Embed Size (px)

Citation preview

Kentucky Horticulture OutlookKentucky Horticulture OutlookFall 2003Fall 2003

Tim Woods and Matt ErnstTim Woods and Matt Ernst

Agricultural Economics

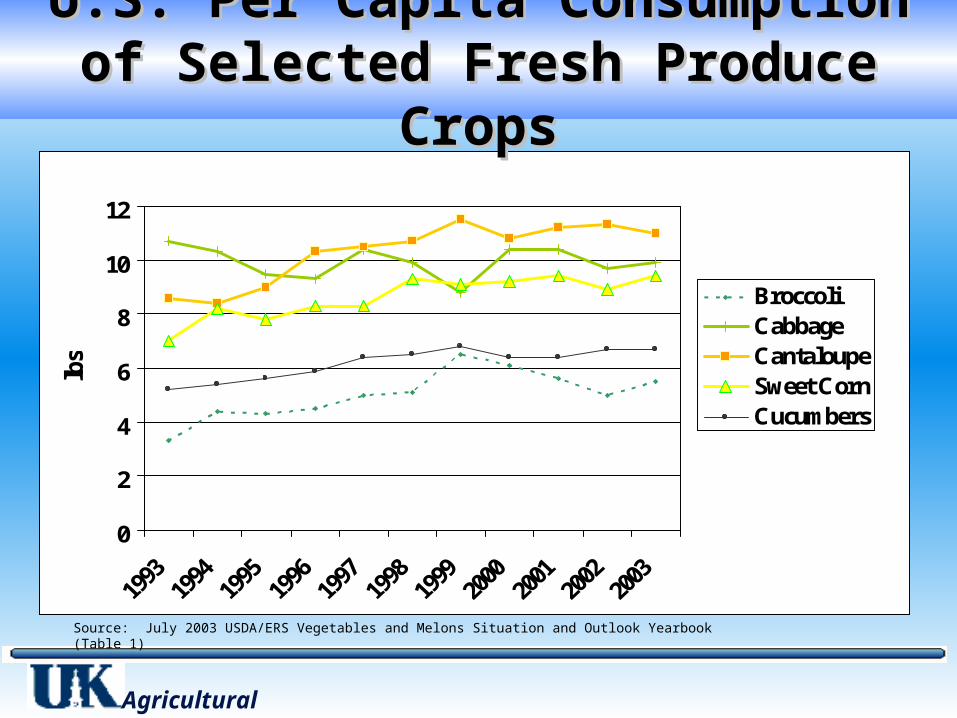

U.S. Per Capita Consumption of Selected U.S. Per Capita Consumption of Selected Fresh Produce CropsFresh Produce Crops

0

2

4

6

8

10

12

lbs

BroccoliCabbageCantaloupeSweet CornCucumbers

Agricultural Economics

Source: July 2003 USDA/ERS Vegetables and Melons Situation and Outlook Yearbook (Table 1)

7 94

74

26 26

0

10

20

30

40

50

60

70

80

Per

cen

t

Percent selling at least 10% of theirproduce into given market channel

Source: 2001-03 KY Produce Marketing Practices Surveys

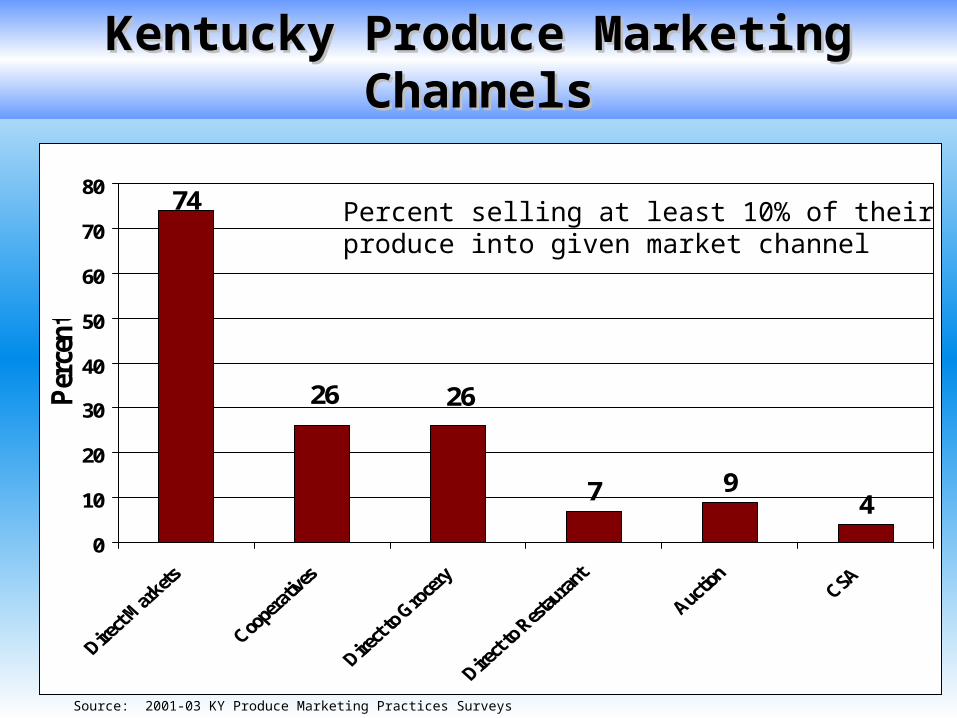

Kentucky Produce Marketing ChannelsKentucky Produce Marketing Channels

• Co-ops generally saw strong prices• Modest growth in acreage• Continued AD Fund support to develop

infrastructure and carry working capital• Management and board challenges• More demonstration programs from UK

– Additional $2 million appropriated for on-farm demos, variety development, applied research

KY Cooperative and Wholesale MarketsKY Cooperative and Wholesale Markets

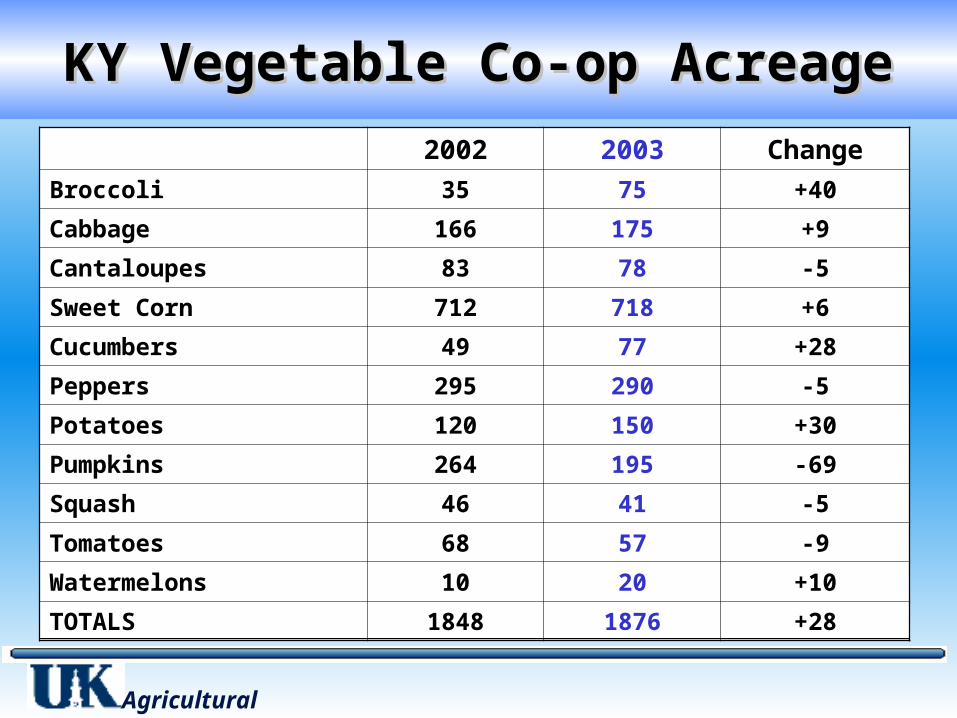

KY Vegetable Co-op AcreageKY Vegetable Co-op Acreage

Agricultural Economics

2002 2003 Change

Broccoli 35 75 +40

Cabbage 166 175 +9

Cantaloupes 83 78 -5

Sweet Corn 712 718 +6

Cucumbers 49 77 +28

Peppers 295 290 -5

Potatoes 120 150 +30

Pumpkins 264 195 -69

Squash 46 41 -5

Tomatoes 68 57 -9

Watermelons 10 20 +10

TOTALS 1848 1876 +28

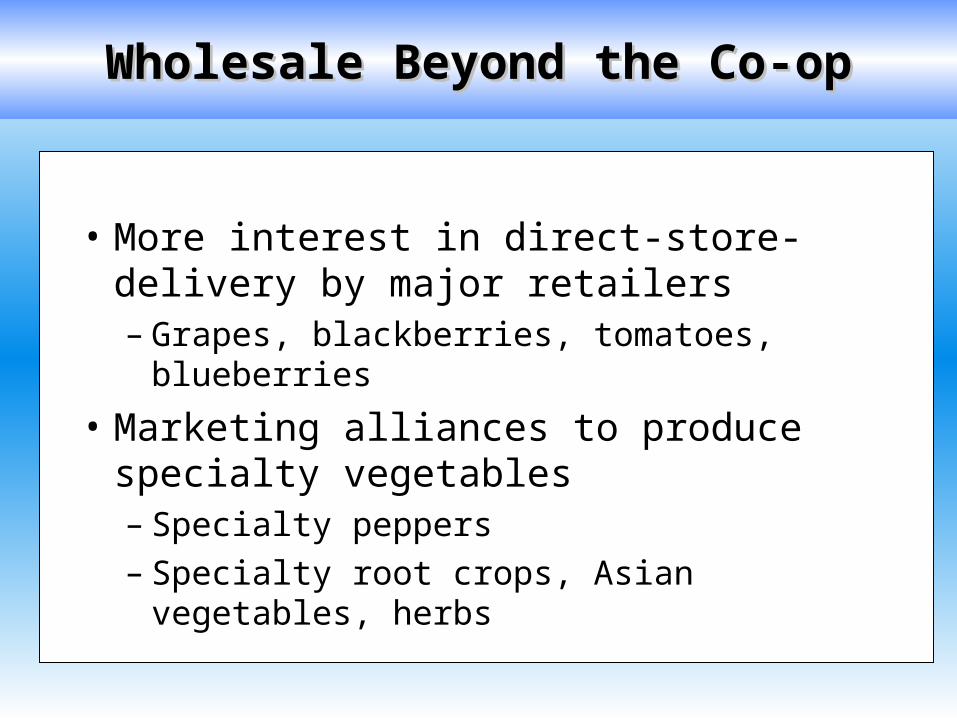

• More interest in direct-store-delivery by major retailers– Grapes, blackberries, tomatoes, blueberries

• Marketing alliances to produce specialty vegetables– Specialty peppers– Specialty root crops, Asian vegetables, herbs

Wholesale Beyond the Co-opWholesale Beyond the Co-op

Fruits and Vegetables: Fruits and Vegetables: Kentucky Gross Farm Sales, 1987-2003Kentucky Gross Farm Sales, 1987-2003

• Co-op sales for 2003: $5-6 million

• 60 Farm Bureau CRMs @ $100,000: Another $6 million

• 80+ community farmers markets gross sales @$50,000: Another $4 million

• Auctions, niche processed products (grapes), wholesale not through co-ops, other direct sales: Another $5-10 million

• Major growth since 1997

0

24

6

8

1012

14

1982 1987 1992 1997 2002 2003M

illio

n $

Produce Sales

Agricultural Economics

Source: USDA/ERS, NASS Ag Census

? ?

U.S. Per Capita Consumption of Selected U.S. Per Capita Consumption of Selected Fresh Produce CropsFresh Produce Crops

02

46

810

1214

1618

20

lbs Tomatoes

Bell Peppers

Agricultural Economics

Source: July 2003 USDA/ERS Vegetables and Melons Situation and Outlook Yearbook (Table 1)

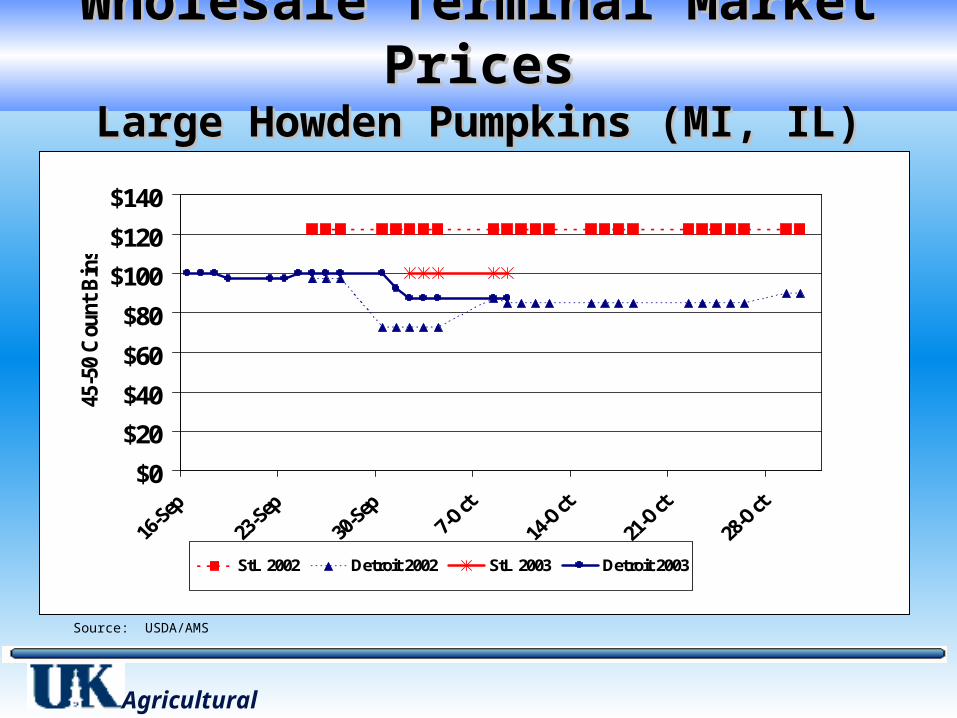

Wholesale Terminal Market PricesWholesale Terminal Market PricesLarge Howden Pumpkins (MI, IL)Large Howden Pumpkins (MI, IL)

Agricultural Economics

$0

$20

$40

$60

$80

$100

$120

$140

45-5

0 C

ount

Bin

s

StL 2002 Detroit 2002 StL 2003 Detroit 2003

Source: USDA/AMS

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

J une J uly August SeasonAverage

$/cw

t

20031997-2002

Source: USDA/ERS, UK Estimates

U.S. Sweet Corn Shipping Point Prices 1997-2002 and 2003

$0$5

$10$15$20$25$30$35$40$45$50

J une J uly August SeasonAverage

$/cw

t 20031997-2002

Source: USDA/ERS, UK Estimates

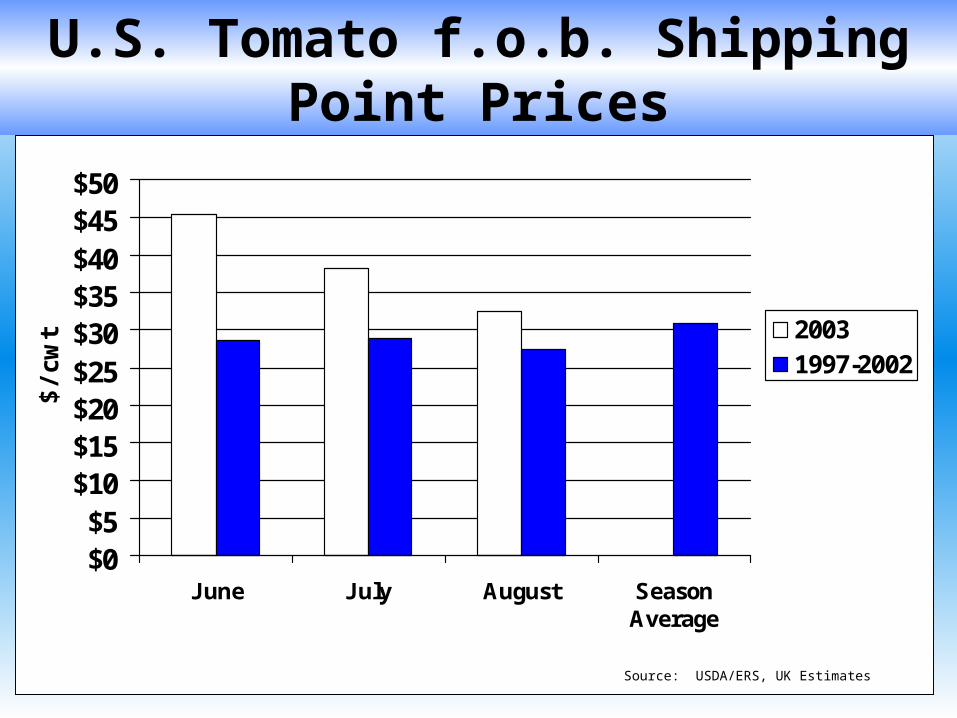

U.S. Tomato f.o.b. Shipping Point Prices

Source: USDA/ERS

Tomato Imports Continue to Grow

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

Other

Netherlands

Mexico

Canada

Million $

U.S. Tomato Imports

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

Pri

ce/cw

t

1997 1998 1999 2000 2001 2002 2003

Avg. Farm PriceSource: USDA/ERS, UK Estimates

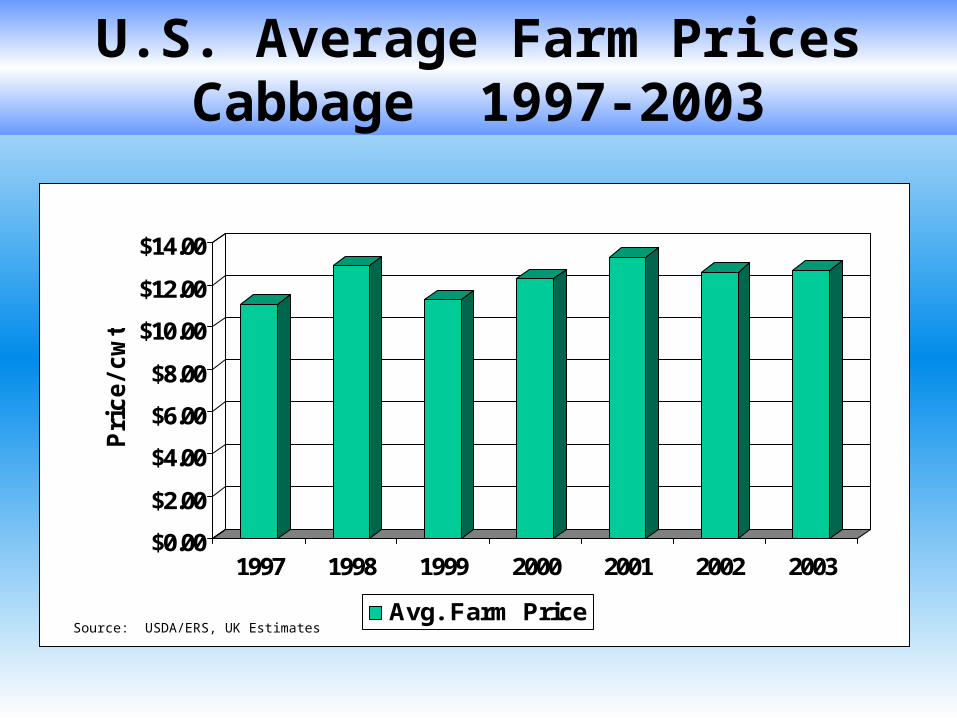

U.S. Average Farm PricesCabbage 1997-2003

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

Pri

ce/cw

t

1997 1998 1999 2000 2001 2002 2003

Avg. Farm PriceSource: USDA/ERS, UK Estimates

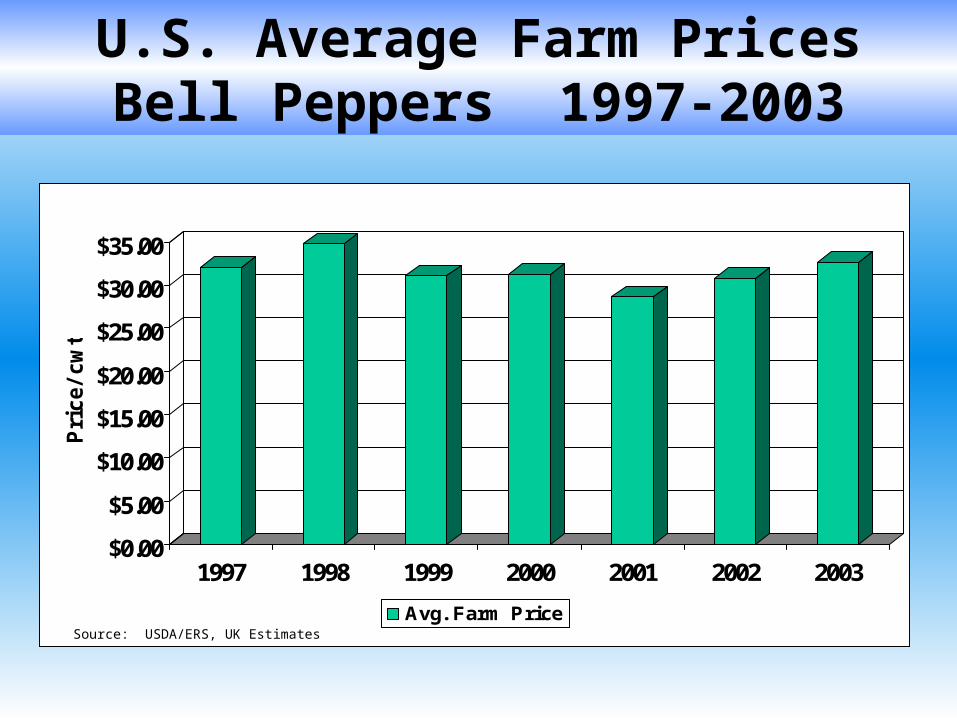

U.S. Average Farm PricesBell Peppers 1997-2003

• Green River Produce Cooperative– Strong marketing alliance

– Market entry with big players

– Outstanding quality (Castellini’s)

• Typical large annual price swings• Net per acre per year has ranged from break-even to

$2,000+

Challenges in the KY Cantaloupe Deal

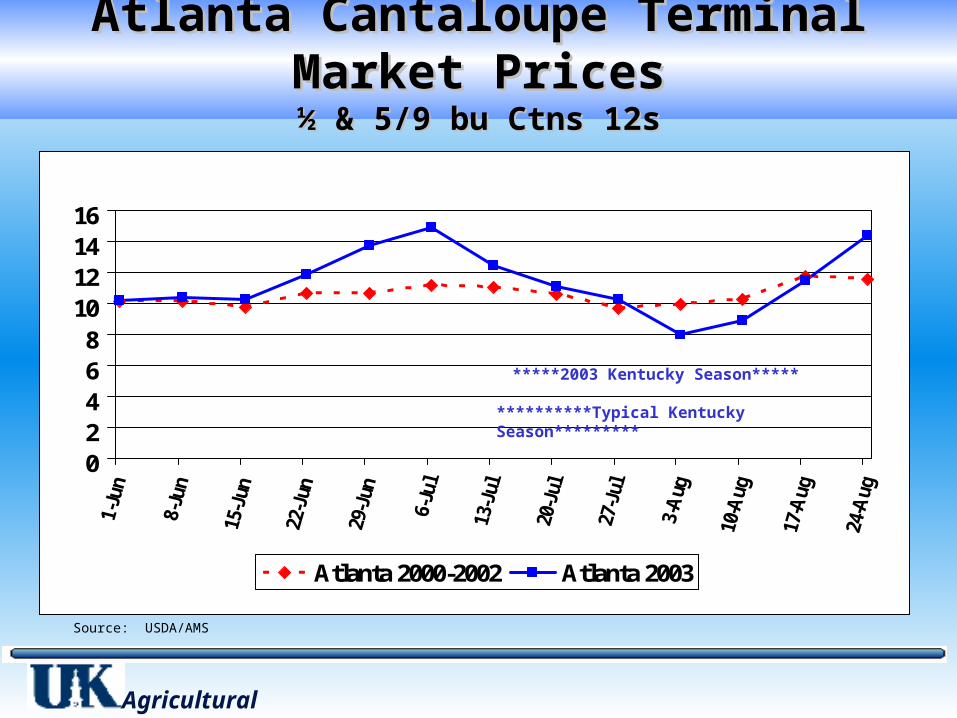

Atlanta Cantaloupe Terminal Market PricesAtlanta Cantaloupe Terminal Market Prices½ & 5/9 bu Ctns 12s½ & 5/9 bu Ctns 12s

Agricultural Economics

Source: USDA/AMS

02468

10121416

Atlanta 2000-2002 Atlanta 2003

**********Typical Kentucky Season*********

*****2003 Kentucky Season*****

Detroit Cantaloupe Terminal Market PricesDetroit Cantaloupe Terminal Market Prices½ & 5/9 bu Ctns 12s½ & 5/9 bu Ctns 12s

Agricultural Economics

Source: USDA/AMS

02468

10121416

Detroit 2000-2002 Detroit 2003

*****2003 Kentucky Season*****

**********Typical Kentucky Season*********

St. Louis Cantaloupe Terminal Market PricesSt. Louis Cantaloupe Terminal Market Prices½ & 5/9 bu Ctns 12s½ & 5/9 bu Ctns 12s

Agricultural Economics

Source: USDA/AMS

02468

1012141618

StL 2000-2002 St. Louis 2003

*****2003 Kentucky Season*****

**********Typical Kentucky Season*********

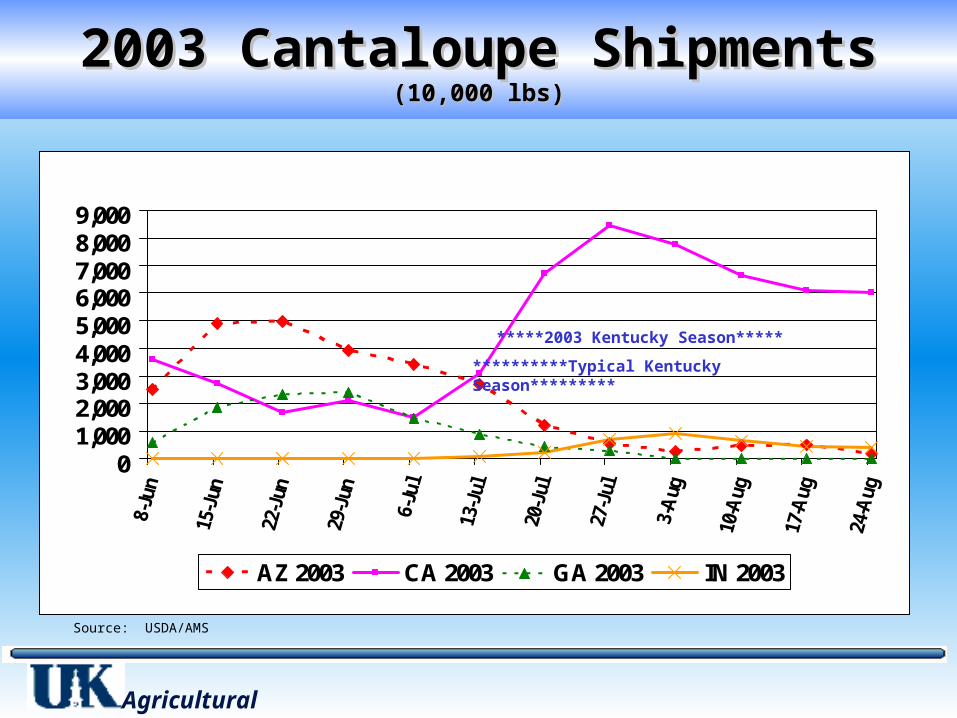

2003 Cantaloupe Shipments2003 Cantaloupe Shipments(10,000 lbs)(10,000 lbs)

Agricultural Economics

Source: USDA/AMS

01,0002,0003,0004,0005,0006,0007,0008,0009,000

AZ 2003 CA 2003 GA 2003 IN 2003

*****2003 Kentucky Season*****

**********Typical Kentucky Season*********

• 400 commercial berry acres—Highest since 1980s

• Outstanding small fruit quality, season length & yields

• Small fruit seasons 7-10 days behind throughout East/SE

• Apple yields at 5-yr high• Excellent tree fruit quality• Strong demand for fresh market

peaches, pears, Asian pears

2003 KY Fruit Season2003 KY Fruit Season

0

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

700,000,000

1987 1992 1997 2002*

Bearing Vines

Nonbearing Vines

Sources: 1987-97: US Ag Census; *2002: USDA/ERS; wineinstitute.org; CA Dept. of Food and Agriculture

2002 estimate includes 1,179,545 acres

U.S. Grape Vines 1987-2002U.S. Grape Vines 1987-2002

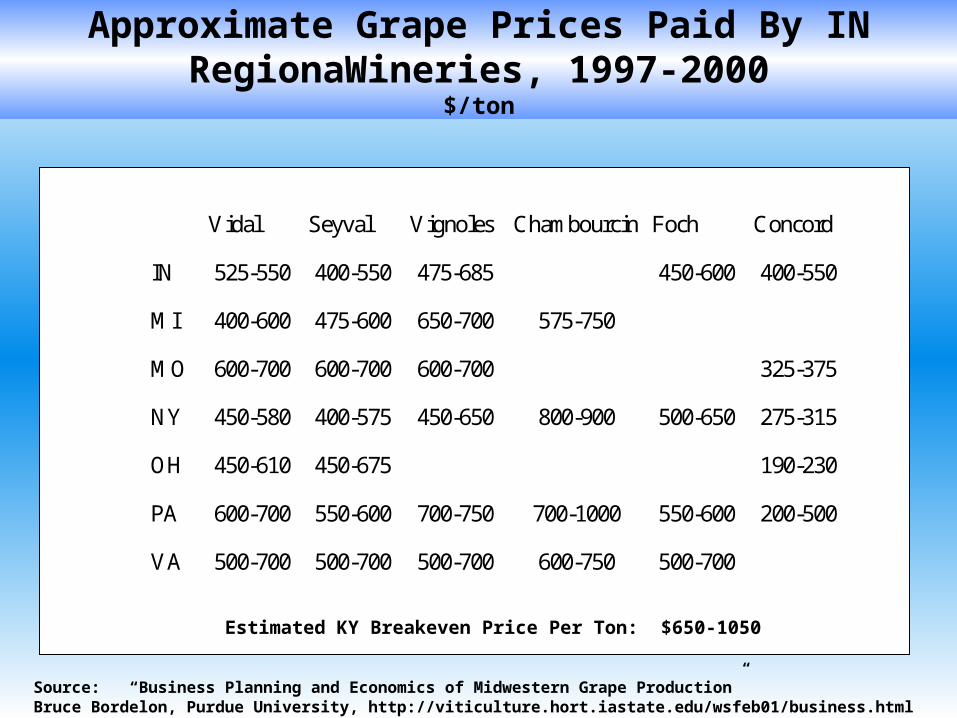

Vidal Seyval Vignoles Chambourcin Foch Concord

IN 525-550 400-550 475-685 450-600 400-550

MI 400-600 475-600 650-700 575-750

MO 600-700 600-700 600-700 325-375

NY 450-580 400-575 450-650 800-900 500-650 275-315

OH 450-610 450-675 190-230

PA 600-700 550-600 700-750 700-1000 550-600 200-500

VA 500-700 500-700 500-700 600-750 500-700

Estimated KY Breakeven Price Per Ton: $650-1050

Source: “Business Planning and Economics of Midwestern Grape Production”Bruce Bordelon, Purdue University, http://viticulture.hort.iastate.edu/wsfeb01/business.html

Approximate Grape Prices Paid By IN RegionaWineries, 1997-2000

$/ton

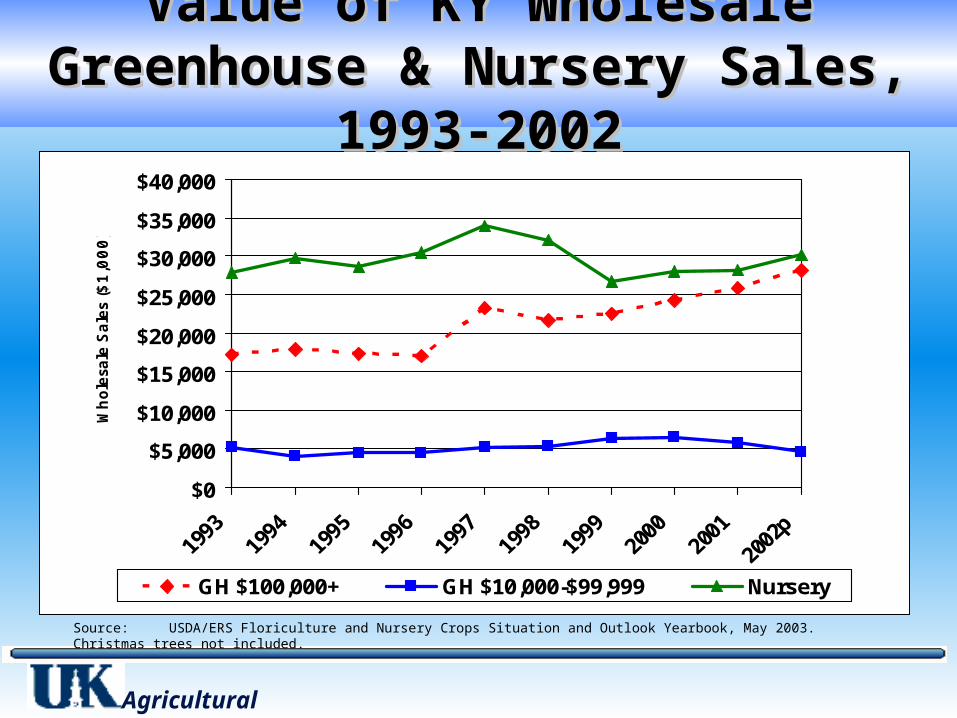

Value of KY Wholesale Greenhouse & Value of KY Wholesale Greenhouse & Nursery Sales, 1993-2002Nursery Sales, 1993-2002

Agricultural Economics

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

Whole

sale

Sale

s ($

1,0

00)

GH $100,000+ GH $10,000-$99,999 Nursery

Source: USDA/ERS Floriculture and Nursery Crops Situation and Outlook Yearbook, May 2003. Christmas trees not included.

![[Ernst Kurth] Ernst Kurth Selected Writings (Camb(BookFi.org)](https://img.pdfslide.us/doc/110x75/55cf92c2550346f57b99475f/ernst-kurth-ernst-kurth-selected-writings-cambbookfiorg.jpg)