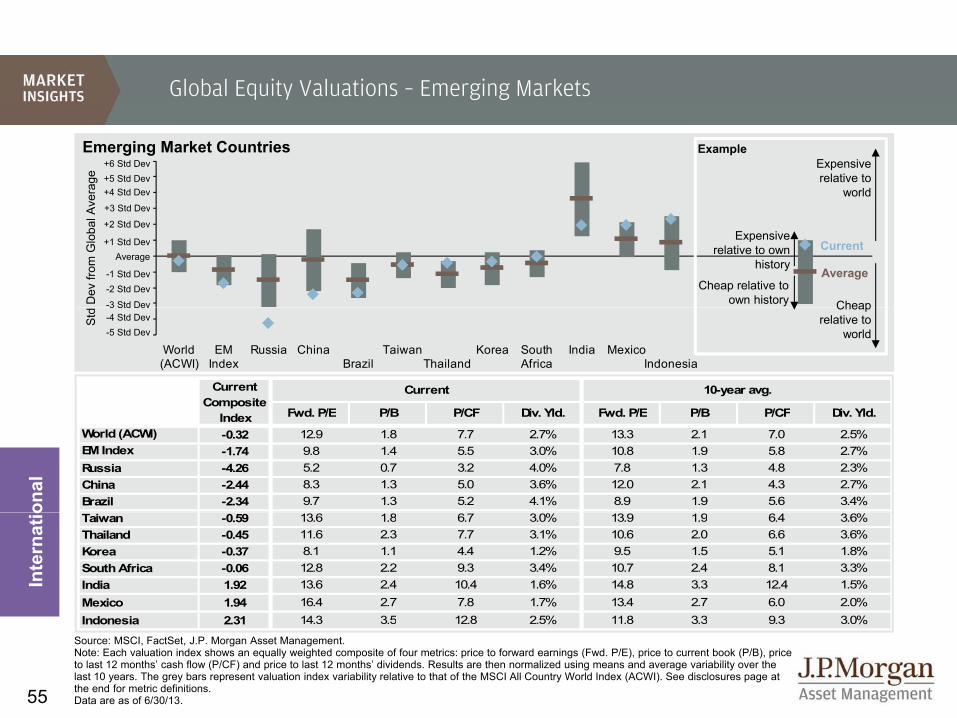

Embed Size (px)

DESCRIPTION

Investors have a lot of things to consider before they make their next move.To help with this, David Kelly and the market strategy team at J.P. Morgan Asset Management have built the best presentation

Citation preview

3Q | 20133Q | 2013As of June 30, 2013

Guide to the Markets®Guide to the Markets

Table of Contents

EQUITIES

ECONOMY

FIXED INCOME

4

17

30FIXED INCOME

INTERNATIONAL

ASSET CLASS

30

39

57

U.S. Market Strategy TeamDr. David P. Kelly, CFA [email protected] S. Tanious, CFA [email protected]és D Garcia-Amaya andres d garcia@jpmorgan comAndrés D. Garcia Amaya [email protected] V. Amoroso, CFA [email protected] D. Odenath [email protected] D. Santos [email protected] M. Wile [email protected]

2Past performance is not indicative of future returns.

Page Reference

4. Returns by Style5. Returns by Sector6. S&P 500 Index at Inflection Points

35. Credit Conditions36. High Yield Bonds37. Municipal Finance38. Emerging Market Debt

Equities

International7. Stock Valuation Measures: S&P 500 Index8. Earnings Estimates and Multiples9. Valuations by Sector and Style10. Corporate Profits and Leverage11. Sources of Earnings per Share Growth12. Confidence and the Capital Markets13. Interest Rates and Equities

39. Global Equity Markets: Returns40. Global Equity Markets: Composition41. Global Economic Growth42. Manufacturing Momentum43. The Importance of Exports44. The Impact of Global Consumers

International

3 te est ates a d qu t es14. Deploying Corporate Cash15. P/E Ratios and Equity Returns16. Equity Correlations and Volatility

17. Economic Growth and the Composition of GDP18 Cyclical Sectors

p45. Sovereign Debt Stresses46. Global Manufacturing Wages47. Global Monetary Policy48. Europe: Economic Growth49. Europe: Austerity50. Eurozone: Sovereign Bond Yields51 China: Growth and Economic Policy

Economy

18. Cyclical Sectors19. The Aftermath of the Housing Bubble20. Consumer Finances21. Federal Finances: Outlays and Revenues22. Federal Finances: Deficits and Debt23. Trade and the U.S. Dollar24. Employment25 Employment and Income by Educational Attainment

51. China: Growth and Economic Policy52. China: Cyclical Indicators53. Japan: Economic Snapshot54. Global Equity Valuations – Developed Markets55. Global Equity Valuations – Emerging Markets56. Emerging Market Equity Composition

Asset Class25. Employment and Income by Educational Attainment26. Consumer Price Index27. Oil and the Economy28. Global Energy Supply29. Consumer Confidence and the Stock Market

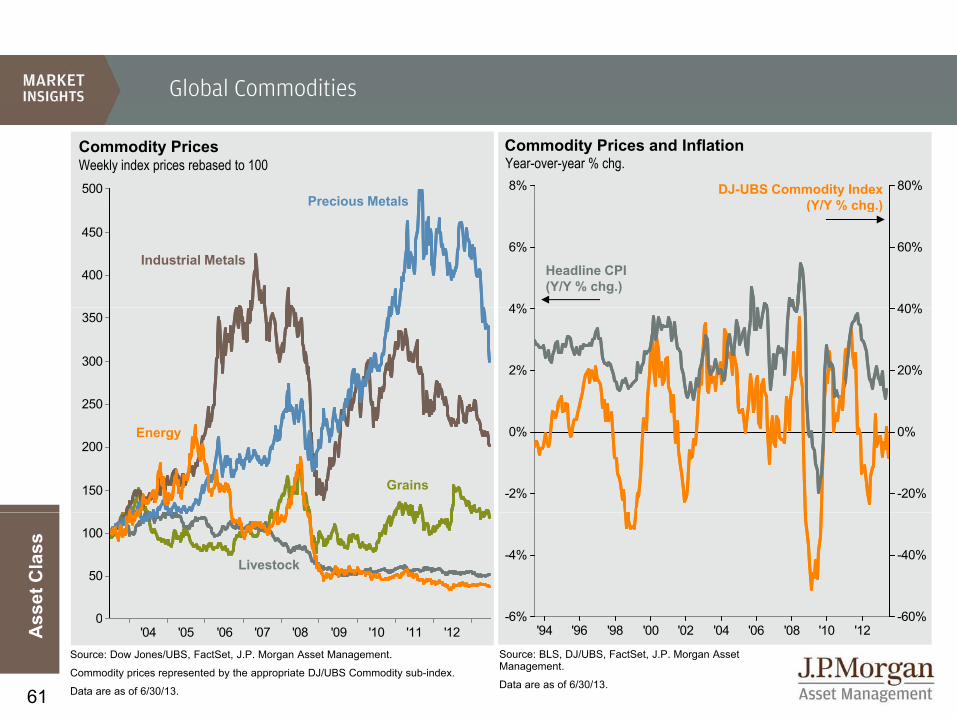

57. Asset Class Returns58. Correlations: 10-Years59. Mutual Fund Flows60. Yield Alternatives: Domestic and Global61. Global Commodities62. Historical Returns by Holding Period

f

Fixed Income

3

30. Fixed Income Sector Returns31. Interest Rates and Inflation32. Fixed Income Yields and Returns33. Correlation to 10-Year Treasury Returns34. The Fed and the Money Supply

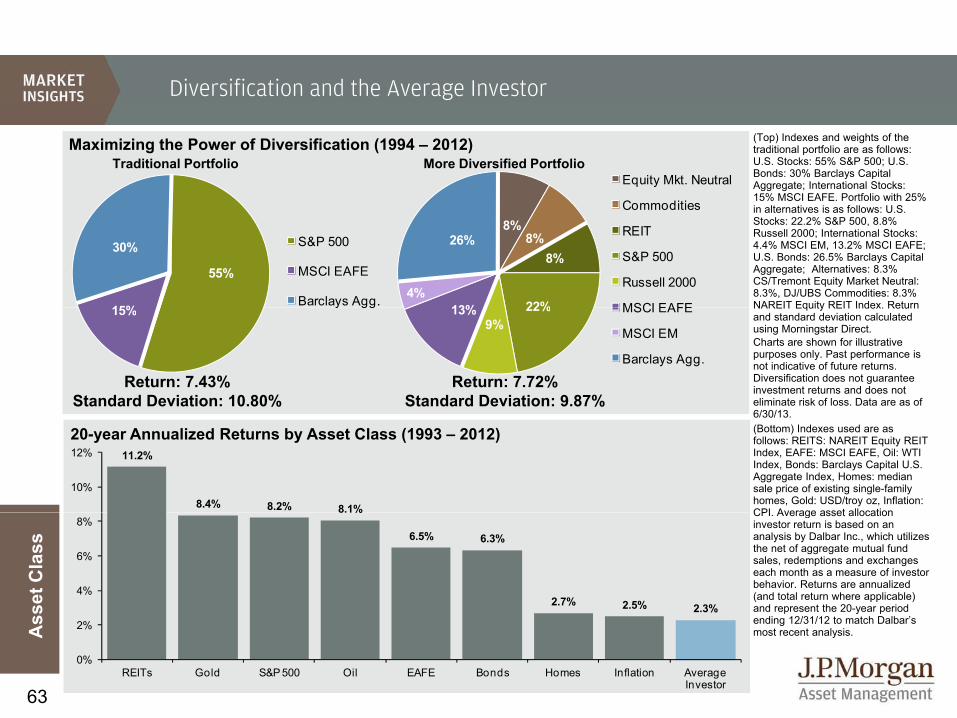

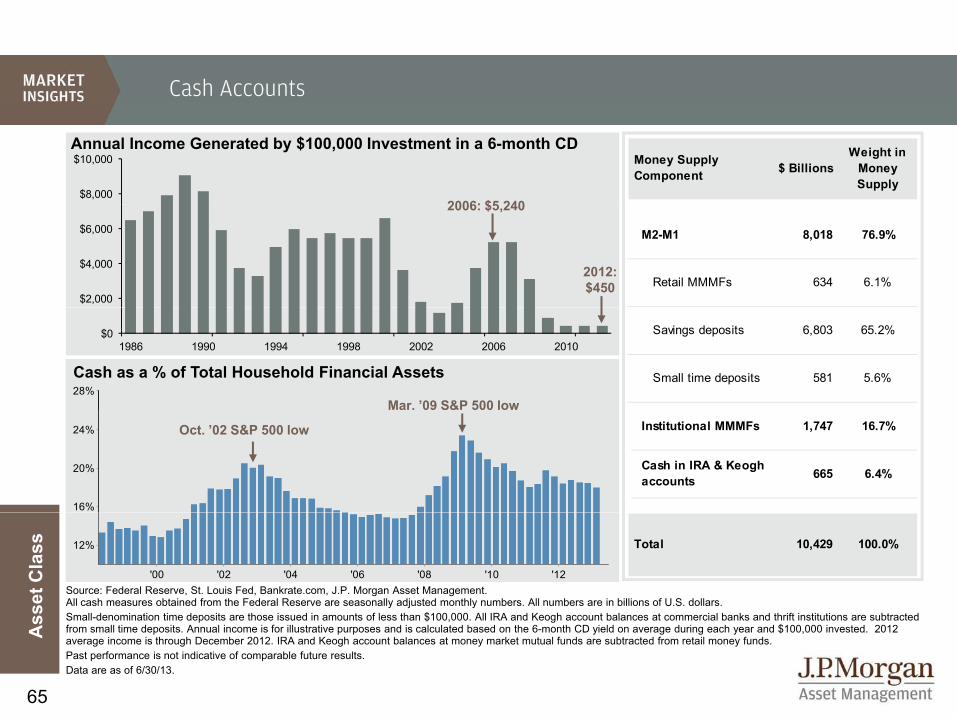

63. Diversification and the Average Investor64. Annual Returns and Intra-year Declines65. Cash Accounts66. Corporate DB Plans and Endowments 67. Stock Market Since 1900

Returns by Style

1,700S&P 500 Index

2Q 2013 YTD 2013

Charts reflect index levels (price change only). All returns and annotations reflect total return, including dividends.

Value Blend Growth Value Blend Growth

1,500

1,600

,

Equi

ties

YTD 2013: +13 8%

2Q 2013: +2.9% La

rge

3.2% 2.9% 2.1%

Larg

e

15.9% 13.8% 11.8%

Mid 1.7% 2.2% 2.9% Mid 16.1% 15.5% 14.7%

1 800

Dec-12 Feb-13 Mar-13 Apr-13 May-13 Jun-131,400

S&P 500 Index

YTD 2013: +13.8%

Since Market Low (March 2009)Since Market Peak (October 2007)

Smal

l

2.5% 3.1% 3.7%

Smal

l

14.4% 15.9% 17.4%

Value Blend Growth Value Blend Growth

1 000

1,200

1,400

1,600

1,800 Since 10/9/07 Peak: +16.5%

Since 3/9/09

Value Blend Growth Value Blend GrowthLa

rge

9.6% 16.5% 26.0%

Larg

e

173.2% 160.3% 157.0%M

id 27.7% 28.7% 28.0% Mid 226.1% 210.5% 196.0%

Dec-06 Apr-08 Aug-09 Nov-10 Mar-12 Jun-13600

800

1,000

Source: Russell Investment Group, Standard & Poor’s, FactSet, J.P. Morgan Asset Management.

All calculations are cumulative total return including dividends reinvested for the stated period Since Market Peak represents period 10/9/07 – 6/30/13 illustrating

Since 3/9/09Low: +160.3%

Smal

l

20.8% 25.4% 29.3%

Smal

l

198.8% 202.3% 205.2%

4

All calculations are cumulative total return, including dividends reinvested for the stated period. Since Market Peak represents period 10/9/07 6/30/13, illustrating market returns since the most recent S&P 500 Index high on 10/9/07. Since Market Low represents period 3/9/09 – 6/30/13, illustrating market returns since the S&P 500 Index low on 3/9/09. Returns are cumulative returns, not annualized. For all time periods, total return is based on Russell-style indexes with the exception of the large blend category, which is reflected by the S&P 500 Index. Past performance is not indicative of future returns.

Data are as of 6/30/13.

Returns by Sector

Financia

ls

Technology

Health C

are

Industri

als

Energy

Cons. Disc

r.

Cons. Stap

les

Teleco

m

Utilitie

s

Materia

ls

S&P 500 In

dex

Equi

ties S&P Weight 16.7% 17.8% 12.7% 10.2% 10.5% 12.2% 10.5% 2.8% 3.3% 3.3% 100.0%

Russell Growth Weight 4.9% 28.2% 13.1% 13.0% 4.1% 17.7% 12.6% 2.3% 0.2% 3.9% 100.0%Russell Value Weight 28.7% 7.0% 11.8% 9.0% 15.3% 8.6% 7.1% 3.0% 6.3% 3.3% 100.0%

2Q13 7.3 1.7 3.8 2.8 -0.4 6.8 0.5 1.0 -2.7 -1.8 2.9

YTD 2013 19.5 6.4 20.3 13.8 9.8 19.8 15.2 10.6 9.9 2.9 13.8

Wei

ght

(%)

Since Market Peak (October 2007)

-38.5 23.1 48.3 12.2 11.3 64.7 67.1 17.9 15.9 2.3 16.5

Since Market Low (March 2009)

235.5 158.0 139.1 208.5 103.8 281.2 134.3 125.3 102.9 143.6 160.3

Beta to S&P 500 1.44 1.13 0.68 1.20 1.00 1.12 0.55 0.65 0.48 1.31 1.00

Forward P/E Ratio 12 1x 13 0x 14 8x 14 2x 11 7x 16 5x 16 3x 16 6x 15 2x 13 7x 13 9x

Ret

urn

S S d d & P ’ R ll I G F S J P M A M

Forward P/E Ratio 12.1x 13.0x 14.8x 14.2x 11.7x 16.5x 16.3x 16.6x 15.2x 13.7x 13.9x15-yr avg. 12.7x 23.4x 18.0x 16.8x 14.4x 18.5x 17.8x 17.3x 13.6x 16.0x 16.4x

Trailing P/E Ratio 15.6x 15.2x 19.3x 16.9x 11.9x 17.9x 18.9x 41.0x 18.7x 17.9x 16.5x20-yr avg. 16.0x 26.4x 24.2x 20.4x 17.9x 19.3x 21.2x 20.3x 14.5x 19.3x 19.5x

Dividend Yield 1.9% 1.7% 1.9% 2.2% 2.3% 1.6% 2.7% 4.5% 4.0% 2.6% 2.0%20-yr avg. 2.1% 0.6% 1.4% 1.7% 1.8% 1.0% 2.1% 3.9% 4.4% 2.1% 1.7%

P/E

Div

Source: Standard & Poor’s, Russell Investment Group, FactSet, J.P. Morgan Asset Management.

All calculations are cumulative total return, not annualized, including dividends for the stated period. Since Market Peak represents period 10/9/07 – 6/30/13. Since Market Low represents period 3/9/09 – 6/30/13.

Forward P/E Ratio is a bottom-up calculation based on the most recent S&P 500 Index price, divided by consensus estimates for earnings in the next 12 months (NTM), and is provided by FactSet Market Aggregates. Trailing P/E ratios are bottom-up values defined as month-end price divided by the last 12 months of available reported earnings. Historical data can change as new information becomes available. Note that P/E ratios for the S&P 500 may differ from estimates elsewhere in this book due to the use of a bottom-up calculation of constituent earnings (as described) rather than a top-down calculation. This methodology is used to allow proper comparison of sector level data to broad index level data Dividend yields are bottom-up values defined as the

5

This methodology is used to allow proper comparison of sector level data to broad index level data. Dividend yields are bottom up values defined as the annualized value of the most recent cash dividend as a percent of month-end price. Beta calculations are based on 10 years of monthly price returns for the S&P 500 and its sub-indices.

Past performance is not indicative of future returns.

Data are as of 6/30/13.

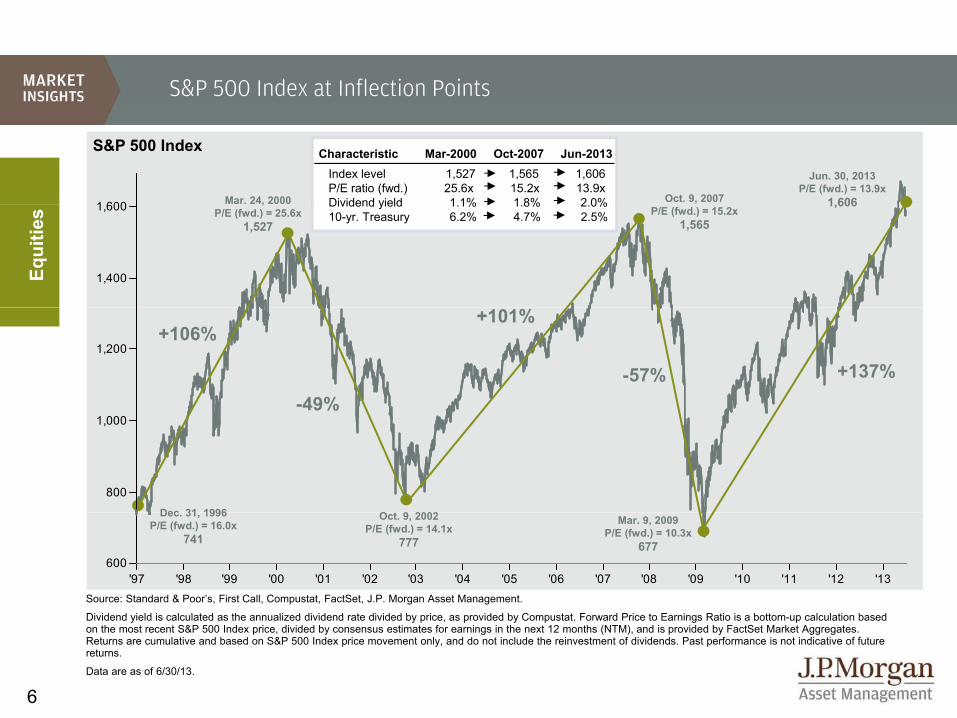

S&P 500 Index at Inflection Points

1 600

Index level 1,527 1,565 1,606P/E ratio (fwd.) 25.6x 15.2x 13.9xDividend yield 1 1% 1 8% 2 0%

S&P 500 Index

Mar. 24, 2000

Jun. 30, 2013 P/E (fwd.) = 13.9x

1,606Oct. 9, 2007

Characteristic Mar-2000 Oct-2007 Jun-2013

1,400

1,600 Dividend yield 1.1% 1.8% 2.0% 10-yr. Treasury 6.2% 4.7% 2.5%

Equi

ties

,P/E (fwd.) = 25.6x

1,527

1,606P/E (fwd.) = 15.2x

1,565

1,200

-49%

+101%

-57% +137%

+106%

800

1,00049%

O t 9 2002Dec 31 1996

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13600

Source: Standard & Poor’s, First Call, Compustat, FactSet, J.P. Morgan Asset Management.

Di idend ield is calc lated as the ann ali ed di idend rate di ided b price as pro ided b Comp stat For ard Price to Earnings Ratio is a bottom p calc lation based

Oct. 9, 2002 P/E (fwd.) = 14.1x

777

Dec. 31, 1996 P/E (fwd.) = 16.0x

741 Mar. 9, 2009

P/E (fwd.) = 10.3x 677

6

Dividend yield is calculated as the annualized dividend rate divided by price, as provided by Compustat. Forward Price to Earnings Ratio is a bottom-up calculation based on the most recent S&P 500 Index price, divided by consensus estimates for earnings in the next 12 months (NTM), and is provided by FactSet Market Aggregates. Returns are cumulative and based on S&P 500 Index price movement only, and do not include the reinvestment of dividends. Past performance is not indicative of future returns.

Data are as of 6/30/13.

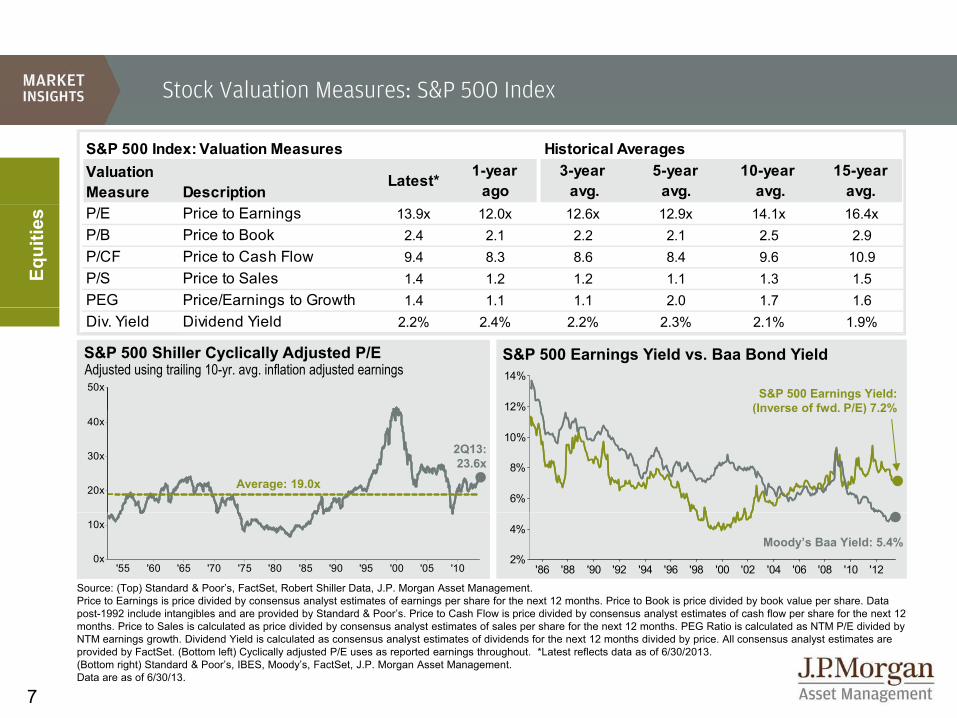

Stock Valuation Measures: S&P 500 Index

S&P 500 Index: Valuation Measures Historical AveragesValuation Measure Description

Latest* 1-year ago

3-year avg.

5-year avg.

10-year avg.

15-year avg.

Equi

ties P/E Price to Earnings 13.9x 12.0x 12.6x 12.9x 14.1x 16.4x

P/B Price to Book 2.4 2.1 2.2 2.1 2.5 2.9P/CF Price to Cash Flow 9.4 8.3 8.6 8.4 9.6 10.9P/S Price to Sales 1.4 1.2 1.2 1.1 1.3 1.5PEG Price/Earnings to Growth 1.4 1.1 1.1 2.0 1.7 1.6

12%

14%50x

S&P 500 Shiller Cyclically Adjusted P/EAdjusted using trailing 10-yr. avg. inflation adjusted earnings

S&P 500 Earnings Yield vs. Baa Bond Yield

S&P 500 Earnings Yield: (Inverse of fwd P/E) 7 2%

gDiv. Yield Dividend Yield 2.2% 2.4% 2.2% 2.3% 2.1% 1.9%

6%

8%

10%

12%

20x

30x

40x(Inverse of fwd. P/E) 7.2%

2Q13: 23.6x

Average: 19.0x

'86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '122%

4%

'55 '60 '65 '70 '75 '80 '85 '90 '95 '00 '05 '100x

10x

Moody�’s Baa Yield: 5.4%

Source: (Top) Standard & Poor’s, FactSet, Robert Shiller Data, J.P. Morgan Asset Management. Price to Earnings is price divided by consensus analyst estimates of earnings per share for the next 12 months. Price to Book is price divided by book value per share. Data post-1992 include intangibles and are provided by Standard & Poor’s Price to Cash Flow is price divided by consensus analyst estimates of cash flow per share for the next 12

7

post 1992 include intangibles and are provided by Standard & Poor s. Price to Cash Flow is price divided by consensus analyst estimates of cash flow per share for the next 12 months. Price to Sales is calculated as price divided by consensus analyst estimates of sales per share for the next 12 months. PEG Ratio is calculated as NTM P/E divided by NTM earnings growth. Dividend Yield is calculated as consensus analyst estimates of dividends for the next 12 months divided by price. All consensus analyst estimates are provided by FactSet. (Bottom left) Cyclically adjusted P/E uses as reported earnings throughout. *Latest reflects data as of 6/30/2013.(Bottom right) Standard & Poor’s, IBES, Moody’s, FactSet, J.P. Morgan Asset Management.Data are as of 6/30/13.

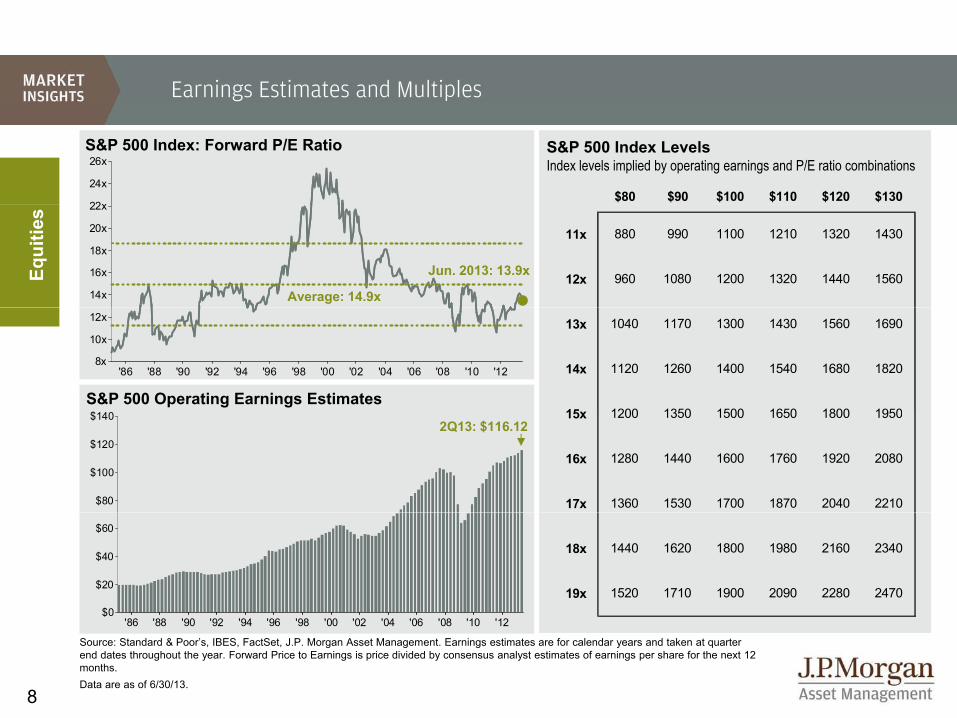

Earnings Estimates and Multiples

22x

24x

26xS&P 500 Index: Forward P/E Ratio S&P 500 Index Levels

Index levels implied by operating earnings and P/E ratio combinations

$80 $90 $100 $110 $120 $130

14x

16x

18x

20x

22x

Average: 14.9x

Jun. 2013: 13.9xEqui

ties

11x 880 990 1100 1210 1320 1430

12x 960 1080 1200 1320 1440 1560

'86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '128x

10x

12x

S&P 500 Operating Earnings Estimates

13x 1040 1170 1300 1430 1560 1690

14x 1120 1260 1400 1540 1680 1820

15 1200 1350 1500 1650 1800 1950

$80

$100

$120

$1402Q13: $116.12

15x 1200 1350 1500 1650 1800 1950

16x 1280 1440 1600 1760 1920 2080

17x 1360 1530 1700 1870 2040 2210

$0

$20

$40

$60

18x 1440 1620 1800 1980 2160 2340

19x 1520 1710 1900 2090 2280 2470

8

'86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12$0

Source: Standard & Poor’s, IBES, FactSet, J.P. Morgan Asset Management. Earnings estimates are for calendar years and taken at quarter end dates throughout the year. Forward Price to Earnings is price divided by consensus analyst estimates of earnings per share for the next 12 months.Data are as of 6/30/13.

Valuations by Sector and Style

1.3x

Defensive vs. Cyclical Sector Valuations

y y

Next 12-month P/E ratio for defensives / next 12-month P/E ratio for cyclicalsCurrent P/E vs. 20-year avg. P/E

13.4 13.9 16.6

Value Blend Growth

ge

1.1x

1.2x

Equi

ties

Defensive Sectors premium valuation

13.9 16.2 20.9

14.7 16.3 18.6

14.0 16.3 21.8

Larg

Mid

0.9x

1.0x

Average: 1.0xCurrent P/E as % of 20-year avg. P/E

E.g.: Large Cap Blend stocks are 13.8%

15.3 17.0 19.1

14.2 17.1 21.3Smal

l

0.7x

0.8xValue Blend Growth

Larg

e

96.4% 86.2% 79.4%

Cyclical Sectors

g g pcheaper than their historical average.

0.5x

0.6x

Mid 104.7% 100.0% 85.5%

Smal

l

107.2% 99.5% 89.6%

Cyclical Sectors premium valuation

9

'96 '98 '00 '02 '04 '06 '08 '10 '120.5x

Source: Standard & Poor’s, Russell Investment Group, IBES, FactSet, J.P. Morgan Asset Management.Defensive vs. Cyclical sector analysis based on GICS sectors and excludes Financials. Defensives sectors are comprised of Health Care, Consumer Staples, Utilities and Telecommunications Services. Cyclical sectors are comprised of Information Technology, Industrials, Energy, Consumer Discretionary and Materials. P/E ratios are calculated and provided by Russell based on IBES consensus estimates of earnings over the next 12 months except for large blend, which is the S&P 500.Data are as of 6/30/13.

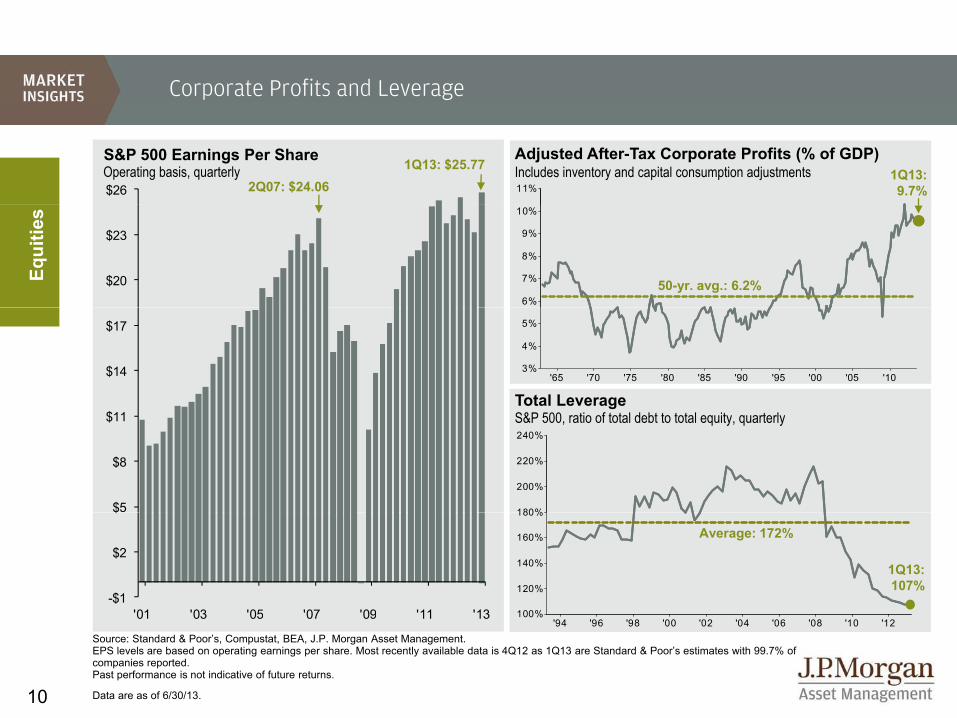

Corporate Profits and Leverage

$26

S&P 500 Earnings Per ShareOperating basis, quarterly

Adjusted After-Tax Corporate Profits (% of GDP)Includes inventory and capital consumption adjustments11%

1Q13:9.7%

1Q13: $25.772Q07: $24.06

$20

$23

Equi

ties

6%

7%

8%

9%

10%

50-yr. avg.: 6.2%

$14

$17

'65 '70 '75 '80 '85 '90 '95 '00 '05 '103%

4%

5%

Total Leverage

$5

$8

$11

180%

200%

220%

240%S&P 500, ratio of total debt to total equity, quarterly

-$1

$2

$

'13'11'09'07'05'03'01 100%

120%

140%

160%

180%

1Q13: 107%

Average: 172%

10

13110907050301

Source: Standard & Poor’s, Compustat, BEA, J.P. Morgan Asset Management.EPS levels are based on operating earnings per share. Most recently available data is 4Q12 as 1Q13 are Standard & Poor’s estimates with 99.7% of companies reported.Past performance is not indicative of future returns.

Data are as of 6/30/13.

'94 '96 '98 '00 '02 '04 '06 '08 '10 '12100%

Sources of Earnings per Share Growth

50%Margin Share of EPS Growth

S&P 500 Year-Over-Year EPS GrowthGrowth broken into revenue growth and margin expansion, quarterly

30%

40%

Equi

ties Margin Share of EPS Growth

Revenue Share of EPS Growth

0%

10%

20%

-20%

-10%

0%

-40%

-30%

1Q131Q111Q091Q071Q051Q031Q011Q991Q971Q95

11

Source: Standard & Poor’s, Compustat, J.P. Morgan Asset Management.EPS levels are based on operating earnings per share. Most recently available data is 4Q12 as 1Q13 are Standard & Poor’s estimates with 99.7% of companies reported. Past performance is not indicative of future returns. 4Q2008, 1Q2010 and 2Q2010 reflect -101%, 92% and 51% growth in operating earnings, and are adjusted on the chart.

Data are as of 6/30/13.

Confidence and the Capital Markets

110

120

24x

26x

Multiple Expansion and Contraction

Consumer SentimentForward P/ES&P 500 forward P/E based on consensus EPS estimates Est. impact of a 10pt. rise in sentiment: +2.0 multiple points*

70

80

90

100

110

16x

18x

20x

22x

24x

Equi

ties

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '1250

60

70

10x

12x

14x

Sentiment & Real Yields Est impact of a 10pt rise in sentiment: +54 basis points*

Correlation Coefficient: 0.75

90

100

110

120

3%

4%

5%

6% Consumer SentimentReal 10-year YieldReal yield based on nominal 10-yr. yield minus year-over-year core CPI Est. impact of a 10pt. rise in sentiment: +54 basis points*

60

70

80

90

0%

1%

2%

3%

Correlation Coefficient: 0.68

12

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '1250-1%

Source: (Top) Standard & Poor’s, FactSet, J.P. Morgan Asset Management. (Bottom) U.S. Treasury, BLS, University of Michigan, J.P. Morgan Asset Management. Price to Earnings is price divided by consensus analyst estimates of earnings per share for the next twelve months. Real 10-year Treasury yields are calculated as the daily Treasury yield less year-over-year core inflation for that month. *Estimated impact based on coefficients from regression analysis. Data are as of 6/30/13.

13

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

0% 2% 4% 6% 8% 10% 12% 14% 16%

Sector Correlations to Rates 2-year rolling, 1994-2013

Correlations Between Weekly Stock Returns and Interest Rate Movements Weekly S&P 500 returns, 10-year Treasury yield, rolling 2-year correlation, 1963-2013

US Treasury, FactSet, J.P. Morgan Asset Management. Returns are based on price index only and do not include dividends. Grey bars in the right chart represent the historic range in correlations for each sector. Data are as of 6/30/13.

Equi

ties

Positive relationship between yield movements and stock returns

Negative relationship between yield movements and stock returns

When yields are below 5%, rising rates are generally associated with rising stock prices

10-Year Treasury Yield

Cor

rela

tion

Coef

ficie

nt

Max Average

Current Min

-1.00 -0.50 0.00 0.50 1.00

Utilities

Telecom

Cons. Staples

Materials

Technology

Health Care

Energy

Cons. Disc.

S&P 500

Industrials

Financials

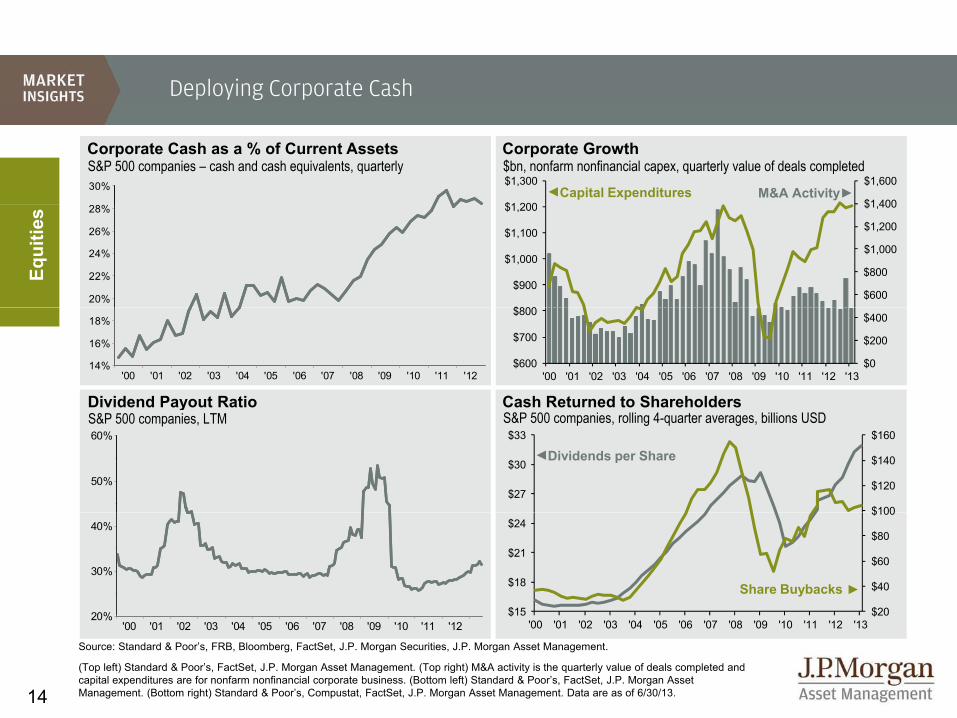

Deploying Corporate Cash

Corporate Cash as a % of Current AssetsS&P 500 companies – cash and cash equivalents, quarterly

%

30%

Corporate Growth

Capital Expenditures M&A Activity

$bn, nonfarm nonfinancial capex, quarterly value of deals completed

$1 400

$1,600

$1 200

$1,300

Equi

ties

20%

22%

24%

26%

28%

$600

$800

$1,000

$1,200

$1,400

$800

$900

$1,000

$1,100

$1,200

Cash Returned to ShareholdersDividend Payout Ratio

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '1214%

16%

18%

$0

$200

$400

$600

$700

$800

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

50%

60%

yS&P 500 companies, rolling 4-quarter averages, billions USDS&P 500 companies, LTM

Dividends per Share

$100

$120

$140

$160

$27

$30

$33

20%

30%

40%

Share Buybacks$20

$40

$60

$80

$100

$15

$18

$21

$24

14

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '1220%

Source: Standard & Poor’s, FRB, Bloomberg, FactSet, J.P. Morgan Securities, J.P. Morgan Asset Management.

(Top left) Standard & Poor’s, FactSet, J.P. Morgan Asset Management. (Top right) M&A activity is the quarterly value of deals completed and capital expenditures are for nonfarm nonfinancial corporate business. (Bottom left) Standard & Poor’s, FactSet, J.P. Morgan Asset Management. (Bottom right) Standard & Poor’s, Compustat, FactSet, J.P. Morgan Asset Management. Data are as of 6/30/13.

$20$15'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

P/E Ratios and Equity Returns

60%60%

P/E and Total Return Over 5-yr. Annualized PeriodsP/E and Total Return Over 1-yr. PeriodsQuarterly, 1Q 1952 to 1Q 2008Quarterly, 1Q 1952 to 1Q 2012

Current P/E: 14.5x Current P/E: 14.5x

40%40%

Equi

ties

20%20%

0%5x 10x 15x 20x 25x 30x

0%5x 10x 15x 20x 25x 30x

-40%

-20%

-40%

-20%

15

Source: BEA, FRB, J.P. Morgan Asset Management. Prices are based on the market value of all U.S. corporations and include quarterly dividends. Valuation based on long-term P/E ratio. Note: Orange line denote results of linear regression with R-squared of 0.15 for 1-yr. returns (left) and 0.36 for 5-yr. returns (right). Data are as of 6/30/13.

Equity Correlations and Volatility

60%

70%

Large Cap StocksCorrelations Among Stocks

Sovereign Debt Crisis

Lehman Bankruptcy

Great Depression /World War II

30%

40%

50%

60%

Equi

ties Bankruptcy

Tech Bust & 9/11

1987 CrashWorld War II

OPEC Oil Crisis

Cuban Missile Crisis

0%

10%

20%

'26 '32 '38 '44 '50 '56 '62 '68 '74 '80 '86 '92 '98 '04 '10

Daily Volatility of DJIA

Average: 26.9% Jun. 2013: 34.2%

2 0%

2.5%

3.0%

3.5%

60

75

90Volatility Measure �’08 Peak Average Latest DJIA (Left) 3.30% 0.72% 0.60%VIX (Right) 80.9 20.3 16.9

Daily Volatility of DJIA

DJIA vol. shownin 3-month

moving average

0.5%

1.0%

1.5%

2.0%

15

30

45

16

'30 '35 '40 '45 '50 '55 '60 '65 '70 '75 '80 '85 '90 '95 '00 '05 '100.0% 0

Source: (Top) Empirical Research Partners LLC, Standard & Poor’s, J.P. Morgan Asset Management. Capitalization weighted correlation of top 750 stocks by market capitalization, daily returns, 1926 – Jun. 30, 2013. (Bottom) CBOE, Dow Jones, J.P. Morgan Asset Management. DJIA volatility are represented as three-month moving averages of the daily absolute percentage change in the Dow Jones Industrial Average.Charts shown for illustrative purposes only. Data are as of 6/30/13.

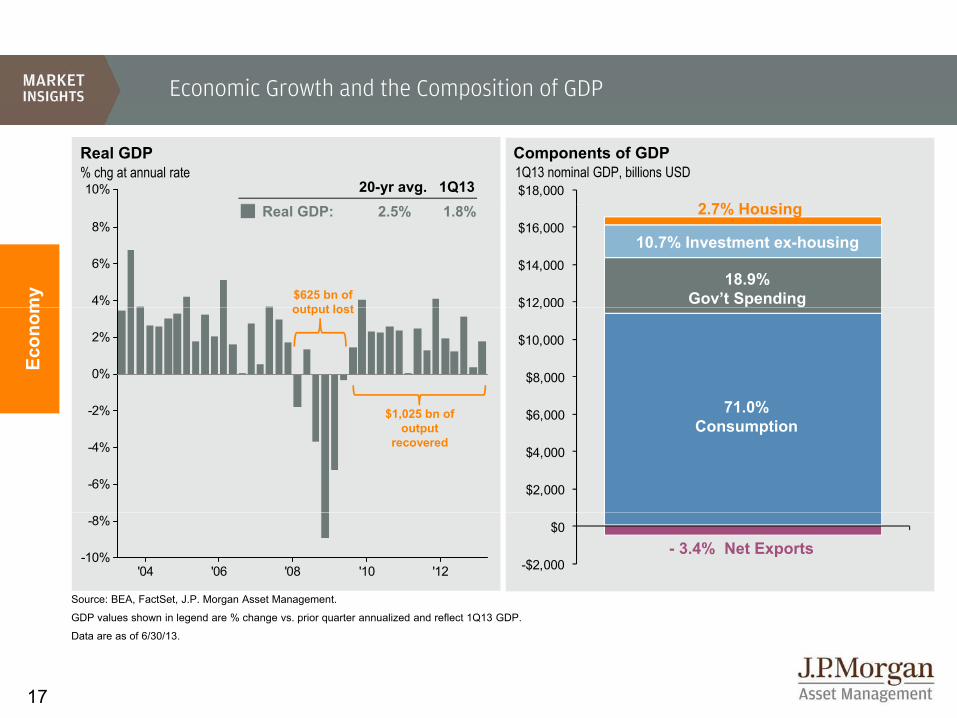

Economic Growth and the Composition of GDP

$18,00010%

Real GDP % chg at annual rate

20-yr avg. 1Q13

Components of GDP1Q13 nominal GDP, billions USD

2 7% H i

$12,000

$14,000

$16,000

4%

6%

8%

my

Real GDP: 2.5% 1.8%

10.7% Investment ex-housing

18.9% Gov�’t Spending

2.7% Housing

$625 bn of output lost

$

$8,000

$10,000

$ ,

2%

0%

2%

Econ

om

71 0%

output lost

$1 025 b f

$2,000

$4,000

$6,000

-6%

-4%

-2% 71.0% Consumption

$1,025 bn of output

recovered

-$2,000

$0

'04 '06 '08 '10 '12-10%

-8%

Source: BEA, FactSet, J.P. Morgan Asset Management.

GDP l h i l d % h i t li d d fl t 1Q13 GDP

- 3.4% Net Exports

17

GDP values shown in legend are % change vs. prior quarter annualized and reflect 1Q13 GDP.

Data are as of 6/30/13.

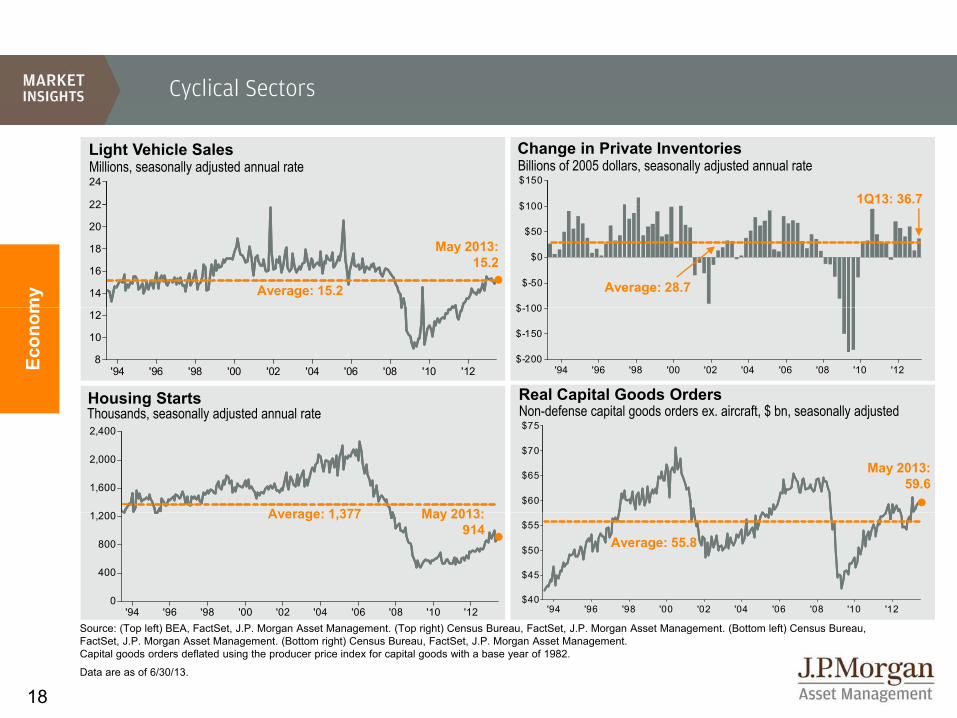

Cyclical Sectors

22

24Millions, seasonally adjusted annual rateLight Vehicle Sales

$100

$150

Change in Private InventoriesBillions of 2005 dollars, seasonally adjusted annual rate

1Q13: 36.7

14

16

18

20

22

my Average: 15.2

May 2013:15.2

$ 100

$-50

$0

$50

$100

Average: 28.7

'94 '96 '98 '00 '02 '04 '06 '08 '10 '128

10

12

Econ

om

Real Capital Goods OrdersNon defense capital goods orders ex aircraft $ bn seasonally adjusted

Housing StartsTh d ll dj t d l t

'94 '96 '98 '00 '02 '04 '06 '08 '10 '12$-200

$-150

$-100

$60

$65

$70

$75

1 200

1,600

2,000

2,400

Non-defense capital goods orders ex. aircraft, $ bn, seasonally adjusted

May 2013:

Thousands, seasonally adjusted annual rate

May 2013:59.6

Average: 1 377

'94 '96 '98 '00 '02 '04 '06 '08 '10 '12$40

$45

$50

$55

'94 '96 '98 '00 '02 '04 '06 '08 '10 '120

400

800

1,200 May 2013:914

Average: 55.8

Average: 1,377

18

94 96 98 00 02 04 06 08 10 12Source: (Top left) BEA, FactSet, J.P. Morgan Asset Management. (Top right) Census Bureau, FactSet, J.P. Morgan Asset Management. (Bottom left) Census Bureau,FactSet, J.P. Morgan Asset Management. (Bottom right) Census Bureau, FactSet, J.P. Morgan Asset Management. Capital goods orders deflated using the producer price index for capital goods with a base year of 1982.

Data are as of 6/30/13.

The Aftermath of the Housing Bubble

$1,100150

Monthly Rent vs. Monthly Mortgage PaymentVacant propertiesIndexed to 100, seasonally adjusted

Home Prices

M thlCase Shiller 20-city

$500

$650

$800

$950

140

my

2Q13*:$727

Monthly Mortgage Payment

Case Shiller 20-cityFHFA Purchase OnlyAverage Existing Home

$200

$350

'88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12

120

130

Econ

om

Home InventoriesMilli l t ll dj t d

2Q13*: $529Monthly Rent

110

Millions, annual rate, seasonally adjusted

3 0

3.5

4.0

4.5

'03 '04 '05 '06 '07 '08 '09 '10 '11 '1290

100

'94 '96 '98 '00 '02 '04 '06 '08 '10 '121.5

2.0

2.5

3.0

May 2013: 2.2

19

Sources: (Left) National Association of Realtors, Standard & Poor’s, FHFA, FactSet, J.P. Morgan Asset Management. (Top right) Census Bureau, J.P. Morgan Asset Management. Monthly mortgage payment assumes a 20% down payment at prevailing 30-year fixed-rate mortgage rates; analysis based on median asking rent and median mortgage payment based on asking price. (Bottom right) Census Bureau, National Association of Realtors, J.P. Morgan Asset Management. *2Q13 rent and mortgagepayment values are J.P. Morgan Asset Management estimates.

Data are as of 6/30/13.

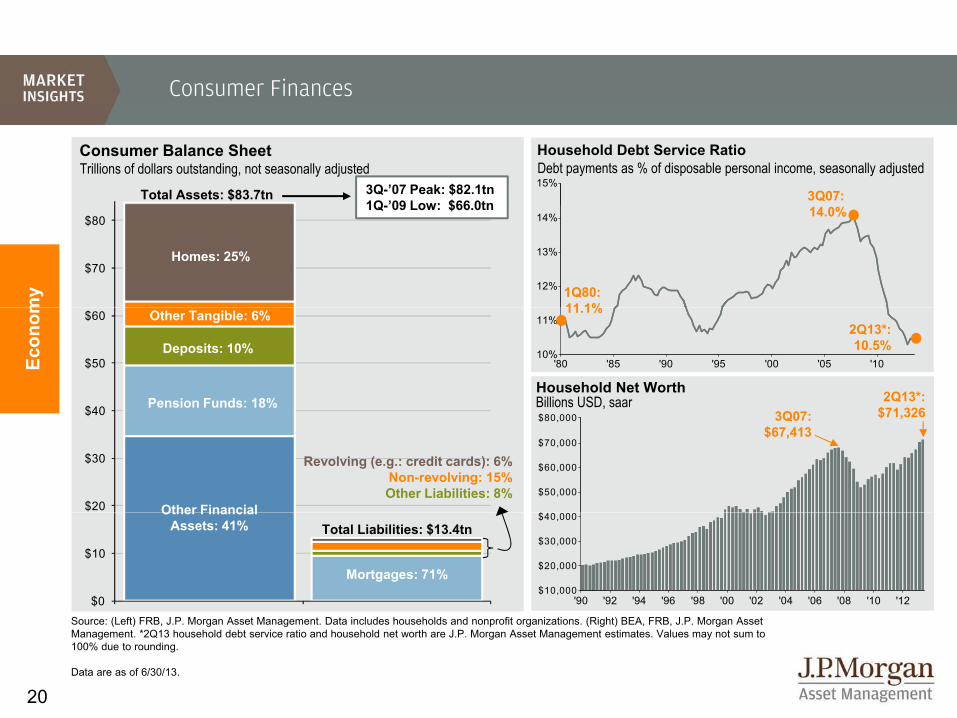

Consumer Finances

15%

Household Debt Service RatioDebt payments as % of disposable personal income, seasonally adjusted

3Q07:

Consumer Balance SheetTrillions of dollars outstanding, not seasonally adjusted

Total Assets: $83.7tn 3Q-�’07 Peak: $82.1tn1Q �’09 Low: $66 0tn

$70

$80

12%

13%

14%

my 1Q80:

11 1%

14.0%

Homes: 25%

1Q- 09 Low: $66.0tn

$40

$50

$60

'80 '85 '90 '95 '00 '05 '1010%

11%

Econ

om 11.1%2Q13*:10.5%

Household Net WorthBillions USD, saar 2Q13*:

$71 326

Deposits: 10%

Pension Funds: 18%

Other Tangible: 6%

$20

$30

$40

$

$50,000

$60,000

$70,000

$80,000 $71,3263Q07:$67,413

Other Financial

Revolving (e.g.: credit cards): 6%Non-revolving: 15%Other Liabilities: 8%

$0

$10

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12$10,000

$20,000

$30,000

$40,000Total Liabilities: $13.4tn

Other Financial Assets: 41%

Mortgages: 71%

20

Source: (Left) FRB, J.P. Morgan Asset Management. Data includes households and nonprofit organizations. (Right) BEA, FRB, J.P. Morgan Asset Management. *2Q13 household debt service ratio and household net worth are J.P. Morgan Asset Management estimates. Values may not sum to 100% due to rounding.

Data are as of 6/30/13.

Federal Finances: Outlays and Revenues

26%$4.0

The 2013 Federal BudgetCBO Baseline forecast, trillions USD

Federal Outlays and Receipts1960 – 2013, % of GDP

24%

$3.0

$3.5

my

Total Spending: $3.5tnOther

$359bn (10%)

Non defense Disc :

Net Int.: $223bn (6%)

Borrowing:$642bn (19%)

$

20%

22%

$2.0

$2.5

Econ

om

Defense:$751bn (22%)

Non-defense Disc.:$461bn (13%)

Average: 20.5% 2013: 21.5%

Social Insurance:$952bn (28%)

Other: $237bn (7%)

16%

18%

$1.0

$1.5Social Security:$809bn (23%)

Income:

Average: 17.9%

2013: 17.5%Corp.: $291bn (8%)

14%

16%

1960 1970 1980 1990 2000 2010$0.0

$0.5

Total Government Spending Sources of Financing

Medicare & Medicaid:$852bn (25%)

Income:$1,333bn (39%) Revenues

Outlays

21

Source: U.S. Treasury, BEA, OMB, CBO, J.P. Morgan Asset Management.2013 Federal Budget is based on the CBO’s May 2013 Baseline Scenario. Other spending includes, but is not limited to, health insurance subsidies, income security, and federal civilian and military retirement. Note: Years shown are fiscal years (Oct. 1 through Sep. 30). Data are as of 6/30/13.

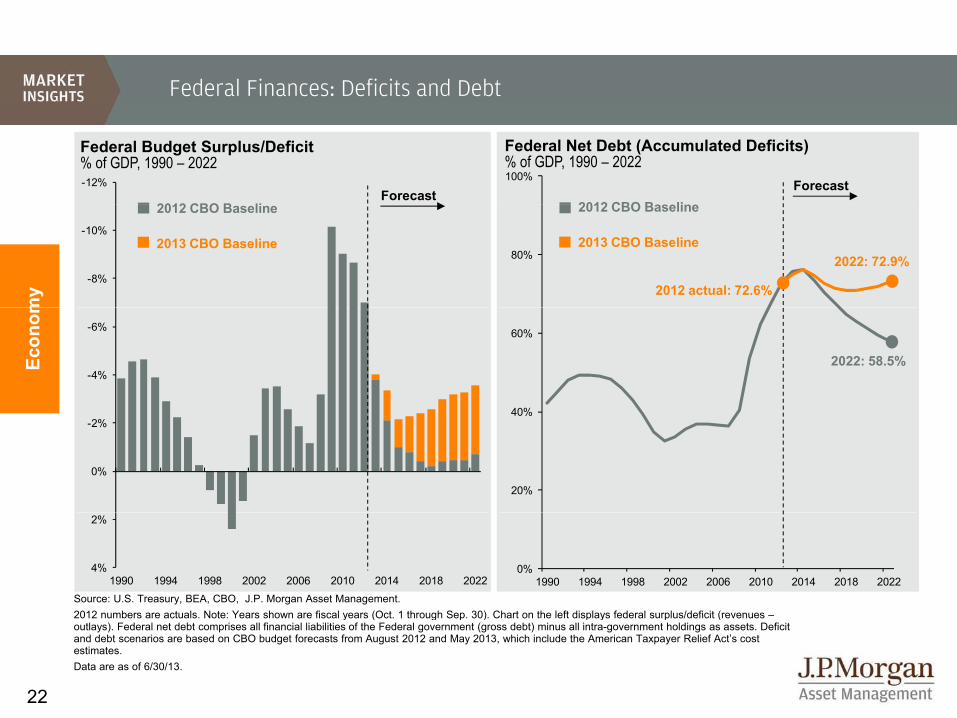

Federal Finances: Deficits and Debt

-12% 100%

Federal Budget Surplus/Deficit Federal Net Debt (Accumulated Deficits)% of GDP, 1990 – 2022 % of GDP, 1990 – 2022

2012 CBO B liForecast

Forecast2012 CBO Baseline

-10%

-8%

80%

my

2012 CBO Baseline

2012 actual: 72.6%

2013 CBO Baseline2022: 72.9%

2012 CBO Baseline

2013 CBO Baseline

-6%

-4%

40%

60%

Econ

om

2022: 58.5%

-2%

0%

20%

40%

2%

4%1990 1994 1998 2002 2006 2010 2014 2018 2022

0%1990 1994 1998 2002 2006 2010 2014 2018 2022

Source: U.S. Treasury, BEA, CBO, J.P. Morgan Asset Management.2012 numbers are actuals Note: Years shown are fiscal years (Oct 1 through Sep 30) Chart on the left displays federal surplus/deficit (revenues

22

2012 numbers are actuals. Note: Years shown are fiscal years (Oct. 1 through Sep. 30). Chart on the left displays federal surplus/deficit (revenues –outlays). Federal net debt comprises all financial liabilities of the Federal government (gross debt) minus all intra-government holdings as assets. Deficit and debt scenarios are based on CBO budget forecasts from August 2012 and May 2013, which include the American Taxpayer Relief Act’s cost estimates. Data are as of 6/30/13.

Trade and the U.S. Dollar

115-8%Current Account Balance, % of GDP U.S. Dollar Index

Nominal trade-weighted exchange index: major currencies

100

105

110

-6%

4Q05:-6.5%

my

90

95

100

-4%

Mar 2009:

Econ

om

80

85

-2%1Q13:-2.7%

Mar. 2009: 84.0

Jun. 2013: 76.1

'94 '96 '98 '00 '02 '04 '06 '08 '10 '1265

70

75

'94 '96 '98 '00 '02 '04 '06 '08 '10 '12

0% Mar. 2008: 70.3

23

94 96 98 00 02 04 06 08 10 1294 96 98 00 02 04 06 08 10 12Source: BEA, FactSet, J.P. Morgan Asset Management.

Data are as of 6/30/13.

Source: Federal Reserve, FactSet, J.P. Morgan Asset Management.

Data are as of 6/30/13.

Employment

60012%

Civilian Unemployment Rate Employment �– Total Private Payroll Seasonally adjusted Total job gain/loss (thousands)

200

400

10%

11%

my 8.8mm

jobs lost

-200

0

8%

9%

Econ

om

May 2013: 7.6%

jobs lost

6.9mm jobs

gained

-600

-400

%

6%

7%gained

-1,000

-800

3%

4%

5% 50-yr. avg.: 6.1%

24

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12,

'70 '80 '90 '00 '10Source: BLS, FactSet, J.P. Morgan Asset Management.

Data are as of 6/30/13.Source: BLS, FactSet, J.P. Morgan Asset Management.

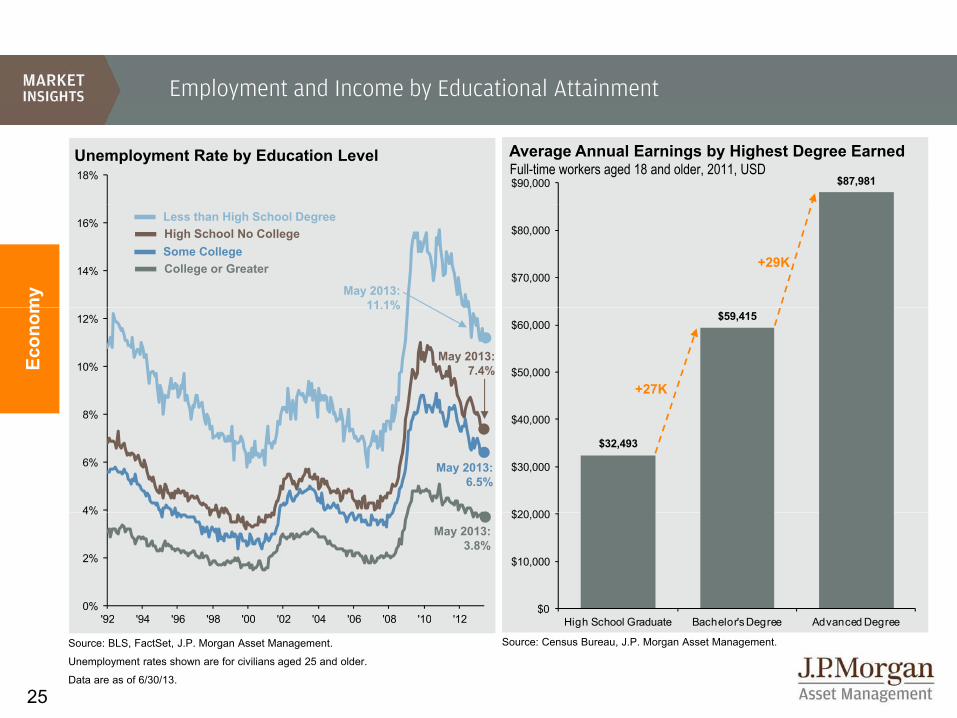

Employment and Income by Educational Attainment

18% $87,981$90,000

Average Annual Earnings by Highest Degree EarnedFull-time workers aged 18 and older, 2011, USD

Unemployment Rate by Education Level

14%

16%

$70,000

$80,000

my

+29K

May 2013:11 1%

Less than High School DegreeHigh School No CollegeSome CollegeCollege or Greater

10%

12% $59,415

$50,000

$60,000

Econ

om

+27K

May 2013:7.4%

11.1%

4%

6%

8%

$32,493

$20 000

$30,000

$40,000

May 2013:6.5%

0%

2%

4%

'92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12$0

$10,000

$20,000May 2013:

3.8%

25

'92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 High School Graduate Bachelor's Degree Advanced Degree

Source: Census Bureau, J.P. Morgan Asset Management.Source: BLS, FactSet, J.P. Morgan Asset Management.

Unemployment rates shown are for civilians aged 25 and older.

Data are as of 6/30/13.

Consumer Price Index

15%

CPI and Core CPI50-yr. Avg. May 2013

Headline CPI: 4.2% 1.4%

% change vs. prior year, seasonally adjustedCPI Components

Weight in CPI

12-month Change

Food & Bev. 15.3% 1.4%

12%

my

Core CPI: 4.1% 1.7%Housing 41.0% 2.2%

Apparel 3.6% 0.2%

Transportation 16.8% -0.5%

6%

9%

Econ

om Medical Care 7.2% 2.2%

Recreation 6.0% 0.8%

Educ. & Comm. 6.8% 1.3%

Other 3 4% 1 8%

0%

3%

Other 3.4% 1.8%

Headline CPI 100.0% 1.4%

Less:

Energy 9.6% -0.8%

'65 '70 '75 '80 '85 '90 '95 '00 '05 '10-3%

Source: BLS, FactSet, J.P. Morgan Asset Management.

Food 14.3% 1.4%

Core CPI 76.1% 1.7%

26

CPI used is CPI-U and values shown are % change vs. 1 year ago and reflect May 2013 CPI data. CPI component weights are as of December 2012 and 12-month change reflects non-seasonally adjusted data through May 2013. Core CPI is defined as CPI excluding food and energy prices.

Data are as of 6/30/13.

Oil and the Economy

$160 $4.50

4%

WTI Crude Oil & Retail Gasoline PricesOil Gas12/31/00 6/30/13

Oil $26.72 $96.56Gas $1 41 $3 58

Economic Drag From Oil PricesU.S. petroleum imports as a % of GDP

3Q08: 3.8%

$120

$140

$3.50

$4.00

2%

3%

my

Gas $1.41 $3.58

$80

$100

$2.50

$3.00

'70 '75 '80 '85 '90 '95 '00 '05 '100%

1%

Econ

om 2Q13*: 2.5%

Total U.S. Energy Net Imports

$40

$60

$1.50

$2.00Energy Spending by Income Level% of after-tax income

20%

25%

30%

35%

Total U.S. Energy Net Imports% of total energy consumption

EIA forecast

$0

$20

$0.50

$1.00

0%

5%

10%

15%

20%

27

'94 '96 '98 '00 '02 '04 '06 '08 '10 '12$0 $0.50

Source: U.S. Department of Energy, FactSet, J.P. Morgan Asset Management. Price of gas based on U.S. retail national average of all formulations and WTI for crude. Imports are mostly crude oil, petroleum and natural gas while consumption includes oil, gas, coal, nuclear, hydropower and bio-fuels.

Data are as of 6/30/13.

Source: (Top) BEA, FactSet, J.P. Morgan Asset Management. (Bottom) EIA, J.P. Morgan Asset Management. *2Q13 drag on growth is a J.P. MorganAsset Management estimate.

0%'90 '95 '00 '05 '10 '15 '20

Global Energy Supply

30

U.S. Natural Gas ProductionTrillions of cubic meters, USD EIA

forecastKuwaitSyria

Middle East Energy Production & Chokepoints Percent of global liquid fuel production, 2012*

10

15

20

25

my Other

Shale Gas

Iran3.9%

Iraq3.9%

3.4%Syria0.2%

Suez Canal2.2%

0

5

1990 1995 2000 2005 2010 2015 2020 2025Econ

om Libya1.8%

Egypt0.8%

S d

Saudi Arabia12.9%

Strait of Hormuz17 0%

Natural Gas Prices by CountrySudan0.1%

UAE3.5%

17.0%

Bab el-Mandeb

y yUSD per mmBTU*

$13.70 $14.10

$10

$12

$14

$16

Bab el Mandeb3.4%

$4.03

$10.11

$2

$4

$6

$8

Major Producers Major ConsumersPercent of global total, 2012 Percent of global total, 2012

Saudi Arabia 13% China 5% United States 21% India 4%United States 12% Canada 4% China 11% Saudi Arabia 3%

28

Source: EIA, J.P. Morgan Asset Management.Forecasts are from the EIA Annual Energy Outlook 2013. *mmBTU represents 10,000 million British thermal units. Natural gas prices are as of June 2012. *Production numbers as of 2012, while chokepoints are 2011 data.

Data are as of 6/30/13.

$0United States United Kingdom China Japan

United States 12% Canada 4% China 11% Saudi Arabia 3%Russia 12% Iran 4% Japan 5% Brazil 3%

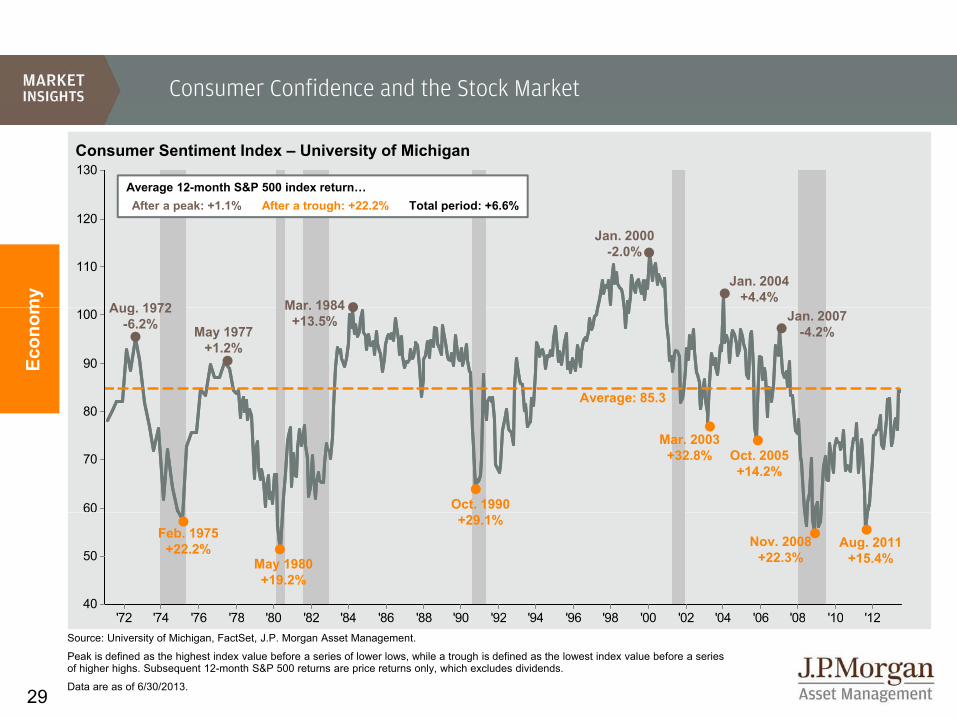

Consumer Confidence and the Stock Market

130Consumer Sentiment Index �– University of Michigan

Average 12-month S&P 500 index return�…After a peak: +1 1% After a trough: +22 2% Total period: +6 6%

110

120

my

Mar 1984

Jan. 2000-2.0%

Jan. 2004+4.4%

Aug 1972

After a peak: +1.1% After a trough: +22.2% Total period: +6.6%

80

90

100

Average: 85.3

Econ

om

Mar. 1984+13.5%

May 1977+1.2%

Aug. 1972-6.2% Jan. 2007

-4.2%

60

70

80

Oct. 1990

Mar. 2003+32.8% Oct. 2005

+14.2%

'72 '74 '76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '1240

50

Feb. 1975+22.2%

May 1980+19.2%

+29.1%Nov. 2008

+22.3%Aug. 2011

+15.4%

29

'72 '74 '76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12Source: University of Michigan, FactSet, J.P. Morgan Asset Management.

Peak is defined as the highest index value before a series of lower lows, while a trough is defined as the lowest index value before a series of higher highs. Subsequent 12-month S&P 500 returns are price returns only, which excludes dividends.

Data are as of 6/30/2013.

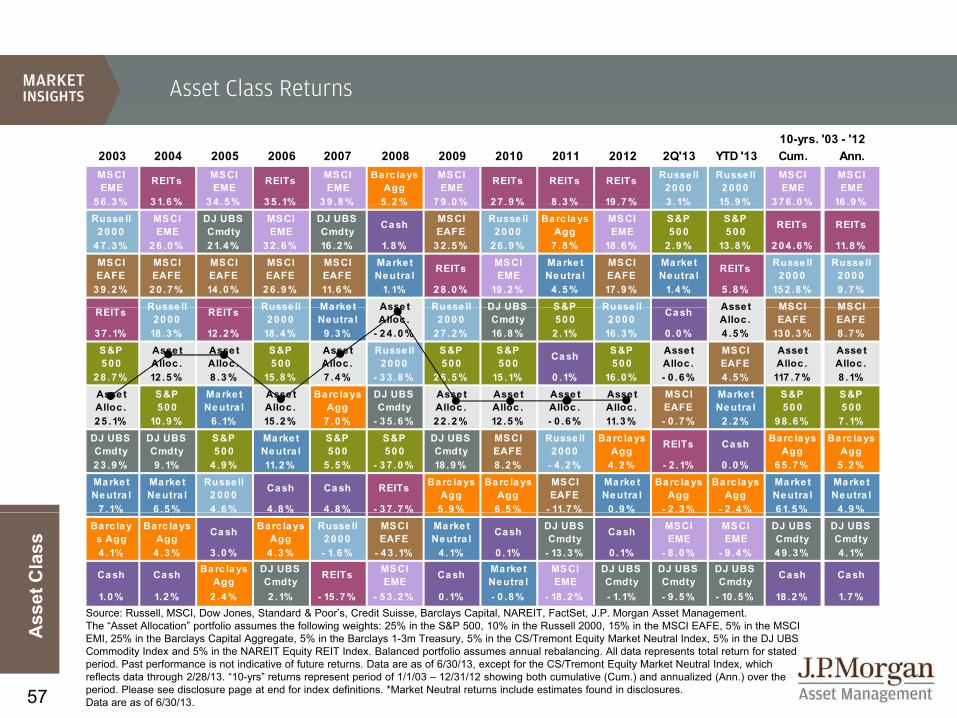

Fixed Income Sector Returns

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 YTD 2Q13 Cum. Ann.

High Yield EMD EMD High Yield TIPS Treas. High Yield High Yield TIPS EMD High Yield High Yield EMD EMD

10-yrs. '03 - '12

29.0% 11.9% 12.3% 11.8% 11.6% 13.7% 58.2% 15.1% 13.6% 17.9% 1.4% -1.4% 200.3% 11.6%

EMD High Yield Asset Alloc. EMD Treas. MBS EMD EMD Muni High Yield MBS Treas. High Yield High Yield

26.9% 11.1% 3.6% 10.0% 9.0% 8.3% 34.2% 12.8% 10.7% 15.8% -2.0% -1.9% 174.3% 10.6%Asset Alloc. TIPS Muni MBS Barclays

AggBarclays

Agg Corp. Corp. Treas. Corp. Treas. MBS Asset Alloc.

Asset Alloc.

9 7% 8 5% 3 5% 5 2% 7 0% 5 2% 18 7% 9 0% 9 8% 9 8% 2 1% 2 0% 94 3% 6 9%9.7% 8.5% 3.5% 5.2% 7.0% 5.2% 18.7% 9.0% 9.8% 9.8% -2.1% -2.0% 94.3% 6.9%

TIPS Asset Alloc. TIPS Asset

Alloc. MBS Asset Alloc.

Asset Alloc.

Asset Alloc.

Asset Alloc.

Asset Alloc.

Barclays Agg

Barclays Agg TIPS TIPS

8.4% 6.3% 2.8% 5.1% 6.9% -1.4% 15.8% 7.6% 8.9% 7.8% -2.4% -2.3% 90.4% 6.7%

Corp. Corp. Treas. Muni Asset Alloc. TIPS Muni Barclays

Agg Corp. TIPS Muni Muni Corp. Corp.

8.2% 5.4% 2.8% 4.8% 6.2% -2.4% 12.9% 6.5% 8.1% 7.0% -2.7% -3.0% 84.7% 6.3%

ncom

e

Muni MBS High Yield Barclays Agg EMD Muni TIPS TIPS Barclays

Agg Muni Asset Alloc.

Asset Alloc.

Barclays Agg

Barclays Agg

5.3% 4.7% 2.7% 4.3% 5.2% -2.5% 11.4% 6.3% 7.8% 6.8% -3.1% -3.1% 65.7% 5.2%Barclays

Agg Muni MBS Corp. Corp. Corp. Barclays Agg Treas. EMD Barclays

Agg Corp. Corp. Muni Muni

4.1% 4.5% 2.6% 4.3% 4.6% -4.9% 5.9% 5.9% 7.0% 4.2% -3.4% -3.3% 64.5% 5.1%Barclays Barclays

Fixe

d In

MBS Barclays Agg

Barclays Agg Treas. Muni EMD MBS MBS MBS MBS EMD EMD MBS MBS

3.1% 4.3% 2.4% 3.1% 3.4% -14.7% 5.9% 5.4% 6.2% 2.6% -6.5% -5.1% 64.1% 5.1%

Treas. Treas. Corp. TIPS High Yield High Yield Treas. Muni High Yield Treas. TIPS TIPS Treas. Treas.

2.2% 3.5% 1.7% 0.4% 1.9% -26.2% -3.6% 2.4% 5.0% 2.0% -7.4% -7.0% 59.0% 4.7%Source: Barclays Capital, FactSet, J.P. Morgan Asset Management.

30

Past performance is not indicative of future returns. Fixed income sectors shown above are provided by Barclays Capital and are represented by: Barclays Capital U.S. Aggregate Index; MBS: Fixed Rate MBS Index; Corporate: U.S. Corporates; Municipals: Muni Bond Index; Emerging Debt: Emerging Markets USD Index; High Yield: Corporate High Yield Index; Treasuries: Barclays Capital U.S. Treasury; TIPS: Barclays Capital TIPS. The “Asset Allocation” portfolio assumes the following weights:10% in MBS, 20% in Corporate, 15% in Municipals, 10% in Emerging Debt, 10% in High Yield, 25% in Treasuries, 10% in TIPS. Asset allocation portfolio assumes annual rebalancing.Data are as of 6/30/13.

Interest Rates and Inflation

20%Nominal and Real 10-year Treasury Yields

S 30 1981

15%

Sep. 30, 1981: 15.84%

Average 6/30/13 Nominal Yields 6.42% 2.49%Real Yields 2.55% 0.81%

10%

ncom

e Nominal 10-year Treasury Yield

5%

Fixe

d In Jun. 30, 2013: 2.49%

Real 10-year Treasury Yield

-5%

0%

Jun. 30, 2013: 0.81%

Treasury Yield

Rising Rate Corp. Bonds S&P 500 1958-1981 3.0% 8.6% Ann. Inflation 5.0% 5.0% Ann. Real Return -2.0% 3.5%

Falling Rate Corp. Bonds S&P 500 1982-2012 10.1% 11.0% Ann. Inflation 3.1% 3.1% Ann. Real Return 6.8% 7.7%

31

'60 '65 '70 '75 '80 '85 '90 '95 '00 '05 '10-5%

Source: Federal Reserve, BLS, J.P. Morgan Asset Management.Real 10-year Treasury yields are calculated as the daily Treasury yield less year-over-year core inflation for that month except for June 2013, where real yields are calculated by subtracting out May 2013 year-over-year core inflation. All returns above reflect annualized total returns, which include reinvestment of dividends. Corporate bond returns are based on a composite index of investment grade bond performance.Data are as of 6/30/13.

Fixed Income Yields and Returns

Price Impact of a 1% Rise/Fall in Interest Rates*

+1%-1%

-4 9%

-2.0%4.9%

0.7%

5y UST

2y USTUS Treasuries # of issues Correlation to

10-yearAvg.

Maturity 6/30/2013 6/30/2012 2Q13 YTD 2013

Yield Return

-20.0%

-9.3%

-7.2%

-4.9%

20.0%

9.3%

7.2%

30y UST

10y UST

TIPS 2-Year 77 0.69 2 years 0.36% 0.33% -0.09% 0.00%

5-Year 60 0.92 5 1.41% 0.72% -2.43% -2.26%

10-Year 20 1.00 10 2.52% 1.67% -4.57% -4.87%

30-Year 18 0.92 30 3.52% 2.76% -6.13% -9.01%

TIPS 34 0 63 10 0 53% 0 46% 7 05% 7 39%

ncom

e

-4.9%

-4.4%

-3.0%

-0.1%

4.9%

4.4%

3.5%

0.0%

EMD (LCL)

US HY

Convertibles

Floating Rate TIPS 34 0.63 10 0.53% -0.46% -7.05% -7.39%

Sector

Broad Market 8,413 0.88 7.5 years 2.35% 1.98% -2.32% -2.44%

MBS 766 0.83 7.1 3.12% 2.44% -1.96% -2.01%

Municipals 9,054 0.54 9.9 2.79% 2.26% -3.11% -2.77%

Fixe

d In

-6.6%

-5.9%

-5.5%

-5.2%

6.6%

5.9%

5.5%

5.2%

Munis

EMD ($)

US Aggregate

MBSp ,

Corporates 4,632 0.53 10.2 3.35% 3.27% -3.31% -3.41%

High Yield 2,057 -0.19 6.7 6.66% 7.35% -1.44% 1.42%

Floating Rate 31 -0.21 2.9 1.64% 3.16% -0.15% 1.03%

Convertibles 490 -0.29 -- 1.09% 0.90% 1.80% 9.24%

Source: U.S. Treasury, Barclays Capital, FactSet, J.P. Morgan Asset Management.Fixed income sectors shown above are provided by Barclays Capital and are represented by – Broad Market: Barclays U.S. Aggregate; MBS: Fixed Rate MBS Index; Corporate: U.S. Corporates; Municipals: Muni Bond Index; EMD ($): Emerging Markets (USD); High Yield: Corporate High Yield Index; TIPS: Treasury Inflation Protection Securities (TIPS). EMD (LCL): Barclays Emerging Market Local Currency Government; Floating Rate: Barclays U.S. Floating Rate Notes (BBB); Convertibles: Barclays U.S. Convertibles Composite. Treasury securities

-6.9%6.9%

-30% -20% -10% 0% 10% 20% 30%

IG Corps EMD ($) 1,125 0.25 9.3 5.40% 5.44% -5.14% -6.52%

EMD (LCL) 460 0.03 6.9 5.55% 5.57% -6.48% -6.16%

32

y g g y g y g ( ) y p ydata for # of issues based on U.S. Treasury benchmarks from Barclays Capital. Yield and return information based on Bellwethers for Treasury securities. Sector yields reflect yield to worst, while Treasury yields are yield to maturity. Correlations are based on 10-years of monthly returns for all sectors except Floating Rate and EMD (LCL), which are based on monthly returns from May 2004 and July 2008, respectively, due to data availability. Change in bond price is calculated using both duration and convexity according to the following formula: New Price = (Price + (Price * -Duration * Change in Interest Rates))+(0.5 * Price * Convexity * (Change in Interest Rates)^2). *Calculation assumes 2-year Treasury interest rate falls 0.36% to 0.00%,as interest rates can only fall to 0.00%. Chart is for illustrative purposes only. Past performance is not indicative of future results. Data are as of 6/30/13.

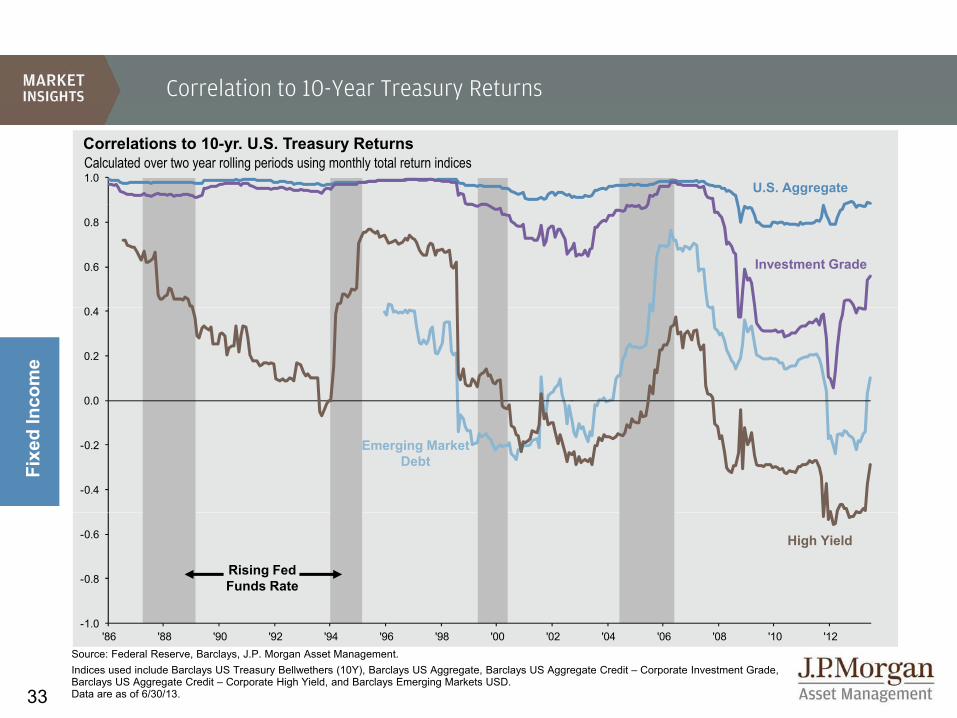

Correlation to 10-Year Treasury Returns

1.0

Correlations to 10-yr. U.S. Treasury Returns

U.S. Aggregate

Calculated over two year rolling periods using monthly total return indices

0.6

0.8

Investment Grade

0.0

0.2

0.4

ncom

e

-0.4

-0.2 Emerging Market DebtFi

xed

In

-0.8

-0.6

Rising Fed Funds Rate

High Yield

33

-1.0'86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12

Source: Federal Reserve, Barclays, J.P. Morgan Asset Management.Indices used include Barclays US Treasury Bellwethers (10Y), Barclays US Aggregate, Barclays US Aggregate Credit – Corporate Investment Grade, Barclays US Aggregate Credit – Corporate High Yield, and Barclays Emerging Markets USD.Data are as of 6/30/13.

The Fed and the Money Supply

Money MultiplierM2 / Monetary Base

Fed�’s Balance Sheet: Assets$ trillions

9 x

10.x

Oth$3 5

$4.0

5.x

6.x

7.x

8.x

9.xOtherU.S. TreasuriesAgency MBS

Jun. 2013:3 3x

$1.5

$2.0

$2.5

$3.0

$3.5

Fed�’s Balance Sheet: Liabilities$ t illinc

ome

Federal Funds Rate & FOMC Interest Rate Projections

'04 '05 '06 '07 '08 '09 '10 '11 '122.x

3.x

4.x 3.3x

$0.0

$0.5

$1.0

'04 '05 '06 '07 '08 '09 '10 '11 '12

$2 0

$2.5

$3.0

$3.5

$4.0

6%

8%

10%

12%$ trillions

Fixe

d In

Long-term Fed projection

Other LiabilitiesExcess Reserves

Required Reserves

'04 '05 '06 '07 '08 '09 '10 '11 '12$0.0

$0.5

$1.0

$1.5

$2.0

0%

2%

4%

'84 '88 '92 '96 '00 '04 '09 '12 '14

Jun. 30, 2013:0.0%-0.25%

34

Source: Federal Reserve, FactSet, J.P. Morgan Asset Management.

Monetary base is defined as the total amount of a currency that is either circulated in the hands of the public or in the commercial bank deposits held in the central bank's reserves. Money multiplier defined as M2 divided by the monetary base. Long-term Fed projection is based on average expectations of FOMC members. Other liabilities of the Federal Reserve primarily consist of the monetary base.

Data are as of 6/30/13.

Credit Conditions

760 60%

Commercial & Industrial Loan DemandNet percent of banks reporting stronger demand

Small Firms

Lending Standards for Approved Mortgage LoansAverage FICO score based on origination date

700

720

740

-40%

-20%

0%

20%

40% Large & Medium Firms

6%

8%Apr. 2013:

745

660

680

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Delinquency RatesAll b k ll dj t dnc

ome

Common Equity as a % of Total AssetsAll FDIC insured institutions 1934 2012

'94 '96 '98 '00 '02 '04 '06 '08 '10 '12-80%

-60%

-40% 6%

10%

12%

14%

8%

10%

12%

Consumer LoansResidential Mortgages

All banks, seasonally adjusted

Fixe

d In

Commercial and Industrial Loans 9.7%

All FDIC insured institutions, 1934 – 2012

2012:11.1%

4%

6%

8%

'34 '41 '48 '55 '62 '69 '76 '83 '90 '97 '04 '11'92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12

2%

4%

6%

1.5%

2.5%

Average: 7.6%

35

34 41 48 55 62 69 76 83 90 97 04 11Source: (Top left) McDash, J.P. Morgan Securitized Product Research, J.P. Morgan Asset Management. (Top right) Federal Reserve, FactSet, J.P. Morgan Asset Management. (Bottom left): Federal Reserve, FactSet, J.P. Morgan Asset Management. (Bottom right) FDIC, J.P. Morgan Asset Management.All data reflect most recently available releases. Data are as of 6/30/13.

High Yield Bonds

15%

20%Average Latest

HY Spreads 5.9% 5.4%Lev. Loan Spreads 5.1% 4.1%HY Defaults Rates 4.2% 1.1%

High Yield Spreads and Defaults

L L S dHY Spreads

5%

10%

15% Lev. Loan Spreads

HY Default Rates

0%'88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12

ncom

e

Historical High Yield Recovery RatesHigh yield bonds, cents on the dollar

Annual Flows into High Yield and Leveraged Loan FundsMutual funds & ETFs, billions USD YTD 2013: $30 0bn

$20

$30

$40

$50

Fixe

d In

g y e d bo ds, ce ts o t e do a

Average: 40.1¢

, YTD 2013: $30.0bn

High YieldLeveraged Loans

40¢

50¢

60¢

70¢

-$20

-$10

$0

$10

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '130¢

10¢

20¢

30¢

'88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12

36

Source (Top chart): U.S. Treasury, J.P. Morgan, Strategic Insight, J.P. Morgan Asset Management. Default rates are defined as the par value percentage of the total market trading at or below 50% of par value and include any Chapter 11 filing, prepackaged filing or missed interest payments. (Bottom left): J.P Morgan, Fitch, J.P. Morgan Asset Management. (Bottom right): Strategic Insight, J.P. Morgan Asset Management. Spreads indicated are benchmark yield to worst less comparable maturity Treasury yields. 2013 recovery rate is a weighted average number as of May 2013. Yield to worst is defined as the lowest potential yield that can be received on a bond without the issuer actually defaulting and reflects the possibility of the bond being called at an unfavorable time for the holder. Flows include ETFs and are as of May 2013. Past performance is not indicative of comparable future results.Data are as of 6/30/13.

Municipal Finance

8%

State & Local Government Debt Service% of current expenditures

Muni/Treasury RatioRatio of Barclays 10-year Municipal Bond yield to 10-year Treasury240%

5%

6%

7%

200%

220%

1Q13: 5.2%

4%

5%

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12

ncom

e

Municipal Bond Issuance*Billions USD, revenue and GO issues140%

160%

180%

Fixe

d In

o s US , e e ue a d GO ssues

100%

120%

140%

$300bn

$400bn

$500bn

'00 '02 '04 '06 '08 '10 '1260%

80% Jun. 30, 2013:111%

$0bn

$100bn

$200bn

'96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

37

Source (Left chart): Barclays Capital, U.S. Treasury, FactSet, J.P. Morgan Asset Management. (Top right) BEA, J.P. Morgan Asset Management. (Bottom right) SIFMA,J.P. Morgan Asset Management.*Excludes maturities of 13 months or less and private placements. 2013 issuance data is as of May 2013.

Data are as of 6/30/13.

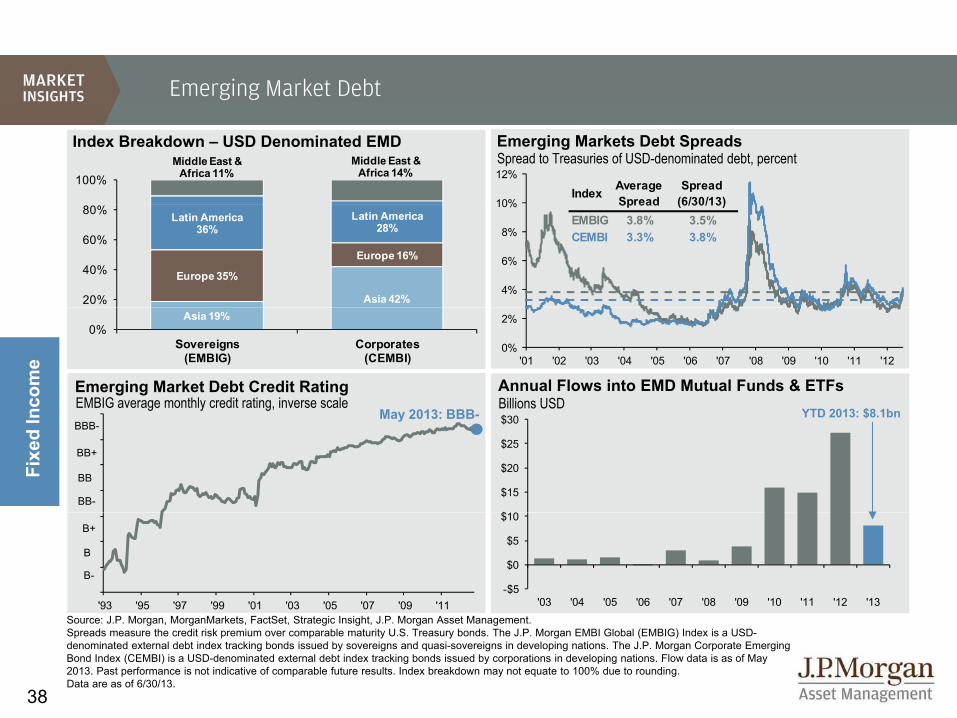

Emerging Market Debt

10%

12%

Emerging Markets Debt SpreadsSpread to Treasuries of USD-denominated debt, percent

Index Breakdown �– USD Denominated EMDMiddle East &

Africa 11%Middle East &

Africa 14%100%Index Average

SpreadSpread

(6/30/13)

4%

6%

8%

10%

Asia 42%

Europe 35%

Europe 16%

Latin America36%

Latin America28%

20%

40%

60%

80%Spread (6/30/13)

EMBIG 3.8% 3.5%CEMBI 3.3% 3.8%

0%

2%

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

ncom

e

Annual Flows into EMD Mutual Funds & ETFsBillions USD

Emerging Market Debt Credit RatingEMBIG average monthly credit rating, inverse scale

M 2013 BBB YTD 2013 $8 1b

Asia 19%0%

Sovereigns(EMBIG)

Corporates(CEMBI)

$10

$15

$20

$25

$30

Fixe

d In

g y gMay 2013: BBB-

BB+

BBB-

BB

BB-

YTD 2013: $8.1bn

'93 '95 '97 '99 '01 '03 '05 '07 '09 '11-$5

$0

$5

$10

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

B-

B

B+

38

Source: J.P. Morgan, MorganMarkets, FactSet, Strategic Insight, J.P. Morgan Asset Management. Spreads measure the credit risk premium over comparable maturity U.S. Treasury bonds. The J.P. Morgan EMBI Global (EMBIG) Index is a USD-denominated external debt index tracking bonds issued by sovereigns and quasi-sovereigns in developing nations. The J.P. Morgan Corporate Emerging Bond Index (CEMBI) is a USD-denominated external debt index tracking bonds issued by corporations in developing nations. Flow data is as of May 2013. Past performance is not indicative of comparable future results. Index breakdown may not equate to 100% due to rounding.Data are as of 6/30/13.

Global Equity Markets: Returns

MSCI EAFE Index: Return Needed to Reach 2007 PeakAnalysis as of Jun. 30, 2013, implied average annualized total return

47.0%1 YrCountry / Region

2Q13 YTD 2013

Local USD Local USD

23.2%

16.2%

2 Yrs

3 Yrs

Regions / Broad IndexesUSA (S&P 500) - 2.9 - 13.8

EAFE 1.4 -0.7 11.4 4.5

Europe ex U K 0 4 0 9 6 2 4 0

MSCI EME Index: Return Needed to Reach 2007 Peak

12.9%

10.9%

4 Yrs

5 Yrs

Europe ex-U.K. 0.4 0.9 6.2 4.0

Pacif ic ex-Japan -2.9 -10.9 3.9 -4.6

Emerging Markets -4.3 -8.0 -4.7 -9.4

MSCI: Selected Countries

onal

Analysis as of Jun. 30, 2013, implied average annualized total return

28.1%

14.8%

1 Yr

2 Yrs

MSCI: Selected CountriesUnited Kingdom -2.0 -2.1 7.5 0.3

France 2.2 3.5 5.6 4.1

Germany 2.2 3.4 5.2 3.7

Japan 10 2 4 3 34 0 16 6

Inte

rnat

i

10.7%

8.7%

7 5%

3 Yrs

4 Yrs

5 Yrs

Japan 10.2 4.3 34.0 16.6

China -6.6 -6.5 -10.7 -10.8

India 3.2 -5.6 -0.2 -8.0

Brazil -9.3 -17.2 -11.4 -17.8

39

Source: Standard & Poor’s, MSCI, IMF, FactSet, J.P. Morgan Asset Management.All return values are MSCI Gross Index (official) data. Definition of emerging markets is based on MSCI data. Data assume dividend yields as of 6/30/13 (MSCI EAFE: 3.4% and MSCI EM: 2.9%). Chart is for illustrative purposes only. Past performance is not indicative of future results. Please see disclosure page for index definitions. Data as of 6/30/13.

7.5%5 YrsRussia -4.1 -8.3 -5.8 -11.2

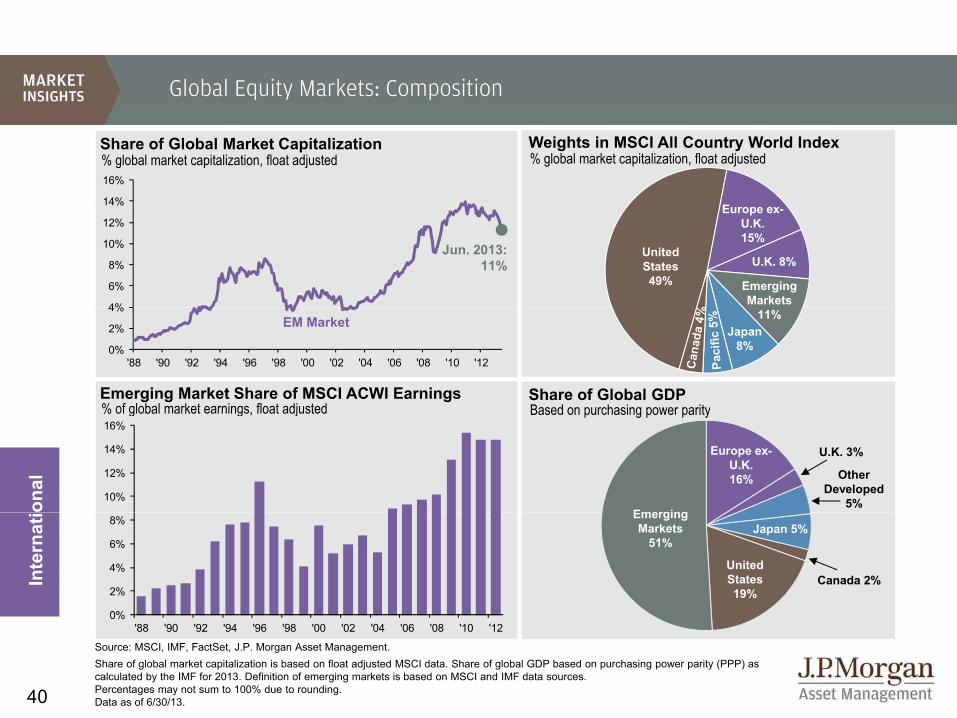

Global Equity Markets: Composition

14%

16%

Weights in MSCI All Country World Index% global market capitalization, float adjusted

E

Share of Global Market Capitalization% global market capitalization, float adjusted

4%

6%

8%

10%

12%

14%

United States49%

Europe ex-U.K.15%

U.K. 8%

EmergingMarkets

Jun. 2013: 11%

0%

2%

4%

'88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12

Share of Global GDPBased on purchasing power parity

11%Japan

8%

Emerging Market Share of MSCI ACWI Earnings% of global market earnings float adjusted

EM Market

onal

Based on purchasing power parity

Emerging

Other Developed

5%

Europe ex-U.K.16%

U.K. 3%

% of global market earnings, float adjusted

10%

12%

14%

16%

Canada 2%Inte

rnat

i EmergingMarkets

51%

United States19%

Japan 5%

0%

2%

4%

6%

8%

40

Source: MSCI, IMF, FactSet, J.P. Morgan Asset Management.Share of global market capitalization is based on float adjusted MSCI data. Share of global GDP based on purchasing power parity (PPP) as calculated by the IMF for 2013. Definition of emerging markets is based on MSCI and IMF data sources. Percentages may not sum to 100% due to rounding.Data as of 6/30/13.

0%'88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12

Global Economic Growth

Year-over-year % chg. – forecasts from JPMSIEmerging Market Country Real GDP Growth

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

Historical

1Q14

JPMSI Forecast

10%

0%

2%

4%

6%

8%

Developed Market Country Real GDP Growth Historical JPMSI Forecast

-4%

-2%

0%

Emerging Markets China India Mexico South Africa Korea Russia Brazil

Year-over-year % chg. – forecasts from JPMSI

onal

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

Historical

1Q14

JPMSI Forecast

4%

6%

8%

10%

Inte

rnat

i

-4%

-2%

0%

2%

Developed Countries

U.S. Canada U.K. Japan Germany France Italy

41

Source: J.P. Morgan Global Economic Research, J.P. Morgan Asset Management.

Forecast and aggregate data come from J.P. Morgan Global Economic Research. Historical growth data collected from FactSet Economics.

Data are as of 6/30/13.

Manufacturing Momentum

Global Purchasing Managers�’ Index for Manufacturing

ul'1

1

ug'1

1

ep'1

1

ct'1

1

ov'1

1

ec'1

1

an'1

2

eb'1

2

ar'1

2

pr'1

2

ay'1

2

un'1

2

ul'1

2

ug'1

2

ep'1

2

ct'1

2

ov'1

2

ec'1

2

an'1

3

eb'1

3

ar'1

3

pr'1

3

ay'1

3

un'1

3

Ju Au

Se Oc

No

De

Ja Fe Ma

Ap

Ma

Ju Ju Au

Se Oc

No

De

Ja Fe Ma

Ap

Ma

Ju

Global 51.3 51.2 50.5 50.7 49.6 50.3 51.0 51.2 51.6 51.3 50.2 49.7 48.8 48.7 48.7 48.8 49.6 50.0 51.5 50.9 51.2 50.4 50.6 50.6U.S. 52.6 53.9 53.7 53.6 53.4 53.9 54.3 53.6 56.0 56.0 54.0 52.5 51.4 51.5 51.1 51.0 52.8 54.0 55.8 54.3 54.6 52.1 52.3 51.9U.K. 50.3 49.7 51.3 48.9 47.9 49.2 50.7 51.1 51.8 49.9 46.1 48.3 45.6 49.7 48.9 47.7 49.0 50.9 50.9 48.2 49.0 50.2 51.5 52.5Germany 52.0 50.9 50.3 49.1 47.9 48.4 51.0 50.2 48.4 46.2 45.2 45.0 43.0 44.7 47.4 46.0 46.8 46.0 49.8 50.3 49.0 48.1 49.4 48.6France 50.5 49.1 48.2 48.5 47.3 48.9 48.5 50.0 46.7 46.9 44.7 45.2 43.4 46.0 42.7 43.7 44.5 44.6 42.9 43.9 44.0 44.4 46.4 48.4France 50.5 49.1 48.2 48.5 47.3 48.9 48.5 50.0 46.7 46.9 44.7 45.2 43.4 46.0 42.7 43.7 44.5 44.6 42.9 43.9 44.0 44.4 46.4 48.4Italy 50.1 47.0 48.3 43.3 44.0 44.3 46.8 47.8 47.9 43.8 44.8 44.6 44.3 43.6 45.7 45.5 45.1 46.7 47.8 45.8 44.5 45.5 47.3 49.1Spain 45.6 45.3 43.7 43.9 43.8 43.7 45.1 45.0 44.5 43.5 42.0 41.1 42.3 44.0 44.5 43.5 45.3 44.6 46.1 46.8 44.2 44.7 48.1 50.0Greece 45.2 43.3 43.2 40.5 40.9 42.0 41.0 37.7 41.3 40.7 43.1 40.1 41.9 42.1 42.2 41.0 41.8 41.4 41.7 43.0 42.1 45.0 45.3 45.4Ireland 48.2 49.7 47.3 50.1 48.5 48.6 48.3 49.7 51.5 50.1 51.2 53.1 53.9 50.9 51.8 52.1 52.4 51.4 50.3 51.5 48.6 48.0 49.7 50.3Australia 43.4 43.3 42.3 47.4 47.8 50.2 51.6 51.3 49.5 43.9 42.4 47.2 40.3 45.3 43.0 42.8 44.3 44.3 40.2 45.6 44.4 36.7 43.8 49.6J 52 1 51 9 49 3 50 6 49 1 50 2 50 7 50 5 51 1 50 7 50 7 49 9 47 9 47 7 48 0 46 9 46 5 45 0 47 7 48 5 50 4 51 1 51 5 52 3

onal

Japan 52.1 51.9 49.3 50.6 49.1 50.2 50.7 50.5 51.1 50.7 50.7 49.9 47.9 47.7 48.0 46.9 46.5 45.0 47.7 48.5 50.4 51.1 51.5 52.3China 49.3 49.9 49.9 51.0 47.7 48.7 48.8 49.6 48.3 49.3 48.4 48.2 49.3 47.6 47.9 49.5 50.5 51.5 52.3 50.4 51.6 50.4 49.2 48.2Indonesia 50.9 50.8 49.7 51.6 50.1 48.8 48.5 50.6 50.8 50.5 48.1 50.2 51.4 51.6 50.5 51.9 51.5 50.7 49.7 50.5 51.3 51.7 51.6 51.0Korea 51.3 49.7 47.5 48.0 47.1 46.4 49.2 50.7 52.0 51.9 51.0 49.4 47.2 47.5 45.7 47.4 48.2 50.1 49.9 50.9 52.0 52.6 51.1 49.4Taiwan 46.1 45.2 44.5 43.7 43.9 47.1 48.9 52.7 54.1 51.2 50.5 49.2 47.5 46.1 45.6 47.8 47.4 50.6 51.5 50.2 51.2 50.7 47.1 49.5India 53.6 52.6 50.4 52.0 51.0 54.2 57.5 56.6 54.7 54.9 54.8 55.0 52.9 52.8 52.8 52.9 53.7 54.7 53.2 54.2 52.0 51.0 50.1 50.3

Source: Markit, J.P. Morgan Asset Management.

H t l b d PMI l ti t th 50 l l hi h i di t i t ti f th t f th ti i d h

Inte

rnat

i

Brazil 47.8 46.0 45.5 46.5 48.7 49.1 50.6 51.4 51.1 49.3 49.3 48.5 48.7 49.3 49.8 50.2 52.2 51.1 53.2 52.5 51.8 50.8 50.4 50.4Mexico 54.7 51.7 53.0 54.7 53.7 53.1 52.2 53.7 53.8 56.3 55.2 55.9 55.2 55.1 54.4 55.5 55.6 57.1 55.0 53.4 52.2 51.7 51.7 51.3Russia 49.8 49.9 50.0 50.4 52.6 51.6 50.8 50.7 50.8 52.9 53.2 51.0 52.0 51.0 52.4 52.9 52.2 50.0 52.0 52.0 50.8 50.6 50.4 51.7

42

Heatmap colors are based on PMI relative to the 50 level, which indicates expansion or contraction of the sector, for the time period shown.

Data are as of 6/30/13.

The Importance of Exports

1.0%1.7% 2.1% 5.2%Brazil

Latest 12 months, goods exportedExports as a % of GDP

U.S. Eurozone BRIC Other9 9%1.0%

1.9%

4.3%

2.0%

1.7%

2.0%

2.8%

7.3%

2.1%

1.4%

1.6%

0.6%

5.2%

11.5%

17.5%

21.1%

Brazil

India

China

Russia

9.9%

16.8%

26.2%

31.0%

1.8%

1.2% 1.2%

2.2%

7.5%

9.1%

U.S.

Eurozone

10.0%

13.2%

2.4%

2.7%

2.1%

0.9%

8.6%

10.0%

2.8%

1.6%

1.1%

7.3%

6.6%

8.6%

Japan

U.K.

France

onal

19.5%

21.9%

13.5%

1.7%

3.3%

13.0%

15.5%

1.8%

4.7%

8.4%

17.9%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Italy

Germany

Source: IMF MDIC Indian Ministry of Commerce & Industry China Customs Bank of Russia BEA Japan Customs ONS French Ministry of Economy Finance &

Inte

rnat

i

24.8%

41.3%

43

Source: IMF, MDIC, Indian Ministry of Commerce & Industry, China Customs, Bank of Russia, BEA, Japan Customs, ONS, French Ministry of Economy, Finance & Industry, ISTAT, German Federal Statistics Office, FactSet, J.P. Morgan Asset Management.

Values may not sum to total exports due to rounding.

Data are as of 6/30/13.

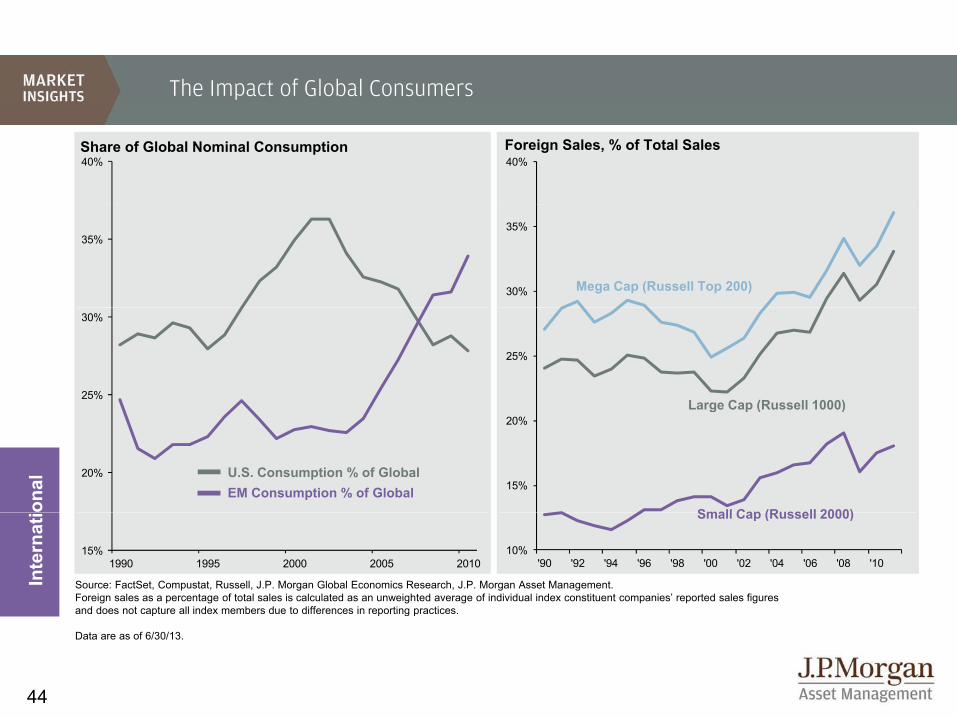

The Impact of Global Consumers

40% 40%Share of Global Nominal Consumption Foreign Sales, % of Total Sales

35%

30%

35%

Mega Cap (Russell Top 200)

25%

30%

25%

Large Cap (Russell 1000)

20%15%

20%

onal

U.S. Consumption % of GlobalEM Consumption % of Global

Small Cap (Russell 2000)

g p ( )

15%1990 1995 2000 2005 2010

10%'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10

Source: FactSet, Compustat, Russell, J.P. Morgan Global Economics Research, J.P. Morgan Asset Management.Foreign sales as a percentage of total sales is calculated as an unweighted average of individual index constituent companies’ reported sales figures and does not capture all index members due to differences in reporting practices.

Inte

rnat

i Small Cap (Russell 2000)

44

p p g p

Data are as of 6/30/13.

Sovereign Debt Stresses

China

10%Bubble size = 10-year

government bond yield

GDP Growth, Gross Debt to GDP and Borrowing Costs

India

Indonesia

Malaysia

10%

5%

4%

6%

8%

014F

)

Brazil

South Africa

Mexico

US

Turkey

Korea

FranceGermany

Japan

Russia Singapore

EU

Australia

UK0%

2%

4%

Gro

wth

(201

2 �–

2

Greece

ItalySpain

Portugal

-4%

-2%

Rea

l GD

P G

onal

-8%

-6%

0% 20% 40% 60% 80% 100% 120% 140% 160% 180% 200%G D bt t GDP R ti (2013F)

Developed MarketsEmerging Markets

Inte

rnat

i

240%

45

Gross Debt-to-GDP Ratios (2013F)Source: IMF, FactSet, Bloomberg, J.P. Morgan Economics, Barclays, J.P. Morgan Asset Management.

Growth and debt data are based on the April 2013 World Economic Outlook.Borrowing costs based on local currency debt. EU overall borrowing cost based on Barclays Capital Euro-Aggregate 7-10 year treasury. South Africa’sborrowing cost is based on 7-year government bond yield due to data availability.

Data as of 6/30/13.

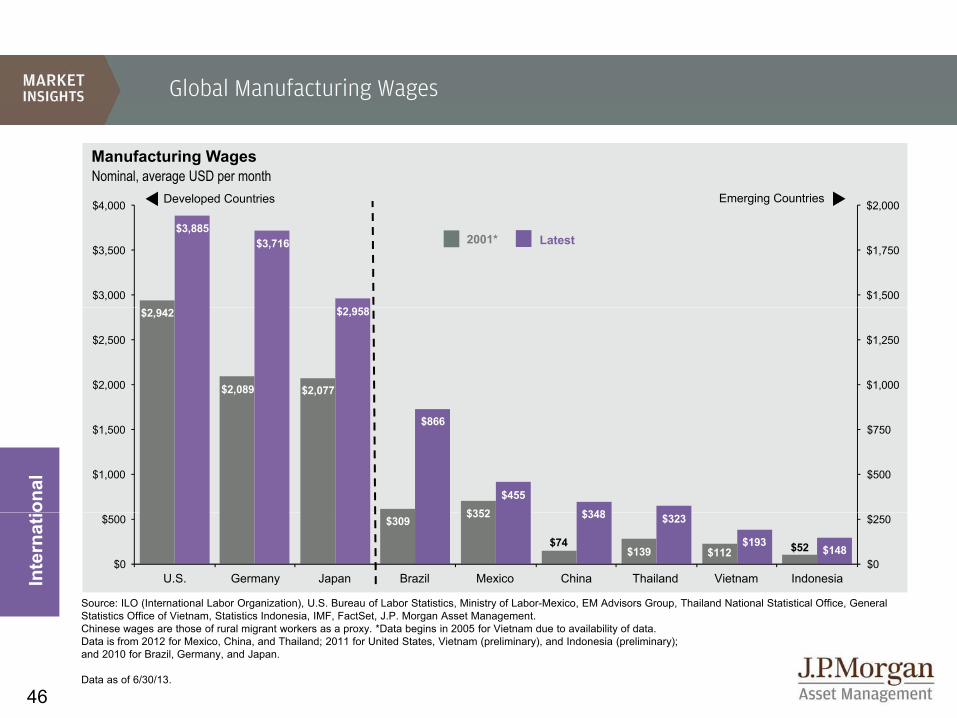

Global Manufacturing Wages

$2 000$4 000

Manufacturing WagesNominal, average USD per month

Developed Countries Emerging Countries

$3,885$3,716

$2 9 8$1,500

$1,750

$2,000

$3,000

$3,500

$4,000

Latest2001*

p

$2,942

$2,089 $2,077

$2,958

$1,000

$1,250

$2,000

$2,500

$352

$866

$455

$348

$500

$750

$1,000

$1,500

onal

$309$352

$74$139 $112 $52

$348 $323

$193$148

$0

$250

$0

$500

Source: ILO (International Labor Organization), U.S. Bureau of Labor Statistics, Ministry of Labor-Mexico, EM Advisors Group, Thailand National Statistical Office, General Statistics Office of Vietnam Statistics Indonesia IMF FactSet J P Morgan Asset Management

Inte

rnat

i

Brazil Mexico China Thailand Vietnam IndonesiaU.S. Germany Japan

46

Statistics Office of Vietnam, Statistics Indonesia, IMF, FactSet, J.P. Morgan Asset Management. Chinese wages are those of rural migrant workers as a proxy. *Data begins in 2005 for Vietnam due to availability of data.Data is from 2012 for Mexico, China, and Thailand; 2011 for United States, Vietnam (preliminary), and Indonesia (preliminary); and 2010 for Brazil, Germany, and Japan.

Data as of 6/30/13.

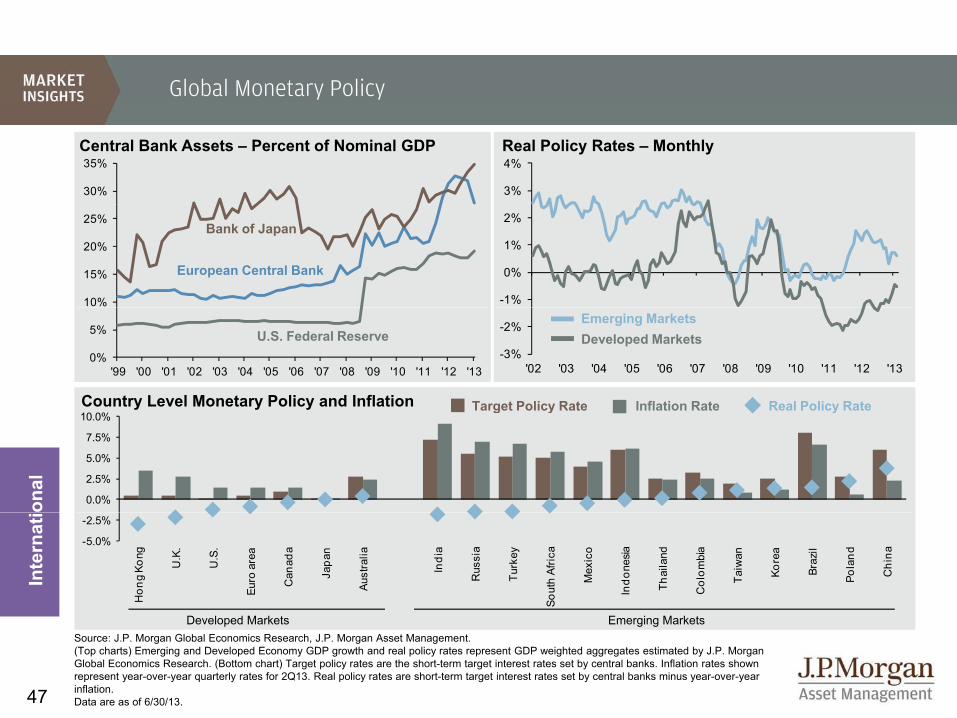

Global Monetary Policy

3%

4%

30%

35%Central Bank Assets �– Percent of Nominal GDP Real Policy Rates �– Monthly

-1%

0%

1%

2%

10%

15%

20%

25%

European Central Bank

Bank of Japan

-3%

-2%

'02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '130%

5%

'99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Developed Markets

Country Level Monetary Policy and Inflation

Emerging Markets

Inflation Rate Real Policy RateTarget Policy Rate

U.S. Federal Reserve

onal

Inflation Rate Real Policy RateTarget Policy Rate

0.0%

2.5%

5.0%

7.5%

10.0%

Inte

rnat

i

-5.0%

-2.5%

Hon

g Ko

ng

U.K

.

U.S

.

Euro

are

a

Can

ada

Japa

n

Aust

ralia

Indi

a

Rus

sia

Turk

ey

Sout

h Af

rica

Mex

ico

Indo

nesia

Thai

land

Col

ombi

a

Taiw

an

Kore

a

Braz

il

Pola

nd

Chi

na

47

Source: J.P. Morgan Global Economics Research, J.P. Morgan Asset Management.(Top charts) Emerging and Developed Economy GDP growth and real policy rates represent GDP weighted aggregates estimated by J.P. Morgan Global Economics Research. (Bottom chart) Target policy rates are the short-term target interest rates set by central banks. Inflation rates shownrepresent year-over-year quarterly rates for 2Q13. Real policy rates are short-term target interest rates set by central banks minus year-over-year inflation.Data are as of 6/30/13.

Developed Markets Emerging Markets

Europe: Economic Growth

6%

Europe Real GDP Year-over-year % change

Avg. Since 1999 1Q13

Real GDP 1.5% -0.7%

Latest Unemployment Rates for European CountriesMay 2013, seasonally adjusted

3 7%N

2%

0%

2%

4%Average:

1.5%

7 0%

6.6%

5.4%

4.9%

3.7%

Denmark

Netherlands

Germany

Austria

Norway

'00 '02 '04 '06 '08 '10 '12-6%

-4%

-2%

E rope Inflation Avg Since8.4%

8.4%

7.9%

7.8%

7.0%

Belgium

Finland

Sweden

U.K.

Denmark

Europe InflationYear-over-year % change

3%

4%

5%

Avg. Since 1999 May 2013

Headline CPI 2.1% 1.4%

Core CPI 1.7% 1.3%

onal

13.5%

12.0%

11.0%

11.0%

Ireland

Italy

France

European Union

'99 '01 '03 '05 '07 '09 '11

0%

1%

2%

Inte

rnat

i

27.0%

26.8%

17.8%

0% 5% 10% 15% 20% 25% 30%

Greece

Spain

Portugal

48

Source: Eurostat, FactSet, J.P. Morgan Asset Management.

Data are as of 6/30/13.

Europe: Austerity

General Government Deficit Reduction% of GDP, fiscal drag measured as difference in government deficit between stated years7%

2010-2013

2013-20166.2%

5%

6%

3.3%

4.4%

3.8%

3.4%3.1% 3 1%

4.0%

3.6%4%

5%

onal

3.1% 3.1%

1.8%1.9%

2.8%

2%

3%

Inte

rnat

io

1.1%

0.3% 0.4%

0.8%

0%

1%

49

Source: IMF, J.P. Morgan Asset Management.Government deficits calculated by the IMF as general government net lending/borrowing (revenue minus total expenditure). Data are based on the April 2013 World Economic Outlook. Data are as of 6/30/13.

Eurozone Greece Portugal Germany France U.K. Spain Italy

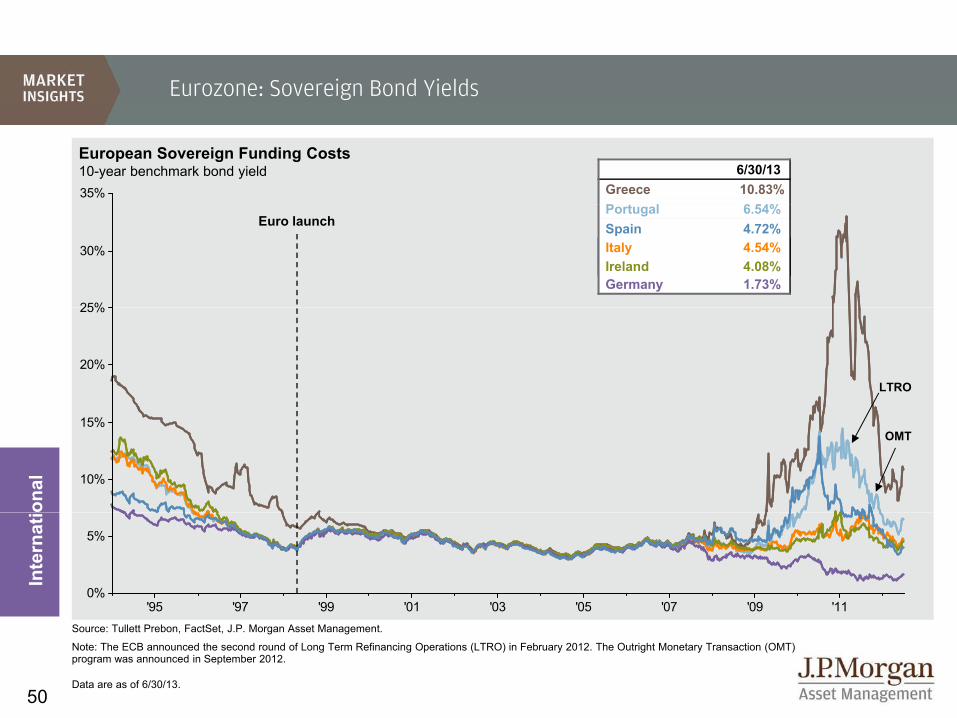

Eurozone: Sovereign Bond Yields

European Sovereign Funding Costs10-year benchmark bond yield35%

6/30/13Greece 10.83%P t l 6 54%

25%

30%

Portugal 6.54%Spain 4.72%

Ireland 4.2%Germany 1.73%Ireland 4.08%

Euro launch

Italy 4.54%

20%

25%

LTRO

10%

15%OMT

onal

'95 '97 '99 '01 '03 '05 '07 '09 '110%

5%

Inte

rnat

i

50

Source: Tullett Prebon, FactSet, J.P. Morgan Asset Management.

Note: The ECB announced the second round of Long Term Refinancing Operations (LTRO) in February 2012. The Outright Monetary Transaction (OMT) program was announced in September 2012.

Data are as of 6/30/13.

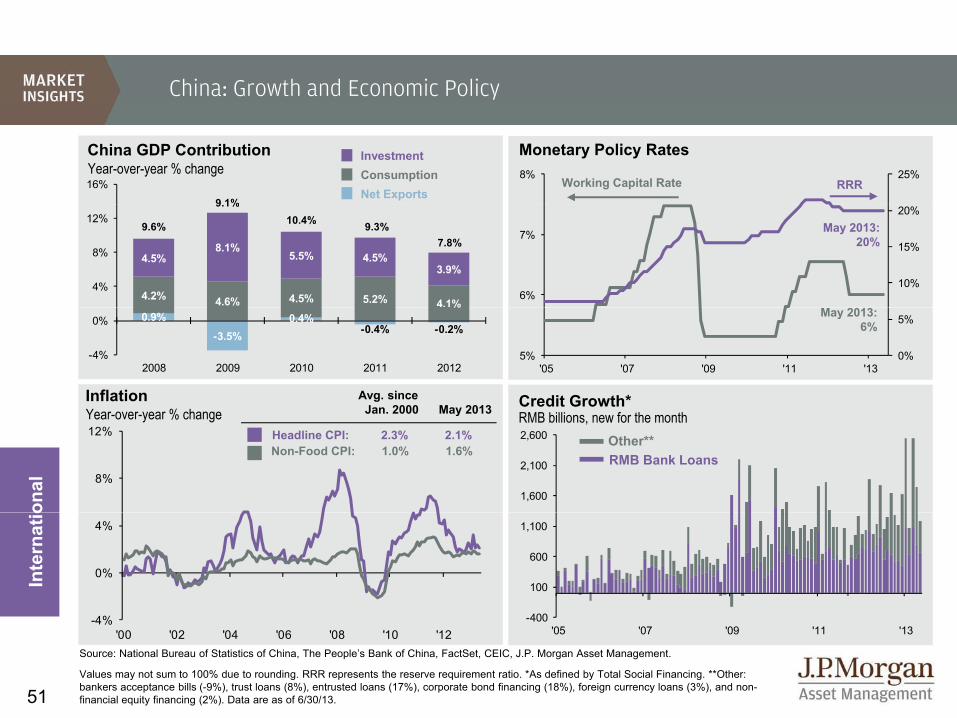

China: Growth and Economic Policy

25%8%

China GDP ContributionYear-over-year % change

InvestmentConsumptionNet Exports

RRRWorking Capital Rate

Monetary Policy Rates

16%

9 1%

10%

15%

20%

6%

7% May 2013: 20%

4.2% 4.6% 4.5% 5.2% 4.1%

4.5%8.1%

5.5% 4.5%3.9%

4%

8%

12%9.6%

9.1%10.4% 9.3%

7.8%

0%

5%

5%'05 '07 '09 '11 '13

Credit Growth*InflationY % h

Avg. since Jan 2000 May 2013

May 2013: 6%

0.9%

-3.5%0.4%

-0.4% -0.2%

%

-4%

0%

2008 2009 2010 2011 2012

8%

12%

onal

RMB billions, new for the month

RMB Bank LoansOther**

Year-over-year % change Jan. 2000 May 2013

Headline CPI: 2.3% 2.1% Non-Food CPI: 1.0% 1.6%

1,600

2,100

2,600

0%

4%

Inte

rnat

io

400

100

600

1,100

51

-4%'00 '02 '04 '06 '08 '10 '12

Source: National Bureau of Statistics of China, The People’s Bank of China, FactSet, CEIC, J.P. Morgan Asset Management.

Values may not sum to 100% due to rounding. RRR represents the reserve requirement ratio. *As defined by Total Social Financing. **Other: bankers acceptance bills (-9%), trust loans (8%), entrusted loans (17%), corporate bond financing (18%), foreign currency loans (3%), and non-financial equity financing (2%). Data are as of 6/30/13.

-400'05 '07 '09 '11 '13

China: Cyclical Indicators

170

Fixed Asset Investment Year-over-year % change, 3-month moving average35%

Index, rebased 2007=100, national averageResidential Real Estate Price

Property Tightening Measures Announced

25%

30%

140

Auto and Retail Sales

15%

20%

'06 '07 '08 '09 '10 '11 '12 '13

May 2013: 20.2%

11020%

25%

40%

60%

80%

onal

Year-over-year % changeRetail Sales

May 2013: 12.9%

80'07 '08 '09 '10 '11 '12 '13

5%

10%

15%

-20%

0%

20%

'10 '11 '12 '13

Inte

rnat

i

Auto Sales May 2013: 9.7%

52

'07 '08 '09 '10 '11 '12 '13'10 '11 '12 '13

Source: National Bureau of Statistics of China, China Association of Automobile Manufacturers, China Ministry of Construction, FactSet, J.P. Morgan Asset Management.

Data are as of 6/30/13.

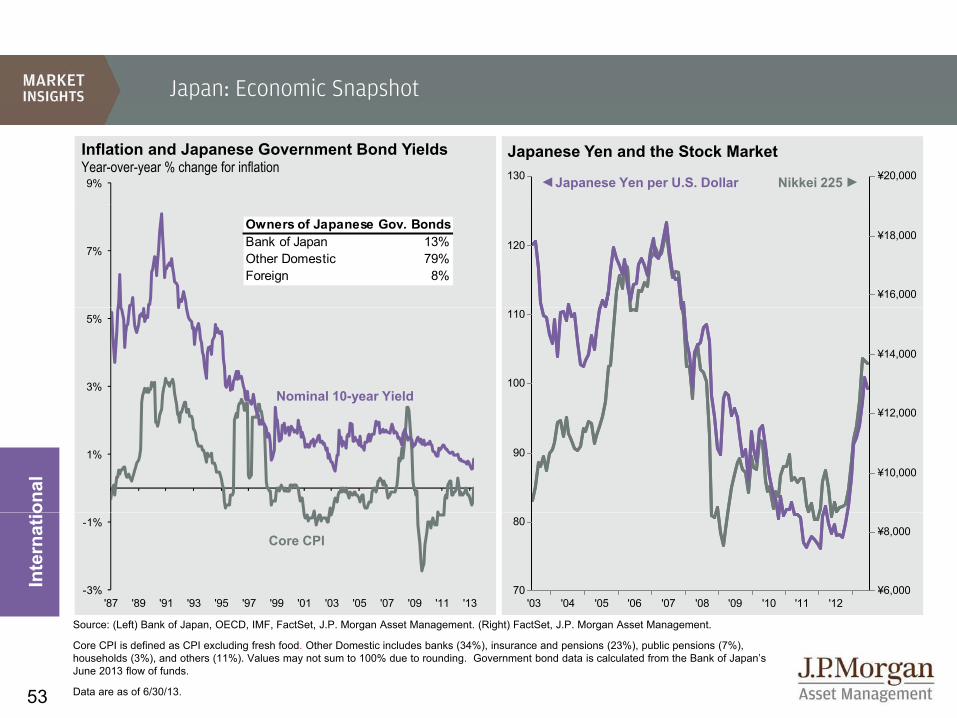

Japan: Economic Snapshot

9%130 ¥20,000

Inflation and Japanese Government Bond Yields Year-over-year % change for inflation

Japanese Yen per U.S. Dollar Nikkei 225

Japanese Yen and the Stock Market

7% 120

¥16,000

¥18,000Bank of Japan 13%Other Domestic 79%Foreign 8%

Owners of Japanese Gov. Bonds

3%

5%

100

110

¥12 000

¥14,000

Nominal 10-year Yield

1% 90

¥10,000

¥12,000

onal

'87 '89 '91 '93 '95 '97 '99 '01 '03 '05 '07 '09 '11 '13-3%

-1%

'03 '04 '05 '06 '07 '08 '09 '10 '11 '1270

80

¥6,000

¥8,000

Inte

rnat

io

Core CPI

53

Source: (Left) Bank of Japan, OECD, IMF, FactSet, J.P. Morgan Asset Management. (Right) FactSet, J.P. Morgan Asset Management.

Core CPI is defined as CPI excluding fresh food. Other Domestic includes banks (34%), insurance and pensions (23%), public pensions (7%), households (3%), and others (11%). Values may not sum to 100% due to rounding. Government bond data is calculated from the Bank of Japan’s June 2013 flow of funds.

Data are as of 6/30/13.

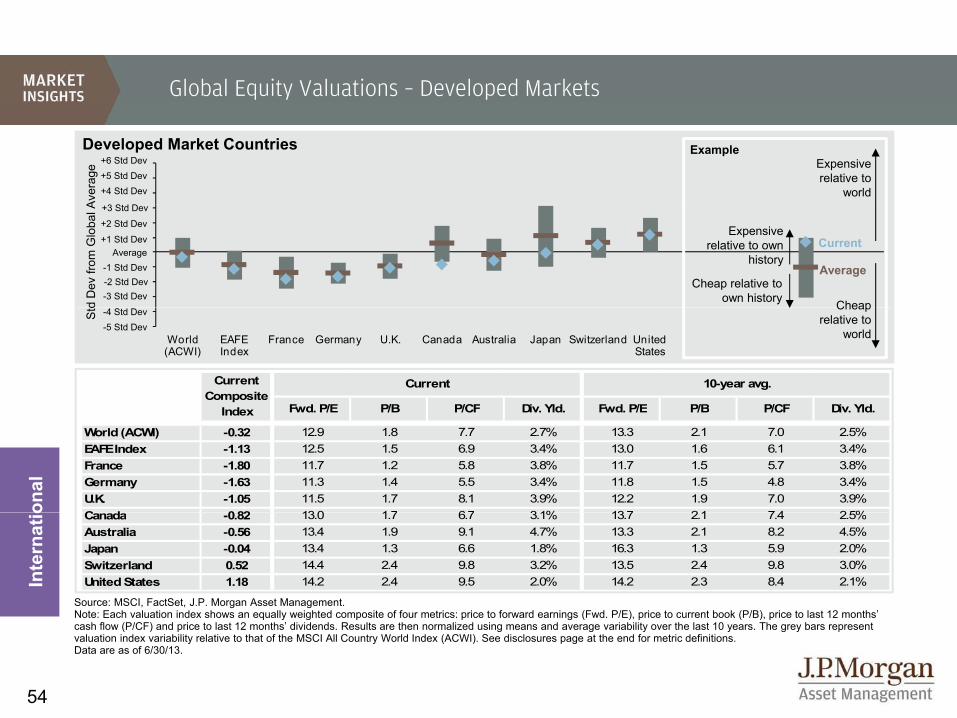

Global Equity Valuations – Developed Markets

Developed Market Countries

Ave

rage

Expensive relative to

world

Example

3 Std D

+5 Std Dev+4 Std Dev

+6 Std Dev

d D

ev fr

om G

loba

l A

Expensive relative to own

history

Cheap relative to own history

Average

Current

Cheap

+3 Std Dev

+2 Std Dev

+1 Std DevAverage

-1 Std Dev-2 Std Dev-3 Std Dev

Fwd P/E P/B P/CF Div Yld Fwd P/E P/B P/CF Div Yld

Current Composite

Index

Current 10-year avg.

World (ACWI)

EAFE Index

France Germany U.K. Canada Australia Japan Switzerland United States

Std Cheap

relative to world

-4 Std Dev-5 Std Dev

Fwd. P/E P/B P/CF Div. Yld. Fwd. P/E P/B P/CF Div. Yld.

World (ACWI) -0.32 12.9 1.8 7.7 2.7% 13.3 2.1 7.0 2.5% EAFE Index -1.13 12.5 1.5 6.9 3.4% 13.0 1.6 6.1 3.4%

France -1.80 11.7 1.2 5.8 3.8% 11.7 1.5 5.7 3.8%Germany -1.63 11.3 1.4 5.5 3.4% 11.8 1.5 4.8 3.4%U.K. -1.05 11.5 1.7 8.1 3.9% 12.2 1.9 7.0 3.9%C d 082 130 17 67 31% 137 21 74 25%

Index

onal

Canada -0.82 13.0 1.7 6.7 3.1% 13.7 2.1 7.4 2.5%Australia -0.56 13.4 1.9 9.1 4.7% 13.3 2.1 8.2 4.5%Japan -0.04 13.4 1.3 6.6 1.8% 16.3 1.3 5.9 2.0%Switzerland 0.52 14.4 2.4 9.8 3.2% 13.5 2.4 9.8 3.0%

United States 1.18 14.2 2.4 9.5 2.0% 14.2 2.3 8.4 2.1%