Embed Size (px)

Citation preview

June 1985

... -J

Staff Paper No. 239

EFFECT OF IMITATION OR

FILLED DAIRY PRODUCTS

by

Truman F. Graf

University of Wisconsin Madison, Wisconsin

EFFECT OF IMITATION OR FILLED DAIRY PRODUCTS

by

Truman F. Graf Department of Agricultural Economics

University of Wisconsin-Madison

Presented at Eightieth Annual Meeting

American Dairy Science Association University of Illinois

Urbana-Champaign, Illinois June 12, 1985

Introduction

The dairy industry is confronted with a myriad of problems including

stagnant prices, increasing costs, surpluses, lagging per capita consumption,

subsidized imports, an unfavorable international market, and imitation dairy

products. Many of the other problems derive in part from the imitation problem,

which in turn derives from profit maximization decisions independent of

dairying, and thus is less subject to correction by the dairy industry than are

many of its other problems. Many therefore feel the imitation problem is the

greatest single challenge facing the dairy industry. This paper analyzes the

economic effects of imitation dairy products.

Imitation Impact

Harket Impact

Research findings of the United Dairy Industry Association (UDIA), reported

by the Chief Executive Officer, at the group's 1982 Annual Heeting, quantified

the U.S. dairy imitation volume as follows:

(a) 30% of the overall market for dairy products;

(b) 72% of the butter market;

(c) 50% of the cream market;

(d) 15% of the fluid milk market;

(e) 5% of the cheese market; and

(f) 1.7% of the ice cream market.

- 2 -

The large proportion of the dairy market claimed by imitations, naturally

has a tremendously negative impact on the dairy market.

Product Impact

UDIA research indicated the following imitation vulnerability ranking of

dairy products:

(1) cheese;

(2) cream;

(3) fluid milk;

(4) ice cream;

(5) butter;

(6) cottage cheese; and

(7) yogurt.

Unfortunately cheese which is the second heaviest utilizer of milk (29% in

1984), is the most vulnerable to increased competition from imitations.

Imitation cheese consumption continues to increase, and poses an increasing

challenge to the dairy industry.

Dairy Industry Impact

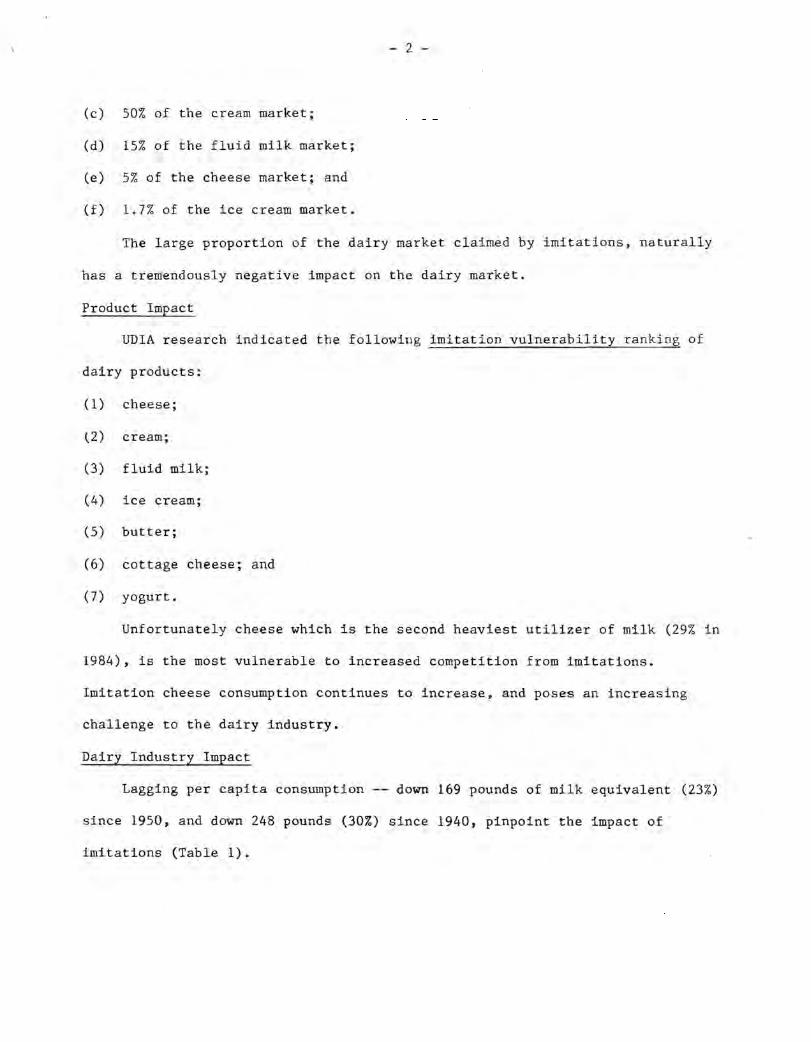

Lagging per capita consumption -- down 169 pounds of milk equivalent (23%)

since 1950, and down 248 pounds (30%) since 1940, pinpoint the impact of

imitations (Table 1).

- 3 -

TABLE 1

Per Capita Civilian Consumption of Milk Equivalent

Pounds

1940 830

1950 751

1960 653

1970 561

1980 544

1984 582

Increased use of imitation dairy products are important factors in the

reduction in dairy consumption.

Vegetable Fat Impact

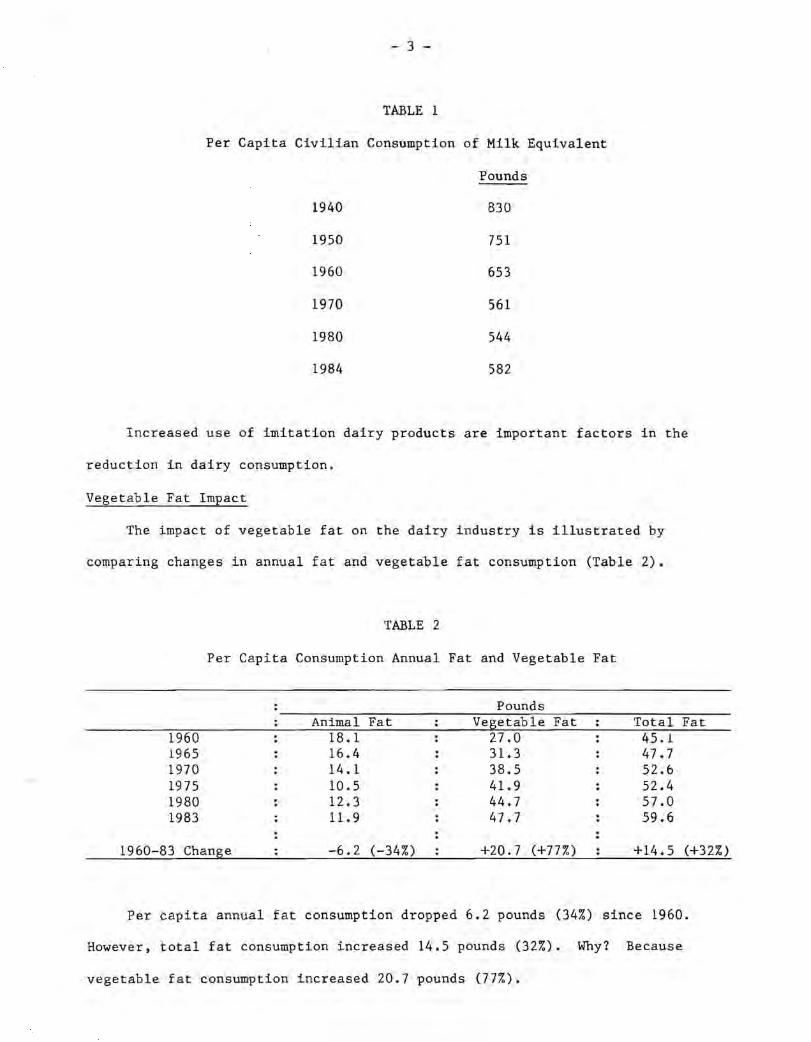

The impact of vegetable fat on the dairy industry is illustrated by

comparing changes in annual fat and vegetable fat consumption (Table 2).

TABLE 2

Per Capita Consumption Annual Fat and Vegetable Fat

Pounds Animal Fat Vegetable Fat Total Fat

1960 18.1 27.0 45.1 1965 16.4 31.3 47.7 1970 14.1 38.5 52.6 1975 10.5 41.9 52.4 1980 12.3 44.7 57.0 1983 11.9 47.7 59.6

1960-83 Change -6.2 (-34%) +20.7 (+77%) +14.5 (+32%)

Per capita annual fat consumption dropped 6.2 pounds (34%) since 1960.

However, total fat consumption increased 14.5 pounds (32%). Why? Because

vegetable fat consumption increased 20.7 pounds (77%).

- 4 -

People are eating more fat than ever,---not less as is commonly believed.

However, the dairy indu~try is not sharing in the increase in fat consumption.

Instead its products are being displaced by vegetable products.

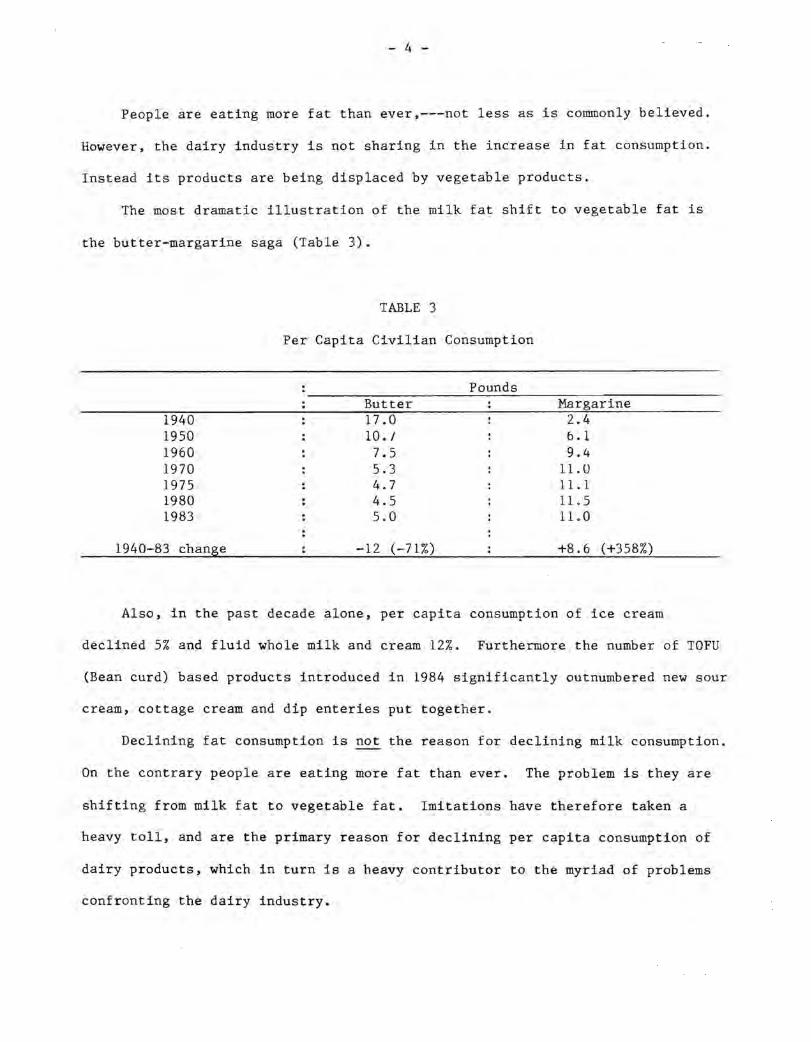

The most dramatic illustration of the milk fat shift to vegetable fat is

the butter-margarine saga (Table 3).

1940 1950 1960 1970 1975 1980 1983

1940-83 change

TABLE 3

Per Capita Civilian Consumption

Butter 17.0 10. / 7.5 5.3 4.7 4.5 5.0

-12 (-71%)

Pounds Margarine

2.4 b.l 9.4

11.0 11.1 11.5 11.0

+8.6 (+358%)

Also, in the past decade alone, per capita consumption of ice cream

declined 5% and fluid whole milk and cream 12%. Furthermore the number of TOFU

(Bean curd) based products introduced in 1984 significantly outnumbered new sour

cream, cottage cream and dip enteries put together.

Declining fat consumption is not the reason for declining milk consumption.

On the contrary people are eating more fat than ever. The problem is they are

shifting from milk fat to vegetable fat. Imitations have therefore taken a

heavy toll, and are the primary reason for declining per capita consumption of

dairy products, which in turn is a heavy contributor to the myriad of problems

confronting the dairy industry.

- 5 -

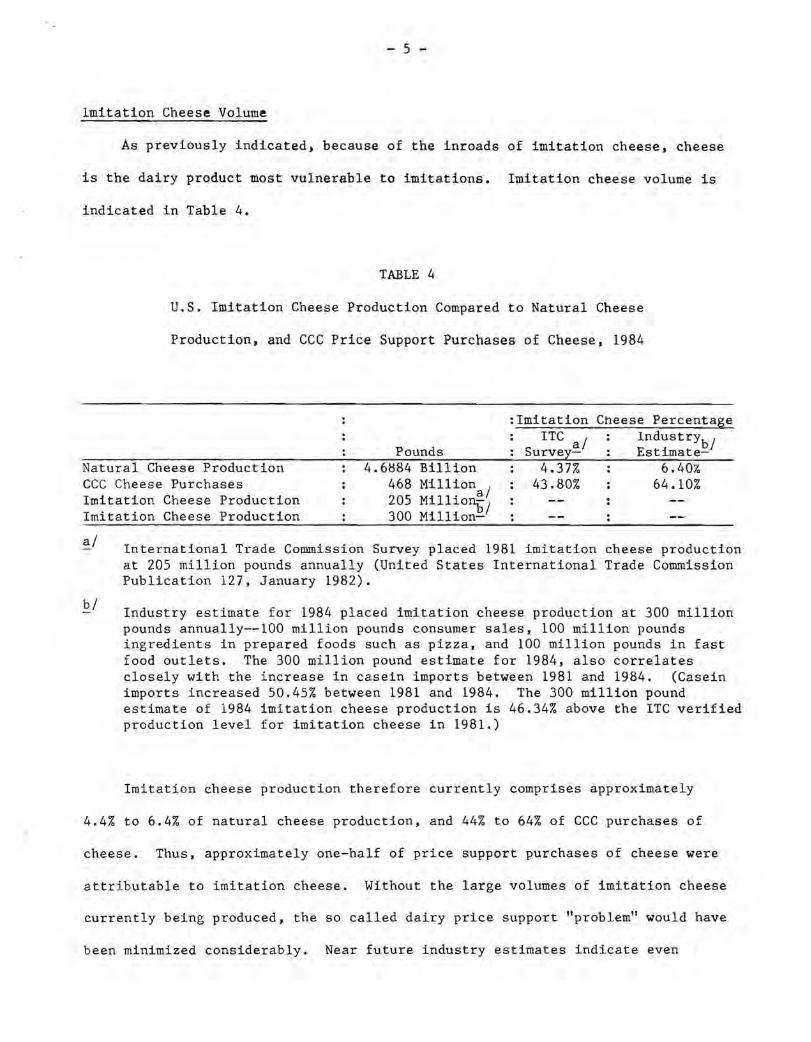

Imitation Cheese Volume

As previously indicated, because of the inroads of imitation cheese, cheese

is the dairy product most vulnerable to imitations. Imitation cheese volume is

indicated in Table 4.

TABLE 4

U.S. Imitation Cheese Production Compared to Natural Cheese

Production, and CCC Price Support Purchases of Cheese, 1984

Pounds

: Imitation ITC al

Survey-

Cheese Percentage IndustrYbl

. Estimate-

Natural Cheese Production CCC Cheese Purchases Imitation Cheese Production Imitation Cheese Production

4.6~84 Billion 468 Million I 205 Millio~1 300 Million-

4.37% 43.80%

6.407-64.10%

al

bl

International Trade Commission Survey placed 1981 imitation cheese production at 205 million pounds annually (United States International Trade Commission Publication 127, January 1982).

Industry estimate for 1984 placed imitation cheese production at 300 million pounds annually--100 million pounds consumer sales, 100 million pounds ingredients in prepared foods such as pizza, and 100 million pounds in fast food outlets. The 300 million pound estimate for 1984, also correlates closely with the increase in casein imports between 1981 and 1984. (Casein imports increased 50.45% between 1981 and 1984. The 300 million pound estimate of 1984 imitation cheese production is 46.34% above the ITC verified production level for imitation cheese in 1981.)

Imitation cheese production therefore currently comprises approximately

4.4% to 6.4% of natural cheese production, and 44% to 64% of CCC purchases of

cheese. Thus, approximately one-half of price support purchases of cheese were

attributable to imitation cheese. Without the large volumes of imitation cheese

currently being produced, the so called dairy price support "problem" would have

been minimized considerably. Near future industry estimates indicate even

- 6 -

larger imitation cheese production,---ranging from 8% to 15% of natural cheese

production. SAMI a private research group concludes 1984 imitation cheese sales

increased 6% over 1983 sales.

Imitation cheese therefore poses a considerable competitive threat to

natural cheese--and its competitive challenge is increasing. Industry estimates

suggest approximately 90% of imitation cheese is used by food processors,

restaurants and institutional feeding operations. Fast food operations appear

to be the fastest growing outlet for imitation cheese, with increasing use of

imitation cheese in pizza, fondue and blended dips, and cheeseburgers.

Imitation Cheese Competitive Position

Retail prices for imitation and natural cheese, and products they are used

in were collected by the author in twelve states (and Washington, D.C.) where

considerable quantities of imitation cheese is sold. This data was collected in

a personal survey of a random sample of 26 supermarkets in late 1981 and early

1982. States surveyed were: Iowa, Minnesota, Ohio, Illinois, Arizona,

California, Kentucky, Tennessee, New York-New Jersey, Wisconsin, Florida (and

Washington, D.C.).

Imitation cheese, and pizza with imitation cheese, is generally priced

lower at retail, than natural cheese--60% of the time for processed cheese, 80%

of the time for unshredded cheese, 74% of the time for pizza, and 99% of the

time for shredded cheese. However, a substantial variation existed between

states in the proportion of the time that im1tation theese retail prices are

lower than natural cheese prices--56% to 100% of the time for ghredded cheese,

43% to 100% of the time for processed cheese, and 54% to 89% of the time for

pizza.

Retail price variations between states are generally less for natural

cheese than for imitation cheese. As a result, wider variations exist in profit

- 7 -

margins for imitation cheese t than for natural cheese. This can encourage

retail expansion of imitation cheese. thereby creating increased competition for

natural cheese.

When imitation and natural cheese with the same brand name were compared,

imitation underpriced natural by the following amounts:

Type Unshredded Shredded Processed Cheese pizza

Amount less/lb. $0.)2 $1.02 $0.55 $0.47

Percent less/lb. 16 32 22 14

Average retail price discounts for imitation cheese compared to natural

cheese regardless of brand were:

Type Unshredded Shredded Processed Cheese pizza

Amount less/lb. $0.34 $1.15 $0.)4 $0.29

Percent less/lb. 12 35 21 11

Retail prices for unshredded imitation cheddar, colby, and mozarella cheese

were below their natural cheese counterparts by the following average amounts

per pound.

Iowa $.91 California $.19

Florida $.69 New York-New Jersey $.14

Tennessee $.47 Illinois $.08

Ohio $.28 Washington, D.C. $.03

Kentucky $.23

An earlier national study by the author in 1980 revealed that average

wholesale prices for imitation cheeses were below average wholesale prices for

natural cheese by the following amounts per pound.

Mozarella; $.78 Cheddar; $.25 C-olby; $.16

- 8 -

Agai n , there was a substantial difference between states. Overall,

however, imitat ion cheese underprices its natural counterpart by a wide margin.

Consumers can buy imitation cheese only if it's on the supermarket shelf.

The aut hor f ound that an average of 16 percent of shredded cheese retail shelf

spa ce was used for imitation cheese. But relatively little shelf space was used

f or packaged imita t ion cheese--1 .6 percent for unshredded and 1.7 percent for

process ed.

The story is completely different for pizza. More than one-half (57

percent ) o f piz za r e t a il shelf space was used for pizza with imitation cheese.

The use of imitation cheese in pizza is substantial .•• and growing.

In the 26 supermarkets surveyed, natural cheese brands outnumbered

imitation cheese brands by an average of 26 to 1 for unshredded cheese, 12 to 1

for processed cheese and 7 t o 1 for shredded cheese. But the situation was

reversed for pizza where brands with imitation cheese outnumbered those with

only natural cheese 18 to 14.

Imi t ation cheese in the 26 supermarkets was manufactured by 17 different

firms. and the imitation cheese pizzas were made by 20 different firms. This

further emphasizes the competitive problem natural cheese faces.

Strategies For Dealing With Imitations

Restrict Casein Imports

Imported casein (milk protein) is a major ingredient of imitation cheese.

Although the U.S. dairy industry has petitioned for import quotas on casein.

none have been imposed. Therefor e , casein can be imported in unlimited

quantities for manufacture into imitation cheese. which in turn competes with

cheese manufactured from domestic milk supplies.

· ,

- 9 -

u.s. import prices for casein used in imitation cheese of approximately

$.945 per pound (April 1985) are only three-eights of the $2.54 per pound price

for domestic nonfat dry milk solids of comparable protein content, used in

natural cheese. (One pound of casein has about three times as much protein as

one pound of nonfat dry milk solids. Therefore, to get a similar protein

quantity, three pounds of nonfat is needed, which at the current support price

of 84 3/4~ per pound equals $2.54.) The 192 million pounds of casein imports in

1984 are equivalent in protein to 577 million pounds of nonfat dry milk--85% of

nonfat dry milk price support purchases by CCC in 1984.

EEC export subsides on casein have been averaging approximately $.95 per

pound. These export subsidies have in turn driven down the world and therefore

u.s. price for casein, contributing to the low price for imitation cheese.

u.s. casein data is as follows:

(a) Imports--192.3 million pounds (1984)--21% above 1983 imports and 27% above

1980 imports.

(b) Imports as percent of world production--42% (1984).

(c) Casein used (1981 ITC Survey).

36% 9% 4% 4% 5%

12% 70% 16% 14%

Imitation cheese Coffee whitener Bakery products Frozen desserts Medical products Other foods TOTAL Food Animal Feed Industrial uses TOTAL 100%

Conclusions which can be drawn from u.S. casein import data are:

(a) The U.S. imports a disproportionate share of world casein production (42%).

(b) A major portion of imported casein is used for imitation cheese (36%).

(c) Virtually all imported casein is used for food and feed (86%) and therefore

is competitive with domestic nonfat dry milk.

- 10 -

(d ) U.S. casein imports are heavily subsidized by foreign exporters thereby

driving the U.S. landed price to only three-eights of the U.s. domestic

price for comparable qualities of milk protein.

Proponents of casein import quotas contend unlimited subsidized casein

imports result in increased production of imitation cheese, thereby increasing

USDA dairy price support purchases. Opponents contend consumer prices for

cheese and dairy products would increase if import quotas were imposed, and

therefore argue for free trade • . Thus far opponents of .casein import quotas have

prevailed through three ITC Hearings, one Congressional Hearing, three ITC and

USDA study reports, and three different Presidential rejections of casein import

quotas (Ford, Carter and Reagan).

Two separate bills have been introduced in the current Congressional

session to limit casein imports to 50% of the average levels ot the past 5

years. For 1985 this would restrict imports to 81 million pounds,---42% of 1984

imports. The 81 million pound limit on casein imports would still be

approximately 50 million pounds more than the quantity of casein used for

industrial products, and 22 million pounds more than the total used for

industrial products plus animal feed. Thus it would primarily limit use of

imported casein in imitation cheese and other food products, where casein is

competitive with dairy products.

The House subcommittee on dairy, livestock, and poultry held a hearing on

these bills on June 5. Realistically however, it is extremely doubtful that

legislation imposing import quotas on casein thereby restricting imports will be

enacted. Based on the three previous Presidential actions it is also doubtful

President Reagan will impose import quotas on casein. However, the

Administration and Congress have both taken a strong stand against EEC export

subsidies on dairy products including casein. If this challenge results in

- 11 -

elimination or even reduction in EEC export subsidies on casein, the price

advantage of imported casein and therefore imitation cheese would be reduced.

Also a further reduction in the U.S. dairy price support level is likely, which

would also reduce the price advantage of imitation cheese compared to natural

cheese.

However, if casein imports are restricted either through import quotas, or

pricing revision, nondairy ingredients such as soy isolates show promise as

substitutes for casein and nonfat dry milk in imitation cheese. Therefore

imitation cheese is likely to continue to be an important factor in the dairy

industry, and the industry must therefore plan its future accordingly.

Labeling and Content Revision

Proponents justify labeling and content revision on the basis (a) consumers

should know what they are buying and (b) food products using imitation dairy

products should also contain some natural dairy products.

With respect to imitation cheese, USDA has formally proposed that frozen

pizzas containing meat and imitation cheese, prominently label the inclusion of

imitation cheese in a type of least one-half the size of the largest type on the

package. USDA also proposed frozen meat pizzas contain at least 12% cheese, of

which at least 6% would have to be natural cheese.

However, USDA received more than ~,OOO comments on the proposal, and it is

uncertain when, or if it will be promulgated. More prominent labeling of

imitation component~like1y stands a better chance of surviving legal

challenges, than does mandatory minimum natural dairy product content

requirements, unless the minimums can be justified on a nutrition and health

basis.

Butterb1end Products

As previously indicated per capita consumption of butter declined 5.7

pounds since 1950, compared to an increase of 4.9 pounds for margarine.

- 12 -

Butterblend products which are part margarine and part butter offer an

opportunity for reversing this trend. Based on research by the author,

but terblend has resulted in an overall increase in butterfat sales. This is

because the product is more competitive with margarine, than with all but the

lower grades of butter.

The chief selling point to the consumer seems to be price. Retail prices

in the Midwest have been averaging approximately $1.45 per pound of butterblend,

compared with $1 for corn-oil margarine, and $1.90 for butter. At these prices,

the butter used in butterblend becomes more competitive with margarine than when

it is sold as butter.

Butterblend offers the dairy industry a chance to recapture some butterfat

sales, whether price or cholesterol lost them to begin with. For example, one

major dairy projects annual sales of 50 million pounds of butterblend, of which

20 million pounds will be butter.

Since there appears to be little likelihood of ever recapturing anything

close to butter sales of the 1940s or even the 1950s, the industry should give

serious consideration to a vigorous campaign to sell butterblend.

Research indicates approximately one-twelfth of consumers now use butter/

margarine blends away from home, and one-fifth of consumers use butter/margarine

blends at home. Heaviest use is at dinner, with breakfast and lunch use almost

identical,--and only slightly less than at dinner.

Butterblends therefore offer a distinct possibility for dealing with the

imitation problem.

Increased Promotion

The current national program of promotion, research and nutrition education

is financed by a mandatory assessment of 15 cents per hundredweight on all milk

marketed commercially in the 48 contiguous States until October 1, 1985.

- 13 -

Current estimates project a total annual income of about $197 million from this

15-cent assessment. The National Dairy Promotoion and Research Board (NDPRB)

is projected to receive approximately $87 million of this, while state and

regional programs will retain the remaining funds--approximately $110 million

for dairy promotional activities ($197 million - $87 million = $110 million).

Generic promotion programs in place when the legislation was passed spent

approximately $96 million annually. The impact of this legislation is to add

approximately $101 million annually to dairy promotion efforts ($197 million -

$96 million = $101 million).

Combatting imitations should have high priority in allocating these

promotional expenditures. Promotional considerations to combat dairy imitations

include:

1. Increased cheese promotion could be stressed in light of its relatively low

promotion expenditures compared to fluid milk, more favorably demand for

cheese than for most other dairy products, and tremendous growth and

competition of imitation cheese. Increased cheese promotion funding would

also permit targeting cheese ads to "local" cheese preferences, and also

permit greater emphasis on advertising specialty cheeses. Now most

emphasis is on hard cheese.

Research indicates that a given investment in cheese promotion

consistenly will generate a sales response about three times larger than a

similar investment in fluid milk promotion.ll

2. Future butter promotion funding allocations should be correlated with

1/

margarine's response to the increased butter promotion resulting from the

"Increasing Returns to Dairy Farmers by Generic Promotion of Milk and Dairy Products; The Issue of Which Products to Promote," Department of Agricultural Economics, The Ohio State University, ESO 1162, April, 1985.

- 14 -

national checkoff. If margarine promotion is stepped up substantially,

further increases in butter promotion should be given serious

consideration.

3. Consideration should be given to major promotion programs for ice cream and

fluid cream. This recommendation is made because ot substantial increases

in per capita consumption of both products, and the vigorous competition

from imitations. Increases usage of heavy cream, sour cream, whipping

cream, and salad dressing has resulted from the increasing popularity of

gourmet dining, away from horne dining, and use of creams in cooking.

Popularity, of high fat "premium" ice cream in turn has resulted in

increased usage of both ice cream and butterfat. Capitalizing on these

trends can help in dealing with competitive imitation products.

4. The dairy industry will likely find it to its advantage to have national

budget promotion funding decisions coordinated with local and regional

groups decisions, rather than each group going its own separate way. This

approach would give the dairy industry greater leverage in attempting to

maintain a fair allocation of advertising funds for cheese and other

manufactured dairy products particularly susceptible to competition from

imitation products. Also, this procedure could permit the national budget

to "fill in the gaps," from local funding, thereby more effectively

combatting imitations, rather than attempting to have widely diverse local

groups get together to fill in promotion gaps of national funding.

One total promotion strategy will be needed for the long term, if promotion

effectiveness in dealing with imitations is to be maximized. Divorcing NDPRB

promotion funding from local and regional funding sacrifices coordinated

promotional activities of approximately $85 million annually by NDPRB, and $112

million annually by State and Regional organizations; This would be very

counterproductive in competing with imitations.

· ~

- 15 -

Continued coordination of dairy promotional activities of NDPRB, and State

and Regional organizations, is essential to derive maximum return on the $197

million annually currently being deducted from farmers milk checks, for dairy

promotion in combatting imitation dairy products.

Summary

People are eating more fat than ever--an increase of 14.5 pounds (32%) per

person since 1960. However, per capita consumption of annual fat dropped 6.2

pounds (34%) while vegetable fat consumption increased 20.7 pounds (77%). This

shift in consumption from milk fat to vegetable fat contributed to milk fat

surpluses, downward price pressures, and is a continuing problem for the dairy

industry.

The most important imitation problem for the dairy industry is imitation

cheese. The 205 plus million pounds of imitation cheese production is 44% of

1984 USDA price support purchases of cheese. Import prices for casein used in

imitation cheese are only three-eights the price of domestic nonfat milk solids

of comparable protein content, used in natural cheese.

The $.52 to $1.02 (16%-32%) lower average retail price per pound for

imitation cheese than natural cheese of the same brand, and $.47 per pound (14%)

lower price for pizza with imitation cheese than pizza with natural cheese of

the same brand, indicates vigorous across-the-board competition by imitation

cheese. Pizza with imitation cheese has already claimed over one-half (57%) of

the shelf space in the supermarkets in the twelve major states (and Washington,

D.C.) surveyed. It also has 16% of the shredded cheese shelf space, and about

2% of the unshredded and process cheese shelf space.

Pizza brands with imitation cheese outnumbered pizza brands, with only

natural cheese 18 to 14. Natural brands of unshredded, process, and shredded

cheese outnumbered imitation brands.

- 16 -

Imitation cheese in the 26 supermarkets surveyed was manufactured by 17

different firms, and pizza with imitation cheese was manufactured by twenty

different firms. Thus, a wide variety of companies are manufacturing imitation

cheese. and pizza with imitation cheese.

Imitation cheese therefore impacts substantially on the dairy industry.

Imitation cheese is likely to continue to be an important factor in the dairy

industry. and the industry must plan its future accordingly.

Alternative strategies for dealing with imitation dairy products include:

(a) Reducing casein imports. However if casein imports are restricted,

nondairy ingredients such as soy isolates show promise as substitutes for

casein and nonfat dry milk in imitation cheese. Therefore, working to

reduce or terminate EEC export subsidies which are driving import prices

down to three-eights of domestic nonfat dry milk prices will likely be more

helpful in reducing or eliminating the competitive price advantage

imitation cheese has over natural cheese.

(b) Clearer and more prominent labeling of imitation dairy products, so

consumers know what they are buying.

(c) Greater emphasis on butterblend products which compete better price wise

with imitation products, than do natural dairy products.

(d) Increased allocation of promotion funds from the $197 million annually now

available from farmer checkoffs, .to products such as cheese. cream, and ice

cream, which are particularly vulnerable to imitations. Increased

promotion of cheese in particular is very important because of the intense

competition from imitation cheese, coupled with the fact that the sales

response from cheese promotion is about three times larger than the sales

response from a similar investment in fluid milk promotion.