Embed Size (px)

DESCRIPTION

Financial Performance & Margin Management Issue

Citation preview

www.EthanolProducer.com

JUNE 2015

INSIDE: FUEL ETHANOL: STARTING POINT FOR REVOLUTION

EPMJune 2015

NEW CHEMISTRY 21 MMgy Facility Aims for High-Value Biotech Market

PLUSA Seller’s

Market, Still

Strategic Planning for Healthy Finances

,Page 36

Page 46

Page 52

2015: THE YEAR OF

THANKS FOR BEING SOME OF THE FIRST RETAILERS TO OFFER E15.

Growth Energy commends CENEX, Kum & Go, MAPCO, Minnoco, Murphy USA, Petro Serve USA, Protec Fuel,

Sheetz and Zarco USA for their pioneering spirit and efforts to expand consumer access to higher blends of

renewable fuels. They offer consumers a choice and savings at the pump, while investing in a homegrown industry

that supports farmers across the country.

Together we’re making progress toward the next generation of sustainable, renewable fuels.

Learn more at GrowthEnergy.org/E15

1020 E. 19th St. Wichita, KS 67214 USA

316.264.4604tramcoinc.com

The World’s Most Complete Line of Chain and Enclosed Belt Conveyors.

4 | Ethanol Producer Magazine | JUNE 2015

JUNE 2015 VOLUME 21 ISSUE 6CONTENTS

FEATURES

BUSINESS How Deals Square Up Ten companies bought 13 ethanol plants in 2013, compared to only fi ve transitions in 2014 By Tom Bryan

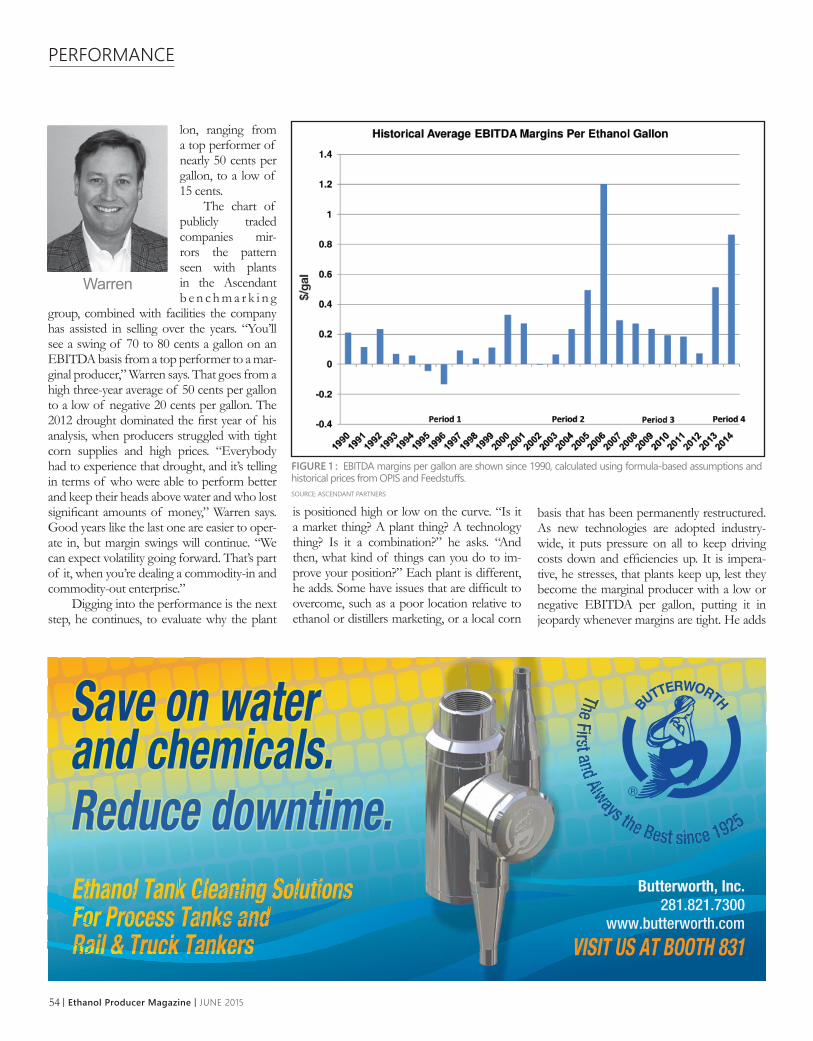

PROFITABLITY Riding the Performance Curve Lessons learned for long-term business viability By Susanne Retka Schill

36PROFILE ‘Back to the Future’ with N-butanol A Minnesota ethanol plant will be retrofi tted to produce high-value chemicals By Holly Jessen

46

MARGINS Follow the Money Refl ecting on what ethanol producers did with money earned during high profi tabilityBy Holly Jessen

62

54

52

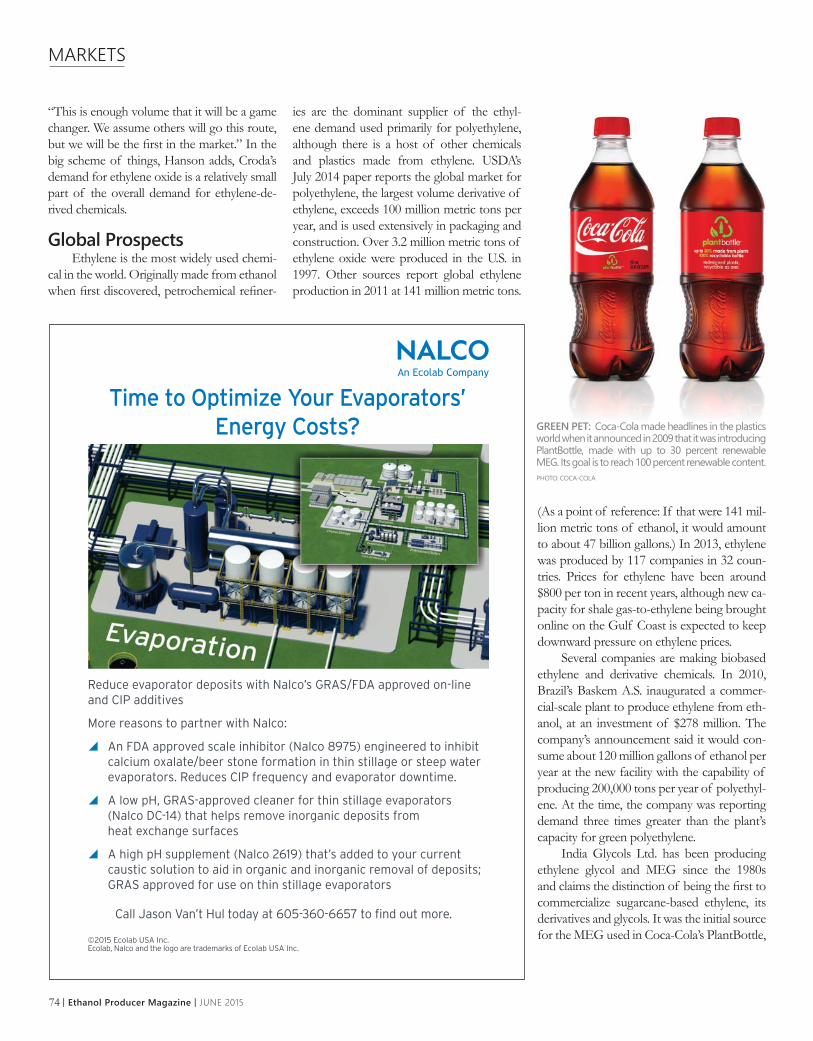

MARKETS Stepping Up to a Currency Model Companies pursue plans to turn fuel ethanol into renewable chemicals By Susanne Retka Schill

70

Reason

You’re

www.uswaterservices.comFEW Booth #413

6 | Ethanol Producer Magazine | JUNE 2015

JUNE 2015 VOLUME 21 ISSUE 6CONTENTS

Ethanol Producer Magazine: (USPS No. 023-974) June 2015, Vol. 21, Issue 6. Ethanol Producer Magazine is published monthly by BBI International. Principal Offi ce: 308 Second Ave. N., Suite 304, Grand Forks, ND 58203. Periodicals Postage Paid at Grand Forks, North Dakota and additional mailing offi ces. POSTMASTER: Send address changes to Ethanol Producer Magazine/Subscriptions, 308 Second Ave. N., Suite 304, Grand Forks, North Dakota 58203.

INVESTING New Laws, Rules Off er Options For Raising Capital Crowdfunding, SEC exemptions and amendments off er diff erent benefi ts, restrictions By Todd Taylor

EMISSIONS Small Changes Aff ect Sampling Methods Seemingly subtle changes in test methodology, plant operations can impact emissions monitoring By Edward “EJ” Juers

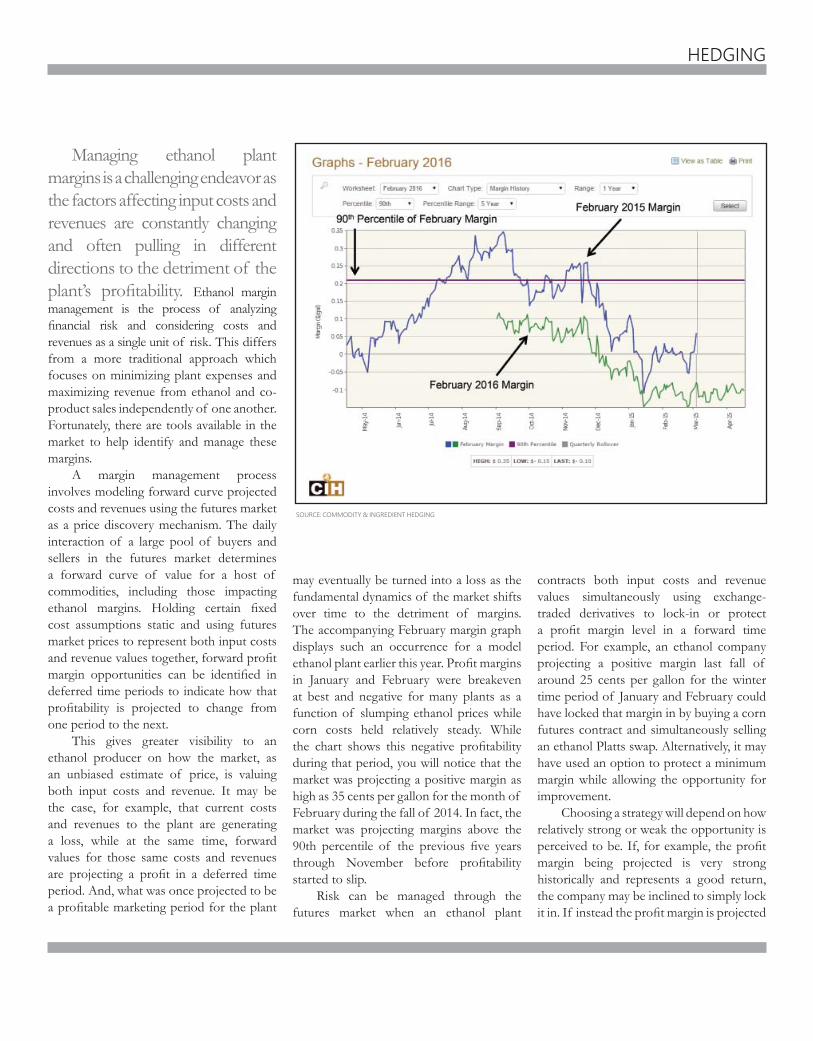

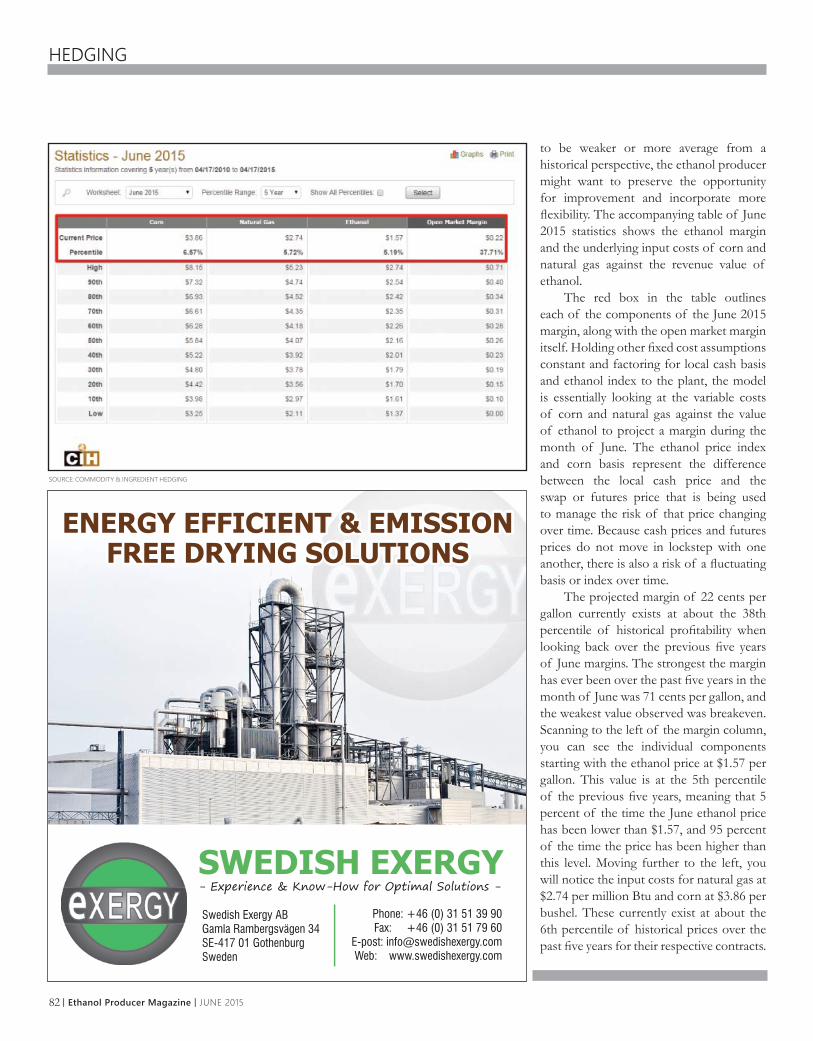

76HEDGING Market Tools Help Identify, Manage Margins Considering costs, revenues as a single unit of risk is important hedging strategy By Chip Whalen

80

CONTRIBUTIONS

FINANCE Long-Term Planning Mitigates Risks from Prolonged Downturns Financial advisors can help with lender communications By Frank Baumgardt

8884

DEPARTMENTS8 EDITOR'S NOTE Matchmaking, Money And Makeovers By Tom Bryan

9 AD INDEX

12 THE WAY I SEE IT Present Day Ethanol Trumps Good Ol' Days By Mike Bryan

13 EVENTS CALENDAR

14 VIEW FROM THE HILL Waves of Ethanol Misinformation By Bob Dinneen

16 DRIVE High Hurdle Race By Tom Buis

18 GRASSROOTS VOICE Following the Cool Guys By Ron Lamberty

20 GLOBAL SCENE End the Food Vs Fuel Debate By Bliss Baker

22 BUSINESS BRIEFS

24 COMMODITIES

28 DISTILLED

94 BUSINESS MATTERS Weathering Tight Margins By Donna Funk

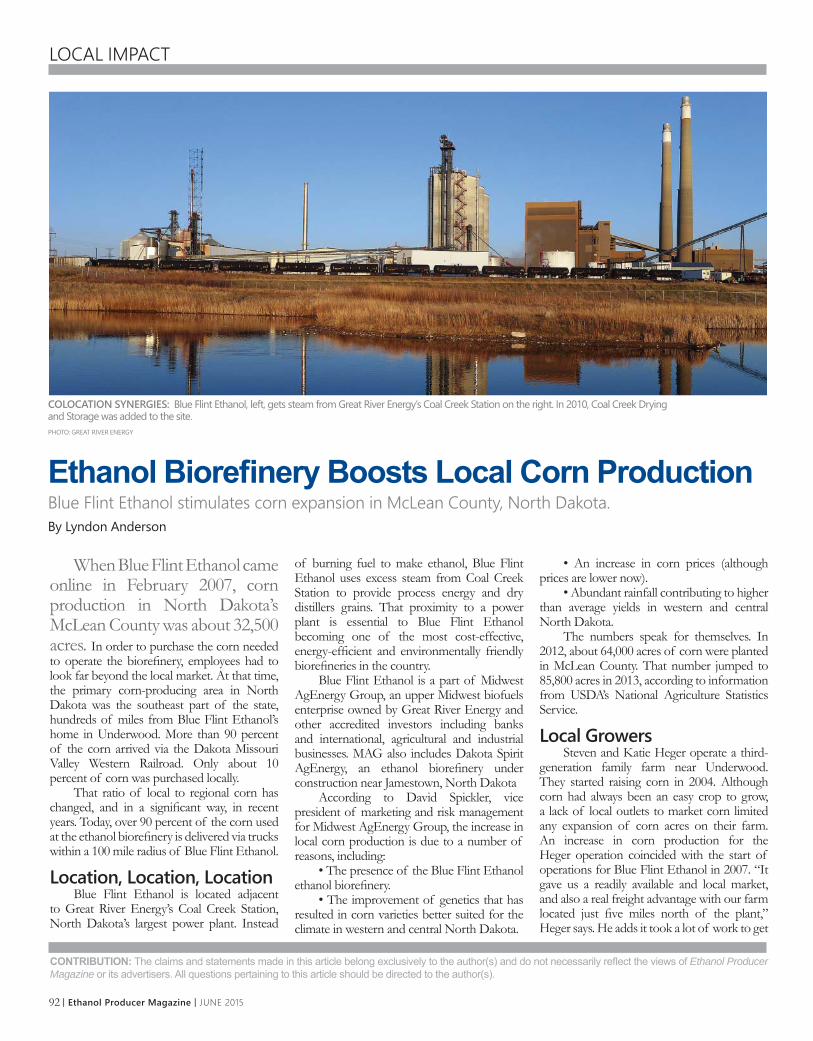

96 MARKETPLACE LOCAL IMPACT Ethanol Biorefi nery Boosts Local Corn Production Area farmers benefi t from new market, new storage option By Lyndon Anderson

92

PHOTO: KIMM ANDERSON

ON THE COVER

JUNE 2015 | Ethanol Producer Magazine | 7

VOLUME 21 ISSUE 6

TM

Customer Service Please call 1-866-746-8385 or email us at [email protected]. Subscriptions to Ethanol Producer Magazine are free of charge to everyone with the exception of a shipping and handling charge of $49.95 for anyone outside the United States. To subscribe, visit www.EthanolProducer.com or you can send your mailing address and payment (checks made out to BBI International) to: Ethanol Producer Magazine Subscriptions, 308 Second Ave. N., Suite 304, Grand Forks, ND 58203. You can also fax a subscription form to 701-746-5367. Back Issues, Reprints and Permissions Select back issues are available for $3.95 each, plus shipping. Article reprints are also available for a fee. For more information, contact us at 866-746-8385 or [email protected]. Advertising Ethanol Producer Magazine provides a specifi c topic delivered to a highly targeted audience. We are committed to editorial excellence and high-quality print production. To fi nd out more about Ethanol Producer Magazine advertising opportunities, please contact us at 866-746-8385 or [email protected]. Letters to the Editor We welcome letters to the editor. Send to Ethanol Producer Magazine Letters to the Editor, 308 2nd Ave. N., Suite 304, Grand Forks, ND 58203 or email to [email protected]. Please include your name, address and phone number. Letters may be edited for clarity and/or space.

COPYRIGHT © 2015 by BBI InternationalPlease recycle this magazine and remove inserts or samples before recycling

EDITORIALPresident & Editor in Chief

Tom Bryan [email protected]

Vice President of Content & Executive EditorTim Portz [email protected]

Managing EditorHolly Jessen [email protected]

Senior EditorSusanne Retka Schill [email protected]

News EditorErin Voegele [email protected]

Copy Editor

Jan Tellmann [email protected]

ARTArt Director

Jaci Satterlund [email protected] Designer

Raquel Boushee [email protected]

PUBLISHINGChairman

Mike Bryan [email protected]

Joe Bryan [email protected]

SALES Vice President of Operations

Matthew Spoor [email protected] Business Development Director

Howard Brockhouse [email protected] Account Manager/Bioenergy Team Leader

Chip Shereck [email protected] Account Manager

Jeff Hogan [email protected] Account Manager

Tami Pearson [email protected] Sales & Marketing Director

John Nelson [email protected] Circulation Manager

Jessica Beaudry [email protected] c & Marketing Coordinator

Marla DeFoe [email protected]

Ethanol Producer IS THE

#1 SOURCEOF NEWS AND INFORMATION ABOUT ETHANOL PRODUCERS AND INDUSTRY PROSWith subscribers in more than 46 countries, Ethanol Producer Magazine is the world’s largest and longest-running ethanol magazine.• The only ethanol magazine in the world• 11,250+ circulation• Distributed monthly to every ethanol plant in North America• We’ll create your advertisement for free of charge

8 | Ethanol Producer Magazine | JUNE 2015

FOR INDUSTRY NEWS: WWW.ETHANOLPRODUCER.COM OR FOLLOW US: TWITTER.COM/ETHANOLMAGAZINE

The U.S. ethanol industry has appreciably matured in the past six years, but it hasn’t lost its youthful propensity to take chances and explore new things. American ethanol producers are, today, among the most effi cient, disciplined and fi nancially sophisticated agribusinesses in the world. At the same time, the industry’s 200-plus facilities, still owned by roughly 100 different companies, are hungry for innovation, open to change and fl exible enough to look at almost anything. This month’s issue of Ethanol Producer Magazine examines the ethanol industry’s current fi nancial condition against the backdrop of its remarkable affi nity for adaptation.

Our inspection of money management in the ethanol business begins with an instructive look at recent mergers and acquisitions within the sector. In “How Deals Square Up,” on page 36, we see that ethanol plant M&A has historically been driven by distress and more transactions occur on the heels of downturns than after profi table periods. For comparison, there were nearly three dozen ethanol plants sold after the industry’s well-chronicled 2008-’09 downturn, but just fi ve transactions during and after the recent period of record margins (see “Follow the Money” on page 62 for more insight on what producers did, or plan to do, with last year’s earnings).

Investment bankers tell us, however, that fi nancial distress isn’t the only thing that prompts ethanol plants to be sold. One recent deal, for example, included a seller that was a nonlong-term investor looking to cash out on a healthy asset. Another transaction was based on a strategy to convert a relatively small ethanol plant into a facility that can produce higher-margin chemicals, which is the focus of our cover story, “‘Back to the Future’ with N-butanol,” on page 46. In this feature, EPM Managing Editor Holly Jessen goes inside Green Biologic’s recent acquisition of Central Minnesota Ethanol Co-op in Little Falls, Minnesota. Green Biologic’s plan is to retrofi t the plant to produce n-butanol and acetone while still making some ethanol. The nature of the deal illustrates the incredible versatility of dry-mill ethanol plants and shows us that acquisitions can be carried out with real people in mind. The deal was structured in a way that benefi tted existing shareholders, plant employees and area farmers.

We look more downstream at biobased chemicals in “Stepping Up to a Currency Molecule,” on page 70. In this piece, EPM Senior Editor Susanne Retka Schill reports on how a growing global demand for sustainable products is opening a huge door for renewable chemicals, some of which can be derived from, or made with, ethanol.

Finally, we look closely at the overall fi nancial state of U.S. ethanol plants and how producers are leveraging the hard lessons of their recent past to run their businesses better. We learn in “Riding the Performance Curve,” on page 52, that most producers are still fi nancially comfortable, operating with healthy levels of working capital and generally looking at ways to reinvest in new assets and next-stage technologies.

EDITOR'S NOTE

Matchmaking, Money And Makeovers

Tom BryanPresident & Editor in [email protected]

JUNE 2015 | Ethanol Producer Magazine | 9

ADVERTISER INDEX

2015 Fuel Ethanol Conference & Expo 26-272015 National Advanced Biofuels Conference & Expo 974B Components, Ltd. 100ACE American Coalition For Ethanol 19 & 29Arisdyne Systems 39 BBI Project Development 95BetaTec Hop Products 10-11Bilfi nger Water Technologies 38Buckman 28Butterworth, Inc. 54Cereal Process Technologies 42Cloud/Sellers Cleaning Systems 78Direct Automation 50DuPont Industrial Biosciences 45Eco-Energy Inc. 79EcoEngineers 90Ethanol 101 59Fagen Inc. 91Fluid Quip Process Technologies, LLC 17Fuel Ethanol Industry Directory 33GEA Westfalia Separator 13Growth Energy 2Hengye USA 51Hydro-Klean LLC 61ICM, Inc. 86Interra Global Corporation 66INTL FCStone Inc. 43Iowa Economic Development Authority 68J.C. Ramsdell Enviro Services, Inc. 22Lallemand Biofuels & Distilled Spirits 34Leaf Technologies 30Louis Dreyfus 73Mason Manufacturing, LLC 55Minnesota Bio-Fuels Association 65

VOLUME 21 ISSUE 6

Mist Chemical & Supply Company 48Nalco, an Ecolab Company 74Natwick Associates Appraisal Services 67NCAT, Inc. 31New Holland Agriculture 15North American Industrial Services 23Novozymes 35Ocean Park Advisors 41Pan American Hydrogen, Inc. 72Phibro Ethanol Performance Group 99POET-DSM Advanced Biofuels 98Premium Plant Services, Inc. 83ProQuip, Inc. 40Renewable Fuels Association 87RPMG, Inc 75 Seneca Companies 49Solenis LLC 21Sukup Manufacturing Co. 69Swedish Exergy AB 82Syngenta: Enogen 60Thermal Refractory 64Tower Performance, Inc. 44Tramco, Inc. 3U.S. Water Services 5Valicor Separation Technologies 57WestAgro Executive Brands 56WINBCO 58Zeochem LLC 93

12 | Ethanol Producer Magazine | JUNE 2015

Some long for the good ol’ days, when cars were simple and you could do much of the repair work yourself. When in the evening the 9 o’clock whistle blew and you had to get home, or writing a letter meant pen and paper.

Myself, I’m glad we no longer live in the good ol’ days. I don’t want to work on my car. The cars today are much more reliable and more fun to drive. I really am not terribly concerned that kids spend more time on the computer than they do playing outside. It’s the age we live in and they are preparing themselves for a new and exciting future. Frankly, I like being able to send an email rather than sit down and handwrite a letter, and I am a better communicator as a result.

I’ve heard some say that they long for the good ol’ days of the ethanol industry, when it was young and we all felt a sense of comradery and we knew who the enemy was. Frankly, I’m not interested in reliving the past of the ethanol industry either. It was often painful. We are much more sophisticated now, we have years of research under our belts and can stand toe-to-toe with the enemy rather than throw rocks and sticks at them, as that’s all we had back then.

I don’t think there is a better time to be in this industry, with technology moving forward at breakneck pace. We have matured and replaced the rocks and sticks with billions of miles of trouble-free consumer use and reams of data that substantiate the viability and performance of ethanol. We have a whole new generation of bright young talent working in the industry who will carry us into the next tier of success.

Many of us remember when a woman named Roberta Nichols from Ford Motor Co. introduced the fi rst fl exible fuel vehicle. Exciting as it was, it seems so long ago now, given where things are with E85 today. The good ol’ days sometimes consisted of organizing corn farmers to stand at service stations handing out

ethanol brochures and offering to fi ll the customer’s car up for them, just to get product recognition. While it was fun at the time, I don’t want to do that anymore.

There are lots of things that had to be done to get the industry where it is today, that most of us who did them would not really want to do again. The young talent in the industry today are creating their own good ol’ days and a decade or two from now will likely write a column reminiscing about those days, glad that they don’t have to relive them.

Personally, I’m happy where the industry is today, still with challenges, still with much work to be done, but with the ability to do that work on a much more level playing fi eld. We have set aside the rocks and sticks and replaced them irrefutable facts and a mountain of well-researched data. We have moved from a niche industry to a major contributor to energy security, cleaner air and economic stability.

So for me, while I may look back from time to time with fond memories of the battles and the things we did to build the industry, I think now is the best time ever to be in the ethanol industry. Besides, there is little need to look back, because, before you know it, today will be one of the good ol’ days.

That’s the way I see it.

Present Day EthanolTrumps Good Ol’ Days By Mike Bryan

Author: Mike BryanChairman, BBI International

THE WAY I SEE IT

ACE ConferenceAugust 19-21, 2015Omaha, NebraskaHilton OmahaACE’s annual conference is tailored to the interests and needs of the people of ethanol, the folks in the trenches. It’s a gathering of ACE’s commitment to connect ethanol producers with the farmers, researchers, retailers, and support businesses to continue what all of them started a long time ago. It’s also an excellent place to learn and share ideas. And, it has all the fun of a family reunion.605-334-3381www.ethanol.org/events/conference

National Advanced Biofuels Conference & ExpoOctober 26-28, 2015Hilton OmahaOmaha, NebraskaProduced by BBI International, this national event will feature the world of advanced biofuels and biobased chemicals—technology scale-up, project fi nance, policy, national markets and more—with a core focus on the industrial, petroleum and agribusiness alliances defi ning the national advanced biofuels industry.866-746-8385www.advancedbiofuelsconference.com

International Biomass Conference & ExpoApril 11-14, 2016Charlotte, North CarolinaOrganized by BBI International and produced by Biomass Magazine, this event brings current and future producers of bioenergy and biobased products together with waste generators, energy crop growers, municipal leaders, utility executives, technology providers, equipment manufacturers, project developers, investors and policy makers. It’s a true one-stop shop—the world’s premier educational and networking junction for all biomass industries. 866-746-8385www.biomassconference.com

International Fuel Ethanol Workshop & ExpoJune 20-23, 2016Wisconsin Center, Milwakee, WINow in its 32nd year, the FEW provides the ethanol industry with cutting-edge content and unparalleled networking opportunities in a dynamic business-to-business environment. As the largest, longest running ethanol conference in the world, the FEW is renowned for its superb programming—powered by Ethanol Producer Magazine —that maintains a strong focus on commercial-scale ethanol production, new technology, and near-term research and development. 866-746-8385www.fuelethanolworkshop.com

EVENTS CALENDAR

2019

T

engineering for a better world

GEA GroupCentrifuges & Separation EquipmentPhone: 201-767-3900 · Toll-Free: 800-722-6622www.gea.com

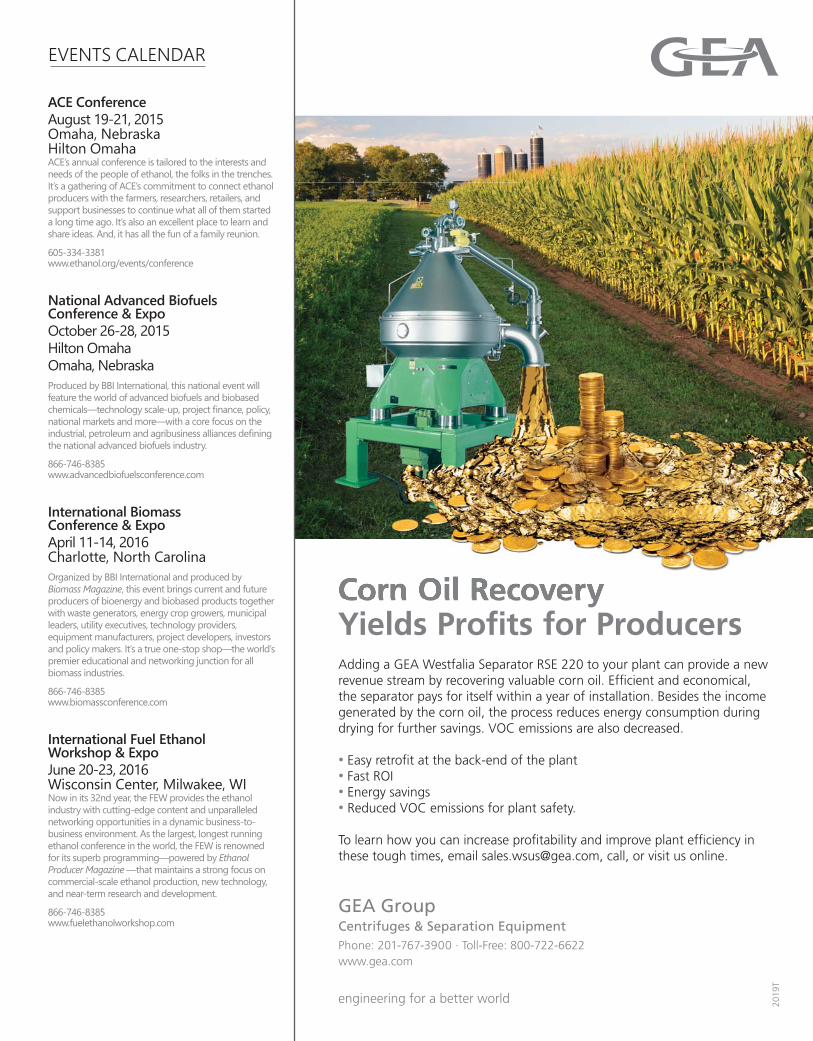

Adding a GEA Westfalia Separator RSE 220 to your plant can provide a new revenue stream by recovering valuable corn oil. Effi cient and economical, the separator pays for itself within a year of installation. Besides the income generated by the corn oil, the process reduces energy consumption during drying for further savings. VOC emissions are also decreased.

• Easy retrofi t at the back-end of the plant • Fast ROI• Energy savings • Reduced VOC emissions for plant safety.

To learn how you can increase profi tability and improve plant effi ciency in these tough times, email [email protected], call, or visit us online.

Corn Oil Recovery Yields Profits for Producers

14 | Ethanol Producer Magazine | JUNE 2015

There is nothing quite like the feeling of being on the water on a clear summer day. Tennis champion Rafael Nadal once described it as, “I like fi shing. Not actual fi shing, I like the peace and quiet of being at sea. It’s different.” Boating is a beloved pastime for many Americans, whether taking part in fi shing, water skiing or simply enjoying the exhilarating feeling of cruising on the water.

Over the years, a lot of misinformation has been creating waves when it comes to ethanol use in marine engines. In a sign of their desperation, API actually ran ads last year claiming that ethanol—and the renewable fuel standard (RFS)—will strand boaters on the water. Nothing could be further from the truth. But as the summer months rapidly approach, we must once again equip the boating community with the facts they need to cut through the wake of misinformation being churned up by the petroleum industry.

All boaters must know that E10 can safely be used in their marine engines. Oftentimes marine publications will exaggerate concerns about E15 marine use to vilify all ethanol blends; but E15 is not approved for use in these engines. However, E10 is perfectly fi ne for marine engines. It doesn’t matter whether their boat has a two-stroke or four-stroke engine, an in-board or out-board motor, or a built-in or portable fuel tank.

But, don’t just take my word for it. Every marine engine manufactured today provides warranty coverage for E10. The Honda owner’s manual for the BF25A/30A Outboard Motor states that “You may use gasoline containing up to 10 percent ethanol by volume.” Additionally, Yamaha owner’s manual for the F115 notes that “Gasohol containing ethanol can be used if ethanol content does not exceed 10 percent and the fuel meets minimum octane ratings.” Manufacturers would certainly not approve a fuel

that would harm the product or the consumer. Similar language appears in the owner’s manuals for Kawasaki, Mercury Marine, OMC (Johnson/Evinrude), Pleasurecraft, Tigershark (Artco) and Tracker marine engines.

In addition to the owner’s manuals clearly approving E10, Vernon Barfi eld, former vice president and technical chairman of the National Boat Racing Association said that “There is a myth out there that 10 percent ethanol is not good for marine engines, but we have been operating for over 20 years and have not had any issues with it whatsoever.” He continues, “…there are absolutely no problems running on 10 percent ethanol.”

We now have the facts from manufacturers and experts alike. So how do we disseminate the information? The new digital age offers a plethora of opportunities to easily get the word out at very little cost. It can be as easy as posting the information on Facebook or Twitter. E-mail also offers a quick and easy way to send the information to family and friends.

But, let’s not forget traditional media and the power of one-on-one interaction. Individuals or groups can write an op-ed or submit a letter to the editor of the local paper, ultimately reaching a larger audience. But, nothing can compete with one-on-one conversation. Have a conversation with boaters fi lling up at the local gas stations, strike up a discussion when launching your boat at the boat dock or chat with the local gas station owner to make sure they have the correct facts for their customers. Every little bit helps calm the waves of ethanol misinformation and create a more informed boating community.

Author: Bob DinneenPresident and CEO,

Renewable Fuels Association202-289-3835

Waves of Ethanol Misinformation By Bob Dinneen

VIEW FROM THE HILL

CHOP AND WINDROW IN ONE PASS.

THAT’S NEW HOLLAND SMART.When you use the Cornrower™ attachment with your New Holland CR combine and chopping corn head, you windrow corn stover at the same time you harvest, eliminating extra trips through the fi eld and associated labor and fuel costs. That’s SMART for your bottom line. The Cornrower™ attachment “catches” stalk material under the chopping corn head, creating a uniform windrow, then the CR combine drops high-energy chopped cobs and husks on top—without dirt or rocks that spoil your corn stover, and without hindering combine performance or maneuverability. Find out how you can save with the New Holland Cornrower.

Learn how to farm smart at nhSMART.com/clauson

© 2015 CNH Industrial America LLC. All rights reserved. New Holland Agriculture is a trademark registered in the United States and many other countries, owned by or licensed to CNH Industrial N.V., its subsidiaries or affi liates. New Holland Construction is a trademark in the United States and many other countries, owned by or licensed to CNH Industrial N.V., its subsidiaries or affi liates.

16 | Ethanol Producer Magazine | JUNE 2015

The journey to making E15 the standard fuel option across the country is like a high hurdle race. As soon as we clear one hurdle, we have to focus on the next. Although we are making constant progress with retailers and E15 is now available at more than 120 stations in 18 states, there are still challenges ahead. The largest regulatory obstacle standing between consumers and access to higher ethanol blends is the absence of a Reid vapor pressure (RVP) volatility waiver for E15.

Currently, E15 and higher ethanol blends do not receive the same 1-pound RVP volatility waiver that is granted to E10, which restricts summertime sales of E15 in many states. This regulatory restriction creates a disincentive for retailers to sell E15 or higher biofuel blends and denies consumers access to a fuel that meets their price and performance needs. E15 should not be treated as a seasonal fuel and the American consumer should not have to check their calendar to see if they will have a choice when they pull up to the pump.

Since Growth Energy applied for a fuel waiver for E15 in 2009, the ethanol industry has repeatedly asked the U.S. EPA to level the playing fi eld and grant a similar 1-pound RVP waiver for ethanol blends above 10 percent. Unfortunately, when EPA fi nalized the misfueling mitigation rule for E15, they explicitly stated that they would not grant a RVP waiver for E15, even though E15 is a cleaner, higher performing, less expensive fuel.

We commend Sens. Chuck Grassley, R-Iowa, and Rand Paul, R-Ky, Reps. Rod Blum, R-Iowa, and Adrian Smith. R-Neb., for recognizing the need for competition in the marketplace and taking leadership on this important issue in U.S. Congress. These congressmen have introduced legislation in both the Senate and the House of Representatives to remove regulations that limit market access to higher ethanol blends and restrict consumer choice at the pump. They agree that the regulatory treatment of E15 is unfair

and is preventing the adoption of new fuels that could benefi t our environment, our economy and our energy security. We know that others will soon follow their lead and work together to move these measures forward.

For the ethanol industry, E15 is the low-hanging fruit. It’s the most tested fuel in history and is compatible with more than 80 percent of the cars on the road. Nationwide, moving to E15 would create another 136,000 American jobs that can’t be outsourced, reduce the demand for foreign oil by 7 billion gallons and eliminate up to 8 million metric tons of greenhouse gas emissions per year—the equivalent of taking 1.68 million vehicles off the road—all while saving consumers money at the pump. E15 is projected to save consumers between 5 and 15 cents per gallon. And, because ethanol increases the available fuel supply, it will help to drive down the price of gasoline for all drivers. In a time when roughly 8 percent of our annual incomes are being used for commuting costs, those savings really add up.

The oil industry recognizes the obvious benefi ts to consumers and will continue to throw up every hurdle they can to protect their market share and keep our nation addicted to fossil fuels. But each of those hurdles we clear sends a positive signal that America is ready for cleaner technologies that provide consumers with a choice and savings at the pump. As an industry, we know that hurdles are just a series of barriers that are meant to be jumped over, and in the end, we will win this race.

Call your elected offi cials today and let them know that you support S. 889, H.R. 1944 and H.R. 1736.

Author: Tom BuisCEO, Growth Energy

DRIVE

High Hurdle Race By Tom Buis

Process Technologies

50%ProteinPurity

Still Pro 50™ = 3 x Value of DDGS

Get More $$$ OutOf Your DDGS:

MSC™ Technology -patented and operating for over 5 years

www.FQPTech.comUS Patent# 8,778,433 937-310-1425

Still Pro 50™ brings a proven high value co-product to your plant portfolio that trades in the specialty protein market. The MSC System has been in full-scale operation for over 5 years.

Fluid Quip ProcessTechnologies® brings anexperienced corn wet milling team and equipment design experts to provide SOLUTIONS THAT WORK.

18 | Ethanol Producer Magazine | JUNE 2015

Following the Cool Guys By Ron Lamberty

Every year, surveys are performed by advertising and marketing companies to try and measure trust. Who or what do people trust when they are looking for the answer to a question, a recommendation on a purchase, or information about a controversial topic? While the results reshuffl e a little bit each year, near the top of the list in every survey is “someone like me,” or “people I know.”

In reality, sure, we want to know what people like us think, but come on, if you were offered advice from, let’s say, Pat Hawkins, a guy I grew up with in Hilltop, or noted theoretical physicist Stephen Hawking, you’d listen to the guy who is considered one of the greatest minds of our time, right?

Not me. I’m going to listen to Pat, because—I forgot to mention this—the subject is “winning strategies for ‘cans,’” a game that was invented by Pat, my brother Greg and me … and maybe Todd Nussbaum… I don’t remember. Anyway, we would all kick Hawking’s butt in cans. And I bet he can’t give you any tips on hot-waxing a pop can either. Pat could. Pat was awesome at that. If you’re looking for that kind of advice, you can just say, “thanks for nothing, Professor Hawking.”

I guess the point is, for most decisions, studies and spokespeople are important, but most of us still want to get the recommendations of “people like me.” However, we prefer the opinions of leaders and innovators, like Pat. Guys who care enough to fi nd out if waxing a pop can makes a difference, and who don’t mind if it doesn’t, because now they know (and it still looked cool).

The convenience store industry is often described as one where “everyone wants to be fi rst to be second.” Maybe that’s true of most industries, and the meaning is the same in all of them: Before business owners invest time and money in a new product or new line, they want to see it in action. And, whenever possible, they want to talk to people who have already been there and done that, to fi nd out how it’s really working out. Fuel marketers go to trade shows and petroleum industry events to see that stuff and talk to those people.

The challenge for a new product like E15 is most marketers don’t know a station owner who sells E15, and what they think they know has been warped by the ongoing E15 smear campaign. The American Coalition for Ethanol’s Flex Forward campaign introduces fuel marketers to other real, live marketers, who saw through those ghost stories, added E15, and made more money. We can’t bring experienced E15 marketers with us to every trade show or workshop ACE attends, so we’ve done the next best thing. We’ve brought their stories to ethanol.org and fl exfuelforward.com where they will be available 24/7, for marketers who live and work in the 24/7 convenience store world.

Beyond that, in the c-store world, just like every other “world,” there are operators who are watched more closely by other retailers. They are the innovators, retailers who try things nobody else has tried. When it works, they reap the rewards, if it doesn’t, they fi nd a way to make it work. That’s why it was a big deal when Sheetz Inc. announced it will be putting E15 in 60 stations this year. Sheetz is one of those companies. They have a reputation for being an innovator. If you doubt that, the next time you’re talking to a prospective E15 retailer, just drop this into the conversation: “Sheetz is going to sell E15 in 60 of their stores.” Watch for the reaction.

A lot of time and money has been spent to encourage some high-profi le retailers to offer E15. The only way that investment pays off is if other fuel retailers notice and want to “be the fi rst to be second.” Drop those names. Not just Sheetz. Mention Mapco. Murphy. Whoever sells E15 in your area. Every chance you get, let station owners know “someone like you” is selling E15. And it’s one of the cool guys.

Author: Ron LambertySenior Vice President

American Coalition for Ethanol605-334-3381

GRASSROOTS VOICE

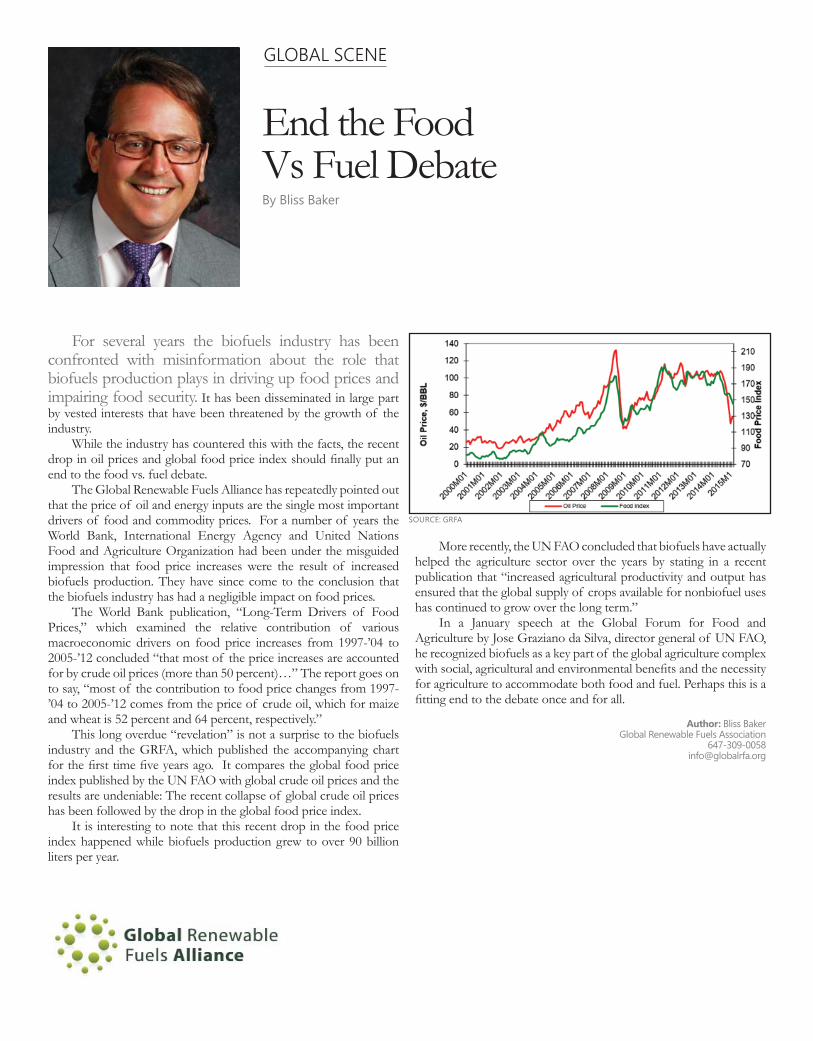

End the Food Vs Fuel Debate By Bliss Baker

For several years the biofuels industry has been confronted with misinformation about the role that biofuels production plays in driving up food prices and impairing food security. It has been disseminated in large part by vested interests that have been threatened by the growth of the industry.

While the industry has countered this with the facts, the recent drop in oil prices and global food price index should fi nally put an end to the food vs. fuel debate.

The Global Renewable Fuels Alliance has repeatedly pointed out that the price of oil and energy inputs are the single most important drivers of food and commodity prices. For a number of years the World Bank, International Energy Agency and United Nations Food and Agriculture Organization had been under the misguided impression that food price increases were the result of increased biofuels production. They have since come to the conclusion that the biofuels industry has had a negligible impact on food prices.

The World Bank publication, “Long-Term Drivers of Food Prices,” which examined the relative contribution of various macroeconomic drivers on food price increases from 1997-’04 to 2005-’12 concluded “that most of the price increases are accounted for by crude oil prices (more than 50 percent)…” The report goes on to say, “most of the contribution to food price changes from 1997-’04 to 2005-’12 comes from the price of crude oil, which for maize and wheat is 52 percent and 64 percent, respectively.”

This long overdue “revelation” is not a surprise to the biofuels industry and the GRFA, which published the accompanying chart for the fi rst time fi ve years ago. It compares the global food price index published by the UN FAO with global crude oil prices and the results are undeniable: The recent collapse of global crude oil prices has been followed by the drop in the global food price index.

It is interesting to note that this recent drop in the food price index happened while biofuels production grew to over 90 billion liters per year.

More recently, the UN FAO concluded that biofuels have actually helped the agriculture sector over the years by stating in a recent publication that “increased agricultural productivity and output has ensured that the global supply of crops available for nonbiofuel uses has continued to grow over the long term.”

In a January speech at the Global Forum for Food and Agriculture by Jose Graziano da Silva, director general of UN FAO, he recognized biofuels as a key part of the global agriculture complex with social, agricultural and environmental benefi ts and the necessity for agriculture to accommodate both food and fuel. Perhaps this is a fi tting end to the debate once and for all.

Author: Bliss Baker Global Renewable Fuels Association

GLOBAL SCENE

SOURCE: GRFA

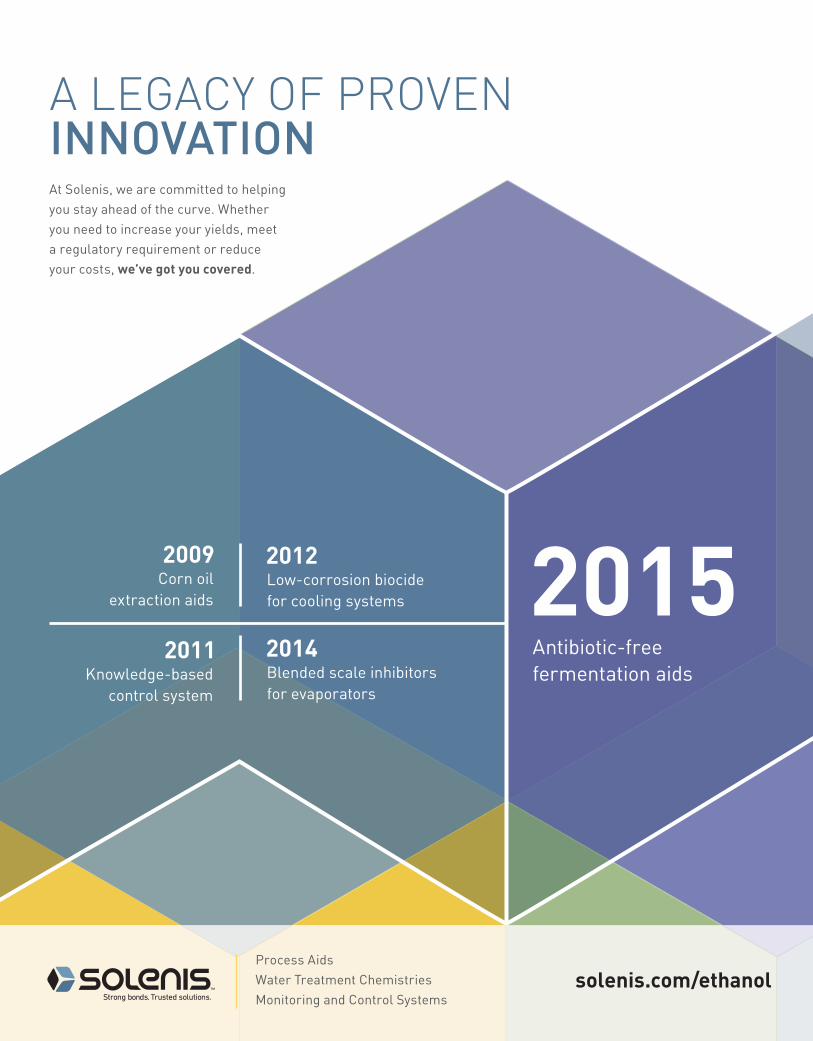

solenis.com/ethanol

2015

At Solenis, we are committed to helping you stay ahead of the curve. Whether you need to increase your yields, meet a regulatory requirement or reduceyour costs, we’ve got you covered.

Antibiotic-free fermentation aids

2009Corn oil

extraction aids

2012Low-corrosion biocide for cooling systems

2011Knowledge-based

control system

2014Blended scale inhibitors for evaporators

A LEGACY OF PROVEN INNOVATION

Process AidsWater Treatment ChemistriesMonitoring and Control Systems

22 | Ethanol Producer Magazine | JUNE 2015

Vecoplan LLC has promoted Misty Turner to the position of as-sistant service manager. Responsibilities of her new position include connecting customers and fi eld technicians with Vecoplan’s internal

troubleshooting service technicians. She will also oversee the organization and schedul-ing of Vecoplan’s network of certifi ed service personnel throughout North America. Turner joined Vecoplan in March 2012 as a service administrator. She brings 10 years of man-agement and service experience to her new job, including three years as accounts receiv-able manager at HEP Direct and four years in customer service with Furniture USA.

American Ethanol reached a new mile-stone at the Phoenix International Raceway in March, when it topped 7 million miles of rac-ing. Th at equates with roughly 30 trips from the Earth to the moon or 281 laps around Earth. NASCAR began running E15 in 2011. Th e fuel change was in conjunction with its NASCAR Green Platform, which has become one of the most comprehensive recycling, tree planting and renewable energy programs in professional sports. American Ethanol is a partnership of the National Corn Growers As-sociation and Growth Energy.

Aemetis Inc. has appointed Satya Chill-ara as vice president of corporate develop-ment. Chillara has more than 24 years of ex-perience in the cleantech and semiconductor industries and on Wall Street. He previously served as managing director and equity re-search analyst working for several investment banks and hedge funds.

VAC-U-MAX has announced its 55MW industrial sump vacuum cleaner allows op-erators to quickly empty machine tool sumps, machining beds, oil/water separators, parts washers, rinse tanks and clean up liquid spills. Included with the complete system, the chip basket and liner separates solid particles from collected liquid at 1 to 2 gallons per second; and, with the turn of a lever, this industrial vacuum will pump out the fi ltered liquid con-tents of the drum through the discharge hose to a central fi ltration system for coolant/oils or approved fl oor drain at up to 14 gallons per minute.

Celtic Renewables has received £500,000 ($746,150) in a new round of investment, taking its valuation to £10 million. Th e com-pany announced an investment of £250,000 from the Scottish Investment Bank, with an additional £250,000 equity stake acquired by an existing private investor. Scottish Renew-ables converts whiskey waste into biofuels.

asdfGrowmark Inc. and Magellan Pipeline Co. PL have entered into an agreement in which Growmark will acquire the refi ned fuels terminal near St. Joseph, Missouri. Terms of the acquisition were not disclosed. Acquisition of the facility will enable Growmark to ensure continued supply of refi ned fuels. In addition to the current diesel fuel availability at the terminal, Growmark intends to off er ethanol blends of gasoline in the future.

asdfIogen has appoint-ed Gordon McLen-nan vice president of business development. McLennan has 35 years experience in domestic and international sales, revenue generation, project development,

operations management, change management and leadership. As vice president of business development, he will be responsible for de-veloping and delivering new commercial op-portunities, including Iogen’s current strategic initiatives both within and beyond cellulosic ethanol. Gordon will play a key role in build-ing upon Iogen’s commercial initiatives.

asdfAmerplast has entered into a supply part-nership agreement with Braskem to market green polyethylene (Green PE) obtained from a renewable source, sugar cane ethanol. While

BUSINESS BRIEFS People, Partnerships & Deals

Turner

McLennan

JUNE 2015 | Ethanol Producer Magazine | 23

environmentally sustainable, Green PE has the performance characteristics of a traditional PE. For Amerplast’s customers, such as tissue producers, it off ers an environmentally sound alternative for meeting packaging needs.

asdfTh e Nebraska Corn Board recently pre-sented Duane Kristensen of Chief Ethanol Fuels Inc. with its Ethanol Industry Appre-ciation Award, which recognizes a producer or person in the industry who has worked hard to develop ethanol markets and expand demand for ethanol in the state while appre-ciating the value of the corn checkoff and its involvement in ethanol market development. Kristensen was selected for his leadership in Nebraska as well as his involvement and en-gagement in ethanol advocacy groups on a statewide, national, and global basis.

asdfMethes Energies International Ltd. recently announced it has received an initial payment for the sale of a Denami 600 bio-diesel processor and a PP-MEC pre-treatment system to be installed in Havelock, Ontario, Canada. Th e buyer, Drain Bros, will become the fi rst facility in the world to use Methes' pretreatment system using the PP-MEC cata-lyst to process corn oil from a local ethanol plant.

asdfEner-Core Inc., a provider of power oxi-dation technology and equipment that gener-ates clean power from low-quality and waste gases from a wide vari-ety of industries, has ap-pointed John Millard as director of Europe and

the Middle East region and Mark Owen as director of sales. Millard and Owen will both report directly to Alain Castro, CEO of Ener-Core. Millard has previously served as CEO of a Swiss energy consulting company focusing on demand-side energy management and most recently the development of smart energy sys-tems. Owen is an internationally recognized expert on industrial pollution control systems and processes. He has 30 years experience in

the commercialization, installation and op-erational servicing of various types of air pol-lution control and waste treatment systems.

asArcher Daniels Mid-land Co. has announced several management ap-pointments in its corn business unit. Craig Wil-lis, a 23-year company veteran, has been named president of the ethanol

group. He had been a vice president of the business since 2011. Prior to joining the etha-nol group in 2007, Willis’ broad-based ADM tenure included experience as commercial manager of three large oilseeds crush plants. He also managed origination and transporta-tion assets within the company’s agricultural services business unit. In addition, Kris Lutt and Andy Moore have been named president and vice president, respectively, of sweeten-ers and starches; Luther Pohlmann has been named vice president of corn operations, and Gary Towne will continue to serve as president of risk management for the corn business unit.In addition, ADM has announced that Mark Schweitzer has been appointed vice president of investor relations, where he will represent the company to the investment community and act as an advocate for shareholder value creation. Schweitzer previously served as man-aging director of ADM’s intermodal and in-ternational container freight business.

Duane Kristensen (left) accepts Ethanol Industry Appreciation Award from Dennis Gengenbach, farmer-director on the Nebraska Corn Board.

Millard

24 | Ethanol Producer Magazine | JUNE 2015

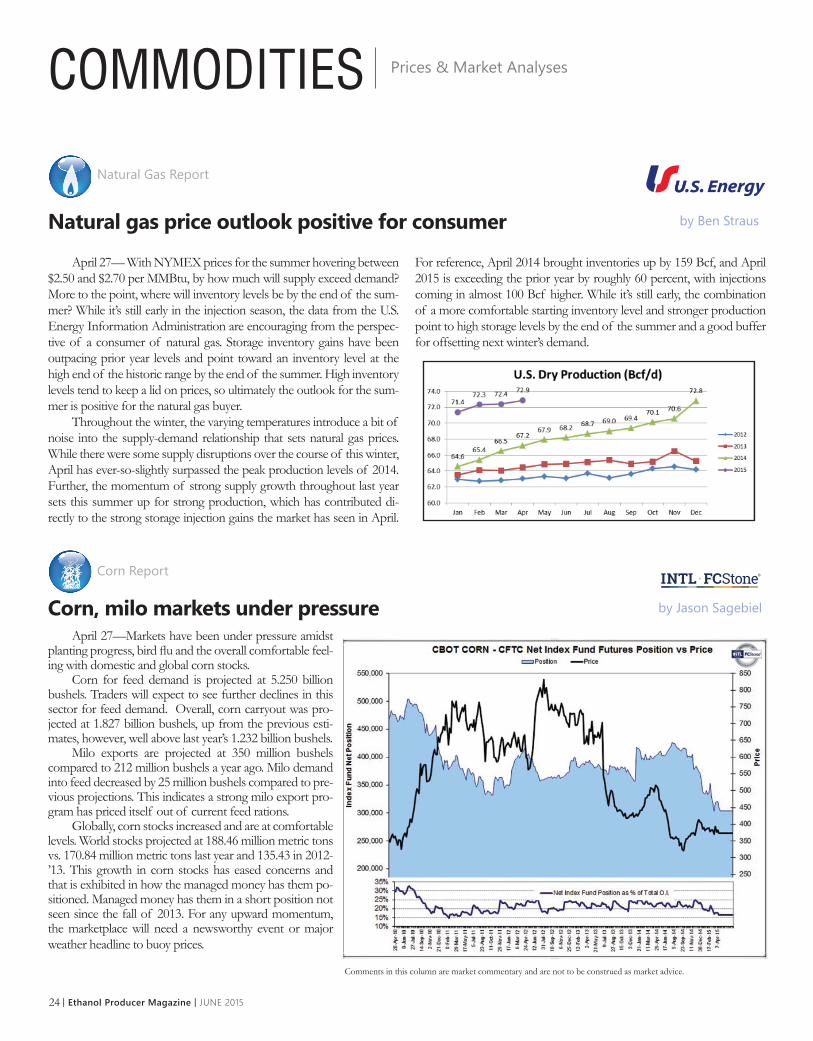

April 27— With NYMEX prices for the summer hovering between $2.50 and $2.70 per MMBtu, by how much will supply exceed demand? More to the point, where will inventory levels be by the end of the sum-mer? While it’s still early in the injection season, the data from the U.S. Energy Information Administration are encouraging from the perspec-tive of a consumer of natural gas. Storage inventory gains have been outpacing prior year levels and point toward an inventory level at the high end of the historic range by the end of the summer. High inventory levels tend to keep a lid on prices, so ultimately the outlook for the sum-mer is positive for the natural gas buyer.

Throughout the winter, the varying temperatures introduce a bit of noise into the supply-demand relationship that sets natural gas prices. While there were some supply disruptions over the course of this winter, April has ever-so-slightly surpassed the peak production levels of 2014. Further, the momentum of strong supply growth throughout last year sets this summer up for strong production, which has contributed di-rectly to the strong storage injection gains the market has seen in April.

For reference, April 2014 brought inventories up by 159 Bcf, and April 2015 is exceeding the prior year by roughly 60 percent, with injections coming in almost 100 Bcf higher. While it’s still early, the combination of a more comfortable starting inventory level and stronger production point to high storage levels by the end of the summer and a good buffer for offsetting next winter’s demand.

Natural Gas Report

Corn Report

April 27—Markets have been under pressure amidst planting progress, bird fl u and the overall comfortable feel-ing with domestic and global corn stocks.

Corn for feed demand is projected at 5.250 billion bushels. Traders will expect to see further declines in this sector for feed demand. Overall, corn carryout was pro-jected at 1.827 billion bushels, up from the previous esti-mates, however, well above last year’s 1.232 billion bushels.

Milo exports are projected at 350 million bushels compared to 212 million bushels a year ago. Milo demand into feed decreased by 25 million bushels compared to pre-vious projections. This indicates a strong milo export pro-gram has priced itself out of current feed rations.

Globally, corn stocks increased and are at comfortable levels. World stocks projected at 188.46 million metric tons vs. 170.84 million metric tons last year and 135.43 in 2012-’13. This growth in corn stocks has eased concerns and that is exhibited in how the managed money has them po-sitioned. Managed money has them in a short position not seen since the fall of 2013. For any upward momentum, the marketplace will need a newsworthy event or major weather headline to buoy prices.

Natural gas price outlook positive for consumer by Ben Straus

Corn, milo markets under pressure by Jason Sagebiel

COMMODITIES Prices & Market Analyses

Comments in this column are market commentary and are not to be construed as market advice.

JUNE 2015 | Ethanol Producer Magazine | 25

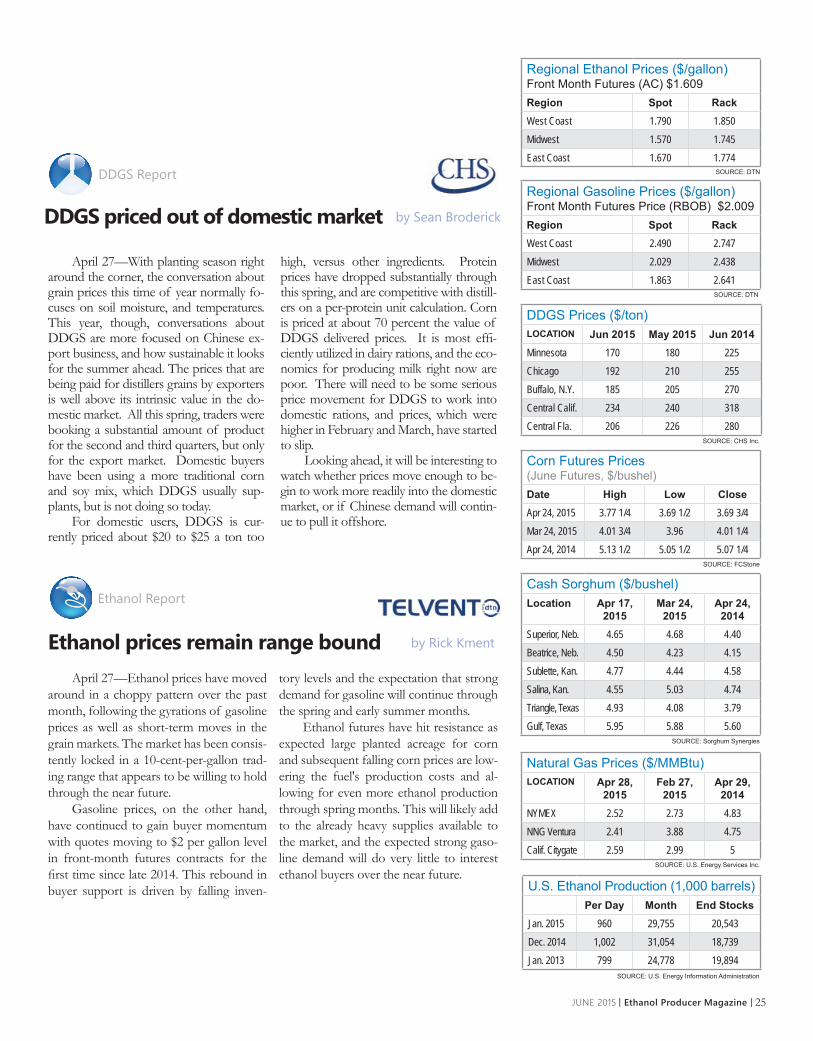

DDGS Report

Ethanol Report

April 27—Ethanol prices have moved around in a choppy pattern over the past month, following the gyrations of gasoline prices as well as short-term moves in the grain markets. The market has been consis-tently locked in a 10-cent-per-gallon trad-ing range that appears to be willing to hold through the near future.

Gasoline prices, on the other hand, have continued to gain buyer momentum with quotes moving to $2 per gallon level in front-month futures contracts for the fi rst time since late 2014. This rebound in buyer support is driven by falling inven-

tory levels and the expectation that strong demand for gasoline will continue through the spring and early summer months.

Ethanol futures have hit resistance as expected large planted acreage for corn and subsequent falling corn prices are low-ering the fuel's production costs and al-lowing for even more ethanol production through spring months. This will likely add to the already heavy supplies available to the market, and the expected strong gaso-line demand will do very little to interest ethanol buyers over the near future.

April 27—With planting season right around the corner, the conversation about grain prices this time of year normally fo-cuses on soil moisture, and temperatures. This year, though, conversations about DDGS are more focused on Chinese ex-port business, and how sustainable it looks for the summer ahead. The prices that are being paid for distillers grains by exporters is well above its intrinsic value in the do-mestic market. All this spring, traders were booking a substantial amount of product for the second and third quarters, but only for the export market. Domestic buyers have been using a more traditional corn and soy mix, which DDGS usually sup-plants, but is not doing so today.

For domestic users, DDGS is cur-rently priced about $20 to $25 a ton too

high, versus other ingredients. Protein prices have dropped substantially through this spring, and are competitive with distill-ers on a per-protein unit calculation. Corn is priced at about 70 percent the value of DDGS delivered prices. It is most effi -ciently utilized in dairy rations, and the eco-nomics for producing milk right now are poor. There will need to be some serious price movement for DDGS to work into domestic rations, and prices, which were higher in February and March, have started to slip.

Looking ahead, it will be interesting to watch whether prices move enough to be-gin to work more readily into the domestic market, or if Chinese demand will contin-ue to pull it offshore.

Regional Ethanol Prices ($/gallon)Front Month Futures (AC) $1.609Region Spot RackWest Coast 1.790 1.850Midwest 1.570 1.745East Coast 1.670 1.774

SOURCE: DTN

Regional Gasoline Prices ($/gallon)Front Month Futures Price (RBOB) $2.009Region Spot RackWest Coast 2.490 2.747Midwest 2.029 2.438East Coast 1.863 2.641

SOURCE: DTN

DDGS Prices ($/ton)LOCATION Jun 2015 May 2015 Jun 2014Minnesota 170 180 225Chicago 192 210 255Buffalo, N.Y. 185 205 270Central Calif. 234 240 318Central Fla. 206 226 280

SOURCE: CHS Inc.

Corn Futures Prices (June Futures, $/bushel)Date High Low CloseApr 24, 2015 3.77 1/4 3.69 1/2 3.69 3/4Mar 24, 2015 4.01 3/4 3.96 4.01 1/4Apr 24, 2014 5.13 1/2 5.05 1/2 5.07 1/4

SOURCE: FCStone

Cash Sorghum ($/bushel)Location Apr 17,

2015Mar 24,

2015Apr 24,

2014Superior, Neb. 4.65 4.68 4.40Beatrice, Neb. 4.50 4.23 4.15Sublette, Kan. 4.77 4.44 4.58Salina, Kan. 4.55 5.03 4.74Triangle, Texas 4.93 4.08 3.79Gulf, Texas 5.95 5.88 5.60

SOURCE: Sorghum Synergies

Natural Gas Prices ($/MMBtu)LOCATION Apr 28,

2015Feb 27,

2015Apr 29,

2014NYMEX 2.52 2.73 4.83NNG Ventura 2.41 3.88 4.75Calif. Citygate 2.59 2.99 5

SOURCE: U.S. Energy Services Inc.

U.S. Ethanol Production (1,000 barrels)Per Day Month End Stocks

Jan. 2015 960 29,755 20,543Dec. 2014 1,002 31,054 18,739Jan. 2013 799 24,778 19,894

SOURCE: U.S. Energy Information Administration

DDGS priced out of domestic market by Sean Broderick

Ethanol prices remain range bound by Rick Kment

Sponsors, Supporting Organizations, Media Partners & Exhibitors

PLATINUM SPONSORS

GOLD SPONSORS

SUPPORTING ORGANIZATIONS

MEDIA PARTNERS

SILVER SPONSORS

JUNE 1- 4,2015MINNEAPOLIS, MN

31st ANNUAL

EXHIBITORS __________________________________________________________________________________________________________

4B Components, Ltd.A&B Process Systems CorporationAaron Equipment CompanyAbengoaADF Engineering, Inc.ADI Systems, Inc.AggrekoAgra Industries, Inc.Air Resource Specialists, Inc.Alfa LavalAllied Locke IndustriesAmec Foster WheelerAmerican Coalition for EthanolAmerican Lung Association in MinnesotaAnderson Chemical Co.Andritz, Inc.Andy J. Egan Co., Inc.Angel Yeast Co., Ltd.AnitoxApache Stainless Equipment CorporationArisdyne Systems, Inc.Arkema, Inc.Barr EngineeringBASF Enzymes, LLCBeta Tec Hop ProductsBiofuels International MagazineBioFuels JournalBion AnalyticalBismarck State College-National Energy Center of ExcellenceBliss Industries, LLCBriggs of Burton, Inc.Brown Tank, LLCBruker OpticsBuckmanBulk Conveyors, Inc.Buresh Building Systems, Inc.Butamax Advanced Biofuels, LLCButterworth, Inc.CarbolineCarter Day International, Inc.CenterPoint Energy Services, Inc.Cereal Process Technologies, LLCChemTreatChristianson & AssociatesCHS, Inc.Clayton IndustriesCloud/Sellers Cleaning SystemsColumbia Pipe & Supply Co.CompuWeigh Corp.Consolidated Water SolutionsConveyor Engineering & ManufacturingCooling Technology InstitueCooling Tower Depot, Inc.CPM Roskamp ChampionCTE Global, Inc.Direct AutomationDPC Industries, Inc.DuPontDürr Systems, Inc.EAD CorporateEcoEngineersEdeniq

Eisenmann CorporationEmerson Process ManagementEnerquip, LLCEnviro-Dyne Industrial Services, Inc.ERI Solutions, Inc.eRPortal Software Group, LLCEthanol Producer MagazineFagen, Inc.Ferm Solutions, Inc.Flottweg Separation Technology, Inc.FLSmidthFluid EngineeringFluid Quip Process Technologies, LLCFremont IndustriesFrontline Warning SystemsGE Water & Process TechnologiesGEA Flow ComponentsGEA GroupGEA PHE SystemsGenesis IIIGlobal Refractory Installers and SuppliersGolder Associates, inc.GreenShit CorporationGrowth EnergyHealthmate International, Inc.Hengye, Inc.HTH CompaniesHydrite Chemical Co.Hydro-Klean, LLCHydro-Thermal CorporationIBT Industrial SolutionsICM, Inc.Inbicon/ DONG EnergyIndustrial Equipment & PartsInnospec Fuel SpecialtiesIntegrated Power ServicesIntegroEnergy Group, Inc.Interpoll Laboratories, Inc.Interra Global CorporationInterstates CompaniesIntertekINTL FCStoneIvanhoe Industries, Inc.J&D Construction, Inc.J.C. Ramsdell Enviro Services, Inc.Jacobs CorporationJatrodieselJMENG Industries, Ltd.JMPK & L Equipment Mechanical, Inc.K·Coe IsomKATZEN International, Inc.Kubco Decanter Services, Inc.Laidig Systems, Inc.LAKOS Separators and Filtration SolutionsLallemand Biofuels & Distilled SpiritsLarson Engineering, Inc.Leaf TechnologiesLotus Mixers, Inc.Luoyang Jianlong Chemical Industrial Co., Ltd.Maas CompaniesMagnetec Inspection, Inc.

Mapcon TechnologiesMason ManufacturingMcC, Inc.Merjent, Inc.Metrohm USAMidland Scientific, Inc.Minnesota Bio-Fuels Association, Inc.Mist Chemical & Supply CompanyMole Master Services CorporationMonitortech CorporationMSW Consulting, Inc.MVTL LaboratoriesNalco, an Ecolab CompanyNational Corn-to-Ethanol Research CenterNationwide Boiler, Inc.Nelson Engineering, Inc.Neogen CorporationNew Age CryoNew Holland Agriculture & ConstructionNew York Blower CompanyNorth American Industrial Services, Inc.NovaspectNovozymesOlsson AssociatesOrbijet, Inc. and Tank Cleaning Technologies, Inc.Pace Analytical ServicesPainters USA, Inc.Pan American Hydrogen, Inc.Paques, Inc.Paul Mueller CompanyPentairPepper MaintenancePerten Instruments-A PerkinElmer CompanyPhibro Ethanol Performance GroupPinnacle Engineering, Inc.PK SafetyPlant Maintenance ServicesPneumat SystemsPOET-DSM Advanced Biofuels, LLCPolar CleanPraj Industries LimitedPremium Plant Services, Inc.ProQuip, Inc.Protectoseal Company, ThePumping Solutions, Inc.Purina Animal Nutrition, LLCQuality Liquid FeedsRayeman Elements, Inc.Refractory & Insulation Supply, Inc.Refractory Service, Inc.Renewable Fuels AssociationRenewal Service, Inc.Roadway Worker TrainingRotary Airlock, LLCRTP Environmental Associates, Inc.Schimberg CompanySchneider Electric-InvensysSchroeder Environmental Cleaning Services, Inc.Scott Equipment CompanySeneca Companies

SiemensSinobios (Shanghai) Imp. & Exp. Co., Ltd.SolenisSorghum CheckoffSOS Leak RepairSponge-Jet, Inc.Sukup ManufacturingSulzer Pumps Solutions, Inc.Sundial SolarSunson Industry Group Co., Ltd.Superior Process TechnologiesSwagelok MinnesotaSwanson Flo-Systems Co.SyngentaTank Consultants, Inc.Team Industrial ServicesThe Cary CompanyThe Walling CompanyThermal Energy Products, Inc.Thorpe Special Services CorporationTotal Filtration Services, Inc.Tower Performance, Inc.TracercoTRAMCO (AGI)Tranter, Inc.Trident Automation, Inc.Trihydro CorporationTrillium Industrial ServicesU.S. Energy ServicesU.S. Grains CouncilU.S. WaterVAA, LLCVAC-U-MAXValicorVeolia Water TechnologiesVertical Software, Inc.Victory EnergyViking Automatic Sprinkler Co.VistaCommVogelbusch USAWalinga USA, Inc.Warrior Mfg., LLCWaters CorporationWB Services, LLCWCR IncorporatedWestmor Fluid SolutionsWhistler Center for Carbohydrate Research, Purdue UniversityWhitefox Technologies LimitedWINBCOZachry Engineering CorporationZeochem, LLC

Reserve 2016 Exhibit Space TodayVisit Ethanol Producer Magazine @ Booth #2025

SAVE THE DATE - 2016 EventInternational Fuel Ethanol Workshop & ExpoJune 20-23, 2016 | Wisconsin Center | Milwaukee, WI

As of May 6, 2015

28 | Ethanol Producer Magazine | JUNE 2015

DISTILLED Ethanol News & Trends

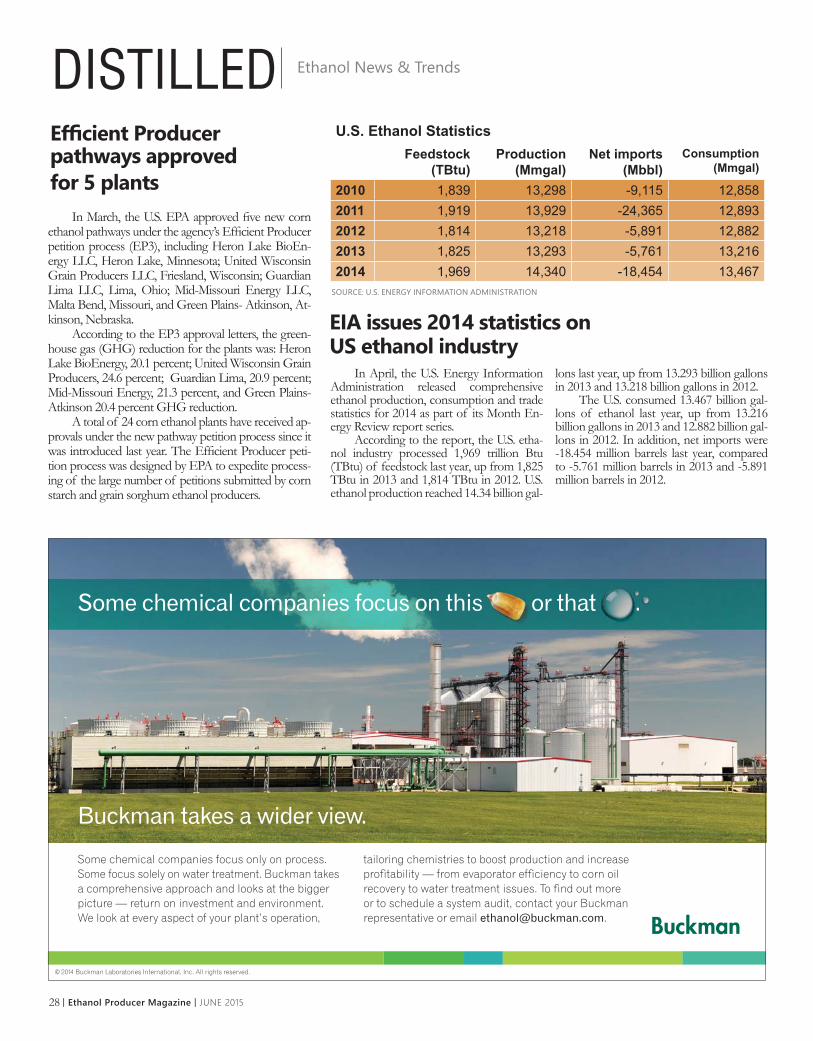

In April, the U.S. Energy Information Administration released comprehensive ethanol production, consumption and trade statistics for 2014 as part of its Month En-ergy Review report series.

According to the report, the U.S. etha-nol industry processed 1,969 trillion Btu (TBtu) of feedstock last year, up from 1,825 TBtu in 2013 and 1,814 TBtu in 2012. U.S. ethanol production reached 14.34 billion gal-

lons last year, up from 13.293 billion gallons in 2013 and 13.218 billion gallons in 2012.

The U.S. consumed 13.467 billion gal-lons of ethanol last year, up from 13.216 billion gallons in 2013 and 12.882 billion gal-lons in 2012. In addition, net imports were -18.454 million barrels last year, compared to -5.761 million barrels in 2013 and -5.891 million barrels in 2012.

EIA issues 2014 statistics on US ethanol industry

In March, the U.S. EPA approved fi ve new corn ethanol pathways under the agency’s Effi cient Producer petition process (EP3), including Heron Lake BioEn-ergy LLC, Heron Lake, Minnesota; United Wisconsin Grain Producers LLC, Friesland, Wisconsin; Guardian Lima LLC, Lima, Ohio; Mid-Missouri Energy LLC, Malta Bend, Missouri, and Green Plains- Atkinson, At-kinson, Nebraska.

According to the EP3 approval letters, the green-house gas (GHG) reduction for the plants was: Heron Lake BioEnergy, 20.1 percent; United Wisconsin Grain Producers, 24.6 percent; Guardian Lima, 20.9 percent; Mid-Missouri Energy, 21.3 percent, and Green Plains- Atkinson 20.4 percent GHG reduction.

A total of 24 corn ethanol plants have received ap-provals under the new pathway petition process since it was introduced last year. The Effi cient Producer peti-tion process was designed by EPA to expedite process-ing of the large number of petitions submitted by corn starch and grain sorghum ethanol producers.

Effi cient Producer pathways approved for 5 plants

SOURCE: U.S. ENERGY INFORMATION ADMINISTRATION

U.S. Ethanol Statistics Feedstock

(TBtu)Production

(Mmgal)Net imports

(Mbbl)Consumption

(Mmgal)

2010 1,839 13,298 -9,115 12,8582011 1,919 13,929 -24,365 12,8932012 1,814 13,218 -5,891 12,8822013 1,825 13,293 -5,761 13,2162014 1,969 14,340 -18,454 13,467

Some chemical companies focus only on process. Some focus solely on water treatment. Buckman takes a comprehensive approach and looks at the bigger picture — return on investment and environment. We look at every aspect of your plant’s operation,

tailoring chemistries to boost production and increase profitability — from evaporator efficiency to corn oil recovery to water treatment issues. To find out more or to schedule a system audit, contact your Buckman representative or email [email protected].

© 2014 Buckman Laboratories International, Inc. All rights reserved.

Some chemical companies focus on this or that .

Buckman takes a wider view.

JUNE 2015 | Ethanol Producer Magazine | 29

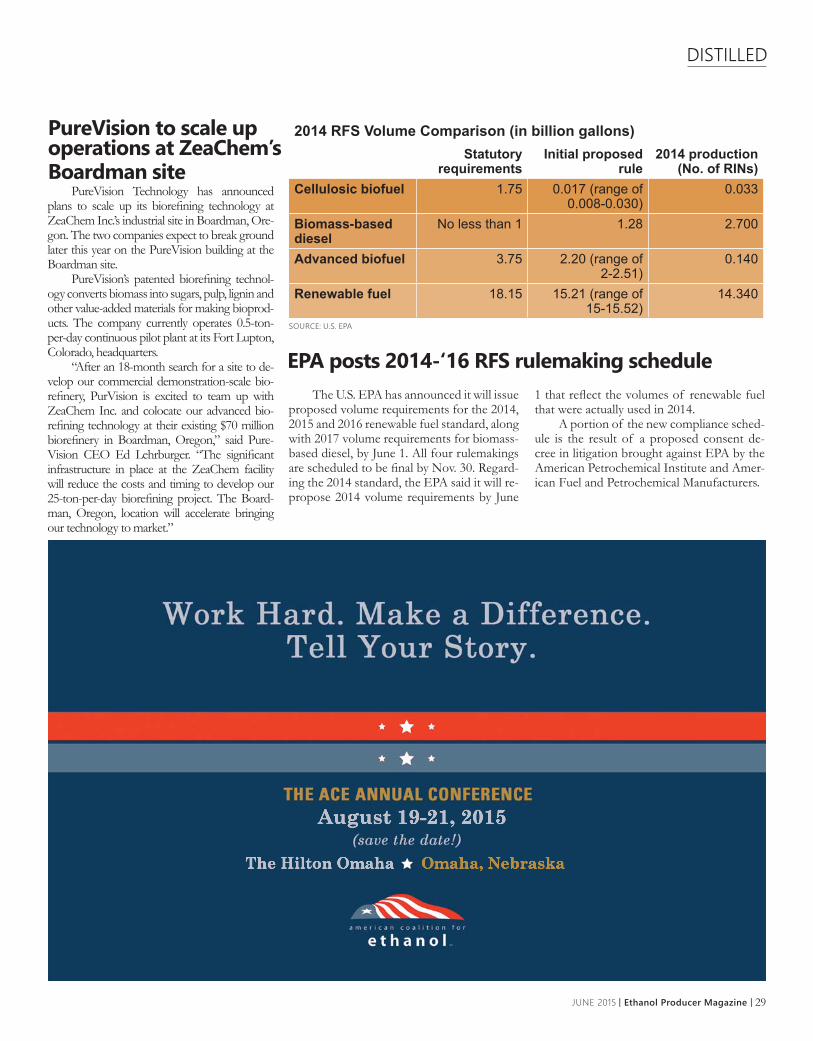

EPA posts 2014-‘16 RFS rulemaking schedule The U.S. EPA has announced it will issue

proposed volume requirements for the 2014, 2015 and 2016 renewable fuel standard, along with 2017 volume requirements for biomass-based diesel, by June 1. All four rulemakings are scheduled to be fi nal by Nov. 30. Regard-ing the 2014 standard, the EPA said it will re-propose 2014 volume requirements by June

1 that refl ect the volumes of renewable fuel that were actually used in 2014.

A portion of the new compliance sched-ule is the result of a proposed consent de-cree in litigation brought against EPA by the American Petrochemical Institute and Amer-ican Fuel and Petrochemical Manufacturers.

DISTILLED

PureVision Technology has announced plans to scale up its biorefi ning technology at ZeaChem Inc.’s industrial site in Boardman, Ore-gon. The two companies expect to break ground later this year on the PureVision building at the Boardman site.

PureVision’s patented biorefi ning technol-ogy converts biomass into sugars, pulp, lignin and other value-added materials for making bioprod-ucts. The company currently operates 0.5-ton-per-day continuous pilot plant at its Fort Lupton, Colorado, headquarters.

“After an 18-month search for a site to de-velop our commercial demonstration-scale bio-refi nery, PurVision is excited to team up with ZeaChem Inc. and colocate our advanced bio-refi ning technology at their existing $70 million biorefi nery in Boardman, Oregon,” said Pure-Vision CEO Ed Lehrburger. “The signifi cant infrastructure in place at the ZeaChem facility will reduce the costs and timing to develop our 25-ton-per-day biorefi ning project. The Board-man, Oregon, location will accelerate bringing our technology to market.”

PureVision to scale up operations at ZeaChem’s Boardman site

2014 RFS Volume Comparison (in billion gallons)Statutory

requirements Initial proposed

rule 2014 production

(No. of RINs)Cellulosic biofuel 1.75 0.017 (range of

0.008-0.030)0.033

Biomass-based diesel

No less than 1 1.28 2.700

Advanced biofuel 3.75 2.20 (range of 2-2.51)

0.140

Renewable fuel 18.15 15.21 (range of 15-15.52)

14.340

SOURCE: U.S. EPA

The Iowa Renewable Fuels As-sociation recently announced that data published by the Iowa Department of Revenue shows a record-setting 11.96 million gallons of E85 was sold in the state last year. The nearly 12 million gallons sold in 2014 beat the previous record set in 2013 by more than 1 mil-lion gallons.

“Another year, and another E85 sales record in Iowa,” said Monte Shaw, executive director of the IRFA.

“The most impressive aspect of this record is that retail gasoline prices dropped signifi cantly in the second half of the fourth quarter of 2014, yet Iowa motorists remained committed to the homegrown, cleaner-burning fuel by setting a new fourth-quarter record for E85 purchases.

According to the IRFA, E85 is currently sold at approximately 200 fueling stations in Iowa.

DISTILLED

Iowa sets annual E85 sales record

Croda to convert ethanol to ethylene oxide

Croda Inc. has announced plans to construct a $170 million upgrade at its Atlas Point manufactur-ing site in Delaware that will convert ethanol into ethylene oxide. Construction is expected to take ap-proximately two years.

Once complete, the company will begin con-verting between 10 MMgy and 14 MMGy of etha-nol into ethylene oxide, opening a new market for U.S. ethanol. Ethylene oxide is the primary chemical used in the manufacture of nonionic surfactants.

“This will be the fi rst facility of its kind in North America,” said Richard Hanson, managing director of performance technologies and indus-trial chemicals for the U.K.-headquartered specialty chemical company.

Currently, Croda rails in ethylene oxide manu-factured on the Gulf Coast from petrochemical-based ethane or naptha. The new project will provide a renewable alternative to traditional fossil-based ethylene oxide. Customers are increasingly looking for sustainable, renewable materials, Hanson said.

SOURCE: IOWA DEPARTMENT OF REVENUE

Iowa E85 gallons sold (in millions)Q1 Q2 Q3 Q4

2014 2.71 2.98 3.34 2.932013 1.83 2.62 3.61 2.782012 2.32 2.31 2.78 1.662011 2.52 3.70 2.57 1.942010 1.62 2.77 2.85 2.08

L E S A F F R E A D V A N C E D F E R M E N T A T I O N T E C H N O L O G I E S

When you’ll head to cellulosic ethanol you’ll want to de-risk your fermentation process. CelluXTM is Leaf Technologies bioengineered yeast with proven results in operating second generation ethanol plants. Pioneers chose CelluX™ in their fermentation operations, so should you. Because when it comes to reliability, performance and yield, CelluX™ makes the difference.

www.leaftechnologies.com reliability performance yield

JUNE 2015 | Ethanol Producer Magazine | 31

In March, Oregon Gov. Kate Brown signed S.B. 324 into law. The bill removes the Dec. 31, 2015 sunset date from the state’s Clean Fuels Program. By signing S.B. 324, Brown has allowed the program to be implemented past the end of this year.

The program, which is similar to California’s Low Carbon Fuel Standard, requires a 10 percent reduction of green-house gases from transportation fuels over a 10-year period.

“I strongly support SB 324's goal to reduce greenhouse gas emissions. It is diffi cult to deny that we are seeing the ef-fects of a warming planet,” Brown said. “This year, 85 percent of our state is ex-periencing drought, with 33 percent ex-periencing extreme drought. This directly impacts 1.5 million Oregonians, hitting our rural communities the hardest. With California, Washington, and British Co-lumbia moving forward with their own

clean fuels programs, which will shape the West Coast market, it is imperative not only that Oregon does its part to re-duce greenhouse gas emissions but also that we build a program that meets the needs of Oregonians.”

Sunset date removed from Oregon Clean Fuels Program

California plant produces low-carbon,whole-beet ethanol

DISTILLED

Mendota Bioenergy LLC’s phase one dem-onstration plant in Fresno County, California, has successfully produced whole-beet ethanol. Project Manager Jim Tischer said the results that arrived in March were quite favorable. “We’ve made the fi rst whole-beet, low-carbon ethanol in the United States,” he said.

The developers now need California En-ergy Commission approval before moving on to phase two, proving the process in larger reactors and with more complex equipment. Though the demo facility has a 1 MMgy capac-ity, Tischer said the initial production runs will be smaller, dependent upon the availability of feedstock. The Phase II demonstration is ex-pected to run in mid- to late-summer, when the next crop of energy beets is ready for harvest.

Sugar beets are a familiar ethanol feed-stock, but until now that feedstock has been produced from the standard sugar extraction process using steam. Mendota Bioenergy’s pro-cess sizes down the whole beets, warms them up and liquefi es using enzymes.

Oregon Clean Fuels StandardRequired reduction

2016 0.25%2017 0.50%2018 1.00%2019 1.50%2020 2.50%2021 3.50%2022 5.00%2023 6.50%2024 8.00%2025 and beyond

10.00%

SOURCE: OREGON DEPARTMENT OF ENVIRONMENTAL QUALITY

32 | Ethanol Producer Magazine | JUNE 2015

The Advanced Energy Economy recently commissioned a study com-pleted by Navigant Research that found the U.S. advanced energy market grew by 14 percent last year, which is fi ve times the rate of the U.S. economy overall. Ac-cording to the report, the U.S. advanced energy market was worth an estimated $199.5 billion in 2014.

According to the report, fuel pro-duction was the fourth largest advanced energy segment last year, with an estimat-ed $148.1 billion in global revenue. The segment grew by an estimated 4 percent from 2013 to 2014, with a 34 percent

increase from 2011 to 2014. “Ethanol and butanol, including both sales of fuel and investment in refi nery infrastructure, continued to be the leading source of revenue with a combined $78 billion in revenue, representing 2 percent growth over 2013,” said Navigant Research in the report.

Globally, sales of ethanol and bu-tanol reached approximately 25.8 billion gallons last year, up from 23.4 billion in 2011. Ethanol made up the majority of that volume. U.S. sales of ethanol totaled an estimated 14.2 billion gallons, equat-ing to $39.1 billion in revenue.

DISTILLED

Report illustrates value of US, global ethanol market

Ceres, Raízen announce sweet sorghum project

Ceres Inc. and Brazil-based Raízen S.A. have signed a multiyear collaboration agreement to de-velop and produce sweet sorghum on an industrial scale. Sweet sorghum can be grown to complement existing feedstock supplies, extending the operating season of Brazilian sugarcane-to-ethanol mills.

Under the agreement, the companies will con-tribute in-kind services and resources and share in the revenue from the ethanol produced from Ceres’ sweet sorghum above certain levels. This season, Raízen has planted Ceres’ sweet sorghum in a single location and plans to expand to multiple mills in the future.

“The ethanol industry in Brazil has a history of successfully competing against low-priced oil and we believe that sweet sorghum, which has lower production costs than sugarcane, can be further developed and scaled up as an integral part of the industry’s feedstock supply,” said Richard Hamilton, president and CEO of Ceres.

SOURCE: NAVIGANT RESEARCH, "ADVANCED ENERGY NOW 2015 MARKET REPORT"

Ethanol and butanol fuel production revenue (millions) 2011 2012 2013 2014 (estimate)

U.S. $39,140 $41,730 $40,371 $40,932Global $68,140 $84,240 $76,645 $77,956

JUNE 2015 | Ethanol Producer Magazine | 33

Environmental Entrepreneurs (E2) recently released its fourth-quarter and year-end 2014 jobs report, which shows contin-ued growth of clean energy and clean trans-portation jobs in the U.S.

For the full year 2014, E2 reported 46,783 clean energy and clean transportation jobs were announced at 177 projects. A to-tal of 23,625 renewable energy jobs at 112 projects were announced last year, including

813 biofuel jobs at eight projects, 125 bio-gas jobs at four projects, and 399 biomass power jobs at seven projects. The remain-ing renewable energy jobs were announced for geothermal, solar and wind projects. The 46,783 jobs announced last year also included 16,015 manufacturing jobs, 2,266 jobs classifi ed as “other,” 2,000 public trans-portation jobs, 1,932 recycling jobs and 925 building effi ciency jobs.

E2 report tallies 2014 biofuel industry jobs

Report highlights corn ethanol's role in cellulosic development

DISTILLED

Third Way recently released a report highlight-ing the connection between fi rst- and second-gener-ation ethanol and the need for continued implemen-tation of the renewable fuels standard (RFS).

According to Third Way, 80 percent of com-mercial cellulosic ethanol capacity in the U.S. has been developed by companies with extensive back-grounds in corn ethanol. The report stresses invest-ment from these companies is critical to growing U.S. cellulosic capacity, especially in the near-term. First Way also notes that certain proposals to re-form the RFS would discourage engagement from the corn ethanol industry, causing delays in the com-mercialization of cellulosic ethanol in the U.S. and potentially driving investment overseas.

Within the report, Third Way said the four cel-lulosic ethanol companies it examined all have plans to rapidly expand their technologies to additional facilities. This expansion could help bring the cost of cellulosic ethanol down. Efforts to alter the RFS, however, could derail those plans.

2014 job announcements No. of jobs No. of job

announcements Renewable energy jobs 23,625 112

Biofuel 813 8Biogas

(generation)125 4

Biomass (generation)

399 7

Total clean energy jobs 46,783 177SOURCE: ENVIRONMENTAL ENTREPRENEURS

find it online at

directory.ethanolproducer.com

BROWSE CATEGORIES BROWSE COMPANIES

maintenance services| FINDOne FREE Listing per Company

34 | Ethanol Producer Magazine | JUNE 2015©2015 Lallemand Biofuels & Distilled Spirits. All rights reserved.©20©20©20151515 LalLalLalLallemlemlemmandandand BiBiBiofuofuofuofuelselselsels & &&& DisDisDisDistiltiltiltilledledleded SpSpSpSpiriririts.ts.t AlAll rl rrrighighig ts ts ts resresservervr ed.ed.

DRY YEAST

(Bio-Ferm®)

CAKE YEAST

(Thermosacc® Gold)

LIQUID YEAST

(Stabilized Liquid Yeast)

(

GA PRODUCING YEAST

(TransFerm®)

GA PRODUCING &

YIELD BOOSTING YEAST

(TransFerm® Yield+)

WE DIDN’T JUST

CHANGE THE GAMEWE DIDN’T JUST

CHANGE THE GAME

WE WROTE THE RULESSince day one, Lallemand Biofuels & Distilled Spirits has been the driver behind many modern ethanol fermentation advancements. No other company has delivered more technological breakthroughs to help make ethanol production efficient and profitable.

Our customer partners fuel our pursuit of innovation. We reward these partnerships by offering the industry’s highest quality products, service and educational resources.

As writers of The Alcohol Textbook and organizers of The Alcohol School, we have established new industry standards. Through our innovation we’ve changed the game to your advantage.

Contact us today at +1-866-342-7026 or www.lallemandbds.com.

JUNE 2015 | Ethanol Producer Magazine | 35

36 | Ethanol Producer Magazine | JUNE 2015

AAfterr aa lloonngg sttrreettcchh ooff pprroofi ttabiility, tthherree aare ffeeww U..SS. eetthhaannooll pprroodduucceerrs "aapppproaacchhinngg tthe ttaabblee"" tto sseellll. BBuutt tthhaat ccoouulldd chaannggee. BByyy Tooommm Bryyyyaaannn

How DealsSquare UP

BUSINESS

JUNE 2015 | Ethanol Producer Magazine | 37

BUSINESS

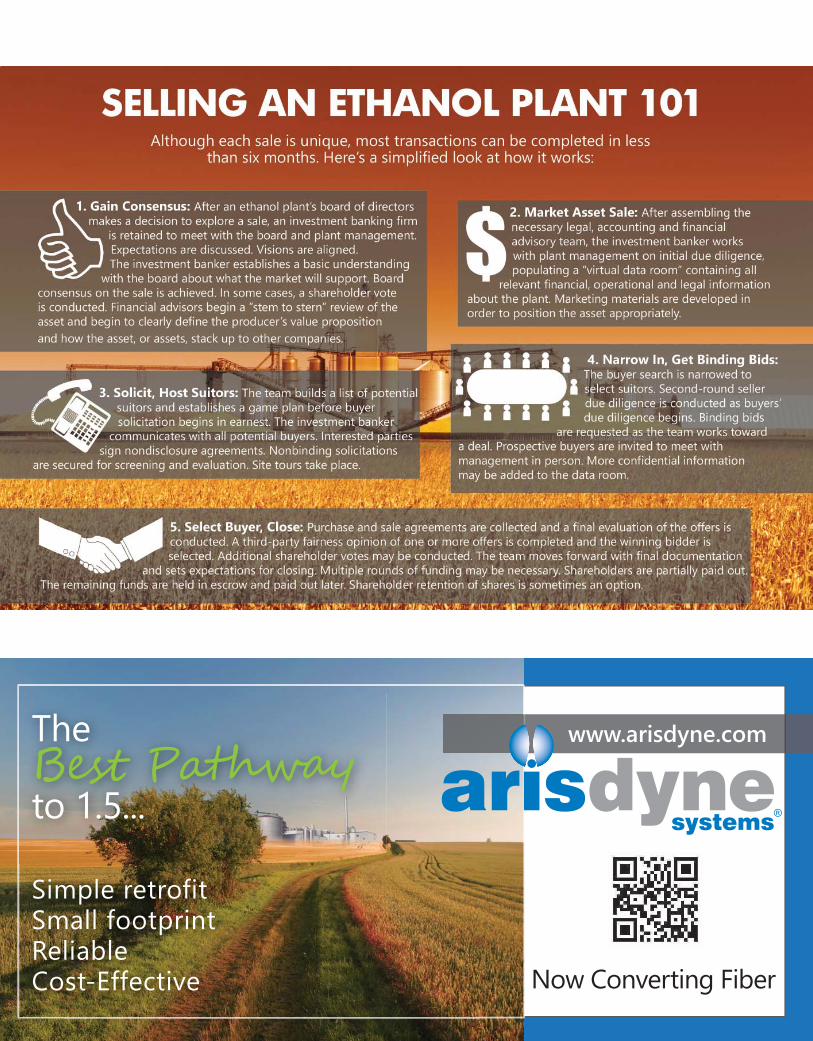

Like golf, ethanol mergers and acquisitions (M&A) is game of opposites. A golfer swings right to draw the ball left, left to cut it right, down to send it up. Ethanol M&A, too, work on ironic inverse relationships. Transaction numbers spike after bad times and dip during good times. High margins work against deals. Low margins produce them. Simply put, when profi tability goes up, ethanol M&A activity generally goes down.

After the 2008 downturn, for example, 29 ethanol plants traded hands in 18 transactions before the end of 2010, accord-ing to Mark Fisler, managing director at Los Angeles-based in-vestment banking fi rm Ocean Park Advisors. “That was a huge amount of volume over a two-year stretch,” Fisler says, explain-ing that improved margins, starting in 2010, yielded only fi ve ethanol plant acquisitions in four deals in 2011. Then low M&A activity continued through the fi rst half of 2012 following a generally profi table 2011.

Production margins sagged in 2012, spurring the sale of six ethanol plants late in the year and setting the stage for double-digit transactions in 2013. “We saw 13 ethanol plants acquired in 10 transactions that year,” Fisler says. “It was driven mostly by weak balance sheets and distress coming off 2012. “Clearly, the industry sees more transactions on the heels of distressed cycles than it does during or after good times.”

That last big M&A run ended when the ethanol industry cycled into an epic 18-month stretch of record margins from

mid-2013 through late 2014. “I would characterize the last year and a half as a period of low M&A activity, but it depends on what you compare it to,” Fisler says, explaining that there were fi ve ethanol asset transactions completed in 2014. “There are a lot of reasons for that, includ-ing the fact that ethanol margins were so good through most of 2013 and 2014.”

Most but not all M&A ac-tivity in the ethanol industry since 2008 has been a story of leaders acquiring laggards. A vast majority of the deals were fi nancially distressed independent plants acquired by large, inte-grated ethanol producers. Today, Fisler says, “strategic produc-ers” remain interested in acquiring ethanol plants, but sellers are scarce. “We’re four months into the year and there really isn’t an announced 2015 deal at this point,” he says. “There are whis-pers about deals—and we are in talks with various people—but ethanol producers just aren’t approaching the table. So there’s a lot of interest in transactions but very few producers looking at a sale.”

Fisler continues, “When you talk to a producer who just made 60, 70, 80 cents a gallon last year, it’s pretty hard for them to get excited about where plants are trading. Ethanol plants are [selling for] roughly $1.60 per gallon on nameplate capacity or

DIEMME® FILTRATION

FILTER PRESSES FOR THE

BIOETHANOL PROCESS

Over the years Diemme® Filtration developed a sound experience in solid/liquid separation in the process of Bioethanol Second Generation production, thanks to its unique know how and its unrivalled R&D capabilities.

BILFINGER WATER TECHNOLOGIESwww.water.bilfinger.com

______

______

Fisler

BUSINESS

JUNE 2015 | Ethanol Producer Magazine | 39

Simple retrofitSmall footprintReliableCost-Effective

The to 1.5...

www.arisdyne.com

Now Converting Fiber

40 | Ethanol Producer Magazine | JUNE 2015

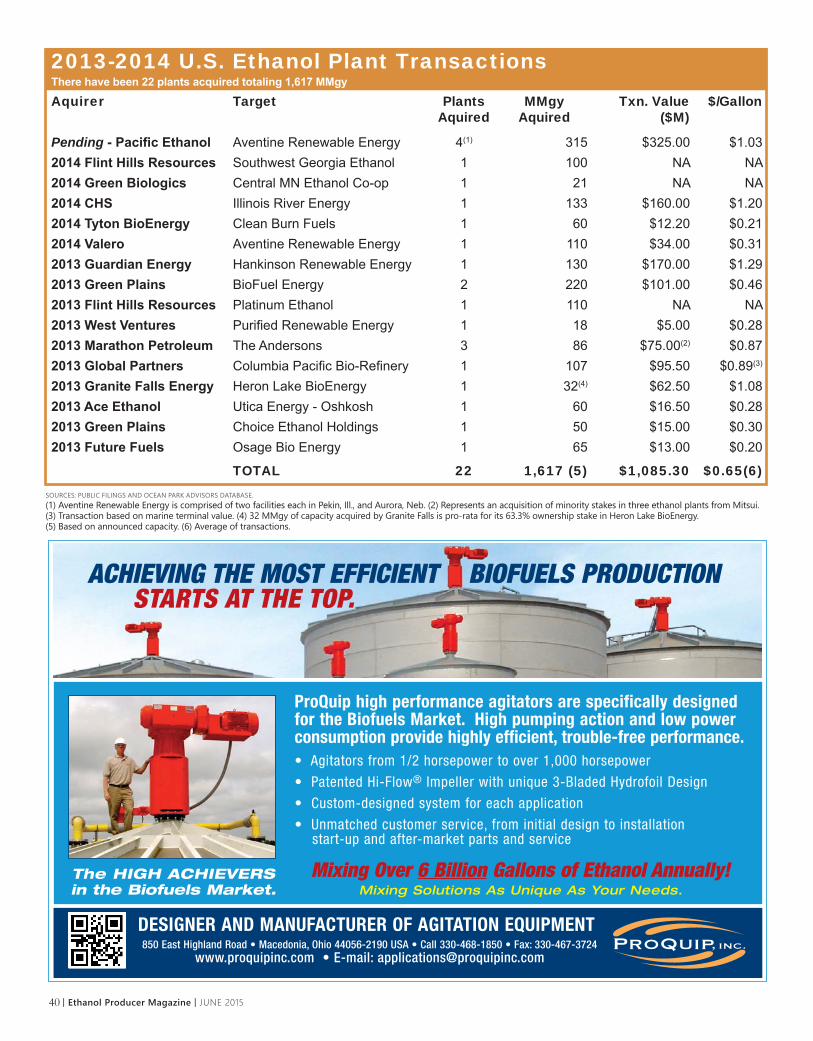

2013-2014 U.S. Ethanol Plant TransactionsThere have been 22 plants acquired totaling 1,617 MMgyAquirer Target Plants

AquiredMMgy

AquiredTxn. Value

($M)$/Gallon

Pending - Pacifi c Ethanol Aventine Renewable Energy 4(1) 315 $325.00 $1.032014 Flint Hills Resources Southwest Georgia Ethanol 1 100 NA NA2014 Green Biologics Central MN Ethanol Co-op 1 21 NA NA2014 CHS Illinois River Energy 1 133 $160.00 $1.202014 Tyton BioEnergy Clean Burn Fuels 1 60 $12.20 $0.212014 Valero Aventine Renewable Energy 1 110 $34.00 $0.312013 Guardian Energy Hankinson Renewable Energy 1 130 $170.00 $1.292013 Green Plains BioFuel Energy 2 220 $101.00 $0.462013 Flint Hills Resources Platinum Ethanol 1 110 NA NA2013 West Ventures Purifi ed Renewable Energy 1 18 $5.00 $0.282013 Marathon Petroleum The Andersons 3 86 $75.00(2) $0.872013 Global Partners Columbia Pacifi c Bio-Refi nery 1 107 $95.50 $0.89(3)

2013 Granite Falls Energy Heron Lake BioEnergy 1 32(4) $62.50 $1.082013 Ace Ethanol Utica Energy - Oshkosh 1 60 $16.50 $0.282013 Green Plains Choice Ethanol Holdings 1 50 $15.00 $0.302013 Future Fuels Osage Bio Energy 1 65 $13.00 $0.20

TOTAL 22 1,617 (5) $1,085.30 $0.65(6)SOURCES: PUBLIC FILINGS AND OCEAN PARK ADVISORS DATABASE.(1) Aventine Renewable Energy is comprised of two facilities each in Pekin, Ill., and Aurora, Neb. (2) Represents an acquisition of minority stakes in three ethanol plants from Mitsui.(3) Transaction based on marine terminal value. (4) 32 MMgy of capacity acquired by Granite Falls is pro-rata for its 63.3% ownership stake in Heron Lake BioEnergy.(5) Based on announced capacity. (6) Average of transactions.

ACHIEVING THE MOST EFFICIENT BIOFUELS PRODUCTIONSTARTS AT THE TOP.

ProQuip high performance agitators are specifically designed for the Biofuels Market. High pumping action and low power consumption provide highly efficient, trouble-free performance.• Agitators from 1/2 horsepower to over 1,000 horsepower

• Patented Hi-Flow® Impeller with unique 3-Bladed Hydrofoil Design

• Custom-designed system for each application

• Unmatched customer service, from initial design to installationstart-up and after-market parts and service

The HIGH ACHIEVERS in the Biofuels Market.

850 East Highland Road • Macedonia, Ohio 44056-2190 USA • Call 330-468-1850 • Fax: 330-467-3724www.proquipinc.com • E-mail: [email protected]

DESIGNER AND MANUFACTURER OF AGITATION EQUIPMENT

Mixing Over 6 Billion Gallons of Ethanol Annually!Mixing Solutions As Unique As Your Needs.

JUNE 2015 | Ethanol Producer Magazine | 41

Seven buyers have bought 64 percent of plants and 68 percent of capacity since 2009. In all there have been 28 buyers in fi ve years.

SOURCE: OCEAN PARK ADVISORS

Single Acquisition BuyersGreen Biologics / 21 MMgy - 2014CHS / 133 MMgy - 2014Global LP / 107 MMgy - 2013Central Farmers Co-op / 100 MMgy - 2009Poet / 90 MMgy - 2010SiemKapital & North Atlantic Value(1) /87 MMgy - 2011Marathon Petroleum /86 MMgy - 2013Future Fuels / 65 MMgy - 2013TytonBioEnergy / 60 MMgy - 2014Ace Ethanol / 60 MMgy - 2013Aemetis / 55 MMgy - 2012Pratt Biofuel / 55 MMgy - 2012The Andersons / 55 MMgy - 2012Carbon Green / 50 MMgy - 2009REX / 50 MMgy - 2011Nebraska Corn Processing / 44 MMgy - 2009Palmer Energy / 40 MMgy - 2012Aventine / 38 MMgy - 2010Granite Falls / 32 MMgy - 2013Gevo /22 MGPY - 2010West Ventures /18 MMgy - 2013