Embed Size (px)

Citation preview

Kensington and Chelsea Retail and Leisure Needs Study Update Royal Borough of Kensington & Chelsea

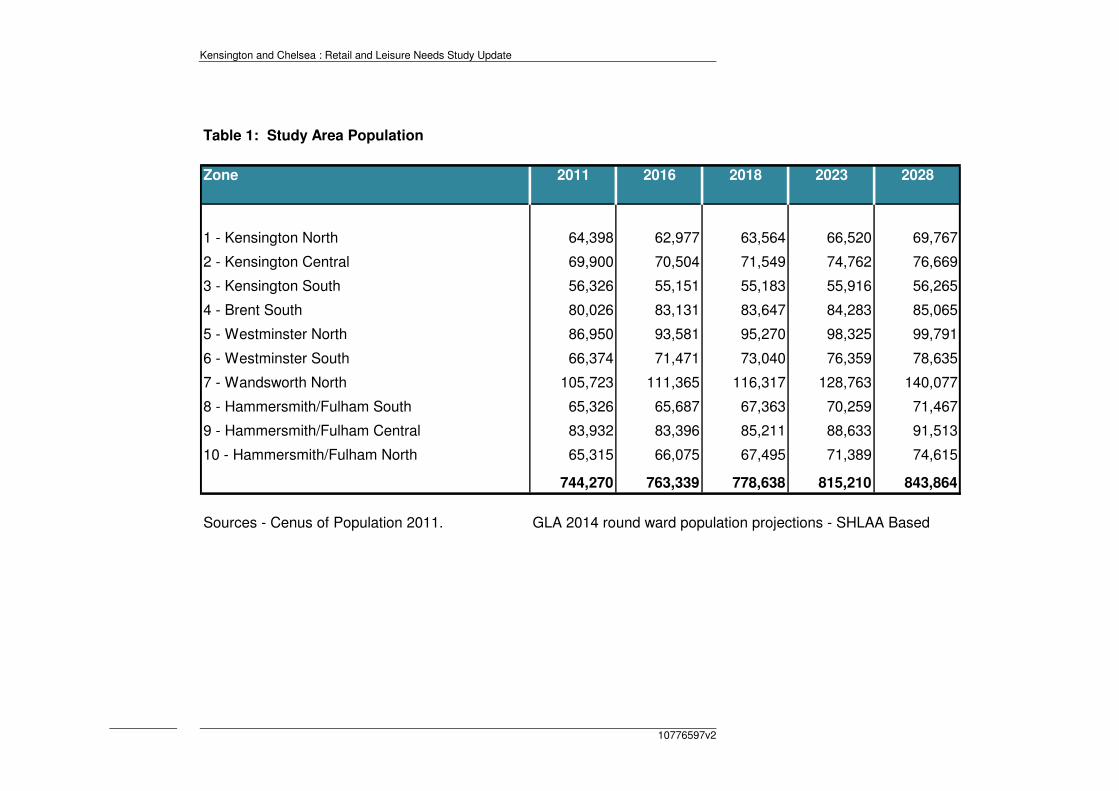

18 April 2016

11416/03/PW/PW

Nathaniel Lichfield & Partners 14 Regent's Wharf All Saints Street London N1 9RL nlpplanning.com

This document is formatted for double sided printing. © Nathaniel Lichfield & Partners Ltd 2016. Trading as Nathaniel Lichfield & Partners. All Rights Reserved. Registered Office: 14 Regent's Wharf All Saints Street London N1 9RL All plans within this document produced by NLP are based upon Ordnance Survey mapping with the permission of Her Majesty’s Stationery Office. © Crown Copyright reserved. Licence number AL50684A

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2

Contents

1.0 Introduction 1

Background ...................................................................................................... 1

2.0 Recent Changes and Retail Trends 2

Retail and High Street Trends .......................................................................... 2

The Shopping Hierarchy .................................................................................. 8

Town Centre Hierarchy Analysis ...................................................................... 9

3.0 Retail Need Assessment 2

Introduction ...................................................................................................... 2

Study Area ....................................................................................................... 2

Population and Expenditure ............................................................................. 3

Existing Retail Floorspace ................................................................................ 3

Existing Spending Patterns 2016 ..................................................................... 3

Qualitative Need .............................................................................................. 7

4.0 Other Town Centre Uses 11

Service Uses .................................................................................................. 11

Commercial Leisure Uses .............................................................................. 12

5.0 Accommodating Future Growth 16

Potential Development Opportunities ............................................................. 17

6.0 Conclusions 18

Meeting Shopping and Leisure Needs ........................................................... 18

Class A Retail Floorspace Projections ........................................................... 18

Commercial Leisure ....................................................................................... 19

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P1

1.0 Introduction

Background

1.1 Nathaniel Lichfield & Partners (NLP) was commissioned by the Royal Borough

of Kensington and Chelsea to prepare the Retail and Leisure Needs Study

published in July 2008 (RLNS 2008). The RLNS 2008 included:

• an assessment of the future needs for additional retail and commercial

leisure facilities within the authority area up to 2028;

• an analysis of the role and function of existing centres in the Borough.

1.2 NLP has been commissioned to provide a partial update to the 2008 study,

providing information on recent changes/trends in retail and leisure and an

update of the needs assessment. This update report should be read alongside

the RLNS 2008.

1.3 The update identifies recent changes including the National Planning Policy

Framework (NPPF) and adopts the latest available information, e.g. population,

expenditure and turnover levels.

1.4 The key elements of work updated include:

1 revised retail floorspace data for the seven main centres1 based on the

latest Goad Plan data;

2 updated turnover estimates for existing and proposed retail floorspace;

3 Experian’s latest 2014 local expenditure data;

4 2011 census and GLA's 2014 round of population projections;

5 Experian’s latest (October 2015) expenditure growth projections and

home shopping projections;

6 update of benchmark turnovers for existing food stores (Mintel November

2015 data);

7 impact implications of commitments implemented since 2008 (primarily

Westfield) and pipeline proposals including further expansion at Brent

Cross and Westfield, the new high street and facilities at Earls Court and

development under-construction at Battersea Power Station; and

8 market commentary of recent changes and forecast for home shopping

and how these will influence the demand for new floorspace and retail

capacity projections.

1 Goad survey seven centres including King’s Road East/West and Fulham Road East/West combined.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P2 10776597v2

2.0 Recent Changes and Retail Trends

Retail and High Street Trends

2.1 This section considers the changes in the retail and leisure sector nationally

and the implications for Kensington and Chelsea.

2.2 The economic downturn had a significant impact on the retail sector. A large

number of national operators failed (e.g. Phones 4 U, Blockbuster, Comet,

HMV, JJB Sports, Jessops, Clinton Cards, Woolworths, MFI, Land of Leather,

Borders, Game, Firetrap, Peacocks, La Senza, Past Times, Barratts and

Habitat), leaving major voids within town centres and on retail parks.

2.3 Many town centre development schemes were delayed or cancelled. The

demand for traditional retail warehouse operators was, and still is affected. The

main food store operators have seen a reduction in growth, with proposed new

foods cancelled.

2.4 Assessing future expenditure levels within this study needs to take into account

the likely speed of the economic recovery. Careful consideration is needed to

establish the appropriate level of expenditure growth to be adopted. This study

takes a long term view recognising the cyclical nature of expenditure growth.

Trends in population growth, home shopping/internet sales and growth in

turnover efficiency also need to be carefully considered and a balanced

approach taken.

2.5 An overview of national trends within the retail and leisure sector is set out

below.

Expenditure Growth

2.6 Historic retail trends indicate that expenditure has consistently grown in real

terms in the past, generally following a cyclical growth trend. The underlying

trend shows consistent growth and this trend is expected to continue in the

future. However the recovery from the economic downturn is expected to result

in slower growth in the short term.

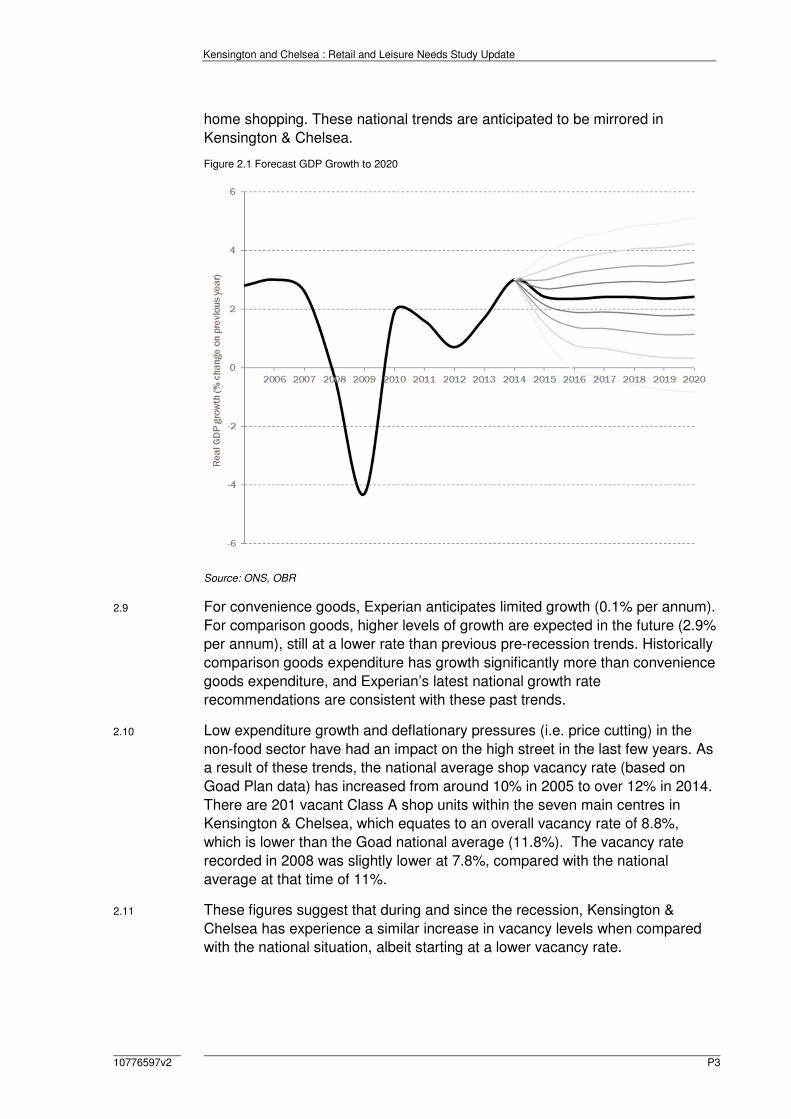

2.7 Figure 2.1 shows the Office for Budget Responsibility’s (OBR) forecast for

GDP up to 2020. After the recession in 2008, growth rebounded and from 2012

grew to the high of 3% in 2014. The OBR forecasts that growth will be slightly

above 2% per year from 2015 onwards.

2.8 In the past, expenditure growth has fuelled growth in retail floorspace, including

major out-of-centre development, particularly in the 1980s and 1990s. The

speed of recovery from the economic downturn has been slow. The high pre-

recession growth rates are unlikely to be achieved in the short term, but the

underlying trend over the medium and long terms is expected to lead to a need

for further modern retail floorspace, even allowing for continued growth in

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P3

home shopping. These national trends are anticipated to be mirrored in

Kensington & Chelsea.

Figure 2.1 Forecast GDP Growth to 2020

Source: ONS, OBR

2.9 For convenience goods, Experian anticipates limited growth (0.1% per annum).

For comparison goods, higher levels of growth are expected in the future (2.9%

per annum), still at a lower rate than previous pre-recession trends. Historically

comparison goods expenditure has growth significantly more than convenience

goods expenditure, and Experian’s latest national growth rate

recommendations are consistent with these past trends.

2.10 Low expenditure growth and deflationary pressures (i.e. price cutting) in the

non-food sector have had an impact on the high street in the last few years. As

a result of these trends, the national average shop vacancy rate (based on

Goad Plan data) has increased from around 10% in 2005 to over 12% in 2014.

There are 201 vacant Class A shop units within the seven main centres in

Kensington & Chelsea, which equates to an overall vacancy rate of 8.8%,

which is lower than the Goad national average (11.8%). The vacancy rate

recorded in 2008 was slightly lower at 7.8%, compared with the national

average at that time of 11%.

2.11 These figures suggest that during and since the recession, Kensington &

Chelsea has experience a similar increase in vacancy levels when compared

with the national situation, albeit starting at a lower vacancy rate.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P4 10776597v2

New Forms of Retailing

2.12 New forms of retailing (multi-channel shopping) have continued to grow.

Home/electronic shopping has increased with the growth in the use of personal

computers, smart phones and the internet. Click and collect shopping has

become more popular. The future growth of multi-channel retailing including

home computing, internet connections and interactive TV will continue to have

an effect on retailing in the high street and from traditional stores. Trends within

this sector will have implications for retailing within Kensington & Chelsea.

2.13 Recent trends suggest continued strong growth in this sector. Experian’s Retail

Planner Briefing Note 13 (October 2015) states:

“The strong increase in online shopping in the past decade has lifted the share

of special forms of trading (SFT) to a level where it now accounts for over a

tenth of total retail sales…

The rising share of internet sales in total retail transactions dominates the

picture of SFT. Internet sales’ share of total retail sales stood at 11.7% in mid-

2015 against 4.7% in June 2008...

…non-store retailing continues to grow rapidly, outpacing traditional forms of

spending. We retain our assumption that non-store retailing will increase at a

faster pace than total retail sales well into the long term. There were 57.3

million internet users in the UK (representing 88.4% of the population) in mid-

year 2014 according to Internet World Stats. So growth of the internet user

base will be less of a driver than in the past decade. But growth momentum will

be sustained as new technology such as browsing and purchasing through

mobile phones and the development of interactive TV shopping boost internet

retailing. We expect that the SFT market share will continue to increase over

the forecast period, although the pace of e-commerce growth will moderate

markedly after about 2020. Our forecast has the SFT share of total retail sales

reaching 17.8% by 2020 rising to 19.6% by the mid-2030s.”

2.14 This retail update makes an allowance for future growth in e-tailing based on

Experian projections. It will be necessary to monitor the amount of sales

attributed to home shopping in the future in order to review future policies and

development allocations.

2.15 The implications for the demand for retail space have been carefully

considered. Some retailers operate on-line sales from their traditional retail

premises e.g. food store operators and click and collect operations, therefore

growth in on-line sales may not always mean there is a reduction in the need

for retail floorspace.

2.16 Given the likelihood that multi-channel shopping is likely to grow at a faster

pace than total retail expenditure, the retail study assessment has adopted

relatively cautious growth projections for retail expenditure (as set out in the

retail capacity methodology, Appendix 1), and allowance has been made for

retailers to increase their turnover density, due to growth in home shopping

and click and collect.

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P5

2.17 In addition to new forms of retailing, retail operators have responded to

changes in customers’ requirements. Retailers have also changed their trading

formats to include smaller store formats capable of being accommodated

within town centres (such as the Tesco Express/Metro, Sainsbury’s Central/

Local store and Marks and Spencer’s Simply Foods formats). The number of

Tesco Express, Sainsbury’s Local and Little Waitrose stores has increased

significantly during the last decade. This trend has been particularly evident in

Kensington & Chelsea, with numerous local convenience stores operated by

the main food store retailers.

2.18 A number of proposed larger food stores have not been implemented across

the country, but this trend is less evident in London, perhaps due to the high

growth in population and the absence of available sites for larger food stores.

2.19 The expansion of European discount food operators Aldi and Lidl has been

rapid during the last decade. This trend is not evident in Kensington & Chelsea,

probably due to the absence of large sites/premises for discount stores.

2.20 Comparison retailers have also responded to market conditions. The bulky

goods warehouse sector has rationalised, including a number of mergers and

failures, and scaled down store sizes. Other traditional high street retailers

often seek large out-of-centre stores, for example Boots, Next, TK Maxx and

Poundstretcher. Matalan has also opened numerous discount clothing stores

across the UK. Sports clothing retail warehouses including Decathlon have

also expanded out-of-centre.

2.21 The demand for premises within the bulky goods sector, i.e. furniture, carpets,

electrical and DIY goods, has been particularly weak during and after the

recession. This has led to voids on retail warehouse parks and proposals to

extend the range of goods sold to non-bulky goods.

2.22 The retail warehouse sector is not represented in Kensington & Chelsea, since

the closure of the Homebase store at Warwick Road. High land values and the

lack of large development sites will restrict the potential for retail warehouses in

the Borough in the future.

2.23 The charity shop sector has grown steadily over the past 20 years and there is

no sign this trend will halt. In many centres, charity shops have occupied

vacated shop premises during the recession. In many cases charity shops can

afford higher rents than small independent occupiers because of business rate

discounts, therefore it does not follow that these charity shops will be replaced

by traditional shops when the market recovers, particularly in secondary

frontages. This trend is evident in Kensington & Chelsea although charity

shops account for 2.8% of all comparison shops within the seven Goad

centres, compared with the national average of 8.4%.

2.24 The discount comparison sector has also grown significantly in recent years

e.g. pound shops. This sector is under represented in Kensington & Chelsea.

2.25 The growth of money lending/pay day loan shops and betting shops has also

raised concerns amongst planning authorities, and has resulted in a change to

Kensington and Chelsea : Retail and Leisure Needs Study Update

P6 10776597v2

permitted development rights in order to control the growth of these uses in

town centres. This trend is not as evident in Kensington & Chelsea.

2.26 Within town centres, many high street multiple comparison retailers have

changed their format. For over a decade, high street national multiples have

increasingly sought larger modern shop units (over 200 sq.m) with an

increasing polarisation of activity into the larger national, regional and sub-

regional centres, e.g. Central London, Brent Cross and Westfield.

2.27 In general operator demand for space has decreased during the recession

and, of those national multiples looking for space, many prefer to locate in

larger centres.

2.28 The continuation of these trends will influence future operator requirements in

Kensington & Chelsea with smaller vacant units becoming less attractive for

new multiple occupiers, and retailers increasingly looking to relocate into larger

units in higher order centres. However, smaller vacant units could still be

attractive to independent traders and non-retail services.

2.29 Recent and proposed changes to the General Permitted Development Order

(GPDO) may also have an impact on town centres. These measures allow for

greater flexibility for changes of use from retail to non-retail uses e.g. Class A

uses to C3 residential use and Class A1 to A2 use. These measures could

change the composition of town centres, in particular the amount of Class A1

space could reduce. The measures may lead to a reduction in vacant shop

premises, particularly in peripheral shop frontages, but this could have an

impact on the ability of operators to find space, in areas where demand is high.

It is unlikely these changes will have a significant impact on Kensington &

Chelsea, because the centres already have a broad mix of retail and non-retail

uses, and a relatively low vacancy rate.

2.30 These trends are not new and have been affecting the High Street for many

years. In response to these trends, town centres have changed and diversified.

The food and beverage, leisure and non-retail service sectors have been

successful in occupying space no longer suitable for shopping. There have

been cyclical trends in vacancy rates reflecting the macro economic trends, but

in most cases town centres recovered during periods of stronger growth. The

High Street is more resilient than many commentators give it credit.

2.31 Shopping behaviour will continue to change and the High Street will need to

continue to respond. All town centres will need to focus on the advantages they

have over other forms of multi-channel shopping, for example using the

internet as an extended shop window, click and collect facilities and providing a

combined retail and leisure experience. There will always be demand for a day

out and customers cannot eat or drink on-line.

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P7

Services, Food and Beverage

2.32 Service uses perform an important role in the overall offer of a centre, and

encourage customers to shop locally. The service uses are categorised as

follows:

• Class A1 services cover a range of uses, including hairdressers, dry

cleaners, travel agents, some sandwich shops (those not categorised as

Class A3), funeral parlours and post offices.

• Class A2 services include banks, building societies, financial services,

betting offices, pawnbrokers, estate agents and employment agencies.

• Class A3/A5 includes restaurants, cafés (A3) and takeaways (A5).

• Class A4 pubs/bars (Class A4).

2.33 Food and beverages is a fast moving and creative sector, with a steady flow of

new concepts emerging. Within this sector there has been a significant

increase in the number of national multiple chains. These national chains have

sought to increase their geographical coverage. These types of food and drink

operators (Class A3 and A4) i.e. restaurants, bars and pubs have supported

other major leisure uses, in particular cinema developments. Within town

centres, the demand has increased, including a significant expansion in the

number of coffee shops, such as Starbucks, Costa Coffee and Café Nero.

Themed restaurants have also expanded rapidly.

2.34 The key categories for food and beverage offers are:

1 impulse: characterised by their produce range that is typically highly

visual and hand-held so that it can be eaten “on the go”;

2 speed eating fast food: food that can be purchased and consumed

quickly, therefore price is low and ambience is less important. This sector

is dominated by traditional high volume fast food offers such as burgers

and fried chicken;

3 refuel and relax: a drink and snacks and a short break in a pleasant

environment rather than focusing on eating a main meal; and

4 casual dining/leisure dining: incorporating a number of food styles,

types and ethnic origins. The ambience and environment of casual dining

is as important as the food, drink and service provided. The style is

informal but is normally table service.

2.35 Food and beverage establishments (Class A3, A4 and A5) including

restaurants, bars and pubs have supported other major leisure uses on leisure

and retail parks and are important services within town and local centres.

National information available from Experian Goad indicates that the proportion

of non-retail uses within town centres across the country has increased

significantly. A balance between Class A1 and Class A3 to A5 uses needs to

be maintained.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P8 10776597v2

The Shopping Hierarchy

2.36 The National Planning Policy Framework (NPPF) indicates (paragraph 23) that

planning policies should be positive, promote competitive town centre

environments and set out policies for the management and growth of centres

over the plan period. Development plans are expected to define a network and

hierarchy of centres that is resilient to anticipated future economic changes.

2.37 The National Planning Practice Guidance (NPPG) replaced the PPS4 guidance

on town centres in 2012. In terms of plan-making the NPPG’s emphasis is on

developing strategies for town centres that are appropriate and realistic to the

role of centres in the hierarchy. Town centre strategies should be based on the

current state of a centre and opportunities to meet development needs. These

town centre strategies should seek to support the town centre vitality and

viability, and should assess if changes to the role and hierarchy of centres are

appropriate. This section provides an overview of the shopping hierarchy in

Kensington and Chelsea and the surrounding sub-region.

The Designation of Town Centres

2.38 The NPPF indicates that local planning authorities should adopt a positive and

proactive approach to planning for growth and the future of the centres within

their areas. Local planning authorities are expected to identify the hierarchy of

centres and how the role of different centres will contribute to the overall vision

for their area. The town centre hierarchy is clearly set out in the RBKC

Consolidated Local Plan and the Further Alterations London Plan 2015 (FALP).

2.39 In terms of the London Plan hierarchy, Kensington and Chelsea contains:

International Centre

• Knightsbridge

Major Centres

• Kensington High Street

• Kings Road East (Goad Plan name = Chelsea Kings Road)

District Centres

• Earls Court Road (Neighbourhood Centre in the RBKC Local Plan)

• Fulham Road East (Brompton Cross DC in the RBKC Local Plan)

• Fulham Road West (Fulham Road DC in the RBKC Local Plan)

• Kings Road West (Goad Plan name = Chelsea Worlds End)

• Notting Hill Gate

• Portobello Road (Special District Centre in the RBKC Local Plan)

• South Kensington

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P9

2.40 Below District Centres, the FALP refers to Neighbourhood and Local Centres,

but these centres are not individually identified.

2.41 In addition to the 10 main centres designated within the FALP, the RBKC

Consolidated Local Plan identifies Westbourne Grove as a Special District

Centre and 36 Neighbourhood Town Centre (including Earls Court Road

identified as a District Centre in the FALP. In total Kensington and Chelsea

has 46 designated centres.

Town Centre Hierarchy Analysis

2.42 Venuescore ranks the UK’s top 3,000 retail destinations including town

centres, malls, retail warehouse parks and factory outlet centres. The results

for Kensington and Chelsea and other selected centres are shown in Table

2.1. Each destination is given a weighted score for the number of multiple

retailers present; the score attached to each retailer is weighted depending on

their overall impact on shopping patterns. The Venuescore data for more

centres is also shown on Figure 2.2.

2.43 The Venuescore usually closely correlates to the actual market size of the

shopping destination in terms of consumer expenditure, however some larger

shopping centres such as Westfield with fewer but larger stores and town

centres with a high proportion of independent stores can generate spending

levels in excess of their relative Venuescore.

2.44 Venuescore also assess the market position of the larger town centres based

on the retailers present and the centre’s relative position along a spectrum

running from discount to luxury (i.e. lower, middle to upscale).

2.45 Knightsbridge and Kings Road are top tier “upscale” centres, similar to other

major shopping destinations such as Westfield and Covent Garden, suggesting

they have an excellent and high quality comparison retail offer comparable with

other top destinations in Central London.

2.46 Kensington High Street is figures relatively high in the rankings, at a slightly

lower market position i.e. “upper middle”.

2.47 Portobello Road, Notting Hill, Earls Court, Fulham Road East, Fulham Road

West and South Kensington feature in the Venuescore rankings but achieve

relatively much lower scores, suggesting they are third or fourth tier centres in

the Venuescore hierarchy. However in terms of market position these centres

are still relatively high quality i.e. “upper middle” to “upscale”. These centres

have a specialist role.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P10 10776597v2

Table 2.1 Venuescore UK shopping Index 2015

Centre UK Rank Venuescore Market Position

Oxford Street 10 502 Upper Middle

Westfield White City 24 343 Upscale

Covent Garden 29 317 Upscale

Knightsbridge 41 285 Upscale

Kings Road 78 212 Upscale

Brent Cross 100 188 Upper Middle

Richmond Upon Thames 107 185 Upscale

Regents Street 107 185 Upscale

Wimbledon 123 172 Upper Middle

Ealing 126 170 Middle

Hammersmith 126 170 Middle

Clapham Junction 135 167 Upper Middle

Kensington High Street 138 166 Upper Middle

Putney 142 163 Upper Middle

Chiswick 166 144 Upper Middle

Hounslow 186 136 Lower Middle

Wandsworth 196 127 Middle

Victoria 225 113 Upper Middle

Bayswater/Queensway 230 111 Upper Middle

Kilburn 259 101 Lower Middle

Edgware Road 360 78 Upper Middle

Portobello Road 390 73 Upscale

Notting Hill 480 61 Upper Middle

Fulham Broadway 659 47 Upper Middle

Earls Court 659 47 Middle

Fulham Road West 735 42 Upper Middle

South Kensington 2034 15 Upscale

Fulham Road East 2577 11 Upscale

Source: Venuescore, Javelin Group 2015: BOLD indicates shopping destinations located in RBKC

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P1

Figure 2.2: Venuescore Centres in Central/West London

Source: Javelin Venuescore 2015

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P1

Provision in Royal Borough of Kensington and Chelsea

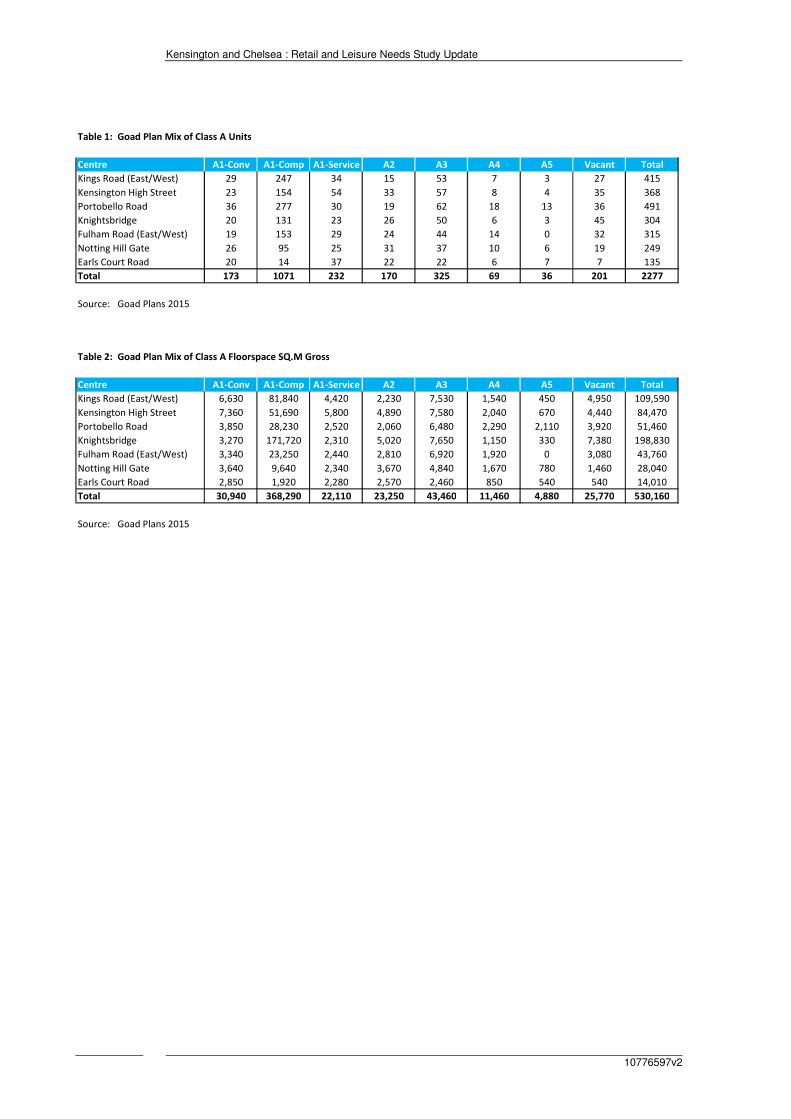

2.48 A summary of existing retail provision within Goad Plan centres in Kensington

and Chelsea is provided in Table 2.2.

Table 2.2 Existing Retail Provision in RB Kensington and Chelsea

Centre

Number

Shop

Units

Convenience

Floorspace

(sq.m gross)

Comparison

Floorspace

*(sq.m gross)

Food and

Beverage

(sq.m gross)

Knightsbridge 304 3,270 171,720 9,130

King’s Road (East and West) 415 6,630 81,840 9,520

Kensington High Street 368 7,360 51,690 10,290

Fulham Road (East and West) 315 3,340 23,250 8,840

Portobello Rd (incl. Westbourne G) 491 3,850 28,230 8,770

Notting Hill Gate 249 3,640 9,640 7,290

Earls Court Road 135 2,850 1,920 3,850

Total 2,277 30,940 368,290 57,690

Sources: Goad Plans 2015 * includes upper trading floors

2.49 A more detailed breakdown of the existing retail provision in the main centres

is provided in Appendix 2.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P2 10776597v2

3.0 Retail Need Assessment

Introduction

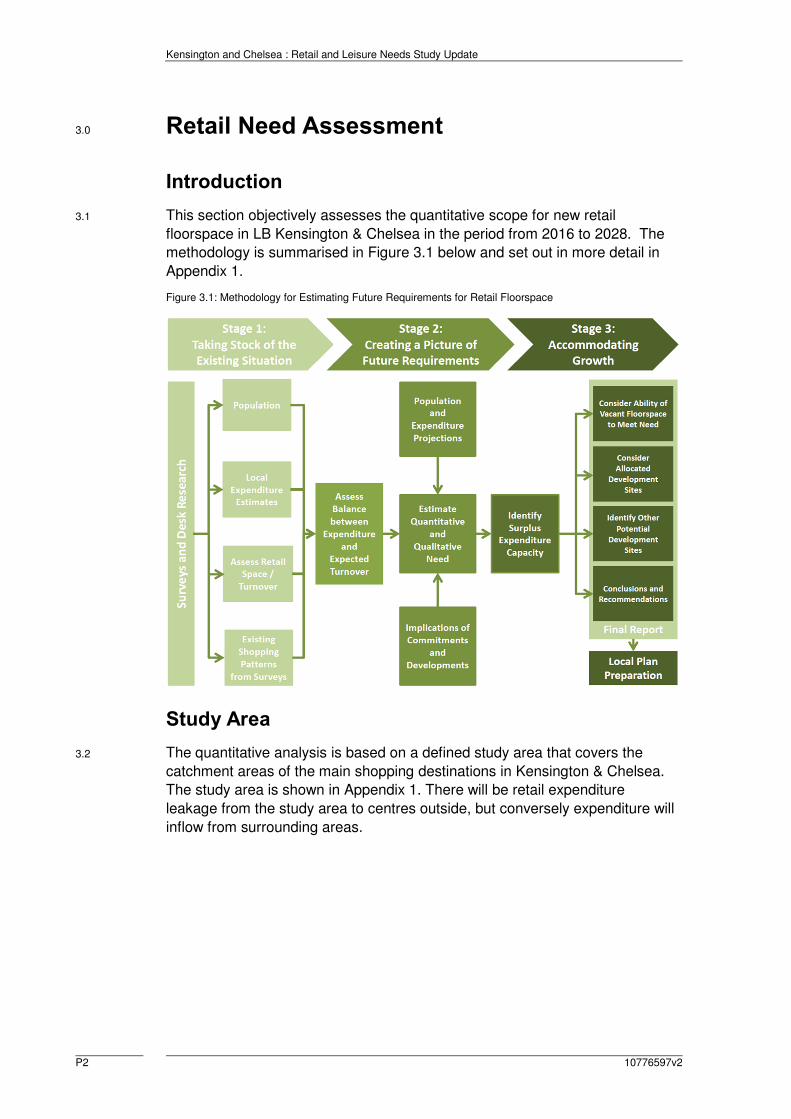

3.1 This section objectively assesses the quantitative scope for new retail

floorspace in LB Kensington & Chelsea in the period from 2016 to 2028. The

methodology is summarised in Figure 3.1 below and set out in more detail in

Appendix 1.

Figure 3.1: Methodology for Estimating Future Requirements for Retail Floorspace

Study Area

3.2 The quantitative analysis is based on a defined study area that covers the

catchment areas of the main shopping destinations in Kensington & Chelsea.

The study area is shown in Appendix 1. There will be retail expenditure

leakage from the study area to centres outside, but conversely expenditure will

inflow from surrounding areas.

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P3

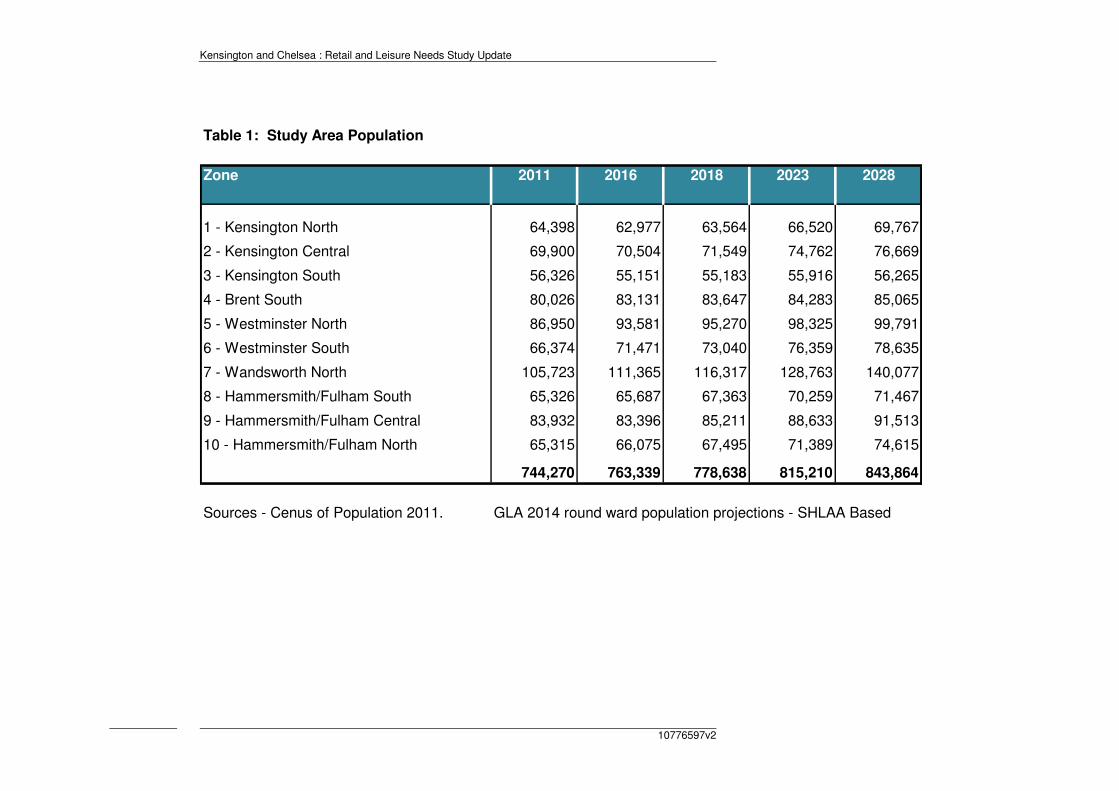

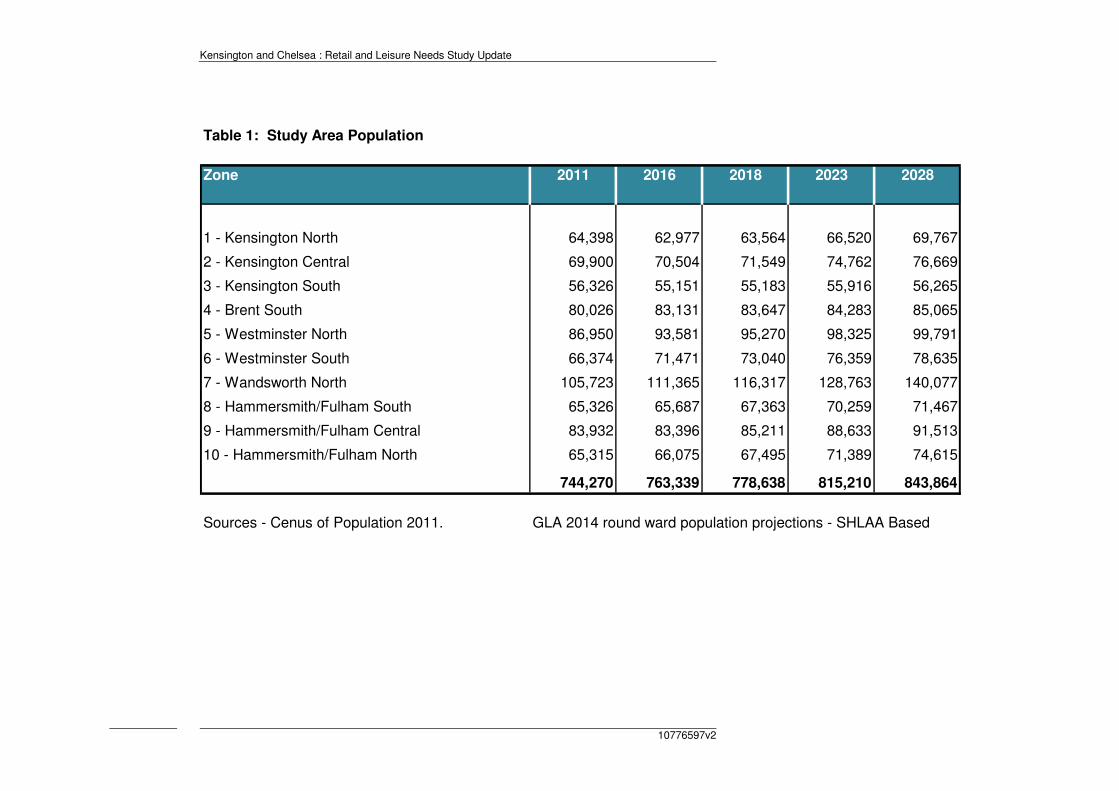

Population and Expenditure

3.3 The study area population for 2011 to 2028 is set out in Table 1 in Appendix 3.

The 2011 base year population for each zone has been obtained and projected

to 2031 using the GLA 2014 Round of Demographic Projections ward (SHLAA

bases) projections.

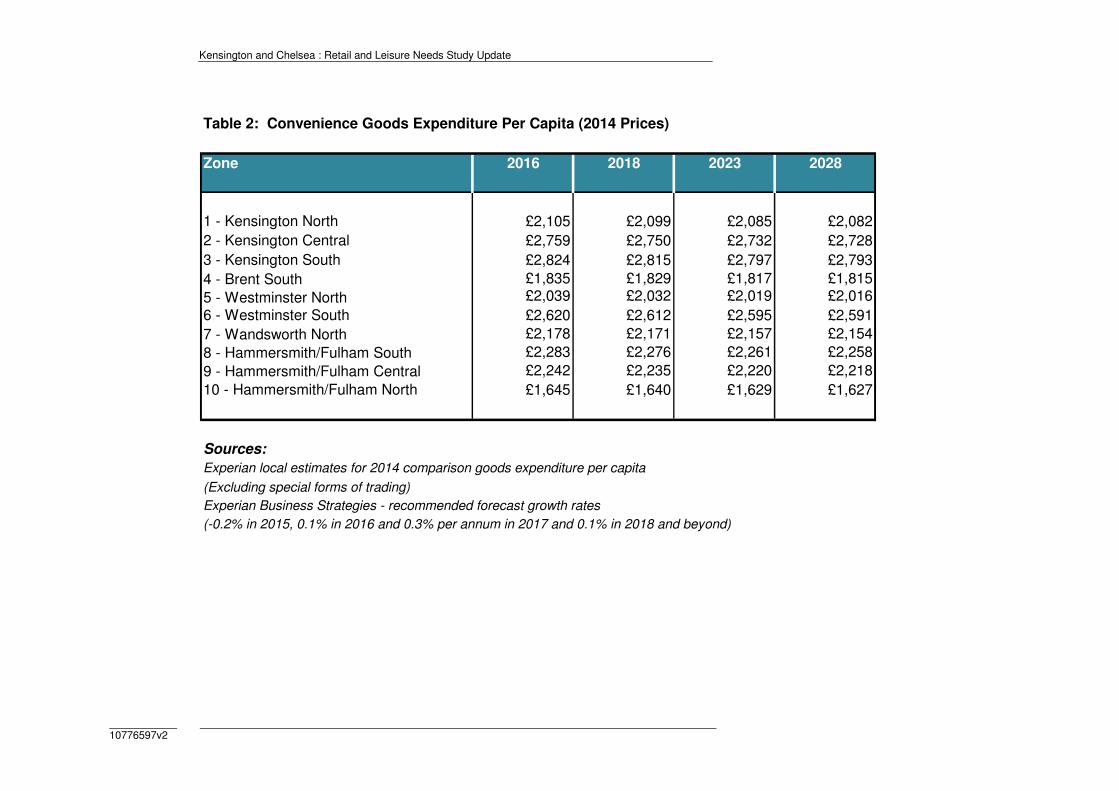

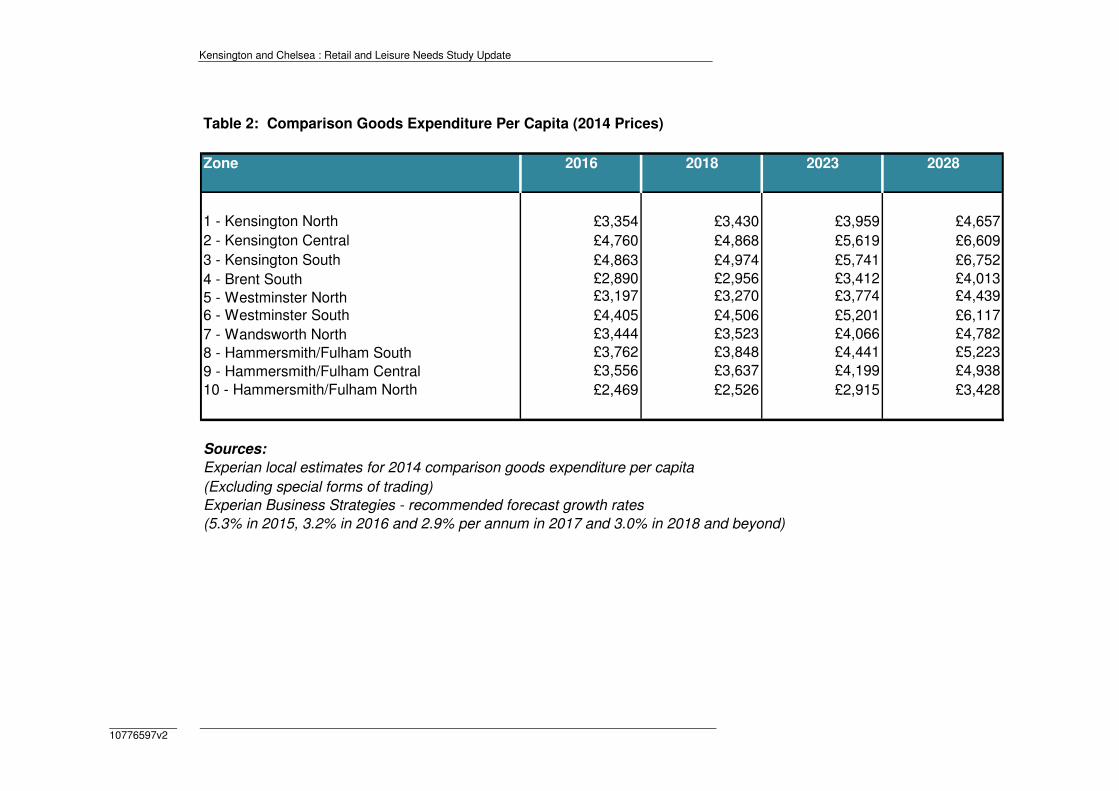

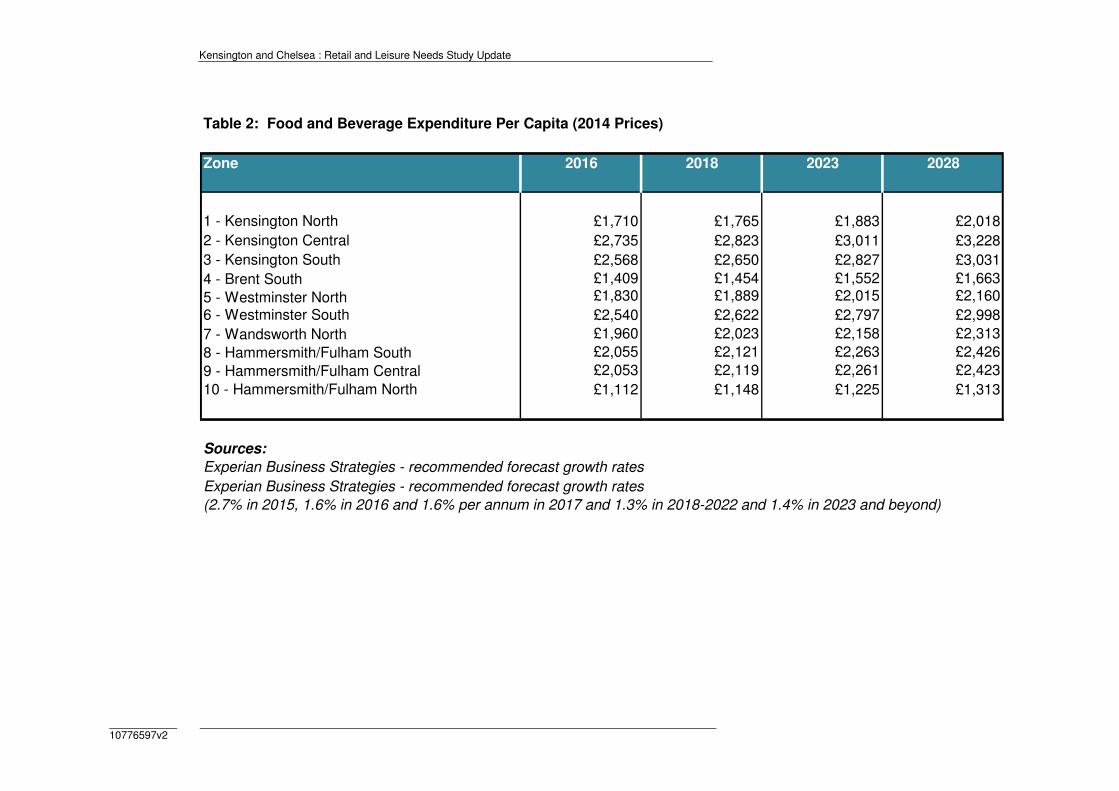

3.4 Table 2 in Appendix 3 sets out the forecast growth in spending per head for

convenience goods within each zone in the study area up to 2028. Forecasts

of comparison goods spending per capita are shown in Table 2 in Appendix 4.

3.5 Based on the GLA population projections, as a consequence of growth in

population and per capita spending, convenience goods spending within the

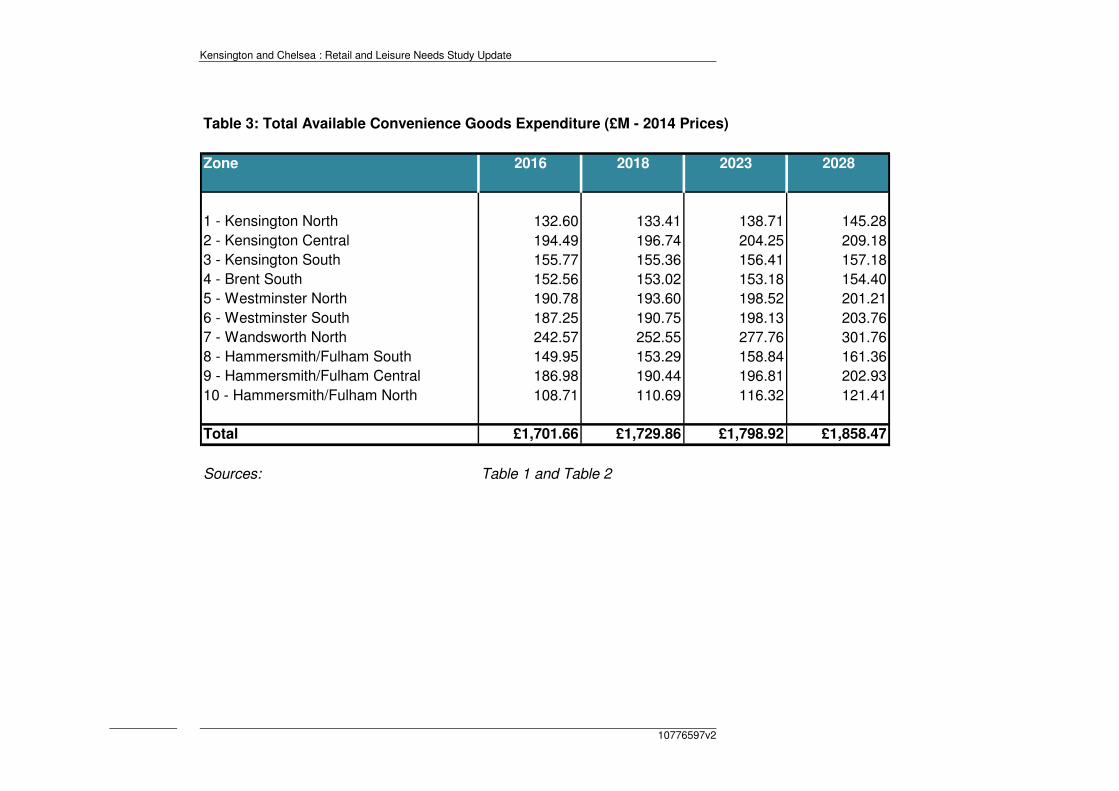

study area is forecast to increase by 9.2% from £1,701 million in 2016 to

£1,858 million in 2028, as shown in Table 3 (Appendix 2).

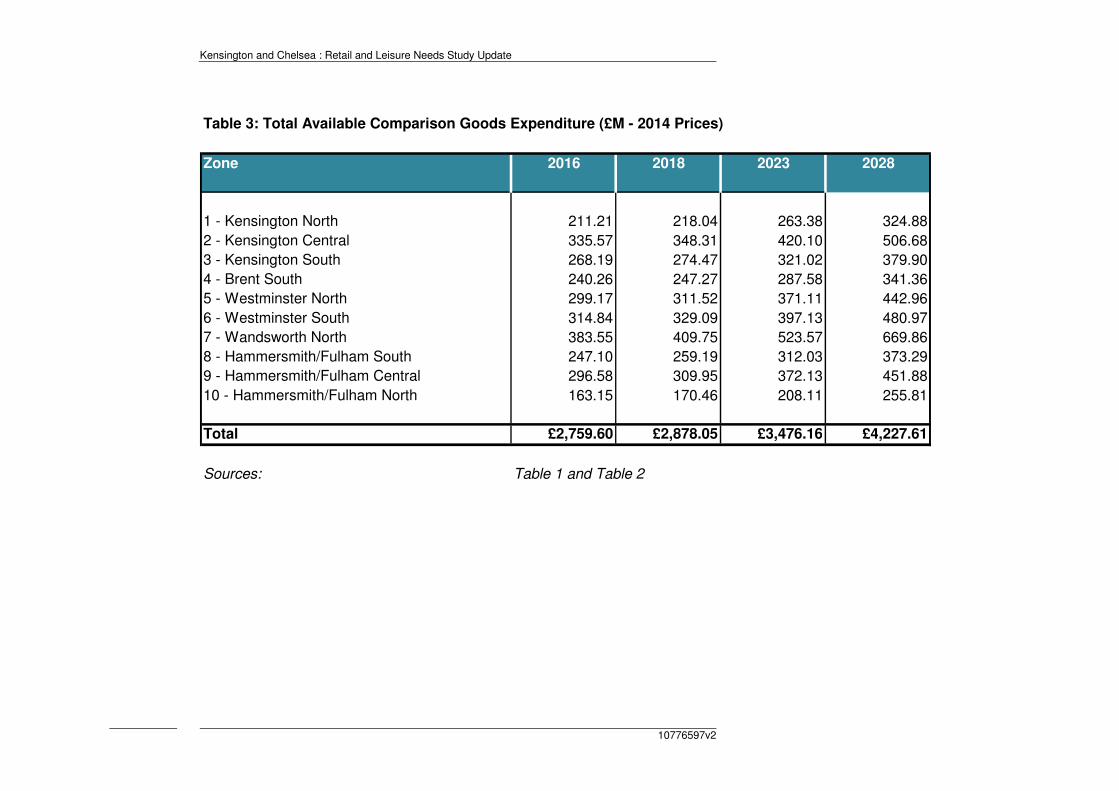

3.6 Comparison goods spending is forecast to increase by 53% between 2016 and

2028, increasing from £2,759 million in 2016 to £4,227 million in 2028, as

shown in Table 3 (Appendix 3).

3.7 It should be noted that comparison goods spending is forecast to increase

more than convenience spending as the amount spent on food and beverage

does not increase proportionately with disposable income, whereas spending

on non-food goods is more closely linked to income.

3.8 These figures relate to real growth and exclude inflation.

Existing Retail Floorspace

3.9 Existing convenience goods retail sales floorspace within Kensington &

Chelsea is around 50,200 sq.m net, as set out in Table 10 in Appendix 3. This

floorspace figure excludes comparison sales floorspace within food stores.

This floorspace is relatively evenly spread throughout the Kensington &

Chelsea. The amount of convenience goods sales floorspace has increase by

10% from 45,500 sq.m net in 2008, due primarily to new small convenience

stores. There are now 38 food stores operated by the main food retailers

(source: ORC’s StorePoint), compared with 31 stores in 2008.

3.10 Comparison goods retail sales floorspace within Kensington & Chelsea was

estimated to be around 269,700 sq.m net in 2008. This net sales floorspace is

estimated to have fallen slightly to 267,700 sq.m net in 2015, based on the

latest Goad Plan information.

Existing Spending Patterns 2016

3.11 The results of the household shopper questionnaire survey undertaken by

NEMS in February 2008 were adopted to estimate base year shopping

patterns within the study area zones. The RLNS 2008 adjusted market shares

to reflect know commitments at that time, e.g. Westfield White City. These

adjusted market shares have been adopted for the new 2016 base year, with

Kensington and Chelsea : Retail and Leisure Needs Study Update

P4 10776597v2

further adjustments made based on household survey information, obtained

from more recent retail studies/impact assessments.

Convenience Shopping

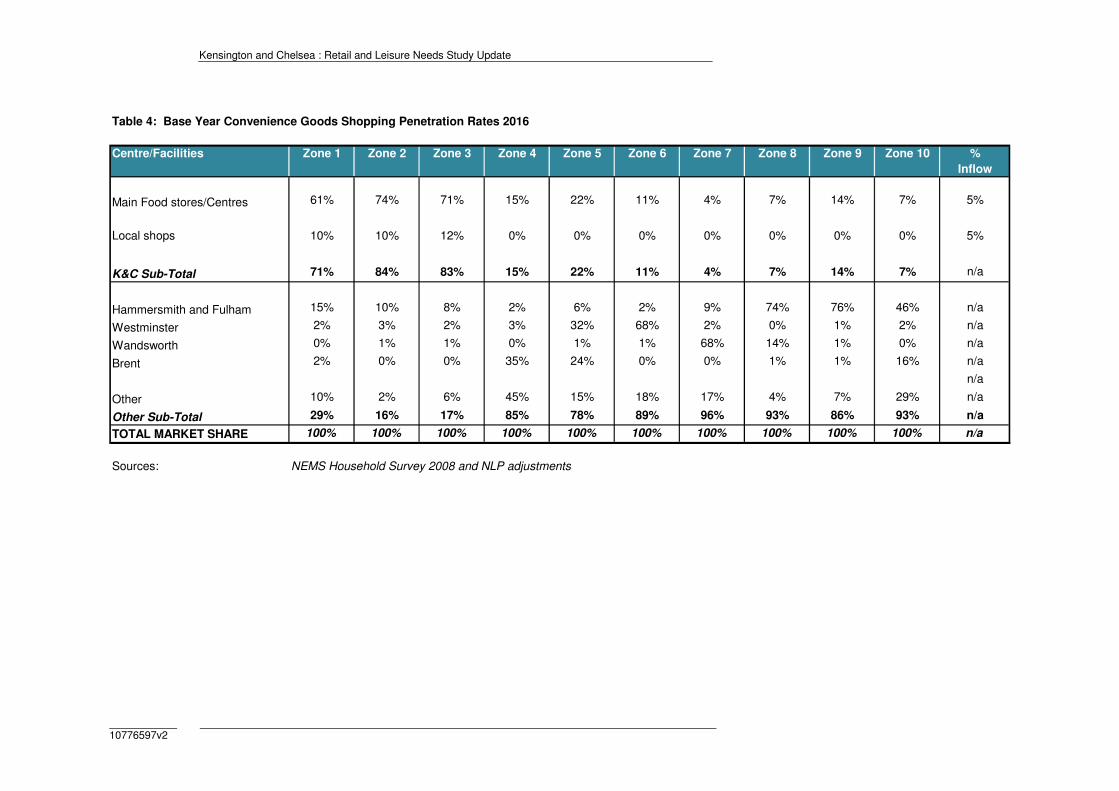

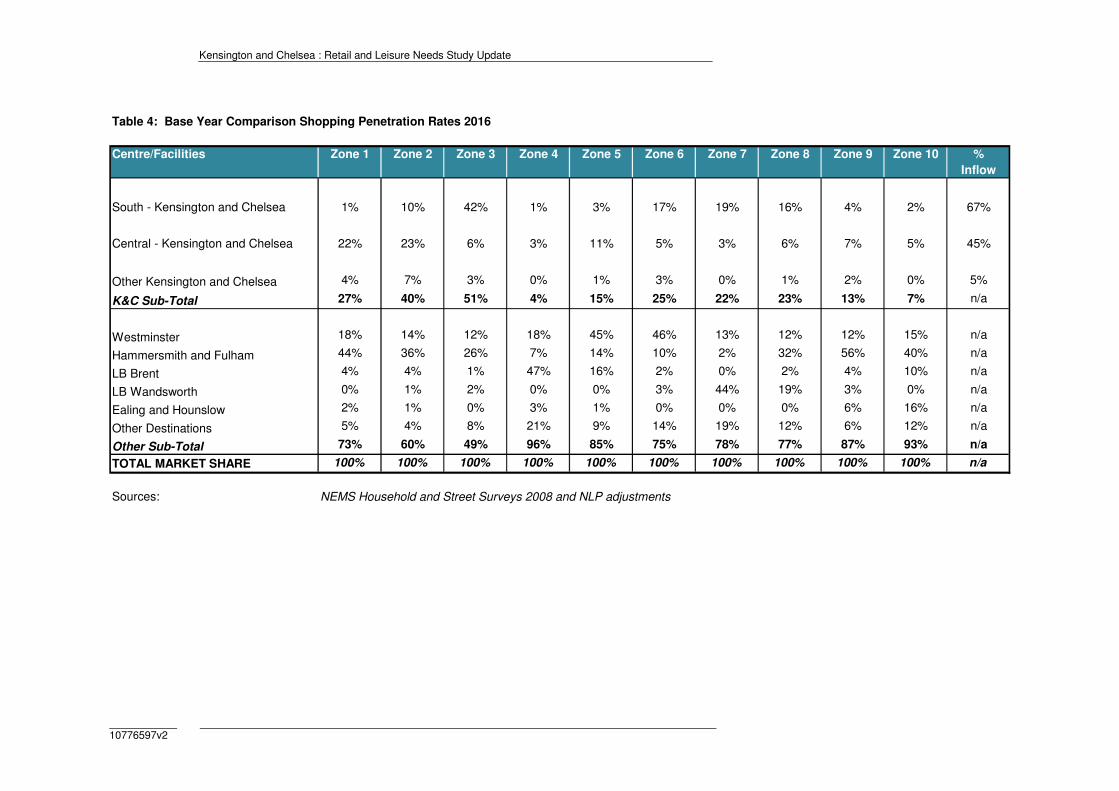

3.12 The adjusted estimates of market share or penetration within each study area

zone are shown in Table 4, Appendix 3. The proportion of convenience goods

expenditure retained within Kensington & Chelsea (Zones 1- 3) is relatively

high at 80%. Based on NLP’s experience from other recent studies across

London, this level of convenience goods expenditure retention is relatively

high. There appears to be limited scope to increase the retention of

convenience goods expenditure within the Kensington & Chelsea area.

3.13 The level of convenience goods expenditure attracted to shops/stores in LB

Kensington & Chelsea in 2016 is estimated to be £554 million as shown in

Table 5, Appendix 3. This includes estimates of inflow from beyond the study

area, applying the adjusted market shares set out in Table 4.

3.14 The total benchmark turnover of identified existing convenience sales

floorspace within Kensington & Chelsea, based on company average sales

densities is £500 million (Table 10 in Appendix 3), compared with the actual

turnover of £554 million. These figures suggest that convenience retail sales

floorspace in Kensington & Chelsea is trading healthily at 11% above the

expected benchmark. This suggests a base year expenditure surplus of £54

million.

3.15 Based on NLP’s recent experience, food stores within London tend to trade

above national average sales densities, which may reflect higher property

costs and more affluent households. Furthermore, food stores in London tend

to be smaller with less circulation space and therefore the sales density per

unit of floorspace is likely to be higher.

3.16 The future levels of available convenience goods expenditure in 2018, 2023

and 2028 are shown at Tables 7 to 9 in Appendix 3. These projections are

based on adjusted market shares to reflect committed food store proposals

within the Vauxhall, Nine Elms and Battersea regeneration area.

3.17 The total level of convenience goods expenditure available for shops in

Kensington & Chelsea between 2016 and 2028 is summarised in Table 11 in

Appendix 3. Allowing for population and expenditure per capita growth and

increased market shares, convenience goods expenditure available to

shopping facilities in Kensington & Chelsea is expected to increase from £554

million in 2016 to £579 million in 2028, an additional £25 million.

3.18 The expenditure projections are converted into potential new floorspace

estimates in Table 12 in Appendix 3. Expenditure growth is converted into

floorspace estimates based on an average sales density figure of £10,244 per

sq.m net for the main stores/centres, based on the average derived from the

benchmark turnover. A density of 38,000 per sq.m net is adopted for other

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P5

local shops. No increase in sales density has been assumed for convenience

goods, in line with Experian forecasts.

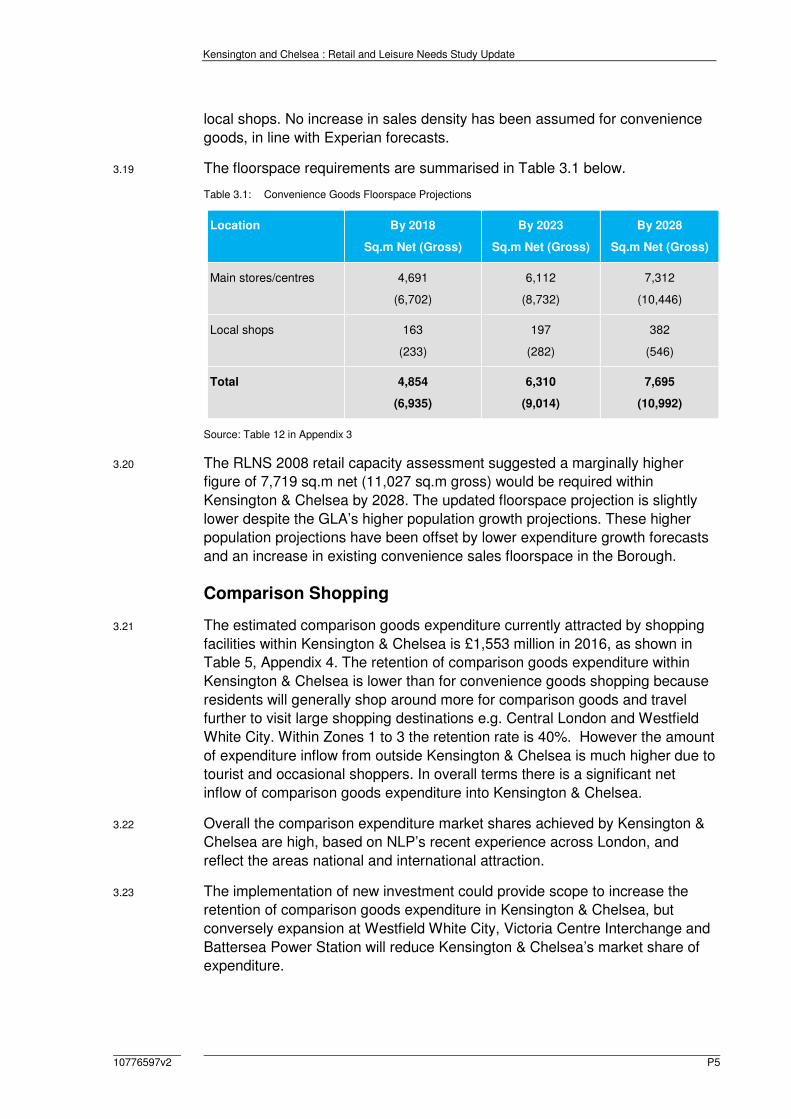

3.19 The floorspace requirements are summarised in Table 3.1 below.

Table 3.1: Convenience Goods Floorspace Projections

Location By 2018

Sq.m Net (Gross)

By 2023

Sq.m Net (Gross)

By 2028

Sq.m Net (Gross)

Main stores/centres 4,691

(6,702)

6,112

(8,732)

7,312

(10,446)

Local shops 163

(233)

197

(282)

382

(546)

Total 4,854

(6,935)

6,310

(9,014)

7,695

(10,992)

Source: Table 12 in Appendix 3

3.20 The RLNS 2008 retail capacity assessment suggested a marginally higher

figure of 7,719 sq.m net (11,027 sq.m gross) would be required within

Kensington & Chelsea by 2028. The updated floorspace projection is slightly

lower despite the GLA’s higher population growth projections. These higher

population projections have been offset by lower expenditure growth forecasts

and an increase in existing convenience sales floorspace in the Borough.

Comparison Shopping

3.21 The estimated comparison goods expenditure currently attracted by shopping

facilities within Kensington & Chelsea is £1,553 million in 2016, as shown in

Table 5, Appendix 4. The retention of comparison goods expenditure within

Kensington & Chelsea is lower than for convenience goods shopping because

residents will generally shop around more for comparison goods and travel

further to visit large shopping destinations e.g. Central London and Westfield

White City. Within Zones 1 to 3 the retention rate is 40%. However the amount

of expenditure inflow from outside Kensington & Chelsea is much higher due to

tourist and occasional shoppers. In overall terms there is a significant net

inflow of comparison goods expenditure into Kensington & Chelsea.

3.22 Overall the comparison expenditure market shares achieved by Kensington &

Chelsea are high, based on NLP’s recent experience across London, and

reflect the areas national and international attraction.

3.23 The implementation of new investment could provide scope to increase the

retention of comparison goods expenditure in Kensington & Chelsea, but

conversely expansion at Westfield White City, Victoria Centre Interchange and

Battersea Power Station will reduce Kensington & Chelsea’s market share of

expenditure.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P6 10776597v2

3.24 Based on the base year estimate of comparison goods expenditure attracted to

facilities within Kensington & Chelsea, the average sales density for existing

comparison sales floorspace (267,695 sq.m net) is £5,800 per sq.m net. The

Kensington & Chelsea average was £6,442 per sq.m net in 2008 (2006 prices).

Part of this reduction in average sales density is due to deflation in comparison

good from 2006 to 2014 prices. The deflation adjusted sales density for 2008 is

£6,088 per sq.m net, which is still 5% higher than the updated 2016 base year

average turnover density.

3.25 The average sales density may have reduced due to the effects of the

recession and the impacts of recent developments. However, the current sales

density £5,800 per sq.m net is still satisfactory, although lower than the healthy

trading levels estimated in 2008.

3.26 The comparisons goods turnover of facilities in the Borough was £1,642 million

in 2008 (adjusted to 2014 prices), which is 5.4% higher than the current 2016

turnover. Between 2008 and 2016 the amount of comparison goods

expenditure within the study area increased by 25%, due to population growth

and growth in expenditure per person. If facilities in Kensington & Chelsea had

maintained their market share of expenditure between 2008 to 2016, then one

would expect the 2016 turnover to be around 30% higher than the estimate set

out above (around £2,019 million rather than £1,553 million). These figures

suggest that the cumulative impacts of Westfield and other developments

implemented between 2008 to 2016 was around 30%, but most of this impact

has been offset by expenditure growth. As a result current 2016 trading levels

are only 5.4% lower than the pre-Westfield turnover in 2008.

3.27 The RLNS 2008 predicted the post Westfield turnover of facilities in Kensington

& Chelsea would be £2,044 million in 2016. This figure is much higher than the

revised projection (£1,553 million), because total comparison goods

expenditure within the study area at 2016 is 8.1% lower than the previous

projected estimate in the RLNS 2008, and the impact of Westfield and other

developments implemented between 2008 and 2016 has been much higher

than that predicted in 2008.

3.28 These figures suggest that, despite population and comparison expenditure

growth between 2008 and 2016, growth has been offset and exceeded by the

impact of development since 2008, most notably being the opening of

Westfield. Available comparison goods expenditure has been projected

forward to 2018, 2023 and 2028 in Tables 6 to 9 in Appendix 4, based on

adjusted market shares to reflect current commitments. The results are

summarised in Table 11. Available comparison expenditure to facilities within

Kensington & Chelsea is expected to increase from £1,533 million in 2016 to

£2,089 million in 2028.

3.29 For the purposes of this assessment, the existing comparison goods

floorspace is estimated to be trading at equilibrium in 2016 (i.e. satisfactory

levels). Table 10 assumes that the turnover of comparison floorspace will

increase in real terms in the future. A growth rate of 2% per annum is adopted,

as recommended by Experian. This growth will help to maintain the health and

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P7

viability of town centres. Trends indicate that comparison retailers historically

will achieve some growth in trading efficiency.

3.30 Surplus comparison expenditure has been converted into net comparison sales

floorspace projections at Table 12 in Appendix 4, adopting average sales

densities in 2016 of £6,000 per sq.m, which is projected to grow by 2% in the

future due to improved turnover efficiency. The surplus expenditure at 2028

could support 15,754 sq.m net of comparison sales floorspace (21,005 sq.m

gross). The floorspace projections are summarised in Table 3.2 below.

Table 3.2: Comparison Goods Floorspace Projections

Area By 2023

Sq.m (gross)

By 2028

Sq.m (gross)

South Kensington & Chelsea 0 7,818 (10,424)

Central Kensington & Chelsea 0 6,651 (8,868)

Rest of Kensington & Chelsea 259 (345) 1,284 (1,712)

Total 259 (345) 15,754 (21,005)

Source: Table 12 in Appendix 4

3.31 The projections suggests there is limited capacity in the short to medium term

up to 2023, due to the implementation of planned commitments in

neighbouring boroughs, as listed at the foot of Table 7 in Appendix 4.

3.32 The RLNS 2008 retail capacity assessment suggested a much higher

projection for comparison goods retail floorspace (144,881 sq.m gross by

2028). The main reasons for this reduction are as follows.

1 Experian’s local expenditure estimate for the study area at 2016 is 9%

lower than previously projected in 2008, due to the effects of the

recession.

2 Future comparison expenditure was previously projected to increase by

3.5% per annum between 2016 and 2028. Experian’s latest

recommended growth rate is only 3% per annum.

3 The deduction for special forms of trading was only 9.2% at 2028.

Experian’s latest forecast for 2028 is 15%.

4 As a result of the above, expenditure per capita projections in 2028 are

now 19% lower the projection in the RLNS 2008.

Qualitative Need

3.33 The assessment in this section quantifies the theoretical capacity to support

new retail floorspace within Kensington & Chelsea, based on the population

projections and growth in expenditure. The qualitative need for retail facilities

also needs to be considered.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P8 10776597v2

3.34 Qualitative need can be assessed through consideration of the following

factors:

• deficiencies or ‘gaps’ in existing provision;

• consumer choice and competition;

• overtrading, congestion and overcrowding of existing stores;

• location specific needs such as underserved markets; and

• the quality of existing provision.

3.35 As indicated in Section 2, Kensington and Chelsea has a designated

International Centre (Knightsbridge) and two Major Centres (Kensington High

Street and Kings Road East). These three centres are major shopping

destinations within central London. These centres are supported by relatively

large designated District Centres. The network of centres serves shoppers

from the Borough and across London, and also tourist visitors.

Mix of Uses and Occupier Representation

3.36 The seven main centres surveyed by Experian Goad in 2015 have 2,277

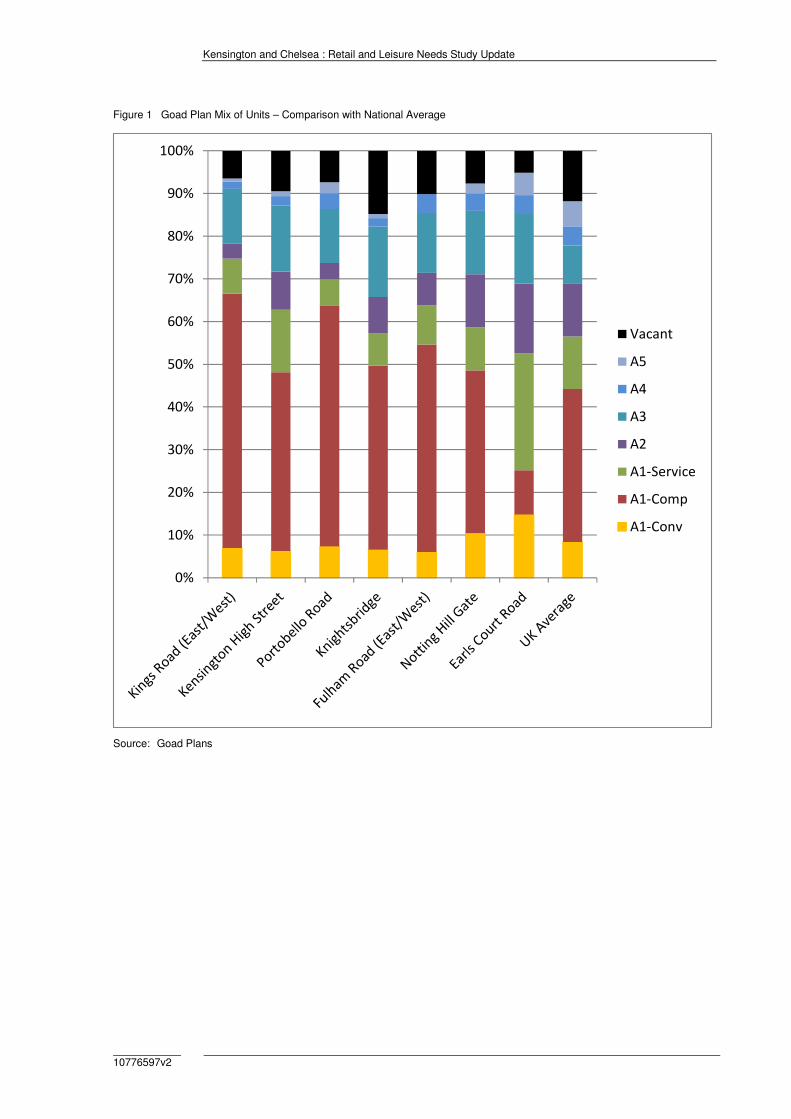

retail/service units (excluding non-retail Class A uses). Tables 1 and 2 in

Appendix 2 set out the mix of uses in these seven main centres. Figure 1 in

Appendix 2 compares the mix of units within each centre with the Goad

national average.

3.37 The proportion of comparison goods retail units is higher than the national

average in all centres accept for Earls Court Road, which has a high proportion

of non-retail services. All centres have a high proportion of Class A3

restaurants/café, reflecting the strong evening economy and tourist attractions

in the Borough. Vacancy rates are generally lower than the national average,

with the exception of Knightsbridge. Knightsbridge has a large number of

properties undergoing alternation at the time of the Goad survey (May 2015).

3.38 The number of vacant units has increased from 157 recorded in 2008 to 201 in

2012. This increase may be due to the continuing effects of the recession and

the impact of major development (i.e. Westfield).

3.39 The increase in vacant units is not significant and there are no obvious

concentrations of vacant units within centres, a part from units under alteration

in Knightsbridge. The overall vacancy rate (8.8%) remains below the national

average (11.8%).

Convenience Goods Retailer Representation

3.40 Food store provision is set out in Table 10 in Appendix 2. There are three food

superstores (2,500 sq.m net or more) in the Borough i.e. Sainsbury stores at

Ladbroke Grove and Cromwell Road and Tesco West Cromwell Road. These

food superstores are supported by other large/medium food stores (around

1,000 to 2,000 sq.m net) that are also suitable for bulk/weekly food and grocery

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P9

shopping e.g. Waitrose and Tesco Metros stores and Marks & Spencer Food

Halls.

3.41 There are a large number of small convenience stores (less than 500 sq.m net)

that are suitable for basket and top-up food shopping e.g. Marks & Spencer

Simply Food, Little Waitrose, Tesco Express and Sainsbury’s Local stores. In

addition to food stores, centres within Kensington and Chelsea have a good

selection of small independent convenience shops.

3.42 In Kensington & Chelsea a higher proportion of household shop at smaller

stores, by bus or on foot, when compared with other parts of the Country and

outer London. This is reflected in the existing mix of food store in the Borough.

The provision of food stores in the Borough is shown in Table 10, Appendix 3.

3.43 Residents in the Borough have excellent access to a choice of food stores and

convenience shops.

Comparison Goods Retailer Representation

3.44 The total number of comparison goods shops is 1,071. The number recorded

in these centres in 2008 was 1,095, which suggests this sector reduced only

slightly despite the effects of the recession.

3.45 The network of centres in Kensington and Chelsea provide an extensive range

and choice comparison shops, including many national multiples and

independent specialists. The centres provide a spread of comparison shopping

destinations across the centre and south of the Borough, however there is

limited comparison provision in the north of the Borough. Portobello Road and

Westbourne Grove serve the northern part of the Borough, but they are more

specialist destinations and do not provide the same range and choice of

comparison shopping when compare with the Major and International Centres.

Nevertheless, residents in this part of the Borough have excellent access to the

Westfield Shopping Centre at White City.

3.46 Within Kensington & Chelsea the main department stores offer an extensive

range of furniture and electrical items and there is also a good provision of high

street and independent furniture, carpet and electrical shops. There are a large

number of antique shops and art galleries throughout the Borough, which

reflects the high proportion of affluent residents within the Borough and the

areas national and international reputation for specialist antiques shopping.

3.47 The Homebase on Warwick Road was the only traditional large retail

warehouse in Kensington & Chelsea, but this has now closed. Large retail

warehouses are unlikely to be viable in the Borough due to high land values

and the absence of large development sites. Retail warehouses in London are

generally concentrated in outer London Boroughs. The potential to improve

retail warehouse provision within the Borough is limited.

3.48 Despite the lack of retail warehouses within the Borough, there are a selection

of retail warehouses within close proximity to the Borough including Homebase

& B&Q in Wandsworth, Comet and Currys in Wembley and other standalone

Kensington and Chelsea : Retail and Leisure Needs Study Update

P10 10776597v2

stores in Hammersmith, Fulham, Acton and Chiswick. The Borough has a good

selection of traditional hardware stores, furniture shops and interior design

specialists.

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P11

4.0 Other Town Centre Uses

Service Uses

4.1 The network of centres in the Borough has an extensive range and choice of

service uses. Tables 1 and 2 in Appendix 2 indicate that the Goad surveyed

centres within the Borough have 232 Class A1 services e.g. hairdressers,

beauty parlours, travel agents and dry cleaners.

4.2 There are 170 Class A2 financial and professional services e.g. banks, building

societies and estate agents. Food and beverage outlets (A3/A4/A5) total 430,

with a particularly strong provision of Class A3 restaurants/cafés.

4.3 Food and beverage establishments (Class A3, A4 and A5) including

restaurants, bars and pubs are important services within town and local

centres. National information available from Experian Goad indicates that the

proportion of non-retail uses within town centres across the country has

increased significantly. The current UK average for Goad town centres

indicates that 14.7% of units are in Class A3/A5 (restaurants, café and

takeaway) and 2.9% of units are Class A4 (public houses/bars). A balance

between Class A1 and Class A3 to A5 uses needs to be maintained. The mix

of uses in the main centres in Kensington and Chelsea is shown in Appendix 2.

4.4 The Goad Plan surveys indicate the proportions of Class A3/A5/A4 within

Kensington and Chelsea are higher than the national average. In particular

there is an excellent provision of Class A3 restaurants/café.

Food and Beverage Expenditure

4.5 Experian's latest 2014 local expenditure figures have been adopted. Food and

beverage expenditure per capita projections are shown in Table 2 in Appendix

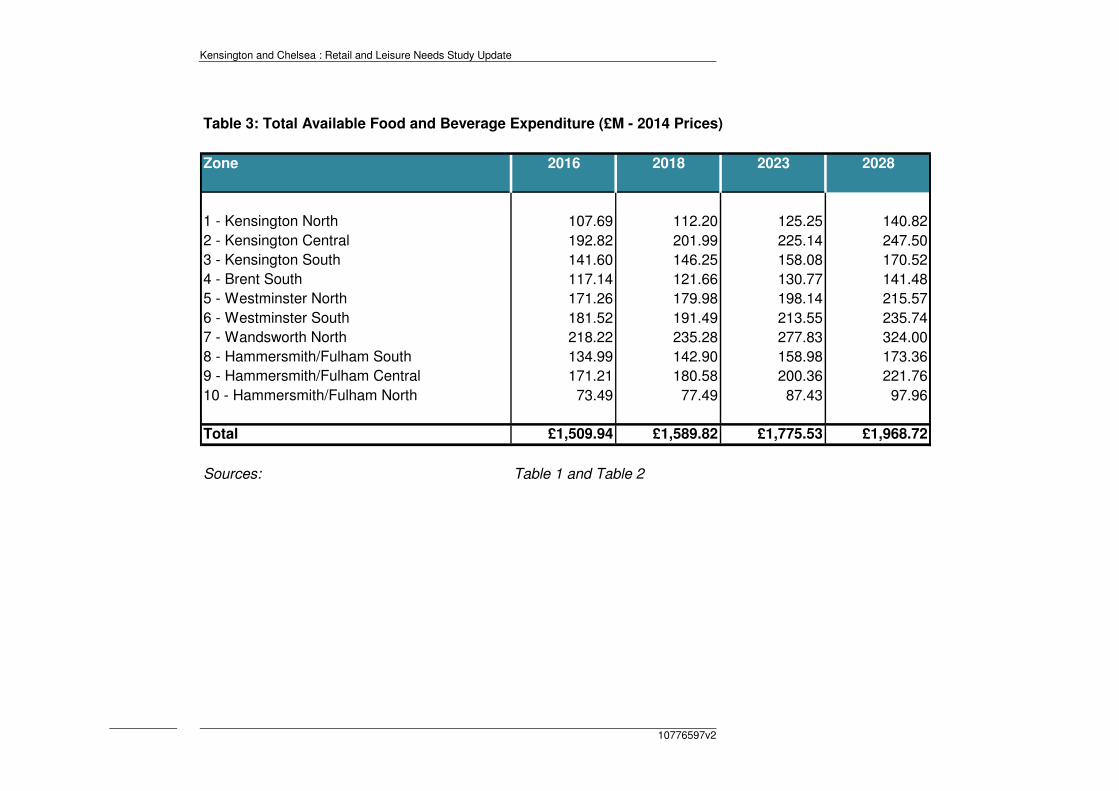

5. The total food and beverage expenditure in the study area is £1,510 million

at 2016. Food and beverage expenditure per capita is expected to increase in

real terms (excluding inflation) by 30% between 2016 and 2028. Taking into

account population growth, total food and beverage expenditure within the

study area is expected to increase from £1,510 million in 2016 to £1,969 million

in 2028 (Table 3 in Appendix 5).

4.6 Existing food and beverage expenditure patterns have been modelled based

on previous household survey results. The penetration rates are shown in

Table 4 in Appendix 5 and expenditure patterns are shown in Table 4. The

estimated expenditure currently attracted to facilities within Kensington and

Chelsea is £536 million in 2016.

4.7 Based on the estimate of food and beverage expenditure attracted to facilities

within the Borough, the average annual turnover of the 430 food and beverage

outlets in the main centres is over £1.1 million per outlet, with an average

turnover density of about £8,000 per sq.m gross, although the Goad floorspace

will exclude upper and basement floors.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P12 10776597v2

Future Food and Beverage Capacity

4.8 Available food and beverage expenditure has been projected forward to 2028

based on adjusted market shares in Tables 6 to 8 in Appendix 5. Existing

facilities are expected to increase their turnover by 1% per annum. Future

available expenditure is compared with the projected turnover of existing

facilities in Table 10 in Appendix 5.

4.9 Surplus expenditure has been converted into floorspace projections in Table

15 in Appendix 4, using an average sales density of £8,000 per sq.m for the

main centres and £5,000 per sq.m elsewhere, inflated by 1% per annum. The

floorspace projections are broken down in Table 4.1 below.

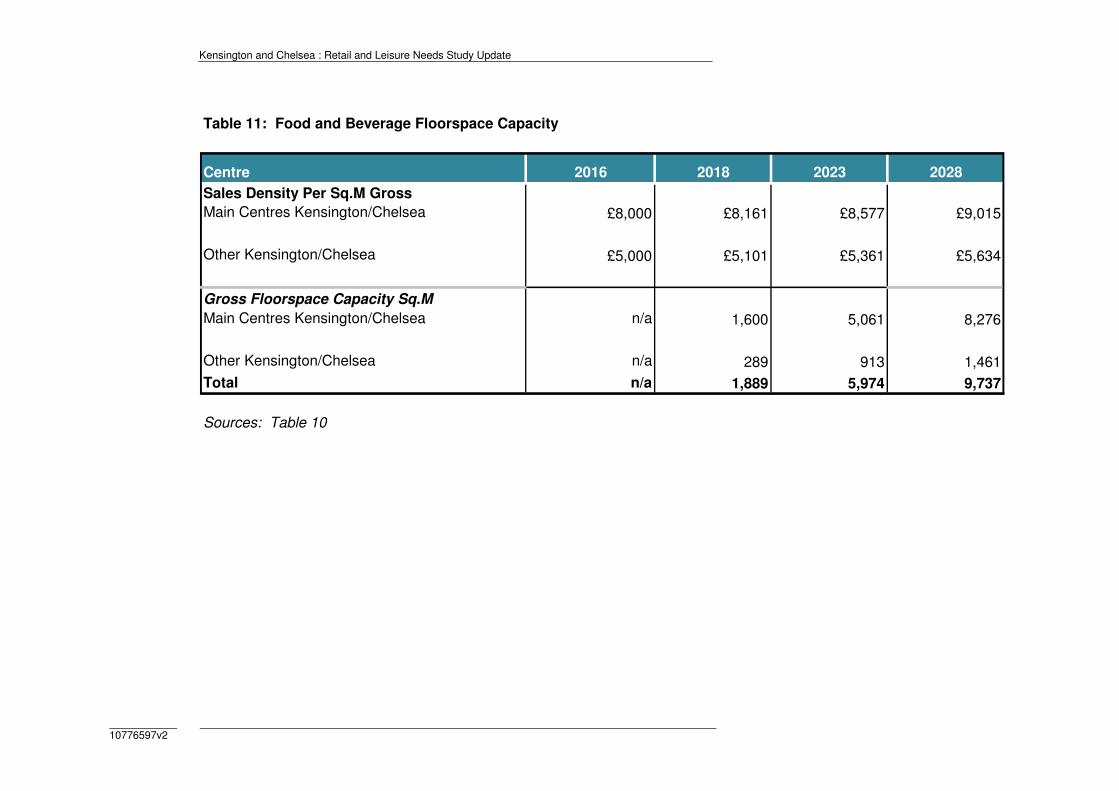

Table 4.1: Food and Beverage Floorspace Projections

Location By 2018

Sq.M Gross

By 2023

Sq.M Gross

By 2028

Sq.M Gross

Main centres 1,600 5,061 8,276

Other 289 913 1,461

Total 1,889 5,974 9,737

Source: Table 11 in Appendix 5

Commercial Leisure Uses

4.10 This section assesses the potential for commercial leisure uses including

cinema/multiplex, tenpin bowling, bingo, nightclubs and private health and

fitness clubs.

4.11 Residents in Kensington and Chelsea have good access to a range of

commercial leisure and entertainment, including facilities in neighbouring

boroughs and Central London. Most of the key sectors are represented.

Cinemas

4.12 There are 9 cinemas within Kensington and Chelsea including the two

Cineworld cinemas. The Odeon on Kensington High Street has recently

closed. The remaining cinemas provide 8 screens and 4,600 seats. Residents

in the Borough also have good access to a number of cinemas in Westminster.

4.13 The study area population in 2016 (156,000 people) will generate around

440,000 cinema trips per annum, based on the national average visitation rate

(2.8 trips per annum). Based on the national average population per cinema

screen (47,000 trips per screen), 440,000 trips generates demand for 9 cinema

screens. In terms of seats, the national average (230 trips per seat) suggests

440,000 trips could support around 1,900 seats. The existing cinemas in

Kensington and Chelsea have only 8 screens but 4,600 seats.

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P13

4.14 Based on national average visitation rates, Kensington and Chelsea’s

population at 2028 (167,000) would generate demand for 10 cinema screens

or 2,033 seats.

4.15 There is limited need for further cinema facilities within Kensington and

Chelsea.

Theatres

4.16 The main theatres in Kensington and Chelsea including the Chelsea Theatre,

Finborough Theatre, Gate Theatre and 20th Century Theatre. Accessibility to

theatres within Central London will have an impact on the likely demand for

theatre facilities in Kensington and Chelsea. If proposals emerge for new

theatres then these proposals could help to claw back theatre trips currently

attracted to Central London, or alternatively attract tourist visitors to Kensington

and Chelsea.

Health and Fitness Clubs

4.17 The UK health club market has expanded rapidly as public awareness about

personal fitness has increased. The value of the UK fitness market is now

around £4 billion. Private health clubs in the UK range from small independent

clubs to large operators such as Cannons, David Lloyd, Esporta, Fitness First,

Virgin Active, Bannatyne and LA Fitness. Public sector sports centres are also

important, and the market has increased significantly over the last 10 years.

4.18 The Sport England/Active Places data indicates there are 27 health and fitness

suites in the Borough, of which 5 are for private use only. These private uses

facilities are relatively small, with 96 fitness stations in total. There are 10

suites open to the general public with 478 fitness stations as shown below.

4.19 Kensington and Chelsea’s population is 156,000 in 2016, and the GLA’s

projections (2014 round ward projections) suggest population will grow to

167,000 by 2028. Kensington and Chelsea currently has 9.2 fitness stations

per 1,000 people (1,442 stations in total).

4.20 Greater London has 1,049 Sport England registered health and fitness suites

with 56,387 fitness stations (average of 53 stations per suite). This existing

provision equates to 6.4 fitness stations per 1,000 people in London.

4.21 If Kensington and Chelsea had the same provision per head of population as

the London average then the number of fitness stations would be only 1,003,

which implies an existing over-supply of 439 stations. This apparent over-

supply may be due in part a net in-commuting into the Borough.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P14 10776597v2

Table 4.1: Kensington and Chelsea Health and Fitness Clubs (Sport England/Active Places Data 2015)

4.22 On the basis that Kensington and Chelsea continues to provide 9.2 stations

per 1,000 people, the projected supply of fitness stations to meet future

demand would be 60 additional stations in 2023 or 99 additional stations in

2028 due to population. This equates to 1-2 new health and fitness suites over

the plan period.

Tenpin Bowling

4.23 There are no tenpin bowling facilities in Kensington and Chelsea. The nearest

facilities are at Queensway, Acton and Brentford.

4.24 Kensington and Chelsea’s population (156,000 in 2016) could theoretically

support 13 lanes, based on one lane per 12,000 people (national average).

The population at 2028 (167,500) could support 14 lanes.

4.25 There appears to be theoretical potential for a ten pin bowling facility within the

Borough, but operators’ space requirements may limit this opportunity.

Furthermore high land values in Kensington & Chelsea may make low density

tenpin bowling facilities unviable.

Name Type Fitness Stations

ANYTIME FITNESS (KENSINGTON) Registered Membership use 24

ANYTIME FITNESS (LONDON CHELSEA) Registered Membership use 31

AQUILLA HEALTH & FITNESS CENTRE Registered Membership use 30

BAGLIONI SPA Registered Membership use 7

BODYWORKS WEST AT LAMBTON PLACE Registered Membership use 50

CHELSEA ACADEMY Private Use 15

CHELSEA SPORTS CENTRE Pay and Play 55

DAVID LLOYD CLUB (KENSINGTON) Registered Membership use 171

EMOTION LEISURE Pay and Play 24

EQUINOX KENSINGTON Registered Membership use 100

FITNESS FIRST HEALTH CLUB (SOUTH KENSINGTON) Pay and Play 20

HER'S GYM & SPA Pay and Play 17

HOLLAND PARK SCHOOL Private Use 26

KENSINGTON GREEN GYM Private Use 18

KENSINGTON LEISURE CENTRE Pay and Play 120

KX GYM PRIVATE MEMBERS CLUB Registered Membership use 60

LAX (SOUTH KENSINGTON) Pay and Play 91

PORTOBELLO GREEN FITNESS CLUB Registered Membership use 90

SION-MANNING RC SCHOOL FOR GIRLS Private Use 12

SOHO GYMS (EARLS COURT) Pay and Play 62

ST CHARLES CATHOLIC SIXTH FORM COLLEGE Private Use 25

THE GYM WAY (KENSINGTON) Pay and Play 12

THE PEAK HEALTH CLUB & SPA Pay and Play 55

VIRGIN ACTIVE CLASSIC (THE KENSINGTON CLUB) Registered Membership use 130

VIRGIN ACTIVE CLUB (CHELSEA) Registered Membership use 66

VIRGIN ACTIVE CLUB (NOTTING HILL) Registered Membership use 109

WESTWAY SPORTS CENTRE Pay and Play 22

TOTAL 1442

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P15

Nightclubs/Live Music Venues

4.26 The value of the nightclub market is around £2 billion in 2014 with around

7,000 businesses (source: IBIS World), about one per 8,500 people.

Legislation that has extended licensing hours for other drinking establishments

and banned smoking indoors in public buildings has removed the industry's

main competitive advantage over pubs or bars. Nightclubs have also come

under pressure from the economic downturn.

4.27 The provision of nightclubs in Central London will limit the potential for major

new nightclubs in the Borough but small or medium nightclub facilities may be

viable.

Bingo

4.28 Mecca and Gala are the main bingo operators, controlling over half of the UK

market. Marketing of the bingo sector has been more proactive in recent years

and Gala and Mecca have invested in premises, moving out of dated premises

(i.e. converted cinemas) into purpose built units. Bingo clubs have become

increasingly sophisticated, and have actively sought to attract all age groups.

The bingo sector usually prefers central locations that are accessible by public

transport and by foot. Major bingo operators require buildings of between 2,000

- 3,000 sq.m, capable of seating up to 2,000 people, with a catchment

population of 50,000 to 70,000 within freestanding towns (source: BISL).

4.29 There are no major bingo facilities in Kensington and Chelsea. The adult (over

18) population of Kensington and Chelsea (approximately 129,000 in 2016)

could generate about 180,000 admissions based on the national participation

rate (1.4 trips per adult). Based on national average figures (133,000

admissions per club), the population of Kensington and Chelsea could support

one bingo hall.

4.30 There are currently no bingo clubs in the Borough and there is theoretical

scope for these types of facilities in the Borough. However the lack of available

sites or large premises and high land values/property prices may limit potential

in Kensington & Chelsea.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P16 10776597v2

5.0 Accommodating Future Growth

5.1 The sequential approach suggests that designated town centres should be the

first choice for retail and leisure development, which is supported by policies

within the London Plan. In Kensington & Chelsea the preferred location for

retail and leisure development needs to be carefully considered, particularly for

major development which may have an extensive catchment area. Major

development should be located within the International, Major and District

Centres, as suggested in the London Plan.

5.2 Some facilities will be needed to serve more localised catchment areas. Some

development will be more appropriate within local centres. All development

should be appropriate in terms of scale and nature to the centre in which it is

located.

5.3 The existing stock of premises may have a role to play in accommodating

projected growth. The capacity analysis in this report assumes that existing

retail floorspace can, on average, increase its turnover to sales floorspace

densities. A growth rate of 2% per annum is assumed for comparison

floorspace and 1% for food and beverage floorspace. In addition to the growth

in sales densities, vacant shops could help to accommodate future growth.

5.4 There were 201 vacant shop units within the main centres in Kensington and

Chelsea, a vacancy rate of about 8.8%, which is below the Goad national

average (11.8%). Vacant floorspace totals 25,770 sq.m gross. The number of

vacant units increased between 2008 to 2012 (157 to 2012).

5.5 Vacant premises should help to accommodate growth. For example, if the

current vacancy level fell from 8.8% to 5% (i.e. the target vacancy rate

envisaged in the RLNS 2008) then the reoccupation of 87 vacant properties

could be achieved. This reoccupied space could accommodate about 11,300

sq.m gross of commercial space. Based on existing vacancy levels, this

potential re-occupied space could be distributed as follows:

• Knightsbridge 4,900 sq.m gross;

• Kensington High Street 2,100 sq.m gross;

• Fulham Road (East/West) 1,500 sq.m gross;

• Portobello Road/Westbourne Grove 1,200 sq.m gross;

• King’s Road (East/West) 1,100 sq.m gross;

• Notting Hill Gate 500 sq.m gross.

5.6 If this reduction in vacant units can be achieved this would reduce the need for

new floorspace to be provided through development. The reoccupation of

vacant units will reduce the baseline Class A1 to A5 floorspace projection for

new development up to 2028 from 41,734 sq.m gross to 30,434 sq.m gross.

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P17

5.7 Vacant units could accommodate 74% of the retail floorspace projection up to

2023 (15,333 sq.m gross), and about 27% of the floorspace projection up to

2028 (41,734 sq.m gross).

5.8 These figures suggest that, in addition to the reoccupation of vacant

floorspace, major development sites may not be required to be implemented

until around 2022.

Potential Development Opportunities

5.9 A review of potential development sites was undertaken in the RLNS in 2008.

Sites in each centre were evaluated, in terms of their implications on the scope

and need for additional retail and leisure facilities in the Borough. In total 12

potential development sites were identified that could accommodate retail,

leisure or other town centre uses.

5.10 The RLNS 2008 indicated that many of the sites had constraints and their

availability for redevelopment was uncertain, with most of the sites in active

use. The sites most likely to deliver a significant net increase in retail, leisure or

other town use floorspace were:

• S1 – Chelsea Farmers Market (edge-of-centre – King’s Road East);

• S2 – The Clearings, Draycott Avenue (edge-of-centre - Fulham Road

East);

• S4 – Iranian Embassy (edge-of-centre – South Kensington);

• S5 – High Street Kensington Station (within centre – Kensington High

Street);

• S6 – Odeon Cinema/Post Office (edge-of-centre – Kensington High

Street);

• S7– LEB Depot, Victoria Gardens (edge-of-centre – Notting Hill Gate);

• S8 – Newcombe House (within centre – Notting Hill Gate);

• S9 – Telephone Exchange and TA Centre, Warwick Road (out-of-centre);

• S11 – Earl’s Court Exhibition Centre (edge-of-centre – Earl’s Court Road)

• S12 – Portobello Court Estate (edge-of-centre – Portobello Road).

5.11 The RLNS 2008 noted that if implemented the sites allocated for retail use in

the UDP/LDF at that time could deliver up to 9,000 sq.m gross of Class A use,

4,000 sq.m gross in the south part of the Borough and 5,000 sq.m gross in the

north/central part of the Borough.

5.12 If these opportunities are still available then they could accommodate about

22% of the floorspace projection up to 2028, and with reoccupied vacant

floorspace could accommodate nearly half of the floorspace projection.

Kensington and Chelsea : Retail and Leisure Needs Study Update

P18 10776597v2

6.0 Conclusions

6.1 This report provides an update of the Borough wide needs assessment for

retail and leisure development in Kensington and Chelsea and should be read

alongside the RLNS 2008. The conclusions of the analysis contained within

this study are summarised below.

Meeting Shopping and Leisure Needs

6.2 The NPPF states that local planning authorities should assess the quantitative

and qualitative needs for land or floorspace for retail and leisure development

over the plan period.

6.3 When planning for growth in their town centres, local planning authorities

should allocate a range of suitable sites to meet the scale and type of retail

development needed. It is important that the needs for retail and other main

town centre uses are met in full and not compromised by limited site

availability.

6.4 Long term forecasts beyond 2023 may be more susceptible to change, due to

unforeseen circumstances. Projected surplus expenditure beyond 2023 is

attributable to projected growth in spending per capita as well as population

growth. If the growth in expenditure is lower than that forecast then the scope

for additional space will reduce. Long term projections should be monitored

and kept under review. The implications of major developments surrounding

the Borough should also be monitored along with the affect proposals may

have on the demand for additional development in Kensington and Chelsea.

Class A Retail Floorspace Projections

6.5 The expenditure projections in this study take into account home shopping

made through non-retail businesses, because special forms of trading have

been excluded. The quantitative assessment of the potential capacity for new

retail floorspace suggests that there is scope for new retail development within

Kensington and Chelsea. The projections suggest new floorspace should be

distributed and phased as shown in Tables 6.1, 6.2 and 6.3 below.

Table 6.1: Comparison Goods Retail Floorspace Projections

Location Additional Retail Floorspace Sq.M Gross

2016-2018 2018-2023 2023-2028 Total 2016-2028

Main Centres South K&C 400 - 10,000 10,400

Main Centres Central K&C - - 8,900 8,900

Rest of K&C - 300 1,400 1,700

Total 400 300 20,300 21,000

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2 P19

Table 6.2: Convenience Goods Retail Floorspace Projections

Location Additional Retail Floorspace Sq.M Gross

2016-2018 2018-2023 2023-2028 Total 2016-2028

Main Centres 6,700 2,000 1,700 10,400

Local Centres 200 100 300 600

Total 6,900 2,100 2,000 11,000

Table 6.3: Food and Beverage (A3/A4/A5) Retail Floorspace Projections

Location Additional Retail Floorspace Sq.M Gross

2016-2018 2018-2023 2023-2028 Total 2016-2028

Main centres 1,600 3,500 3,200 8,300

Local Centres 300 600 500 1,400

Total 1,900 4,100 3,700 9,700

6.6 The revised retail capacity projections suggest there is scope for up to 41,700

sq.m gross Class A1 to A5 retail floorspace in Kensington & Chelsea Borough

as a whole by 2028, of which at least 11,300 sq.m gross could be

accommodated in vacant floorspace.

Commercial Leisure

6.7 Residents in Kensington and Chelsea have good access to a range of

commercial leisure and entertainment, including facilities in neighbouring

boroughs and Central London. Most of the key sectors are represented. The

Borough’s location close to the West End may limit the potential for further

commercial leisure and entertainment facilities. High land/property values in

the Borough may also make large format leisure uses commercially unviable

e.g. tenpin bowling and bingo clubs, despite the theoretical capacity for these

uses, unless they are part of a major mixed use development.

6.8 The existing cinema provision within and around the Borough suggests there is

limited potential for further cinema facilities up to 2028. There may be scope for

1-2 new health club facilities over the plan period due to population growth.

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2

Appendix 1 Study Area and Methodology

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2

Retail Capacity Methodology and Data

This section highlights the methodology and key assumptions adopted within

the retail update. The update broadly adopts the approach within the

Kensington & Chelsea Retail and Leisure Needs Study 2008 (RLNS 2008).

Study Area and Population

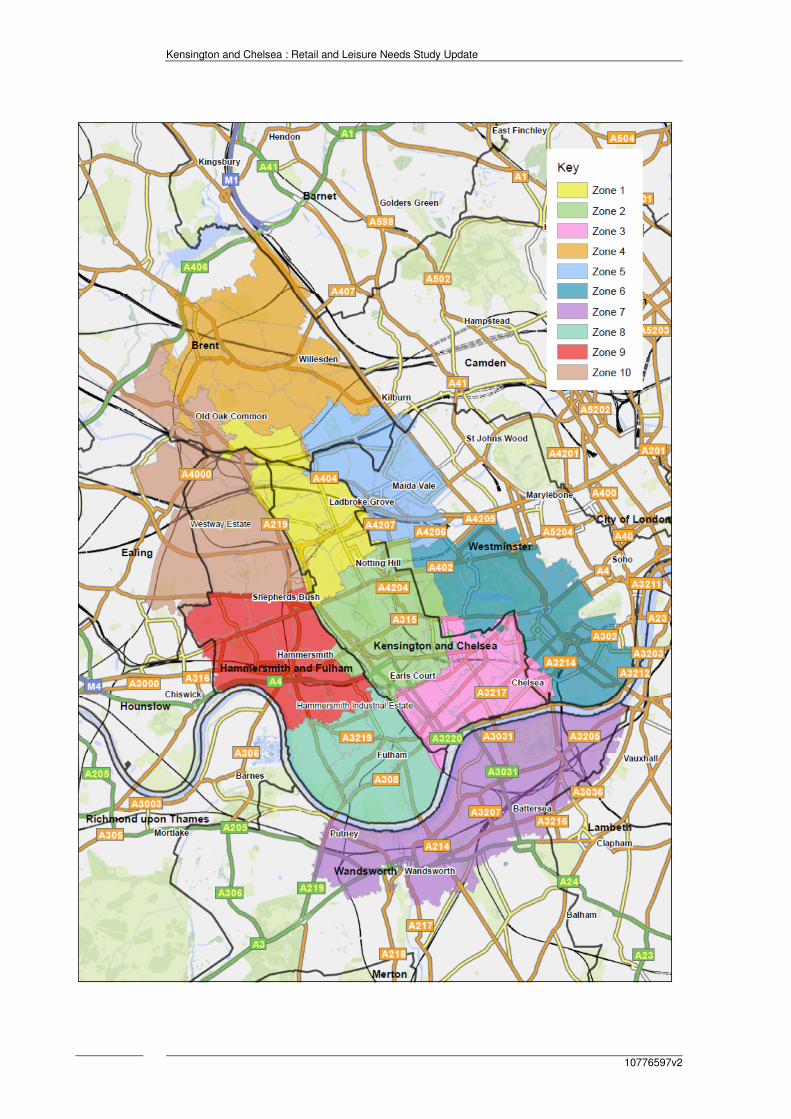

RLNS 2008 adopted a study area based on 10 sub-zones. The study includes

all parts of Kensington & Chelsea Borough and parts of neighbouring boroughs,

where the primary catchment areas of main centres extend beyond

administrative boundaries.

The RLNS 2008 adopted 2001 Census based population projections for the

postcode sector based zones. Population has been updated based on 2011

Census data and the GLA’s latest ward level population projections to 2028

(2014 round ward population projections – SHLAA based), as shown in Table 1

in Appendix 3.

The RLNS 2008 suggested the study area population would grow to around

726,000 in 2015. The revised projection for 2015 is now higher (+4.7%) at

around 760,000. The RLNS 2008 projected the study area population would

increase to about 756,000 in 2028. The revised projection for 2028 is about

844,000. Population growth is much higher due in part to major growth at

Vauxhall Nine Elms Battersea in Zone 7 in LB Wandsworth and potentially

growth at Earls Court in Zone 2.

Retail Expenditure Data

All monetary values expressed in this study are at 2014 prices, consistent with

Experian's base year expenditure figures for 2014 (Retail Planner Briefing Note

13, October 2015) which is the most up to date information available.

The level of available expenditure to support retailers is based on first

establishing per capita levels of spending for the study area population.

Experian's local consumer expenditure estimates for comparison and

convenience goods for each of the study area zones for the year 2014 have

been obtained.

Experian's EBS national expenditure information (Experian Retail Planner

Briefing Note 13) has been used to forecast expenditure within the study area.

Experian's forecasts are based on an econometric model of disaggregated

consumer spending. This model takes a number of macro-economic forecasts

(chiefly consumer spending, incomes and inflation) and uses them to produce

forecasts of consumer spending volumes, prices and value, broken down into

separate categories of goods. The model incorporates assumptions about

income and price elasticities.

Experian's EBS growth forecast rates for 2014 to 2017 reflect the current

economic circumstances and provide an appropriate growth rate for the short

term (for convenience goods: -0.2% for 2014 to 2015, +0.1% for 2015 to 2016

Kensington and Chelsea : Retail and Leisure Needs Study Update

10776597v2

and +0.3% for 2017; for comparison goods: +5.3% for 2014-2015, +3.2% for

2015-2016 and +2.9% for 2017.

In the longer term it is more difficult to forecast year on year changes in

expenditure. Experian's longer term growth average forecasts have been

adopted i.e. 0.1% per annum for convenience goods after 2016 and 3% per

annum growth for comparison goods. These growth rates are relatively cautious

when compared with past growth rates, but in our view represent realistic

forecast for future growth. These growth figures relate to real growth and

exclude inflation.

Special Forms of Trading (SFT) or non-store activity is included within

Experian's Goods Based Expenditure (GBE) estimates. SFT includes other

forms of retail expenditure not spent in shops e.g. mail order sales, some

internet sales, vending machines, party plan selling, market stalls and door to

door selling. SFT needs to be excluded from retail assessments because it

relates to expenditure not spent in shops and does not have a direct

relationship with the demand for retail floorspace. The growth in home

computing, internet connections and interactive TV may lead to a growth in

home shopping and may have effects on retailing in the high street. Experian