Embed Size (px)

Citation preview

Kamdar & Co.,CA 1

FINANCE BILL 2010 INDIRECT TAXES

Malad Goregaon CPE Study Circle

14-3-2010

CA H H Kamdar

Kamdar & Co.,CA 2

• GST• SERVICE TAX-New Services-Changes in existing services-Changes in exemptions-Changes in import/export Rules-Other Changes• CENTRAL EXCISE-Changes in Act-Changes in CE Rules-Changes in Cenvat Rules-Changes in Tariff

Kamdar & Co.,CA 3

GST• Expected from 1-4-2011• Issues to be sorted out

Compensation to states

State power to make rate changes

Constitutional amendments

Tax information net work• FM hopeful that GST will be made applicable

from 1-4-2011

Kamdar & Co.,CA 4

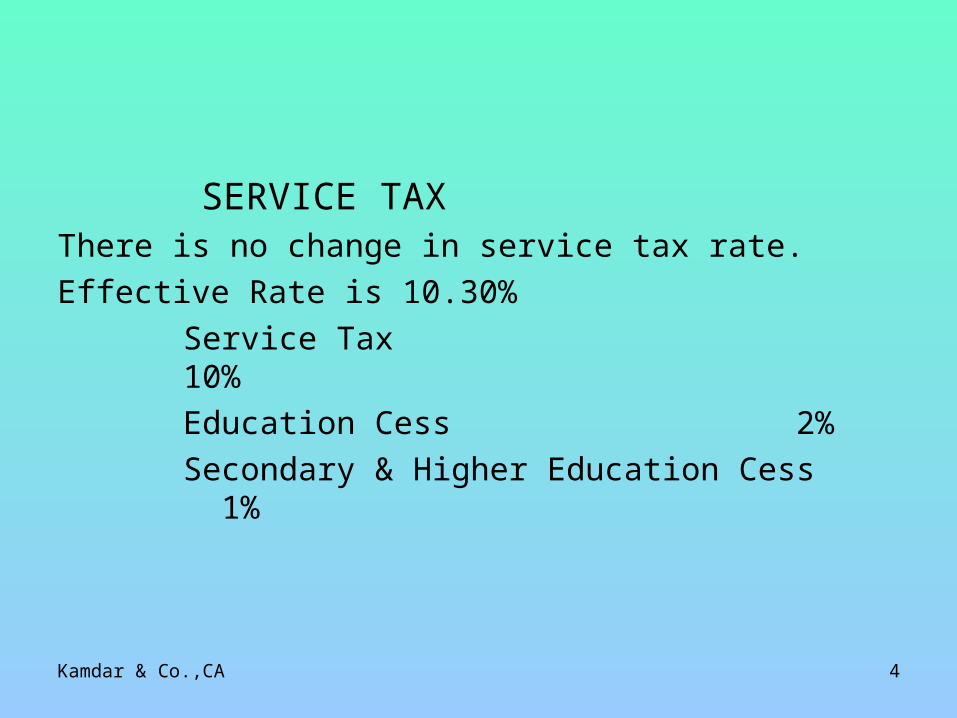

SERVICE TAXThere is no change in service tax rate.

Effective Rate is 10.30%

Service Tax 10%

Education Cess 2%

Secondary & Higher Education Cess 1%

Kamdar & Co.,CA 5

• NEW SERVICES – 8 New Services are brought under service tax net (effective from the date to be notified).

• Clauses ZZZZ N to clauses ZZZZ U –

Eight new clauses are added to Section 65 –sub section 105 of the Finance Act,1994 after clause ZZZZM- total services increased from 109 to 117.

Kamdar & Co.,CA 6

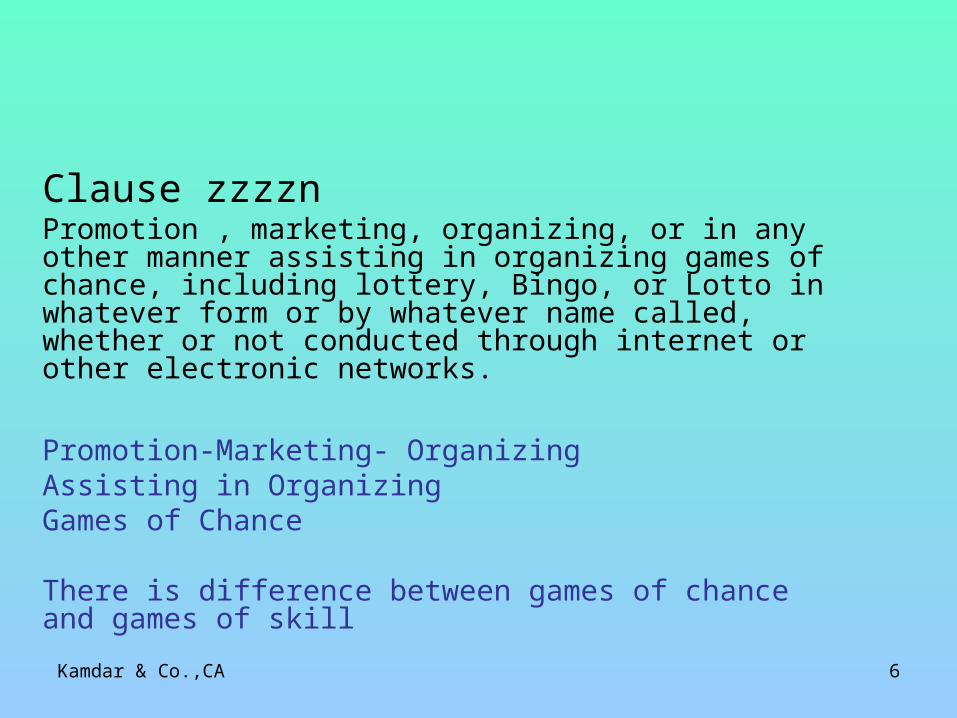

Clause zzzznPromotion , marketing, organizing, or in any other manner assisting in organizing games of chance, including lottery, Bingo, or Lotto in whatever form or by whatever name called, whether or not conducted through internet or other electronic networks.

Promotion-Marketing- OrganizingAssisting in OrganizingGames of Chance

There is difference between games of chance and games of skill

Kamdar & Co.,CA 7

Clause- zzzo• Service provided by any hospital, nursing home, or

multi specialty clinic,--• to an employee of any business entity, in relation to

health check up, or preventive care, where the payment of such check up or preventive care is made by such business entity directly to such hospital, nursing home or multi specialty clinic; or

• to a person covered by health insurance scheme, for any health check up or treatment, where the payment for such health check up or treatment is made by the insurance company directly to such hospital, nursing home or multi specialty clinic.

Kamdar & Co.,CA 8

Clause- zzzo (contd….)

• Service by individual doctors not covered• Services where payment is made by individuals not

covered• Under technical testing and analysis service, taxable

service does not include any testing or analysis service provided in relation to human beings or animals. This exclusion is partly diluted by introduction of this service.

• Persons other than employees not covered- health check up prior to employment / for directors who are not employees. Reimbursement to employee not covered.

• Only cashless insurance is covered.

Kamdar & Co.,CA 9

Clause ZZZZP• Services in relation to storing, keeping, or maintaining of

medical records of employees of business entity.• Many companies, particularly multinationals, air –lines,

oil exploration companies etc. keep medical records of their employees. The work is normally outsourced to an organisation that specializes in this type of work so that authenticated information is recorded.

• Services provided by Medical Transcription Centers in respect of transcribing medical history, treatment, medical observation etc are already taxable under Business Auxiliary services. Is there any duplication?

Kamdar & Co.,CA 10

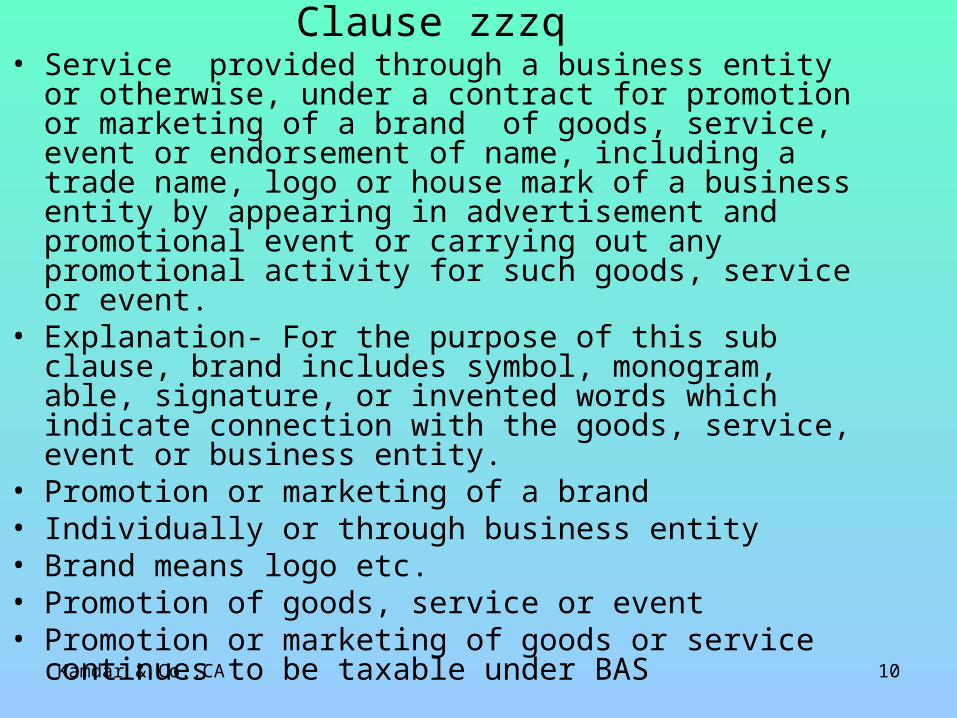

Clause zzzq• Service provided through a business entity or otherwise,

under a contract for promotion or marketing of a brand of goods, service, event or endorsement of name, including a trade name, logo or house mark of a business entity by appearing in advertisement and promotional event or carrying out any promotional activity for such goods, service or event.

• Explanation- For the purpose of this sub clause, brand includes symbol, monogram, able, signature, or invented words which indicate connection with the goods, service, event or business entity.

• Promotion or marketing of a brand• Individually or through business entity• Brand means logo etc.• Promotion of goods, service or event• Promotion or marketing of goods or service continues to

be taxable under BAS

Kamdar & Co.,CA 11

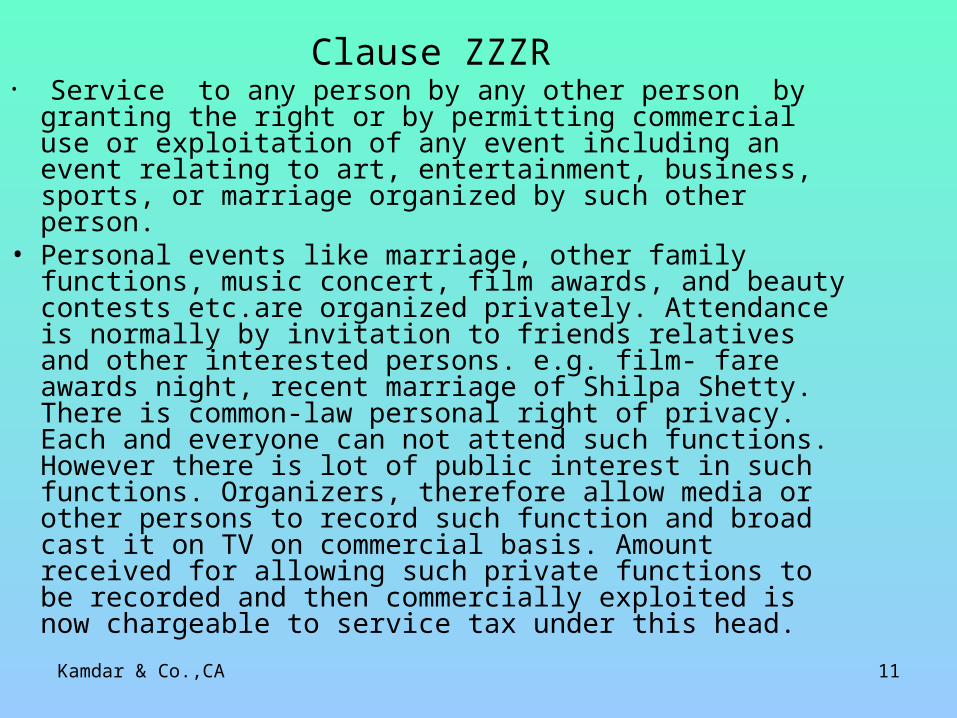

Clause ZZZR• Service to any person by any other person by granting

the right or by permitting commercial use or exploitation of any event including an event relating to art, entertainment, business, sports, or marriage organized by such other person.

• Personal events like marriage, other family functions, music concert, film awards, and beauty contests etc.are organized privately. Attendance is normally by invitation to friends relatives and other interested persons. e.g. film- fare awards night, recent marriage of Shilpa Shetty. There is common-law personal right of privacy. Each and everyone can not attend such functions. However there is lot of public interest in such functions. Organizers, therefore allow media or other persons to record such function and broad cast it on TV on commercial basis. Amount received for allowing such private functions to be recorded and then commercially exploited is now chargeable to service tax under this head.

Kamdar & Co.,CA 12

Clauses – ZZZZS• Services provided by an electricity exchange, by

whatever name called, approved by the Central Electricity Regulatory Commission, constituted under section 76 of the Electricity Act, 2003, in relation to trading processing clearing or the settlement of spot contracts, term ahead contracts, seasonal contracts, derivatives or any other electricity related contracts

• Like stock exchange, commodity exchange services of electricity exchange are made taxable.

Kamdar & Co.,CA 13

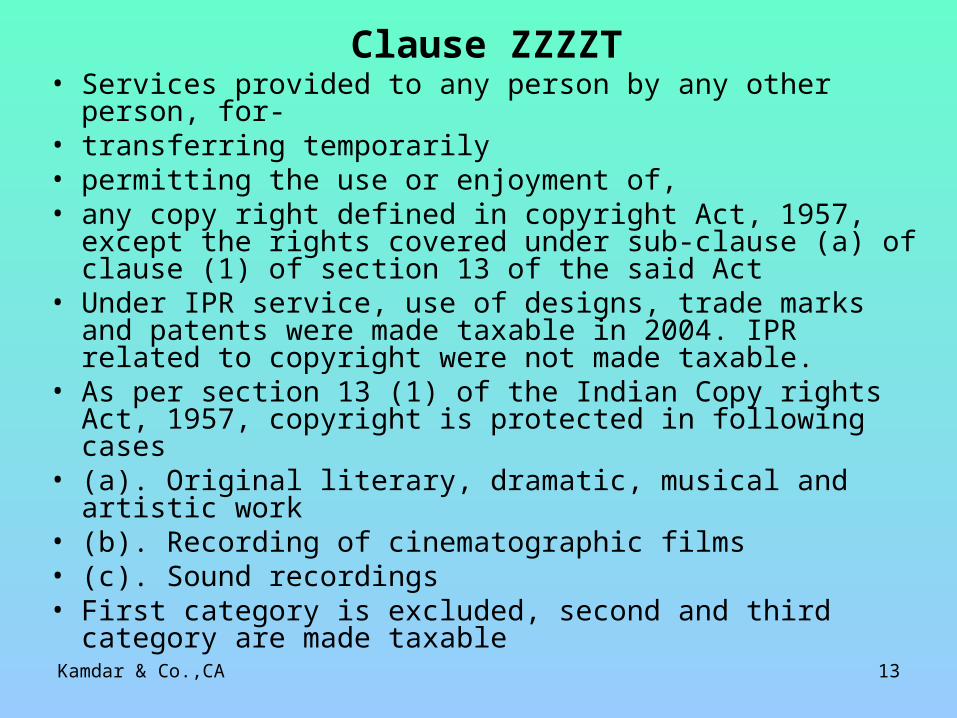

Clause ZZZZT• Services provided to any person by any other person, for-• transferring temporarily• permitting the use or enjoyment of,• any copy right defined in copyright Act, 1957, except the

rights covered under sub-clause (a) of clause (1) of section 13 of the said Act

• Under IPR service, use of designs, trade marks and patents were made taxable in 2004. IPR related to copyright were not made taxable.

• As per section 13 (1) of the Indian Copy rights Act, 1957, copyright is protected in following cases

• (a). Original literary, dramatic, musical and artistic work• (b). Recording of cinematographic films• (c). Sound recordings• First category is excluded, second and third category are

made taxable

Kamdar & Co.,CA 14

Clause ZZZZU• Service provided to a buyer, by a builder of a residential complex, or

a commercial complex, or any other person authorised by such builder, for providing preferential location or development of such complex but does not include services covered under sub-clauses (zzg), (zzq), (zzzh) and in relation to parking place

• Construction, finishing, repairs, alterations, renovation or restoration of complex is chargeable to service tax.

• Amount charged for prime/preferential location, sea facing, and park facing, and corner flat, floor preference, lucky number flats chargeable.

• Internal/ external development charges for developing parks, common lighting, fire fighting installations, power back up, club house, swimming pool etc are also taxable.

• Exclusions-• Maintenance and repair charges.• Commercial Construction service• Construction of complex• Parking place • This service is classified as separate service. No abatement is

allowed

Kamdar & Co.,CA 15

AMENDMENTS

TO

EXISTING

SERVICES

Kamdar & Co.,CA 16

PORT SERVICE• Section 65,- Clause 82• Existing-• “port service” means any service rendered by a port or other port or any

person authorised by such port or other port , in any manner, in relation to vessel or goods.

• Changed to- “port service” means any service rendered within a port or other port ,in any manner.

• Clause- 105 (zn)• Existing- • Taxable service means any service provided to any person, by a port or any

person authorised by port ,in relation to port services in any manner. Changes to- Taxable service means any service provided or to be provided to any person, in relation to port services in a port, in any manner

• Conditions removed-• service to be provided by port or any person authorised by port• in relation to vessel or goods• condition added-• service to be provided within port - Any service provided by any body within

the port area is taxable under port service. Service need not be taxable service.

• Classification provisions of section 65A not to apply to port service.• Cargo service/ transport service within port taxable only under port service.

Kamdar & Co.,CA 17

COMMERCIAL TRAINING & COACHING SERVICE

• Clause zzc• Taxable service provided to any person , by a commercial training

or coaching centre in relation to commercial training and coaching• An Explanation is added with effect from 1st July 2003• Explanation- For removal of doubts, it is hereby declared that the

expression ‘commercial training or coaching centre’ occurring in this sub clause and in clauses (26), (27), and (90a), shall include any centre or institute ,by whatever name called, where training or coaching is imparted for consideration, whether or not such centre or institute is registered as trust or society or similar other organisation under any law for the time being in force and carrying its activity with or without profit motive and the expression “commercial training or coaching ‘ shall construed accordingly.

• Clarificatory amendment for removal of doubts w.e.f.1-7-2003• Commercial training or coaching centre include any centre or

institute where such training or coaching is imparted for consideration

Kamdar & Co.,CA 18

COMMERCIAL TRAINING & COACHING SERVICE

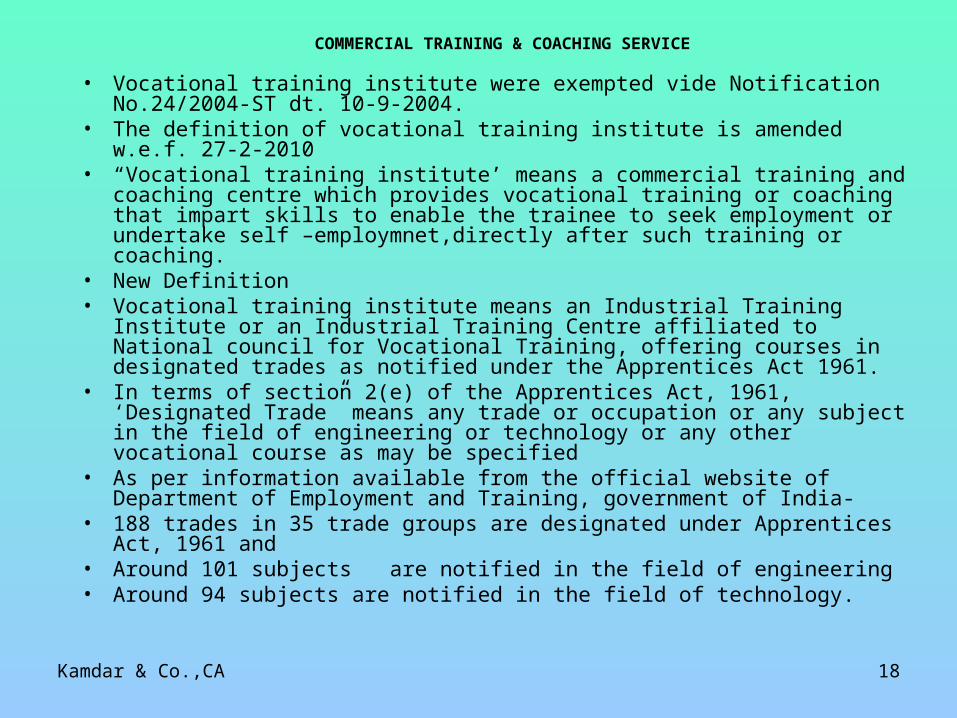

• Vocational training institute were exempted vide Notification No.24/2004-ST dt. 10-9-2004.

• The definition of vocational training institute is amended w.e.f. 27-2-2010• “Vocational training institute’ means a commercial training and coaching

centre which provides vocational training or coaching that impart skills to enable the trainee to seek employment or undertake self –employmnet,directly after such training or coaching.

• New Definition• Vocational training institute means an Industrial Training Institute or an

Industrial Training Centre affiliated to National council for Vocational Training, offering courses in designated trades as notified under the Apprentices Act 1961.

• In terms of section 2(e) of the Apprentices Act, 1961, ‘Designated Trade” means any trade or occupation or any subject in the field of engineering or technology or any other vocational course as may be specified

• As per information available from the official website of Department of Employment and Training, government of India-

• 188 trades in 35 trade groups are designated under Apprentices Act, 1961 and

• Around 101 subjects are notified in the field of engineering • Around 94 subjects are notified in the field of technology.

Kamdar & Co.,CA 19

COMMERCIAL OR INDUSTRIAL CONSTRUCTION SERVICES• Clause- zzq• Existing clause-• Services provided to any person by any other person in relation to commercial or industrial

construction service.• Changes made-• (i)- The word service is omitted.• (ii). The following explanation is inserted-• Explanation- For the purpose of this sub-clause, the construction of a new building which is

intended for sale, wholly or partly, by a builder or any other person authorised by the builder before, during or after construction ( except in cases for which no sum is received from or on behalf of prospective buyer by the builder or the person authorised by the builder before grant of completion certificate by the authority competent to issue such certificate under any law for the time being in force) shall be deemed to be service provided by the builder to the buyer.

• Deeming provision• Negative exception• Consideration paid for completed ready possession construction sold outright – no service

tax.• Agreement to sale constructed property - property under construction- No transfer-

consideration payment in stages- sale deed on completion.• Sale of undivided share in land- construction agreement- possession and transfer on

completion.• Explanation provides that construction services by a builder to a prospective buyer will be

taxable if consideration is received before completion certificate is obtained.• Even if apart consideration is received before completion, service tax will be payable on total

consideration, even if it is paid after completion. • Similar changes in construction of residential complex service.

Kamdar & Co.,CA 20

SPONSORSHIP SERVICE• Clause ZZZN• Existing clause-• Services provided to any body corporate or firm, by any

person receiving sponsorship, in relation to such sponsorship, in any manner, but does not include services in relation to sponsorship of sports events.

• Changed to-• Services provided to any person, by other person

receiving sponsorship, in relation to such sponsorship, in any manner.

• Services provided to only body corporate and firm were taxable. Now services provided to any person is taxable. Individual, trust, societies etc are also included.

• Exclusion to sports event is deleted. Sponsorship of sports events is also taxable.

• Service tax payment on reverse charge basis continues.

Kamdar & Co.,CA 21

TRANSPORT OF PASSENGERS BY AIR SERVICE• Clause ZZZO• Existing clause• Services provided to any passenger, by an air craft

operator, in relation to scheduled or non scheduled air transport of such passenger embarking in India for international journey, in any class other than economy class.

• Changed to-• Services provided to any passenger, by an air craft

operator, in relation to scheduled or non scheduled air transport of such passenger embarking in India for domestic journey or international journey.

• Domestic journey is also chargeable to tax• Journey in all classes including in economy class is

chargeable to tax.• Suitable exemptions/abatements would be prescribed.

Kamdar & Co.,CA 22

AUCTIONER’S SERVICE• Clause ZZZR• ‘Auction by government, is excluded from the taxable

service.• This phrase has created confusion• Goods belonging to or vested in State/Central

Government is auctioned by private organizations. • Government bodies like Tobacco Board/Tea Board/

Rubber Board etc auction goods belonging to private individuals/organizations.

• T0 clarify an Explanation is added to clause ZZZR• Explanation – For removal of doubts, it is hereby

declared that for the purposes of this sub-clause. “Auction by the Government” means the government property being auctioned by any person acting as auctioneer.

• The exclusion is for the Government property and not for private property.

Kamdar & Co.,CA 23

RENTING OF IMMOVABLE PROPERTY SERVICE• Clause ZZZZ• Existing clause-• Service provided to any person, by any other person, in relation to

renting of immovable property for use in the course of furtherance of business or commerce.

• Changed to-• Service provided to any person, by any other person, by renting of

immovable property, or any other service in relation to such renting, for use in the course of or, for furtherance of , business or commerce.

• Service in relation to renting ------ replaced by renting of• Any service in related to such renting is added.• Renting itself is now considered as service.• With retrospective effect from 1-6-2007.• Home solution Retail India Ltd vs Union of India [2009 14 STR 433]

wherein it was held that renting itself is not a taxable service.

Kamdar & Co.,CA 24

RENTING OF VACANT LAND• Clause ZZZZ Explanation -1• For the purpose of this sub clause, “immovable property’’ includes ---• (i). building and part of building and land appurtenant thereto,• (ii) Land incidental to the use of such building or part of the building. • (iii). the common or shared areas and facilities thereto,• (iv). in case building is located in a complex, or an industrial estate, all

common areas and facilities relating thereto, within such complex or estate.• Item (v) is added-• (v). vacant land, given on lease or license for construction of building

or temporary structure at a latter stage to be used for furtherance of business or commerce.

• Lease of vacant land-• Building or temporary structure to be constructed• For furtherance of business or commerce.• MIDC- 99 year’s lease of land for factory building• Land lease for building hotels, resorts, etc• BPT land for offices/godowns• At the time of leasing if intention is to allow the land for building structure for

commercial use, the tax will be levied.

Kamdar & Co.,CA 25

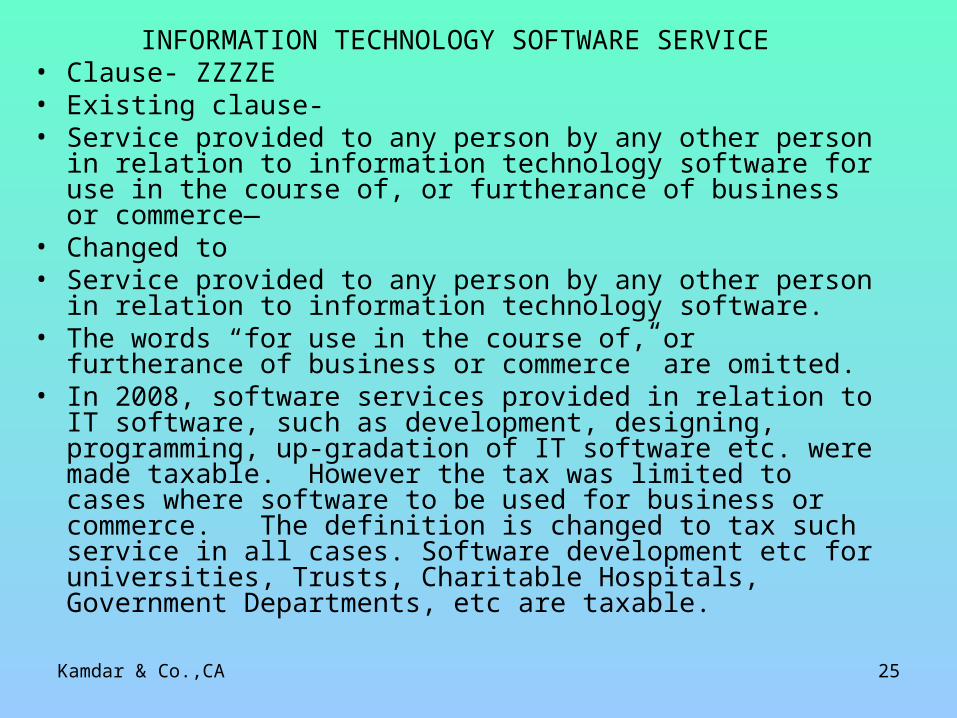

INFORMATION TECHNOLOGY SOFTWARE SERVICE• Clause- ZZZZE• Existing clause-• Service provided to any person by any other person in relation

to information technology software for use in the course of, or furtherance of business or commerce—

• Changed to • Service provided to any person by any other person in relation

to information technology software. • The words “for use in the course of, or furtherance of

business or commerce” are omitted.• In 2008, software services provided in relation to IT software,

such as development, designing, programming, up-gradation of IT software etc. were made taxable. However the tax was limited to cases where software to be used for business or commerce. The definition is changed to tax such service in all cases. Software development etc for universities, Trusts, Charitable Hospitals, Government Departments, etc are taxable.

Kamdar & Co.,CA 26

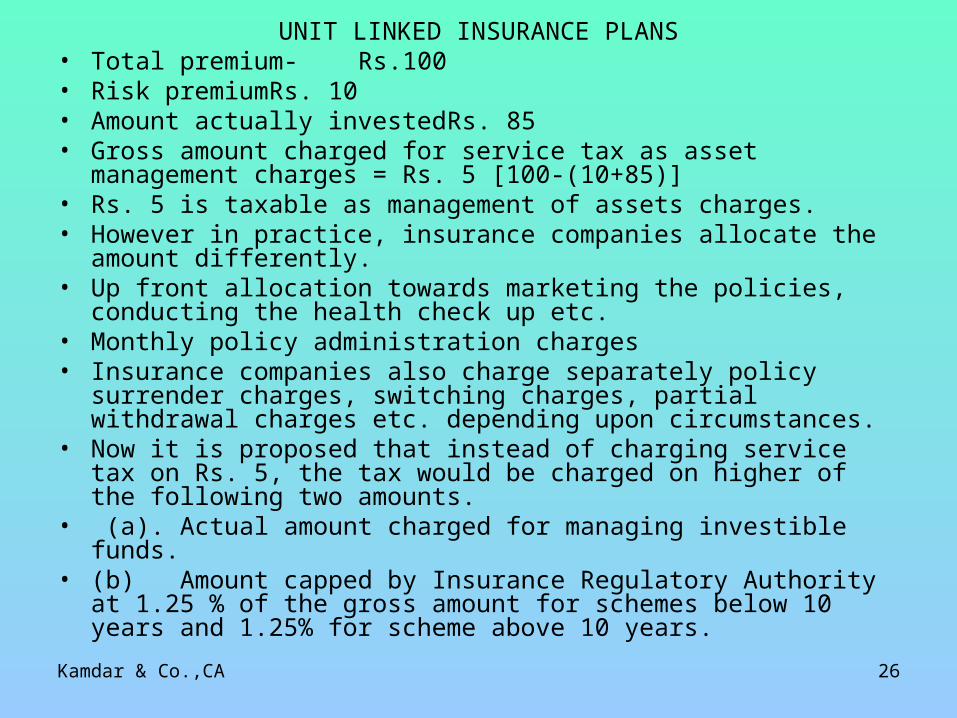

UNIT LINKED INSURANCE PLANS• Total premium- Rs.100• Risk premium Rs. 10• Amount actually invested Rs. 85• Gross amount charged for service tax as asset management

charges = Rs. 5 [100-(10+85)]• Rs. 5 is taxable as management of assets charges. • However in practice, insurance companies allocate the amount

differently. • Up front allocation towards marketing the policies, conducting the

health check up etc.• Monthly policy administration charges• Insurance companies also charge separately policy surrender

charges, switching charges, partial withdrawal charges etc. depending upon circumstances.

• Now it is proposed that instead of charging service tax on Rs. 5, the tax would be charged on higher of the following two amounts.

• (a). Actual amount charged for managing investible funds.• (b) Amount capped by Insurance Regulatory Authority at 1.25

% of the gross amount for schemes below 10 years and 1.25% for scheme above 10 years.

Kamdar & Co.,CA 27

CHANGES IN EXEMPTIONS• Software use [Notification N0.02/2010-ST dt 27-2-2010]• Providing right to use software is taxable under item (v) of clause zzzze.• Packaged or canned software, intended for single use and packed

accordingly exempted from• whole of service tax subject to following conditions.• (i). Document providing right to use software is packed with software• (ii). The manufacturer/duplicator has paid excise duty thereon• (iii). Benefit under notification No.17/2010-CE-dt 27 -2-2010 is not

availed.• Central excise duty is payable on manufacturer of packaged or canned

software on total• sale price consisting of-• Value of media on which software is loaded.• Value for right to use/commercially exploit/duplicate the software

• Notification 17 Exempts the manufacturer from the payment of duty on value for right to use the software.

• Exemption under notification 2/2010-ST is available only if benefit of Notification 17-CE is not availed. In other words, manufacturer should have paid the excise duty on total value of the single use software.

Kamdar & Co.,CA 28

• Goods Transport Agency Service [Notification 04/2010-ST.dt.27-2-2010]

• In respect of GTA service, under Notification No. 33/2004-ST dt. 3-12-2004, transport of fruits, vegetables, eggs and milk is exempted. Now food grains and pulses are added to list.

• No service tax is payable on transport of food grains and pulses.

Kamdar & Co.,CA 29

• TRANSPORT OF GOODS BY RAIL [Notification No. 7/2010-ST dt. 27-7-2010]

• Service tax on transport of goods by any person other than government railway, in containers was imposed from 1-5-2006

• From 1-9-2009, service tax was imposed on service provided by government railway also.

• This was opposed by railway and therefore an exemption was provided.

• Notification No 33/2009-ST-dt. 1-9-2009 exempted the service tax on taxable services provided in relation to transport of goods by rail other than transport of goods by any person other than government railway.

• This exemption Notification is rescinded. Transport of goods by railway is taxable w.e.f. .

• 1-4-2010.• Exemptions for specific goods and abatement @70 %

are notified.

Kamdar & Co.,CA 30

• TECHNICAL TESTING AND ANAYLYSIS SERVICE/TECHNICAL INSPECTION

• AND CERTIFICATION SERVICE• [Notification 10/2010-ST-dt.27-2-2010]• Taxable service provided by-• (i). Any Central or State Seed Testing

Laboratory; and• (ii) Central or State Seed Certification Agency • Notified under the Seeds Act, 1966,• Exempted from payment of service tax on,

Technical testing and analysis andTechnical inspection and certification of

seeds.

Kamdar & Co.,CA 31

TRANSMISSION OF ELECTICITY SERVICE• [Notification No. 11/2010-ST-dt.27-2-2010]• There is no specific head like transmission of

electricity service. In case electricity• company, say, Reliance Power, allows the use

of its cable network for transmission of• electricity to another company, say Tata power,

the service is taxable as infrastructural• support service taxable under business support

service. This service is now exempted• from payment of service tax.

Kamdar & Co.,CA 32

ERECTION, COMMISSIONING, AND INSTALLATION SERVICE

• [Notification 12/2010-ST-dt.27-2-2010]• Erection, installation and commissioning

services in respect of• mechanized food grain handling systems• setting up or substantial expansion of cold

storage. • initial setting up or substantial expansion of

units for processing of agriculture, apiary, horticulture,dairy,poultry,aquatic and marine products and meat

• The exemption is given in order to help food processing industry.

Kamdar & Co.,CA 33

ON LINE INFORMATION AND DATABASE ACCESS AND RETRIVAL SERVICES/BUSINESS AUXILIARY

SERVICES

• [Notification 13/2010-ST-dt. 27-2-2010]• Service tax payable under these two services given to an

Indian News Agency subject to conditions• a). Such news agency is set up in India solely for

collection and distribution of news which are specified under clause (22B) of Section 10 of the Income Tax Act, 1961;and

• (b). Such news agency applies income for collection and distribution of news and does not distribute in any manner to its members.

• Agencies like PTI etc are exempted.

Kamdar & Co.,CA 34

EXPORT OF SERVICE RULES 2005• [Notification no. 06/2010-ST dt. 27-2-2010]• Rule 3(1) sub rule (i) and (ii) are amended.• a). Mandap Keeper’s Service is shifted from performance based category to

situs based category. (location of immovable property)• b). Chartered Accountant, Cost Accountant and company Secretary

Services are shifted from performance based category to service recipient based category.

• CA need not go out of India for claiming Export of service. If recipient is located outside India CA service will be considered as export of service. No service tax to foreign clients.

• In rule 3(2) vide clause (a), the following condition is required to be complied with in order to consider a service as Export Service.

• such service is provided from India and used outside India• This condition is now. deleted.

• There was a lot of confusion about this condition of use outside India. e.g. if service is provided by an Indian Agent to a foreign supplier of goods in India. the question was whether this service is used in India or outside India.

• On 24-2-2009, CBEC clarified vide circular 111/2209 that if benefits of services accrued outside India, it is an export of service.

• In the case of Microsoft corporation Delhi Bench of CESTAT refused stay of pre-deposit of duty demand.

• Since condition itself is now deleted, this will bring clarity.

Kamdar & Co.,CA 35

EXTENSION OF SERVICE TAX

• Under Notification No.1/2002-ST dt. 1-3-2002, Chapter V of the Finance Act, was

• extended to installations, structures, and vessels in the continental shelf of India and the exclusive economic zones.

• This notification is now superseded and new Notification No.14/2010-ST dt.27-2-1010 is issued .

• Chapter V of the Finance Act, i.e. service tax provisions are now applicable to any service provided for all activities pertaining to construction of installments, structures and vessels for the purposes of prospecting or extraction or production of mineral oil and natural gas and supply thereof. In the whole of continental shelf and economic zone of India.

• Similarly, service tax provisions are also made applicable to any service provided by or to such installations, structures, and vessels and for supply of any goods connected with the said activity.

• Corresponding provisions are made Export /Import Rules by amending Explanation to include such installation as part of India. {Notification 6/2010 ST and Notification 16/2010ST dt.27-2-2010.

Kamdar & Co.,CA 36

CHANGE IN VALUATION RULES

• [Notification 15/2010-ST dt. 27-2-2010]• In Rule 6(2) of Service Tax (Determination of

Value) Rules, lists items which are not to be included in valuation of service provided , like initial telephone deposit, air fare in air ticket, interest on loans etc. One more item is added to this list-

• The taxes levied by any government on any passenger traveling by air, if shown separately on the ticket or the invoice for such ticket, issued to the passenger.

Kamdar & Co.,CA 37

AMENDMENTS TO FINANCE ACT 1994• The Finance Act, 1994, is being amended to,• a). insert an Explanation in sub section (3) of

Section 73 to clarify that no penalty shall be imposed where service tax along with interest has been paid before issue of show cause notice by the department,

• This would be effective from the enactment of the Finance Bill 2010

• b). provide definition of the term ‘business entity’ so as to include association of persons, body of individual, company or firm but to excluded an individual

• This would be effective from the date to be notified.

Kamdar & Co.,CA 38

CHANGES IN CENVAT CREDIT RULES-2004• 1. In case computers on which Cenvat credit is

availed, is removed after use, reversal at the rate of 10/8/5/and 1 percent per quarter for first five years, instead of 2.5 percent per quarter which applicable to capital goods.

• 2. An eligible SSI unit can avail 100 % Cenvat Credit in the year in which capital goods are received instead of 50% in the year of receipt and balance 50 % in subsequent year.

• 3. Cenvat credit wrongly taken or utilised, penalty is provided in addition to interest. {Rule-15}

• 4. Retrospective amendment in Rule 6 – incase of dispute regarding credit of inputs used for

production of excisable goods and non excisable goods- proportionate credit relating to use in exempted goods to be reversed.

Kamdar & Co.,CA 39

CHANGES IN CENTRAL EXCISE ACT /RULES• Explanation –Section 11 (2B)- penalty will not

be levied if excise duty and interest thereon is paid before issue of Show Cause Notice-

• Section 37- authority to make rules for withdrawals of monthly payment facilities or imposition of penalty, including restriction for utilization of Cenvat credit. - for evasion of duty.

• An eligible SSI unit can pay duty on quarterly basis. Returns also to be filed quarterly before 10th of the first month of next quarter.

Kamdar & Co.,CA 40

CHANGES IN CENTRAL EXCISE TARIFF• Standard rate of excise duty for non petroleum

goods increased from 8% to 10%. No change in Education Cess /Secondary and Higher Education Cess.

• The rate of duty on Motor sprit (petrol), and HSD (diesel) increased by Rs. 1 per litre.

• Cutting, sawing or polishing of stones to make tiles /slabs will amount to manufacture.

• Drawing of pipes will be process of manufacture• See BCA website [bcasonline.org] for changes

in the rate structure for different products.

Kamdar & Co.,CA 41

OTHER CHANGES

• Eligible SSI manufactures- plastic bottles/containers bearing brand name – eligible for SSI benefits.

• Requirement of pre-authentication of Invoices done away with.

• Clean Energy Cess imposed on production of coal, lignite, and peat.

Kamdar & Co.,CA 42

THANKS

MALAD-GOREGAON CPE STUDY CIRCLE

CA SUNIL SHAH

AND

ALL THE PARTICIPANTS