Embed Size (px)

Citation preview

I N V E S T O R P R E S E N TAT I O N

J U N E 2 0 1 7

GGP Inc.’s mission is to own and operate best-in-class retail properties that provide an outstanding environment and experience for our Communities, Retailers, Employees, Consumers

and Shareholders. GGP is an S&P 500 company focused exclusively on owning, managing, leasing, and redeveloping high-quality retail properties throughout the United States.

GGP defines best-in-class retail and modern luxury through curated merchandising and elegant culinary experiences set against the backdrop of refined ambience across

this distinguished collection of destinations.

DO THE RIGHT THING

ATTITUDE

HUMILITY

TOGETHER

O W N I T

Headquarters Chicago

Retail Properties 127

States 40

Inline & Freestanding GLA

56 million

Total Retail GLA 121 million

Equity Market

Cap$20.6 billion

Enterprise Value $39.0 billion

S & P 5 0 0 R E A L E S T A T E I N V E S T M E N T T R U S T ( a )

2a. As of 3/31 / 17

E X E C U T I V E T E A M

SANDEEP MATHRANIChief Executive Officer

SHOBI KHANPresident and Chief Operating Officer

MICHAEL BERMANExecutive Vice President and Chief Financial Officer

JARED CHUPAILAExecutive Vice President, Leasing

RICHARD PESINExecutive Vice President, Anchors, Development and Construction

ROSEMARY FEITExecutive Vice President, General Counsel

BRIAN McCARTHYExecutive Vice President, Asset Management

JULIE KNUDSONSenior Vice President and Chief Human Resources Officer

TARA MARSZEWSKISenior Vice President, Chief Accounting Officer

3

GLA (in millions)

SF Per Capita

% of Total High-Quality GLA

High-Quality (a) Regional Shopping Center GLA 495 1.6 40%

High-Quality (b) Open-Air Center GLA 732 2.3 60%

Total High-Quality Retail Real Estate 1,227 3.9 100%

T O T A L U . S . R E A L E S T A T E G L A

a. “High- Qual i t y ” def ined as a regional shopping center rated B+ or bet ter.b. “High- Qual i t y ” def ined as a Trade Area Power score of 75 -100 for s t r ip centers .

H I G H Q U A L I T Y R E T A I L P R O P E R T I E S

GGP owns 8.2% of all High-Quality Retail Real Estate

High-Quality Retail Real Estate 1.2 billion sf 3.9 sf per capita

High-Quality Regional Shopping Centers

Regional Shopping Centers 1.1 billion sf 3.4 sf per capita

Open-air Centers 6.4 billion sf 20.2 sf per capita

Mid- to Low-Quality Retail Real Estate 6.3 billion sf 19.7 sf per capita

T Y P E Q U A L I T Y

High-Quality Open-Air Centers

4

Source: GGP

Top Retail Properties

NOI Weighted Sales PSF(b)

% of Company NOI

Lease Spreads

Top 10 $924 23% 16.1%

Top 30 $828 49% 15.7%

Top 50 $770 67% 11.8%

Top 100 $710 95% 11.0%

Total Retail Properties $705 100% 10.1%

75 Class A Retail Properties $764 77% 13.7%

S A L E S A N D N O I C O N T R I B U T I O N S ( a )

a. Retai l proper t ies ranked by NOI .

b. Weighted Sales per square foot for t rai l ing 12 months ended March 31 , 2017 for comparable tenants occupying space less than 10,000 square feet .

I R R E P L A C E A B L E R E T A I L R E A L E S T A T E I N T H E U . S .

GGP owns 100 of the top 500 regional shopping centers in the U.S.

5

R E T A I L R E A L E S T A T E

STRIP MALL

CONVENIENCE

COMMUNITY

OUTLET

SUPER-REGIONAL

LIFESTYLE

POWER

NEIGHBORHOOD

REGIONAL

C H A N G I N G T H E V O C A B U L A R Y

Retailers, restaurants and entertainment venues are property type agnostic and want to be in high-quality retail

locations that attract heavy traffic.

S O U R C E S O F “ N E W ” D E M A N D

Restaurants Entertainment Fitness & Beauty Grocery

6

R E S T A U R A N T S

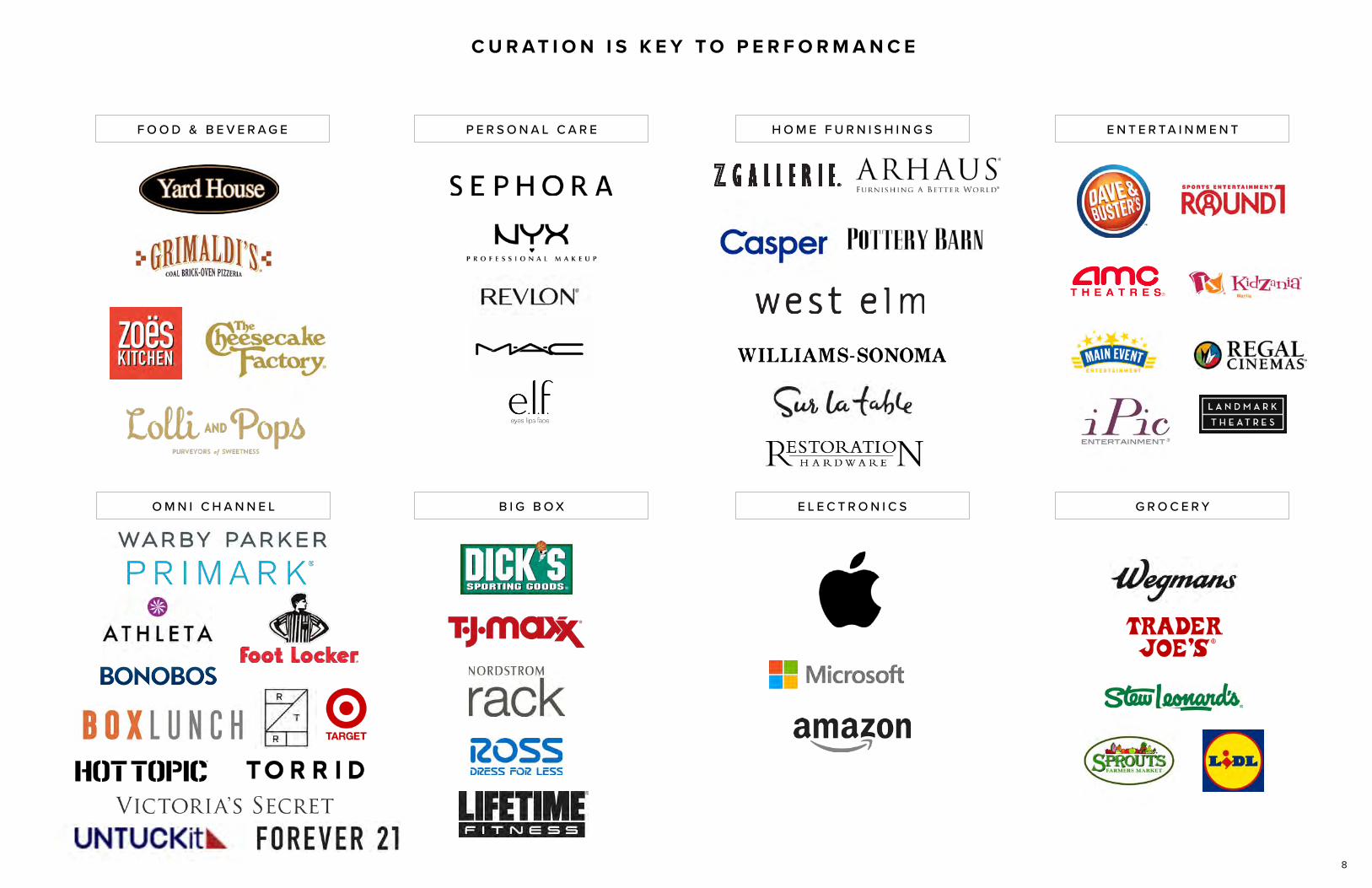

C U R A T I O N I S K E Y T O P E R F O R M A N C E

P E R S O N A L C A R E H O M E F U R N I S H I N G S E N T E R T A I N M E N T

O M N I C H A N N E L B I G B O X E L E C T R O N I C S G R O C E R Y

7

F O O D & B E V E R A G E

O M N I C H A N N E L B I G B O X E L E C T R O N I C S G R O C E R Y

P E R S O N A L C A R E H O M E F U R N I S H I N G S E N T E R T A I N M E N T

C U R A T I O N I S K E Y T O P E R F O R M A N C E

8

S U S T A I N A B I L I T Y

2 0 1 6 I M P A C T AT A G L A N C E

Composted as additional 160 tons of food waste; a 7.6% increase from 2015.

In October 2016, the Solar Industries Energy Association (“SEIA”) ranked GGP 9th among all U.S. companies based on installed solar generation capacity & ranked GGP 3rd based on the solar capacity it installed in calen-dar year 2016.

Completed lighting and HVAC up-grades with projected savings of 80.4 million kilowatt hours of electricity annually; the equivalent of removing 8,300 homes from the grid.

Reduced its carbon footprint by 25,600 metric tons of carbon dioxide equivalents; the equivalent of remov-ing approximately 19,800 cars from U.S. roads.

Since 2011, reduced grid-purchased electricity consumption by 267.9 million kilowatt hours; enough electricity to power all of the homes in Napa, CA for one year.

Diverted more than 55,200 tons of waste from landfills; enough to fill more than 6,200 garbage trucks.

S e c t o r L e a d e r 2 0 1 4

® ®

G r e e n S t a r 2 0 1 4

9

10

D E B T P R O F I L E a

D E B T M A T U R I T Y L A D D E R b

$ I N B I L L I O N S A T G G P S H A R E

$0.0

2017 2018

$0.5

2019

$2.1

2020

$3.1

2021

$3.0

2022

$2.4

2023

$1.9

2024

$1.6

2025

$1.7

2026

$0.5

2027+

$0.5

A V E R A G E R E M A I N I N G T E R M

N E T D E B T / E B I T D A c

I N T E R E S T C O V E R A G E

5 . 2 Y E A R S

4 7. 4 %

7. 8 X

2 . 8 X

a. As of 3/31 /2017

b. Assumes maturi t y ex tension opt ions are exercised and approved.

c. Net debt as of 3/31 /2017 div ided by 2017 projected EBITDA.

18

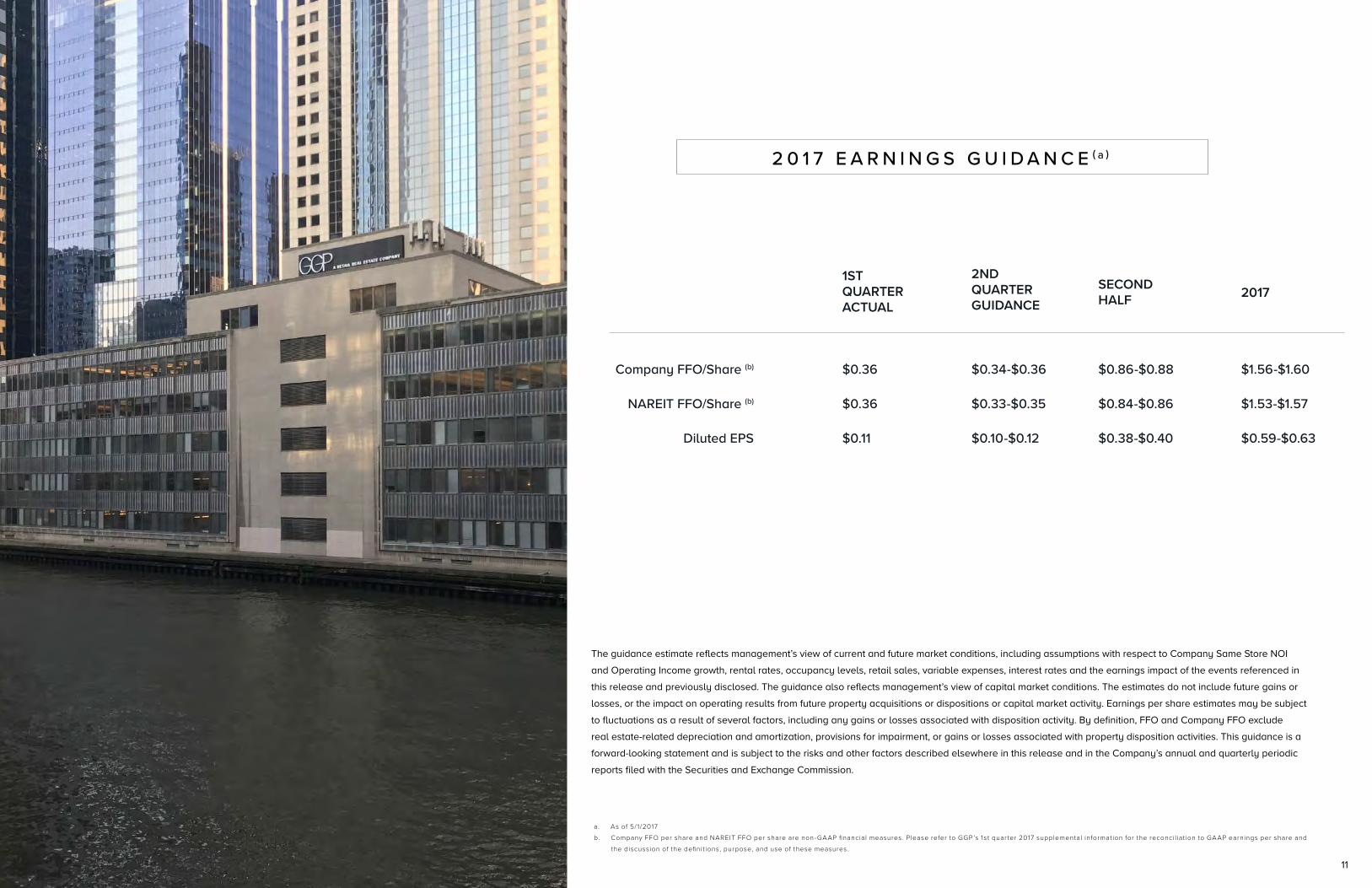

Company FFO/Share (b)

NAREIT FFO/Share (b)

Diluted EPS

1ST QUARTER ACTUAL

$0.36

$0.36

$0.11

$0.34-$0.36

$0.33-$0.35

$0.10-$0.12

2ND QUARTER GUIDANCE

$0.86-$0.88

$0.84-$0.86

$0.38-$0.40

SECOND HALF

$1.56-$1.60

$1.53-$1.57

$0.59-$0.63

2017

The guidance estimate reflects management’s view of current and future market conditions, including assumptions with respect to Company Same Store NOI

and Operating Income growth, rental rates, occupancy levels, retail sales, variable expenses, interest rates and the earnings impact of the events referenced in

this release and previously disclosed. The guidance also reflects management’s view of capital market conditions. The estimates do not include future gains or

losses, or the impact on operating results from future property acquisitions or dispositions or capital market activity. Earnings per share estimates may be subject

to fluctuations as a result of several factors, including any gains or losses associated with disposition activity. By definition, FFO and Company FFO exclude

real estate-related depreciation and amortization, provisions for impairment, or gains or losses associated with property disposition activities. This guidance is a

forward-looking statement and is subject to the risks and other factors described elsewhere in this release and in the Company’s annual and quarterly periodic

reports filed with the Securities and Exchange Commission.

2 0 1 7 E A R N I N G S G U I D A N C E a

a. As of 5/ 1 /2017

b. Company FFO per share and NAREIT FFO per share are non-GAAP financial measures. Please refer to GGP’s 1st quar ter 2017 supplemental informat ion for the reconcil iat ion to GAAP earnings per share and

the discussion of the definit ions, purpose, and use of these measures.

11

S T O R E S T H R I V E

S T O R E S T H R I V E

Retailers focused on three key factors will succeed

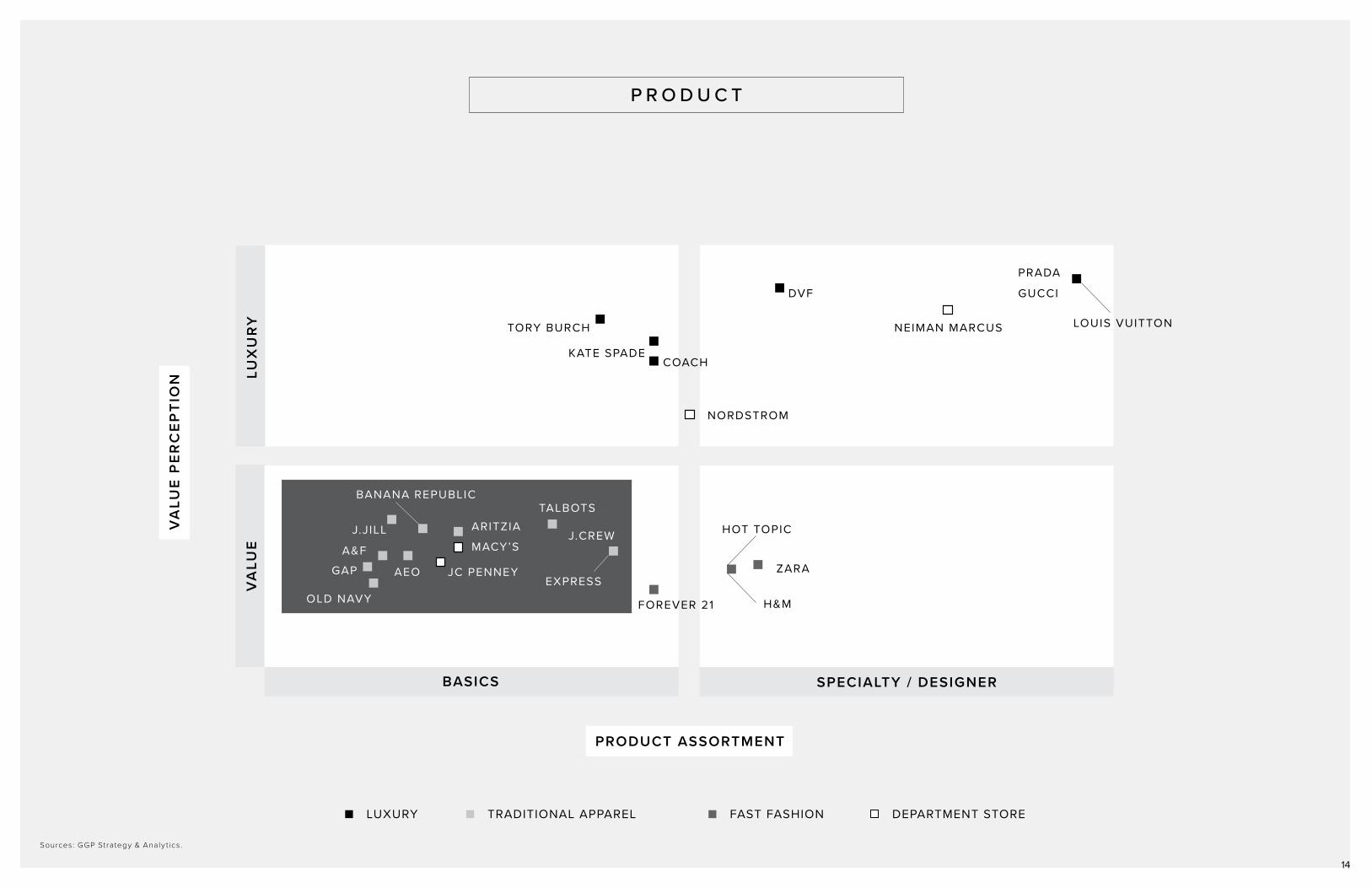

P R O D U C T

THE RIGHT ASSORTMENT

featuring current, relevant,and occasion-appropriatemerchandise that delightsthe target consumer

COMPELLING VALUE

balancing the total benefit of the shopping experience against the cost

APPROPRIATE QUALITY

for the price and brand promise

S E R V I C E

EXPERT GUIDANCE

curating product and styling recommendations beyond what a shopper can research online

SUPPORT A CONSISTENT BRAND EXPERIENCE

with the right visual merchandising, stocking levels, and store aesthetic

REMOVE FRICTION

from the experience with fast,convenient returns and check out

E X P E R I E N C E

LIVE YOUR BRAND

with a compelling, differentiated and consistent experience in-store

PROVIDE THERIGHT AMBIANCE

that is brand-appropriate

PERSONALIZE SERVICES AND OFFERINGS

to what best delights the target consumer and builds loyalty

Source: GGP Strategy & Analy t ics .

13

P R O D U C T

LUXURY TRADITIONAL APPAREL FAST FASHION DEPARTMENT STORE

VA

LUE

TORY BURCH

KATE SPADECOACH

NORDSTROM

HOT TOPIC

ZARA

H&MFOREVER 21

TALBOTS

J.CREW

EXPRESSJC PENNEY

MACY’SA&F

GAP

OLD NAVY

AEO

ARITZIA

BANANA REPUBLIC

J.J ILL

DVF

NEIMAN MARCUS

PRADA

GUCCI

LOUIS VUITTON

VA

LUE

PE

RC

EP

TIO

N

PRODUCT ASSORTMENT

LUX

UR

Y

BASICS SPECIALTY / DESIGNER

Sources: GGP Strategy & Analy t ics .

14

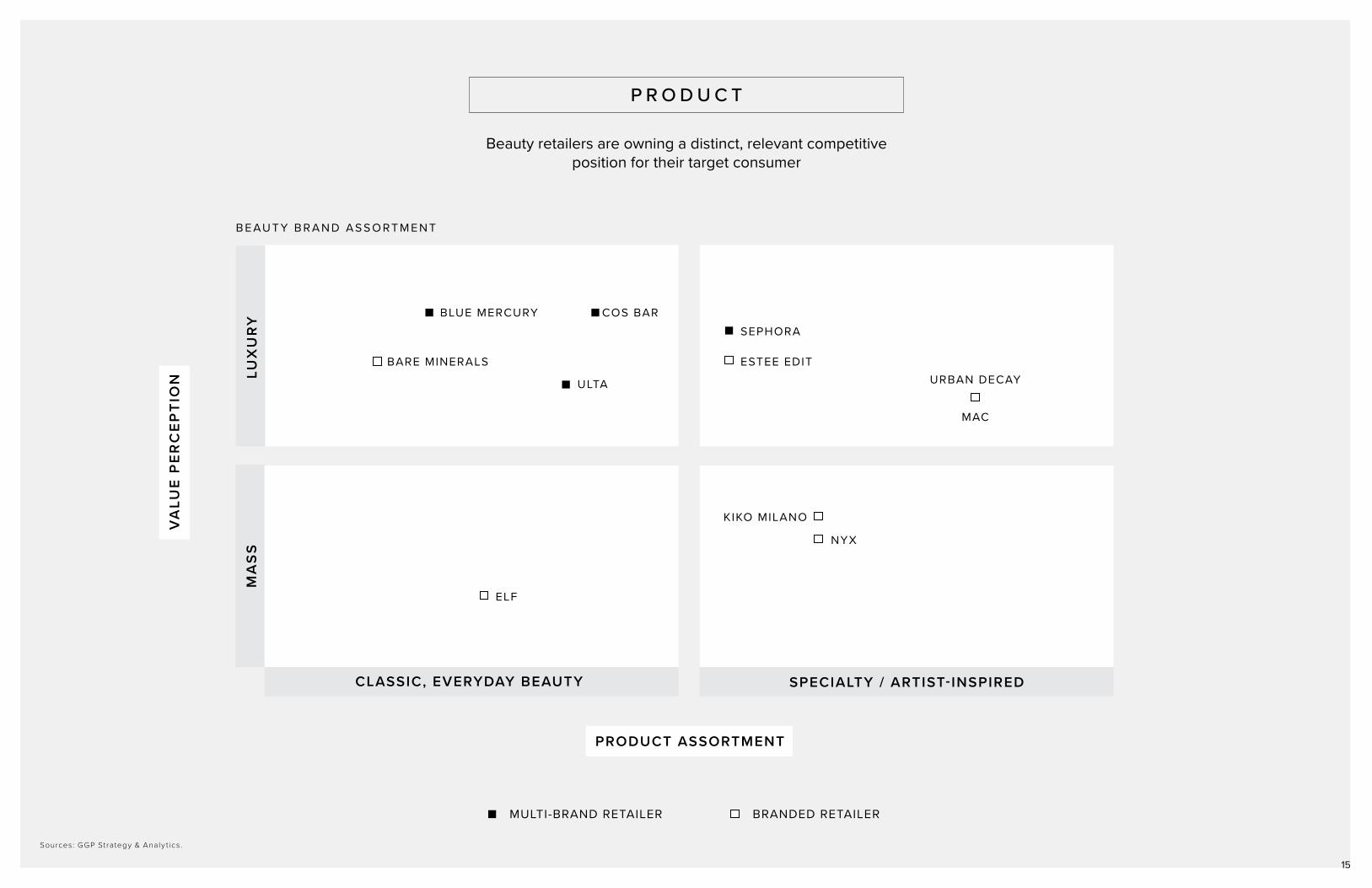

P R O D U C T

Beauty retailers are owning a distinct, relevant competitive position for their target consumer

Sources: GGP Strategy & Analy t ics .

MULTI-BRAND RETAILER BRANDED RETAILER

B E AU T Y B R A N D AS S O R T M E N T

MA

SS

VA

LUE

PE

RC

EP

TIO

N

PRODUCT ASSORTMENT

LUX

UR

Y

CLASSIC, EVERYDAY BEAUTY SPECIALTY / ARTIST-INSPIRED

BLUE MERCURY

BARE MINERALS

ULTA

COS BAR

SEPHORA

ESTEE EDITURBAN DECAY

MAC

NYX

KIKO MILANO

ELF

15

S E R V I C E

To generate sales retailers need knowledgeable,skilled staff to meet consumer expectations

Q: What do you value most when you are shopping in a retail store?

Q: When helped by a knowledgeable associate, how likely are you to buy?

Q: If you try on clothes in a dressing room and find you need a different size or color – but no associate is available to help, how often do you consider abandoning the dressing room and leaving the store?

PROMPT SERVICE

PERSONALIZED EXPERIENCE

SMART RECOMMENDATIONS

47%

26%

17%

0% 10% 20% 30% 40% 50%

EVERYTIME

SOMETIMES

NEVER

21%

NOT LIKELY

12%

50%

29%

Sources: T imeTrade The State of Retai l 2017

16

LIKELY

88%

S E R V I C E

Constraining SG&A prohibits sufficient sales associates on the floor

PWC 2014 -2016 Retai l and Consumer Insight Benchmarking Studies

M E D I A N S G & A AS A % O F S A L E S N E T S A L E S G R OW T H

24

23

22

21

20

19

18

17

16

15

20

15

10

5

0

2009 2010 2011 2012 2013 2014 2015

3.5%

7.5%

9.4%7.8%

3.6%

5.7%

3.8%

SG&A AS A % OF SALES NET SALES GROWTH

7 8 % o f c o n s u m e r s s a y t h e y w a n t s a l e s a s s o c i a t e s w i t h d e e p k n o w l e d g e o f t h e p r o d u c t r a n g e

17

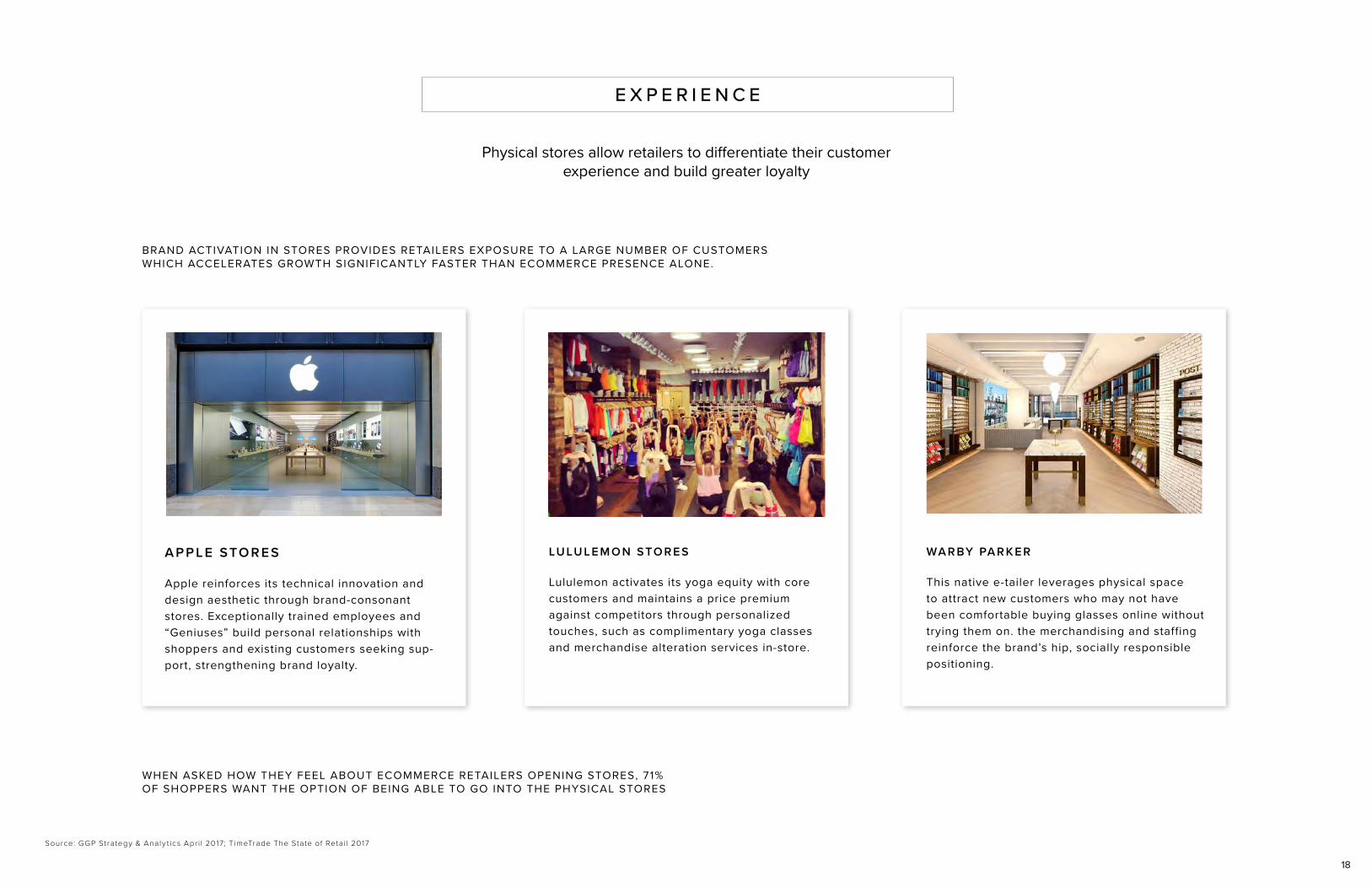

E X P E R I E N C E

Physical stores allow retailers to differentiate their customer experience and build greater loyalty

Source: GGP Strategy & Analy t ics Apr i l 2017; T imeTrade The State of Retai l 2017

BRAND ACTIVATION IN STORES PROVIDES RETAILERS EXPOSURE TO A LARGE NUMBER OF CUSTOMERSWHICH ACCELERATES GROWTH SIGNIFICANTLY FASTER THAN ECOMMERCE PRESENCE ALONE.

WHEN ASKED HOW THEY FEEL ABOUT ECOMMERCE RETAILERS OPENING STORES, 71%OF SHOPPERS WANT THE OPTION OF BEING ABLE TO GO INTO THE PHYSICAL STORES

A P P L E S TO R E S

Apple reinforces its technical innovation and design aesthetic through brand-consonant stores. Exceptionally trained employees and “Geniuses” build personal relationships with shoppers and existing customers seeking sup-port, strengthening brand loyalty.

LU LU L E M O N S TO R E S

Lululemon activates its yoga equity with core customers and maintains a price premium against competitors through personalized touches, such as complimentary yoga classes and merchandise alteration services in-store.

WA R BY PA R K E R

This native e-tailer leverages physical space to attract new customers who may not have been comfortable buying glasses online without trying them on. the merchandising and staffing reinforce the brand’s hip, socially responsible positioning.

18

E X P E R I E N C E

Physical stores allow retailers to differentiate their customer experience and build greater loyalty

Source: GGP Strategy & Analy t ics Apr i l 2017; T imeTrade The State of Retai l 2017

BRAND ACTIVATION IN STORES PROVIDES RETAILERS EXPOSURE TO A LARGE NUMBER OF CUSTOMERSWHICH ACCELERATES GROWTH SIGNIFICANTLY FASTER THAN ECOMMERCE PRESENCE ALONE.

Z A R A

Zara puts customers first, actively mining feedback for product and experience insights. To cater to its millennial consumers, Zara uses technology like RFID tags and self-service checkouts to enhance inventory visibility and remove friction from the shopping experience, enabling employees to focus on assisting customers with their styling needs.

F O OT LO C K E R

Footlocker revitalized its merchandising and in-store experience with a focus on active performance and becoming more brand and trend-focused. The refreshed store features sleek lighting and dark interiors, letting the product shine.

P R I M A R K

Primark offers fast fashion, merchandised by occasion at very low prices. Its dynamic, vibrant aesthetic engages shoppers with video walls, hip seating areas, and neon signage. They do not sell online but digitally engage consumers via Primania, where brand fans post their looks to inspire other shoppers.

19

B R I C K S & C L I C K S W I N

Total Sales (billions)

% of Total Sales

$4,200 91.0% Direct brick and mortar sales

+ $97 2.3% Online sales from Retailers with Brick and Mortar presence (Omni-channel)

$4,297 93.3% Brick and mortar related sales

+ $139 3.6% Mail order and E-commerce Auction sales

+ $29 0.6% Non-merchandise receipts ( including shipping, service charges)

+ $169 3.6% Pure-play E-commerce

$4,634 100% Total retail sales

B R I C K A N D M O R T A R C A P T U R E S 9 3 % O F R E T A I L S A L E S

21Source: ICSC analysis of 2015 U.S. Census data 21Sources: 2015 U.S . Census Retai l Trade Sales Annual Repor ts & ICSC Research

Pure Play E-commerce

Sales

Non Merchandise Receipt: (shipping & handling, auction commissions and other costs)

Mail Order & E-Commerce Auction Sales

Brick & Mortar Online Sales

Other Sales $434 B 9.2% of Total

Brick & Mortar In-Store Sales

$4.2 T

22

CUSTOMER ACQUISTITION COSTS

LAST MILE OF DISTRBIUTION

UPSELLING IN BRICKS AND MORTAR STORES

O N E - C H A N N E L G E N E R A T E S H I G H E R S A L E S

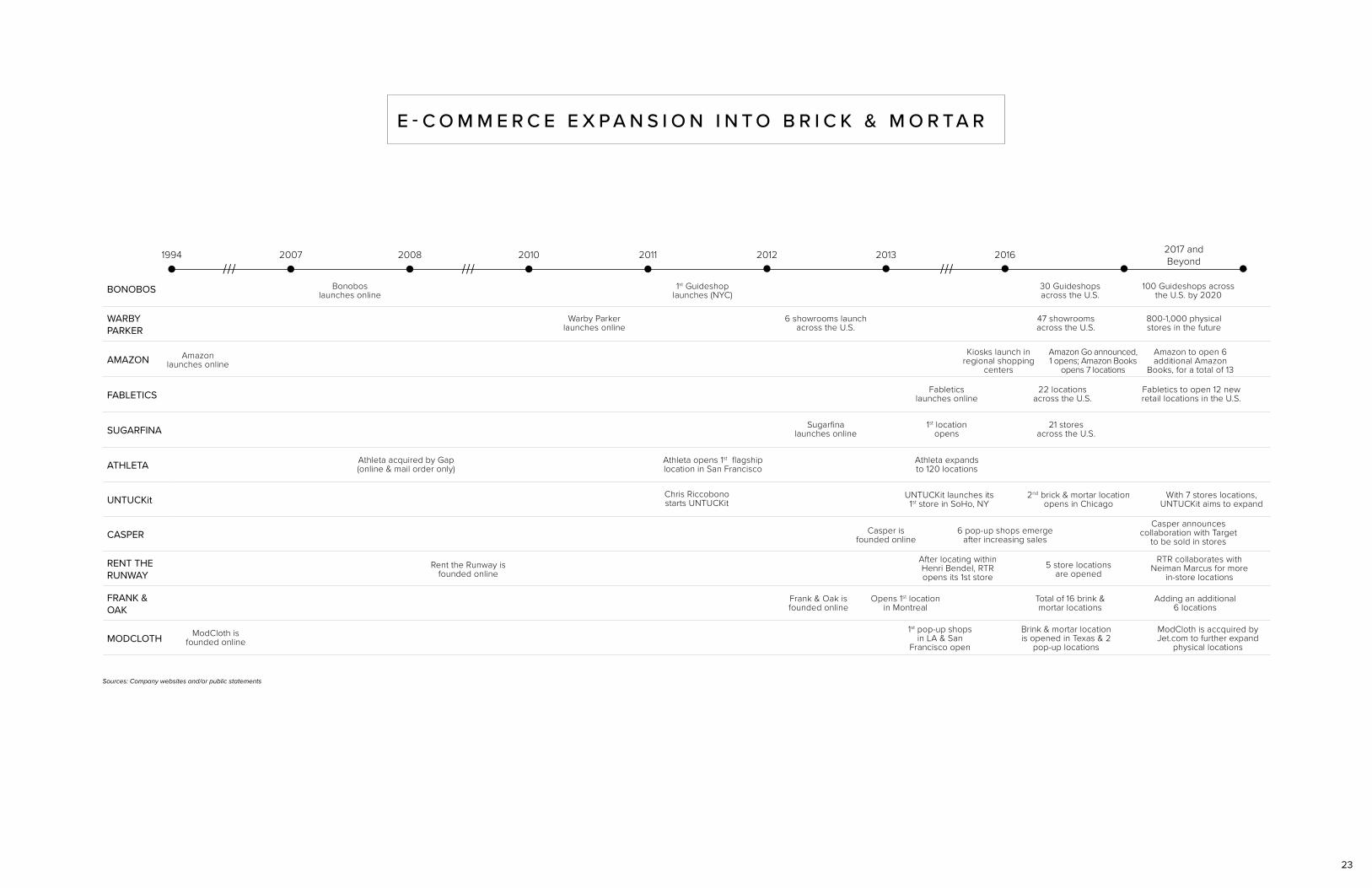

BONOBOS

WARBY PARKER

AMAZON

FABLETICS

SUGARFINA

ATHLETA

UNTUCKit

CASPER

RENT THE RUNWAY

FRANK & OAK

MODCLOTH

1994 2007 2008 2010 2011 2012 2013 2016 2017 and Beyond

Athleta expands to 120 locations

Kiosks launch in regional shopping

centers

Amazon Go announced, 1 opens; Amazon Books

opens 7 locations

22 locations across the U.S.

Fabletics to open 12 new retail locations in the U.S.

21 stores across the U.S.

100 Guideshops across the U.S. by 2020

800-1,000 physical stores in the future

47 showrooms across the U.S.

Amazon to open 6 additional Amazon

Books, for a total of 13

1st Guideshop launches (NYC)

30 Guideshops across the U.S.

Athleta opens 1st flagship location in San Francisco

6 showrooms launch across the U.S.

Sugarfina launches online

Fabletics launches online

1st location opens

Amazonlaunches online

ModCloth is founded online

1st pop-up shops in LA & San

Francisco open

Brink & mortar location is opened in Texas & 2

pop-up locations

ModCloth is accquired by Jet.com to further expand

physical locations

Rent the Runway is founded online

After locating within Henri Bendel, RTR opens its 1st store

5 store locations are opened

Frank & Oak is founded online

Opens 1st location in Montreal

Total of 16 brink & mortar locations

Adding an additional 6 locations

RTR collaborates with Neiman Marcus for more

in-store locations

Chris Riccobono starts UNTUCKit

UNTUCKit launches its 1st store in SoHo, NY

Casper is founded online

6 pop-up shops emerge after increasing sales

Casper announces collaboration with Target

to be sold in stores

2nd brick & mortar location opens in Chicago

With 7 stores locations, UNTUCKit aims to expand

Bonoboslaunches online

Athleta acquired by Gap (online & mail order only)

Warby Parker launches online

E - C O M M E R C E E X P A N S I O N I N T O B R I C K & M O R TA R

Sources: Company websites and/or public statements

/// /// ///

23

$1.27T $1.46T $1.51T

2012

$1.39T

20112010

$1.32T

2009

$1.65T$1.57T

2013 2014 2015200820072006

$1.32T$1.33T$1.29T

Willi

ams

Sono

ma,

Inc.

*

Urb

an O

utfit

ters

, Inc

.

J.Cre

w

Appl

e

Nei

man

Mar

cus

Aber

crom

bie

& Fi

tch

Co.

New

Yor

k &

Com

pany

Nor

dstro

m

Cabe

la’s

The

Child

ren’

s Pl

ace

Lulu

lem

on

Asce

na R

etai

l Gro

up

Mac

y’s

Fini

sh L

ine

Gap

, Inc

.

L Br

ands

Zum

iez

Hud

son’

s Ba

y Co

mpa

ny

Foot

lock

er

Gam

eSto

p

Gym

bore

e

J.C.P

enne

y

Dic

k's

Spor

ting

Goo

ds

Chic

o's

FAS,

Inc.

PacS

un

Mic

hael

Kor

s

Tiffa

ny &

Co.

franc

esca

's

5%6%7%8%10%12%12%13%13%13%14%15%16%16%18%18%19%19%20%

22%22%25%26%

30%

37%38%38%

52%

19%Avg.

Source: : US Depar tment of Labor Bureau of Labor Stat is t ics: Personal Income and i t s Dis t r ibut ion. Categor ies include Furni ture and Furnishings, Glassware, Tableware, and utensi ls , Spor t ing Equipment , Recreat ional Books, Musical Ins t ruments , Jewelr y, Luggage, Telephone equipment , Clothing and Footwear, Personal Care Produc ts , and Food Ser v ices. eMarketer Retai l Index . *Wi l l iams Sonoma eCommerce includes regis t r y sales;

C O N S U M E R S P E N D I N G I S U P

N E A R LY A L L R E T A I L E R S H A V E F U L LY F U N C T I O N I N G E C O M M E R C E S I T E S

F Y 2 0 1 6 E - C O M M E R C E P E N E T R A T I O N A S A % O F T O T A L S A L E S

9 -Y E A R C A G R

+ 2 . 8 %

C O N S U M E R S S H I F T I N G C H A N N E L S D O E S N O T E X P L A I N R E T A I L E R P E R F O R M A N C E .

$1.27T $1.46T $1.51T

2012

$1.39T

20112010

$1.32T

2009

$1.65T$1.57T

2013 2014 2015200820072006

$1.32T$1.33T$1.29T

Will

iam

s So

nom

a, In

c.*

Urb

an O

utfit

ters

, Inc

.

J.C

rew

App

le

Nei

man

Mar

cus

Abe

rcro

mbi

e &

Fitc

h C

o.

New

Yor

k &

Com

pany

Nor

dstr

om

Cab

ela’

s

The

Chi

ldre

n’s

Plac

e

Lulu

lem

on

Asc

ena

Reta

il G

roup

Mac

y’s

Fini

sh L

ine

Gap

, Inc

.

L B

rand

s

Zum

iez

Hud

son’

s B

ay C

ompa

ny

Foot

lock

er

Gam

eSto

p

Gym

bore

e

J.C

.Pen

ney

Dic

k's

Spor

ting

Goo

ds

Chi

co's

FA

S, In

c.

PacS

un

Mic

hael

Kor

s

Tian

y &

Co.

franc

esca

's

5%6%7%8%10%

12%12%13%13%13%14%15%16%16%18%18%19%19%20%22%22%

25%26%

30%

37%38%38%

52%

19%Avg.

24

O M N I C H A N N E L I S H E R E T O S TAY

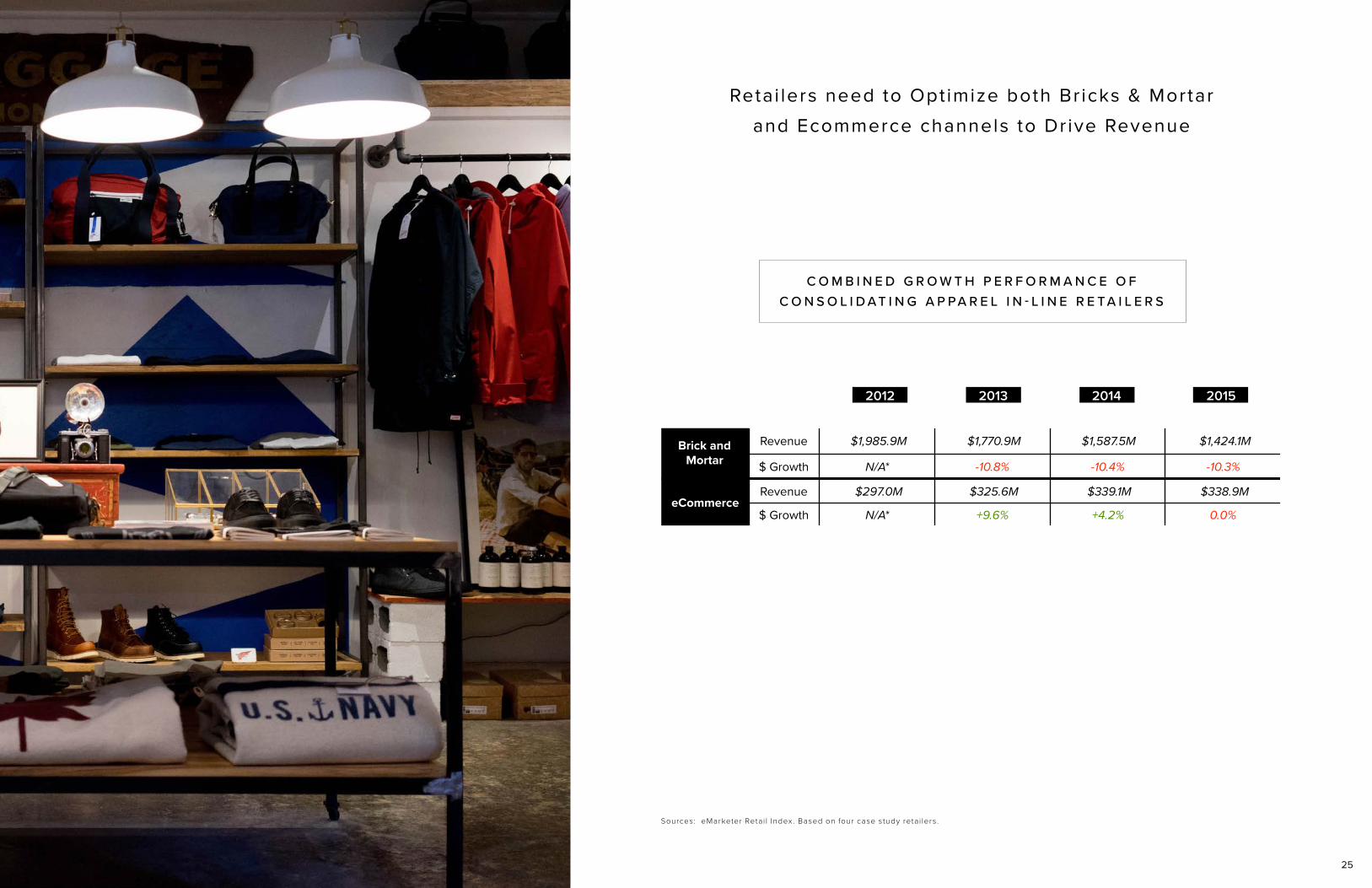

Retai lers need to Opt imize both Br icks & Mortar

and Ecommerce channels to Dr ive Revenue

Sources: eMarketer Retai l Index . Based on four case s tudy retai lers .

2012

Brick and Mortar

Revenue $1,985.9M $1,770.9M $1,587.5M $1,424.1M

$ Growth N/A* -10.8% -10.4% -10.3%

eCommerceRevenue $297.0M $325.6M $339.1M $338.9M

$ Growth N/A* +9.6% +4.2% 0.0%

Brick and Mortar

Revenue $24,935.6M $24,676.2M $24,380.0M $22,972.3M $21,156.5M

$ Growth +2.0% -1.0% -1.2% -5.8% -7.9%

eCommerceRevenue $2,750.4M $3,254.8M $3,725.0M $4106.7M $4,621.5M

$ Growth +41.0% +18.3% +14.4% +10.2% +12.5%

2013 2014 2015

2012 2013 2014 2015 2016

25

C O M B I N E D G R O W T H P E R F O R M A N C E O F C O N S O L I D A T I N G A P PA R E L I N - L I N E R E T A I L E R S

aaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaa

S H O P P I N G C E N T E R O F T H E F U T U R E

New deals in recent years have focused on non-apparel categor ies

Source/Note: GGP Strategy & Analy t ics , non-anchor mutual ly approved and/or executed deals wi th rent commencement dates af ter 12 /31 /2012.

27

N E W D E A L S B Y C A T E G O R Y

0%

25%

50%

75%

100%

2013 2017

22%27%

22%20%

18%4%

13%

7%

25%

43%

Apparel Beauty & Personal Services Entertainment Food Other

PERCENTAGE OF GLA LEASED

P E R C E N T O F

G L A L E A S E D

Apparel F & B Entertainment Other

Existing 72% 7% 0% 21%

Expansion 15% 12% 55% 18%

G L A

S E A R S R E D E V E L O P M E N T A T S T A T E N I S L A N D M A L L

B E F O R E A F T E R

S T A T E N I S L A N D M A L L R E D E V E L O P M E N T

28

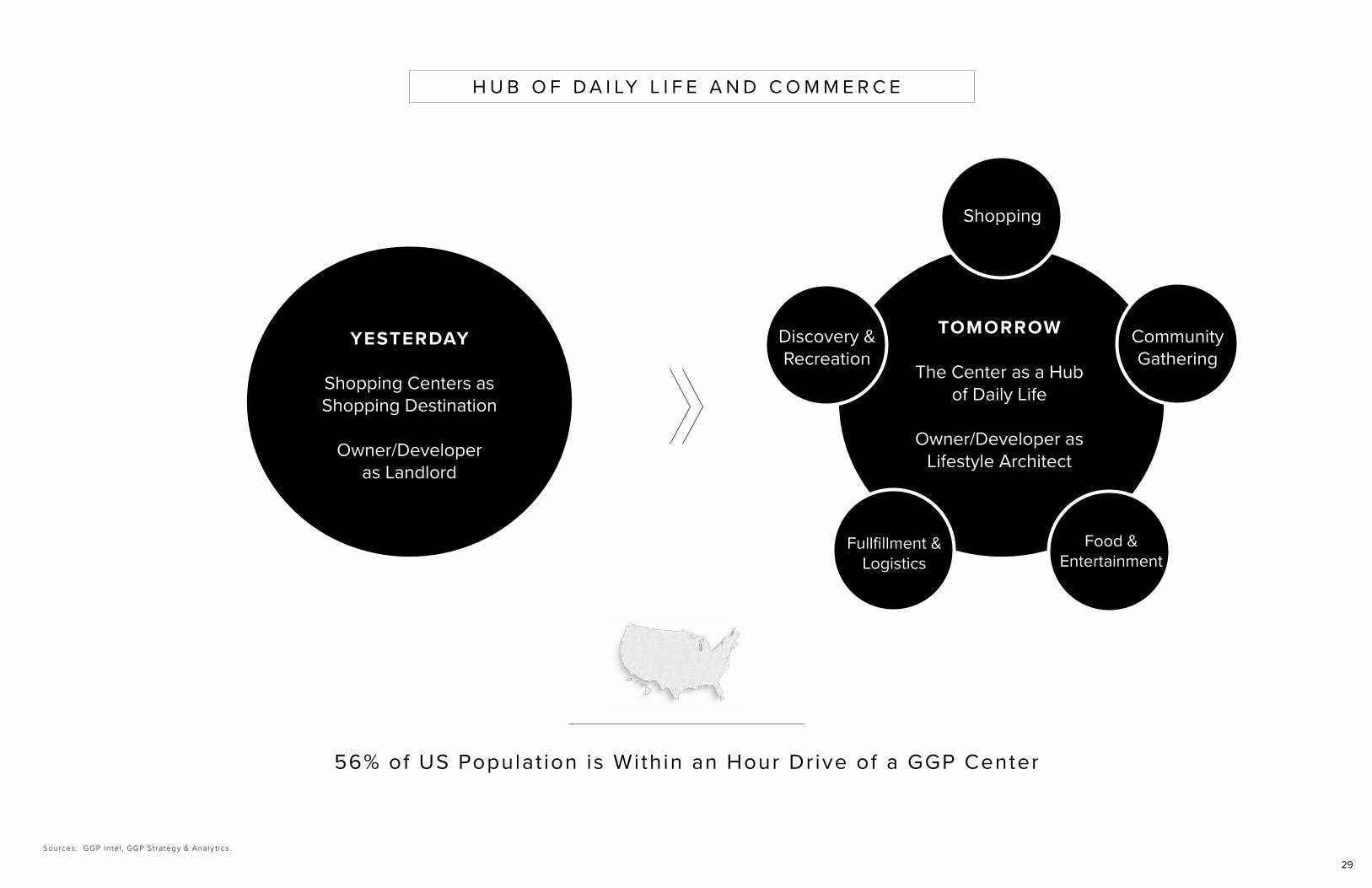

Sources: GGP Intel , GGP Strategy & Analy t ics .

YESTERDAY

Shopping Centers as Shopping Destination

Owner/Developer as Landlord

H U B O F D A I LY L I F E A N D C O M M E R C E

29

TOMORROW

The Center as a Hub of Daily Life

Owner/Developer as Lifestyle Architect

Shopping

CommunityGathering

Discovery &Recreation

Food &Entertainment

Fullfillment &Logistics

56% of US Populat ion is Within an Hour Dr ive of a GGP Center

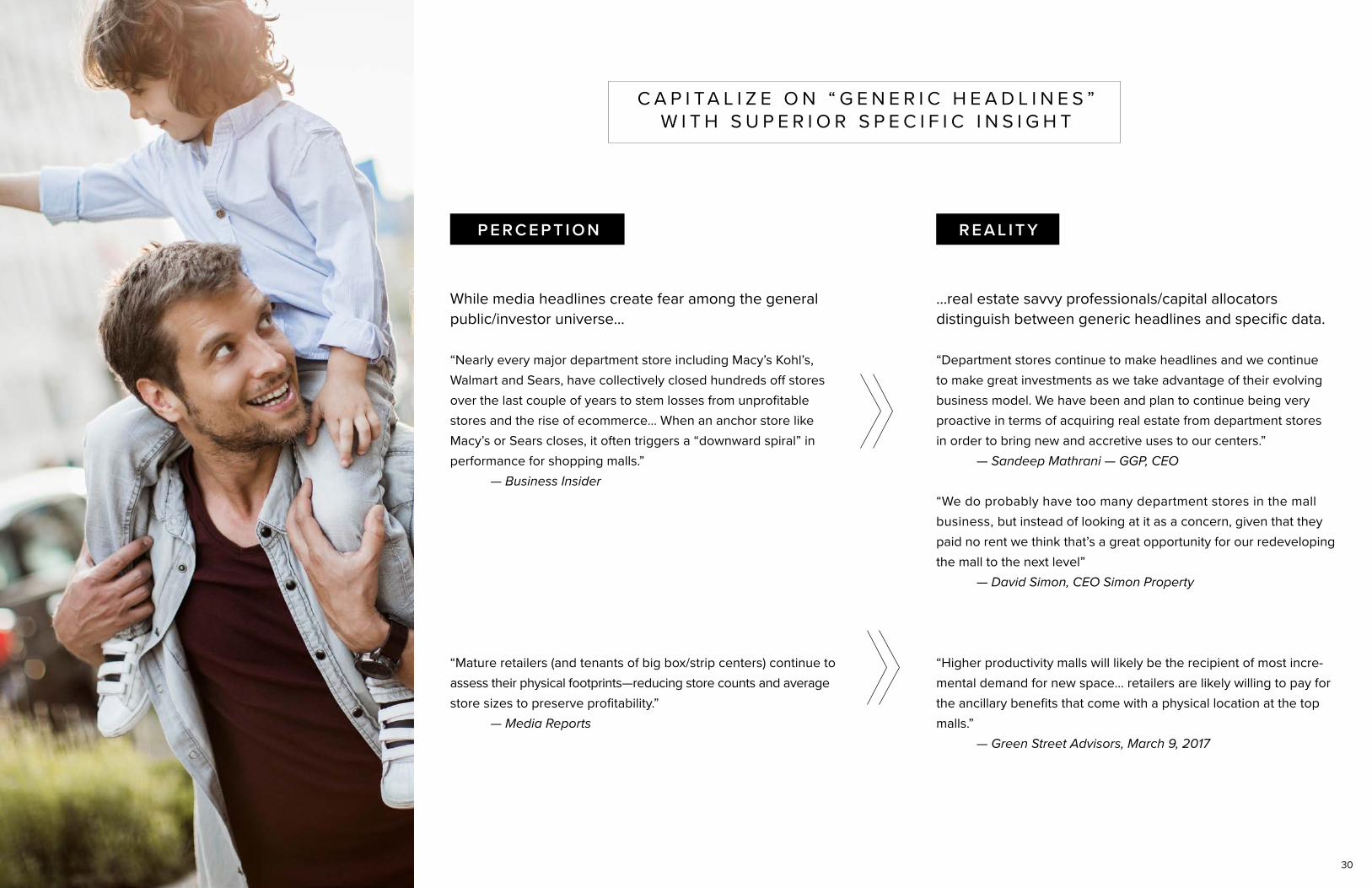

While media headlines create fear among the general public/investor universe…

“Nearly every major department store including Macy’s Kohl’s, Walmart and Sears, have collectively closed hundreds off stores over the last couple of years to stem losses from unprofitable stores and the rise of ecommerce… When an anchor store like Macy’s or Sears closes, it often triggers a “downward spiral” in performance for shopping malls.” — Business Insider

“Mature retailers (and tenants of big box/strip centers) continue to assess their physical footprints—reducing store counts and average store sizes to preserve profitability.” — Media Reports

…real estate savvy professionals/capital allocators distinguish between generic headlines and specific data.

“Department stores continue to make headlines and we continue to make great investments as we take advantage of their evolving business model. We have been and plan to continue being very proactive in terms of acquiring real estate from department stores in order to bring new and accretive uses to our centers.” — Sandeep Mathrani — GGP, CEO

“We do probably have too many department stores in the mall business, but instead of looking at it as a concern, given that they paid no rent we think that’s a great opportunity for our redeveloping the mall to the next level” — David Simon, CEO Simon Property

“Higher productivity malls will likely be the recipient of most incre-mental demand for new space... retailers are likely willing to pay for the ancillary benefits that come with a physical location at the top malls.” — Green Street Advisors, March 9, 2017

C A P I T A L I Z E O N “ G E N E R I C H E A D L I N E S ” W I T H S U P E R I O R S P E C I F I C I N S I G H T

P E R C E P T I O N R E A L I T Y

30

MICHAEL BERMANExecutive Vice President and

Chief Financial [email protected]

C O N T A C T I N F O R M A T I O N F O R W A R D - L O O K I N G S T A T E M E N T S

Certain statements made in this presentation may be deemed “forward-looking statements”

within the meaning of the Private Securities Litigation Reform Act of 1995. Although the

Company believes the expectations reflected in any forward-looking statement are based

on reasonable assumption, it can give no assurance that its expectations will be attained,

and it is possible that actual results may differ materially from those indicated by these for-

ward-looking statements due to a variety of risks, uncertainties and other factors. Such fac-

tors include, but are not limited to, the Company’s ability to refinance, extend, restructure or

repay near and intermediate term debt, its indebtedness, its ability to raise capital through

equity issuances, asset sales or the incurrence of new debt, retail and credit market condi-

tions, impairments, its liquidity demands, and economic conditions. The Company discusses

these and other risks and uncertainties in its annual and quarterly periodic reports filed

with the Securities and Exchange Commission. The Company may update that discussion

in its periodic reports, but otherwise takes no duty or obligation to update or revise these

forward-looking statements, whether as a result of new information, future developments,

or otherwise.

Investors and others should note that the Company posts this Investor Presentation on the

Investors page of its website at www.ggp.com. From time to time, the Company updates

the Investor Presentation and when it does, it will be posted on the Investors section of its

website at www.ggp.com. It is possible that the updates could include information deemed

to be material information. Therefore, the Company encourages investors, the media and

others interested in the Company to review the information posted on the Investors section

of its website at www.ggp.com from time to time.

KEVIN BERRYSenior Vice President

Investor & Public [email protected]

31