Embed Size (px)

Citation preview

Jump to first page

1

4. Cost Estimates The aggregate cost of work units

described in the work breakdown structure.

The work unit approach makes cost estimating more manageable.

There are situations where an overall cost of a project is required for the initial decision and before WBS is done.

Jump to first page

2

4. Costs Tangible – easier to estimate.

E.g., routers, switches, connectors, cables, servers, and human resources.

Intangible – difficult to evaluate. E.g., cost benefit analysis of outsourcing

or offshoring information system function in terms of security, privacy, know how, innovation, etc.

Jump to first page

3

4. Costs Direct – associated with a work unit

E.g., hours worked on a unit or the portion of management time (direct overhead costs) used for a work unit.

Indirect – difficult to assignE.g., promotional expenses for the entire

organization; difficult to prorate portion of this cost to a work unit or a project.

Jump to first page

4

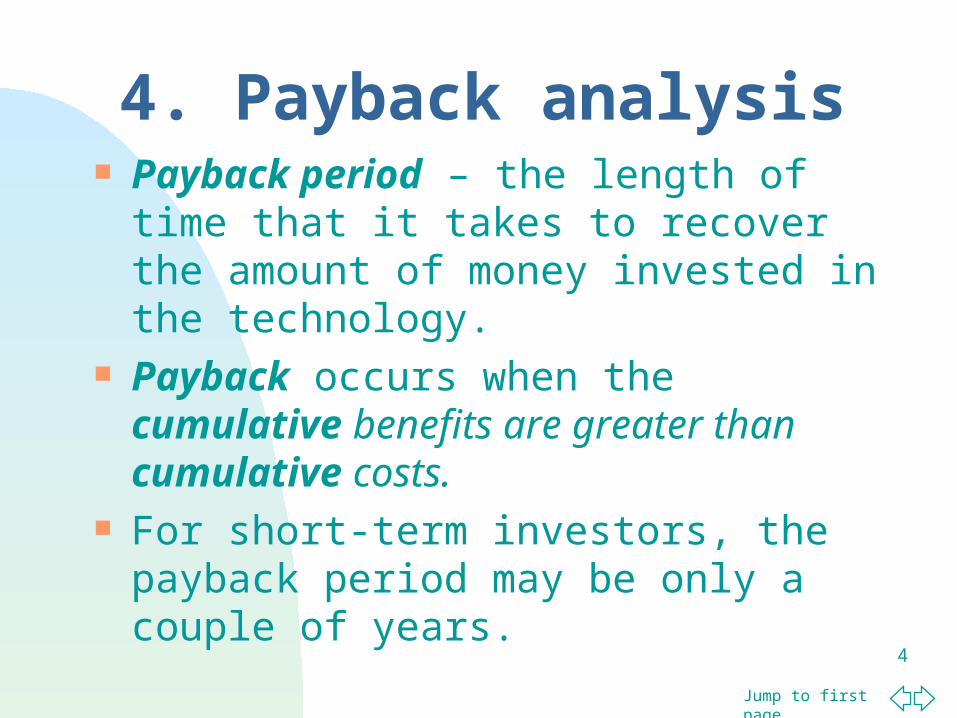

4. Payback analysis Payback period – the length of time

that it takes to recover the amount of money invested in the technology.

Payback occurs when the cumulative benefits are greater than cumulative costs.

For short-term investors, the payback period may be only a couple of years.

Jump to first page

5

4. Payback analysis for two projects Project A Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Total

Cost 20,000 20,000 10,000 10,000 5,000 5,000 70,000

Revenue 0 0 30,000 40,000 30,000 20,000 120,000

Difference (20,000) (20,000) 20,000 30,000 25,000 15,000 50,000

Cumulative (20,000) (40,000) (20,000) 10,000 35,000 50,000

Project B Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Total

Cost 25,000 25,000 15,000 10,000 5,000 5,000 85,000

Revenue 10,000 15,000 45,000 30,000 20,000 10,000 120,000

Difference (15,000) (10,000) 30,000 20,000 15,000 5,000 45,000

Cumulative (15,000) (25,000) 5,000 25,000 40,000 45,000

Jump to first page

6

4. Net Present Value The formula for calculating NPV is:

NPV = ∑t=1 …n A/(1+r)t

where t represents the year in which cash flow occurs, A represents the amount of cash flow for that year, and r represents the discount rate.

Using a specified rate of interest, this formula sums up the present value for the number of years that estimates have been made.

Jump to first page

7

4. NPV example The present value of $3,000 cost projected

for the third year of a project with an interest rate of 15% is $1972.50; calculated as:

$3000 * 1/(1+0.15)3 or $3000 * 0.6575 = $1972.50

If the projected revenue for the same project in the third year is $2,000 then the present value will be $1512.20; calculated as:

$2000 * 1/(1+0.15)3 or $2000 * 0.6575 = $1512.30

Jump to first page

8

4. Discount factors at 15%

Year Formula Discount factor

1 1/(1+0.15)1 0.8696

2 1/(1+0.15)2 0.7561

3 1/(1+0.15)3 0.6575

4 1/(1+0.15)4 0.5718

5 1/(1+0.15)5 0.4972

6 1/(1+0.15)6 0.4323

Jump to first page

9

4. Payback analysis for Project A

Project A Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Total

Cost 20,000 20,000 10,000 10,000 5,000 5,000 70,000

Revenue 0 0 30,000 40,000 30,000 20,000 120,000

Difference (20,000) (20,000) 20,000 30,000 25,000 15,000 50,000

Cumulative (20,000) (40,000) (20,000) 10,000 35,000 50,000

Jump to first page

10

4. NPV for Project A Year 1 = .8696 * ($20,000) = ($17,392) Year 2 = .7561 * ($20,000) = ($15,122) Year 3 = .6575 * $20,000 = $13,150 Year 4 = .5718 * $30,000 = $17,154 Year 5 = .4972 * $25,000 = $12,430 Year 6 = .4323 * $15,000 = $6,485

NPV (Project A) = ∑t=1 …n A/(1+r)t

= $16,705

Jump to first page

11

4. ROI analysis for Project AYear Factor Revenue Disc. Rev. Cost Disc. Cost

1 0.8696 $0 $0 ($20,000) ($17,392)

2 0.7561 $0 $0 ($20,000) ($15,122)

3 0.6575 $30,000 $19,725 ($10,000) ($6,575)

4 0.5718 $40,000 $22,872 ($10,000) ($5,718)

5 0.4972 $30,000 $14,916 ($5,000) ($2,486)

6 0.4323 $20,000 $8,646 ($5,000) ($2,162)

Total $120,000 $66,159 ($70,000) ($49,455)

Jump to first page

12

4. ROI analysis for Project BYear Factor Revenue Disc. Rev. Cost Disc. Cost

1 0.8696 $10,000 $8,696 ($25,000) ($21,740)

2 0.7561 $15,000 $11,342 ($25,000) ($18,903)

3 0.6575 $45,000 $29,588 ($15,000) ($9,863)

4 0.5718 $30,000 $17,154 ($10,000) ($5,718)

5 0.4972 $20,000 $9,944 ($5,000) ($2,486)

6 0.4323 $10,000 $4,323 ($5,000) ($2,162)

Total $120,000 $81,047 ($85,000) ($60,872)

Jump to first page

13

4. ROI – Projects A & B ROI for Project A:

($66,159 – $49,455)/49,455 * 100 = 33.8%

ROI for Project B:

($81,047 – $60,872)/60,872 * 100 = 33.1%

Jump to first page

14

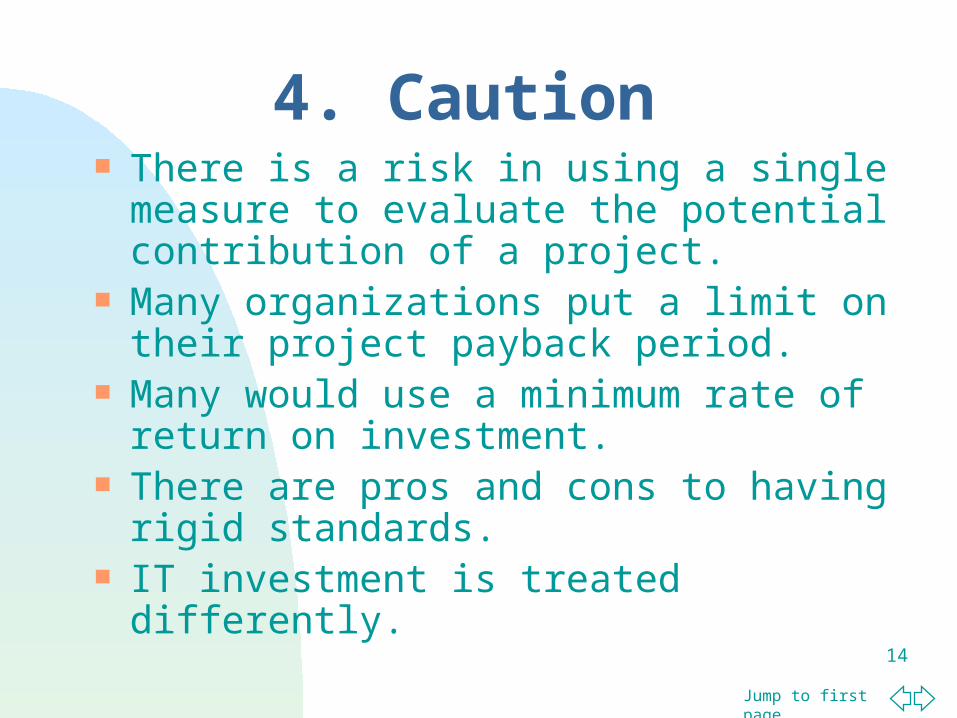

4. Caution There is a risk in using a single

measure to evaluate the potential contribution of a project.

Many organizations put a limit on their project payback period.

Many would use a minimum rate of return on investment.

There are pros and cons to having rigid standards.

IT investment is treated differently.

Jump to first page

15

4. Sources of estimates Experience – individuals within the

organization. this method considers workplace

culture, talent pool, interorganizational relations, and HR policies.

Overestimation? Underestimation? ‘Safe’ estimates?

Jump to first page

16

4. Sources of estimates Documentation – archival information from

previous projects. Relatively current? Similar projects? Free from bias? Politics? Based on actual recorded numbers. Adjustment may be necessary if changes

have occurred since the document was prepared – new laws, new equipment, change in working hours, and holidays.

Jump to first page

17

4. Sources of estimates Expert opinion – widely used and

includes a broad pool of internal and external experts. Similar to experience in pros and cons Used for new and innovative systems

where little record exists. More formalized and expensive. May require visits by external experts

and sharing of information.

Jump to first page

18

4. Considerations A combination of internal and external

estimates, while costly, has advantages. Team members should be involved with

providing estimates but the project manager must be aware of biases.

Provide supporting material on methods of estimation.

Establish guidelines for cost and time estimation.

Jump to first page

19

4. Considerations Based on history and experience, project

managers may adjust estimates given by individuals.

This, in turn, will result in further adjustment (overestimation or underestimation) by those providing estimates.

This cycle creates ‘game play’ and a non-productive environment.

It may be necessary to work out some kind of reward for reliable and accurate estimates.

Jump to first page

20

4. Hints Use work units and bottom-up approach. Define clearly work units and tasks. Avoid memory recollection. Involve team members to improve

commitments and match tasks and skills. Obtain multiple estimates:

The best case scenario. The most probable scenario. The worst case scenario.

Assign weights to these estimates.

Jump to first page

21

4. Multiple estimates Use average scores and variance. Provide contingency resources for

estimates with large variance. Calculate ‘upper limit’ and ‘lower limit’

measures for project duration. Example: A project is estimated to take

165 hours to complete with a standard deviation of 29 hours. Assuming + and – 3 standard deviations, we will have:

Jump to first page

22

4. Multiple estimates The project upper limit:

(3 * 29 + 165) = 252 hours The project lower limit:

(-3 * 29 + 165) = 78 hours Upper limit as % of estimate:

(252/165)100 = 152.73% Lower limit as % of estimate:

(78/165)100 = 47.27%

There is a high probability that the project will be complete within 78 to 252 hours. The project completion time may be over extended or under extended by about 53%.

Jump to first page

23

Jump to first page

24

4. Phase estimating Sometimes, due to uncertainty, estimates are

feasible for initial phase only. Only rough estimates of subsequent phases

are initially feasible. Project development life cycle (initiation,

planning, development, implementation, closure) can be the base for phase estimating.

Project owners and sponsors must commit to a project with incomplete information about cost and time – not always an easy situation.

Jump to first page

25

4. Considerations Estimates are used to request funding, make

decisions, schedule, negotiate, set goals, evaluate performance, etc.

Events happen, technology advances, priorities change, and biases creep in.

Credibility of the estimates and those preparing them must be considered.

Methods, their appropriateness, strengths, and weaknesses must be explained.

Assume ‘normal conditions’ – free from extreme case assumptions.

Jump to first page

26

4. Contingency plan For out-of-ordinary situations. Extreme or extraordinary situations. Funds must be appropriated at the planning

phase of the project development life cycle. Document and communicate contingency

situations. Such funds are not directly accessible by the

project manager. Simply adding a margin to estimates must be

avoided; suggests poor planning, interpreted as add-on slush money by watchful sponsors.

Jump to first page

27

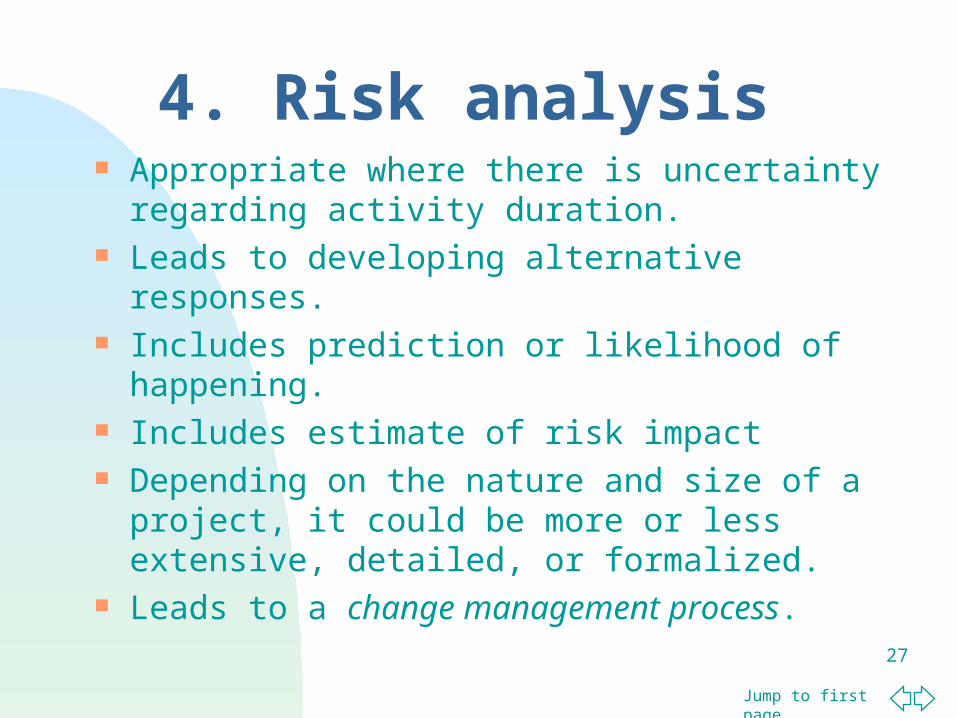

4. Risk analysis Appropriate where there is uncertainty

regarding activity duration. Leads to developing alternative responses. Includes prediction or likelihood of happening. Includes estimate of risk impact Depending on the nature and size of a

project, it could be more or less extensive, detailed, or formalized.

Leads to a change management process.

Jump to first page

28

4. Change management Change is beneficial - innovative ideas or

suggestions are often made by team members.

A change management committee can facilitate and encourage change proposals.

With the approval of management, additional resources can be provided through contingency funds.

Jump to first page

29

4. Change management Membership includes stakeholders from the

entire organization. Change management committee must: identify possible risks predict the likelihood of risks happening estimate risks impact communicate risks to stakeholders prepare alternative response.

Jump to first page

30

4. Change management Changes must be consistent with the overall

goals and objectives of the organization and the broad scope of the project.

Responses to change requests must be timely, especially for time-sensitive changes.

Proposals to drastically change a project may replace the project with a new one.

Jump to first page

31

Jump to first page

32

4. Discussion question Assume you are working for an organization

that is keen to invest in information technology to improve employee innovation, productivity, customer satisfaction, and management control. However, top management in your organization has a short-term payback expectation for their technology investment. Explain to the leadership of your organization why such a policy may be dysfunctional in the long term.

Jump to first page

33

4. Discussion question This chapter argues that organizational

game play and politics are a function of management decision-making style. Do you agree with this statement? Why?

Is it possible to totally eliminate organizational politics?

Jump to first page

34

4. Discussion question Assume you are an IT project manager.

How would you deal with issues of politics and game play that affect time and cost estimates for your projects?

Jump to first page

35

4. Discussion question Would your reaction be the same

overestimation and underestimation of cost and time?

When do you think ‘overestimation’ happens? ‘Underestimation’?

Jump to first page

36

Work Package Estimates

Jump to first page

37

4. In-class assignment Do exercise 4.10-c in Chapter 4 (payback

analysis, NPV, and ROI for two projects).