Embed Size (px)

Citation preview

Copyright © 2010 Jindal Steel & Power Ltd.

Jindal Steel and Power LtdJune 2011

Disclaimer

Certain statements in the presentations and, if applicable, the subsequent question and answer session and

discussions concerning our future growth prospects, are forward looking statements which involve a number of risks,

uncertainties and other factors that may cause our actual results, performance or achievements to differ materially

from future results, performance or achievements expressed or implied by such forward-looking statements. The

risks and uncertainties relating to these statements include, but are not limited to, general political, social and

economic conditions in India, Bolivia, and elsewhere, accidents, natural disasters or outbreaks of disease,

government policies regarding the steel ,power and diamond industry(ies), including industrial licensing,

environmental regulations, safety regulations, import restrictions and duties, excise duties and sales taxes, our

ability to successfully implement our strategy, our growth and expansion plans and technological changes,

increasing competition in, and the conditions of the global and Indian steel , power and diamond industry, changes

in laws and regulations that apply to the Indian and global steel, power and diamond industry, significant

movements in the prices of key materials, terms on which we finance our working capital and capital and product

requirements affecting our company and our industry and other development expenditure requirements, general

economic conditions factors beyond our control.

2

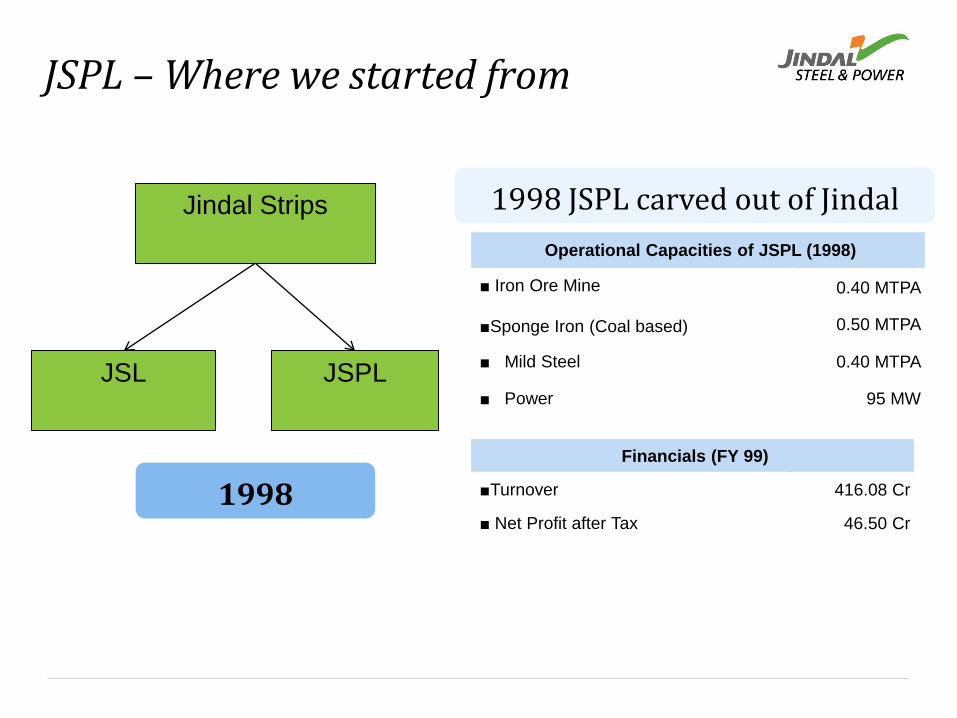

JSPL – Where we started from

1998 JSPL carved out of Jindal

Strips

1998

Financials (FY 99)

■Turnover 416.08 Cr

■ Net Profit after Tax 46.50 Cr

Jindal Strips

JSL JSPL

Operational Capacities of JSPL (1998)

■ Iron Ore Mine

■Sponge Iron (Coal based)

0.40 MTPA

0.50 MTPA

■ Mild Steel 0.40 MTPA

■ Power 95 MW

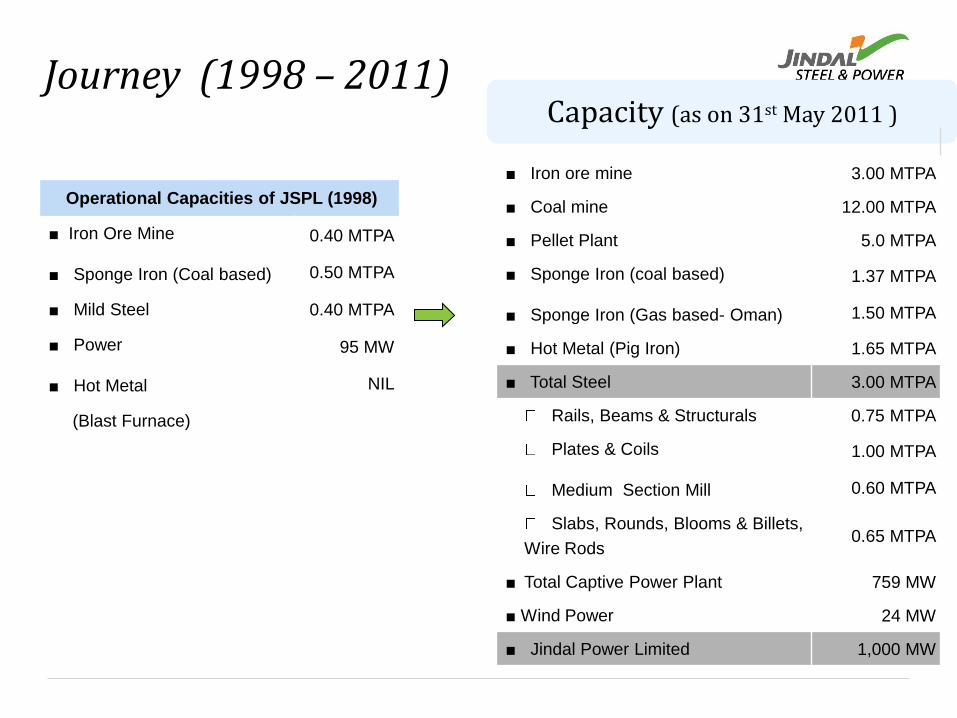

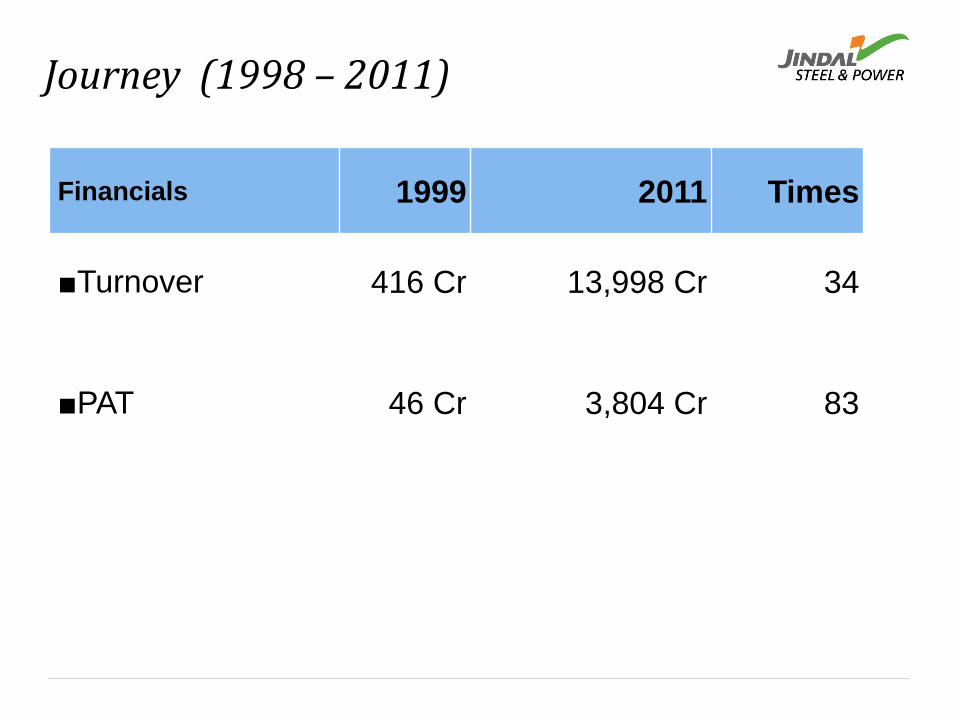

Journey (1998 – 2011)Capacity (as on 31st May 2011 )

Operational Capacities of JSPL (1998)

■ Iron Ore Mine

■ Sponge Iron (Coal based)

0.40 MTPA

0.50 MTPA

■ Mild Steel 0.40 MTPA

■ Power

■ Hot Metal

95 MW

NIL

(Blast Furnace)

■ Iron ore mine 3.00 MTPA

■ Coal mine 12.00 MTPA

■ Pellet Plant 5.0 MTPA

■ Sponge Iron (coal based)

■ Sponge Iron (Gas based- Oman)

1.37 MTPA

1.50 MTPA

■ Hot Metal (Pig Iron) 1.65 MTPA

■ Total Steel 3.00 MTPA

Rails, Beams & Structurals 0.75 MTPA

Plates & Coils

Medium Section Mill

1.00 MTPA

0.60 MTPA

Slabs, Rounds, Blooms & Billets,

Wire Rods0.65 MTPA

■ Total Captive Power Plant 759 MW

■ Wind Power 24 MW

■ Jindal Power Limited 1,000 MW

Journey (1998 – 2011)

Financials 1999 2011 Times

■Turnover 416 Cr 13,998 Cr 34

■PAT 46 Cr 3,804 Cr 83

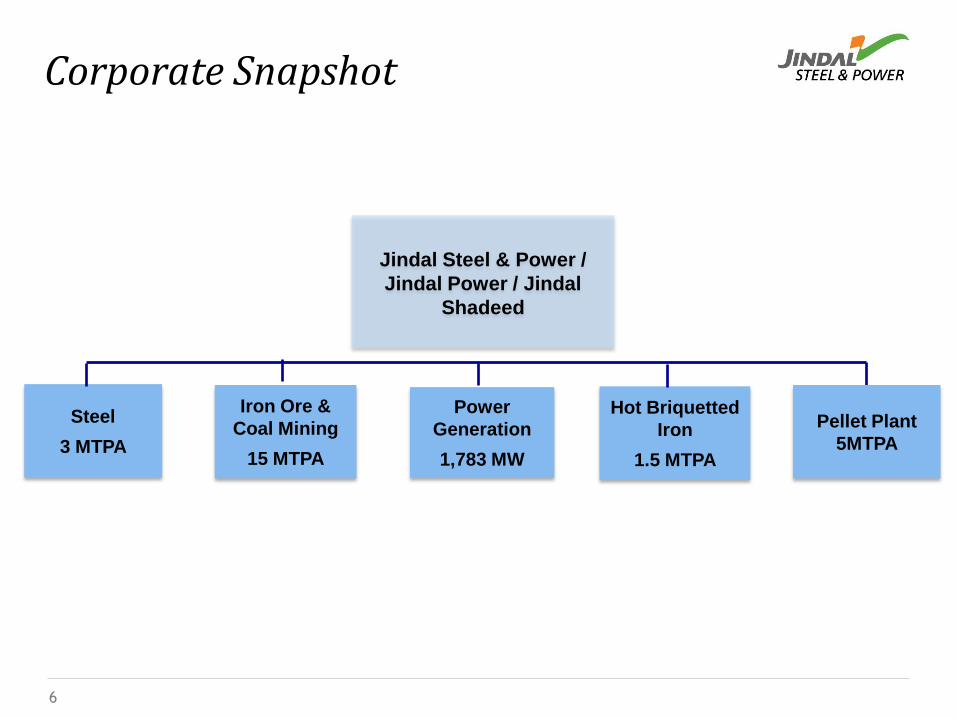

Jindal Steel & Power /

Jindal Power / Jindal

Shadeed

Steel

3 MTPA

Power

Generation

1,783 MW

Pellet Plant

5MTPA

Iron Ore &

Coal Mining

15 MTPA

Hot Briquetted

Iron

1.5 MTPA

Corporate Snapshot

6

7

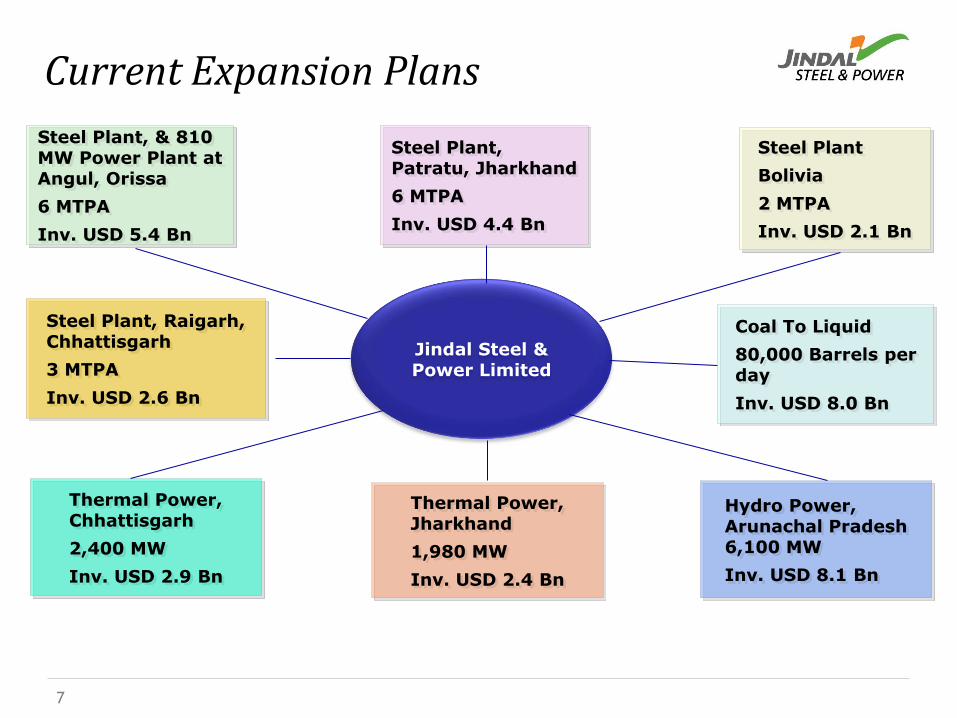

Jindal Steel & Power Limited

Steel Plant, & 810 MW Power Plant at Angul, Orissa

6 MTPA

Inv. USD 5.4 Bn

Steel Plant, Patratu, Jharkhand

6 MTPA

Inv. USD 4.4 Bn

Steel Plant

Bolivia

2 MTPA

Inv. USD 2.1 Bn

Thermal Power, Chhattisgarh

2,400 MW

Inv. USD 2.9 Bn

Thermal Power, Jharkhand

1,980 MW

Inv. USD 2.4 Bn

Hydro Power, Arunachal Pradesh 6,100 MW

Inv. USD 8.1 Bn

Steel Plant, Raigarh, Chhattisgarh

3 MTPA

Inv. USD 2.6 Bn

Coal To Liquid

80,000 Barrels per day

Inv. USD 8.0 Bn

Current Expansion Plans

Steel business overview

Power business overview

Financial overview

Growth drivers

Sustainability Initiatives

8

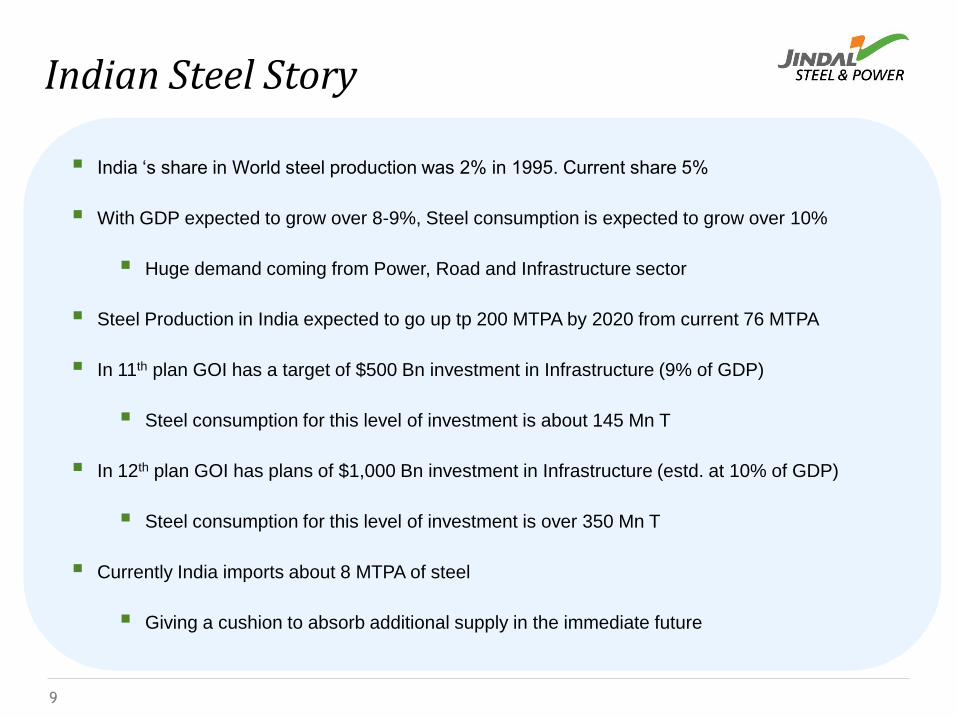

Indian Steel Story

India „s share in World steel production was 2% in 1995. Current share 5%

With GDP expected to grow over 8-9%, Steel consumption is expected to grow over 10%

Huge demand coming from Power, Road and Infrastructure sector

Steel Production in India expected to go up tp 200 MTPA by 2020 from current 76 MTPA

In 11th plan GOI has a target of $500 Bn investment in Infrastructure (9% of GDP)

Steel consumption for this level of investment is about 145 Mn T

In 12th plan GOI has plans of $1,000 Bn investment in Infrastructure (estd. at 10% of GDP)

Steel consumption for this level of investment is over 350 Mn T

Currently India imports about 8 MTPA of steel

Giving a cushion to absorb additional supply in the immediate future

9

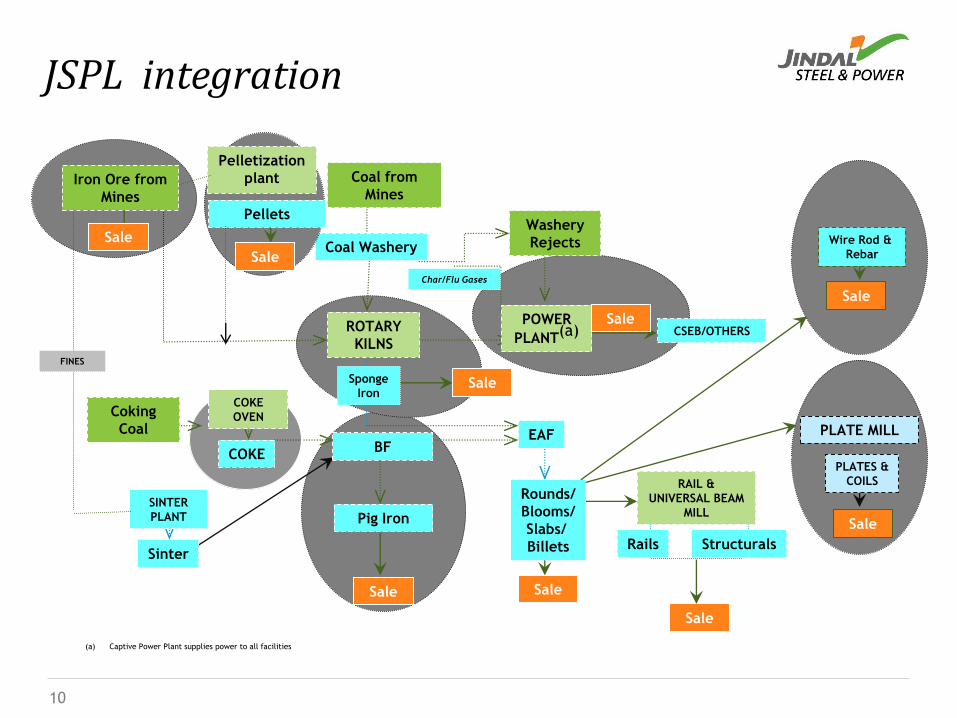

(a) Captive Power Plant supplies power to all facilities

JSPL integration

Sale

FINES

Iron Ore from

Mines

Coal from

Mines

Coal Washery

BF

Coking

Coal

Pig Iron

POWER

PLANT(a) CSEB/OTHERS

EAF

RAIL &

UNIVERSAL BEAM

MILL

ROTARY

KILNS

Rails Structurals

Washery

Rejects

Sponge

Iron

Char/Flu Gases

Rounds/

Blooms/

Slabs/

Billets

Sale

Sale

Sale

Sale

Sale

SINTER

PLANT

PLATE MILL

PLATES &

COILS

Sinter

COKE

OVEN

COKE

Sale

Wire Rod &

Rebar

Pellets

Sale

Pelletization

plant

Sale

10

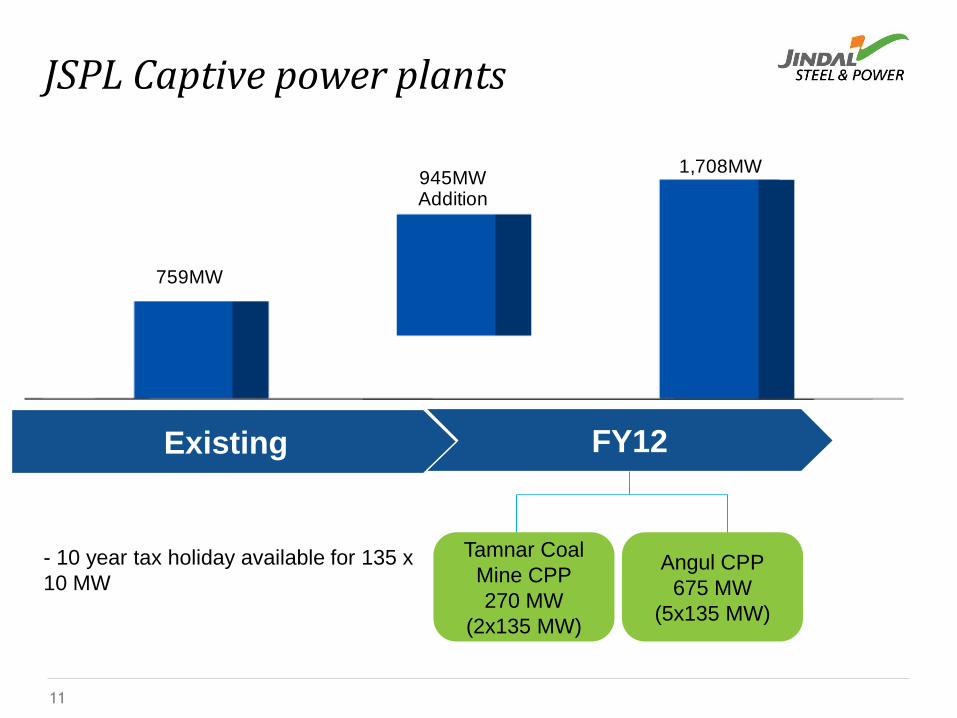

JSPL Captive power plants

759MW

945MWAddition

1,708MW

FY12

Angul CPP

675 MW

(5x135 MW)

Existing

11

Tamnar Coal

Mine CPP

270 MW

(2x135 MW)

- 10 year tax holiday available for 135 x

10 MW

Steel business overview

Power business overview

Financial overview

Growth drivers

Sustainability Initiatives

12

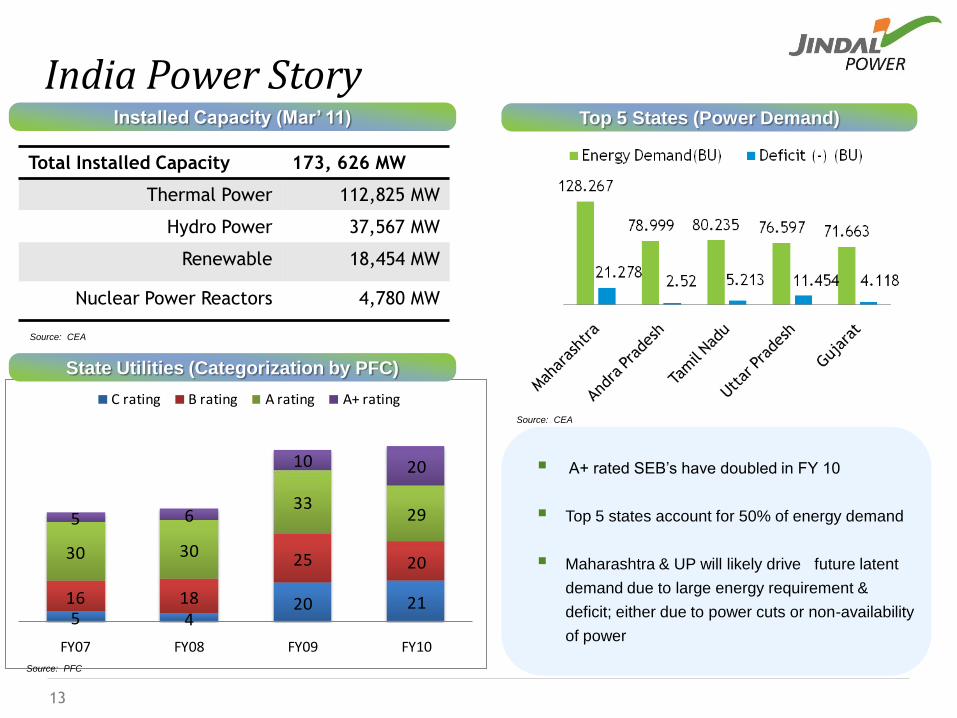

India Power Story

13

Installed Capacity (Mar’ 11) Top 5 States (Power Demand)

Source: CEA

Source: CEA

A+ rated SEB‟s have doubled in FY 10

Top 5 states account for 50% of energy demand

Maharashtra & UP will likely drive future latent

demand due to large energy requirement &

deficit; either due to power cuts or non-availability

of power

Total Installed Capacity 173, 626 MW

Thermal Power 112,825 MW

Hydro Power 37,567 MW

Renewable 18,454 MW

Nuclear Power Reactors 4,780 MW

5 420 2116 18

25 2030 30

33295 6

10 20

FY07 FY08 FY09 FY10

C rating B rating A rating A+ rating

Source: PFC

State Utilities (Categorization by PFC)

Location

Fuel

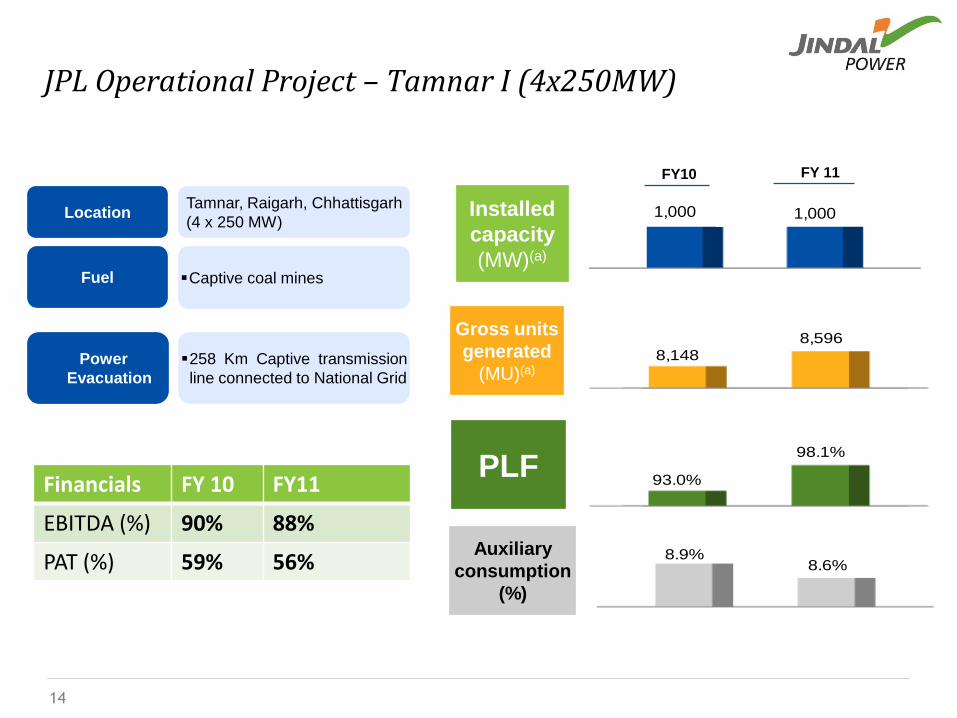

JPL Operational Project – Tamnar I (4x250MW)

Tamnar, Raigarh, Chhattisgarh

(4 x 250 MW)

Captive coal mines

Power

Evacuation

258 Km Captive transmission

line connected to National Grid

14

FY10

Installed

capacity

(MW)(a)

1,000 1,000

Gross units

generated

(MU)(a)8,148

8,596

PLF93.0%

98.1%

Auxiliary

consumption

(%)

8.9%8.6%

FY 11

Financials FY 10 FY11

EBITDA (%) 90% 88%

PAT (%) 59% 56%

15

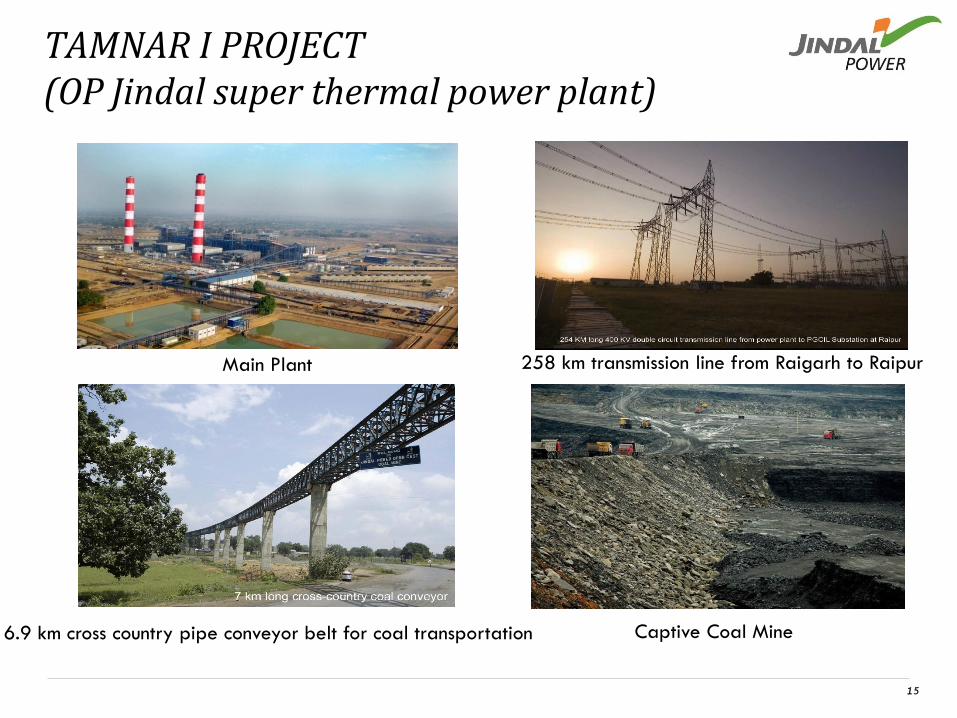

TAMNAR I PROJECT (OP Jindal super thermal power plant)

Main Plant 258 km transmission line from Raigarh to Raipur

6.9 km cross country pipe conveyor belt for coal transportation Captive Coal Mine

Steel business overview

Power business overview

Financial overview

Growth drivers

Sustainability Initiatives

16

0

500

1000

1500

2000

2500

3000

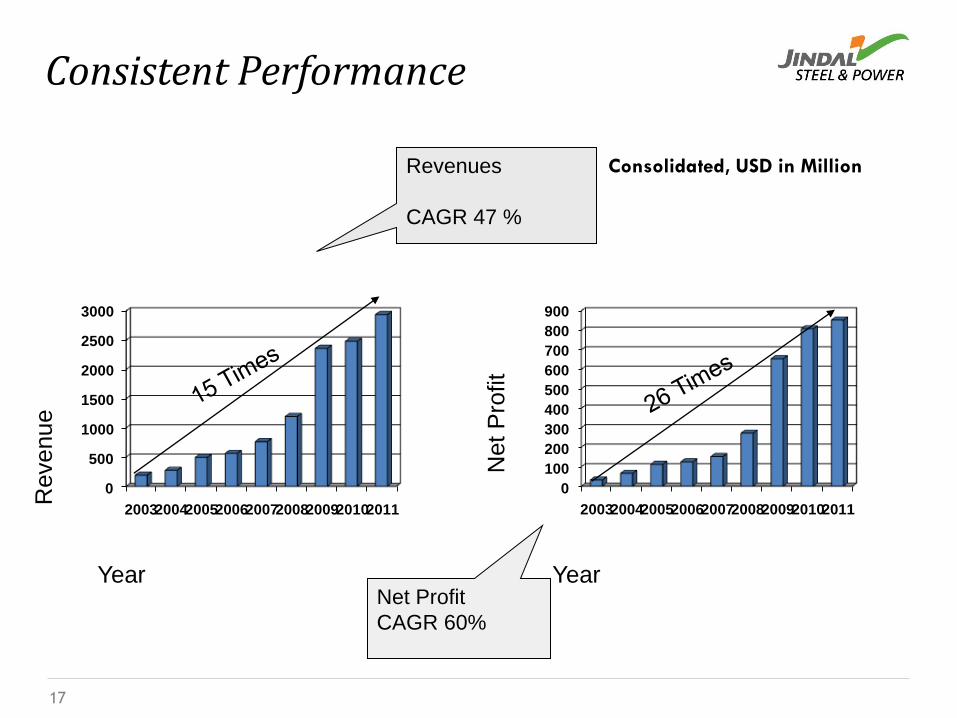

200320042005200620072008200920102011

0

100

200

300

400

500

600

700

800

900

200320042005200620072008200920102011

Year

Revenue

Revenues

CAGR 47 %

Year

Net P

rofit

Net Profit

CAGR 60%

Consolidated, USD in Million

Consistent Performance

17

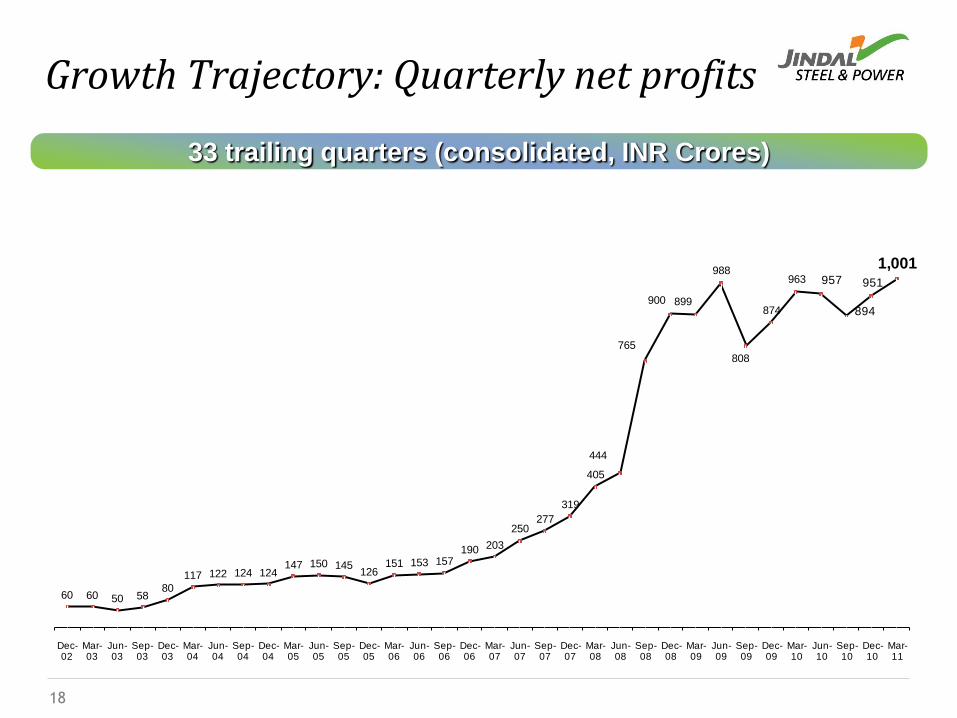

Growth Trajectory: Quarterly net profits

33 trailing quarters (consolidated, INR Crores)

60 60 50 5880

117 122 124 124147 150 145

126151 153 157

190 203

250277

319

405

444

765

900 899

988

808

874

963 957

894

951

1,001

Dec-02

Mar-03

Jun-03

Sep-03

Dec-03

Mar-04

Jun-04

Sep-04

Dec-04

Mar-05

Jun-05

Sep-05

Dec-05

Mar-06

Jun-06

Sep-06

Dec-06

Mar-07

Jun-07

Sep-07

Dec-07

Mar-08

Jun-08

Sep-08

Dec-08

Mar-09

Jun-09

Sep-09

Dec-09

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

18

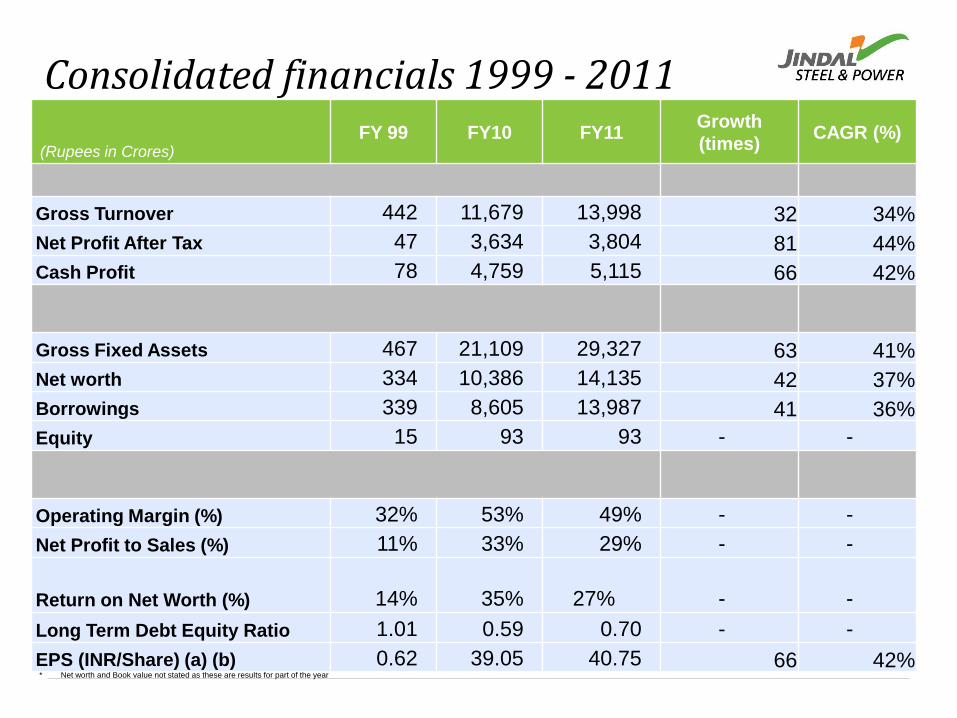

Consolidated financials 1999 - 2011

Note: EPS adjusted to reflect a 1:5 stock split w.e.f 27 Dec,07

Note: EPS adjusted to reflect a bonus issue of 5:1

* Net worth and Book value not stated as these are results for part of the year

(Rupees in Crores)FY 99 FY10 FY11

Growth

(times)CAGR (%)

Gross Turnover 442 11,679 13,998 32 34%

Net Profit After Tax 47 3,634 3,804 81 44%

Cash Profit 78 4,759 5,115 66 42%

Gross Fixed Assets 467 21,109 29,327 63 41%

Net worth 334 10,386 14,135 42 37%

Borrowings 339 8,605 13,987 41 36%

Equity 15 93 93 - -

Operating Margin (%) 32% 53% 49% - -

Net Profit to Sales (%) 11% 33% 29% - -

Return on Net Worth (%) 14% 35% 27% - -

Long Term Debt Equity Ratio 1.01 0.59 0.70 - -

EPS (INR/Share) (a) (b) 0.62 39.05 40.75 66 42%

Steel business overview

Power business overview

Financial overview

Growth drivers

Sustainability Initiatives

20

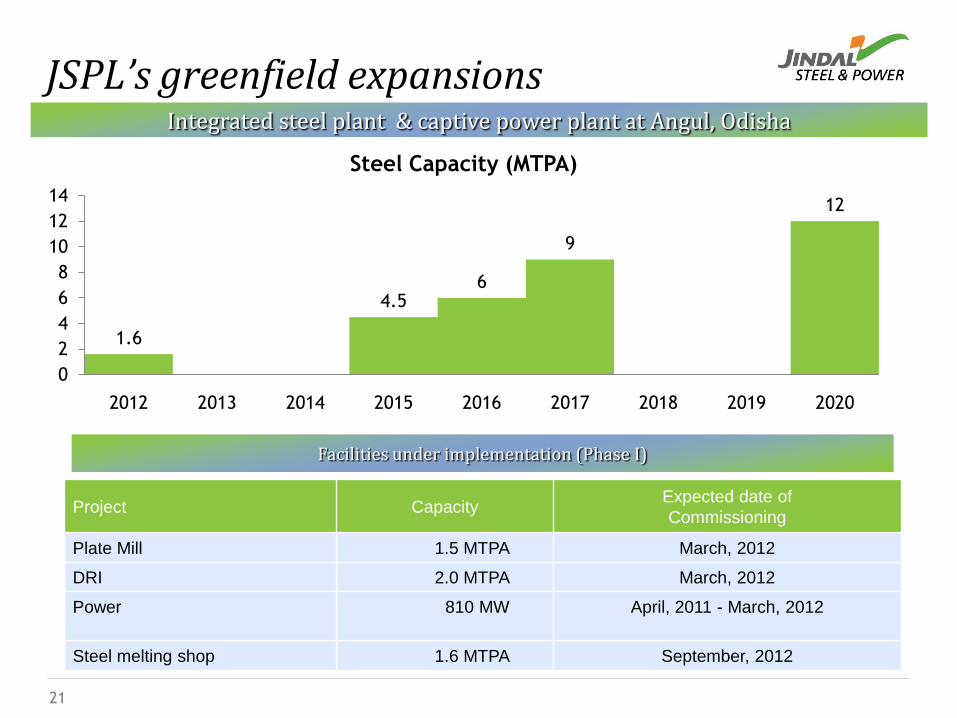

Project CapacityExpected date of

Commissioning

Plate Mill 1.5 MTPA March, 2012

DRI 2.0 MTPA March, 2012

Power 810 MW April, 2011 - March, 2012

Steel melting shop 1.6 MTPA September, 2012

Facilities under implementation (Phase I)

Integrated steel plant & captive power plant at Angul, Odisha

JSPL’s greenfield expansions

21

1.6

4.56

9

12

0

2

4

6

8

10

12

14

2012 2013 2014 2015 2016 2017 2018 2019 2020

Steel Capacity (MTPA)

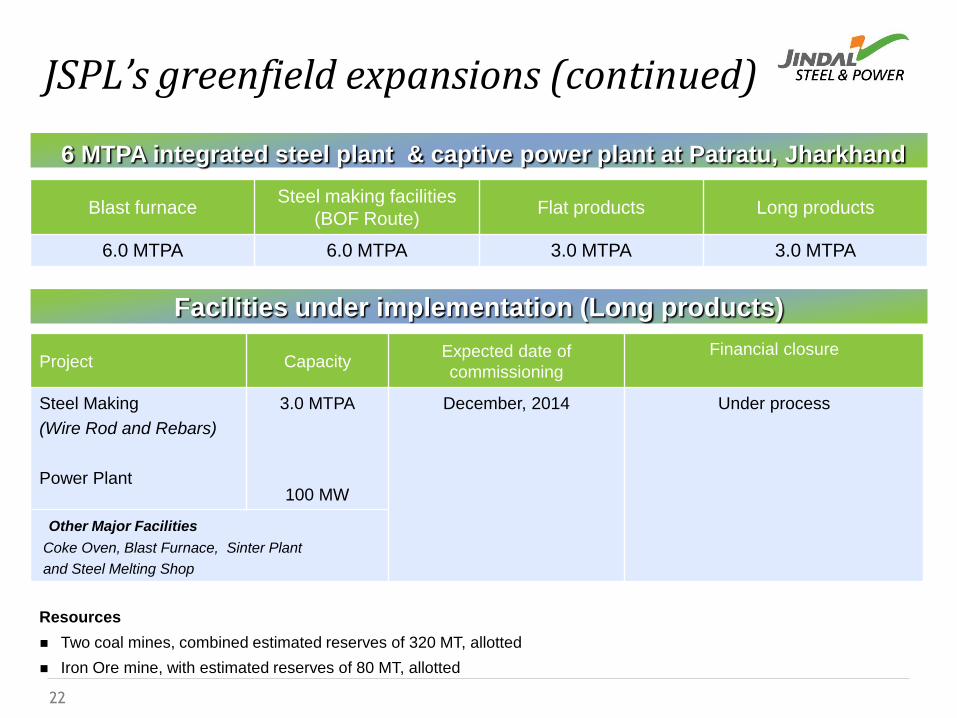

Project CapacityExpected date of

commissioning

Financial closure

Steel Making

(Wire Rod and Rebars)

Power Plant

3.0 MTPA

100 MW

December, 2014 Under process

Other Major Facilities

Coke Oven, Blast Furnace, Sinter Plant

and Steel Melting Shop

Facilities under implementation (Long products)

Resources

Two coal mines, combined estimated reserves of 320 MT, allotted

Iron Ore mine, with estimated reserves of 80 MT, allotted

Blast furnace Steel making facilities

(BOF Route)Flat products Long products

6.0 MTPA 6.0 MTPA 3.0 MTPA 3.0 MTPA

6 MTPA integrated steel plant & captive power plant at Patratu, Jharkhand

JSPL’s greenfield expansions (continued)

22

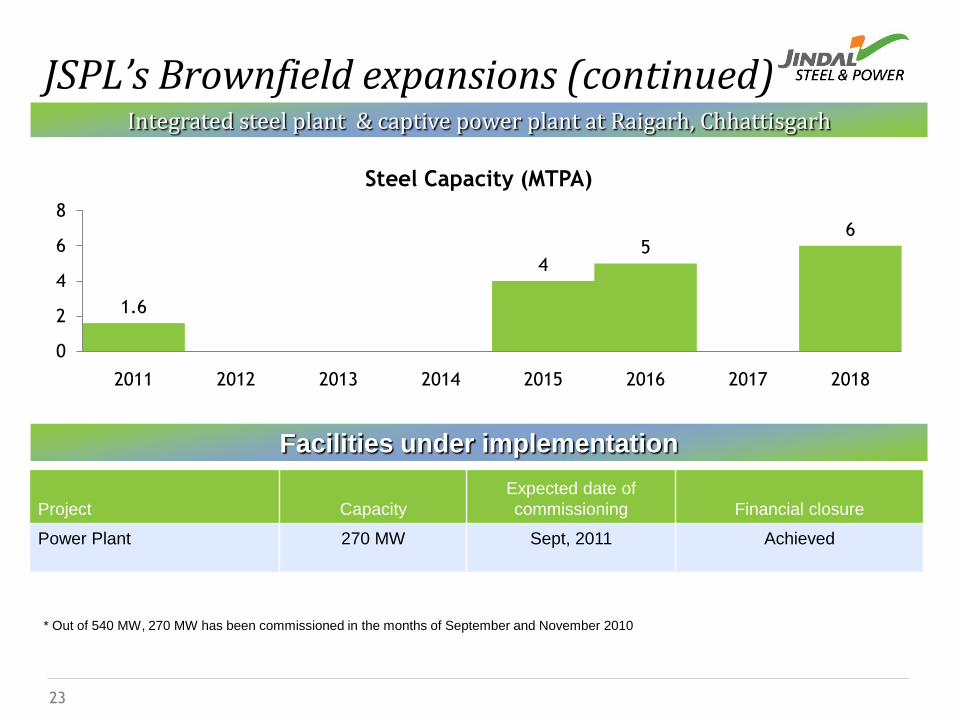

Project Capacity

Expected date of

commissioning Financial closure

Power Plant 270 MW Sept, 2011 Achieved

Facilities under implementation

JSPL’s Brownfield expansions (continued)

* Out of 540 MW, 270 MW has been commissioned in the months of September and November 2010

23

1.6

45

6

0

2

4

6

8

2011 2012 2013 2014 2015 2016 2017 2018

Steel Capacity (MTPA)

Integrated steel plant & captive power plant at Raigarh, Chhattisgarh

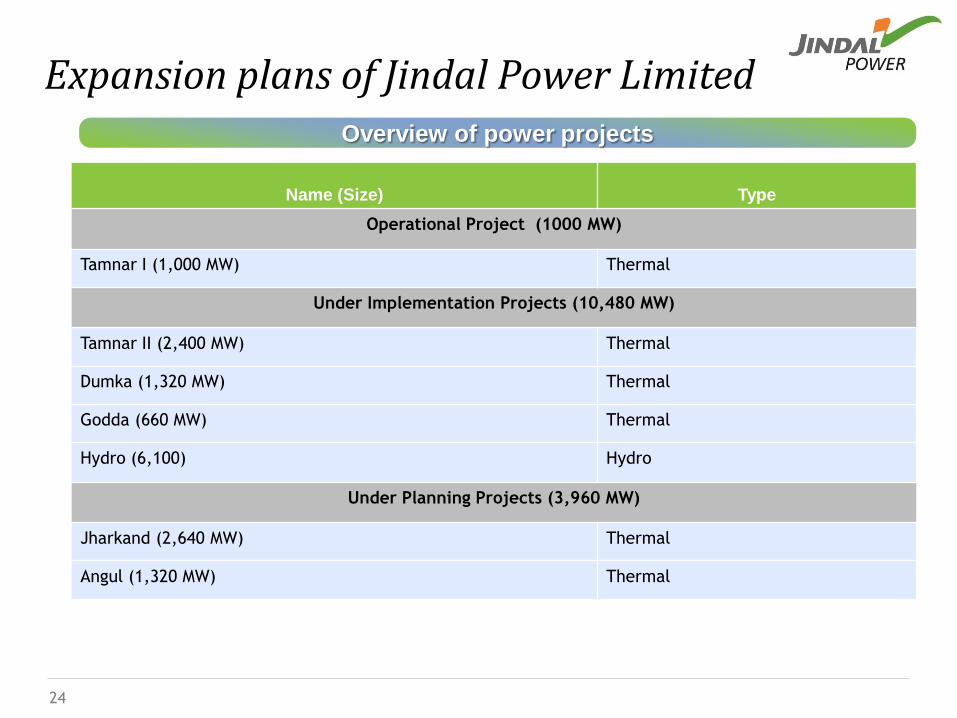

Expansion plans of Jindal Power LimitedOverview of power projects

Name (Size) Type

Operational Project (1000 MW)

Tamnar I (1,000 MW) Thermal

Under Implementation Projects (10,480 MW)

Tamnar II (2,400 MW) Thermal

Dumka (1,320 MW) Thermal

Godda (660 MW) Thermal

Hydro (6,100) Hydro

Under Planning Projects (3,960 MW)

Jharkand (2,640 MW) Thermal

Angul (1,320 MW) Thermal

24

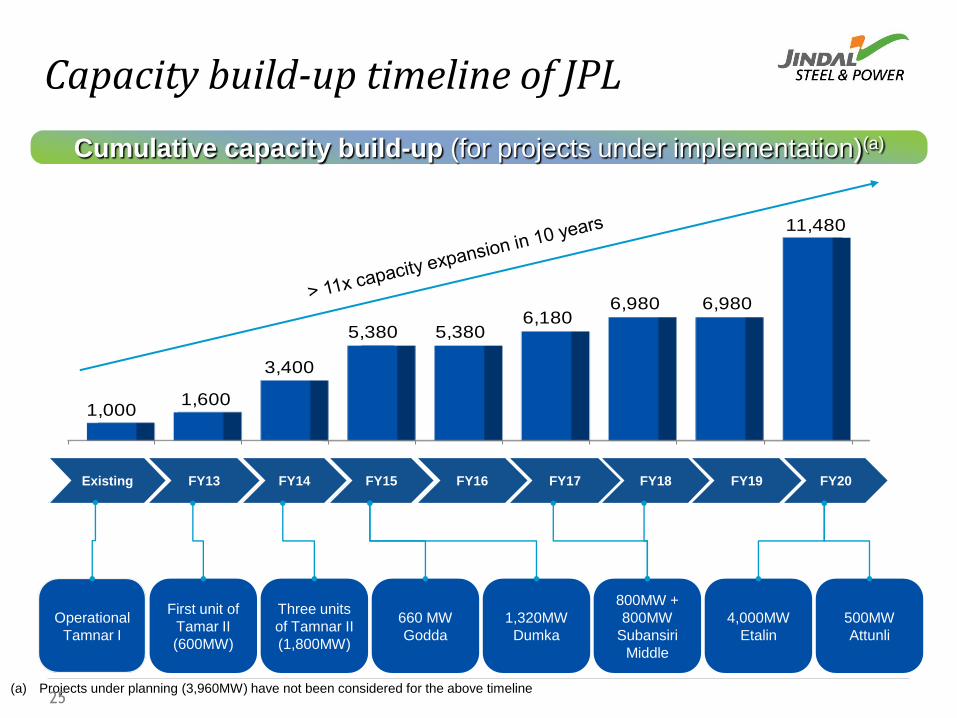

Capacity build-up timeline of JPL

Cumulative capacity build-up (for projects under implementation)(a)

1,0001,600

3,400

5,380 5,3806,180

6,980 6,980

11,480

FY14 FY15 FY16 FY17 FY18 FY19 FY20Existing

500MW

Attunli

660 MW

Godda

1,320MW

Dumka

4,000MW

Etalin

800MW +

800MW

Subansiri

Middle

Three units

of Tamnar II

(1,800MW)

Operational

Tamnar I

FY13

First unit of

Tamar II

(600MW)

(a) Projects under planning (3,960MW) have not been considered for the above timeline25

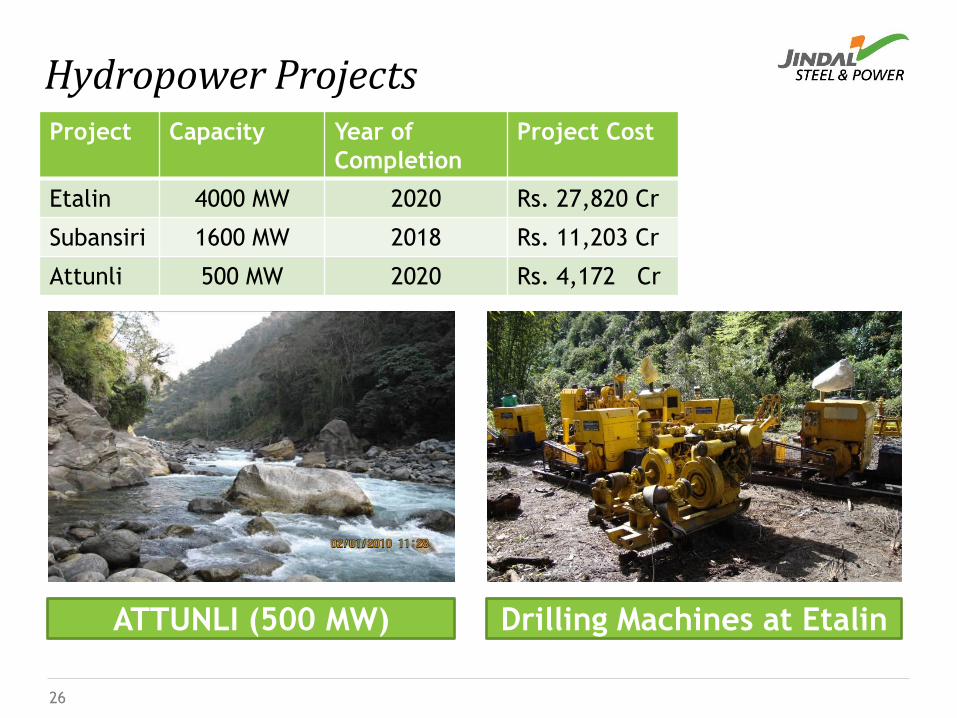

26

Hydropower ProjectsProject Capacity Year of

Completion

Project Cost

Etalin 4000 MW 2020 Rs. 27,820 Cr

Subansiri 1600 MW 2018 Rs. 11,203 Cr

Attunli 500 MW 2020 Rs. 4,172 Cr

ATTUNLI (500 MW) Drilling Machines at Etalin

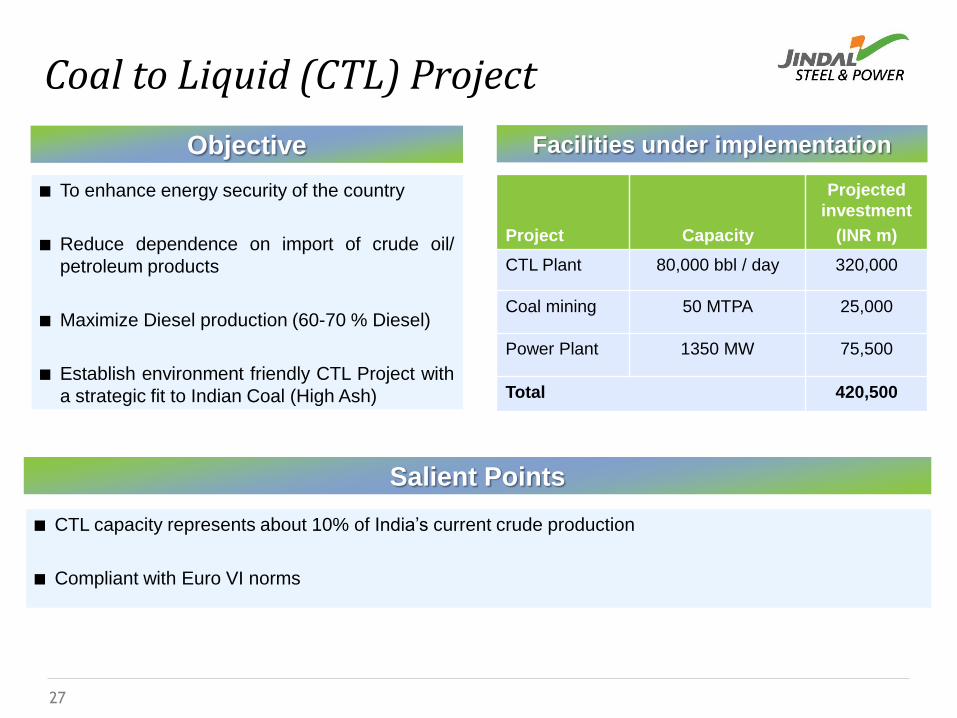

Project Capacity

Projected

investment

(INR m)

CTL Plant 80,000 bbl / day 320,000

Coal mining 50 MTPA 25,000

Power Plant 1350 MW 75,500

Total 420,500

Facilities under implementation

Coal to Liquid (CTL) Project

Objective

■ To enhance energy security of the country

■ Reduce dependence on import of crude oil/

petroleum products

■ Maximize Diesel production (60-70 % Diesel)

■ Establish environment friendly CTL Project with

a strategic fit to Indian Coal (High Ash)

27

■ CTL capacity represents about 10% of India‟s current crude production

■ Compliant with Euro VI norms

Salient Points

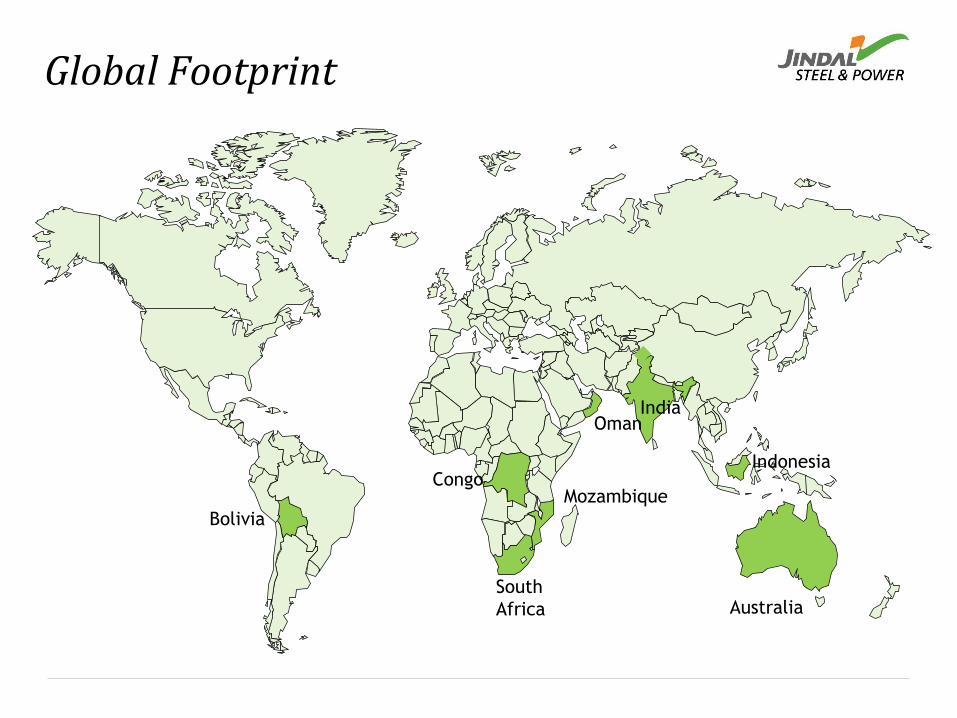

IndiaOman

Bolivia

South

Africa

Mozambique

IndonesiaCongo

Global Footprint

Georgia Australia

29

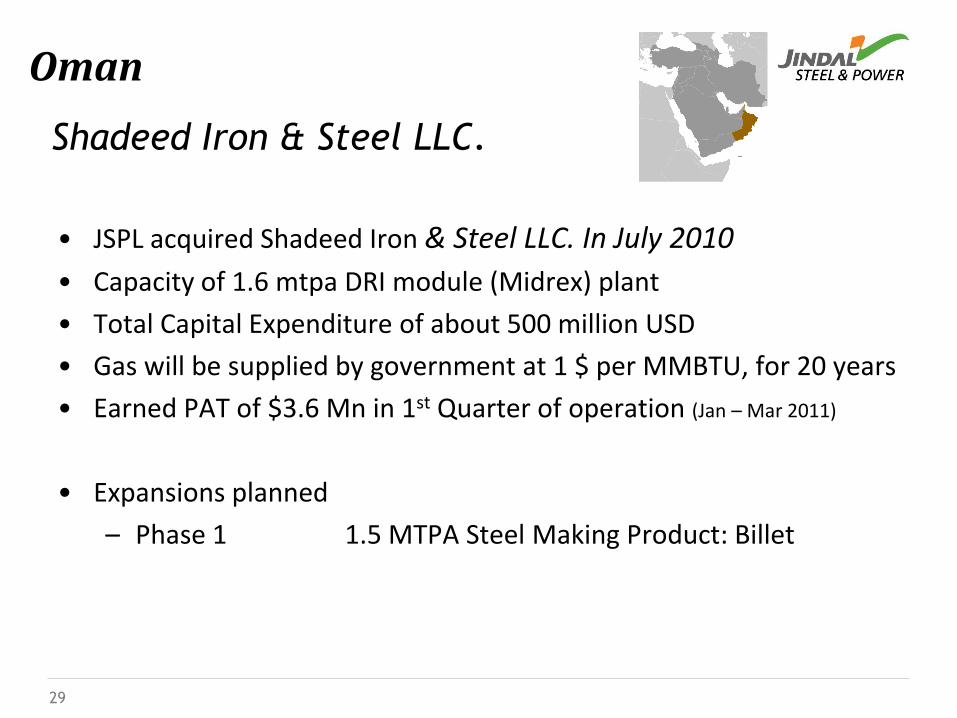

Oman

• JSPL acquired Shadeed Iron & Steel LLC. In July 2010

• Capacity of 1.6 mtpa DRI module (Midrex) plant

• Total Capital Expenditure of about 500 million USD

• Gas will be supplied by government at 1 $ per MMBTU, for 20 years

• Earned PAT of $3.6 Mn in 1st Quarter of operation (Jan – Mar 2011)

• Expansions planned

– Phase 1 1.5 MTPA Steel Making Product: Billet

Shadeed Iron & Steel LLC.

30

Oman

31

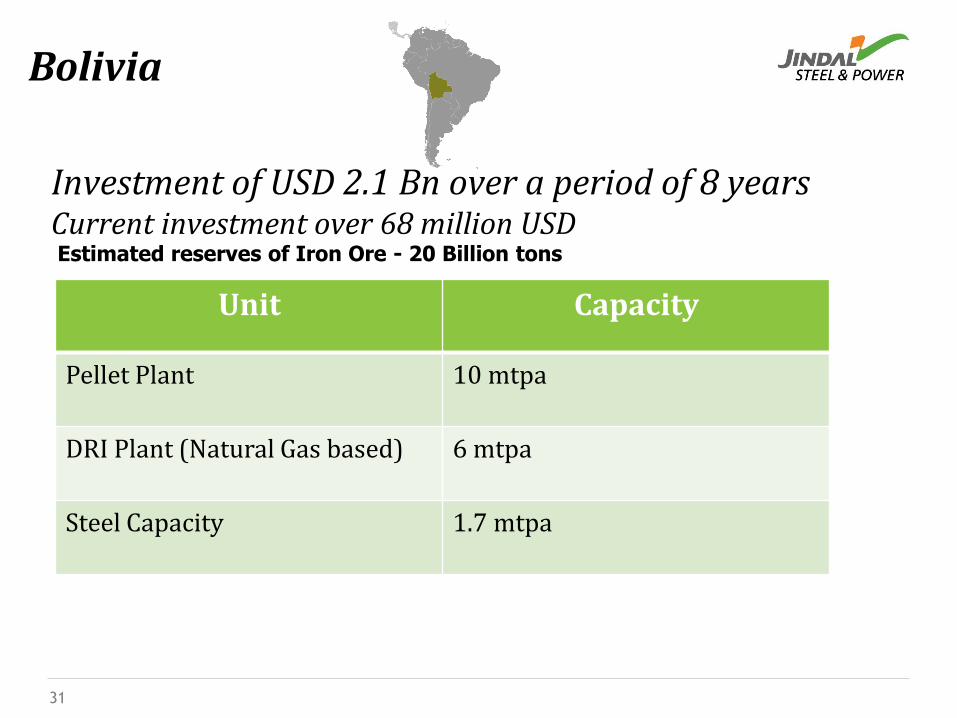

Bolivia

Estimated reserves of Iron Ore - 20 Billion tons

Investment of USD 2.1 Bn over a period of 8 yearsCurrent investment over 68 million USD

Unit Capacity

Pellet Plant 10 mtpa

DRI Plant (Natural Gas based) 6 mtpa

Steel Capacity 1.7 mtpa

32

AFRICA- SOUTH AFRICA

• Coal Mine in Piet Retief, Mpumalanga

• 20 MT mineable coal (Anthracite & Lean Bituminous)

• Calorific Value 6,800 Kcal / kg, Ash 16% -18%

• Mining started in December 2009

• Annual Products 1 MTPA

• Current Market Price US $ 110 ex. Mine

• Distance covered from Mine to Richards Bay Port- 320 km

33

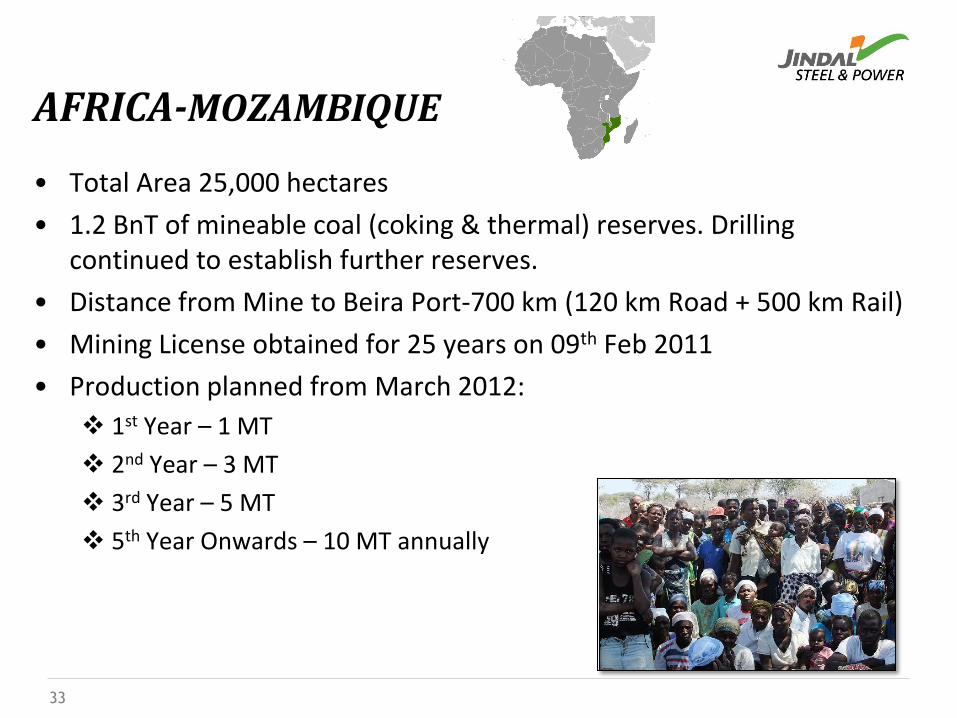

AFRICA-MOZAMBIQUE

• Total Area 25,000 hectares

• 1.2 BnT of mineable coal (coking & thermal) reserves. Drilling continued to establish further reserves.

• Distance from Mine to Beira Port-700 km (120 km Road + 500 km Rail)

• Mining License obtained for 25 years on 09th Feb 2011

• Production planned from March 2012:

1st Year – 1 MT

2nd Year – 3 MT

3rd Year – 5 MT

5th Year Onwards – 10 MT annually

34

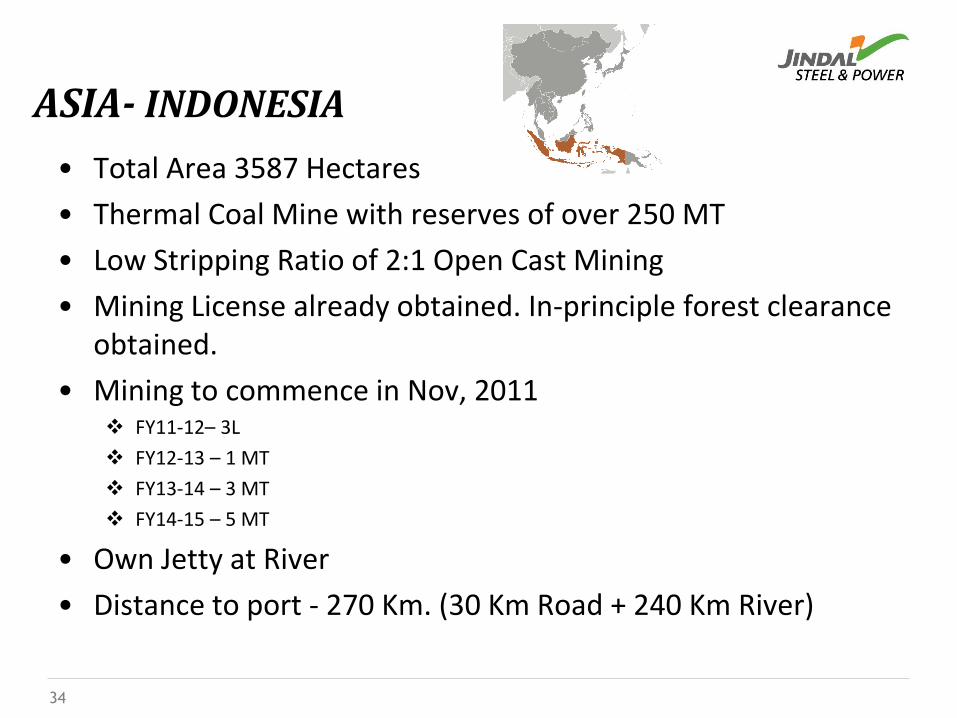

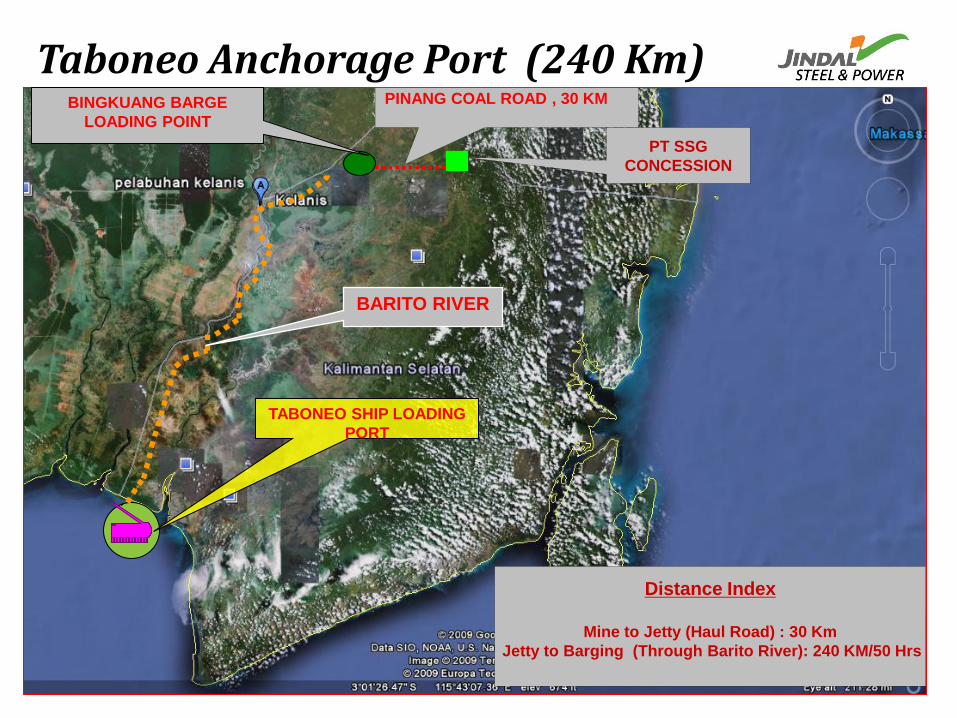

ASIA- INDONESIA

• Total Area 3587 Hectares

• Thermal Coal Mine with reserves of over 250 MT

• Low Stripping Ratio of 2:1 Open Cast Mining

• Mining License already obtained. In-principle forest clearance obtained.

• Mining to commence in Nov, 2011 FY11-12– 3L

FY12-13 – 1 MT

FY13-14 – 3 MT

FY14-15 – 5 MT

• Own Jetty at River

• Distance to port - 270 Km. (30 Km Road + 240 Km River)

TABONEO SHIP LOADING

PORT

BINGKUANG BARGE

LOADING POINT

BARITO RIVER

Taboneo Anchorage Port (240 Km)PINANG COAL ROAD , 30 KM

Distance Index

Mine to Jetty (Haul Road) : 30 Km

Jetty to Barging (Through Barito River): 240 KM/50 Hrs

PT SSG

CONCESSION

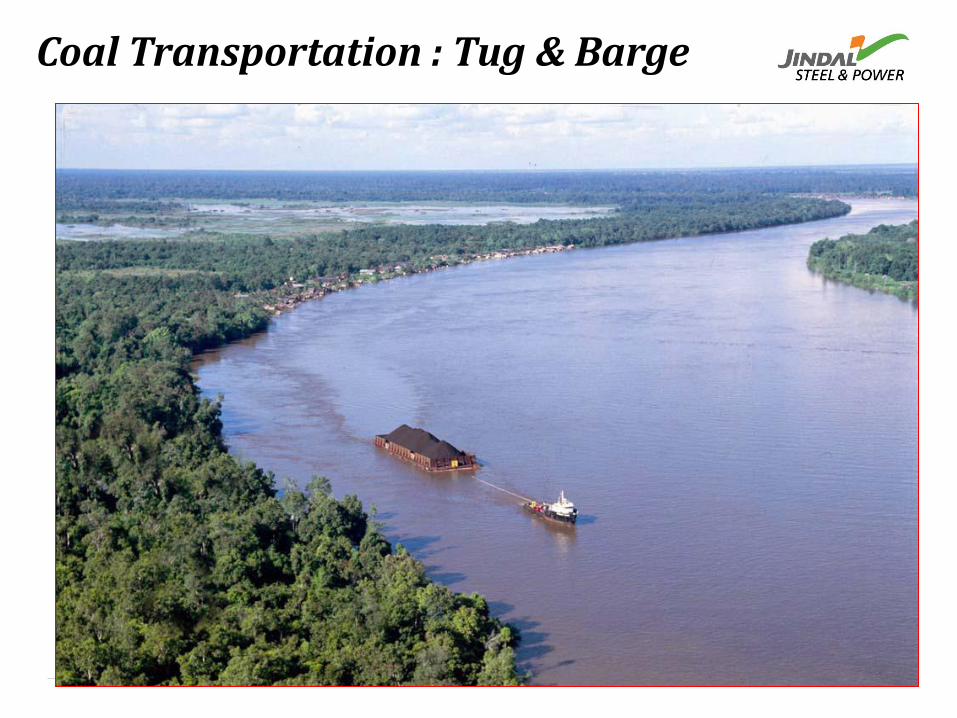

Coal Transportation : Tug & Barge

37

AUSTRALIA

• Acquired 15% stake in Rockland Richfield Ltd. - anASX Listed company having 3 Tenements

• Propose to complete acquisition in due course

• Major achievement by acquiring 3 greenfield minesfrom Govt. of Queensland - 2 Thermal Coal and 1Coking/Thermal Coal

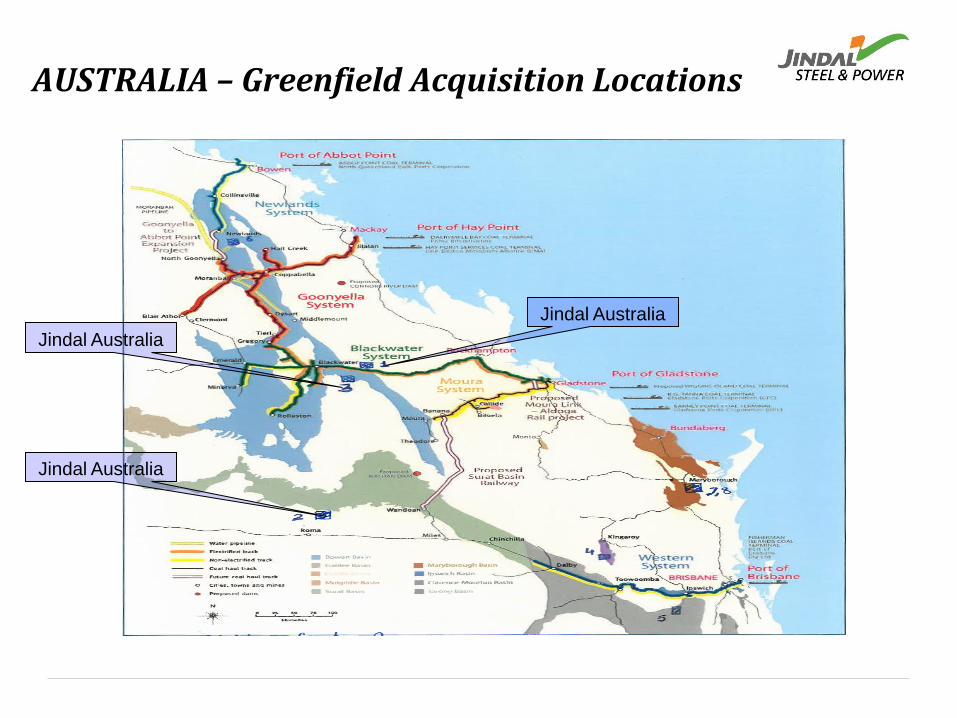

Jindal Australia

Jindal Australia

Jindal Australia

AUSTRALIA – Greenfield Acquisition Locations

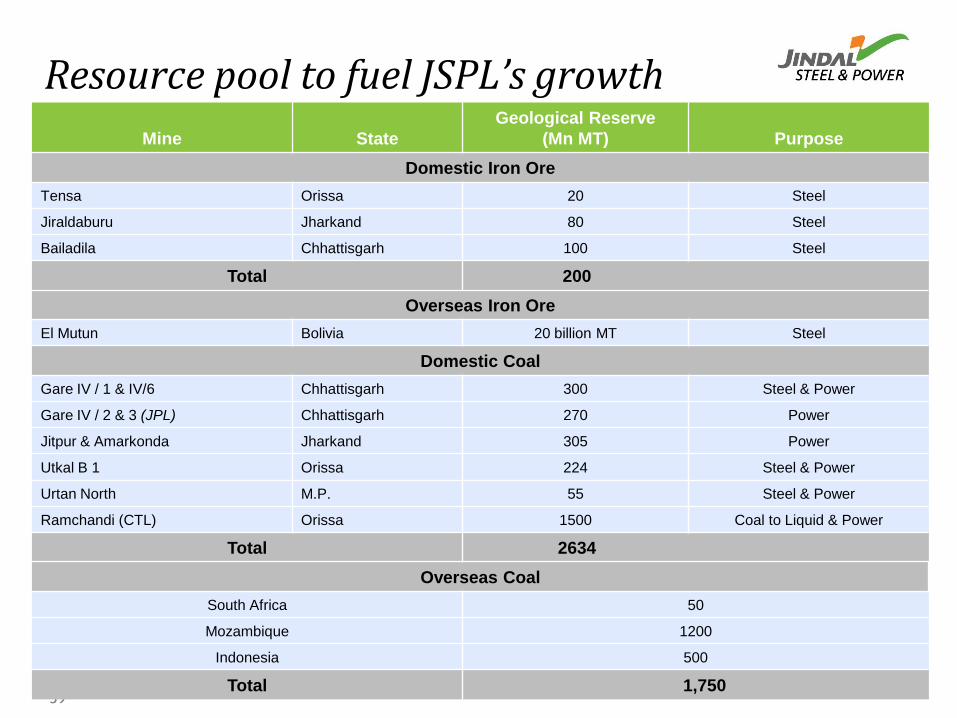

Resource pool to fuel JSPL’s growth

39

Mine State

Geological Reserve

(Mn MT) Purpose

Domestic Iron Ore

Tensa Orissa 20 Steel

Jiraldaburu Jharkand 80 Steel

Bailadila Chhattisgarh 100 Steel

Total 200

Overseas Iron Ore

El Mutun Bolivia 20 billion MT Steel

Domestic Coal

Gare IV / 1 & IV/6 Chhattisgarh 300 Steel & Power

Gare IV / 2 & 3 (JPL) Chhattisgarh 270 Power

Jitpur & Amarkonda Jharkand 305 Power

Utkal B 1 Orissa 224 Steel & Power

Urtan North M.P. 55 Steel & Power

Ramchandi (CTL) Orissa 1500 Coal to Liquid & Power

Total 2634

Overseas Coal

South Africa 50

Mozambique 1200

Indonesia 500

Total 1,750

40

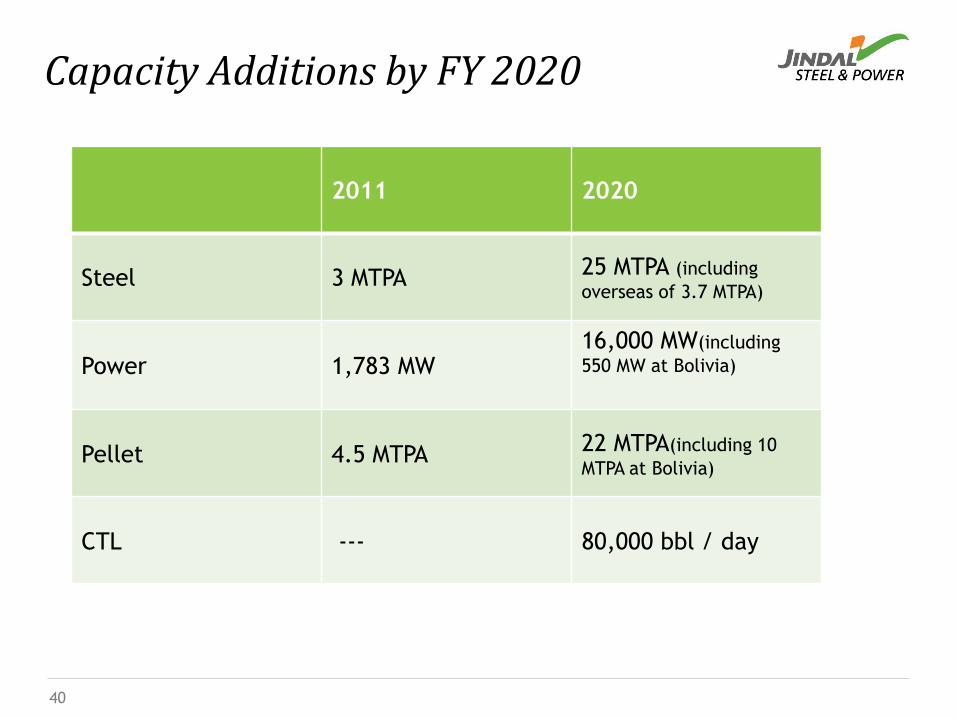

Capacity Additions by FY 2020

2011 2020

Steel 3 MTPA 25 MTPA (including

overseas of 3.7 MTPA)

Power 1,783 MW16,000 MW(including

550 MW at Bolivia)

Pellet 4.5 MTPA 22 MTPA(including 10

MTPA at Bolivia)

CTL --- 80,000 bbl / day

Steel business overview

Power business overview

Financial overview

Growth drivers

Sustainability Initiatives

41

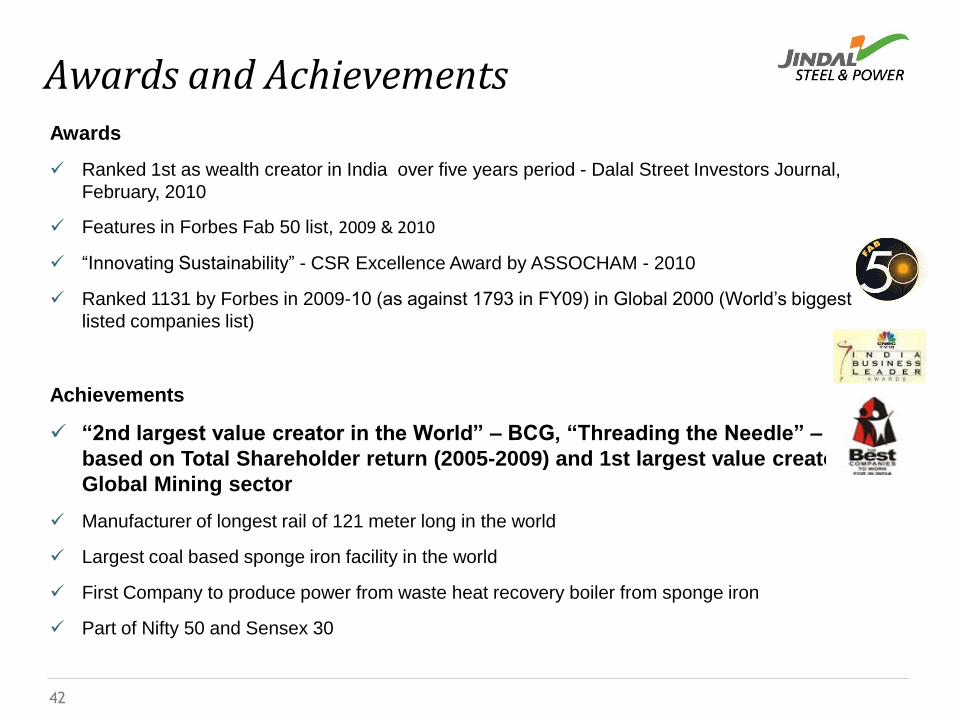

Awards

Ranked 1st as wealth creator in India over five years period - Dalal Street Investors Journal,

February, 2010

Features in Forbes Fab 50 list, 2009 & 2010

“Innovating Sustainability” - CSR Excellence Award by ASSOCHAM - 2010

Ranked 1131 by Forbes in 2009-10 (as against 1793 in FY09) in Global 2000 (World‟s biggest

listed companies list)

Achievements

“2nd largest value creator in the World” – BCG, “Threading the Needle” – 2010

based on Total Shareholder return (2005-2009) and 1st largest value creator in

Global Mining sector

Manufacturer of longest rail of 121 meter long in the world

Largest coal based sponge iron facility in the world

First Company to produce power from waste heat recovery boiler from sponge iron

Part of Nifty 50 and Sensex 30

Awards and Achievements

42

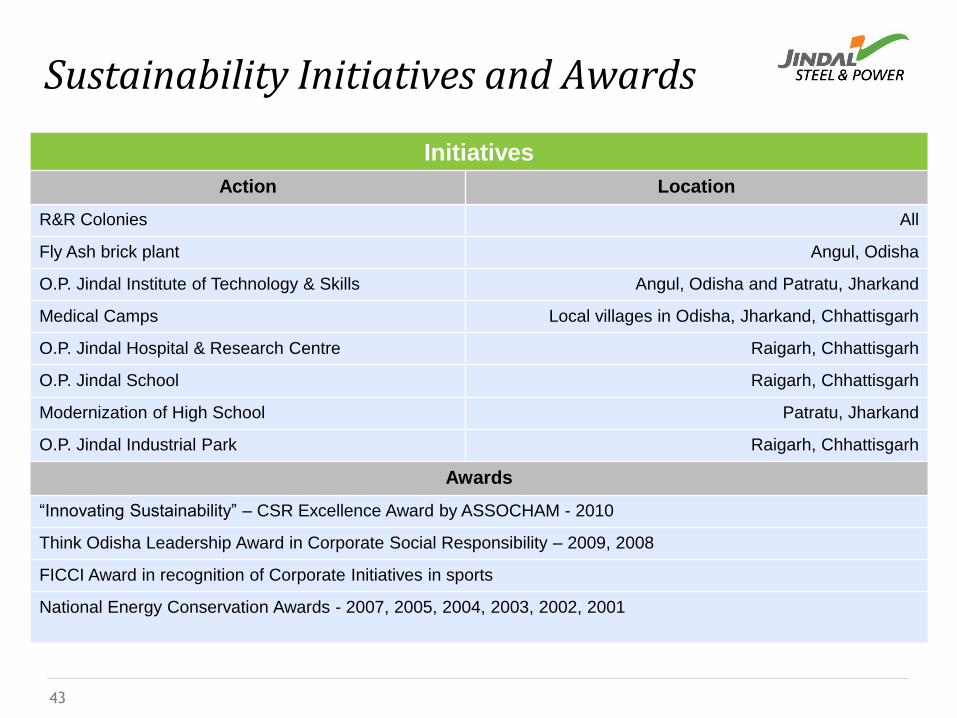

Sustainability Initiatives and Awards

Initiatives

Action Location

R&R Colonies All

Fly Ash brick plant Angul, Odisha

O.P. Jindal Institute of Technology & Skills Angul, Odisha and Patratu, Jharkand

Medical Camps Local villages in Odisha, Jharkand, Chhattisgarh

O.P. Jindal Hospital & Research Centre Raigarh, Chhattisgarh

O.P. Jindal School Raigarh, Chhattisgarh

Modernization of High School Patratu, Jharkand

O.P. Jindal Industrial Park Raigarh, Chhattisgarh

Awards

“Innovating Sustainability” – CSR Excellence Award by ASSOCHAM - 2010

Think Odisha Leadership Award in Corporate Social Responsibility – 2009, 2008

FICCI Award in recognition of Corporate Initiatives in sports

National Energy Conservation Awards - 2007, 2005, 2004, 2003, 2002, 2001

43

Copyright © 2010 Jindal Steel & Power Ltd.

Thank you