Embed Size (px)

Citation preview

Keep Up with the Trends and Best Practices of E-Billing Carlos Seoane, General Manager, eBillingHub

2 © Thomson Reuters, 2013

QUICK INTRODUCTORY NOTE

• eBillingHub does will not share any firm or client-specific information

• All data presented here refers to US or international firms who are currently using eBillingHub to submit their electronic bills

• The data shared in this presentation is a sampling of the data available within our system and should not be construed as being representative of any particular client or law firm.

• Copyright © Thomson Reuters, 2013. All Rights Reserved. No part of this document may be reproduced without Thomson Reuter's express consent.

3 © Thomson Reuters, 2013

BILLING STAFF

e-BILLING VENDORS CLIENT

T&B Syst

LAW FIRM

eBILLINGHUB

eBIllingHub takes a very central position in a firm’s eBilling process

4 © Thomson Reuters, 2013

eBILLINGHUB IN NUMBERS

1,909,776 eBills Processed in last 12 months

$19,600,000,000 dollars submitted

in the last 12 months

330+ Large Law Firms

3,500 Clients Mapped

4,600 Billing Professionals

Using the system

5 © Thomson Reuters, 2013

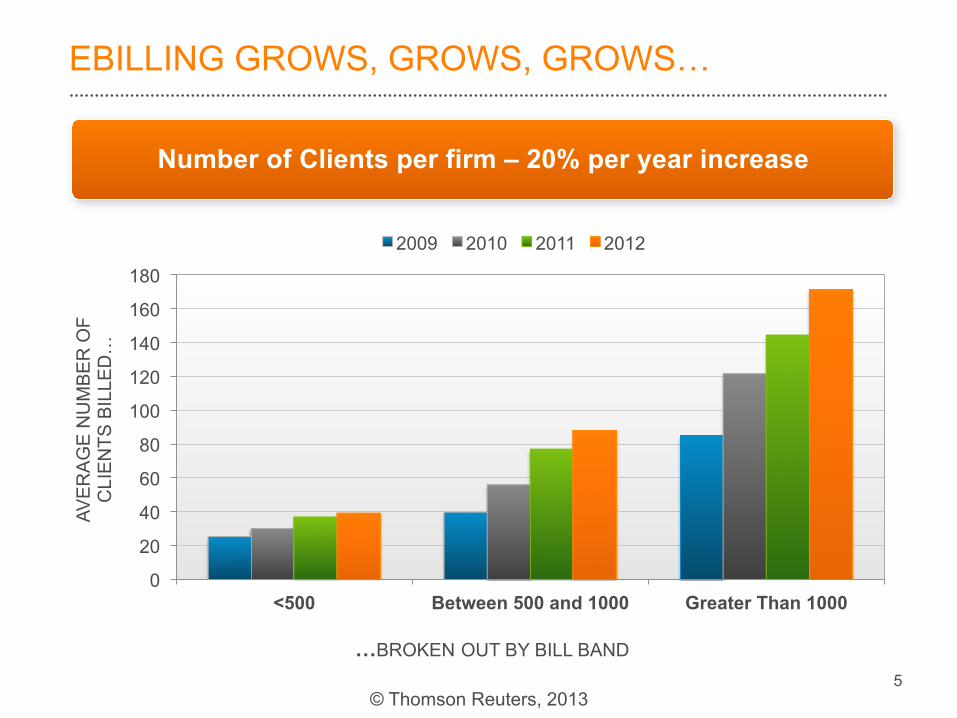

EBILLING GROWS, GROWS, GROWS… AV

ER

AG

E N

UM

BE

R O

F C

LIE

NTS

BIL

LED

…

…BROKEN OUT BY BILL BAND

0

20

40

60

80

100

120

140

160

180

<500 Between 500 and 1000 Greater Than 1000

2009 2010 2011 2012

Number of Clients per firm – 20% per year increase

6 © Thomson Reuters, 2013

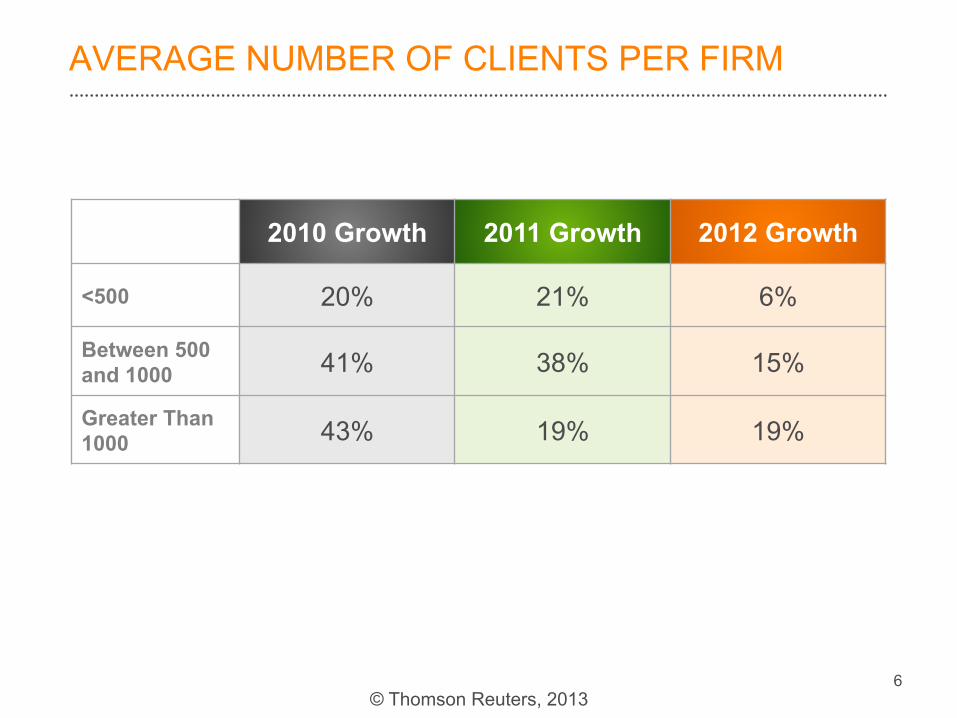

AVERAGE NUMBER OF CLIENTS PER FIRM

2010 Growth 2011 Growth 2012 Growth

<500 20% 21% 6%

Between 500 and 1000 41% 38% 15%

Greater Than 1000 43% 19% 19%

7 © Thomson Reuters, 2013

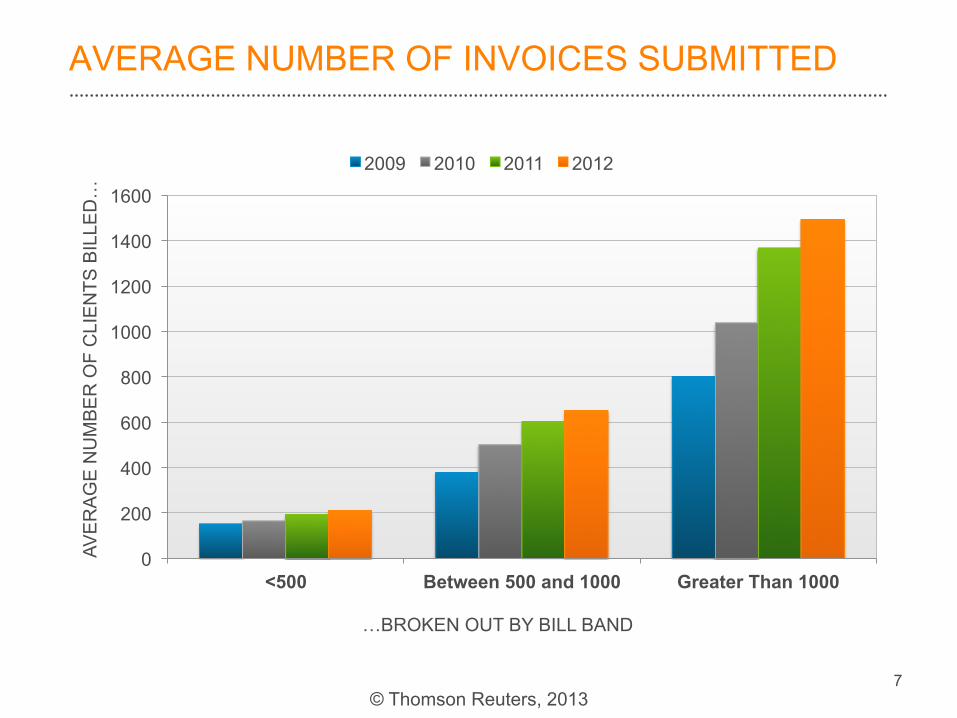

AVERAGE NUMBER OF INVOICES SUBMITTED

0

200

400

600

800

1000

1200

1400

1600

<500 Between 500 and 1000 Greater Than 1000

AVE

RA

GE

NU

MB

ER

OF

CLI

EN

TS B

ILLE

D…

…BROKEN OUT BY BILL BAND

2009 2010 2011 2012

8 © Thomson Reuters, 2013

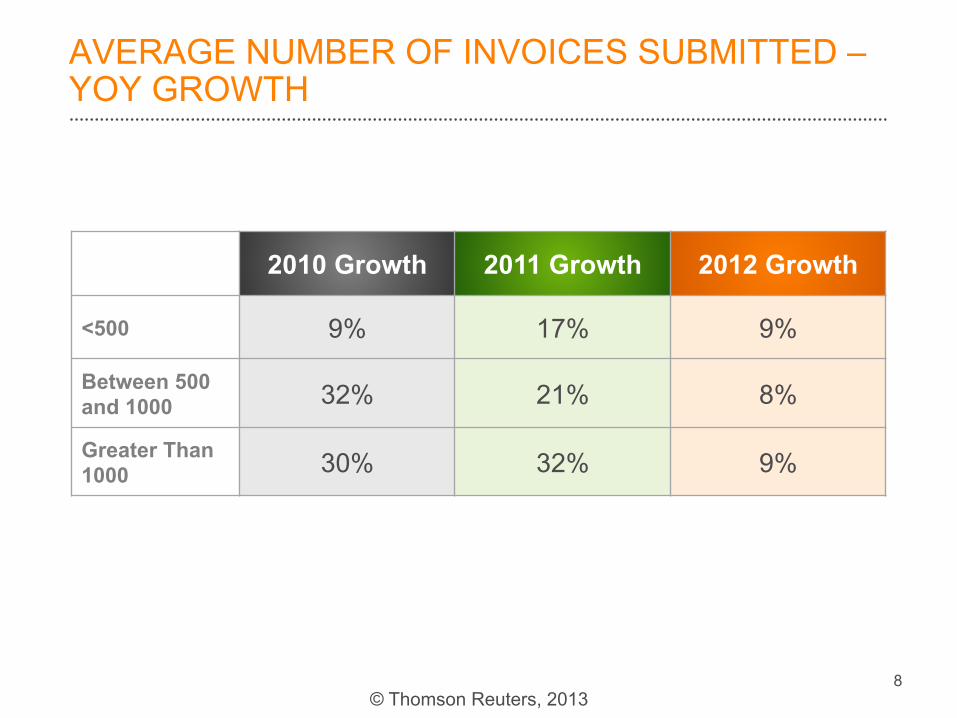

AVERAGE NUMBER OF INVOICES SUBMITTED – YOY GROWTH

2010 Growth 2011 Growth 2012 Growth

<500 9% 17% 9%

Between 500 and 1000 32% 21% 8%

Greater Than 1000 30% 32% 9%

9 © Thomson Reuters, 2013

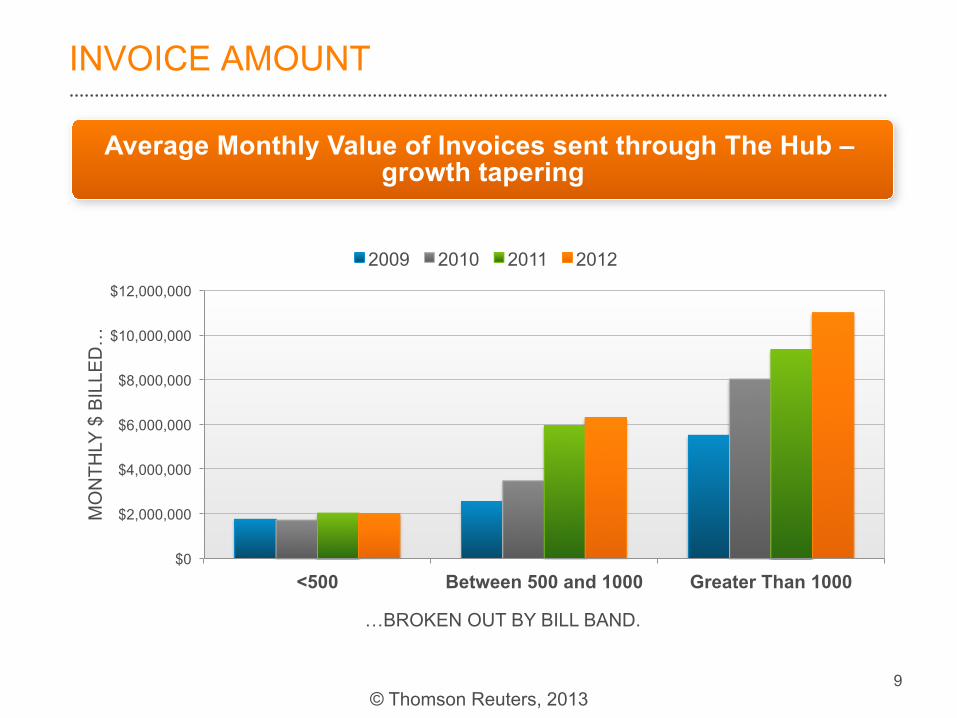

INVOICE AMOUNT

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

<500 Between 500 and 1000 Greater Than 1000

MO

NTH

LY $

BIL

LED

…

…BROKEN OUT BY BILL BAND.

2009 2010 2011 2012

Average Monthly Value of Invoices sent through The Hub – growth tapering

10 © Thomson Reuters, 2013

INVOICE AMOUNT

2010 Growth 2011 Growth 2012 Growth

<500 9.8% 17% 9%

Between 500 and 1000 37% 71% 6%

Greater Than 1000 45% 16% 18%

11 © Thomson Reuters, 2013

GROWTH MOVING DOWNMARKET

2010 Growth 2011 Growth 2012 Growth <500 20% 21% 6% Between 500 and 1000 41% 38% 15% Greater Than 1000 43% 19% 19%

2010 Growth 2011 Growth 2012 Growth <500 9.8% 17% 9% Between 500 and 1000 37% 71% 6% Greater Than 1000 45% 16% 18%

CLIENT GROWTH:

INVOICE AMOUNT GROWTH:

12 © Thomson Reuters, 2013

NEW CLIENT SET-UP – MONTHLY AVERAGE

0

20

40

60

80

100

120

NE

W C

LIE

NTS

AD

DE

D T

O

THE

HU

B’S

LIB

RA

RY

…

…MONTH BY MONTH

New Clients Setup Total

13 © Thomson Reuters, 2013

NEW CLIENT SET-UP – MONTHLY AVERAGE

Year Average

2009 38.1

2010 27.3

2011 35.1

2012 37.0

2013 YTD 54.6

14 © Thomson Reuters, 2013

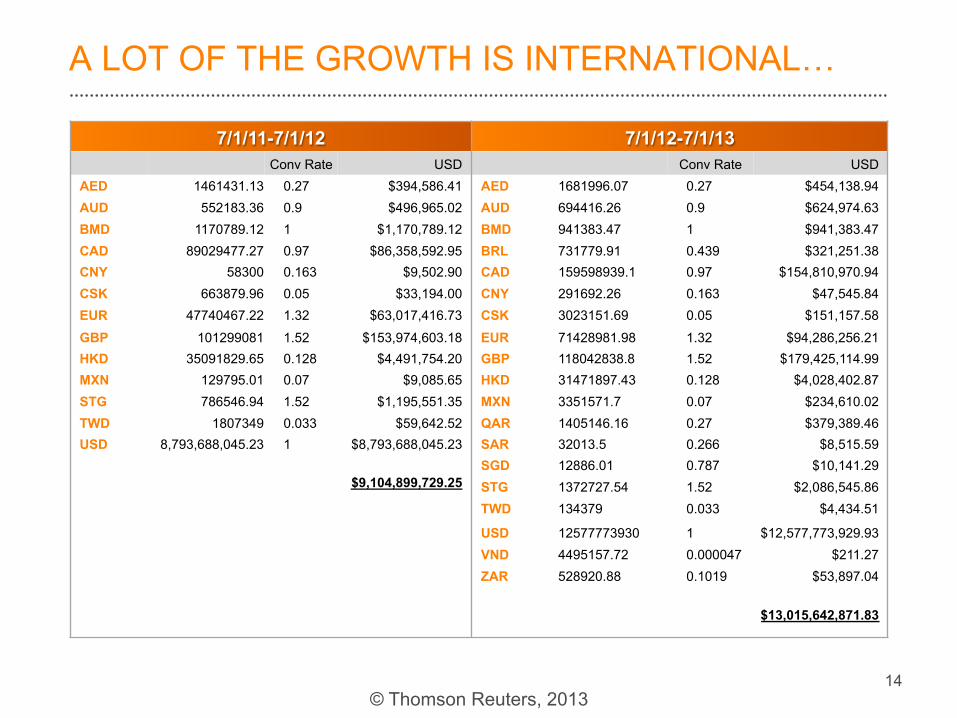

A LOT OF THE GROWTH IS INTERNATIONAL…

7/1/11-7/1/12 7/1/12-7/1/13 Conv Rate USD Conv Rate USD

AED 1461431.13 0.27 $394,586.41 AED 1681996.07 0.27 $454,138.94 AUD 552183.36 0.9 $496,965.02 AUD 694416.26 0.9 $624,974.63 BMD 1170789.12 1 $1,170,789.12 BMD 941383.47 1 $941,383.47 CAD 89029477.27 0.97 $86,358,592.95 BRL 731779.91 0.439 $321,251.38 CNY 58300 0.163 $9,502.90 CAD 159598939.1 0.97 $154,810,970.94 CSK 663879.96 0.05 $33,194.00 CNY 291692.26 0.163 $47,545.84 EUR 47740467.22 1.32 $63,017,416.73 CSK 3023151.69 0.05 $151,157.58

GBP 101299081 1.52 $153,974,603.18 EUR 71428981.98 1.32 $94,286,256.21 HKD 35091829.65 0.128 $4,491,754.20 GBP 118042838.8 1.52 $179,425,114.99 MXN 129795.01 0.07 $9,085.65 HKD 31471897.43 0.128 $4,028,402.87 STG 786546.94 1.52 $1,195,551.35 MXN 3351571.7 0.07 $234,610.02 TWD 1807349 0.033 $59,642.52 QAR 1405146.16 0.27 $379,389.46 USD 8,793,688,045.23 1 $8,793,688,045.23 SAR 32013.5 0.266 $8,515.59

SGD 12886.01 0.787 $10,141.29 $9,104,899,729.25 STG 1372727.54 1.52 $2,086,545.86

TWD 134379 0.033 $4,434.51

USD 12577773930 1 $12,577,773,929.93 VND 4495157.72 0.000047 $211.27 ZAR 528920.88 0.1019 $53,897.04

$13,015,642,871.83

15 © Thomson Reuters, 2013

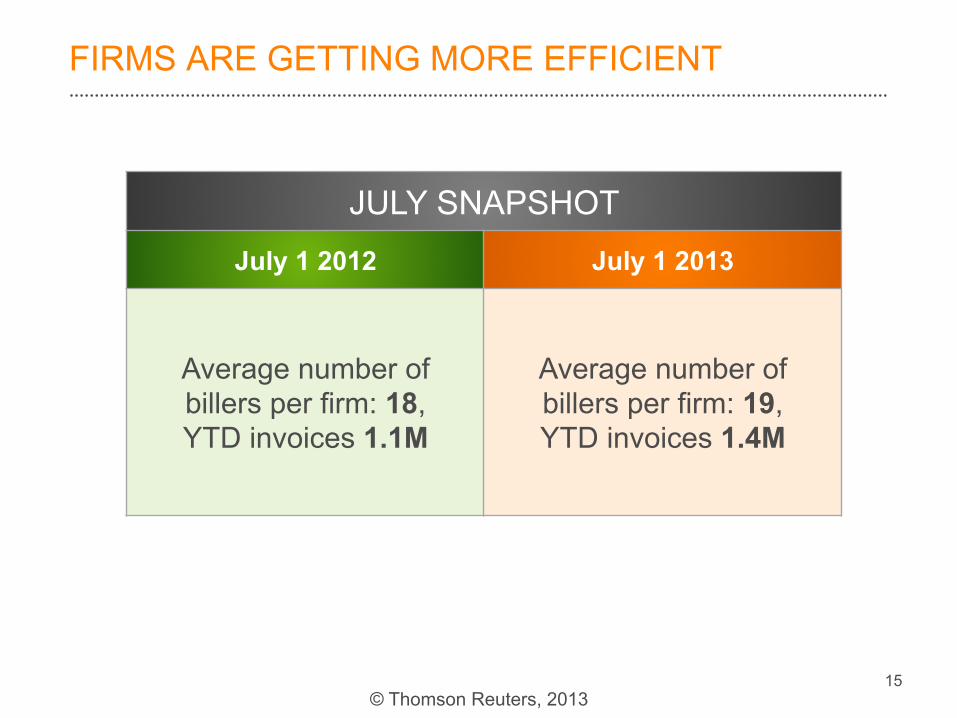

FIRMS ARE GETTING MORE EFFICIENT

JULY SNAPSHOT

July 1 2012 July 1 2013

Average number of billers per firm: 18, YTD invoices 1.1M

Average number of billers per firm: 19, YTD invoices 1.4M

16 © Thomson Reuters, 2013

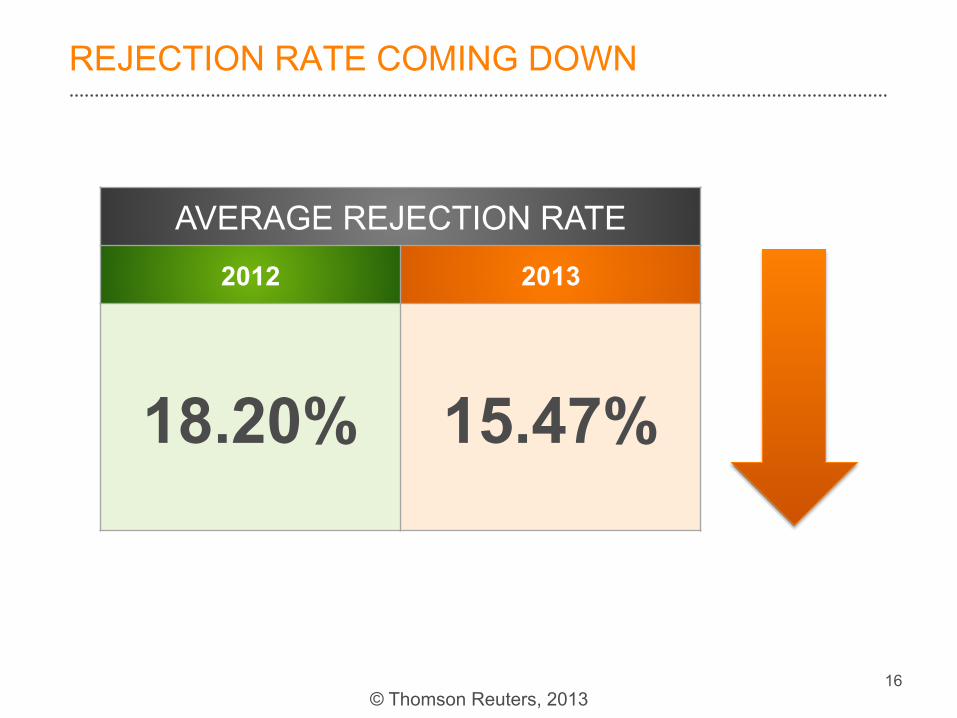

REJECTION RATE COMING DOWN

AVERAGE REJECTION RATE

2012 2013

18.20% 15.47%

17 © Thomson Reuters, 2013

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

PE

RC

EN

TAG

E O

F B

ILLS

RE

JEC

TED

TOP 22 VENDORS

Rejection % By Vendor

Total

KNOW YOUR VENDORS!!!

Avg 15.5%

18 © Thomson Reuters, 2013

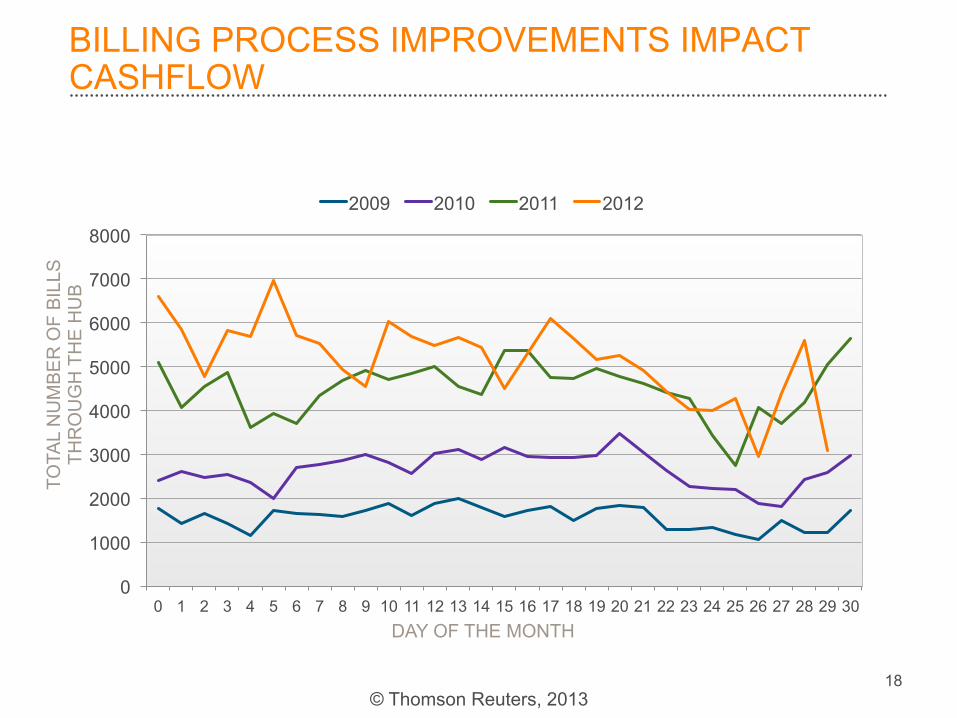

BILLING PROCESS IMPROVEMENTS IMPACT CASHFLOW

0

1000

2000

3000

4000

5000

6000

7000

8000

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

2009 2010 2011 2012

DAY OF THE MONTH

TOTA

L N

UM

BE

R O

F B

ILLS

TH

RO

UG

H T

HE

HU

B

19 © Thomson Reuters, 2013

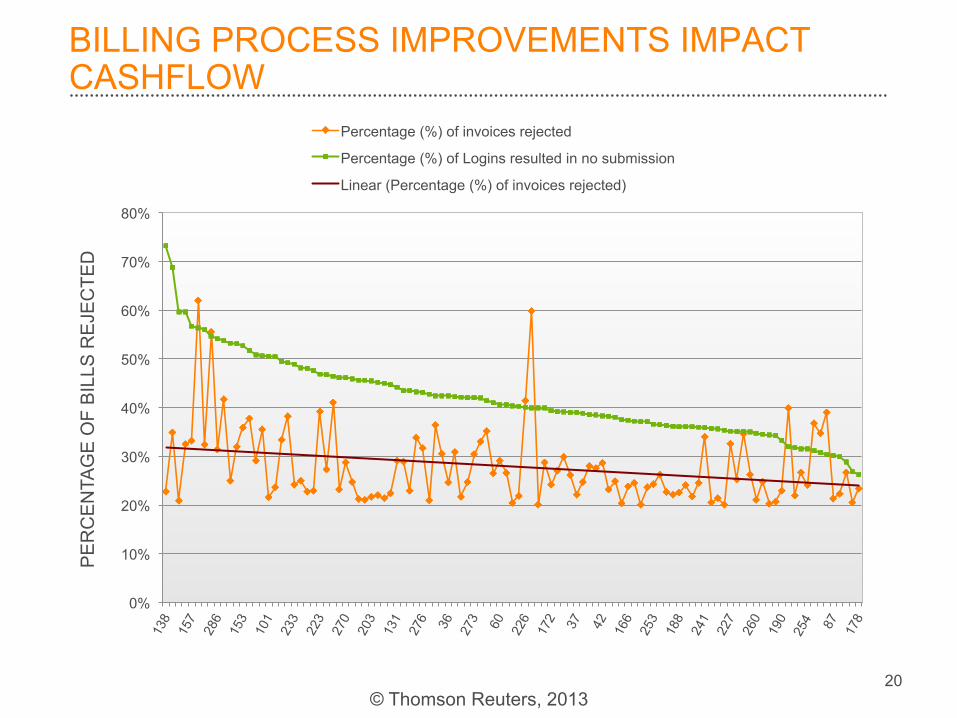

BILLING PROCESS IMPROVEMENTS IMPACT CASHFLOW

0

50

100

150

200

250

300

350

400

450

500

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

NU

MB

ER

OF

BIL

LS T

HR

OU

GH

TH

E H

UB

(EA

CH

FIR

M)

DAY OF THE MONTH

20 © Thomson Reuters, 2013

BILLING PROCESS IMPROVEMENTS IMPACT CASHFLOW

PE

RC

EN

TAG

E O

F B

ILLS

RE

JEC

TED

0%

10%

20%

30%

40%

50%

60%

70%

80%

Percentage (%) of invoices rejected

Percentage (%) of Logins resulted in no submission

Linear (Percentage (%) of invoices rejected)

21 © Thomson Reuters, 2013

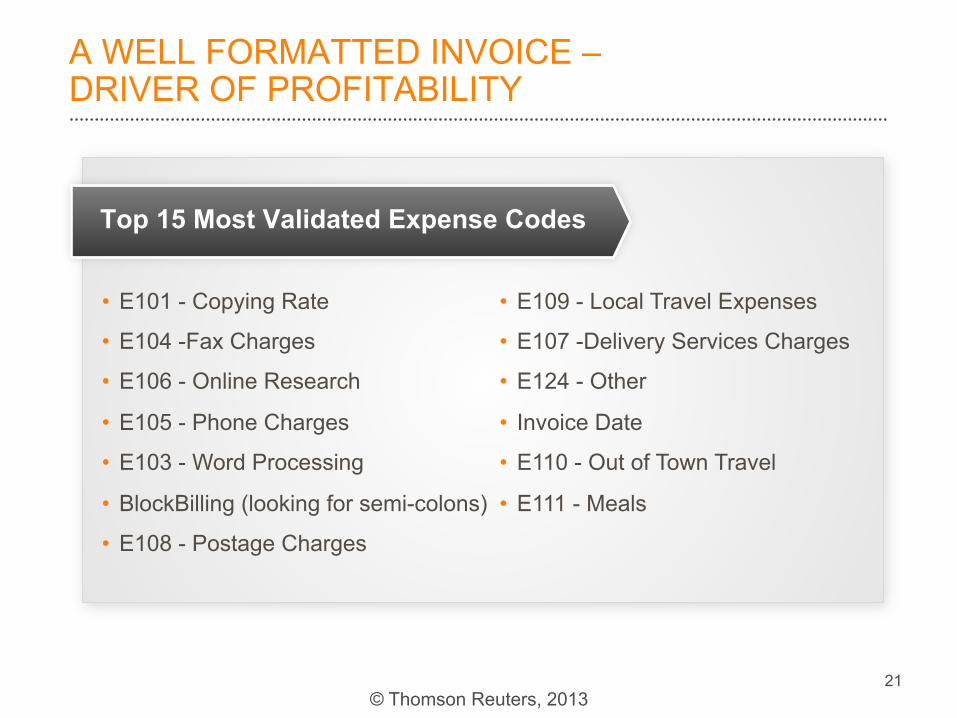

A WELL FORMATTED INVOICE – DRIVER OF PROFITABILITY

Top 15 Most Validated Expense Codes

• E101 - Copying Rate

• E104 -Fax Charges

• E106 - Online Research

• E105 - Phone Charges

• E103 - Word Processing

• BlockBilling (looking for semi-colons)

• E108 - Postage Charges

• E109 - Local Travel Expenses

• E107 -Delivery Services Charges

• E124 - Other

• Invoice Date

• E110 - Out of Town Travel

• E111 - Meals

22 © Thomson Reuters, 2013

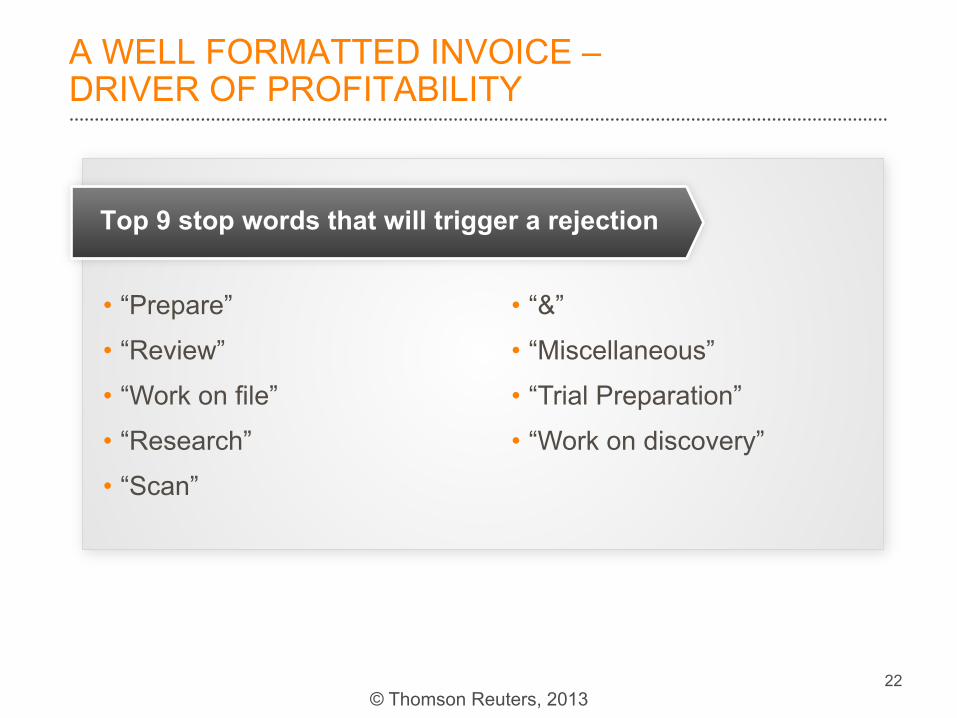

A WELL FORMATTED INVOICE – DRIVER OF PROFITABILITY

Top 9 stop words that will trigger a rejection

• “Prepare”

• “Review”

• “Work on file”

• “Research”

• “Scan”

• “&”

• “Miscellaneous”

• “Trial Preparation”

• “Work on discovery”

23 © Thomson Reuters, 2013

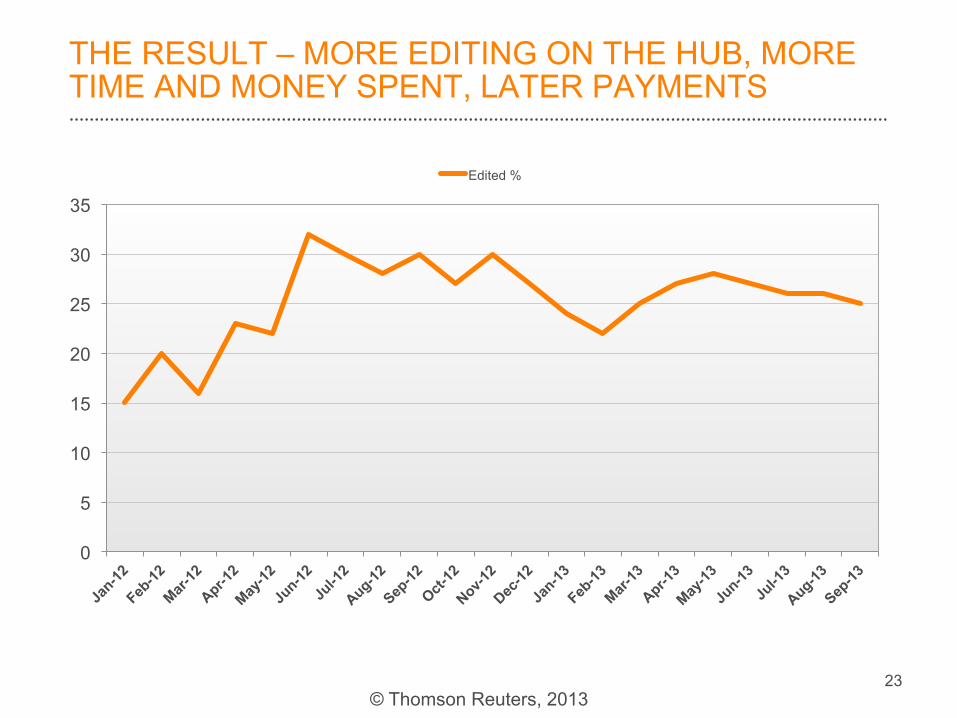

THE RESULT – MORE EDITING ON THE HUB, MORE TIME AND MONEY SPENT, LATER PAYMENTS

0

5

10

15

20

25

30

35

Edited %

24 © Thomson Reuters, 2013

25 © Thomson Reuters, 2013

26 © Thomson Reuters, 2013

FORMATTING IS NOT ENOUGH – TRAIN YOUR CLIENT!

85%

15%

Invoices

Approved Rejected 83%

17%

Rejected Invoices

Invoice Content/Format Issues Clerical Reasons

50% 50%

Clerical Reasons

■ Matter Set up ■ 1. Budget Exceeded

2. Incorrect/Missing/Expired Credentials