Embed Size (px)

Citation preview

JOINT VENTURE OPPORTUNITY

NON-DISCLOSURE AND DISCLAIMER >>This Alliance Realty Group Partners, LLC ("ARGP") summary is for informational purposes only and is not intended as an offer or solicitation. An investment in the

joint venture described in this summary may only be made pursuant to the terms of a separate agreement (“Agreement”). Investments in real estate involve

risks and prospective investors should carefully review the Agreement. All information and disclosures in the Agreement shall supersede information in this

summary and any other information, written or oral, that has been provided with respect to this investment. This material is not intended to address the

particular circumstances or needs of any specific person or entity. Prior to making an investment decision, investors should independently evaluate the relevant risks

involved and ensure that such investment is appropriate and suitable for the investor in light of the investor's investment objectives, experience, time horizon, financial

resources and other relevant circumstances. The material contained in this summary is directed only at qualified persons or entities in any jurisdiction where such access to

information and its use is not contrary to local law or regulation. By accepting this information, you agree to maintain its confidentiality and not reproduce, publish, or

distribute it, in whole or in part, for any purpose. By accepting and reading this summary you agree to be bound by the terms hereof and agree to inform your financial and

legal advisors of the fact that they are bound by the terms hereof. If you do not wish to be bound by the terms of this confidentiality agreement, please destroy this

summary. The numbers, projections and statistical data contained herein are based upon information that have been obtained by sources believed to be reliable and

accurate, but are not necessarily complete, cannot be guaranteed, and no representations or warranty, express or implied, are made by ARGP or any other person as to

their accuracy, completeness or correctness. Errors and omissions are expected. The projections regarding the likelihood of various investment outcomes are not guarantees

of future results. Further, all opinions and estimates contained herein constitute the judgment of ARGP as of the date of this summary and are subject to change without

notice. Prospective investors are not to construe the contents of this summary as legal, investment, tax or other advice. Each prospective investor must rely on his, her or

its own representatives, including his or her own legal counsel and accountants, as to legal, economic, tax and related aspects.

AN INVESTMENT MAY ONLY BE MADE PURSUANT TO THE TERMS OF A JOINT VENTURE AGREEMENT BETWEEN THE PARTIES. THIS CONFIDENTIAL PRESENTATION IS NEITHER AN OFFER NOR A SOLICITATION OF AN OFFER TO INVEST.

TABLE OF CONTENTS >>1 . E X E C U T I V E S U M M A RYCompany Overview Organizational Chart History

11 . I N V E S T M E N T S U M M A RYNational ReachTrack Record SummaryJoint Venture StrategyInvestment Criteria

111 . A R G P S T R AT E G I C A D V A N TA G EWhy ARGP?Business StrategyKeys to Our SuccessInvestment Life CycleInvestor CriteriaDistributions & FeesSample Pipeline Transactions

BRET A BROADDUS

Managing Principal / Broker [email protected]

BRETT R KEENAN

PAUL SAMEK

CFO719.494.7479 [email protected]

323 E Wacker Dr iveSui te 152Chicago, IL 60601312.624.9614

AN INVESTMENT IN ARG LLC MAY ONLY BE MADE PURSUANT TO THE TERMS OF A JOINT VENTURE AGREEMENT BETWEEN THE PARTIES. THIS CONFIDENTIAL PRESENTATION IS NEITHER AN OFFER NOR A SOLICITATION OF AN OFFER TO INVEST.

CONFIDENTIAL 4

S E C T I O N 1 >> E X E C U T I V E S U M M A R Y

5

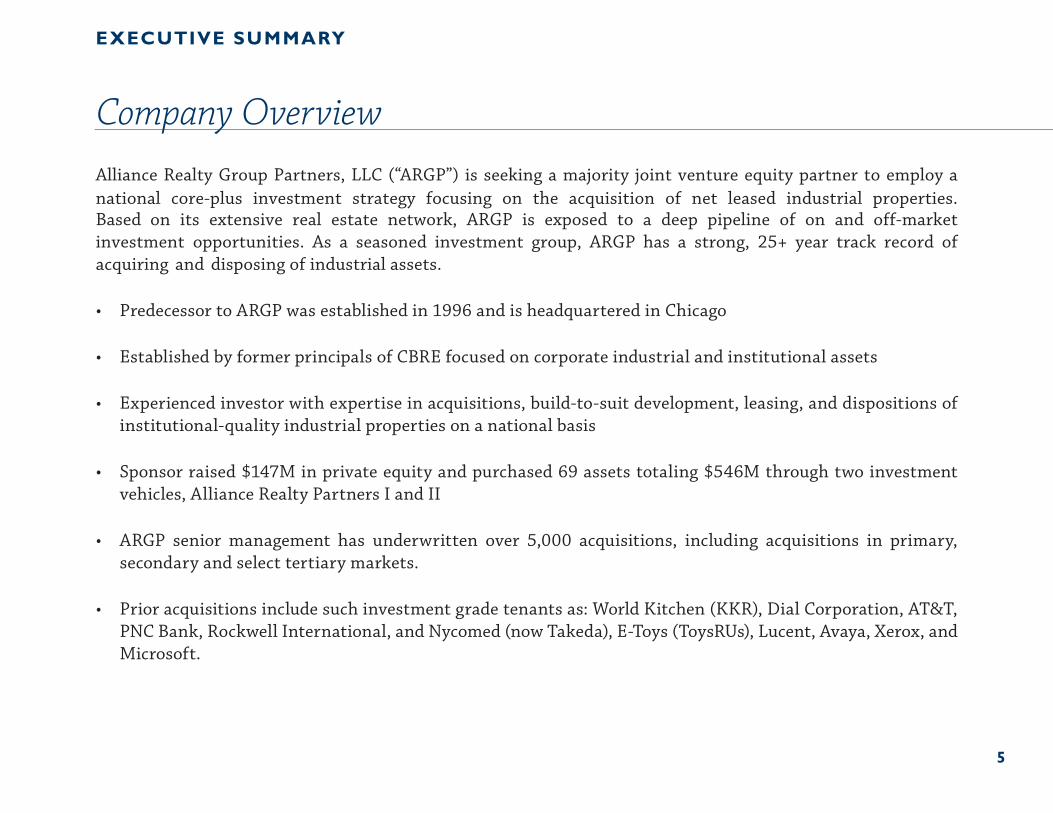

• Predecessor to ARGP was established in 1996 and is headquartered in Chicago

• Established by former principals of CBRE focused on corporate industrial and institutional assets

• Experienced investor with expertise in acquisitions, build-to-suit development, leasing, and dispositions ofinstitutional-quality industrial properties on a national basis

• Sponsor raised $147M in private equity and purchased 69 assets totaling $546M through two investmentvehicles, Alliance Realty Partners I and II

• ARGP senior management has underwritten over 5,000 acquisitions, including acquisitions in primary,secondary and select tertiary markets.

• Prior acquisitions include such investment grade tenants as: World Kitchen (KKR), Dial Corporation, AT&T,PNC Bank, Rockwell International, and Nycomed (now Takeda), E-Toys (ToysRUs), Lucent, Avaya, Xerox, andMicrosoft.

EXECUTIVE SUMMARY

Company OverviewAlliance Realty Group Partners, LLC (“ARGP”) is seeking a majority joint venture equity partner to employ a national core-plus investment strategy focusing on the acquisition of net leased industrial properties. Based on its extensive real estate network, ARGP is exposed to a deep pipeline of on and off-market investment opportunities. As a seasoned investment group, ARGP has a strong, 25+ year track record of acquiring and disposing of industrial assets.

6

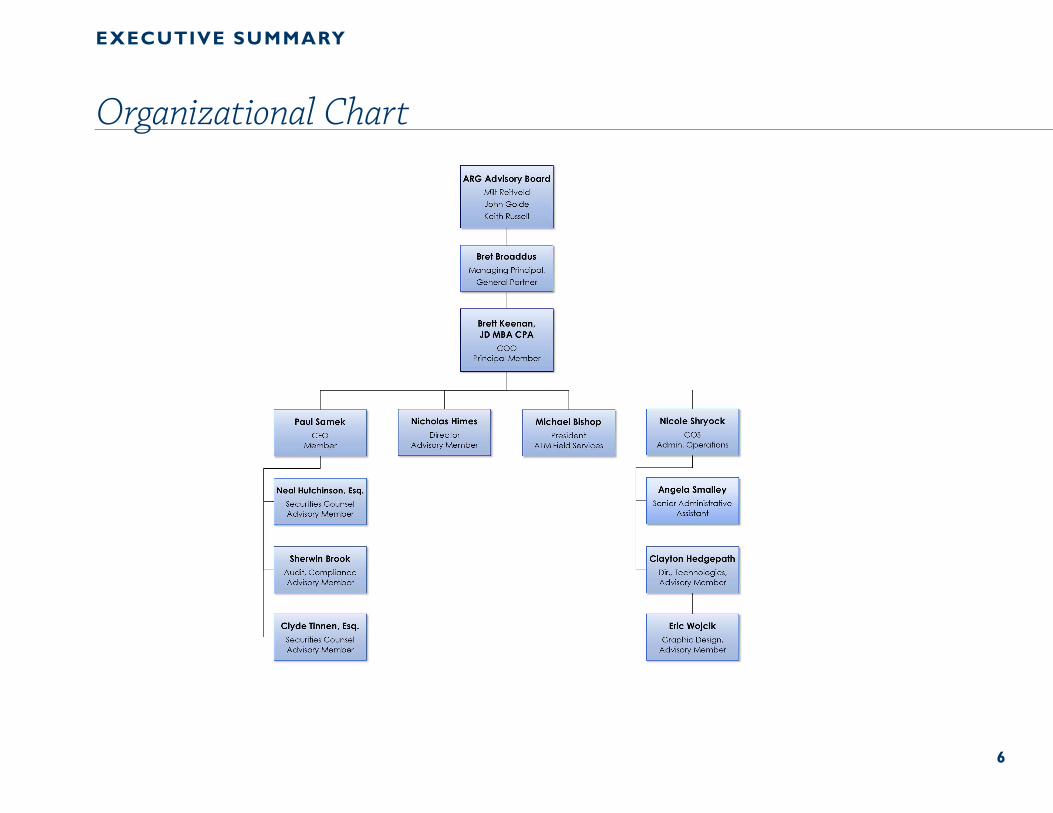

EXECUTIVE SUMMARY

Organizational Chart

7

EXECUTIVE SUMMARY

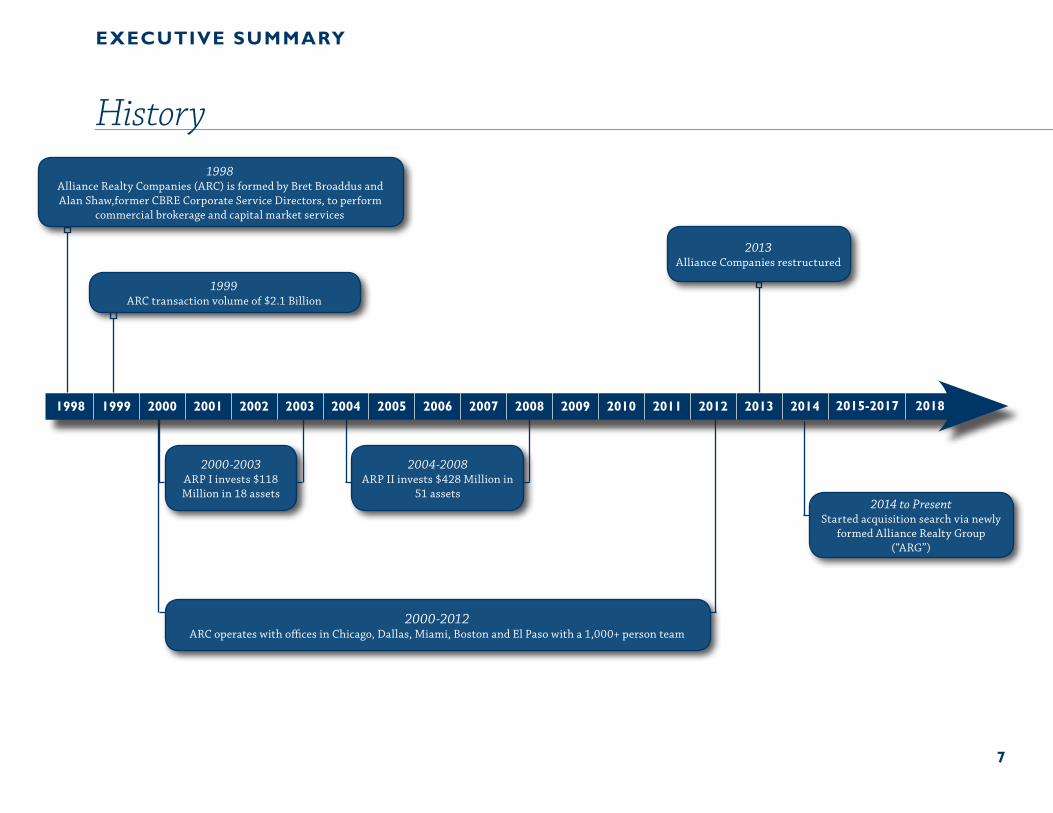

History1998

Alliance Realty Companies (ARC) is formed by Bret Broaddus and Alan Shaw,former CBRE Corporate Service Directors, to perform

commercial brokerage and capital market services

1999ARC transaction volume of $2.1 Billion

2000-2012ARC operates with offices in Chicago, Dallas, Miami, Boston and El Paso with a 1,000+ person team

2013Alliance Companies restructured

2014 to PresentStarted acquisition search via newly

formed Alliance Realty Group (“ARG”)

2000-2003ARP I invests $118 Million in 18 assets

2004-2008ARP II invests $428 Million in

51 assets

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015-2017 2018

AN INVESTMENT IN ARG LLC MAY ONLY BE MADE PURSUANT TO THE TERMS OF A JOINT VENTURE AGREEMENT BETWEEN THE PARTIES. THIS CONFIDENTIAL PRESENTATION IS NEITHER AN OFFER NOR A SOLICITATION OF AN OFFER TO INVEST.

CONFIDENTIAL 8

S E C T I O N 2 >> I N V E S T M E N T S U M M A R Y

9

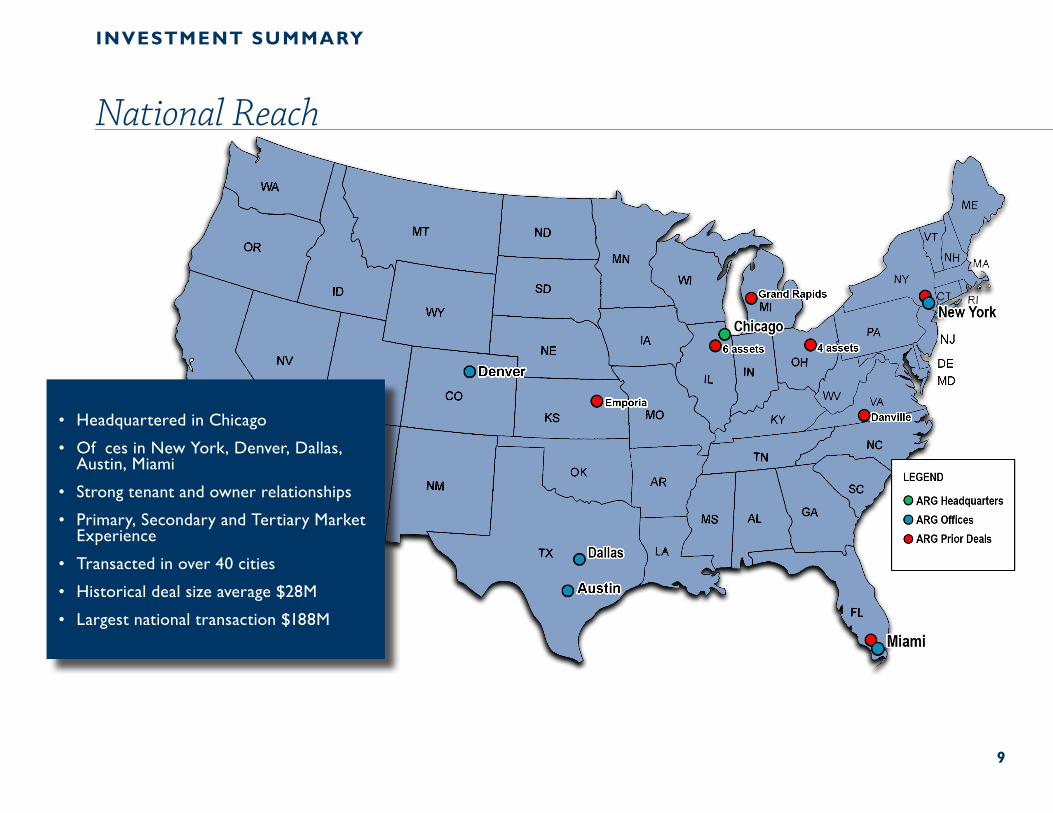

National Reach

INVESTMENT SUMMARY

• Headquartered in Chicago

• Of�ces in New York, Denver, Dallas,Austin, Miami

• Strong tenant and owner relationships

• Primary, Secondary and Tertiary MarketExperience

• Transacted in over 40 cities

• Historical deal size average $28M

• Largest national transaction $188M

INVESTMENT SUMMARY

Tenant Location Property Type Square FootageWickes Lumber National Portfolio Office, Field Operations Portfolo 2,034,000

BTR/Allsteel Montgomery, IL Industrial 1,435,456

American Converting Maspeth, NY Industrial Portfolio 1,095,000

CP&P Cleveland, OH Industrial DC 1,050,000

Eaton Grand Rapids, MI Industrial 786,000

Lexmark Seymour, IN Industrial/Office 763,000

E-Toys Danville, VA Industrial, HQ 740,000

ECH World Kitchen Monee, IL Industrial, Office 700,200

Doral-Sprint Miami, FL Industrial/Office 620,000

AT&T Montgomery, IL Industrial 463,000

Rockwell Mayfield Heights, OH Industrial 460,000

Hopkins Inc. Emporia, KS Industrial Production 320,764

Earle M. Jorgeson Company Schaumburg, IL Industrial 155,000

BRK Industries Aurora, IL Industrial 150,000

Mead Paper Dayton, OH Office Hq 146,000

Bekins Van Lines Hillside, IL Office HQ 130,000

Nycomed Amersham Arlington Heights, IL Industrial R&D 101,501

First Alert Aurora, IL Office HQ 101,000

Titan L3 Glendale Heights, IL Industrial, Office 60,500

Intech, EDM Co. Broadview, IL Industrial HQ 57,350

PNC R&D Office Miamisburg, OH Office 47,812

Acquisition Track Record Examples

CONFIDENTIAL 10

11

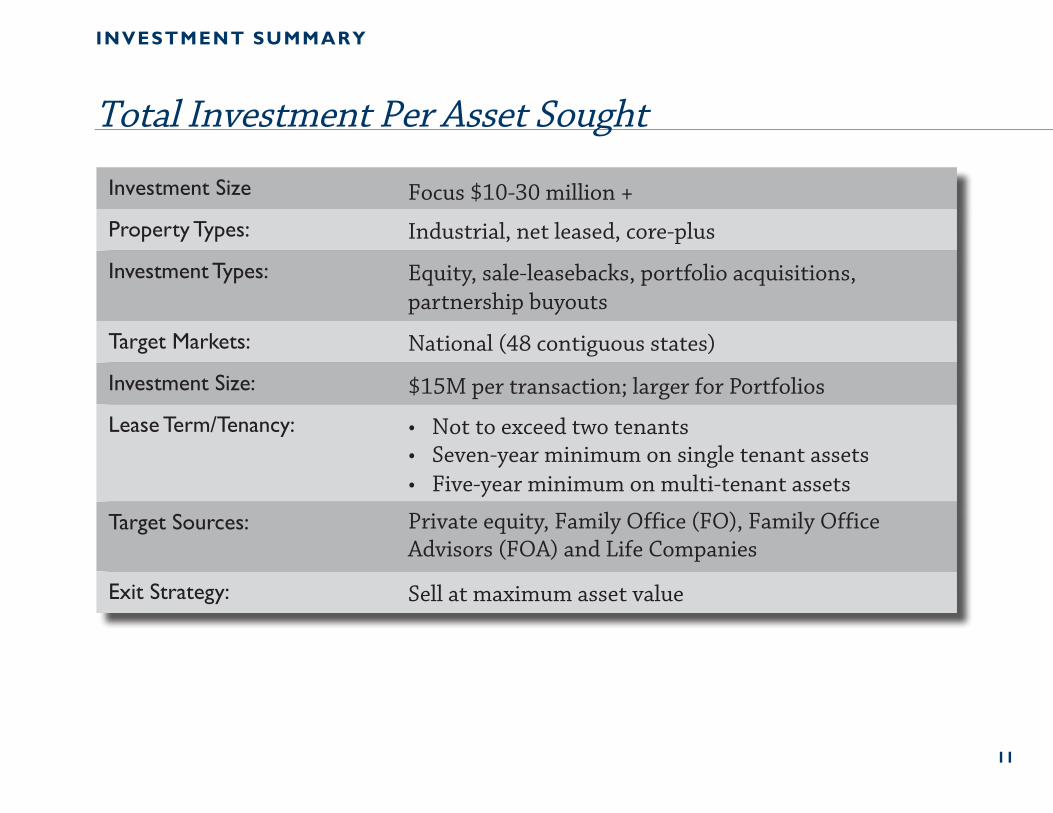

Investment Size Focus $10-30 million +

Property Types: Industrial, net leased, core-plus

Investment Types: Equity, sale-leasebacks, portfolio acquisitions, partnership buyouts

Target Markets: National (48 contiguous states)

Investment Size: $15M per transaction; larger for Portfolios

Lease Term/Tenancy:

Target Sources:

• Not to exceed two tenants• Seven-year minimum on single tenant assets• Five-year minimum on multi-tenant assets

Private equity, Family Office (FO), Family Office Advisors (FOA) and Life Companies

Exit Strategy: Sell at maximum asset value

INVESTMENT SUMMARY

Total Investment Per Asset Sought

12

INVESTMENT SUMMARY

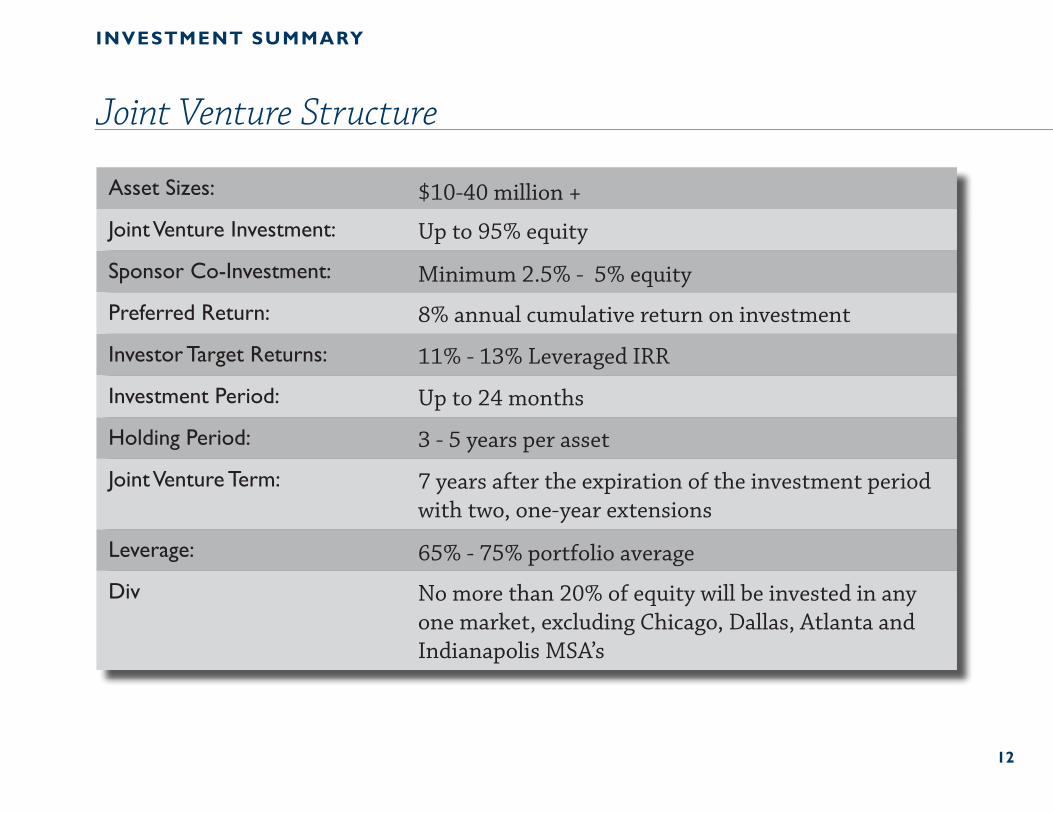

Asset Sizes: $10-40 million +

Joint Venture Investment: Up to 95% equity

Sponsor Co-Investment: Minimum 2.5% - 5% equity

Preferred Return: 8% annual cumulative return on investment

Investor Target Returns: 11% - 13% Leveraged IRR

Investment Period: Up to 24 months

Holding Period: 3 - 5 years per asset

Joint Venture Term: 7 years after the expiration of the investment period with two, one-year extensions

Leverage: 65% - 75% portfolio average

Div������� No more than 20% of equity will be invested in any one market, excluding Chicago, Dallas, Atlanta and Indianapolis MSA’s

Joint Venture Structure

13

WHY US?

• Experienced real estate investor with over $1B + of industrial acquisitions

• Twenty-five year + history underwriting commercial real estate acqusitions

• Unparrelled relationships with principals, brokers and lenders results in asteady pipeline of “off market” deal flow

• National investment experience in primary, secondary and tertiary markets

• No legacy issues from prior investments

• Completed corporate service and investment transactions in over forty markets

• Niche investment focus capitalizes on the Sponsor’s co-investment,transactional and operational strengths

Why ARGP?

14

S E C T I O N 3 >> A R G P S T R AT E G I C A D V A N TA G E

15

ARGP STR ATEGIC ADVANTAGE

MISSIONTo create a portfolio of one and two-tenant net leased (or additional where required) industrial assets of the highest caliber focusing on Class A & B properties priced below replacement cost with credit tenancy.

OPPORTUNITYLeverage our nationwide relationships to source deals that are off-market or marketed on a limited basis. Acquire cash flowing assets with minimal capital expenditure exposure.

BUSINESS MODELSeek value by identifying specific industries, asset class specific or locations that will result in increased value and pricing premium upon disposition.

TARGET RESULTTo consistently continue to reach and exceed our investment return parameters and outperform other comparable investment platforms.

Business Strategy

16

ARGP STR ATEGIC ADVANTAGE

Keys to Our Success

ARGP STR ATEGIC ADVANTAGE

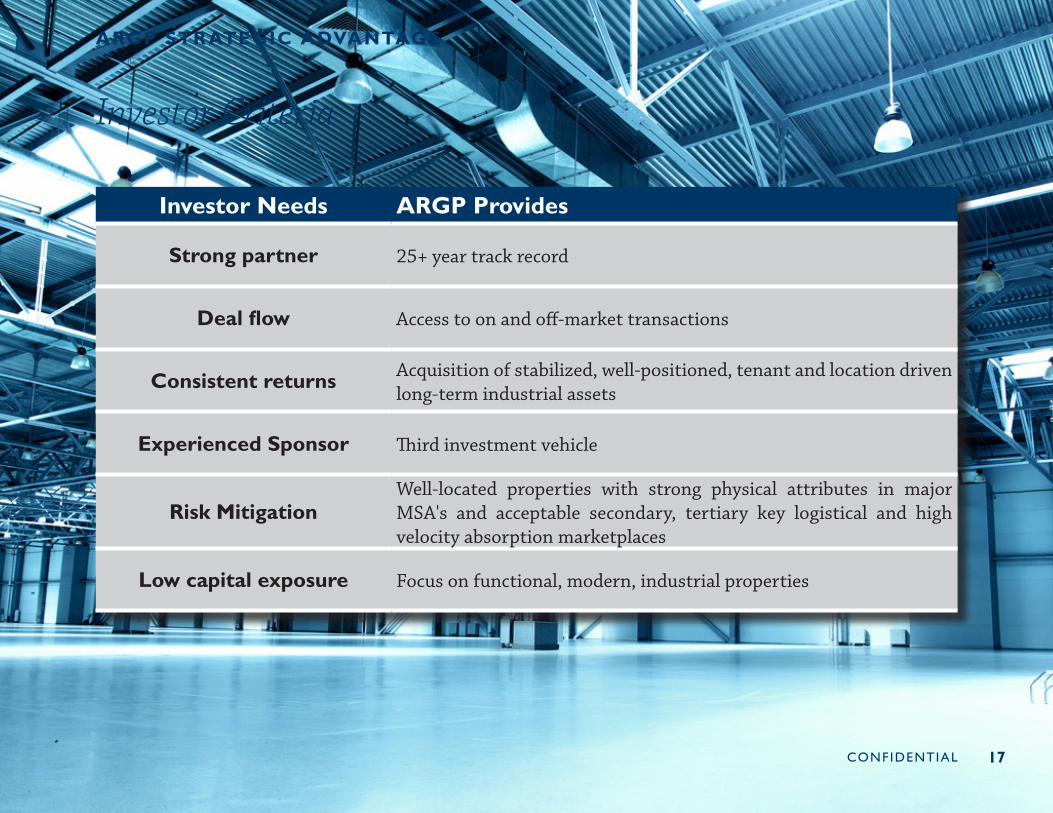

Investor Criteria

Investor Needs ARGP Provides

Strong partner 25+ year track record

Deal flow Access to on and off-market transactions

Consistent returns Acquisition of stabilized, well-positioned, tenant and location driven long-term industrial assets

Experienced Sponsor Third investment vehicle

Risk MitigationWell-located properties with strong physical attributes in major MSA's and acceptable secondary, tertiary key logistical and high velocity absorption marketplaces

Low capital exposure Focus on functional, modern, industrial properties

CONFIDENTIAL 17

CONFIDENTIAL 18

ARGP STR ATEGIC ADVANTAGE

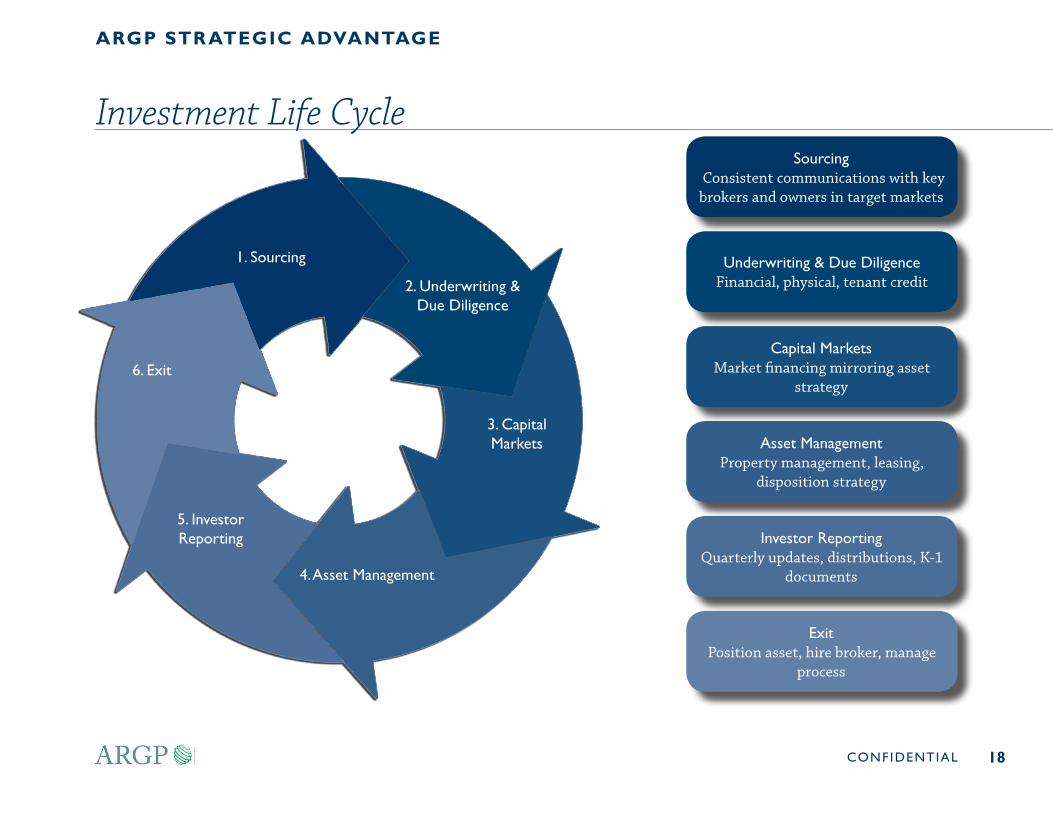

Investment Life Cycle

1. Sourcing

2. Underwriting &Due Diligence

3. CapitalMarkets

4.Asset Management

5. InvestorReporting

6. Exit

Sourcing Consistent communications with key brokers and owners in target markets

Underwriting & Due DiligenceFinancial, physical, tenant credit

Capital MarketsMarket financing mirroring asset

strategy

Asset ManagementProperty management, leasing,

disposition strategy

Investor ReportingQuarterly updates, distributions, K-1

documents

ExitPosition asset, hire broker, manage

process

19

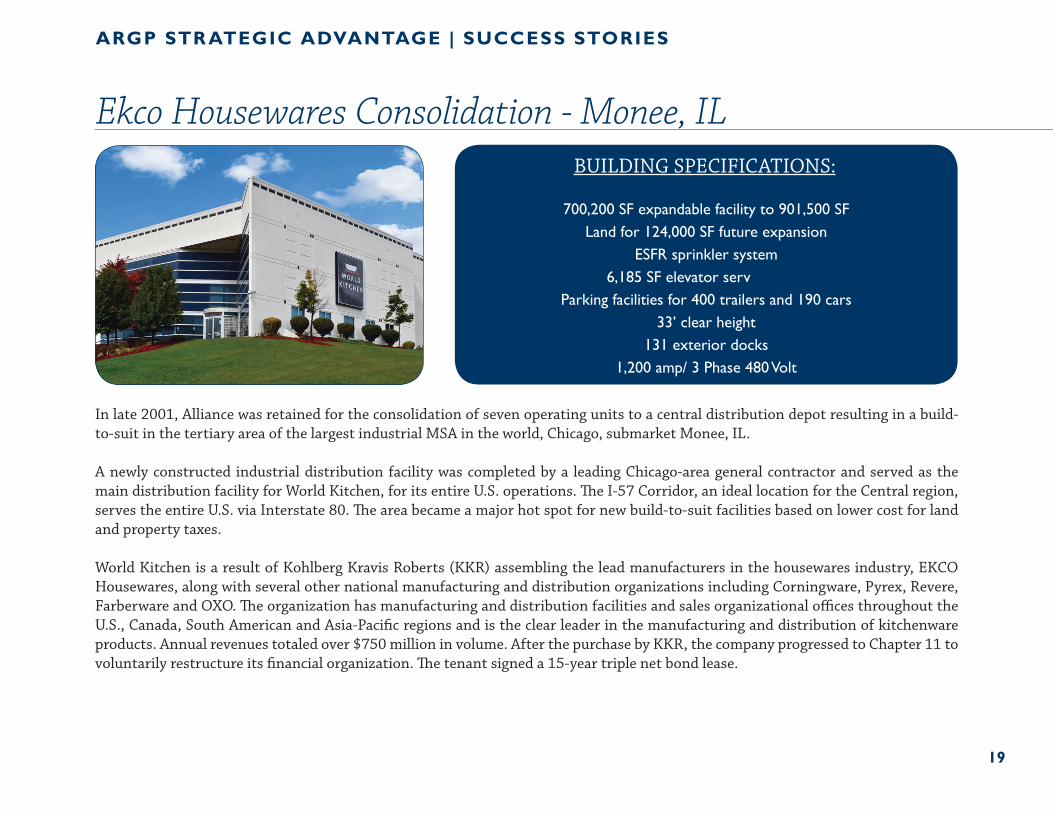

Ekco Housewares Consolidation - Monee, IL

ARGP STR ATEGIC ADVANTAGE | SUCCESS STORIES

In late 2001, Alliance was retained for the consolidation of seven operating units to a central distribution depot resulting in a build-to-suit in the tertiary area of the largest industrial MSA in the world, Chicago, submarket Monee, IL.

A newly constructed industrial distribution facility was completed by a leading Chicago-area general contractor and served as the main distribution facility for World Kitchen, for its entire U.S. operations. The I-57 Corridor, an ideal location for the Central region, serves the entire U.S. via Interstate 80. The area became a major hot spot for new build-to-suit facilities based on lower cost for land and property taxes.

World Kitchen is a result of Kohlberg Kravis Roberts (KKR) assembling the lead manufacturers in the housewares industry, EKCO Housewares, along with several other national manufacturing and distribution organizations including Corningware, Pyrex, Revere, Farberware and OXO. The organization has manufacturing and distribution facilities and sales organizational offices throughout the U.S., Canada, South American and Asia-Pacific regions and is the clear leader in the manufacturing and distribution of kitchenwareproducts. Annual revenues totaled over $750 million in volume. After the purchase by KKR, the company progressed to Chapter 11 tovoluntarily restructure its financial organization. The tenant signed a 15-year triple net bond lease.

BUILDING SPECIFICATIONS:

700,200 SF expandable facility to 901,500 SFLand for 124,000 SF future expansion

ESFR sprinkler system6,185 SF elevator serv�����

Parking facilities for 400 trailers and 190 cars33’ clear height

131 exterior docks1,200 amp/ 3 Phase 480 Volt

20

ARGP STR ATEGIC ADVANTAGE | SUCCESS STORIES

E-Toys Consolidation - Danville, VA

In early 2001, Alliance was retained for the consolidation of several operating units throughout the northeast and the US marketplace for a new distribution and fulfillment center for the E-Toys continuing expansion. After an extensive consolidation study by Alliance Commercial, Danville, Virginia was chosen for the site.

The newly constructed industrial distribution, fulfillment and logistics center was chosen in Danville, Virginia and reduced taxes in the Roanoke Marketplace. It is located just north of the I-85 and I-74 Interchange in High Point, North Carolina.

BUILDING SPECIFICATIONS:

740,000 SF BTS30' clear height

87 exterior docks5 DIDs

Less than an hour to Charlotte161 Acres

21

ARGP STR ATEGIC ADVANTAGE | SUCCESS STORIES

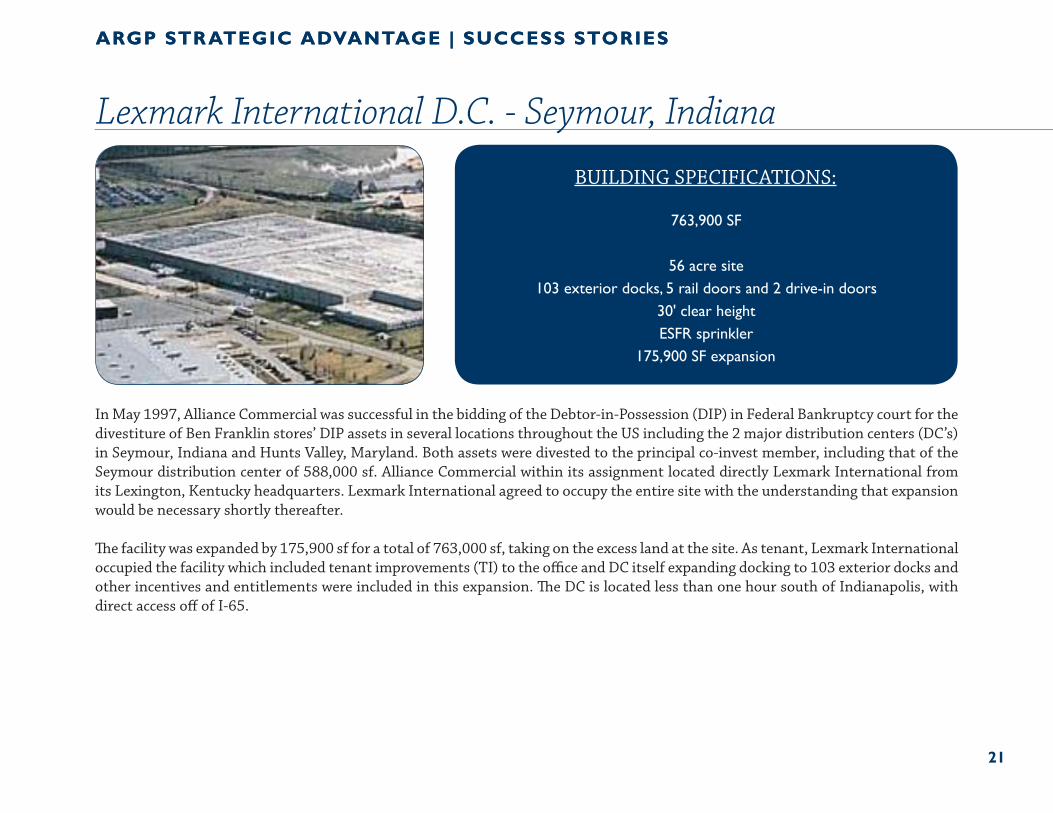

Lexmark International D.C. - Seymour, Indiana

ARGP STR ATEGIC ADVANTAGE | SUCCESS STORIES

In May 1997, Alliance Commercial was successful in the bidding of the Debtor-in-Possession (DIP) in Federal Bankruptcy court for the divestiture of Ben Franklin stores’ DIP assets in several locations throughout the US including the 2 major distribution centers (DC’s) in Seymour, Indiana and Hunts Valley, Maryland. Both assets were divested to the principal co-invest member, including that of the Seymour distribution center of 588,000 sf. Alliance Commercial within its assignment located directly Lexmark International from its Lexington, Kentucky headquarters. Lexmark International agreed to occupy the entire site with the understanding that expansion would be necessary shortly thereafter.

The facility was expanded by 175,900 sf for a total of 763,000 sf, taking on the excess land at the site. As tenant, Lexmark International occupied the facility which included tenant improvements (TI) to the office and DC itself expanding docking to 103 exterior docks and other incentives and entitlements were included in this expansion. The DC is located less than one hour south of Indianapolis, with direct access off of I-65.

BUILDING SPECIFICATIONS:

763,900 SF�������������

56 acre site103 exterior docks, 5 rail doors and 2 drive-in doors

30' clear heightESFR sprinkler

175,900 SF expansion

22

ARGP STR ATEGIC ADVANTAGE

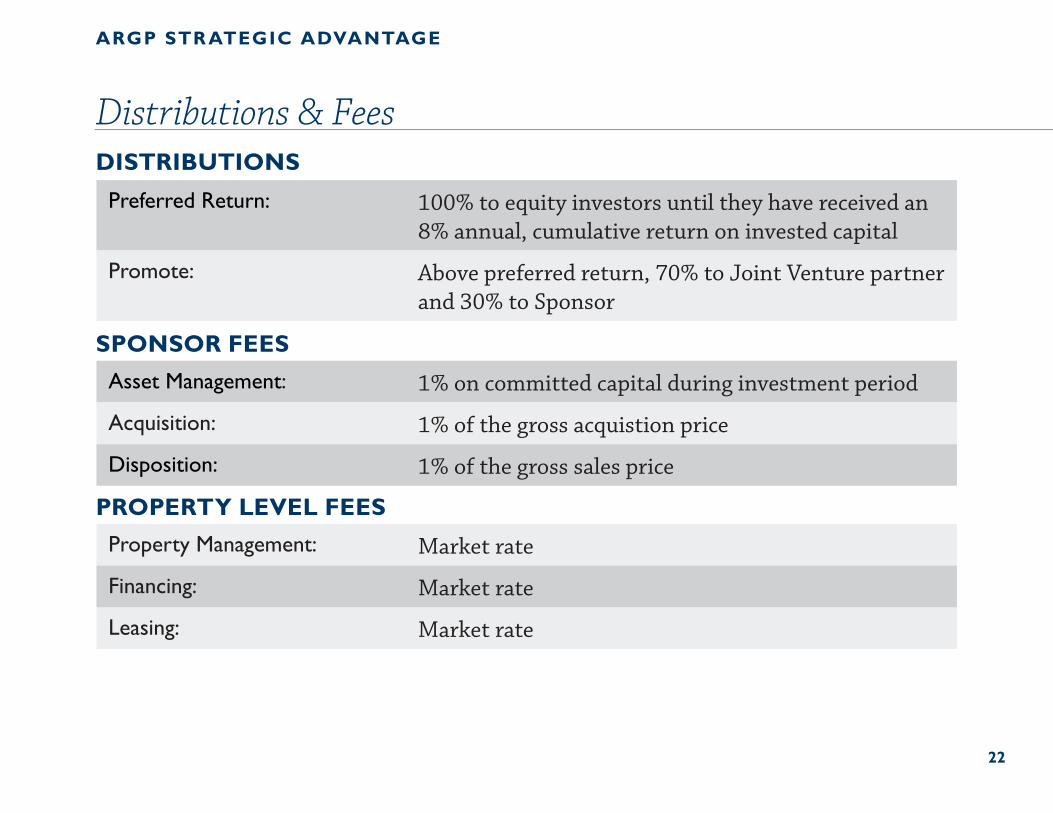

Distributions & Fees

Preferred Return: 100% to equity investors until they have received an 8% annual, cumulative return on invested capital

Promote: Above preferred return, 70% to Joint Venture partner and 30% to Sponsor

DISTRIBUTIONS

Asset Management: 1% on committed capital during investment period

Acquisition: 1% of the gross acquistion price

Disposition: 1% of the gross sales price

SPONSOR FEES

Property Management: Market rate

Financing: Market rate

Leasing: Market rate

PROPERTY LEVEL FEES

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #1

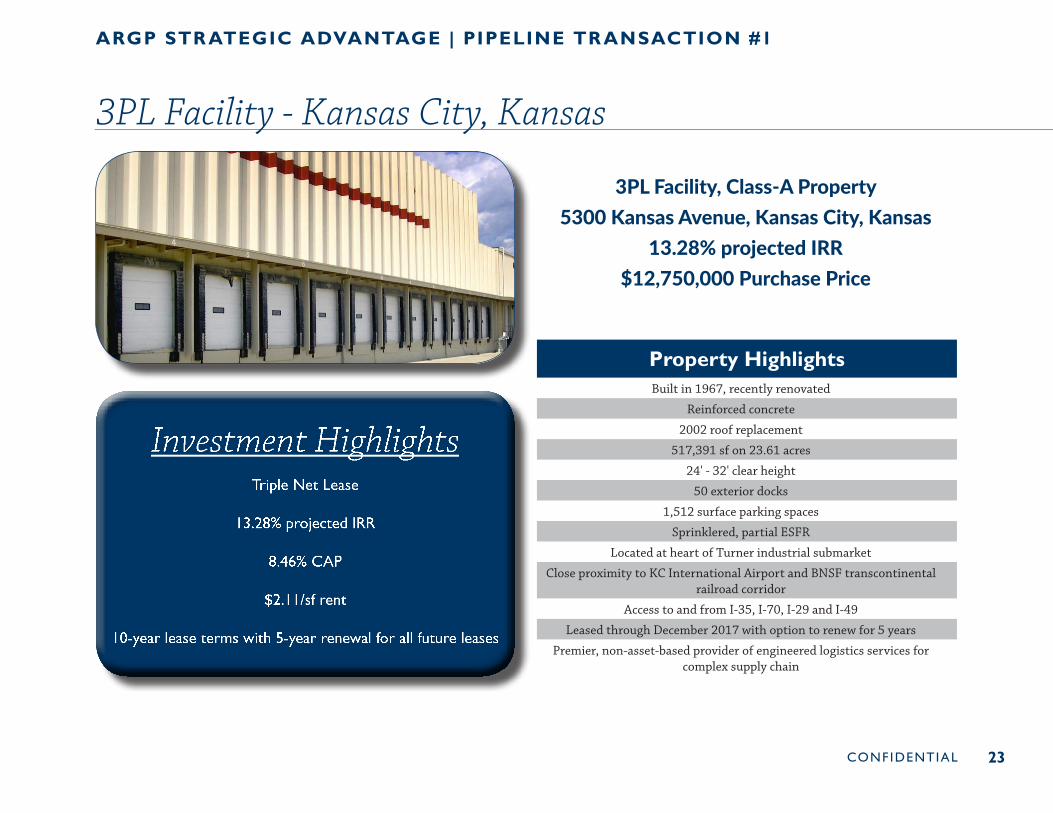

3PL Facility - Kansas City, Kansas

CONFIDENTIAL 23

Investment HighlightsTriple Net Lease

13.28% projected IRR

8.46% CAP

$2.11/sf rent

10-year lease terms with 5-year renewal for all future leases

Property HighlightsBuilt in 1967, recently renovated

Reinforced concrete

2002 roof replacement

517,391 sf on 23.61 acres

24' - 32' clear height

50 exterior docks

1,512 surface parking spaces

Sprinklered, partial ESFR

Located at heart of Turner industrial submarket

Close proximity to KC International Airport and BNSF transcontinental railroad corridor

Access to and from I-35, I-70, I-29 and I-49

Leased through December 2017 with option to renew for 5 years

Premier, non-asset-based provider of engineered logistics services for complex supply chain

3PL Facility, Class-A Property5300 Kansas Avenue, Kansas City, Kansas

13.28% projected IRR $12,750,000 Purchase Price

24

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #1

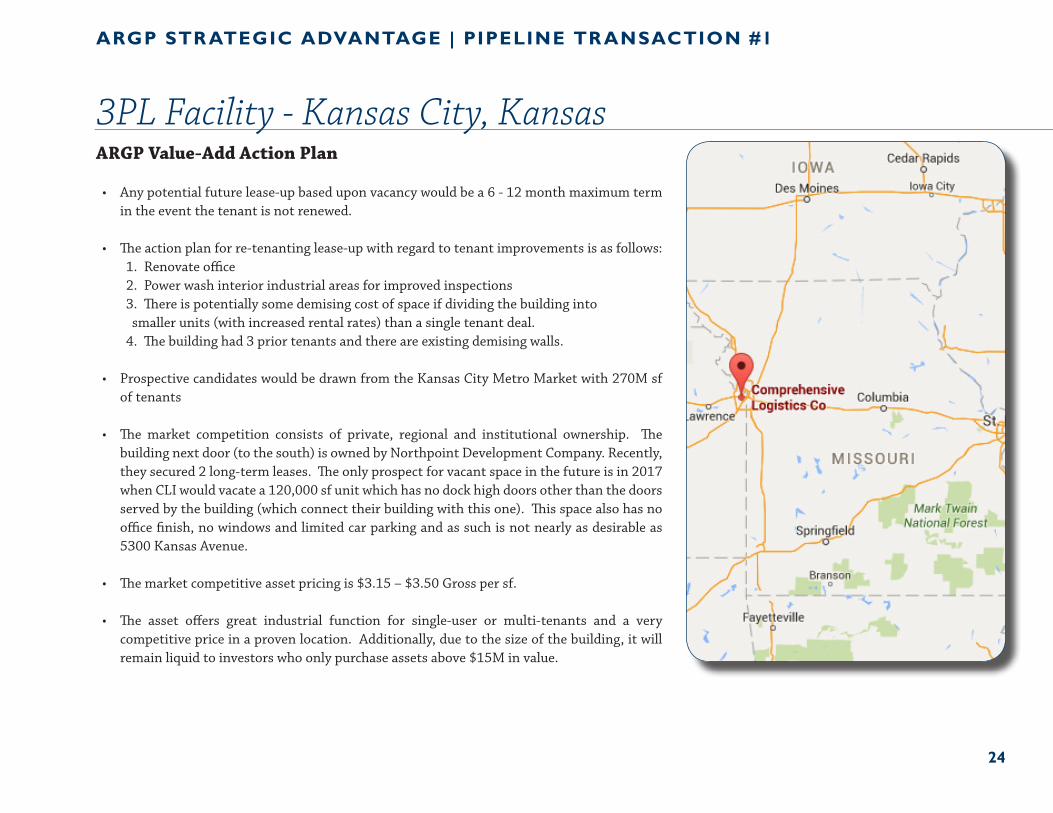

3PL Facility - Kansas City, KansasARGP Value-Add Action Plan

• Any potential future lease-up based upon vacancy would be a 6 - 12 month maximum termin the event the tenant is not renewed.

• The action plan for re-tenanting lease-up with regard to tenant improvements is as follows:1. Renovate office2. Power wash interior industrial areas for improved inspections3. There is potentially some demising cost of space if dividing the building intosmaller units (with increased rental rates) than a single tenant deal.

4. The building had 3 prior tenants and there are existing demising walls.

• Prospective candidates would be drawn from the Kansas City Metro Market with 270M sfof tenants

• The market competition consists of private, regional and institutional ownership. Thebuilding next door (to the south) is owned by Northpoint Development Company. Recently,they secured 2 long-term leases. The only prospect for vacant space in the future is in 2017when CLI would vacate a 120,000 sf unit which has no dock high doors other than the doorsserved by the building (which connect their building with this one). This space also has nooffice finish, no windows and limited car parking and as such is not nearly as desirable as5300 Kansas Avenue.

• The market competitive asset pricing is $3.15 – $3.50 Gross per sf.

• The asset offers great industrial function for single-user or multi-tenants and a verycompetitive price in a proven location. Additionally, due to the size of the building, it willremain liquid to investors who only purchase assets above $15M in value.

25

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #1

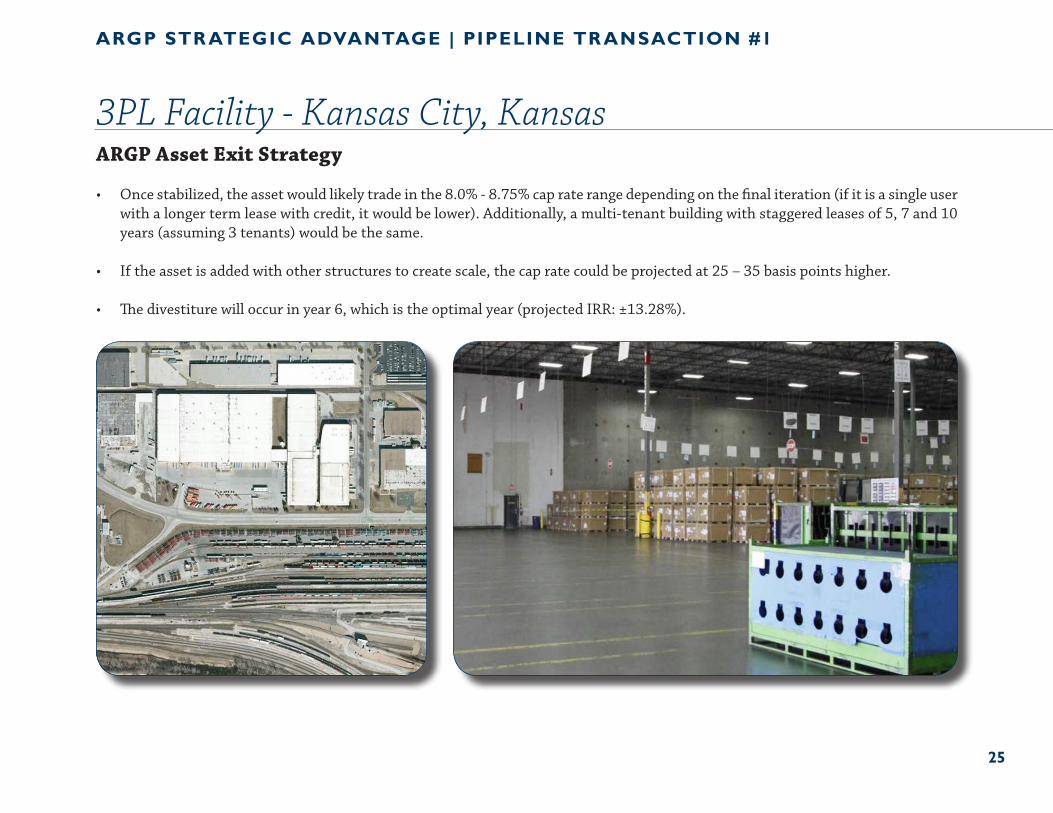

3PL Facility - Kansas City, KansasARGP Asset Exit Strategy

• Once stabilized, the asset would likely trade in the 8.0% - 8.75% cap rate range depending on the final iteration (if it is a single userwith a longer term lease with credit, it would be lower). Additionally, a multi-tenant building with staggered leases of 5, 7 and 10years (assuming 3 tenants) would be the same.

• If the asset is added with other structures to create scale, the cap rate could be projected at 25 – 35 basis points higher.

• The divestiture will occur in year 6, which is the optimal year (projected IRR: ±13.28%).

26

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #1

3PL Facility - Kansas City, Kansas

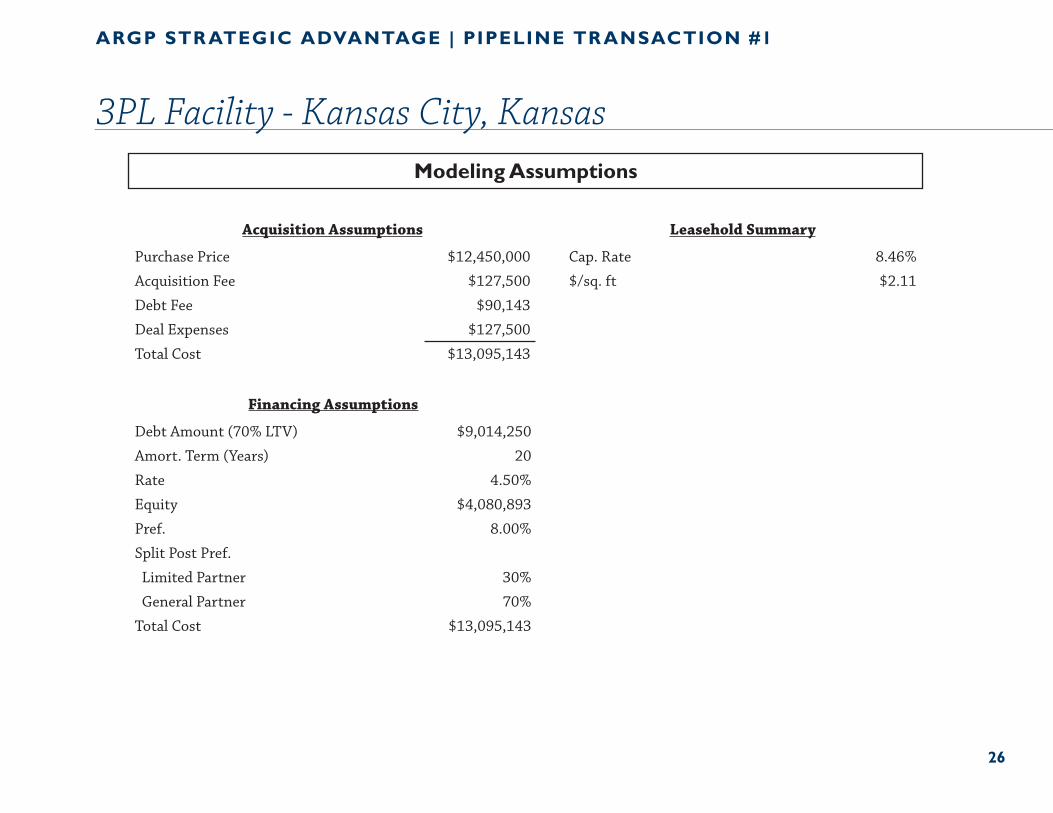

Acquisition Assumptions Leasehold Summary

Purchase Price $12,450,000 Cap. Rate 8.46%

Acquisition Fee $127,500 $/sq. ft $2.11

Debt Fee $90,143

Deal Expenses $127,500

Total Cost $13,095,143

Financing Assumptions

Debt Amount (70% LTV) $9,014,250

Amort. Term (Years) 20

Rate 4.50%

Equity $4,080,893

Pref. 8.00%

Split Post Pref.

Limited Partner 30%

General Partner 70%

Total Cost $13,095,143

Modeling Assumptions

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #2

CONFIDENTIAL 27

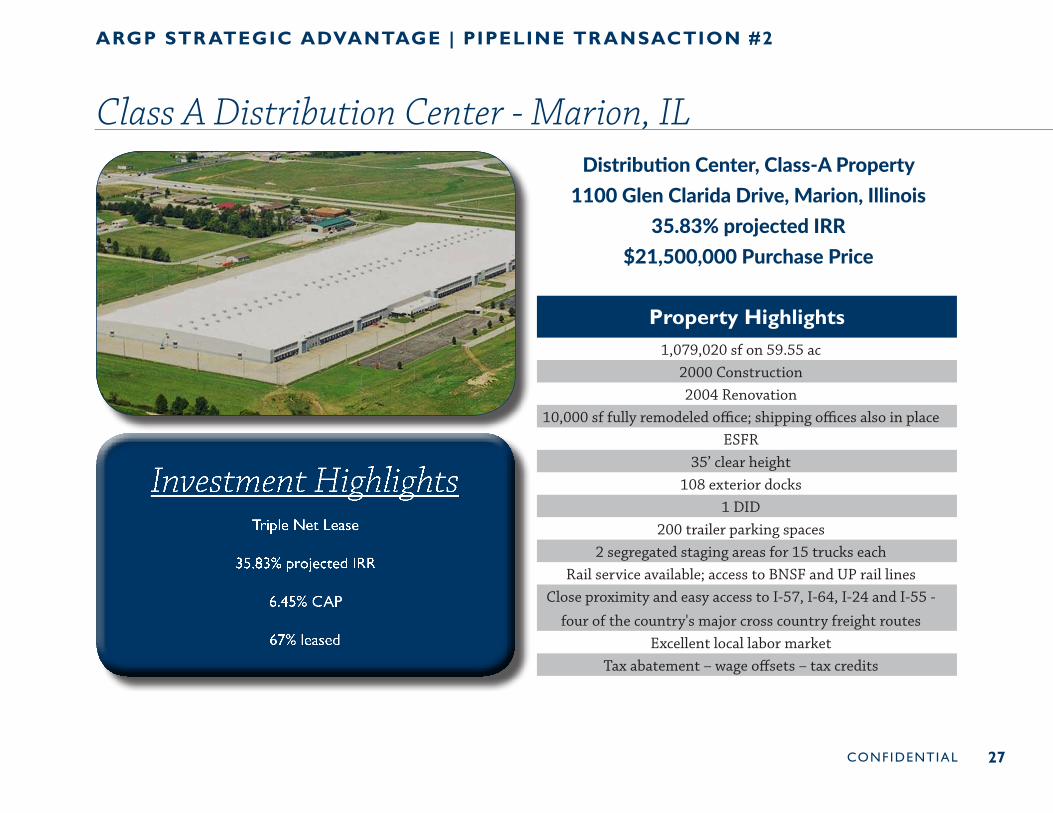

Class A Distribution Center - Marion, IL

Investment HighlightsTriple Net Lease

35.83% projected IRR

6.45% CAP

67% leased

Property Highlights1,079,020 sf on 59.55 ac

2000 Construction2004 Renovation

10,000 sf fully remodeled office; shipping offices also in placeESFR

35’ clear height108 exterior docks

1 DID200 trailer parking spaces

2 segregated staging areas for 15 trucks eachRail service available; access to BNSF and UP rail lines

Close proximity and easy access to I-57, I-64, I-24 and I-55 -

four of the country's major cross country freight routesExcellent local labor market

Tax abatement – wage offsets – tax credits

Distribution Center, Class-A Property1100 Glen Clarida Drive, Marion, Illinois

35.83% projected IRR$21,500,000 Purchase Price

28

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #2

CONFIDENTIAL

Class A Distribution Center - Marion, ILARGP Value-Add Action Plan

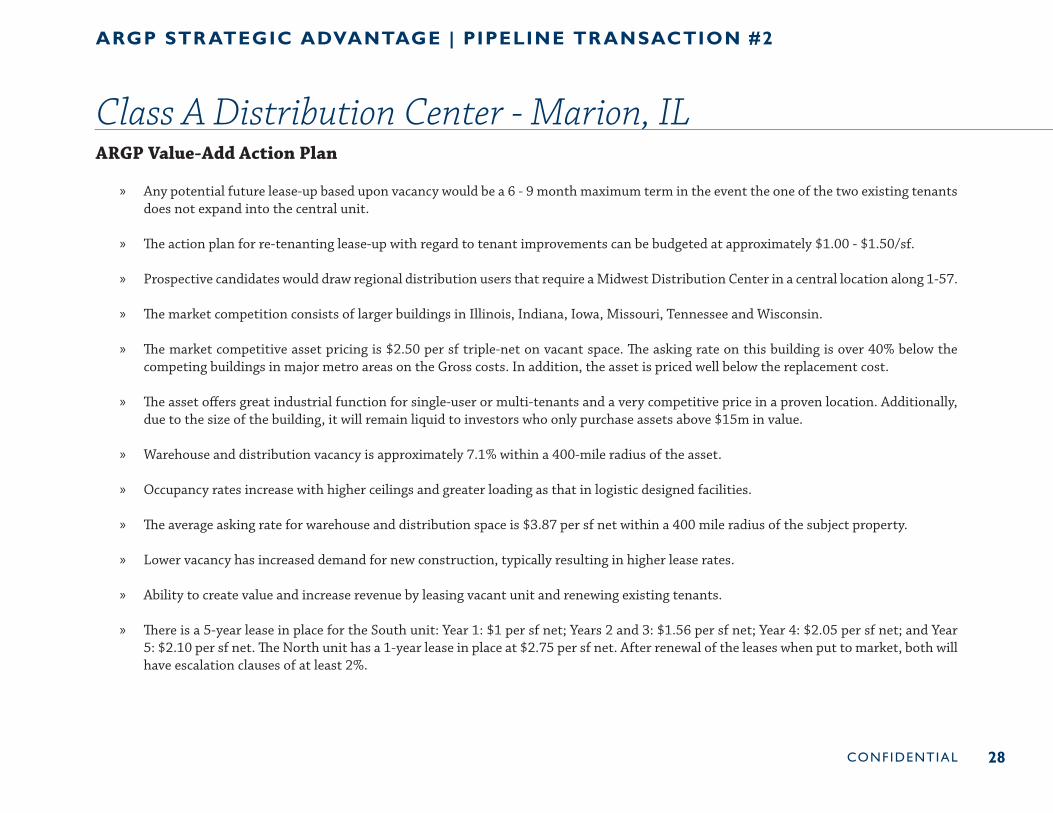

» Any potential future lease-up based upon vacancy would be a 6 - 9 month maximum term in the event the one of the two existing tenantsdoes not expand into the central unit.

» The action plan for re-tenanting lease-up with regard to tenant improvements can be budgeted at approximately $1.00 - $1.50/sf.

» Prospective candidates would draw regional distribution users that require a Midwest Distribution Center in a central location along 1-57.

» The market competition consists of larger buildings in Illinois, Indiana, Iowa, Missouri, Tennessee and Wisconsin.

» The market competitive asset pricing is $2.50 per sf triple-net on vacant space. The asking rate on this building is over 40% below thecompeting buildings in major metro areas on the Gross costs. In addition, the asset is priced well below the replacement cost.

» The asset offers great industrial function for single-user or multi-tenants and a very competitive price in a proven location. Additionally,due to the size of the building, it will remain liquid to investors who only purchase assets above $15m in value.

» Warehouse and distribution vacancy is approximately 7.1% within a 400-mile radius of the asset.

» Occupancy rates increase with higher ceilings and greater loading as that in logistic designed facilities.

» The average asking rate for warehouse and distribution space is $3.87 per sf net within a 400 mile radius of the subject property.

» Lower vacancy has increased demand for new construction, typically resulting in higher lease rates.

» Ability to create value and increase revenue by leasing vacant unit and renewing existing tenants.

» There is a 5-year lease in place for the South unit: Year 1: $1 per sf net; Years 2 and 3: $1.56 per sf net; Year 4: $2.05 per sf net; and Year5: $2.10 per sf net. The North unit has a 1-year lease in place at $2.75 per sf net. After renewal of the leases when put to market, both willhave escalation clauses of at least 2%.

29

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #2

Class A Distribution Center - Marion, IL

Procter & Gamble Co.

Newell Rubbermaid

Continental Tire

Kellogg’s

Napa Auto Parts

Walgreens Distribution Center

Gilster-Mary Lee Corp.

Berry Plastics Corp.

Tyson Foods Inc.

T J Maxx

Sears Logistics

Anheuser Busch-Inbev

Unilever

Hershey Foods

Ozburn Hessey

Spectrum Brands

Dial Corp.

World Wide Technology

Walgreens

Save-A-Lot

Yazaki

Jacobson Companies

Whirlpool

Trane, Inc.

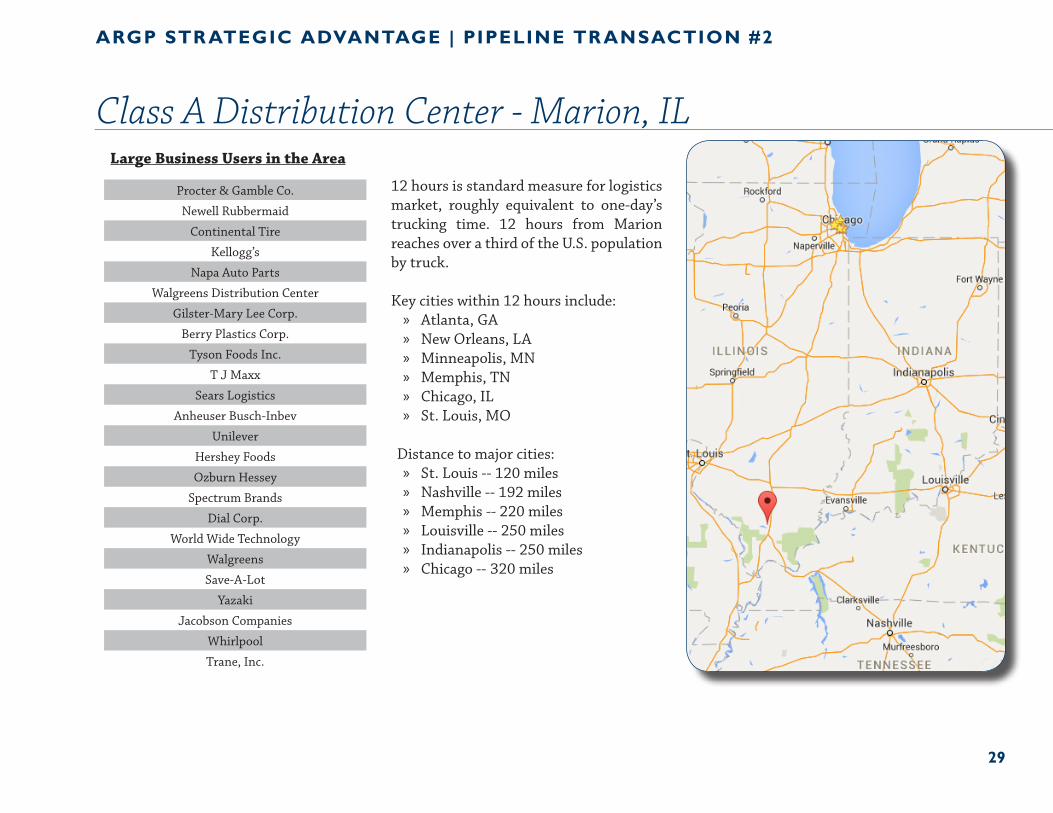

Large Business Users in the Area

12 hours is standard measure for logistics market, roughly equivalent to one-day’s trucking time. 12 hours from Marion reaches over a third of the U.S. population by truck.

Key cities within 12 hours include:» Atlanta, GA» New Orleans, LA» Minneapolis, MN» Memphis, TN» Chicago, IL» St. Louis, MO

Distance to major cities:» St. Louis -- 120 miles» Nashville -- 192 miles» Memphis -- 220 miles» Louisville -- 250 miles» Indianapolis -- 250 miles» Chicago -- 320 miles

30

ARGP Asset Exit Strategy

• Most value-add sales have been to U.S. companies while long-term, single tenant triple-net-leased (3NL) transactions have beenpurchased primarily by public and private REITs and international buyers (United Arab Emirates, Canada, China, Singapore,Norway, Australia and Germany).

• Large Logistical, Distribution Centers are attractive to many asset acquiring group sectors including PNTRs, public REITs, SWFs,endowments, CRE Equity Funds Family Office and FO Advisory operators allowing for the placement of additional size for theunderwriting required. Particularly attractive are institutional grade assets with ESFR, divisibility, non-functionally restrictedclear cube ceiling heights, dock-per square foot favorable in addition to the favorable entitlements and lower operating costs oflabor and goods. ARGP underwriting recognizes the favorable cost basis which will allow for certain value-add either from an EUand investor standpoint as end-users will find very little to no competing assets allowing for the low-cost-provider features fromthe specification, occupancy and operating standpoints offered herein.

• The divestiture will occur in year 6, which is the optimal year (projected IRR: ±35.83%).

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #2

Class A Distribution Center - Marion, IL

31

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #2

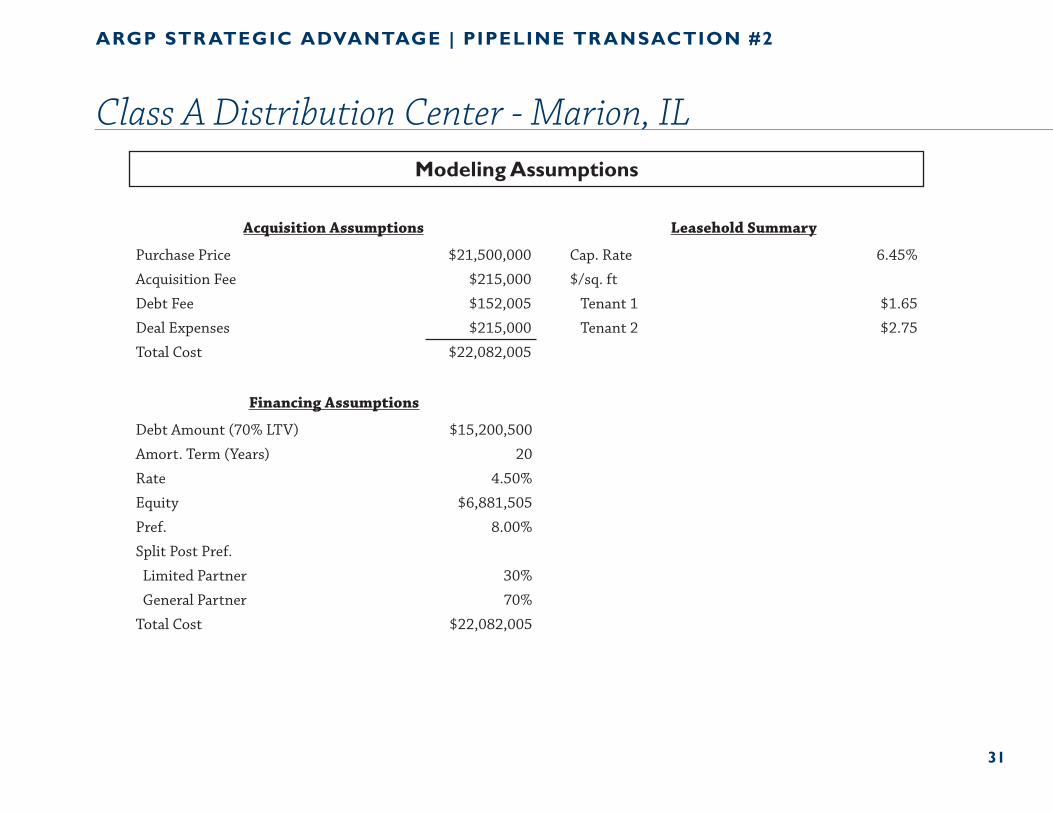

Class A Distribution Center - Marion, IL

Acquisition Assumptions Leasehold Summary

Purchase Price $21,500,000 Cap. Rate 6.45%

Acquisition Fee $215,000 $/sq. ft

Debt Fee $152,005 Tenant 1 $1.65

Deal Expenses $215,000 Tenant 2 $2.75

Total Cost $22,082,005

Financing Assumptions

Debt Amount (70% LTV) $15,200,500

Amort. Term (Years) 20

Rate 4.50%

Equity $6,881,505

Pref. 8.00%

Split Post Pref.

Limited Partner 30%

General Partner 70%

Total Cost $22,082,005

Modeling Assumptions

32

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #3

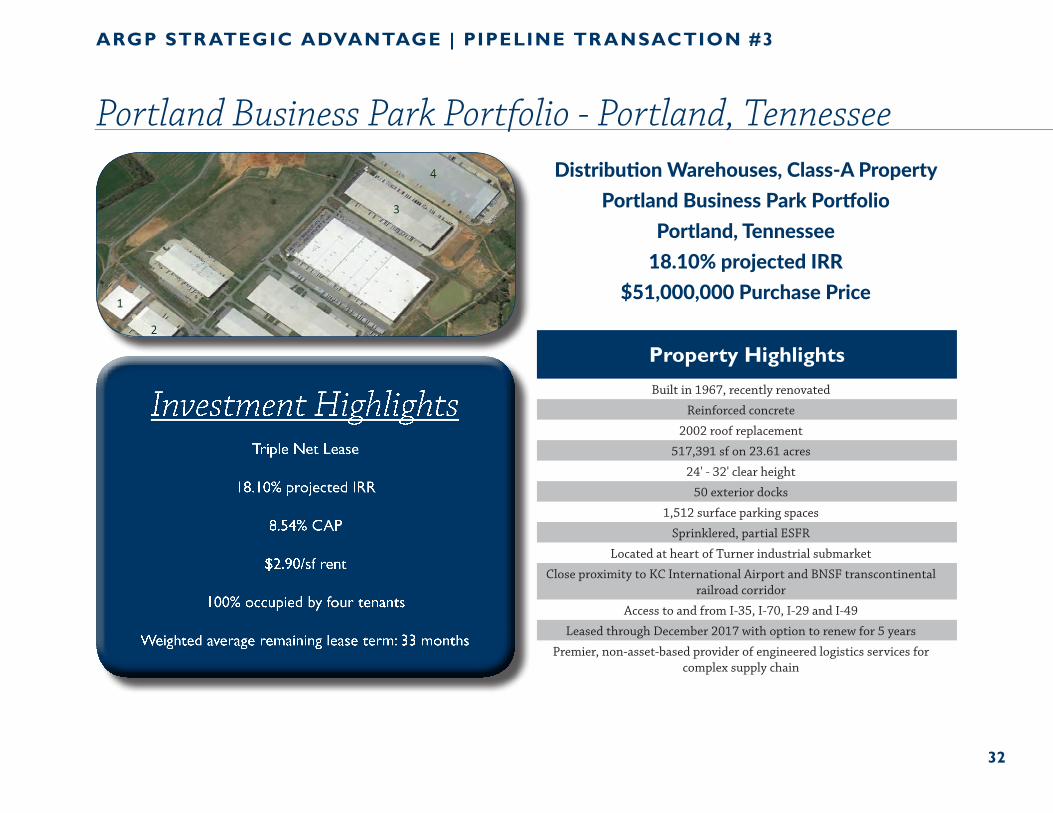

Portland Business Park Portfolio - Portland, Tennessee

Investment HighlightsTriple Net Lease

18.10% projected IRR

8.54% CAP

$2.90/sf rent

100% occupied by four tenants

Weighted average remaining lease term: 33 months

Property HighlightsBuilt in 1967, recently renovated

Reinforced concrete

2002 roof replacement

517,391 sf on 23.61 acres

24' - 32' clear height

50 exterior docks

1,512 surface parking spaces

Sprinklered, partial ESFR

Located at heart of Turner industrial submarket

Close proximity to KC International Airport and BNSF transcontinental railroad corridor

Access to and from I-35, I-70, I-29 and I-49

Leased through December 2017 with option to renew for 5 years

Premier, non-asset-based provider of engineered logistics services for complex supply chain

Distribution Warehouses, Class-A PropertyPortland Business Park Portfolio

Portland, Tennessee18.10% projected IRR

$51,000,000 Purchase Price

33

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #3

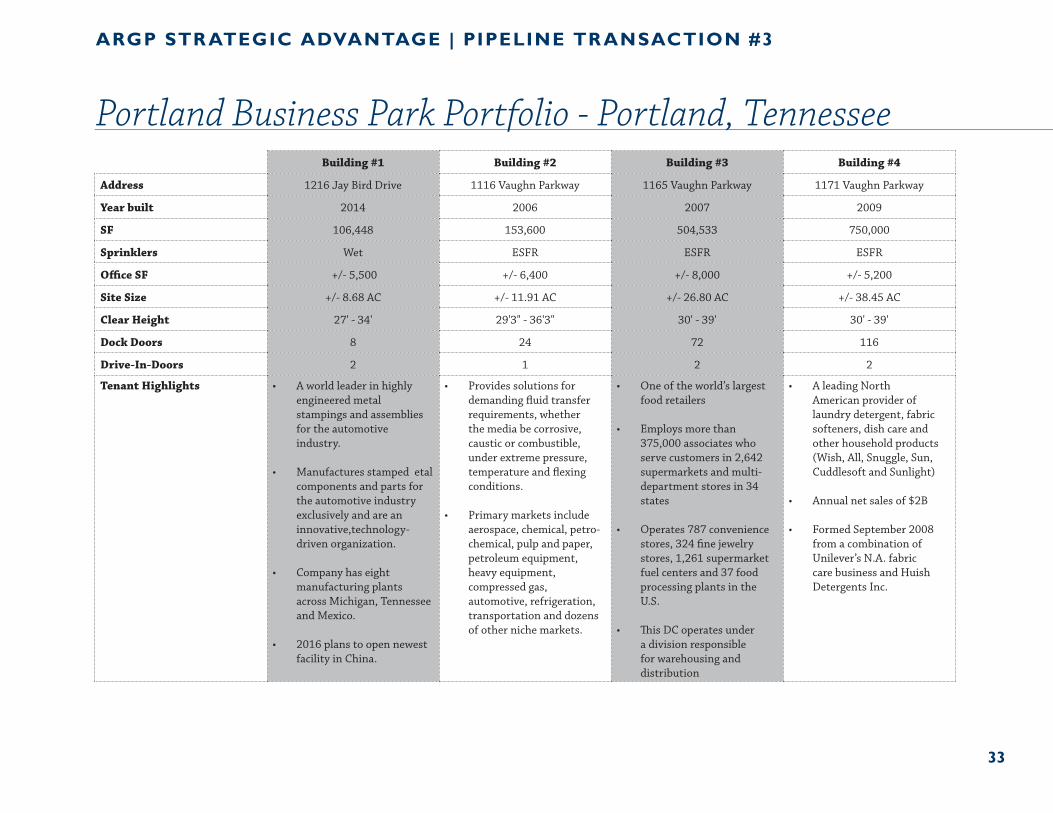

Portland Business Park Portfolio - Portland, TennesseeBuilding #1 Building #2 Building #3 Building #4

Address 1216 Jay Bird Drive 1116 Vaughn Parkway 1165 Vaughn Parkway 1171 Vaughn Parkway

Year built 2014 2006 2007 2009

SF 106,448 153,600 504,533 750,000

Sprinklers Wet ESFR ESFR ESFR

Office SF +/- 5,500 +/- 6,400 +/- 8,000 +/- 5,200

Site Size +/- 8.68 AC +/- 11.91 AC +/- 26.80 AC +/- 38.45 AC

Clear Height 27' - 34' 29'3" - 36'3" 30' - 39' 30' - 39'

Dock Doors 8 24 72 116

Drive-In-Doors 2 1 2 2

Tenant Highlights • A world leader in highly engineered metal stampings and assemblies for the automotive industry.

• Manufactures stamped etal components and parts for the automotive industry exclusively and are an innovative,technology-driven organization.

• Company has eight manufacturing plants across Michigan, Tennessee and Mexico.

• 2016 plans to open newest facility in China.

• Provides solutions for demanding fluid transfer requirements, whether the media be corrosive, caustic or combustible, under extreme pressure, temperature and flexing conditions.

• Primary markets include aerospace, chemical, petro-chemical, pulp and paper, petroleum equipment, heavy equipment, compressed gas, automotive, refrigeration, transportation and dozens of other niche markets.

• One of the world’s largest food retailers

• Employs more than 375,000 associates who serve customers in 2,642 supermarkets and multi-department stores in 34 states

• Operates 787 convenience stores, 324 fine jewelry stores, 1,261 supermarket fuel centers and 37 food processing plants in the U.S.

• This DC operates under a division responsible for warehousing and distribution

• A leading North American provider of laundry detergent, fabric softeners, dish care and other household products (Wish, All, Snuggle, Sun, Cuddlesoft and Sunlight)

• Annual net sales of $2B

• Formed September 2008 from a combination of Unilever’s N.A. fabric care business and Huish Detergents Inc.

34

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #3

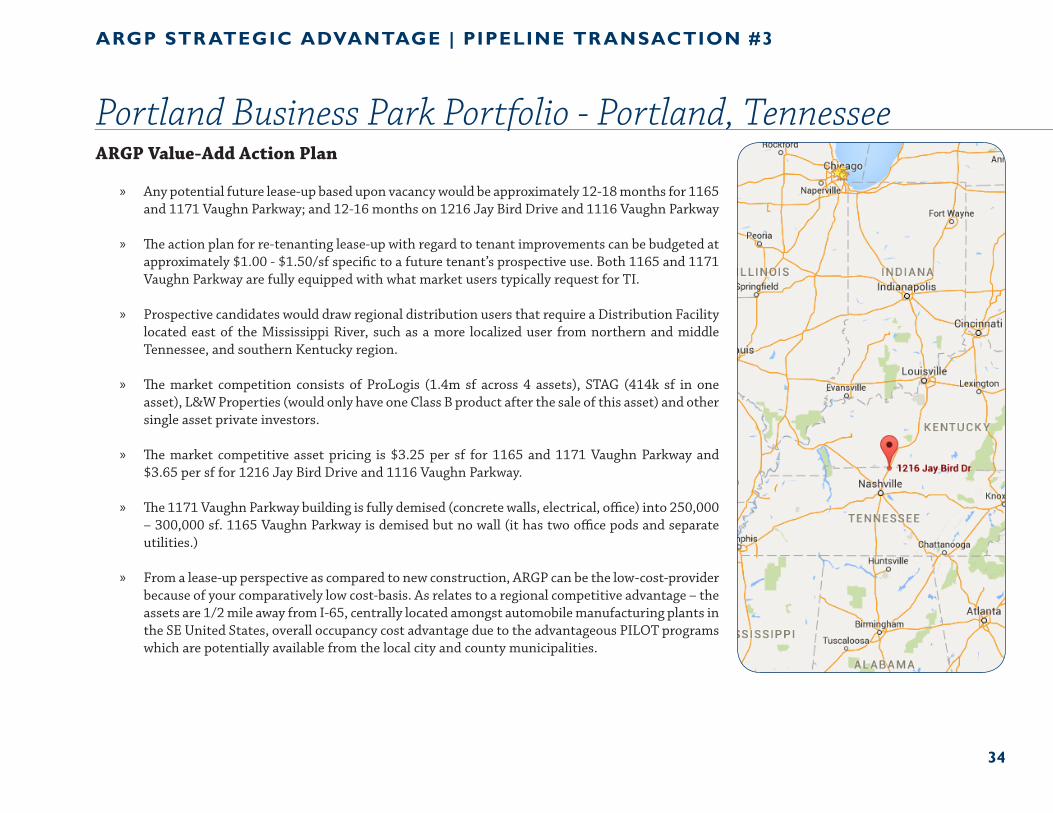

Portland Business Park Portfolio - Portland, TennesseeARGP Value-Add Action Plan

» Any potential future lease-up based upon vacancy would be approximately 12-18 months for 1165 and 1171 Vaughn Parkway; and 12-16 months on 1216 Jay Bird Drive and 1116 Vaughn Parkway

» The action plan for re-tenanting lease-up with regard to tenant improvements can be budgeted atapproximately $1.00 - $1.50/sf specific to a future tenant’s prospective use. Both 1165 and 1171Vaughn Parkway are fully equipped with what market users typically request for TI.

» Prospective candidates would draw regional distribution users that require a Distribution Facilitylocated east of the Mississippi River, such as a more localized user from northern and middleTennessee, and southern Kentucky region.

» The market competition consists of ProLogis (1.4m sf across 4 assets), STAG (414k sf in oneasset), L&W Properties (would only have one Class B product after the sale of this asset) and other single asset private investors.

» The market competitive asset pricing is $3.25 per sf for 1165 and 1171 Vaughn Parkway and$3.65 per sf for 1216 Jay Bird Drive and 1116 Vaughn Parkway.

» The 1171 Vaughn Parkway building is fully demised (concrete walls, electrical, office) into 250,000 – 300,000 sf. 1165 Vaughn Parkway is demised but no wall (it has two office pods and separateutilities.)

» From a lease-up perspective as compared to new construction, ARGP can be the low-cost-providerbecause of your comparatively low cost-basis. As relates to a regional competitive advantage – theassets are 1/2 mile away from I-65, centrally located amongst automobile manufacturing plants in the SE United States, overall occupancy cost advantage due to the advantageous PILOT programswhich are potentially available from the local city and county municipalities.

35

ARGP Asset Exit Strategy

• Once the assets are leased-up with longer term leases (5, 7 and 10 year leases), we believe the capital markets will underwrite a100 bps spread or more.

• The divestiture will occur year 5, which is the optimal year (projected IRR: ±18.10%).

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #3

Portland Business Park Portfolio - Portland, Tennessee

36

Portland Business Park Portfolio - Portland, Tennessee

ARGP STR ATEGIC ADVANTAGE | PIPELINE TR ANSACTION #3

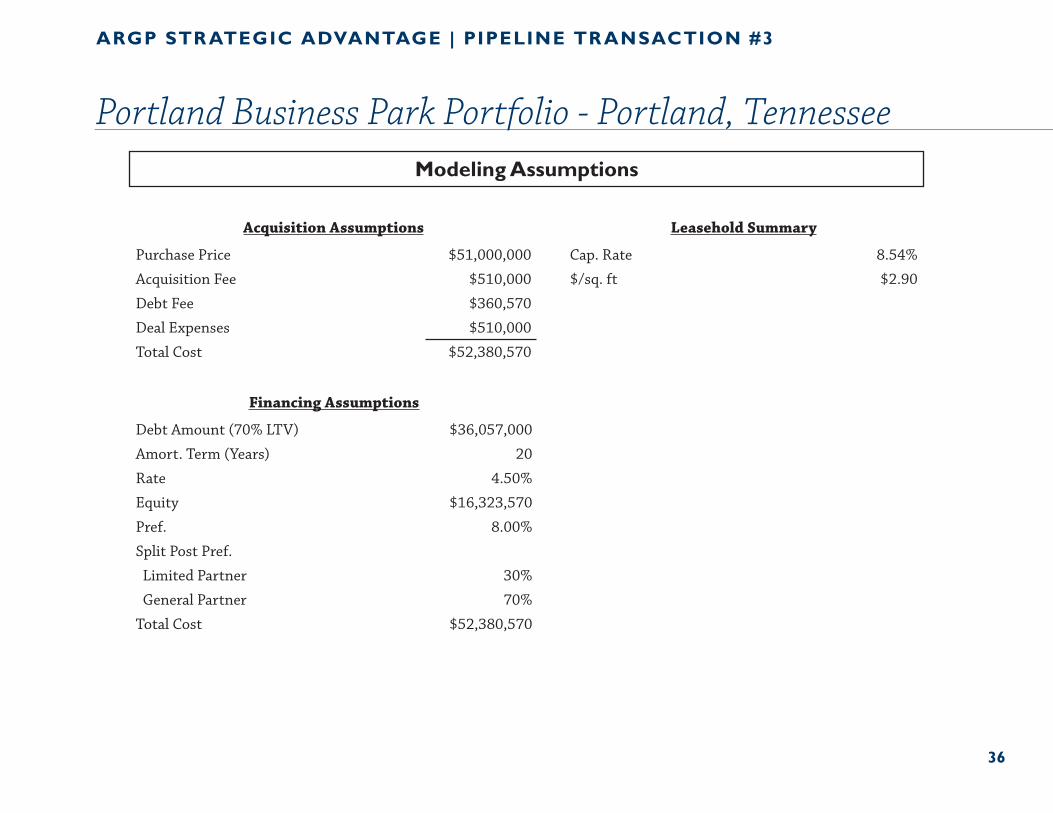

Acquisition Assumptions Leasehold Summary

Purchase Price $51,000,000 Cap. Rate 8.54%

Acquisition Fee $510,000 $/sq. ft $2.90

Debt Fee $360,570

Deal Expenses $510,000

Total Cost $52,380,570

Financing Assumptions

Debt Amount (70% LTV) $36,057,000

Amort. Term (Years) 20

Rate 4.50%

Equity $16,323,570

Pref. 8.00%

Split Post Pref.

Limited Partner 30%

General Partner 70%

Total Cost $52,380,570

Modeling Assumptions

ARGP

![FROM NEED TO OPPORTUNITY [social enterprise rural alliance]](https://img.pdfslide.us/doc/110x75/5681323c550346895d98a840/from-need-to-opportunity-social-enterprise-rural-alliance.jpg)