Embed Size (px)

Citation preview

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

2-1

^:

28

MILBERG WEISS BERSHAD ORIGINALHYNES & LERACH LLP

WILLIAM S. LERACH (68581)PATRICK J. COUGHLIN (111070)HENRY ROSEN (156963)KRISTEN McCULLOCH (177558)600 West Broadway, Suite 1800San Diego, CA 92101Telephone: 619/231-1058

EUGENE MIKOLAJCZYK (106929)1165 N. BienvenedaPacific Palisades, CA 90272Telephone: 310/454-8435

WECHSLER HARWOOD HALEBIAN& FEFFER LLP

ROBERT I. HARWOODRICHARD B. BRUALDI805 Third Avenue7th FloorNew York, NY 10022Telephone: 212/935-7400

Attorneys for Plaintiffs

F7 ri

JUN 2 3 ..a7 .

Cl ERK, U . S. Gigi" CTCOURTCENTRAL DISTRf CF CALIFORNIA

[Additional counsel appear on signature page.]

UNITED STATES DISTRICT COURT

CENTRAL DISTRICT OF CALIFORNIA

SOUTHERN DIVISION

PETER KALMUS , et al., On Behalf ofT em-seIve-s, and All Others SimilarlySituated,` ,

Plaintiffs,o

Y L+ ':IWB ti; WERTZ , et al.,N Du

Defendants.

No. SACV-96-1250-GLT(Eex)

CLASS ACTION

FIRST AMENDED CLASS ACTIONAND INDIVIDUAL COMPLAINTFOR VIOLATIONS OF THESECURITIES EXCHANGE ACT OF1934

Plaintiffs Demand aTrial By Jury

[Caption continued on following page.]

INrraED ON DiS_^^

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

RICHARD AVON, KEN AVON, JEANCHARLENT, DUANE D'AGOSTINO, STEPHEN

MADDEN, ROBERT MASESSA, LOUIS ANDROSE ARGENZIANO, ROBERT AND MICHELEBACON, FRED BERGMAN, LAURA J. BOHN,

DR. JUAN C. CARIONI, P.C., JUAN C.CARIONI, CHARLES COSTELLO, JOSEPHDEROSA, HENRY AND MARISOLDIGIROLAMO, WILBUR ECKERSON,CARMINE GESUALDI, CARMINE ANDKATHLEEN GESUALDI, J. DAVIDJOHNSON, DONALD AND KAREN JONES,BARBARA LOONEY, WILLIAM LOONEY,GEORGE AND GEORGIANNA MARINARI,GEORGE MARINARI, ANTHONY AND GLORIAMARSICO, JOHN P. MCKENNA, JOHN J.MELLETT, DR. ARTHUR ROSE, DONALDSCOVIRA, GLEN AND YOLAN SLATER,YOLAN SLATER, BRET SLATER, ANTHONYAND CARMEN SPERDUTO, ERNA BERGER,ROBERT L. AND CAROLE J. CERASIA,DR. PATRICK CICCONE, DR. LOUISPADAVANO, STEPHEN J. COHEN, DR.JOHN PETILLO, ARTHUR C. ASCHOFF, A.DAVID ASCHOFF, JOHN CHRABASZ,KENNETH BARBOZA, COREY AND TERRYDUVALL, SUZANNE EIKEN, ERIC ANDHALLIE SWERDLIN, ERIC SWERDLIN,JERRY CHAIT, THE ELLIE WATSONTRUST, RONALD FEIGER, DONNA GEILS,MARK GLASS, DAVID HAYES, GOLDIEMILLER, CLIFF SAMARA, JEROME ANDSUSAN SCHLICHTER, JOYCE SWERDLIN,DAVID WOLFSON, DAVID WOLFSON TRUSTUWO, AND ZARINELO AND LENETTEORTEGA,

Plaintiffs,

vs.

STEVEN E. LEVY, KEITH M. BERMAN,JAMES J. KEEGAN, JOHN D. GARBER,PHILIP BECTON, CORBIN & WERTZ, ANDFENWICK & WEST,

Defendants.

No. SACV-97-191-GLT(Eex)

CLASS ACTION

1 SUMMARY OF ACTION

2 1. This is an individual and class action on behalf of all

3 persons who purchased the securities of Access HealthNet, Inc.

4 ("Access HealthNet" or the "Company"), between January 25, 1995 and

5 December 29, 1995 (the "Class Period") , seeking to pursue remedies

6 under Sections 10(b) and 20(a) of the Securities Exchange Act of

7 1934 ("Exchange Act") and Rule 10b-5 promulgated thereunder (the

8 "Class"). This action involves a course of conduct by Access

9 HealthNet insiders, officers and directors of the Company, the

10 Company's auditors and United States Securities and Exchange

11 Commission ("SEC") counsel that was designed to and did defraud

12 those who purchased Access HealthNet securities during the Class

13 Period.

14 2. This case involves defendants' use of manipulative

15 devices and their dissemination of false financial statements and

16 other false and misleading information about Access HealthNet's

17 business, all of which was, inter alia , designed to and did:

18 (a) artificially inflate the price of Access HealthNet securities

19 during the Class Period; (b) induce investors to purchase shares of

20 Access HealthNet stock; (c) allow certain defendants to sell or

21 offer to sell millions of dollars of their own Access HealthNet

22 shares at artificially inflated levels; and (d) allow defendants to

23 sell or offer to sell millions of dollars of Access HealthNet

24 securities to private investors in various private placement

25 transactions.

26 3. Not until December 29, 1995, did the true extent of

27 defendants' wrongful conduct become apparent, since on that date

28 Access HealthNet announced that it would liquidate pursuant to

- 2 -

1 Chapter 7 of the Federal Bankruptcy Code. Access HealthNet remains

2 in bankruptcy through the current time.

3 INTRODUCTION

4 4. Access HealthNet developed and sold computer operated

5 information and communication systems to the healthcare industry,

6 including hospitals, commercial and biomedical research

7 laboratories, physicians offices and clinics. Access HealthNet

8 products were designed to operate on commercially available off-

9 the-shelf computer hardware to allow easy communication between

10 clinical laboratories, physicians offices and hospitals. The

11 Company's computer systems were all modular, i.e., an entry level

12 system that could be upgraded into a more powerful system. Access

13 HealthNet's computer systems were ostensibly designed to collect

14 and report analytical as well as billing and general office data.

15 5. The Company designed its various hardware and software

16 products to appeal to the needs and demands of particular

17 healthcare market niches. The Company's flagship products included

18 three trademark products: LabACCESS, RemoteACCESS and ACCESS

19 MedLink. LabACCESS was designed for use in medical laboratories as

20 an adjunct to clinical testing instruments by collecting data

21 directly from laboratory devices, performing specialized data

22 manipulation functions and reporting the results to laboratory

23 personnel. LabACCESS also incorporated software that managed

24 regulatory and quality assurance protocols, as well as billing

25 functions. RemoteACCESS was designed to allow physicians to order

26 laboratory tests and retrieve and code laboratory test results

27 directly from the physician's office. RemoteACCESS also included

28 a wide range of other features such as back office accounting

- 3 -

1 functions, electronic mail and billing. ACCESS MedLink was an

2 enhanced version of RemoteACCESS designed to provide direct

3 communication between the physician's office and the hospital,

4 laboratory, pharmacy or radiology center. ACCESS MedLink also

5 included additional software packages including two word-processing

6 programs, electronic mail, auto-fax, billing and electronic mail

7 transfer of insurance claims to Medicare. Each of the Company's

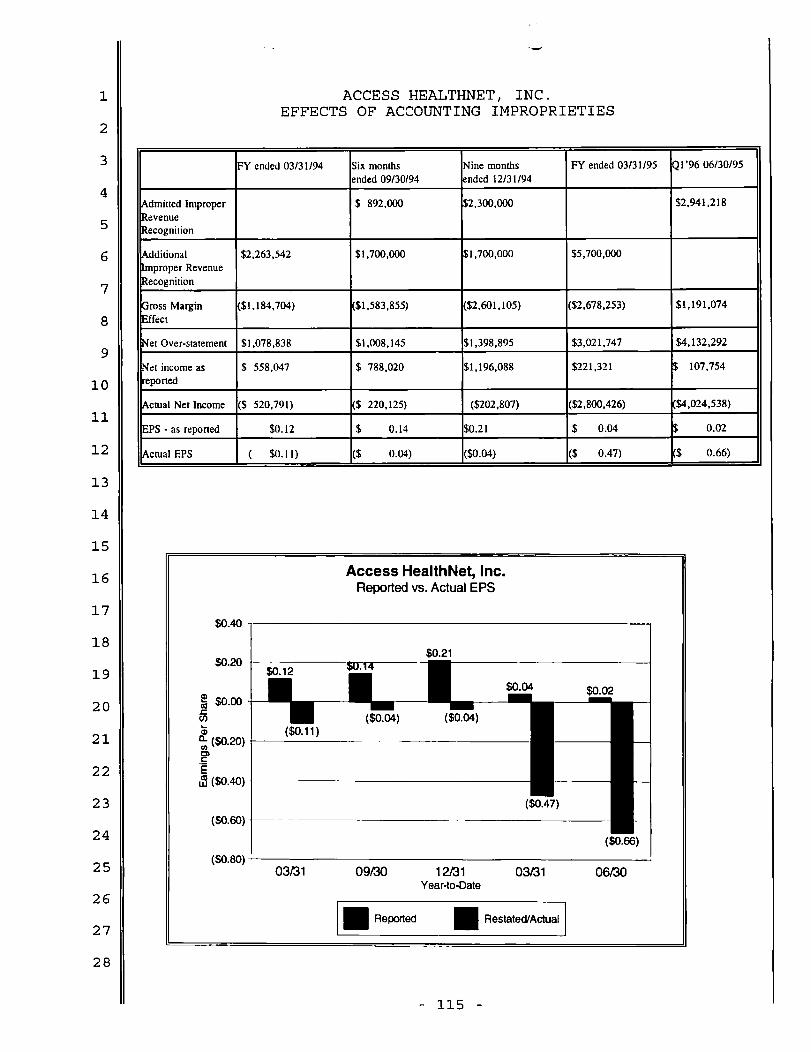

8 products were designed to be specially tailored to fit the needs of

9 each individual customer.

10 6. Access HealthNet commenced business in 1989. The Company

11 was incorporated in Delaware with its principal place of business

12 in California. Until June 1992 the Company's business consisted

13 primarily of selling its LabACCESS laboratory information systems

14 to small hospital clinical laboratories. In July 1992, the Company

15 shipped its first remote communication product, RemoteACCESS.

16 Based upon the purported success of its LabACCESS and RemoteACCESS

17 products as well as its ACCESS MedLink product which was introduced

18 in March 1994, the Company reported "' record sales and earnings ,'"

19 and represented to the market that it was experiencing consistent

20 increases in revenues and income throughout 1994 and 1995 . In

21 fact, however, to the contrary, defendants were "cooking the books"

22 at Access HealthNet. During the period of time alleged herein,

23 Access HealthNet prematurely and improperly recognized lease and

24 sales revenues in violation of Generally Accepted Accounting

25 Principles ("GAAP") and utilizing the false financial statements

26 that resulted therefrom, certain of Access HealthNet's officers and

27 directors, in conjunction with the Company's accountants Corbin &

28

11

Wertz and attorneys Fenwick & West, artificially inflated the price

- 4 -

1 of Access HealthNet stock and thereafter raised millions of dollars

2 from investors through open market sales and private placements of

3 Access HealthNet securities. Moreover, certain of Access

4 HealthNet's officers and directors successfully capitalized on

5 their false and misleading statements by selling hundreds of

6 thousands of dollars of their own Access HealthNet holdings at

7 artificially inflated prices.

8 7. On January 25, 1995, the beginning of the Class Period,

9 the Company became listed on the NASDAQ National Market System. On

10 the same day, each of the defendants signed, prepared, disseminated

11 and/or wilfully participated in: (a) the filing of the Registration

12 Statement on Form SB-2 and amendments thereto (the "Registration

13 Statement"), which included a Prospectus (the "Prospectus"); and

14 (b) the dissemination of the Prospectus. By means of the

15 Prospectus, defendants registered Access HealthNet shares for sale

16 to create a trading market, thereby liquefying Access HealthNet

17 stock. With the wilful participation of the Company's auditors and

18 SEC counsel -- defendants Corbin & Wertz and Fenwick & West,

19 respectively -- defendants were able to file multiple drafts and

20 the final Registration Statement and Prospectus that contained

21 materially false and misleading statements, including false

22 financial statements for fiscal year 1994 ended March 31, 1994, the

23 three month period ended June 30, 1994 and the six month period

24 ended September 30, 1994. The drafts and final Registration

25 Statement and Prospectus also omitted material information

26 regarding the Company's actual operating performance in that the

27 Company: (a) faced huge liquidity problems; (b) was not converting

28 accounts receivable; (c) was improperly recognizing massive amounts

- 5 -

1 of revenue from distributors that were actually related parties;

2 (d) revenue recognition policies violated GAAP; (e) equity

3 structure was in dispute; (f) future business prospects were bleak;

4 and (g) was unable to report accurate financial information, as

5 described in detail at ¶¶110-54.

6 8. Despite the misleading statements in and omissions from

7 the Prospectus, the selling stockholders, including certain

8 defendants, nonetheless registered 2,738,085 shares and offered

9 them for sale. On the same day the Registration Statement was

10 declared effective and Access HealthNet shares were listed on the

11 NASDAQ National Market System, defendant John D. Garber ("Garber")

12 sold 20,000 shares on the open market.

13 9. On February 10, 1995, the Company falsely reported

14 "RECORD" revenues of $3.3 million for the first nine months of

15 fiscal 1995 ended December 31, 1994, an increase of over 3000 from

16 the prior year and net income of approximately $408,068. The

17 Company claimed that the increase in revenues was " primarily a

18 result of increased sales to distributors ." Thereafter, the

19 defendants continued to assert that the Company was experiencing

20 " RECORD " results and that they were "' excited '" about the Company's

21 prospects. To the contrary, the true facts at that time were that:

22 (a) defendants Steven E. Levy ("Levy"), Keith M. Berman ("Berman"),

23 James J. Keegan ("Keegan") , Garber and Corbin & Wertz caused and/or

24 allowed Access HealthNet to report artificially inflated revenues

25 and earnings; and (b) the Company faced serious liquidity problems.

26 Consequently, to hide their misrepresentations and material

27 omissions, the defendants found it necessary to repeatedly comfort

28 the market with announcements regarding Access HealthNet's future

- 6 -

1 financing programs which purportedly would allow Access HealthNet

2 to readily convert Access HealthNet's lease receivables into cash.

3 The defendants made these false representations despite the fact

4 that a majority of such leases had not even been executed or had

5 been executed on terms that rendered them unsalable to third party

6 institutions. Consistently throughout the Class Period, the

7 defendants maintained that they were improving the Company's

8 liquidity through such financing agreements.

9 10. In July 1995, Access HealthNet announced that it was

10 necessary to restate its "RECORD" interim financials, admitting

11 that the defendants had overstated 1995 revenues by a total of $4.4

12 million. In response to this adverse announcement, the price of

13 Access HealthNet stock dropped by more than 10% on heavy volume,

14 but continued to trade at artificially inflated levels because

15 defendants failed to reveal the full amount of falsely recognized

16 revenue and instead steadfastly represented that revenue had been

17 and would be recognized only " upon complete delivery " and

18 " acceptance by the customer or distributor ." With the complicity

19 of Corbin & Wertz, the defendants were able to falsely convince the

20 market that Access HealthNet was now recognizing and reporting

21 revenue properly. Furthermore, the defendants maintained that al

22 majority of the " adjustments " made in connection with the fiscal

23 1995 audit would be recognized during fiscal 1996. The Company

24 also announced that defendant Levy would take over day-to-day

25 control of Access HealthNet. Despite such assurances to the market

26 that the Company was recognizing revenue properly and that the

27 Company would recognize the adjusted revenue in 1996, defendants

28 were aware that at least an additional $5.7 million of 1995 revenue

- 7 -

1 had been improperly recognized in violation of GAAP. Defendants

2 were also aware that Corbin & Wertz had not conducted its 1995

3 audit in accordance with Generally Accepted Auditing Standards

4 ("GRAS") and that no reasonable basis existed for the statement

5 that the Company expected to recognize most of the revenue adjusted

6 in 1995 during fiscal 1996.

7 11. In a further attempt to deceive the market by alleviating

8 concerns regarding the liquidity of certain of Access HealthNet's

9 assets, the defendants continued to represent, as late as August

10 1995, that most of the Company's $14 million in accounts receivable

11 would be converted into cash within the next 180 days .

12 Furthermore, with respect to Access HealthNet's accounting

13 policies, defendants Levy, Berman, Keegan and Garber continued to

14 cause the Company to falsely represent that its financial

15 statements reflected " all adjustments . considered necessary

16 for a fair presentation ." Moreover, the defendants represented

17 that they were "' very excited '" and " very pleased '" with Access

18 HealthNet's prospects, at the same time they continued to approve

19 and disseminate fraudulent financial statements.

20 12. In late September 1995, Horace Hertz ("Hertz"), formerly

21 the Corbin & Wertz concurring partner of the Access HealthNet

22 audit, became the Senior Vice President in charge of Finance at

23 Access HealthNet.

24 13. To further maintain defendants' charade, on or about

25 October 18, 1995, defendant Levy disseminated a letter to

26 shareholders in which he stated that his sole objective was "to

27 maximize shareholder value ;" that the Company had " more than 70

28 proposals outstandincr, which represent[ed] over $20,000,000 in

- 8 -

1 revenues ;" that the Company was " in the process of implementing a

2 program " that would enable it to liquify existing obligations owed

3 to it; and that the Company " expect[ed] to complete a significant

4 number of installations in the quarter ending March 31, 1996 ."

5 14. At the same time, however, that defendants were assuring

6 the market of their efforts to "maximize shareholder value," the

7 Company actually faced severe liquidity problems and was in dire

8 need of a capital infusion in order to continue its operations.

9 Therefore, defendants set about to offer for sale the private

10 placement of Access HealthNet securities in September and October

11 1995, as a result of which the Company raised approximately $2

12 million.

13 15. Throughout October, November and December 1995,

14 defendants continued to represent that they had taken steps to

15 strengthen the Company and turn it around. At the same time,

16 however, defendants knew, or should have known, that customers were

17 cancelling contracts with Access HealthNet because the Company

18 could not install systems that functioned properly nor possessed

19 the capabilities promised by the Company. Such customers included

20 Community Health Systems, Unilab Corporation ("Unilab") and

21 Physicians Clinical Laboratory, Inc. ("PCL") as well as the

22 Company's largest distributor in Southern California. Furthermore,

23 by October 1995, the Company had returned substantial amounts of

24 hardware to Digital Equipment Corp. ("Digital Equipment") and

25 placed a moratorium on equipment purchases.

26 16. It was not until December 1995, approximately two months

27 after raising $2 million in private placements, that the Company

28 11 revealed to the public its "'huge burn rate.'" Thereafter, on

- 9 -

1

1 December 29, 1995, leaving Access HealthNet's shareholders who had

2 purchased stock at artificially inflated prices holding the bag,

3 defendants announced that Access HealthNet had sought protection

4 under Chapter 7 of the Federal Bankruptcy Code. Consequently,

5 after having traded as high as $13-3/8 per share during the class

6 Period, Access HealthNet stock became worthless and was delisted

7 from NASDAQ.

8 17. Defendants' wrongful conduct, therefore, involved stock

9 manipulation by corporate insiders who intentionally issued false

10 and misleading statements for the purposes of offering to sell

11 and/or inducing the purchase of Access HealthNet securities,

12 despite the fact that they knew or should have known of the falsity

13 of their representations. The defendants' false statements

14 inflated the price of Access HealthNet stock, allowing certain

15 defendants and the Company to sell millions of dollars of Access

16 HealthNet securities at inflated prices to the investing public.

17 Defendants' wrongful conduct also includes at least reckless

18 participation by defendants Corbin & Wertz and Fenwick & West in

19 the other defendants' wrongful acts of selling or offering to sell

20 Access HealthNet stock while making material misrepresentations

21 and/or omissions.

22 18. Although plaintiffs, both individual and Class and the

23 Class they seek to represent, purchased shares of Access HealthNet

24 stock at artificially inflated prices and they were left with

25 worthless stock following the Company's filing of bankruptcy,

26 certain defendants fared better by selling their own Access

27 HealthNet stock at prices artificially inflated by their fraud.

28

11 - 10 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

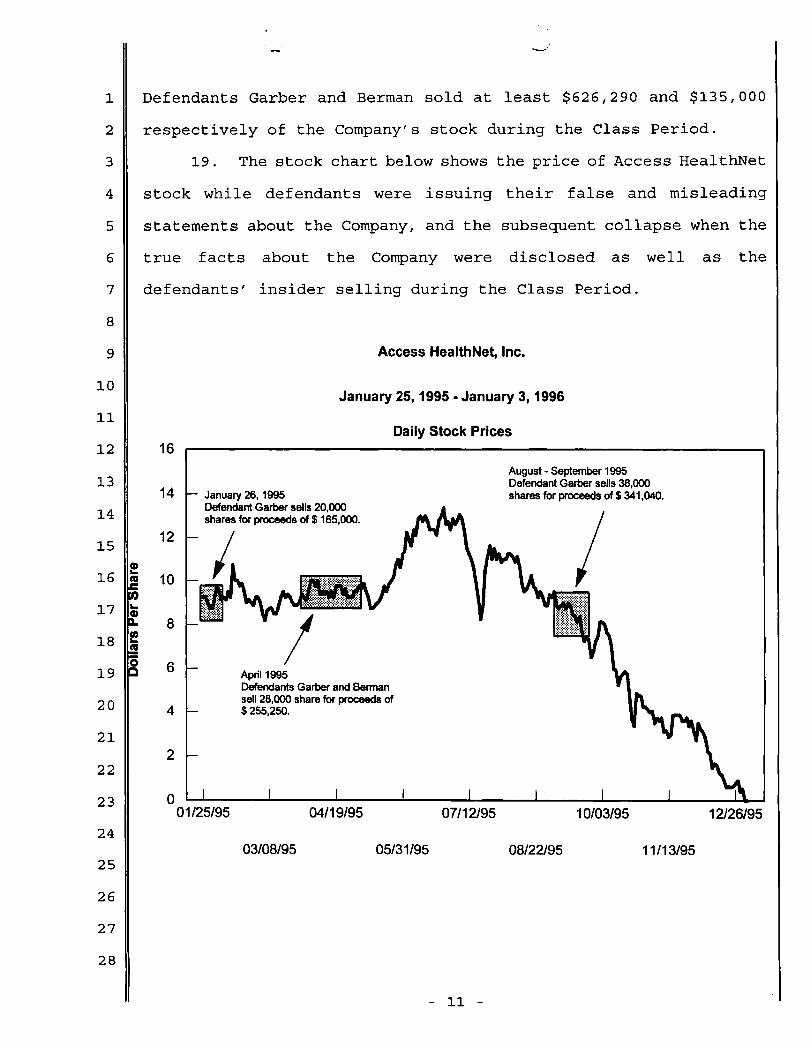

Defendants Garber and Berman sold at least $626,290 and $135,000

respectively of the Company's stock during the Class Period.

19. The stock chart below shows the price of Access HealthNet

stock while defendants were issuing their false and misleading

statements about the Company, and the subsequent collapse when the

true facts about the Company were disclosed as well as the

defendants' insider selling during the Class Period.

Access HealthNet, Inc.

16

14

12

10

8

6

4

2

January 25, 1995 - January 3, 1996

Daily Stock Prices

January 26, 1995Defendant Garber sells 20,000shares for proceeds of $ 165,000.

l-

April 1995Defendants Garber and Bermansell 28 ,000 share for proceeds of$ 255,250.

August - September 1995Defendant Garber sells 38,000shares for proceeds of $ 341,040.

1A

0 1 101/25/95

Vr

04/19/95

03/08/95 05/31/95

07/12/95 10/03/95

08/22/95 11/13/95

12126/95

- 11 -

1 JURISDICTION AND VENUE

2 20. This Court has jurisdiction over this action pursuant to

3 §27 of the Exchange Act, 15 U.S.C. §78aa, and 28 U.S.C. §1331. The

4 claims asserted herein arise under H10(b) and 20(a) of the

5 Exchange Act, 15 U.S.C. §§78j (b) and 78t(a), and Rule lOb-5, 17

6 C.F.R. §240.10b-5, promulgated thereunder by the SEC.

7 21. Venue is proper in this District pursuant to §27 of the

8 Exchange Act and 28 U.S.C. §1391(b). Many of the acts giving rise

9 to the violations complained of, including the dissemination of

10 false and misleading information, occurred in this District.

11 22. In connection with the wrongs complained' of, the

12 defendants used the instrumentalities of interstate commerce, the

13 United States mails and the facilities of the national securities

14 markets.

15 THE PARTIES

16 23. (a) Plaintiff Peter Kalmus purchased 2,000 shares of

17 Access HealthNet common stock on July 5, 1995 at $12-7/8 and has

18 been damaged thereby. Peter Kalmus is a resident and citizen of

19 New York.

20 (b) Plaintiff Leslie Rubell purchased 450 shares of

21 Access HealthNet common stock on June 28, 1995 at $12-7/8 and has

22 been damaged thereby. Leslie Rubell is a resident and citizen of

23 New York.

24 (c) Plaintiff Volunteer Limited Partnership purchased

25 8,300 shares of Access HealthNet common stock on August 1, 1995 for

26 $75,322; S,000 shares on September 20, 1995 for $40,250; and 33,333

27 shares on October 23, 1995 for $99,999 and has been damaged

28 thereby.

- 12 -

1 (d) Plaintiffs William Hirschberg and Elisa Hirschberg

2 purchased 5,000 shares of Access HealthNet common stock on March

3 28, 1995 for $46,650; 5,000 shares on March 28, 1995 for $47,275;

4 3,000 shares on March 31, 1995 for $27,990; and 12,500 shares on

5 June 1, 1995 for $100,000 and have been damaged thereby.

6 (e) Plaintiff Sigma Pairs purchased 60,000 shares of

7 Access HealthNet common stock on July 6, 1994 for $495,000; 5,000

8 shares on August 2, 1994 for $50,000; and 10,000 shares on August

9 4, 1994 at $102,500 and has been damaged thereby.

10 (f) Plaintiff Jerry Karel purchased 2,000 shares of

11 Access HealthNet common stock on August 5, 1994 for $16,785; and

12 10,000 shares on August 5, 1994 for $83,750 and has been damaged

13 thereby.

14 (g) Plaintiff Karel Private Managers Fund Series TE

15 purchased 1,200 shares of Access HealthNet common stock on August

16 2, 1994 for $11,796; and 4,800 shares on August 2, 1994 for $48,384

17 and has been damaged thereby.

18 (h) Plaintiff Karel Private Managers Fund purchased 200

19 shares of Access HealthNet common stock on August 2, 1994 for

20 $1,966; 800 shares on August 2, 1994 for $8,064; and 2,600 shares

21 on November 29, 1994 for $18,637 and has been damaged thereby.

22 (i) Plaintiff Western Hospital Corp. Retirement Trust

23 purchased 2,500 shares of Access HealthNet common stock on October

24 6, 1994 for $22,700 and has been damaged thereby.

25 (j) Plaintiff Access Self Liquidating Trust purchased

26 95,000 shares of Access HealthNet common stock on June 30, 1995 for

27 $725,750; and 25,000 shares of Access HealthNet preferred stock on

28 October 10, 1995 for $75,000 and has been damaged thereby.

- 13 -

1 (k) Plaintiff Collins Group Trust III purchased 2,500

2 shares of Access HealthNet common stock on July 18, 1995 for

3 $24,500; 3,000 shares on July 18, 1995 for $28,275; 10,000 shares

4 on July 18, 1995 for $95,500; 10,000 shares on July 20, 1995 for

5 $90,800; 66,115 shares on July 26, 1995 for $600,000; 10,000 shares

6 on September 11, 1995 for $90,500; 5,000 shares on September 12,

7 1995 for $45,250; 83,333 shares on November 11, 1995 for $249,999;

8 and 25,000 shares on December 20, 1995 for $17,387 and has been

9 damaged thereby.

10 (1) Plaintiff Compass Series E purchased 126,900 shares

11 of Access HealthNet common stock on December 22, 1994 for $999,337;

12 162,500 shares on January 31, 1995 for $1,404,812; 7,000 shares on

13 March 31, 1995 for $65,310; 126,900 shares on April 3, 1995 for

14 $970,785; 16,667 shares on April 26, 1995 for $155,003; 5,000

15 shares on May 31, 1995 for $55,875; 5,500 shares on May 31, 1995

16 for $71,225; 90,000 shares on July 31, 1995 for $816,750; 10,000

17 shares on September 12, 1995 for $91,750; 2,000 shares on October

18 31, 1995 for $8,100; 2,000 shares on October 31, 1995 for $8,350;

19 3,000 shares on October 31, 1995 for $12,900; and 5,000 shares on

20 October 31, 1995 for $20,875 and has been damaged thereby.

21 (m) Plaintiff Renaud Anselin beneficially purchased

22 10,000 shares of Access HealthNet common stock on February 14, 1995

23 for $107,500; and 2,500 shares on February 15, 1995 for $25,000 and

24 has been damaged thereby.

25 (n) Plaintiff The Charles Talbot Fund purchased 8,300

26 shares of Access HealthNet common stock on August 1, 1995 for

27 $75,322 and has been damaged thereby.

28

- 14 -

1 (o) Plaintiff Michael B. Targoff purchased 66,667 shares

2 of Access HealthNet common stock on October 24, 1995 for $200,001

3 and has been damaged thereby.

4 (p) Plaintiff Hinton Family Revocable Living Trust

5 purchased 5,000 shares of Access' HealthNet common stock on

6 September 13, 1995 for $45,875; 5,000 shares on September 18, 1995

7 for $40,875; 5,000 shares on September 20, 1995 for $40,250; and

8 33,333 shares on October 13, 1995 for $99,999 and has been damaged

9 thereby.

10 24. (a) Plaintiff Richard Avon is a New Jersey resident who

11 owned 2,300 shares of Access HealthNet stock at relevant periods,

12 2,000 of which he purchased on or about July 20, 1995 and 300 of

13 which he purchased on or about September 20, 1995 and has been

14 damaged thereby.

15 (b) Plaintiff Ken Avon is a New Jersey resident who

16 owned 2,000 shares of Access HealthNet stock at relevant periods,

17 which he purchased on or about July 20, 1995 and has been damaged

18 thereby.

19 (c) Plaintiff Jean Charlent is a resident of Belgium who

20 owned 1,000 shares of Access HealthNet stock at relevant periods,

21 which he purchased on or about July 24, 1995 and has been damaged

22 thereby.

23 (d) Plaintiff Duane D'Agostino is a New Jersey resident

24 who owned 500 shares of Access HealthNet stock at relevant periods,

25 which he purchased on or about July 20, 1995 and has been damaged

26 thereby.

27 (e) Plaintiff Stephen Madden is a New Jersey resident

28 who owned 500 shares of Access HealthNet stock at relevant periods,

- 15 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

which he purchased on or about July 20, 1995 and has been damaged

thereby.

(f) Plaintiff Robert Masessa is a New Jersey resident

who owned 500 shares of Access HealthNet stock at relevant periods,

which he purchased on or about July 20, 1995 and has been damaged

thereby.

(g) Plaintiffs Louis and Rose Argenziano are New Jersey

residents who owned 2,000 shares of Access HealthNet stock at

relevant periods, which they purchased between February 1995 and

January 1996 and have been damaged thereby.

(h) Plaintiffs Robert and Michele Bacon are Colorado

residents who owned 6,000 shares of Access HealthNet stock at

relevant periods: 4,000 shares were purchased on or about

September 27, 1995; and 2,000 shares were purchased on or about

September 29, 1995 and have been damaged thereby.

(i) Plaintiff Fred Bergman is a New York resident who

owned 2,300 shares of Access HealthNet stock at relevant periods,

which he purchased on or about October 13, 1995 and has been

damaged thereby.

(j) Plaintiff Laura J. Bohn is a New York resident who

owned 2,000 shares of Access HealthNet stock at relevant periods:

1,000 shares were purchased on or about July 26, 1995; and 1,000

shares were purchased on or about September 18, 1995 and has been

damaged thereby.

(k) Plaintiff Dr. Juan C. Carioni, P.C. is a Michigan

professional corporation which owned 2,000 shares of Access

Healthnet stock at relevant periods, which were purchased on or

about July 18, 1995 and has been damaged thereby.

- 16 -

-J

1 (1) Plaintiff Juan C. Carioni is a Michigan resident who

2 owned 1,000 shares of Access HealthNet stock at relevant periods,

3 which he purchased on or about August 14 , 1995 and has been damaged

4 thereby.

5 (m) Plaintiff Charles Costello is a Florida resident who

6 owned 2,500 shares of Access HealthNet stock at relevant periods:

7 1,500 shares were purchased on or about July 24, 1995; and 1,000

8 shares were purchased on or about September 6, 1995 and has been

9 damaged thereby.

10 (n) Plaintiff Joseph DeRosa is a New Jersey resident who

11 owned 2 , 000 shares of Access HealthNet stock at relevant periods:

12 1,000 shares were purchased on or about July 24, 1995 ; and 1,000

13 shares were purchased on or about September 18, 1995 and has been

14 damaged thereby.

15 (o) Plaintiffs Henry and Marisol DeGirolamo are New

16 Jersey residents who owned 400 shares of Access HealthNet stock at

17 relevant periods, which they purchased on or about October 13, 1995

18 and have been damaged thereby.

19 (p) Plaintiff Wilbur Eckerson is a New Jersey resident

20 who owned 4,000 shares of Access HealthNet stock at relevant

21 periods: 2,000 shares were purchased on or about August 24, 1995;

22 and 2,000 shares were purchased on or about September 22, 1995 and

23 has been damaged thereby.

24 (q) Plaintiff Carmine Gesualdi is a New Jersey resident

25 who owned 3,800 shares of Access HealthNet stock at relevant

26 periods , which she purchased on or about July 24, 1995 and has been

27 damaged thereby.

28

- 17 -

1 (r) Plaintiffs Carmine and Kathleen Gesualdi are New

2 Jersey residents who owned 1,000 shares of Access HealthNet stock

3 at relevant periods, which they purchased on or about August 18,

4 1995 and have been damaged thereby.

5 (s) Plaintiff J. David Johnson is a Pennsylvania

6 resident who owned 400 shares of Access HealthNet stock at relevant

7 periods, which he purchased on or about August 24, 1995 and has

8 been damaged thereby.

9 (t) Plaintiffs Donald and Karen Jones are New Jersey

10 residents who owned 1,000 shares of Access HealthNet stock at

11 relevant periods, which they purchased on or about September 27,

12 1995 and have been damaged thereby.

13 (u) Plaintiff Barbara Looney is a New Jersey resident

14 who owned 4,000 shares of Access HealthNet stock at relevant

15 periods: 1,000 shares were purchased on or about July 28, 1995;

16 1,000 shares were purchased on or about August 14, 1995; and 2,000

17 shares were purchased on or about September 7, 1995 and has been

18 damaged thereby.

19 (v) Plaintiff William Looney is a New Jersey resident

20 who owned 1,100 shares of Access HealthNet stock at relevant

21 periods: 1,000 shares were purchased on or about July 24, 1995;

22 and 100 shares were purchased on or about September 7, 1995 and has

23 been damaged thereby.

24 (w) Plaintiffs George and Georgianna Marinari are

25 Pennsylvania residents who owned 1,600 shares of Access HealthNet

26 stock at relevant periods, which they purchased on or about

27 September 19, 1995 and have been damaged thereby.

28

- 18 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

(x) Plaintiff George Marinari -is a Pennsylvania resident

who owned 1,500 shares of Access HealthNet stock at relevant

periods, which he purchased on or about August 24, 1995 and has

been damaged thereby.

(y) Plaintiffs Anthony and Gloria Marsico are New Jersey

residents who owned 3,000 shares of Access HealthNet stock at

relevant periods: 1,000 shares were purchased on or about July 24,

1995; 1,000 shares were purchased on or about August 14, 1995; and

1,000 shares were purchased on or about September 6, 1995 and have

been damaged thereby.

(z) Plaintiff John P. McKenna is a New York resident who

owned 1,500 shares of Access HealthNet stock at relevant periods,

which he purchased on or about August 8, 1995 and has been damaged

thereby.

(aa) Plaintiff John J. Mellett is a New York resident who

owned 3,000 shares of Access HealthNet stock at relevant periods:

2,000 shares were purchased on or about July 18, 1995; and 1,000

shares were purchased on or about September 21, 1995 and has been

damaged thereby.

(ab) Plaintiff Dr. Arthur Rose is a Michigan resident who

owned 3,000 shares of Access HealthNet stock at relevant periods:

2,000 shares were purchased on or about August 24, 1995; and 1,000

shares were purchased on or about September 25, 1995 and has been

damaged thereby.

(ac) Plaintiff Donald Scovira is an Arizona resident who

owned 4,500 shares of Access HealthNet stock at relevant periods:

1,000 shares were purchased on or about July 24, 1995; 1,500 shares

were purchased on or about August 21, 1995; and 1,000 shares were

- 19 -

1 purchased on or about September 7, 1995 and has been damaged

2 thereby.

3 (ad) Plaintiffs Glen and Yolan Slater are New York

4 residents who owned 2,000 shares of Access HealthNet stock at

5 relevant periods: 1,000 shares were purchased on or about July 27,

6 1995; and 1,000 shares were purchased on or about September 7, 1995

7 and have been damaged thereby.

8 (ae) Plaintiff Yolan Slater is a New York resident who

9 owned 1,200 shares of Access HealthNet stock at relevant periods,

10 which she purchased on or about September 7, 1995 and has been

11 damaged thereby.

12 (af) Plaintiff Bret Slater is New York resident who

13 owned 500 shares of Access HealthNet stock at relevant periods,

14 which he purchased on or about November 6, 1995 and has been

15 damaged thereby.

16 (ag) Plaintiffs Anthony and Carmen Sperduto are New York

17 residents who owned 2,000 shares of Access HealthNet stock at

18 relevant periods: 1,000 shares were purchased on or about July 24,

19 1995; and 1,000 shares were purchased on or about September 25,

20 1995 and have been damaged thereby.

21 (ah) Plaintiff Erna Berger is a New York resident who

22 owned 2,000 shares of Access HealthNet stock at relevant periods,

23 which she purchased on or about July 25, 1995 and has been damaged

24 thereby.

25 (ai) Plaintiff Robert L. Cerasia is a New Jersey resident

26 who owned 2,000 shares of Access HealthNet stock at relevant

27 periods: 1,000 shares were purchased on or about July 14, 1995;

28

- 20 -

1 and 1,000 shares were purchased on or about August 30, 1995 and has

2 been damaged thereby.

3 (aj) Plaintiff Carole J. Cerasia is a New Jersey resident

4 who owned 10,000 shares of Access HealthNet stock at relevant

5 periods: 2,000 shares were purchased on or about April 27, 1995;

6 4,000 shares were purchased on or about July 13, 1995; 2,000 shares

7 were purchased on or about July 24, 1995; and 2,000 shares were

8 purchased on or about October 20, 1995 and has been damaged

9 thereby.

10 (ak) Plaintiff Dr. Patrick Ciccone is a New Jersey

11 resident who owned 2,000 shares of Access HealthNet stock at

12 relevant periods, which he purchased on or about July 26, 1995 and

13 has been damaged thereby.

14 (al) Plaintiff Stephen J. Cohen is a Florida resident who

15 owned 98,000 shares of Access HealthNet stock at relevant periods:

16 8,000 shares were purchased on or about June 8, 1995; 10,000 shares

17 were purchased on or about October 30, 1995; 2,000 shares were

18 purchased on or about October 31, 1995; 8,000 shares were purchased

19 on or about November 1, 1995; 15,000 shares were purchased on or

20 about November 6, 1995; 5,000 shares were purchased on or about

21 November 8, 1995; 10,000 shares were purchased on or about November

22 10, 1995; 30,000 shares were purchased on or about November 13,

23 1995; 5,000 shares were purchased on or about November 16, 1995;

24 2,000 shares were purchased on or about November 17, 1995; and

25 3,000 shares were purchased on or about November 20, 1995 and has

26 been damaged thereby.

27 (am) Plaintiff Dr. Louis Padavano is a New York resident

28 who owned 1,000 shares of Access HealthNet stock at relevant

- 21 -

1 periods: 500 shares were purchased on or about August 29, 1995;

2 and 500 shares were purchased on or about October 24, 1995 and has

3 been damaged thereby.

4 (an) Plaintiff Dr. John Petillo is a New Jersey resident

5 who owned 3,000 shares of Access HealthNet stock at relevant

6 periods: 1,500 shares were purchased on or about July 14, 1995;

7 500 shares were purchased on or about August 29, 1995; and 1,000

8 shares were purchased on or about October 24, 1995 and has been

9 damaged thereby.

10 (ao) Plaintiff Arthur C. Aschoff is a Massachusetts

11 resident who owned 1,500 shares of Access HealthNet stock at

12 relevant periods: 500 shares were purchased on or about July 25,

13 1995; 500 shares were purchased on or about July 26, 1995; and 500

14 shares were purchased on or about August 24, 1995 and has been

15 damaged thereby.

16 (ap) Plaintiff A. David Aschoff is a Vermont resident who

17 owned 1,500 shares of Access HealthNet stock at relevant periods:

18 300 shares were purchased on or about July 24, 1995; 200 shares

19 were purchased on or about July 25, 1995; 400 shares were purchased

20 on or about August 9, 1995; and 600 shares were purchased on or

21 about September 28, 1995 and has been damaged thereby.

22 (aq) Plaintiff John Chrabasz is a New Jersey resident who

23 owned 1,000 shares of Access HealthNet stock at relevant periods:

24 500 shares were purchased on or about July 27, 1995; and 500 shares

25 were purchased on or about September 19, 1995 and has been damaged

26 thereby.

27 (ar) Plaintiff Kenneth Barboza is a new York resident who

28 owned 1,000 shares of Access HealthNet stock at relevant periods:

- 22 -

1 500 shares were purchased on or about July 25, 1995; and 500 shares

2 were purchased on or about July 27, 1995 and has been damaged

3 thereby.

4 (as) Plaintiffs Corey and Terry Duvall are New Jersey

5 residents who owned 700 shares of Access HealthNet stock at

6 relevant periods: 300 were purchased on or about July 25, 1995;

7 200 shares were purchased on or about September 11, 1995; and 200

8 shares were purchased on or about September 27, 1995 and have been

9 damaged thereby.

10 (at) Plaintiff Suzanne Eiken is a New Jersey resident who

11 owned 580 shares of Access HealthNet stock at relevant periods:

12 400 shares were purchased on or about July 28, 1995; and 180 shares

13 were purchased on or about September 29, 1995 and has been damaged

14 thereby.

15 (au) Plaintiffs Eric and Hallie Swerdlin are New Jersey

16 residents who owned 1,000 shares of Access HealthNet stock at

17 relevant periods, which they purchased on or about July 26, 1995

18 and have been damaged thereby.

19 (av) Plaintiff Eric Swerdlin is a New Jersey resident who

20 owned 1,000 shares of Access HealthNet stock at relevant periods,

21 which he purchased on or about July 31, 1995 and has been damaged

22 thereby.

23 (aw) Plaintiff Jerry Chait is a New Jersey resident who

24 owned 600 shares of Access HealthNet stock at relevant periods,

25 which he purchased on or about July 24, 1995 and has been damaged

26 thereby.

27 (ax) Plaintiff The Ellie Watson Trust is a Colorado trust

28 which owned 1,000 shares of Access HealthNet stock at relevant

- 23 -

1 periods, which it purchased on or about August 1, 1995 and has been

2 damaged thereby.

3 (ay) Plaintiff Ronald Feiger is a New Jersey resident who

4 owned 300 shares of Access HealthNet stock at relevant periods,

5 which he purchased on or about July 1995 and has been damaged

6 thereby.

7 (az) Plaintiff Donna Geils is a Florida resident who

8 owned 300 shares of access HealthNet stock at relevant periods,

9 which she purchased on or about July 1995 and has been damaged

10 thereby.

11 (ba) Plaintiff Mark Glass i s a Missouri resident who

12 owned 1,000 shares of Access HealthNet stock at relevant periods,

13 which he purchased on or about July 1995 and has been damaged

14 thereby.

15 (bb) Plaintiff David Hayes is a Florida resident who

16 owned 1,000 shares of Access HealthNet stock at relevant periods,

17 which he purchased on or about July 1995 and has been damaged

18 thereby.

19 (bc) Plaintiff Goldie Miller is a Missouri resident who

20 owned 400 shares of Access HealthNet stock at relevant periods,

21 which she purchased on or about July 1995 and has been damaged

22 thereby.

23 (bd) Plaintiff Cliff Samara is a New York resident who

24 owned 2,000 shares of Access HealthNet stock at relevant periods,

25 which he purchased on or about July 1995 and has been damaged

26 thereby.

27 (be) Plaintiffs Jerome and Susan Schlichter are Missouri

28 residents who owned 2,000 shares of Access HealthNet stock at

- 24 -

1 relevant periods, which they purchased on or about July 1995 and

2 have been damaged thereby.

3 (bf) Plaintiff Joyce Swerdlin is a New York resident who

4 owned 1,000 shares of Access HealthNet stock at relevant periods,

5 which she purchased on or about July 1995 and has been damaged

6 thereby.

7 (bg) Plaintiff David Wolfson is a California resident who

8 owned 1,000 shares of Access HealthNet stock at relevant periods,

9 which he purchased on or about July 1995 and has been damaged

10 thereby.

11 (bh) Plaintiff David Wolfson Trust UWO is a California

12 trust which owned 1,500 shares of Access HealthNet stock at

13 relevant periods, which it purchased on or about July 1995 and has

14 been damaged thereby.

15 (bi) Plaintiffs Zarinelo and Lennette Ortega are Illinois

16 residents who owned 1,000 shares of Access HealthNet stock at

17 relevant periods, which they purchased on or about July 1995 and

18 have been damaged thereby.

19 25. Plaintiffs referenced in ¶24(a)-(bi), with the exception

20 of plaintiff Bret Slater, are brokers or retail customers who

21 purchased Access HealthNet stock through the Florham Park, New

22 Jersey, office of Smith Barney & Co. The stock was purchased

23 through brokers Steven Jones, Donald Jones, Robert Cerasia, and

24 Thomas Aschoff. These brokers, along with other brokers and

25 financial analysts, including Eric Swerdlin formerly of Smith

26 Barney's Florham Park office -- now employed by Swerdlin Financial

27 Service, Inc. of Chester, New Jersey -- and Gregory Cook, formerly

28 of the Dallas, Texas, office of Bear Stearns & Co., received

- 25 -

1 various information from Access HealthNet and its officers and

2 directors which they shared in good faith and in reliance with

3 their customers and each other. Their customers also shared this

4 information with each other and with various of the forenamed

5 brokers. Plaintiff Bret Slater purchased Access HealthNet stock

6 based, in part, on information provided by the defendants to the

7 Florham Park, New Jersey, office of Smith Barney & Co.

8 26. Defendant Corbin & Wertz was, at all material times

9 hereto, a firm of certified public accountants with its only office

10 in California. Corbin & Wertz was engaged by Access HealthNet to

11 provide independent accounting, consulting and auditing services.

12 Prior to and during the Class Period, Corbin & Wertz, through its

13 partners Hertz, Joseph Johnson ("Johnson"), and other employees,

14 gave the Company, defendants Levy, Berman, Keegan and Garber in

15 addition to former member of management Michael McMahon

16 ("McMahon"), accounting advice and consultation regarding Access

17 HealthNet's annual and quarterly reports filed with the SEC.

18 Corbin & Wertz, through its partners and other employees, assisted

19 in the preparation and filing of the Registration Statement and

20 Prospectus, consented to being named as experts therein and caused

21 its opinion to be included in the Registration Statement and

22 Prospectus. During the process of obtaining final approval of the

23 Registration Statement and Prospectus from the SEC, Corbin & Wertz

24 participated in conference calls with the SEC accounting staff

25 during which Corbin & Wertz defended the Company's false financial

26 statements and revenue recognition policies. Corbin & Wertz

27 reviewed, assisted in the preparation of and/or knowingly approved

28 materially false reports which were made in connection with Access

- 26 -

1

1 HealthNet's fiscal year 1994 audited financials, fiscal 1995

2 interim financials (both of which were included in the Prospectus),

3 its fiscal year 1995 audited financials and its first fiscal

4 quarter 1996 interim financials. Members and employees of Corbin

5 & Wertz, including Johnson, assisted in the preparation and review

6 of Access HealthNet's quarterly financial statements prior to the

7 public release of the results and knew, or recklessly disregarded,

8 the material falsity of Access HealthNet's press releases and SEC

9 filings reporting those results. In the course of rendering

10 services to Access HealthNet, Corbin & Wertz knew, or recklessly

11 disregarded, that Access HealthNet was improperly reporting

12 revenues and income. Corbin & Wertz knew, or should have known,

13 that these transactions suffered from serious defects as detailed

14 in ¶$110-54, which made reporting virtually all this income

15 improper and/or required write-offs and/or writedowns under GAAP.

16 In addition, Corbin & Wertz knew, or should have known, that its

17 audit was not conducted in accordance with GAAS. See 1$155-200.

18 27. Defendant Fenwick & West was, at all relevant times, a

19 partnership engaged in the practice of law with its office located

20 at 2 Palo Alto Square, Suite 800, Palo Alto, California. During

21 the period early 1993 to late 1995, Fenwick & West served as

22 corporate counsel to Access HealthNet and advised the Company on

23 numerous matters, including several private offerings of Access

24 HealthNet securities. Fenwick & West served as legal counsel to

25 Access HealthNet in connection with the registration of the

26 Company's securities on January 25, 1995 and the listing of the

27 Company's shares on the NASDAQ National Market System the same day.

28 In that capacity, Fenwick & West passed on various legal matters in

- 27 -

1 connection with the registration and listing on the NASDAQ National

2 Market System and allowed its name to be displayed in the

3 Registration Statement and Prospectus. In return for such

4 services, Fenwick & West received substantial fees from Access

5 HealthNet throughout the Class Period. Fenwick & West, through its

6 attorneys responsible for working on the Access HealthNet

7 engagement, assisted in the preparation and filing of the

8 Registration Statement and Prospectus, consented to being named as

9 experts therein and caused its opinion to be included in the

10 Registration Statement and Prospectus. During the process of

11 obtaining final approval of the Registration Statement and

12 Prospectus from the SEC, Fenwick & West corresponded and

13 participated in conference calls with the SEC. During such

14 interaction with the SEC, along with defendant Corbin & Wertz,

15 Fenwick & West defended the Company's false financial statements

16 and revenue recognition policies. Through its due diligence

17 investigations of Access HealthNet while assisting in the

18 preparation and drafting of different versions of the Registration

19 Statement and Prospectus filed with the SEC, Fenwick & West

20 negligently or recklessly disregarded the falsity of the

21 Registration Statement, the Prospectus, their own statements made

22 to the SEC and statements made by other defendants including Corbin

23 & Wertz. Because of Fenwick & West's position as SEC counsel to

24 the Company, they had access to the non-public information about

25 Access HealthNet's business, accounting practices, finances,

26 products, markets and present and future business prospects via

27 access to internal corporate documents (including the Company's

28 operating plans, budgets and forecasts and reports of actual

- 28 -

1 operations compared thereto), conversations and connections with

2 other corporate officers and employees, attendance at management

3 and Board of Directors meetings and committees thereof and via

4 reports and other information provided to them in connection

5 therewith. Fenwick & West had access to material non-public

6 information regarding the Company's improper accounting practices,

7 including impropriety of certain revenue recognized, and based on

8 such information, knew, or recklessly disregarded, that the Company

9 was improperly reporting revenues and income by issuing false

10 financial results in press releases and SEC filings as detailed in

11 ¶¶110-54 and 201-05.

12 28. (a) Defendant Levy was, at all relevant times, the sole

13 stockholder of Kalorama Corporation, the Managing General Partner

14 of Threshold Technology Partners, L.P. ("Threshold"), which, as of

15 December 31, 1994, was the Company's largest shareholder, owning

16 16.46 of the Company's stock, most of which was acquired at

17 approximately $1.04 per share in a marked contrast to the public

18 shareholders' purchase prices. Defendant Levy also controlled an

19 additional 565,000 shares which were held by parties related to

20 defendant Levy, including certain limited partners in Threshold.

21 Even prior to July 18, 1995, defendant Levy controlled Access

22 HealthNet and certain of the other defendants through his large

23 holdings of Access HealthNtet stock. His control over Access

24 HealthNet is further evidenced by his July 1995 "reorganization" of

25 the Company. After July 18, 1995, defendant Levy functioned as

26 Chairman of the Board and Chief Executive Officer of the Company.

27 Because of Levy's position with the Company, he had access to the

28 non-public information about Access HealthNet's business,

- 29 -

1 accounting practices, finances, products, markets and present and-

2 future business prospects via access to internal corporate

3 documents (including the Company's operating plans, budgets and

4 forecasts and reports of actual operations compared thereto),

5 conversations and connections with other corporate officers and

6 employees, attendance at management and Board of Directors meetings

7 and committees thereof and via reports and other information

8 provided to him in connection therewith. During his tenure as

9 Chairman and Chief Executive officer, defendant Levy knew, or

10 should have known, that customers, including PCL, Community Health

11 Systems and Unilab, were cancelling existing contracts. During the

12 Class Period, defendant Levy also engaged in a series of

13 transactions designed solely to manipulate the price of Access

14 HealthNet stock.

15 (b) Defendant Berman was, at all relevant times prior to

16 July 18, 1995, Chief Executive Officer and a director of the

17 Company, and until his termination in October 1995, President of

18 the Company. Defendant Berman signed, prepared, and/or

19 disseminated the Registration Statement and Prospectus for the

20 purpose of selling and/or offering to sell Access HealthNet

21 securities. Furthermore, defendant Berman disseminated additional

22 false statements during the Class Period -for the purpose of

23 inflating the price of Access HealthNet stock and inducing others

24 to purchase his shares of Access HealthNet stock. Because of

25 Berman's position with the Company, he had access to the non-public

26 information about Access HealthNet's business, accounting

27 practices, finances, products, markets and present and future

28 business prospects via access to internal corporate documents

- 30 -

1 (including the Company's operating plans, budgets and forecasts and

2 reports of actual operations compared thereto), conversations and

3 connections with other corporate officers and employees, attendance

4 at management and Board of Directors meetings and committees

5 thereof and via reports and other information provided to him in

6 connection therewith. Defendant Berman had access to material non-

7 public information regarding the Company's fraudulent accounting

8 practices, including the impropriety of certain recognized revenue,

9 as well as the Company's inability to fulfill orders and install

10 products as represented. Based on such information, Berman knew,

11 or should have known, that the Company was improperly reporting

12 revenues and income by issuing false financial results in press

13 releases and SEC filings. In connection with Access HealthNet's

14 1994 and 1995 SEC filings and private placement offerings,

15 defendant Berman prepared and disseminated fraudulent financial

16 statements. During the Class Period and as part of the fraudulent

17 scheme, Berman sold $135,000 of Access HealthNet stock based on

18 inside information.

19 (c) Defendant Keegan was, at all relevant times, until

20 late September 1995 with the appointment of Hertz as Senior Vice

21 President - Finance, the Company's Chief Financial officer and

22 Treasurer. Defendant Keegan signed, prepared and/or disseminated

23 the Registration Statement and Prospectus for the purpose of

24 selling and/or offering to sell Access HealthNet securities.

25 Because of Keegan's position with the Company, he had access to the

26 non-public information about Access HealthNet's business,

27 accounting practices, finances, products, markets and present and

28 future business prospects via access to internal corporate

- 31 -

1 documents (including the Company's operating plans, budgets and

2 forecasts and reports of actual operations compared thereto),

3 conversations and connections with other corporate officers and

4 employees, attendance at management and Board of Directors meetings

5 and committees thereof and via reports and other information

6 provided to him in connection therewith. Defendant Keegan had

7 access to material non-public information regarding the Company's

8 fraudulent accounting practices, including the impropriety of

9 certain recognized revenue, as well as the Company's inability to

10 fulfill orders and install products as represented. Based on such

11 information, Keegan knew, or should have known, that the Company

12 was improperly reporting revenues and income by issuing false

13 financial results in press releases and SEC filings. In connection

14 with Access HealthNet's 1994 and 1995 SEC filings and private

15 placement offerings, defendant Keegan prepared and disseminated

16 fraudulent financial statements.

17 (d) Defendant Garber was, at all relevant times, a

18 director of the Company and as of December 31, 1994, beneficially

19 owned over 555,000 shares of Access HealthNet common stock. For

20 the purpose of offering to sell and selling his own Access

21 HealthNet shares and inducing the purchase of Access HealthNet

22 securities by others, defendant Garber signed the Registration

23 Statement and assisted in the preparation and dissemination of the

24 Prospectus and made other statements during the Class Period,

25 despite the fact that, because of his attendance at monthly Board

26 of Director meetings and his membership on the Audit Committee, he

27 was familiar with certain fictitious sales and knew, or should have

28 11 known, that the various financial results contained in the

- 32 -

1 Registration Statement and Prospectus reflected egregious

2 violations of GAAP and included the recognition of revenue for

3 contracts which had not been executed and for sales to certain

4 distributors neither of which could be recognized pursuant to GAAP .

5 Because of Garber's position with the Company, he had access to the

6 non-public information about Access HealthNet's business,

7 accounting practices, finances, products, markets and present and

8 future business prospects via access to internal corporate

9 documents (including the Company's operating plans, budgets and

10 forecasts and reports of actual operations compared thereto),

11 conversations and connections with other corporate officers and

12 employees, attendance at management and Board of Directors meetings

13 and committees thereof and via reports and other information

14 provided to him in connection therewith. Despite the fact that he

15 knew or should have known of the adverse facts alleged in 11110-54,

16 defendant Garber reviewed and signed the false Report on Form

17 10-KSB and made other false statements, while selling at least

18 71,000 shares of his own Access HealthNet stock during the Class

19 Period for as much as $9.25 per share, for proceeds of $626,290.

20 (e) Defendant Philip Becton ("Becton") was, at all

21 relevant times since July 1995, a director of the Company.

22 Defendant Becton was also, at all relevant times, the sole

23 stockholder of Flagship Corporation, the Administrative General

24 Partner of Threshold. Because of Becton's position with Threshold

25 and the Company, he had access to the non-public information about

26 Access HealthNet's business, finances, products, markets and

27 present and future business prospects via access to internal

28 corporate documents (including the Company's operating plans,

- 33 -

1 budgets and forecasts and reports of actual operations compared

2 thereto), conversations and connections with other corporate

3 officers and employees, attendance at management and Board of

4 Directors meetings and committees thereof and via reports and other

5 information provided to him in connection therewith. As an officer

6 and director of Access HealthNet, defendant Becton had a duty to

7 Access HealthNet shareholders to act honestly and in good faith.

8 In connection with his positions with Access HealthNet and

9 Threshold, defendant Becton along with defendant Levy engaged in a

10 series of transactions which were designed to manipulate the price

11 of Access HealthNet securities.

12 (f) The individuals named as plaintiffs in (a) - (e) above

13 are sometimes referred to herein as the "Individual Defendants."

14 29. Defendants Levy, Berman, Keegan and Becton by reason of

15 their stock ownership, management position and/or membership on the

16 Company's Board of Directors, were controlling persons of Access

17 HealthNet and had the power and influence, and exercised the same,

18 to cause the other defendants to engage in the conduct complained

19 of herein. Evidence of their control is further evidenced by

20 defendant Levy's and Becton's orchestration of the reorganization

21 of Access HealthNet in mid-1995.

22 30. As officers, directors and/or controlling persons of a

23 publicly-held company whose stock is registered with the SEC under

24 the Exchange Act and traded on the NASDAQ National Market System

25 and NYSE, the Individual Defendants had a duty to promptly

26 disseminate accurate and truthful information with respect to the

27 Company's operations, business, products, markets, management,

28 earnings, and present and future business prospects, to correct any

- 34 -

1 previously issued statements that had become untrue and to disclose

2 any adverse trends that would materially affect the present and

3 future financial operating results of the Company, so that the

4 market price of the Company's stock would be based upon truthful

5 and accurate information.

6 31. The Individual Defendants, because of their positions

7 with the Company, controlled the contents of its quarterly and

8 annual reports, press releases and presentations to securities

9 analysts. The Individual Defendants were provided with copies of

10 the Company's reports and press releases alleged herein to be

11 misleading prior to or shortly after their issuance and had the

12 ability and opportunity to prevent their issuance or cause them to

13 be corrected. Because of their positions and access to material

14 non-public information available to them but not the public, each

15 of these defendants knew or recklessly disregarded that the adverse

16 facts specified herein had not been disclosed to and were being

17 concealed from the public and that the positive representations

18 which were being made were then false and misleading. As a result,

19 each of the Individual Defendants is responsible for the accuracy

20 of the corporate reports, filings and releases detailed herein as

21 "group published" information and is therefore responsible and

22 liable for the representations contained therein.

23 DEFENDANTS' MOTIVE AND OPPORTUNITY

24 32. The defendants' motive to engage in this conduct included

25 a desire to inflate the price of Access Health-Net stock sales and

26 to: (a) cover up and conceal the mismanagement of Access HealthNet

27 by the Individual Defendants while protecting and enhancing their

28 executive positions and the substantial compensation and prestige

- 35 -

1 they obtained thereby; (b) enhance the value of their holdings of

2 Access HealthNet stock and/or options to purchase Access HealthNet

3 stock; (c) inflate the reported profits of Access HealthNet or

4 falsify its progress in order to obtain larger payments under the

5 Company's officer bonus compensation plan and/or via discretionary

6 individual performance bonuses; (d) permit Access HealthNet and

7 Company insiders to sell their Access HealthNet stock at inflated

8 prices; (e) permit Access HealthNet to register its stock for sale

9 to the open market; and (f) permit Corbin & Wertz and Fenwick &

10 West to earn substantial fees.

11 33. Each of the Individual Defendants had the opportunity to

12 commit and participate in the fraud. The Individual Defendants

13 were the top officers, directors and/or controlling persons of

14 Access HealthNet and controlled its press releases, corporate

15 reports, SEC filings, the preparation of its financial statements

16 and its communications with analysts. Thus, the Individual

17 Defendants controlled the public dissemination of, and could

18 falsify, the information about Access HealthNet's business,

19 finances and future prospects that reached the public and impacted

20 the price of its stock.

21 ACCESS HEALTHNET'S INTERNAL FORECASTS,PLANS AND PROJECTIONS

2234. A key management tool for Access HealthNet's top

23executives was Access HealthNet's annual budget or forecast. The

24

Individual Defendants closely monitored the Company's actual25

performance, i.e., actual results of operations, compared to the26

budgeted and/or forecasted results. Each of the Individual27

Defendants was aware of Access HealthNet's 1995 and 1996 forecasts28

- 36 -

1 and budgets and of internal reports circulated monthly, comparing

2 Access HealthNet's actual results to those previously budgeted

3 and/or forecasted. Access HealthNet's top executives used its 1995

4 and 1996 budgets and forecasts as the basis for the statements they

5 publicly made about the Company's performance during 1995.

6 Furthermore, throughout the Class Period, each of the defendants

7 disseminated false financial projections for the purpose of

8 inducing the purchase of Access HealthNet warrants, common stock,

9 preferred stock and subordinated debentures ("securities").

10 STATUTORY SAFE HARBOR

11 35. The statutory safe harbor provided for forward-looking

12 statements under certain circumstances does not apply to any of the

13 allegedly false forward-looking statements pled in this Complaint

14 because the statements pled in ¶¶37, 40, 46-48, 50, 56, 60, 63-67,

15 69-74, 76-79, 81-84, 86-90, 93-96, 98-100, 102-04, 160, 181 and 186

16 were made prior to the enactment of the statutory safe harbor on

17 December 22, 1995, via legislation that may not be applied

18 retroactively. Alternatively, none were identified as "forward-

19 looking statements" when made. Nor was it stated that actual

20 results "could differ materially from those projected." Nor did

21 meaningful cautionary statements identifying important factors that

22 could cause actual results to differ materially from those in the

23 forward-looking statements accompany those forward-looking

24 statements. Alternatively, to the extent that the statutory safe

25 harbor does apply to any forward-looking statements pled in ¶¶37,

26 40, 46-48, 50, 56, 60, 63-67, 69-74, 76-79, 81-84, 86-90, 93-96,

27 98-100, 102-04, 160, 181 and 186, the defendants are liable for

28 those false forward-looking statements because at the time each of

- 37 -

1 those forward-looking statements was made, the speaker knew the

2 forward-looking statement was false and the forward-looking

3 statement was authorized and/or approved by an executive officer of

4 Access HealthNet who knew that those statements were false when

5 made.

6 DEFENDANTS' FRAUDULENT SCHEME AND COURSE OF BUSINESS

7 36. Each of the defendants is liable as a participant in a

8 fraudulent scheme and course of business that operated as a fraud

9 or deceit on purchasers of Access HealthNet stock, by making false

10 and misleading statements and/or concealing material adverse facts,

11 including certain fraudulent accounting practices and issuing or

12 certifying false financial statements. The fraudulent scheme and

13 course of business: (a) artificially inflated the price of Access

14 HealthNet stock; (b) deceived the investing public, including

15 plaintiffs and Class members, regarding Access HealthNet's

16 financial condition and business; (c) caused plaintiffs and members

17 of the Class to purchase Access, HealthNet stock at inflated prices;

18 (d) permitted Access HealthNet and defendants Berman and Garber to

19 sell, or otherwise dispose of, their Access HealthNet stock at

20 artificially inflated prices; (e) permitted defendants to sell or

21 offer to sell millions of dollars of Access HealthNet securities to

22 private investors in various private placement transactions; and

23 (f) permitted Corbin & Wertz and Fenwick & West to earn substantial

24 fees.

25 DEFENDANTS' PRE-CLASS PERIOD CONDUCT AND STATEMENTS

26 37. On December 1, 1993, Access HealthNet filed a

27 Registration Statement on Form SB-2 in which Fenwick & West was

28 prominently featured on the front page as SEC counsel to the

- 38 -

1 Company. In preparing the December 1993 Registration Statement and

2 the subsequent four amendments, Fenwick & West knew of the

3 following "red flags" which should have prevented the filing of a

4 Registration Statement:

5 (a) Fenwick & West knew as early January 1993 that

6 McMahon, Access Healthnet's Chief Financial Officer from 1989 to

7 late 1994, had confessed to fraud when, McMahon, then a Chief

8 Executive Officer of an equipment leasing business, had

9 intentionally induced investors to advance funds for the purchase

10 of lease equipment that his company did not own ;

11 (b) Approximately 700 of the customers of Access

12 HealthNet financed their purchase through a leasing option,

13 however, most of the Company's leasing documentation was not signed

14 by either party and in most cases the original proposal was only

15 signed by Access HealthNet;

16 (c) No customer agreements existed relating to

17 RemoteACCESS, the Company's newest product;

18 (d) Some of Access HealthNet's distributors were on the

19 Company's payroll, received Company benefits and had their local

20 officers subsidized by Access HealthNet, a representation initially

21 made by McMahon as early as May 1993;

22 (e) The basis of Access HealthNet's technology remained

23 at issue in that no license agreement existed and no promissory

24 note for the purchase of such technology from defendant Berman's

25 former company, SDI Holding Company, was verified;

26 (f) A June 1993 draft of Cooper & Lybrand's management

27 letter to the Individual Defendants listing approximately ten

28 reportable conditions involving significant deficiencies in the

- 39 -

v r.il

1 Company's internal control structure that could adversely affect

2 the Company's ability to report data consistent with management's

3 representations and with the Company's financial statements;

4 (g) The reportable conditions found by Coopers & Lybrand

5 included the Company's lack of paperwork to evidence customers'

6 orders, no organized shipping system, no purchasing system, limited

7 documentation for capitalized software costs, items in accounts

8 receivable misclassified, accounts receivables mixed lease

9 receivables currently due and receivables collected on behalf of

10 lease investors, failing to record capitalized lease obligations

11 according to GAAP, lack of warehouse security, and lack of

12 documentation for sales, credit and collection policies; and

13 (h) In multiple conversations between Fenwick & West,

14 defendant Levy advised Fenwick & West that defendant Berman

15 intentionally withheld significant documents from auditors (July

16 26, 1993) and that "Berman is cavalier about everything" (late

17 June/early July 1993).

18 38. Handwritten notes made by Fenwick & West during Fenwick

19 & West's representation of the Company prior to the effective date

20 of the Registration Statement while they were conducting their due

21 diligence investigation state that Fenwick & West was concerned

22 with the accuracy of the Company's financial statements and

23 compliance with relevant securities laws.

24 39. The same handwritten notes also reflect that a key issue

25 is whether a new auditor can adequately deal with issues raised by

26 former auditors, Coopers & Lybrand, as " [t]hese local guys might

27 not be smart enough (i) to deal w/ the questions raised by the SEC

28 or (ii) to deal w/ fairness issues on California permit

- 40 -

1 application." In addition, these notes reflect concern about the

2 search for a new Chief Financial Officer to replace McMahon.'

3 40. On March 14, 1994, Amendment No. 1 to the Form SB-2 was

4 filed by the Company, again listing Fenwick & West as SEC counsel.

5 41. Throughout 1994, after interviews with and approval by

6 Fenwick & West, Access HealthNet hired at least four different

7 individuals to replace McMahon as Chief Financial Officer. On

8 three occasions, these individuals resigned shortly thereafter.

9 For example, Alan Geddes was hired in early July 1994, only to

10 resign on July 25, 1994. On July 25, 1994, Geddes told Fenwick &

11 West that his resignation was based, in part, upon the following:

12 (a) Berman's position on revenue recognition "is very aggressive;"

13 (b) Corbin & Wertz wants to write down revenue but Berman refuses;

14 (c) "[f]inancial systems are weak;" (d) Geddes "would not endorse

15 the numbers;" and (e) problems exist with customer satisfaction on

16 certain accounts due to an absence of customer support and

17 servicing.

18 42. On July 26, 1994, Corbin & Wertz informed Fenwick & West

19 that the auditors lacked enough information to verify numbers.

20 According to Corbin & Wertz, shipping records as well as other

21 records are "not very good," and signed lease contracts and revenue

22 confirmation letters was missing. As to revenue recognition,

23 Corbin & Wertz could not agree that revenue could be recognized

24 before the systems were installed when installation is significant

25 and occurs many months (or quarters) later. As to leasing

26 documentation, Berman rewrites leases without any documentation.

27

28 Coopers & Lybrand withdrew as Access HealthNet's auditor inSeptember 1993.

- 41 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Finally, when information is requested from the Company, it arrives

late and only raises more questions. The auditors tell Fenwick &

West that a " [p7 attern [is] evolving raisingquestions of what's

going on. "

43. On August 11, 1994, Corbin & Wertz again contacted

Fenwick & West asking for a legal opinion as to whether anti-fraud

rules have been violated and requesting a contingent liability note

allowing rescission of sale offer if a violation is found. As to

the March 31, 1994 audit, the audit still remains incomplete in

August 1994.

44. On August 19, 1994, Levy advised Fenwick & West that

Corbin & Wertz was "just about done" with the audit of the March

31, 1994 numbers.

45. On September 12, 1994, Levy and Fenwick & West discussed

the Company's on-going problems with hiring and retaining a Chief