Embed Size (px)

Citation preview

Banking industry between hope and fear – strong Q1 2012 performance

but market uncertainties remain

I ssue 1 | 11 Ap r i l 2012

K e y t o p i c s

/ The current economic environment is still unstable especially in Western Europe, but there are some positive signs from the US and BRICS countries (p. 2)

/ Reduction of market uncertainties as key driver for positive

performance (p. 5)

/ Market capitalisation of banks recovered significantly since the

end of 2011, especially US banks and national commercial

banks had a very good performance (p. 10)

2

Issue 1 11 April 2012

I. Global economic climate

Economic growth perspectives

In Q1 2012, the economic environment remains unstable and exhibits further divergence across the regions. Western European growth rates, including Germany’s, continued to decline with a weak outlook for the full year 2012. The US, however, continued their economic recovery showing promising GDP growth rates and a positive outlook for 2012/13. Forecasts for 2013 and economic sentiments indicate a more positive outlook for all major regions.

Fig. 1: GDP growth and forecasts (real GDP, year-over-year growth rates, in %)

Western Europe includes the euro area, Denmark, Norway, Sweden, Switzerland, United Kingdom. BRICS: Brazil, Russia, India, China, South Africa. Full

year data shown as long-term reference figures for comparative purposes. Q1 2012 data not yet available at the time of writing.

Source: Bloomberg, zeb/research

/ In Q4 2011, the recent trend of a three-speed world continued: whereas GDP growth rates in Western Europe and Germany fell for a third quarter in a row, the US economy continued their recovery and BRICS countries grow at a rate of 6.5-7.0%

/ The debt crisis will further hamper Western European economies, as forecasts see a stagnation of the GDP for 2012, which could worsen the situation for already stumbling European banks

Fig. 2: Change of GDP outlook (difference between GDP forecasts Q1 12 to Q4 11, in %p)

Source: Bloomberg, zeb/research

/ Current GDP forecasts for Western European economies for 2012 and 2013 were reduced by 0.2%p and 0.1%p compared to the forecasts from Q4 2011, underlining the current uncertainty

/ The outlook for Germany improved as GDP growth forecasts for 2012 increased by 0.3%p / Full year 2012 expectations for BRICS countries were adjusted downwards but remain on a high

level and are expected to improve in 2013 again

Forecasts for Western Europe substantially reduced

Economic downturn in Western Europe continues

0

2

4

6

8

10

12

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 FY11 FY12f FY13f

Germany

Western Europe

United States

BRICS

0.3

-0.2

0.1

-0.2

0.1

-0.1 -0.1

0.2

Germany Western Europe United States BRICS

∆ real GDP forecast FY12

∆ real GDP forecast FY13

3

Issue 1 11 April 2012

Fig. 3: Economic sentiments (ifo Business Climate Index – ifo Geschäftsklimaindex)

The ifo Business Climate Index is an indicator for economic activity based on a survey among companies about their current business situation and

outlook for the upcoming six months (2005 = 100). The ifo Institute only provides data for selected countries and regions. North America includes

Canada and the US, no separate data for BRICS countries available.

Source: ifo Institute for Economic Research, zeb/research

/ Western European business climate remained on a very low level, which underlines the pessimistic GDP expectations (fig. 1) for the region

/ Sentiments for Germany increased slightly, which may feed into upward adjustments to GDP forecasts in the coming months

/ North America currently shows a very promising development, which fosters the economic recovery started in 2011 and could be an early indicator of an even better GDP growth in 2012

Inflation and interest rates

Despite decreasing economic growth dynamics in Western Europe and Germany, the inflation rates are still significantly higher than in 2010. Also in the US, the inflation rate remains relatively high.

Fig. 4: Inflation rates and forecasts (annual change of average consumer prices, in %)

Q1 2012 data not yet available at the time of writing.

Source: Bloomberg, zeb/research

/ In Q4 2011, inflation rates in Western Europe and Germany continued to increase to almost 3%, but are predicted to decline especially in 2012 due to the expected economic downturn

/ In the US, the current inflation rate still exceeds 3% but it decreased slightly in Q4 2011 despite the faster US GDP growth

Global inflation outlook still positive

Sentiments exhibit positive trends

60

70

80

90

100

110

120

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

Germany

Western Europe

North America

World

0

1

2

3

4

5

6

7

8

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 FY11 FY12f FY13f

Germany

Western Europe

United States

BRICS

4

Issue 1 11 April 2012

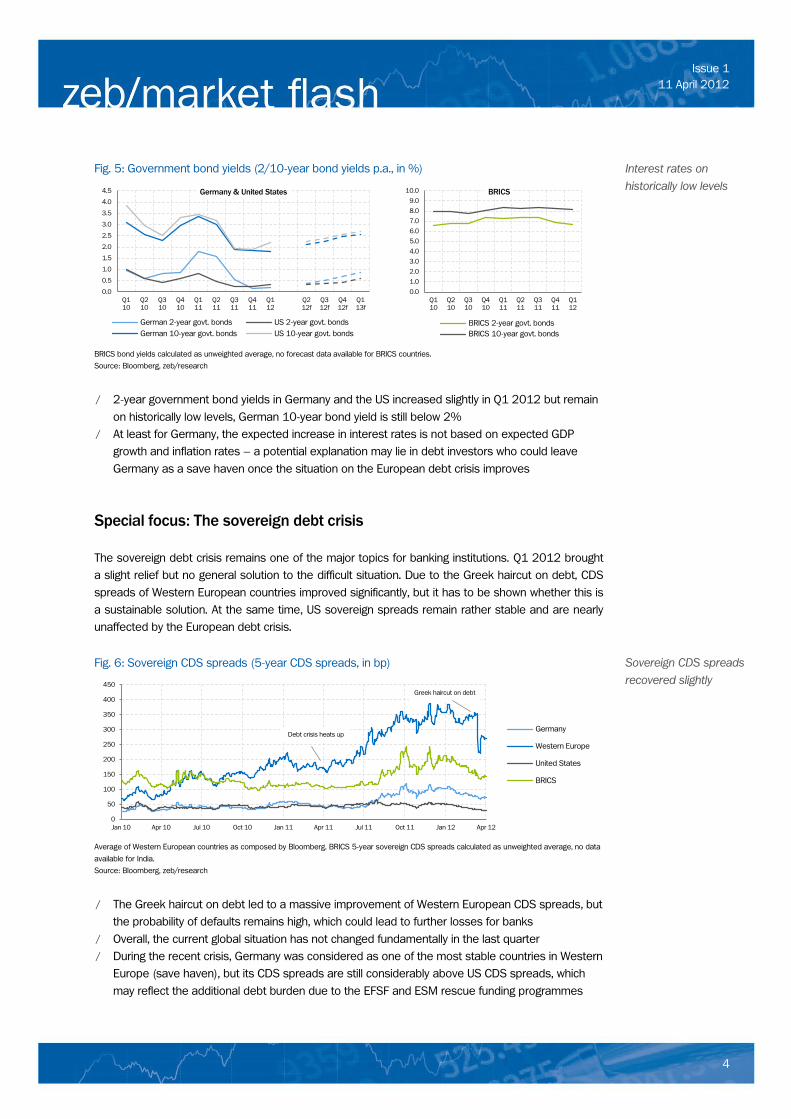

Fig. 5: Government bond yields (2/10-year bond yields p.a., in %)

BRICS bond yields calculated as unweighted average, no forecast data available for BRICS countries.

Source: Bloomberg, zeb/research

/ 2-year government bond yields in Germany and the US increased slightly in Q1 2012 but remain on historically low levels, German 10-year bond yield is still below 2%

/ At least for Germany, the expected increase in interest rates is not based on expected GDP growth and inflation rates – a potential explanation may lie in debt investors who could leave Germany as a save haven once the situation on the European debt crisis improves

Special focus: The sovereign debt crisis

The sovereign debt crisis remains one of the major topics for banking institutions. Q1 2012 brought a slight relief but no general solution to the difficult situation. Due to the Greek haircut on debt, CDS spreads of Western European countries improved significantly, but it has to be shown whether this is a sustainable solution. At the same time, US sovereign spreads remain rather stable and are nearly unaffected by the European debt crisis.

Fig. 6: Sovereign CDS spreads (5-year CDS spreads, in bp)

Average of Western European countries as composed by Bloomberg. BRICS 5-year sovereign CDS spreads calculated as unweighted average, no data

available for India.

Source: Bloomberg, zeb/research

/ The Greek haircut on debt led to a massive improvement of Western European CDS spreads, but the probability of defaults remains high, which could lead to further losses for banks

/ Overall, the current global situation has not changed fundamentally in the last quarter / During the recent crisis, Germany was considered as one of the most stable countries in Western

Europe (save haven), but its CDS spreads are still considerably above US CDS spreads, which may reflect the additional debt burden due to the EFSF and ESM rescue funding programmes

Interest rates on historically low levels

Sovereign CDS spreads recovered slightly

0

50

100

150

200

250

300

350

400

450

Jan 10 Apr 10 Jul 10 Oct 10 Jan 11 Apr 11 Jul 11 Oct 11 Jan 12 Apr 12

Germany

Western Europe

United States

BRICS

Debt crisis heats up

Greek haircut on debt

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12f

Q3 12f

Q4 12f

Q1 13f

Germany & United States

German 2-year govt. bonds US 2-year govt. bonds German 10-year govt. bonds US 10-year govt. bonds

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

BRICS

BRICS 2-year govt. bonds BRICS 10-year govt. bonds

5

Issue 1 11 April 2012

Fig. 7: Sovereign refinancing needs (bonds and loans outstanding with maturity 2012/13, in % of nominal GDP)

Figure contains only currently outstanding bonds and loans, without net new borrowings.

Source: Bloomberg, zeb/research

/ As of 30 March 2012, the US and Italy have the highest refinancing needs among the countries considered, with refinancing needs of 16.8% of their nominal GDP in 2012

/ Average BRICS refinancing needs are well below the levels of the other countries considered

II. Key banking drivers

Selected capital market indicators

Capital markets calmed down in Q1 2012. Especially the volatilities of stock markets declined significantly. In the currency markets, the steady depreciation of the euro against the US dollar and BRICS currencies stopped.

Fig. 8: Stock market volatilities (in bp)

The BRICS volatility index is calculated as unweighted average of CBOE Brazil Volatility Index, Russian Volatility Index, India NSE Volatility Index,

AlphaShares Chinese Volatility Index, JSE Securities South African Volatility Index.

Source: Bloomberg, zeb/research

/ Current market volatilities on mature European and US capital markets returned to their Q1/Q2 2011 level, before the European debt crisis caused a significant volatility jump in mid-2011

/ The Euro Stoxx volatility has reached the average BRICS volatility especially in the second half of the sample

The US and Italy have the highest refinancing needs in 2012

Lower market volatilities

0

10

20

30

40

50

60

Jan 10 Apr 10 Jul 10 Oct 10 Jan 11 Apr 11 Jul 11 Oct 11 Jan 12 Apr 12

Mature capital markets

Euro Stoxx 50 Vola Index VIX (S&P 500) 0

10

20

30

40

50

60

Jan 10 Apr 10 Jul 10 Oct 10 Jan 11 Apr 11 Jul 11 Oct 11 Jan 12 Apr 12

BRICS

6.3

12.3

16.8

11.3

16.8

3.4

6.5 8.2

11.6

9.4 9.1

2.1

Germany Portugal Italy Spain United States BRICS

2012 2013

6

Issue 1 11 April 2012

Fig. 9: FX rates (EUR/USD, EUR/BRICS basket)

EUR/BRICS basket represents a custom index of EUR/BRL, EUR/RUB, EUR/INR, EUR/CNY and EUR/ZAR exchange rates. Individual exchange rates are

indexed by 1/1/2010. The basket is then calculated as an unweighted average of individual exchange rate indices.

Source: Bloomberg, zeb/research

/ Compared to the US dollar, the euro was able to recover in Q1 2012, after suffering a strong depreciation between April 2011 and January 2012 due to the debt crisis

/ At the end of Q1 2012, EUR/BRICS-rate increased again, reverting the depreciation of the euro which started in November 2011 – overall the impact of the debt crisis has been less severe as risk-averse investors are more likely to move their funds to the US instead of the BRICS countries

Funding costs and margins

The interbank funding situation of banks improved steadily in Q1 2012. Especially the short-term spread curve decreased noticeably. In the euro area, deposits interest rates for private customers continued to increase strongly, whereas loan interest rates declined further.

Fig. 10: Interbank market rates (interbank offered rates and overnight indexed swaps)

Source: Bloomberg, zeb/research

9M 3M

Euro able to stabilise valuation

Interbank funding situation improved

1D 6M 1Y 2Y 3Y 4Y 5Y 10Y

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

Jan 10 Apr 10 Jul 10 Oct 10 Jan 11 Apr 11 Jul 11 Oct 11 Jan 12 Apr 12

EUR/USD

0.85

0.90

0.95

1.00

1.05

Jan 10 Apr 10 Jul 10 Oct 10 Jan 11 Apr 11 Jul 11 Oct 11 Jan 12 Apr 12

EUR/BRICS

0.0

0.5

1.0

1.5

2.0

2.5 Money market curves (as of 30/3/2012, in %)

EUR OIS USD OIS EURIBOR (Swap) LIBOR (Swap)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Jan 10 Apr 10 Jul 10 Oct 10 Jan 11 Apr 11 Jul 11 Oct 11 Jan 12 Apr 12

Spread of interbank offered rates over OIS rates (in %p)

EURIBOR/EUR OIS spread (3M)

LIBOR/USD OIS spread (3M)

7

Issue 1 11 April 2012

/ On 30 March 2012, EURIBOR and LIBOR curves still were unusually steep and well above corresponding EUR and USD OIS curves, indicating that banks still see a high probability of defaults in the interbank market and therefore prefer interest rate swaps over interbank lending

/ Nevertheless, the 3-month spreads declined significantly in Q1 2012 (almost -0.6%p in the euro interbank system) confirming previous findings that markets calmed down after the turmoil in the second half of 2011

Fig. 11: Deposits and loans interest rates in the euro area (new business rates) and EURIBOR (in %)

Source: European Central Bank, zeb/research

/ In Q1 2012, the competition for customer deposits as a cheap and stable funding source intensified further, leading to increasing deposits interest rates for households and lower margins for banks

/ For households, mortgage loans rate almost remained on previous quarter’s level / Corporate deposit and lending margins remain stable, as corporate interest rates followed the

reference rate closely

Investment banking activities

The investment banking industry profits from an increased total market volume regarding corporate bond issuances and equity offerings, leading to increased fee pools and earnings, respectively. In contrast, financial advisory related to M&A continued the downward trend of recent quarters.

Fig. 12: Corporate bonds issuance business by home region of issuing company

Retail margins narrow

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

Households

Deposits (≤ 1Y) Mtg. loans (1Y-5Y)

EURIBOR (3M)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

Corporates

Deposits (≤ 1Y) Loans (1Y-5Y)

EURIBOR (3M)

Significant increase in bonds issuances

275 147 188 140

257 197 103 98

317

130

85 148

127

145 131

100 103

173 49

45

66

40

56 70

49 97

85 96

89

128

115

124 108

80 107

166 551

366

531

422

582 507

331 405

741

0

100

200

300

400

500

600

700

800

900

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

Total volume of corporate bond issuances (in EUR bn)

Western Europe United States BRICS Others T

8

Issue 1 11 April 2012

Fee volume (left-hand axis) and global average fee rate (right-hand axis) are estimated based on offering volume and volume-weighted average of all

available fees.

Source: Bloomberg, zeb/research

/ In Q1 2012, the volume of global corporate bond issuances increased to EUR 741 bn, a level well above recent quarters and first quarters of 2010 (+27.4%) and 2011 (+34.5%)

/ Especially Western European companies more than tripled their funding activity regarding corporate bonds after low issuance volumes in 2011 – this reflects a growing investor appetite for European corporate bonds since European sovereign debt exhibited either low interest rates or elevated risk levels

/ The global average fee rate has been rather stable in recent quarters, therefore the growth in banks’ fee earnings is primarily driven by the business volume effect

Fig. 13: Equity offering business by home region of issuing company

Equity offering business includes initial public offerings and additional equity listings. Fee volume (left-hand axis) and global average fee rate (right-hand

axis) are estimated based on offering volume and volume-weighted average of all available fees.

Source: Bloomberg, zeb/research

/ Volume of global equity business denoted an increase of EUR 32 bn to EUR 83 bn in Q1 2012, mainly driven by US and Western European customers – but level of previous year’s quarter (Q1 2011) could not be reached

Equity offering business stops downward trend

1.3 0.7 1.0 0.7 1.0 0.9

0.4 0.5

1.4

0.8

0.6 1.0

0.8 0.8

0.8

0.6 0.6

1.1 0.2

0.2

0.4

0.2 0.2 0.3

0.2 0.5

0.4 0.5

0.4

0.7

0.6 0.5 0.5

0.4 0.5

0.8 2.8

2.0

3.0

2.3

2.6 2.5

1.6 2.1

3.7

0.35

0.40

0.45

0.50

0.55

0.60

0

1

2

3

4

5

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

Fee volume (in EUR bn) and global average fee (in %)

Western Europe United States BRICS Others T Global avg. fee (%)

15 8 6 21 20 18 9 5 14 21 25 18

55 39 39

13 18 35

24 21 60

39

23 20

18 11

10 33 27

28

67

30 23

15 16

23

93 81

111

182

111 100

55 51

83

0

50

100

150

200

250

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

Total volume of global equity offerings (in EUR bn)

Western Europe United States BRICS Others T

0.5 0.3 0.2 0.5 0.7 0.5 0.2 0.2 0.5

0.9 1.1 0.7

1.4 1.3 1.3

0.5 0.8 1.2

0.7 0.8 1.2

1.2 1.0 0.8

0.6 0.5

0.5 1.1 0.8 0.9

1.8 1.1

0.7

0.5 0.6

0.9

3.2 3.0 3.0

5.0

4.1

3.3

1.9 2.0

3.1

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0

1

2

3

4

5

6

7

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

Fee volume (in EUR bn) and global average fee (in %)

Western Europe United States BRICS Others T Global avg. fee (%)

9

Issue 1 11 April 2012

/ The volume effect is damped by a slight decrease in the average fee – nevertheless the global fee volume of financial institutions grew significantly

Fig. 14: Deal volume of M&A business by home region of acquired company (in EUR bn)

Category “Others“ includes all M&A transactions with target companies from regions different than those specified and deals with targets in multiple

regions not further specified. All transactions classified by announcement date.

Source: Bloomberg, zeb/research

/ M&A activity further declined in Q1 2012 – global M&A volume dropped to EUR 277 bn, which is in line with global sentiments (fig. 3) as these typically lead M&A activity by a few months

/ The decrease in volume continues the downward trend, which first affected BRICS countries in Q1 2011 and later the Western European and US markets in Q3 2011

/ Given the recent increase of sentiments, M&A activities are likely to pick up in the next quarters

III. State of the banking industry

Market valuation

The banking sector looks back at a very good quarter in terms of market valuation. Market capitalisation is now significantly higher than in Q3 2011, when the debt crisis hit banks very hard. With regard to business models, it is remarkable that national commercial banks are still valued higher than international banks or banks with a high share of investment banking. In Q1 2012, this has not changed fundamentally.

Fig. 15: Market capitalisation of the banking sector (end of quarter, in EUR tr)

All banks include all banks worldwide according to Bloomberg classification. Global top 100 banks contain largest banks by market capitalisation.

Source: Bloomberg, zeb/research

Market valuation of banks improved further

M&A business continues to decline

54 49 56 65 78 91 50 48 54

74 91 94 89 91 106

77 73 62

31 38 58 66 41 46

38 34 34

140 132

183 221

165 156

166 150 126

299 310

391 441

374 398

331 304

277

0

100

200

300

400

500

600

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

Western Europe United States BRICS Others T

4.3 4.1

4.3 4.6 4.5

4.2

3.6 3.8

4.3

3.2 3.0 3.2

3.4 3.3 3.1

2.6 2.8

3.2

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

All banks Global top 100

10

Issue 1 11 April 2012

/ In Q1 2012, the global banking industry continued its recovery from the downturn in the second half of 2011

/ With EUR 3.2 tr (+13.7%) and EUR 4.3 tr (+13.0%), respectively, market capitalisation of global top 100 institutions and all banks reached pre-sovereign debt crisis levels again in Q1 2012

Fig. 16: Market capitalisation of global top 100 banks by region (in EUR tr)

Source: Bloomberg, zeb/research

/ On average, especially Western European banks were hit hard by the market turmoil in Q3 2011, but since the beginning of 2012, they were able to increase their valuation again despite the relatively problematic economic environment in Western Europe

/ Within the last two years the relative weights have changed: Global top 100 banks from BRICS countries as a group now have the highest market capitalisation whereas Western European and US banks are now on the same level

Fig. 17: Price-to-book ratio of global top 100 banks

Diversified banking institutions generate more than 30% of their earnings from investment banking/trading/non-classic banking activities, international

commercial banks generate more than 70% of their earnings from classic banking in culturally different types of international markets, commercial

banks from mature/growing markets generate more than 70% of their earnings from classic banking activities in their respective market type.

Source: Bloomberg, zeb/research

/ Based on the recent recovery of the capital markets, the price-to-book ratio of all banks improved across business models and regions

/ In Q1 2012, the price-to-book ratio especially of financial institutions from the US continued to improve, which can be linked to the macroeconomic development in recent quarters

/ In spite of these developments, the last quarter brought no change to the general differences between price-to-book ratios of business models, as capital markets still favour national commercial banks and their stable customer deposits funding base and less volatile business

National commercial banks have highest valuation

Regional weights in market capitalisation have shifted

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

Western Europe

United States

BRICS

0.0

0.5

1.0

1.5

2.0

2.5

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

By region

Western Europe United States BRICS

0.0

0.5

1.0

1.5

2.0

2.5

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

By business model

Div. banking inst. Int. comm. banks Comm. banks (mat. m.) Comm. banks (grow. m.)

11

Issue 1 11 April 2012

Equity performance

The equity performance of banks was very promising in the first quarter of 2012. However, on an annual basis, the average total shareholder return (TSR) of banks is still well behind other sectors. Within the banking sector, commercial banks have the best TSR performance, whereas Western European banks rank last with strongly negative TSRs.

Fig. 18: Total shareholder return of industry sectors worldwide (in %)

Total shareholder return of industry sectors based on global sector total return indices, aggregated and provided by Datastream.

Source: Datastream, zeb/research

/ In Q1 2012, the banking industry profits from the recovery of the capital markets, the Greek haircut on debt and the corresponding ECB interventions, achieving the second best total shareholder return performance among all industry sectors

/ Nevertheless, based on a one year moving average, the TSR of banking institutions is still negative with -12.9%

Fig. 19: Total shareholder return of global top 100 banks (4/2011-3/2012, in %)

Average total shareholder returns are weighted by the market capitalisation of each bank.

Source: Bloomberg, zeb/research

/ The global top 100 banks achieved a TSR of -6.2% over the last year, with -20.7% institutions from Western Europe clearly rank last (on average) among all regions

/ As seen before, banks from the US and BRICS as well as national commercial banks performed best among the global top 100 banks

-6.2

1.1

-4.5

-10.5

-23.6

Global top 100

Comm. banks (mat. m.)

Comm. banks (grow. m.)

Div. banking inst.

Int. comm. banks

By business model

Banks among top industry sectors in Q1 2012

National commercial banks lead TSR ranking

11.5

11.5

10.3

8.8

0.2

-4.8

-8.1

-8.9

-12.9

-18.6

Technology

Health care

Consumer goods

Consumer services

Telecommunications

Industrials

Utilities

Oil and gas

Banks

Basic materials

One year (4/2011-3/2012)

20.8

18.0

14.6

13.4

11.9

10.9

7.6

7.5

4.8

4.7

Technology

Banks

Industrials

Consumer goods

Consumer services

Basic materials

Oil and gas

Health care

Telecommunications

Utilities

Q1 2012 (4/2011-3/2012)

-6.2

-20.7

-2.4

-8.7

4.2

Global top 100

Western Europe

United States

BRICS

Others

By region

12

Issue 1 11 April 2012

Fig. 20: Top/low TSR performers among global top 100 banks (4/2011-3/2012, in %)

Global

Top performers Country TSR Low performers Country TSR

Siam Commercial Bank PCL Thailand 36.3

UniCredit SpA Italy -66.7

Credicorp Ltd Peru 28.2

Credit Agricole SA France -58.0

FirstRand Ltd South Africa 27.1

Societe Generale SA France -50.1

Kasikornbank PCL Thailand 23.6

Lloyds Banking Group PLC Britain -42.2

Nedbank Group Ltd South Africa 22.8

CaixaBank Spain -39.3

Western Europe

Top performers Country TSR Low performers Country TSR

Svenska Handelsbanken AB Sweden 6.7

UniCredit SpA Italy -66.7

Swedbank AB Sweden 0.0

Credit Agricole SA France -58.0

Standard Chartered PLC Britain -0.1

Societe Generale SA France -50.1

Deutsche Bank AG Germany -8.6

Lloyds Banking Group PLC Britain -42.2

HSBC Holdings PLC Britain -8.9

CaixaBank Spain -39.3

Source: Bloomberg, zeb/research

/ To no surprise, banks with the lowest TSR performance between April 2011 and March 2012 are exclusively located in Western European countries, whereas all top performers are from emerging markets

/ The list of top TSR performers in Western Europe is dominated by banks from Northern Europe – it has to be noted however, that Svenska Handelsbanken is actually the only bank that created value for its shareholders in the last twelve months

Fig. 21: RoE after taxes and yearly RoE forecast changes of global top 100 banks (in %)

Western European banks lead list of low performers

Global profitability outlook for banks revised downwards

By region

(9.2) (10.7) (11.2)

7.5

4.8 6.9

8.1

FY10 FY11f FY12f FY13f

Western Europe

(11.4) (12.4) (12.7)

10.8 10.4 10.2 10.8

FY10 FY11f FY12f FY13f

Global top 100

(17.4) (17.8) (17.7) 20.4

21.3

17.5 17.1

FY10 FY11f FY12f FY13f

BRICS

(8.4) (9.8) (10.1)

6.6 6.8 7.3 8.1

FY10 FY11f FY12f FY13f

United States Est. 31/3/2011

Est. 31/3/2012

13

Issue 1 11 April 2012

Figure compares different consensus forecasts of return on equity of global top 100 banks based on market capitalisation. Forecasts are calculated as

equity-weighted averages of analysts’ consensus forecasts as available in Bloomberg.

Source: Bloomberg, zeb/research

/ The changes in RoE forecasts overall have a downward trend but are very heterogeneous across regions and business models

/ Forecasts for BRICS countries and commercial banks in growing markets were high already and further improved

/ Forecasts especially for international commercial banks and banks in Western Europe were significantly reduced, which is in line with our previous findings

Debt perspective

Despite the recent recovery described above, the credit quality of banks themselves remains unstable. Banks’ CDS spreads have improved in Q1 2012 but are still on an elevated level and the number of rating downgrades has been abnormally high in the last two quarters.

Fig. 22: CDS spreads of global top 100 banks (avg. 5-year CDS spreads, in bp)

CDS spreads decrease but remain on high level

By business model

(8.2) (9.9) (10.7)

6.4

2.9 6.0

7.5

FY10 FY11f FY12f FY13f

International commercial banks

(16.8) (17.2) (17.3) 19.6

20.4

16.8 16.6

FY10 FY11f FY12f FY13f

Commercial banks (grow. markets)

(9.1) (10.2) (10.4)

7.4 6.5 7.2 8.0

FY10 FY11f FY12f FY13f

Diversified banking institutions

0

50

100

150

200

250

300

350

400

450

500

Jan 10 Apr 10 Jul 10 Oct 10 Jan 11 Apr 11 Jul 11 Oct 11 Jan 12 Apr 12

By region

Western Europe

United States

BRICS

(10.9) (11.9) (12.2)

9.7 10.1 10.5 11.0

FY10 FY11f FY12f FY13f

Commercial banks (mat. markets)

Est. 31/3/2011

Est. 31/3/2012

14

Issue 1 11 April 2012

5-year CDS spreads are calculated as unweighted average of CDS spreads of each bank.

Source: Bloomberg, zeb/research

/ In Q1 2012, CDS spreads of global top 100 banks decreased substantially but remain on elevated levels

/ Overall, investors have started to differentiate across business models in the last two years – whereas CDS spreads of all business models except for the banks in growing markets had almost identical spreads in January 2010 there is now a substantial differentiation with international commercial banks having even higher CDS spreads than the average commercial bank in a growing market

Fig. 23: Rating changes of global top 100 banks

Rating changes consider number of upward and downward revisions of long-term rating of global top 100 banks as provided by Standard & Poor’s,

Moody’s, Fitch Ratings. Outlook revisions are excluded. Up-to-downgrade ratio (right-hand axis) is a harmonised index calculated as (number of

upgrades – number of downgrades) / sum of upgrades and downgrades.

Source: Bloomberg, zeb/research

/ The number of rating downgrades has reached record levels in the last two quarters – taken together more than 60 downgrades occurred

/ For the entire year 2011, the up-to-downgrade ratio has been below zero, which indicates that there is substantial uncertainty in the market concerning the stability and business perspective of banks

Rating downgrades dominate

0

50

100

150

200

250

300

350

400

450

500

Jan 10 Apr 10 Jul 10 Oct 10 Jan 11 Apr 11 Jul 11 Oct 11 Jan 12 Apr 12

By business model

Div. banking inst.

Int. comm. banks

Comm.banks (mat. m.)

Comm.banks (grow. m.)

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

0

5

10

15

20

25

30

35

40

45

50

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

Upgrades Downgrades Up-to-downgrade ratio

15

Issue 1 11 April 2012

About zeb/market flash

The zeb/market flash is a quarterly compilation of market data putting the total shareholder return (TSR) performance of the global banking industry, economic fundamentals and key value drivers into perspective. It is published by zeb/rolfes.schierenbeck.associates. All data and calculations of this issue are based on the due date 2 April 2012.

zeb/rolfes.schierenbeck.associates is a management consultancy specialising in the financial services sector with thirteen offices in Germany (Berlin, Frankfurt, Hamburg, Munich, Münster, Ulm), Austria (Vienna), Switzerland (Zurich), Luxembourg, Poland (Warsaw), the Czech Republic (Prague), Ukraine (Kiev) and Hungary (Budapest). With more than 750 employees and several subsidiaries, zeb/ is among the leading consulting firms for banks, insurance companies and other financial service providers.

For more information: www.zeb.de

Contact

Dr. Dirk Holländer Partner Hammer Straße 165 D-48153 Münster Phone +49.251.97128.182 Fax +49.251.97128.101 E-mail [email protected]

Volker Abel Senior Manager Taunusanlage 19 D-60325 Frankfurt am Main Phone +49.69.719153.453 Fax +49.69.719153.410 E-mail [email protected]

Oliver Rosenthal Head of Research Hammer Straße 165 D-48153 Münster Phone +49.251.97128.135 Fax +49.251.97128.101 E-mail [email protected]