Embed Size (px)

Citation preview

Copyright @ 2014 Jindal Steel & Power Limited 1

1Q FY15 (June’ 14)

Jindal Steel and Power Ltd

Investor Presentation

Copyright @ 2014 Jindal Steel & Power Limited 2

Index

S. No Particulars Slide No

1 JSPL at a Glance 3-5

2 Group Executive Committee - JSPL 6-9

3 Shareholding Pattern - JSPL 10-11

4 Operational Capacity at a Glance 13-15

5 Indian Economy at Glance 16-20

6 Industry Development - Steel 21-26

7 Industry Development - Power 27-38

8 Operations 39-65

9 JPL 66-70

10 Global Ventures 71-80

11 Financials 81-91

12 Way Forward 92-99

13 Projects 100-112

Copyright @ 2014 Jindal Steel & Power Limited 3

Jindal Steel & Power Limited Face of Youthful Dynamism

Aerial View of Raigarh Plant

Copyright @ 2014 Jindal Steel & Power Limited 4

O P Jindal Group

Jindal Saw Mr. P.R. Jindal

JSL Limited Mr. Ratan Jindal

JSW Steel/JSW Energy Mr. Sajjan Jindal

Jindal Steel & Power (JSPL) Mr. Naveen Jindal

Copyright @ 2014 Jindal Steel & Power Limited 4

Ownership Structure - O P Jindal Group

Copyright @ 2014 Jindal Steel & Power Limited 5

Annual turnover of JSPL

US$ 3.3 bn+

Future investments committed across continents

US$ 30 bn

Steel making capacity Mining capacity

22.56 MTPA

Power capacity

4,532 MW

Pellet making capacity

9 MTPA 29 Countries

Ensuring pan-India presence, covering 400 districts for retail

business

People strengths

16000+

Lives impacted by JSPL’s social endeavours

9 Lakh+

Saplings planted

7.4 mn+

7.50 MTPA

Export presence

1,472 Dealers

JSPL at a Glance - Part of US$ 18 bn OP Jindal Group

Copyright @ 2014 Jindal Steel & Power Limited 6 Copyright @ 2014 Jindal Steel & Power Limited 6

Mr. Naveen Jindal – Chairman

• Ranked amongst the Asia’s 25 Hottest People in Business by the Fortune Asia magazine for turning a struggling steel company into one of Asia’s blue-chip giants

• India’s Best CEO by the BT-INSEAD-HBR Study of the top value creators for the period 1995 to 2011 by the Business Today

• Featured among the top ten of India Inc's Most Powerful CEOs 2011 by IMRB survey for Economic Times-Corporate Dossier

• Conferred with the Ernst and Young Entrepreneur of the Year Award 2010 in the field of Energy and Infrastructure

Mr. Ravi Uppal – Managing Director & Group CEO

• Over 37 years of experience in engineering and infrastructure

• Previously whole-time Director and President & CEO – L&T Group. Also held senior positions at ABB and Volvo

• Advanced MBA from Wharton, MBA from IIM Ahmedabad, and B.Tech. from IIT Delhi

Mr. Anand Goel – Chief Advisor

• Over 37 years of experience with the O.P. Jindal Group

• Master's Degree in Business Administration from BITS, Pilani

• Member of the National Steel & National Mining committees of FICCI and National Mining Committee of CII

Mr. K Raja Gopal – Director & Group CFO

• Over 32 years of experience out of which about 21 years has been with ABB

• Chartered Account from the Institute of Chartered Accountants of India

Group Executive Committee - JSPL

Copyright @ 2014 Jindal Steel & Power Limited 7 Copyright @ 2014 Jindal Steel & Power Limited 7

Mr. Rajesh Bhatia – CEO Global Ventures

• Over 21 years of experience in the field of Finance, Accounts, Taxation, Administration and Commercial

• Played an important role in JSPL's overseas acquisitions in Australia, Indonesia, South Africa, Mozambique, Madagascar, Mongolia & Oman, apart from arranging financing for greenfield expansion in Orissa and Jharkhand in India.

Mr. Subrat Ratho – MD, CTL & Head of Odisha operations

• Previously Managing Director of Maharashtra State Power Generation Company Ltd. and Mahaguj Collieries Ltd.

• Managing Director of the Maharashtra State Electricity Transmission Company Ltd. and MSEB Holding Company Ltd.

• Joined IAS in 1986

Mr. R S Sharma – Managing Director & CEO, JPL

• Over 40 years of experience in the power sector

• Previously he was the Chairman and Managing Director, NTPC Ltd.

• He has been honoured with several awards including honorary fellowship from International Project Management Association, fellowship of World Academy of Productivity Science

Group Executive Committee - JSPL

Copyright @ 2014 Jindal Steel & Power Limited 8

Mr. V K Mehta – ED Marketing

• Over 37 years of experience in marketing

• Previously, he was working with SAIL, Kolkata as its Executive Director, Marketing and was also on the Board of Directors of Mjunction and SAIL-SCI Shipping Co.

Mr. Jayant Kawale – Managing Director – Hydro & Renewables

• Over 29 years in administration in various functional fields both at State and Central Government levels

• Worked as Joint Secretary (Hydro) in Government of India

• Drafted the current Hydro Power Policy of 2008 and has served on the Boards of all hydro PSUs of Government of India

Mr. Rajeev Bhadauria – Director Group HR

• More than 29 years as a HR professional across Public and Private sectors

• Previously Regional HR head – NTPC and President HR – Reliance ADA Group

• Post Graduate in Industrial Relations from the Power Management Institute, NTPC and LLB from Allahabad University

Group Executive Committee - JSPL

Copyright @ 2014 Jindal Steel & Power Limited 9

Group Executive

Committee

Senior Management Committee

Core Management

Team

UniCo

For each Location

ManCo

For each Business

Business Segments

Global Ventures

Mines & Minerals

Power

Steel & Cement

Strategic Governance Structure Operational Governance Structure

Moving Towards Plural Leadership

Implementation of Strategic & Operational Governance Structure

Copyright @ 2014 Jindal Steel & Power Limited 10

March, 2011

March, 2012

March, 2013

March, 2014

June, 2014

Promoters 58.41% 58.91% 59.13% 60.41% 60.41%

Institutional Investors 29.54% 28.96% 27.45% 26.45% 27.15%

Public and other share holding

12.05% 12.13% 13.42% 13.14% 12.44%

Total 100.00% 100.00% 100.00% 100.00% 100.00%

Number of share holders 1,23,842 1,26,678 1,32,311 1,35,593 1,35,237

123842

126678

132311

135593 135237

115000

120000

125000

130000

135000

140000

31.03.11 31.03.12 31.03.13 31.03.14 30.06.14

Number of share holders

Number of share holders

Shareholding Pattern - JSPL

Copyright @ 2014 Jindal Steel & Power Limited 11

March, 2011

March, 2012

March, 2013

March, 2014

June, 2014

Foreign Inst’ Investors 23.44% 22.14% 20.76% 22.32% 22.38%

Insurance 4.06% 4.09% 3.23% 2.47% 3.17%

Mutual funds 2.00% 2.71% 3.41% 1.61% 1.49%

Others -financial institutions

0.04% 0.02% 0.05% 0.05% 0.11%

Total Inst’ share holding 29.54% 28.96% 27.45% 26.45% 27.15%

FII’s Continues to Keep Faith in JSPL

Institutional Shareholding - JSPL

Copyright @ 2014 Jindal Steel & Power Limited 12

Steel & Cement Power

Mines & Minerals

Business segments

Global Ventures

JSPL

Steel 7.50 MTPA

Mining 22.56 MTPA

Power 4532 MW

Business segments

Current Capacities – Domestic & Global

Business Segments

Copyright @ 2014 Jindal Steel & Power Limited 13

Capacity in deail

Raigarh

SMS 3 MTPA

BF 1.67 MTPA

DRI 1.37 MTPA

Plate Mill 1 MTPS

RUBM 0.75 MTPA

MLSM 0.60 MTPA

CPP 851 MW

Angul

SMS 2.5 MTPA

DRI 1.8 MTPA

CGP 225,000 Nm3/Hr

Plate Mill 1.2 MTPA

CPP 810 MW

Barbil

Pellet Plant

9 MTPA

Patratu

WRM 0.6 MTPA

Rebar Mill 1.0 MTPA

Oman

SMS 2.0 MTPA

HBI 1.5 MTPA

JPL

Tamnar 2800 MW

Mining

Iron Ore 3.11 MTPA

Coal Domestic

12.25 MTPA

Coal Overseas

7.20 MTPA

Operational Capacity at a Glance

Copyright @ 2014 Jindal Steel & Power Limited 14

Raigarh

3 MTPA Steel Plant

Thermal Coal 6MTPA: Gare IV / 1

Iron Ore: 3.11 MTPA Tensa Mine & Pellet from Barbil

Coking Coal: Import

Angul

2.5 MTPA Steel Plant

Thermal Coal: Either Utkal B1 / e-auction

Iron Ore: Pellet from Barbil

Coking Coal: Not Required

Barbil

9 MTPA Pellet Plant

Thermal Coal: NA

Iron Ore: External

Coking Coal: NA

Oman

2 MTPA Steel Plant

Natural Gas: MoU with Govt of Oman

Pellet: Local sources

Coking Coal: Not Required

Raw Material Sourcing - Steel

Copyright @ 2014 Jindal Steel & Power Limited 15

Tensa Orissa 3.11MT Raigarh Steel

Jeraldaburu Jharkand - Asanboni Steel

Gare IV / 1 Chhattisgarh 6.00 MT Raigarh DRI & Captive Power PlantGare IV / 2 & 3 (JPL) Chhattisgarh 6.25MT JPL Power

Utkal B 1 Orissa 5.5MT DRI at Angul & Captive Power PlantGare IV / 6 Chhattisgarh 4 MT Raigarh Steel & CPPJitpur Jharkand 2.5MT JSPL's CPP at GoddaUrtan North* M.P. 0.6 MT Raigarh Steel Amarkonda* Jharkhand - Power plant at Patratu and DumkaRamchandi (CTL)* Orissa - Coal to Liquid & CPP based on Middlings

For Existing Operations

For Future Expansion

For Existing Operations

For Future Expansion

Wollongong coal Limited, Australia

Domestic Coal

* Stay obtained from HC against De-allocation by MOC .

Overseas Coal

South Africa Under OperationMozambique Under Operation

Indonesia Under DevelopmentBotswana Under Development

Under Operation

Mine State

Annual extraction

(Approved capacity as

per mine plan)

End Use

Domestic Iron Ore

Overview of Mines

Copyright @ 2014 Jindal Steel & Power Limited 16

Copyright @ 2014 Jindal Steel & Power Limited 17

Economic Growth – Top of the Agenda (5.5% to 6% during FY14-15)

Indian Economy – Dawn of a NEW ERA (14-15)

Likely new Policy trends (1/2)

Enhanced participation and ownership of foreign companies

Increased E - Governance

Empowerment & accountability of Bureaucracy

Simplification of Tax Regime & introduction of GST

Larger role and delegation for State Government

De - Regulation of Economy

Copyright @ 2014 Jindal Steel & Power Limited 18

Indian Economy – Dawn of a NEW ERA (14-15)

Likely new Policy trends (2/2)

Dilution of “Land Bill” for Infrastructure & Housing

Speedier “Environmental & Forest Clearances”

Reduction of Subsidies

Focus on Inflation Control

Focus on Infrastructure & Manufacturing

Divestment of Public Sector

Transparency in allocation of Mines & Minerals

Copyright @ 2014 Jindal Steel & Power Limited 19

IIP

Copyright @ 2014 Jindal Steel & Power Limited 20

Index of 8 core industries grows at 7.3% in June, fastest since October last year

Electricity Sector: Latest estimates show growth at 15.7% in June, compared with 6.3% in May

Steel Sector: Growth of 4.2% in June as compared to 2% in May

Cement Sector: Grew at 13.6% in Jun against 8.7% in May

Economic Survey expects India's economy to expand by 5.4 - 5.9% this fiscal

Positive Indications

Copyright @ 2014 Jindal Steel & Power Limited 21

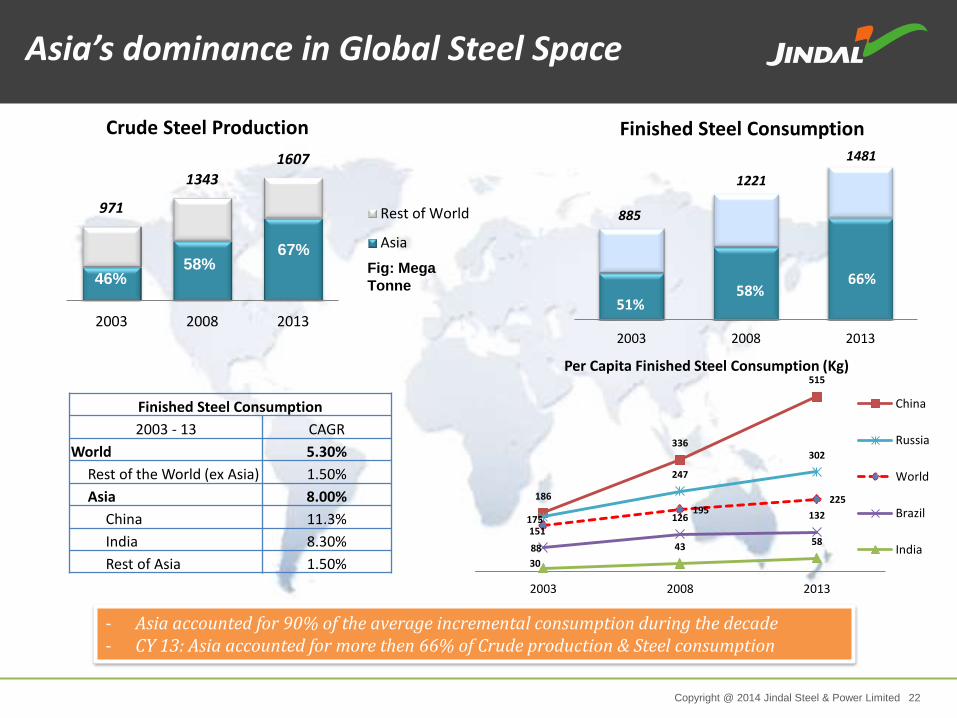

Copyright @ 2014 Jindal Steel & Power Limited 22

971

1343

1607

2003 2008 2013

Crude Steel Production

Rest of World

Asia67%

58% 46%

Fig: Mega

Tonne

186

336

515

175

247

302

151

195 225

88

126 132

30

43 58

2003 2008 2013

Per Capita Finished Steel Consumption (Kg)

China

Russia

World

Brazil

India

885

1221

1481

2003 2008 2013

Finished Steel Consumption

66% 58%

51%

Finished Steel Consumption

2003 - 13 CAGR

World 5.30%

Rest of the World (ex Asia) 1.50%

Asia 8.00%

China 11.3%

India 8.30%

Rest of Asia 1.50%

- Asia accounted for 90% of the average incremental consumption during the decade - CY 13: Asia accounted for more then 66% of Crude production & Steel consumption

Asia’s dominance in Global Steel Space

Copyright @ 2014 Jindal Steel & Power Limited 23

801

540

84

54.4 59

23 13 8

821

555

87

53.9 60

22 14 8

World Asia EU CIS North America South America Middle East Africa

MillionTonne

Jan - June '13 Jan - June '14

2.5%

2.9%

3.8% 1.7

% 9.3%

1.2%

1 %

2.6%

Production

Jan – June 2014 - Global Steel production

Copyright @ 2014 Jindal Steel & Power Limited 24

77

20 20

81

21 21

CY (12 Vs 13) Jan-March (13 Vs 14) April-June (13 Vs 14)

India

India: - Steel production (Jan- April’14) up by 1.6% (y-o-y) - Steel production (April- June’14) up by 1.1% (y-o-y)

5.0%

1.6% 1.1%

Production trend of Indian Steel Industry

Copyright @ 2014 Jindal Steel & Power Limited 25

April ‘14 – July ‘14: Price movement: Domestic Prices: - TMT & WR prices on

uptrend. International Prices: - ~ 9% decrease in TMT

(FOB China) - ~ 5% decrease in Wire

rod (FOB China)

440

460

480

500

520

540

560

30000

32000

34000

36000

38000

40000

42000

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Last week Latest

Pri

ces

( R

s/M

T-B

asic

)

Price Movement : TMT & Wire Rod Domestic (Delhi-Rs/MT) Vs International ($/MT)

TMT Rebar-Delhi

Wire Rod-Delhi

TMT Rebar-FOB China

Wire Rod -FOB China

Price trend – Long products

Domestic

International

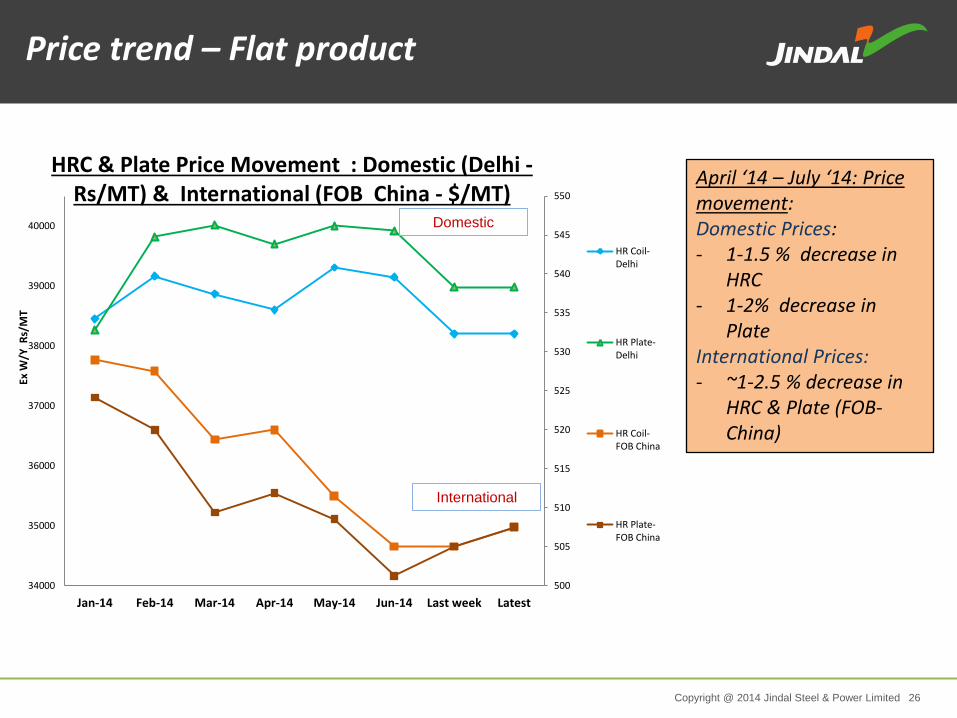

Copyright @ 2014 Jindal Steel & Power Limited 26

April ‘14 – July ‘14: Price movement: Domestic Prices: - 1-1.5 % decrease in

HRC - 1-2% decrease in

Plate International Prices: - ~1-2.5 % decrease in

HRC & Plate (FOB-China)

500

505

510

515

520

525

530

535

540

545

550

34000

35000

36000

37000

38000

39000

40000

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Last week Latest

Ex W

/Y R

s/M

T

HRC & Plate Price Movement : Domestic (Delhi -Rs/MT) & International (FOB China - $/MT)

HR Coil-Delhi

HR Plate-Delhi

HR Coil-FOB China

HR Plate-FOB China

International

Domestic

Price trend – Flat product

Copyright @ 2014 Jindal Steel & Power Limited 27

Copyright @ 2014 Jindal Steel & Power Limited 28

Power Scenario – Installed Capacity

(As on 30th June 2014)

172,286

4,780

40,730 31,692

249,488

-

50,000

100,000

150,000

200,000

250,000

300,000

3,804

21,136

4,014

107

2,632

Small Hydro Wind BM/Cogen Waste to Energy Solar

(in MW)

Source: CEA

(in GW)

59.5%

9.1%

0.5%

1.9%

16.3%

12.7%

Coal Gas Diesel Nuclear Hydro RES

148 159

174

200

223

243

0

50

100

150

200

250

300

FY09 FY10 FY11 FY12 FY13 FY14

All India – Installed Capacity

Renewable Sources All India –

Installed Capacity (in MW)

Copyright @ 2014 Jindal Steel & Power Limited 29

Growth in Thermal Capacity vs PLF

Source: CEA

94 102

112

132

152

168 172 77.20% 77.50%

75.07%

73.32%

69.95% 65.55%

68.54%

50.00%

55.00%

60.00%

65.00%

70.00%

75.00%

80.00%

0

20

40

60

80

100

120

140

160

180

200

FY09 FY10 FY11 FY12 FY13 FY14 Q1FY15

Inst.Cap (in GW) PLF (in %age)

Copyright @ 2014 Jindal Steel & Power Limited 30

Effective Power Capacity

Gross Capacity (MW) Max PLF Effective Capacity @100%

availability (MW)

Thermal

1,72,286 85%

1,46,443

Hydro / Small hydro

44,534 40%

17,814

Wind

21,136 25%

5,284

Solar

2,632 15%

395

Nuclear

4,780 60%

2,868

Other Renewable

4,120 40%

1,648

Total

2,49,488

1,74,452

Copyright @ 2014 Jindal Steel & Power Limited 31

Private Sector Contribution in Generation

11 12 13 14 15 18 20 27 31 34 35

89 88 87 86 85 82 80 73 69 66 65

0%

20%

40%

60%

80%

100%133 125 113 160 149 174 200 144 224

Private Government

Source: CEA; Planning commission; Infraline; Analyst report; Company Web sites

243 249

Increasing share of private sector

In GW

Copyright @ 2014 Jindal Steel & Power Limited 32

Demand Supply scenario Q1 FY15

83 82 73

30

3

271

78 81 69

30

3

260

-5%

-1%

-6%

-1%

-8%

-4%

-9%

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

-

50

100

150

200

250

300

Northern Western Southern Eastern North Eastern All India

Demand Supply Deficit

Power Demand Supply Position (BU)

Demand Supply gap of 10.8 billion units in 1QFY15

Copyright @ 2014 Jindal Steel & Power Limited 33

India’s per capita consumption of Electricity

631 672

717 734 779

819

884 917

0

100

200

300

400

500

600

700

800

900

1000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Annual Per Capita Consumption (Kwh)

Source: CEA

Copyright @ 2014 Jindal Steel & Power Limited 34

Comparison of Per-capita consumption

13394

10177

6452 5736

2944 2384

884

0

2000

4000

6000

8000

10000

12000

14000

16000

US Australia Russia UK China Brazil India

2011-12 Annual Per Capita Energy Consumption (kWh)

Copyright @ 2014 Jindal Steel & Power Limited 35

Country wise generation of Electricity

5362

4260

3260

1103 1088 1061

634 627 568 557

0

1000

2000

3000

4000

5000

6000

Country-wise Electricity Generation - 2013 (in TWh)

Copyright @ 2014 Jindal Steel & Power Limited 36

Power deficit states

4.8% 5.0% 5.5% 5.9% 6.2% 7.0% 8.4% 10.5%

13.4%

20.0%

24.6%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

4.1% 4.8% 4.9% 5.6% 5.8% 6.9% 8.1% 10.0%

12.9% 15.9%

20.0%

Source: CEA

Peak Deficit

All India Avg. 3.7%

(Apr’14 to Jun’14)

All India Avg. 4.0%

(Apr’14 to Jun’14)

Base Deficit

Copyright @ 2014 Jindal Steel & Power Limited 37

Challenges faced by Indian Power Industry

•Lack of sufficient growth in domestic coal Production • Regulatory changes in markets such as Indonesia • Shortage of gas supply

Fu

el

Ge

ne

rati

on

• Inordinate delays in environmental clearances • Tightening of norms from financial institutions

Copyright @ 2014 Jindal Steel & Power Limited 38

Challenges faced by Indian Power Industry

•Network not sufficient to meet growth • Several Transmission projects developing slowly • Success of Southern Grid integration and open access depends on expansion of Transmission capacity • Development of Regional & National Grids

Tra

nsm

issi

on

D

istr

ibu

tio

n • SEBs financial losses

• High AT&C losses • SEBs resorting to load shedding in peak hours • Entry of Private players in T&D

Copyright @ 2014 Jindal Steel & Power Limited 39

Copyright @ 2014 Jindal Steel & Power Limited 40

In FY14 In FY 15

5 MTPA

2800 MW

~2x

~2.8x

2 MTPA add

Steel - India 3 MTPA

Power 1000 MW

Oman 0 MTPA

Pellet 4.5 MTPA 9 MTPA ~2x

Business Achievements…

In terms of Capacity addition ..another JSPL is added to JSPL

Copyright @ 2014 Jindal Steel & Power Limited 41

12,100 Cr. 3.5 MTPA Liquid Steel 2.35 MTPA Finished Steel 851 MW 5200 Investment Capacity Steel Power Workforce

JSPL at Raigarh

Copyright @ 2014 Jindal Steel & Power Limited 42

Flow Diagram of Process in Raigarh

Copyright @ 2014 Jindal Steel & Power Limited 43

18500 Cr. + 1.5 MTPA Steel 1.2 MTPA Finished Steel 810 MW 2723 Investment Capacity Capacity Power Workforce

JSPL at Angul

Copyright @ 2014 Jindal Steel & Power Limited 44

Product usage

Ship Building Line Pipes High End Structural

Boilers Wind Mills Engineering Pressure Vessels

Coal Gasification Gas Based DRI EAF

Plates Plate Mill Slab Caster

Link Link Link

Link Link Link

Flow Diagram of Process in Angul

Copyright @ 2014 Jindal Steel & Power Limited 45

2,388Cr. 9 MTPA Pellet 660 Investment Capacity Workforce

JSPL at Barbil

Copyright @ 2014 Jindal Steel & Power Limited 46

Flow Diagram of Process in Barbil

Copyright @ 2014 Jindal Steel & Power Limited 47

Process of Pelletisation

Copyright @ 2014 Jindal Steel & Power Limited 48

1,764 Cr. 1.6 MTPA Finished Steel 1,373 Investment Capacity Workforce

JSPL at Patratu

Copyright @ 2014 Jindal Steel & Power Limited 49

Bar Mill Processing Panther TMT Rebar

WRM Processing Wire Rod

Rebar Service Centre Processing Taking Shape Cut & Bend

Flow Diagram of Process in Patratu

Copyright @ 2014 Jindal Steel & Power Limited 50

Plant Installed

Capacity (Ton)

Covered area (Sq. Mts)

Angul (Odisa)

84,000 32,000

Plant Installed

Capacity (Ton)

Covered area (Sq. Mts)

Punjipatra (Raigarh)

1,20,000 60,000

Structural Steel Division

Copyright @ 2014 Jindal Steel & Power Limited 51

At Angul

• Widest Plate Mill (5m) in India with 4th generation Heat Reversible Treat Plate Leveler

• Roll Trip-steel/Silicon Steel/DD/EDD/IF grades : opens up opportunity for new and high margin product segments.

• Further processing to address value added markets: Galvanized & Coated Steel

• Largest BF in India (4554 m3), few among the world

Investing in State-of-the-Art Technologies & manufacturing system for high margin products

New Products & Technology Initiatives

Copyright @ 2014 Jindal Steel & Power Limited 52

At Raigarh

• RUBM to be leveraged with Head Hardened Rail Facility: To cater to metro boom in Indian cities.

• Only manufacturer of high margin HH rail in India.

• Galvanizing facility of structures: Catering to high margin TLT segment.

At Patratu

• State-of-the-art Wire-Rod Mill: Forward integrated with wire-drawing

New Products & Technology Initiatives

Copyright @ 2014 Jindal Steel & Power Limited 53

At Oman • Commissioned its 2-MTPA ISP in Oman: Rode into the league of the three biggest steel

makers in the Arab peninsula. • SMS complex : EAF (200MT) largest in Middle East, a Ladle Furnace (200MT), Continuous

Billet Caster and Vacuum Degassing Furnace Facility • The new steel plant is among the most compact and advanced anywhere in the world:

commissioned from scratch in an astounding 23 months flat.

New Products & Technology Initiatives

Copyright @ 2014 Jindal Steel & Power Limited 54

• Expanding Geographical reach of Steel sales – New offices setup in South Africa, Dubai,

Indonesia

• Launch of Channel financing in retail segment and Increasing the turnover by 3 times.

• Revamping "key account managers" concept for steel business

New Initiatives

Copyright @ 2014 Jindal Steel & Power Limited 55

Fabricated Structures Hot Rolled Plates

and Coils Parallel Flange Beams

Wire Rods Power

Angles and Channels

TMT Rebars Rails

JSPL Product Range

Copyright @ 2014 Jindal Steel & Power Limited 56

Presence in 27 states and 5 Union Territories covering 500 districts

Over 41 distributors

More than 1,300 dealers across country

27 Retail Sales Managers and 207 Distributors ASOs

731 Hoardings installed

450 Shop boards installed across country. More underway

Panther Brand was launched on 5th August 2013 (National Event Organized)

Training sessions for Distributors & Dealers being organized across country

Panther TMT Bars Brand

Copyright @ 2014 Jindal Steel & Power Limited 57

Performance Highlights – Q1 FY 2014-15

Copyright @ 2014 Jindal Steel & Power Limited 58

Finished goods Inventory Reduction by 27%

Finished Steel sales grew by 11%

Retails sales grew by 284%

Over 25% growth in Retail Dealer network from March 2014

1.24 lakh MT steel exported - increase of 6% over Q1 last year

8% growth in NSR of Steel in Q1 FY 15 vs Q1 FY 14 Captive power generation increased by 29%

Key Highlights: Q1 FY14-15

Copyright @ 2014 Jindal Steel & Power Limited 59

• Modernization of BF – 1 completed

• Revamp of EAF - 1 completed in 15 days

• Slag Processing plant commissioned

Performance Highlights – Raigarh

Copyright @ 2014 Jindal Steel & Power Limited 60

Investing in State-of-the-Art Technologies & manufacturing system for high margin products

• Coal Gasification plant commissioned.

• DRI plant commissioned - Production started

• Use of syn gas in Re heating furnace Plate Mill, Lime and Dolo Kilns & SMS in

place of LDO/HSD.

• Started dispatch of CGP By products in the market

Performance Highlights – Angul

Copyright @ 2014 Jindal Steel & Power Limited 61

• Jindal Shadeed commissioned its state of the art 2 MTPA Steel Melting Shop, first &

largest integrated Steel Plant in Oman, on 23rd April 2014

Performance Highlights – Oman

Copyright @ 2014 Jindal Steel & Power Limited 62

Growth in Distributor Network (from 5 – 41)

Growth in Dealer Network (from 267 to 1472)

5

15 17 20 23 25 25 30

40 41 41 41 41 41 41 41

0

20

40

Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14

267 357 495 511 532 571 653 721 759

955 1014 1128 1216 1261 1360

0

200

400

600

800

1000

1200

1400

Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14

1472

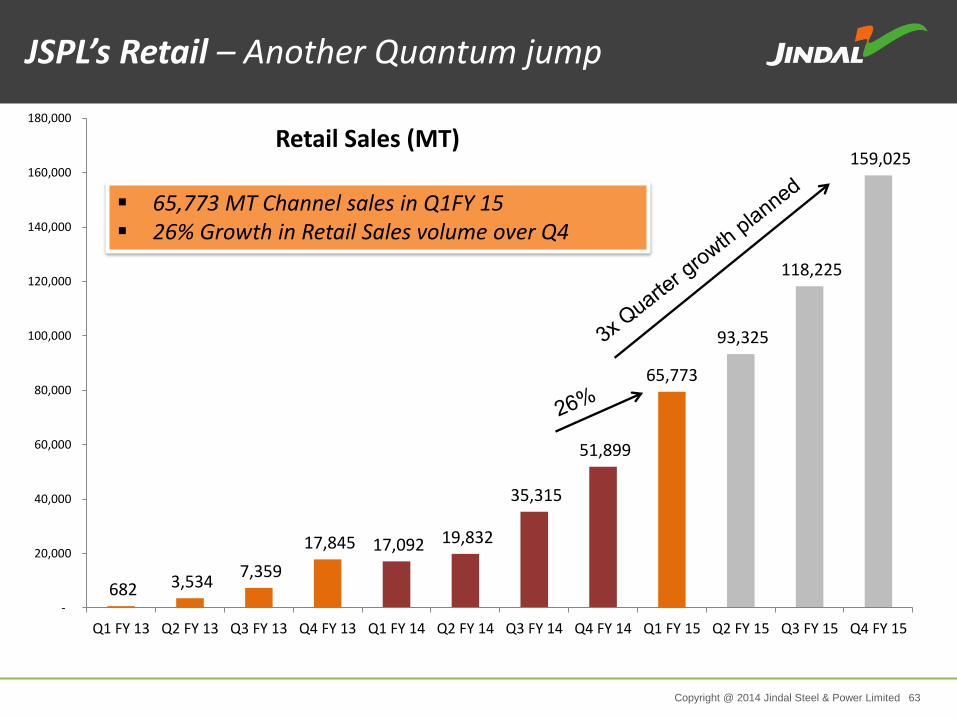

JSPL’s Retail – Network growth

Copyright @ 2014 Jindal Steel & Power Limited 63

682 3,534 7,359

17,845 17,092 19,832

35,315

51,899

65,773

93,325

118,225

159,025

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Q1 FY 13 Q2 FY 13 Q3 FY 13 Q4 FY 13 Q1 FY 14 Q2 FY 14 Q3 FY 14 Q4 FY 14 Q1 FY 15 Q2 FY 15 Q3 FY 15 Q4 FY 15

Retail Sales (MT)

65,773 MT Channel sales in Q1FY 15 26% Growth in Retail Sales volume over Q4

JSPL’s Retail – Another Quantum jump

Copyright @ 2014 Jindal Steel & Power Limited 64

19

104

140

170

119

138

150 141

124

-

20

40

60

80

100

120

140

160

180

Q1 FY 13 Q2 FY 13 Q3 FY 13 Q4 FY 13 Q1 FY 14 Q2 FY 14 Q3 FY 14 Q4 FY 14 Q1 FY 15

Export Sales (in MT) 4% growth in Export Sales in Q1 FY 15 (vs Q1 FY 14)

Focus on growth in Exports

Copyright @ 2014 Jindal Steel & Power Limited 65

89

57

13 17

10

142

79

145

147

96

63

6

18 13

143

93

128

166

-

20

40

60

80

100

120

140

160

180

200

Structural MLSM Conv Wld Beam Rail TMT Wire Rod Semis Plates

Q1 FY 14 Q1 FY 15

Growth uniform across products

Product wise Steel Sales

(volume in 000’ MT)

Copyright @ 2014 Jindal Steel & Power Limited 66 Power Plant at Tamnar

POWER

Copyright @ 2014 Jindal Steel & Power Limited 67

96.43% subsidiary of JSPL

Existing Units Phase I - 1000MW (4 X 250) Phase II - 1800MW (3 X 600)

Under Implementation 600MW (1 X 600)

JINDAL POWER LIMITED

Copyright @ 2014 Jindal Steel & Power Limited 68

Particulars Net Sales

(Cr.) PAT (Cr.)

Generation (MU)

PLF

Year 2013-14 2411 1107 8282 92%

Year 2012-13 2420 1113 7973 91%

Year 2011-12 2980 1765 8589 98%

JPL Financials

Copyright @ 2014 Jindal Steel & Power Limited 69

Quarter 1

Growth (%) 2014-15 2013-14

Turnover 702 647 9%

EBITDA 427 423 1%

EBITDA% 61% 65% -

PBT 246 406 (39%)

PBT% 35% 63% -

PAT 195 321 (39%)

PAT% 28% 50% -

Depreciation + Amortization 130 66 97%

Cash Profit 328 394 (17%)

Generation (million units) 2446 2184 12%

JPL Financials – Q1 FY 15

Copyright @ 2014 Jindal Steel & Power Limited 70

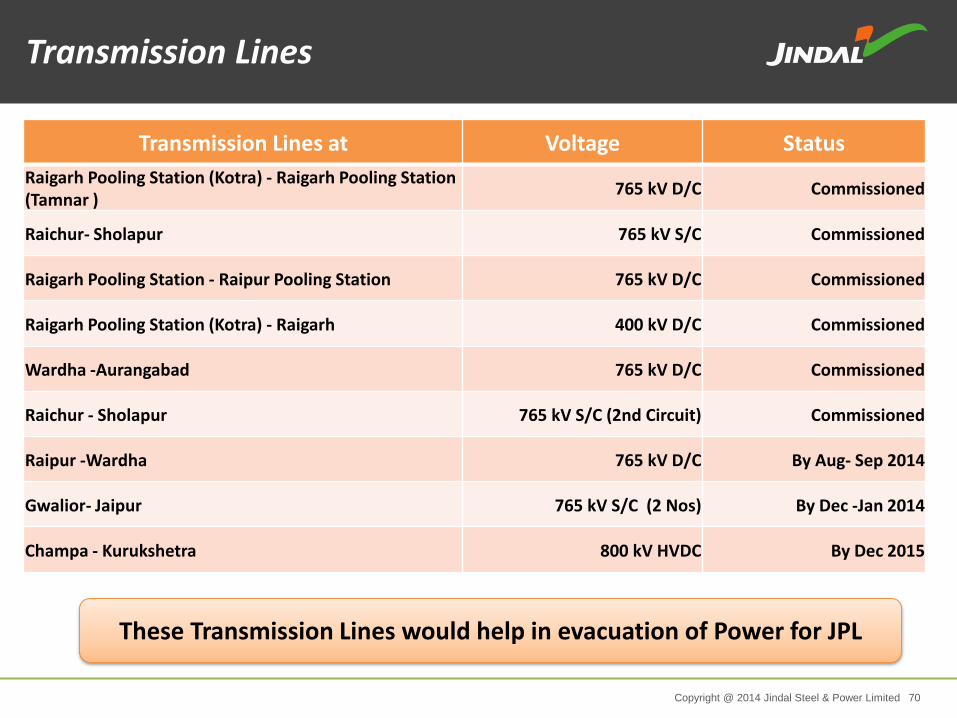

Transmission Lines at Voltage Status

Raigarh Pooling Station (Kotra) - Raigarh Pooling Station (Tamnar )

765 kV D/C Commissioned

Raichur- Sholapur 765 kV S/C Commissioned

Raigarh Pooling Station - Raipur Pooling Station 765 kV D/C Commissioned

Raigarh Pooling Station (Kotra) - Raigarh 400 kV D/C Commissioned

Wardha -Aurangabad 765 kV D/C Commissioned

Raichur - Sholapur 765 kV S/C (2nd Circuit) Commissioned

Raipur -Wardha 765 kV D/C By Aug- Sep 2014

Gwalior- Jaipur 765 kV S/C (2 Nos) By Dec -Jan 2014

Champa - Kurukshetra 800 kV HVDC By Dec 2015

These Transmission Lines would help in evacuation of Power for JPL

Transmission Lines

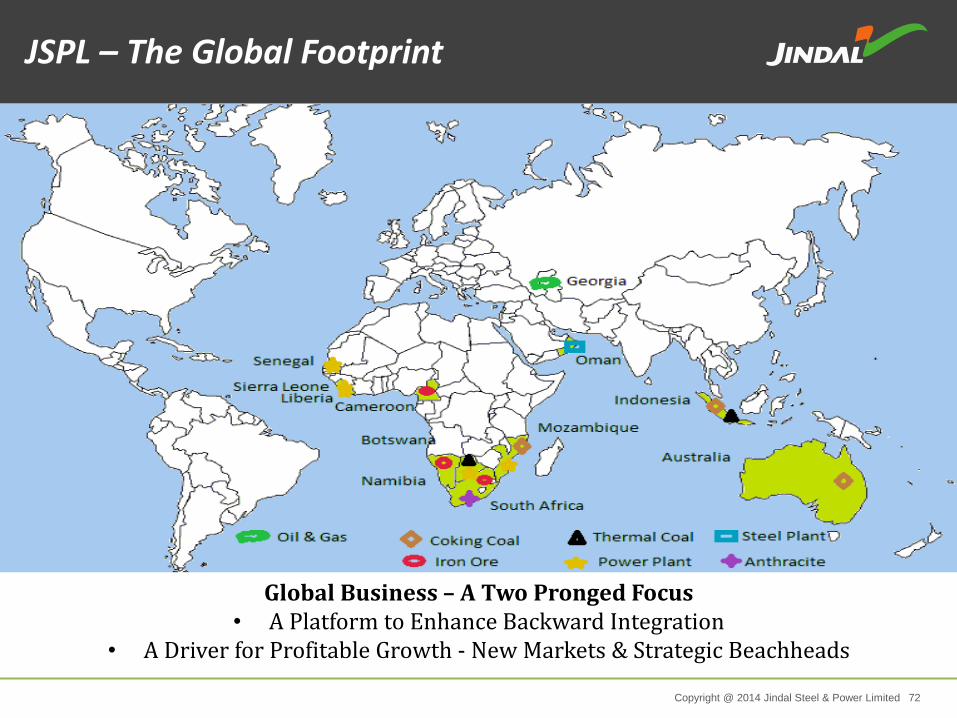

Copyright @ 2014 Jindal Steel & Power Limited 71 Corporate Office, Jindal Africa

Copyright @ 2014 Jindal Steel & Power Limited 72

Global Business – A Two Pronged Focus • A Platform to Enhance Backward Integration

• A Driver for Profitable Growth - New Markets & Strategic Beachheads

JSPL – The Global Footprint

Copyright @ 2014 Jindal Steel & Power Limited 73

Developing a coal mine

(3 MTPA) in

Mozambique’s coal-rich

Moatize region

Coal resources

estimated at 1.2 bn

tonnes including coking

coal

Mozambique, Africa

JSPL’s Kiepersol Colliery produces about 1.2

MTPA of Anthracite coal, sold domestically and

internationally Plans to ramp up capacity to 2

MTPA

South Africa, Africa

Botswana, Africa Acquired CIC Energy in 2012 for 120 mn USD

Coal Mine with Resource of over 3 bn MT (high

grade thermal coal)

Proposed Cement Plant

Madagascar, Africa

Acquired 74.39% controlling

stake in Wollongong Coal

(Erstwhile Gujarat NRE coking

coal Limited)

Australia

1.5 MT HBI Plant – plan to make

it an Integrated Steel Plant

Shadeed, Oman Medium to large size

deposits of prime hard

coking and low ash – low

sulphur thermal coal for

open-cast operation

Indonesia, Asia

Summary of International Operations

Copyright @ 2014 Jindal Steel & Power Limited 74

Production HBI (MT): 353,727 Sales (MT): 312,046 Sales (Million USD): 111 EBITDA (million USD): 22

OMAN

Production (MT): 69,914 Sales (MT): 59,166 Sales (Million USD): 6 EBITDA (million USD): (1)

SOUTH AFRICA

Production (MT): 111,565 Sales (MT): 99,616 Sales (Million USD): 7.5 EBITDA (million USD): (5)

MOZAMBIQUE

Production (MT): 42,145 Sales (MT): 85,636 Sales (Million USD): 15 EBITDA (million USD): 3

Wollongong Coal Ltd

Global Ventures - Production & Sales – Q1 FY 14-15

Copyright @ 2014 Jindal Steel & Power Limited 75

In July 2010, JSPL acquired Shadeed Iron & Steel Co. LLC, a company incorporated under

the laws of the Sultanate of Oman

• Gas-based 1.5 MTPA HBI plant at Sohar Industrial Port commenced production in January 2011

• Commissioned steelmaking facility of 2 MTPA in CY14

Investment

US$ 525 mn

Capacity

2 MTPA Steel

Jindal Shadeed – Oman

Copyright @ 2014 Jindal Steel & Power Limited 76

• Potential Resource: 2 bn MT

• Grade: Semi Hard coking coal , High Grade Thermal Coal

• Current Mining @ 3 MTPA run rate

• 3 MTPA Coal Washery commissioned

Mozambique, Africa

Copyright @ 2014 Jindal Steel & Power Limited 77

Mining Operations taken over with effect from 1st July 2014

Reverse Freight Contract finalized for carrying 3,00,000 Tonnes of cargo from Beira to Moatize

Floatation Plant to be commissioned in August, 14 which would reduce ash content in Coking coal

Mozambique - Key Operational Highlights

Copyright @ 2014 Jindal Steel & Power Limited 78

Unique unmatched location with significant strategic advantages

Unique Geographic Location • Wollongong (80 kms. South of

Sydney) experienced mining community

available • Port Kembla: < 20 kms. with

sufficient coal handling and Cape size capacity

• Easy and reliable connectivity through Rail and Road

Activities :

Manpower reduced from 590 to 241

Restructuring of Bank Loans

Arrangement made with most of the suppliers for their past liabilities though phased payment plans(About A$ 24 million paid out of A$ 41 million)

Wollongong Coal Limited- Australia

Copyright @ 2014 Jindal Steel & Power Limited 79

• Southern Africa head office is based in Johannesburg, South Africa

• Operations include Kiepersol Colliery outside the town of Piet Retief in Mpumalanga province

• The mine produces high-quality anthracite coal, sold nationally and internationally

• Underground mining with 1.2 MTPA capacity annually

South Africa, Africa

Copyright @ 2014 Jindal Steel & Power Limited 80

Thermal Coal Asset

• Large size deposit of low ash – low sulphur thermal coal for open cast operation

• Coal mining license obtained in 2009 for 10 years till March 2018 for over 35.9 square Kilometres

• Permit received from the Ministry of Forest for the entire concession area

• MoU signed with Bupati Barito to develop road for coal hauling

• 139 hectares acquired for the first phase of mining

• Acquired 17.7 hectares for the development of captive coal terminal for coal handling and

barge loading at Barito River

Coking Coal Asset

Exploration License over 100 square kilometre in Central Kalimantan

Medium to large size deposits of prime hard coking and thermal coal for open-cast operation Pit Sampling

Indonesia, Asia

Copyright @ 2014 Jindal Steel & Power Limited 81

Financial Performance

Copyright @ 2014 Jindal Steel & Power Limited 82

Consolidated Financials at a Glance

(Rupees in Crores) FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 Q1 FY 15

INCOME STATEMENT

Revenue 1,273 2,271 2,618 3,549 5,539 10,913 11,152 13,194 18,351 19,807 20,004 4,870

EBITDA 512 908 1,034 1,428 2,253 5,908 5,232 6,398 6,935 6,669 5,776 1,626

PAT 305 516 573 703 1,251 3,007 3,635 3,804 4,002 2,912 1,894 402

Cash Profit 434 766 858 1,170 1,810 4,194 4,760 5,115 5,575 4,593 3,876 1,149

BALANCE SHEET

Gross Block 1,967 2,876 5,198 8,690 10,680 14,928 21,109 29,317 35,802 45,912 63,056 65,181

Net Worth 854 1,317 1,899 2,540 3,824 7,021 10,387 14,088 17,931 21,150 21,191 21,564

Borrowings 1,026 1,495 2,745 3,507 6,996 8,113 8,605 13,987 17,058 24,618 36,368 37,111

Equity 15 15 15 15 15 15 93 93 93 93.48 91.49 91.49

SIGNIFICANT RATIOS

Operating Margin (%) 40% 40% 40% 41% 41% 48% 53% 49% 39% 34% 28% 33%

Net Profit to Sales (%) 24% 23% 22% 20% 23% 28% 33% 29% 22% 15% 9% 8%

Return on Net Worth (%) 36% 39% 31% 28% 34% 43% 35% 27% 22% 14% 9% 7%

Long Term Debt Equity Ratio 1.09 1.11 1.2 1.07 1.74 1.03 0.59 0.7 0.61 0.77 1.29 1.3

EPS (INR/Share) (a) (b) 3.34 5.58 6.31 7.64 13.54 32.44 39.05 40.75 42.42 31.13 20.53 3.35

Copyright @ 2014 Jindal Steel & Power Limited 83

854 1,317 1,899 2,540 3,824

7,021

10,387

14,088

17,931

21,150 21,191

-

5,000

10,000

15,000

20,000

25,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Net Worth

Net worth zooms by 2381% in 10 Years

Net Worth

Rs. In Cr.

Copyright @ 2014 Jindal Steel & Power Limited 84

Capacity Enhancement

1,967 2,876 5,1988,690 10,680

14,928

21,109

29,317

35,802

45,912

63,056

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Gross Block

Gross Block

Rs. In Cr.

Copyright @ 2014 Jindal Steel & Power Limited 85

1,2732,271 2,618

3,549

5,539

10,913 11,152

13,194

18,35119,807 20,004

0

5,000

10,000

15,000

20,000

25,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Revenue Increased around 15 times over the last 10 years

Revenue

Rs. In Cr.

Copyright @ 2014 Jindal Steel & Power Limited 86

512908 1,034

1,428

2,253

5,908

5,232

6,398

6,9356,669

5,776

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Healthy EBITDA margin continues year after year

EBITDA

Rs. In Cr.

Copyright @ 2014 Jindal Steel & Power Limited 87

Financial Results Q1- FY15 – Consolidated

Interest, 268

Depreciation , 422

PBT, 669

PAT, 501

EBITDA, 1,305

Interest, 535

Depreciation , 667

PBT, 517

PAT, 402

EBITDA, 1,626

Q1 FY14 Q1 FY15

Increased Interest & Depreciation cost drops profit

EBITDA continues to Rise

Copyright @ 2014 Jindal Steel & Power Limited 88

Financial Results – Standalone Q1 FY15

Particulars (Rupees in Crores) For the Quarter ending %

30.06.2014 31.03.2014 30.06.2013 Y ON Y Q ON Q

Turnover-Total 3,584 3,813 3,425 4.6% -6.0%

EBITDA 1,192 972 848 40.6% 22.7%

Depreciation 415 316 304 36.8% 31.6%

Finance costs 428 405 232 84.8% 5.8%

PBT 370 385 319 16.2% -3.9%

Profit after Tax 306 431 239 28.2% -28.9%

Cash Profit 786 777 555 41.4% 1.1%

CAPEX 720 1,101 1,228

Copyright @ 2014 Jindal Steel & Power Limited 89

Ratio (%) 2014-15 2013-14 2013-14 2013-14

Q1 Q4 Q1 Annual

Raw Material to turnover 26.7 31.6 34.8 32.5

EBITDA to turnover 33.3 25.5 24.7 27.6

Profit before tax to turnover 10.3 10.1 9.3 11.0

Profit after tax to turnover 8.5 11.3 7.0 8.9

Debt Equity Ratio 1.8 1.8 1.6 1.8

Current Ratio 0.7 0.9 1.0 0.9

Interest Service Coverage Ratio 2.1 2.2 2.4 2.2

Debt Service Coverage Ratio 1.2 1.3 1.8 1.3

Financial Ratios – Standalone Q1 FY15

Copyright @ 2014 Jindal Steel & Power Limited 90

30.06.2014 31.03.2014 30.06.2013 Y ON Y Q ON Q

Turnover-Total 4,978 5,267 4,540 9.6% -5.5%

EBITDA 1,626 1,314 1,305 24.6% 23.8%

Depreciation 667 514 422 58.2% 29.8%

Finance costs 535 423 268 100.1% 26.5%

PBT 517 396 669 -22.8% 30.4%

Profit after Tax 402 378 501 -19.8% 6.2%

Cash Profit 1,149 947 929 23.7% 21.3%

CAPEX 2,172 2,832 2,568

Particulars (Rupees in Crores)For the Quarter ending %

Financial Results – Consolidated Q1 FY15

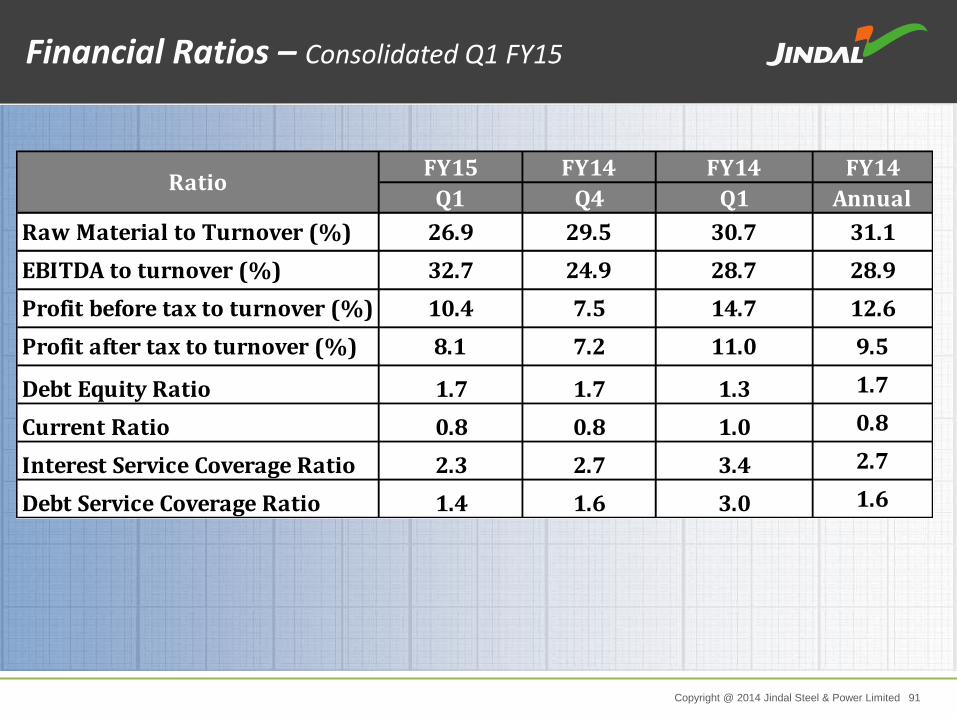

Copyright @ 2014 Jindal Steel & Power Limited 91

FY15 FY14 FY14 FY14

Q1 Q4 Q1 Annual

Raw Material to Turnover (%) 26.9 29.5 30.7 31.1

EBITDA to turnover (%) 32.7 24.9 28.7 28.9

Profit before tax to turnover (%) 10.4 7.5 14.7 12.6

Profit after tax to turnover (%) 8.1 7.2 11.0 9.5

Debt Equity Ratio 1.7 1.7 1.3 1.7

Current Ratio 0.8 0.8 1.0 0.8

Interest Service Coverage Ratio 2.3 2.7 3.4 2.7

Debt Service Coverage Ratio 1.4 1.6 3.0 1.6

Ratio

Financial Ratios – Consolidated Q1 FY15

Copyright @ 2014 Jindal Steel & Power Limited 92

Way Forward

Copyright @ 2014 Jindal Steel & Power Limited 93

Commission the balance one

unit of 600 MW at Tamnar in H2 of FY 15

Target “Break - Even” performance in Mozambique by

FY 15

Stabilize production from CGP and DRI in

Angul.

To target 15% to 20% of total

revenue from exports

To bring down Net

Debt/EBITDA

< 4X

Going Forward: Prime Focus in FY15

Copyright @ 2014 Jindal Steel & Power Limited 94

Making Sustainability a Focus Priority

Copyright @ 2014 Jindal Steel & Power Limited 95

9 PILLARS OF CSR

A Responsible Corporate Citizen

Copyright @ 2014 Jindal Steel & Power Limited 96

A Responsible Corporate Citizen

Copyright @ 2014 Jindal Steel & Power Limited 97

2014 Shrishti Global Award -2014 Global HR Excellence Award-2014

2013 International Safety Award with merit 2014 by British Safety Council, UK. World CSR Congress Award 2013 Greentech CSR Award 2013

2012 Golden Peacock National CSR Award 2012

2011

Ranked No.1 as Wealth Creator in India over a 10- year period (Business World)

Awarded the Dun & Bradstreet- Rolta Corporate Awards 2011

Ranked 3rd in the Metals Category of Business World’s India’s Most Respected Companies Survey

Received the Forbes Asia’s ‘Fabulous 50’ International Award

Golden Peacock Innovation Management Awards

Greentech Award for 1st Position in Metal & Mining Industries

World HRD Congress CSR Award on women empowerment

2010

Rated the World’s 2nd Largest Value Creator by Boston Consulting Group (BCG), based on Total Shareholder Return from 2005-2009, and the largest Value Creator in Mining and Materials category

Received the Forbes Asia’s ‘Fabulous 50’ International Award

Golden Peacock Innovation Management Awards

CSR Excellence Award 2010 by ASSOCHAM for promoting and propagating Corporate Social Responsibility initiatives

2009

Received the CNBC’s Most Promising Entrant into the Big League at IBLA

National Energy Conservation Award

Golden Peacock Innovation Award 2009

Winner of ‘Shrishti Green Cube Award 2009

SAIL HR Excellence Award 2009

Award and Accolades

Copyright @ 2014 Jindal Steel & Power Limited 98

SAFETY INDUCTION ON-THE-JOB SAFETY TRAINING

SAFETY REVIEWS SAFETY AUDITS / INSPECTIONS

Health & Safety Best Practices

Copyright @ 2014 Jindal Steel & Power Limited 99

TOOL BOX MEETINGS SAFETY AWARDS/REWARDS

MEDICAL EXAMINATIONS/ WORLD CLASS PPEs MOCK DRILLS

Health & Safety Best Practices

Copyright @ 2014 Jindal Steel & Power Limited 100

Copyright @ 2014 Jindal Steel & Power Limited 101

Raigarh Blast Furnace - I

Copyright @ 2014 Jindal Steel & Power Limited 102

Angul - Coal Gasification Plant

Copyright @ 2014 Jindal Steel & Power Limited 103

Angul - DRI

Copyright @ 2014 Jindal Steel & Power Limited 104

Angul – Steel Melting Shop (SMS)

Copyright @ 2014 Jindal Steel & Power Limited 105

Angul – Plate Mill

Copyright @ 2014 Jindal Steel & Power Limited 106

Angul – 6 x 135 MW Captive Power Plant

Copyright @ 2014 Jindal Steel & Power Limited 107

Angul – 6 x 135 MW Captive Power Plant

Copyright @ 2014 Jindal Steel & Power Limited 108

SMS - Jindal Shadeed, Oman

Copyright @ 2014 Jindal Steel & Power Limited 109

Jindal Shadeed, Oman

Copyright @ 2014 Jindal Steel & Power Limited 110

Rolling Mill Under Construction : Jindal Shadeed,

Oman

Copyright @ 2014 Jindal Steel & Power Limited 111

Barbil Pellet Plant

Copyright @ 2014 Jindal Steel & Power Limited 112

Marketing Network

Copyright @ 2014 Jindal Steel & Power Limited 113

D.Balasubramanyam Head of Investor Relations Tel: 011-26739109, Mobile: 8130755166 Email: [email protected]

Ms. Pallavi Kumari Investor Relations Tel: 011-26739165, Mobile: 8800094171 Email: [email protected]

For any information please contact : -

Copyright @ 2014 Jindal Steel & Power Limited 114

Thank You