on March -9, 36 increased by 33.9/ per

cent to %s. 4B,96/.6B crore as on March -9, 3B. The average growth rate during 356 was 9D.-3 per cent.

-RO.H OF HO/%*0- LO0% FRO) 122341225

Tenure5wise 1nalysis of #oan Portfolio

"ased on the data received from HF$s and an analysis of trends, the report observes thatthe loans with tenure above seven years, which formed 6.B4 per cent of the total housingloans outstanding as on March -9, 36 increased to B-.9/ per cent as on March -9,

3B. This displays borrowers< preference for long5term loans.

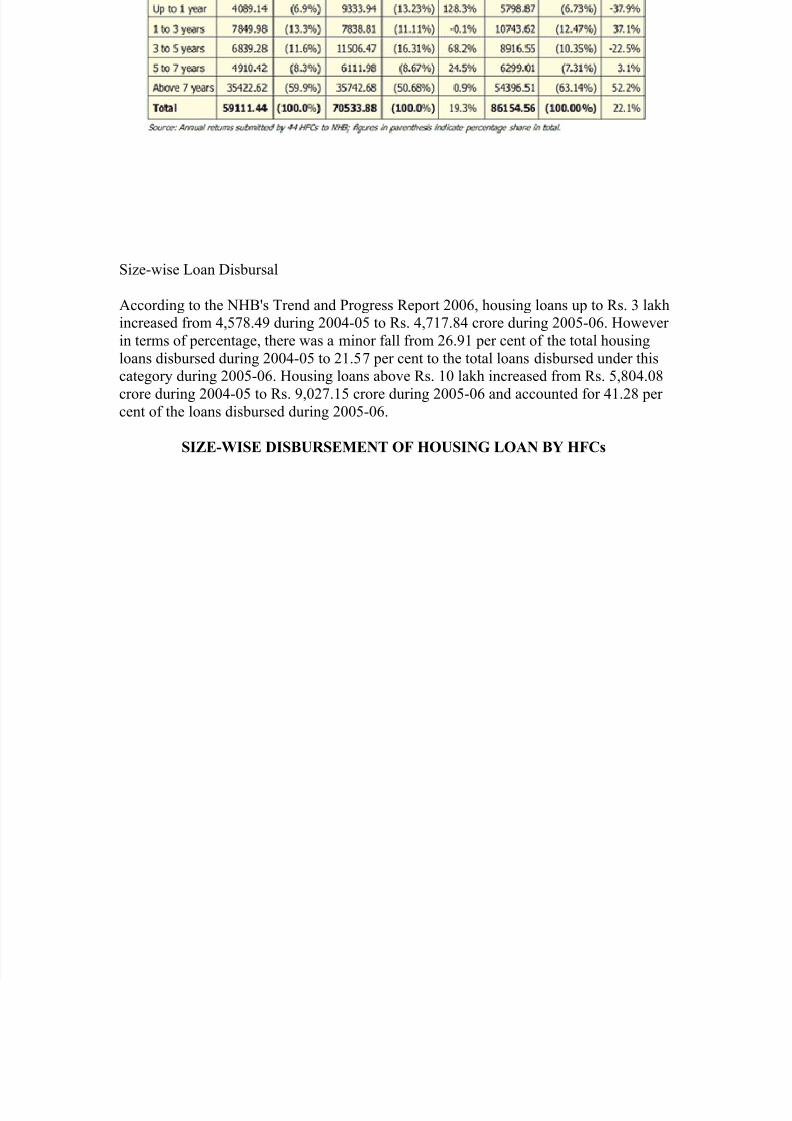

Term5wise Housing #oan +utstanding by HF$s

6R)4.*%6 HO/%*0- LO0 O/%0"*0- B+ HFCs

8/12/2019 Key Trends in the Indian Housing Finance Sector Important

http://slidepdf.com/reader/full/key-trends-in-the-indian-housing-finance-sector-important 13/13

Si0e5wise #oan 'isbursal

1ccording to the &H"<s Trend and Progress %eport 3B, housing loans up to %s. - lahincreased from /,6?4./D during 3/56 to %s. /,?9?.4/ crore during 365B. However

in terms of percentage, there was a minor fall from 3B.D9 per cent of the total housing

loans disbursed during 3/56 to 39.6? per cent to the total loans disbursed under thiscategory during 365B. Housing loans above %s. 9 lah increased from %s. 6,4/.4

crore during 3/56 to %s. D,3?.96 crore during 365B and accounted for /9.34 percent of the loans disbursed during 365B.

%*764.*%6 "*%B/R%6)60 OF HO/%*0- LO0 B+ HFCs