Embed Size (px)

Citation preview

Disclaimer & Disclosures

This report must be read with the disclosures in the Disclosure appendix, and

with the Disclaimer, which forms part of it.

Disclosures for companies can be accessed via the hyperlinks to the original

published research, which can be found in the title

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

View HSBC Global Research at:

https://www.research.hsbc.com

THIS CONTENT MAY NOT BE DISTRIBUTED TO THE PEOPLE'S REPUBLIC OF CHINA (THE "PRC") (EXCLUDING SPECIAL ADMINISTRATIVE REGIONS OF HONG KONG AND MACAO)

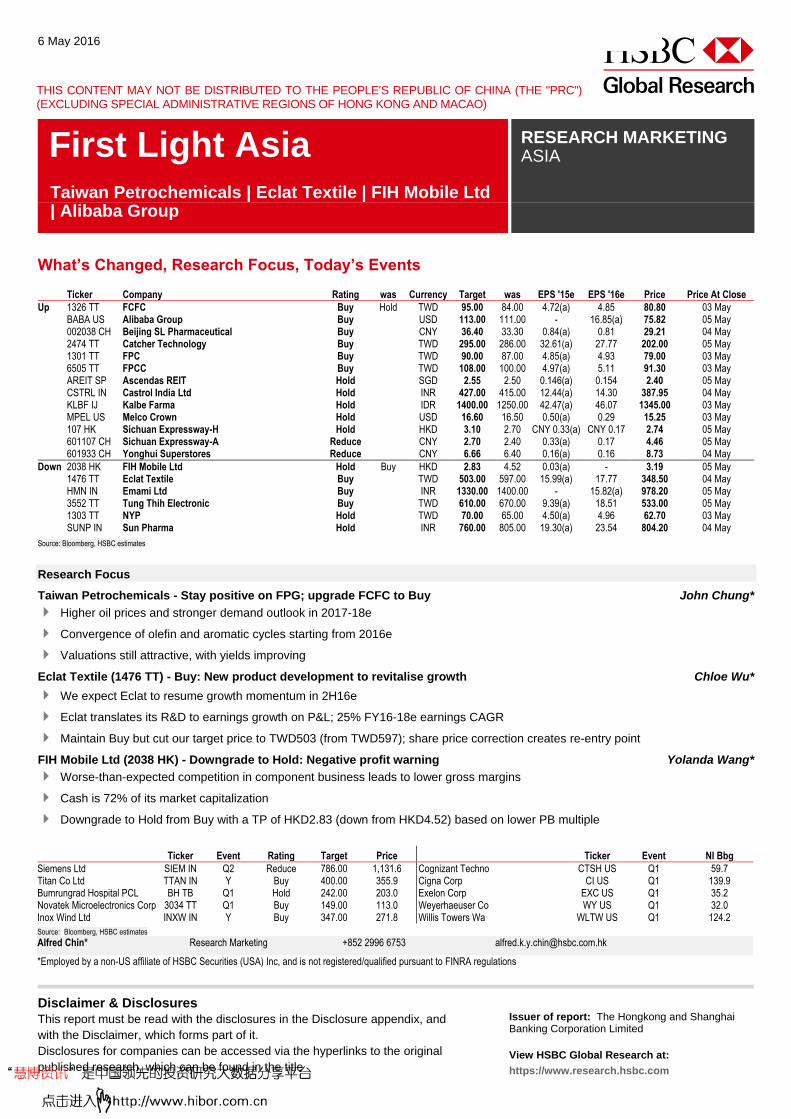

What’s Changed, Research Focus, Today’s Events

Ticker Company Rating was Currency Target was EPS '15e EPS '16e Price Price At Close

Up 1326 TT FCFC Buy Hold TWD 95.00 84.00 4.72(a) 4.85 80.80 03 May BABA US Alibaba Group Buy USD 113.00 111.00 - 16.85(a) 75.82 05 May 002038 CH Beijing SL Pharmaceutical Buy CNY 36.40 33.30 0.84(a) 0.81 29.21 04 May 2474 TT Catcher Technology Buy TWD 295.00 286.00 32.61(a) 27.77 202.00 05 May 1301 TT FPC Buy TWD 90.00 87.00 4.85(a) 4.93 79.00 03 May 6505 TT FPCC Buy TWD 108.00 100.00 4.97(a) 5.11 91.30 03 May AREIT SP Ascendas REIT Hold SGD 2.55 2.50 0.146(a) 0.154 2.40 05 May CSTRL IN Castrol India Ltd Hold INR 427.00 415.00 12.44(a) 14.30 387.95 04 May KLBF IJ Kalbe Farma Hold IDR 1400.00 1250.00 42.47(a) 46.07 1345.00 03 May MPEL US Melco Crown Hold USD 16.60 16.50 0.50(a) 0.29 15.25 03 May 107 HK Sichuan Expressway-H Hold HKD 3.10 2.70 CNY 0.33(a) CNY 0.17 2.74 05 May 601107 CH Sichuan Expressway-A Reduce CNY 2.70 2.40 0.33(a) 0.17 4.46 05 May 601933 CH Yonghui Superstores Reduce CNY 6.66 6.40 0.16(a) 0.16 8.73 04 May

Down 2038 HK FIH Mobile Ltd Hold Buy HKD 2.83 4.52 0.03(a) - 3.19 05 May 1476 TT Eclat Textile Buy TWD 503.00 597.00 15.99(a) 17.77 348.50 04 May HMN IN Emami Ltd Buy INR 1330.00 1400.00 - 15.82(a) 978.20 05 May 3552 TT Tung Thih Electronic Buy TWD 610.00 670.00 9.39(a) 18.51 533.00 05 May 1303 TT NYP Hold TWD 70.00 65.00 4.50(a) 4.96 62.70 03 May SUNP IN Sun Pharma Hold INR 760.00 805.00 19.30(a) 23.54 804.20 04 May Source: Bloomberg, HSBC estimates

Research Focus

Taiwan Petrochemicals - Stay positive on FPG; upgrade FCFC to Buy John Chung*

Higher oil prices and stronger demand outlook in 2017-18e

Convergence of olefin and aromatic cycles starting from 2016e

Valuations still attractive, with yields improving

Eclat Textile (1476 TT) - Buy: New product development to revitalise growth Chloe Wu*

We expect Eclat to resume growth momentum in 2H16e

Eclat translates its R&D to earnings growth on P&L; 25% FY16-18e earnings CAGR

Maintain Buy but cut our target price to TWD503 (from TWD597); share price correction creates re-entry point

FIH Mobile Ltd (2038 HK) - Downgrade to Hold: Negative profit warning Yolanda Wang*

Worse-than-expected competition in component business leads to lower gross margins

Cash is 72% of its market capitalization

Downgrade to Hold from Buy with a TP of HKD2.83 (down from HKD4.52) based on lower PB multiple

6 May 2016

First Light Asia RESEARCH MARKETING ASIA

Ticker Event Rating Target Price Ticker Event NI Bbg

Siemens Ltd SIEM IN Q2 Reduce 786.00 1,131.6 Cognizant Techno CTSH US Q1 59.7 Titan Co Ltd TTAN IN Y Buy 400.00 355.9 Cigna Corp CI US Q1 139.9 Bumrungrad Hospital PCL BH TB Q1 Hold 242.00 203.0 Exelon Corp EXC US Q1 35.2 Novatek Microelectronics Corp 3034 TT Q1 Buy 149.00 113.0 Weyerhaeuser Co WY US Q1 32.0 Inox Wind Ltd INXW IN Y Buy 347.00 271.8 Willis Towers Wa WLTW US Q1 124.2

Source: Bloomberg, HSBC estimates

Alfred Chin* Research Marketing +852 2996 6753 [email protected]

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/qualified pursuant to FINRA regulations

Taiwan Petrochemicals | Eclat Textile | FIH Mobile Ltd | Alibaba Group

RESEARCH MARKETING ASIA

6 May 2016

Research Focus (Contd.,)

Alibaba Group (BABA US) - Buy: Leveraging data to raise the value of its platform Chi Tsang*

Core e-commerce business posts fastest growth in 6 quarters

Stable GMV growth but rising monetization

Maintain Buy and raise SOTP TP to USD113 from USD111; Alibaba is an HSBC Asia Super Ten portfolio constituent

In this document HSBC may comment on the potential economic impact dependent on the outcome of the UK Referendum. HSBC

is not taking a political position and this document and the information contained herein are not intended to promote or procure, or

otherwise be in connection with promoting or procuring, a particular outcome in relation to the question asked in the UK

Referendum.

RESEARCH MARKETING ASIA

6 May 2016

Regional

Asia Chart of the Week - Nope, false signal Frederic Neumann

So, we published a chart earlier this week that caused a bit of excitement among our readers. It shows a spike in the new order-to-

inventory ratio for emerging Asia (based on the latest crop of PMIs).

This, ordinarily, points to an acceleration in industrial output in the region.

Trouble is, as helpful as the indicator often proves, at times it can send false signals.

China & Hong Kong

Hong Kong Retail Sales (March 2016) - Pace of decline moderates Julia Wang

The contraction in retail sales eased in March after the Chinese New Year effect faded, but remains at a weak level.

Both the luxury goods sector and the consumer durable goods sector continued to pose double-digit contractions, as a result of a

11% YTD contraction in inbound tourists.

Food and supermarket sales however, held up relatively better.

Nikkei Hong Kong PMI (Apr 2016) - Contracting further John Zhu

The headline Nikkei Hong Kong PMI fell further to 45.3 in April, down from 45.5 in March, signalling a faster deterioration in private

sector activity.

New orders fell at a faster pace, underscoring the overall weakness in demand conditions.

Firms continue to cut jobs as output remains weak.

The Great Mall of China - Air conditioner makers yearning for a hot summer [Corrected] Erwan Rambourg*

April is normally the start of the peak season for air conditioner sales.

However, demand has yet to show strong signs of picking up, based on our recent visits to appliance retailers in south China.

Appliance makers and retailers are hoping for the weather to warm up to drive demand in the peak season.

Beijing SL Pharmaceutical (002038 CH) - Buy: Generic Lenalidomide getting closer to approval Zhijie Zhao*

CFDA announced it had started its on-site inspection of SL Pharm’s generic Lenalidomide

We expect Lenalidomide to contribute RMB4.9bn to SL Pharm at peak sales

Raise TP to RMB36.4 from RMB33.30 on higher PE multiple, reiterate Buy

MGM China (2282 HK) - Buy: 1Q16 in line; Cotai continues to target 1Q17 Scott Chan*

1Q16 was in-line but dampened by unfavorable luck

Cotai construction should be completed in October/November and continues to target 1Q17 opening

Maintain Buy rating and unchanged target price of HKD14.2

Melco Crown (MPEL US) - Hold: 1Q16 in line, repurchasing stake from Crown Scott Chan*

Bad debt provision at Altira offset favourable win rate impact

MPEL to repurchase 9.5% of its shares from Crown Resorts

Maintain Hold and raise TP to USD16.6 from USD16.5

Sichuan Expressway (107 HK/601107 CH) - H: Hold/A: Reduce – Forecast delay in profit ramp up Wei Sim*

Six months delay in the Suining roads’ contribution itself is not a concern, but profitability ramp up will take a few years

We forecast insignificant impact on earnings from the increase in non-toll revenue contribution

Raise H share TP to HKD3.1 (from HKD2.7) maintain Hold, raise A share TP to RMB2.8 (from RMB2.4) maintain Reduce

CNOOC Ltd. (883 HK) - Reduce: Wildfire impact a function of outage duration Thomas C. Hilboldt*

Along with other oil sands operators, Long Lake oil sands facility in Ft. McMurray, Alberta will shut to ensure staff safety

CNOOC Canadian output was c.60kb/d in 2015 or 4% of production; downtime may raise risk to production target

Maintain Reduce with TP of HKD5.55; shares have moved ahead of likely fundamental outcomes

Yonghui Superstores (601933 CH) - Reduce: Unlikely to live up to expectations Lina Yan*

Strong performance in 1Q might not be sustainable

We think market expectations on margins are too high

We increase our DCF-based TP to RMB6.66 (from RMB6.40)

RESEARCH MARKETING ASIA

6 May 2016

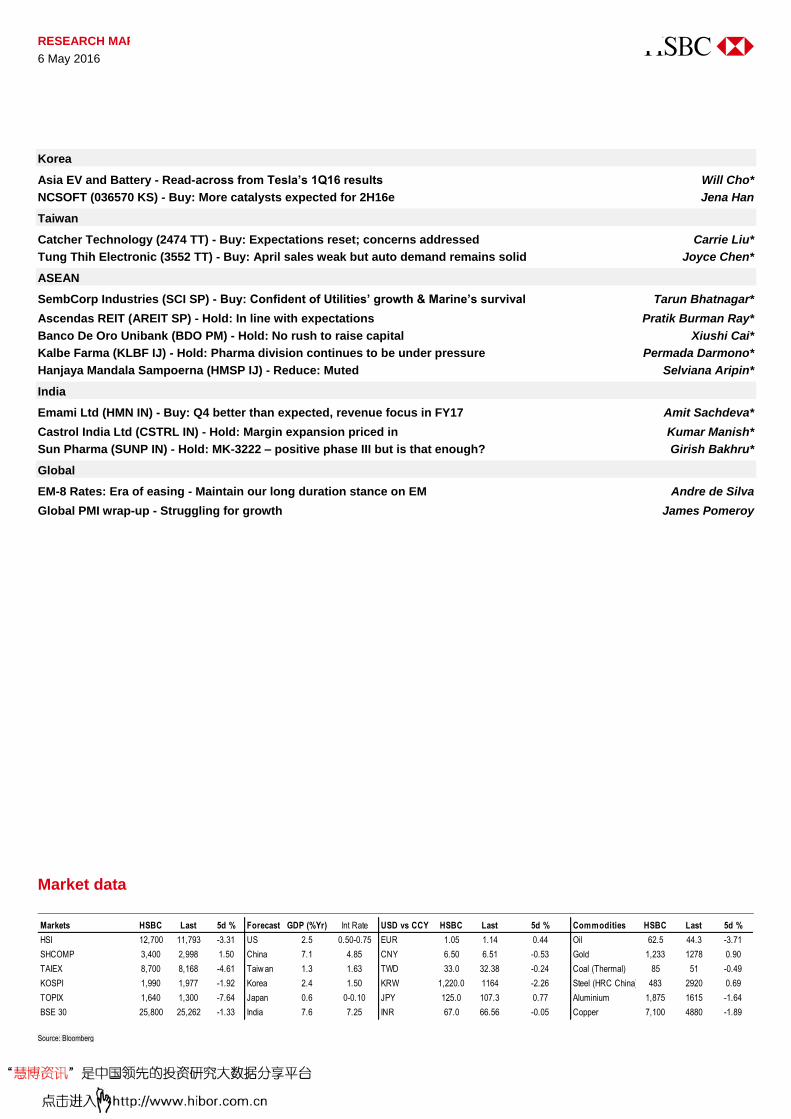

Korea

Asia EV and Battery - Read-across from Tesla’s 1Q16 results Will Cho*

NCSOFT (036570 KS) - Buy: More catalysts expected for 2H16e Jena Han

Taiwan

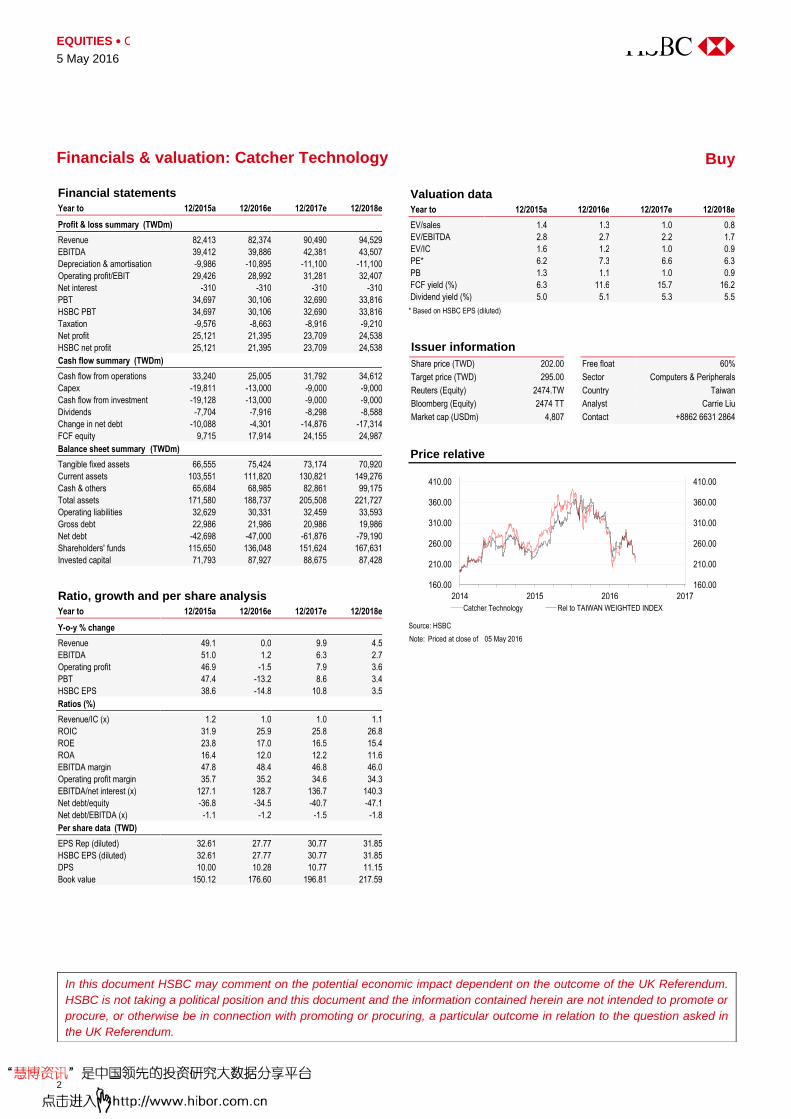

Catcher Technology (2474 TT) - Buy: Expectations reset; concerns addressed Carrie Liu*

Tung Thih Electronic (3552 TT) - Buy: April sales weak but auto demand remains solid Joyce Chen*

ASEAN

SembCorp Industries (SCI SP) - Buy: Confident of Utilities’ growth & Marine’s survival Tarun Bhatnagar*

Ascendas REIT (AREIT SP) - Hold: In line with expectations Pratik Burman Ray*

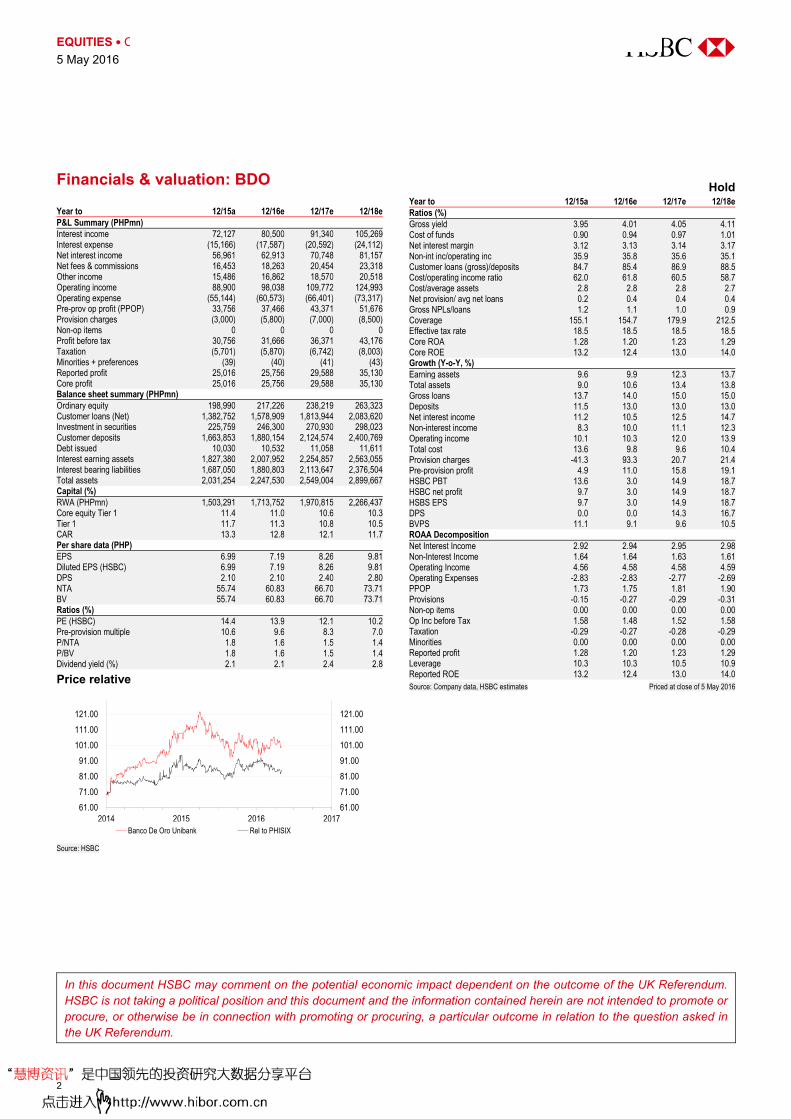

Banco De Oro Unibank (BDO PM) - Hold: No rush to raise capital Xiushi Cai*

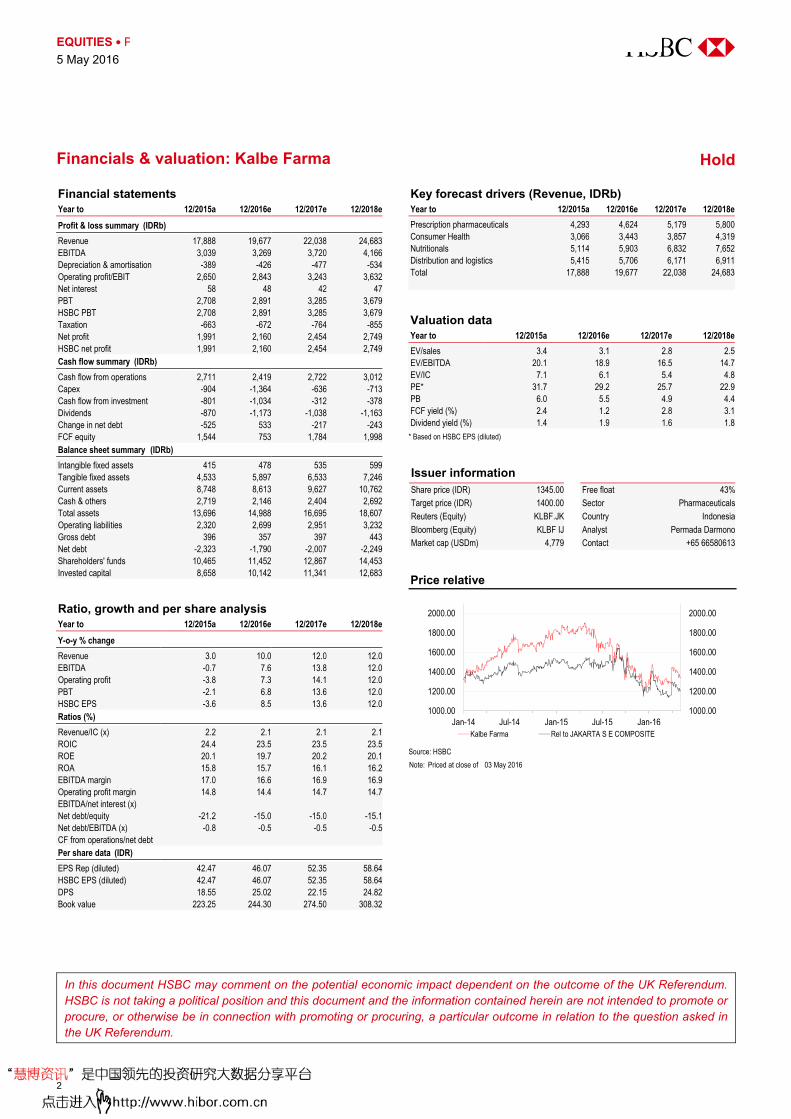

Kalbe Farma (KLBF IJ) - Hold: Pharma division continues to be under pressure Permada Darmono*

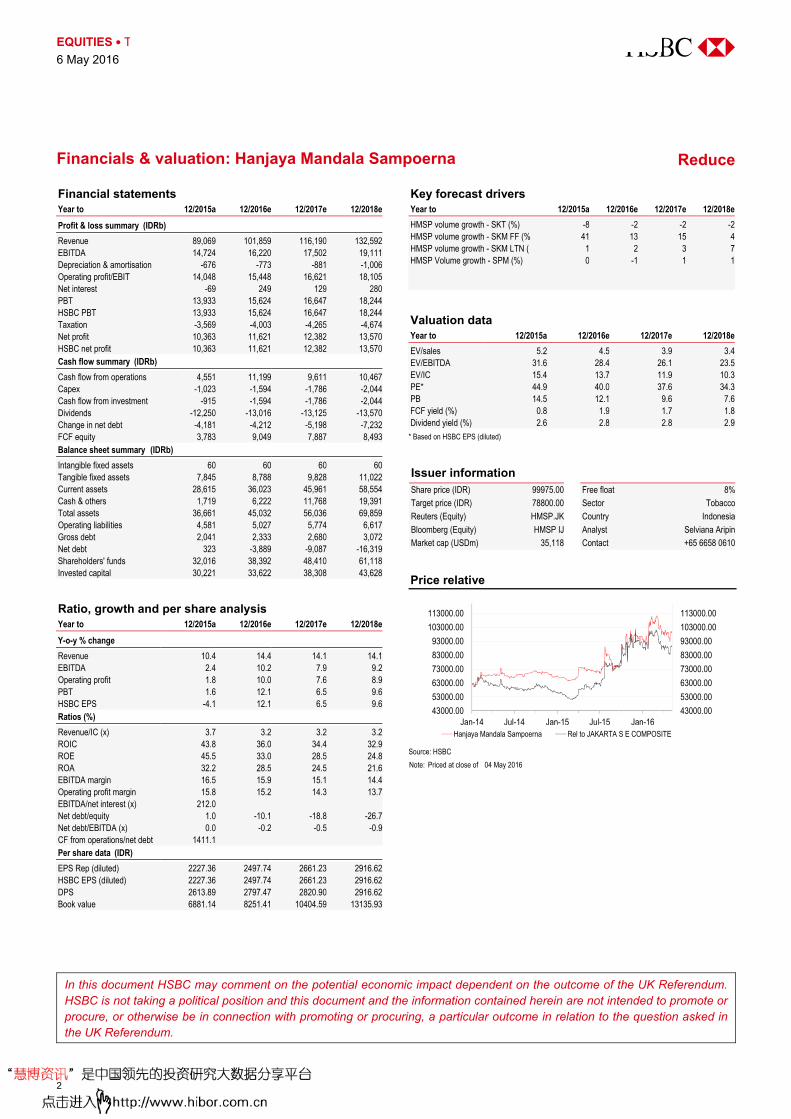

Hanjaya Mandala Sampoerna (HMSP IJ) - Reduce: Muted Selviana Aripin*

India

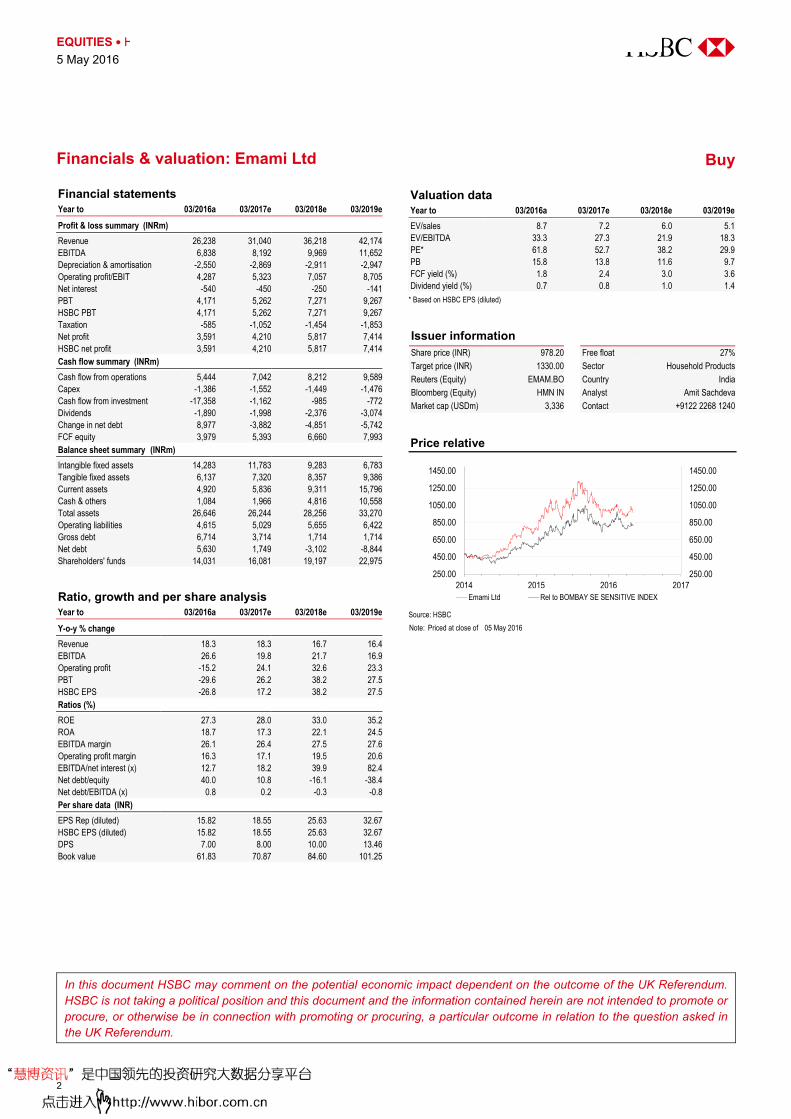

Emami Ltd (HMN IN) - Buy: Q4 better than expected, revenue focus in FY17 Amit Sachdeva*

Castrol India Ltd (CSTRL IN) - Hold: Margin expansion priced in Kumar Manish*

Sun Pharma (SUNP IN) - Hold: MK-3222 – positive phase III but is that enough? Girish Bakhru*

Global

EM-8 Rates: Era of easing - Maintain our long duration stance on EM Andre de Silva

Global PMI wrap-up - Struggling for growth James Pomeroy

Market data

Source: Bloomberg

Markets HSBC Last 5d % Forecast GDP (%Yr) Int Rate USD vs CCY HSBC Last 5d % Commodities HSBC Last 5d %

HSI 12,700 11,793 -3.31 US 2.5 0.50-0.75 EUR 1.05 1.14 0.44 Oil 62.5 44.3 -3.71

SHCOMP 3,400 2,998 1.50 China 7.1 4.85 CNY 6.50 6.51 -0.53 Gold 1,233 1278 0.90

TAIEX 8,700 8,168 -4.61 Taiw an 1.3 1.63 TWD 33.0 32.38 -0.24 Coal (Thermal) 85 51 -0.49

KOSPI 1,990 1,977 -1.92 Korea 2.4 1.50 KRW 1,220.0 1164 -2.26 Steel (HRC China) 483 2920 0.69

TOPIX 1,640 1,300 -7.64 Japan 0.6 0-0.10 JPY 125.0 107.3 0.77 Aluminium 1,875 1615 -1.64

BSE 30 25,800 25,262 -1.33 India 7.6 7.25 INR 67.0 66.56 -0.05 Copper 7,100 4880 -1.89

Disclosures & Disclaimer

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: HSBC Securities (Taiwan) Corporation Limited

View HSBC Global Research at:

https://www.research.hsbc.com

THIS CONTENT MAY NOT BE DISTRIBUTED TO THE PEOPLE’S REPUBLIC OF CHINA (THE “PRC”) (EXCLUDING THE SPECIAL ADMINISTRATIVE REGIONS OF HONG KONG AND MACAO)

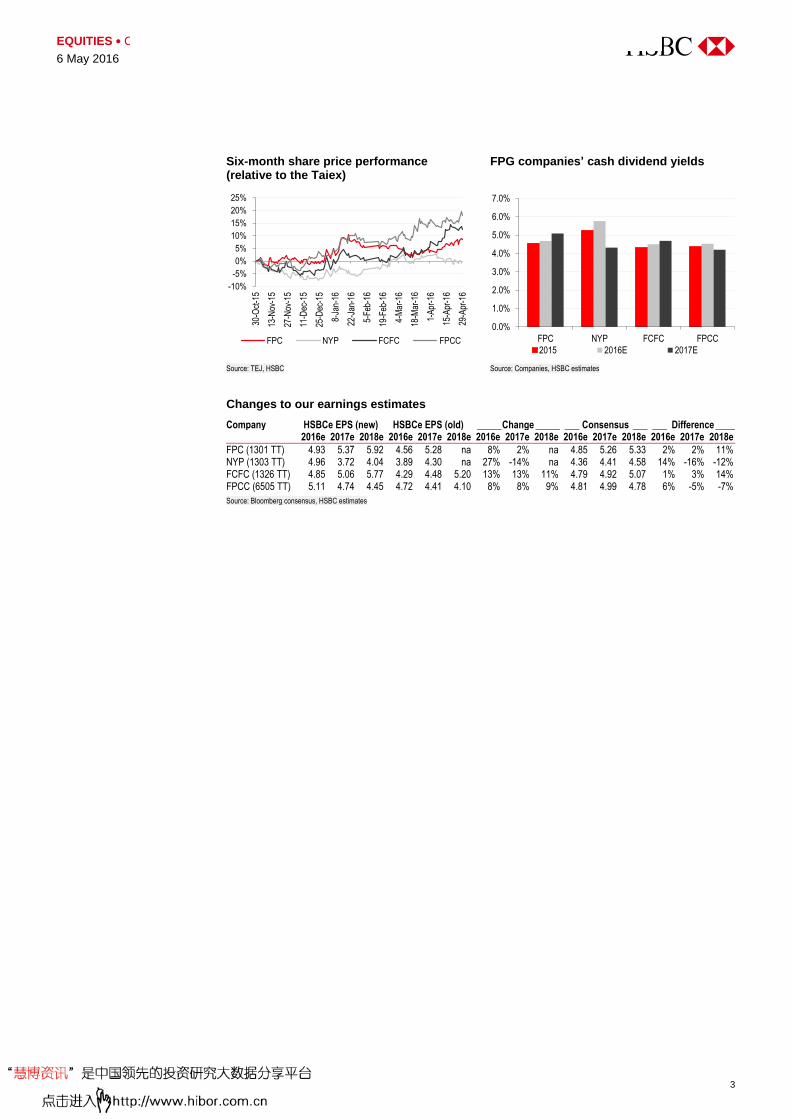

Higher oil prices and stronger demand outlook in 2017-18e

Convergence of olefin and aromatic cycles starting from 2016e

Valuations still attractive, with yields improving

Positive earnings momentum and attractive dividend yields. We upgrade Formosa

Chemicals & Fibre (FCFC) shares from Hold to Buy. We maintain our Buy ratings on

Formosa Plastics (FPC) and Formosa Petrochemical (FPCC) and our Hold rating on

Nan Ya Plastics (NYP). We raise our fair value target prices and our 2016e earnings

estimates by an average of 14% to reflect stronger-than-expected olefin margins (for

FPCC), styrene chain product spreads (for FCFC), PVC margins (for FPC), and one-

off share disposal gains (for NYP). We believe positive earnings momentum and

attractive dividend yields will continue to support valuations in the next 12 months.

Positive implications from rising crude oil prices. HSBC forecasts a recovery in

the Brent crude oil price from USD45/b in 2016e to USD60/b in 2017e and USD75/b

in 2018e. Rising crude oil prices have positive implications for refining and

petrochemical companies, and we believe FPCC is best positioned for earnings

upside in a rising crude oil price environment. FPC is also well positioned with the

highest equity stake in FPCC and FPC USA, a gas-based petrochemical producer

that should see strong margin expansion when the oil price eventually rises.

Improving petrochemical supply demand outlook. We believe petrochemical

demand will strengthen going into 2017e because we expect (1) growth of emerging

economies to accelerate and (2) accelerating GDP growth rates to lead to a higher

petrochemical demand GDP multiplier. On the supply side, light olefins should see new

capacity growth in the next two years, and even more in 2018e, while the aromatics

chain should have relatively limited capacity additions in 2017-18e. We believe FCFC

is best positioned in the medium-term recovery of the aromatics cycle.

Valuation and risks. We continue to base our target prices on DCF. Our 2016e EPS

estimates are 2%, 14%, 1%, and 6% above consensus for FPC, NYP, FCFC, and

FPCC, respectively. Key risks to our stock calls include weaker-than-expected oil

price and petrochemical spreads and unexpected operational issues.

6 May 2016

John Chung*

Head of Research, Taiwan

HSBC Securities (Taiwan) Corporation Limited

+886 2 6631 2868

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations

Taiwan Petrochemicals EQUITIES CHEMICALS

Taiwan

HSBC Taiwan Petrochemical Sector (TWD)

Company Ticker 3 May _____ TP ______ ___ Rating ___ Upside/ ____ PE (x) ____ ___ PB (x) ____ __ EPS y-o-y ___ ____ ROE _____ Dividend yield price Old New Old New downside 2016e 2017e 2016e 2017e 2016e 2017e 2016e 2017e 2016e 2017e

FPC 1301 TT 79.00 87.00 90.00 Buy Buy 14% 16.0 14.7 1.7 1.6 2% 9% 11% 11% 5% 5% NYP 1303 TT 62.70 65.00 70.00 Hold Hold 12% 12.7 16.9 1.3 1.3 10% -25% 11% 8% 6% 4% FCFC 1326 TT 80.80 84.00 95.00 Hold Buy 18% 16.7 16.0 1.4 1.4 3% 4% 8% 9% 5% 5% FPCC 6505 TT 91.30 100.00 108.00 Buy Buy 18% 17.9 19.3 3.1 3.1 3% -7% 18% 16% 5% 4%

Source: Bloomberg, HSBC estimates

Stay positive on FPG; upgrade FCFC to Buy

3

EQUITIES CHEMICALS

6 May 2016

Six-month share price performance (relative to the Taiex)

FPG companies’ cash dividend yields

Source: TEJ, HSBC Source: Companies, HSBC estimates

Changes to our earnings estimates

Company HSBCe EPS (new) HSBCe EPS (old) _____ Change _____ ___ Consensus ___ ___ Difference ____ 2016e 2017e 2018e 2016e 2017e 2018e 2016e 2017e 2018e 2016e 2017e 2018e 2016e 2017e 2018e

FPC (1301 TT) 4.93 5.37 5.92 4.56 5.28 na 8% 2% na 4.85 5.26 5.33 2% 2% 11% NYP (1303 TT) 4.96 3.72 4.04 3.89 4.30 na 27% -14% na 4.36 4.41 4.58 14% -16% -12% FCFC (1326 TT) 4.85 5.06 5.77 4.29 4.48 5.20 13% 13% 11% 4.79 4.92 5.07 1% 3% 14% FPCC (6505 TT) 5.11 4.74 4.45 4.72 4.41 4.10 8% 8% 9% 4.81 4.99 4.78 6% -5% -7%

Source: Bloomberg consensus, HSBC estimates

-10%

-5%

0%

5%

10%

15%

20%

25%

30-O

ct-1

5

13-N

ov-1

5

27-N

ov-1

5

11-D

ec-1

5

25-D

ec-1

5

8-Ja

n-16

22-J

an-1

6

5-Fe

b-16

19-F

eb-1

6

4-M

ar-1

6

18-M

ar-1

6

1-A

pr-1

6

15-A

pr-1

6

29-A

pr-1

6

FPC NYP FCFC FPCC

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

FPC NYP FCFC FPCC

2015 2016E 2017E

Disclosures & Disclaimer

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: HSBC Securities (Taiwan) Corporation Limited

View HSBC Global Research at:

https://www.research.hsbc.com

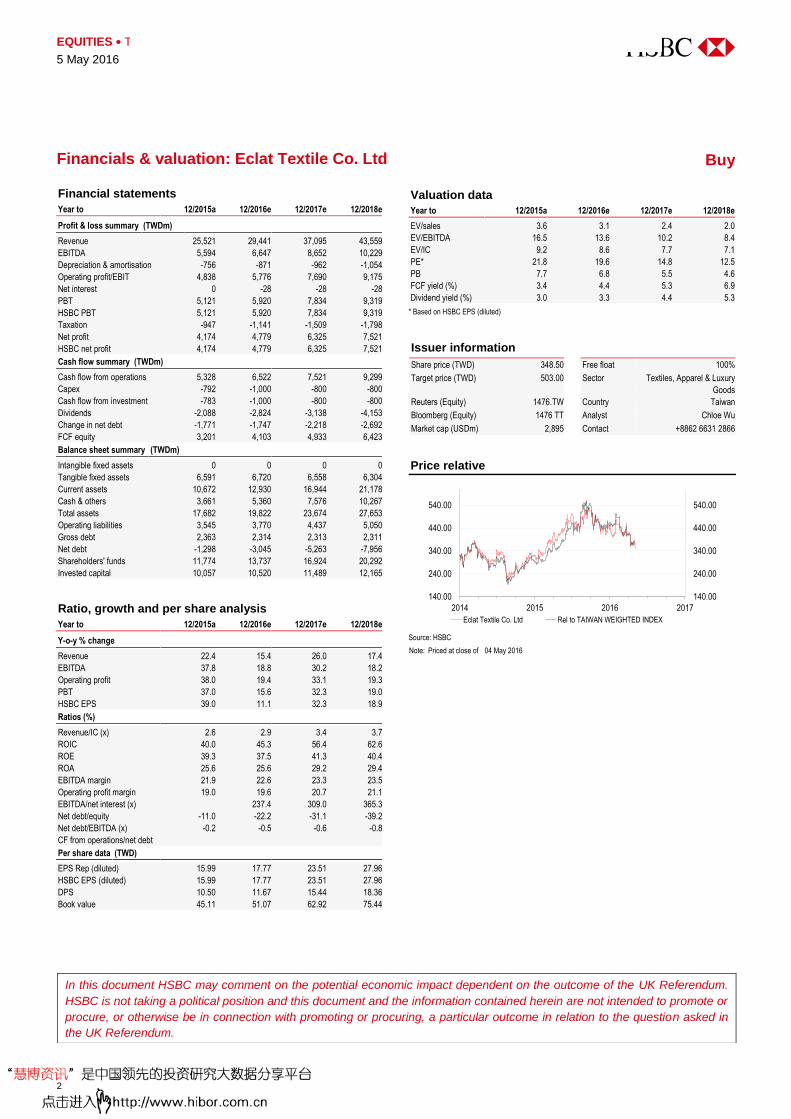

We expect Eclat to resume growth momentum in 2H16e

Eclat translates its R&D to earnings growth on P&L; 25%

FY16-18e earnings CAGR

Maintain Buy but cut our target price to TWD503 (from

TWD597); share price correction creates re-entry point

Growth momentum to resume in 2H16e: Eclat’s share price has corrected 30% from

the peak in early 4Q15, driven by the market’s concern about slowing growth. Learning

from the 1Q16 sales result, we see a delay in orders from clients, but we expect Eclat to

resume growth momentum in 2H16e, driven by (1) the high season effect; (2) new

products to launch in 2H16e; and (3) capacity expansion in FY17e. Eclat will start the

shipment of new high-end personalized functional sportswear in 2H16e, and we expect

new products to account for 7%/30% of FY16/17e group sales, respectively. The new

products enjoy higher ASPs as well as higher margin, and we expect Eclat’s gross margin

to increase to 29.6% in FY17e, up from 28.0% in FY15. The capacity expansion of two

garment plants in mid-1H17e of nearly 30% (for in-house production only) from the

current level should support the manufacture of new products.

Strong R&D as core competitive advantage for Eclat. The “Athleisure” trend has

been the main growth driver in the global apparel market for years, and more

and more non-sports apparel brands have joined the “Athleisure” market. We

expect the rising competition to push these brands to be more aggressive in

new product development. Eclat’s core competitive advantage of strong R&D,

particularly the high-end nylon-based textiles, makes the company superior to

competitors. Eclat’s new high-end products are 100% researched and

developed by Eclat.

Maintain Buy but cut target price to TWD503 (from TWD597), based on 25x (from

28x) forward 12-month 2H16-1H17e PE (rolled over from 2Q16-1Q17e). We cut our

target PE to 25x, which is the high-end of the historical trading band starting from 2012.

We cut FY16/17e EPS forecast by 11.2%/11.7%, respectively to reflect the delay in

orders resulting from channel client’s inventory issue in 1H16 and capacity constraints

until 2H17e. Despite that, we remain positive on Eclat’s FY17e growth; in view of (1) high

season in 2H16e; (2) positive 2H16e outlook from key clients; (3) new products effect;

and (4) capacity expansion in FY17e. We think the market’s low expectation on Eclat’s

1H16e growth is priced in, and it’s time to position for strong growth in FY17e. Our fair

value TP implies 44.3% upside and we maintain a Buy rating. Catalyst: stronger sales

growth and margin expansion, led by new high-end garment products, in 2H16e and

FY17e. Downside risks are macro uncertainties and lower order visibility.

5 May 2016

MAINTAIN BUY

TARGET PRICE (TWD) PREVIOUS TARGET (TWD)

503.00 597.00

SHARE PRICE (TWD) UPSIDE/DOWNSIDE

348.50 +44.3% (as of 04 May 2016)

MARKET DATA Market cap (TWDm) 93,742 Free float 69%

Market cap (USDm) 2,895 BBG 1476 TT

3m ADTV (USDm) 21.3 RIC 1476.TW

FINANCIALS AND RATIOS (TWD) Year to 12/2015a 12/2016e 12/2017e 12/2018e

HSBC EPS 15.99 17.77 23.51 27.96

HSBC EPS (prev) - 20.02 26.62 -

Change (%) - -11.2 -11.7 -

Consensus EPS 15.54 18.48 22.89 26.11

PE (x) 21.8 19.6 14.8 12.5

Dividend yield (%) 3.0 3.3 4.4 5.3

EV/EBITDA (x) 16.5 13.6 10.2 8.4

ROE (%) 39.3 37.5 41.3 40.4

52-WEEK PRICE (TWD)

Source: Thomson Reuters IBES, HSBC estimates

Chloe Wu* Non-tech Analyst

HSBC Securities (Taiwan) Corporation Limited

+8862 6631 2866

John Chung* Head of Research, Taiwan HSBC Securities (Taiwan) Corporation Limited

+8862 6631 2868

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations

Eclat Textile (1476 TT) EQUITIES TEXTILES, APPAREL & LUXURY GOODS

Taiwan

320.00

440.00

560.00

May 15 Nov 15 May 16

Target price: 503.00High: 529.05 Low: 354.00 Current: 348.50

Buy: New product development to revitalise growth

EQUITIES TEXTILES, APPAREL & LUXURY GOODS

5 May 2016

2

Financial statements

Year to 12/2015a 12/2016e 12/2017e 12/2018e

Profit & loss summary (TWDm)

Revenue 25,521 29,441 37,095 43,559

EBITDA 5,594 6,647 8,652 10,229

Depreciation & amortisation -756 -871 -962 -1,054

Operating profit/EBIT 4,838 5,776 7,690 9,175

Net interest 0 -28 -28 -28

PBT 5,121 5,920 7,834 9,319

HSBC PBT 5,121 5,920 7,834 9,319

Taxation -947 -1,141 -1,509 -1,798

Net profit 4,174 4,779 6,325 7,521

HSBC net profit 4,174 4,779 6,325 7,521

Cash flow summary (TWDm)

Cash flow from operations 5,328 6,522 7,521 9,299

Capex -792 -1,000 -800 -800

Cash flow from investment -783 -1,000 -800 -800

Dividends -2,088 -2,824 -3,138 -4,153

Change in net debt -1,771 -1,747 -2,218 -2,692

FCF equity 3,201 4,103 4,933 6,423

Balance sheet summary (TWDm)

Intangible fixed assets 0 0 0 0

Tangible fixed assets 6,591 6,720 6,558 6,304

Current assets 10,672 12,930 16,944 21,178

Cash & others 3,661 5,360 7,576 10,267

Total assets 17,682 19,822 23,674 27,653

Operating liabilities 3,545 3,770 4,437 5,050

Gross debt 2,363 2,314 2,313 2,311

Net debt -1,298 -3,045 -5,263 -7,956

Shareholders' funds 11,774 13,737 16,924 20,292

Invested capital 10,057 10,520 11,489 12,165

Ratio, growth and per share analysis

Year to 12/2015a 12/2016e 12/2017e 12/2018e

Y-o-y % change

Revenue 22.4 15.4 26.0 17.4

EBITDA 37.8 18.8 30.2 18.2

Operating profit 38.0 19.4 33.1 19.3

PBT 37.0 15.6 32.3 19.0

HSBC EPS 39.0 11.1 32.3 18.9

Ratios (%)

Revenue/IC (x) 2.6 2.9 3.4 3.7

ROIC 40.0 45.3 56.4 62.6

ROE 39.3 37.5 41.3 40.4

ROA 25.6 25.6 29.2 29.4

EBITDA margin 21.9 22.6 23.3 23.5

Operating profit margin 19.0 19.6 20.7 21.1

EBITDA/net interest (x) 237.4 309.0 365.3

Net debt/equity -11.0 -22.2 -31.1 -39.2

Net debt/EBITDA (x) -0.2 -0.5 -0.6 -0.8

CF from operations/net debt

Per share data (TWD)

EPS Rep (diluted) 15.99 17.77 23.51 27.96

HSBC EPS (diluted) 15.99 17.77 23.51 27.96

DPS 10.50 11.67 15.44 18.36

Book value 45.11 51.07 62.92 75.44

Valuation data

Year to 12/2015a 12/2016e 12/2017e 12/2018e

EV/sales 3.6 3.1 2.4 2.0

EV/EBITDA 16.5 13.6 10.2 8.4

EV/IC 9.2 8.6 7.7 7.1

PE* 21.8 19.6 14.8 12.5

PB 7.7 6.8 5.5 4.6

FCF yield (%) 3.4 4.4 5.3 6.9

Dividend yield (%) 3.0 3.3 4.4 5.3

* Based on HSBC EPS (diluted)

Issuer information

Share price (TWD) 348.50 Free float 100%

Target price (TWD) 503.00 Sector Textiles, Apparel & Luxury

Goods

Reuters (Equity) 1476.TW Country Taiwan

Bloomberg (Equity) 1476 TT Analyst Chloe Wu

Market cap (USDm) 2,895 Contact +8862 6631 2866

Price relative

Source: HSBC Note: Priced at close of 04 May 2016

140.00

240.00

340.00

440.00

540.00

140.00

240.00

340.00

440.00

540.00

2014 2015 2016 2017

Eclat Textile Co. Ltd Rel to TAIWAN WEIGHTED INDEX

Financials & valuation: Eclat Textile Co. Ltd Buy

In this document HSBC may comment on the potential economic impact dependent on the outcome of the UK Referendum.

HSBC is not taking a political position and this document and the information contained herein are not intended to promote or

procure, or otherwise be in connection with promoting or procuring, a particular outcome in relation to the question asked in

the UK Referendum.

Disclosures & Disclaimer This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: HSBC Securities (Taiwan) Corporation Limited

View HSBC Global Research at:

https://www.research.hsbc.com

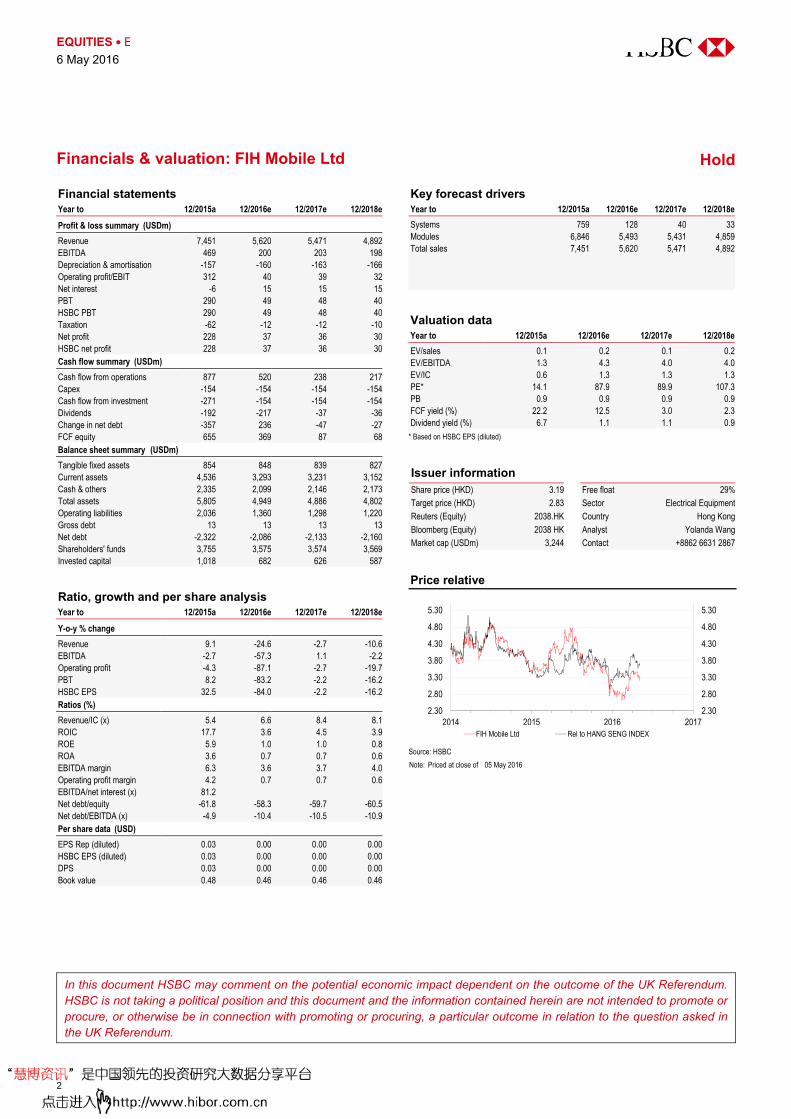

Worse-than-expected competition in component business

leads to lower gross margins

Cash is 72% of its market capitalization

Downgrade to Hold from Buy with a TP of HKD2.83 (down from HKD4.52) based on lower PB multiple

Negative profit warning for 1H16. FIH Mobile issued a profit warning post market

close that the company’s net profit will range from USD10m to USD20m (down

84-92% YoY) in 1H16 on sales of less than USD2.456bn (down 35%+ YoY). Both

sales and net profit are far below consensus estimates of USD3.69bn and USD109m,

respectively. This implies net margin will shrink substantially from 3% in 1H15 to less

than 1%, far below consensus of 3%. The company attributed the shortfall to lower

demands from some of the major customers as a result of customer transition, and

lower other income such as service fees and molding sales from these customers.

The company is scheduled to report interim results in August.

Margins of components likely much lower than expected. FIH Mobile has two

major parts of its business – the lower-margin assembly business and the much more

profitable component business. The gross margin of assembly is merely 1% and we

had initially assumed a rising adoption of FIH components would drive its gross

margin to reach 6.2% in 2016. Assuming a similar level of operating costs, the

company’s guidance implies that the gross margin of components is slightly better

than 2%, implying much worse-than-expected competition in China. We reset our

gross margin assumption from 6.2% to 2.5% in 2016e/2017e.

Affected by weaker-than-expected demand from more profitable customers.

Xiaomi (unlisted) is the most profitable customer because FIH supplies higher margin

components to Xiaomi in addition to assembly, which we estimate accounted for

more than 20-30% of FIH’s 2015 profit. Also, its major global customers including

Sony (6758.JP, not rated), Blackberry (not listed) and Amazon (AMAZ.US, not rated)

all suffer from smartphone growth slowdown with some exiting the market. We

estimate these global brands accounted for 50% of its 1H15 sales. FIH has been

trying to work more closely with Huawei (not listed), the largest Chinese brand,

especially in components, but the progress appears to be slow.

To factor in the shrinking business from global brands, we lower our 2016e/17e sales

by 27%/31% and EPS by 87%/88%. As a result, we estimate RoE will decrease from

7% to 1% in 2016. Downgrade to Hold with new TP of HKD2.83. Assuming much

lower gross margin and lower RoE, we reduce our PB-based TP from HKD4.52 to

HKD2.83 on a lower multiple of 0.8x (from 1.2x). 0.8x is where FIH traded in the

product down-cycle with an RoE of roughly 1% in 2009 since its IPO. Cash (HKD2.3

per share) is 72% of its market cap, which should provide downside support.

FLASHNOTE

6 May 2016

DOWNGRADE TO HOLD

TARGET PRICE (HKD) PREVIOUS TARGET (HKD)

2.83 4.52 SHARE PRICE (HKD) UPSIDE/DOWNSIDE

3.19 -11.3% (as of 05 May 2016)

MARKET DATA Market cap (HKDm) 25,181 Free float 29%Market cap (USDm) 3,244 BBG 2038 HK3m ADTV (USDm) 3.74 RIC 2038.HK

FINANCIALS AND RATIOS (USD) Year to 12/2015a 12/2016e 12/2017e 12/2018eHSBC EPS 0.03 0.00 0.00 0.00HSBC EPS (prev) - 0.03 0.04 0.04Change (%) - -100.0 -100.0 -100.0Consensus EPS 0.03 0.03 0.04 0.04PE (x) 14.1 87.9 89.9 107.3Dividend yield (%) 6.7 1.1 1.1 0.9EV/EBITDA (x) 1.3 4.3 4.0 4.0ROE (%) 5.9 1.0 1.0 0.8

52-WEEK PRICE (HKD)

Source: Thomson Reuters IBES, HSBC estimates

Yolanda Wang* AnalystHSBC Securities (Taiwan) Corporation Limited [email protected] +8862 6631 2867

Joyce Chen* AnalystHSBC Securities (Taiwan) Corporation Limited [email protected] +8862 6631 2862

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations

FIH Mobile Ltd (2038 HK) EQUITIES ELECTRICAL EQUIPMENT

Hong Kong

2.30

3.70

5.10

May 15 Nov 15 May 16

Target price: 2.83 High: 4.77 Low: 2.62 Current: 3.19

Downgrade to Hold: Negative profit warning

abc

EQUITIES ELECTRICAL EQUIPMENT

6 May 2016

2

Financial statements Year to 12/2015a 12/2016e 12/2017e 12/2018eProfit & loss summary (USDm) Revenue 7,451 5,620 5,471 4,892EBITDA 469 200 203 198Depreciation & amortisation -157 -160 -163 -166Operating profit/EBIT 312 40 39 32Net interest -6 15 15 15PBT 290 49 48 40HSBC PBT 290 49 48 40Taxation -62 -12 -12 -10Net profit 228 37 36 30HSBC net profit 228 37 36 30Cash flow summary (USDm) Cash flow from operations 877 520 238 217Capex -154 -154 -154 -154Cash flow from investment -271 -154 -154 -154Dividends -192 -217 -37 -36Change in net debt -357 236 -47 -27FCF equity 655 369 87 68Balance sheet summary (USDm) Tangible fixed assets 854 848 839 827Current assets 4,536 3,293 3,231 3,152Cash & others 2,335 2,099 2,146 2,173Total assets 5,805 4,949 4,886 4,802Operating liabilities 2,036 1,360 1,298 1,220Gross debt 13 13 13 13Net debt -2,322 -2,086 -2,133 -2,160Shareholders' funds 3,755 3,575 3,574 3,569Invested capital 1,018 682 626 587

Ratio, growth and per share analysis Year to 12/2015a 12/2016e 12/2017e 12/2018eY-o-y % change Revenue 9.1 -24.6 -2.7 -10.6EBITDA -2.7 -57.3 1.1 -2.2Operating profit -4.3 -87.1 -2.7 -19.7PBT 8.2 -83.2 -2.2 -16.2HSBC EPS 32.5 -84.0 -2.2 -16.2Ratios (%) Revenue/IC (x) 5.4 6.6 8.4 8.1ROIC 17.7 3.6 4.5 3.9ROE 5.9 1.0 1.0 0.8ROA 3.6 0.7 0.7 0.6EBITDA margin 6.3 3.6 3.7 4.0Operating profit margin 4.2 0.7 0.7 0.6EBITDA/net interest (x) 81.2Net debt/equity -61.8 -58.3 -59.7 -60.5Net debt/EBITDA (x) -4.9 -10.4 -10.5 -10.9Per share data (USD) EPS Rep (diluted) 0.03 0.00 0.00 0.00HSBC EPS (diluted) 0.03 0.00 0.00 0.00DPS 0.03 0.00 0.00 0.00Book value 0.48 0.46 0.46 0.46

Key forecast drivers Year to 12/2015a 12/2016e 12/2017e 12/2018eSystems 759 128 40 33Modules 6,846 5,493 5,431 4,859Total sales 7,451 5,620 5,471 4,892

Valuation data Year to 12/2015a 12/2016e 12/2017e 12/2018eEV/sales 0.1 0.2 0.1 0.2EV/EBITDA 1.3 4.3 4.0 4.0EV/IC 0.6 1.3 1.3 1.3PE* 14.1 87.9 89.9 107.3PB 0.9 0.9 0.9 0.9FCF yield (%) 22.2 12.5 3.0 2.3Dividend yield (%) 6.7 1.1 1.1 0.9

* Based on HSBC EPS (diluted)

Issuer information Share price (HKD) 3.19 Free float 29%Target price (HKD) 2.83 Sector Electrical EquipmentReuters (Equity) 2038.HK Country Hong KongBloomberg (Equity) 2038 HK Analyst Yolanda WangMarket cap (USDm) 3,244 Contact +8862 6631 2867

Price relative

Source: HSBC Note: Priced at close of 05 May 2016

2.30

2.80

3.30

3.80

4.30

4.80

5.30

2.30

2.80

3.30

3.80

4.30

4.80

5.30

2014 2015 2016 2017FIH Mobile Ltd Rel to HANG SENG INDEX

Financials & valuation: FIH Mobile Ltd Hold

In this document HSBC may comment on the potential economic impact dependent on the outcome of the UK Referendum. HSBC is not taking a political position and this document and the information contained herein are not intended to promote or procure, or otherwise be in connection with promoting or procuring, a particular outcome in relation to the question asked in the UK Referendum.

Disclaimer & Disclosures

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

View HSBC Global Research at:

https://www.research.hsbc.com

Core e-commerce business posts fastest growth in 6 quarters

Stable GMV growth but rising monetization

Maintain Buy and raise SOTP TP to USD113 from USD111;

Alibaba is an HSBC Asia Super Ten portfolio constituent

Big data driving revenue acceleration. The main value of Alibaba’s business to sellers

is its ability to promote brands, sell products, acquire customers, and maintain customer

relations. This is exemplified by the sheer scale of the platform (423m buyers and

RMB742bn in GMV in the March quarter). Underpinning this is a huge amount of

customer data that management is beginning to offer to merchants to increase its value

even further. This is leading to higher monetization and revenue acceleration. For

example, using customer data, Tmall merchants can customize their virtual stores for

customer types (first time visitor or fan), as well as recommendations, which leads to

more relevant content and higher conversion. China retail revenue grew 41% y-o-y, to

RMB18.3bn, the fastest growth in 6 quarters. Alibaba’s data business, Cloud computing,

also exhibited accelerating growth, up 175% y-o-y to RMB1bn, driven by a doubling of

paying customers (500K) and higher spending.

Strong revenue and margins. Total revenue grew 39% y-o-y to RMB24.2bn, 4%

above our estimate. Monetization for the China e-commerce retail business grew

30bp y-o-y to 2.47%, 6bp higher than our estimate. GMV grew 24% y-o-y, 2ppts

faster than our forecast, and mobile contributed 73% of GMV. Lower spending on

S&M and G&A led to a 6% beat in EBITDA and margins of 48%. EPS of USD0.47

was 5% below our estimate due to losses from Ant Financial. Alibaba generated

RMB4.4bn in free cash flow in the March quarter and RMB51bn in fiscal 2016.

Estimate changes. We raise our revenue estimates on higher monetization and faster

growth for Cloud computing. We also raise margins slightly to reflect better cost control.

We include losses from Lazada. We lower fiscal 2017/2018 EPS by 2%/3%

respectively. Management will give full fiscal-year revenue guidance at its investor day

in June, along with a deep dive on Ant Financial.

Maintain Buy and raise our SOTP TP to USD113 from USD111. Our thesis rests

on three points. First, Alibaba is best positioned to benefit from rising rural

consumption. Second, it will benefit from expanding its selection of quality products

and improving delivery. Third, we see option value in its stake in Ant Financial. At

current levels, Alibaba trades at 24x (17x core) PE for fiscal 2017, for 32% EPS

CAGR from fiscal 2016-2019. We continue to value Alibaba on SOTP basis, using a

DCF for the core business, and assessing its stake in Ant Financial and its

investments at book value. Alibaba is an HSBC Asia Super Ten portfolio constituent.

FLASHNOTE

6 May 2016

MAINTAIN BUY

TARGET PRICE (USD) PREVIOUS TARGET (USD)

113.00 111.00

SHARE PRICE (USD) UPSIDE/DOWNSIDE

75.82 +49.0% (as of 05 May 2016)

MARKET DATA Market cap (USDm) 190,492 Free float 31%

Market cap (USDm) 190,492 BBG BABA US

3m ADTV (USDm) 1,645 RIC BABA.N

FINANCIALS AND RATIOS (CNY) Year to 03/2016a 03/2017e 03/2018e 03/2019e

HSBC EPS 16.85 20.23 29.14 38.95

HSBC EPS (prev) 16.98 20.74 30.27 -

Change (%) -0.8 -2.5 -3.7 -

Consensus EPS 17.26 20.95 26.37 35.69

PE (x) 29.2 24.4 16.9 12.7

Dividend yield (%) 0.0 0.0 0.0 0.0

EV/EBITDA (x) 31.8 22.4 12.4 7.2

ROE (%) 23.5 22.2 27.2 29.3

52-WEEK PRICE (USD)

Source: HSBC estimates, ThomsonReuters IBES

Chi Tsang,* CFA Head of Internet Research, Asia Pacific

The Hongkong and Shanghai Banking Corporation Limited

+852 2822 2590

Alice Cai* Associate analyst The Hongkong and Shanghai Banking Corporation Limited

+852 2996 6584

Qin Wang* Associate

The Hongkong and Shanghai Banking Corporation Limited

+852 2822 4393

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations

Alibaba Group (BABA US) EQUITIES INTERNET

China

50.00

85.00

120.00

May 15 Nov 15 May 16

Target price: 113.00High: 93.88 Low: 57.39 Current: 75.82

Buy: Leveraging data to raise the value of its platform

EQUITIES INTERNET

6 May 2016

2

Financials & valuation

Financial statements

Year to 03/2016a 03/2017e 03/2018e 03/2019e

Profit & loss summary (CNYm)

Revenue 101,143 149,264 197,905 258,850

EBITDA 32,872 42,897 69,071 99,023

Depreciation & amortisation -3,770 -4,605 -4,642 -4,674

Operating profit/EBIT 29,102 38,292 64,429 94,349

Net interest 50,308 2,388 4,334 7,346

PBT 79,738 38,774 68,357 101,289

HSBC PBT 51,361 62,430 91,091 122,288

Taxation -8,449 -9,975 -16,687 -24,084

Net profit 71,460 29,746 52,401 77,313

HSBC net profit 42,912 51,495 74,201 99,154

Cash flow summary (CNYm)

Cash flow from operations 75,901 85,089 106,596 143,629

Capex -8,636 -1,502 -1,909 -4,783

Cash flow from investment -49,152 -43,949 -1,909 -4,783

Dividends 0 0 0 0

Change in net debt 13,399 -41,140 -104,687 -138,846

FCF equity 71,962 48,572 77,957 112,687

Balance sheet summary (CNYm)

Intangible fixed assets 87,015 84,043 81,071 78,099

Tangible fixed assets 24,795 32,068 40,280 51,246

Current assets 134,070 177,378 286,199 434,007

Cash & others 111,518 148,354 249,241 387,608

Total assets 366,733 456,789 570,850 726,653

Operating liabilities 50,319 73,996 108,074 156,263

Gross debt 6,175 1,871 -1,929 -2,408

Net debt -105,343 -146,483 -251,170 -390,016

Shareholders' funds 218,225 245,864 299,296 376,528

Invested capital 84,043 71,138 50,235 19,482

Ratio, growth and per share analysis

Year to 03/2016a 03/2017e 03/2018e 03/2019e

Y-o-y % change

Revenue 32.7 47.6 32.6 30.8

EBITDA 29.1 30.5 61.0 43.4

Operating profit 25.8 31.6 68.3 46.4

PBT 159.4 -51.4 76.3 48.2

HSBC EPS 21.3 20.0 44.1 33.6

Ratios (%)

Revenue/IC (x) 1.6 1.9 3.3 7.4

ROIC 39.9 36.7 80.2 206.3

ROE 23.5 22.2 27.2 29.3

ROA 23.4 7.4 10.4 12.1

EBITDA margin 32.5 28.7 34.9 38.3

Operating profit margin 28.8 25.7 32.6 36.4

EBITDA/net interest (x)

Net debt/equity -42.0 -52.6 -75.7 -95.3

Net debt/EBITDA (x) -3.2 -3.4 -3.6 -3.9

CF from operations/net debt

Per share data (CNY)

EPS reported (diluted) 28.07 11.68 20.58 30.37

HSBC EPS (diluted) 16.85 20.23 29.14 38.95

DPS 0.00 0.00 0.00 0.00

Book value 85.71 96.57 117.56 147.89

Valuation data

Year to 03/2016a 03/2017e 03/2018e 03/2019e

EV/sales 10.3 6.4 4.3 2.8

EV/EBITDA 31.8 22.4 12.4 7.2

EV/IC 12.4 13.5 17.0 36.8

PE* 29.2 24.4 16.9 12.7

PB 5.7 5.1 4.2 3.3

FCF yield (%) 6.3 4.4 7.0 10.2

Dividend yield (%) 0.0 0.0 0.0 0.0

* Based on HSBC EPS (diluted)

Price relative

Source: HSBC Note: Priced at close of 05 May 2016

49.00

59.00

69.00

79.00

89.00

99.00

109.00

119.00

129.00

49.00

59.00

69.00

79.00

89.00

99.00

109.00

119.00

129.00

2014 2015 2016 2017Alibaba Group Rel to NASDAQ 100 INDEX

In this document HSBC may comment on the potential economic impact dependent on the outcome of the UK Referendum.

HSBC is not taking a political position and this document and the information contained herein are not intended to promote or

procure, or otherwise be in connection with promoting or procuring, a particular outcome in relation to the question asked in

the UK Referendum.

Disclaimer & Disclosures

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

View HSBC Global Research at:

https://www.research.hsbc.com

So, we published a chart earlier this week that caused a bit of excitement among

our readers. It shows a spike in the new order-to-inventory ratio for emerging Asia

(based on the latest crop of PMIs). This, ordinarily, points to an acceleration in

industrial output in the region. Trouble is, as helpful as the indicator often proves,

at times it can send false signals. And this is probably one of those times. In fact,

look closely and it quickly becomes clear that the rise in the new order-to-inventory

measure is largely due to a drop in the latter, and not a rise in the former. True, you

might still expect some improvement in production in coming months as stocks

are replenished. However, without a convincing pick-up in new orders, the bounce

will prove decidedly short-lived. In fact, another interpretation is entirely possible:

producers may have allowed inventory to fall in anticipation of weaker demand

ahead. In short, don’t get too excited about the spike in the new order-to-inventory

ratio. Growth can’t be sustained by restocking alone.

A Waldorf salad? I think we’re out of Waldorfs.

Basil Fawlty

Here is the chart that caused a bit of excitement. In our monthly PMI wrap-up, we showed

that a leading indicator for industrial production growth -- new orders minus inventory --

spiked (see Frederic Neumann and Abanti Bhaumik, Who stole my spring bounce:

What the latest PMIs mean for Asia, 2 May, 2016). On the face of it, impressive stuff.

But, as we also noted, it’s important to dig a little deeper. It turns out that our measure

rose largely because of a drop in inventory, not because of a notable pick-up in new

orders. “Same difference” you might argue: after all, the measure has generally

proven to be a useful lead indicator. And, yes, some acceleration in output growth

might occur. But, we suspect, it will disappoint optimists. Consider Chart 2. This

shows the underlying new order and inventory series.

6 May 2016

Frederic Neumann

Economist

The Hongkong and Shanghai Banking Corporation Limited

+852 2822 4556

Abanti Bhaumik

Economics Associate Bangalore

Asia Chart of the Week ECONOMICS ASIA

Chart 1: PMI new orders minus inventory and industrial production growth

Source: Markit, CEIC, HSBC

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

-10

-8

-6

-4

-2

0

2

4

6

8

10

Asia x JN new orders minus inventories (LHS) IP % 3m/3m, Asia weighted avg. ex HK & JP (RHS)

Nope, false signal

ECONOMICS ASIA

6 May 2016

2

Chart 2: Asia ex Japan PMI inventory and new orders (3mma)

Source: Markit, HSBC

Note the plunge inventories in recent months. Ordinarily, that should be positive, prompting a rise

in production as shelves are restocked. However, new orders barely rose (in fact, in April, they

were unchanged compared to March), and the index is still below its rather shallow highs of the

last several years. Contrast this, for example, with the run-up to the Global Financial Crisis, when

new orders soared but inventory plunged; or its aftermath, when the latter could barely keep up

with the former. Surely, for sustained growth, and not just a temporary output bump, new orders

have to rise briskly as well.

Ah, yes, many readers argued, but look at the US. Here, the equivalent ISM measure also points

to a rise in production ahead. This, in turn, should be positive for Asian exports and help support

local output. Well, yes. But it’s important to keep things in perspective. Take a look at Chart 3. This

shows the ISM ‘new orders minus inventory’ series and new export orders for emerging Asia. Given

the correlation between the two, a little lift could still occur, perhaps. But the chart hardly signals an

impending surge in shipments. In fact, last month, new export orders were still contracting. At the

moment, therefore, this particular indicator is more noise than signal.

35

40

45

50

55

60

65

45

46

47

48

49

50

51

52

Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15

inventory new orders

In this document HSBC may comment on the potential economic impact dependent on the outcome of the UK Referendum. HSBC is not taking a political position and this document and the information contained herein are not intended to promote or procure, or otherwise be in connection with promoting or procuring, a particular outcome in relation to the question asked in the UK Referendum.

Chart 3: US ISM new orders minus inventory and Asia ex Japan new export orders

Source: Markit, CEIC, HSBC

30

35

40

45

50

55

60

65

70

-20

-15

-10

-5

0

5

10

15

20

25

30

35

Apr-06 Apr-07 Apr-08 Apr-09 Apr-10 Apr-11 Apr-12 Apr-13 Apr-14 Apr-15

US ISM new orders minus inventory Asia ex Japan PMI new export orders (RHS)

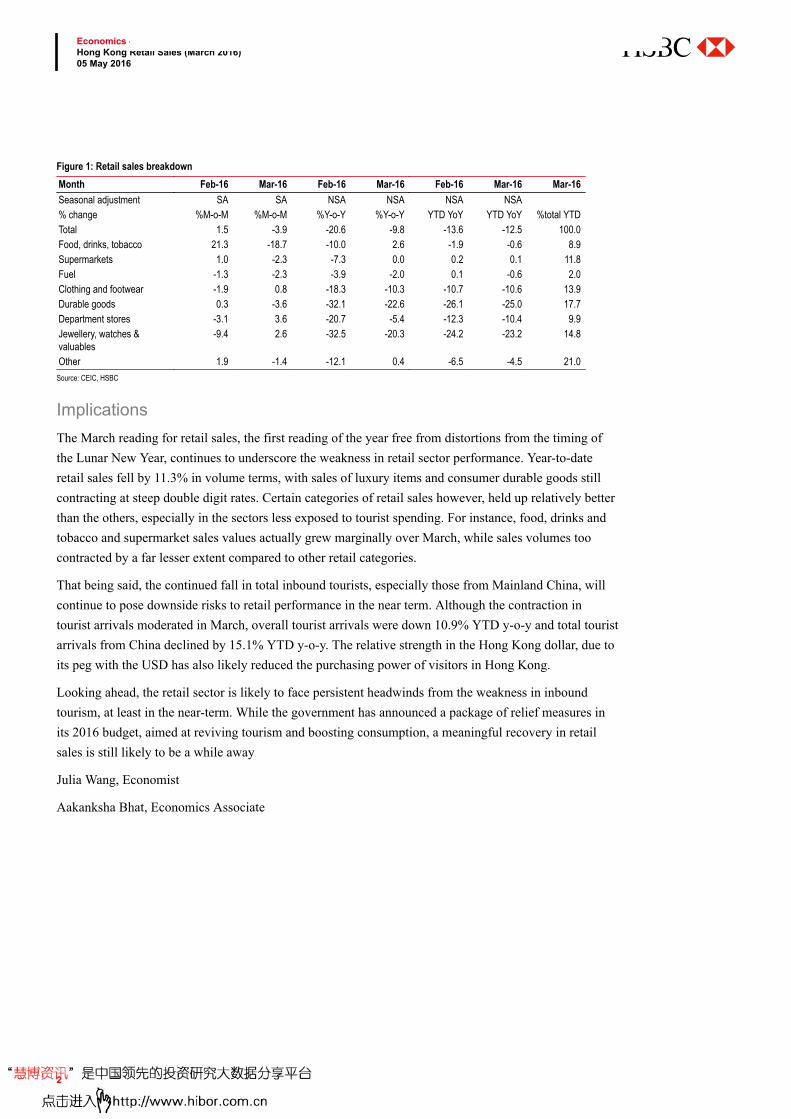

Hong Kong Retail Sales (March 2016)Pace of decline moderates The contraction in retail sales eased in March after the Chinese New Year effect faded, but remains at a weak level. Both the luxury goods sector and the consumer durable goods sector continued to pose double-digit contractions, as a result of a 11% YTD contraction in inbound tourists. Food and supermarket sales however, held up relatively better. On balance, the retail sector continues to face headwinds from the slowdown in tourism and the relative strength of the Hong Kong Dollar. This is likely to limit the pace of recovery in the near-term.

Facts• March retail sales values contracted at a slower pace of 9.8% y-o-y, compared with a contraction of 20.6% y-o-y in February and a fall of 13.6% y-o-y over the Jan-Feb period (Bbg: -8.8%, HSBC: -5.5%)

• For Q1-16 as a whole, sales values were down 12.5% y-o-y, compared with a contraction of 6.4% y-o-y in Q4-15

• March retail sales volumes also contracted at a slower pace of 8.8% y-o-y, down from a contraction of 19.5% y-o-y in February and a fall of 12.4% y-o-y over the Jan-Feb period (Bbg: -6.9%, HSBC: -4.6%)

• For Q1-16 as a whole, sales volumes fell by 11.3% y-o-y, compared with a decline of 3.7% y-o-y in Q4-15

• In terms of broad type of retail outlet, consumer durable goods and jewellery, watches and clocks and valuable gifts, continued to be the worst performers both in value and volume terms

• Sales values of jewellery, watches and clocks and valuable gifts contracted by 20.3% y-o-y in March, while sales volumes were down 17.7% y-o-y

• March consumer durable goods sales values fell by 22.6% y-o-y, while sales volumes were down 17.7% y-o-y

Economics - Data Reactions

05 May 2016

JuliaWang

Economist, Greater ChinaThe Hongkong and ShanghaiBanking Corporation Limited+852 3604 [email protected]

View HSBC Global Research at:http://www.research.hsbc.com

Issuer of reportThe Hongkong and ShanghaiBanking Corporation Limited

Disclosures & DisclaimerThis report must be read with thedisclosures and the analystcertifications in the Disclosureappendix, and with the Disclaimer,which forms part of it

In this document HSBC maycomment on the potentialeconomic impact dependent onthe outcome of the UKReferendum. HSBC is not taking apolitical position and this documentand the information containedherein are not intended to promoteor procure, or otherwise be inconnection with promoting orprocuring, a particular outcome inrelation to the question asked inthe UK Referendum.

Figure 1: Retail sales breakdownMonth Feb-16 Mar-16 Feb-16 Mar-16 Feb-16 Mar-16 Mar-16 Seasonal adjustment SA SA NSA NSA NSA NSA % change %M-o-M %M-o-M %Y-o-Y %Y-o-Y YTD YoY YTD YoY %total YTD Total 1.5 -3.9 -20.6 -9.8 -13.6 -12.5 100.0 Food, drinks, tobacco 21.3 -18.7 -10.0 2.6 -1.9 -0.6 8.9 Supermarkets 1.0 -2.3 -7.3 0.0 0.2 0.1 11.8 Fuel -1.3 -2.3 -3.9 -2.0 0.1 -0.6 2.0 Clothing and footwear -1.9 0.8 -18.3 -10.3 -10.7 -10.6 13.9 Durable goods 0.3 -3.6 -32.1 -22.6 -26.1 -25.0 17.7 Department stores -3.1 3.6 -20.7 -5.4 -12.3 -10.4 9.9 Jewellery, watches &valuables

-9.4 2.6 -32.5 -20.3 -24.2 -23.2 14.8

Other 1.9 -1.4 -12.1 0.4 -6.5 -4.5 21.0 Source: CEIC, HSBC

ImplicationsThe March reading for retail sales, the first reading of the year free from distortions from the timing of the Lunar New Year, continues to underscore the weakness in retail sector performance. Year-to-date retail sales fell by 11.3% in volume terms, with sales of luxury items and consumer durable goods still contracting at steep double digit rates. Certain categories of retail sales however, held up relatively better than the others, especially in the sectors less exposed to tourist spending. For instance, food, drinks and tobacco and supermarket sales values actually grew marginally over March, while sales volumes too contracted by a far lesser extent compared to other retail categories.

That being said, the continued fall in total inbound tourists, especially those from Mainland China, will continue to pose downside risks to retail performance in the near term. Although the contraction in tourist arrivals moderated in March, overall tourist arrivals were down 10.9% YTD y-o-y and total tourist arrivals from China declined by 15.1% YTD y-o-y. The relative strength in the Hong Kong dollar, due to its peg with the USD has also likely reduced the purchasing power of visitors in Hong Kong.

Looking ahead, the retail sector is likely to face persistent headwinds from the weakness in inbound tourism, at least in the near-term. While the government has announced a package of relief measures in its 2016 budget, aimed at reviving tourism and boosting consumption, a meaningful recovery in retail sales is still likely to be a while away

Julia Wang, Economist

Aakanksha Bhat, Economics Associate

Economics - Data ReactionsHong Kong Retail Sales (March 2016)05 May 2016

2

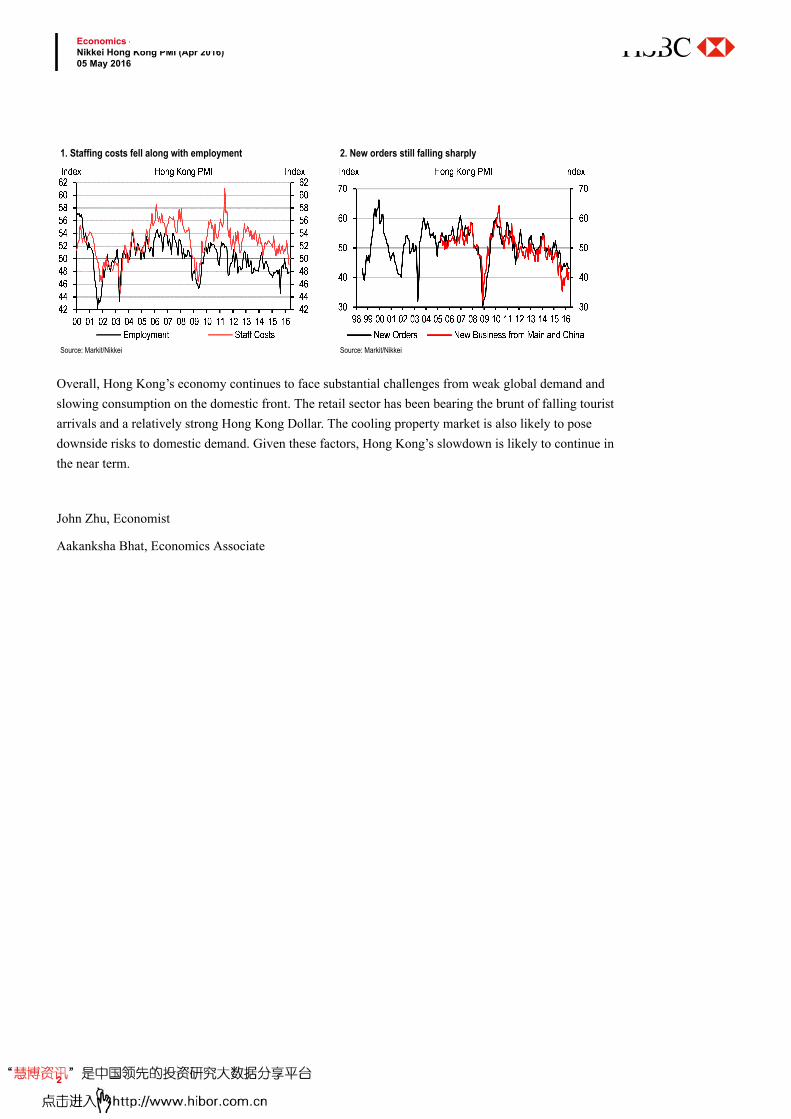

Nikkei Hong Kong PMI (Apr 2016)Contracting furtherThe headline Nikkei Hong Kong PMI fell further to 45.3 in April, down from 45.5 in March, signalling a faster deterioration in private sector activity. New orders fell at a faster pace, underscoring the overall weakness in demand conditions. Firms continue to cut jobs as output remains weak. Weak demand at home and from abroad mean Hong Kong’s economic slowdown is likely to continue in the near-term.

Facts4 The headline Nikkei Hong Kong PMI index fell to 45.3 in April, down from 45.5 in March.

The latest reading is the lowest in eight months.4 The output sub-index was unchanged from March and has remained below 50 for over a year

now.4 The employment sub-index ticked up marginally in April, although it continues to remain

below the 50 level. April marks the fourth straight month that firms cut employment overall.4 The new orders sub-index contracted at a faster pace in April, and is at a seven month low.4 The new business from China sub-index continued to contract in April, albeit at a slower pace

than in March.4 Purchase prices rose to above 50 in April, the first expansion in six months. Staff costs

however, fell below the 50 level, marking the first contraction since July 2009.

ImplicationsThe April PMI reading once again underlined the weakness in Hong Kong’s private sector, which has been stuck in contraction for over a year. Both output and new orders remain very weak, suggesting continued contraction in domestic and external demand conditions. Furthermore, China’s slow pace of economic recovery continues to weigh on economic activity in Hong Kong. New orders from China remained in deep contraction in April, although there was an improvement from March. The labour market, which has so far been relatively resilient, has also started to show signs of strain, as staff costs contracted for the first time since July 2009.

Economics - Data Reactions

05 May 2016

JohnZhu

EconomistThe Hongkong and ShanghaiBanking Corporation Limited+852 2996 [email protected]

View HSBC Global Research at:http://www.research.hsbc.com

Issuer of reportThe Hongkong and ShanghaiBanking Corporation Limited

Disclosures & DisclaimerThis report must be read with thedisclosures and the analystcertifications in the Disclosureappendix, and with the Disclaimer,which forms part of it

In this document HSBC maycomment on the potentialeconomic impact dependent onthe outcome of the UKReferendum. HSBC is not taking apolitical position and this documentand the information containedherein are not intended to promoteor procure, or otherwise be inconnection with promoting orprocuring, a particular outcome inrelation to the question asked inthe UK Referendum.

1. Staffing costs fell along with employment

Source: Markit/Nikkei

2. New orders still falling sharply

Source: Markit/Nikkei

Overall, Hong Kong’s economy continues to face substantial challenges from weak global demand and slowing consumption on the domestic front. The retail sector has been bearing the brunt of falling tourist arrivals and a relatively strong Hong Kong Dollar. The cooling property market is also likely to pose downside risks to domestic demand. Given these factors, Hong Kong’s slowdown is likely to continue in the near term.

John Zhu, Economist

Aakanksha Bhat, Economics Associate

Economics - Data ReactionsNikkei Hong Kong PMI (Apr 2016)05 May 2016

2

Disclaimer & Disclosures

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

View HSBC Global Research at:

https://www.research.hsbc.com

This content may not be distributed to the People's Republic of China (The "PRC")

(excluding special administrative regions of Hong Kong and Macao)

What’s on our mind?

April is normally the start of the peak season for air conditioner sales. However,

demand has yet to show strong signs of picking up, based on our recent visits to

appliance retailers in south China. Appliance makers and retailers are hoping for the

weather to warm up to drive demand in the peak season. Thanks to wholesale supply

discipline, channel inventory has come down 20-30% vs. the worst time last year.

Positive is that retail prices have held up quite well due to less aggressive

discounting. The sector might be ready for a rebound if sales grow in the peak

season – The HK/China Consumer Team

What’s headline news (see page 2 for other news)

Hong Kong visitor arrivals: Visitor arrivals from mainland China to Hong Kong during

the Labour Day Holiday was up 7% y-o-y (30 April-2 May in 2016 vs. 1-3 May in 2015).

Our latest views (see page 3 for other research)

Jewellery retailers – Higher gold prices did not stop slide in sales 15 Apr

January-March gold jewellery sales disappointed, especially in China. The industry has

entered a phase of slow growth and further re-rated capped by earning cuts.

Downgrade CTF to Reduce, cut TP to HKD4.00 from HKD4.30, LF to Hold, cut TP to

HKD16.30 from HKD20.70, and remain Buy on CSS with a HKD15.90 TP, implying

36% upside.

This note replaces the version of the same date and title published earlier to correct the

old and new rating columns on page 1.

5 May 2016

Erwan Rambourg*

Global Co-Head Consumer & Retail Research

The Hongkong and Shanghai Banking Corporation Limited

+852 2996 6572

Lina Yan*

HK/China Discretionary Research

The Hongkong and Shanghai Banking Corporation Limited

+852 2822 4344

Christopher Leung* HK/China Staples Research

The Hongkong and Shanghai Banking Corporation Limited

+852 2996 6531

Scott Chan*

Macau Gaming Research

The Hongkong and Shanghai Banking Corporation Limited

+852 3941 7005

Vishal Goel*

Associate

Bangalore

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations

The Great Mall of China EQUITIES CONSUMER & RETAIL

China

Recent target price and rating changes

Date Ticker Company Old TP New TP Old Rating New Rating

5-May MPEL.OQ Melco Crown Entertainment 16.50 16.60 Hold Unchanged 30-Apr 600690.SS Qingdao Haier Co Ltd 10.10 11.10 Buy Unchanged 29-Apr 000858.SZ Wuliangye Yibin Co Ltd 36.00 38.00 Buy Unchanged 23-Apr 600138.SS China CYTS Tours 26.50 25.30 Buy Buy 20-Apr 0027.HK Galaxy Entertainment 31.90 33.30 Buy Unchanged 20-Apr 0200.HK Melco International 11.60 10.70 Buy Hold 20-Apr 2282.HK MGM China 13.70 14.20 Buy Unchanged 20-Apr 1928.HK Sands China 25.00 27.20 Hold Unchanged 20-Apr 0880.HK SJM Holdings 6.10 5.00 Buy Hold 19-Apr 600519.SS Kweichow Moutai Co Ltd 292.00 284.00 Buy Unchanged 18-Apr 2331.HK Li Ning 4.40 4.00 Buy Hold 15-Apr 1929.HK Chow Tai Fook Jewellery 4.30 4.00 Hold Reduce 15-Apr 0590.HK Luk Fook 20.70 16.30 Buy Hold 14-Apr 1913.HK Prada SPA 28.00 26.00 Buy Hold 12-Apr 0322.HK Tingyi 6.70 6.50 Reduce Unchanged 11-Apr 600612.SS Lao Feng Xiang A 64.00 35.00 Buy Reduce 11-Apr 900905.SS Lao Feng Xiang B 7.73 3.05 Buy Reduce 8-Apr 1382.HK Pacific Textiles 12.60 12.00 Hold Unchanged 8-Apr 0551.HK Yue Yuen Industrial 31.60 30.90 Buy Unchanged 6-Apr 1128.HK Wynn Macau 8.50 9.50 Hold Reduce 1-Apr 0493.HK Gome Electrical Appliance 1.52 1.37 Buy Unchanged

Source: HSBC estimates

Air conditioner makers yearning for a hot summer

EQUITIES CONSUMER & RETAIL

5 May 2016

2

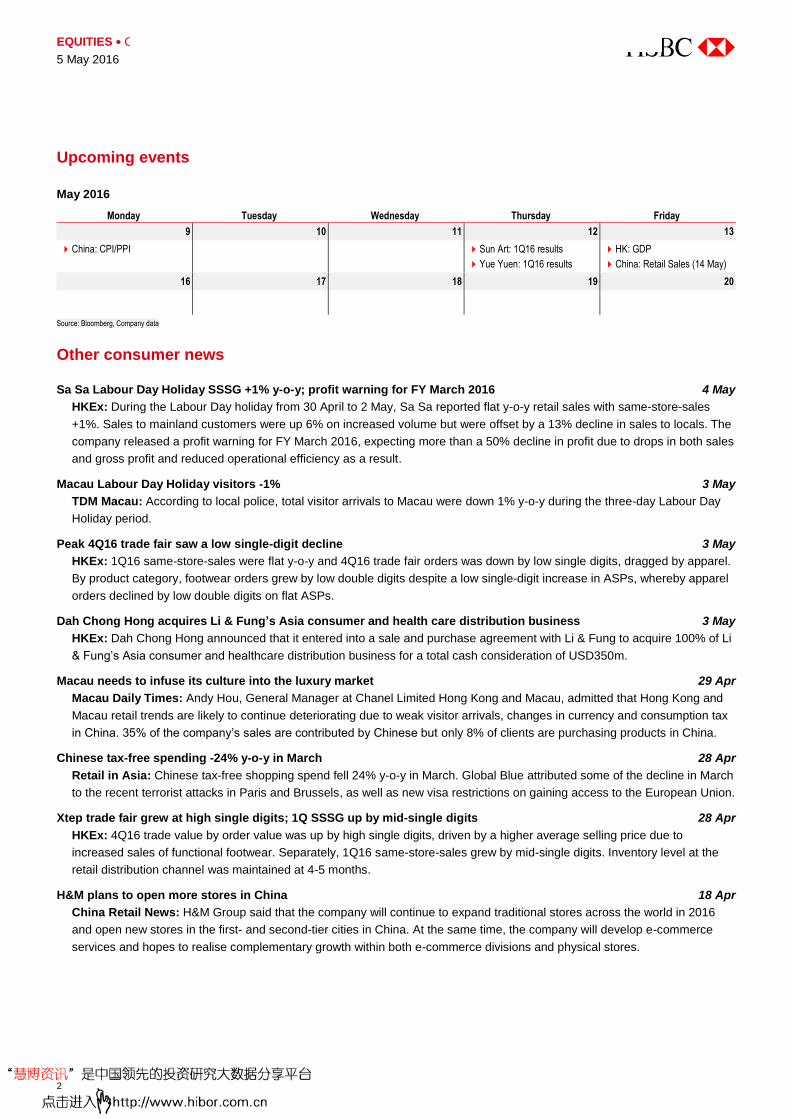

Upcoming events

May 2016

Monday Tuesday Wednesday Thursday Friday

9 10 11 12 13

China: CPI/PPI Sun Art: 1Q16 results

Yue Yuen: 1Q16 results

HK: GDP

China: Retail Sales (14 May)

16 17 18 19 20

Source: Bloomberg, Company data

Other consumer news

Sa Sa Labour Day Holiday SSSG +1% y-o-y; profit warning for FY March 2016 4 May

HKEx: During the Labour Day holiday from 30 April to 2 May, Sa Sa reported flat y-o-y retail sales with same-store-sales

+1%. Sales to mainland customers were up 6% on increased volume but were offset by a 13% decline in sales to locals. The

company released a profit warning for FY March 2016, expecting more than a 50% decline in profit due to drops in both sales

and gross profit and reduced operational efficiency as a result.

Macau Labour Day Holiday visitors -1% 3 May

TDM Macau: According to local police, total visitor arrivals to Macau were down 1% y-o-y during the three-day Labour Day

Holiday period.

Peak 4Q16 trade fair saw a low single-digit decline 3 May

HKEx: 1Q16 same-store-sales were flat y-o-y and 4Q16 trade fair orders was down by low single digits, dragged by apparel.

By product category, footwear orders grew by low double digits despite a low single-digit increase in ASPs, whereby apparel

orders declined by low double digits on flat ASPs.

Dah Chong Hong acquires Li & Fung’s Asia consumer and health care distribution business 3 May

HKEx: Dah Chong Hong announced that it entered into a sale and purchase agreement with Li & Fung to acquire 100% of Li

& Fung’s Asia consumer and healthcare distribution business for a total cash consideration of USD350m.

Macau needs to infuse its culture into the luxury market 29 Apr

Macau Daily Times: Andy Hou, General Manager at Chanel Limited Hong Kong and Macau, admitted that Hong Kong and

Macau retail trends are likely to continue deteriorating due to weak visitor arrivals, changes in currency and consumption tax

in China. 35% of the company’s sales are contributed by Chinese but only 8% of clients are purchasing products in China.

Chinese tax-free spending -24% y-o-y in March 28 Apr

Retail in Asia: Chinese tax-free shopping spend fell 24% y-o-y in March. Global Blue attributed some of the decline in March

to the recent terrorist attacks in Paris and Brussels, as well as new visa restrictions on gaining access to the European Union.

Xtep trade fair grew at high single digits; 1Q SSSG up by mid-single digits 28 Apr

HKEx: 4Q16 trade value by order value was up by high single digits, driven by a higher average selling price due to

increased sales of functional footwear. Separately, 1Q16 same-store-sales grew by mid-single digits. Inventory level at the

retail distribution channel was maintained at 4-5 months.

H&M plans to open more stores in China 18 Apr

China Retail News: H&M Group said that the company will continue to expand traditional stores across the world in 2016

and open new stores in the first- and second-tier cities in China. At the same time, the company will develop e-commerce

services and hopes to realise complementary growth within both e-commerce divisions and physical stores.

Disclaimer & Disclosures

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

View HSBC Global Research at:

https://www.research.hsbc.com

THIS CONTENT MAY NOT BE DISTRIBUTED TO THE PEOPLE'S REPUBLIC OF CHINA (THE "PRC") (EXCLUDING SPECIAL ADMINISTRATIVE REGIONS OF HONG KONG AND MACAO)

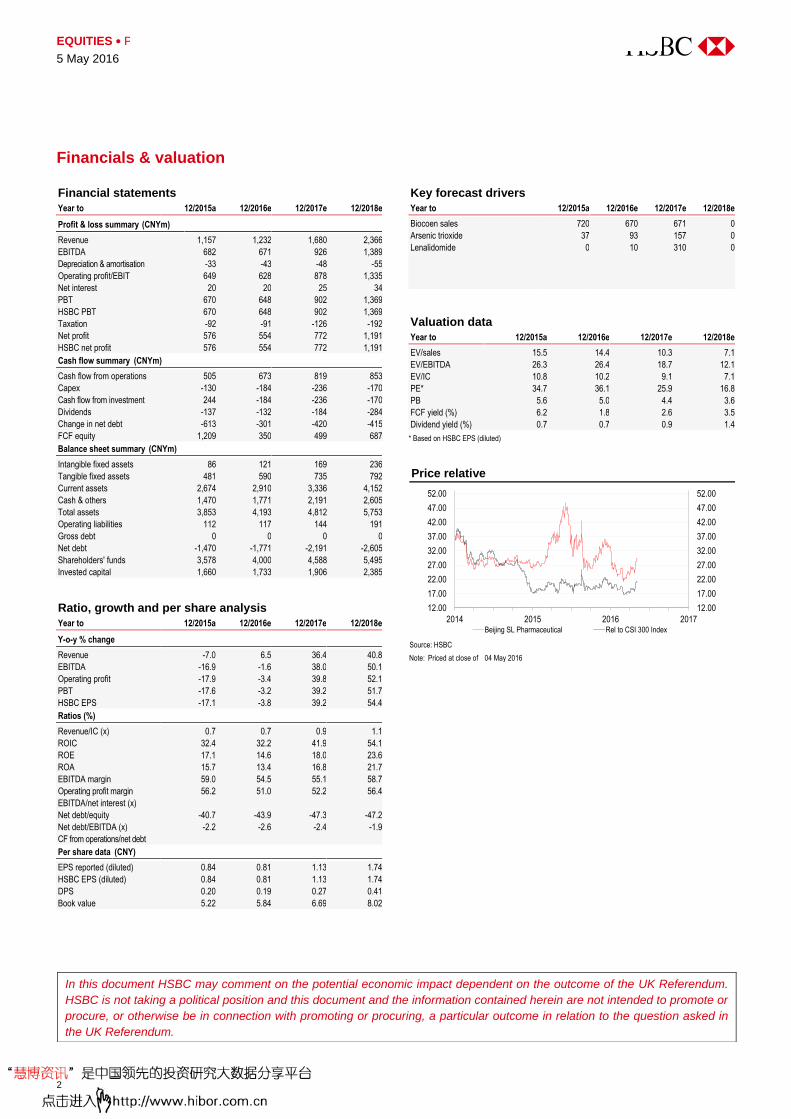

CFDA announced it had started its on-site inspection of SL

Pharm’s generic Lenalidomide

We expect Lenalidomide to contribute RMB4.9bn to SL Pharm

at peak sales

Raise TP to RMB36.4 from RMB33.30 on higher PE multiple,

reiterate Buy

Another milestone: SL Pharm’s long-anticipated generic Lenalidomide is advancing

in the CFDA’s (China Food and Drug Administration) drug review. After the CFDA

said on 1 May it would grant it fast-track approval, it announced on 3 May that it

would start on-site inspection of Lenalidomide, which is generally perceived as the

last step of a drug’s review. In our opinion, the risk of product withdrawal or rejection

of Lenalidomide is low. Along with Lenalidomide, Hengrui’s white blood stimulator

19K is also on the inspection list. They are both survivors of the CFDA’s harsh

clinical trial data inspection in the past year, following which over 80% of the

applications were withdrawn.

Potential market size in China: Lenalidomide is a chemotherapy drug developed by

US pharma giant Celgene (CELG, USD102.84, not rated). It was approved by the US

FDA as a treatment for Myelodysplastic Syndromes (MDS) in December 2005 and for

Multiple Myeloma (MM) in June 2006. In 2015, Celgene’s global sales of

Lenalidomide totaled USD5.8bn. Lenalidomide is recommended as the first-line

treatment for MDS and second-line treatment for MM. Incidence cases for MDS and

MM are 52k and 26k respectively in China. Based on treatment costs and courses of

treatments, we forecast the market size of patent Lenalidomide for MDS and MM at

RMB45.7bn and RMB3.8bn, respectively. Some charities dealing with rare diseases

in developed areas are sponsoring Lenalidomide’s giveaway campaign on a “buy 3

get 7 free” basis. NHFPC (National Health and Family Planning Commission) has

initiated a program to cut the price of five patent drugs indicated for critical disease

including Celgene’s Lenalidomide by 50%. If Celgene agrees to the price, we think

SL Pharm is likely to price its generic Lenalidomide at a further 50% discount.

Consequently, we have what we think is a conservative estimate of RMB12.3bn

market size (see detailed calculation on page 3). Assuming SL Pharm takes a 40%

market share, we expect Lenalidomide to contribute RMB4.9bn revenue and

RMB1.5bn net profit (30% margin) at peak sales.

Reiterate Buy rating: We cut our 2016/17e EPS by 15%/10% due to the delayed

timeline of product launch from the previous schedule and extend our forecasts to

2018. We expect EPS to grow at 45% CAGR in 2016-18, given the expected fast

ramp-up of Lenalidomide once approved. Our new TP of RMB36.4 from RMB33.3 is

based on a new 2016e PE of 45x (vs 35x) based on 1.0 PEG (2016e PE/2016-17e

CAGR), a discount of 38% to the industry average of 1.6 PEG (due to the uncertainty

of Lenalidomide’s promotion) and implying 32x/21x 2017/18e PE.

5 May 2016

MAINTAIN BUY

TARGET PRICE (CNY) PREVIOUS TARGET (CNY)

36.40 33.30

SHARE PRICE (CNY) UPSIDE/DOWNSIDE

29.21 +24.6% (as of 04 May 2016)

MARKET DATA Market cap (CNYm) 20,016 Free float 100%

Market cap (USDm) 3,081 BBG 002038 CH

3m ADTV (USDm) 35.2 RIC 002038.SZ

FINANCIALS AND RATIOS (CNY) Year to 12/2015a 12/2016e 12/2017e 12/2018e

HSBC EPS 0.84 0.81 1.13 1.74

HSBC EPS (prev) 0.89 0.95 1.25 -

Change (%) -5.6 -14.7 -9.6 -

Consensus EPS 1.19 1.25 1.09 1.52

PE (x) 34.7 36.1 25.9 16.8 Dividend yield (%) 0.7 0.7 0.9 1.4

EV/EBITDA (x) 26.3 26.4 18.7 12.1

ROE (%) 17.1 14.6 18.0 23.6

52-WEEK PRICE (CNY)

Source: Thomson Reuters IBES, HSBC estimates

Zhijie Zhao* Analyst, Healthcare

The Hongkong and Shanghai Banking Corporation Limited

+852 2996 6591

Yumeng Wang* Analyst, Healthcare

The Hongkong and Shanghai Banking Corporation Limited

+852 2996 6586

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations

Beijing SL Pharmaceutical (002038 CH)

EQUITIES PHARMACEUTICALS

China

17.00

35.00

53.00

May 15 Nov 15 May 16

Target price: 36.40High: 48.87 Low: 21.34 Current: 29.21

Buy: Generic Lenalidomide getting closer to approval

EQUITIES PHARMACEUTICALS

5 May 2016

2

Financials & valuation

Financial statements

Year to 12/2015a 12/2016e 12/2017e 12/2018e

Profit & loss summary (CNYm)

Revenue 1,157 1,232 1,680 2,366

EBITDA 682 671 926 1,389

Depreciation & amortisation -33 -43 -48 -55

Operating profit/EBIT 649 628 878 1,335

Net interest 20 20 25 34

PBT 670 648 902 1,369

HSBC PBT 670 648 902 1,369

Taxation -92 -91 -126 -192

Net profit 576 554 772 1,191

HSBC net profit 576 554 772 1,191

Cash flow summary (CNYm)

Cash flow from operations 505 673 819 853

Capex -130 -184 -236 -170

Cash flow from investment 244 -184 -236 -170

Dividends -137 -132 -184 -284

Change in net debt -613 -301 -420 -415

FCF equity 1,209 350 499 687

Balance sheet summary (CNYm)

Intangible fixed assets 86 121 169 236

Tangible fixed assets 481 590 735 792

Current assets 2,674 2,910 3,336 4,152

Cash & others 1,470 1,771 2,191 2,605

Total assets 3,853 4,193 4,812 5,753

Operating liabilities 112 117 144 191

Gross debt 0 0 0 0

Net debt -1,470 -1,771 -2,191 -2,605

Shareholders' funds 3,578 4,000 4,588 5,495

Invested capital 1,660 1,733 1,906 2,385

Ratio, growth and per share analysis

Year to 12/2015a 12/2016e 12/2017e 12/2018e

Y-o-y % change

Revenue -7.0 6.5 36.4 40.8

EBITDA -16.9 -1.6 38.0 50.1

Operating profit -17.9 -3.4 39.8 52.1

PBT -17.6 -3.2 39.2 51.7

HSBC EPS -17.1 -3.8 39.2 54.4

Ratios (%)

Revenue/IC (x) 0.7 0.7 0.9 1.1

ROIC 32.4 32.2 41.9 54.1

ROE 17.1 14.6 18.0 23.6

ROA 15.7 13.4 16.8 21.7

EBITDA margin 59.0 54.5 55.1 58.7

Operating profit margin 56.2 51.0 52.2 56.4

EBITDA/net interest (x)

Net debt/equity -40.7 -43.9 -47.3 -47.2

Net debt/EBITDA (x) -2.2 -2.6 -2.4 -1.9

CF from operations/net debt

Per share data (CNY)

EPS reported (diluted) 0.84 0.81 1.13 1.74

HSBC EPS (diluted) 0.84 0.81 1.13 1.74

DPS 0.20 0.19 0.27 0.41

Book value 5.22 5.84 6.69 8.02

Key forecast drivers

Year to 12/2015a 12/2016e 12/2017e 12/2018e

Biocoen sales 720 670 671 0

Arsenic trioxide 37 93 157 0

Lenalidomide 0 10 310 0

Valuation data

Year to 12/2015a 12/2016e 12/2017e 12/2018e

EV/sales 15.5 14.4 10.3 7.1

EV/EBITDA 26.3 26.4 18.7 12.1

EV/IC 10.8 10.2 9.1 7.1

PE* 34.7 36.1 25.9 16.8

PB 5.6 5.0 4.4 3.6

FCF yield (%) 6.2 1.8 2.6 3.5

Dividend yield (%) 0.7 0.7 0.9 1.4

* Based on HSBC EPS (diluted)

Price relative

Source: HSBC Note: Priced at close of 04 May 2016

12.00

17.00

22.00

27.00

32.00

37.00

42.00

47.00

52.00

12.00

17.00

22.00

27.00

32.00

37.00

42.00

47.00

52.00

2014 2015 2016 2017Beijing SL Pharmaceutical Rel to CSI 300 Index

In this document HSBC may comment on the potential economic impact dependent on the outcome of the UK Referendum.

HSBC is not taking a political position and this document and the information contained herein are not intended to promote or

procure, or otherwise be in connection with promoting or procuring, a particular outcome in relation to the question asked in

the UK Referendum.

Disclaimer & Disclosures

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

View HSBC Global Research at:

https://www.research.hsbc.com

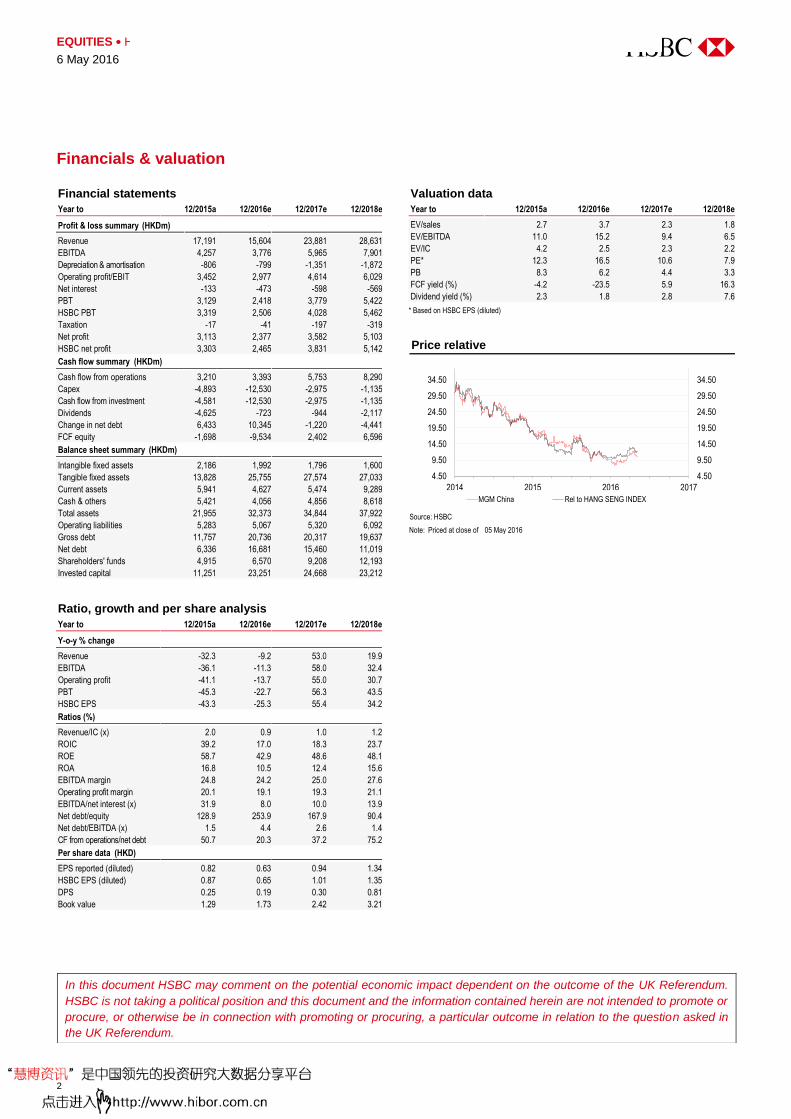

1Q16 was in-line but dampened by unfavorable luck

Cotai construction should be completed in October/November

and continues to target 1Q17 opening

Maintain Buy rating and unchanged target price of HKD14.2

Results highlights: Property EBITDA came in at USD128m (-11%qoq or -23%yoy),

largely in line with HSBCe/consensus estimate. After two quarters of sequential

improvement, margin came off 1.8ppt qoq. Margin was dragged by: 1) unfavorable

luck for in-house VIP and premium mass; 2) lack of bad debt reversal (vs 4Q15) and

3) gaming mix change. Excluding bad debt reversal and adjusting for luck, EBITDA

would have been flat qoq. By segment:

VIP tracked industry growth: VIP volume was down 2%qoq, largely in line with

industry junket volume drop. Revenue was -2%qoq too as win rate was flat qoq

despite the fact that direct VIP did not hold as well.

Mass was dragged by luck: Poor hold in premium mass dampened overall

mass performance. After strong growth in 4Q15, mass revenue was -4%qoq,

underperforming market at large, which grew +3% in the same period. Slot also

saw a weak quarter, -14%qoq, yielding 12% market share vs 14% in 4Q15.

Non-gaming faced keener competition: RevPAR was down 10% qoq on both

lower room rates and occupancy, likely impacted by new hotel room supply in Cotai.

Looking ahead: Management was upbeat about the May Golden Week period. On

newsflow about potential ban of phone betting (Bloomberg, 4 May), the company

expects the government to clarify in the next few days but sees little impact given

86% of their EBITDA is from mass segment. MGM targets to complete construction

of Cotai in late-Oct or early-Nov and continues to aim for 1Q17 opening, subject to

government approval. The company expects to shift 500 full time employees from

existing properties, which would result in 25-30bps improvement in margin.

Maintain Buy with unchanged TP of HKD14.2: MGM continues to remain one of

our preferred stocks in the space due to its valuation and attractive risk/reward

profile. Trading at 10% and 30% discount to sector, based on FY17e EV/EBITDA and

P/E, we believe the Cotai project has barely been priced in. We make no changes to

our forecast and maintain our SoTP target price of HKD14.20. With 33% upside to

our TP, we reiterate Buy rating on MGM China.

FLASHNOTE

6 May 2016

MAINTAIN BUY

TARGET PRICE (HKD) PREVIOUS TARGET (HKD)

14.20

SHARE PRICE (HKD) UPSIDE/DOWNSIDE

10.68 +33.0% (as of 05 May 2016)

MARKET DATA Market cap (HKDm) 40,584 Free float 22%

Market cap (USDm) 5,229 BBG 2282 HK

3m ADTV (USDm) 8.66 RIC 2282.HK

FINANCIALS AND RATIOS (HKD) Year to 12/2015a 12/2016e 12/2017e 12/2018e

HSBC EPS 0.87 0.65 1.01 1.35

HSBC EPS (prev) - - - -

Change (%) - - - -

Consensus EPS 0.82 0.62 0.67 0.99

PE (x) 12.3 16.5 10.6 7.9

Dividend yield (%) 2.3 1.8 2.8 7.6

EV/EBITDA (x) 11.0 15.2 9.4 6.5

ROE (%) 58.7 42.9 48.6 48.1

52-WEEK PRICE (HKD)

Source: Thomson Reuters IBES, HSBC estimates

Scott Chan* Analyst

The Hongkong and Shanghai Banking Corporation Limited

+852 3941 7005

Erwan Rambourg* Global Co-Head of Consumer & Retail Research The Hongkong and Shanghai Banking Corporation Limited

+852 2996 6572

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations

MGM China (2282 HK) EQUITIES HOTELS RESTAURANTS & LEISURE

Hong Kong

6.60

12.80

19.00

May 15 Nov 15 May 16

Target price: 14.20 High: 17.44 Low: 7.84 Current: 10.68

Buy: 1Q16 in line; Cotai continues to target 1Q17

EQUITIES HOTELS RESTAURANTS & LEISURE

6 May 2016

2

Financials & valuation

Financial statements

Year to 12/2015a 12/2016e 12/2017e 12/2018e

Profit & loss summary (HKDm)

Revenue 17,191 15,604 23,881 28,631

EBITDA 4,257 3,776 5,965 7,901

Depreciation & amortisation -806 -799 -1,351 -1,872

Operating profit/EBIT 3,452 2,977 4,614 6,029

Net interest -133 -473 -598 -569

PBT 3,129 2,418 3,779 5,422

HSBC PBT 3,319 2,506 4,028 5,462

Taxation -17 -41 -197 -319

Net profit 3,113 2,377 3,582 5,103

HSBC net profit 3,303 2,465 3,831 5,142

Cash flow summary (HKDm)

Cash flow from operations 3,210 3,393 5,753 8,290

Capex -4,893 -12,530 -2,975 -1,135

Cash flow from investment -4,581 -12,530 -2,975 -1,135

Dividends -4,625 -723 -944 -2,117

Change in net debt 6,433 10,345 -1,220 -4,441

FCF equity -1,698 -9,534 2,402 6,596

Balance sheet summary (HKDm)

Intangible fixed assets 2,186 1,992 1,796 1,600

Tangible fixed assets 13,828 25,755 27,574 27,033

Current assets 5,941 4,627 5,474 9,289

Cash & others 5,421 4,056 4,856 8,618

Total assets 21,955 32,373 34,844 37,922

Operating liabilities 5,283 5,067 5,320 6,092

Gross debt 11,757 20,736 20,317 19,637

Net debt 6,336 16,681 15,460 11,019

Shareholders' funds 4,915 6,570 9,208 12,193

Invested capital 11,251 23,251 24,668 23,212

Ratio, growth and per share analysis

Year to 12/2015a 12/2016e 12/2017e 12/2018e

Y-o-y % change

Revenue -32.3 -9.2 53.0 19.9

EBITDA -36.1 -11.3 58.0 32.4

Operating profit -41.1 -13.7 55.0 30.7

PBT -45.3 -22.7 56.3 43.5

HSBC EPS -43.3 -25.3 55.4 34.2

Ratios (%)

Revenue/IC (x) 2.0 0.9 1.0 1.2

ROIC 39.2 17.0 18.3 23.7

ROE 58.7 42.9 48.6 48.1

ROA 16.8 10.5 12.4 15.6

EBITDA margin 24.8 24.2 25.0 27.6

Operating profit margin 20.1 19.1 19.3 21.1

EBITDA/net interest (x) 31.9 8.0 10.0 13.9

Net debt/equity 128.9 253.9 167.9 90.4

Net debt/EBITDA (x) 1.5 4.4 2.6 1.4

CF from operations/net debt 50.7 20.3 37.2 75.2

Per share data (HKD)

EPS reported (diluted) 0.82 0.63 0.94 1.34

HSBC EPS (diluted) 0.87 0.65 1.01 1.35

DPS 0.25 0.19 0.30 0.81

Book value 1.29 1.73 2.42 3.21

Valuation data

Year to 12/2015a 12/2016e 12/2017e 12/2018e

EV/sales 2.7 3.7 2.3 1.8

EV/EBITDA 11.0 15.2 9.4 6.5

EV/IC 4.2 2.5 2.3 2.2

PE* 12.3 16.5 10.6 7.9

PB 8.3 6.2 4.4 3.3

FCF yield (%) -4.2 -23.5 5.9 16.3

Dividend yield (%) 2.3 1.8 2.8 7.6

* Based on HSBC EPS (diluted)

Price relative

Source: HSBC Note: Priced at close of 05 May 2016

4.50

9.50

14.50

19.50

24.50

29.50

34.50

4.50

9.50

14.50

19.50

24.50

29.50

34.50

2014 2015 2016 2017

MGM China Rel to HANG SENG INDEX

In this document HSBC may comment on the potential economic impact dependent on the outcome of the UK Referendum.

HSBC is not taking a political position and this document and the information contained herein are not intended to promote or

procure, or otherwise be in connection with promoting or procuring, a particular outcome in relation to the question asked in

the UK Referendum.

Disclaimer & Disclosures

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

View HSBC Global Research at:

https://www.research.hsbc.com

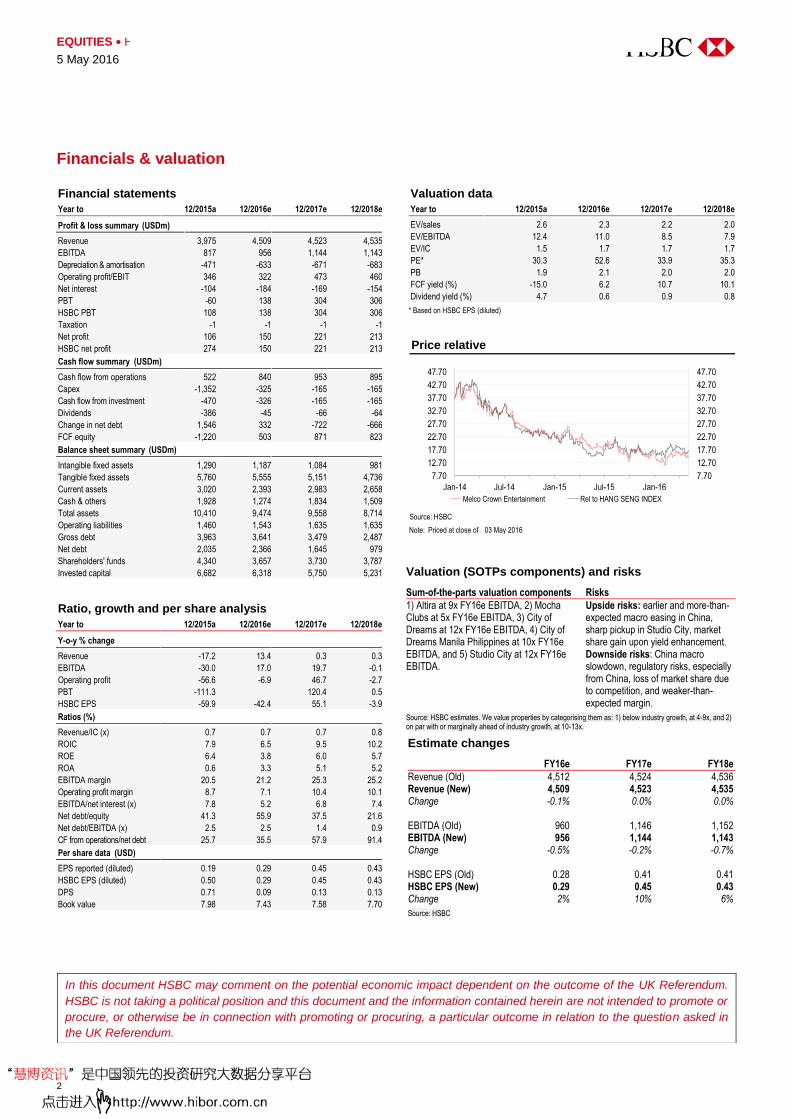

Bad debt provision at Altira offset favourable win rate impact

MPEL to repurchase 9.5% of its shares from Crown Resorts

Maintain Hold and raise TP to USD16.6 from USD16.5

Results highlight: Property EBITDA in 1Q16 was USD249m (+6% qoq, flat yoy),

largely in line with consensus estimates and HSBCe. Favourable win rate boosted

EBITDA by USD15m but the impact was offset by a USD18m bad debt provision at

Altira. Excluding these, EBITDA would have been flat qoq. Per management, it has