Embed Size (px)

Citation preview

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 1/13

Economic outlook, Germany

2 July 2010

Please direct inquiries, if any, to:

Tina Winther Frandsen, Senior Macroeconomic Analyst

+

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 2/13

Summary - Germany

Prospect of fair growth just below 2% this year and in 2011• Exports will have greater importance as engine for the economy while the fiscal

policy will have an adverse effect as of 2011. We expect that private consumption and investment.

• The inflationary pressure is moderate and interest rates will remain low. We expect the firstmoderate hike from the ECB in June 2011.

• The drastic easing of the fiscal and monetary policies helped pull the German economy out of the

deep recession and continued fiscal easing will support the economy throughout 2010.

• However, as of 2011, the situation will be different because the fiscal policy will be tightened to.

private consumption and investment. The tightening measures will be moderate in 2011 but willincrease over the next years.

• Germany's economy is highly dependent on exports that account for about 40% of GDP. We

expect that for the period ahead, exports will be lifted by a continued improvement of the world

economy and significant depreciation of the euro.

Private consumption and investment will soon pick up• Investment has fallen sharply but we expect it to turn around very soon. There are, however, only

prospects of moderate rises.

-

private consumption is still weak. However, the adverse effect from the labour market has abated.Wage growth will stay very low, and combined with continued uncertainty and fiscal tightening asof 2011, this means that we only expect a small increase in private consumption in future.

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 3/13

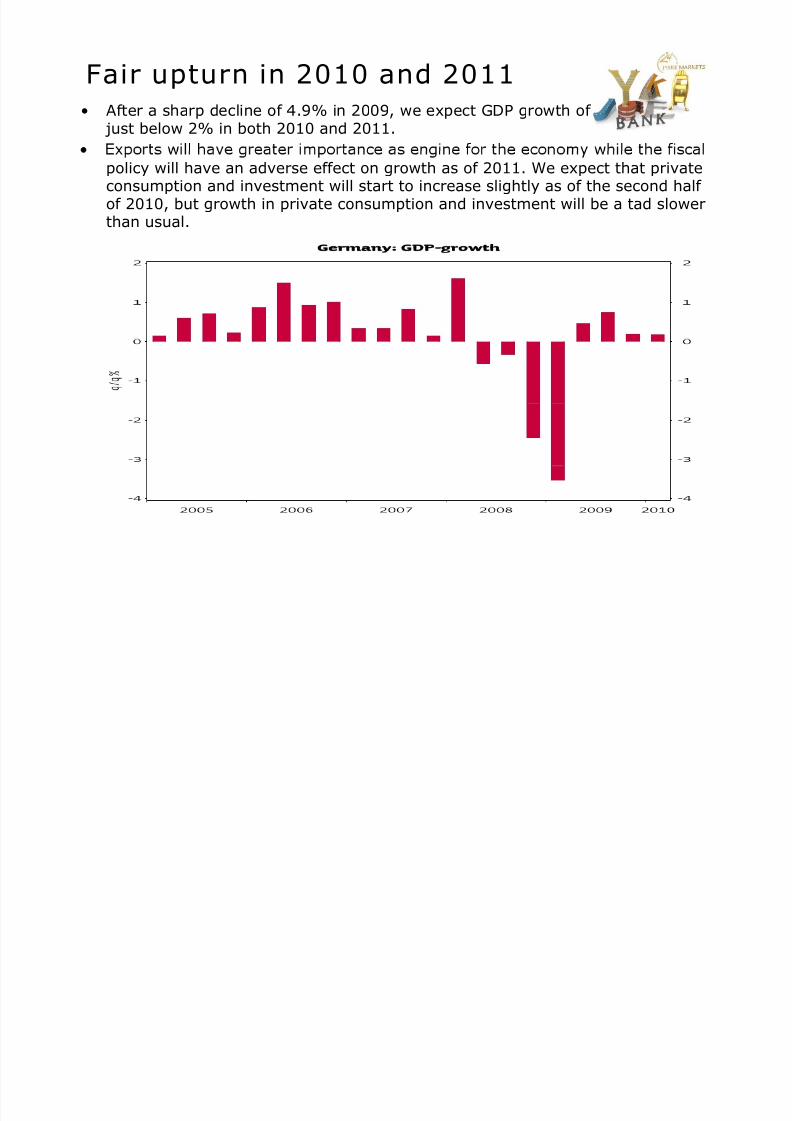

Fair upturn in 2010 and 2011

• After a sharp decline of 4.9% in 2009, we expect GDP growth of just below 2% in both 2010 and 2011.

policy will have an adverse effect on growth as of 2011. We expect that privateconsumption and investment will start to increase slightly as of the second half of 2010, but growth in private consumption and investment will be a tad slowerthan usual.

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 4/13

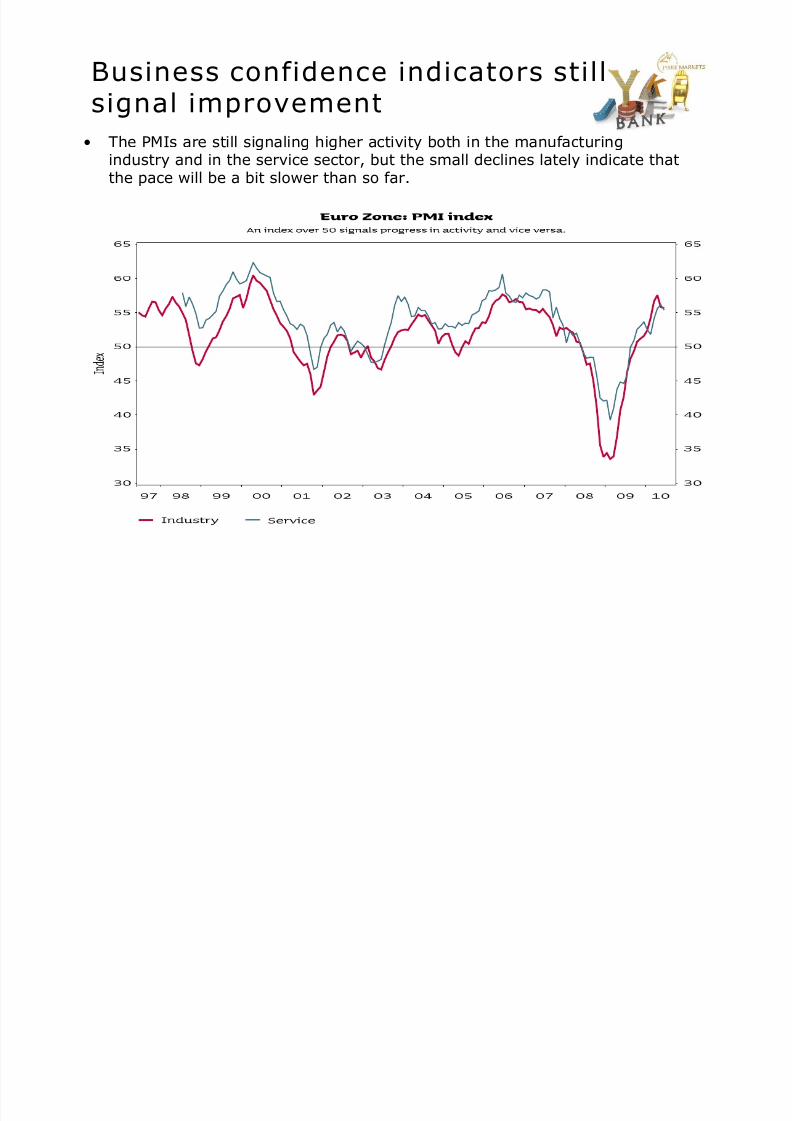

Business confidence indicators still

signal improvement• The PMIs are still signaling higher activity both in the manufacturing

industry and in the service sector, but the small declines lately indicate thatthe pace will be a bit slower than so far.

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 5/13

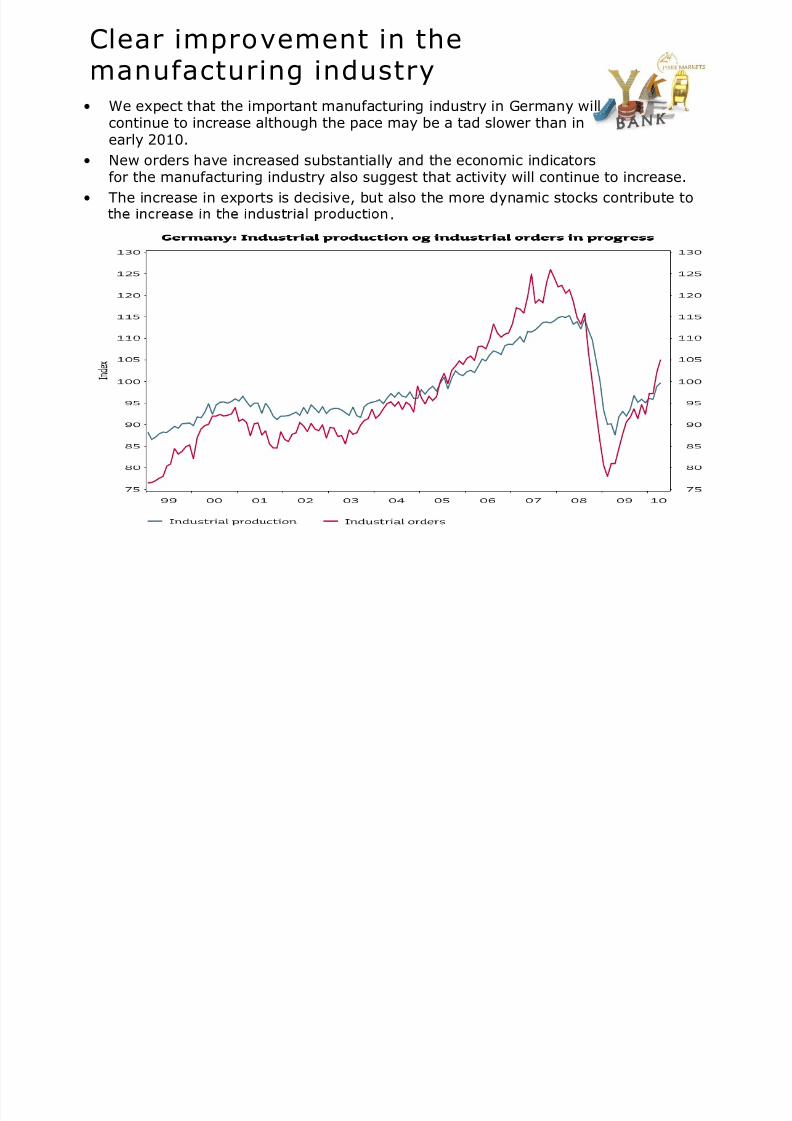

Clear improvement in themanufacturing industry

• We expect that the important manufacturing industry in Germany willcontinue to increase although the pace may be a tad slower than inearly 2010.

• New orders have increased substantially and the economic indicatorsfor the manufacturing industry also suggest that activity will continue to increase.

• The increase in exports is decisive, but also the more dynamic stocks contribute to.

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 6/13

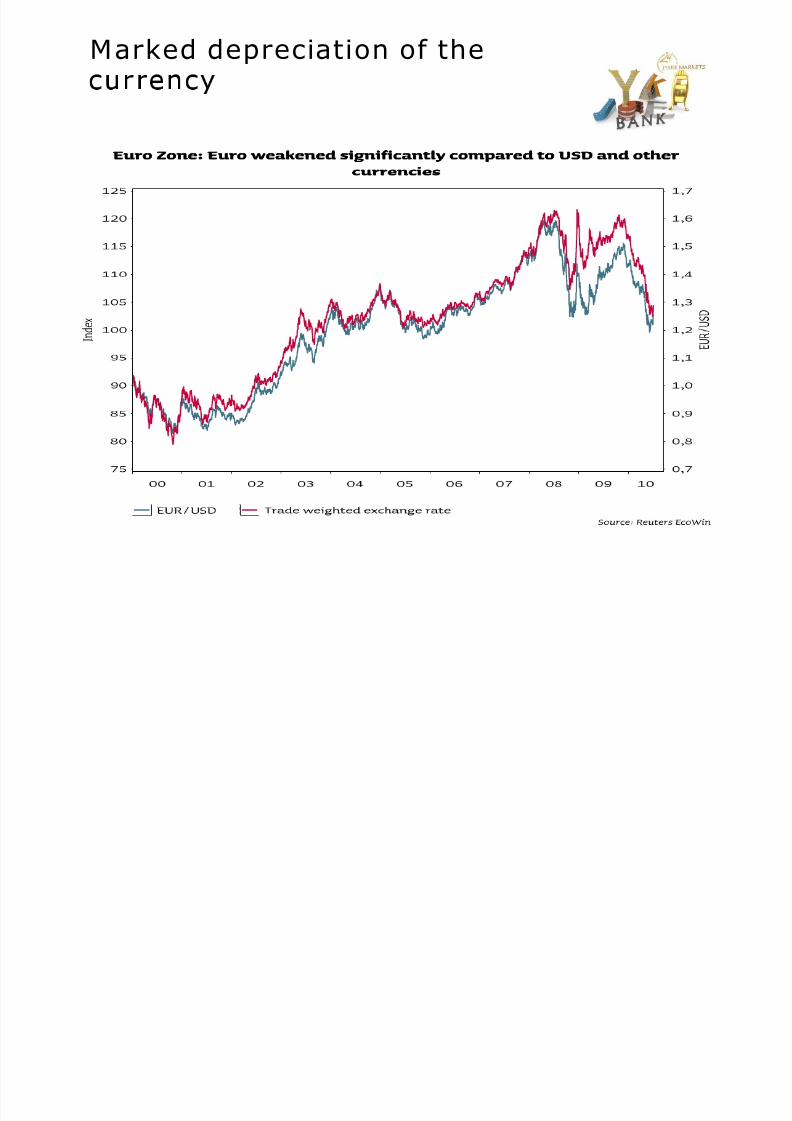

Ex orts on the increase

• Germany's economy is highly dependent on exports thataccount for about 40% of GDP.

significant depreciation of the euro.

• We expect that exports will go on increasing, and thus contribute to gettingthe German econom oin in future.

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 7/13

Marked depreciation of the

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 8/13

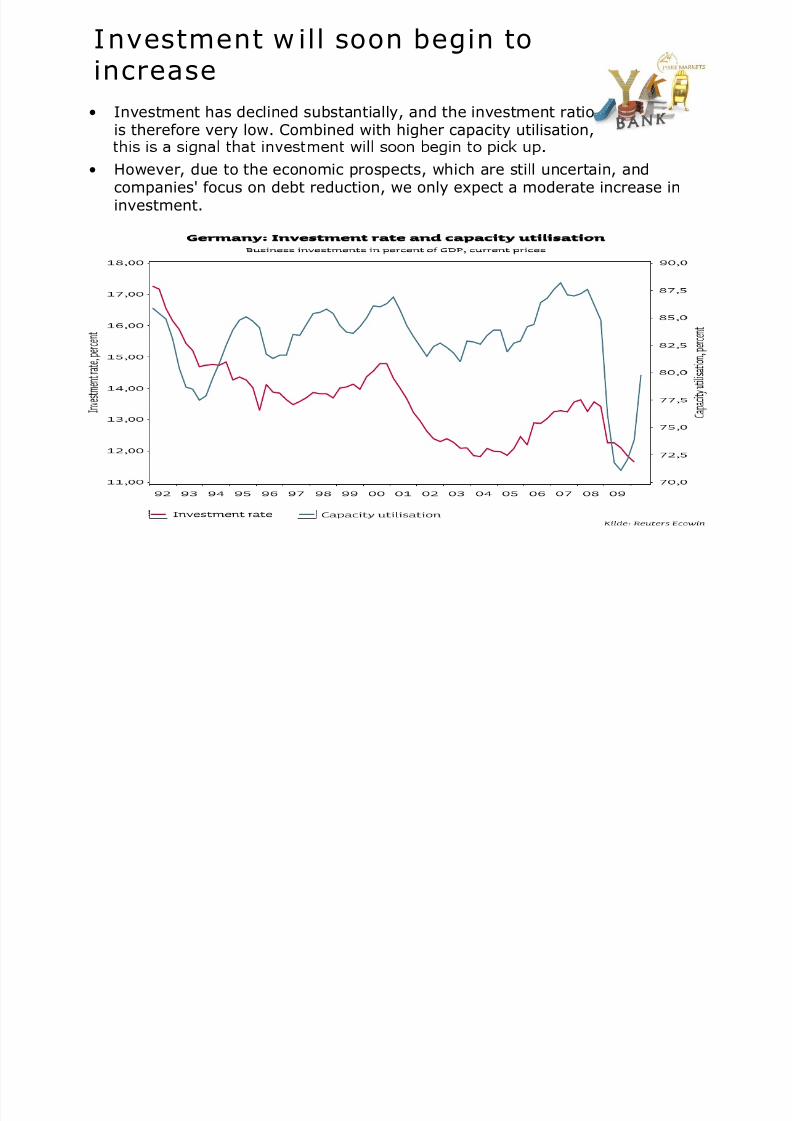

Investment w ill soon begin toincrease

• Investment has declined substantially, and the investment ratiois therefore very low. Combined with higher capacity utilisation,

• However, due to the economic prospects, which are still uncertain, andcompanies' focus on debt reduction, we only expect a moderate increase ininvestment.

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 9/13

Private consumption is still weak• Consumers have been through a very hard period, but now it

seems that retail sales are stabilising.

• The adverse effect from the labour market will abate but wa e rowth willstay very low, and combined with continued uncertainty and fiscal tighteningas of 2011, this means that we only expect a small increase in private

consumption for the period ahead.

• In advance, the German consumers are well-known for being eager to save.

3 month gliding average

Germany: Retailsales (ex. autos and gas)

101,0101,0

Percent of disposible income

Germany: Savings rate

11,75

99,5

100,0

100,5

99,5

100,0

100,5

11,25

11,50

98 0

98,5

99,0

I n d e x

98 0

98,5

99,0

P e r c e n t

10,75

11,00

97,0

97,5

97,0

97,5

10,25

10,50

Source: Reuters EcoWin

2003 2004 2005 2006 2007 2008 2009 2010

96,0

96,5

96,0

96,5

Source: Reuters EcoWin

2003 2004 2005 2006 2007 2008 2009

10,00

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 10/13

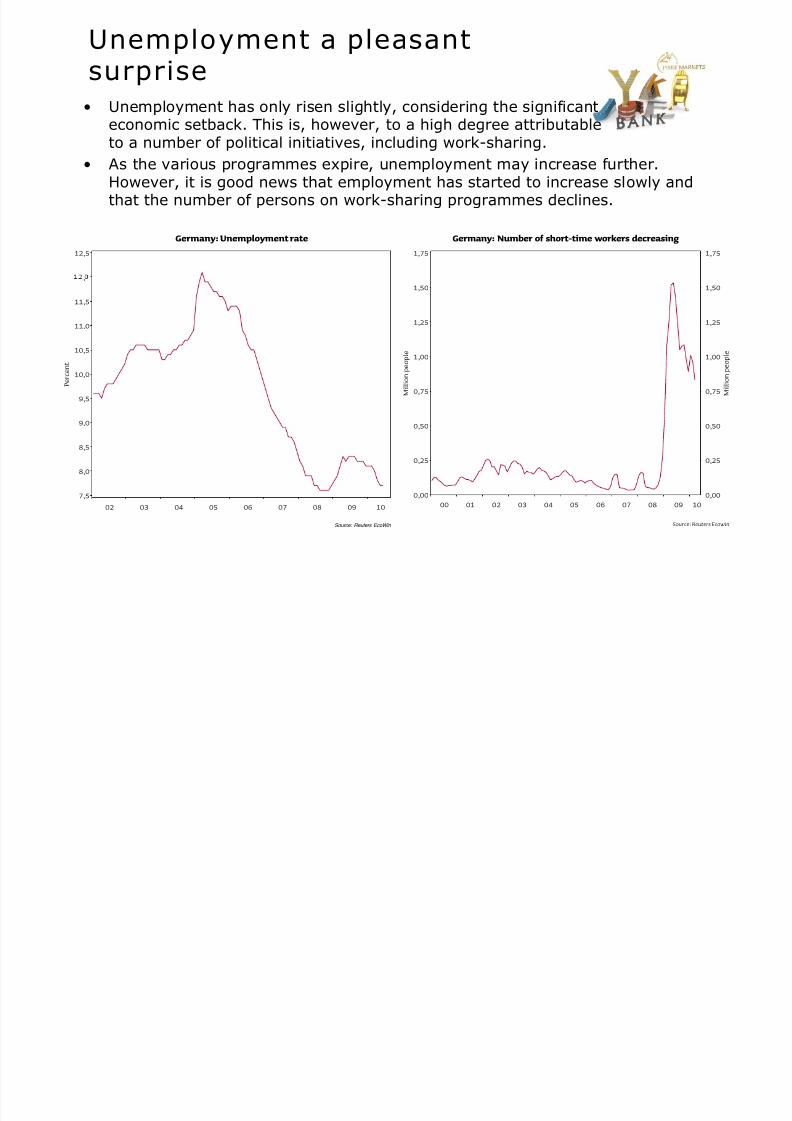

Unemployment a pleasantsurprise

• Unemployment has only risen slightly, considering the significanteconomic setback. This is, however, to a high degree attributableto a number of political initiatives, including work-sharing.

• As the various programmes expire, unemployment may increase further.However, it is good news that employment has started to increase slowly and

that the number of persons on work-sharing programmes declines.

Germany: Unemployment rate

12,5

Germany: Number of short-time workers decreasing

1,751,75

11,0

11,5

,

1,25

1,50

1,25

1,50

P e r c e n t

9,5

10,0

10,5

M

i l l i o n p e o p l e

0,75

1,00

M

i l l i o n p e o p l e

0,75

1,00

8,5

9,0

0,25

0,50

0,25

0,50

Source: Reuters EcoWin

02 03 04 05 06 07 08 09 10

7,5

8,0

Source: Reuters Ecowin

00 01 02 03 04 05 06 07 08 09 10

0,000,00

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 11/13

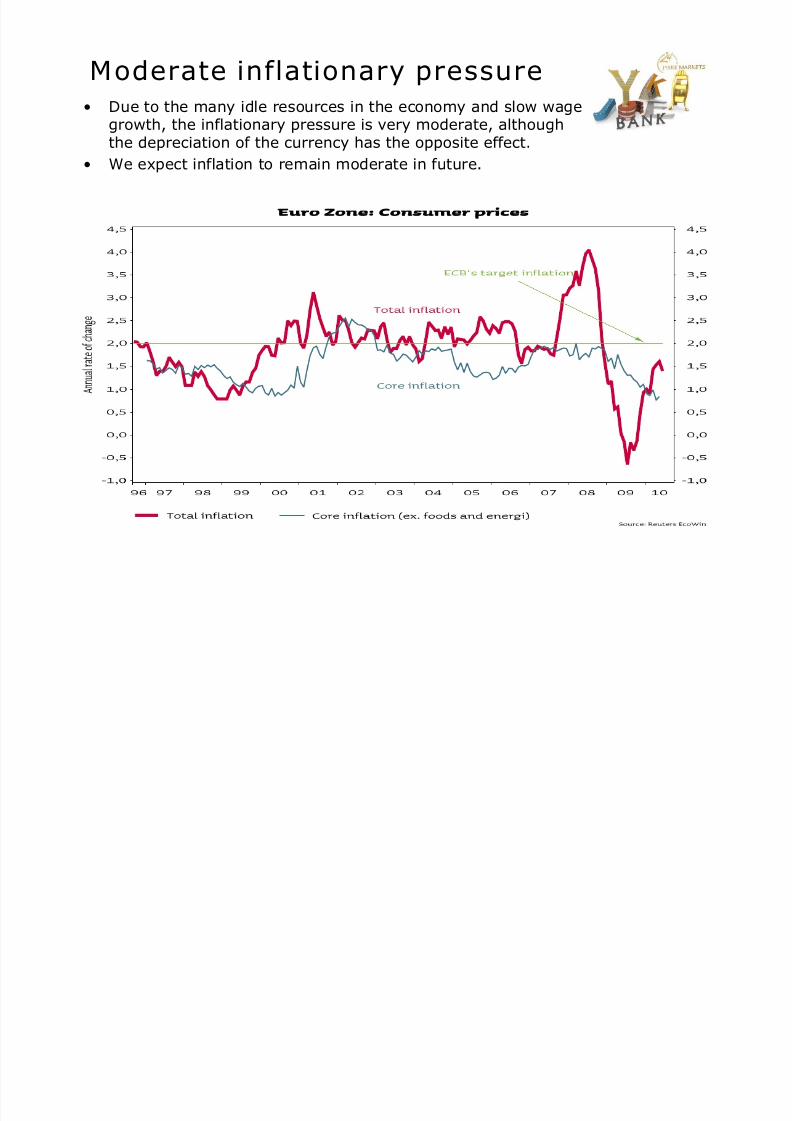

Moderate inflationary pressure

• Due to the many idle resources in the economy and slow wagegrowth, the inflationary pressure is very moderate, althoughthe depreciation of the currency has the opposite effect.

• We expect inflation to remain moderate in future.

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 12/13

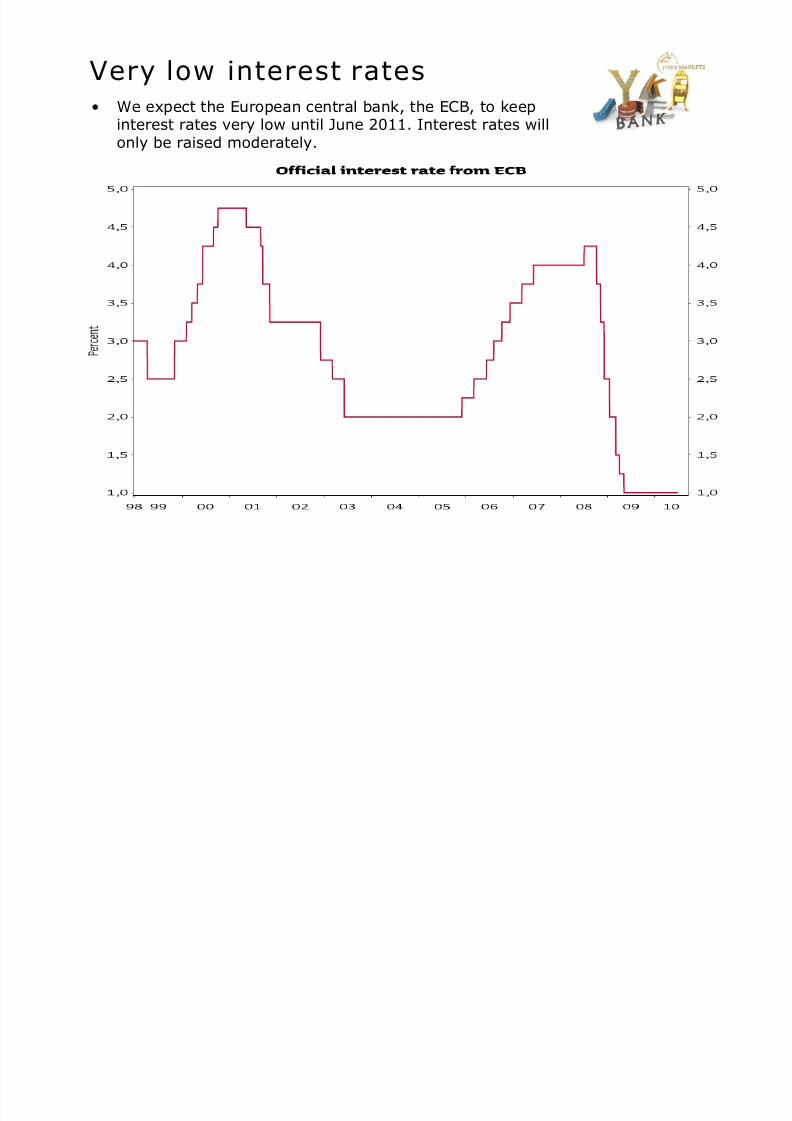

Very low interest rates

• We expect the European central bank, the ECB, to keepinterest rates very low until June 2011. Interest rates willonly be raised moderately.

8/9/2019 JYSKE Bank JUL 02 Eco Outlook Germany

http://slidepdf.com/reader/full/jyske-bank-jul-02-eco-outlook-germany 13/13

Discla im er & D isclosu r e

Jyske Bank is supervised by the Danish Financial Supervisory Authority.Jys e Ban s ana ysts are su ject to t e recommen ations o T e Danis Securities Dea ersAssociation on the handling of conflicts of interest within investment banks.The analysis is based on information which Jyske Bank finds reliable, but Jyske Bankdoes not assume any responsibility for the correctness of the material nor for transactionsmade on the basis of the information or the estimates of the research report. The estimates and

.personal use of Jyske Bank's customers and may not be copied. This report is an investment research report.

Co n f l i ct s o f i n t e r e st

Jyske Bank has prepared procedures to prevent and preclude conflicts of interest thus ensuring that analyses.

procedures covering the research activities of Jyske Markets, a business unit of Jyske Bank.Read more about Jyske Bank's policy on conflicts of interest at www.jyskemarkets.comJyske Bank's analysts may not hold positions in the instruments for which they prepare research reports.Jyske Bank may hold positions and/or have interests in the instruments for which such reports are prepared.The anal sts receive no a ment from ersons interested in individual research re orts.

Th e f i r s t p u b l i ca t i o n d a t e o f t h e r es ea r ch r e p or t

See the front page. All prices stated are the latest closing prices before the release of the report, unlessotherwise stated.

Financ ia l m ode ls

Jyske Bank uses one or more models based on traditional econometric and financial methods. The data usedare solely data available to the public.

Investment may involve risk, so assessments and recommendations, if any, in this research report mayinvolve risk. See the research report for an assessment of risk, if any.

Go o d a d vi ce

e u ure an s or ca re urns es ma e n e researc repor are s a e as re urns e ore cos s s ncereturns after costs depend on a number of factors relating to individual customer relations, custodian charges,

volume of trade as well as market-, currency- and product-specific factors.