Embed Size (px)

Citation preview

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 307

A COMPARATIVE STUDY OF CUSTOMER PREFERENCES TOWARDS THE PUBLIC AND PRIVATE SECTOR BANKS OF INDIA

Dr. Virender Khanna

Head of Department, FDDI School of Business & Entrepreneurship ABSTRACT Research aims to study the customer preference towards using various parameters such as; interest rate, transaction time, transaction charges and safety in transaction etc. in public and private sector banks. The purpose behind this survey is to know which parameters are more important that makes a customer to prefer a particular bank over others. The study was conducted on a sample of 400 customers of public and private banks of India, who are availing any type of international banking services from these four banks such as; foreign exchange, factoring, bank guarantee or letter of credit. Total four banks have been surveyed during the study namely; HDFC and ICICI from private banks and PNB and SBI from public banks. It was found from the study that there is a there is a significant difference in the customer preferences of public and private sector banks’ customers towards the various parameters which influence them to select a particular bank for getting international banking services. Customers of public sector banks prefer banks due to low interest rates, safety in transactions, low transaction charges, wide variety of product portfolio, IT enabled services, and size of the banks or large network of branches in the country and overseas. Customers of private sector banks prefer private banks due to high brand image, ease of operations, high level of customer services, and low transaction time. KEYWORDS: Customer preferences, Public banks, Private Banks, Customer services, Brand Image and Bank transactions. 1. INTRODUCTION Indian banking sector is one of the core sector of Indian economy which is contributing highly to the growth of the economy. It is the life blood of Indian economy. Indian banking sector plays an important and dynamic role in flow of funds from the surplus unit to deficit unit. Banking sector comes under service sector, and among service sector banking sector is the highest growing sector, in terms of contribution to GDP of the country. Earlier, the scope or function of the banks was limited to the deposit and lending money, but now banks are becoming versatile. Banking functions have expanded so widely which creates the segregation of different type of banking such as; investment banking, corporate banking, retail banking etc. With the technological development, banking services mode has also changed. Earlier banking services were confined to the branch only, now there are various modes of banking services such as; branch banking, home banking, phone banking, mobile banking, online banking etc. There is a huge competition in the banking sector. After liberalization process, various new banks came into existence; foreign banks also started their functions in the country, which increased the intensity of the competition in the banking sector. Banking industry is a service oriented industry, thus there are no physical products and the success of the banks purely depends on the delivery of the services. Thus, customers and employees both play an important role in the success of the banks. Due to drastic change in the demographic profile of the customers, needs and expectations of the customers have also changed. Demographic changes such as; size of family, income of citizens, life styles of the

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 308

people, risk taking capacity, future planning, working status of females, more focused on education of children, desires for luxury life has increased. Accordingly, the need of the banking products is also changing. All the banks are providing same products, and then it becomes more challenging for the banks to differentiate from competitors. The only weapon in the hands of the bankers is to provide the quality services, provide something extra with the banking products in order to attract the customers. Service quality of the banks plays an important role in attracting the customers (Mistry, 2013). Highly customized services, less pain to customers for getting services and delivering the services on time and fulfilling the promises are essential elements which can help not only in attracting the new customers but also in retaining the existing customers (Rabb, 2015 and Van & Lee, 2012). Banks have various types of customers such as; retail customers, corporate customers etc. among all these types of customers the most important customers are those who get the services of the banks for international banking such as; import bill, export bill, letter of credit, bank guarantee, and factors services. Banks are an important component of the cross border businesses. Bank plays as a third party role to cover the risk of the national party. Export, import these are two main pillar of balance of payment of any country. In international banking, the transactions are less in numbers but the amount involved in the transactions is very high. Due to this fact, it becomes more important for the banks to attract the customers who give high value business to the banks. Similarly, it also becomes important for bank to keep these customers happy and satisfied towards the service quality as these are businessman and they are repeated customers of the banks. Customers who are satisfied will only come back to the banks for repetitive services (Khurshid and Singh, 2013, Sharma, 2011). Thus, it is very important for the banks to make its customers highly satisfied with the services quality and products who are getting banking services related to international banking from the banks. Thus, keeping in view the importance of customer satisfaction in international banking, researcher has made an attempt to measure the customer preferences towards the parameters which influences the decision of customers to select a bank for getting international banking services. 2. REVIEW OF LITERATURE There is a vast literature available on service quality and customer satisfaction in retail banks, toward online banking, e-banking, branch banking, or technological developments of banks. Researchers (Akgam, 2016, Chandra & Bhattacharya, 2013, Mkoma, 2014, Nagabhushanam, 2015) have highlighted various factors which makes a customer satisfied with the services of the banks. These factors are mainly; employees’ behaviour, tangible work environment, customer services of the bank, interest rates etc. Retail bank customers mostly prefer the banks which offer ow interest rates on loans have variety of products and have large number of branches (Anita & Singh, 2013). E-banking customers shows more concern towards the safety in transactions and confidentiality thus, prefers the banks which provides high safety, secure norms, and keeps the information of the customers confidential (Jayshree & Ahmad, 2015). Corporate customers usually show more preference towards the banking transactions, such as time taken by the bank to complete a transaction, charges involved in a transaction and the self-services or technological developments. Anubhav (2010) stated in their study that reliability is found as a highest significant factor which leads to customer satisfaction in banking sector. Customer’s avails banking services from the banks on whom they can trust. Trust of the customers depends on the various factors such as; accuracy of records, no hidden charges, less time in banking transactions, high transparency norms, and disclosure practices of the bank (Chitra, 2013, Maduku, 2013, Joicey, 2013). Banking environment also plays an important role in attracting potential customers. High quality IT enabled services, latest equipment, interior of the banks and the other technological development influences the

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 309

decision of the customers to select a bank for getting services (Daikh, 2015 and Ganesh, 2012). There is a huge literature available on retail customers, online customers but there is a lack of studies where the researchers have measured the preferences of customers who avail the international banking services. Researchers have measured the difference in service quality, customer satisfaction, in private and public sector banks. Kumar et al. (2010) researchers have extracted total five dimensions of services quality of private retail banks which have a direct influence on the customer loyalty and customer satisfaction towards the retail banking services. These factors or attributes of service quality are mainly; customer services, employees, physical environment, trust, and corporate image. It was stated that private retail banks need to focus on the practices of hidden charges, reducing the service charges and ensuring the safety of the transactions and interest of the customers to improve the customer satisfaction towards the retail banking services of the private sector banks in India. Bedi (2010) made a comparison of customer satisfaction in the banks towards the retail banking services. It was found that service quality is higher in private sector banks than public sector banks. Customers’ perception towards the four dimensions of service quality of retail banking is higher for private banks than public banks. Vimi and Kaleem (2008) stated that there are various factors where both the public and private sector banks need to work such as; willingness of the banking staff to resolve the complaints of the customers, to respond to the queries of the customers, providing prompt services, keeping the promises to the customers for providing any services, and the helpful nature of the employees towards the customers. These are some of the measures that both the public and private banks can implement to improve the level of customer satisfaction, to retain the existing customers for long term, and to make a positive image in the market. There is a lack of studies where researchers have made a comparison of customers’ preferences towards the public or private sector banks. Current study will try to bridge the gap found from the literature review. 3. OBJECTIVES 1. To measure the customer preferences towards the parameters of banks. 2. To make a comparative study of customer preferences towards the private and public sector banks of

India.

4. RESEARCH METHODOLOGY Current study is based on the opinions of the customers towards the various parameters of the banks which help them in selection of a bank for getting international banking services. Data has been collected from the 400 customers of the four public and private sector banks namely; HDFC, ICICI, PNB and SBI bank. Researchers have obtained a list of corporate customers of the bank who are getting services of the banks related to export or import bill, bank guarantees, letter of credit, or factoring services. These customers were contacted personally and through email to fill the survey designed by the researchers. Ten parameters have been selected by the researchers based on the review of literature and the customers’ preferences have been measured towards these parameters. A comparison has been made among public and private sector banks related to the customers’ preferences. Following hypothesis have been formulated and tested during the current study: Null Hypothesis: There is no significant difference between the customers’ preferences towards international banking of public and private sector banks. Null Hypothesis: There is no significant difference between the customers’ preferences towards international banking of selected four banks namely; ICICI, PNB, SBI and HDFC.

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 310

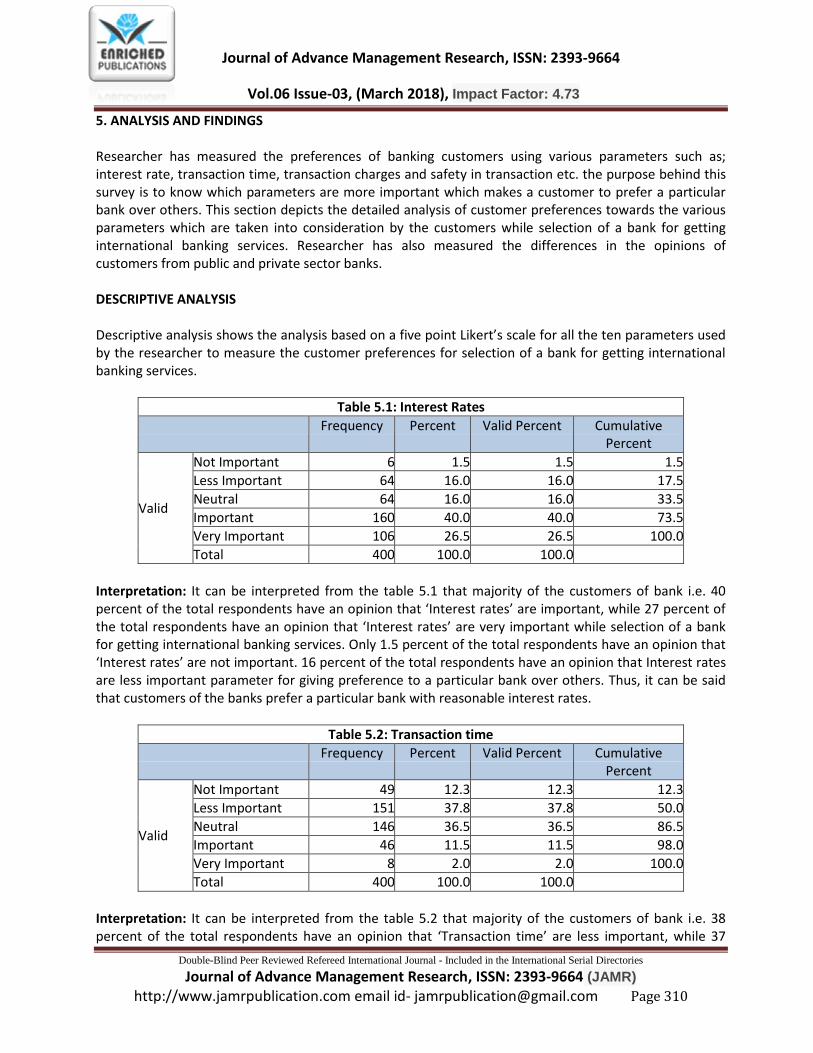

5. ANALYSIS AND FINDINGS Researcher has measured the preferences of banking customers using various parameters such as; interest rate, transaction time, transaction charges and safety in transaction etc. the purpose behind this survey is to know which parameters are more important which makes a customer to prefer a particular bank over others. This section depicts the detailed analysis of customer preferences towards the various parameters which are taken into consideration by the customers while selection of a bank for getting international banking services. Researcher has also measured the differences in the opinions of customers from public and private sector banks. DESCRIPTIVE ANALYSIS Descriptive analysis shows the analysis based on a five point Likert’s scale for all the ten parameters used by the researcher to measure the customer preferences for selection of a bank for getting international banking services.

Table 5.1: Interest Rates

Frequency Percent Valid Percent Cumulative Percent

Valid

Not Important 6 1.5 1.5 1.5

Less Important 64 16.0 16.0 17.5

Neutral 64 16.0 16.0 33.5

Important 160 40.0 40.0 73.5

Very Important 106 26.5 26.5 100.0

Total 400 100.0 100.0

Interpretation: It can be interpreted from the table 5.1 that majority of the customers of bank i.e. 40 percent of the total respondents have an opinion that ‘Interest rates’ are important, while 27 percent of the total respondents have an opinion that ‘Interest rates’ are very important while selection of a bank for getting international banking services. Only 1.5 percent of the total respondents have an opinion that ‘Interest rates’ are not important. 16 percent of the total respondents have an opinion that Interest rates are less important parameter for giving preference to a particular bank over others. Thus, it can be said that customers of the banks prefer a particular bank with reasonable interest rates.

Table 5.2: Transaction time

Frequency Percent Valid Percent Cumulative Percent

Valid

Not Important 49 12.3 12.3 12.3

Less Important 151 37.8 37.8 50.0

Neutral 146 36.5 36.5 86.5

Important 46 11.5 11.5 98.0

Very Important 8 2.0 2.0 100.0

Total 400 100.0 100.0

Interpretation: It can be interpreted from the table 5.2 that majority of the customers of bank i.e. 38 percent of the total respondents have an opinion that ‘Transaction time’ are less important, while 37

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 311

percent of the total respondents have an opinion that ‘Transaction time’ are neither important nor unimportant while selection of a bank for getting international banking services. Only 2.0 percent of the total respondents have an opinion that ‘Transaction time’ is very important. 12 percent of the total respondents have an opinion that ‘Transaction time’ is not important parameter for giving preference to a particular bank over others. Thus, it can be said that customers of the banks prefer a particular bank with minimum transaction time.

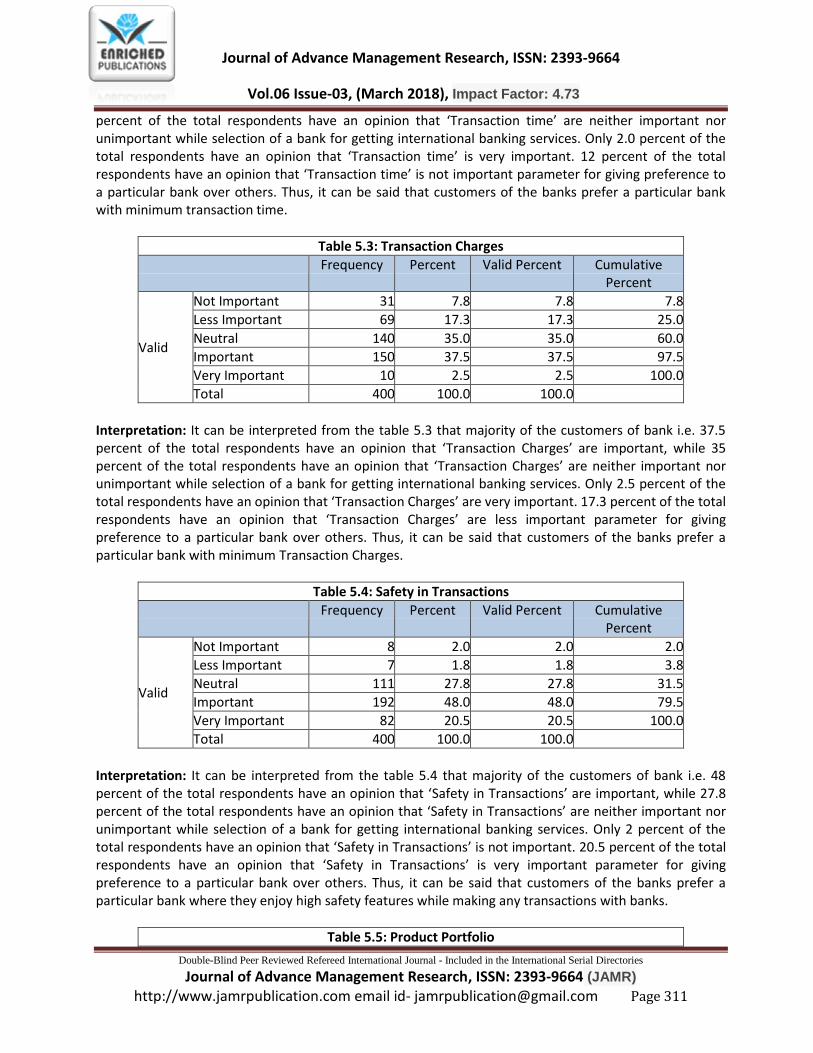

Table 5.3: Transaction Charges

Frequency Percent Valid Percent Cumulative Percent

Valid

Not Important 31 7.8 7.8 7.8

Less Important 69 17.3 17.3 25.0

Neutral 140 35.0 35.0 60.0

Important 150 37.5 37.5 97.5

Very Important 10 2.5 2.5 100.0

Total 400 100.0 100.0

Interpretation: It can be interpreted from the table 5.3 that majority of the customers of bank i.e. 37.5 percent of the total respondents have an opinion that ‘Transaction Charges’ are important, while 35 percent of the total respondents have an opinion that ‘Transaction Charges’ are neither important nor unimportant while selection of a bank for getting international banking services. Only 2.5 percent of the total respondents have an opinion that ‘Transaction Charges’ are very important. 17.3 percent of the total respondents have an opinion that ‘Transaction Charges’ are less important parameter for giving preference to a particular bank over others. Thus, it can be said that customers of the banks prefer a particular bank with minimum Transaction Charges.

Table 5.4: Safety in Transactions

Frequency Percent Valid Percent Cumulative Percent

Valid

Not Important 8 2.0 2.0 2.0

Less Important 7 1.8 1.8 3.8

Neutral 111 27.8 27.8 31.5

Important 192 48.0 48.0 79.5

Very Important 82 20.5 20.5 100.0

Total 400 100.0 100.0

Interpretation: It can be interpreted from the table 5.4 that majority of the customers of bank i.e. 48 percent of the total respondents have an opinion that ‘Safety in Transactions’ are important, while 27.8 percent of the total respondents have an opinion that ‘Safety in Transactions’ are neither important nor unimportant while selection of a bank for getting international banking services. Only 2 percent of the total respondents have an opinion that ‘Safety in Transactions’ is not important. 20.5 percent of the total respondents have an opinion that ‘Safety in Transactions’ is very important parameter for giving preference to a particular bank over others. Thus, it can be said that customers of the banks prefer a particular bank where they enjoy high safety features while making any transactions with banks.

Table 5.5: Product Portfolio

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 312

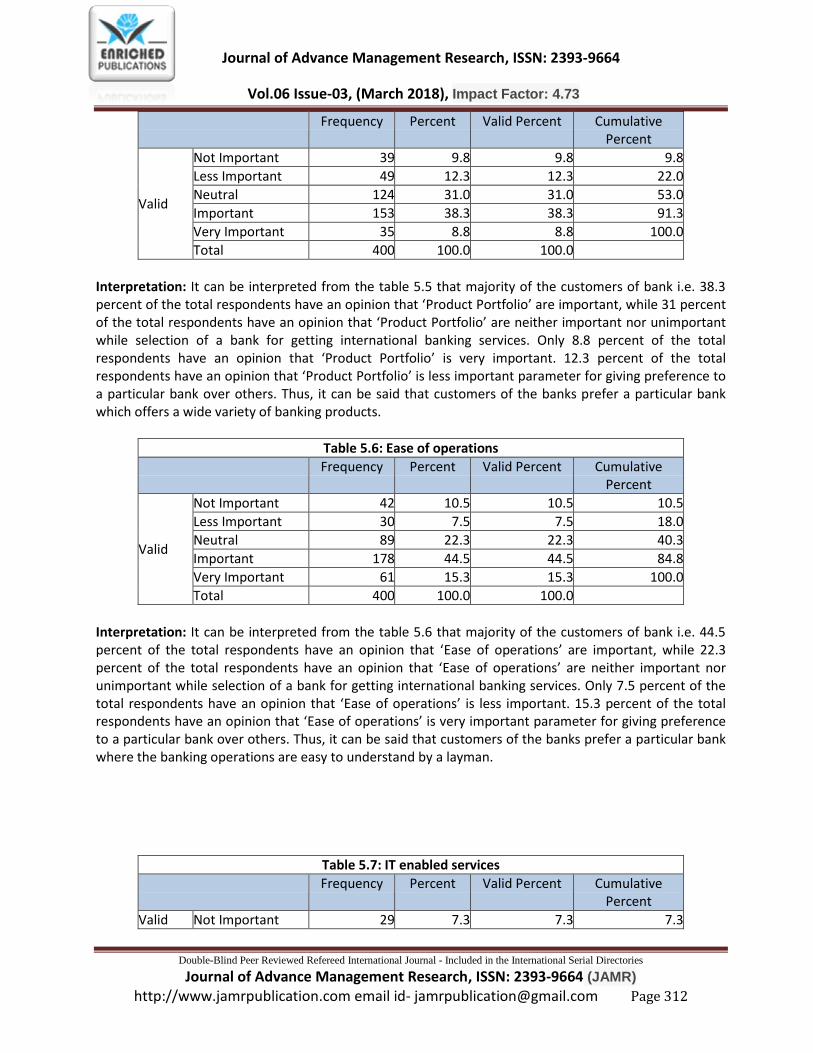

Frequency Percent Valid Percent Cumulative Percent

Valid

Not Important 39 9.8 9.8 9.8

Less Important 49 12.3 12.3 22.0

Neutral 124 31.0 31.0 53.0

Important 153 38.3 38.3 91.3

Very Important 35 8.8 8.8 100.0

Total 400 100.0 100.0

Interpretation: It can be interpreted from the table 5.5 that majority of the customers of bank i.e. 38.3 percent of the total respondents have an opinion that ‘Product Portfolio’ are important, while 31 percent of the total respondents have an opinion that ‘Product Portfolio’ are neither important nor unimportant while selection of a bank for getting international banking services. Only 8.8 percent of the total respondents have an opinion that ‘Product Portfolio’ is very important. 12.3 percent of the total respondents have an opinion that ‘Product Portfolio’ is less important parameter for giving preference to a particular bank over others. Thus, it can be said that customers of the banks prefer a particular bank which offers a wide variety of banking products.

Table 5.6: Ease of operations

Frequency Percent Valid Percent Cumulative Percent

Valid

Not Important 42 10.5 10.5 10.5

Less Important 30 7.5 7.5 18.0

Neutral 89 22.3 22.3 40.3

Important 178 44.5 44.5 84.8

Very Important 61 15.3 15.3 100.0

Total 400 100.0 100.0

Interpretation: It can be interpreted from the table 5.6 that majority of the customers of bank i.e. 44.5 percent of the total respondents have an opinion that ‘Ease of operations’ are important, while 22.3 percent of the total respondents have an opinion that ‘Ease of operations’ are neither important nor unimportant while selection of a bank for getting international banking services. Only 7.5 percent of the total respondents have an opinion that ‘Ease of operations’ is less important. 15.3 percent of the total respondents have an opinion that ‘Ease of operations’ is very important parameter for giving preference to a particular bank over others. Thus, it can be said that customers of the banks prefer a particular bank where the banking operations are easy to understand by a layman.

Table 5.7: IT enabled services

Frequency Percent Valid Percent Cumulative Percent

Valid Not Important 29 7.3 7.3 7.3

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 313

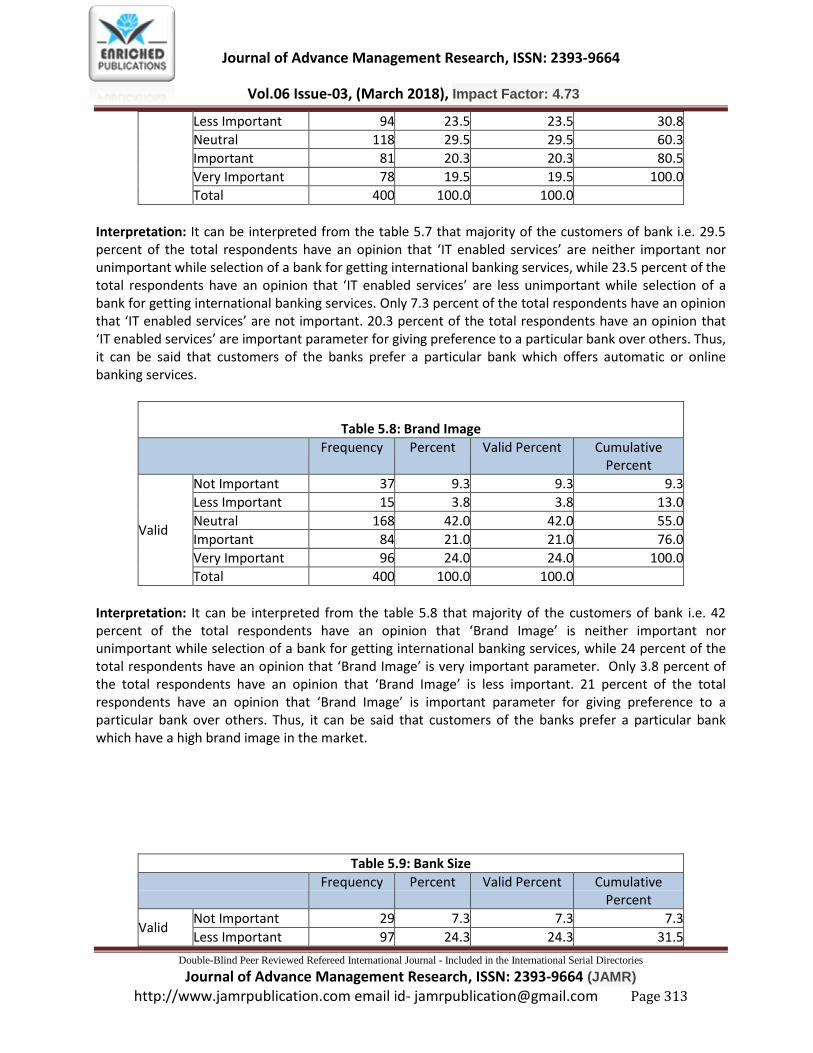

Less Important 94 23.5 23.5 30.8

Neutral 118 29.5 29.5 60.3

Important 81 20.3 20.3 80.5

Very Important 78 19.5 19.5 100.0

Total 400 100.0 100.0

Interpretation: It can be interpreted from the table 5.7 that majority of the customers of bank i.e. 29.5 percent of the total respondents have an opinion that ‘IT enabled services’ are neither important nor unimportant while selection of a bank for getting international banking services, while 23.5 percent of the total respondents have an opinion that ‘IT enabled services’ are less unimportant while selection of a bank for getting international banking services. Only 7.3 percent of the total respondents have an opinion that ‘IT enabled services’ are not important. 20.3 percent of the total respondents have an opinion that ‘IT enabled services’ are important parameter for giving preference to a particular bank over others. Thus, it can be said that customers of the banks prefer a particular bank which offers automatic or online banking services.

Table 5.8: Brand Image

Frequency Percent Valid Percent Cumulative Percent

Valid

Not Important 37 9.3 9.3 9.3

Less Important 15 3.8 3.8 13.0

Neutral 168 42.0 42.0 55.0

Important 84 21.0 21.0 76.0

Very Important 96 24.0 24.0 100.0

Total 400 100.0 100.0

Interpretation: It can be interpreted from the table 5.8 that majority of the customers of bank i.e. 42 percent of the total respondents have an opinion that ‘Brand Image’ is neither important nor unimportant while selection of a bank for getting international banking services, while 24 percent of the total respondents have an opinion that ‘Brand Image’ is very important parameter. Only 3.8 percent of the total respondents have an opinion that ‘Brand Image’ is less important. 21 percent of the total respondents have an opinion that ‘Brand Image’ is important parameter for giving preference to a particular bank over others. Thus, it can be said that customers of the banks prefer a particular bank which have a high brand image in the market.

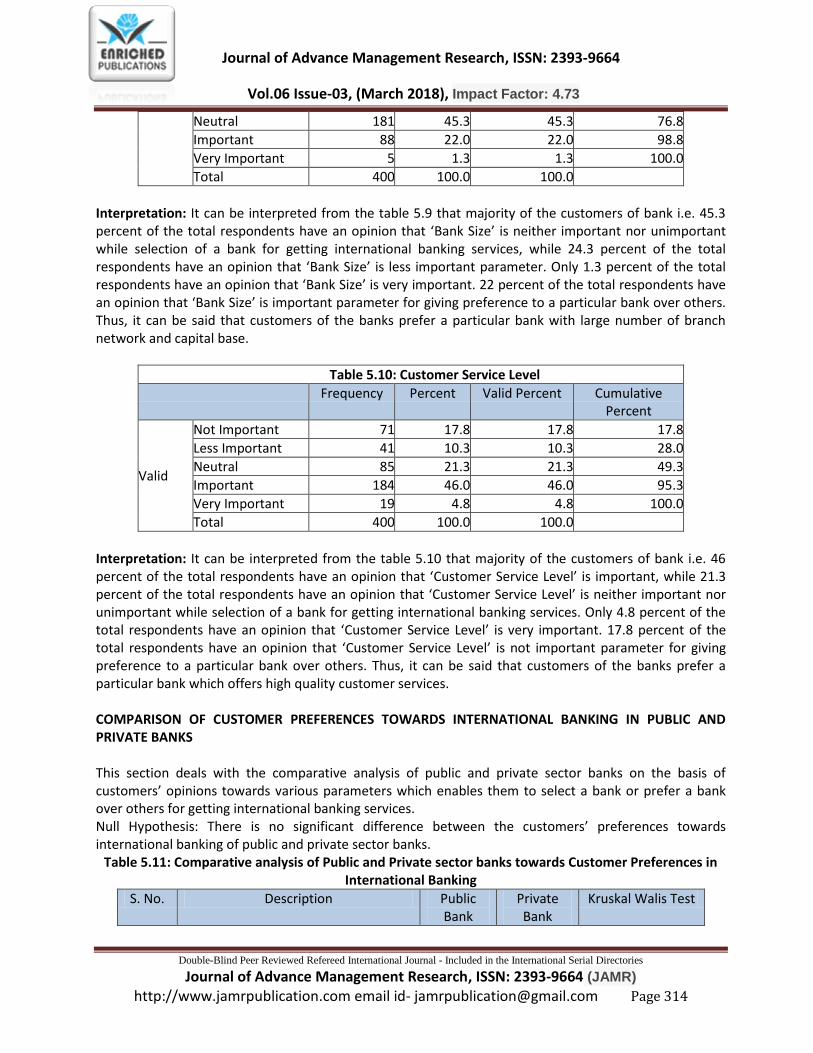

Table 5.9: Bank Size

Frequency Percent Valid Percent Cumulative Percent

Valid Not Important 29 7.3 7.3 7.3

Less Important 97 24.3 24.3 31.5

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 314

Neutral 181 45.3 45.3 76.8

Important 88 22.0 22.0 98.8

Very Important 5 1.3 1.3 100.0

Total 400 100.0 100.0

Interpretation: It can be interpreted from the table 5.9 that majority of the customers of bank i.e. 45.3 percent of the total respondents have an opinion that ‘Bank Size’ is neither important nor unimportant while selection of a bank for getting international banking services, while 24.3 percent of the total respondents have an opinion that ‘Bank Size’ is less important parameter. Only 1.3 percent of the total respondents have an opinion that ‘Bank Size’ is very important. 22 percent of the total respondents have an opinion that ‘Bank Size’ is important parameter for giving preference to a particular bank over others. Thus, it can be said that customers of the banks prefer a particular bank with large number of branch network and capital base.

Table 5.10: Customer Service Level

Frequency Percent Valid Percent Cumulative Percent

Valid

Not Important 71 17.8 17.8 17.8

Less Important 41 10.3 10.3 28.0

Neutral 85 21.3 21.3 49.3

Important 184 46.0 46.0 95.3

Very Important 19 4.8 4.8 100.0

Total 400 100.0 100.0

Interpretation: It can be interpreted from the table 5.10 that majority of the customers of bank i.e. 46 percent of the total respondents have an opinion that ‘Customer Service Level’ is important, while 21.3 percent of the total respondents have an opinion that ‘Customer Service Level’ is neither important nor unimportant while selection of a bank for getting international banking services. Only 4.8 percent of the total respondents have an opinion that ‘Customer Service Level’ is very important. 17.8 percent of the total respondents have an opinion that ‘Customer Service Level’ is not important parameter for giving preference to a particular bank over others. Thus, it can be said that customers of the banks prefer a particular bank which offers high quality customer services. COMPARISON OF CUSTOMER PREFERENCES TOWARDS INTERNATIONAL BANKING IN PUBLIC AND PRIVATE BANKS This section deals with the comparative analysis of public and private sector banks on the basis of customers’ opinions towards various parameters which enables them to select a bank or prefer a bank over others for getting international banking services. Null Hypothesis: There is no significant difference between the customers’ preferences towards international banking of public and private sector banks.

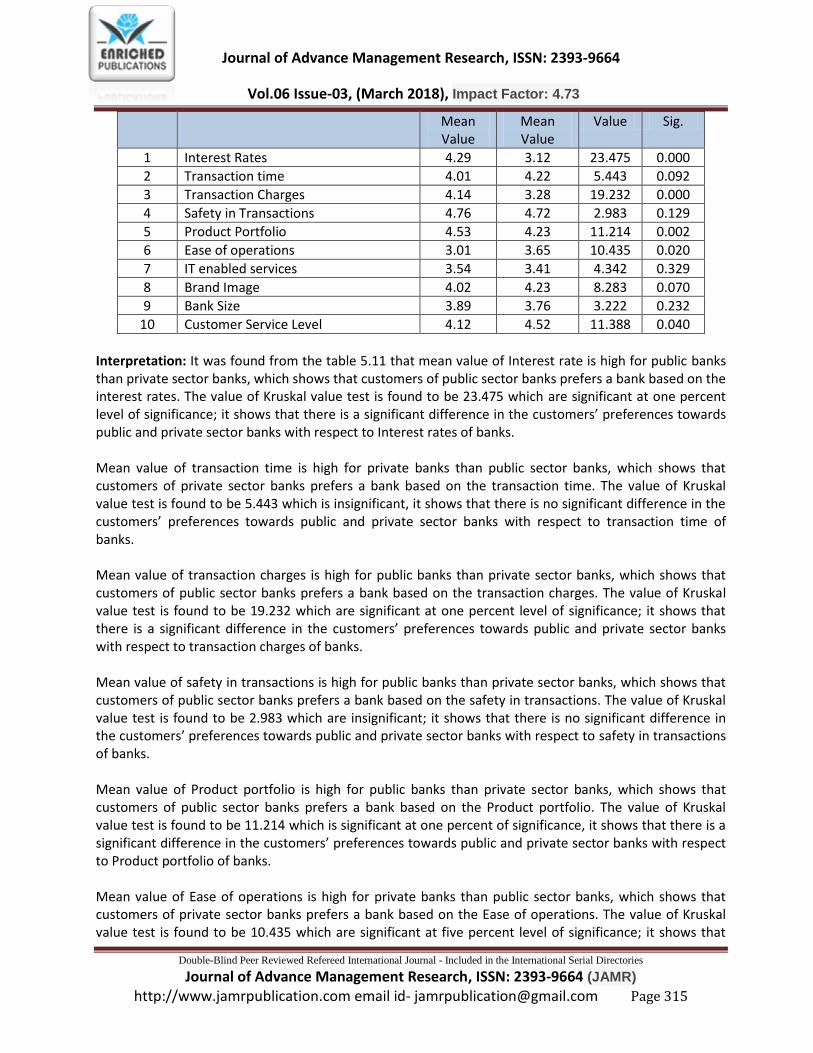

Table 5.11: Comparative analysis of Public and Private sector banks towards Customer Preferences in International Banking

S. No. Description Public Bank

Private Bank

Kruskal Walis Test

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 315

Mean Value

Mean Value

Value Sig.

1 Interest Rates 4.29 3.12 23.475 0.000

2 Transaction time 4.01 4.22 5.443 0.092

3 Transaction Charges 4.14 3.28 19.232 0.000

4 Safety in Transactions 4.76 4.72 2.983 0.129

5 Product Portfolio 4.53 4.23 11.214 0.002

6 Ease of operations 3.01 3.65 10.435 0.020

7 IT enabled services 3.54 3.41 4.342 0.329

8 Brand Image 4.02 4.23 8.283 0.070

9 Bank Size 3.89 3.76 3.222 0.232

10 Customer Service Level 4.12 4.52 11.388 0.040

Interpretation: It was found from the table 5.11 that mean value of Interest rate is high for public banks than private sector banks, which shows that customers of public sector banks prefers a bank based on the interest rates. The value of Kruskal value test is found to be 23.475 which are significant at one percent level of significance; it shows that there is a significant difference in the customers’ preferences towards public and private sector banks with respect to Interest rates of banks. Mean value of transaction time is high for private banks than public sector banks, which shows that customers of private sector banks prefers a bank based on the transaction time. The value of Kruskal value test is found to be 5.443 which is insignificant, it shows that there is no significant difference in the customers’ preferences towards public and private sector banks with respect to transaction time of banks. Mean value of transaction charges is high for public banks than private sector banks, which shows that customers of public sector banks prefers a bank based on the transaction charges. The value of Kruskal value test is found to be 19.232 which are significant at one percent level of significance; it shows that there is a significant difference in the customers’ preferences towards public and private sector banks with respect to transaction charges of banks. Mean value of safety in transactions is high for public banks than private sector banks, which shows that customers of public sector banks prefers a bank based on the safety in transactions. The value of Kruskal value test is found to be 2.983 which are insignificant; it shows that there is no significant difference in the customers’ preferences towards public and private sector banks with respect to safety in transactions of banks. Mean value of Product portfolio is high for public banks than private sector banks, which shows that customers of public sector banks prefers a bank based on the Product portfolio. The value of Kruskal value test is found to be 11.214 which is significant at one percent of significance, it shows that there is a significant difference in the customers’ preferences towards public and private sector banks with respect to Product portfolio of banks. Mean value of Ease of operations is high for private banks than public sector banks, which shows that customers of private sector banks prefers a bank based on the Ease of operations. The value of Kruskal value test is found to be 10.435 which are significant at five percent level of significance; it shows that

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 316

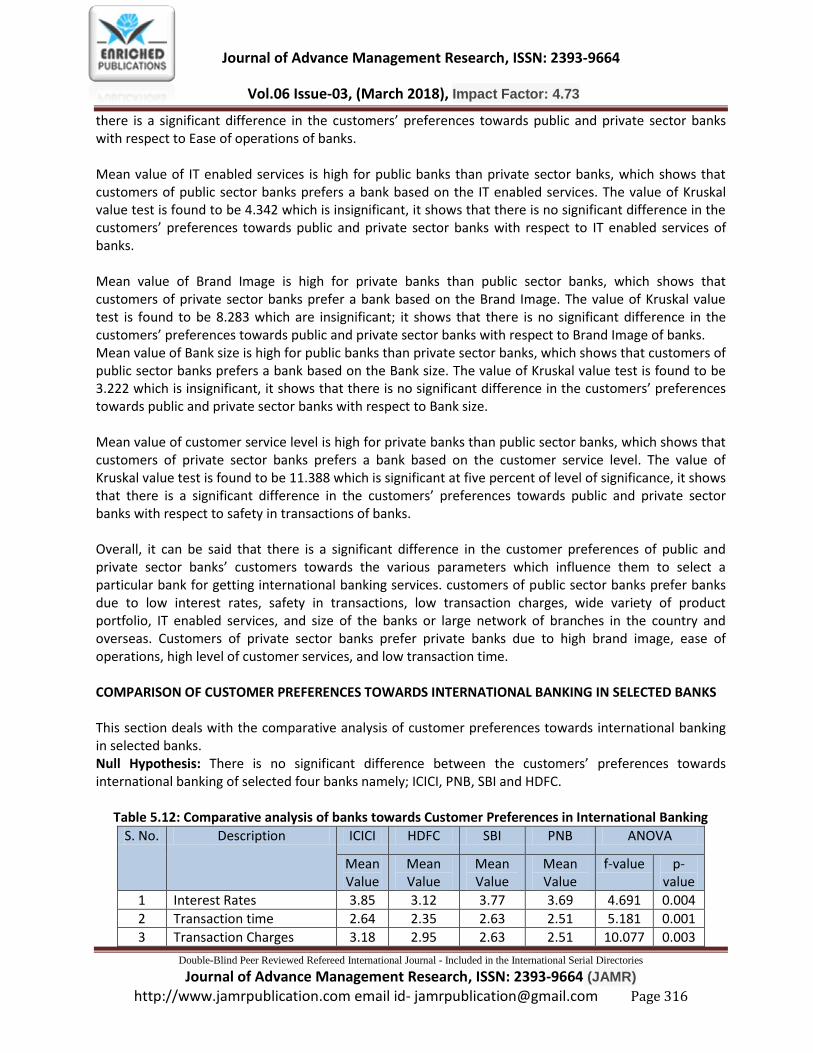

there is a significant difference in the customers’ preferences towards public and private sector banks with respect to Ease of operations of banks. Mean value of IT enabled services is high for public banks than private sector banks, which shows that customers of public sector banks prefers a bank based on the IT enabled services. The value of Kruskal value test is found to be 4.342 which is insignificant, it shows that there is no significant difference in the customers’ preferences towards public and private sector banks with respect to IT enabled services of banks. Mean value of Brand Image is high for private banks than public sector banks, which shows that customers of private sector banks prefer a bank based on the Brand Image. The value of Kruskal value test is found to be 8.283 which are insignificant; it shows that there is no significant difference in the customers’ preferences towards public and private sector banks with respect to Brand Image of banks. Mean value of Bank size is high for public banks than private sector banks, which shows that customers of public sector banks prefers a bank based on the Bank size. The value of Kruskal value test is found to be 3.222 which is insignificant, it shows that there is no significant difference in the customers’ preferences towards public and private sector banks with respect to Bank size. Mean value of customer service level is high for private banks than public sector banks, which shows that customers of private sector banks prefers a bank based on the customer service level. The value of Kruskal value test is found to be 11.388 which is significant at five percent of level of significance, it shows that there is a significant difference in the customers’ preferences towards public and private sector banks with respect to safety in transactions of banks. Overall, it can be said that there is a significant difference in the customer preferences of public and private sector banks’ customers towards the various parameters which influence them to select a particular bank for getting international banking services. customers of public sector banks prefer banks due to low interest rates, safety in transactions, low transaction charges, wide variety of product portfolio, IT enabled services, and size of the banks or large network of branches in the country and overseas. Customers of private sector banks prefer private banks due to high brand image, ease of operations, high level of customer services, and low transaction time. COMPARISON OF CUSTOMER PREFERENCES TOWARDS INTERNATIONAL BANKING IN SELECTED BANKS This section deals with the comparative analysis of customer preferences towards international banking in selected banks. Null Hypothesis: There is no significant difference between the customers’ preferences towards international banking of selected four banks namely; ICICI, PNB, SBI and HDFC.

Table 5.12: Comparative analysis of banks towards Customer Preferences in International Banking

S. No. Description ICICI HDFC SBI PNB ANOVA

Mean Value

Mean Value

Mean Value

Mean Value

f-value p-value

1 Interest Rates 3.85 3.12 3.77 3.69 4.691 0.004

2 Transaction time 2.64 2.35 2.63 2.51 5.181 0.001

3 Transaction Charges 3.18 2.95 2.63 2.51 10.077 0.003

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 317

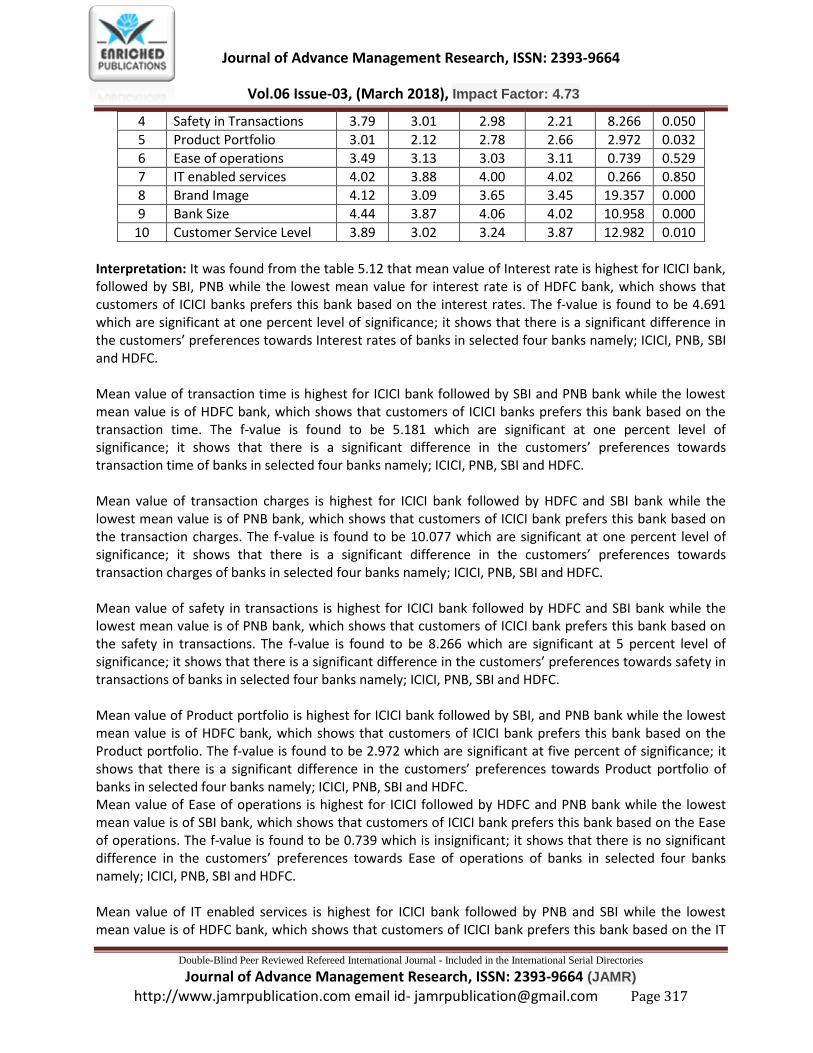

4 Safety in Transactions 3.79 3.01 2.98 2.21 8.266 0.050

5 Product Portfolio 3.01 2.12 2.78 2.66 2.972 0.032

6 Ease of operations 3.49 3.13 3.03 3.11 0.739 0.529

7 IT enabled services 4.02 3.88 4.00 4.02 0.266 0.850

8 Brand Image 4.12 3.09 3.65 3.45 19.357 0.000

9 Bank Size 4.44 3.87 4.06 4.02 10.958 0.000

10 Customer Service Level 3.89 3.02 3.24 3.87 12.982 0.010

Interpretation: It was found from the table 5.12 that mean value of Interest rate is highest for ICICI bank, followed by SBI, PNB while the lowest mean value for interest rate is of HDFC bank, which shows that customers of ICICI banks prefers this bank based on the interest rates. The f-value is found to be 4.691 which are significant at one percent level of significance; it shows that there is a significant difference in the customers’ preferences towards Interest rates of banks in selected four banks namely; ICICI, PNB, SBI and HDFC. Mean value of transaction time is highest for ICICI bank followed by SBI and PNB bank while the lowest mean value is of HDFC bank, which shows that customers of ICICI banks prefers this bank based on the transaction time. The f-value is found to be 5.181 which are significant at one percent level of significance; it shows that there is a significant difference in the customers’ preferences towards transaction time of banks in selected four banks namely; ICICI, PNB, SBI and HDFC. Mean value of transaction charges is highest for ICICI bank followed by HDFC and SBI bank while the lowest mean value is of PNB bank, which shows that customers of ICICI bank prefers this bank based on the transaction charges. The f-value is found to be 10.077 which are significant at one percent level of significance; it shows that there is a significant difference in the customers’ preferences towards transaction charges of banks in selected four banks namely; ICICI, PNB, SBI and HDFC. Mean value of safety in transactions is highest for ICICI bank followed by HDFC and SBI bank while the lowest mean value is of PNB bank, which shows that customers of ICICI bank prefers this bank based on the safety in transactions. The f-value is found to be 8.266 which are significant at 5 percent level of significance; it shows that there is a significant difference in the customers’ preferences towards safety in transactions of banks in selected four banks namely; ICICI, PNB, SBI and HDFC. Mean value of Product portfolio is highest for ICICI bank followed by SBI, and PNB bank while the lowest mean value is of HDFC bank, which shows that customers of ICICI bank prefers this bank based on the Product portfolio. The f-value is found to be 2.972 which are significant at five percent of significance; it shows that there is a significant difference in the customers’ preferences towards Product portfolio of banks in selected four banks namely; ICICI, PNB, SBI and HDFC. Mean value of Ease of operations is highest for ICICI followed by HDFC and PNB bank while the lowest mean value is of SBI bank, which shows that customers of ICICI bank prefers this bank based on the Ease of operations. The f-value is found to be 0.739 which is insignificant; it shows that there is no significant difference in the customers’ preferences towards Ease of operations of banks in selected four banks namely; ICICI, PNB, SBI and HDFC. Mean value of IT enabled services is highest for ICICI bank followed by PNB and SBI while the lowest mean value is of HDFC bank, which shows that customers of ICICI bank prefers this bank based on the IT

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 318

enabled services. The f-value is found to be 0.266 which is insignificant; it shows that there is no significant difference in the customers’ preferences towards IT enabled services of banks in selected four banks namely; ICICI, PNB, SBI and HDFC. Mean value of Brand Image is highest ICICI bank followed by SBI and PNB while the lowest mean value for Brand Image is of HDFC bank, which shows that customers of ICICI bank prefers this bank based on the Brand Image. The f-value is found to be 19.357 which are significant at one percent level of significance; it shows that there is a significant difference in the customers’ preferences towards Brand Image of banks in selected four banks namely; ICICI, PNB, SBI and HDFC. Mean value of Bank size is highest for ICICI bank followed by SBI and PNB while the lowest mean value for Bank size is of HDFC bank, which shows that customers of ICICI bank prefers this bank based on the Bank size. The f-value is found to be 10.958 which are significant at one percent of level of significance; it shows that there is a significant difference in the customers’ preferences towards Bank size in selected four banks namely; ICICI, PNB, SBI and HDFC. Mean value of customer service level is highest for ICICI bank followed by PNB, and SBI, while the lowest mean value for customer service level is of HDFC bank, which shows that customers of ICICI prefers this bank based on the customer service level. The f-value is found to be 12.982 which is significant at one percent of level of significance, it shows that there is a significant difference in the customers’ preferences towards safety in transactions in selected four banks namely; ICICI, PNB, SBI and HDFC. CONCLUSION Overall, it can be concluded that there is a significant difference in the customer preferences towards international banking of selected four banks namely; ICICI, PNB, SBI and HDFC. It can be seen from the comparative analysis that customers of ICICI bank preferred this particular bank due to all the mentioned parameters, while the customers of HDFC bank have not considered these ten parameters as important for selection of a bank or giving preference to a particular bank over other for getting international banking services. Thus, it can be said that customers of different banks have different opinions about the importance of various parameters for selection of a bank or giving preference to a particular bank over other for getting international banking services. LIMITATIONS AND FUTURE SCOPE Current research is based on the primary data and primary data may suffer from personal biasness of respondents. Sample size of the study is 400 which are very small in comparison to the total number of customers of commercial banks. Data has been collected from the two private sector and two public sector banks of India which is very less in comparison to the number of commercial banks in India. Study can be extended to the other banks also such as; foreign and regional rural banks. Comparative study of public, private and foreign banks can be done to measure the preferences of customers using same parameters. MANAGERIAL IMPLICATIONS

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 319

Study is relevant for the bankers while framing strategy to increase the customer data base, to retain existing customers, and attracting new customers. Study revealed the parameters which can be of utmost important for the customers and which makes the customer to select a particular bank for getting international banking services. International banking services involves huge funds and risk as well, thus it is very important for banks to know about the preferences of this category of customers. REFERENCES 1. Akgam Haitham (2016), “Study of customer satisfaction in the banking sector in Libya”, Doctoral

Thesis submiited to University of Utara, Malaysia, pp. 1-80. 2. Anita and Mahavir Singh (2013). “Customer Satisfaction & Retail Banking: A Study of Customer

Satisfaction in Retail Banking”, International Journal of Reviews, Surveys and Research, pp.1-16. 3. Anubhav Anand (2010). “Factors Affecting Customers’ Satisfaction and their Relative Importance in

the Retail Banking Sector: An Empirical Study”, The IUP Journal of Management Research, Vol. 10, No.3, pp.6-23.

4. Kumar Arun, S, Tamilmani, B, Mahalingam, S and Vanjikovan, M (2010). “Influence of Service Quality on Attitudinal Loyalty in Private Retail Banking: An Empirical Study”, the IUP Journal of Management Research, Vol. 9, No.4, pp. 21-38.

5. Chitra, B (2013). “A Study on Consumer Attitude towards Retail Banking with Respect to State Bank of India,” International Research Journal of Business and Management, Vol. II, August, pp.56-61.

6. Daikh Jiana (2015), “A research proposal: the relationship between customer satisfaction and consumer loyalty”, Johnson & Wales University, pp. 1-15.

7. Ganesh, P (2012). “Measuring the Service Quality Gap between the Perceived and Expected Services in Retail Banking”, International Journal of Marketing and Technology, Vol.2, No.1, January, pp.248-260.

8. Jayshree Chavan and Faizan Ahmad (2013). “Factors Affecting on Customer Satisfaction in Retail Banking: An Empirical Study”, International Journal of Business and Management Invention, Vol.2, No.1, January, pp.55-62.

9. Joicey Jose (2013). “A Study on Customer Satisfaction on Hi-Tech Banking Services of ICICI Bank with Special Reference to Kanjirappally Branch”, Research Journal of Commerce, Vol.1, No.1, November, pp.1-9.

10. Khurshid Ahmad Bhat and Singh Maurya (2013). “A Study on Sales of Retail Banking Products and Customer Satisfaction of ICICI Bank Limited”, Scholarly Research Journal for Humanity Science and English Language, Vol.1, No.1, December, pp.86-99.

11. Maduku, D.K (2013). “Predicting Retail Banking Customers’ Attitude towards Internet Banking Services in South Africa”, Southern African Business Review, Vol.17, No.3, pp.76-100.

12. Mistry Snehal (2013), “Measuring customer satisfaction in banking sector: with special reference to banks of Surat city”, Asia Pacific Journal of marketing & Management Review, Vol. 2 (7), pp. 132-140.

13. Mkoma Hussein (2014), “Analysis of customer satisfaction with banking services: A case study of Standard Chartered Bank, Tanzania”, Doctoral Thesis submitted to The Open University of Tanzania, pp. 1-84.

14. Bedi Monica (2010). “An Integrated Framework for Service Quality, Customer Satisfaction and Behavioural Responses in Indian Banking Industry: A Comparison of Public and Private Sector Banks”, Journal of Services Research, Vol.10, No.1, April-September, pp.157-172.

15. Nagabhushanam Manasa (2015), “A study on customer services quality of banks in India”, Research report of Analyz Research Solutions, Bangalore, pp. 1-58.

Journal of Advance Management Research, ISSN: 2393-9664

Vol.06 Issue-03, (March 2018), Impact Factor: 4.73

Double-Blind Peer Reviewed Refereed International Journal - Included in the International Serial Directories

Journal of Advance Management Research, ISSN: 2393-9664 (JAMR)

http://www.jamrpublication.com email id- [email protected] Page 320

16. Chandra Mandal and Bhattacharya Sujoy (2013). “Customer Satisfaction in Indian Retail Banking: A Grounded Theory Approach”, The Qualitative Report, Vol.8, No.56, pp.1-21.

17. Rabb Abdul (2015), “A study on customer’s satisfaction towards banking services of State Bank of India in Kanyakumari District”, International journal of management and commerce innovations, Vol. 2 (2), pp. 429-443.

18. Sharma Ravi Kant (2011). “Service Quality in the Retail Banking Sector: A Study of India vs. China,” World Review of Business Research, Vol.1. No.5. November, pp.78-90.

19. Van Dinh and Lee Pickler (2012). “Examining Service Quality and Customer Satisfaction in the Retail Banking Sector in Vietnam”, Journal of Relationship Marketing, Vol.11, pp.199-214.

20. Vimi Jham and Kaleem Mohd Khan (2008). “Determinants of Performance in Retail Banking: Perspectives of Customer Satisfaction and Relationship Marketing”, Singapore Management Review, Vol.30, No.2, pp.35-44.