Embed Size (px)

Citation preview

UNITED STATES DISTRICT COURTSOUTHERN DISTRICT OF ILLINOIS

Kathi Cooper, et al. ))

Plaintiffs, ))

vs. ) CIVIL NO. 99-829-GPM)

IBM Personal Pension Plan and IBM )Corporation, )

)Defendants. )

MOTION FOR AWARD OF ATTORNEYS’ FEES, COSTSAND INCENTIVE AWARDS

Class counsel, pursuant to Rule 54, Fed.R.Civ.P., respectfully requests that this Court

award attorneys’ fees and costs pursuant to the common fund doctrine, and incentive awards to

be paid from the attorneys’ fees for the two named plaintiffs.

Introduction

This litigation was commenced nearly six years ago--on November 1, 1999--and will

continue for at least another year as the parties continue to litigate two of the central issues

before the United States Court of Appeals and potentially the United States Supreme Court. This

case arose from IBM’s 1995 implementation of a so-called pension equity formula (referred to in

the IBM Plan as the “pension credit formula” or “PCF”) and its 1999 implementation of a so-

called cash balance formula (“CB”). Among other things, Plaintiffs alleged that the manner in

which benefits accrue under the PCF and CB formulas, as well as IBM’s use of the so-called

Always Cash Balance or “ACB” formula to calculate opening account balances effective July 1,

1999, violated ERISA § 204(b)(1)(H).

At the time the litigation was commenced in 1999, only two decisions had considered

legal challenges to cash balance plans, and both decisions were summary judgment orders

rejecting the plaintiffs’ claims. See Esden v. BankBoston, 182 F.R.D. 432 (D. Vt. 1999); Lyons

2

v. Georgia Pacific Corp. Salaried Ret. Plan, 66 F.Supp.2d 1328 (N.D. Ga. 1999). Shortly after

this case was filed, another district court rejected a claim that cash balance plans violate ERISA

§ 411(b)(1)(H). See Eaton v. Onan Corp., 117 F. Supp.2d 812 (S.D. Ind. 2000). Several other

courts also have reached that erroneous conclusion. No case had ever addressed plaintiffs’ PCF,

wear-away or ACB claims. To date, Class Counsel are the only attorneys in the country who

have prevailed on the claim that a pension equity formula or a cash balance plan formula violate

ERISA § 411(b)(1)(H).

In 1999, literally no other law firm in the country with the necessary qualifications to

handle this complex ERISA litigation would do so. Declaration of Kathi Cooper (“Cooper

Dec.”) at ¶ 5; Declaration of Jeffrey Lewis (“Lewis Dec.”) at ¶¶ 11-14; Declaration of William

K. Carr (“Carr Dec.”) at ¶¶ 8-14; Affidavit of Douglas Sprong (“Sprong Aff.”) at ¶ 3. For

example, in the summer of 1999, representatives of an IBM employee group met with members

of several prominent law firms from across the country in an effort to persuade one or more of

them to undertake the litigation. Carr Dec. at ¶¶ 8-10. After examining the case, the lead firm of

Bell, Boyd & Lloyd declined to undertake to represent the employees, and none of the other

firms took the case on either. Id. at ¶13. Referencing IBM’s decision to allow “choice” to

employees over 40 years of age with more than 10 years of service, Bell Boyd’s Christopher G.

MacKaronis wrote “In light of this and related developments, we do not intend to pursue the

1A copy of the letter is attached as Exhibit 1. Mr. Mackaronis is the author of numerousarticles on employee benefits and age discrimination issues and has testified before jointhearings of the U.S. Senate and House labor and education committees on age discriminationand employee benefit plans.

2Also refusing to join the fray were the Treasury Department, the Labor Department, or anyother governmental agency with authority to take action on the matter.

3

matter any further.”1 Carr Dec., at ¶13, Exhibit A. And no one other than Class Counsel ever

stepped forward to represent the employees.2

In addition to the very substantial litigation risks, Class Counsel also faced the risk posed

by the Cash Balance advocates’ efforts (which began well before the filing of this suit) to

persuade the United States Treasury Department and Congress to bar litigation challenging

pension equity and cash balance plans. The very real risks posed by those efforts is evidenced

by the fact that numerous members of Congress (and the United States Treasury Department

after 2000) have actively attempted to immunize pension equity and cash balance plans from

legal challenge. That effort continues to this date. In fact, within the last month the Chairperson

of the U. S. House Committee on Education and the Workplace attempted to introduce

retroactive legislation to bar such legal challenges.

In addition to facing a difficult and uphill legal and political battle, it was equally clear

that anyone representing plaintiffs would be required to overcome a well-financed adversary

(along with numerous similarly aligned and well-funded industry groups) and prominent defense

counsel with abundant financial and legal resources at their disposal. In short, at the time Class

Counsel undertook their representation of the plaintiffs, the odds were low that Plaintiffs would

prevail. That no doubt explains the absence of experienced counsel willing to take on such a

gargantuan fight.

4

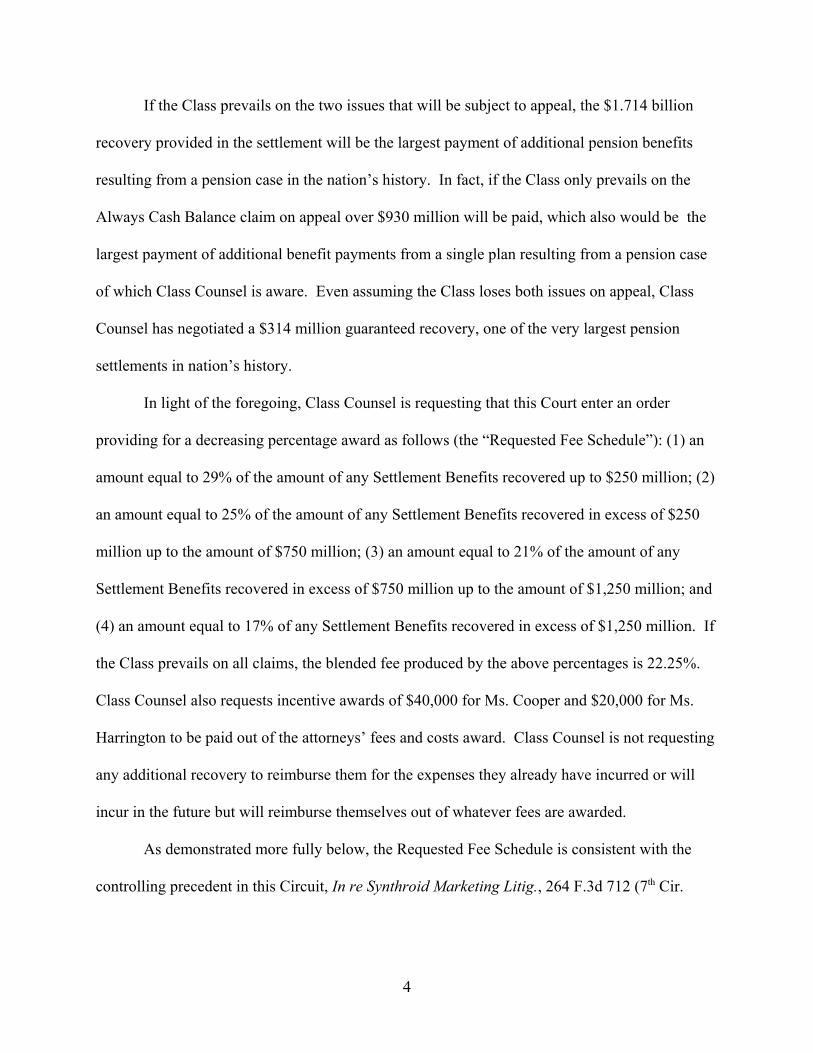

If the Class prevails on the two issues that will be subject to appeal, the $1.714 billion

recovery provided in the settlement will be the largest payment of additional pension benefits

resulting from a pension case in the nation’s history. In fact, if the Class only prevails on the

Always Cash Balance claim on appeal over $930 million will be paid, which also would be the

largest payment of additional benefit payments from a single plan resulting from a pension case

of which Class Counsel is aware. Even assuming the Class loses both issues on appeal, Class

Counsel has negotiated a $314 million guaranteed recovery, one of the very largest pension

settlements in nation’s history.

In light of the foregoing, Class Counsel is requesting that this Court enter an order

providing for a decreasing percentage award as follows (the “Requested Fee Schedule”): (1) an

amount equal to 29% of the amount of any Settlement Benefits recovered up to $250 million; (2)

an amount equal to 25% of the amount of any Settlement Benefits recovered in excess of $250

million up to the amount of $750 million; (3) an amount equal to 21% of the amount of any

Settlement Benefits recovered in excess of $750 million up to the amount of $1,250 million; and

(4) an amount equal to 17% of any Settlement Benefits recovered in excess of $1,250 million. If

the Class prevails on all claims, the blended fee produced by the above percentages is 22.25%.

Class Counsel also requests incentive awards of $40,000 for Ms. Cooper and $20,000 for Ms.

Harrington to be paid out of the attorneys’ fees and costs award. Class Counsel is not requesting

any additional recovery to reimburse them for the expenses they already have incurred or will

incur in the future but will reimburse themselves out of whatever fees are awarded.

As demonstrated more fully below, the Requested Fee Schedule is consistent with the

controlling precedent in this Circuit, In re Synthroid Marketing Litig., 264 F.3d 712 (7th Cir.

3The parties have settled on a total fund that will include any fees awarded. The Plan hasdetermined that it is appropriate to pay any fee award as an administrative expense. Even if theattorney’s fee award is, consequently, viewed as separate from the amount to be distributed toclass members, the common fund analysis is still appropriate to determine the fee award’sreasonableness. See Manual for Complex Litigation Third (1995) at section 30.42, pages 239-40(“If an agreement is reached on the amount of a settlement fund and separately providing anamount for attorneys’ fees and expenses, ... the sum of the two amounts ordinarily should betreated as a settlement fund for the benefit of the class”); In re General Motors Corp. Pick-upTruck Fuel Tank Litigation, 55 F.3d 768, 822 (3rd Cir. 1995).

4Class counsel has incurred over $330,000 in costs to date which Class Counsel proposes toreimburse out of the fees awarded rather than seeking an additional amount for suchreimbursement.

5

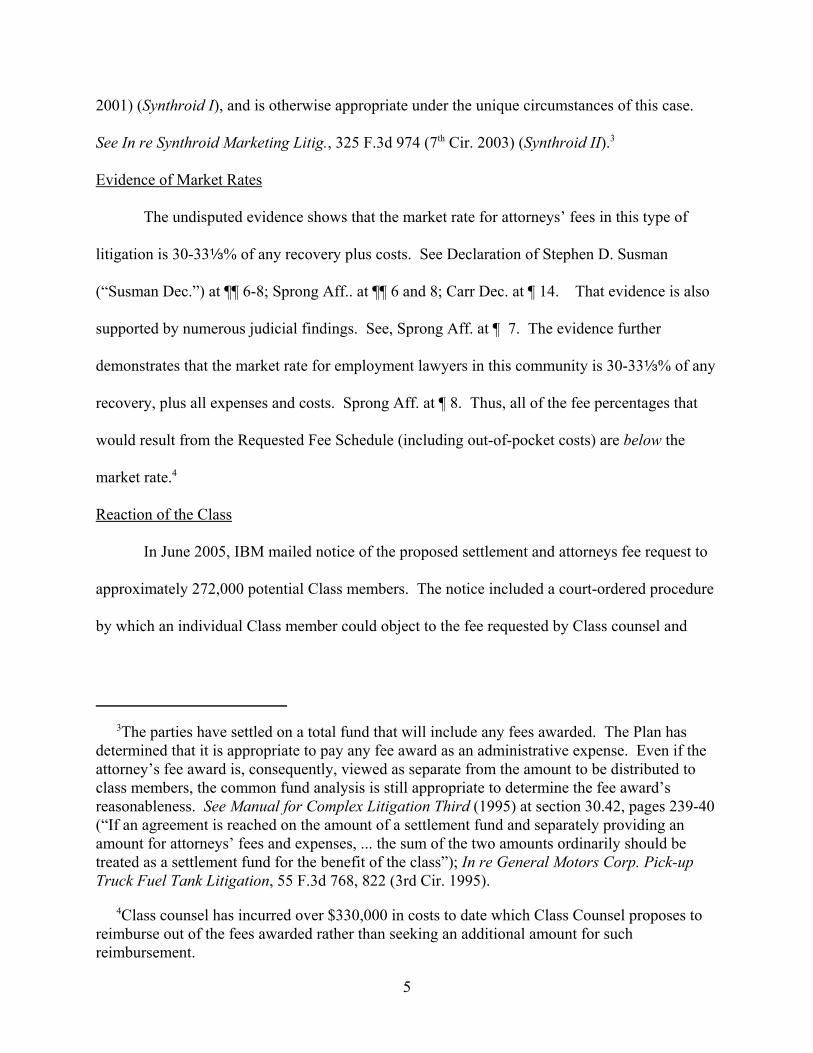

2001) (Synthroid I), and is otherwise appropriate under the unique circumstances of this case.

See In re Synthroid Marketing Litig., 325 F.3d 974 (7th Cir. 2003) (Synthroid II).3

Evidence of Market Rates

The undisputed evidence shows that the market rate for attorneys’ fees in this type of

litigation is 30-33a% of any recovery plus costs. See Declaration of Stephen D. Susman

(“Susman Dec.”) at ¶¶ 6-8; Sprong Aff.. at ¶¶ 6 and 8; Carr Dec. at ¶ 14. That evidence is also

supported by numerous judicial findings. See, Sprong Aff. at ¶ 7. The evidence further

demonstrates that the market rate for employment lawyers in this community is 30-33a% of any

recovery, plus all expenses and costs. Sprong Aff. at ¶ 8. Thus, all of the fee percentages that

would result from the Requested Fee Schedule (including out-of-pocket costs) are below the

market rate.4

Reaction of the Class

In June 2005, IBM mailed notice of the proposed settlement and attorneys fee request to

approximately 272,000 potential Class members. The notice included a court-ordered procedure

by which an individual Class member could object to the fee requested by Class counsel and

5Two other people objected to the fee, Russell Callaway and Barry Gordon, but they are notmembers of the Class and have no standing to object.

6

required that such objections be filed with the Court by July 11, 2005. In all, forty-five (45)5 of

the Class members timely objected to the requested fee, or less than two-one hundredths of one

percent (0.02 %) of the total number of Class Members. Even this minuscule number was

significantly inflated due to the efforts of one objector, Mr. James Leas. Using internet chat

boards, Mr. Leas posted his objection (which contains a number of inaccuracies regarding the

case and the settlement agreement and libelous statements regarding Class Counsel), and

encouraged Class members to simply copy his objection or write to the Court “agreeing” with

his letter. Despite that concerted and misleading effort by Mr. Leas, only 32 people followed

Mr. Leas’ request and filed anything with the Court, an insignificant number given the immense

size of the Class.

The “Leas Objectors” agree that Class Counsel should receive a percentage of the

settlement funds, but argue that the requested percentages are too high. The sole support for

their objection is a Cornell Law article which they contend mandates a lower percentage. In

point of fact, as set forth below, the Cornell Law article supports the reasonableness of the

Requested Fee Schedule. The handful of other objections to the requested fee fall into two

categories: 1) unsupported assertions that the fee is too high or should be based on hours; and 2)

the contention that the fee should be paid by IBM As outlined below, those arguments are

legally incorrect and unjustified.

7

Legal Analysis

1. A Common Benefit Fee Is Appropriate.

It is entirely appropriate to award Class Counsel a percentage of recovery fee in this

ERISA litigation. Florin v. Nationsbank, 34 F.3d 560, 563 (7th Cir. 1994); Tullock v. K-Mart

Corporation Employee Retirement Plan, No. 99-289-DRH (S.D. Ill. July 2002); Malloy v.

Ameritech, et al., Civ. No. 98-1044 GPM (S.D. Ill. July 21, 2000); Seifert v. May Department

Stores Pension Plan, Civ. No. 96-1028 GPM (S.D. Ill., the Honorable G. Patrick Murphy,

presiding); Medeika v. SNET Pension Plan, Civ. No. 3:97CV01123(DJS) (D. Conn. 1999); Local

56, United Food and Commercial Workers Union v. Campbell Soup Company, 954 F. Supp.

1000 (D.N.J. 1997); In re Unisys Corporation Retiree Medical Benefits ERISA Litigation, 886 F.

Supp. 445, 456 (E.D. Pa. 1995); Bowen v. Southtrust Bank of Alabama, 760 F. Supp. 889 (M.D.

Ala. 1991); New York State Teamsters Conference Pension and Retirement Fund v. Hoh, 561 F.

Supp. 687 (N.D.N.Y. 1983); Eaves v. Penn, 587 F.2d 453 (10th Cir.1978); Mark Berlind,

Attorney’s Fees under ERISA: When is an Award Appropriate?, 71 Cornell L. Rev. 1037, 1060-

61 (1986) (“Applying the common benefit doctrine reflects the statute’s purpose.... Nothing in

ERISA indicates that Congress intended to preempt the common benefit doctrine.”).

As the Ninth Circuit stated in Staton v. Boeing Company, 327 F.3d 938 (9th Cir. 2003),

“We conclude, as have the two other circuits that have addressed the issue, that there is no

preclusion on recovery of common fund fees where a fee-shifting statute applies.” Citing, e.g.,

Brytus v. Spang & Co., 203 F.3d 238, 246-247 (3d Cir. 2000) (holding that common fund fees

can be appropriate in both settled and litigated cases where statutory fees are potentially

available); Cook v. Niedert, 142 F.3d 1004 (7th Cir. 1998) (approving fees measured by common

fund rather than statutory principles where statutory fees were potentially available). See also

8

Boeing v. Van Gemert, 444 U.S. 472, 478, 62 L. Ed. 2d 676, 100 S. Ct. 745 (1980) (applying

common benefit fee in case litigated to judgment). This reasoning is particularly appropriate

here, where an award of attorneys fees under ERISA’s fee-shifting statute is not automatic and

depends upon a variety of factors. E.g. Quinn v. Blue Cross & Blue Shield Ass’n., 161 F.3d 472,

478 (7th Cir. 1998) . Thus, even where the plaintiffs’ attorney believes from the outset that his

clients’ case will likely prevail, which was not the case here, there is no guarantee that a victory

on the merits will result in a statutory fee award.

2. Percentage of the Fund is an Appropriate Award.

The Seventh Circuit has indicated that “the decision whether to use a percentage method

or a lodestar method remains in the discretion of the district court.” Florin v. Nationsbank of

Georgia, N.A., 34 F.3d 560, 566 (7th Cir. 1994). The Seventh Circuit has noted that in common

fund/benefit cases, “the measure of what is reasonable [as an attorney fee] is what an attorney

would receive from a paying client in a similar case.” Montgomery v. Aetna Plywood, Inc., 231

F.3d 399, 408 (7th Cir. 2000) (affirming district court’s award of 25% of the common fund and

reversing district court’s refusal to also award class counsel a share of the stock obtained for the

class); see also In re Continental Illinois Securities Litigation, 985 F.2d 867 (7th Cir. 1992) (writ

of mandamus issued to district court for failure to base contingent fee sought by class counsel on

contingent fees set by arms-length contracts in comparable commercial litigation). Thus, "[t]he

approach favored in the Seventh Circuit is to compute attorney's fees as a percentage of the

benefit conferred upon the class," particularly where that percentage of the benefit approach

replicates the market. Williams v. General Electric Capital Auto Lease, 1995 WL 765266, *9

(N.D. Ill. 1995); see also Long v. Transworld Airlines, Inc., 1993 WL 121824, *1 (N.D. Ill.

1993). This is particularly true in light of the Synthroid I and Synthroid II decisions, wherein the

9

Seventh Circuit now essentially dictates a percentage fee where the evidence before the district

court shows that such a fee is the “market” for such litigation.

In this case, the uncontested evidence is that plaintiffs could not afford to retain counsel

on any basis other than a contingent fee. Cooper Dec. at ¶ 3. Class representative Kathi Cooper

testified that she would not have hired Class counsel on an hourly basis. Id. Nor is there any

reason to believe that any other class member would have been willing to pay hourly fees in the

hope that the case would be successful and the fees paid ultimately recovered from IBM. Class

counsel, who are nationally recognized experts in ERISA pension benefit cases, have testified

that they have not and would not accept a similar case on any basis other than a contingency fee

basis. Sprong Aff. at ¶ 6; see also Susman Dec. at ¶¶ 6-7. And, as the evidence referenced

above confirms, no other capable counsel were willing to take the case on any basis. Thus, the

undisputed evidence is that the market for legal services for this litigation is a contingency fee.

3. Size of the Fund/Benefits.

The Seventh Circuit has rejected the so-called megafund cap. Synthroid I, 264 F.3d at

717 (reversing trial court’s 10% fee award for a determination of the market rate for such

litigation). Thus, the size of the recovery in this case (between $314 million and $1.714 billion)

does not impact the determination of an appropriate percentage fee. As the Synthroid case

instructs, a cap

cannot be reconciled with the approach our opinions adopt. We have held repeatedlythat, when deciding on appropriate fee levels in common-fund cases, court must do theirbest to award counsel the market price for legal services, in light of the risk of non-payment and the normal rate of compensation in the market at the time.

264 F.3d at 717. The Synthroid I Court instructed

On remand, the district court must estimate the terms of the contract that private plaintiffswould have negotiated with their lawyers, had bargaining occurred at the outset of thecase (that is, when the risk of loss still existed). The best time to determine this rate is

10

the beginning of the case, not the end (when hindsight alters the perception of the suit’sriskiness, and sunk costs make it impossible for the lawyers to walk away if the fee is toolow). This is what happens in actual markets. Individual clients and their lawyers neverwait until after recovery is secured to contract for fees.

Id. at 718 (emphasis in original).

4. The Percentage Requested Is Appropriate.

As noted, the Seventh Circuit has emphasized that the appropriate method to set a fee is

to award Plaintiffs' counsel the same percentage of the common benefit that they could have

expected to receive if they had negotiated a percentage contingent fee contract with a private

client in comparable commercial litigation. Synthroid I, 264 F.3d at 718; Gaskill v. Gordon, 160

F.3rd 361 (7th Cir. 1998) (affirming 38% fee award), citing Maksym v. Loesch, 937 F.2d 1237,

1246 (7th Cir. 1991); see also Matter of Continental Illinois Securities Litigation, 962 F.2d 566

(7th Cir. 1992), ("Continental Illinois I"), later proceeding, 985 F.2d 867 (7th Cir. 1993),

("Continental Illinois II"). As Judge Posner emphasized in Continental Illinois I:

The object in awarding a reasonable attorneys fee. . . is to simulate the market. . . Theclass counsel are entitled to the fee they would have received had they handled a similarsuit on a contingent fee basis with a similar outcome, for a paying client.

Continental Illinois I, 962 F.2d at 572.

The Synthroid I decision sets forth three benchmarks in reaching the “market rate,” the

first and foremost of which is the actual agreement negotiated prior to commencement of the

litigation. Id. at 718-19. The actual agreements negotiated prior to commencement of this case

call for the payment of 30% of any recovery plus costs. Thus, the primary benchmark identified

by the Synthroid I Court recommends an award higher than the Requested Fee Schedule.

Class Counsel’s contractual fee percentage is not unique. The uncontested evidence in

this matter shows that the 22.8% to 29% range of any recovery, without costs, is below the

market rate in similar contingency fee matters. Susman Dec. at ¶¶ 6-8; Sprong Aff. at ¶ 6-8.

11

Jeffrey Lewis, a very experienced and nationally recognized pension lawyer from San Francisco

has testified that his firm has regularly received fee award of 25 percent of the common funds

created for the classes in cases with less risk that this one. Lewis Dec. at ¶ 17. In addition to

demonstrating the reasonableness of Class Counsel’s Requested Fee Schedule, Mr. Lewis also

noted that Class Counsel are “among the few counsel in the country with the expertise to bring

this type of case.” Lewis Dec. at ¶ 13.

The second and third “benchmarks” the Synthroid I Court identified—fee agreements by

large claimants in similar litigation and auction criteria in securities disputes—are specifically

identified by the Synthroid I Court as securities-oriented criteria. As such, they are difficult to

apply to this litigation. A typical pension dispute involves a claim of at most several thousand

dollars by an individual who likely has limited understanding of the complex actuarial concepts

that underlie his claim. Moreover, there are no court supervised “auctions” to determine class

counsel fees in ERISA cases. In fact, unlike the securities field where there are frequently

dozens of firms competing to represent the class, thereby resulting in such “auctions” among

competing law firms, in the pension area in general, and in the context of this case in particular,

there is a paucity of law firms able and willing to take the enormous risks involved. As Mr.

Lewis has testified, because of the “risks and uncertainty inherent in [challenging a cash balance

plan as discriminatory], we did not initiate any such litigation until after this Court’s July 31,

2003 Opinion.” Lewis Dec. ¶ at 14.

Nevertheless, even if one were to apply the large claimant criterion in this case it clearly

supports the requested Fee Percentages. The Synthroid II Court noted that the sophisticated

third-party payors (the insurance companies) in that litigation negotiated a flat 22% rate even

after the risk of the litigation had passed and a recovery was assured. 325 F.3d at 976 and

12

978 (explaining the 22% rate was agreed to “after a good deal of the risk had been dissipated”

and that the TPPs still “had to offer 22% to sign up lawyers on a contingent fee.”). Applying

that reasoning to this case, with the undisputed risk attendant in all ERISA litigation and the

unique risk involved in this complex and novel litigation as well as the difficulty locating

experienced counsel to accept such litigation, clearly support the percentages set forth in the

Requested Fee Schedule. See also ETSI Pipeline Project v. Burlington No., Civ. No. B-84-979

CA (E.D. Tex. 1989) (plaintiffs’ counsel prosecuted a private case on a 33% contingency fee and

a third of a $635 million settlement).

The evidentiary record here in support of Class Counsel’s application is irrefutable.

Several of the best and most prominent employment firms in the country specifically refused to

take the case on behalf of the IBM employees on any terms. As nationally known pension

lawyer Mr. Lewis opines, there are only a handful of lawyers in the country who have the

expertise and background to practice in this area (compare this to the thousands of attorneys who

practice securities litigation) and none of whom he was aware were pursuing cases challenging

cash balance plans in 1999 or for years thereafter. Lewis Dec. at ¶¶ 12-14. So an “auction,” if

one had in fact taken place, inevitably would have produced exactly the percentages that Class

Counsel is suggesting here or even higher percentages. Susman Dec. at ¶ 8; Carr Dec. at ¶ 14.

Even assuming the Court could devise an imagined “auction” for this case, on the basis

of the evidence and the testimony before the Court from the various benefits lawyers, the only

reasonable conclusions would be that the rates would be the same or more than the Requested

Fee Schedule, and that Class Counsel’s skill and expertise in handling such matters would have

prevailed over a lesser bid from less experienced and accomplished counsel. As Stephen

Susman, a nationally known attorney with vast experience in large complex litigation, has

6See, e.g., In re Mercury Fin. Co., No. 97 C 3035 (N.D. Ill. July 6, 2001) (awarding one-thirdof fund); Retsky Family Ltd. Partnership v. PriceWaterhouse LLP, 2001 U.S. Dist. LEXIS 20397

(continued...)

13

testified, “if the Court had held an auction at the beginning of this case for qualified counsel to

undertake this litigation, no qualified firm would have proposed a fee structure below what Class

Counsel is requesting in this case.” Susman Dec. at ¶ 8; see also Carr Dec. at ¶ 14. Mr. Lewis

similarly testified that the rate proposed in the Requested Fee Schedule is reasonable and that his

firm has regularly received fees in the neighborhood of 25% in cases involving lower degrees of

risk.. Lewis Dec. at ¶ 17. Thus, the undisputed evidence before this Court indicates that under

the standards enunciated in Synthroid I and Synthroid II, Class Counsel’s Requested Fee

Schedule (inclusive of costs) is at or below what application of an “auction” scenario–or a

negotiated fee agreement with a group of nonclass clients comparable to the class in this case--

would have determined.

In this Circuit, a fee award of 33a% in class action litigation is not uncommon. The

utilization of the market percentage method in the courts of the Seventh Circuit, as one Court has

observed, results in awards of attorneys' fees "equal to approximately one-third or more of the

recovery." See Goldsmith v. Technology Solutions Co., 1995 U.S. Dist. LEXIS 15093 at *27

(N.D. Ill. Oct. 10, 1995) (citations omitted); In re Mexico Money Transfer Litig., 164 F.Supp.2d

1002, 1033 (N.D. Ill 2000) (recognizing “the established 30% benchmark for an award of fees in

class actions.”). The Seventh Circuit recently affirmed a 30% fee award even though the parties

settled at an early point in the litigation. Taubenfeld v. Aon Corp., 2005 U.S. App. LEXIS 13310

(7th Cir. July 5, 2005). Numerous Northern District of Illinois decisions, which are based on the

Seventh Circuit "marketplace" analysis typified by Continental I and II, reflect an actual range

of 29% to 39% of the recovery.6 Following the foregoing precedent, this Court recently awarded

6(...continued)(N.D. Ill. Dec. 10, 2001) (one-third); Gaskill v. Gordon, 942 F. Supp. 382 (N.D. Ill. 1998)(38%); Liebhard v. Square D Co., No. 91 C 1103 (N.D. Ill. June 6, 1993) (one-third); Goldsmithv. Technology Solutions Co., 1995 U.S. Dist. LEXIS 15093 (N.D. Ill. Oct. 10, 1995) (one-third);Hammond v. Hendrickson, No. 85 C 9829 (N.D. Ill. Nov. 20, 1992) (one-third); Long v. TransWorld Airlines, 1993 U.S. Dist. LEXIS 5063 (N.D. Ill. Apr. 15, 1993) (32%); Wanninger v.SPNV Holdings, No. 85 C 2081 (N.D. Ill. May 10, 1993) (32%); In re Caremark InternationalSec. Lit., No. 94 C 4751 (N.D. Ill. Dec. 15, 1997) (33%); In re Nuveen Fund Lit., No. 94 C 360(N.D. Ill. June 3, 1997) one-third); In re Soybean Futures Lit., No. 89 C 7009 (N.D. Ill. Nov. 27,1996) (one-third); Feldman v. Motorola, Inc., No. 90 C 5887 (N.D. Ill. June 28, 1995) (30%);Spicer v. Chicago Board Options Exchange, Inc., 844 F. Supp. 1226 (N.D. Ill. 1993) (29%);First Interstate Bank of Nevada, N.A. v. National Republic Bank of Chicago, No. 80 C 6401(N.D. Ill. Feb. 12, 1988) (39%).

14

Class Counsel 29% in the settlement of the Subclass 3 claims. Similarly, Judge Herndon

awarded the same percentage in Berger, Tullock and the MCI litigation, and this Court awarded

Class Counsel 29% in the Malloy litigation three years ago and in the Seifert action

approximately four years ago. These judicial findings are confirmed by Stephen Susman who

testified that if he had been requested to undertake this case for a group of clients on a nonclass

basis, he “would have done so only if they had agree[d] to pay expenses and also my standard 33

1/3 contingent fee.” Susman Dec. ¶ 6.

5. The Class Member Objections Should Be Overruled.

The fee request is strongly supported by the negligible number of objections that were

submitted by Class members. The percentage of Class members opposing the request is much

lower than the rates of opposition and exclusion in class action settlements that have been

approved by courts: see, e.g., Stoetzner v. U.S. Steel Corp., 897 F.2d 115, 118-19 (3d Cir. 1990)

(the fact that “only” approximately 10% of class members objected “strongly favors

settlement”); Grant v. Bethlehem Steel Corp., 823 F.2d 20, 24 (2d Cir. 1987) (affirming district

court’s approval of class action settlement over opposition of 36% of class); TBK Partners, Ltd.

v. Western Union Corp., 675 F.2d 456, 462 (2d Cir. 1982) (affirming district court’s approval of

7The study can be found at http://w4.stern.nyu.edu/emplibrary/03-017.pdf

15

class action settlement despite objection of class member who owned 50% of shares affected by

settlement); Cotton v. Hinton, 559 F.2d 1326, 1331 (5th Cir. 1977) (approving settlement over

objections of counsel purporting to represent nearly 50% of class). The de minimis level of

Class member disapproval here is especially significant in light of the extensive direct notices

that have been provided and the national attention both this case and the proposed settlement

received.

The Leas Objections

Leas' fee argument ignores Synthroid and any other relevant authority. Instead, it relies

almost totally on information he selectively culls from a Cornell statistical study of class action

fee awards.7 It is a dense study, so perhaps that explains why Mr. Leas did not read it very

carefully. For instance, he omits the study’s recommendation concerning how a court should use

its results.

After a review of voluminous data, the study constructs a table showing fee percentages

for non fee-shifting class action settlements between 1993 and 2002 in ten more or less equally

sized "deciles" of recovery amount. This case falls into the 10th decile - cases with recoveries

of more than $190 million. For each decile, the study shows the mean fee percentage ( the mean

is arrived at by averaging the percentage recoveries for the cases in that decile), the median fee

percentage (the median is the mid point between the highest percentage amount and the lowest

percentage amount), and the "standard deviation" ( which is a statistical construct used to reflect

how wide the spread is for the actual numbers that make up the mean and median calculations).

The Study explains how a court evaluating a fee request should use those numbers:

16

Our suggestion is that fee requests falling within one standard deviation above or below the mean should be viewed as generally reasonable and approved by the court unless reasons are shown to question the fee. Fee requests falling within one and two standard deviations above or below the mean should be viewed as potentially reasonable but in need of affirmative justification.

Study, p. 38.

For the Cornell cases in the over $190 million decile, which had an average recovery

amount of $929 million, the mean fee percentage is 12.0 and the median is 10.1. The standard

deviation percentage is 8.1. Using those numbers the way the authors recommend, a fee request

of up to 20.1% (the mean of 12.0 plus the standard deviation of 8.1) on a recovery of $929

million should be presumptively reasonable and a fee of 28.2% would be "potentially

reasonable." Study, p. 38. The authors enumerated several factors that appeared to have

supported fee awards in the "potentially reasonable" range. These include the complexity of the

case and the court's assessment of the risk involved. Study, pp. 38-40. Another factor appearing

from the Study is that the fee percentage tended to differ from the mean depending upon the type

of case involved. In that regard, securities, ERISA, employment and civil rights cases tended to

have fees that were a higher percentage of the recovery than the mean, while tort, consumer, and

tax refund cases tended to result in fee percentages below the mean.

The complexity and risks associated with this case clearly support the Court utilizing an

upward deviation of approximately 1½ times the standard deviation. In short, the Cornell Study

that forms the entire basis for the Leas’ objections actually demonstrates the reasonableness of

the Requested Fee Schedule.

It is also significant that the numbers in the 10th decile are highly impacted by one case.

According to the study, in 2000, a class action settlement of $3.6 billion had a fee award of "over

$200 million." Study, p. 24. Even if one assumes that the fee was $250 million, the fee was only

8Removing that very unique and anomalus case from the study would further demonstrate thereasonableness of the Requested Fee Schedule.

9Stuart J. Logan, Jack Moshman & Beverly C. Moore, Jr., Attorney Fee Awards in CommonFund Class Actions, 24 Class Action Rep. 169 (2003).

17

6.9% of the recovery. Such a very low percentage fee on such a huge recovery (which flies in

the face of Synthroid’s requirements) necessarily skewed the mean and median percentages for

the decile considerably downward from what they would have been if that “outlier”case were left

out of the sample (something that most statisticians probably would have done).8

Some of that skewing effect can be seen, and corrected, by looking at the results from

data used in the Class Action Reports study,9 for which the sample size was about twice as large

as the Cornell Study. In CAR's study, for the over $190 million decile, the mean fee percentage

was 16.4%, the median was 17.6%, and the standard deviation was 9.6%. So, using the CAR

percentages, a fee award of 26% on a $929 recovery would be presumptively reasonable and an

award of up to 35.6% potentially could be reasonable, depending on the complexity of the case

and the risks involved.

Objections that the Fee Is too High or Should Be Hourly

The undisputed evidence in this matter shows that the declining percentages requested

are at or below the market rate. Susman Dec. at ¶¶ 6-8; Sprong Aff. at ¶¶ 6-8; Lewis Dec. at 17;

Carr at ¶ 14. As explained above, the goal in the Seventh Circuit in setting a percentage is to

mirror the market. The market is determined before the recovery is known for, as Judge

Easterbrook notes in Synthroid I, no one negotiates a fee after the case is over. It is undisputed

that at the time this case was filed the risks of the litigation were enormous. Lewis Dec. at ¶14;

Cooper Dec. at ¶ 3. It is therefore not surprising that the undisputed evidence in this matter is

18

that the market rate or percentage for litigation of this type with comparable risk is the same or

higher than what Class Counsel are requesting. Susman Dec. at ¶¶ 6-8.

An hourly award likewise is not what the market dictates for this litigation and would be

improper under Synthroid. According to the testimony of Class counsel, no qualified attorney

would take on this type of litigation in return for the possibility of receiving an hourly award.

Sprong Aff. at ¶ 6; Susman Dec. at ¶ 6; Lewis Dec. at ¶¶ 16-17. Moreover, no plaintiff could

afford to pay an hourly fee as the case proceeded in the hopes that his attorney would recover

those fees at the end of the case. Cooper Dec. at ¶ 3.. For those reasons, the undisputed

evidence before this Court is that the standard fee agreement in the market for this type of case is

a contingency fee where the plaintiffs’ counsel expends all of the time and resources necessary

to prosecute the case and receives a percentage of any recovery, whether by settlement or

judgment.

Objections that IBM Pay the Fee.

The existence of a possible shifting of hourly fees and costs to the Plan does not affect

the propriety of awarding fees based on the common fund or benefit achieved. Florin v.

Nationsbank, 34 F.3d 560, 563 (7th Cir. 1994), quoting Mark Berlind, “Attorney’s Fees under

ERISA: When is an Award Appropriate?,” 71 Cornell L. Rev. 1037, 1060-61 (1986) (“Applying

the common benefit doctrine reflects the statute’s purpose.... Nothing in ERISA indicates that

Congress intended to preempt the common benefit doctrine.”); see also Staton v. Boeing Co.,

327 F.3d 938 (9th Cir. 2003) (no bar to common benefit award merely because a fee shift might

have been awarded); Cook v. Niedart, 142 F.3d 1004 (7th Cir. 2001) (same); Brytus v. Spang &

Co., 203 F.3d 238 (3rd Cir. 2000) (same in a case litigated to judgment). There is no case holding

that the presence of a fee-shifting statute precludes awarding fees under the equitable common

10Quinn shows that statutory fees are used to deter defendants from asserting bad faithdefenses. In contrast, common fund awards are used to provide incentives to plaintiffs’ counselto bring difficult but meritorious cases.

19

benefit doctrine. Indeed, a fee awarded against the Plan under ERISA’s fee shifting provision

would be calculated under the lodestar hourly approach without any multiplier for risk, but the

undisputed testimony before the Court is that no competent attorney would take this type of

litigation in return for possibly receiving an hourly fee from the defendant. E.g. Lewis Dec. at ¶

16.

It is also critical that statutory fees under ERISA are governed by Quinn v. Blue Cross &

Blue Shield Ass’n., 161 F.3d 472, 478 (7th Cir. 1998). Quinn sets out a five factor test on

whether to award fees to the “prevailing party.” In general, the party must show that the losing

party’s case or defense was asserted in bad faith and was interposed simply to harass the other

side. Given that several other district courts have ruled that cash balance formulas do not violate

ERISA § 204(b)(1)(H), this Court repeatedly stated that the case was a complex one that it

believed would ultimately be resolved by the United States Supreme Court, and the fact that the

IRS, the Treasury Department and the Department of Labor have failed to condemn pension

equity or cash balance formulas, the Class could not have shown that IBM’s defense was not in

good faith and was interposed simply for the purpose of harassment. Thus, statutory fees would

not be available to the Class even if the Class prevailed on all issues.10

Awarding an Incentive Fee Is Appropriate.

Finally, incentive fees of $40,000 for Ms. Cooper and $20,000 Ms. Harrington are

appropriate. The Seventh Circuit has indicated that incentive fees are designed to encourage

individuals to become named plaintiffs. Continental I, 962 F.2d at 571-72. Here, Ms. Cooper

and Ms. Harrington should be rewarded for their willingness to pursue relatively modest

20

monetary claims against their former employer’s pension plan on behalf of thousands of former

colleagues. Granting an incentive fee will serve the added purpose of encouraging other

individuals to pursue similar litigation in an effort to recover additional retirement benefits under

the law.

Conclusion

For all the foregoing reasons, Class Counsel ask the Court to award Class Counsel fees

and costs in accord with the Requested Fee Schedule. Such an award would be below the

market rate for comparable litigation and is within the customary range of awards in this Circuit.

The Court should also find that the requested incentive fees for the class representatives are

appropriate.

WHEREFORE, Class counsel prays the Court enter its Order 1) awarding Class Counsel

fees and costs in accord with the Requested Fee Schedule to be paid in accord with the

Settlement Agreement, and 2) approving payment of a $40,000 incentive award to Kathi Cooper

and a $20,000 incentive award to Beth Harrington, both to be paid from the attorneys’ fee award.

Respectfully submitted,

/s/ Douglas R. SprongDouglas R. Sprong Steven A. KatzKorein Tillery, LLC701 Market, Suite 300St. Louis, MO 63101(314) 241-4844Fax: (314) 588-7036

Robert F. HillJohn H. EvansHill & Robbins, P.C.100 Blake Street Building1441 Eighteenth StreetDenver, CO 80202

21

(303) 296-8100Fax: (303) 296-2388

William K. CarrLaw Offices of William K. Carr2222 E. TennesseeDenver, CO 80209(303) 296-6383Fax: (303) 296-6652

Attorneys for the Class

CERTIFICATE OF SERVICE

I certify that on August 2, 2005, I electronically filed the foregoing with the Clerk ofCourt using the CM/ECT system which will send notification of such filings to the following:

Frederick J. Hess [email protected], Rice & Fingersh325 South High StreetBelleville, IL 62220

Jeffrey G. Huvelle [email protected] D. Wick [email protected] Covington & Burling1201 Pennsylvania Ave., N.W.Washington, D.C. 20044-7566

I certify, in addition, a copy of the fee request was mailed by UPS Second Day Air toobjectors (or by regular mail to objectors providing only a P.O. Box).

/s/ Douglas R. Sprong