Embed Size (px)

Citation preview

Page 1 of 19

28 January 2014

Susanna Chui

(852) 2235 7131

Trading data

52-Week Range (HK$)

3 Mth Avg Daily Vol (m)

No of Shares (m)

Market Cap (HK$m)

Major Shareholders (%)

Auditors

Result Due

3.10/5.91

5.31

1,167.37

5,813.48

Southern Asia

Management (25%)

ERNST & YOUNG

FY13E: Mar Company description

Established in 2000, Juteng is the largest plastic

notebook casing maker, with ~30.0% share of the

global notebook casing market followed by Hon

Hai and Huan Hsin. Its customers are mainly

major notebook ODMs, such as Compal

(2324.TT), Wistron (3231.TT), Quanta (2382.TT),

Pegatron (4938.TT), and Inventec (2356.TT), for

major PC-brand vendors, such as Lenovo

(992.HK), HP (HPQ.US), ASUS (2357.TT), Acer

(2353.TT), and Dell (DELL.US). The company is

shifting focus from plastic casings to

metal/composite casings, and penetrating into

tablet market (Google (GOOG.US)’s Nexus 7)

from 2H12 and smartphone market (Moto X) from

2H13.

Price chart

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

HK$

A diversifying casing leader

Rating Buy Initiation

Target Price HKD 7.62

Current price

HKD 5.00 Upside +52%

A leader in notebook casing, harvesting from diversification

Juteng is the largest plastic notebook casing maker, with ~30.0% share of

the global notebook casing market followed by Hon Hai and Huan Hsin.

The company is shifting focus from plastic casings to metal/ composite

casings, and penetrating into tablet/ smartphone market from 2H12 and

2H13 respectively, supported by its comprehensive product offering and

solid relationships with ODMs/ OEMs.

Notebooks turning to metal/ composite casing

We expect its notebook revenue decline to moderate to -2.7% in FY14E

from -4.2% in FY13E, on the back of market decline slowdown and

product-mix improvement. Revenue from metal/ composite material

casings has been catching up, given the general trend for ultrabooks/

convertible notebooks, and higher ASPs of metal/ composite casings

(>US$10/piece) compared with those of plastic casings (~US$5/piece).

Growth coming from tablets and smartphones

Tablet shipment surpasses notebook shipment from 2013, and

smartphone shipment has been even 5.6 times of notebook one. With

increasing market share from customers and higher ASPs, we expect

tablet/ smartphone revenue to grow 71.0%/ 279.9% in FY14E. Its tablet/

smartphone sales mix will further expand to ~15.0%/10.0% in FY14E from

~10.0%/3.0% in FY13E.

A large potential from Google/ Moto and Microsoft/ Nokia

In 2013, Microsoft has announced the acquisition of Nokia, followed by

the Google/ Moto acquisition in 2011. We believe Google and Microsoft

are exercising the similar strategy to monetize their Android and Windows

platforms, through the capabilities of their hardware devices. They could

potentially be a major clan in the smartphone market. Juteng, one of the

players in Google and Microsoft’s supply chain, will probably catch up with

their device strategies.

We initiate coverage on Juteng with BUY

We initiate coverage on Juteng with BUY. The company is trading at 6.1x

FY14E PER, which is 47.5% lower than average 11.6x of the peers. With

dominant industry position in casing with new growth driver of tablets/

smartphones, we believe Juteng’s valuation will rise to near average of

the peers. We initiate coverage on the stock with target price of HK$7.62,

based on 9.3x FY14E PER and 20.0% discount to average of the peers.

HKD million FY11A FY12A FY13E FY14E FY15E

Revenue 8,235 9,201 9,242 10,534 12,031

Net Profit 257 601 715 928 1,089

Consensus NP 715 941 1,120

EPS (HKD) 0.23 0.53 0.63 0.82 0.96

P/E (x) 22.0 9.4 7.9 6.1 5.2

Sources: Bloomberg, CIRL estimates

Juteng International | 3336.HK

China Puti

Page 2 of 19

A leader in notebook casing, harvesting from

diversification

Established in 2000, Juteng is the largest plastic notebook casing maker, with ~30.0%

share of the global notebook casing market followed by Hon Hai and Huan Hsin. Its

customers are mainly major notebook ODMs, such as Compal (2324.TT), Wistron

(3231.TT), Quanta (2382.TT), Pegatron (4938.TT), and Inventec (2356.TT). The

company is shifting focus from plastic casings to metal/composite casings, and

penetrating into tablet market (Google (GOOG.US)’s Nexus 7) from 2H12 and

smartphone market (Moto X) from 2H13.

Exhibit 1: Global notebook casing market share

Source: Company data, CIRL

Exhibit 2: FY13E revenue mix by customers

Source: Company data, CIRL

Juteng, 30%

Hon Hai, 20%Huan

Hsin, 10%

Others , 40%

Compal23%

Wistron19%

Quanta17%

Pegatron17%

Inventec15%

Others9%

Page 3 of 19

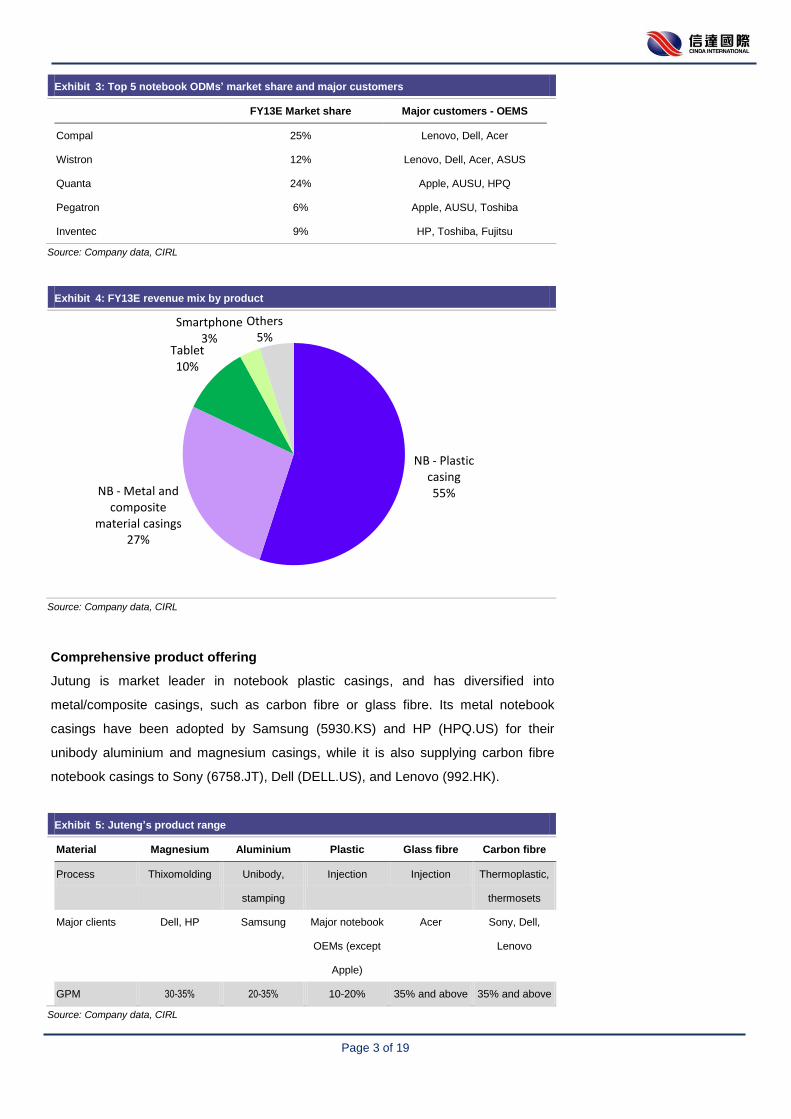

Exhibit 3: Top 5 notebook ODMs’ market share and major customers

FY13E Market share Major customers - OEMS

Compal 25% Lenovo, Dell, Acer

Wistron 12% Lenovo, Dell, Acer, ASUS

Quanta 24% Apple, AUSU, HPQ

Pegatron 6% Apple, AUSU, Toshiba

Inventec 9% HP, Toshiba, Fujitsu

Source: Company data, CIRL

Exhibit 4: FY13E revenue mix by product

Source: Company data, CIRL

Comprehensive product offering

Jutung is market leader in notebook plastic casings, and has diversified into

metal/composite casings, such as carbon fibre or glass fibre. Its metal notebook

casings have been adopted by Samsung (5930.KS) and HP (HPQ.US) for their

unibody aluminium and magnesium casings, while it is also supplying carbon fibre

notebook casings to Sony (6758.JT), Dell (DELL.US), and Lenovo (992.HK).

Exhibit 5: Juteng’s product range

Material Magnesium Aluminium Plastic Glass fibre Carbon fibre

Process Thixomolding Unibody,

stamping

Injection Injection Thermoplastic,

thermosets

Major clients Dell, HP Samsung Major notebook

OEMs (except

Apple)

Acer Sony, Dell,

Lenovo

GPM 30-35% 20-35% 10-20% 35% and above 35% and above

Source: Company data, CIRL

NB - Plastic casing55%NB - Metal and

composite material casings

27%

Tablet10%

Smartphone3%

Others5%

Page 4 of 19

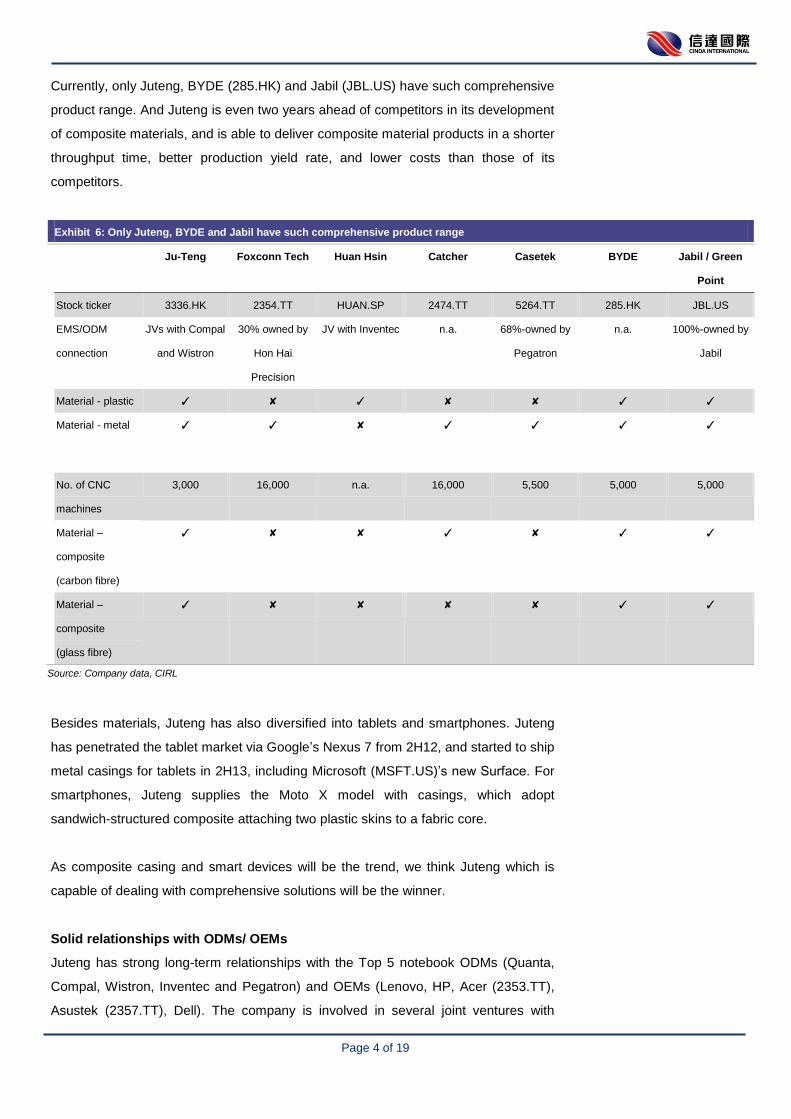

Currently, only Juteng, BYDE (285.HK) and Jabil (JBL.US) have such comprehensive

product range. And Juteng is even two years ahead of competitors in its development

of composite materials, and is able to deliver composite material products in a shorter

throughput time, better production yield rate, and lower costs than those of its

competitors.

Exhibit 6: Only Juteng, BYDE and Jabil have such comprehensive product range

Ju-Teng Foxconn Tech Huan Hsin Catcher Casetek BYDE Jabil / Green

Point

Stock ticker 3336.HK 2354.TT HUAN.SP 2474.TT 5264.TT 285.HK JBL.US

EMS/ODM

connection

JVs with Compal

and Wistron

30% owned by

Hon Hai

Precision

JV with Inventec n.a. 68%-owned by

Pegatron

n.a. 100%-owned by

Jabil

Material - plastic ✓ ✘ ✓ ✘ ✘ ✓ ✓

Material - metal ✓ ✓ ✘ ✓ ✓ ✓ ✓

No. of CNC

machines

3,000 16,000 n.a. 16,000 5,500 5,000 5,000

Material –

composite

(carbon fibre)

✓ ✘ ✘ ✓ ✘ ✓ ✓

Material –

composite

(glass fibre)

✓ ✘ ✘ ✘ ✘ ✓ ✓

Source: Company data, CIRL

Besides materials, Juteng has also diversified into tablets and smartphones. Juteng

has penetrated the tablet market via Google’s Nexus 7 from 2H12, and started to ship

metal casings for tablets in 2H13, including Microsoft (MSFT.US)’s new Surface. For

smartphones, Juteng supplies the Moto X model with casings, which adopt

sandwich-structured composite attaching two plastic skins to a fabric core.

As composite casing and smart devices will be the trend, we think Juteng which is

capable of dealing with comprehensive solutions will be the winner.

Solid relationships with ODMs/ OEMs

Juteng has strong long-term relationships with the Top 5 notebook ODMs (Quanta,

Compal, Wistron, Inventec and Pegatron) and OEMs (Lenovo, HP, Acer (2353.TT),

Asustek (2357.TT), Dell). The company is involved in several joint ventures with

Page 5 of 19

Compal and Wistron, which are the two largest contributors to the company’s revenue.

We believe the solid relationships can secure good order allocations from these

ODMS/ OEMs.

Exhibit 7: Juteng’s major joint ventures with ODMs

JV Entity Stake owned by Juteng Product

Compal Compal Precision (prev.

Wah Yuen Holding)

57% Notebook metal and

plastic casing

Wis Precision - Kunshan Notebook plastic casing

Wistron Lian-Yi Precision 71% TV casing

Wis Precision - Taizhou Notebook plastic casing

Source: Company data, CIRL

Page 6 of 19

Notebooks turning to metal/ composite casing

The notebook segment is still Juteng’s key revenue contributor. We expect the rate of

notebook revenue decline to slow to -2.7% in FY14E from -4.2% in FY13E, on the

back of stabilized market and product-mix improvement from plastic casings to metal/

composite material casings. Revenue from metal/ composite material casings has

been catching up, given the general trend for ultrabooks/ convertible notebooks to

have thin-and-light designs, and higher ASPs of metal/ composite casings

(>US$10/piece) compared to those of plastic casings (~US$5/piece).

2014 notebook shipment decline will moderate, and ultrabooks/ convertible

notebooks will outperform

Windows 8 launch in 4Q12 has admittedly failed to deflect 2013’s declining PC

shipments. Due to the continuous cannibalization from more powerful and cheaper

tablets, we believe notebook units will continue to decline into 2014 despite slower

rate of decline. IDC also forecasts notebook decline to moderate to 6% in 2014 after

declining 10% in 2013.

Exhibit 8: Worldwide notebook shipment

Source: IDC, CIRL

Ultrabooks and convertible notebooks will outperform, however. To reduce

cannibalization impacts from tablets, Intel, Microsoft and PC brand vendors took

aggressive actions in 1) ultrabooks with thinner and lighter form factors, power-saving

platforms and longer battery life; and 2) convertible notebooks with one product

accounting for two (notebook and tablet) functionalities;

202 185 155

134 115

4 10

21 31

42

-

50

100

150

200

250

2011 2012 2013E 2014E 2015E

mn

un

its

Traditional notebook shipment

Ultrabooks and convertible notebook shipments

Page 7 of 19

As some PC vendors cut their selling prices to <US$600 to promote their ultrabooks/

convertible notebooks, we believe their penetration rate will increase to 19% of the

total notebook, and the shipment will continue to grow at 48% in 2014.

Exhibit 9: Ultrabooks and convertible notebook shipment

Source: IDC, CIRL

And corporate notebooks will improve as Win XP is being phased out

We believe corporate users may be at last transitioning away from Windows XP

before the expiry of support in April 2014. It is clearly leading to more stability in the

corporate segments. ODMs such as Inventec has also guided that commercial NB

shipments will be flat but consumer NB shipments will decline.

Metal/ composite casings catching up, given the trend for ultrabooks/

convertible notebooks with thin-and-light designs

The trend of thinner and lighter ultrabooks/ convertible notebooks and corporate

notebooks, will definitely favor demand for metal/ composite material casing, given

their functionality and differentiation.

Juteng has a comprehensive product range in casing material, ranging from plastic,

aluminium, magnesium, carbon fibre, to glass fibre composite material. And it is two

years ahead of competitors in its development of composite materials and is able to

deliver composite material products in shorter throughput times, better production

yield rate, and lower costs than those of its competitors. Therefore, we believe Juteng

is well positioned to seize emerging opportunities in ultrabook/ convertible notebook

and corporate notebook casings with its strength in offering composite material.

0%

5%

10%

15%

20%

25%

30%

-

5

10

15

20

25

30

35

40

45

2011 2012 2013E 2014E 2015E

mn

un

its

Ultrabooks and convertible notebook shipments Penetration rate

Page 8 of 19

Stable notebook revenue growth from product-mix improvement

Metal/ composite casings command much higher ASPs (>US$10/piece) compared

with those of plastic casings (~US$5/piece). With better product-mix, we expect

notebook revenue decline to moderate to -2.7% in FY14E from -4.2% in FY13E.

Page 9 of 19

Growth from tablets and smartphones

Tablet shipment surpasses notebook shipment from 2013, and smartphone shipment

has been even 5.6 times of notebook one. In order to capture these two huge markets,

Juteng has penetrated tablet market (Google’s Nexus 7) from 2H12 and smartphone

market (Moto X) from 2H13. With robust market growth, increasing market share from

new customers, and higher ASPs albeit using fewer pieces per set than notebooks,

we expect its tablet/ smartphone sales mix will further expand to ~15.0%/10.0% in

FY14E from ~10.0%/3.0% in FY13E.

Exhibit 10: Google’s Nexus 7 and Moto X

Source: Company data, CIRL

Exhibit 11: Global smart device shipment

Source: IDC, CIRL

202 185 155 134 115 4 10 21 31 42

60 116 197 266 338 473

716

976 1,219

1,425

-

500

1,000

1,500

2,000

2,500

2011 2012 2013E 2014E 2015E

mn

un

its

Smartphones

Tablets

Ultrabooks and convertible notebooks

Traditional notebooks

Page 10 of 19

Tablet shipment surpasses notebook shipment from 2013

The global tablet shipments will surpass notebook shipments significantly in 2013. We

believe the momentum will persist in 2014, given increasing number of cheaper tablet

products pushed by local brands in China and PC camps (needing tablet sales to help

reduce slowing notebook demand impacts). We estimate global tablet shipments will

grow by 35% yoy to 266m units in 2014 from 197m units in 2013.

Exhibit 12: Global tablet shipment

Source: IDC, CIRL

Exhibit 13: Tablet with Windows (most PC camp) platform is gaining market share

Source: IDC, CIRL

473

716

976

1,219

1,425

0.00

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

1,600.00

2011 2012 2013E 2014E 2015E

mn

un

its

68%56% 56% 54% 51%

32%43% 41% 41% 42%

0% 1% 3% 5% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013E 2014E 2015E

iOS Android Windows (mostly PC camp)

Page 11 of 19

Continuous robust smartphone momentum, in the “fashion” story

We see 2014 as another year of strong growth for smartphones, with still low

penetration rate of 34% in 2013. We estimate global smartphone shipments will grow

by 25% yoy to 1,219m units in 2014 from 976m units in 2013.

However, consumers may get bored of specification migrations. We can see

smartphone vendors’ flagship smartphones have moved up to quad-core

processor/5”+ display/13MP+ camera. With slow innovation curve, the “fashion” story

like the one in notebook market will occur once again in smartphone market. After

New HTC One (Metal + Plastic) and Moto X (sandwich-structured composite attaching

two plastic skins to a fabric core, supplied by Juteng), more and more smartphones

will be expected to turn from plastic casing to metal/ composite casing.

Samsung has announced a new smartphone, Galaxy J, a device which mashes

Galaxy S4 and Galaxy Note 3, in the metal look. It has been rumored the coming

Galaxy S5 and Galaxy F (a premium edition of Galaxy S5) will be built from metal/

composite materials. And in Consumer Electronics Show (CES), China smartphone

brands, such as ZTE and TCL, have adopted metal/ composite casing for the new

models in 2014.

Exhibit 14: Global smartphone shipment

Source: IDC, CIRL

473

716

976

1,219

1,425

0.00

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

1,600.00

2011 2012 2013E 2014E 2015E

mn

un

its

Page 12 of 19

Exhibit 15: Smartphone highlight in CES 2014

Huawei

Mate2

LG

G Flex

ZTE

Grand S2

ZTE

Iconic Phablet

ZTE

Sonata

Sony

Z1S

Plastic Plastic Metal Composite

(metal + plastic)

Plastic Glass

Sony

Z1 compact

TCL

Idol X+

TCL

Idol Alpha

Asus

Zenfone

Asus

Padfone mini

Acer

Liquid Z5

Glass Plastic Composite

(metal +

transparent

material)

Plastic Plastic Plastic

Source: Company data, CIRL

Rising tablet/ smartphone contribution

Juteng has diversified into tablets and smartphones. The company has penetrated

into tablet market via Google’s Nexus 7 from 2H12, and started to ship metal casings

for tablets in 2H13, including for Microsoft (MSFT.US)’s new Surface. For

smartphones, Juteng supplies the Moto X model from 2H13 with casings, adopting

sandwich-structured composite attaching two plastic skins to a fabric core.

These order gain has proven its capability in composite-material and tablet/

smartphone market, and also new relationship with internet/ software companies

(Google and Microsoft). We believe there will be potential for the company to catch up

with Google and Microsoft’s device strategies.

Page 13 of 19

And it can also leverage on these relationships with its long built customers, notebook

ODMs and OEMs. ODMs have provided optimistic guidance about smart device

shipments in 2014, due to OEMs’ more aggressive launch of cheaper tablets and

smartphones.

Exhibit 16: ODMs’ FY14E guidance

Compal NB OEMs will reduce the number of ODM vendors to 2~3 from 3~4 and most orders will

move to Compal and Quanta in FY14. It expects 40mn (2% yoy) NB units and

15mn/20mn (100% yoy) tablets/smartphones in 2014.

Quanta It sets a NB shipment target of 42~44mn units (up 3~5% yoy), but flat tablet shipments

of 20mn.

Wistron It expects NB shipment to be 19~20mn units (down 18% yoy), but FY14 smart device

shipment will grow to 32~33mn units (up around 15% yoy).

Pegatron It forecasts a decline as industry level in the computing segment while the consumer

and communication segment will continue to grow.

Inventec It guides that commercial NB shipments will be flat but consumer NB shipments will

decline. It expects its non-notebook businesses to drive its growth in 2014. Specifically,

it is positive on growth from its smart device s and solar business; and expects stable

growth for its server business.

Source: Company data, CIRL

Therefore, we expect tablet/ smartphone revenue to grow 71.0%/ 279.9% in FY14E,

with its customers’ increasing exposure to tablets and smartphones, of which market

is delivering rapid growth.

Page 14 of 19

A large Potential from Google/ Moto and

Microsoft/ Nokia

In 2013, Microsoft has announced the acquisition of Nokia, followed by the Google/

Moto acquisition in 2011. As Apple has a full stack of hardware (smart devices) and

operating system (iOS, the 2rd

mobile operating systems), Google and Microsoft are

exercising the similar strategy to merchandise hardware devices, which would in turn

solidify their foothold in operating system (Android and Windows platforms, the 1st and

3rd

mobile operating systems) and monetize them. Especially for Windows Phone

which is still a minority player, Nokia seems to be its ultimate solution in combating the

threats from the popularity of smart devices that use Android and iOS platform.

Microsoft has aggressive target, and Google is not expected to be far behind

Microsoft has set to have 15% market share and 255M unit shipments by 2018.

Though it is a long way to this aggressive target, Nokia’s Lumia series appears to be

off to a solid start. Windows Phone’s share in global smartphone market has

increased to 3.6% in 3Q13 from 2.0% in 3Q12, thanks to the satisfactory sales of

Lumia series in developing markets such as India. We believe Google’s target will not

be far behind. Therefore, there will be potential for Moto and Nokia to become the

notable competitors to Apple and Samsung down the road.

Exhibit 17: Google and Microsoft aim at increasing share and monetization of their platforms

Source: Company data, CIRL

36%

47%

57%53%

59%

69%75%

70%75%

79% 81%

18% 19%14%

23% 23%17% 15%

21%17%

13% 13%

3% 2% 1% 1% 2% 3% 2% 3% 3% 4% 4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Android iOS Windows Phone

Page 15 of 19

Providing devices in differentiating form and in competitive price

To fight for market share and monetization of their Android and Windows platform,

Google and Microsoft probably have to cut margins in providing devices either in

differentiating form for flagship devices or in competitive price for affordable devices.

Exhibit 18: Moto X has provided the fresh look in alternate materials

Source: Company data, CIRL

Moto X has tried the fresh look in alternate materials, of which woven white and black

(supplied by Juteng) are sandwich-structured composite attaching two plastic skins to

a fabric core. As for Nokia, its portfolio continues to expand from flagship devices like

the Nokia Lumia 928/1020/1520, to affordable devices like the Lumia 520/625/1320.

Potentially catching up with Google and Microsoft

Google and Microsoft will prefer casing makers, with low exposure to Apple and also

comprehensive product range. Therefore, Juteng has become one of the players in

Google and Microsoft’s supply chain and will probably catch up with their device

strategies.

Page 16 of 19

More metal/composite, higher GPM

Riding on improving product mix (notebook - plastic casing segment decreasing from

~61% in FY12 to ~37% in FY15E), the overall GPM will be pulled up. It is because

GPM on plastic casings is about 10-15%, but that for others can be 15-35%.

Exhibit 19: Juteng’s product mix

Source: Company data, CIRL

Exhibit 20: Juteng’s FY13E margins

GPM

Notebook - Plastic casing 10-15%

Notebook - Metal and composite material casings 30-35%

Tablet 15-20%

Smartphone 30-35%

Overall 19%

Source: Company data, CIRL

72%61%

55%45%

37%

20%

25%27%

25%

23%

0%4% 10%

15%

20%

0% 0%3%

10% 15%

8% 10% 5% 5% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013E 2014E 2015E

Others

Smartphone

Tablet

NB - Metal and composite material casings

NB - Plastic casing

Page 17 of 19

Financial analysis and valuation

We forecast revenue to grow by 0.4%/14.0%/14.2% for FY13E/FY14E/FY15E

mainly driven by the growth of tablet/ smartphone segments.

GPM keeps uptrend from 15.2% in FY12 to 20.2% in FY15E, riding on improving

product mix (notebook - plastic casing segment decreasing from ~61% in FY12 to

~37% in FY15E). GPM on plastic casings is 10-15%, but that for others can be

15-35%.

SG&A expense will increase from 6.0% in FY12 to 7.2% in FY15E, on the back of

developing tablet/ smartphone segments. We expect that net profit will rise

18.9%/29.9%/17.4% to HKD714.6mn/ HKD928.1mn/ HKD1,089.5mn in

FY13E/FY14E/FY15E.

Payout will maintain a ~23.0% of net profit in FY13E-FY15E representing

2.8%/3.7%/4.3% of FY13E/FY14E/FY15E dividend yield.

We initiate coverage on Juteng with BUY. The company is trading at 6.1x FY14E

PER, which is 47.5% lower than average 11.6x of the peers. With dominant industry

position in casing with new growth driver of tablets/ smartphones, we believe Juteng’s

valuation will rise to near average of the peers. We initiate coverage on the stock with

target price of HK$7.62, based on 9.3x FY14E PER and 20.0% discount to average of

the peers.

Risk Factors

Downside risks include: 1) slower than expected growth of tablets/ smartphones; 2)

slower than expected expansion of market share; 3) slower than expected growth of

its clients; 4) more-than-expected competition; and 5) rapidly changing technology

trends.

Page 18 of 19

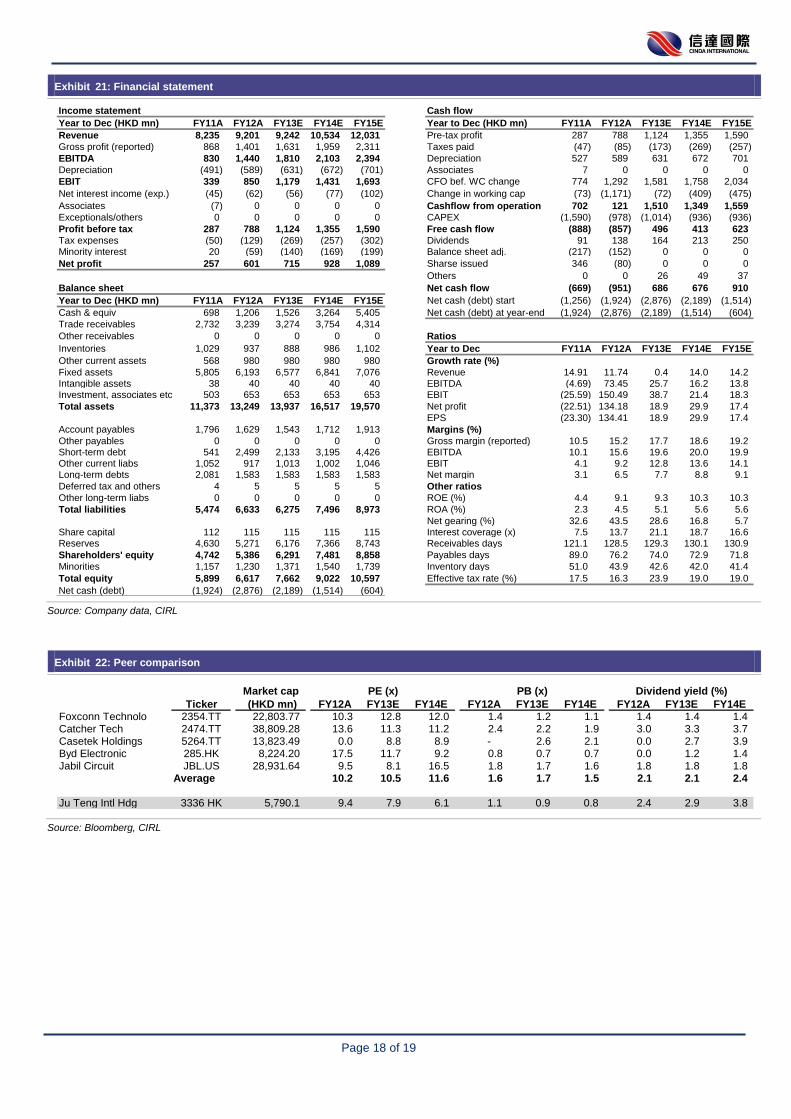

Exhibit 21: Financial statement

Source: Company data, CIRL

Exhibit 22: Peer comparison

Source: Bloomberg, CIRL

Income statement Cash flow

Year to Dec (HKD mn) FY11A FY12A FY13E FY14E FY15E Year to Dec (HKD mn) FY11A FY12A FY13E FY14E FY15E

Revenue 8,235 9,201 9,242 10,534 12,031 Pre-tax profit 287 788 1,124 1,355 1,590

Gross profit (reported) 868 1,401 1,631 1,959 2,311 Taxes paid (47) (85) (173) (269) (257)

EBITDA 830 1,440 1,810 2,103 2,394 Depreciation 527 589 631 672 701

Depreciation (491) (589) (631) (672) (701) Associates 7 0 0 0 0

EBIT 339 850 1,179 1,431 1,693 CFO bef. WC change 774 1,292 1,581 1,758 2,034

Net interest income (exp.) (45) (62) (56) (77) (102) Change in working cap (73) (1,171) (72) (409) (475)

Associates (7) 0 0 0 0 Cashflow from operation 702 121 1,510 1,349 1,559

Exceptionals/others 0 0 0 0 0 CAPEX (1,590) (978) (1,014) (936) (936)

Profit before tax 287 788 1,124 1,355 1,590 Free cash flow (888) (857) 496 413 623

Tax expenses (50) (129) (269) (257) (302) Dividends 91 138 164 213 250Minority interest 20 (59) (140) (169) (199) Balance sheet adj. (217) (152) 0 0 0

Net profit 257 601 715 928 1,089 Sharse issued 346 (80) 0 0 0

Others 0 0 26 49 37

Balance sheet Net cash flow (669) (951) 686 676 910

Year to Dec (HKD mn) FY11A FY12A FY13E FY14E FY15E Net cash (debt) start (1,256) (1,924) (2,876) (2,189) (1,514)

Cash & equiv 698 1,206 1,526 3,264 5,405 Net cash (debt) at year-end (1,924) (2,876) (2,189) (1,514) (604)

Trade receivables 2,732 3,239 3,274 3,754 4,314

Other receivables 0 0 0 0 0 Ratios

Inventories 1,029 937 888 986 1,102 Year to Dec FY11A FY12A FY13E FY14E FY15E

Other current assets 568 980 980 980 980 Growth rate (%)

Fixed assets 5,805 6,193 6,577 6,841 7,076 Revenue 14.91 11.74 0.4 14.0 14.2Intangible assets 38 40 40 40 40 EBITDA (4.69) 73.45 25.7 16.2 13.8Investment, associates etc 503 653 653 653 653 EBIT (25.59) 150.49 38.7 21.4 18.3

Total assets 11,373 13,249 13,937 16,517 19,570 Net profit (22.51) 134.18 18.9 29.9 17.4

EPS (23.30) 134.41 18.9 29.9 17.4

Account payables 1,796 1,629 1,543 1,712 1,913 Margins (%)

Other payables 0 0 0 0 0 Gross margin (reported) 10.5 15.2 17.7 18.6 19.2Short-term debt 541 2,499 2,133 3,195 4,426 EBITDA 10.1 15.6 19.6 20.0 19.9Other current liabs 1,052 917 1,013 1,002 1,046 EBIT 4.1 9.2 12.8 13.6 14.1Long-term debts 2,081 1,583 1,583 1,583 1,583 Net margin 3.1 6.5 7.7 8.8 9.1

Deferred tax and others 4 5 5 5 5 Other ratios

Other long-term liabs 0 0 0 0 0 ROE (%) 4.4 9.1 9.3 10.3 10.3

Total liabilities 5,474 6,633 6,275 7,496 8,973 ROA (%) 2.3 4.5 5.1 5.6 5.6

Net gearing (%) 32.6 43.5 28.6 16.8 5.7Share capital 112 115 115 115 115 Interest coverage (x) 7.5 13.7 21.1 18.7 16.6Reserves 4,630 5,271 6,176 7,366 8,743 Receivables days 121.1 128.5 129.3 130.1 130.9

Shareholders' equity 4,742 5,386 6,291 7,481 8,858 Payables days 89.0 76.2 74.0 72.9 71.8

Minorities 1,157 1,230 1,371 1,540 1,739 Inventory days 51.0 43.9 42.6 42.0 41.4

Total equity 5,899 6,617 7,662 9,022 10,597 Effective tax rate (%) 17.5 16.3 23.9 19.0 19.0

Net cash (debt) (1,924) (2,876) (2,189) (1,514) (604)

Market cap PE (x) PB (x) Dividend yield (%)

Ticker (HKD mn) FY12A FY13E FY14E FY12A FY13E FY14E FY12A FY13E FY14EFoxconn Technolo 2354.TT 22,803.77 10.3 12.8 12.0 1.4 1.2 1.1 1.4 1.4 1.4Catcher Tech 2474.TT 38,809.28 13.6 11.3 11.2 2.4 2.2 1.9 3.0 3.3 3.7Casetek Holdings 5264.TT 13,823.49 0.0 8.8 8.9 - 2.6 2.1 0.0 2.7 3.9Byd Electronic 285.HK 8,224.20 17.5 11.7 9.2 0.8 0.7 0.7 0.0 1.2 1.4Jabil Circuit JBL.US 28,931.64 9.5 8.1 16.5 1.8 1.7 1.6 1.8 1.8 1.8

Average 10.2 10.5 11.6 1.6 1.7 1.5 2.1 2.1 2.4

Ju Teng Intl Hdg 3336 HK 5,790.1 9.4 7.9 6.1 1.1 0.9 0.8 2.4 2.9 3.8

Page 19 of 19

Rating Policy

Rating Definition

Stock Rating Buy Outperform HSI by 15%

Neutral Between -15% ~ 15% of the HSI

Sell Underperform HSI by -15%

Sector Rating Accumulate Outperform HSI by 10%

Neutral Between -10% ~ 10% of the HSI

Reduce Underperform HSI by -10%

Analysts List

Antony Cheng Research Director (852) 2235 7127 [email protected]

Hayman Chiu Senior Research Analyst (852) 2235 7677 [email protected]

Kenneth Li Senior Research Analyst (852) 2235 7619 [email protected]

Lewis Pang Research Analyst (852) 2235 7847 [email protected]

Susanna Chui Research Analyst (852) 2235 7131 [email protected]

Shawn Yang Research Assistant (852) 2235 7617 [email protected]

Analyst Certification

I, Susanna Chui hereby certify that all of the views expressed in this report accurately reflect my personal views about

the subject company or companies and its or their securities. I also certify that no part of my compensation was / were,

is / are or will be directly or indirectly, related to the specific recommendations or views expressed in this report / note.

Disclaimer

This report has been prepared by the Cinda International Research Limited. Although the information and opinions

contained in this report have been compiled or arrived at from sources believed to be reliable, Cinda International

cannot and does not warrant the accuracy or completeness of any such information and analysis. The report should not

be regarded by recipients as a substitute for the exercise of their own judgment. Recipients should understand and

comprehend the investment objectives and its related risks, and where necessary consult their own financial advisers

prior to any investment decision. The report may contain some forward-looking estimates and forecasts derived from

the assumptions of the future political and economic conditions with inherently unpredictable and mutable situation, so

uncertainty may contain. Any opinions expressed in this report are subject to change without notice. The report is

published solely for information purposes, it does not constitute any advertisement and should not be construed as an

offer to buy or sell securities. Cinda International will not accept any liability whatsoever for any direct or consequential

loss arising from any use of the materials contained in this report. This document is for the use of intended recipients

only, the whole or a part of this report should not be reproduced to others.