Embed Size (px)

Citation preview

june

2008

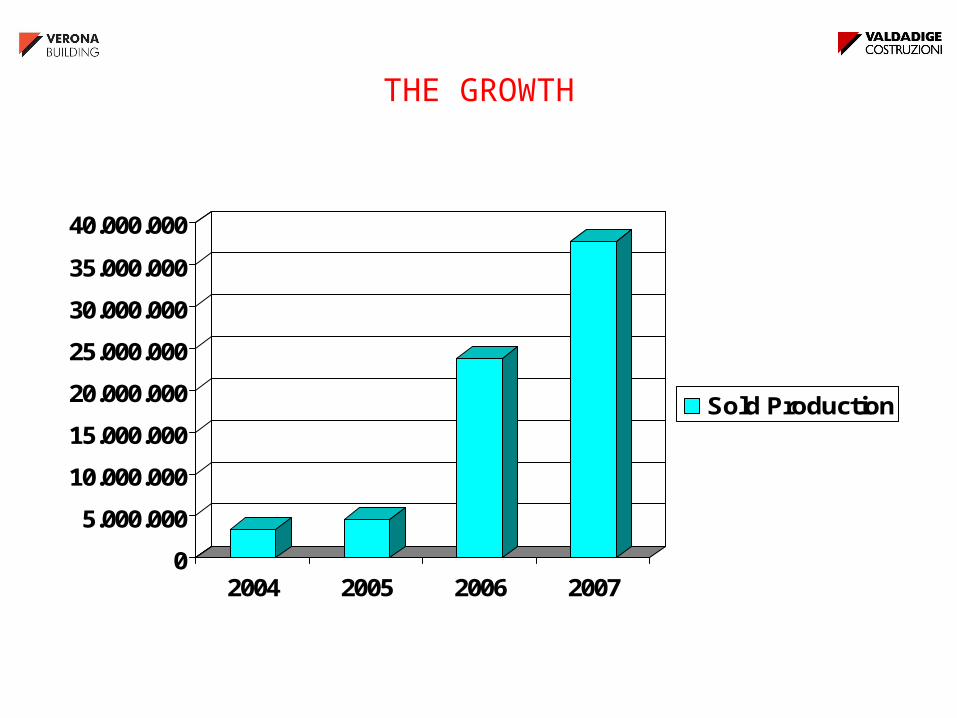

THE GROWTH

0

5.000.000

10.000.000

15.000.000

20.000.000

25.000.000

30.000.000

35.000.000

40.000.000

2004 2005 2006 2007

Sold Production

0

5

10

15

20

25

30

35

2004 2005 2006 2007

Staff

STAFF

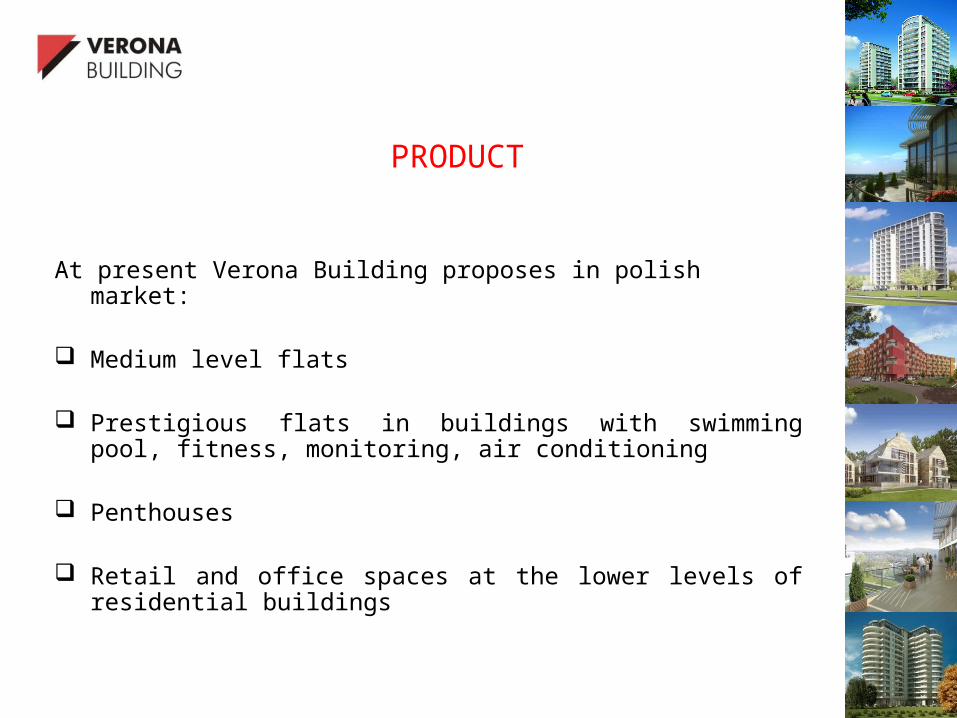

PRODUCT

At present Verona Building proposes in polish market:

Medium level flats

Prestigious flats in buildings with swimming pool, fitness, monitoring, air conditioning

Penthouses

Retail and office spaces at the lower levels of residential buildings

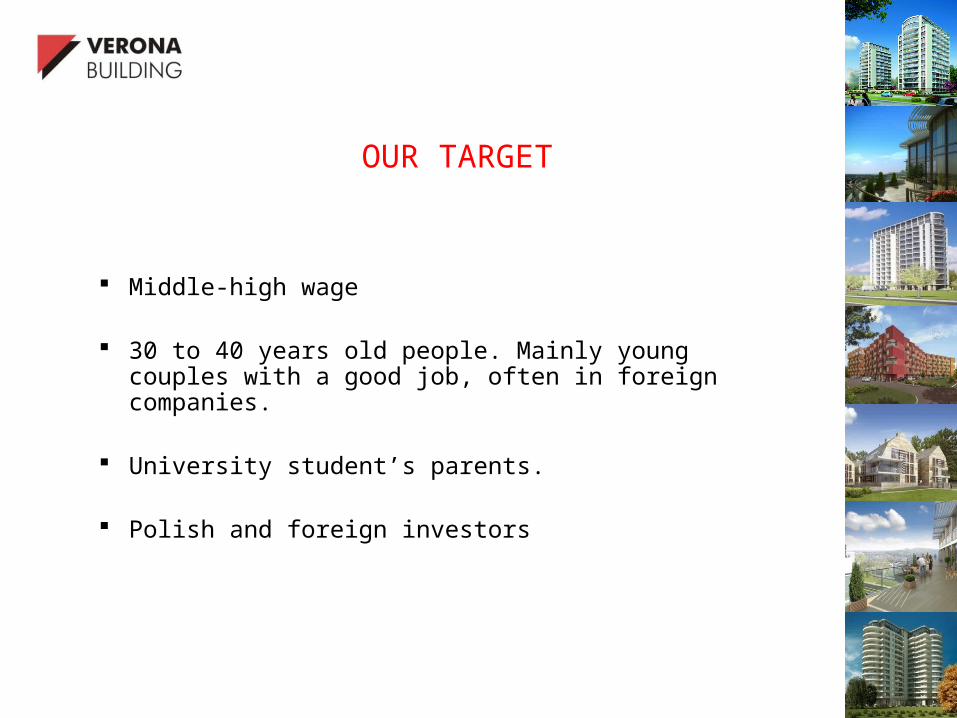

OUR TARGET

Middle-high wage

30 to 40 years old people. Mainly young couples with a good job, often in foreign companies.

University student’s parents.

Polish and foreign investors

MARKETING STRATEGY

Each project conceived as Unique Selling Proposition.

Advertisement (press, web..), specialized fairs, outdoor events, billboards.

Strong corporate identity

UNDER CONSTRUCTION AND SECURED PIPELINE

• Surface: 12 000 m2 (145 flats, 1.600 m2 retail, 1.600 m2 office)

• Start: July 2006

• End: December 2008

• Sales: 22 mln Euro

• All sold out

• Surface : 10.000 m2 (166 flats, swimming pool, fitness)

• Start: July 2006 • End: October 2008

• Sales: 20 mln € • 85% sold

TARASY VERONA 2

• Surface: 5.000 m2 (90 flats + retail) • Start: November 2008 • End: December 2010 • Sales: 12 mln €

• Surface: 9.700 m2 (182 flats, 700 m2 retail)

• Start: September 2007

• End: December 2009

• Sales : 20 mln €

• 65% sold

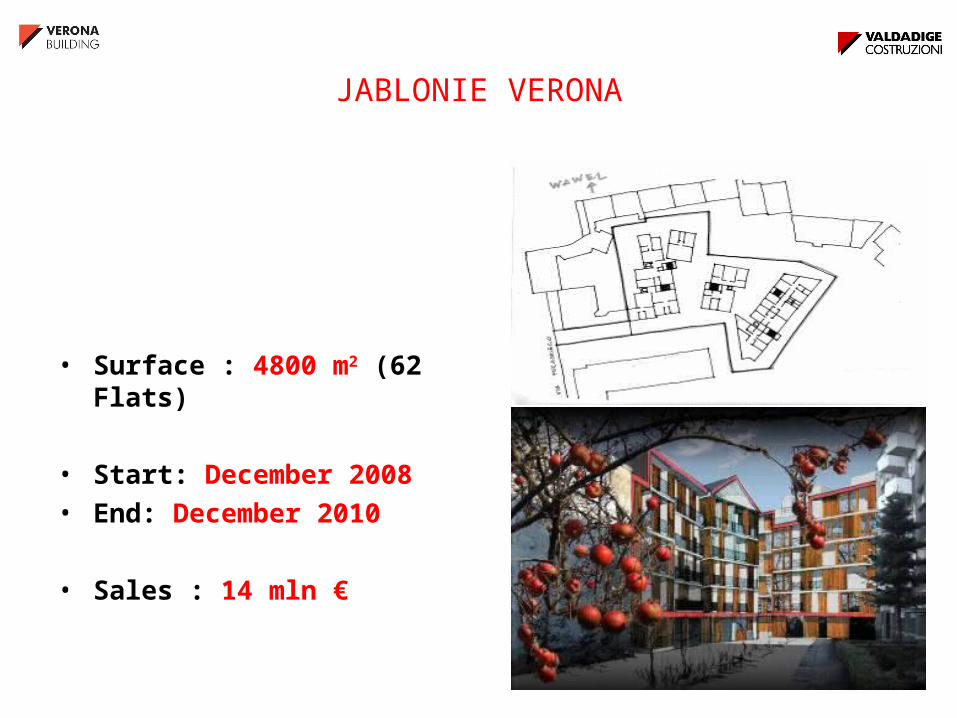

JABLONIE VERONA

• Surface : 4800 m2 (62 Flats)

• Start: December 2008 • End: December 2010

• Sales : 14 mln €

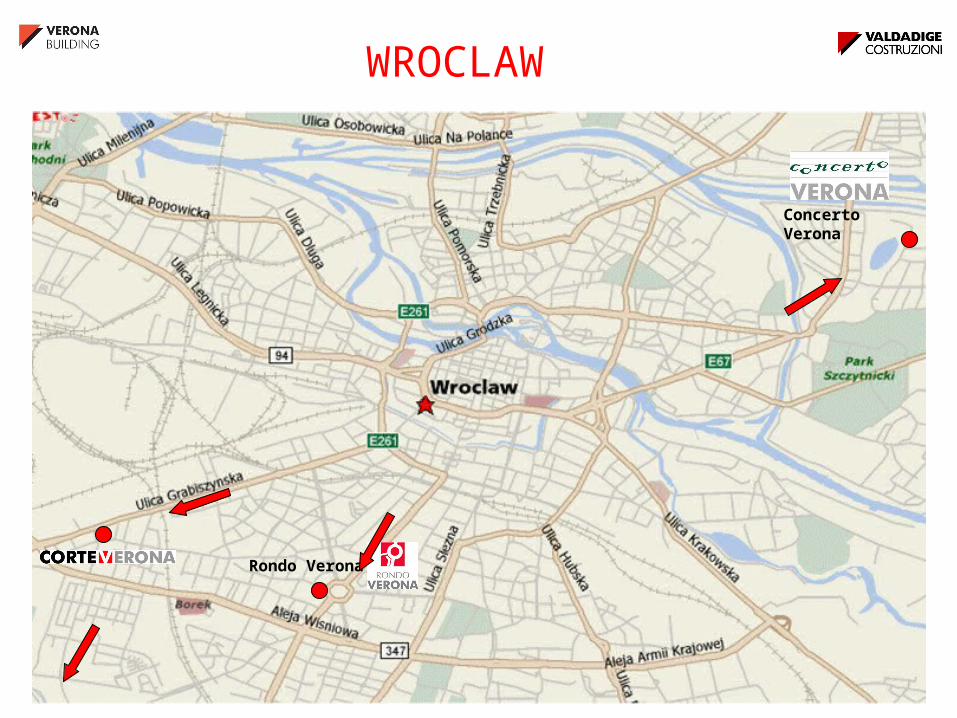

WROCLAW

Rondo Verona

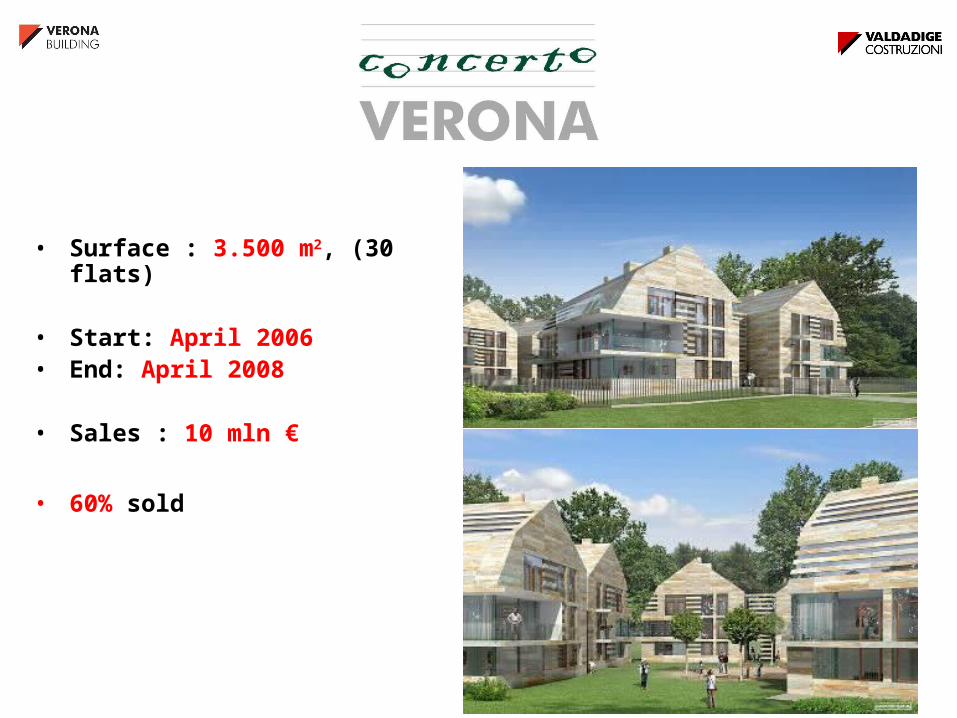

Concerto Verona

• Surfaces: 14.000 m2, (145 flats3.000 m2 retail, 3.000 m2 offices)

• Start: October 2004 • End: July 2007

• Sales: 25 mln €• All sold out

• Surface : 3.500 m2, (30 flats)

• Start: April 2006 • End: April 2008

• Sales : 10 mln €

• 60% sold

• Surface : 23.500 m2, (350 flats, 2.700 m2 retail, 1.500 m2 offices)

• Start: April 2007 • End: December 2009

• Sales : 46 mln €

• 50% sold

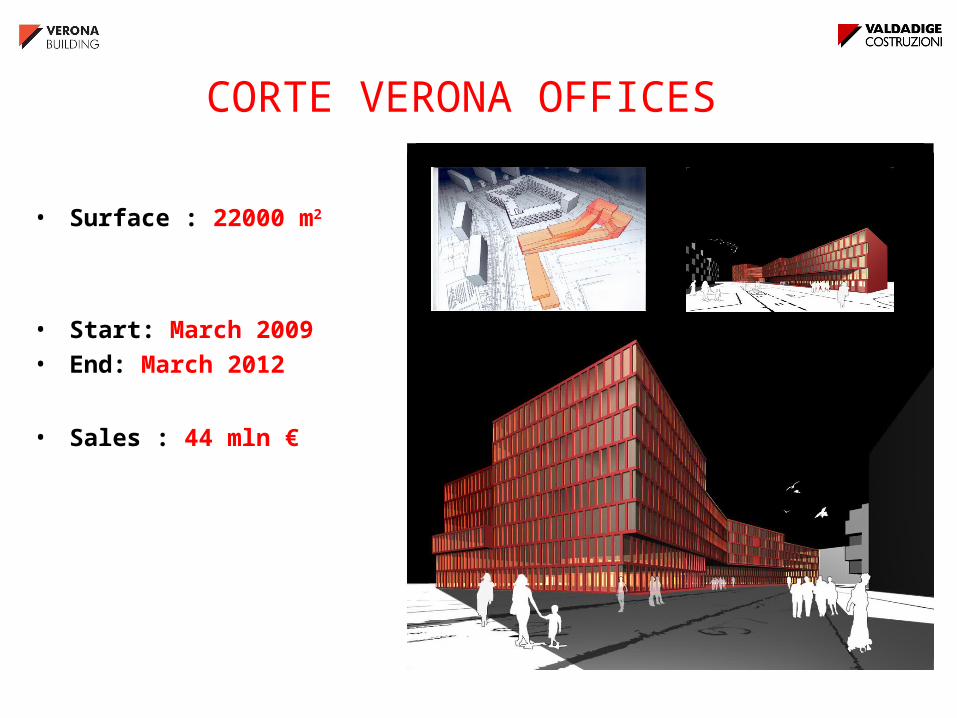

CORTE VERONA OFFICES

• Surface : 22000 m2

• Start: March 2009

• End: March 2012

• Sales : 44 mln €

OPOROW

• Surface (1+2): 26000m2

• Start: April 2009

• End: June 2013

• Sales 55 mln €

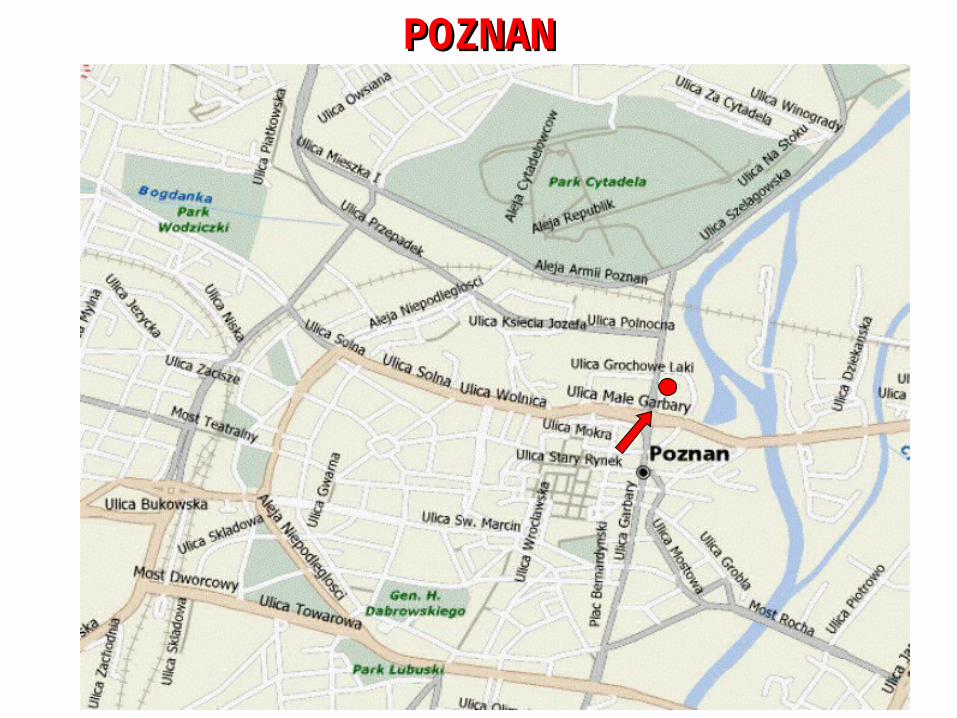

POZNANPOZNAN

GARBARY VERONA

• Surface : 8.000 m2

(120 Flats, 800 m2 Retail)

• Start: Marzo 2008

• End: Giugno 2010

• Sales: 21,5 mln €

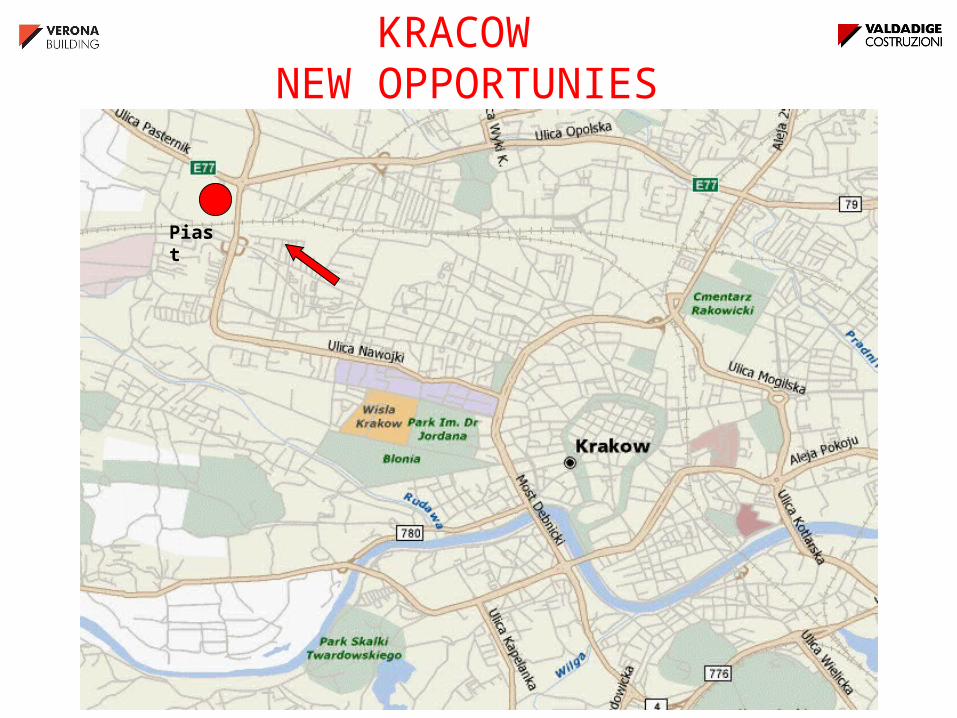

KRACOW NEW OPPORTUNIES

Piast

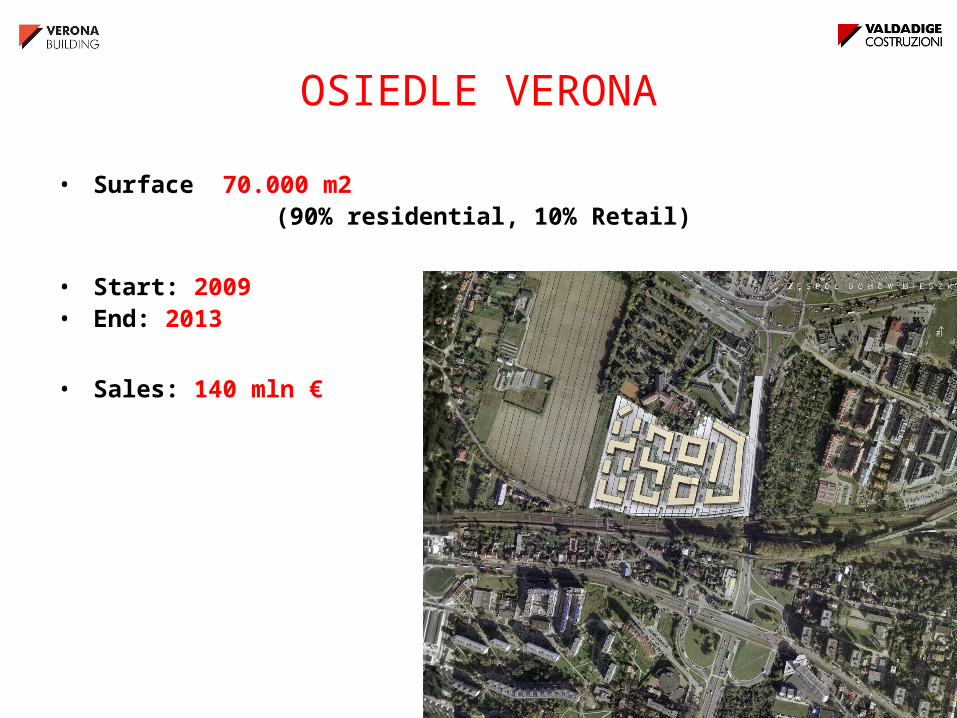

OSIEDLE VERONA

• Surface 70.000 m2 (90% residential, 10% Retail)

• Start: 2009 • End: 2013

• Sales: 140 mln €

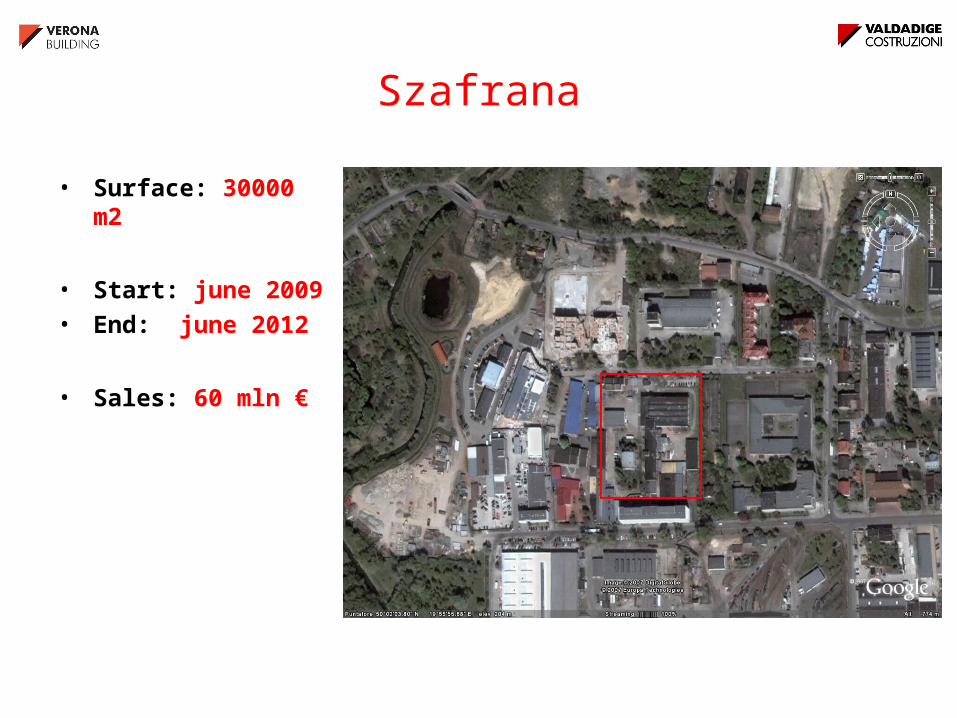

Szafrana

• Surface: 30000 m2

• Start: june 2009

• End: june 2012

• Sales: 60 mln €

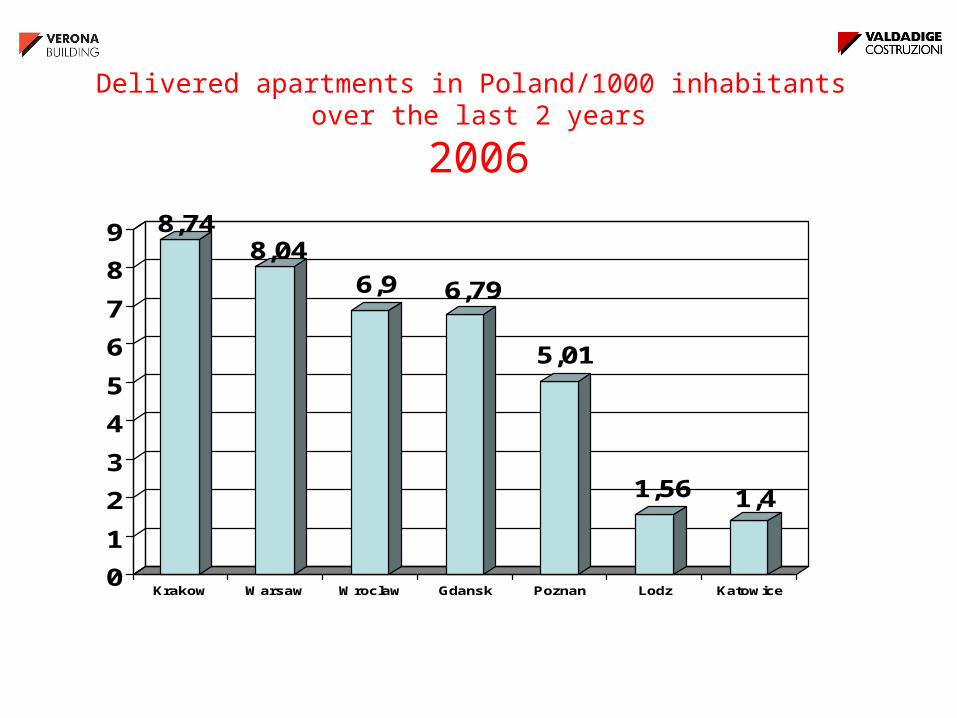

Delivered apartments in Poland/1000 inhabitants over the last 2 years

20068,74

8,04

6,9 6,79

5,01

1,56 1,4

0

1

2

3

4

5

6

7

8

9

Krakow Warsaw Wroclaw Gdansk Poznan Lodz Katowice

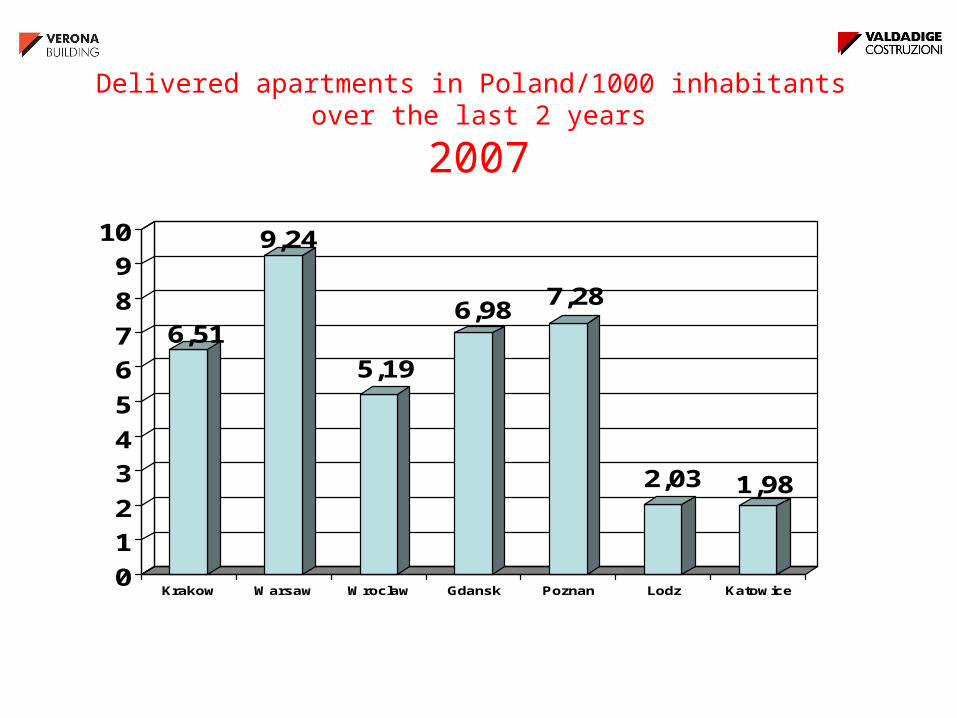

Delivered apartments in Poland/1000 inhabitants over the last 2 years

2007

6,51

9,24

5,19

6,987,28

2,03 1,98

0

1

2

3

4

5

6

7

8

9

10

Krakow Warsaw Wroclaw Gdansk Poznan Lodz Katowice

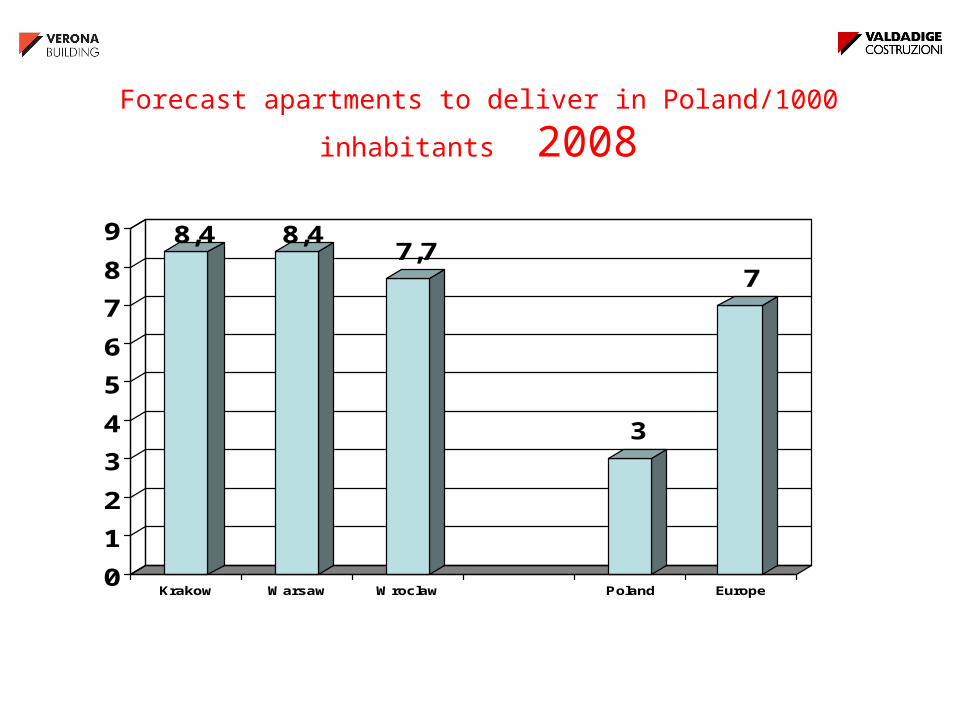

Forecast apartments to deliver in Poland/1000 inhabitants 2008

8,4 8,47,7

3

7

0

1

2

3

4

5

6

7

8

9

Krakow Warsaw Wroclaw Poland Europe

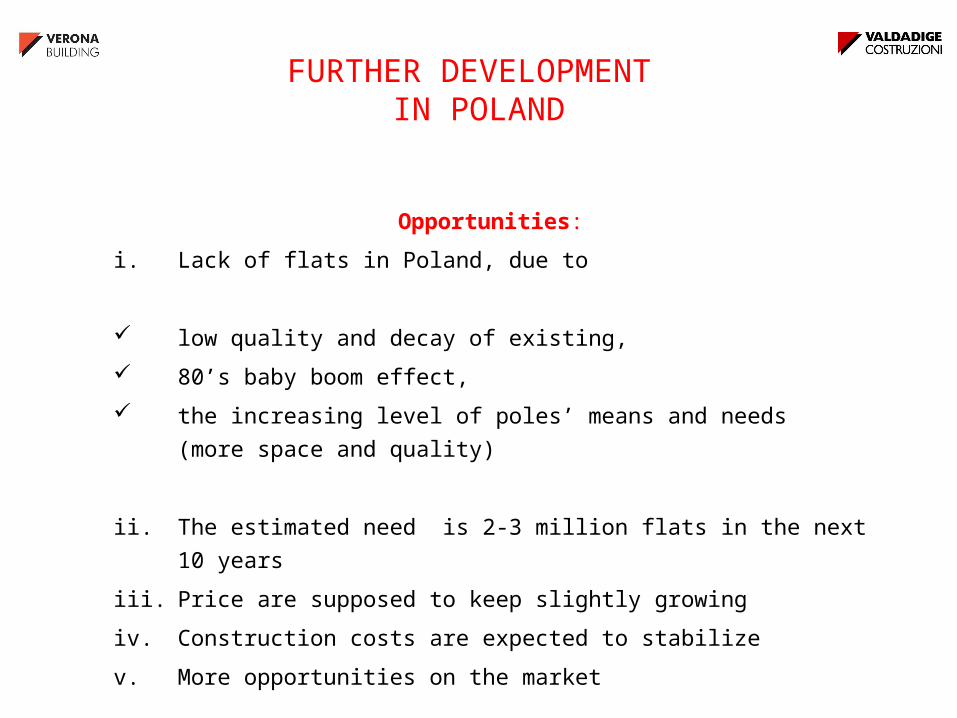

FURTHER DEVELOPMENT IN POLAND

Opportunities:

i. Lack of flats in Poland, due to

low quality and decay of existing,

80’s baby boom effect,

the increasing level of poles’ means and needs (more space

and quality)

ii. The estimated need is 2-3 million flats in the next 10 years

iii. Price are supposed to keep slightly growing

iv. Construction costs are expected to stabilize

v. More opportunities on the market

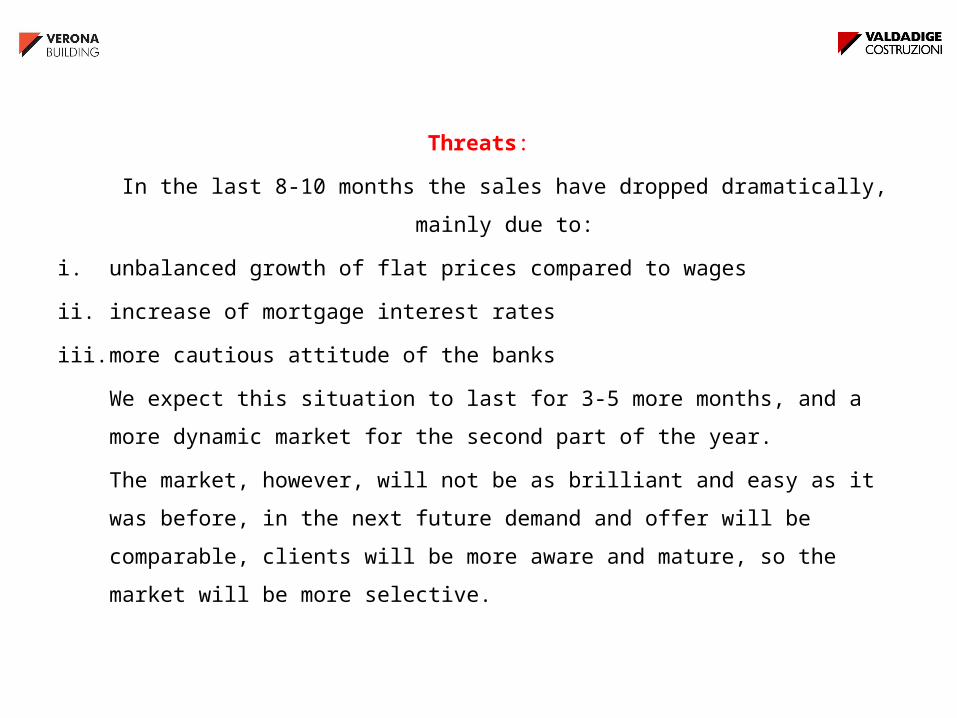

Threats:

In the last 8-10 months the sales have dropped dramatically, mainly due to:

i. unbalanced growth of flat prices compared to wages

ii. increase of mortgage interest rates

iii. more cautious attitude of the banks

We expect this situation to last for 3-5 more months, and a more dynamic market for

the second part of the year.

The market, however, will not be as brilliant and easy as it was before, in the next

future demand and offer will be comparable, clients will be more aware and mature,

so the market will be more selective.

If this is the scenario we will have to:

Select the opportunities with more caution as far as location, size and price

are concerned

Keep average price per sqm compatible with average families’ means

(today 2000 €), except for locations and projects intended for a different

target.

Spread the activity in the country (one new town every 1,5-2 years)

Keep quality level and customer satisfaction as first priority

Give every project an outstanding peculiarity

Use all means for an effective and innovating communication policy

FURTHER DEVELOPMENT IN EAST EUROPE

• Romania

• Serbia

• Bulgaria

US