Embed Size (px)

Citation preview

An in-depth analysis of the amendments

made by the Finance (no. 2) Bill, 2014

With the maiden budget of the government formed by

a clear majority being presented, we, at Kantilal Patel

& Co., have compiled the impact that it will be having

on the road ahead. The impact analysis of the Budget

has been done with the vision to benefit each reader,

be it the corporates, the individuals or even the

students alike. The ease of accessing and

understanding the following publication has been

achieved by its contributors by putting themselves in

the reader’s shoes. It would be improper if we don’t

recognize the untiring efforts put in by Hemant, Kajol,

Manali, Satish, Suchit and Vishal for bringing this

publication in the final form. Finessing the publication

was a result of the review done by Shri Rajesh Shah.

-Dipam Patel

KANTILAL PATEL & CO.

Chartered Accountants

Ahmedabad

[Last updated: 19.07.2014]

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

1

When the UPA alliance had come to power in 2009, India witnessed

its tenth successive coalition government in 20 years. The now Prime

Minister, Narendra Modi has been voted for change. After so many

years, India has been able to see a government that could be formed

by a single party. The ruling party had assumed office and in less than

45 days, brought out its first budget. People of India wanted to see a

huge change in the budget; which it perceived, because of the

dramatic victory of the ruling party. The government delivered a few

hits but it did not turn out to be a clean sweep, as one would call it.

Most of the economists were satisfied with the budget and all could

possibly attribute it to a resounding reason, DIRECTION! In a number

of interviews of the top economists and practitioners, a common

mention was found for the direction that the budget mentioned. A

mention was found to the various planned schemes of the

government towards growth and a number of allocations were made

to the various schemes directed to nurture growth in the economy.

The key highlights of the budget are presented herewith for your

reference.

We have divided the publication under three parts; Figures, Direct Tax

and Service Tax. In addition to just providing the highlights of the

changes proposed by the Finance Bill, 2014; we have strived to put

together the implication that the proposed changes would be having

on your business. We strive to disseminate information in a manner

that adds value in the readers. In our endeavour, we have included

even the dates with effect from which the provisions will get

applicable as well as the planning (wherever available) that can be

done by the tax payers before the proposed amendments become

effective.

We hope that you enjoy reading the budget analysis made by our

dedicated team. We wish to hear from you with your opinion on how

did you find the reading material? Write to us at [email protected].

Happy reading!

P

R

E

F

A

C

E

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

2

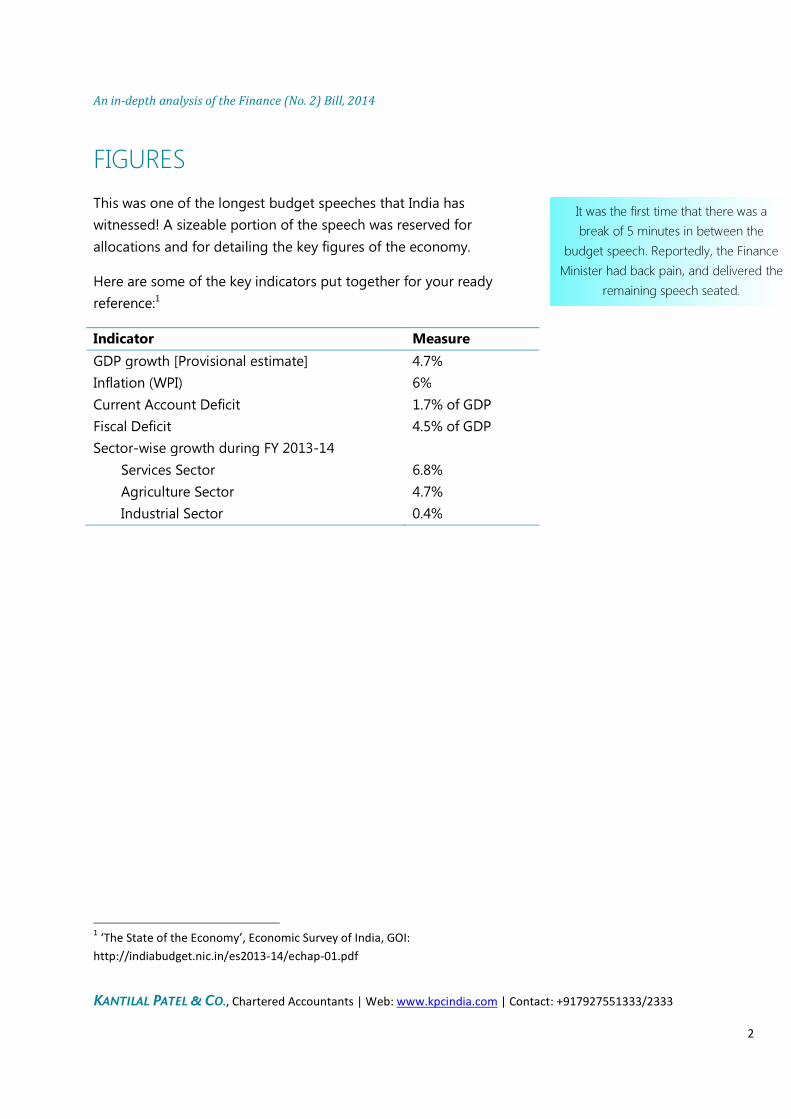

FIGURES

This was one of the longest budget speeches that India has

witnessed! A sizeable portion of the speech was reserved for

allocations and for detailing the key figures of the economy.

Here are some of the key indicators put together for your ready

reference:1

Indicator Measure

GDP growth [Provisional estimate] 4.7%

Inflation (WPI) 6%

Current Account Deficit 1.7% of GDP

Fiscal Deficit 4.5% of GDP

Sector-wise growth during FY 2013-14

Services Sector 6.8%

Agriculture Sector 4.7%

Industrial Sector 0.4%

1 ‘The State of the Economy’, Economic Survey of India, GOI:

http://indiabudget.nic.in/es2013-14/echap-01.pdf

It was the first time that there was a

break of 5 minutes in between the

budget speech. Reportedly, the Finance

Minister had back pain, and delivered the

remaining speech seated.

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

3

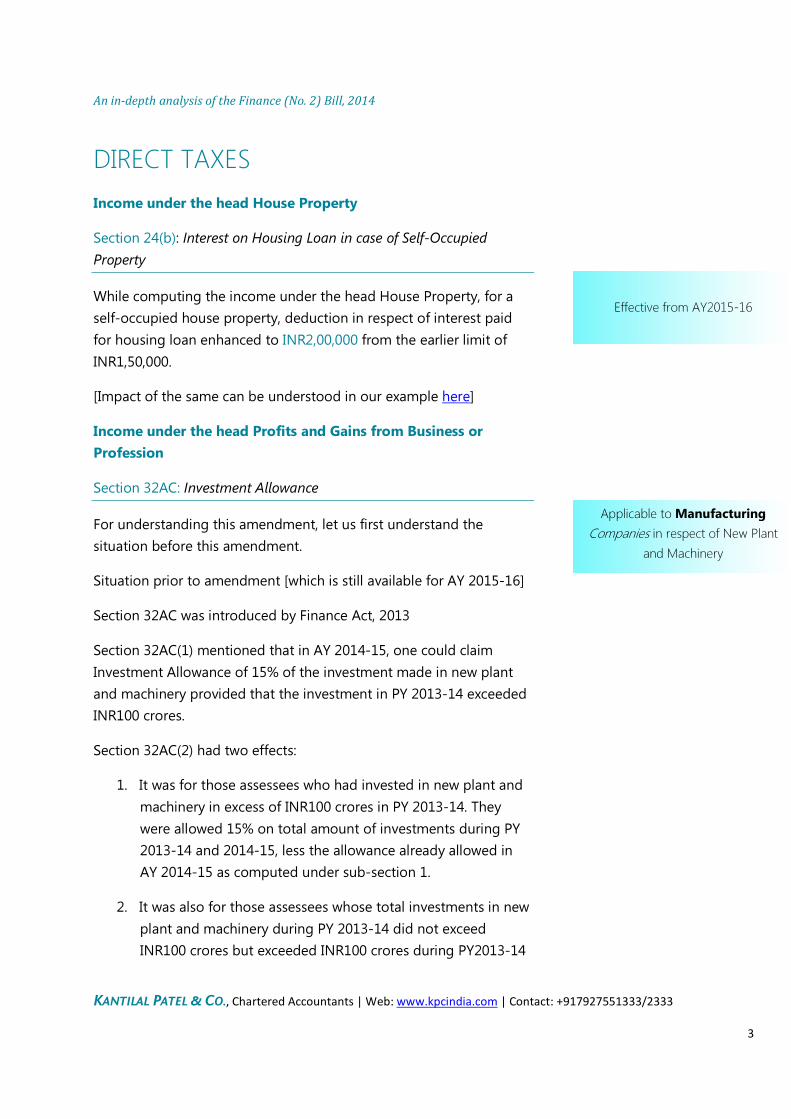

DIRECT TAXES

Income under the head House Property

Section 24(b): Interest on Housing Loan in case of Self-Occupied

Property

While computing the income under the head House Property, for a

self-occupied house property, deduction in respect of interest paid

for housing loan enhanced to INR2,00,000 from the earlier limit of

INR1,50,000.

[Impact of the same can be understood in our example here]

Income under the head Profits and Gains from Business or

Profession

Section 32AC: Investment Allowance

For understanding this amendment, let us first understand the

situation before this amendment.

Situation prior to amendment [which is still available for AY 2015-16]

Section 32AC was introduced by Finance Act, 2013

Section 32AC(1) mentioned that in AY 2014-15, one could claim

Investment Allowance of 15% of the investment made in new plant

and machinery provided that the investment in PY 2013-14 exceeded

INR100 crores.

Section 32AC(2) had two effects:

1. It was for those assessees who had invested in new plant and

machinery in excess of INR100 crores in PY 2013-14. They

were allowed 15% on total amount of investments during PY

2013-14 and 2014-15, less the allowance already allowed in

AY 2014-15 as computed under sub-section 1.

2. It was also for those assessees whose total investments in new

plant and machinery during PY 2013-14 did not exceed

INR100 crores but exceeded INR100 crores during PY2013-14

Effective from AY2015-16

Applicable to Manufacturing

Companies in respect of New Plant

and Machinery

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

4

and 2014-15, and allowance in respect of entire investments

over the period of two years was allowed in the second

assessment year.

This has now been extended in a simpler manner and reduced

threshold with a sunset clause [up to AY 2017-18]:

Investment allowance of 15% of the cost of new plant and machinery

would be allowed as deduction in the AY 2015-16, 2016-17 and 2017-

18, if in the respective previous years, investment in new plant and

machineries exceed INR25 crores.

1. The section has been amended to make it applicable per

financial year instead of spreading it over a period of two

years.

2. Benefit can be availed in all the three assessment years

provided that the investment in each respective previous year

exceeds INR25 crores.

3. Benefit under the inserted sub-section (i.e. sub-section 1A)

cannot be claimed if benefit has been claimed under sub-

section 1 for AY 2015-16.

4. This deduction would be in addition to normal depreciation as

per the rates prescribed under the act. If remaining

unabsorbed, the same shall be allowed to be carried forward

for a period of 8 years as business loss [provided that the

return of income is filed within the prescribed time limit]

[Impact of the same can be understood in our example here]

Section 37: No deduction of CSR Expenses

Section 135 of the Companies Act, 2013 has imposed a

requirement on certain companies to spend a minimum of 2%

of their profits on activities relating to Corporate Social

Responsibility.

Expenditure incurred for the above stated purpose shall not

be considered as incurred for the purpose of business or

Effective from AY2015-16

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

5

profession and therefore shall not be allowable as

expenditure.

The specific explanation has been added to Section 37 only. It does

not disentitle a business from planning to spend in a manner that

enables it to take tax benefit under any other section of the Income

Tax Act, 1961 and at the same time, also fulfilling the requirement of

Section 135 of the Companies Act, 2013.

[Impact of the same can be understood in our example here]

Section 40(a)(i) & 40(a)(ia): Disallowance of Expenditure on account of

Non deduction of TDS

Only 30% of the amount of expenditure shall be disallowed

for non-deduction of TDS on certain payments or non-

payment after deduction of the same before the due date of

filing return of income.

No disallowance of amounts paid/ payable to non-residents

from which taxes are withheld in the previous year and

deposited before the due date of filing of tax return. This

amendment brings the payments made to non-residents at

par with payments made to residents.

The provisions of section 40(a)(ia) did not cover certain

expenses such as Salary, etc. It is now proposed to cover all

expenses on which tax is deductible at source.

[Impact of the same can be understood in our example here]

Income under the head Capital Gains

Section 2(14): Transfer of securities held by FIIs to be taxable under the

head Capital Gain

Definition of Capital Asset as contained in clause 14 of Section 2 of

the Income Tax Act, 1961 has been amended by inserting sub-clause

b which includes securities held by a Foreign Institutional Investor.

This amendment brings to an end the long standing controversy as to

whether such gains were taxable as Business Income or Capital Gains.

Effective from AY2015-16

Effective from AY2015-16

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

6

Section 51: Taxability of advance money forfeited under failed

negotiations for transfer of capital asset to be taxed under the head

Income from Other Sources

This would be the case, even when the sale takes place after the

amendment brought in by the Finance Bill, 2014. The Bill mentions

this amendment to be prospective. Hence, the advance forfeited

before April 1, 2014 will continue to be adjusted to the original cost

of acquisition as per the old provision.

[Impact of the same can be understood in our example here]

Section 54, Section 54F: Only one house to be allowed, that too in

INDIA

Section 54 relates to exemption from Capital Gain arising from

transfer of Long Term Capital Asset, being a residential house

or building; whereas, Section 54F relates to exemption from

Capital Gain arising from transfer of Long Term Capital Asset,

other than that relating to Section 54.

The proposed amendment puts to rest the controversy as to

whether long term capital gain arising from sale of a

residential house [S.54] or long term capital asset [S.54F] can

be invested in more than one house to claim exemption.

It is now proposed that the exemption will be available only

for one house, purchased or constructed as residential house

in India.

Section 54EC: Exemption amount limited to a total of INR50 Lacs

Earlier, the drafting of the section was such that the

practitioners had found a loop hole, providing their clients

with exemption of INR1 crore by timing the investments in a

period of six months over two FYs. This was even supported

by an Ahmedabad ITAT judgment.

The Finance Bill, 2014 has restored the intention of the

government at the time of drafting, by clearly specifying that

the assessee can avail exemption of maximum amount of

Effective from AY2015-16

Effective from AY2015-16

Effective from AY2015-16

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

7

INR50 lacs irrespective of the financial year in which it is

invested.

An important thing to note here is that the Finance Bill, 2014

proposes the effective date of this proposal to be the 1st of

April 2014. Accordingly, it would mean that the persons who

made investment in more than one house, or outside India,

between the 1st of April 2014 and the 30th of June, 2014 will

not be eligible for this deduction. However, if the Finance Act,

2014 amends otherwise, it would result in a different scene.

Section 2(42A): Short term capital asset

Unlisted Securities and units of mutual fund other than equity

oriented funds would be short term capital asset if held for 36

months or less instead of the earlier period of 12 months.

Key Impact of the above mentioned provision relates to the

investors who had planned their investments in the last 12-15

months with the intended outcome of their gain being treated

as long term. They would be required to be pay tax on short

term capital gain arising from transfer of these units.

We would like to draw our readers’ attention to one such

similar case in the past. Finance Bill, 2003 had proposed to

deny exemption to any sum received under an insurance

policy in respect of certain life insurance policies with effect

from April 01, 2003. It had created a fury amongst the holders

of the policy, because the amendment proposed to tax the

consideration received out of the decision that had been

taken at a time when the outcome was not taxable. In this

case, the Finance Act, 2003 had modified the proposed

amendment to tax such insurance policies ISSUED after the

effective date.

One may expect such an outcome this year also, but it is not

possible to comment currently.

[Impact of the same can be understood in our example here]

Effective from AY2015-16

The exemption in this case would be

disallowed for the investment made

outside India as well for the second

house onwards.

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

8

Income from Other Sources

Section 56(2)(ix): Taxability of advance money forfeited under failed

negotiations for transfer of capital asset to be taxed under the head

Income from Other Sources

Refer this part of the document

Deductions under Chapter VI-A

Section 80C:

Limit of deduction has increased from INR1,00,000 to

INR1,50,000.

Accordingly, the limit of contribution to PPF is also increased

from INR1,00,000 to INR1,50,000.

[Impact of the same can be understood in our example here]

Section 80CCE:

The aggregate limit of deduction u/s 80CCE (covering section

80C, 80CCC and 80CCD) is also increased to INR1,50,000.

Section 80IA:

100% deduction is allowable to an undertaking set up for the

generation & distribution of power, transmission and

distribution, renovation and modernization of existing

network of transmission or distribution lines.

Provisions relating to Dividend

Section 115BBD: Dividends from Foreign Companies

Sunset clause for taxing dividend income received from

specified foreign company at the rate of 15% removed. Hence,

dividends received from specified foreign companies to be

taxed at 15% irrespective of the assessment year.

The deduction is now available up to

March 31, 2017.

Effective from AY2015-16

Effective from AY2015-16

Effective from AY2015-16

To be available irrespective of the

assessment year

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

9

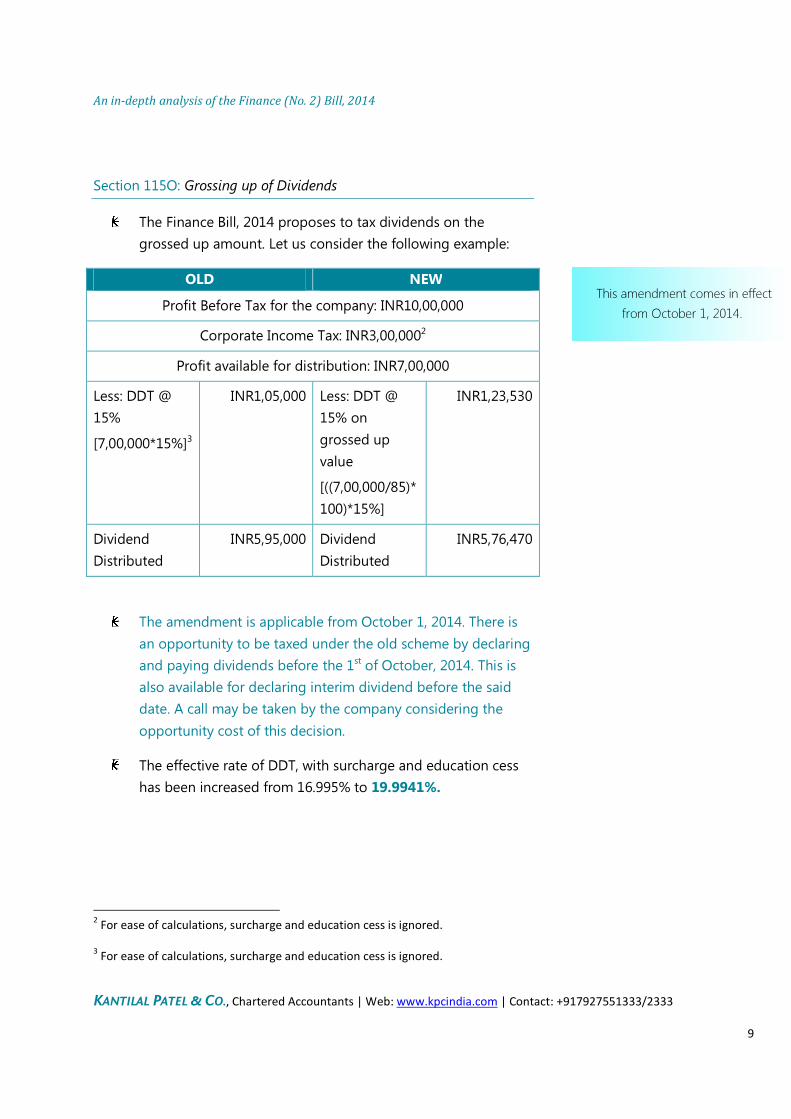

Section 115O: Grossing up of Dividends

The Finance Bill, 2014 proposes to tax dividends on the

grossed up amount. Let us consider the following example:

OLD NEW

Profit Before Tax for the company: INR10,00,000

Corporate Income Tax: INR3,00,0002

Profit available for distribution: INR7,00,000

Less: DDT @

15%

[7,00,000*15%]3

INR1,05,000 Less: DDT @

15% on

grossed up

value

[((7,00,000/85)*

100)*15%]

INR1,23,530

Dividend

Distributed

INR5,95,000 Dividend

Distributed

INR5,76,470

The amendment is applicable from October 1, 2014. There is

an opportunity to be taxed under the old scheme by declaring

and paying dividends before the 1st of October, 2014. This is

also available for declaring interim dividend before the said

date. A call may be taken by the company considering the

opportunity cost of this decision.

The effective rate of DDT, with surcharge and education cess

has been increased from 16.995% to 19.9941%.

2 For ease of calculations, surcharge and education cess is ignored.

3 For ease of calculations, surcharge and education cess is ignored.

This amendment comes in effect

from October 1, 2014.

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

10

Provisions relating to TDS

Section 194DA: Payment in respect of Life Insurance Policy

TDS at the rate 2% to be deducted from payment made to a

resident in excess of INR1,00,000 in a financial year under a

life insurance Policy, other than the amount of policy exempt

under section 10(10D).

Section 194LC: TDS on loan agreements/ bonds

TDS at the rate of 5% extended to interest on all loan

agreements entered into at any time on or after the 1st day of

July, 2012 but before the 1st day of July, 2017.

TDS at the rate of 5% even extended to interest on any long-

term bond including long-term infrastructure bond at any

time on or after the 1st day of October, 2014 but before the 1st

day of July, 2017.

Provisions relating to Transfer Pricing

Transfer Pricing has been an area of litigations with sometimes

absurd adjustments being made to the transfer price.

The scope of deemed international transactions widened a bit.

Advanced Pricing Agreements [APA] are a good way to

determine the Arm’s Length Price or determining the manner

in which the ALP is to be determined in relation to an

international transaction which is to be entered into by a

person.

Currently, the APAs are effective for 5 years prospective. The

Finance Bill, 2014 proposes to amend the provision relating to

APAs to make them effective for even 4 years retrospectively,

i.e. to make them effective for assessments relating to 4

previous years prior to the year in which the APA is entered.

This amendment comes in effect

from October 1, 2014.

Effective from AY2015-16

This amendment comes in effect

from October 1, 2014.

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

11

Provisions relating to Charitable Trusts

Section 11(6): Income from property held for Charitable or religious

Purposes

At present, depreciation is allowed on assets (capital

expenditure) claimed as deduction under application of

income. It is proposed that hence forth, depreciation shall not

be allowed on such assets, which have been claimed under

application of income.

Section 12AA: Cancellation of Registration

It is proposed that the registration under section 12AA can be

withdrawn by the principal Commissioner or the

Commissioner if the activities of trust are carried out in

following manner as referred in Section 13(1).

Income of trust does not ensure for the benefit of general

public.

It is for benefit of any particular religious community or

caste (trust established after commencement of Act).

Income or property of trust is applied for benefit of

specified person.

Funds of trusts are invested in prohibited modes.

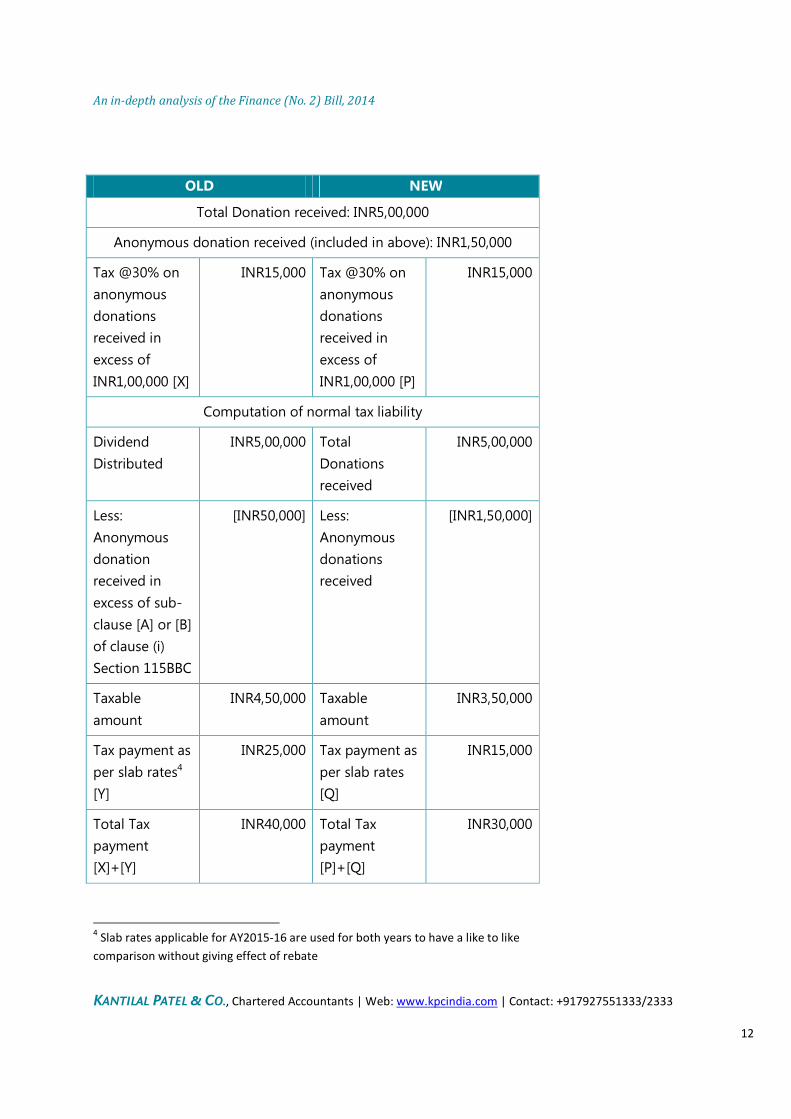

Section 115BBC: Anonymous Donations

It is proposed that the tax on the balance income shall be

charged at normal rates and such balance income shall be the

amount of total income as reduced by the aggregate amount

of Anonymous donation received in excess of the exempted

amount i.e. 5% of the total donation received or INR1,00,000

whichever is higher.

This amendment comes in effect

from October 1, 2014.

Effective from AY2015-16

Effective from AY2015-16

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

12

OLD NEW

Total Donation received: INR5,00,000

Anonymous donation received (included in above): INR1,50,000

Tax @30% on

anonymous

donations

received in

excess of

INR1,00,000 [X]

INR15,000 Tax @30% on

anonymous

donations

received in

excess of

INR1,00,000 [P]

INR15,000

Computation of normal tax liability

Dividend

Distributed

INR5,00,000 Total

Donations

received

INR5,00,000

Less:

Anonymous

donation

received in

excess of sub-

clause [A] or [B]

of clause (i)

Section 115BBC

[INR50,000] Less:

Anonymous

donations

received

[INR1,50,000]

Taxable

amount

INR4,50,000 Taxable

amount

INR3,50,000

Tax payment as

per slab rates4

[Y]

INR25,000 Tax payment as

per slab rates

[Q]

INR15,000

Total Tax

payment

[X]+[Y]

INR40,000 Total Tax

payment

[P]+[Q]

INR30,000

4 Slab rates applicable for AY2015-16 are used for both years to have a like to like

comparison without giving effect of rebate

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

13

Illustrations

Illustration 1:

A person has the following details:

Interest paid on Housing Loan for a self-occupied house: INR1,80,000

Advance money received from a party for failed negotiations over

transfer of a capital asset: INR2,00,000 [Cost of acquisition of the said

asset: INR10,00,000]

Income received on maturity of units of mutual fund other than equity

oriented funds:

Invested in February, 2013

Period of holding: 15 months

Cost of the units: INR 2,00,000

Maturity value: INR 2,50,000

The following expenses were also incurred:

Expenditure on CSR activities: INR1,00,000

Amount paid as professional fees to a management consultant:

INR2,00,000 but no TDS was deducted

Amount paid to a Non-resident: INR1,00,000.

TDS was deducted accordingly, but deposited with the revenue

only on 27th of July of the Assessment year.

Contribution to PPF fund: INR1,20,000

Contribution to LIC Premium: INR40,000

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

14

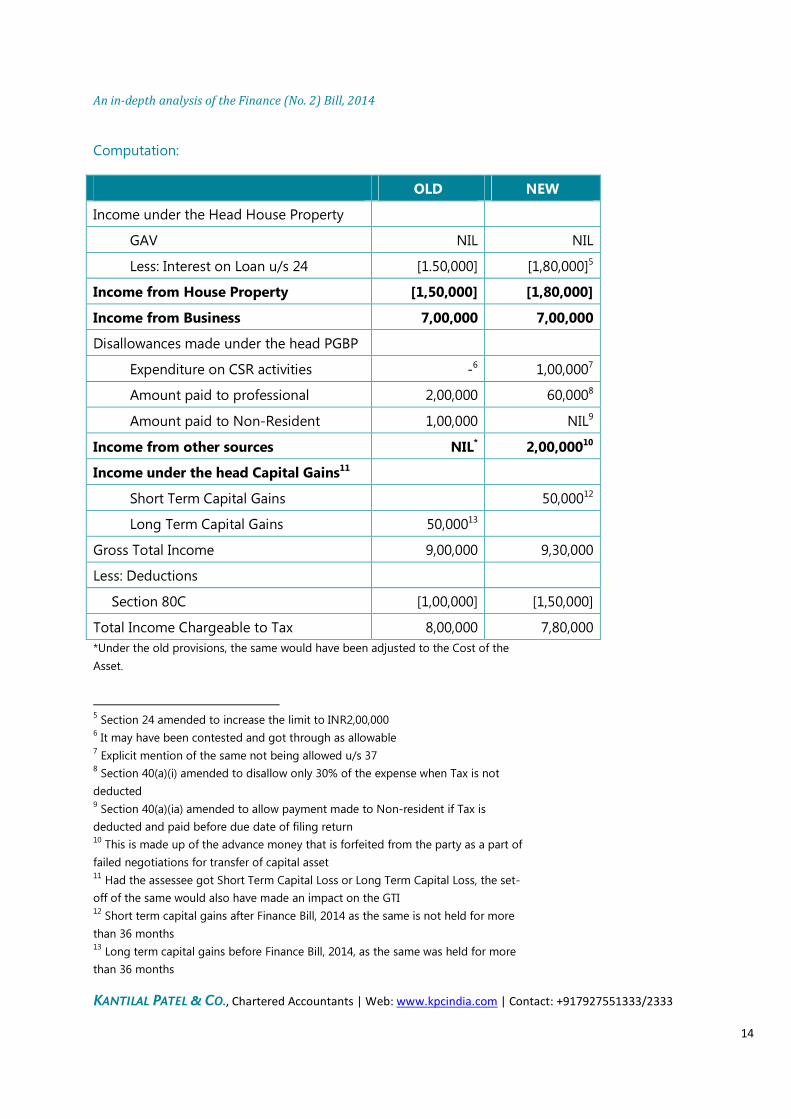

Computation:

OLD NEW

Income under the Head House Property

GAV NIL NIL

Less: Interest on Loan u/s 24 [1.50,000] [1,80,000]5

Income from House Property [1,50,000] [1,80,000]

Income from Business 7,00,000 7,00,000

Disallowances made under the head PGBP

Expenditure on CSR activities -6 1,00,0007

Amount paid to professional 2,00,000 60,0008

Amount paid to Non-Resident 1,00,000 NIL9

Income from other sources NIL* 2,00,00010

Income under the head Capital Gains11

Short Term Capital Gains 50,00012

Long Term Capital Gains 50,00013

Gross Total Income 9,00,000 9,30,000

Less: Deductions

Section 80C [1,00,000] [1,50,000]

Total Income Chargeable to Tax 8,00,000 7,80,000

*Under the old provisions, the same would have been adjusted to the Cost of the

Asset.

5 Section 24 amended to increase the limit to INR2,00,000

6 It may have been contested and got through as allowable

7 Explicit mention of the same not being allowed u/s 37

8 Section 40(a)(i) amended to disallow only 30% of the expense when Tax is not

deducted 9 Section 40(a)(ia) amended to allow payment made to Non-resident if Tax is

deducted and paid before due date of filing return 10 This is made up of the advance money that is forfeited from the party as a part of

failed negotiations for transfer of capital asset 11 Had the assessee got Short Term Capital Loss or Long Term Capital Loss, the set-

off of the same would also have made an impact on the GTI 12 Short term capital gains after Finance Bill, 2014 as the same is not held for more

than 36 months 13 Long term capital gains before Finance Bill, 2014, as the same was held for more

than 36 months

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

15

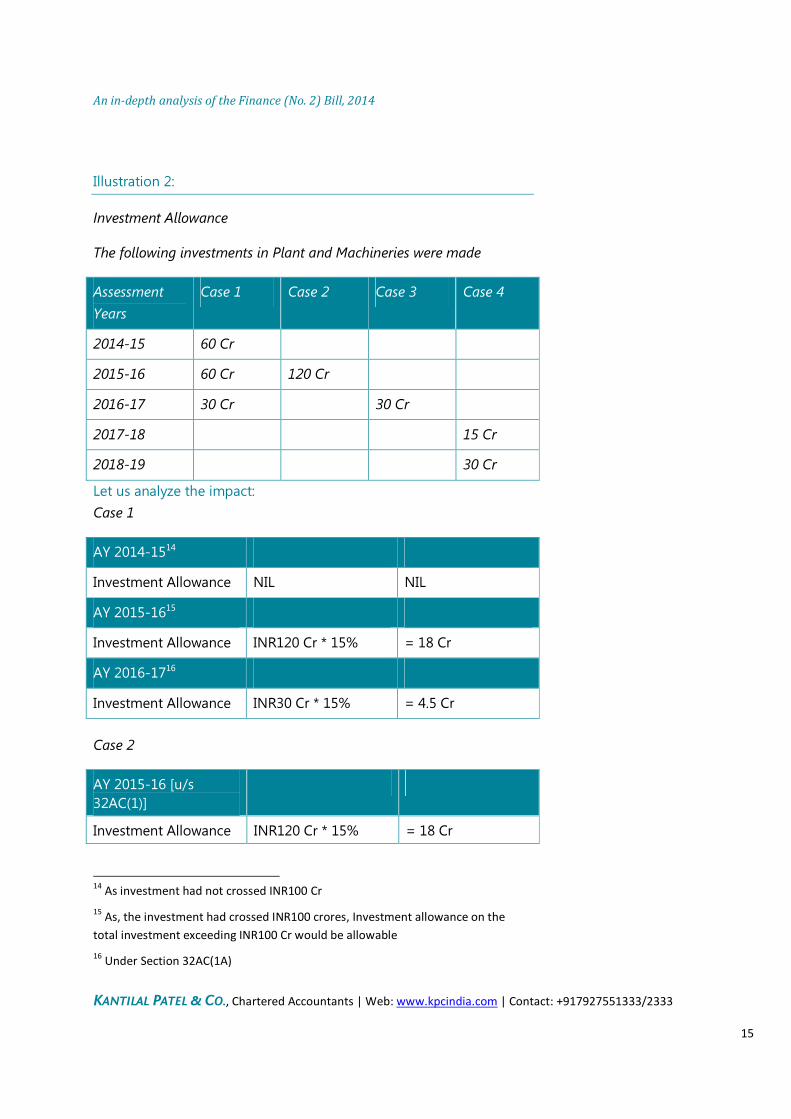

Illustration 2:

Investment Allowance

The following investments in Plant and Machineries were made

Assessment

Years

Case 1 Case 2 Case 3 Case 4

2014-15 60 Cr

2015-16 60 Cr 120 Cr

2016-17 30 Cr 30 Cr

2017-18 15 Cr

2018-19 30 Cr

Let us analyze the impact:

Case 1

AY 2014-1514

Investment Allowance NIL NIL

AY 2015-1615

Investment Allowance INR120 Cr * 15% = 18 Cr

AY 2016-1716

Investment Allowance INR30 Cr * 15% = 4.5 Cr

Case 2

AY 2015-16 [u/s

32AC(1)]

Investment Allowance INR120 Cr * 15% = 18 Cr

14

As investment had not crossed INR100 Cr

15 As, the investment had crossed INR100 crores, Investment allowance on the

total investment exceeding INR100 Cr would be allowable

16 Under Section 32AC(1A)

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

16

Case 3

AY 2016-17 [u/s

32AC(1A)]

Investment Allowance INR30 Cr * 15% = 4.5 Cr

Case 4

AY 2017-1817

Investment Allowance NIL NIL

AY 2018-1918

Investment Allowance NIL NIL

TAX TABLE

[As proposed for resident individuals by the Finance (no. 2) Bill, 2014]

ASSESSMENT YEAR 2015-16

Net Taxable Income Other Senior Citizens

(60-80 years)

Senior Citizens

(above 80 years)

INR* INR* INR*

2,60,000 - - -

2,70,000 - - -

2,80,000 1,030 - -

3,00,000 3,090 - -

3,20,000 5,150 - -

3,30,000 6,180 1,030 -

5,00,000 23,690 18,540 -

5,10,000 27,810 22,660 2,060

10,00,000 1,28,750 1,23,600 1,03,000

10,10,000 1,31,840 1,26,690 1,06,090

* Amount is inclusive of Education cess 2% & SHEC 1%

* Rebate u/s 87A is also considered.

17

As the minimum threshold of INR25 Cr is not achieved

18 As Section 32AC allowance is available only up to AY2017-18

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

17

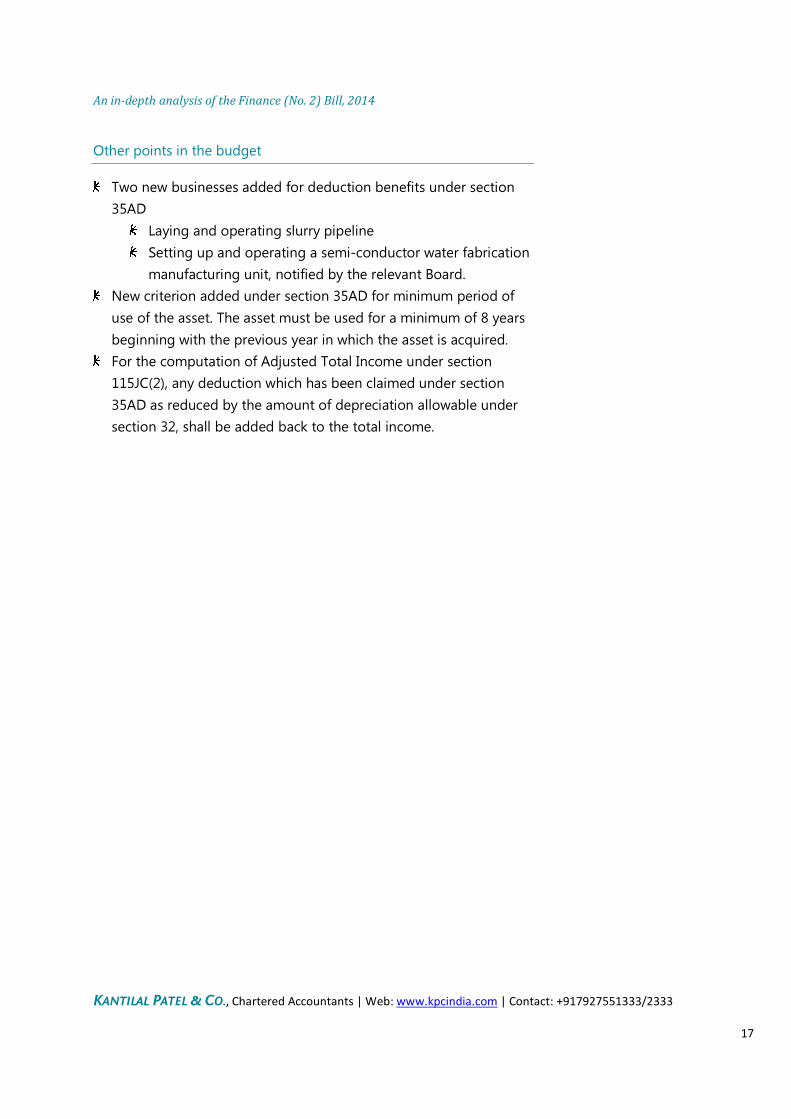

Other points in the budget

Two new businesses added for deduction benefits under section

35AD

Laying and operating slurry pipeline

Setting up and operating a semi-conductor water fabrication

manufacturing unit, notified by the relevant Board.

New criterion added under section 35AD for minimum period of

use of the asset. The asset must be used for a minimum of 8 years

beginning with the previous year in which the asset is acquired.

For the computation of Adjusted Total Income under section

115JC(2), any deduction which has been claimed under section

35AD as reduced by the amount of depreciation allowable under

section 32, shall be added back to the total income.

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

18

SERVICE TAX

The budget has laid large emphasis on collections from this source of

indirect taxation. With a major portion of our GDP coming out of this

sector, the importance cannot be denied. In order to achieve the

targets, the Finance Minister proposed the following changes in the

Service Tax Law:

The following exemptions have been withdrawn and are now brought

under the Service Tax net:

Service tax is levied currently on sale of space or time for

advertisement in broadcast media, namely radio or television.

This has been extended to cover such sales on other segment

like online and mobile advertising. However, print media

remains outside the net of service tax.

Radio taxis or Radio cabs (whether AC or Non AC) will be

taxable and abatement [60%] as given to rent-a-cab has been

allowed to radio taxis.

Service tax would be applicable on Clinical Research

Organization by way of technical testing or analysis of newly

developed drugs, vaccines and herbal remedies on human.

Service tax would be applicable on Transportation of

passengers in air-conditioned contract carriage. An abatement

of 60% is given making the effective rate at 4.994% (E.g.,

Private Bus transport facility provided by various transport

agencies)

The definition of auxiliary educational services has been done

away with. Instead, a list of services which are exempted are

specified which include, transportation of students, faculty and

staff, catering, security, cleaning, housekeeping and services

related to admission or conduct of examination. One major

impact by this amendment is that the services of renting of

immovable property received by the Educational Institution

would be now taxable.

There is no change in rate of service

tax, education cess & higher

education cess i.e. effectively; it will

remain same @ 12.36%

This amendment comes in effect

from a date which would be notified

This amendment comes in effect

from a date which would be notified

This amendment comes in effect

from July 11, 2014.

This amendment comes in effect

from July 11, 2014.

This amendment comes in effect

from July 11, 2014.

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

19

The following changes have been introduced in Reverse Charge

Mechanism

Service provided or agreed to be provided by a Director of a

body corporate to the said body corporate has been brought

under the Reverse Charge Mechanism. Service receiver, who is

a body corporate, will be the person liable to pay Service tax.

[Earlier, this provision covered only directors of companies]

Services provided by Recovery Agents to Banks, Financial

Institutions and NBFCs have also been brought under the

Reverse Charge Mechanism.

The following exemptions have been granted:

Life micro-insurance schemes for the poor, approved by IRDA,

where sum assured does not exceed INR50,000 to be

exempted from service tax.

Service provided by operators of common bio-medical waste

treatment facility to a clinical establishment to be exempted

from service tax.

Earlier, exemption in relation to providing accommodation

services was granted only to hotels, inns, guest houses and

commercial establishments which provided rooms for less

than INR1,000 per day. The word “commercial” has been

removed to extend the benefit to other establishments

providing accommodation facilities

Service by way of loading, unloading, packing, storage or

warehousing, transportation by vessel, rail or road (GTA) of

cotton, ginned or baled, is exempted.

Service by way of transportation of organic manure by vessel,

rail or road (GTA), is exempted.

Services provided by Employees’ State Insurance Corporation

(ESIC) during the period prior to 01-07-2012 would be

exempted from Service Tax.

This amendment comes in effect

from July 11, 2014.

This amendment comes in effect

from July 11, 2014.

This amendment comes in effect

from July 11, 2014.

This amendment comes in effect

from July 11, 2014.

This amendment comes in effect

from July 11, 2014.

This amendment comes in effect

from July 11, 2014.

This amendment comes in effect

from July 11, 2014.

This exemption has been granted

retrospectively since 01.07.2012.

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

20

Change in Point of Taxation Rules in case of Reverse Charge

Mechanism

The Point of Taxation in respect of Reverse Charge under the

first Proviso to Rule 7 of the POT Rules has been amended to

be the payment date or the first day that occurs immediately

after a period of three months from the date of invoice,

whichever is earlier.

This means that the persons responsible for paying Service

Tax under Reverse Charge Mechanism, would be required to

pay service tax at the end of three months from the date of

invoice received, irrespective of the fact whether the payment

has been made or not.

Change in Valuation of Works Contract: Service portion at 70% of

value

In Rule 2A of the Service Tax (Determination of Value) Rules,

2006, category ‘B’ and ‘C’ of Works Contract has been merged

into one single category, with percentage of service portion as

70%, for the chargeability of Service tax.

Change in Tax rate for Renting of a Motor Vehicle

Where the service provider does not take abatement in case

of renting of Motor vehicle, the portion of Service tax payable

by the service receiver has been modified to 50%.

Changes in the Service Tax Rules, 1994:

E-payment of Service tax has been made mandatory.

This is a major amendment which does away with the Challan

mode of payment for the assessee. All the assessees are

required to pay their service tax due electronically only.

This amendment comes in effect

from October 1, 2014.

This amendment comes in effect

from October 1, 2014.

This amendment comes in effect

from July 11, 2014.

This amendment comes in effect

from October 1, 2014.

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

21

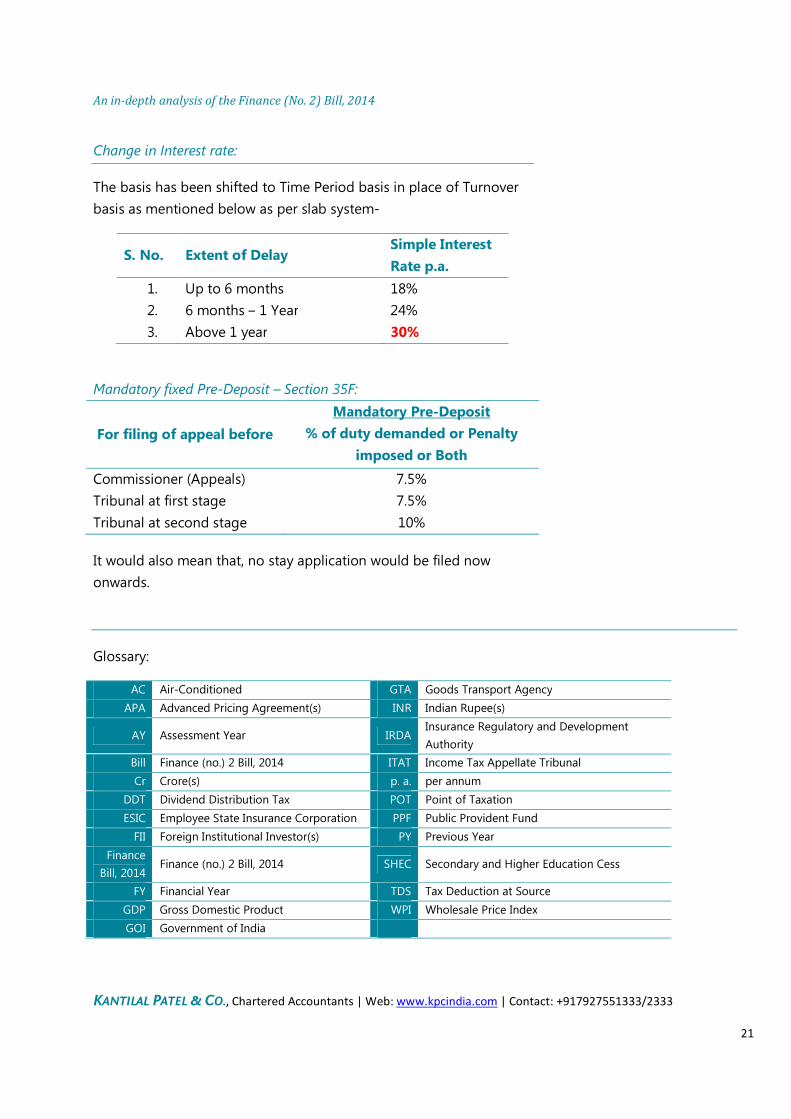

Change in Interest rate:

The basis has been shifted to Time Period basis in place of Turnover

basis as mentioned below as per slab system-

S. No. Extent of Delay Simple Interest

Rate p.a.

1. Up to 6 months 18%

2. 6 months – 1 Year 24%

3. Above 1 year 30%

Mandatory fixed Pre-Deposit – Section 35F:

For filing of appeal before

Mandatory Pre-Deposit

% of duty demanded or Penalty

imposed or Both

Commissioner (Appeals) 7.5%

Tribunal at first stage 7.5%

Tribunal at second stage 10%

It would also mean that, no stay application would be filed now

onwards.

Glossary:

AC Air-Conditioned GTA Goods Transport Agency

APA Advanced Pricing Agreement(s) INR Indian Rupee(s)

AY Assessment Year IRDA Insurance Regulatory and Development

Authority

Bill Finance (no.) 2 Bill, 2014 ITAT Income Tax Appellate Tribunal

Cr Crore(s) p. a. per annum

DDT Dividend Distribution Tax POT Point of Taxation

ESIC Employee State Insurance Corporation PPF Public Provident Fund

FII Foreign Institutional Investor(s) PY Previous Year

Finance

Bill, 2014 Finance (no.) 2 Bill, 2014 SHEC Secondary and Higher Education Cess

FY Financial Year TDS Tax Deduction at Source

GDP Gross Domestic Product WPI Wholesale Price Index

GOI Government of India

An in-depth analysis of the Finance (No. 2) Bill, 2014

KANTILAL PATEL & CO., Chartered Accountants | Web: www.kpcindia.com | Contact: +917927551333/2333

22

CONTACT

KANTILAL PATEL & CO.

202, ‘Paritosh’ Building, Usmanpura, (River Front),

Ahmedabad – 380013

Tel. No.: +91-79-27551333,+91-79-27552333 | Fax

No.: +91-79-27550538 |

Email: [email protected]

This publication contains information in summary form

and is therefore intended for general guidance only. It is

not intended to be substitute for in depth analysis or the

exercise of professional judgment. Kantilal Patel & Co. or

any other member of KPC cannot accept any

responsibility for loss caused to any person acting upon

or refraining from any action as a result of any content

in this publication. We advise that professional advice

must be obtained from appropriate advisor before doing

or refraining from doing any action.

![[XLS] Details/UnpaidDivided-FY... · Web viewJETHALAL HIRABEN PANNA DOSHI HANSABEN DILIP KANTILAL 360002 KETAN TANNA MAGANLAL SHAMJIBHAI BHAI VARSHA NANDLAL 360005 RATILAL RAWAL SHAMJI](https://img.pdfslide.us/doc/110x75/5aa8ec927f8b9a81188c1ec0/xls-detailsunpaiddivided-fyweb-viewjethalal-hiraben-panna-doshi-hansaben-dilip.jpg)