Embed Size (px)

Citation preview

KASPAR Associates Ltd

Residential PanelERES

Dr Karen A Sieracki MRICSVisiting Professor University of Ulster

Director, KASPAR Associates London

5 July 2013

KASPAR Associates Ltd

Introduction UK Residential

Look at the UK Been some

institutional interest State of the market –

demand, supply, performance

Issues

KASPAR Associates Ltd

Residential Vehicles and Capital

Capital raising Jan-May 2013, 2 funds closed total of £455m (23%) out of UK total capital raised £1.94 bn

Possibility of PAIF structure No residential REITs despite trying EG Blackrock in US Single Family Fund 17,000

properties in 12 US markets, $3bn cost + 10% purchase price for refurb, LTV 66%, 20% IRR 5 yr hold

KASPAR Associates Ltd

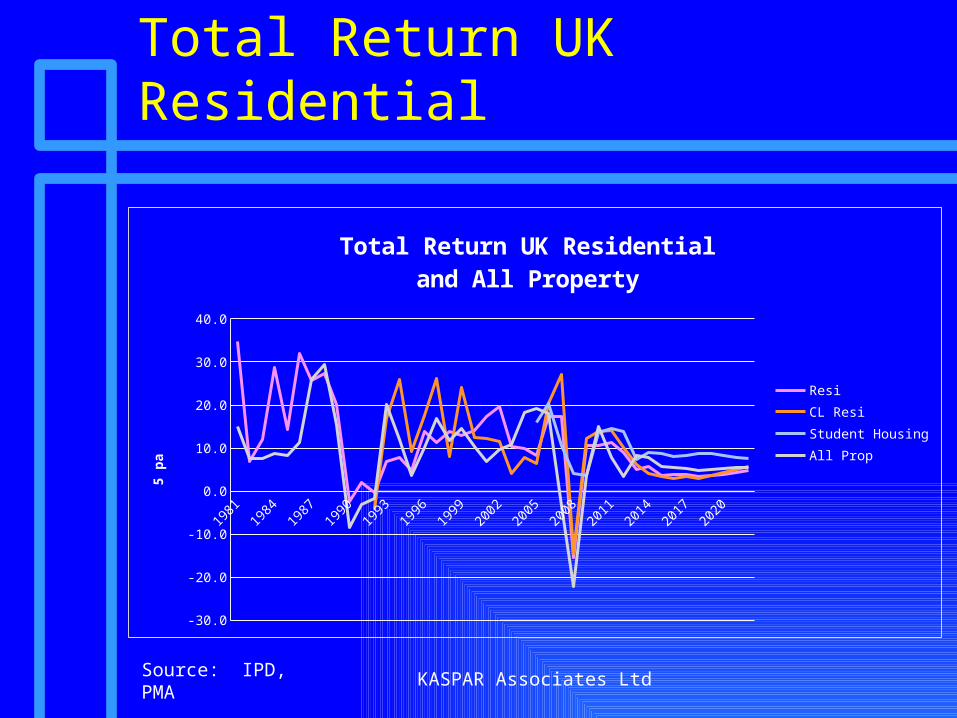

Total Return UK Residential

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

Total Return UK Residential and All Property

Resi

CL Resi

Student Housing

All Prop

5 pa

Source: IPD, PMA

KASPAR Associates Ltd

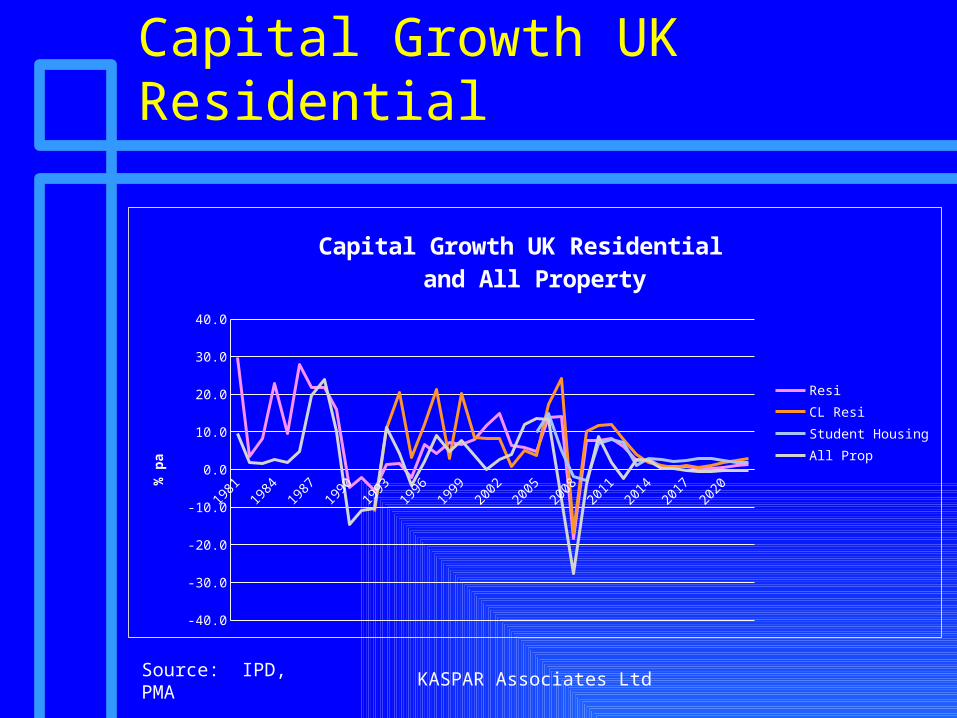

Capital Growth UK Residential

Source: IPD, PMA

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

Capital Growth UK Residential and All Property

Resi

CL Resi

Student Housing

All Prop

% p

a

KASPAR Associates Ltd

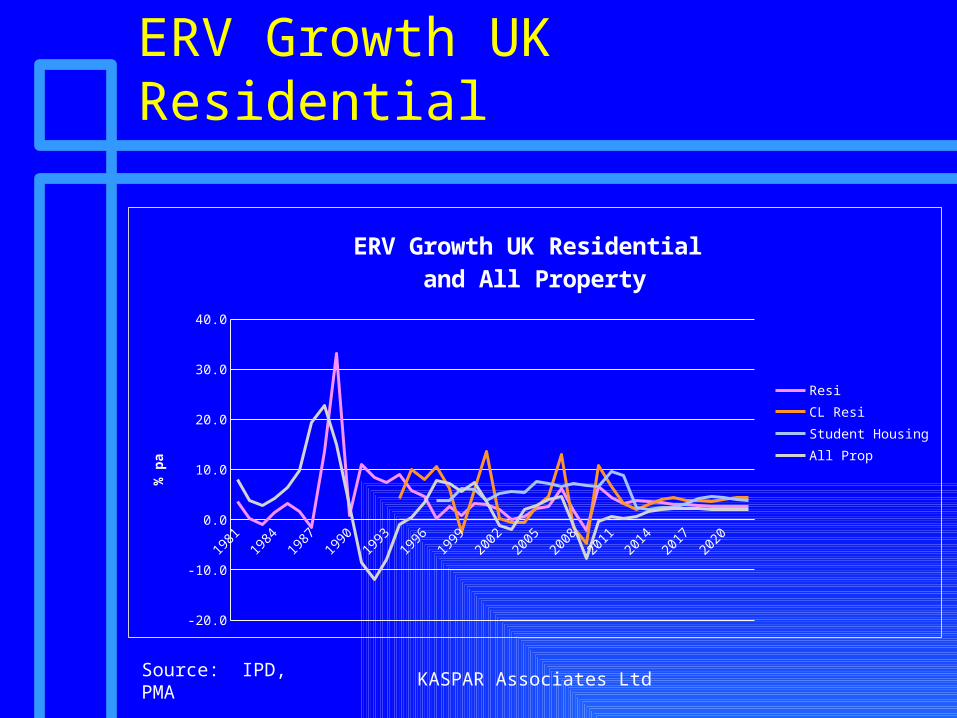

ERV Growth UK Residential

Source: IPD, PMA

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

ERV Growth UK Residential and All Property

Resi

CL Resi

Student Housing

All Prop

% p

a

KASPAR Associates Ltd

Income Return UK Residential

Source: IPD, PMA

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Income Return UK Residential and All Property

Resi

CL Resi

Student Housing

All Prop

% p

a

KASPAR Associates Ltd

UK Residential

Acts as a capital play, not income Valuation on vacant possession High management cost and special skill set required Lack of availability of product to get economies of scale Could link with a homebuilder (eg M&G and Berkeley

Homes which was a sweet heart deal) Need to “build to let” so valued on income Why not special zones for rented housing UK housing market in a bubble, Central London rents

falling Government schemes

KASPAR Associates Ltd

UK Residential

Demand for renting from inbetweenies Affordability to rent and/or buy £4 trillion market, larger than the commercial stock of

£280bn Supply usually individuals doing buy to let single property Lack of modern space

KASPAR Associates Ltd

UK Institutional Requirement

Need size, scale and location Private rented market fragmented with buy to let owners Quality of stock and energy efficiency Have to go out and find it for what return – commercial is

easier

KASPAR Associates Ltd

UK Residential– Trophy or Trash?

KASPAR Associates Ltd

UK Residential

So why bother?

Can make more money elsewhere

Bottom line for investors and the business

![Kummer, kaspar 2 duos for flute and clarinet, op.46[1]](https://img.pdfslide.us/doc/110x75/55633380d8b42a5c7b8b4f8b/kummer-kaspar-2-duos-for-flute-and-clarinet-op461.jpg)