Embed Size (px)

Citation preview

1

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

Japan Retail Fund Investment Corporation (Tokyo Stock Exchange Company Code: 8953) News Release – September 11, 2012

Japan Retail Fund Investment Corporation to Acquire 7 Properties in Japan

The Japan Retail Fund Investment Corporation ("JRF") announced today its planned acquisition of real estate and real estate trust beneficiary rights in Japan (hereinafter referred to as “properties to be acquired”) as outlined below.

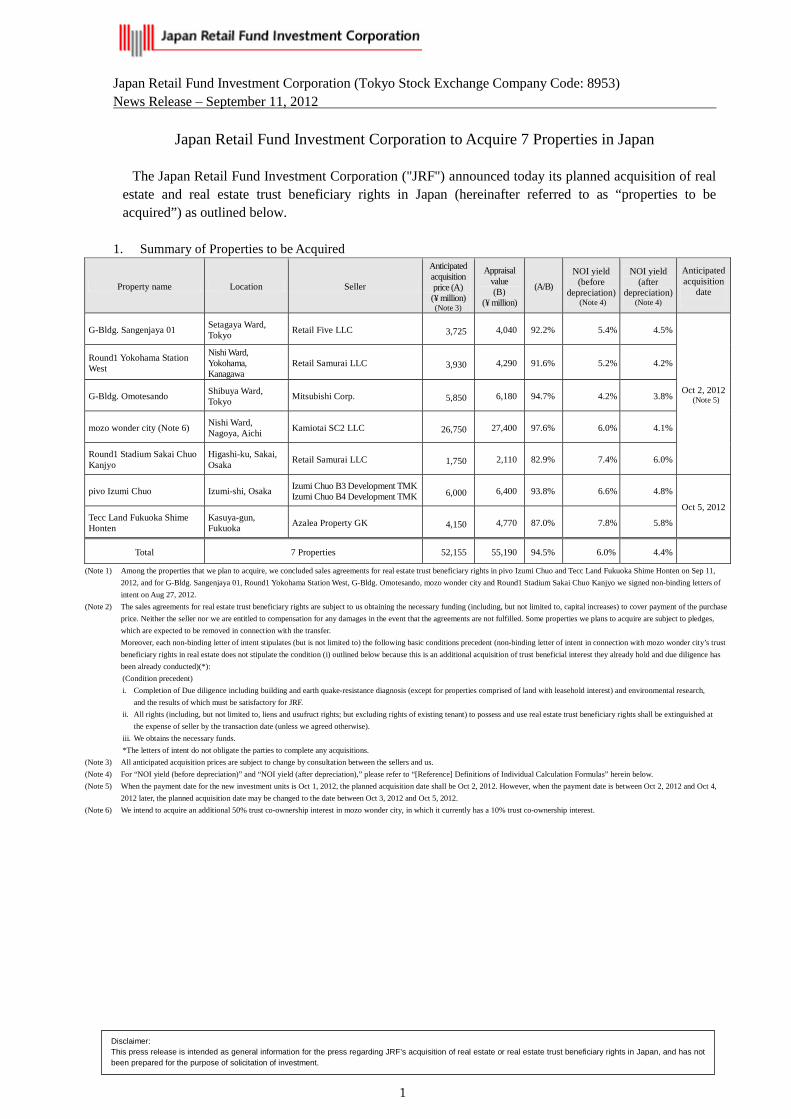

1. Summary of Properties to be Acquired

Property name Location Seller

Anticipated acquisition price (A) (¥ million) (Note 3)

Appraisal value (B)

(¥ million)

(A/B)

NOI yield (before

depreciation) (Note 4)

NOI yield (after

depreciation)

(Note 4)

Anticipated acquisition

date

G-Bldg. Sangenjaya 01 Setagaya Ward, Tokyo Retail Five LLC 3,725 4,040 92.2% 5.4% 4.5%

Oct 2, 2012 (Note 5)

Round1 Yokohama Station West

Nishi Ward, Yokohama, Kanagawa

Retail Samurai LLC 3,930 4,290 91.6% 5.2% 4.2%

G-Bldg. Omotesando Shibuya Ward, Tokyo Mitsubishi Corp. 5,850 6,180 94.7% 4.2% 3.8%

mozo wonder city (Note 6) Nishi Ward, Nagoya, Aichi Kamiotai SC2 LLC 26,750 27,400 97.6% 6.0% 4.1%

Round1 Stadium Sakai Chuo Kanjyo

Higashi-ku, Sakai, Osaka Retail Samurai LLC 1,750 2,110 82.9% 7.4% 6.0%

pivo Izumi Chuo Izumi-shi, Osaka Izumi Chuo B3 Development TMK Izumi Chuo B4 Development TMK 6,000 6,400 93.8% 6.6% 4.8%

Oct 5, 2012 Tecc Land Fukuoka Shime Honten

Kasuya-gun, Fukuoka Azalea Property GK 4,150 4,770 87.0% 7.8% 5.8%

Total 7 Properties 52,155 55,190 94.5% 6.0% 4.4%

(Note 1) Among the properties that we plan to acquire, we concluded sales agreements for real estate trust beneficiary rights in pivo Izumi Chuo and Tecc Land Fukuoka Shime Honten on Sep 11, 2012, and for G-Bldg. Sangenjaya 01, Round1 Yokohama Station West, G-Bldg. Omotesando, mozo wonder city and Round1 Stadium Sakai Chuo Kanjyo we signed non-binding letters of intent on Aug 27, 2012.

(Note 2) The sales agreements for real estate trust beneficiary rights are subject to us obtaining the necessary funding (including, but not limited to, capital increases) to cover payment of the purchase price. Neither the seller nor we are entitled to compensation for any damages in the event that the agreements are not fulfilled. Some properties we plans to acquire are subject to pledges, which are expected to be removed in connection with the transfer. Moreover, each non-binding letter of intent stipulates (but is not limited to) the following basic conditions precedent (non-binding letter of intent in connection with mozo wonder city’s trust beneficiary rights in real estate does not stipulate the condition (i) outlined below because this is an additional acquisition of trust beneficial interest they already hold and due diligence has been already conducted)(*): (Condition precedent) i. Completion of Due diligence including building and earth quake-resistance diagnosis (except for properties comprised of land with leasehold interest) and environmental research,

and the results of which must be satisfactory for JRF. ii. All rights (including, but not limited to, liens and usufruct rights; but excluding rights of existing tenant) to possess and use real estate trust beneficiary rights shall be extinguished at

the expense of seller by the transaction date (unless we agreed otherwise). iii. We obtains the necessary funds. *The letters of intent do not obligate the parties to complete any acquisitions.

(Note 3) All anticipated acquisition prices are subject to change by consultation between the sellers and us. (Note 4) For “NOI yield (before depreciation)” and “NOI yield (after depreciation),” please refer to “[Reference] Definitions of Individual Calculation Formulas” herein below. (Note 5) When the payment date for the new investment units is Oct 1, 2012, the planned acquisition date shall be Oct 2, 2012. However, when the payment date is between Oct 2, 2012 and Oct 4,

2012 later, the planned acquisition date may be changed to the date between Oct 3, 2012 and Oct 5, 2012. (Note 6) We intend to acquire an additional 50% trust co-ownership interest in mozo wonder city, in which it currently has a 10% trust co-ownership interest.

2

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

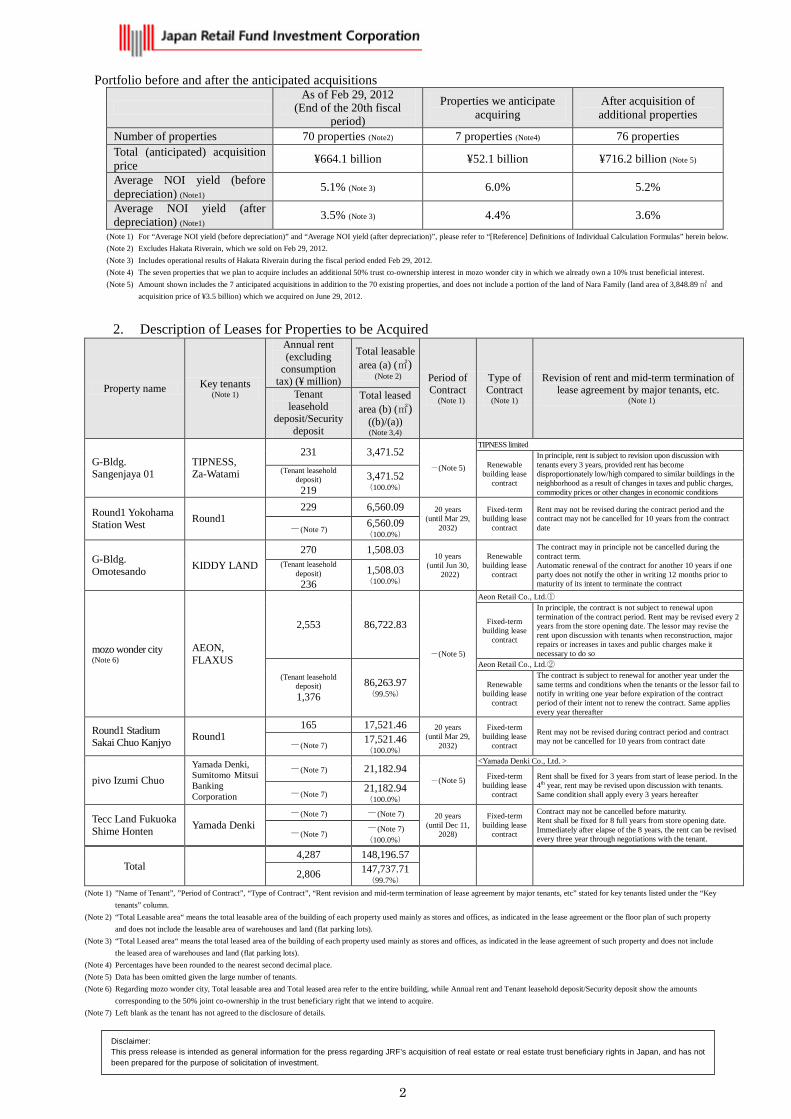

Portfolio before and after the anticipated acquisitions

As of Feb 29, 2012

(End of the 20th fiscal period)

Properties we anticipate acquiring

After acquisition of additional properties

Number of properties 70 properties (Note2) 7 properties (Note4) 76 properties Total (anticipated) acquisition price ¥664.1 billion ¥52.1 billion ¥716.2 billion (Note 5)

Average NOI yield (before depreciation) (Note1) 5.1% (Note 3) 6.0% 5.2%

Average NOI yield (after depreciation) (Note1) 3.5% (Note 3) 4.4% 3.6%

(Note 1) For “Average NOI yield (before depreciation)” and “Average NOI yield (after depreciation)”, please refer to “[Reference] Definitions of Individual Calculation Formulas” herein below. (Note 2) Excludes Hakata Riverain, which we sold on Feb 29, 2012. (Note 3) Includes operational results of Hakata Riverain during the fiscal period ended Feb 29, 2012. (Note 4) The seven properties that we plan to acquire includes an additional 50% trust co-ownership interest in mozo wonder city in which we already own a 10% trust beneficial interest. (Note 5) Amount shown includes the 7 anticipated acquisitions in addition to the 70 existing properties, and does not include a portion of the land of Nara Family (land area of 3,848.89㎡ and

acquisition price of ¥3.5 billion) which we acquired on June 29, 2012.

2. Description of Leases for Properties to be Acquired

Property name Key tenants (Note 1)

Annual rent (excluding

consumption tax) (¥ million)

Total leasable area (a) (㎡)

(Note 2) Period of Contract

(Note 1)

Type of Contract

(Note 1)

Revision of rent and mid-term termination of lease agreement by major tenants, etc.

(Note 1) Tenant

leasehold deposit/Security

deposit

Total leased area (b) (㎡)

((b)/(a)) (Note 3,4)

G-Bldg. Sangenjaya 01

TIPNESS, Za-Watami

231 3,471.52 -(Note 5)

TIPNESS limited

Renewable building lease

contract

In principle, rent is subject to revision upon discussion with tenants every 3 years, provided rent has become disproportionately low/high compared to similar buildings in the neighborhood as a result of changes in taxes and public charges, commodity prices or other changes in economic conditions

(Tenant leasehold deposit) 219

3,471.52 (100.0%)

Round1 Yokohama Station West Round1

229 6,560.09 20 years (until Mar 29,

2032)

Fixed-term building lease

contract

Rent may not be revised during the contract period and the contract may not be cancelled for 10 years from the contract date -(Note 7) 6,560.09

(100.0%)

G-Bldg. Omotesando KIDDY LAND

270 1,508.03 10 years

(until Jun 30, 2022)

Renewable building lease

contract

The contract may in principle not be cancelled during the contract term. Automatic renewal of the contract for another 10 years if one party does not notify the other in writing 12 months prior to maturity of its intent to terminate the contract

(Tenant leasehold deposit) 236

1,508.03 (100.0%)

mozo wonder city (Note 6)

AEON, FLAXUS

2,553 86,722.83

-(Note 5)

Aeon Retail Co., Ltd.①

Fixed-term building lease

contract

In principle, the contract is not subject to renewal upon termination of the contract period. Rent may be revised every 2 years from the store opening date. The lessor may revise the rent upon discussion with tenants when reconstruction, major repairs or increases in taxes and public charges make it necessary to do so

(Tenant leasehold deposit) 1,376

86,263.97 (99.5%)

Aeon Retail Co., Ltd.②

Renewable building lease

contract

The contract is subject to renewal for another year under the same terms and conditions when the tenants or the lessor fail to notify in writing one year before expiration of the contract period of their intent not to renew the contract. Same applies every year thereafter

Round1 Stadium Sakai Chuo Kanjyo Round1

165 17,521.46 20 years (until Mar 29,

2032)

Fixed-term building lease

contract

Rent may not be revised during contract period and contract may not be cancelled for 10 years from contract date -(Note 7) 17,521.46

(100.0%)

pivo Izumi Chuo Yamada Denki, Sumitomo Mitsui Banking Corporation

-(Note 7) 21,182.94 -(Note 5)

<Yamada Denki Co., Ltd. >

Fixed-term building lease

contract

Rent shall be fixed for 3 years from start of lease period. In the 4th year, rent may be revised upon discussion with tenants. Same condition shall apply every 3 years hereafter -(Note 7) 21,182.94

(100.0%)

Tecc Land Fukuoka Shime Honten Yamada Denki

-(Note 7) -(Note 7) 20 years (until Dec 11,

2028)

Fixed-term building lease

contract

Contract may not be cancelled before maturity. Rent shall be fixed for 8 full years from store opening date. Immediately after elapse of the 8 years, the rent can be revised every three year through negotiations with the tenant. -(Note 7) -(Note 7)

(100.0%)

Total 4,287 148,196.57

2,806 147,737.71 (99.7%)

(Note 1) ”Name of Tenant”, ”Period of Contract”, “Type of Contract”, “Rent revision and mid-term termination of lease agreement by major tenants, etc” stated for key tenants listed under the “Key tenants” column.

(Note 2) “Total Leasable area“ means the total leasable area of the building of each property used mainly as stores and offices, as indicated in the lease agreement or the floor plan of such property and does not include the leasable area of warehouses and land (flat parking lots).

(Note 3) “Total Leased area“ means the total leased area of the building of each property used mainly as stores and offices, as indicated in the lease agreement of such property and does not include the leased area of warehouses and land (flat parking lots).

(Note 4) Percentages have been rounded to the nearest second decimal place. (Note 5) Data has been omitted given the large number of tenants. (Note 6) Regarding mozo wonder city, Total leasable area and Total leased area refer to the entire building, while Annual rent and Tenant leasehold deposit/Security deposit show the amounts

corresponding to the 50% joint co-ownership in the trust beneficiary right that we intend to acquire. (Note 7) Left blank as the tenant has not agreed to the disclosure of details.

3

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

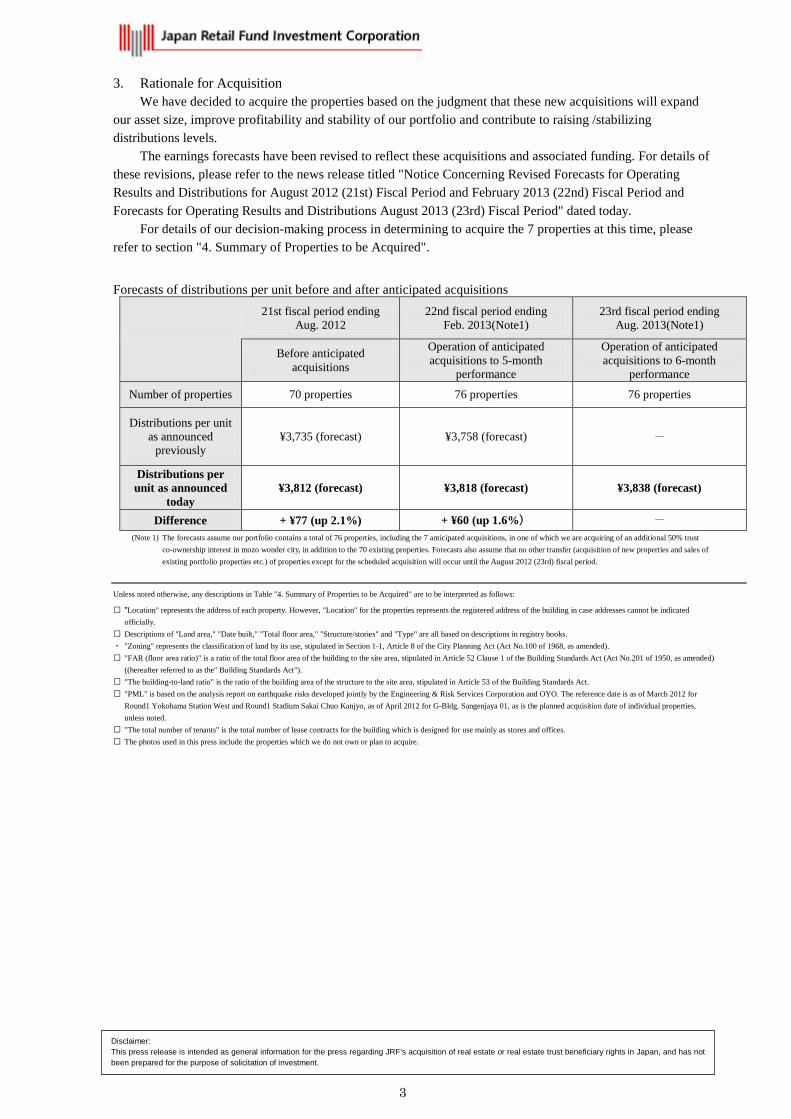

3. Rationale for Acquisition We have decided to acquire the properties based on the judgment that these new acquisitions will expand

our asset size, improve profitability and stability of our portfolio and contribute to raising /stabilizing distributions levels.

The earnings forecasts have been revised to reflect these acquisitions and associated funding. For details of these revisions, please refer to the news release titled "Notice Concerning Revised Forecasts for Operating Results and Distributions for August 2012 (21st) Fiscal Period and February 2013 (22nd) Fiscal Period and Forecasts for Operating Results and Distributions August 2013 (23rd) Fiscal Period" dated today.

For details of our decision-making process in determining to acquire the 7 properties at this time, please refer to section "4. Summary of Properties to be Acquired".

Forecasts of distributions per unit before and after anticipated acquisitions

21st fiscal period ending Aug. 2012

22nd fiscal period ending Feb. 2013(Note1)

23rd fiscal period ending Aug. 2013(Note1)

Before anticipated acquisitions

Operation of anticipated acquisitions to 5-month

performance

Operation of anticipated acquisitions to 6-month

performance

Number of properties 70 properties 76 properties 76 properties

Distributions per unit as announced

previously ¥3,735 (forecast) ¥3,758 (forecast) -

Distributions per unit as announced

today ¥3,812 (forecast) ¥3,818 (forecast) ¥3,838 (forecast)

Difference + ¥77 (up 2.1%) + ¥60 (up 1.6%) - (Note 1) The forecasts assume our portfolio contains a total of 76 properties, including the 7 anticipated acquisitions, in one of which we are acquiring of an additional 50% trust

co-ownership interest in mozo wonder city, in addition to the 70 existing properties. Forecasts also assume that no other transfer (acquisition of new properties and sales of existing portfolio properties etc.) of properties except for the scheduled acquisition will occur until the August 2012 (23rd) fiscal period.

Unless noted otherwise, any descriptions in Table "4. Summary of Properties to be Acquired" are to be interpreted as follows:

"Location" represents the address of each property. However, "Location" for the properties represents the registered address of the building in case addresses cannot be indicated officially.

Descriptions of "Land area," "Date built," "Total floor area," "Structure/stories" and "Type" are all based on descriptions in registry books. ・ "Zoning" represents the classification of land by its use, stipulated in Section 1-1, Article 8 of the City Planning Act (Act No.100 of 1968, as amended). "FAR (floor area ratio)" is a ratio of the total floor area of the building to the site area, stipulated in Article 52 Clause 1 of the Building Standards Act (Act No.201 of 1950, as amended)

((hereafter referred to as the" Building Standards Act"). "The building-to-land ratio" is the ratio of the building area of the structure to the site area, stipulated in Article 53 of the Building Standards Act. "PML" is based on the analysis report on earthquake risks developed jointly by the Engineering & Risk Services Corporation and OYO. The reference date is as of March 2012 for

Round1 Yokohama Station West and Round1 Stadium Sakai Chuo Kanjyo, as of April 2012 for G-Bldg. Sangenjaya 01, as is the planned acquisition date of individual properties, unless noted.

"The total number of tenants" is the total number of lease contracts for the building which is designed for use mainly as stores and offices. The photos used in this press include the properties which we do not own or plan to acquire.

4

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

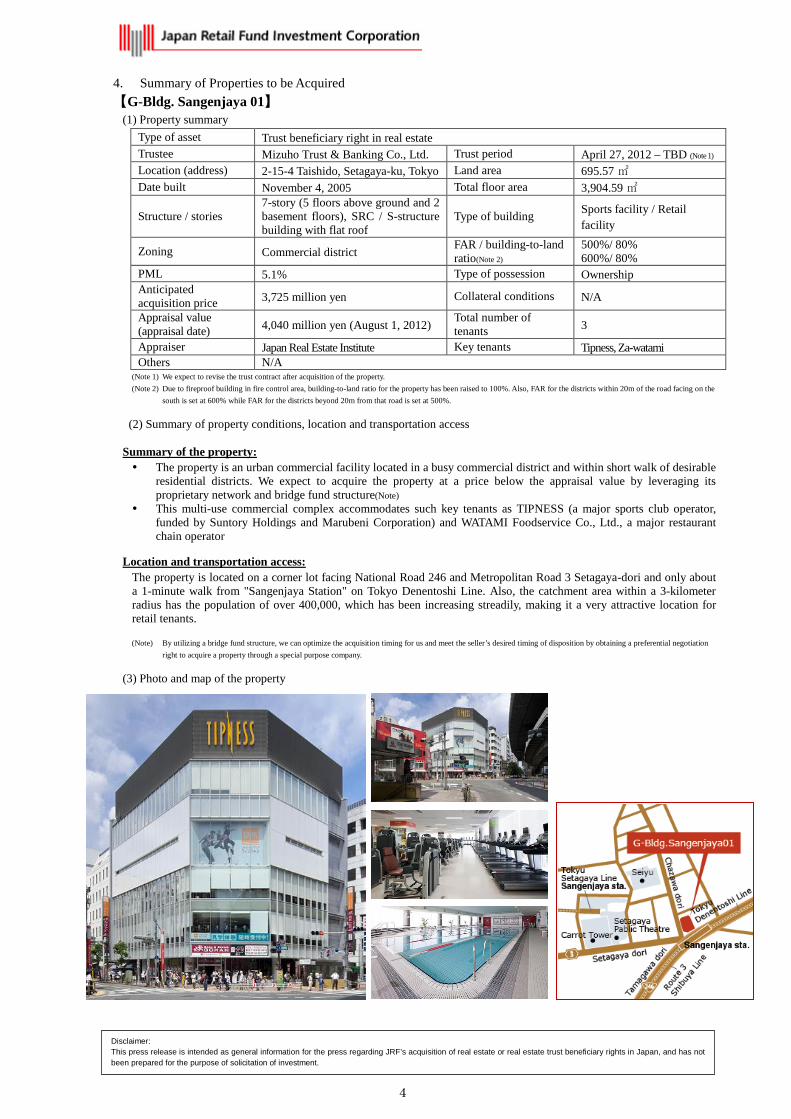

4. Summary of Properties to be Acquired 【G-Bldg. Sangenjaya 01】

(1) Property summary Type of asset Trust beneficiary right in real estate Trustee Mizuho Trust & Banking Co., Ltd. Trust period April 27, 2012 – TBD (Note 1) Location (address) 2-15-4 Taishido, Setagaya-ku, Tokyo Land area 695.57 ㎡ Date built November 4, 2005 Total floor area 3,904.59 ㎡

Structure / stories 7-story (5 floors above ground and 2 basement floors), SRC / S-structure building with flat roof

Type of building Sports facility / Retail facility

Zoning Commercial district FAR / building-to-land ratio(Note 2)

500%/ 80% 600%/ 80%

PML 5.1% Type of possession Ownership Anticipated acquisition price 3,725 million yen Collateral conditions N/A

Appraisal value (appraisal date) 4,040 million yen (August 1, 2012) Total number of

tenants 3

Appraiser Japan Real Estate Institute Key tenants Tipness, Za-watami Others N/A

(Note 1) We expect to revise the trust contract after acquisition of the property. (Note 2) Due to fireproof building in fire control area, building-to-land ratio for the property has been raised to 100%. Also, FAR for the districts within 20m of the road facing on the

south is set at 600% while FAR for the districts beyond 20m from that road is set at 500%.

(2) Summary of property conditions, location and transportation access

Summary of the property: The property is an urban commercial facility located in a busy commercial district and within short walk of desirable

residential districts. We expect to acquire the property at a price below the appraisal value by leveraging its proprietary network and bridge fund structure(Note)

This multi-use commercial complex accommodates such key tenants as TIPNESS (a major sports club operator, funded by Suntory Holdings and Marubeni Corporation) and WATAMI Foodservice Co., Ltd., a major restaurant chain operator

Location and transportation access: The property is located on a corner lot facing National Road 246 and Metropolitan Road 3 Setagaya-dori and only about a 1-minute walk from "Sangenjaya Station" on Tokyo Denentoshi Line. Also, the catchment area within a 3-kilometer radius has the population of over 400,000, which has been increasing streadily, making it a very attractive location for retail tenants. (Note) By utilizing a bridge fund structure, we can optimize the acquisition timing for us and meet the seller’s desired timing of disposition by obtaining a preferential negotiation

right to acquire a property through a special purpose company.

(3) Photo and map of the property

5

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

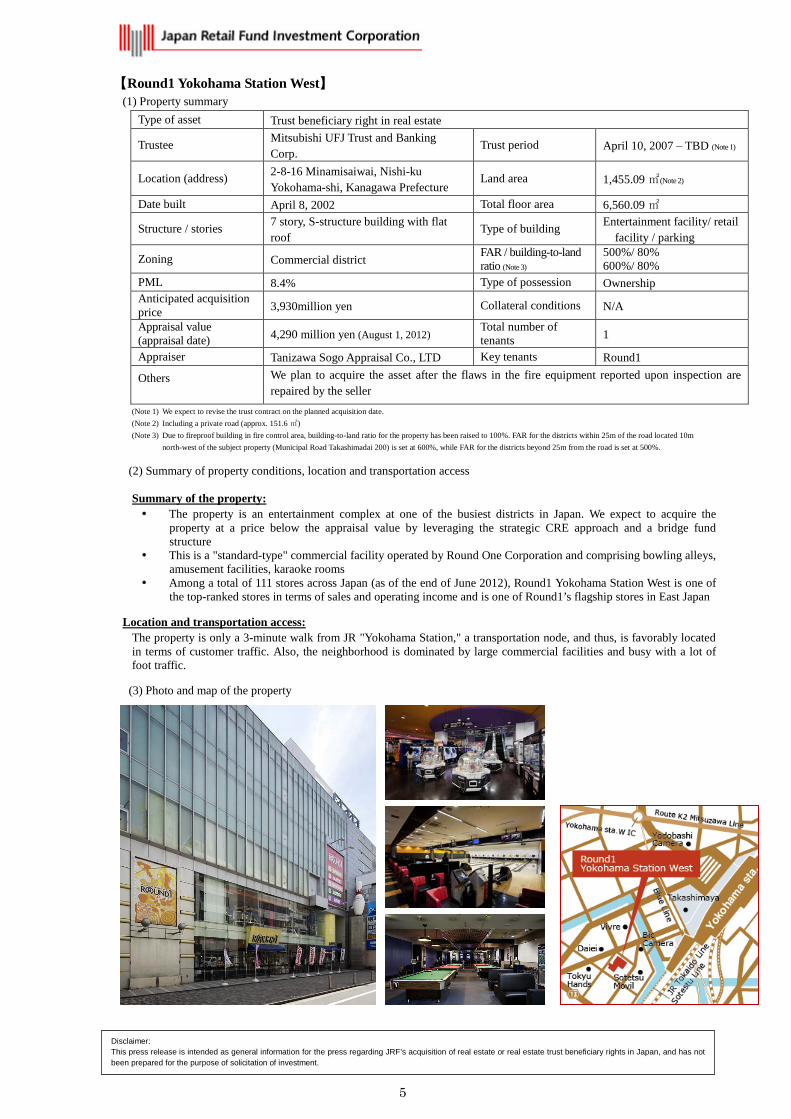

【Round1 Yokohama Station West】 (1) Property summary

Type of asset Trust beneficiary right in real estate

Trustee Mitsubishi UFJ Trust and Banking Corp.

Trust period April 10, 2007 – TBD (Note 1)

Location (address) 2-8-16 Minamisaiwai, Nishi-ku Yokohama-shi, Kanagawa Prefecture

Land area 1,455.09 ㎡(Note 2)

Date built April 8, 2002 Total floor area 6,560.09 ㎡

Structure / stories 7 story, S-structure building with flat roof

Type of building Entertainment facility/ retail facility / parking

Zoning Commercial district FAR / building-to-land ratio (Note 3)

500%/ 80% 600%/ 80%

PML 8.4% Type of possession Ownership Anticipated acquisition price 3,930million yen Collateral conditions N/A

Appraisal value (appraisal date) 4,290 million yen (August 1, 2012) Total number of

tenants 1

Appraiser Tanizawa Sogo Appraisal Co., LTD Key tenants Round1

Others

We plan to acquire the asset after the flaws in the fire equipment reported upon inspection are repaired by the seller

(Note 1) We expect to revise the trust contract on the planned acquisition date. (Note 2) Including a private road (approx. 151.6 ㎡) (Note 3) Due to fireproof building in fire control area, building-to-land ratio for the property has been raised to 100%. FAR for the districts within 25m of the road located 10m

north-west of the subject property (Municipal Road Takashimadai 200) is set at 600%, while FAR for the districts beyond 25m from the road is set at 500%.

(2) Summary of property conditions, location and transportation access

Summary of the property: The property is an entertainment complex at one of the busiest districts in Japan. We expect to acquire the

property at a price below the appraisal value by leveraging the strategic CRE approach and a bridge fund structure

This is a "standard-type" commercial facility operated by Round One Corporation and comprising bowling alleys, amusement facilities, karaoke rooms

Among a total of 111 stores across Japan (as of the end of June 2012), Round1 Yokohama Station West is one of the top-ranked stores in terms of sales and operating income and is one of Round1’s flagship stores in East Japan

Location and transportation access: The property is only a 3-minute walk from JR "Yokohama Station," a transportation node, and thus, is favorably located in terms of customer traffic. Also, the neighborhood is dominated by large commercial facilities and busy with a lot of foot traffic.

(3) Photo and map of the property

6

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

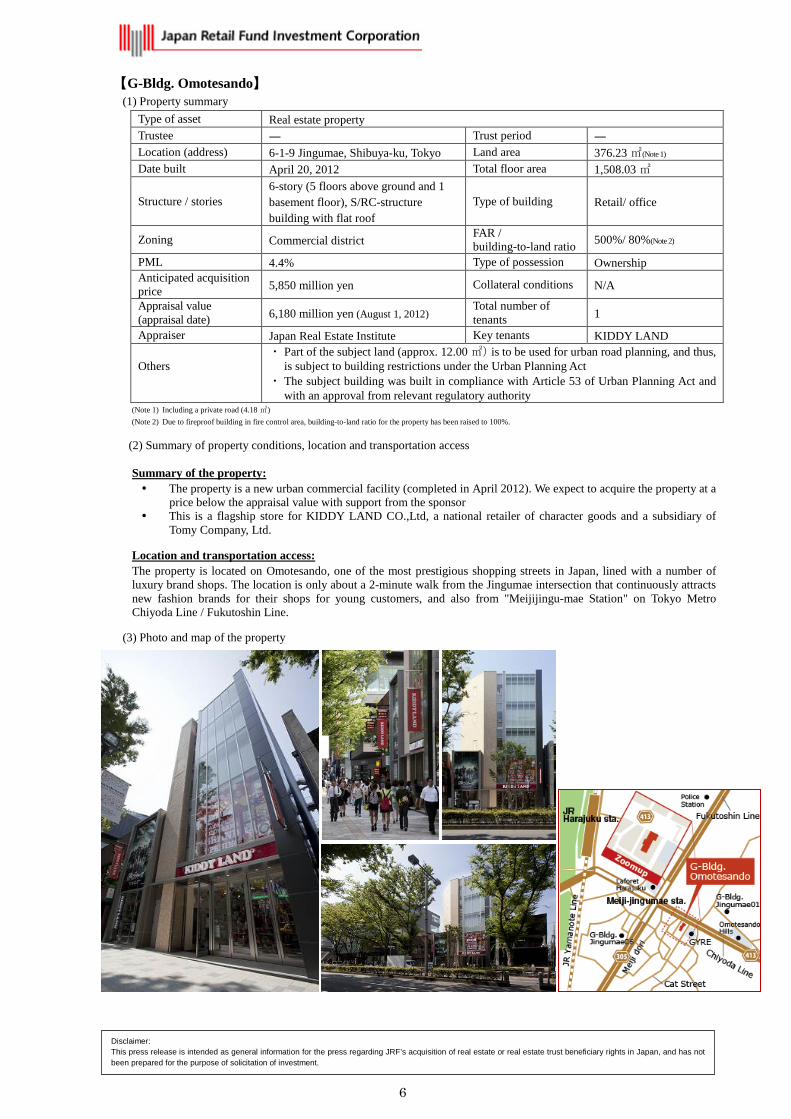

【G-Bldg. Omotesando】 (1) Property summary

Type of asset Real estate property Trustee ― Trust period ― Location (address) 6-1-9 Jingumae, Shibuya-ku, Tokyo Land area 376.23 ㎡(Note 1) Date built April 20, 2012 Total floor area 1,508.03 ㎡

Structure / stories 6-story (5 floors above ground and 1 basement floor), S/RC-structure building with flat roof

Type of building Retail/ office

Zoning Commercial district FAR / building-to-land ratio 500%/ 80%(Note 2)

PML 4.4% Type of possession Ownership Anticipated acquisition price 5,850 million yen Collateral conditions N/A

Appraisal value (appraisal date) 6,180 million yen (August 1, 2012) Total number of

tenants 1

Appraiser Japan Real Estate Institute Key tenants KIDDY LAND

Others

・ Part of the subject land (approx. 12.00 ㎡)is to be used for urban road planning, and thus, is subject to building restrictions under the Urban Planning Act

・ The subject building was built in compliance with Article 53 of Urban Planning Act and with an approval from relevant regulatory authority

(Note 1) Including a private road (4.18 ㎡) (Note 2) Due to fireproof building in fire control area, building-to-land ratio for the property has been raised to 100%.

(2) Summary of property conditions, location and transportation access

Summary of the property: The property is a new urban commercial facility (completed in April 2012). We expect to acquire the property at a

price below the appraisal value with support from the sponsor This is a flagship store for KIDDY LAND CO.,Ltd, a national retailer of character goods and a subsidiary of

Tomy Company, Ltd.

Location and transportation access: The property is located on Omotesando, one of the most prestigious shopping streets in Japan, lined with a number of luxury brand shops. The location is only about a 2-minute walk from the Jingumae intersection that continuously attracts new fashion brands for their shops for young customers, and also from "Meijijingu-mae Station" on Tokyo Metro Chiyoda Line / Fukutoshin Line.

(3) Photo and map of the property

7

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

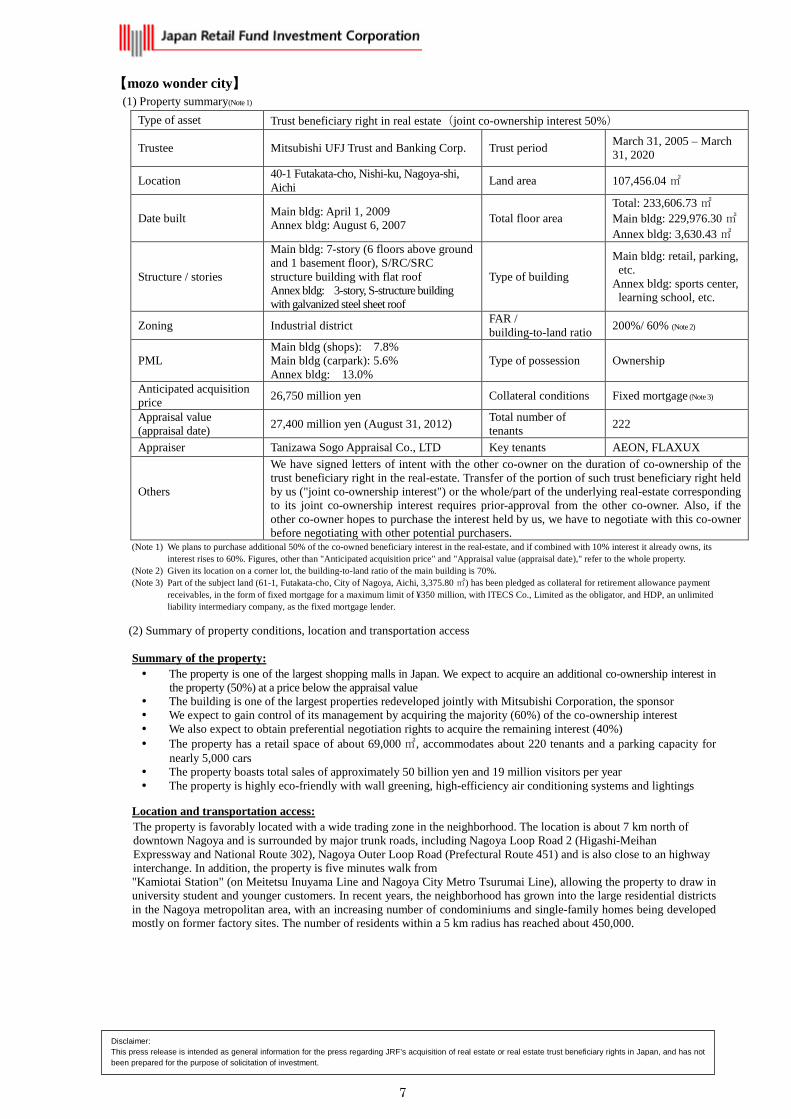

【mozo wonder city】 (1) Property summary(Note 1)

Type of asset Trust beneficiary right in real estate(joint co-ownership interest 50%)

Trustee Mitsubishi UFJ Trust and Banking Corp. Trust period March 31, 2005 – March 31, 2020

Location 40-1 Futakata-cho, Nishi-ku, Nagoya-shi, Aichi Land area 107,456.04 ㎡

Date built Main bldg: April 1, 2009 Annex bldg: August 6, 2007 Total floor area

Total: 233,606.73 ㎡ Main bldg: 229,976.30 ㎡ Annex bldg: 3,630.43 ㎡

Structure / stories

Main bldg: 7-story (6 floors above ground and 1 basement floor), S/RC/SRC structure building with flat roof Annex bldg: 3-story, S-structure building with galvanized steel sheet roof

Type of building

Main bldg: retail, parking, etc.

Annex bldg: sports center, learning school, etc.

Zoning Industrial district FAR / building-to-land ratio 200%/ 60% (Note 2)

PML Main bldg (shops): 7.8% Main bldg (carpark): 5.6% Annex bldg: 13.0%

Type of possession Ownership

Anticipated acquisition price 26,750 million yen Collateral conditions Fixed mortgage (Note 3)

Appraisal value (appraisal date) 27,400 million yen (August 31, 2012) Total number of

tenants 222

Appraiser Tanizawa Sogo Appraisal Co., LTD Key tenants AEON, FLAXUX

Others

We have signed letters of intent with the other co-owner on the duration of co-ownership of the trust beneficiary right in the real-estate. Transfer of the portion of such trust beneficiary right held by us ("joint co-ownership interest") or the whole/part of the underlying real-estate corresponding to its joint co-ownership interest requires prior-approval from the other co-owner. Also, if the other co-owner hopes to purchase the interest held by us, we have to negotiate with this co-owner before negotiating with other potential purchasers.

(Note 1) We plans to purchase additional 50% of the co-owned beneficiary interest in the real-estate, and if combined with 10% interest it already owns, its interest rises to 60%. Figures, other than "Anticipated acquisition price" and "Appraisal value (appraisal date)," refer to the whole property.

(Note 2) Given its location on a corner lot, the building-to-land ratio of the main building is 70%. (Note 3) Part of the subject land (61-1, Futakata-cho, City of Nagoya, Aichi, 3,375.80 ㎡) has been pledged as collateral for retirement allowance payment

receivables, in the form of fixed mortgage for a maximum limit of ¥350 million, with ITECS Co., Limited as the obligator, and HDP, an unlimited liability intermediary company, as the fixed mortgage lender.

(2) Summary of property conditions, location and transportation access

Summary of the property: The property is one of the largest shopping malls in Japan. We expect to acquire an additional co-ownership interest in

the property (50%) at a price below the appraisal value The building is one of the largest properties redeveloped jointly with Mitsubishi Corporation, the sponsor We expect to gain control of its management by acquiring the majority (60%) of the co-ownership interest We also expect to obtain preferential negotiation rights to acquire the remaining interest (40%) The property has a retail space of about 69,000 ㎡, accommodates about 220 tenants and a parking capacity for

nearly 5,000 cars The property boasts total sales of approximately 50 billion yen and 19 million visitors per year The property is highly eco-friendly with wall greening, high-efficiency air conditioning systems and lightings

Location and transportation access: The property is favorably located with a wide trading zone in the neighborhood. The location is about 7 km north of downtown Nagoya and is surrounded by major trunk roads, including Nagoya Loop Road 2 (Higashi-Meihan Expressway and National Route 302), Nagoya Outer Loop Road (Prefectural Route 451) and is also close to an highway interchange. In addition, the property is five minutes walk from "Kamiotai Station" (on Meitetsu Inuyama Line and Nagoya City Metro Tsurumai Line), allowing the property to draw in university student and younger customers. In recent years, the neighborhood has grown into the large residential districts in the Nagoya metropolitan area, with an increasing number of condominiums and single-family homes being developed mostly on former factory sites. The number of residents within a 5 km radius has reached about 450,000.

8

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

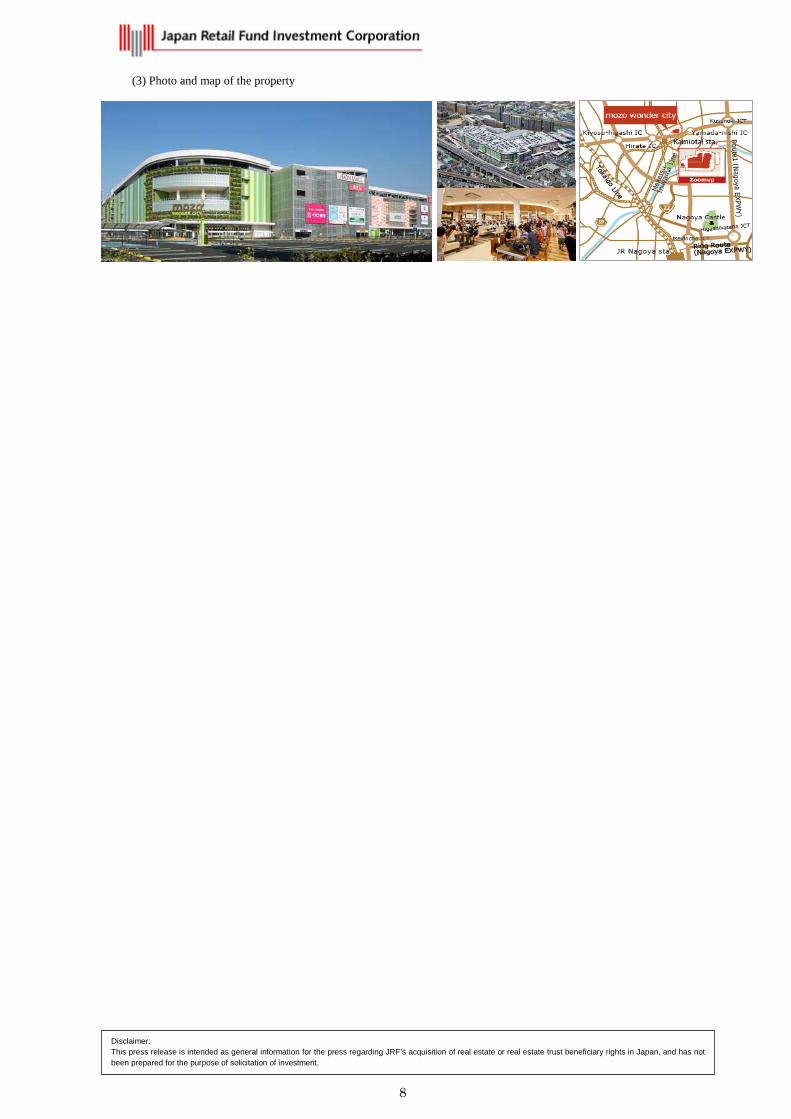

(3) Photo and map of the property

9

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

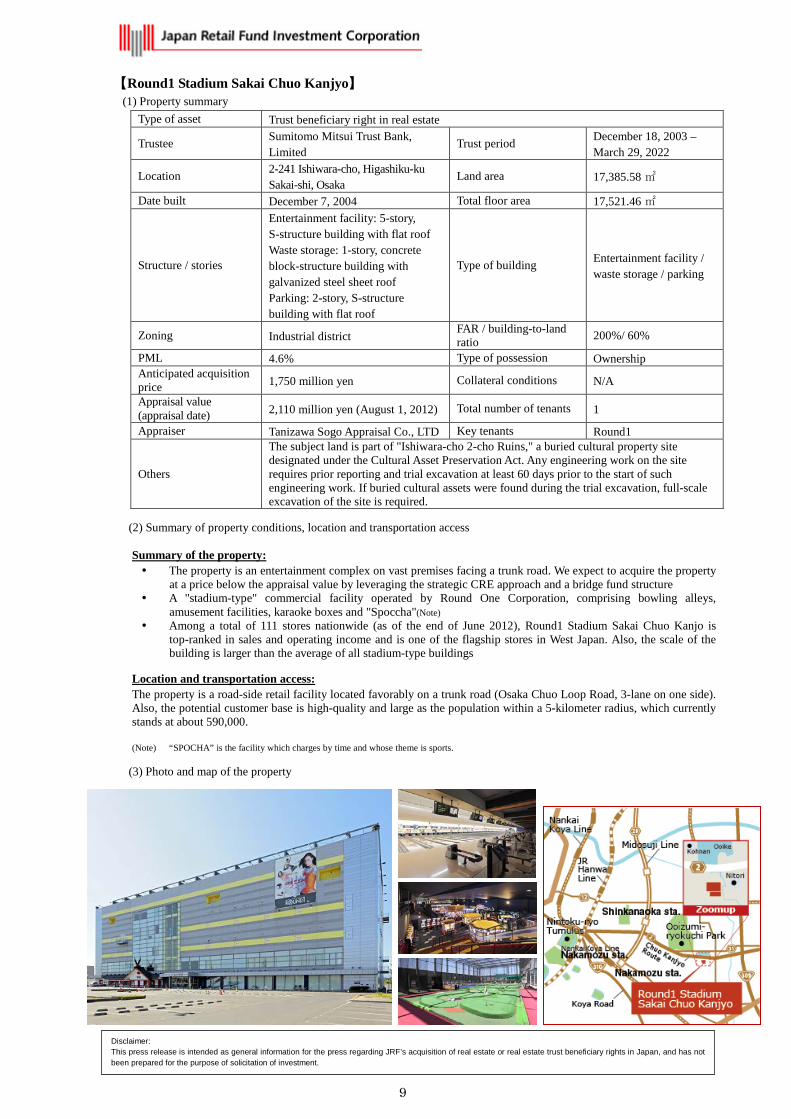

【Round1 Stadium Sakai Chuo Kanjyo】 (1) Property summary

Type of asset Trust beneficiary right in real estate

Trustee Sumitomo Mitsui Trust Bank, Limited

Trust period December 18, 2003 – March 29, 2022

Location 2-241 Ishiwara-cho, Higashiku-ku Sakai-shi, Osaka

Land area 17,385.58 ㎡

Date built December 7, 2004 Total floor area 17,521.46 ㎡

Structure / stories

Entertainment facility: 5-story, S-structure building with flat roof Waste storage: 1-story, concrete block-structure building with galvanized steel sheet roof Parking: 2-story, S-structure building with flat roof

Type of building Entertainment facility / waste storage / parking

Zoning Industrial district FAR / building-to-land ratio 200%/ 60%

PML 4.6% Type of possession Ownership Anticipated acquisition price 1,750 million yen Collateral conditions N/A

Appraisal value (appraisal date) 2,110 million yen (August 1, 2012) Total number of tenants 1

Appraiser Tanizawa Sogo Appraisal Co., LTD Key tenants Round1

Others

The subject land is part of "Ishiwara-cho 2-cho Ruins," a buried cultural property site designated under the Cultural Asset Preservation Act. Any engineering work on the site requires prior reporting and trial excavation at least 60 days prior to the start of such engineering work. If buried cultural assets were found during the trial excavation, full-scale excavation of the site is required.

(2) Summary of property conditions, location and transportation access

Summary of the property: The property is an entertainment complex on vast premises facing a trunk road. We expect to acquire the property

at a price below the appraisal value by leveraging the strategic CRE approach and a bridge fund structure A "stadium-type" commercial facility operated by Round One Corporation, comprising bowling alleys,

amusement facilities, karaoke boxes and "Spoccha"(Note) Among a total of 111 stores nationwide (as of the end of June 2012), Round1 Stadium Sakai Chuo Kanjo is

top-ranked in sales and operating income and is one of the flagship stores in West Japan. Also, the scale of the building is larger than the average of all stadium-type buildings

Location and transportation access: The property is a road-side retail facility located favorably on a trunk road (Osaka Chuo Loop Road, 3-lane on one side). Also, the potential customer base is high-quality and large as the population within a 5-kilometer radius, which currently stands at about 590,000. (Note) “SPOCHA” is the facility which charges by time and whose theme is sports.

(3) Photo and map of the property

10

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

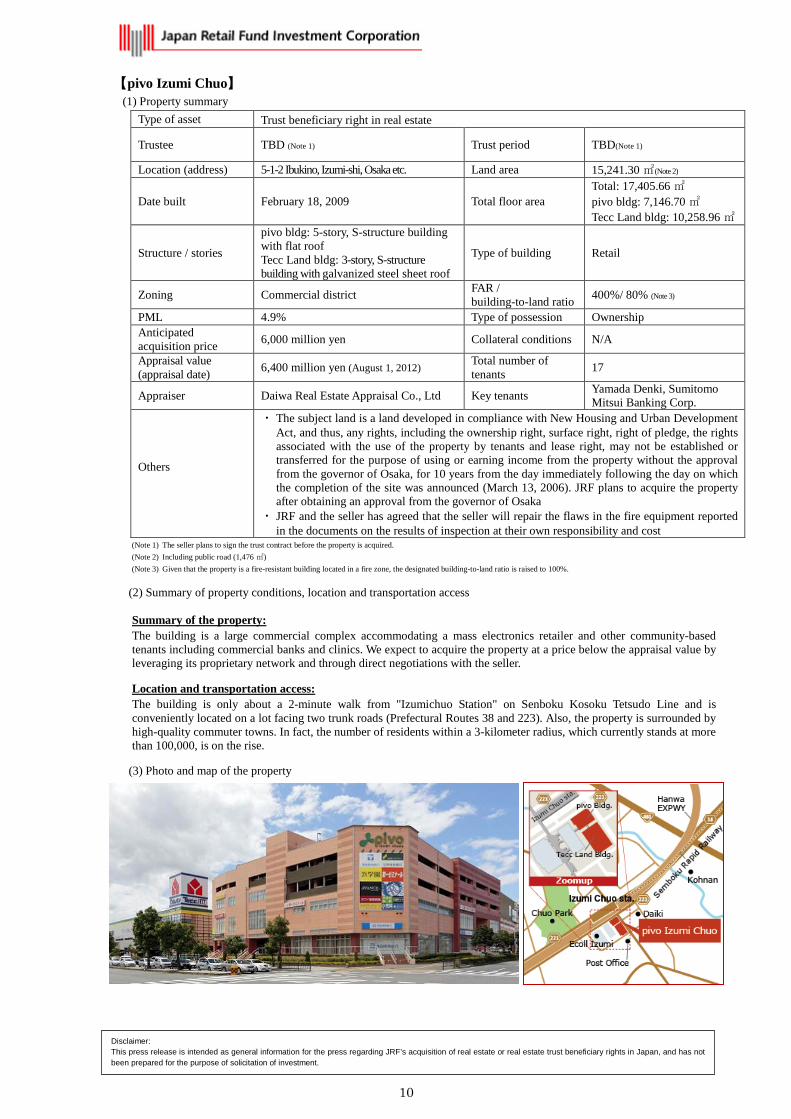

【pivo Izumi Chuo】 (1) Property summary

Type of asset Trust beneficiary right in real estate

Trustee TBD (Note 1) Trust period TBD(Note 1)

Location (address) 5-1-2 Ibukino, Izumi-shi, Osaka etc. Land area 15,241.30 ㎡(Note 2)

Date built February 18, 2009 Total floor area Total: 17,405.66 ㎡ pivo bldg: 7,146.70 ㎡ Tecc Land bldg: 10,258.96 ㎡

Structure / stories

pivo bldg: 5-story, S-structure building with flat roof Tecc Land bldg: 3-story, S-structure building with galvanized steel sheet roof

Type of building Retail

Zoning Commercial district FAR / building-to-land ratio 400%/ 80% (Note 3)

PML 4.9% Type of possession Ownership Anticipated acquisition price 6,000 million yen Collateral conditions N/A

Appraisal value (appraisal date) 6,400 million yen (August 1, 2012) Total number of

tenants 17

Appraiser Daiwa Real Estate Appraisal Co., Ltd Key tenants Yamada Denki, Sumitomo Mitsui Banking Corp.

Others

・ The subject land is a land developed in compliance with New Housing and Urban Development Act, and thus, any rights, including the ownership right, surface right, right of pledge, the rights associated with the use of the property by tenants and lease right, may not be established or transferred for the purpose of using or earning income from the property without the approval from the governor of Osaka, for 10 years from the day immediately following the day on which the completion of the site was announced (March 13, 2006). JRF plans to acquire the property after obtaining an approval from the governor of Osaka

・ JRF and the seller has agreed that the seller will repair the flaws in the fire equipment reported in the documents on the results of inspection at their own responsibility and cost

(Note 1) The seller plans to sign the trust contract before the property is acquired. (Note 2) Including public road (1,476 ㎡) (Note 3) Given that the property is a fire-resistant building located in a fire zone, the designated building-to-land ratio is raised to 100%.

(2) Summary of property conditions, location and transportation access

Summary of the property: The building is a large commercial complex accommodating a mass electronics retailer and other community-based tenants including commercial banks and clinics. We expect to acquire the property at a price below the appraisal value by leveraging its proprietary network and through direct negotiations with the seller.

Location and transportation access: The building is only about a 2-minute walk from "Izumichuo Station" on Senboku Kosoku Tetsudo Line and is conveniently located on a lot facing two trunk roads (Prefectural Routes 38 and 223). Also, the property is surrounded by high-quality commuter towns. In fact, the number of residents within a 3-kilometer radius, which currently stands at more than 100,000, is on the rise.

(3) Photo and map of the property

11

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

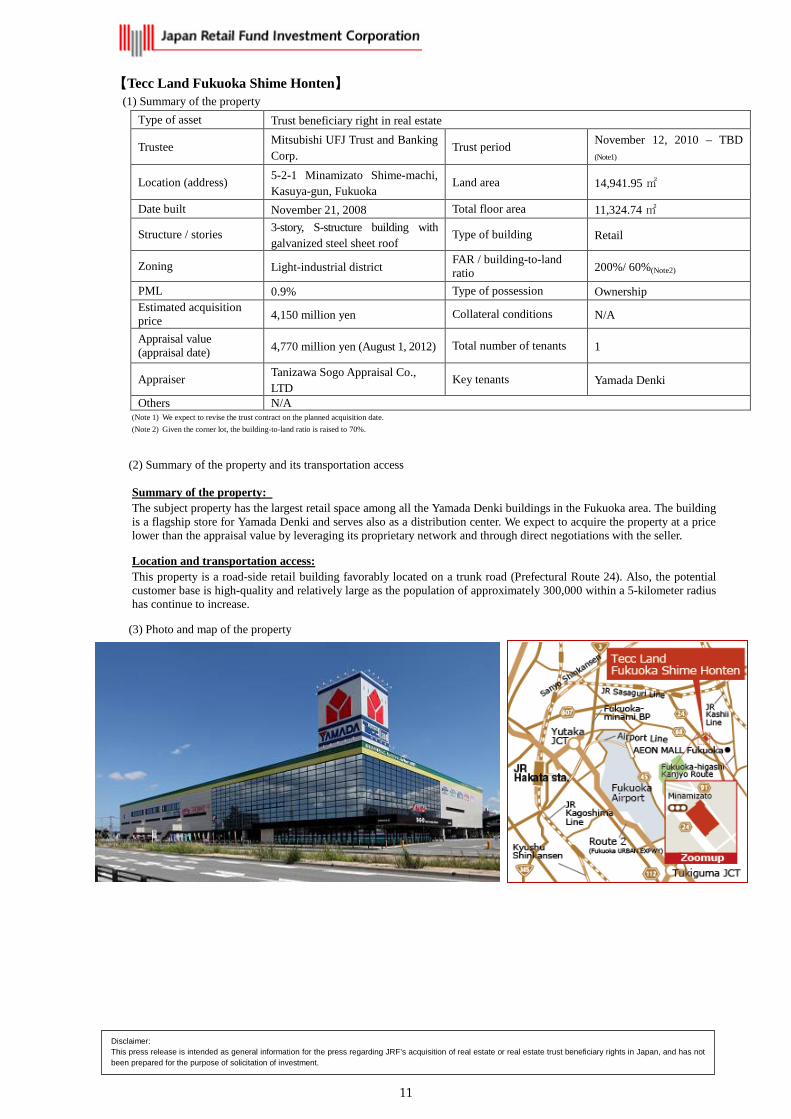

【Tecc Land Fukuoka Shime Honten】 (1) Summary of the property

Type of asset Trust beneficiary right in real estate

Trustee Mitsubishi UFJ Trust and Banking Corp.

Trust period November 12, 2010 – TBD (Note1)

Location (address) 5-2-1 Minamizato Shime-machi, Kasuya-gun, Fukuoka

Land area 14,941.95 ㎡

Date built November 21, 2008 Total floor area 11,324.74 ㎡

Structure / stories 3-story, S-structure building with galvanized steel sheet roof

Type of building Retail

Zoning Light-industrial district FAR / building-to-land ratio 200%/ 60%(Note2)

PML 0.9% Type of possession Ownership Estimated acquisition price 4,150 million yen Collateral conditions N/A

Appraisal value (appraisal date) 4,770 million yen (August 1, 2012) Total number of tenants 1

Appraiser Tanizawa Sogo Appraisal Co., LTD

Key tenants Yamada Denki

Others N/A (Note 1) We expect to revise the trust contract on the planned acquisition date. (Note 2) Given the corner lot, the building-to-land ratio is raised to 70%.

(2) Summary of the property and its transportation access

Summary of the property: The subject property has the largest retail space among all the Yamada Denki buildings in the Fukuoka area. The building is a flagship store for Yamada Denki and serves also as a distribution center. We expect to acquire the property at a price lower than the appraisal value by leveraging its proprietary network and through direct negotiations with the seller.

Location and transportation access: This property is a road-side retail building favorably located on a trunk road (Prefectural Route 24). Also, the potential customer base is high-quality and relatively large as the population of approximately 300,000 within a 5-kilometer radius has continue to increase.

(3) Photo and map of the property

12

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

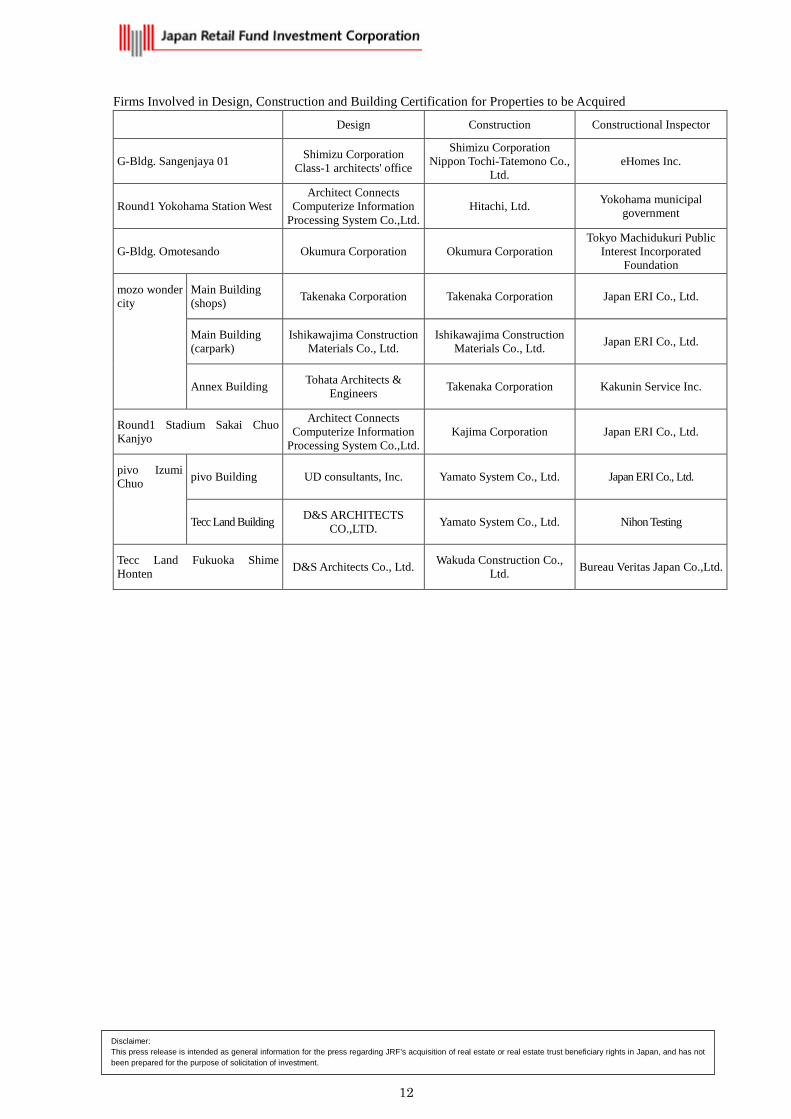

Firms Involved in Design, Construction and Building Certification for Properties to be Acquired

Design Construction Constructional Inspector

G-Bldg. Sangenjaya 01 Shimizu Corporation Class-1 architects' office

Shimizu Corporation Nippon Tochi-Tatemono Co.,

Ltd. eHomes Inc.

Round1 Yokohama Station West Architect Connects

Computerize Information Processing System Co.,Ltd.

Hitachi, Ltd. Yokohama municipal government

G-Bldg. Omotesando Okumura Corporation Okumura Corporation Tokyo Machidukuri Public

Interest Incorporated Foundation

mozo wonder city

Main Building (shops) Takenaka Corporation Takenaka Corporation Japan ERI Co., Ltd.

Main Building (carpark)

Ishikawajima Construction Materials Co., Ltd.

Ishikawajima Construction Materials Co., Ltd. Japan ERI Co., Ltd.

Annex Building Tohata Architects & Engineers Takenaka Corporation Kakunin Service Inc.

Round1 Stadium Sakai Chuo Kanjyo

Architect Connects Computerize Information

Processing System Co.,Ltd. Kajima Corporation Japan ERI Co., Ltd.

pivo Izumi Chuo pivo Building UD consultants, Inc. Yamato System Co., Ltd. Japan ERI Co., Ltd.

Tecc Land Building D&S ARCHITECTS CO.,LTD. Yamato System Co., Ltd. Nihon Testing

Tecc Land Fukuoka Shime Honten D&S Architects Co., Ltd. Wakuda Construction Co.,

Ltd. Bureau Veritas Japan Co.,Ltd.

13

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

5. Profile of Sellers 【G-Bldg. Sangenjaya 01】

(1) Name Retail Five LLC (2) Location Nihonbashi 1-chome Bldg. 1-4-1 Nihonbashi, Chuo-ku, Tokyo

(3) Title & name of representative

Representative Partner: Surf Investment Association Managing Director: Keiichi Omura

(4) Line of business 1. Acquisition, possession and disposal of Real Estate Trust Beneficiary Rights 2. Acquisition, possession, disposal, lease and management of real estate properties 3. Any other auxiliary and/or related businesses to the items described above

(5) Capital ¥100,000 (6) Date established April 6, 2012 (7) Relationship with JRF / the asset manager

Capital relationship Personal relationship Trade relationship

There are no capital, personal or business relationships to note between JRF/the asset management company and this company. In addition, there are no noteworthy capital, personal or business relationships between interested parties and affiliated companies of JRF / the asset management company and those of Retail Five LLC.

Interested parties

This company does not fall under the category of aninterested party of JRF/the asset management company. In addition, none of the interested parties and affiliated companies of this company falls under the category of the interested parties of JRF / the asset management company.

(Note) The "asset management company" denotes, all through this document, Mitsubishi Corp – UBS Realty Inc., the asset management company that takes on asset management for JRF.

【Round1 Yokohama Station West and Round1 Stadium Sakai Chuo Kanjyo】

(1) Name Retail Samurai LLC (2) Location Nihonbashi 1-chome Bldg. 1-4-1 Nihonbashi, Chuo-ku, Tokyo

(3) Title & name of representative

Representative Partner: Surf Investment Association Managing Director: Keiichi Omura

(4) Line of business

1. Acquisition, possession and disposal of Real Estate Trust Beneficiary Rights 2. Acquisition, possession, disposal, lease and management of real estate properties 3. Any other auxiliary and/or related businesses to the items described above

(5) Capital ¥500,000 (6) Date established March 5, 2012 (7) Relationship with JRF or asset manager

Capital relationship Personal relationship Trade relationship

There are no capital, personal or business relationships to note between JRF/the asset management company and this company. In addition, there are no noteworthy capital, personal or business relationships between the interested parties and affiliated companies of JRF / the asset management company and those of Retail Samurai LLC

Interested parties

This company does not fall under the category of aninterested party of JRF/the asset management company. In addition, none of the interested parties and affiliated companies of this company falls under the category of the interested parties of JRF / the asset management company.

14

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

【G-Bldg. Omotesando】 (1) Name Mitsubishi Corporation (2) Location 2-3-1 Marunouchi, Chiyoda-ku, Tokyo

(3) Title & name of representative President and CEO: Ken Kobayashi

(4) Line of business General trading house (5) Capital 204,446 million yen (as of March 31, 2012)

(6) Date established April 1, 1950

(7) Relationship with JRF or asset manager(note)

Capital relationship

The company is a parent company (with an ownership of 51%) of Mitsubishi Corp – UBS Realty Inc., the asset management company for JRF, and thus, falls under the category of an interested party of JRF/the asset management company in the context of "Act on Investment Trusts and Investment Corporations."

Personal relationship Seven of employees (excluding part-time director) of the asset management company are seconded from Mitsubishi Corporation (as of August 31, 2012)

Trade relationship There are no trade relationships between interested parties and affiliated companies of JRF / the asset management company and Mitsubishi Corporation.

Interested parties

The company falls under the category of an interested party of JRF / the asset management company in the context of “Act on Investment Trusts and Investment Corporation.” The company falls under the category of an interested party of the asset management company in the context of the "rules and regulations on business transactions with interested parties of the asset management company".

(Note) This transaction falls under the category of transactions with interested parties, in the context of the asset management company's rules and regulations on business transactions with interested parties. Therefore, this transaction has been affirmed by the Compliance Office in accordance with the bylaws of the asset management company, and also has been approved by the Investment Committee and the board of directors of the asset management company through discussions/deliberations. Approval of the transaction requires at least 6 out of 8 directors voting in favor.

Ownership History of Properties to be Acquired Owner history Previous owner Former owner

Name Mitsubishi Corporation Other than those that have special interest in JRF/the asset management company

Relationship with interested parties of JRF/the asset management company

Parent of the asset management company -

Background/reasons for acquisition Development purposes -

Acquisition price (¥ million) Omitted as the previous owner hold the asset for more than 1 year -

Acquisition date March 29, 2011 -

【mozo wonder city】 (1) Name Kamiotai SC2 LLC (2) Location c/o Sakura Horwath & Co 1-11 Kanda Jinbo-cho, Chiyoda-ku, Tokyo

(3) Title & name of representative

Representative Partner: HNS Association Managing Director: Takao Ando

(4) Line of business

1. Acquisition, possession and disposal of real estate properties 2. Lease and management of real estate properties 3. Acquisition, possession and disposal of Real Estate Trust Beneficiary Rights 4. Any other auxiliary and/or related businesses to the items described above

(5) Capital ¥100,000 (6) Date established March 26, 2010 (7) Relationship with JRF or asset manager

Capital relationship Personal relationship Trade relationship

SPC established for the purpose of acquiring, possessing, and disposing the Real Estate Trust Beneficiary Rights funded by Mitsubishi Corporation, the parent of the asset management company (51% stake). The company falls under the category of the interested parties in the context of “Act on Investment Trusts and Investment Corporation.”.

Interested parties

The company falls under the category of an interested party of JRF / the asset management company in the context of "Act on Investment Trusts and Investment Corporations" and the category of an interested party in the context of the "rules and regulations on business transactions with interested parties" of the asset management company. The company has outsourced asset management to Diamond Realty Management Inc, a wholly-owned subsidiary of Mitsubishi Corporation, the parent of the asset management company.

15

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

(Note) This transaction falls under the category of transactions with interested parties, in the context of the asset management company's rules and regulations on business transactions with interested parties. Therefore, this transaction has been affirmed by the Compliance Office in accordance with the bylaws of the asset management company, and also has been approved by the Investment Committee and the board of directors of the management company through discussions/deliberations. Approval of the transaction requires at least 6 out of 8 directors voting in favor.

Profile of the seller Ownership history Current owner / trustee Former owner / trustee

Name Kamiotai SC2 LLC Kamiotai SC LLC Relationship with interested

parties of JRF/the management company

SPC that the parent company of the asset management company has invested in via

TMK

SPC where the parent of the asset management company has a preferred

stake in Background/purposes of

acquisition For ownership purposes For development purposes

Acquisition price (¥ million) -(Note) - Acquisition date October 4, 2010 August 31, 2007

(Note) The current owner will remain a co-owner of this asset after the transaction. We have obtained preferential negotiation rights over the acquisition of the portion of the asset to be co-owned and expects to negotiate with the current owner over the acquisition of this potion. The price is not listed in the table, however, as the current owner has not disclosed any information regarding the acquisition price. When acquiring this asset, do not need to bearcertain expenses such asthe expenses of establishing an SPC.

【pivo Izumi Chuo】 (1) Name Izumi Chuo B3 Development TMK Izumi Chuo B4 Development TMK (2) Location 3-22-10-201 Toranomon, Minato-ku, Tokyo

(3) Title & name of representative Director: Kazuhiro Matsuzawa

(4) Line of business

1. Business of obtaining specified assets based on asset liquidation plans under the Act on Securitization of Assets and businesses related to management and disposal of those assets

2. Any other auxiliary businesses for securitization of specified assets described above (5) Capital ¥100,000 ¥100,000 (6) Date established November 5, 2007 February 4, 2008 (7) Relationship with JRF or asset manager

Capital relationship Personal relationship Trade relationship

There are no capital, personal or business relationships to note between JRF/the asset management company and this company. In addition, there are no noteworthy capital, personal or business relationships between interested parties and affiliated companies of JRF / the asset management company and those of this TMK.

Interested parties

This TMK does not fall under the category of an interested party of JRF/the asset management company. Also, none of the interested parties and affiliated companies of this TMK fall are interested parties of JRF / the asset management company.

【Tecc Land Fukuoka Shime Honten】

(1) Name Azalea Property GK

(2) Location c/o Tokyo Kyodo Accounting Office 3-1-1 Marunouchi, Chiyoda-ku, Tokyo

(3) Title & name of representative

Representative Partner: MJIA Association Managing Director: Masato Kaida

(4) Line of business 1. Acquisition, possession, disposal, lease and management of real estate properties 2. Acquisition, possession and disposal of Real Estate Trust Beneficiary Rights 3. Any other auxiliary and/or related businesses to the items described above

(5) Capital ¥500,000 (6) Date established October 1, 2010 (7) Relationship with JRF or asset manager

Capital relationship Personal relationship Trade relationship

There are no capital, personal or business relationships to note between JRF/the asset management company and this company. Also, there are no noteworthy capital, personal or business relationships between the interested parties and affiliated companies of JRF / the asset management company and those of this company.

Interested parties

This company does not fall under the category of an interested party of JRF/the asset management company. Also, none of the interested parties and affiliated companies of this company are interested parties of JRF / the asset management company.

16

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

6. Brokers None of the properties (listed in "1. Summary of Properties to be Acquired") are acquired via brokers.

7. Funding and Method of Settlement

Acquisition of the properties will be funded by issuing new investment units, borrowings and cash reserves. For details of the issuance of new investment units, please refer to "Japan Retail Fund Investment Corporation to Issue New Investment Units and Conduct Secondary Offering of Investment Units" dated today. For details of the borrowings, please refer to "Notice Concerning Debt Financing (New Debt Financing and Refinancing)" also dated today.

Additionally, we plan to pay for all properties by way of a lump-sum settlement upon their delivery.

8. Planned Acquisition Schedule Property Name Purchase Agreement

Signing Date Acquisition Date Payment Date

G-Bldg. Sangenjaya 01(Note1)

October 2, 2012(Note2) Round1 Yokohama Station West(Note1) G-Bldg. Omotesando(Note1) mozo wonder city(Note1) Round1 Stadium Sakai Chuo Kanjyo(Note1) pivo Izumi Chuo September 11, 2012 October 5, 2012 Tecc Land Fukuoka Shime Honten

(Note 1) We have agreed with each of relevant parties on the transfer of trust beneficiary rights for "G-Bldg. Sangenjaya 01," "Round1 Yokohama Station West," "G-Bldg. Omotesando," "mozo wonder city" and "Round1 Stadium Sakai Chuo Kanjyo" by signing non-binding letters of intent on August 27, 2012.

(Note 2) When payment date for new investment units trust issued is Oct 1, 2012, planned acquisition date shall be Oct 2, 2012. However, when payment date is between Oct 2, 2012 and Oct 4, 2012 later, planned acquisition date may be changed to the date between Oct 3, 2012 and Oct 5, 2012.

9. Future Outlook

There will be no particular impact on our revenue forecast for the fiscal period ending August 2012 (the 21th period: March 1, 2012 – August 31, 2012).

For our revenue forecast for the fiscal period ending February 2013 (the 22th period: September 1, 2012 – February 28, 2013) after completion of the planned property acquisitions, please refer to "Notice Concerning Revised Forecasts for Operating Results and Distributions for August 2012 (21st) Fiscal Period and February 2013 (22nd) Fiscal Period and Forecasts for Operating Results and Distributions for August 2013 (23rd) Fiscal Period" dated today.

17

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

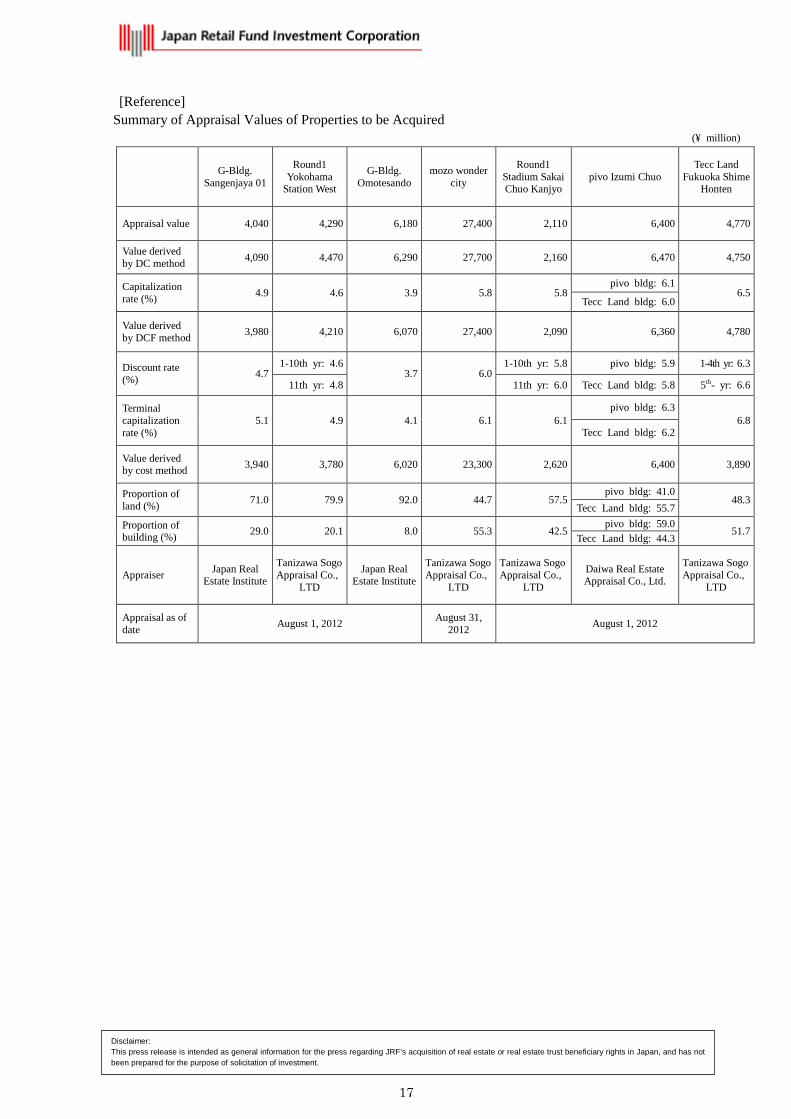

[Reference] Summary of Appraisal Values of Properties to be Acquired

(¥ million)

G-Bldg. Sangenjaya 01

Round1 Yokohama

Station West

G-Bldg. Omotesando

mozo wonder city

Round1 Stadium Sakai Chuo Kanjyo

pivo Izumi Chuo Tecc Land

Fukuoka Shime Honten

Appraisal value 4,040 4,290 6,180 27,400 2,110 6,400 4,770

Value derived by DC method 4,090 4,470 6,290 27,700 2,160 6,470 4,750

Capitalization rate (%) 4.9 4.6 3.9 5.8 5.8

pivo bldg: 6.1 6.5

Tecc Land bldg: 6.0

Value derived by DCF method 3,980 4,210 6,070 27,400 2,090 6,360 4,780

Discount rate (%) 4.7

1-10th yr: 4.6 3.7 6.0

1-10th yr: 5.8 pivo bldg: 5.9 1-4th yr: 6.3

11th yr: 4.8 11th yr: 6.0 Tecc Land bldg: 5.8 5th- yr: 6.6

Terminal capitalization rate (%)

5.1 4.9 4.1 6.1 6.1 pivo bldg: 6.3

6.8 Tecc Land bldg: 6.2

Value derived by cost method 3,940 3,780 6,020 23,300 2,620 6,400 3,890

Proportion of land (%) 71.0 79.9 92.0 44.7 57.5

pivo bldg: 41.0 48.3

Tecc Land bldg: 55.7 Proportion of building (%) 29.0 20.1 8.0 55.3 42.5

pivo bldg: 59.0 51.7

Tecc Land bldg: 44.3

Appraiser Japan Real Estate Institute

Tanizawa Sogo Appraisal Co.,

LTD

Japan Real Estate Institute

Tanizawa Sogo Appraisal Co.,

LTD

Tanizawa Sogo Appraisal Co.,

LTD

Daiwa Real Estate Appraisal Co., Ltd.

Tanizawa Sogo Appraisal Co.,

LTD

Appraisal as of date August 1, 2012 August 31,

2012 August 1, 2012

18

Disclaimer: This press release is intended as general information for the press regarding JRF’s acquisition of real estate or real estate trust beneficiary rights in Japan, and has not been prepared for the purpose of solicitation of investment.

Definitions of Individual Calculation Formulas

① "NOI Yield (before depreciation)," "NOI yield (after depreciation)" ("1. Summary of Properties to be Acquired (Note 4)"), "Average NOI yield (before depreciation)" and "Average NOI yield (after depreciation)" for properties to be acquire ("1. Summary of Properties to be Acquired <Portfolio before and after the anticipated acquisitions> (Note)") are calculated by the following formulas:

・NOI yield (before depreciation) = {((Rental and other operating revenues* – Property-related expenses*) + Depreciations*) of

properties to be acquired} ÷ Expected acquisition price

・NOI yield (after depreciation) = {(Rental and other operating revenues* – Property-related expenses*) of properties to be acquired} ÷

Expected acquisition price

・Average NOI yield (before depreciation) = {(Total of (Rental and other operating revenues* – Property-related expenses*)+ Total

depreciations) of properties to be acquired} ÷ Total expected acquisition price

・Average NOI yield (after depreciation) = {(Total of (Rental and other operating revenues* – Property-related expenses*)) of

properties to be acquired} ÷ Total expected acquisition price

* Rental and other operating revenues, property-related expenses, and depreciations are annual equivalents to the amounts which

are calculated by multiplying by 12 the figures calculated based on the results as of June 2012, which were provided to JRF from

the current beneficiaries or owners of individual properties to acquire, and other information which is expected to affect property

(such as proprietary leases agreements, trust agreements, property management contracts, nonlife insurance, accrual-basis taxes and

public dues, expected depreciations derived from amortization computations based on the acquisition prices and the engineering

report). However, for utility fee, we have used the actual result for one year period as the annual result.

For mozo wonder city, we calculated rental and other operating revenues, property-related expenses, and depreciations based on the

actual recorded performance of 10% interest currently we own through June 30, 2012. Specifically, we have deemed the total of the

actual revenue-based rents recorded for the four-month period ended June 30, 2012 and doubled amount of the actual revenue based

rents for June 2012 as the revenue-based rents for one fiscal period, and have converted it to the annual revenue-based rents. For

utility fee, we have used the actual amount of the 20th fiscal period ended February 29, 2012, and annualized it. For other items, we

calculated annual equivalents by multiplying by 12 the figures calculated based on the results of June 2012 and(such as proprietary

leases, trust agreements, property management contracts, nonlife insurance, accrual-basis taxes and public dues, expected

acquisition prices, and depreciation derived from amortization computations in the engineering report).

② "Average NOI Yield (before depreciation)" and "Average NOI Yield (after depreciation)" for properties as of February 29, 2012 (the last day of the 20th fiscal period) ("1. Summary of Properties to be Acquired <Portfolio before and after anticipated acquisitions> (Note)) are calculated by the following formulas:

・Average NOI Yield (before depreciation) = {(Total of (Rental and other operating revenues* – Property-related expenses*) + Total

depreciations) of owned properties} ÷ Total acquisition price

・Average NOI Yield (after depreciation) = {(Total of (Rental and other operating revenues* – Property-related expenses*)) of owned

properties} ÷ Total acquisition price

* Rental and other operating revenues, property-related expenses and depreciation are annualized amounts for the 20th period

(September 1, 2011 – February 29, 2012), calculated by dividing the results by the number of operating days during the period and

then multiplying by 365 (days).

③ "Average NOI Yield (before depreciation)” and “Average NOI Yield (after depreciation)" for owned properties

after anticipated acquisitions are calculated by the same formulas shown above② , using the sum of the aforementioned figures for the properties owned as last day of the 20th fiscal period and the properties to be acquired.

![PURCHASE AND SALE AGREEMENT Between - RACER · PDF filePURCHASE AND SALE AGREEMENT Between SELLER: [RACER PROPERTIES LLC, a Delaware limited liability company] [Note: The Seller entity](https://img.pdfslide.us/doc/110x75/5a7e75f67f8b9a0a668ec39b/purchase-and-sale-agreement-between-racer-and-sale-agreement-between-seller.jpg)