Embed Size (px)

Citation preview

CIRCULAR DATED 10 APRIL 2012 THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. PLEASE READ IT CAREFULLY. If you are in any doubt about this Circular or the action you should take, you should consult your stockbroker, bank manager, solicitor, accountant, tax adviser or other professional adviser immediately. If you have sold or transferred all your shares in Kencana Agri Limited (the “Company”) held through The Central Depository (Pte) Limited (“CDP”), you need not forward this Circular to the purchaser or transferee as arrangements will be made by CDP for a separate Circular to be sent to the purchaser or transferee. If you have sold or transferred all your shares represented by physical share certificate(s), you should at once hand this Circular to the purchaser or transferee or to the bank, stockbroker or agent through whom you effected the sale or transfer, for onward transmission to the purchaser or transferee. The Singapore Exchange Securities Trading Limited (the “SGX-ST”) assumes no responsibility for the correctness of any of the statements made, reports contained or opinions expressed in this Circular.

KENCANA AGRI LIMITED (Incorporated in the Republic of Singapore)

(Company Registration Number: 200717793E)

CIRCULAR TO SHAREHOLDERS

In relation to

THE PROPOSED INTERESTED PERSON TRANSACTIONS

Independent Financial Adviser to the Independent Directors of the Company

PROVENANCE CAPITAL PTE. LTD.

(Incorporated in the Republic of Singapore) (Company Registration Number: 200309056E)

IMPORTANT DATES AND TIMES:- Last date and time for lodgment of Proxy Form : 24 April 2012 at 4.00 p.m. Date and time of Extraordinary General Meeting : 26 April 2012 at 4.00 p.m. or immediately after the

conclusion of the Annual General Meeting to be held at 3.00 p.m. on the same day and at the same place (or the adjournment thereof)

Place of Extraordinary General Meeting : Coleman Room, Level 1 Grand Park City Hall 10 Coleman Street Singapore 179809

TABLE OF CONTENTS DEFINITIONS ........................................................................................................................................................ 1

1. INTRODUCTION .................................................................................................................................... 4

2. INFORMATION ON THE CONTRACTING PARTIES ...................................................................... 5

3. INFORMATION ON ASP AND BWS................................................................................................... 5

4. INTERESTED PERSON TRANSACTIONS UNDER CHAPTER 9 OF THE LISTING MANUAL.................................................................................................................................. 6

5. INFORMATION ON THE CONTRACTS............................................................................................. 8

6. REVIEW PROCEDURES.................................................................................................................... 17

7. INDEPENDENT FINANCIAL ADVISER’S OPINION ...................................................................... 17

8. VIEWS OF THE AUDIT COMMITTEE AND DIRECTORS’ RECOMMENDATION ................... 17

9. INTEREST OF DIRECTORS AND CONTROLLING SHAREHOLDERS .................................... 18

10. EXTRAORDINARY GENERAL MEETING....................................................................................... 19

11. ACTION TO BE TAKEN BY SHAREHOLDERS.............................................................................. 19

12. DIRECTORS’ RESPONSIBILITY STATEMENT ............................................................................. 19

13. CONSENT OF THE IFA ...................................................................................................................... 20

14. DOCUMENTS AVAILABLE FOR INSPECTION ............................................................................. 20

APPENDIX A: LETTER FROM PROVENANCE CAPITAL PTE. LTD. TO THE INDEPENDENT DIRECTORS OF KENCANA AGRI LIMITED IN RESPECT OF THE INTERESTED PERSON TRANSACTIONS ..................................................................... 21

NOTICE OF EXTRAORDINARY GENERAL MEETING .............................................................................. 40

PROXY FORM .................................................................................................................................................... 41

DEFINITIONS

DEFINITIONS

1

Except where the context otherwise requires, the following definitions apply throughout this Circular: DEFINITIONS

General “Agreement” : Shall have the meaning ascribed to it in

paragraph 1.1 of this Circular “associate” : Has the meaning given to it in Section 4.1.1 of

this Circular “associated companies” : Companies in which at least 20.0% but not more

than 50.0% of its shares are held by the Company or the Group

“Audit Committee” : The audit committee of the Board “Board” or “Board of Directors” : The board of directors of the Company “Circular” : This circular to Shareholders dated 10 April 2012 “Companies Act” : The Companies Act, Chapter 50 of Singapore,

and any regulations made pursuant thereto “Contracting Parties” : PT Sawit Permai Lestari and PT Wira Palm

Mandiri “Contracts” : The Land Clearing and Infrastructure Contracts,

FFB Transportation Contracts and Oil Transportation Contracts collectively

“CPF” : Central Provident Fund “CPKO” : Crude palm kernel oil “CPO” : Crude palm oil “DBP” : has the meaning given in Section 5.1.5 of this

Circular “Director(s)” : A director of the Company as at the date of this

Circular “EGM” : Extraordinary general meeting to be convened

and held on 26 April 2012 “FFB” : Fresh fruit bunch “FFB Transportation Contracts” : has the meaning given in Section 1.1.2 of this

Circular “FFB Transportation Services” : has the meaning given in Section 5.2 of this

Circular “Group” : means the Company and its subsidiaries and

associated companies “FY” : Financial year ended or ending 31 December, as

the case may be

DEFINITIONS

2

“IFA Letter” : Has the meaning given to it in Section 7 of this Circular

“immediate family” : Has the meaning given to it in Section 4.1.1 of

this Circular “Independent Directors” : The Directors who are independent for the

purposes of considering the Contracts, being Tengku Alwin Aziz, Mr Kent Surya, Mr Soh Yew Hock, Mr Leung Yew Kwong, Mr Teo Kim Yong, Mr Ang Kok Min and Mr Sim Idrus Munandar

“Independent Shareholders” : Shareholders other than members of the

Maknawi Family and their respective associates and Shareholders who are also interested in BWS

“Independent Financial Adviser” : Provenance Capital Pte. Ltd. “Interested Person(s)” : ASP and BWS “Land Clearing and Infrastructure Activities” : has the meaning given in Section 5.1.1 of this

Circular “Land Clearing and Infrastructure Contract” : has the meaning given in Section 1.1.1 of this

Circular “Latest Practicable Date” : 2 April 2012 “Listing Manual” : The Listing Manual of the SGX-ST, as may be

amended, varied or supplemented from time to time

“Maknawi Family” : Mr Henry Maknawi and his immediate family “Oil Transportation Contracts” : has the meaning given in Section 1.1.2 of this

Circular “Oil Transportation Services” : has the meaning given in Section 5.3 of this

Circular

“Service Providers” : has the meaning given in Section 3.2 of this Circular

“Shareholder(s)” : Registered holders of Shares, except that where

the registered holder is CDP, the term “Shareholders” shall, in relation to such Shares, mean the Depositors whose Securities Account are credited with Shares

“Shares” : Ordinary shares in the share capital of the

Company “subsidiary” : Shall have the meaning ascribed to it in the

Companies Act as amended from time to time

DEFINITIONS

3

“Substantial Shareholder” : A person who holds directly or indirectly 5.0% or more of the total issued share capital of the Company

Other Corporations or Agencies “ASP” : PT Alamindo Sejahtera Persada “BWS” : PT Berkat Wahana Sukses “CDP” : The Central Depository (Pte) Limited “PT Pertamina” : PT Pertamina (Persero) “SGX-ST” : Singapore Exchange Securities Trading Limited Currencies, Units and Others “km” : Kilometre “MT” : Metric tonnes “Rp” : Indonesian Rupiah, the legal currency of

Indonesia “S$” : Singapore dollars, the legal currency of the

Republic of Singapore “US$” : United States dollars, the legal currency of the

United States of America “%” : Per centum or percentage The terms “Depositor”, “Depository Agent” and “Depository Register” shall have the meanings ascribed to them respectively in Section 130A of the Companies Act. Words importing the singular shall, where applicable, include the plural and vice versa, and words importing the masculine gender shall, where applicable, include the feminine and neuter genders. References to persons shall, where applicable, include corporations. Any reference in this Circular to any enactment is a reference to that enactment as for the time being amended or re-enacted. Any word defined in the Companies Act, the Listing Manual or any statutory modification thereof and used in this Circular shall, where applicable, have the meaning assigned to it under the Companies Act, the Listing Manual or such statutory modification, as the case may be, unless the context otherwise requires. Any reference to a time of day in this Circular shall be a reference to Singapore time, unless otherwise stated. The figures in Rp which are expressed in US$ (and vice-versa) are expressed based on the exchange rate of Rp 8,776: US$1.00, being the average exchange rate between Rp and US$ for the year ended 31 December 2011. Such conversions are provided solely for the purposes of presentation.

LETTER TO SHAREHOLDERS

4

LETER TO SHAREHOLDERS KENCANA AGRI LIMITED (Incorporated in the Republic of Singapore)

(Company Registration Number: 200717793E)

Directors:- Registered Office:- Mr Henry Maknawi, Chairman and Chief Executive Officer Tengku Alwin Aziz, Vice-Chairman and Non-Executive Director Ms Ratna Maknawi, Deputy Chief Executive Officer Mr Kent Surya, Finance Director Mr Soh Yew Hock, Lead Independent Director Mr Leung Yew Kwong, Independent Director Mr Teo Kim Yong, Non-Executive Director Mr Ang Kok Min, Alternate Director to Mr Teo Kim Yong Mr Sim Idrus Munandar, Independent Director

36 Armenian Street #03-02 Singapore 179934

10 April 2012 To: Shareholders of Kencana Agri Limited Dear Sir / Madam PROPOSED INTERESTED PERSON TRANSACTIONS 1. INTRODUCTION 1.1. On 9 April 2012, the Company announced that PT Sawit Permai Lestari and PT Wira Palm

Mandiri, both subsidiaries of the Company, have entered into separate conditional agreements with: 1.1.1. ASP, pursuant to which ASP shall provide land clearing and infrastructure

construction services to the Contracting Parties and their subsidiaries (the “Land Clearing and Infrastructure Contracts”); and

1.1.2. BWS, pursuant to which:

(a) BWS shall provide FFB transportation and logistics services to the Contracting Parties and their subsidiaries (the “FFB Transportation Contracts”); and

(b) BWS shall provide CPO and CPKO transportation and logistics services to the Contracting Parties and their subsidiaries (the “Oil Transportation Contracts”).

The services to be provided by ASP and BWS under the Contracts are similar to the services that they currently provide to the Group on an ongoing basis.

1.2. The total value of the Group’s transactions with ASP and BWS for the financial year ended 31

December 2011 did not exceed the thresholds set out in Rule 906 of the Listing Manual. However, as ASP and BWS are associates of Mr Henry Maknawi (the Chairman and Chief Executive Officer and a controlling shareholder of the Company) and the total value of the transactions to be carried out pursuant to the Contracts could exceed 5% of the Group’s latest audited net tangible assets and constitute “interested person transactions” within the meaning of Chapter 9 of the Listing Manual, in the interests of transparency and good corporate governance, the Company is seeking the approval of Independent Shareholders in respect of the Contracts at an EGM to be convened. The purpose of this Circular is therefore to provide Shareholders with information relating to the Contracts and to seek approval for the same at the EGM.

LETTER TO SHAREHOLDERS

5

2. INFORMATION ON THE CONTRACTING PARTIES

The Contracting Parties are both subsidiaries of the Company. They are principally investment holding companies that hold the Group’s operating plantation subsidiaries. They are also engaged in the wholesale trading of plantation related products.

3. INFORMATION ON ASP AND BWS

3.1. About ASP ASP is a private company incorporated under the laws of Indonesia and domiciled in West Jakarta, with its registered address at Taman Harapan Indah Blok K No. 21A, Jelambar Baru, West Jakarta, Indonesia. ASP has been engaged in the business of providing land clearing services and construction of basic infrastructure such as roads and bridges, and is one of such contractors engaged by the Group on an ongoing basis since its incorporation in 2010. The Group started contracting the services of ASP in 2011. Upon the listing of the Company on the Official List of the SGX-ST, the Group embarked on a series of expansion plans. In order to expand its plantations and to increase its planting of new oil palm trees, the Group needed the services of reliable land clearing contractors to clear uncultivated land and to construct basic infrastructure such as roads and bridges. In the course of implementing its expansion plans, the Group encountered increasing difficulty in sourcing for suitable land clearing contractors who were reliable, financially sound, flexible and adaptable enough for the Group’s operating environment. The shortage of suitable land clearing contractors would hinder the pace of the Group’s expansion plans, especially in some of the Group’s new estates in certain parts of Indonesia, such as Sulawesi. Thus, to address these concerns and to give the Group access to a wider pool of reliable contractors, ASP was established to readily support the expansion plans of the Group and to ensure that the Group will always have access to the services of a dedicated land clearing contractor. As at the Latest Practicable Date, the entire share capital of ASP is owned by PT Alam Semesta Permai (60%) and PT Geo Andalan Buana (40%). PT Alam Semesta Permai is in turn owned by Mr Johan Maknawi (25%), Mr Eddy Maknawi (25%), Ms Jeanny Maknawi (25%) and Mr Albert Maknawi (25%), members of Mr Henry Maknawi’s immediate family. PT Geo Andalan Buana is a party unrelated to the Group or the Maknawi Family. ASP is managed by the management team from PT Geo Andalan Buana, which has extensive experience in the business of land clearing and construction of infrastructure. For the financial year ended 31 December 2011, the aggregate value of transactions entered into between the Group and ASP amounted to approximately US$4.0 million (excluding transactions below S$100,000).

3.2. About BWS BWS is a private company incorporated under the laws of Indonesia and domiciled in West Jakarta, with its registered address at Taman Surya Blok CC/11 RT. 017/02, Kel. Wijaya Kusuma, Kec. Grogol Petamburan, Jakarta Barat, Indonesia. BWS provides land-based transportation and logistics services to the Group on an exclusive basis. As disclosed in the Company’s prospectus dated 17 July 2008, prior to the listing of the Company, the Group had entered into an informal arrangement with Mr Henry Maknawi, Ms Ratna Maknawi and certain employees of the Group (“the Service Providers”) for the provision of transportation services to the Group. The arrangement was formalised when the Service Providers incorporated BWS to provide the transportation services to the Group. As the Group continues to expand, the Group intends to continue engaging the services of BWS

LETTER TO SHAREHOLDERS

6

due to their competitiveness, reliability, flexibility and ability to adapt to the Group’s operating environment. As at the Latest Practicable Date, the shareholders of BWS are Mr Henry Maknawi (28%), Ms Ratna Maknawi (29.5%), and certain former and existing employees of the Group who collectively own 42.5% of BWS. None of these employees are directors of the Company or any of its subsidiaries. The shareholders of BWS are not engaged in the management of BWS, which is managed by experienced third party employees independent of the Group. For the financial year ended 31 December 2011, the aggregate value of the transactions entered into between the Group and BWS amounted to approximately US$1.7 million (excluding transactions below S$100,000).

4. INTERESTED PERSON TRANSACTIONS UNDER CHAPTER 9 OF THE LISTING MANUAL

4.1. Chapter 9 of the Listing Manual

4.1.1. Background

Chapter 9 of the Listing Manual governs transactions in which a listed company or any of its subsidiaries or associated companies (known as an “entity at risk”) enters into or proposes to enter into with a party who is an interested person of the listed company. The purpose is to guard against the risk that interested persons could influence the listed company, its subsidiaries or associated companies to enter into transactions with it that may adversely affect the interests of the listed company or its shareholders.

For the purposes of Chapter 9 of the Listing Manual:-

(a) an “entity at risk” means:-

(i) the listed company;

(ii) a subsidiary of the listed company that is not listed on the SGX-ST or

an approved exchange; or

(iii) an associated company of the listed company that is not listed on the SGX-ST or an approved exchange, provided that the listed company and/or its subsidiaries (the “listed group”), or the listed group and its interested person(s), has control over the associated company;

(b) in the case of a company, an “interested person” means a director, chief

executive officer or controlling shareholder of the listed company or an associate of such director, chief executive officer or controlling shareholder;

(c) in the case of a company, an “associate”:-

(i) in relation to any director, chief executive officer, substantial

shareholder or controlling shareholder (being an individual) includes an “immediate family” member (that is, the spouse, child, adopted-child, step-child, sibling or parent) of such director, chief executive officer, substantial shareholder or controlling shareholder, the trustees of any trust of which the director/his immediate family, the chief executive officer/ his immediate family, the substantial shareholder/his immediate family or controlling shareholder/his immediate family is a beneficiary or, in the case of a discretionary trust, is a discretionary

LETTER TO SHAREHOLDERS

7

object, and any company in which the director/his immediate family, the chief executive officer/his immediate family, the substantial shareholder/ his immediate family or controlling shareholder/his immediate family has or have an aggregate interest (directly or indirectly) of 30.0% or more; and

(ii) in relation to a substantial shareholder or a controlling shareholder

(being a company) means any other company which is its subsidiary or holding company or is a subsidiary of such holding company or one in the equity of which it and/or such other company or companies taken together (directly or indirectly) have an interest of 30.0% or more;

(d) an “approved exchange” means a stock exchange that has rules which

safeguard the interests of shareholders against interested person transactions according to similar principles to Chapter 9 of the Listing Manual; and

(e) an “interested person transaction” means a transaction between an entity

at risk and an interested person, and includes the provision or receipt of financial assistance, the acquisition, disposal or leasing of assets, the provision or receipt of services, the issuance or subscription of securities, the granting of or being granted options, and the establishment of joint ventures or joint investments, whether or not in the ordinary course of business, and whether or not entered into directly or indirectly.

4.1.2. Financial Thresholds

An immediate announcement and/or shareholders’ approval would be required in respect of transactions with interested persons if the value of the transaction is equal to or exceeds certain financial thresholds.

In particular, an immediate announcement is required where:-

(a) the value of a proposed transaction is equal to or exceeds 3.0% of the listed

group’s latest audited consolidated net tangible assets (“Threshold 1”); or

(b) the aggregate value of all transactions entered into with the same interested person during the same financial year, is equal to or more than Threshold 1. In this instance, an announcement will have to be made immediately of the latest transaction and all future transactions entered into with that same interested person during the financial year.

Shareholders’ approval is required where:-

(a) the value of a proposed transaction is equal to or exceeds 5.0% of the listed

group’s latest audited consolidated net tangible assets (“Threshold 2”); or

(b) the aggregate value of all transactions entered into with the same interested person during the same financial year, is equal to or more than Threshold 2. The aggregation will exclude any transaction that has been approved by shareholders previously, or is the subject of aggregation with another transaction that has been previously approved by shareholders.

Pursuant to Rule 909 of the Listing Manual, the value of a transaction is the amount at risk to the issuer. This is illustrated by the following examples:-

LETTER TO SHAREHOLDERS

8

(a) in the case of a partly-owned subsidiary or associate company, the value of the transaction is the issuer’s effective interest in that transaction;

(b) in the case of a joint venture, the value of the transaction includes the equity

participation, shareholders’ loans and guarantees given by the entity at risk; and

(c) in the case of borrowing of funds from an interested person, the value of the

transaction is the interest payable on the borrowing. In the case of lending of funds to an interested person, the value of the transaction is the interest payable on the loan and the value of the loan.

5. INFORMATION ON THE CONTRACTS 5.1. The Land Clearing and Infrastructure Contracts

Under the Land Clearing and Infrastructure Contracts, the Contracting Parties and ASP agreed to a framework pursuant to which the Contracting Parties and/or any of their subsidiaries may contract the services of ASP for the purposes of clearing uncultivated land and constructing basic infrastructure in order to prepare the Group’s unutilised land banks for cultivation of new oil palm estates at the agreed locations. Based on the terms of the Land Clearing and Infrastructure Contracts and the Group’s present expansion and planting plans, the Group estimates that the aggregate value of the transactions with ASP at these locations pursuant to the Land Clearing and Infrastructure Contracts could be in the range of US$20 million to US$30 million over the five (5) year term of the contracts, barring the occurrence of unforeseen circumstances. 5.1.1. Scope of work

The Contracting Parties and/or their subsidiaries may contract the services of ASP to undertake land clearing and construction works, including: (a) clearing of underbrush and felling of trees;

(b) terrace contouring;

(c) construction and maintenance of drains;

(d) construction of roads; and

(e) construction of bridges, at certain agreed locations (the “Land Clearing and Infrastructure Activities”).

5.1.2. Agreed locations The Land Clearing and Infrastructure Activities shall be undertaken at the following estates owned or controlled by the Contracting Parties or their subsidiaries: (a) Bualemo, Banggai, Central Sulawesi, Indonesia; (b) Batui, Banggai, Central Sulawesi, Indonesia; (c) Pohuwato, Gorontalo, Indonesia; and

(d) Bulungan, East Kalimantan, Indonesia.

LETTER TO SHAREHOLDERS

9

As at 31 December 2011, the Group has the right to cultivate approximately 66,461 ha (subject to final measurement by the relevant authorities) of land at these locations, of which the Group estimates that approximately 50% to 60% of the land banks may be available for land clearing and construction of necessary infrastructure. The Contracting Parties and their subsidiaries intend to engage the services of ASP as one of the contractors for the Land Clearing and Infrastructure Activities at parts of the land banks mentioned above.

5.1.3. Term of contract

The Land Clearing and Infrastructure Contracts shall have a term of five (5) years. 5.1.4. Base prices

The Land Clearing and Infrastructure Contracts set out an agreed list of base prices for each unit of the various services to be provided by ASP. The base prices were arrived at on a willing buyer willing seller basis, with reference to independent third party quotes obtained by the Group where available, and taking into account internal price analysis, past transactions with ASP and all relevant factors. The base prices applicable to the different locations may vary due to differences in factors which affect the cost of working at the different locations, such as the remoteness of the location, the nature of the terrain and the logistics costs. The base prices are also subject to certain adjustment mechanisms, which are described in Section 5.1.5 below. Shareholders may refer to the Land Clearing and Infrastructure Contracts for the full list of base prices, which are available for inspection at the registered office of the Company.

5.1.5. Adjustment to base prices

(a) Adjustment for fluctuation in DBP The base prices set out in the Land Clearing and Infrastructure Contracts also take into account the base price of diesel (“DBP”), which was initially fixed at Rp 9,500 per litre. Due to the volatility in the price of diesel and the fact that the cost of diesel represents an important factor in the operating cost of performing the Land Clearing and Infrastructure Activities, the parties have agreed to allow for agreed fixed adjustments to the base prices of the land clearing services for every fluctuation in the DBP of an amount of Rp 250 per litre (whether higher or lower than Rp 9,500 per litre). The value of DBP is benchmarked against the price of diesel as announced by PT Pertamina at the beginning of each month. The applicable DBP for each month shall be determined by the Contracting Parties with reference to the price of diesel as announced by PT Pertamina. The table of agreed adjustments to the base prices of the Land Clearing and Infrastructure Services is also set out in the Land Clearing and Infrastructure Contracts.

(b) Annual base price review The Contracting Parties and ASP may request for a review of the base prices on an annual basis to take into account factors such as the effects of inflation, increase in wages and adjustments to market prices for similar work. Any

LETTER TO SHAREHOLDERS

10

upward or downward price adjustment pursuant to the annual base price review shall not in any case exceed 10% of the base prices for the preceding year and shall be subject to the review and prior approval of the Audit Committee. For the avoidance of doubt, adjustments made due to fluctuations in DBP are separate from and do not count towards the 10% maximum permissible adjustment to the base prices.

5.1.6. Contract Basis

The Land Clearing and Infrastructure Contracts provide the framework under which the Contracting Parties or their subsidiaries may engage the services of ASP for specific Land Clearing and Infrastructure Activities at the various agreed locations. This arrangement was put in place to allow the Group to control the pace at which its uncultivated land banks are cleared to meet its needs for new estates. The Contracting Parties or any of their subsidiaries may engage the services of ASP under the Land Clearing and Infrastructure Contracts on a contract basis by signing a confirmation letter, which will set out the specific terms of each job order, such as the precise location to be cleared, the area involved (in hectares), the type of land clearing and infrastructure services required for the location, the timeline to completion of the job and other material information required to make an assessment of the scope of the work requested by the Group. Acceptance by ASP of the terms set out in the confirmation letter will formalise and confirm the job order.

5.1.7. Payment Terms Payment shall be made on a monthly basis, where 90% of the fees payable in respect of the work done each month shall be paid within four (4) weeks of receipt of a valid invoice supported by an job completion report prepared by ASP and agreed by the Group. The remaining 10% of the fees payable each month (“Monthly Retention Payments”) shall be retained by the Group and the monthly retention amounts shall be aggregated and paid in one lump sum 30 days after final payment is made for the specific job order.

5.1.8. Contractor’s Reimbursement If the Group determines that any of the Land Clearing and Infrastructure Activities performed by ASP has been unsatisfactory, the Group may engage independent third party contractors to correct and/or complete the work done by ASP. ASP shall compensate the Group in full for the difference between the total amount incurred by the Group in respect of the services required under a particular job order (including the fees paid to ASP and the independent third party contractor) and the amount it would have paid to ASP under the Land Clearing and Infrastructure Contracts for those works.

5.1.9. Compensation

In the event that ASP is unable to perform the Land Clearing and Infrastructure Activities under a specific job order made by the Contracting Parties due to the inaccessibility of land specified under that job order arising from social issues amongst the local inhabitants which prohibits the performance of the Land Clearing and Infrastructure Activities, the Group shall be liable to compensate ASP for the idle period, based on the opportunity cost to ASP for the idle equipment and manpower. Such compensation shall not in any event exceed the remaining contract value of that particular job order. The amount of compensation payable in each instance shall be subject to the review and prior approval of the Audit Committee.

LETTER TO SHAREHOLDERS

11

5.1.10. Termination The Group may in its absolute discretion choose to terminate the Land Clearing and Infrastructure Contracts upon the occurrence of certain agreed events, such as a material change in economic conditions, breach of contract or negligence on the part of ASP. The Group shall be entitled to forfeit any Monthly Retention Payments accrued and unpaid up to the termination of the Land Clearing and Infrastructure Contract(s), save in the case of termination due to material changes in economic conditions. The Land Clearing and Infrastructure Contracts do not provide for termination at the discretion of ASP.

5.2. The FFB Transportation Contracts Under the FFB Transportation Contracts, the Contracting Parties and BWS agreed to a framework pursuant to which the Contracting Parties and/or any of their subsidiaries may contract the services of BWS for the purposes of transporting FFB within certain oil palm plantations owned and/or controlled by the Contracting Parties and their subsidiaries (the “FFB Transportation Services”). As stated above, the Group has been contracting the FFB Transportation Services of BWS on a continuing basis for over 10 years. 5.2.1. Agreed Locations

The FFB Transportation Services shall be undertaken at the following estates owned and/or controlled by the Contracting Parties or their subsidiaries: (a) Bangka, Bangka Belitung, Indonesia; (b) Kotabaru, South Kalimantan, Indonesia; (c) Paser, East Kalimantan, Indonesia; and (d) Kutai, East Kalimantan, Indonesia.

5.2.2. Term of contract

The FFB Transportation Contracts shall have a term of five (5) years. 5.2.3. Pricing

The fees payable for the FFB Transportation Services shall be determined in accordance with the following formula: (base price + DBP adjustment (if any) + loading fees) x weight of FFB delivered (MT) (a) Base prices

The FFB Transportation Contracts set out an agreed list of base prices for the transportation of FFB between designated blocks within the Group’s oil palm plantations to its CPO mills. The base prices include the cost of diesel, and were arrived at on a willing buyer willing seller basis, with reference to independent third party quotes obtained by the Group, and taking into account internal cost analysis, past transactions with BWS and all relevant factors.

LETTER TO SHAREHOLDERS

12

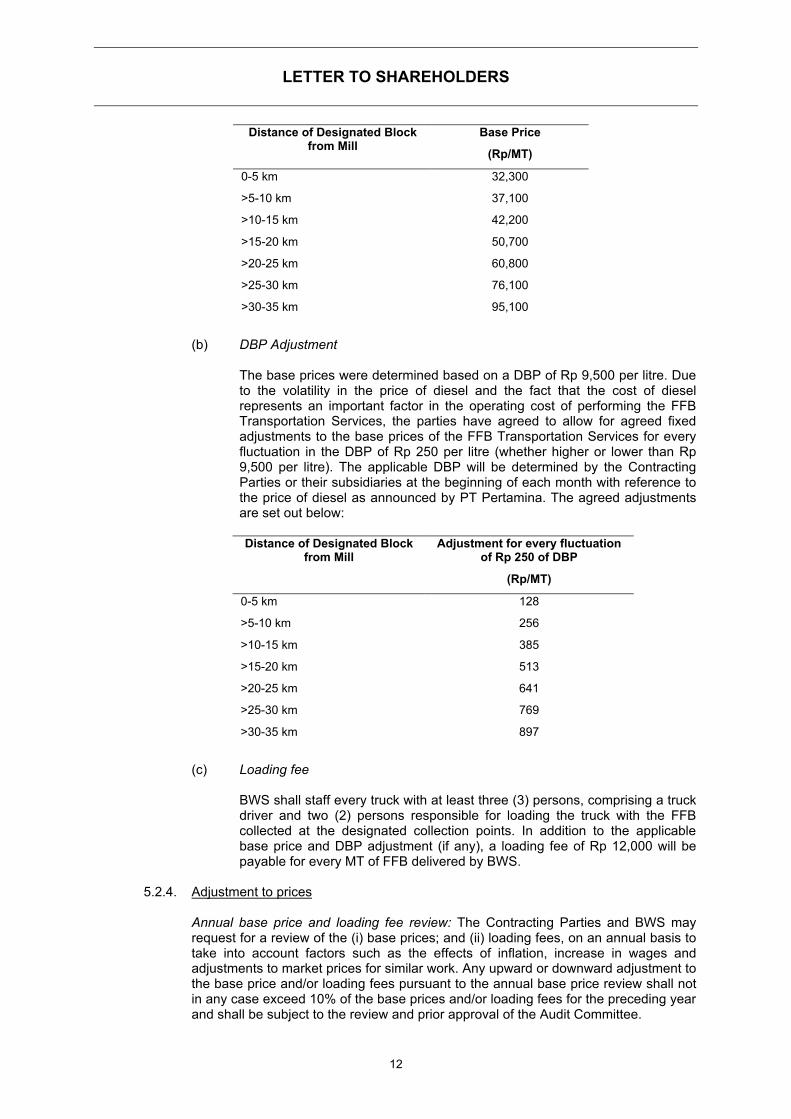

Distance of Designated Block from Mill

Base Price

(Rp/MT)

0-5 km 32,300

>5-10 km 37,100 >10-15 km 42,200 >15-20 km 50,700 >20-25 km 60,800 >25-30 km 76,100 >30-35 km 95,100

(b) DBP Adjustment

The base prices were determined based on a DBP of Rp 9,500 per litre. Due to the volatility in the price of diesel and the fact that the cost of diesel represents an important factor in the operating cost of performing the FFB Transportation Services, the parties have agreed to allow for agreed fixed adjustments to the base prices of the FFB Transportation Services for every fluctuation in the DBP of Rp 250 per litre (whether higher or lower than Rp 9,500 per litre). The applicable DBP will be determined by the Contracting Parties or their subsidiaries at the beginning of each month with reference to the price of diesel as announced by PT Pertamina. The agreed adjustments are set out below: Distance of Designated Block

from Mill Adjustment for every fluctuation

of Rp 250 of DBP

(Rp/MT)

0-5 km 128

>5-10 km 256 >10-15 km 385 >15-20 km 513 >20-25 km 641 >25-30 km 769 >30-35 km 897

(c) Loading fee BWS shall staff every truck with at least three (3) persons, comprising a truck driver and two (2) persons responsible for loading the truck with the FFB collected at the designated collection points. In addition to the applicable base price and DBP adjustment (if any), a loading fee of Rp 12,000 will be payable for every MT of FFB delivered by BWS.

5.2.4. Adjustment to prices

Annual base price and loading fee review: The Contracting Parties and BWS may request for a review of the (i) base prices; and (ii) loading fees, on an annual basis to take into account factors such as the effects of inflation, increase in wages and adjustments to market prices for similar work. Any upward or downward adjustment to the base price and/or loading fees pursuant to the annual base price review shall not in any case exceed 10% of the base prices and/or loading fees for the preceding year and shall be subject to the review and prior approval of the Audit Committee.

LETTER TO SHAREHOLDERS

13

For the avoidance of doubt, adjustments made due to fluctuations in DBP are separate from and do not count towards the 10% maximum permissible adjustment to the base prices.

5.2.5. Contract Basis

The FFB Transportation Contracts provide the framework under which the Contracting Parties or their subsidiaries may engage the services of BWS for the provision of the FFB Transportation Services at the Group’s oil palm plantations. The Contracting Parties or any of their subsidiaries may engage the services of BWS under the FFB Transportation Contract on a contract basis by executing a confirmation letter, which will set out the specific terms of each job order, such as the precise locations of the plantations to be serviced, the estimated weight of FFB to be transported over the duration of each job order and other material information required to make an assessment of the scope of the work requested by the Group. Acceptance by BWS of the terms set out in the confirmation letter will formalise and confirm the job order.

5.2.6. Contractor’s Reimbursement

If the Group finds any of the FFB Transportation Services performed by BWS unsatisfactory, the Group may engage independent third party contractors to complete the work done by BWS. BWS shall compensate the Group in full for the difference between the total amount incurred by the Group in respect of the jobs required under a particular job order (including the fees paid to BWS and the independent third party contractor) and the amount it would have paid to BWS under the FFB Transportation Contracts for those works.

5.2.7. Termination

The Group may in its absolute discretion choose to terminate the FFB Transportation Contracts upon the occurrence of certain agreed events, such as a material change in economic conditions, breach of contract or negligence on the part of BWS. The FFB Transportation Contracts do not provide for termination at the discretion of BWS.

5.3. The Oil Transportation Contracts

Under the Oil Transportation Contracts, the Contracting Parties and BWS agreed to a framework pursuant to which the Contracting Parties and/or any of their subsidiaries may contract the services of BWS for the purpose of transporting CPO and/or CPKO from mills to storage facilities, ports or end customers (the “Oil Transportation Services”). As stated above, the Group has been contracting the Oil Transportation Services of BWS on a continuing basis since 2001. 5.3.1. Term of contract

The Oil Transportation Contracts shall have a term of five (5) years. 5.3.2. Pricing

The fees payable for the Oil Transportation Services shall be determined in accordance with the following formula: (base price + diesel component + DBP adjustment (if any)) x weight of CPO/CPKO delivered (MT)

LETTER TO SHAREHOLDERS

14

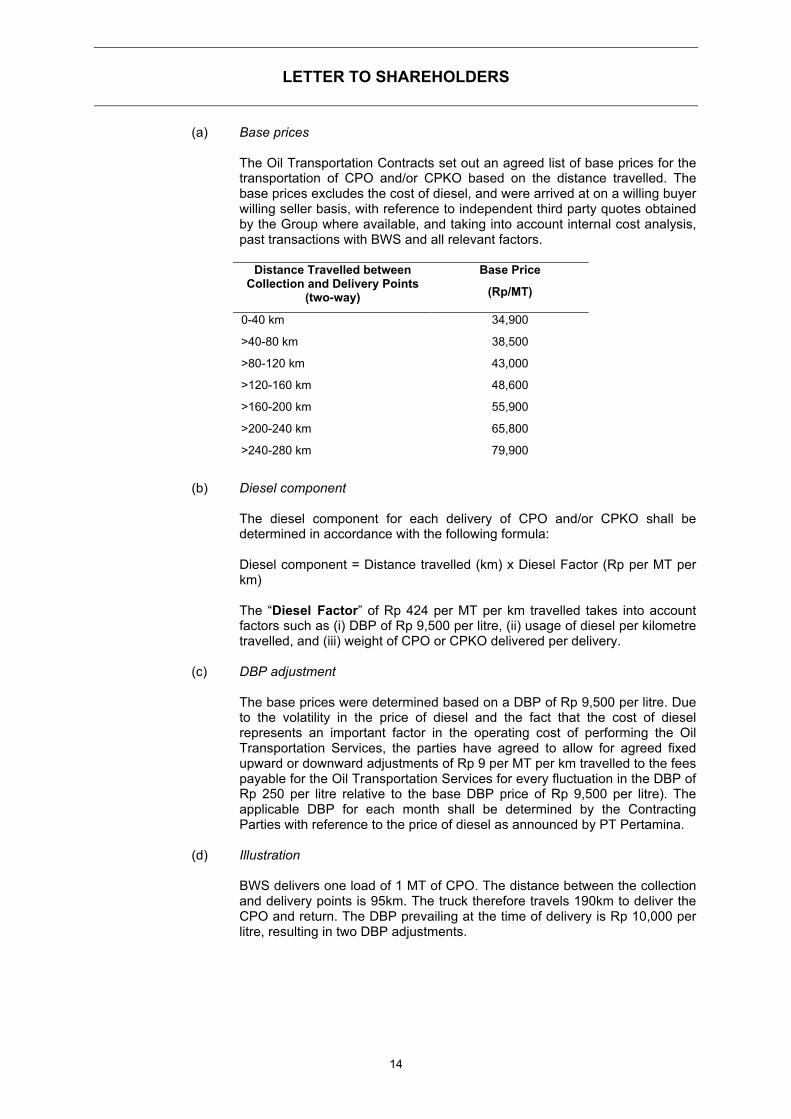

(a) Base prices

The Oil Transportation Contracts set out an agreed list of base prices for the transportation of CPO and/or CPKO based on the distance travelled. The base prices excludes the cost of diesel, and were arrived at on a willing buyer willing seller basis, with reference to independent third party quotes obtained by the Group where available, and taking into account internal cost analysis, past transactions with BWS and all relevant factors.

Distance Travelled between

Collection and Delivery Points (two-way)

Base Price

(Rp/MT)

0-40 km 34,900

>40-80 km 38,500

>80-120 km 43,000

>120-160 km 48,600

>160-200 km 55,900

>200-240 km 65,800

>240-280 km 79,900

(b) Diesel component

The diesel component for each delivery of CPO and/or CPKO shall be determined in accordance with the following formula: Diesel component = Distance travelled (km) x Diesel Factor (Rp per MT per km) The “Diesel Factor” of Rp 424 per MT per km travelled takes into account factors such as (i) DBP of Rp 9,500 per litre, (ii) usage of diesel per kilometre travelled, and (iii) weight of CPO or CPKO delivered per delivery.

(c) DBP adjustment The base prices were determined based on a DBP of Rp 9,500 per litre. Due to the volatility in the price of diesel and the fact that the cost of diesel represents an important factor in the operating cost of performing the Oil Transportation Services, the parties have agreed to allow for agreed fixed upward or downward adjustments of Rp 9 per MT per km travelled to the fees payable for the Oil Transportation Services for every fluctuation in the DBP of Rp 250 per litre relative to the base DBP price of Rp 9,500 per litre). The applicable DBP for each month shall be determined by the Contracting Parties with reference to the price of diesel as announced by PT Pertamina.

(d) Illustration BWS delivers one load of 1 MT of CPO. The distance between the collection and delivery points is 95km. The truck therefore travels 190km to deliver the CPO and return. The DBP prevailing at the time of delivery is Rp 10,000 per litre, resulting in two DBP adjustments.

LETTER TO SHAREHOLDERS

15

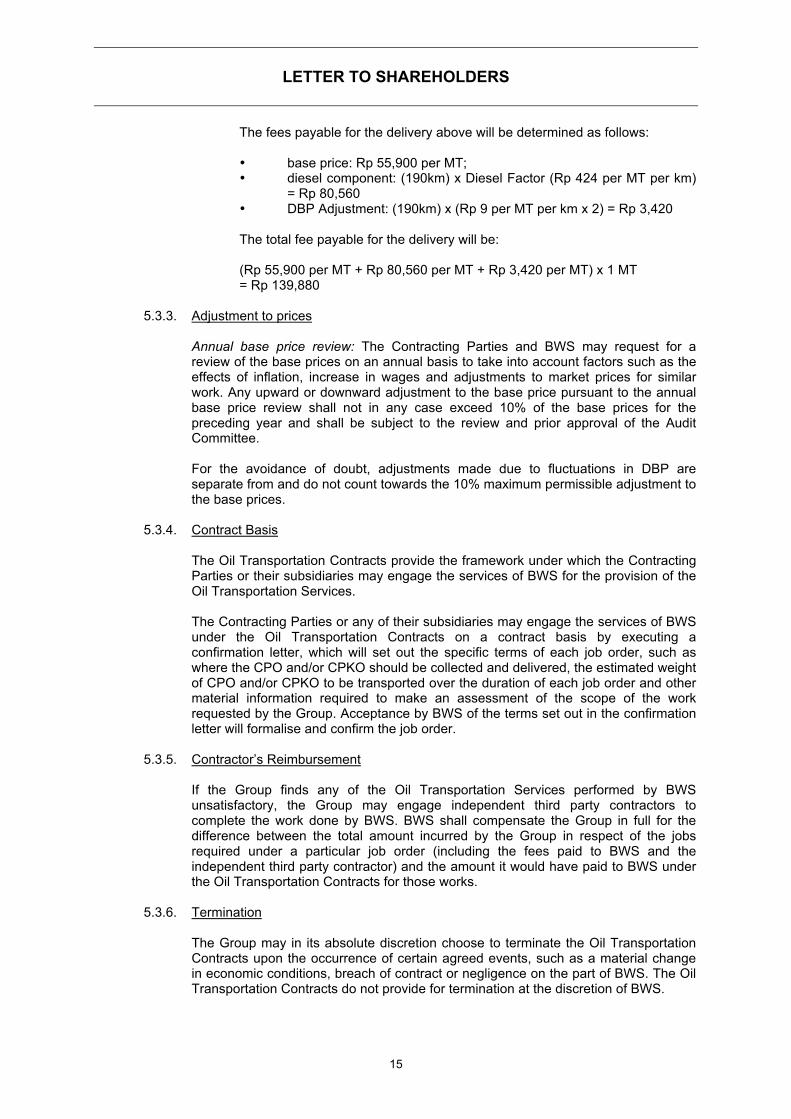

The fees payable for the delivery above will be determined as follows: • base price: Rp 55,900 per MT; • diesel component: (190km) x Diesel Factor (Rp 424 per MT per km)

= Rp 80,560 • DBP Adjustment: (190km) x (Rp 9 per MT per km x 2) = Rp 3,420 The total fee payable for the delivery will be: (Rp 55,900 per MT + Rp 80,560 per MT + Rp 3,420 per MT) x 1 MT = Rp 139,880

5.3.3. Adjustment to prices

Annual base price review: The Contracting Parties and BWS may request for a review of the base prices on an annual basis to take into account factors such as the effects of inflation, increase in wages and adjustments to market prices for similar work. Any upward or downward adjustment to the base price pursuant to the annual base price review shall not in any case exceed 10% of the base prices for the preceding year and shall be subject to the review and prior approval of the Audit Committee. For the avoidance of doubt, adjustments made due to fluctuations in DBP are separate from and do not count towards the 10% maximum permissible adjustment to the base prices.

5.3.4. Contract Basis

The Oil Transportation Contracts provide the framework under which the Contracting Parties or their subsidiaries may engage the services of BWS for the provision of the Oil Transportation Services. The Contracting Parties or any of their subsidiaries may engage the services of BWS under the Oil Transportation Contracts on a contract basis by executing a confirmation letter, which will set out the specific terms of each job order, such as where the CPO and/or CPKO should be collected and delivered, the estimated weight of CPO and/or CPKO to be transported over the duration of each job order and other material information required to make an assessment of the scope of the work requested by the Group. Acceptance by BWS of the terms set out in the confirmation letter will formalise and confirm the job order.

5.3.5. Contractor’s Reimbursement

If the Group finds any of the Oil Transportation Services performed by BWS unsatisfactory, the Group may engage independent third party contractors to complete the work done by BWS. BWS shall compensate the Group in full for the difference between the total amount incurred by the Group in respect of the jobs required under a particular job order (including the fees paid to BWS and the independent third party contractor) and the amount it would have paid to BWS under the Oil Transportation Contracts for those works.

5.3.6. Termination

The Group may in its absolute discretion choose to terminate the Oil Transportation Contracts upon the occurrence of certain agreed events, such as a material change in economic conditions, breach of contract or negligence on the part of BWS. The Oil Transportation Contracts do not provide for termination at the discretion of BWS.

LETTER TO SHAREHOLDERS

16

5.4. Rationale for entering into the Contracts

The Group’s strategy is to focus its resources on its core businesses, being the management and expansion of its oil palm plantation business, production of oil palm products, and improving its distribution of its products. In view of this strategy, the Group outsources certain non-core functions to third party contractors. The Group has entered into five (5) years fixed contracts with ASP and BWS in order to secure certainty of pricing for these services and to ensure the continuity of such services by reliable contractors. This in turn will allow the Group to better plan its expansion and other development costs and reduce the operational risks. The Group is of the view that the five (5) year fixed contracts are necessary and beneficial to the Group, as it expects to scale up its land clearing activities and CPO/CPKO production (which will increase its transportation requirements) over the next five (5) years and it is more efficient to manage these processes on a longer term basis.

The Land Clearing and Infrastructure Contracts

ASP is one of a few land clearing and infrastructure contractors appointed by the Group. ASP has been providing these services to the Group since 2011 and has proven to be a reliable service provider. In addition to the factors mentioned in Section 3.1 above, the Group believes that entering into the Land Clearing and Infrastructure Contracts with ASP will be beneficial to the Group, as ASP is a reliable land clearing contractor that can perform the land clearing services required by the Group in a timely fashion in accordance with the Group’s development schedule. Being related to the Group, ASP is more familiar with the terrain of the Group’s land banks, which will help in the performance of the Land Clearing and Infrastructure Activities. Furthermore, the relationship between the Group and ASP will allow ASP to better understand the needs of the Group in relation to the Group’s need for new plantation land and infrastructure needs.

Land clearing contractors entering new and remote areas, such as the Group’s land banks in parts of Sulawesi and Kalimantan, will require heavy capital investment in order to purchase new heavy equipment. Third party contractors often do not have the ability or do not wish to make the investments required to do so. The Group believes that sourcing for a suitable third party contractor amongst the limited pool of contractors who are able to meet its requirements will be costly. By contracting the services of ASP on a long term contract, not only does the Group enjoy a greater degree of certainty in cost management, it is also assured of the services of a land clearing contractor with sufficient resources to meet the needs of the Group.

The FFB Transportation Contracts and Oil Transportation Contracts

BWS has provided dedicated transportation services to the Group for more than 10 years. Over this period, BWS has demonstrated its reliability and dedication in performing the services required by the Group at competitive prices. BWS does not service other customers, and all its resources are devoted to meeting the needs of the Group. The Group believes that entering into these contracts with BWS will be beneficial to the Group as a whole. The quality of the transportation of FFB is an important factor for the efficient production of one of the Group’s primary products, CPO. FFB are perishable products; freshly picked FFB must be processed within 24 hours in order to maximise CPO yield. The Group’s CPO and CPKO must similarly be delivered in a timely manner in order to meet the Group’s sale orders. The tanks must also be kept clean to prevent contamination of the CPO and CPKO transported. Over the years, BWS has consistently met the needs of the Group and has proven to be a reliable provider of transportation services with a good track record. The Group thus believes that it will be in the interests of the Group to secure the services of BWS under a long term contract. BWS is also familiar with the operations of the Group, thus reducing operational

LETTER TO SHAREHOLDERS

17

risks and ensuring integration between the Group’s operations and BWS’ transportation services.

6. REVIEW PROCEDURES 6.1. Register of Interested Person Transactions

The Group will maintain a register of all transactions carried out pursuant to the Contracts and shall include all information pertinent to these transactions such as, but not limited to the value of the transactions, the basis for determining the applicable DBP, the transaction prices and supporting evidence and quotations obtained to support such basis. The register shall be prepared, maintained and monitored by personnel of the Group (who shall not be interested in any of the Contracts) who are duly delegated to do so by the Audit Committee and reviewed by internal auditors on a quarterly basis and by external auditors on an annual basis.

6.2. Review by Audit Committee

The Audit Committee shall review the quarterly internal audit reports on the transactions entered into under the Contracts to ascertain that the terms of the Contracts have been complied with. If any member of the Audit Committee has an interest in a transaction, he shall abstain from participating in the review and approval process in relation to that transaction.

6.3. Annual Price Review

The Group shall review the base prices under the Contracts and the loading fees under the FFB Transportation Contracts on an annual basis. Following the annual review, the Group will propose adjustments in the prices to ASP and/or BWS (as the case may be), if required. In addition, as part of the Group’s internal control procedures, the Audit Committee shall review and give its prior approval to any price adjustments made pursuant to the annual reviews.

7. INDEPENDENT FINANCIAL ADVISER’S OPINION

Provenance Capital Pte. Ltd. has been appointed as the IFA to advise the Independent Directors on whether the financial terms of the Contracts are on normal commercial terms and are not prejudicial to the interests of the Company and the Independent Shareholders. A copy of the letter dated 10 April 2012 from the IFA (the “IFA Letter”), containing its opinion in full, is set out in Appendix A of this Circular. Shareholders are advised to read the letter in its entirety. Taking into consideration the factors set out in the IFA Letter and subject to the assumptions and qualifications contained therein and the information available to the IFA as at the Latest Practicable Date, the IFA is of the opinion that, on balance, the financial terms of the Contracts are on normal commercial terms and are not prejudicial to the interests of the Company and the Independent Shareholders.

8. VIEWS OF THE AUDIT COMMITTEE AND DIRECTORS’ RECOMMENDATION 8.1. Views of the Audit Committee

Having reviewed, inter alia, the terms and rationale for and the benefits of the Contracts, as well as the opinion and advice of the IFA, the Audit Committee concurs with the opinion of the IFA and is of the view that the Contracts are on normal commercial terms and are not prejudicial to the interests of the Company and the Independent Shareholders.

LETTER TO SHAREHOLDERS

18

8.2. Directors’ Recommendation

Having considered, inter alia, the terms, the rationale for and the benefits of the Contracts, as well as the opinion and advice of the IFA, the Independent Directors are of the view that the Contracts are in the interests of the Company and accordingly recommend that Shareholders vote in favour of the resolution approving the entry by the Group into the Contracts as set out in the notice of EGM. Mr Henry Maknawi and Ms. Ratna Maknawi, being interested in the Contracts, have abstained from making any recommendation on the Contracts.

9. INTEREST OF DIRECTORS AND CONTROLLING SHAREHOLDERS 9.1. Interest of Directors and Controlling Shareholders

As at the Latest Practicable Date, none of the Directors or the Controlling Shareholders of the Company have any direct or indirect interests in the Contracts, save as disclosed below: 9.1.1. members of Mr Henry Maknawi’s immediate family are interested in 60% of the share

capital of ASP;

9.1.2. Mr Henry Maknawi and Ms. Ratna Maknawi, are interested in 57.5% of the share capital of BWS.

9.2. Abstention from Voting

Mr Henry Maknawi and Ms Ratna Maknawi have undertaken to abstain, and ensure that their associates (including Kencana Holdings Pte Ltd) abstain, from voting in respect of the Contracts at the EGM. Edy Suroso and Wisely Antonius are employees and shareholders of the Company. As they also have an interest in BWS, they will abstain from voting in respect of the Contracts. Mr Henry Maknawi and Ms Ratna Maknawi will also abstain from making any recommendation to the Shareholders in respect of the Contracts.

9.3. Directors’ and Substantial Shareholders’ Interests in the Company

As at the Latest Practicable Date, save as disclosed below, none of the Directors has any interest in the Shares of the Company. The interests of the Directors and Substantial Shareholders in the Shares as at the Latest Practicable Date are set out below:

As at Latest Practicable Date

Direct Interest (No. of Shares)

% Deemed Interest (No. of Shares)

%

Directors Henry Maknawi(1) 7,099,880 0.62 610,220,896 53.15 Ratna Maknawi - - 5,666,120 0.49 Tengku Alwin Aziz 1,675,880 0.15 - - Kent Surya 837,440 0.07 - - Soh Yew Hock 200,000 0.02 - - Leung Yew Kwong 400,000 0.03 - - Teo Kim Yong - - - - Ang Kok Min - - - - Sim Idrus Munandar - - - -

LETTER TO SHAREHOLDERS

19

As at Latest Practicable Date Direct Interest

(No. of Shares) % Deemed Interest

(No. of Shares) %

Substantial Shareholders Kencana Holdings Pte. Ltd.

610,220,896 53.15 - -

Newbloom Pte. Ltd. 229,608,944 20.00 - - Wilmar International Limited(2)

- - 229,608,944 20.00

Henry Maknawi(1) 7,099,880 0.62 610,220,896 53.15

Notes: (1) Mr Henry Maknawi is deemed to be interested in the shares held by Kencana Holdings Pte. Ltd. by virtue

of his 43.41% shareholding interest in Kencana Holdings Pte. Ltd. (2) Wilmar International Limited is deemed to be interested in the shares held by Newbloom Pte. Ltd., its

wholly-owned subsidiary. 10. EXTRAORDINARY GENERAL MEETING

The EGM, notice of which is set out on page 40 of this Circular, will be convened at Coleman Room, Level 1, Grand Park City Hall, 10 Coleman Street, Singapore 179809 on 26 April 2012 at 4.00 p.m., or immediately after the conclusion of the Annual General Meeting to be held at 3.00 p.m. on the same day and at the same place (or the adjournment thereof) for the purpose of considering and, if thought fit, passing with or without modifications, the resolutions set out in the Notice of the EGM.

11. ACTION TO BE TAKEN BY SHAREHOLDERS

If a Shareholder is unable to attend the EGM and wishes to appoint a proxy to attend and vote on his behalf, he should complete, sign and return the attached Proxy Form in accordance with the instructions printed thereon as soon as possible and, in any event, so as to reach registered office of the Company at 36 Armenian Street #03-02 Singapore 179934 not later than 4.00 p.m. on 24 April 2012. The completion and return of the Proxy Form by a Shareholder will not prevent him from attending and voting at the EGM in person if he so wishes. A Depositor shall not be regarded as a Shareholder entitled to attend the EGM and to speak and vote thereat unless he is shown to have Shares entered against his name in the Depository Register, as certified by the CDP as at 48 hours before the EGM.

12. DIRECTORS’ RESPONSIBILITY STATEMENT

The Directors collectively and individually accept full responsibility for the accuracy of the information given in this Circular (save for the IFA Letter) and confirm after making all reasonable enquiries that, to the best of their knowledge and belief, this Circular constitutes full and true disclosure of all material facts about the Contracts, the Company and its subsidiaries, and the Directors are not aware of any facts, the omission of which would make any statement in this Circular misleading. Where information in this Circular (save for the IFA Letter) has been extracted from published or otherwise publicly available sources or obtained from a named source, the sole responsibility of the Directors has been to ensure that such information has been accurately and correctly extracted from those sources and/or reproduced in this Circular in its proper form and context.

LETTER TO SHAREHOLDERS

20

With respect to the IFA Letter, the sole responsibility of the Directors has been to ensure that the facts stated with respect to the Contracts and the Group are fair and accurate in all material respects.

13. CONSENT OF THE IFA

The IFA has given and has not withdrawn its written consent to the issue of this Circular with the inclusion of its name and the IFA Letter (attached to this Circular as Appendix A) and all references thereto, in the form and context in which they appear in this Circular.

14. DOCUMENTS AVAILABLE FOR INSPECTION

Copies of the following documents may be inspected at registered office of the Company at 36 Armenian Street #03-02 Singapore 179934 during normal office hours from the date of this Circular up to and including the date of the EGM:

14.1 the Contracts; 14.2 the Memorandum and Articles of Association of the Company; and 14.3 the Annual Report of the Company for the financial year ended 31 December 2011.

Yours faithfully For and on behalf of the Board of Directors of Kencana Agri Limited Henry Maknawi Chairman and Chief Executive Officer

APPENDIX A: LETTER FROM PROVENANCE CAPITAL PTE. LTD. TO THE

INDEPENDENT DIRECTORS OF KENCANA AGRI LIMITED IN RESPECT OF THE INTERESTED PERSON TRANSACTIONS

21

APPENDIX A: LETTER FROM PROVENANCE CAPITAL PTE. LTD. TO THE INDEPENDENT DIRECTORS OF KENCANA AGRI LIMITED IN RESPECT OF THE INTERESTED PERSON TRANSACTIONS

PROVENANCE CAPITAL PTE. LTD. (Company Registration Number: 200309056E)

(Incorporated in the Republic of Singapore) 96 Robinson Road #13-01 SIF Building

Singapore 068899

10 April 2012 To: The Directors of Kencana Agri Limited (deemed to be independent in respect of the Interested Person Transactions) Tengku Alwin Aziz (Vice-Chairman and Non-Executive Director) Mr Kent Surya (Finance Director) Mr Soh Yew Hock (Lead Independent Director) Mr Leung Yew Kwong (Independent Director) Mr Sim Idrus Munandar (Independent Director) Mr Teo Kim Yong (Non-Executive Director) Mr Ang Kok Min (Alternate Director to Mr Teo Kim Yong) Dear Sirs, THE PROPOSED CONTRACTS WITH INTERESTED PERSONS Unless otherwise defined or the context otherwise requires, all terms used herein have the same meanings as defined in the circular to shareholders of the Company dated 10 April 2012 (the “Circular”). 1. INTRODUCTION

On 9 April 2012, Kencana Agri Limited (the “Company”) announced that PT Sawit Permai Lestari and PT Wira Palm Mandiri (the “Contracting Parties”), both subsidiaries of the Company, have entered into separate conditional agreements with: (a) PT Alamindo Sejahtera Persada (“ASP”), pursuant to which ASP shall provide land

clearing and infrastructure construction services to the Contracting Parties and their subsidiaries (the “Land Clearing and Infrastructure Contracts”); and

(b) PT Berkat Wahana Sukses (“BWS”), pursuant to which:

(i) BWS shall provide fresh fruit bunch (“FFB”) transportation and logistics services

to the Contracting Parties and their subsidiaries (the “FFB Transportation Contracts”); and

(ii) BWS shall provide crude palm oil (“CPO”) and crude palm kernel oil (“CPKO”)

transportation and logistics services to the Contracting Parties and their subsidiaries (the “Oil Transportation Contracts”),

(collectively, the “Contracts”).

The services to be provided by ASP and BWS under the Contracts are similar to the services that they currently provide to the Company and its subsidiaries (collectively, the “Group”) on an ongoing basis. The Group’s total transaction values with ASP and BWS for the financial year ended 31 December 2011, amounted to approximately US$4.0 million and US$1.7

APPENDIX A: LETTER FROM PROVENANCE CAPITAL PTE. LTD. TO THE

INDEPENDENT DIRECTORS OF KENCANA AGRI LIMITED IN RESPECT OF THE INTERESTED PERSON TRANSACTIONS

22

million respectively (excluding transactions below S$100,000 each), representing an aggregate of 2.7% of the Group’s audited net tangible assets (“NTA”) as at 31 December 2010. The immediate family members of Mr Henry Maknawi, who is the Chairman and Chief Executive Officer and a controlling shareholder of the Company, have an aggregate interest of 60% in the total issued share capital of ASP as at the Latest Practicable Date. This includes an indirect interest of 15% in the share capital of ASP which is held by Mr Albert Maknawi, who is the Chief Operating Officer of the Company and the son of Mr Henry Maknawi. Mr Henry Maknawi and Ms Ratna Maknawi (who is the Company’s executive director and Deputy Chief Executive Officer and the sister of Mr Henry Maknawi) hold 28.0% and 29.5% of the total issued share capital of BWS respectively as at the Latest Practicable Date. In addition, certain existing employees of the Group hold an aggregate of 21.0% of the total issued share capital of BWS as at the Latest Practicable Date. Accordingly, ASP and BWS are deemed to be associates of Mr Henry Maknawi and Ms Ratna Maknawi, and the Contracts constitute Interested Person Transactions within the meaning of Chapter 9 of the Singapore Exchange Securities Trading Limited Listing Manual (the “Listing Manual”). The total value of the Group’s transactions with ASP and BWS for the financial year ended 31 December 2011 did not exceed the thresholds set out in Rule 906 of the Listing Manual. However, going forward, as the aggregate value of the transactions to be carried out pursuant to the Contracts could exceed 5% of the Group’s audited NTA, pursuant to Rule 906 of the Listing Manual and in the interests of transparency and good corporate governance, the Company is seeking the approval of the Company’s independent shareholders (the “Independent Shareholders”) in respect of the Contracts at an extraordinary general meeting (“EGM”) to be convened.

Provenance Capital Pte. Ltd. (“Provenance Capital”) has been appointed as the independent financial adviser (“IFA”) to advise and render an opinion to the directors of the Company who are considered independent for the purpose of considering the Contracts (the “Independent Directors”) on whether or not the financial terms of the Contracts are on normal commercial terms and whether or not they are prejudicial to the interests of the Company and the Independent Shareholders. This letter (“Letter”) is addressed to the Independent Directors and is to be incorporated into the Circular issued by the Company which provides, inter alia, the details of the Contracts and the recommendations of the Independent Directors thereon.

2. TERMS OF REFERENCE

We have been appointed as the IFA to advise the Independent Directors in respect of the Contracts. We are not and were not involved or responsible, in any aspect, of the negotiations in relation to the Contracts, nor were we involved in the deliberations leading up to the decision on the part of the Independent Directors to propose the Contracts or to obtain the approval of the Independent Shareholders for the Contracts, and we do not, by this Letter, warrant the merits of the Contracts other than to express an opinion on whether the Contracts are prejudicial to the interests of the Company and the Independent Shareholders.

We have confined our evaluation and assessment to the financial terms of the Contracts. It is not within our terms of reference to evaluate or comment on the legal, strategic, commercial and financial merits and/or risks of the Contracts or to compare their relative merits vis-à-vis alternative transactions previously considered by the Company (if any) or that may otherwise

APPENDIX A: LETTER FROM PROVENANCE CAPITAL PTE. LTD. TO THE

INDEPENDENT DIRECTORS OF KENCANA AGRI LIMITED IN RESPECT OF THE INTERESTED PERSON TRANSACTIONS

23

be available to the Company currently or in the future, and we have not made such evaluation or comment. Such evaluation or comment, if any, remains the sole responsibility of the Directors and/or the management of the Company (the “Management”) although we may draw upon the views of the Directors and/or the Management or make such comments in respect thereof (to the extent deemed necessary or appropriate by us) in arriving at our opinion as set out in this Letter. We have not been requested or authorised to solicit, and we have not solicited, any quotations from any third party with respect to the Contracts.

In the course of our evaluation, we have held discussions with the Directors and Management and/or their professional advisers and have examined and relied to a considerable extent on publicly available information collated by us as well as information provided and representations made to us, both written and verbal, by the Directors, the Management and the professional advisers of the Company, including information contained in the Circular. We have not independently verified such information or representations, whether written or verbal, and accordingly cannot and do not make any representation or warranty, express or implied, in respect of, and do not accept any responsibility for the accuracy, completeness or adequacy of such information or representations.

The Directors (including those who may have delegated detailed supervision of the preparation of the Circular) have confirmed that, having made all reasonable enquiries, to the best of their respective knowledge and belief, information and representations as provided by the Directors and Management are accurate and have confirmed to us that, upon making all reasonable enquiries and to their best knowledge and abilities, all material information available to them in connection with the Contracts, the Company and the Group, has been disclosed to us, that such information is true, complete and accurate in all material respects and that there is no other information or fact, the omission of which would cause any information disclosed to us or the facts of or in relation to the Contracts, the Company and the Group stated in the Circular to be inaccurate, incomplete or misleading in any material respect. The Directors have jointly and severally accepted full responsibility for such information described herein.

We have not independently verified and have assumed that all statements of fact, belief, opinion and intention made by the Directors in the Circular have been reasonably made after due and careful enquiry. Whilst care has been exercised in reviewing the information on which we have relied on, we have not independently verified the information but nevertheless have made such enquiry and judgment as were deemed necessary and have found no reason to doubt the accuracy of the information and representations.

Save as disclosed, we would like to highlight that all information relating to the Contracts, the Company and the Group that we have relied upon in arriving at our opinion has been obtained from publicly available information and/or from the Directors and the Management. We have not independently assessed and do not warrant or accept any responsibility as to whether the aforesaid information adequately represents a true and fair position of the financial, operational and business affairs of the Company or the Group at any time or as at 2 April 2012 (the “Latest Practicable Date”). The scope of our appointment does not require us to conduct a comprehensive independent review of the business, operations or financial condition of the Company and/or the Group, or to express, and we do not express, a view on the future growth prospects, value and earnings potential of the Company and/or the Group. Such review or comment, if any, remains the responsibility of the Directors and the Management, although we may draw upon their views or make such comments in respect thereof (to the extent required by the Listing Manual and/or deemed necessary or appropriate by us) in arriving at our advice as set out in this Letter. We have not obtained from the Company and/or the Group any projection of the future performance including financial performance of the Company and/or the Group, and further,

APPENDIX A: LETTER FROM PROVENANCE CAPITAL PTE. LTD. TO THE

INDEPENDENT DIRECTORS OF KENCANA AGRI LIMITED IN RESPECT OF THE INTERESTED PERSON TRANSACTIONS

24

we did not conduct discussions with the Directors and the Management on, and did not have access to, any business plan and financial projections of the Company and/or the Group.

Our view as set out in this Letter is based upon market, economic, industry, monetary and other conditions (if applicable) prevailing as at the Latest Practicable Date and the information provided and representations provided to us as at the Latest Practicable Date. In arriving at our view, with the consent of the Directors or the Company, we have taken into account certain other factors and have been required to make certain assumptions as set out in this Letter. We assume no responsibility to update, revise or reaffirm our opinion in light of any subsequent development after the Latest Practicable Date that may affect our opinion contained herein. Shareholders should further take note of any announcements relevant to the Contracts which may be released by the Company after the Latest Practicable Date.

In rendering our advice, we did not have regard to the specific investment objectives, financial situation, tax position, risk profiles or unique needs and constraints of any Independent Shareholder or any specific group of the Independent Shareholders. As each Independent Shareholder would have different investment objectives and profiles, we recommend that any individual Independent Shareholder or group of the Independent Shareholders who may require specific advice in relation to his or their investment portfolio(s) or objective(s) consult his or their stockbroker, bank manager, solicitor, accountant, tax adviser or other professional adviser immediately.

The Company has been separately advised by its own professional advisers in the preparation of the Circular (other than this Letter). We have had no role or involvement and have not and will not provide any advice (financial or otherwise) in the preparation, review and verification of the Circular (other than this Letter). Accordingly, we take no responsibility for and express no views, whether express or implied, on the contents of the Circular (other than this Letter).

Whilst a copy of this Letter may be reproduced in the Circular, neither the Company nor the Directors may reproduce, disseminate or quote this Letter (or any part thereof) for any purposes other than for the purposes of the Shareholders’ resolution in relation to the Contracts at any time and in any manner without the prior written consent of Provenance Capital in each specific case.

We have prepared this Letter for the use of the Independent Directors in connection with their consideration of the Contracts and their advice to the Independent Shareholders arising thereof. The recommendation made to the Independent Shareholders in relation to the Contracts remains the sole responsibility of the Independent Directors.

Our opinion in relation to the Contracts should be considered in the context of the entirety of this Letter and the Circular.

3. DETAILS OF THE CONTRACTS

A summary of the salient terms of the Contracts is set out below. The details of the Contracts are set out in Section 5 of the Circular.

3.1 The Land Clearing and Infrastructure Contracts

Under the Land Clearing and Infrastructure Contracts, the Contracting Parties and ASP agreed to a framework pursuant to which the Contracting Parties and/or any of their subsidiaries may contract the services of ASP for land clearing and infrastructure activities which includes, inter alia, clearing uncultivated land, carrying out terrace contouring and constructing basic infrastructure such as roads and bridges (the “Land Clearing and Infrastructure Activities”), in order to prepare the Group’s unutilised land bank for cultivation

APPENDIX A: LETTER FROM PROVENANCE CAPITAL PTE. LTD. TO THE

INDEPENDENT DIRECTORS OF KENCANA AGRI LIMITED IN RESPECT OF THE INTERESTED PERSON TRANSACTIONS

25

of new oil palm estates at 4 agreed locations in Indonesia, namely Pohuwato (Gorontalo), Bulungan (East Kalimantan), Batui (Banggai, Central Sulawesi) and Bualemo (Banggai, Central Sulawesi). The Land Clearing and Infrastructure Contracts shall have a term of 5 years. As at 31 December 2011, the Group has the right to cultivate approximately 66,461 ha (subject to final measurement by the relevant authorities) of land at these locations, of which the Group estimates that approximately 50% to 60% of the land banks may be available for land clearing and construction of necessary infrastructure. The Group intends to engage the services of ASP as one of the contractors for the Land Clearing and Infrastructure Activities at parts of the land bank mentioned above. Based on the terms of the Land Clearing and Infrastructure Contracts and the Group’s present expansion and planting plans, the Group estimates that the aggregate value of the transactions with ASP pursuant to the Land Clearing and Infrastructure Contracts could be in the range of between US$20 million and US$30 million over the 5-year term, barring any unforeseen circumstances.

3.1.1 Land Clearing and Infrastructure Base Prices The agreed list of base prices for each unit of the various services to be provided by ASP at each location (the “Land Clearing and Infrastructure Base Prices”), is set out in the Land Clearing and Infrastructure Contract, which is available for inspection at the registered office of the Company until the date of the EGM. The Land Clearing and Infrastructure Base Prices were arrived at on a willing buyer willing seller basis, with reference to independent third party quotes obtained by the Group where available, and taking into account internal pricing analysis, past transactions with ASP and all relevant factors.

3.1.2 Adjustments to the Land Clearing and Infrastructure Base Prices

The Land Clearing and Infrastructure Contracts provide for adjustments to be made to the Land Clearing and Infrastructure Base Prices in certain circumstances as summarised below: (a) Adjustments for fluctuations in Diesel Prices

The Land Clearing and Infrastructure Base Prices take into account the price of diesel (the “Diesel Price”), which is initially fixed at Rp 9,500 per litre (the “Base Diesel Price”). The Diesel Price is benchmarked against the price of diesel as announced by PT Pertamina at the beginning of each month.

Due to the volatility in the price of diesel and the fact that the cost of diesel represents an important factor in the operating cost of performing the Land Clearing and Infrastructure Activities, the parties have agreed to allow for agreed fixed adjustments to the Land Clearing and Infrastructure Base Prices for every fluctuation in the Diesel Price of an amount of Rp 250 per litre of diesel (whether higher or lower than the Base Diesel Price of Rp 9,500 per litre). The applicable Diesel Price will be determined by the Contracting Parties or their subsidiaries at the beginning of each month with reference to the price of diesel as announced by PT Pertamina. The table of adjustments to the Land Clearing and Infrastructure Base Prices for each unit of the various services at each location is also set out in the Land Clearing and Infrastructure Contracts.

APPENDIX A: LETTER FROM PROVENANCE CAPITAL PTE. LTD. TO THE

INDEPENDENT DIRECTORS OF KENCANA AGRI LIMITED IN RESPECT OF THE INTERESTED PERSON TRANSACTIONS

26

(b) Annual review of base prices

The Contracting Parties and ASP may request for a review of the Land Clearing and Infrastructure Base Prices on an annual basis to take into account factors such as the effects of inflation, increase in wages and adjustments to market prices for similar work. Any upward or downward price adjustment pursuant to the annual Land Clearing and Infrastructure Base Price review shall not in any case exceed 10% of the preceding year’s base prices, and shall be subject to the review and prior approval of the Audit Committee. For the avoidance of doubt, adjustments made due to fluctuations in Diesel Prices, as set out in paragraph 3.1.2(a) above, are separate from and do not count towards the 10% maximum permissible adjustment to the Land Clearing and Infrastructure Base Prices.

3.1.3 Other key commercial terms

Other key commercial terms in the Land Clearing and Infrastructure Contracts relating to payment terms, contractor’s reimbursement, compensation and termination are set out in Sections 5.1.7 to 5.1.10 of the Circular.

3.2 The FFB Transportation Contracts

Under the FFB Transportation Contracts, the Contracting Parties and BWS agreed to a framework pursuant to which the Contracting Parties and/or any of their subsidiaries may contract the services of BWS for the purposes of transporting FFB within certain oil palm plantations owned and/or controlled by the Contracting Parties and their subsidiaries (the “FFB Transportation Services”) at the 4 agreed locations in Indonesia, namely Bangka (Bangka Belitung), Kotabaru (South Kalimantan), Paser (East Kalimantan) and Kutai (East Kalimantan). The FFB Transportation Contracts shall have a term of 5 years.

3.2.1 FFB Transportation Fees The fees payable for the FFB Transportation Services (the “FFB Transportation Fees”) shall be determined in accordance with the following formula:

FFB Transportation Fees = (FFB Transportation Base Price + Diesel Price Adjustment (if any) + Loading Cost)

x weight of FFB delivered (in metric tonnes (“MT”)) Details of the components of the FFB Transportation Fees are described below. (a) FFB Transportation Base Prices

The FFB Transportation Contracts set out an agreed list of base prices for the transportation of FFB between designated blocks within the Group’s oil palm plantations to its CPO mills (the “FFB Transportation Base Prices”), as reproduced in Section 5.2.3(a) of the Circular. The FFB Transportation Base Prices include the cost of diesel, and were arrived at on a willing buyer willing seller basis with reference to independent third party quotes obtained by the Group, and taking into account internal cost analysis, past transactions with BWS and all relevant factors.

APPENDIX A: LETTER FROM PROVENANCE CAPITAL PTE. LTD. TO THE

INDEPENDENT DIRECTORS OF KENCANA AGRI LIMITED IN RESPECT OF THE INTERESTED PERSON TRANSACTIONS

27

(b) Diesel Price adjustments