Embed Size (px)

Citation preview

Journal of Corporate Real EstateEmerald Article: Optimising real estate financingGreg Krzysko, Claudia Marciniak

Article information:

To cite this document: Greg Krzysko, Claudia Marciniak, (2001),"Optimising real estate financing", Journal of Corporate Real Estate, Vol. 3 Iss: 3 pp. 286 - 297

Permanent link to this document: http://dx.doi.org/10.1108/14630010110811643

Downloaded on: 08-11-2012

Citations: This document has been cited by 1 other documents

To copy this document: [email protected]

Access to this document was granted through an Emerald subscription provided by The University of British Columbia Library

For Authors: If you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors service. Information about how to choose which publication to write for and submission guidelines are available for all. Please visit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.comWith over forty years' experience, Emerald Group Publishing is a leading independent publisher of global research with impact in business, society, public policy and education. In total, Emerald publishes over 275 journals and more than 130 book series, as well as an extensive range of online products and services. Emerald is both COUNTER 3 and TRANSFER compliant. The organization is a partner of the Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation.

*Related content and download information correct at time of download.

Greg Krzysko is Vice-President of the FinancialConsulting Group at Equis Corporation inChicago. He provides for Equis clients, in-cluding Ameritech/SBC, DaimlerChrysler, DelphiAutomotive and Xerox, creative financial struc-turing strategies that achieve the best overallbusiness outcome. Greg has been successful inproviding real estate solutions that enableclients to pursue new business ventures, toexpand existing real estate assets and to reducecost in existing client portfolios. He received hisdegree of Master of Business Administra-tion majoring in Finance and Strategy fromNorthwestern University’s J. L. Kellogg Schoolof Management in Evanston, Illinois.

Claudia Marciniak is Director of PortfolioServices at Equis Corporation. She providesEquis clients with analyses to administer andalign their real estate portfolios with businessand financial strategies. Claudia has significantexperience in financial structuring and strategicplanning, as well as project, construction andrisk management. She received her degree ofMaster of Business Administration majoring inFinance and Accounting from NorthwesternUniversity’s J. L. Kellogg School of Managementin Evanston, Illinois.

ABSTRACT

This paper discusses ways that corporate realestate managers can use creative financial struc-turing to optimise their real estate portfolios.

The corporate real estate manager can mosteffectively arrive at an optimal decision byconsidering three perspectives: the corporate realestate market, business unit needs, and investorpreferences. After gathering the relevant infor-mation and evaluating the pros and cons of thefull range of financial structures, the real estatemanager can make a sound recommendation tothe business unit and the finance department.The manager knows that the solution isacceptable to the marketplace, can provideflexibility in the event of a changed businessmodel, and provides the space at the mostreasonable cost.

Keywords: finance, capital sources,financial structuring, financing alterna-tives

THE MANAGER’S DILEMMAFinancing real estate projects can be avexing experience for even the mostseasoned corporate real estate manager.Corporate hurdle rates, capital budgets,discount rates, weighted average cost ofcapital, cost of debt, residual valueestimation and changing operating needs— the considerations are many, but nosingle approach helps corporate real estatemanagers understand how to structurefinancing for a given project. Corporatereal estate managers often evaluate aproject for the business unit merely by

Optimising real estate financing

*Greg Krzysko and Claudia MarciniakReceived (in revised form): 30th March, 2001*Equis Corporation, Corporate Headquarters, 321 N. Clark, Suite 1010, Chicago, IL60610, USA; Tel: �1(312) 424 8143; Fax: �1(312) 424 8080; e-mail:[email protected]

Journal of Corporate Real Estate Volume 3 Number 3

Page 286

Journal of Corporate Real EstateVol. 3 No. 3, 2001, pp. 286–297.Henry Stewart Publications,1463–001X

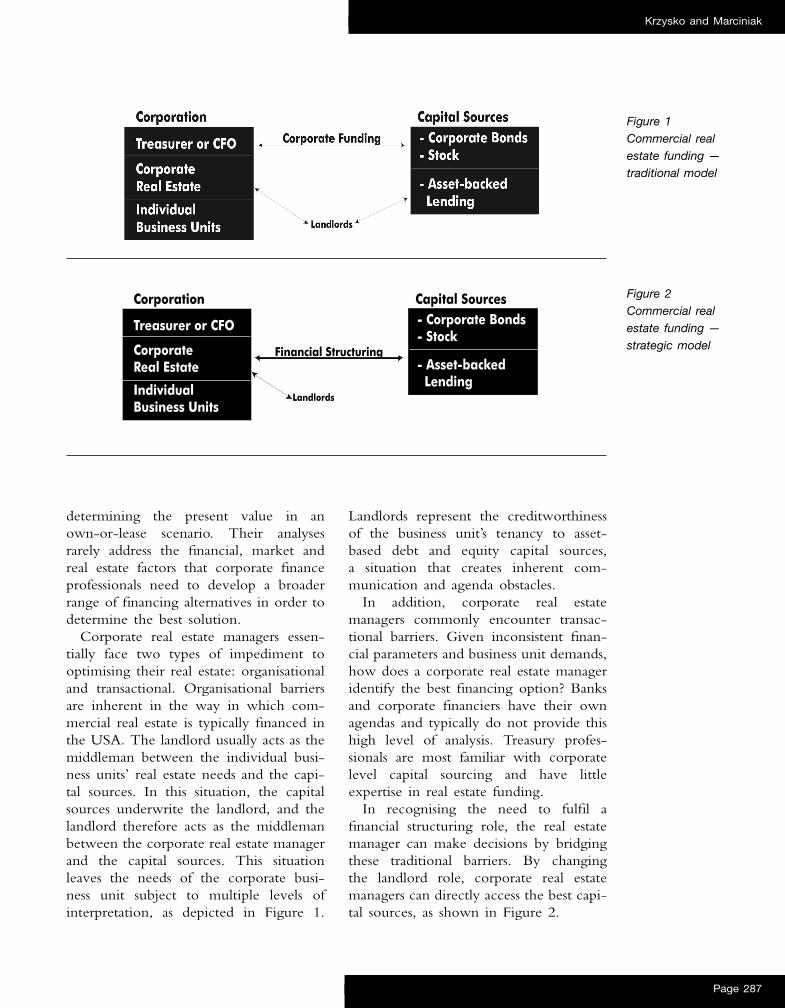

Landlords represent the creditworthinessof the business unit’s tenancy to asset-based debt and equity capital sources,a situation that creates inherent com-munication and agenda obstacles.

In addition, corporate real estatemanagers commonly encounter transac-tional barriers. Given inconsistent finan-cial parameters and business unit demands,how does a corporate real estate manageridentify the best financing option? Banksand corporate financiers have their ownagendas and typically do not provide thishigh level of analysis. Treasury profes-sionals are most familiar with corporatelevel capital sourcing and have littleexpertise in real estate funding.

In recognising the need to fulfil afinancial structuring role, the real estatemanager can make decisions by bridgingthese traditional barriers. By changingthe landlord role, corporate real estatemanagers can directly access the best capi-tal sources, as shown in Figure 2.

determining the present value in anown-or-lease scenario. Their analysesrarely address the financial, market andreal estate factors that corporate financeprofessionals need to develop a broaderrange of financing alternatives in order todetermine the best solution.

Corporate real estate managers essen-tially face two types of impediment tooptimising their real estate: organisationaland transactional. Organisational barriersare inherent in the way in which com-mercial real estate is typically financed inthe USA. The landlord usually acts as themiddleman between the individual busi-ness units’ real estate needs and the capi-tal sources. In this situation, the capitalsources underwrite the landlord, and thelandlord therefore acts as the middlemanbetween the corporate real estate managerand the capital sources. This situationleaves the needs of the corporate busi-ness unit subject to multiple levels ofinterpretation, as depicted in Figure 1.

Figure 1Commercial realestate funding —traditional model

Figure 2Commercial realestate funding —strategic model

Krzysko and Marciniak

Page 287

Treasurer or CFO

Corporation Capital Sources

Corporate

Real Estate

Individual�

Business Units

- Corporate Bonds

- Stock

- Asset-backed

LendingLandlords

Financial Structuring

This process employs strategic thinkingthat links corporate goals to real estateand directly accesses capital sources. Cor-porate real estate departments can place aquantifiable monetary value on the widevariety of financing options available foreach transaction, turning real estate into acompetitive asset.

For example, corporate finance andreal estate departments commonlystruggle when evaluating single-tenantbuildings in an own-versus-lease scenario.Typically, a business operating unit willbudget for a lease at market rates andexpect corporate real estate to secure thatlease. When corporate real estate caninstead purchase the asset and still meetthe business unit needs in lieu of a lease,a debate ensues as to how to considerthe project — financing of an asset thatwill be discounted at an after-tax costof debt, or a project to be discountedat the weighted average cost of capital?Corporate finance and real estatedepartments further consider and debatewhether the property will increase ordiminish in future value, how muchdecrease can be tolerated, the length oftime for which the business will need theproperty, and whether the capital budgetcan accommodate a change from a leasedinto an owned property.

A LOOK AT THE FULL SPECTRUMBy focusing on the internal corporateevaluation criteria only, corporate realestate managers often miss real estate in-dustry perspectives; a sub-optimal deci-sion results. Industry concerns include theamount of leverage a typical real es-tate capital source allows; whether theproject is financeable; and what residualvalue assumption is acceptable to a lenderand/or investor. Managers who incor-porate the industry point of view intotheir decision making help the corpora-

tion to achieve its business objectives atthe best possible cost.

Without embracing the opportunitiesand the dynamics of the real estate invest-ment community, corporate real estatemanagers often create a ‘stock’ or ‘one-size-fits-all’ approach that results in asingle answer or decision for all propertiesof a particular type. For example, a com-pany assumes that office buildings ap-preciate and that the company needs themfor a very long time. The company thenperforms an analysis that compares 100per cent debt ownership and selling theappreciated asset at the end of 15 yearswith just leasing the office for 15 years.In this scenario, owning is clearly thebest option because the company assumesan increase in value and continued oc-cupancy. Alternatively, a business mayneed a call centre for ten years, overwhich time the company believes that theindustry will change dramatically. Thecompany then performs an analysis thatcompares a ten-year lease to a purchasewith 100 per cent debt and no residualvalue. In this scenario, leasing is clearlythe better of the two options because ofthe lack of value at the end of ten years.In all likelihood, the corporation willpursue its next office as a purchase and itsnext call centre as a lease.

However, the corporation’s financingoptions are influenced by a number ofother factors, including shifts within thecompany (such as a merger or acquisition)or in corporate debt rates. Additionally,with the dramatic swings in office demandand building valuations resulting frombusiness cycles and local economic condi-tions, the corporation’s financing optionsmay be affected in response to supplyand demand for a particular space type.The aforementioned lease–buy analysis ig-nores the fact that both properties operatewithin the context of a larger, dynamicuniverse of real estate and that alternatives

Optimising real estate financing

Page 288

like Silicon Valley will constantly considerthe current or future land value forredevelopment, especially during any sale,refinancing or tenanting of the space.Corporations should take a similar ap-proach and consider ongoing and regularreviews of their portfolios or individualprojects. Otherwise they will routinely missopportunities to limit risk and realiseappreciation.

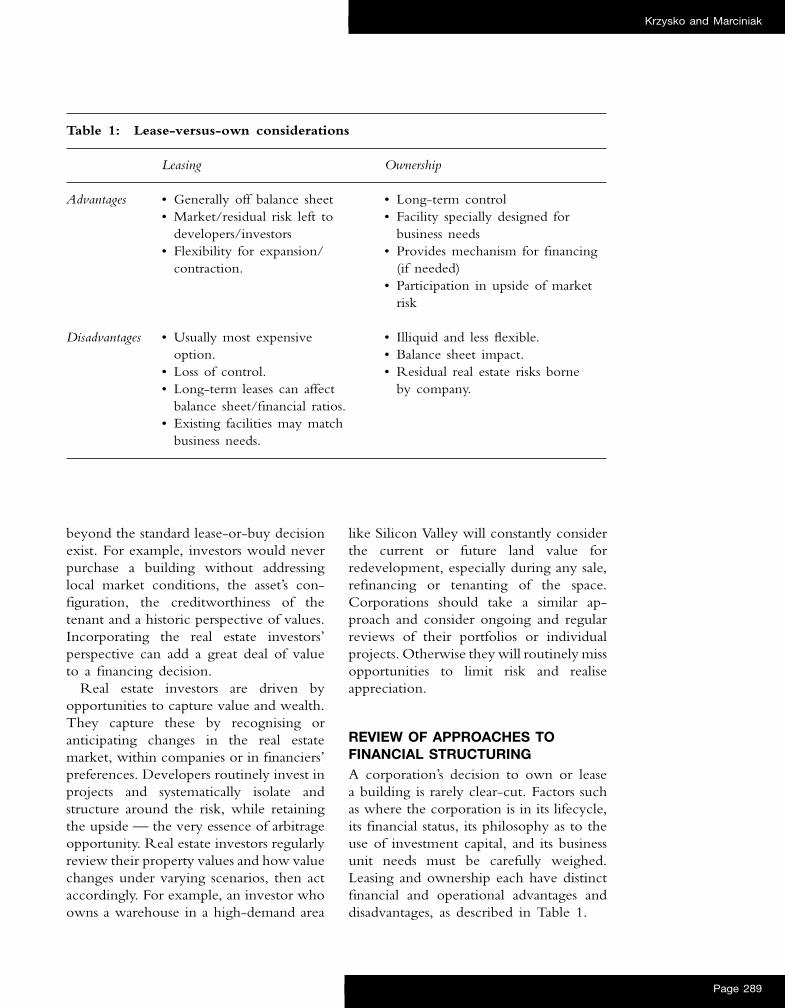

REVIEW OF APPROACHES TOFINANCIAL STRUCTURINGA corporation’s decision to own or leasea building is rarely clear-cut. Factors suchas where the corporation is in its lifecycle,its financial status, its philosophy as to theuse of investment capital, and its businessunit needs must be carefully weighed.Leasing and ownership each have distinctfinancial and operational advantages anddisadvantages, as described in Table 1.

beyond the standard lease-or-buy decisionexist. For example, investors would neverpurchase a building without addressinglocal market conditions, the asset’s con-figuration, the creditworthiness of thetenant and a historic perspective of values.Incorporating the real estate investors’perspective can add a great deal of valueto a financing decision.

Real estate investors are driven byopportunities to capture value and wealth.They capture these by recognising oranticipating changes in the real estatemarket, within companies or in financiers’preferences. Developers routinely invest inprojects and systematically isolate andstructure around the risk, while retainingthe upside — the very essence of arbitrageopportunity. Real estate investors regularlyreview their property values and how valuechanges under varying scenarios, then actaccordingly. For example, an investor whoowns a warehouse in a high-demand area

Krzysko and Marciniak

Page 289

Table 1: Lease-versus-own considerations

Leasing Ownership

Advantages • Generally off balance sheet• Market/residual risk left to

developers/investors• Flexibility for expansion/

contraction.

• Long-term control• Facility specially designed for

business needs• Provides mechanism for financing

(if needed)• Participation in upside of market

risk

Disadvantages • Usually most expensiveoption.

• Loss of control.• Long-term leases can affect

balance sheet/financial ratios.• Existing facilities may match

business needs.

• Illiquid and less flexible.• Balance sheet impact.• Residual real estate risks borne

by company.

Because corporations view, account forand measure financial performance forreal estate investment differently, the realestate manager, the business unit andtreasury team should thoroughly considerthe short and long-term earnings impactand the balance sheet results in addition tothe business unit operational issues des-cribed above. Because real estate canprovide a competitive advantage throughcost and location, the real estate decisionshould be included as an essential partof the corporation’s overall business andfinancial strategy.

Incorporating real estate into the busi-ness and financial strategy can be difficultbecause real estate usually competes withother projects for investment capital. Forexample, a newly formed software com-pany will probably have difficulty secur-ing a loan to construct a building, since

it has limited credit history and needsto plough capital into business develop-ment. For many start-up companies, spaceneeds will grow exponentially and there-fore cannot be accurately predicted. Inthis case, leasing provides the necessaryfinancial and space planning flexibilityand fits ideally into the company’s busi-ness plan. By contrast, a utility companythat needs a building to house its trans-formers — a specialised use in a verylong-term business — should own thereal estate. Ownership makes sense, be-cause developers will not be interested infinancing such a specialised activity, thecompany has a predictable revenue streamand it can pay for the property withminimal risk.

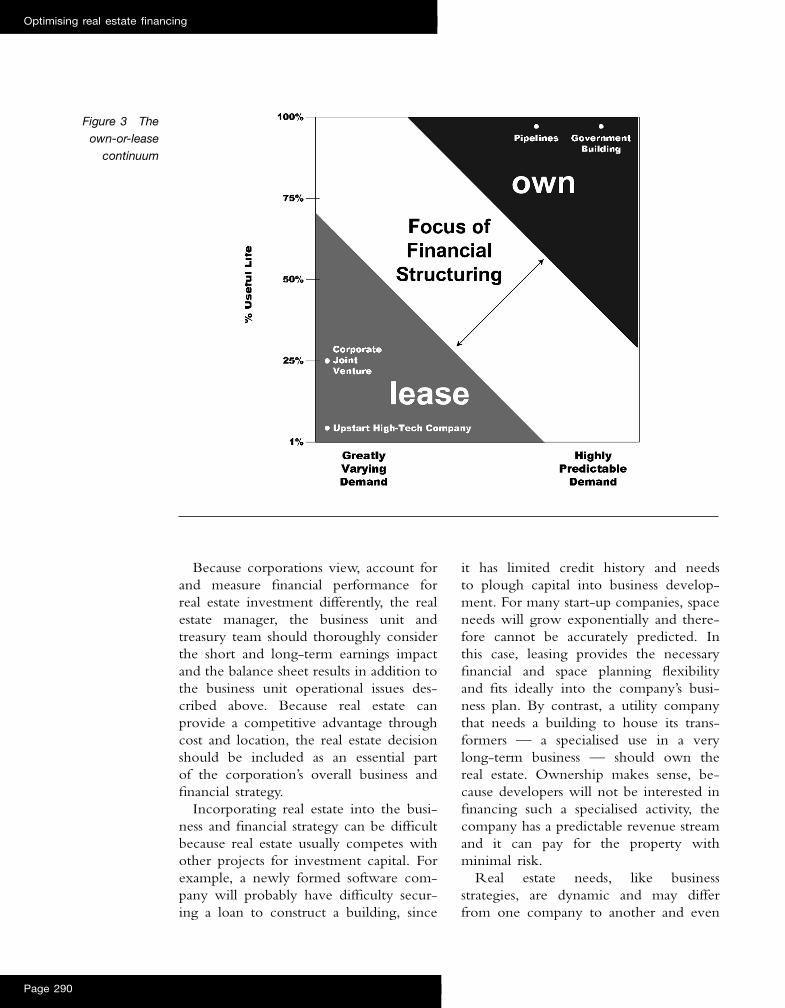

Real estate needs, like businessstrategies, are dynamic and may differfrom one company to another and even

Figure 3 Theown-or-lease

continuum

Optimising real estate financing

Page 290

cent of the portfolio square footage)are small and subject to variable busi-ness needs. Clearly these properties arebest structured as leases; and

— The remaining 979 properties (51 percent of the portfolio square footage)are subject to changing internal cor-porate needs and widespread realestate industry investment, and so arenot clear-cut lease-or-own decisions.These are best addressed throughfinancial structuring.

The authors found a similar distribu-tion and trend across the real estateportfolios of numerous other Fortune500 companies such as DaimlerChrysler,Xerox Corporation, Delphi Automotive,Ameritech Corporation and Square D.Unique, long-term assets were generallyowned; generic spaces were typicallyleased. However, large portions of theportfolios had real estate requirements thatfall between standard and special (logisticcentres, call centres) and therefore werenot straightforward decisions. In thesecases, corporations have sought out finan-cial structuring assistance.

within the same corporation. Unfor-tunately, most corporate real estate spaceand financing decisions are not asclear-cut as the examples cited above.When real estate is an integral part of thestrategic business plan, the real estatedecision becomes more complex. Toaddress these additional concerns andissues, hybrid financing structures haveevolved. As Figure 3 depicts, mostcorporate decisions fall in the middle ofthe own-or-lease continuum, where thefinancing options are varied and confus-ing. In this area, financial structuring ismost valuable to the corporate real estatemanager.

As a case in point; a recent examinationof a Fortune 100 company portfolio withmore than 10,000 properties, consisting of50 million square feet, revealed that:

— More than 9,000 properties (48 percent of the portfolio square footage)are considered ‘specialised’ in support-ing business units whose real estateneeds are stable. As a result, directownership is clearly the best option;

— Only 228 properties (less than 1 per

Figure 4 The tripleapproach

Krzysko and Marciniak

Page 291

A THREE-PRONGED APPROACHFinancial structuring of corporate real es-tate projects involves taking the best prac-tices of real estate developers and investorsand using them to control the risk andparticipate in the appreciation of realestate to achieve lower cost. An effectiveevaluation process used to reduce costand increase flexibility approaches theproblem by examining three considera-tions. The first consideration is the realestate requirement itself: its uniqueness,adaptability, location, ability to be multi-tenanted, place in the broader market, andso on. The second consideration is thebusiness user need and possible variability,including possible future expansions orcontractions. The final consideration isthe investors’ risk – reward objectivesand their desire to buy, sell or benefitfrom a particular corporation’s tenancy. Bycombining the information gathered fromthese three areas, the real estate managerwill have the right information assembledto evaluate all of its financing optionseffectively and to achieve an optimaldecision (Figure 4).

Real estate managers can learn a greatdeal from the real estate marketplaceabout how to structure a deal. Bygathering information about speculativeconstruction projects, considering theamount of construction, financing andinvestment activity and gauging reactionsfrom the investment community about aproposed corporate real estate financing,the real estate manager obtains a big-picture perspective. These considerationsreveal key information about the realestate contemplated in the broader marketcontext.

To the extent possible, the real estatemanager’s goal should be to create realestate opportunities that investors wouldlike to own, in places they would like toown it (‘location, location, location’).Changes in concept, configuration or

location can greatly influence the range ofpossibilities for structuring a project’sfinancing without materially affecting theoccupancy cost or functionality of abusiness operation. For example, saya corporation is considering a one-million-square-foot headquarters buildingwith 250,000 square feet on each offour floors. While this building wouldmeet the operating requirements, thecorporation could alternatively considerfour separate 250,000-square-foot build-ings with 50,000-square-foot floorplatesconnected by bridges. The functionaldifference is probably minimal, but to aninvestor the second scenario represents anopportunity to accommodate multiple50,000-square-foot configurations. Thisconfiguration would reduce the investor’srisk in the long term, and so the real estatewould be priced to reflect a lower riskpremium.

The next key is to understand thebusiness use variability. If the business unitis likely to decrease its space needs by halfor expects to have the same needs for thenext 15 years, having a partial exit strategyfor a portion of the space is more cost-effective over time, since only the re-quired amount of space will be utilised.With businesses undergoing a large degreeof uncertainty due to changing businessmodels, companies place a high value onflexibility.

Finally, the last consideration is theinvestor’s desire to fund certain projects atany particular time. The corporate realestate manager must recognise the impor-tance of adapting the structure and designof each real estate project to changesinfluencing investors. A broad range ofinfluences affect the real estate investor,including taxation, sovereign risk, cur-rency exchange risk, global uncertainty,hostilities and securitisation potential. Inthe mid-1990s, REITs were active andamassed large portfolios of properties

Optimising real estate financing

Page 292

they must structure into leases a variety ofoptions such as purchase, termination,expansion and various hybrid-ownershipoptions.

After developing a market-appropriatephysical and financial model, a corpora-tion can evaluate alternative structures toprovide the best circumstances for itstenancy. In the one-million-square-footexample, the corporation can compare alease with REIT pricing to straightownership, synthetic leases, amortisingoff-balance sheet structures, joint ven-tures, tax-free exchanges and traditionalinvestors.

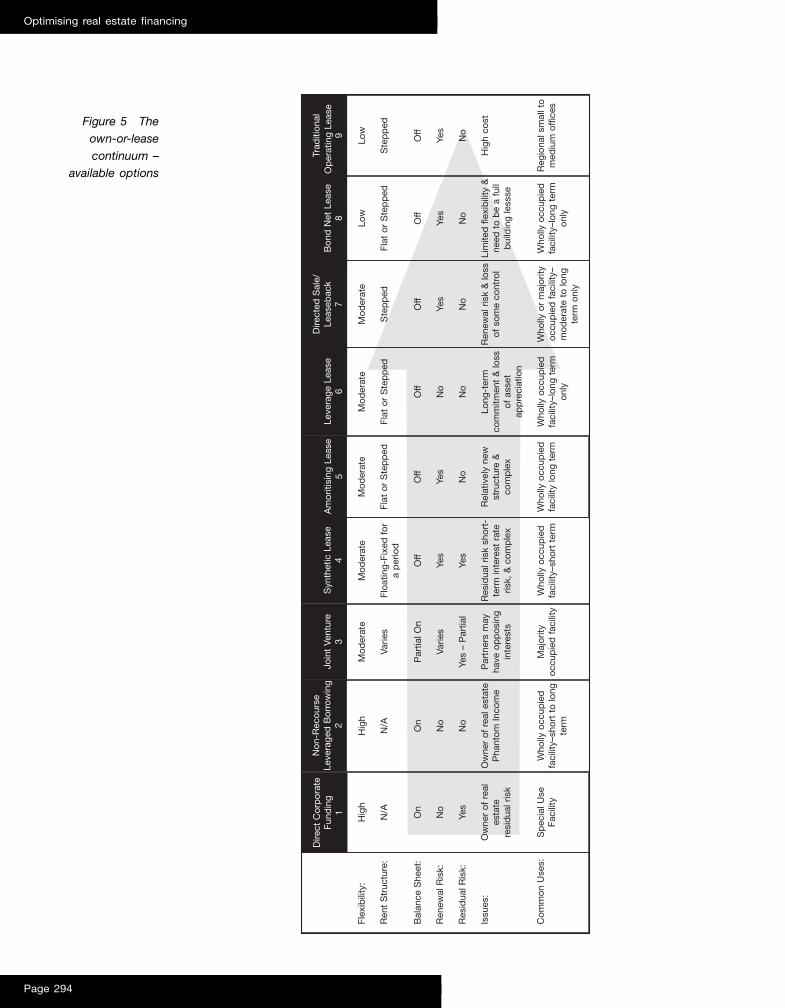

STRUCTURING ALTERNATIVESThe real estate manager now has manystructuring options from which to choose.When evaluating each of the alternatives,the real estate manager must synthesisethe information gathered from the threearenas (business unit, investor and realestate market information) before movingon to a structuring decision. Figure 5depicts a representative sample of optionsavailable, from a build-to-suit to a single-tenant facility; it reflects the continuum,with complete ownership at one extremeand pure leasing at the other. Severalhybrid alternatives are described and showthe various options available to a realestate manager in what was thought to bea simple lease or buy decision.

Direct corporate funding is most ap-propriate for those properties that areunique to a corporation’s operation and insituations where no real estate investorwill value or assume the risk outsidethe corporation’s tenancy. Examples ofthis asset type are manufacturing plants,clean rooms and telephone switch build-ings. Leasing a specialised building is ef-fectively asking real estate investors toact as lender to the company, since thelease would typically be structured to

based on specialisation, as Wall Streetallowed REITs to replace secured debtand equity with stock and corporate debt.Because this recapitalisation of real estatefirms progressed, REITs focused onprojects which provided revenue growthand predictable capital requirements tomeet the Wall Street business model. Realestate projects that met these requirementshad good prospects for acquisition orfinancing by a REIT. Now that REITsare less active in the market, the corporatereal estate manager must redesign for thenext investor market in vogue.

To demonstrate the importance ofevaluating business unit needs, real estatemarket concerns and investor preferences,reconsider the previously proposedproject. It has now evolved into a productthat offers a REIT an opportunity to owna four-building, one-million-square-footproject with annual rent escalations, withthe tenant retaining the ability to giveback 250,000 square feet of contiguousspace in year five of the lease. This projectwould be very attractive to the investorpool, and would remain low cost to thebusiness unit even if the latter’s spaceneeds dropped 25 per cent in five years.

Even after an appropriate structureis implemented and the corporationtakes occupancy, variations in investorpreferences provide continuous oppor-tunity for the re-evaluation of real estateproperties and portfolios. As investorsshift away from real estate, corporationshave opportunities to capture value byrepositioning their portfolio, by enteringinto a long-term lease when markets aresoft or by purchasing leased properties.Since investors favour real estate, corpora-tions again have the opportunity tocapture value by repositioning theirportfolio; for example, by exercising abelow-market purchase option. For cor-porations to take advantage of oppor-tunities in market conditions, however,

Krzysko and Marciniak

Page 293

Figure 5 Theown-or-leasecontinuum –

available options

Optimising real estate financing

Page 294

Dire

ct C

orp

orat

e Fu

ndin

g1

Hig

h

N/A On

No

Yes

Ow

ner

of r

eal

esta

tere

sid

ual r

isk

Sp

ecia

l Use

Faci

lity

Flex

ibili

ty:

Ren

t S

truc

ture

:

Bal

ance

She

et:

Ren

ewal

Ris

k:

Res

idua

l Ris

k:

Issu

es:

Com

mon

Use

s:

Non

-Rec

ours

eLe

vera

ge B

orro

win

g 2

Hig

h

N/A On

No

No

Ow

ner

of r

eal e

stat

eP

hant

om In

com

e

Who

lly o

ccup

ied

faci

lity–

shor

t to

long

term

Syn

thet

ic L

ease

4

Mod

erat

e

Floa

ting-

Fixe

d f

or

a p

erio

d

Off

Yes

Yes

Res

idua

l ris

k sh

ort-

term

inte

rest

rat

eris

k, &

com

ple

x

Who

lly o

ccup

ied

faci

lity–

shor

t te

rm

Join

t Ve

ntur

e3

Mod

erat

e

Varie

s

Par

tial O

n

Varie

s

Yes

– P

artia

l

Par

tner

s m

ayha

ve o

pp

osin

gin

tere

sts

Maj

ority

oc

cup

ied

fac

ility

Am

oriti

zing

Lea

se5

Mod

erat

e

Flat

or

Ste

pp

ed

Off

Yes

No

Rel

ativ

ely

new

st

ruct

ure

&

com

ple

x

Who

lly o

ccup

ied

faci

lity

long

ter

m

Leav

erag

e Le

ase

6

Mod

erat

e

Flat

or

Ste

pp

ed

Off

No

No

Long

-ter

m

com

mitm

ent

& lo

ssof

ass

et

app

reci

atio

n

Who

lly o

ccup

ied

faci

lity–

long

ter

m

only

Dire

cted

Sal

e/Le

aseb

ack

7

Mod

erat

e

Ste

pp

ed

Off

Yes

No

Ren

ewal

ris

k &

loss

of s

ome

cont

rol

Who

lly o

r m

ajor

ityoc

cup

ied

fac

ility

–m

oder

ate

to lo

ngte

rm o

nly

Bon

d N

et L

ease

8

Low

Flat

or

Ste

pp

ed

Off

Yes

No

Lim

ited

fle

xib

ility

&ne

ed t

o b

e a

full

bui

ldin

g le

ssse

Who

lly o

ccup

ied

faci

lity–

long

ter

mon

ly

Trad

ition

alO

per

atin

g Le

ase

9

Low

Ste

pp

ed

Off

Yes

No

Hig

h co

st

Reg

iona

l sm

all t

om

ediu

m o

ffice

s

Dire

ct C

orp

orat

e Fu

ndin

g1

Non

-Rec

ours

eLe

vera

ged

Bor

row

ing

2Jo

int

Vent

ure

3S

ynth

etic

Lea

se4

Am

oriti

sing

Lea

se5

Leve

rage

Lea

se6

Dire

cted

Sal

e/Le

aseb

ack

7B

ond

Net

Lea

se8

Trad

ition

alO

per

atin

g Le

ase

9

The corporation therefore assumes rate,residual and renewal risk while also fullybenefiting from appreciation. The mainattraction of synthetic leases is that theyallow off-balance-sheet ownership of anasset. Analysis of synthetics tends toignore the cost of a reduced residual valueuntil the property is actually vacated andthe company faces a potential write-off.In order to mitigate risk, the corporationshould amortise a portion of the principalbalance in a synthetic lease, in preparationfor dramatic changes in rates or un-favourable renewal terms at the end of thelease.

An amortising off-balance-sheet leasestructure offers a lower lease cost thantraditional leases, is fixed over the term,and matches cost closely with theproperty’s utilisation. At term end,residual risk is eliminated, renewal risk iscontrolled and appreciation is captured atvarying levels. These off-balance-sheetstructures are most effective for long-termproperties with the potential for substan-tial residual value but a history of valuevolatility. For instance, a good applicationof these structures is a Fortune 500company leasing a single-tenant suburbanoffice building.

Leverage leases provide a low rentalcost over a long period, often with lowrenewal options. A major drawback ofthis structure is that any acceleration,termination or reduction in the leaseis exceedingly difficult to achieve, be-cause of the accounting and tax treatmentby the lessor. The corporation cannotparticipate in any property appreciation,but completely avoids residual risk. Thisstructure is best suited for long-term assetsinvolving business units whose needs arevery unlikely to change. In today’s busi-ness environment, the ability to say confi-dently that a requirement will not changefor a long time has diminished — and sohas the use of leverage leases.

amortise the cost fully over the initialterm at an interest rate substantially abovethe company’s borrowing cost. Any con-tinued occupancy beyond the initial termwould enrich the investor, as would anyresidual value if the corporation vacatesthe facility.

Non-recourse borrowing is similar tocorporate borrowing in that it accesseslow-cost funds and the company benefitsfrom appreciation and/or continued oc-cupancy, yet avoids residual risk. Theproperty must be fairly typical and notspecialised, because the lender is mostconcerned with the underlying real es-tate security for the loan, in additionto the mortgagee’s ability to service themortgage.

Joint ventures provide a way to share inresidual value while controlling residualrisk. Real estate with good upside potentialis best suited for this financial structure.Development projects where the corpora-tion controls the opportunity for a larger-scope project with high return potentialover time are ideal for this type of transac-tion. Examples include an office user pre-leasing over 50 per cent of a speculative,multi-tenant project that will not proceedwithout the company’s tenancy. Obtaininga share of development profits realised uponcompletion and also participating in theincome can be a prudent way to lower costwhile controlling risk.

Synthetic leases are often used toprovide a low lease cost during the termbut require a corporate guarantee toensure that the residual real estate value isgreater than 90 per cent of initial cost.This structure essentially acts as aninterest-only loan for up to seven years; itcan be utilised for any type of property,but is best suited to properties that willconsistently maintain a high level of valueand are only required for a relatively shortperiod. Synthetics are priced to indexessuch as LIBOR which regularly fluctuate.

Krzysko and Marciniak

Page 295

Corporations are finding directed sale-leasebacks to be increasingly rewarding.As the markets have tightened, morecompanies are faced with build-to-suitrequirements. Rather than enter into alease, a project is built for the corporationdirectly and then sold off to inves-tors, allowing the company to capturethe profit associated with entrepreneurialrisk as well as that from the long-term investor’s desire for the company’stenancy. Properties best suited for thisapproach are those that are most indemand by long-term investors, in situa-tions where the company needs theproperty delivered within an acceleratedtimeframe. Examples include office build-ings, warehouses and call centres in majorurban office markets.

Bond net leases improve the lease ratescharged to the company, since the tenant’scredit is used directly to obtain borrowingcapacity with little regard to the realestate. When reviewed at a portfolio level,the incremental cost of entering into atraditional lease rather than bond leases isvery high for most major corporations.

This structure should be utilised for anysubstantial lease as a vehicle to lowercost.

Finally, traditional leased facilities arebest used when properties that meet thebusiness unit’s needs are generally avail-able in the market and when the corpora-tion requires flexibility. Leasing is bestused when markets are soft due to exces-sive supply and lease rates are belowreplacement cost for existing properties.

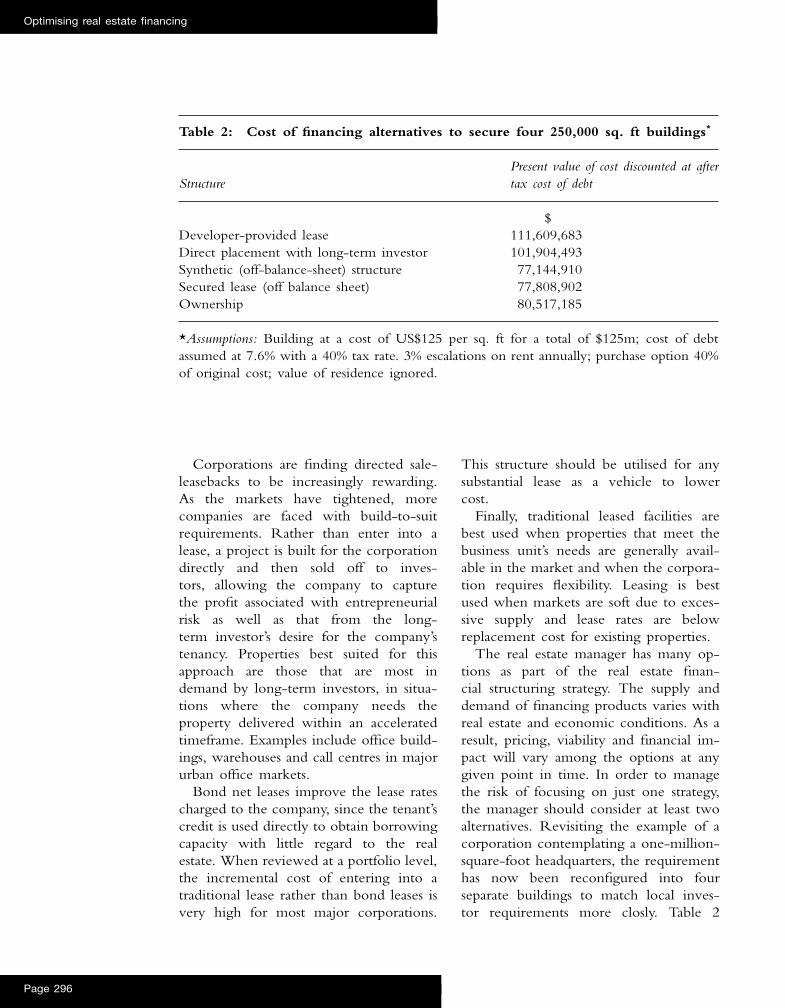

The real estate manager has many op-tions as part of the real estate finan-cial structuring strategy. The supply anddemand of financing products varies withreal estate and economic conditions. As aresult, pricing, viability and financial im-pact will vary among the options at anygiven point in time. In order to managethe risk of focusing on just one strategy,the manager should consider at least twoalternatives. Revisiting the example of acorporation contemplating a one-million-square-foot headquarters, the requirementhas now been reconfigured into fourseparate buildings to match local inves-tor requirements more closly. Table 2

Optimising real estate financing

Page 296

Table 2: Cost of financing alternatives to secure four 250,000 sq. ft buildings*

StructurePresent value of cost discounted at aftertax cost of debt

$Developer-provided lease 111,609,683Direct placement with long-term investor 101,904,493Synthetic (off-balance-sheet) structure 77,144,910Secured lease (off balance sheet) 77,808,902Ownership 80,517,185

*Assumptions: Building at a cost of US$125 per sq. ft for a total of $125m; cost of debtassumed at 7.6% with a 40% tax rate. 3% escalations on rent annually; purchase option 40%of original cost; value of residence ignored.

CONCLUSIONIn order to capture opportunities withina company’s portfolio, financial structuringmust be an integral part of the approachto corporation real estate solutions andportfolio strategies. When integrated, thenumber of unique assets requiring di-rect corporate funding can be reduceddramatically by using real estate marketknowledge, investor preferences and busi-ness unit utilisation as a road map. It isimperative, however, that the real estatemanager and business unit are prepared tomodify their space requirements to en-sure financial and investment communitymarketability. In a portfolio, opportunitiescan be captured by studying shifts in thereal estate market over time and convert-ing that knowledge into lower real estatecost. Using this process, a corporation thatroutinely re-evaluates its portfolio canoptimise the portfolio’s effects on thecorporation’s balance sheet and incomestatement.

�Equis Corporation

shows a sample of some structuring op-tions and the associated resulting costs forthis hypothetical project.

While the present value cost can varydramatically, as the results in the tabledemonstrate, cost should not be thedriving factor alone, because the businessunit needs to evaluate the cost in thebroader context along with operational,accounting and financial impacts andflexibility.

THE DECISIONAfter gathering the relevant informationand evaluating the pros and cons of eachsolution, the real estate manager can makea sound recommendation to the businessunit and the treasury department. Themanager knows that the solution is ac-ceptable to the marketplace, can provideflexibility in the event of a changedbusiness model, and provides the space atthe most reasonable cost, both initiallyand over the corporation’s long-term oc-cupancy.

Krzysko and Marciniak

Page 297