Embed Size (px)

Citation preview

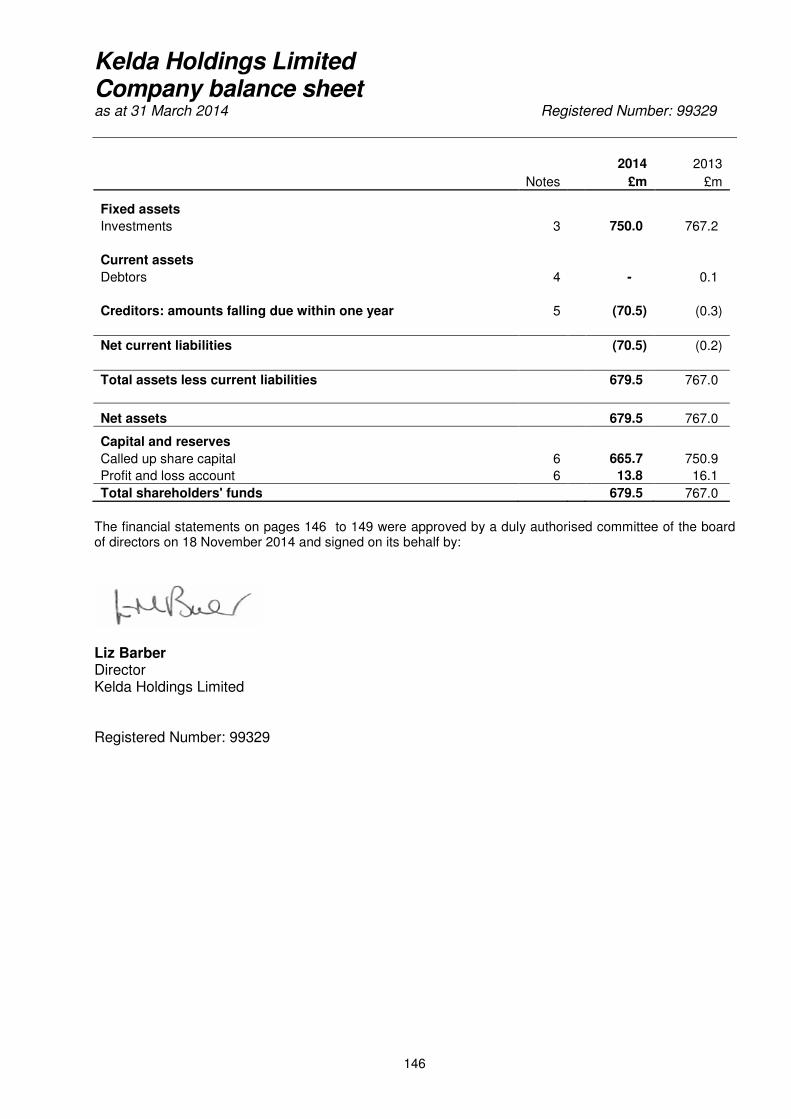

Registered Number: 99329

KELDA HOLDINGS LIMITED

ANNUAL REPORT AND FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 MARCH 2014

KELDA HOLDINGS LIMITED ANNUAL REPORT AND FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 MARCH 2014

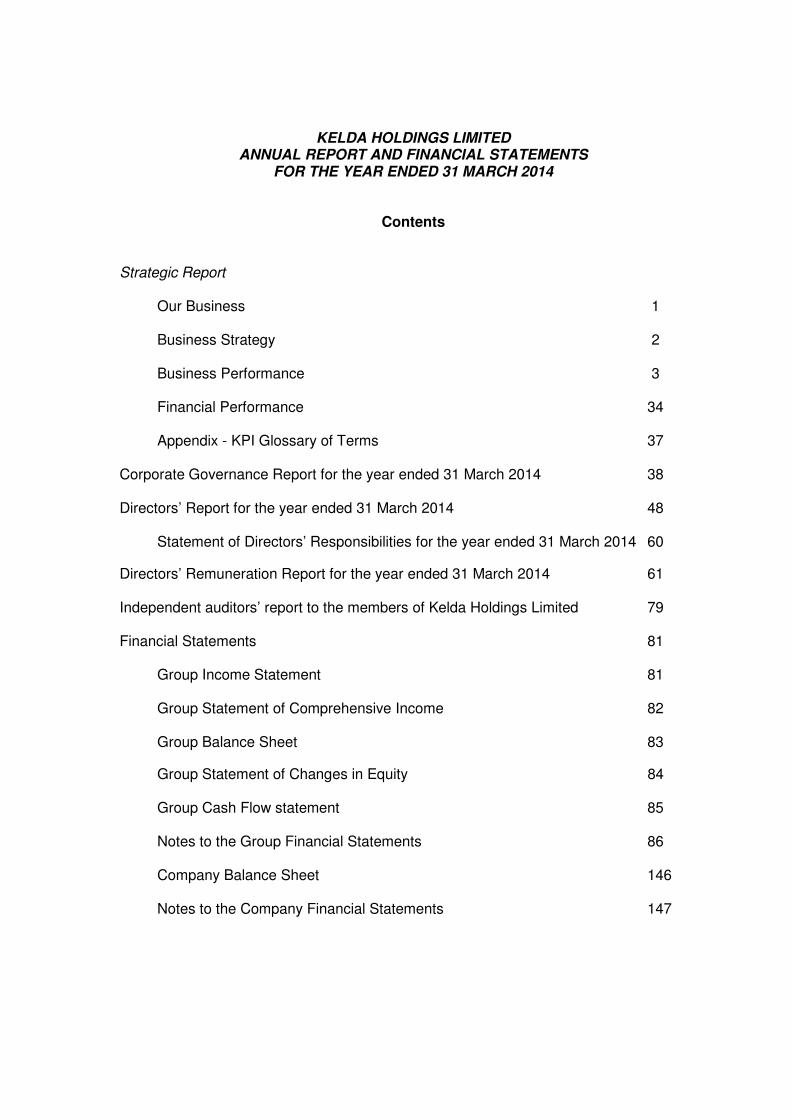

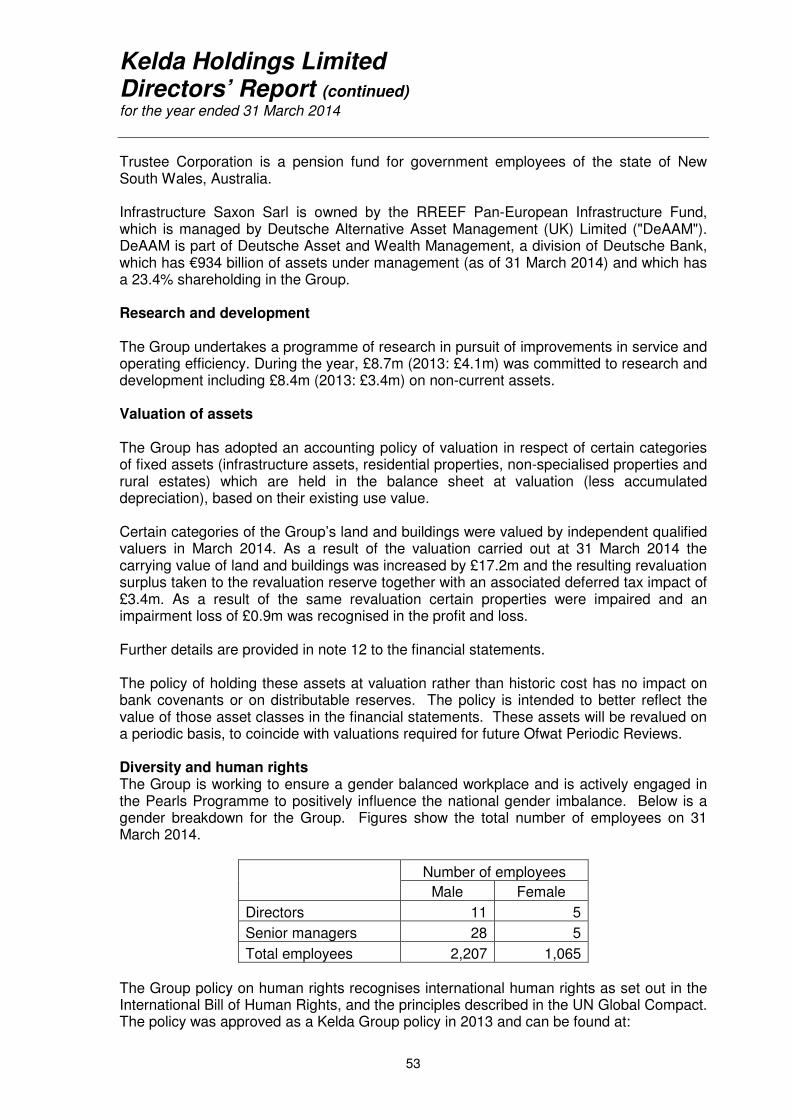

Contents Strategic Report Our Business 1 Business Strategy 2 Business Performance 3 Financial Performance 34 Appendix - KPI Glossary of Terms 37 Corporate Governance Report for the year ended 31 March 2014 38 Directors’ Report for the year ended 31 March 2014 48

Statement of Directors’ Responsibilities for the year ended 31 March 2014 60

Directors’ Remuneration Report for the year ended 31 March 2014 61 Independent auditors’ report to the members of Kelda Holdings Limited 79 Financial Statements 81

Group Income Statement 81 Group Statement of Comprehensive Income 82 Group Balance Sheet 83

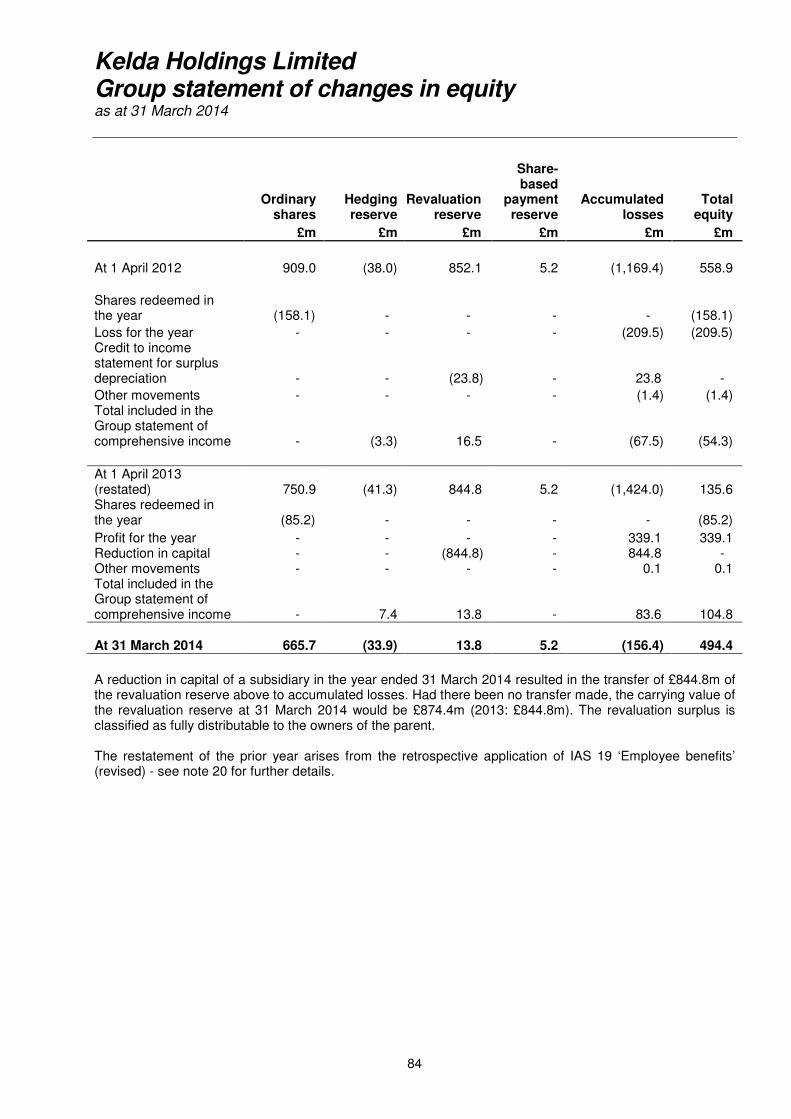

Group Statement of Changes in Equity 84 Group Cash Flow statement 85 Notes to the Group Financial Statements 86 Company Balance Sheet 146 Notes to the Company Financial Statements 147

Kelda Holdings Limited Strategic Report for the year ended 31 March 2014

1

OUR BUSINESS Kelda Holdings Limited (the Company) and its subsidiaries, joint ventures and associates (the Group) is made up of several businesses: Yorkshire Water Yorkshire Water Services Limited (Yorkshire Water) is the principal UK subsidiary of the Group, providing water and waste water services to more than 4.9 million people and 130,000 businesses. Every day, Yorkshire Water supplies around 1.3 billion litres of water to homes and businesses in Yorkshire. Through the efficient operation of its extensive waste water network and treatment facilities, it also ensures that the region’s domestic and industrial waste is returned safely to the environment. Business strategy: Yorkshire Water’s vision is ‘Taking responsibility for the water environment for good’. There are six strategic objectives that shape everything the business does:

• Trusted company; • Safe water; • Excellent catchments, rivers and coasts; • Water efficient regions; • Sustainable resources; and • Strong financial foundations.

UK Service Operations Kelda Water Services Kelda Water Services Limited (KWS) is a major participant in the UK water and waste water contract operations market, with contracts during the year 2013/14 in England, Scotland and Northern Ireland. Business strategy:

• Leveraging the value from Group assets and skills. • Maximising value from our existing business. • Continuing to grow through new opportunities in the water, waste water and related

markets. Loop Loop Customer Management Limited (Loop) specialises in cost effective customer relationship management. Loop’s main contract is to provide customer service support to Yorkshire Water. KeyLand KeyLand Developments Limited (KeyLand) adds value to the Group’s surplus property assets, usually by obtaining planning permission for the most beneficial use and selling into the market or undertaking development in partnership with others. The results of KeyLand include the Group’s share of its associates and joint ventures. Business strategy:

• Adding value to the Group’s surplus property assets and to maximise proceeds from the sale of those assets.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

2

BUSINESS STRATEGY The Group has a vision – ‘taking responsibility for the water environment for good’. The essence of the vision is doing what’s right - for our customers, colleagues, partners and the environment. To achieve the vision the Group has developed a plan and the plan has been named Blueprint. Blueprint is something everyone can contribute towards to make a difference. Our strategic objectives: To deliver the plan the Group has developed six Strategic Business Objectives (SBOs). These SBOs shape everything the Group does. These are our six strategic objectives, that shape everything we do: Trusted company – The way the Group does business means its products, services and promises are trusted by all our stakeholders, now and in the future. Safe Water – The Group works safely to protect public health by ensuring drinking water is always safe to drink and waste water never harms customers or communities at any point in the process. Excellent catchments, rivers and coasts – The Group maintains and improves the water environment from source to sea and influences others to do the same. Water efficient regions – The Group ensures water needs are met now and in the future by using water wisely and inspiring others to do the same. Sustainable resources – The Group is efficient and effective now and in the future, with an industry leading workforce, zero waste and a responsible supply chain. Strong financial foundations – The Group delivers services to customers at a price they are willing and able to pay, whilst providing investors with returns that attract long-term investment. The above strategic business objectives apply to all business of the Group. Kelda Water Services, Loop and KeyLand have additional strategic objectives specific to their circumstances.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

3

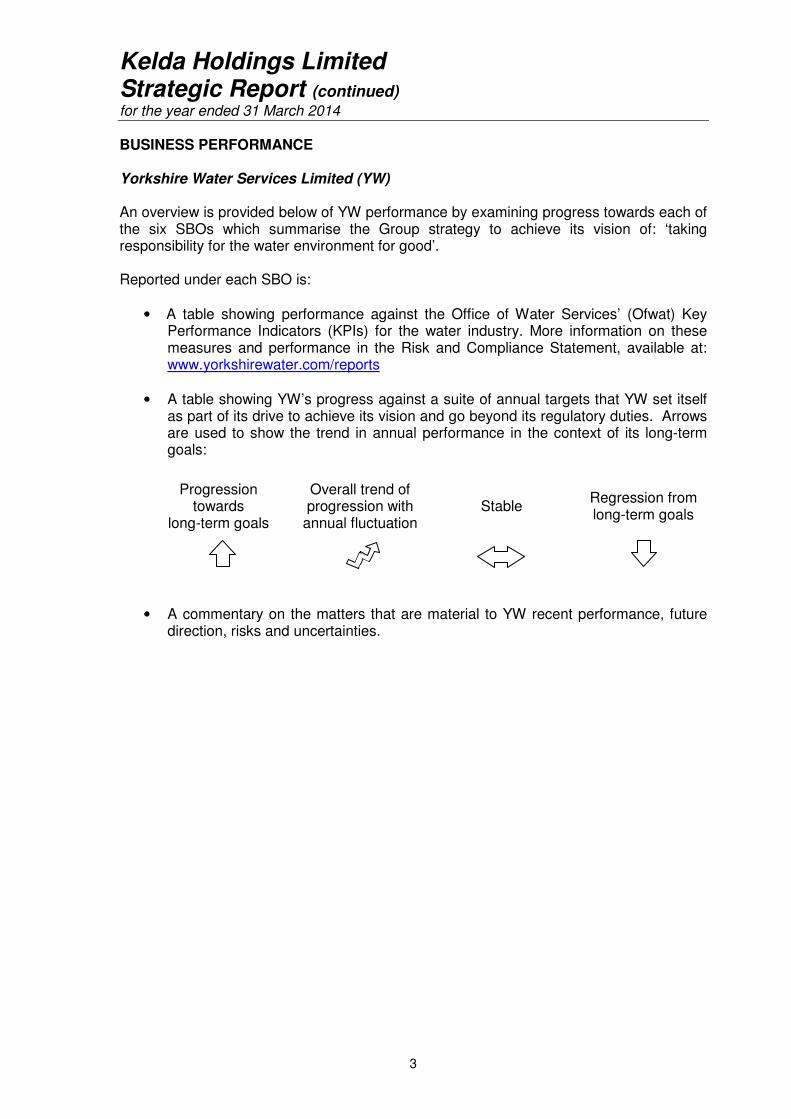

BUSINESS PERFORMANCE Yorkshire Water Services Limited (YW) An overview is provided below of YW performance by examining progress towards each of the six SBOs which summarise the Group strategy to achieve its vision of: ‘taking responsibility for the water environment for good’. Reported under each SBO is:

• A table showing performance against the Office of Water Services’ (Ofwat) Key Performance Indicators (KPIs) for the water industry. More information on these measures and performance in the Risk and Compliance Statement, available at: www.yorkshirewater.com/reports

• A table showing YW’s progress against a suite of annual targets that YW set itself

as part of its drive to achieve its vision and go beyond its regulatory duties. Arrows are used to show the trend in annual performance in the context of its long-term goals:

Progression towards

long-term goals

Overall trend of progression with

annual fluctuation Stable

Regression from long-term goals

• A commentary on the matters that are material to YW recent performance, future

direction, risks and uncertainties.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

4

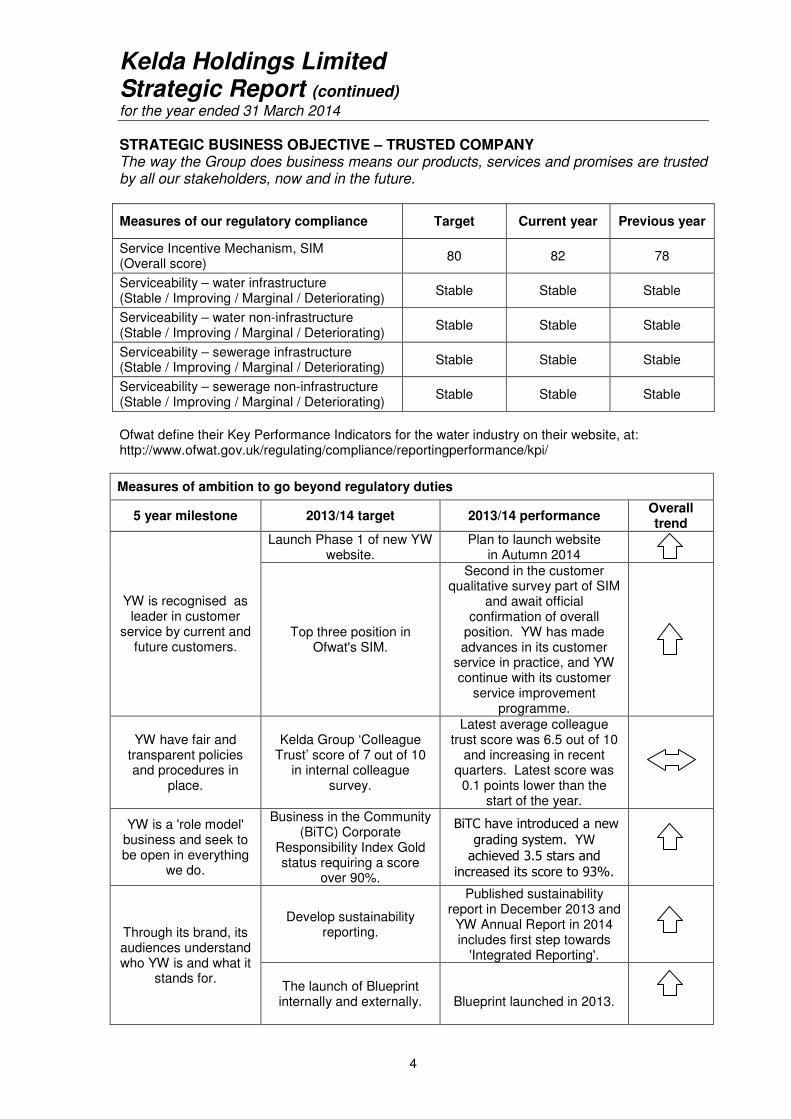

STRATEGIC BUSINESS OBJECTIVE – TRUSTED COMPANY The way the Group does business means our products, services and promises are trusted by all our stakeholders, now and in the future.

Measures of our regulatory compliance Target Current year Previous year

Service Incentive Mechanism, SIM (Overall score)

80 82 78

Serviceability – water infrastructure (Stable / Improving / Marginal / Deteriorating)

Stable Stable Stable

Serviceability – water non-infrastructure (Stable / Improving / Marginal / Deteriorating)

Stable Stable Stable

Serviceability – sewerage infrastructure (Stable / Improving / Marginal / Deteriorating)

Stable Stable Stable

Serviceability – sewerage non-infrastructure (Stable / Improving / Marginal / Deteriorating)

Stable Stable Stable

Ofwat define their Key Performance Indicators for the water industry on their website, at: http://www.ofwat.gov.uk/regulating/compliance/reportingperformance/kpi/

Measures of ambition to go beyond regulatory duties

5 year milestone 2013/14 target 2013/14 performance Overall trend

YW is recognised as leader in customer

service by current and future customers.

Launch Phase 1 of new YW website.

Plan to launch website in Autumn 2014

Top three position in Ofwat's SIM.

Second in the customer qualitative survey part of SIM

and await official confirmation of overall

position. YW has made advances in its customer

service in practice, and YW continue with its customer

service improvement programme.

YW have fair and transparent policies and procedures in

place.

Kelda Group ‘Colleague Trust’ score of 7 out of 10

in internal colleague survey.

Latest average colleague trust score was 6.5 out of 10

and increasing in recent quarters. Latest score was

0.1 points lower than the start of the year.

YW is a 'role model' business and seek to be open in everything

we do.

Business in the Community (BiTC) Corporate

Responsibility Index Gold status requiring a score

over 90%.

BiTC have introduced a new

grading system. YW

achieved 3.5 stars and increased its score to 93%.

Through its brand, its audiences understand who YW is and what it

stands for.

Develop sustainability reporting.

Published sustainability report in December 2013 and

YW Annual Report in 2014 includes first step towards

'Integrated Reporting'.

The launch of Blueprint internally and externally.

Blueprint launched in 2013.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

5

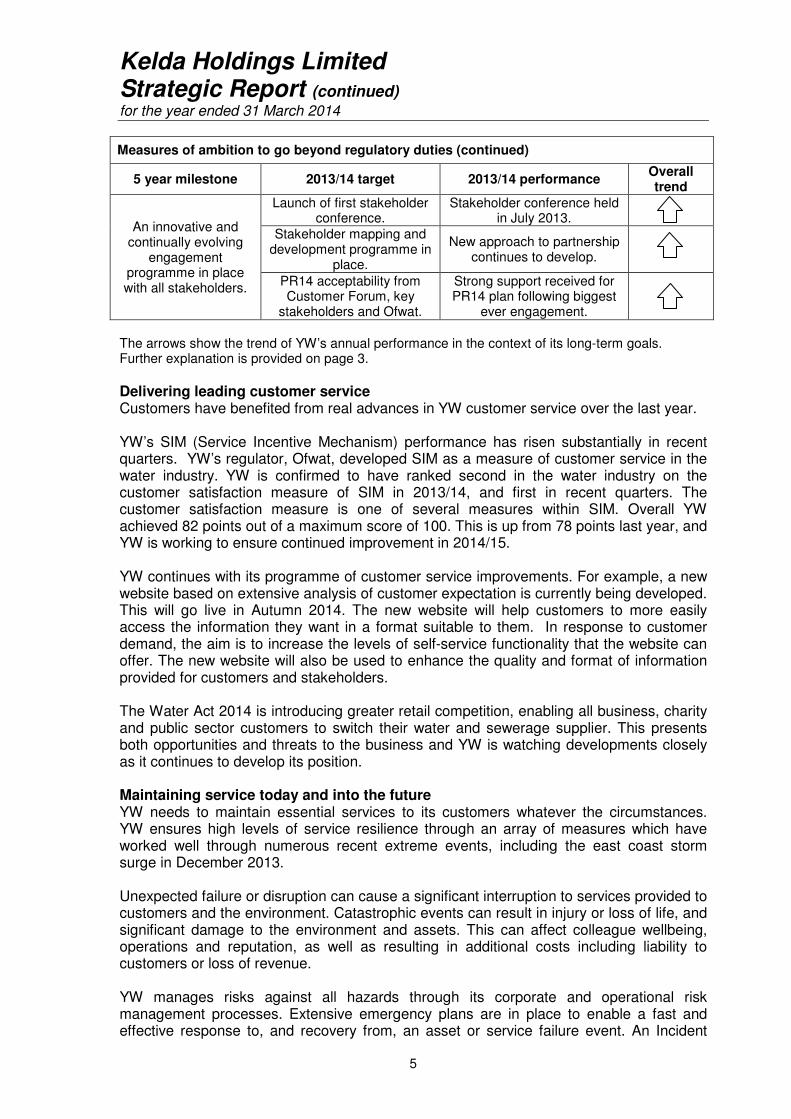

Measures of ambition to go beyond regulatory duties (continued)

5 year milestone 2013/14 target 2013/14 performance Overall trend

An innovative and continually evolving

engagement programme in place with all stakeholders.

Launch of first stakeholder conference.

Stakeholder conference held in July 2013.

Stakeholder mapping and development programme in

place.

New approach to partnership continues to develop.

PR14 acceptability from Customer Forum, key

stakeholders and Ofwat.

Strong support received for PR14 plan following biggest

ever engagement.

The arrows show the trend of YW’s annual performance in the context of its long-term goals. Further explanation is provided on page 3. Delivering leading customer service Customers have benefited from real advances in YW customer service over the last year. YW’s SIM (Service Incentive Mechanism) performance has risen substantially in recent quarters. YW’s regulator, Ofwat, developed SIM as a measure of customer service in the water industry. YW is confirmed to have ranked second in the water industry on the customer satisfaction measure of SIM in 2013/14, and first in recent quarters. The customer satisfaction measure is one of several measures within SIM. Overall YW achieved 82 points out of a maximum score of 100. This is up from 78 points last year, and YW is working to ensure continued improvement in 2014/15. YW continues with its programme of customer service improvements. For example, a new website based on extensive analysis of customer expectation is currently being developed. This will go live in Autumn 2014. The new website will help customers to more easily access the information they want in a format suitable to them. In response to customer demand, the aim is to increase the levels of self-service functionality that the website can offer. The new website will also be used to enhance the quality and format of information provided for customers and stakeholders. The Water Act 2014 is introducing greater retail competition, enabling all business, charity and public sector customers to switch their water and sewerage supplier. This presents both opportunities and threats to the business and YW is watching developments closely as it continues to develop its position. Maintaining service today and into the future YW needs to maintain essential services to its customers whatever the circumstances. YW ensures high levels of service resilience through an array of measures which have worked well through numerous recent extreme events, including the east coast storm surge in December 2013. Unexpected failure or disruption can cause a significant interruption to services provided to customers and the environment. Catastrophic events can result in injury or loss of life, and significant damage to the environment and assets. This can affect colleague wellbeing, operations and reputation, as well as resulting in additional costs including liability to customers or loss of revenue. YW manages risks against all hazards through its corporate and operational risk management processes. Extensive emergency plans are in place to enable a fast and effective response to, and recovery from, an asset or service failure event. An Incident

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

6

Management Framework provides a staged response to ensure the effective allocation of resource to any incident. To ensure that YW can provide services today and long into the future, over a million pounds a day is invested to maintain and enhance the legacy of assets and infrastructure. This includes over 700 treatment works, thousands of pumping stations and enough pipes to stretch around the world. In 2013/14 YW achieved “stable serviceability” in all four asset categories for the second year running. Serviceability is a measure used by the water industry to demonstrate the effectiveness of asset maintenance. Further details on YW’s serviceability performance can be found in YW’s Risk and Compliance Statement publication, available at: www.yorkshirewater.com.reports. Planning for long-term challenges like population growth, climate change and decreasing availability of resources is also in progress. In 2013 YW published a suite of documents about its plans for the future, called Blueprint for Yorkshire. One document examines, and is called, ‘the next 25 years’. YW’s ‘climate change strategy’ explains how it is working to ensure it can affordably maintain and enhance services in the changing climate, and cost-effectively reduce its carbon emissions. Both reports are available at www.BlueprintForYorkshire.com. YW is required to publish an annual Risk and Compliance Statement each year by its regulator, Ofwat. In this year’s Risk and Compliance Statement the YW board identified pollution incidents and discharge permits compliance as material or potentially material risks. Mitigation plans have been put in place to tackle the potential risks, details of which can be obtained in the Statement publication, available at: www.yorkshirewater.com.reports. Details of these risks and the management responses are also found in this report. Further details on company performance and management responses to both these risk areas can be found in the Excellent Catchments, Rivers and Coasts SBO section of this report. Engaging with customers and stakeholders In 2013/14 YW completed its biggest ever customer and stakeholder engagement programme. To inform the development of its business plan for the period from 2015 to 2020 and beyond, the views of more than 30,000 customers and 100 stakeholder groups were obtained. YW established an independent Customer Forum to help ensure that its customers had a fair say in its plans. The independent Forum represents the needs of customers and the environment in the Yorkshire region. The Forum challenged YW to be more transparent, to strike the right balance between customer needs and environmental leadership, and to do everything it could to keep bills low. YW will continue to work with the Forum in the future to ensure that customers have an on-going say in its plans. YW held a stakeholder conference at the Yorkshire Event Centre in Harrogate in July 2013, to share and discuss its plans.The event was attended by representatives from more than 80 different organisations, including Local Authorities, NGO’s, businesses, academic institutions and investor groups. YW aims to have an innovative and continually evolving engagement programme in place with all its stakeholders. One way this will be achieved is through a new research and

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

7

insight team who will manage regular engagement activities and help ensure decisions are based on customer insight. Full details of YW customer engagement and plans can be found at: www.BlueprintForYorkshire.com. Working in partnership Working in partnership is becoming ever more important to effectively and efficiently address priorities such as flooding and pollution. YW has many examples of where it is already working with others to deliver greater benefits for the region, but it also recognises that there is a need to do more of this. YW is currently formalising its approach to partnership and stakeholder relationship management. This will help YW to ensure that it manages stakeholder relationships in a tailored way that best suits both parties, and that it is effective in developing partnerships where they have the biggest benefits for its customers and wider society. YW has worked in partnership with various organisations for many years. For example:

• YW worked closely with the Environment Agency and Local Authorities on the regions flood management by sharing data and hydraulic models, and sharing resources in emergencies;

• YW is an active member of the Yorkshire Bathing Water Partnership that has been successful in growing the number of Blue Flag beaches in the region; and

• YW continues to restore and protect vast areas of Yorkshire’s uplands by working closely with organisations like the Yorkshire Peat Partnership and local land owners.

Supporting the community YW leads an extensive community engagement programme to go beyond its regulatory duties by providing support and help-in-kind to a wide variety of different organisations across Yorkshire. YW encourages and supports colleagues in volunteering, charitable giving and community involvement. One in three employees is active in a wide range of supported community activities. Support was provided in three key areas:

• Education – raising awareness of young people and local communities on the value of water and their role and YW’s in safeguarding this precious resource;

• Environment - playing a key role as one of Yorkshire's largest landowners in enhancing the natural and built environment; and

• Empowerment - providing opportunities for colleagues to share skills with the local community through employee-supported volunteering.

Benchmarking the approach to being a responsible business YW uses the Business in the Community (BiTC) Corporate Responsibility Index as one way to benchmark its performance against its peers each year. The BiTC Index is the UK’s leading voluntary benchmark of corporate responsibility. In 2013/14 YW’s score increased to 93%, up from 90% the previous year. YW has also been awarded a BiTC Big Tick in their Responsible Business Awards 2013/14. The increase in the score and the success in winning a Big Tick provides external assurance that YW is among the leaders in corporate social responsibility and sustainability. Managing colleague trust The strong performance achieved in 2013/14 was as a result of the hard work, commitment and energy of all colleagues. It was a demanding year of change, not least because of an organisational restructure and change to pension plans. In addition,

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

8

colleagues were affected by the external national debate in the media about YW and other utilities. Generally, colleagues say they are proud to work for YW as a provider of essential and quality water and waste services. However, through internal surveys and regular leadership feedback sessions, colleagues indicated that trust fell in the second quarter of 2013/14. Recognising that trust is something that needs regular reinforcement, YW’s business leaders have made colleague trust a business priority in 2014/15. Trust is already a strong foundation for YW and its plan is to continue to build on this, for example through more visible leadership, stronger internal communications and engagement, improved problem resolution, greater employee recognition and increased partnership working with trade unions. Our corporate structure and tax position We provide below an explanation of the Group’s corporate structure and tax position. In addition to the information we provide below, a summary overview of our principal subsidiary Yorkshire Water can be found at: http://www.yorkshirewater.com/reports Corporate structure The structure of the Kelda Group has developed and changed since privatisation of the water industry in 1989. A description of the main operating companies in the Group is given below. A project is taking place to streamline the corporate structure to remove dormant or non-trading companies where it is efficient and expedient to do so. Details of the equity ownership of the company can be found on pages 52 and 53. Details of the debt and capital structures of the company can be found on its website at: http://www.keldagroup.com Kelda Finance (No.2) Limited ("KF2") and Kelda Finance (No.3) plc ("KF3") have been established to raise debt finance (KF2 bank debt, KF3 bond debt) for the Kelda group of companies, outside of the Yorkshire Water ring fenced financing group. Kelda Finance (No.1) Limited has been established to act as a guarantor for KF2 and KF3. Throughout the Group, we abide by the following overriding principles in everything we do regarding our corporate structure and approach to taxation:

•we have and follow a tax policy which requires that we fully comply with the letter and the spirit of UK tax law;

•we structure ourselves to be able to borrow money at the lowest possible rates in order to support low bills for our customers and fair returns for our investors; and

•we do not establish overseas companies in order to avoid paying UK tax.

Yorkshire Water and Whole Business Securitisation In order to borrow at the lowest possible rates, Yorkshire Water established a financing structure known as a "whole business securitisation" (WBS) in 2009. The WBS enhances the creditworthiness of Yorkshire Water by setting strict rules that demonstrate to lenders the company is a safe and reliable business to invest in. Lenders are therefore more prepared to lend to Yorkshire Water at lower rates of interest than would otherwise be the case. Customers share the benefit of the lower rates of interest because the rates at which the industry borrows are factored into prices.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

9

This WBS works by placing a protective ring-fence around Yorkshire Water's business which includes: the way it operates; the way it trades with other Group companies; and, the way it finances itself. The protections include limits on borrowings, dividends and the ability to lend money to other Kelda companies. The protections also require profits to more than cover the amount of interest that Yorkshire Water pays. To enable the WBS it was necessary for Yorkshire Water to establish three companies incorporated in the Cayman Islands. These are:

•Yorkshire Water Services Bradford Finance Limited (issues new corporate debt); •Yorkshire Water Services Odsal Finance Limited (issuer of legacy corporate debt);

and •Yorkshire Water Services Odsal Finance Holdings Limited (a non-trading, holding

company). Due to technical reasons applicable at the time that our owners purchased the Kelda Group and we set up the WBS, it was necessary to establish these companies in the Cayman Islands in order to raise debt listed on bond markets. The technical requirements for these companies are no longer relevant but the cost of unwinding this structure is prohibitive. All three companies are wholly and exclusively resident for tax in the UK and file their tax returns only with Her Majesty’s Revenue and Customs (HMRC). This means that any profit or loss made by these companies is subject only to UK tax. Other Group companies Other companies in the Group fall into three categories. 1.Those operating and resident for tax in the UK The following Group companies operate in the UK and are wholly and exclusively resident for tax in the UK:

•Kelda Water Services Limited (KWS) – operates water and waste water contracts across the UK;

•Loop Customer Management Limited (Loop) – delivers customer service support to Yorkshire Water that includes billing, debt recovery and incident management; and

•KeyLand Developments Limited (KeyLand) – manages the Group's surplus property assets, either on its own or in partnership with outside organisations.

2.Those incorporated overseas and resident for tax in the UK In addition to those companies registered in the Cayman Islands, noted above, the Group contains two other companies that are incorporated in jurisdictions outside the UK but which are wholly and exclusively resident for tax in the UK:

•Kelda Holdings Limited - the ultimate parent company of Yorkshire Water. The company is incorporated in Jersey to allow greater choice as to the manner in which distributions can be made to shareholders; and

•Yorkshire Water Holdings BV - a subsidiary incorporated in the Netherlands. This company is a legacy from previous activity and does not trade.

3.Those incorporated and resident for tax overseas The Group contains three companies that are incorporated and are resident for tax in jurisdictions outside the UK:

•Kelda Group Inc. and KGI Bridgeport Company - two subsidiaries that administered a sewerage contract in Connecticut until the contract ended in December 2013. The companies are resident for tax in the USA and are in the

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

10

process of winding down their operations. The companies did not trade with the rest of Kelda Group; and

•Ridings Insurance Company Limited - insurance company operating and resident for tax purposes in the Isle of Man. The Group operates this insurance company to allow flexibility in how it insures its public liability where the insurance market proves uneconomical or unable to supply the required cover. In 2013/14 this company’s turnover was less than £250,000.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

11

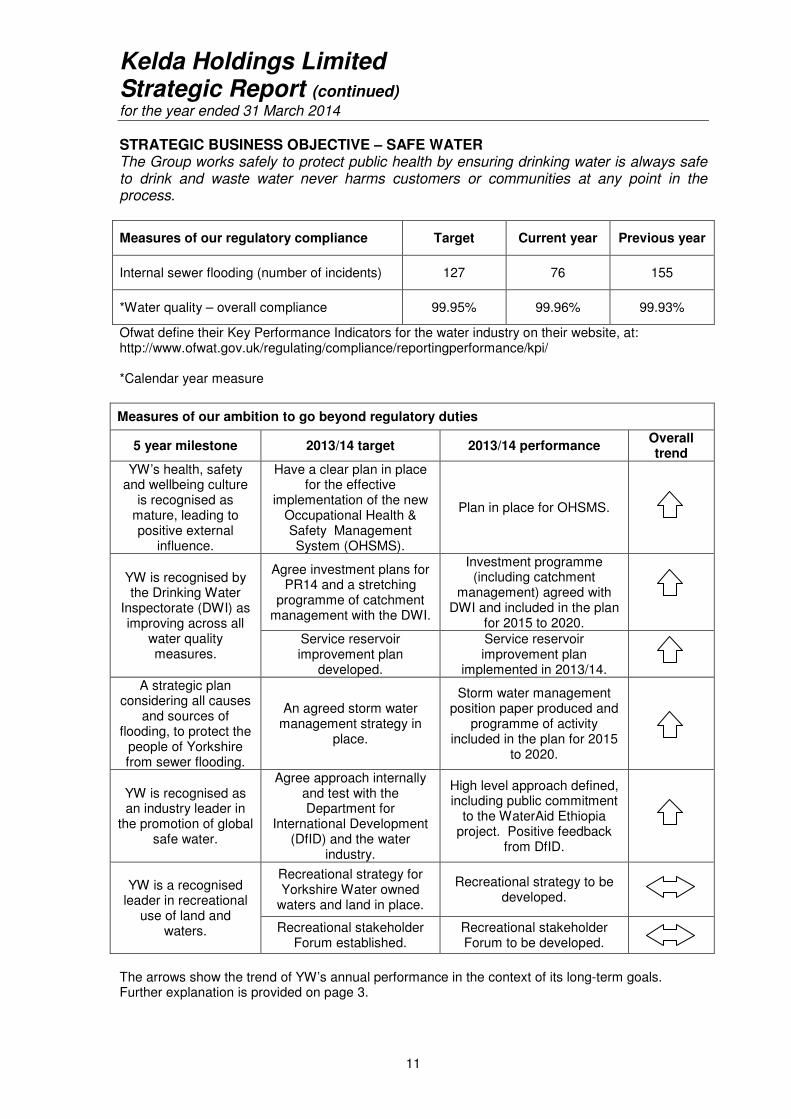

STRATEGIC BUSINESS OBJECTIVE – SAFE WATER

The Group works safely to protect public health by ensuring drinking water is always safe to drink and waste water never harms customers or communities at any point in the process.

Measures of our regulatory compliance Target Current year Previous year

Internal sewer flooding (number of incidents) 127 76 155

*Water quality – overall compliance 99.95% 99.96% 99.93%

Ofwat define their Key Performance Indicators for the water industry on their website, at: http://www.ofwat.gov.uk/regulating/compliance/reportingperformance/kpi/ *Calendar year measure

Measures of our ambition to go beyond regulatory duties

5 year milestone 2013/14 target 2013/14 performance Overall trend

YW’s health, safety and wellbeing culture

is recognised as mature, leading to positive external

influence.

Have a clear plan in place for the effective

implementation of the new Occupational Health & Safety Management System (OHSMS).

Plan in place for OHSMS.

YW is recognised by the Drinking Water

Inspectorate (DWI) as improving across all

water quality measures.

Agree investment plans for PR14 and a stretching

programme of catchment management with the DWI.

Investment programme (including catchment

management) agreed with DWI and included in the plan

for 2015 to 2020.

Service reservoir improvement plan

developed.

Service reservoir improvement plan

implemented in 2013/14.

A strategic plan considering all causes

and sources of flooding, to protect the

people of Yorkshire from sewer flooding.

An agreed storm water management strategy in

place.

Storm water management position paper produced and

programme of activity included in the plan for 2015

to 2020.

YW is recognised as an industry leader in

the promotion of global safe water.

Agree approach internally and test with the Department for

International Development (DfID) and the water

industry.

High level approach defined, including public commitment

to the WaterAid Ethiopia project. Positive feedback

from DfID.

YW is a recognised leader in recreational

use of land and waters.

Recreational strategy for Yorkshire Water owned

waters and land in place.

Recreational strategy to be developed.

Recreational stakeholder Forum established.

Recreational stakeholder Forum to be developed.

The arrows show the trend of YW’s annual performance in the context of its long-term goals. Further explanation is provided on page 3.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

12

Putting people’s health, safety and wellbeing first To achieve the vision and SBOs, it is essential that YW works to prevent harm and protect health across all stages of its business operations, environments and communities. The drive for continual improvement is supported by an Occupational Health & Safety Management System (OHSMS). This enables the company to enhance its health and safety performance and to maintain a clear focus on meeting the needs of our people, stakeholders, customers and members of the public. This is at the heart of the company approach. Further information on the Group’s health and safety approach is detailed in the Directors’ report on pages 56 and 57. Maintaining excellent drinking water quality Protecting public health is a primary duty. Drinking water quality within Yorkshire remains excellent, amongst the best in the world. In 2013/14, YW’s compliance increased to 99.96% of thousands of samples meeting tight regulatory standards. YW completed a large service reservoir inspection and improvement programme in 2013/14 to contribute to this performance improvement and manage a risk of microbiological failures. Further details on YW’s water quality performance can be found in the Risk and Compliance Statement publication, available at: www.yorkshirewater.com.reports. Over the past two decades, raw water quality has deteriorated in many catchment areas. The more polluted raw water is, the more the need to treat it to make it fit for drinking. A twin-track approach is used to ensure that customers receive high quality drinking water despite the deteriorating raw water quality. YW is investing to enhance treatment capabilities where the probability of failure presents an unacceptable risk to customers. The long-standing programme of capital investment will continue with a further £49m of investment in the period from 2015 to 2020, including action at six large treatment works. Investment in catchment management, as a primary long-term response to address the issue at source, is also planned. The approach to catchment management is outlined in the section on the Excellent Catchments, Rivers and Coasts SBO. Reducing flood risk In 2013/14 YW removed 66 properties from being at risk of sewer flooding and reduced the overall number of properties at risk of sewer flooding on the regulated risk register to 204 across the region. YW continues to invest in the region’s drainage network and reduce the number of properties at risk from sewer flooding. Further details on YW’s sewer flooding performance can be found in the Risk and Compliance Statement publication, available at: www.yorkshirewater.com.reports. YW played an active role in the response to the east coast storm surge in December 2013, described as the most serious UK storm surge for over 60 years. YW had representatives at the two Strategic Command Centres which operated in East and North Yorkshire to manage the response. YW assets were utilised in Hull to remove 35,000 tonnes of water from the city. Services were maintained, despite damage to YW assets. YW also offered assistance to the Environment Agency (EA) during the extensive flooding to the south and west of the UK during the early part of 2014. YW is working in ever closer partnership with other flood management authorities, for example:

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

13

• YW worked with Calderdale MBC and the EA on reducing flood risk in the Calder Valley;

• YW is sharing information with the Lead Local Flood Authorities identifying relatively low cost joint funding flood schemes, notably in Sheffield and East Riding of Yorkshire; and

• YW is playing an active part in the Yorkshire Regional Flood and Coastal Committee (RFCC) and all four sub-regional strategic flood management partnerships, by sharing its future flood and investment plans and informing the RFCC of the investment framework and plans.

YW is also investing to protect its own assets from flood risk to enhance the resilience of its services. For example, YW has invested at Hull and Market Weighton to provide a 1 in 1,000 year level of protection at these key sites, and YW is investing at Moor Monkton in 2014/15. Extreme weather and urban growth are causing increasing pressure on the sewer network and the risk of flooding. YW is planning for the future and produced both its climate change strategy and storm water management position paper in 2013. YW will continue to invest to mitigate the risk and manage the consequences of sewer flooding. One part of the plans is a new £8m fund for flood partnership projects. The company is also focusing on customer behaviour by developing education and awareness programmes to sewer blockages caused by customer activities, in particular disposal of fats, oil and greases (FOGs), nappies, wipes and other materials which are inappropriately disposed of via the sewer network. For example, YW has been trialling an approach of customer engagement combined with above ground collection of FOGs in an area of Bradford where the company has observed repeated sewer blockages. Supporting global safe water As Kelda Group, we recognise a moral obligation to support those who do not have access to clean safe drinking water and safe sanitation. Around the world, 3.4 million people die each year from water related diseases and 780 million people lack access to safe clean drinking water. We have a long history of fund raising for WaterAid, and our SBO ambition is to go much further. Our aim is to be globally recognised as a leader in the delivery of safe water. We have recently launched a strategic partnership with WaterAid Ethiopia. This will deliver knowledge sharing on water and sanitation, provide infrastructure support, fundraising and much more. We recognise that we are at the early stages of a long-term ambition and we continue to develop our approach. Providing access to land YW is one of the largest land and open-water owners in Yorkshire. YW owns approximately 29,000 hectares of land which includes upland moors, woodland of mixed age and species, reservoirs, and the land that is rented to farmers. For many years YW has provided open access to much of its large estate, particularly the woodland and upland moors. This has provided a wide range of recreational opportunities that include 100 km of permissive footpath, 33 km of permissive bridleway/cycle routes, two nature reserves, two fisheries and a range of ancillary facilities such as car parks, picnic sites, toilets and information points in addition to 1,100 km of public rights of way and Countryside and Rights of Way Act (CRoW) access land.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

14

YW works to ensure large numbers of people can safely enjoy its land and YW is dedicated to increasing its recreational offering through direct management and lease arrangements. The Tour de France came to Yorkshire in 2014, and YW played its part to make sure the event was a global success, and that YW’s land and waters supported the growing recreational demand brought by the event. Find out more on the website at: http://www.yorkshirewater.com/walks-and-leisure.aspx

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

15

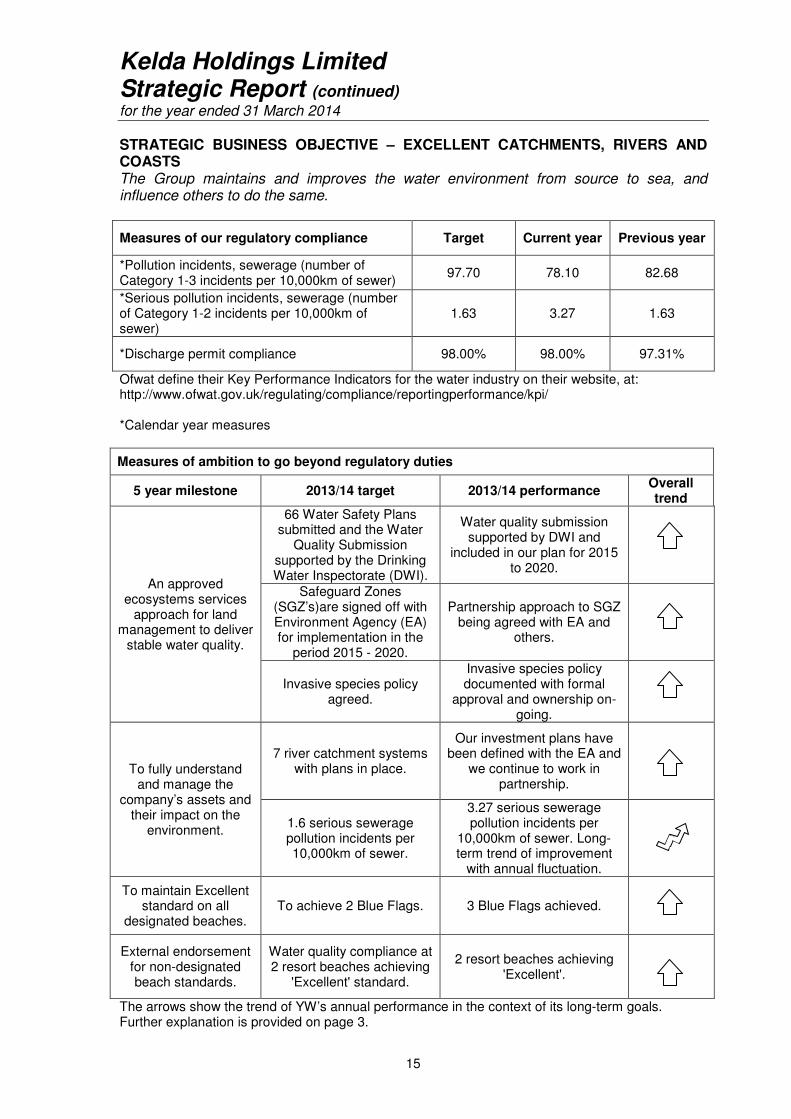

STRATEGIC BUSINESS OBJECTIVE – EXCELLENT CATCHMENTS, RIVERS AND COASTS The Group maintains and improves the water environment from source to sea, and influence others to do the same.

Measures of our regulatory compliance Target Current year Previous year

*Pollution incidents, sewerage (number of Category 1-3 incidents per 10,000km of sewer)

97.70 78.10 82.68

*Serious pollution incidents, sewerage (number of Category 1-2 incidents per 10,000km of sewer)

1.63 3.27 1.63

*Discharge permit compliance 98.00% 98.00% 97.31%

Ofwat define their Key Performance Indicators for the water industry on their website, at: http://www.ofwat.gov.uk/regulating/compliance/reportingperformance/kpi/ *Calendar year measures

Measures of ambition to go beyond regulatory duties

5 year milestone 2013/14 target 2013/14 performance Overall trend

An approved ecosystems services

approach for land management to deliver

stable water quality.

66 Water Safety Plans submitted and the Water

Quality Submission supported by the Drinking Water Inspectorate (DWI).

Water quality submission supported by DWI and

included in our plan for 2015 to 2020.

Safeguard Zones (SGZ’s)are signed off with Environment Agency (EA) for implementation in the

period 2015 - 2020.

Partnership approach to SGZ being agreed with EA and

others.

Invasive species policy agreed.

Invasive species policy documented with formal

approval and ownership on-going.

To fully understand and manage the

company’s assets and their impact on the

environment.

7 river catchment systems with plans in place.

Our investment plans have been defined with the EA and

we continue to work in partnership.

1.6 serious sewerage pollution incidents per 10,000km of sewer.

3.27 serious sewerage pollution incidents per

10,000km of sewer. Long-term trend of improvement

with annual fluctuation.

To maintain Excellent standard on all

designated beaches. To achieve 2 Blue Flags. 3 Blue Flags achieved.

External endorsement for non-designated beach standards.

Water quality compliance at 2 resort beaches achieving

'Excellent' standard.

2 resort beaches achieving 'Excellent'.

The arrows show the trend of YW’s annual performance in the context of its long-term goals. Further explanation is provided on page 3.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

16

Reducing pollution and enhancing river water quality YW is responsible for collecting, treating and returning about 1 billion litres of waste water safely back to the environment every day. Over the last 20 years, by investing to enhance waste water treatment capabilities, YW has delivered a step change in river water quality. YW improved its performance on waste water treatment in 2013/14, with discharge permit compliance reaching 98%. YW also continued its on-going capital investment programme, responding to new legislative drivers and population growth. Plans are in place to further improve discharge permit compliance, details of which can be obtained in the Risk and Compliance Statement publication available at: www.yorkshirewater.com.reports. The total number of pollution incidents from the sewer network has continued to reduce over recent years, from 95.10 incidents per 10,000km of sewer in 2011, to 82.68 in 2012, to 78.1 last year (2013). The number of the most serious pollution incidents (Category 1 and 2) has fluctuated in recent years but shows an overall trend of improvement. Performance has fallen from 4.25 incidents per 10,000km of sewer in 2011, to YW’s best ever performance in 2012 with 1.63 incidents per 10,000 km of sewer, increasing to 3.27 in 2013. Overall, YW’s pollution performance has improved over the course of this Asset Management Period (2010 to 2015). This improvement can be attributed to the Pollution Reduction Plan, which will continue to run throughout 2014/15. YW’s plan includes a range of people, process, technology and capital investment activities. In 2014 YW will be trialling a new proactive intervention technique using weather trigger levels. It is known that dry spells cause blockages that can lead to pollution incidents so YW will jet at hot spot locations after a set number of consecutive dry days to break up and remove sewer litter before it becomes a problem. YW has been working with the EA to model the impact of discharges across the region to understand the ecological implications. Together, a programme of environmental investment and investigation needs, totalling over £300m for the period from 2015 to 2020 has been defined. YW has prioritised a series of sites to remove or bypass barriers to fish passage and in 2013 opened its first fish pass site, at Rodley in Leeds. Investing in the region’s bathing waters Investment of £110m to enhance Yorkshire’s coastal water quality is nearing completion. YW is improving the treatment capabilities of its coastal waste water treatment works, and increasing the storage capacity of its sewer network at key locations. This will help secure a step change in the region’s bathing water quality and will ensure the region’s compliance with the revised Bathing Water Directive which introduces tighter legal standards from 2015. YW is an active member of the multi-agency Yorkshire Bathing Water Partnership. This group of organisations is working together to align the region’s activities on bathing water quality and beach management. This has resulted in all of the region’s 20 bathing beaches meeting the minimum Mandatory Standard in 2013. There were no failing beaches. 16 beaches met the higher Guideline Standard and were recommended in the latest Good Beach Guide by the Marine Conservation Society, which is an improvement of six beaches since last year.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

17

The region has achieved three coveted Blue Flags this season, one more than last year. Hornsea has joined Scarborough North and Whitby and will fly the Blue Flag this bathing season. In the future, the work of the Yorkshire Bathing Water Partnership is expected to secure more beach awards for the region. Protecting raw water quality The quality of the raw water that YW abstracts has been deteriorating in many catchments over the past two decades. This is a consequence of pollution, unsustainable land management practices and climate change. YW invests in enhanced Water Treatment Works (WTW) capabilities to ensure customers always receive the highest quality drinking water. More about this is described in the Safe Water SBO section. In parallel to investment at the WTWs, issues need to be addressed at source. YW has a catchment management programme which is its primary long-term response. This covers a range of water quality parameters including colour, pesticides, nitrates and saline intrusion on reservoir, river and borehole sources. Peat moorlands are particularly important in the region because they are the source catchments for a large proportion of the drinking water. In 2013, together with the EA, Natural England and the National Farmers Union YW is starting to establish a partnership approach to the development and implementation of Safeguard Zones and supporting Safeguard Zone Action Plans. These zones and plans are being established to better protect the catchment areas that influence the quality of water abstracted for drinking water purposes. YW also worked in partnership with the EA to develop plans for each of the seven Water Framework Management catchments in its region. In December 2013 YW published its operational and investment plans for the period from 2015 to 2020. The plans were developed using a multi-agency approach and respond to recent investigations and modelling into the reasons for raw water quality failures. In early 2014, YW’s Catchment Manager joined Defra’s Best Practice Burning Group to help them develop sustainable land management guidance and policy that will better protect and enhance UK uplands. YW is working with a range of relevant organisations including the Moorland Association, Natural England and the National Farmers Union. YW’s future moorland management programme will deliver investigation and implementation activities in the catchments where colour pollution is likely to overwhelm WTW capacity in the longer term. Nitrate and other pollutants that present risks to a number of YW’s groundwater sources will be investigated Managing invasive species Invasive species present increasing challenges to the land and water YW manages, and to its assets and operations. YW has drafted a policy on its approach to invasive species and are currently formalising this internally. The draft policy has been discussed with an independent Environmental Advisory Panel and received their support for the approach. Actions have been included in the plan for 2015 to 2020 to manage invasive species. For example, working in partnership with others on projects to address riparian invasive

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

18

species as part of wider river catchment management plans. This will involve landowners working together collaboratively on whole stretches of river to maximise the success of controlling problem species.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

19

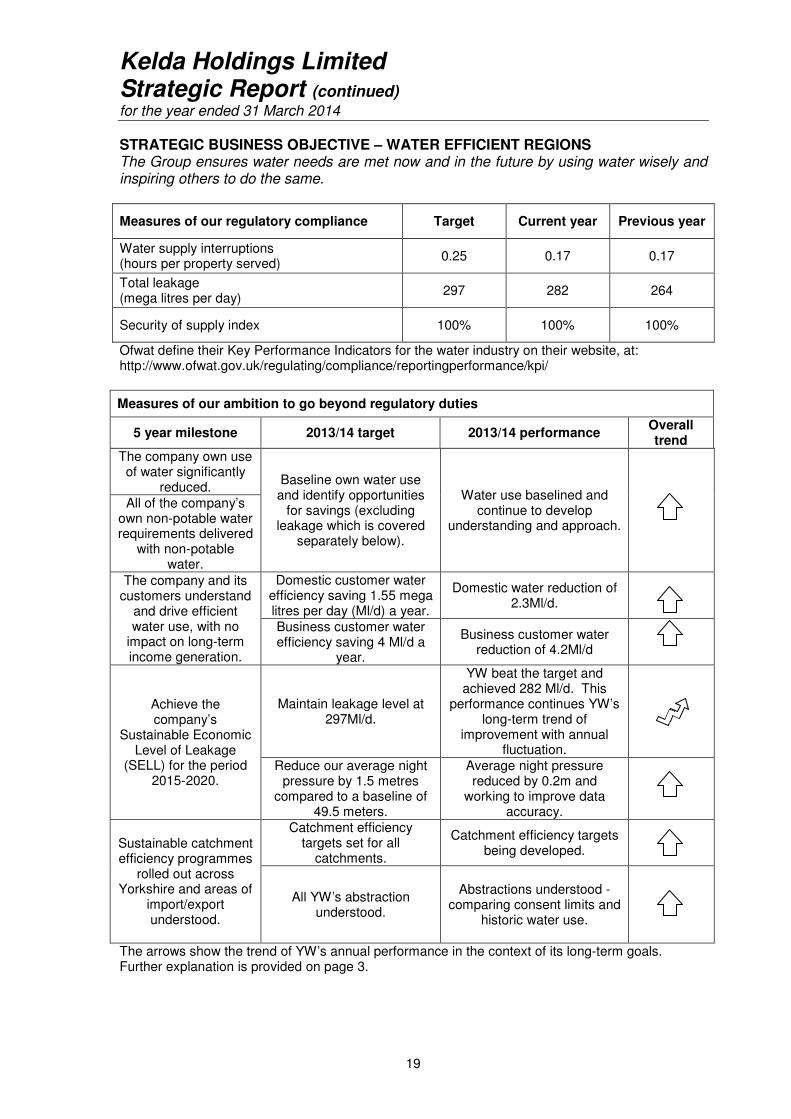

STRATEGIC BUSINESS OBJECTIVE – WATER EFFICIENT REGIONS

The Group ensures water needs are met now and in the future by using water wisely and inspiring others to do the same.

Measures of our regulatory compliance Target Current year Previous year

Water supply interruptions (hours per property served)

0.25 0.17 0.17

Total leakage (mega litres per day)

297 282 264

Security of supply index 100% 100% 100%

Ofwat define their Key Performance Indicators for the water industry on their website, at: http://www.ofwat.gov.uk/regulating/compliance/reportingperformance/kpi/

Measures of our ambition to go beyond regulatory duties

5 year milestone 2013/14 target 2013/14 performance Overall trend

The company own use of water significantly

reduced. Baseline own water use and identify opportunities

for savings (excluding leakage which is covered

separately below).

Water use baselined and continue to develop

understanding and approach.

All of the company’s own non-potable water requirements delivered

with non-potable water.

The company and its customers understand

and drive efficient water use, with no

impact on long-term income generation.

Domestic customer water efficiency saving 1.55 mega litres per day (Ml/d) a year.

Domestic water reduction of 2.3Ml/d.

Business customer water efficiency saving 4 Ml/d a

year.

Business customer water reduction of 4.2Ml/d

Achieve the company’s

Sustainable Economic Level of Leakage

(SELL) for the period 2015-2020.

Maintain leakage level at 297Ml/d.

YW beat the target and achieved 282 Ml/d. This

performance continues YW’s long-term trend of

improvement with annual fluctuation.

Reduce our average night pressure by 1.5 metres

compared to a baseline of 49.5 meters.

Average night pressure reduced by 0.2m and

working to improve data accuracy.

Sustainable catchment efficiency programmes

rolled out across Yorkshire and areas of

import/export understood.

Catchment efficiency targets set for all

catchments.

Catchment efficiency targets being developed.

All YW’s abstraction understood.

Abstractions understood - comparing consent limits and

historic water use.

The arrows show the trend of YW’s annual performance in the context of its long-term goals. Further explanation is provided on page 3.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

20

Securing water supplies Customers place a high value on the reliability of their water supply. YW operates, maintains and enhances over 50 WTWs and a distribution network of over 31,000km of water mains in order to treat and supply around 1.3 billion litres of drinking water each day. YW can be proud that, following extensive investments, Yorkshire has had no service restrictions such as hosepipe bans since the 1995/1996 drought. YW’s performance in 2013/14 remained strong, with improved performance on the length of time involved in supply interruptions, and maintained maximum possible performance on the industry measure for security of supply. YW has also shown strong performance against leakage and other water efficiency targets, which are discussed in the next sections.

The risk of water shortages or supply interruptions is a constant priority because of the consequences to customers, and to operations and finances. In 2013/14 a new Drought Plan, and the revised draft of a new Water Resources Management Plan (WRMP), were published. These plans confirm that climate change presents a growing threat to YW’s ability to maintain the balance between supply and demand. Water resources management is its most mature area of current resilience and future planning. YW has maximised the benefit of the good range and balance of water supply options in its region by developing infrastructure that allows water to be moved around the region to where it is needed. This is called the Yorkshire grid and it covers 99% of customers following completion of an extension to Scarborough in 2013. YW manages its grid to offer one of the most resilient water supply systems in the country. The revised draft WRMP describes how YW will maintain the balance between water supply and demand over the next 25 years. This has been finalised in 2014 following further engagement with Defra. The latest version can be found at: www.yorkshirewater.com/our-environment/water-resources/managing-water-resources.aspx The YW Drought Plan contains a framework of options that allow a drought to be best managed dependent on conditions. In the event of a drought, advance planning enables YW to act quickly because its options have been assessed for their cost and environmental impact, and agreed with the EA. The YW Drought Plan can be found at: www.yorkshirewater.com/our-environment/water-resources/drought-plan.aspx In 2013, YW published its plans for the period from 2015 to 2020. These plans describe the operational and investment programme to manage water services. Activities will include increasing network storage and working on projects to manage network pressure. To respond to bursts and other network problems more effectively, YW will be enhancing its visibility of the network by installing a further 4,500 data loggers that automatically send data to YW’s regional command centre every 30 minutes. Water efficiency is central to YW plans and is described below. Reducing the company’s own water use Leakage is by far the dominant source of water waste. YW measures, reports and reduces leakage, of which about two thirds results from its distribution network and a third is from leaks in customers’ supply pipes. YW have almost halved leakage since 1995 and recorded its lowest ever levels in 2012/13, achieving 264.72 Ml/d. Leakage performance in 2012/13 was not economically

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

21

sustainable so in 2013/14 YW continued to out-perform its regulatory target (297.1 Ml/d) by a substantial margin, with leakage of 282 Ml/d. YW will be investing in further leakage reduction in the period from 2015 to 2020 as this is found to be the most cost and environmentally effective way to mitigate the growing deficit in the balance between water supply and demand. YW plans to reduce its leakage target by a further 10 Ml/d, from 297.1 to 287.1 Ml/d by 2020. YW will strive to out-perform this target and to continue finding ways to sustainably reduce leakage by focusing its operational resources and further innovation. The many ways YW supports customers with their leaks and overall water efficiency is described in the section below. Working with customers to save water YW works hard to actively assist its domestic and business customers in valuing water and becoming water efficient. Its goal is to deliver tangible water efficiencies and sustainable behavioural change. In 2013/14 YW provided more free water saving devices than ever before, nearly 128,000 devices, along with a range of advice and support services. It supported domestic customers to save 2.3 million litres of water per day (Ml/d), against a target of 2.1 Ml/d and business customers also saved 4.2 Ml/d against a target of 4 Ml/d. YW has achieved its water efficiency targets since it introduced them in 2010 and is committed to continuing to do so into the future. More information can be found on the water efficiency section of the website at: http://www.yorkshirewater.com/save-water-and-money.aspx. Reforming abstraction licences The Water Act 2014 introduces new provisions to facilitate the creation of a national water supply network by making it easier for water companies to buy and sell water from each other. YW has traded water with its neighbouring water companies for many years and considers such options as a standard part of its planning. YW has a notable import agreement with Severn Trent Water to use water from the Derwent Valley to support demand in the Sheffield area. YW also exports a small amount of treated water to Anglian Water to support their needs. YW continues to engage in the evolving national approach to abstraction licence reform.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

22

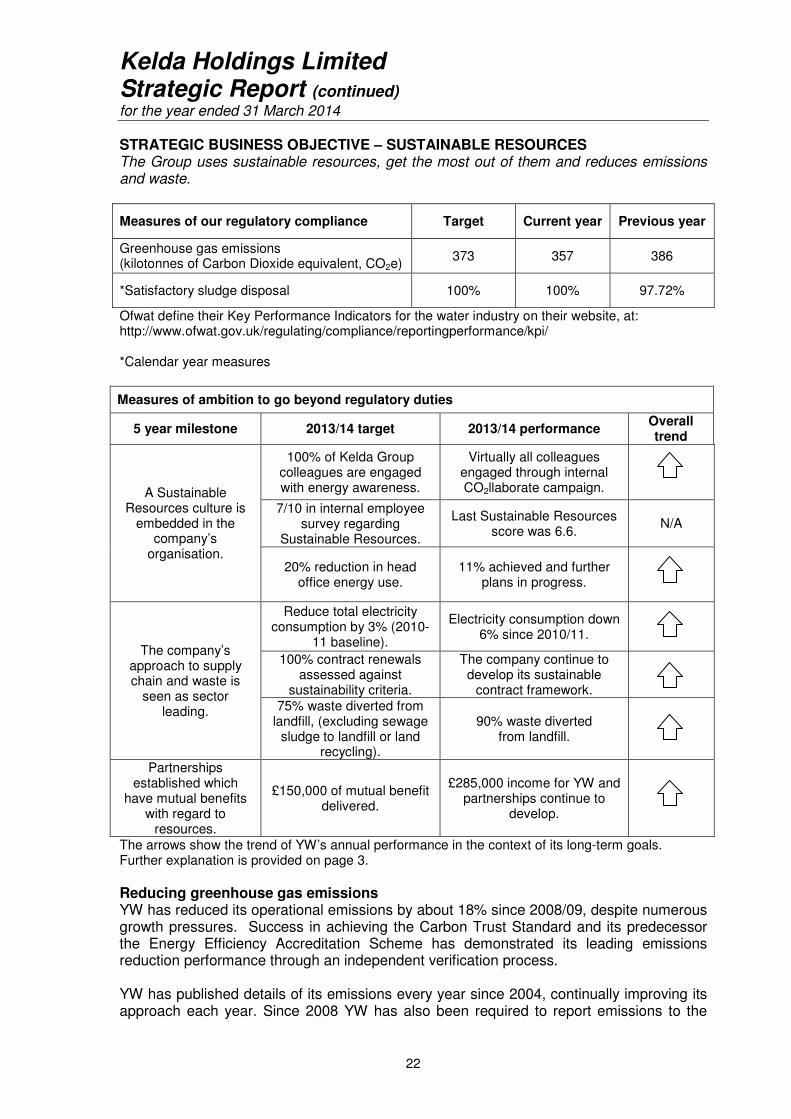

STRATEGIC BUSINESS OBJECTIVE – SUSTAINABLE RESOURCES

The Group uses sustainable resources, get the most out of them and reduces emissions and waste.

Measures of our regulatory compliance Target Current year Previous year

Greenhouse gas emissions (kilotonnes of Carbon Dioxide equivalent, CO2e)

373 357 386

*Satisfactory sludge disposal 100% 100% 97.72%

Ofwat define their Key Performance Indicators for the water industry on their website, at: http://www.ofwat.gov.uk/regulating/compliance/reportingperformance/kpi/ *Calendar year measures

Measures of ambition to go beyond regulatory duties

5 year milestone 2013/14 target 2013/14 performance Overall trend

A Sustainable Resources culture is

embedded in the company’s

organisation.

100% of Kelda Group colleagues are engaged with energy awareness.

Virtually all colleagues engaged through internal CO2llaborate campaign.

7/10 in internal employee survey regarding

Sustainable Resources.

Last Sustainable Resources score was 6.6.

N/A

20% reduction in head office energy use.

11% achieved and further plans in progress.

The company’s approach to supply chain and waste is

seen as sector leading.

Reduce total electricity consumption by 3% (2010-

11 baseline).

Electricity consumption down 6% since 2010/11.

100% contract renewals assessed against

sustainability criteria.

The company continue to develop its sustainable

contract framework.

75% waste diverted from landfill, (excluding sewage

sludge to landfill or land recycling).

90% waste diverted from landfill.

Partnerships established which

have mutual benefits with regard to

resources.

£150,000 of mutual benefit delivered.

£285,000 income for YW and partnerships continue to

develop.

The arrows show the trend of YW’s annual performance in the context of its long-term goals. Further explanation is provided on page 3. Reducing greenhouse gas emissions YW has reduced its operational emissions by about 18% since 2008/09, despite numerous growth pressures. Success in achieving the Carbon Trust Standard and its predecessor the Energy Efficiency Accreditation Scheme has demonstrated its leading emissions reduction performance through an independent verification process. YW has published details of its emissions every year since 2004, continually improving its approach each year. Since 2008 YW has also been required to report emissions to the

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

23

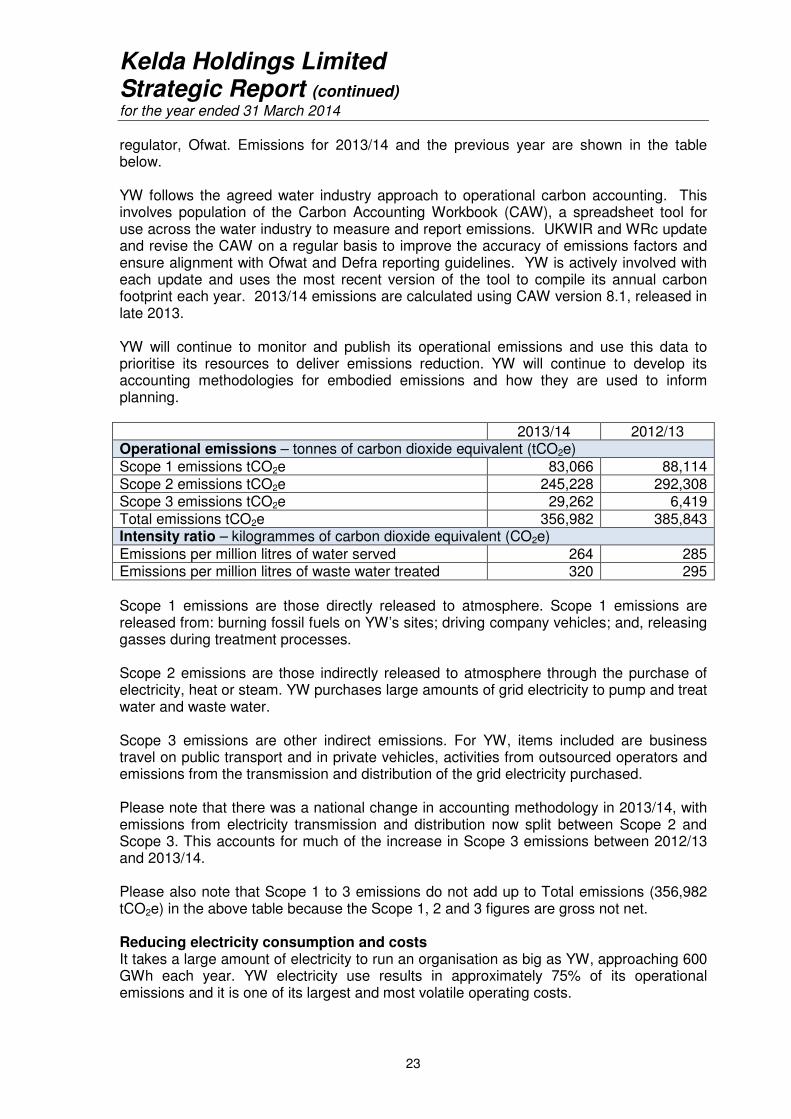

regulator, Ofwat. Emissions for 2013/14 and the previous year are shown in the table below. YW follows the agreed water industry approach to operational carbon accounting. This involves population of the Carbon Accounting Workbook (CAW), a spreadsheet tool for use across the water industry to measure and report emissions. UKWIR and WRc update and revise the CAW on a regular basis to improve the accuracy of emissions factors and ensure alignment with Ofwat and Defra reporting guidelines. YW is actively involved with each update and uses the most recent version of the tool to compile its annual carbon footprint each year. 2013/14 emissions are calculated using CAW version 8.1, released in late 2013. YW will continue to monitor and publish its operational emissions and use this data to prioritise its resources to deliver emissions reduction. YW will continue to develop its accounting methodologies for embodied emissions and how they are used to inform planning. 2013/14 2012/13 Operational emissions – tonnes of carbon dioxide equivalent (tCO2e) Scope 1 emissions tCO2e 83,066 88,114 Scope 2 emissions tCO2e 245,228 292,308 Scope 3 emissions tCO2e 29,262 6,419 Total emissions tCO2e 356,982 385,843 Intensity ratio – kilogrammes of carbon dioxide equivalent (CO2e) Emissions per million litres of water served 264 285 Emissions per million litres of waste water treated 320 295 Scope 1 emissions are those directly released to atmosphere. Scope 1 emissions are released from: burning fossil fuels on YW’s sites; driving company vehicles; and, releasing gasses during treatment processes. Scope 2 emissions are those indirectly released to atmosphere through the purchase of electricity, heat or steam. YW purchases large amounts of grid electricity to pump and treat water and waste water. Scope 3 emissions are other indirect emissions. For YW, items included are business travel on public transport and in private vehicles, activities from outsourced operators and emissions from the transmission and distribution of the grid electricity purchased. Please note that there was a national change in accounting methodology in 2013/14, with emissions from electricity transmission and distribution now split between Scope 2 and Scope 3. This accounts for much of the increase in Scope 3 emissions between 2012/13 and 2013/14. Please also note that Scope 1 to 3 emissions do not add up to Total emissions (356,982 tCO2e) in the above table because the Scope 1, 2 and 3 figures are gross not net. Reducing electricity consumption and costs It takes a large amount of electricity to run an organisation as big as YW, approaching 600 GWh each year. YW electricity use results in approximately 75% of its operational emissions and it is one of its largest and most volatile operating costs.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

24

YW responds to these business risks and opportunities by minimising the electricity it need and maximising its ability to generate its own electricity. This approach helps YW to reduce its emissions and keep costs low too. YW has made great strides in recent years, successfully reducing its total electricity consumption by 6% since 2010/11. This follows many years of growth in electricity demand since privatisation, driven primarily by investment to meet new legislation for environmental water quality. This has been achieved this through a variety of approaches, including cost-effective capital investment, operational efficiencies and targeted training. The energy used at the head office site in Bradford accounts for less than 1% of the company’s total carbon footprint. However, in accommodating over half of YW staff, and with regular visitors and guests, every effort is made to set an example in demand reduction and renewable energy culture. Whilst the ambitious target for a 20% reduction in just one year was not achieved, consumption was reduced by an impressive 11%. Efforts continue. YW has invested to create a substantial portfolio of renewable energy generation assets, mostly using sewage sludge to create low cost, low carbon energy. In 2013/14 two major investments were completed which dramatically increased the ability to generate renewable energy from sewage sludge. Bradford’s waste water treatment works is now approaching self-sufficiency for its substantial energy needs following over £30m of investment. Sheffield's waste water treatment works also has a new large self-generation capability following of investment of £23m. YW forecasts a sharp increase in its consumption and cost of electricity if it does not continue to act. This is caused by a range of factors, including national and global uncertainty in energy sources, the costs of replacing and decarbonising the UK’s aging energy infrastructure and ensuring compliance with new environmental water quality legislation. To mitigate this risk YW continues to plan to reduce its electricity demand and grow its ability to generate low carbon energy. Creating a culture that helps to maximise efficiency and resilience The company is committed to ensuring that all colleagues have the right training and tools to allow them to make informed decisions and to understand their role in sustainable resource use which is lean and resilient. In 2013/14 a new and bespoke web-based environmental awareness course was developed. It provides training on all of YW’s environmental impacts, focusing on energy consumption and energy efficiency. So far over 1,500 (40%) of Kelda Group colleagues have completed the training. A more detailed training programme has also been developed for those in the business who run and optimise YW’s most energy intensive processes. This aims to provide the relevant colleagues with the skills and confidence necessary for them to drive real change and improvement in the business. The training is in the form of a series of modules that ultimately provide the colleagues with their ‘energy passport’ to work. These are just two examples from YW’s cultural change programme ‘CO2llaborate to use less’. Virtually every single colleague has received some form of carbon and energy engagement through the communications and training programme.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

25

Turning waste into resource As a company, YW recognises the need to reduce waste in all its forms, everything from unused construction materials and by-products of treatment processes, to lost time and avoidable travel. Much of what is thought of as waste can actually generate new value through reuse by the company or someone else – creating what is known as a circular economy. Minimising waste and turning it into new resource is essential to the business to help the company remain efficient, reduce its environmental impact, keep bills low for customers and provide returns for investors. Sewage sludge is a large and renewable resource. Through a variety of innovative approaches YW is now able to generate renewable, low cost, low carbon energy from sewage sludge. After treating the sludge products for application to land as a sustainable substitute for petrochemical fertilisers and peat composts are created. After treating the sludge YW also creates products for application to land as a sustainable substitute for petrochemical fertilisers and peat composts. During 2013 YW completed an action plan and improved performance to 100% compliance with sludge disposal regulations. YW forecasts to maintain compliance at 100% in 2014. Further details of the action taken to improve performance can be found in YW’s Risk and Compliance Statement publication, available at: www.yorkshirewater.com.reports. Increasing the rates of recycling from offices, construction sites and operational sites has also been successful and in 2013/14 a target of almost 90% of diverting waste from landfill was achieved. In 2013/14 YW also developed a plan to implement numerous opportunities to work in partnership to deliver mutual benefit. For example, in October 2013 YW established fat, oil and grease (FOG) collection facilities for domestic customers in a known sewer blockage hotspot in Bradford. By helping customers to use their sewers more appropriately, this reduces the need for avoidable sewer maintenance work and potential problems from sewer flooding and pollution while a third party can collect the energy rich material and create power as well as a financial return. This is a pilot trial at present with a view to developing a full scale operation. Achieving SBO ambitions throughout the supply chain Working with the best suppliers is vital to ensure that the company can continue to improve its performance and provide a better service to customers. YW also recognises and manages a risk from interruptions to its supply chain. The ambition is for YW’s global supply chain to share the company’s commitment to the continuous improvement of the water environment and wider sustainable development. In 2013 YW published its new sustainable supply chain policy. This applies across all of its supply chain activities and seeks to articulate a consistent approach with straight forward expectations. YW will work with its supply chain to ensure security of essential supplies and to continually reduce demand for depleting natural resources while enabling a cycle of social, economic and environmental improvements. YW expect that its supply chain partners will deliver a similar message within their own supply chains. YW’s sustainable supply chain policy can be found at: http://www.yorkshirewater.com/about-us/supplying-us.aspx

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

26

Dependent on the nature of the contract, YW’s current evaluation process will consider areas such as energy, resource efficiency, waste management, human rights, labour practices and legal compliance. Environmental policy and governance YW environmental policy recognises that a sustainable water and waste water business is dependent on environmentally sustainable operations. The company is, therefore, committed to integrating environmental best practice and continuous improvement through the efficient, effective and proper conduct of the business. YW uses the Business in The Community (BiTC) Environment Index to help benchmark its environmental performance. YW increased its score to over 95% in 2013/14, reaching BiTC Platinum status. Environmental performance is reported through the website which is regularly updated. This can be viewed at www.yorkshirewater.com/our-environment.aspx

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

27

STRATEGIC BUSINESS OBJECTIVE – STRONG FINANCIAL FOUNDATIONS

The Group delivers services to customers at a price they are willing and able to pay, while providing investors with returns that attract long-term investment. The financial performance of the Group is reviewed on pages 34 to 35. Determining future prices and operational and investment plans The UK water industry is closely regulated to protect society’s interests. At the heart of the regulatory framework is a five yearly Price Review process that requires water companies to produce business plans detailing how they will achieve their legal requirements and customers’ expectations. The plans are submitted to the industry’s economic regulator, Ofwat, to determine limits on customer prices. Through these controls and requirements, the Price Review plays a fundamental role in shaping YW’s financial foundations. In December 2013 YW published its plans for the period from 2015 to 2020. This followed over two years of detailed consultation, investigation and assessment to inform what Yorkshire needs from its water and waste water services. YW developed a plan which aligns with customer priorities and reflects its aim to invest for a sustainable future while keeping bills affordable. Between 2015 and 2020 YW plans to spend £3.8 billion to deliver the resilient services customers and stakeholders said that they need, and 95% of this expenditure relates to customer’s highest priorities. YW bills are already some of the lowest in the industry at £368 per annum for an average household customer in 2013. YW is planning to keep bills low. In 2014/15 YW was allowed to increase prices by 1.6% above RPI. YW decided to cap this increase at RPI. This means in 2014/15 YW will be reducing average household bills by £6 in real terms compared to what was allowed by Ofwat. YW proposes to continue this saving throughout the life of the plan meaning a total average household saving of £36 over six years. In 2013/14 YW completed its biggest ever customer and stakeholder engagement campaign to inform the development of its business plan for the period from 2015 to 2020. Overall 77% of those asked supported YW’s proposals. More is explained about this in the Trusted Company SBO section. Ofwat will conclude the price preview process before the end of 2014. YW believes it has provided robust plans that meet customer and legislative requirements, however there is a risk in that Ofwat is able to alter the plans which would have significant consequences for future operations, investments and financial performance. You can find out full details of the customer engagement and the plans at: www.BlueprintForYorkshire.com. Ensuring affordability and managing customer debt YW customer bills are already some of the lowest in the country and the company is committed to doing everything it can to keep bills low. With that in mind, YW decided not to proceed with the planned 2014/15 price increase agreed with Ofwat in 2009 of RPI plus 1.6%, capping the increase at RPI. As described above, this decision meant that from April 2014 the average household bill in Yorkshire stayed in line with the rate of inflation, with the average bill being £373, £6 lower

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

28

than planned. In the new business plan, the proposal is to maintain this saving for customers through to 2020. By becoming even more efficient and by reducing returns to investors YW can ensure bills stay in line with inflation while maintaining and enhancing the services provided to customers and the environment. Non-recovery of customer debt is a risk. It may cause profitability to suffer in the short-term and increase cost to paying customers in the medium to long-term. Allowance is made by Ofwat in the price limits at each Periodic Review for a proportion of debt deemed to be irrecoverable. To mitigate this risk, YW operates a range of schemes designed to help customers who genuinely cannot pay their bills while having strong processes in place for overall debt collection. During 2013/14 YW was offering more debt support to more people than ever before through a range of assistance packages. New innovative agreements with credit reference agencies are helping us to better target those in most need. The Resolve scheme is just one of the many support arrangements offered customers. This scheme provides customers with an opportunity to clear their debt by maintaining a payment arrangement which will result in the company making a corresponding write-off of the remaining arrears. To qualify customers must have arrears of at least £500 and have a low income. In 2014/15 YW will introduce a new affordability scheme where it will proactively seek to identify vulnerable customers and help them before they get into debt. Preparing for increasing competition in the water industry The Water Act 2014 received Royal Assent in May 2014. The Act includes a range of important measures for the water sector. It will introduce greater freedom for businesses, charities and public sector customers in England to choose their water supplier. This will connect with an existing retail market in Scotland. This presents both opportunities and threats to YW’s business and YW is watching developments closely as the company continues to develop its position. Increasing retail competition will make the Competition Act increasingly relevant to YW’s business and the wider water industry. YW will need to introduce separation between its business retail activities and the rest of the business and it will be implementing the necessary preparations and controls to ensure compliance and fair trading practices. The Water Act will also introduce measures to facilitate water trading. We continue to engage in the evolving national approach to abstraction licence reform and the trading and movement of water nationally. Delivering the company’s capital investment programme YW invests significant capital expenditure to add to and replace plant and equipment. The price limits set by Ofwat every five years take into account the level of capital expenditure expected to be incurred during the relevant period and the associated funding costs and operating costs. In 2013/14 YW has continued to govern closely the effective delivery of the capital programme. A Board Capital Investment Committee (BCIC) with delegated power from the board, monitors the capital programme delivery and provides strategic direction.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

29

If YW were unable to deliver its capital investment programme at expected expenditure levels, were unable to secure the expected level of efficiency savings, or the programme fell behind schedule, profitability may suffer because of a need for increased capital expenditure. Ofwat may also factor such failure into future Price Reviews by seeking to recover amounts equivalent to the “allowed costs” of any parts of the programme that are not delivered. The ability to meet regulatory output targets and environmental performance standards could also be adversely affected by such failure, which may result in penalties imposed by Ofwat of an amount up to 10% of turnover or other sanctions. Governing borrowing requirements Treasury operations are controlled centrally by a treasury department which operates on behalf of all companies in the Group and is controlled by the ultimate parent company. Activities are carried out in accordance with approved board policies, guidelines and procedures. Treasury strategy is designed to manage exposure to fluctuations in interest rates, preclude speculation and to source and structure the Group’s borrowing requirements. The Group uses a combination of fixed capital, retained profits, long term loans, finance leases and bank facilities to finance its operations. Any funding required is raised by the Group treasury department in the name of the appropriate company, operating within the debt covenants. Subject to the restrictions required by the Whole Business Securitisation that applies to YW, funds raised may be lent to or from the company at commercial rates of interest. Cash surplus to operating requirements is invested in short term instruments with institutions having a long term rating of at least A-/A-/A3 and a short term rating of at least A1/F1/P1 issued by Standard and Poor’s, Fitch and Moody’s respectively. Managing financial risk The executive team (Kelda Management Team, ‘KMT’) receives regular reports from all areas of the business to enable prompt identification of financial and other risks so that appropriate actions can be taken. The operation of the treasury function is governed by policies and procedures, which set out guidelines for the management of interest rate risk and foreign exchange risk and the use of financial instruments. Treasury policy and procedures are incorporated within YW’s financial control procedures. The Group’s operations expose it to a variety of financial risks that include the effects of changes in debt market prices, price risk, liquidity risk, interest rate risk and exchange rate risk. Derivative financial instruments, including cross currency swaps, interest rate swaps and forward currency contracts are employed to manage the interest rate and currency risk arising from the primary financial instruments used to finance the company’s activities. The Group actively maintains a broad portfolio of debt, diversified by source and maturity and designed to ensure the Group has sufficient available funds for operations. The Group is exposed to commodity price risk, especially energy price risk, as a result of its operations. The Group aims to manage this risk by fixing contract prices where possible operating within an energy purchasing policy that is designed to manage price volatility risk. The insurance team work to ensure that the Group manages and mitigates its exposure to costs from public liabilities and damage to its assets.

Kelda Holdings Limited Strategic Report (continued) for the year ended 31 March 2014

30