Embed Size (px)

Citation preview

JetBlue Airways

Investor Day

December 5, 2006

This slide presentation and accompanying webcast reflect JetBlue Airways Corporation’s investor presentation as of December 5, 2006 and its projected future financial forecasts, and contain forward-looking information within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities and Exchange Act of 1934, as amended. Forward-looking statements give our current expectations or forecasts of future events. You can identify these statements by the fact that they do not relate strictly to historic or current facts. They use words such as “will,'' “anticipate,'' "estimate,'' "expect,'' "project,'' "intend,'' "plan,'' "believe,'' "target,'' "forecast'' and other words and terms of similar meaning in connection with any discussion of future operating or financial performance. In particular, they may include statements relating to future actions, future performance or results of current and anticipated products and services, capital expenditures, expenses, the outcome of contingencies, such as legal proceedings, and financial results.The forward-looking information included in the investor presentation is subject to a number of risks and uncertainties. Our actual results could differ materially from the information included in the investor presentation, depending in particular upon the risks and uncertainties described in our filings with the Securities and Exchange Commission (SEC), as amended. Existing and prospective investors are cautioned not to place undue reliance on this forward-looking information, which speak only as of the date hereof. We undertake no obligation to update or revise the information in the investor presentation, whether as a result of new information, future events or circumstances, or otherwise

Safe Harbor disclosure

David Neeleman, CEO

Welcome & Overview

1

JetBlue history – initial opportunity

High Quality Coach Product

Low Costs

JFK Home

2

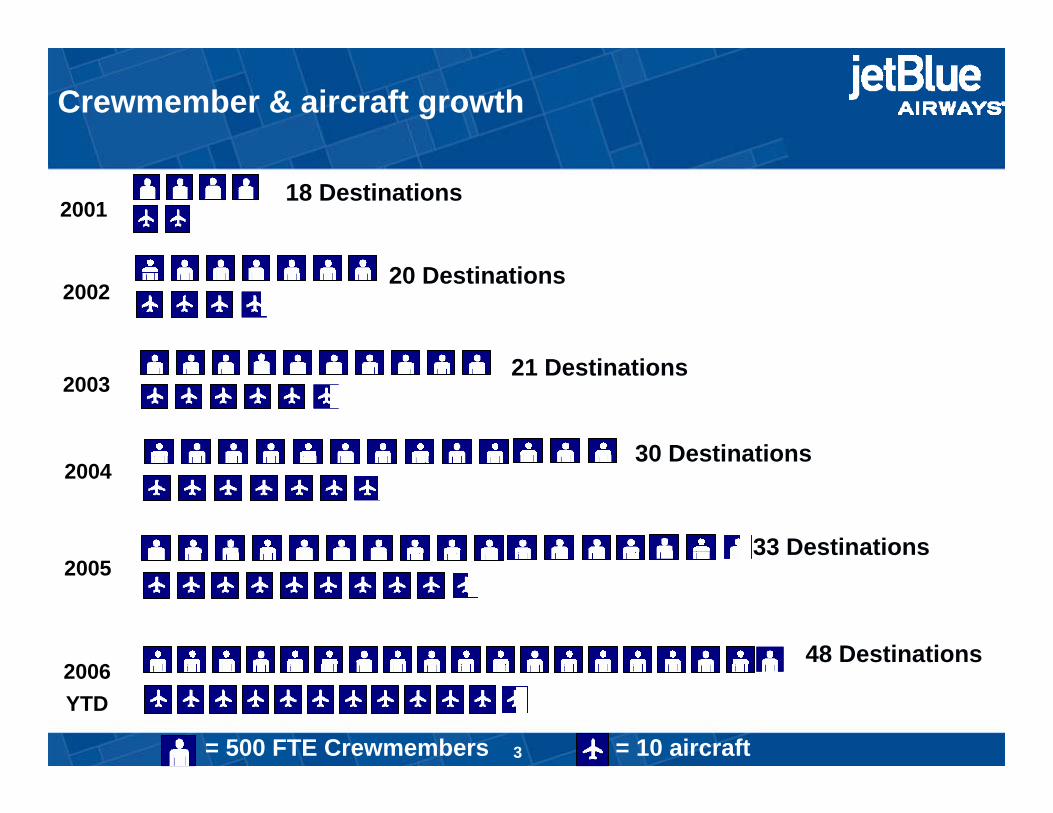

2001

2002

2003

2004

2005

2006YTD

= 500 FTE Crewmembers = 10 aircraft

Crewmember & aircraft growth

18 Destinations

20 Destinations

21 Destinations

30 Destinations

33 Destinations

48 Destinations

3

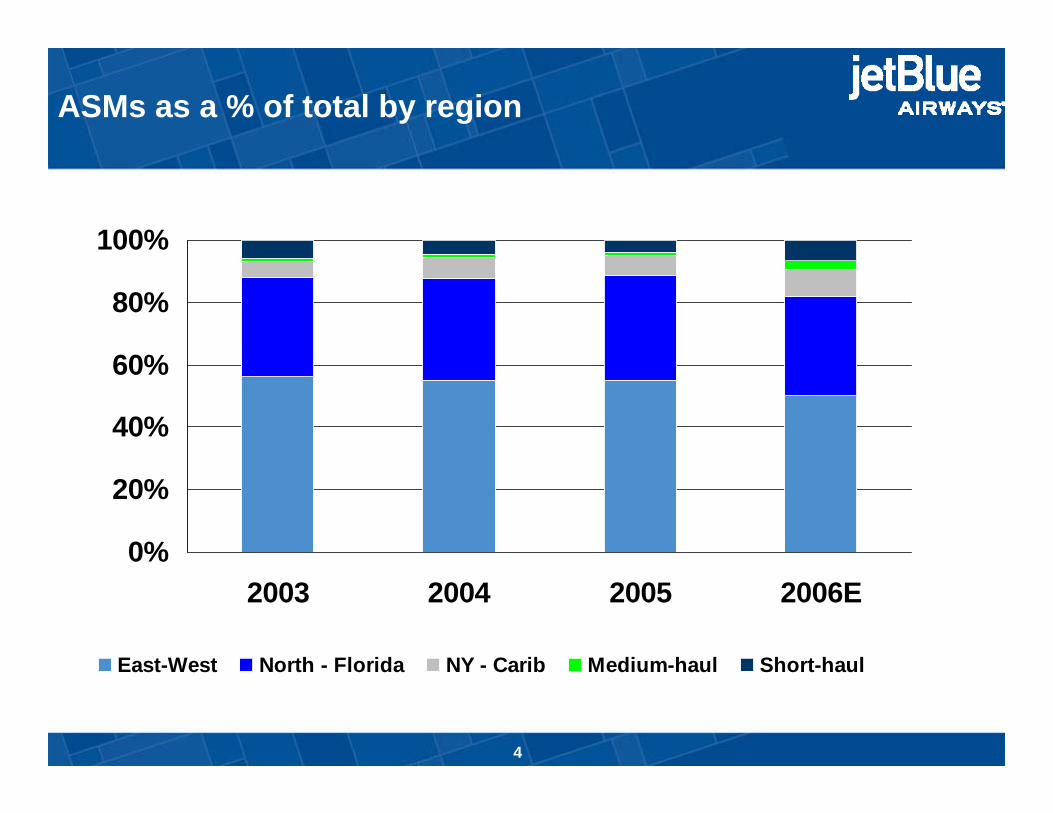

ASMs as a % of total by region

0%

20%

40%

60%

80%

100%

2003 2004 2005 2006E

East-West North - Florida NY - Carib Medium-haul Short-haul

4

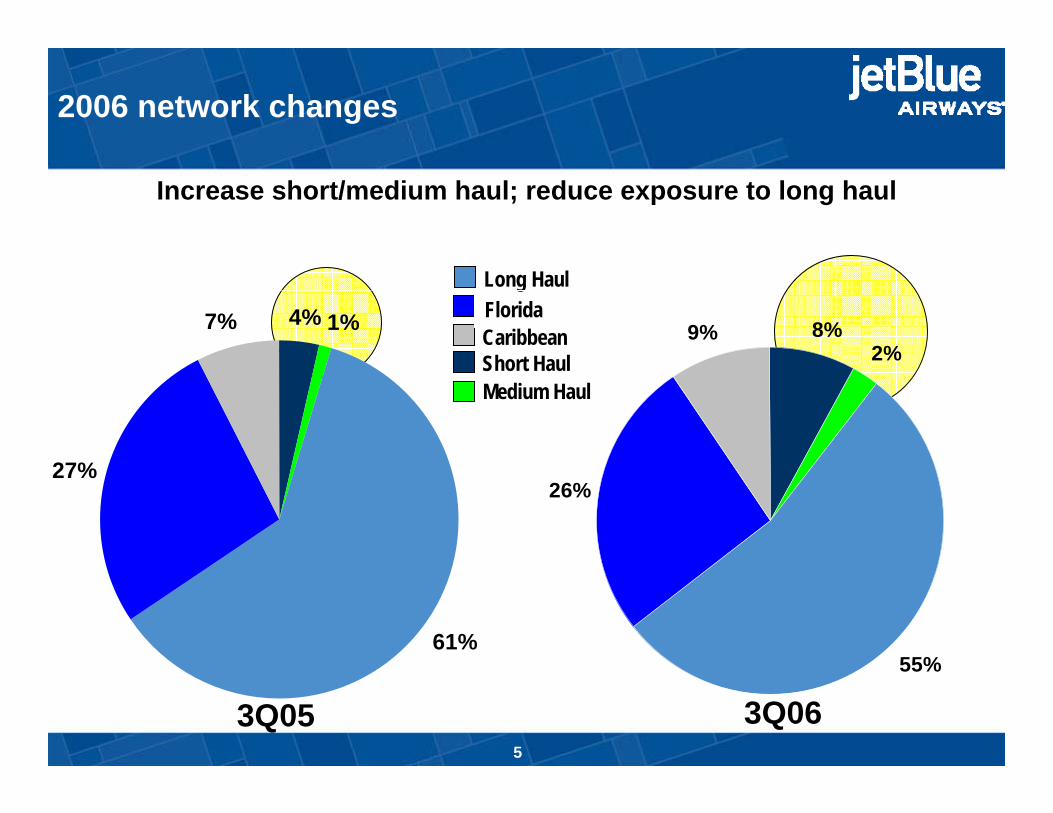

4% 1%

61%

27%

7%

Long HaulFloridaCaribbeanShort HaulMedium Haul

8%2%

55%

26%

9%

Increase short/medium haul; reduce exposure to long haul

2006 network changes

3Q05 3Q065

17% - Additional Frequencies

29% - Connect the Dots

54% - New City Adds

2006 ASMs to Increase 20-22%2006 Growth by Type

2006 – Transitional year of network building

6

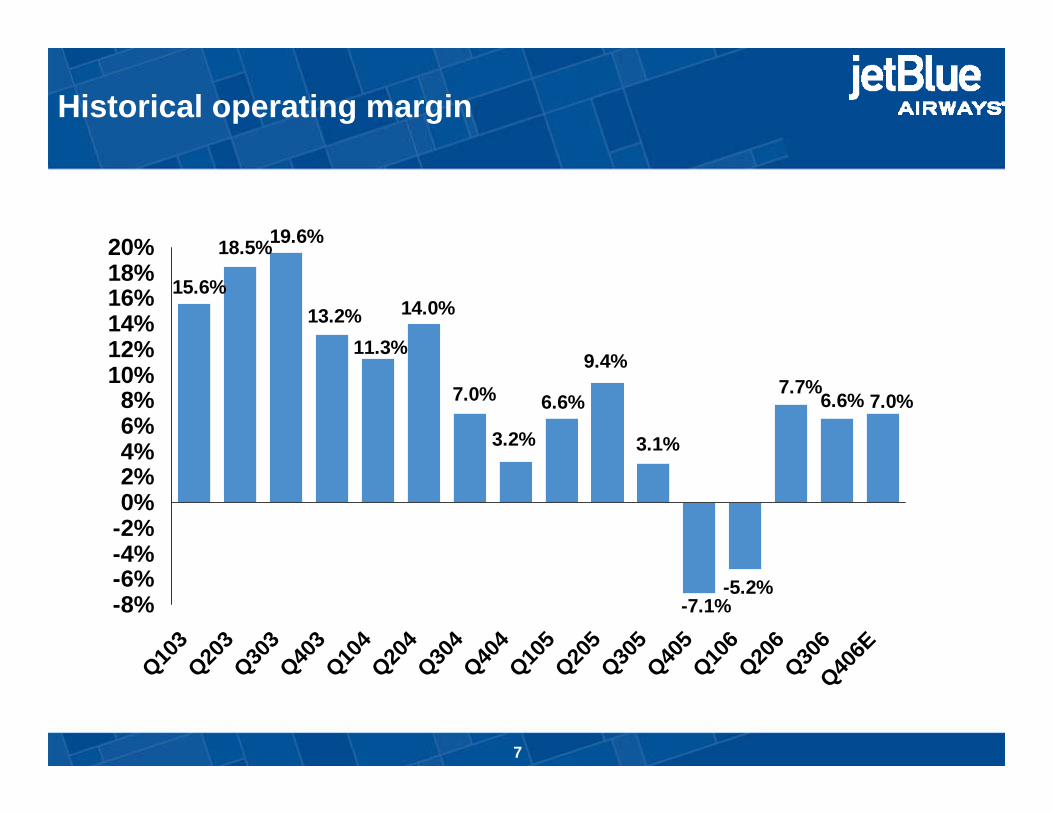

Historical operating margin

7.0%6.6%7.7%

-5.2%-7.1%

3.1%

9.4%

6.6%

3.2%

7.0%

14.0%

11.3%13.2%

19.6%18.5%

15.6%

-8%-6%-4%-2%0%2%4%6%8%

10%12%14%16%18%20%

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406E

7

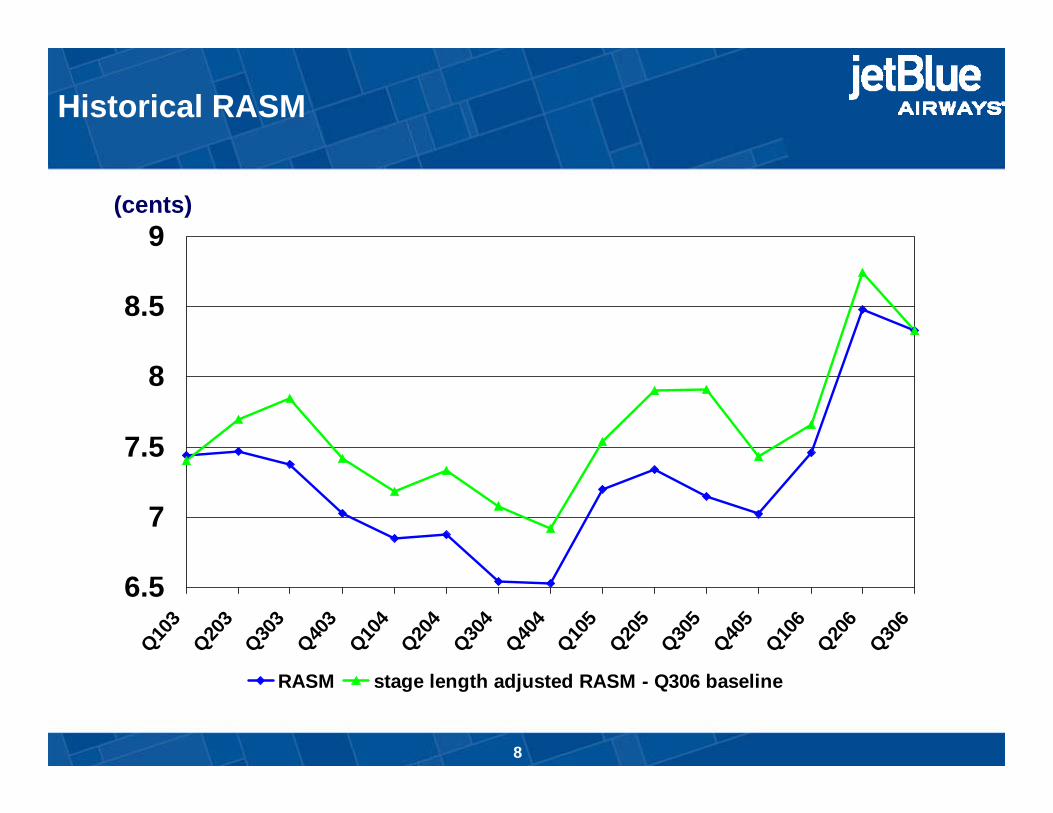

6.5

7

7.5

8

8.5

9

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

RASM stage length adjusted RASM - Q306 baseline

(cents)

Historical RASM

8

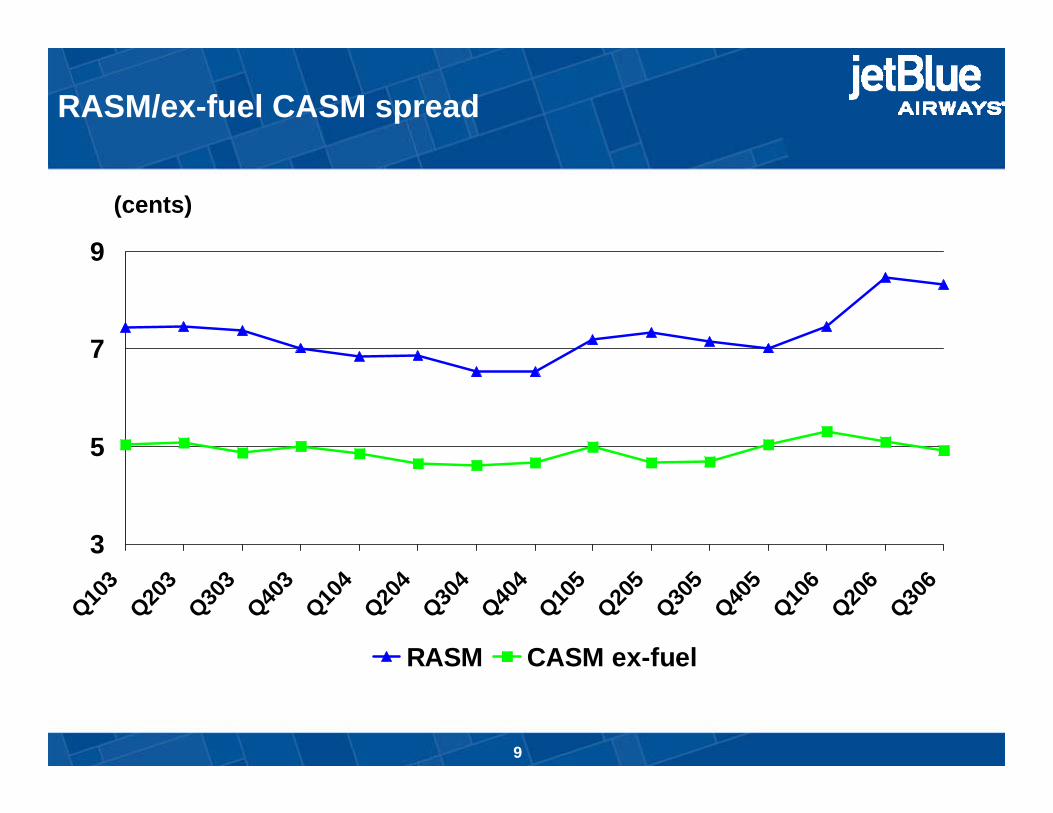

3

5

7

9

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

RASM CASM ex-fuel

RASM/ex-fuel CASM spread

(cents)

9

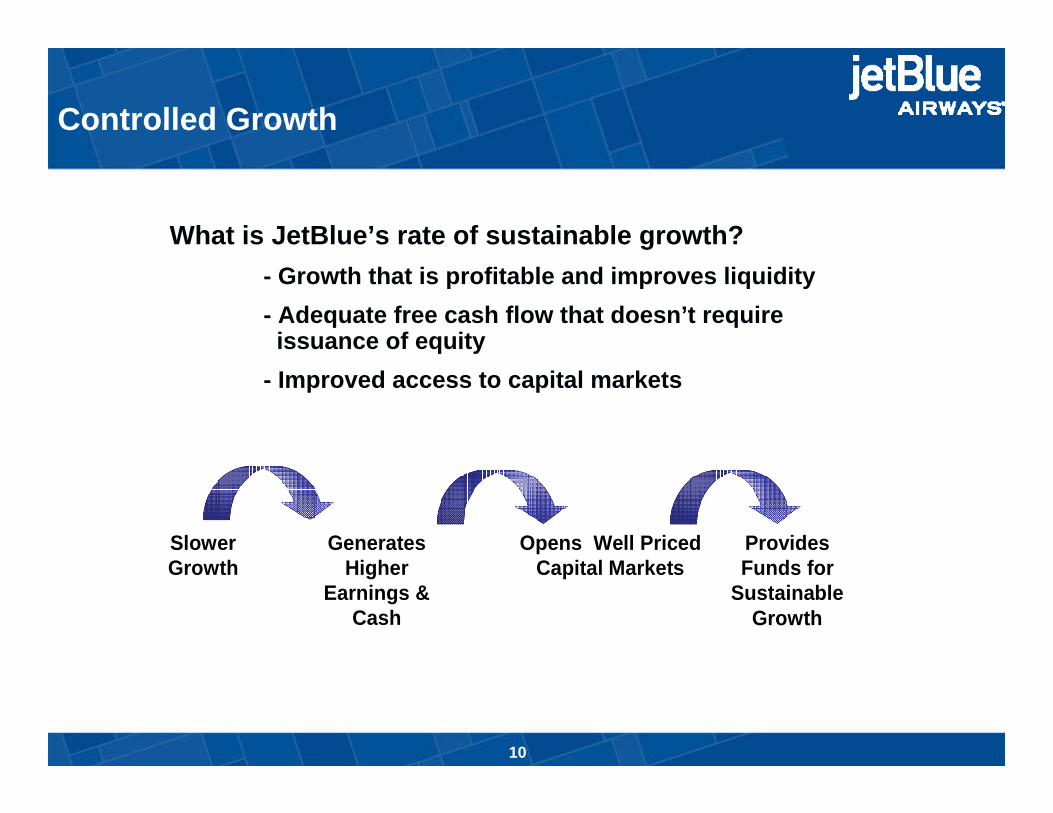

Executive Summary

What is JetBlue’s rate of sustainable growth?- Growth that is profitable and improves liquidity- Adequate free cash flow that doesn’t require issuance of equity

- Improved access to capital markets

Generates Higher

Earnings & Cash

Slower Growth

Opens Well Priced Capital Markets

Provides Funds for

Sustainable Growth

Controlled Growth

10

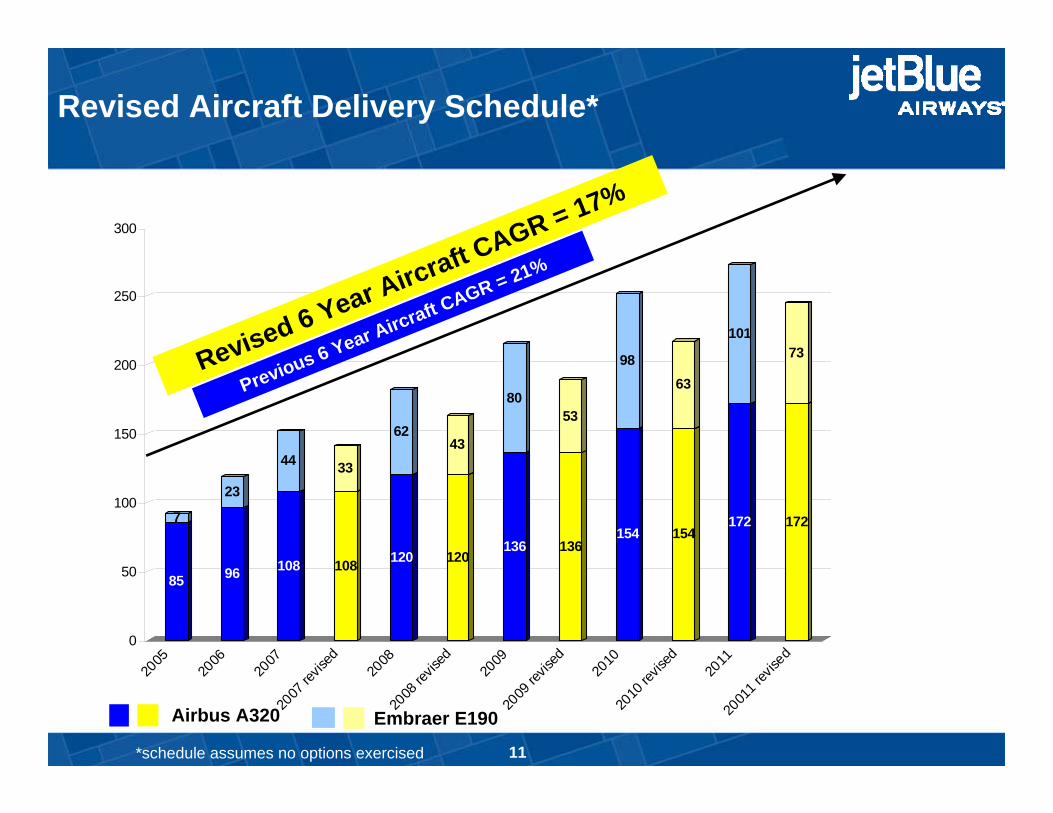

85

7

96

23

108

44

108

33

120

62

120

43

136

80

136

53

154

98

154

63

172

101

172

73

0

50

100

150

200

250

300

2005

2006

2007

2007

revis

ed

2008

2008

revis

ed

2009

2009

revis

ed

2010

2010

revis

ed

2011

2001

1 rev

ised

Revised 6 Year Aircraft CAGR = 17%

Previous 6 Year Aircraft CAGR = 21%

Revised Aircraft Delivery Schedule*

Embraer E190Airbus A320

*schedule assumes no options exercised 11

Trey Urbahn

Chief Revenue Officer

12

Arial 14 bold –dark blue font

Leveraging JetBlue’s revenue potential:

• - Being a low cost carrier isn’t what it used to be….

• - Legacy airlines have dramatically narrowed their CASM disadvantage with low cost carriers: − - Restructuring and Bankruptcy

− - Equalizing impact of rising fuel cost

− - Structural and permanent, rather than a cyclical change

• - Need to create and maintain sustainable profitability advantage by leveraging revenue as well as lower costs

13

Arial 14 bold –dark blue font

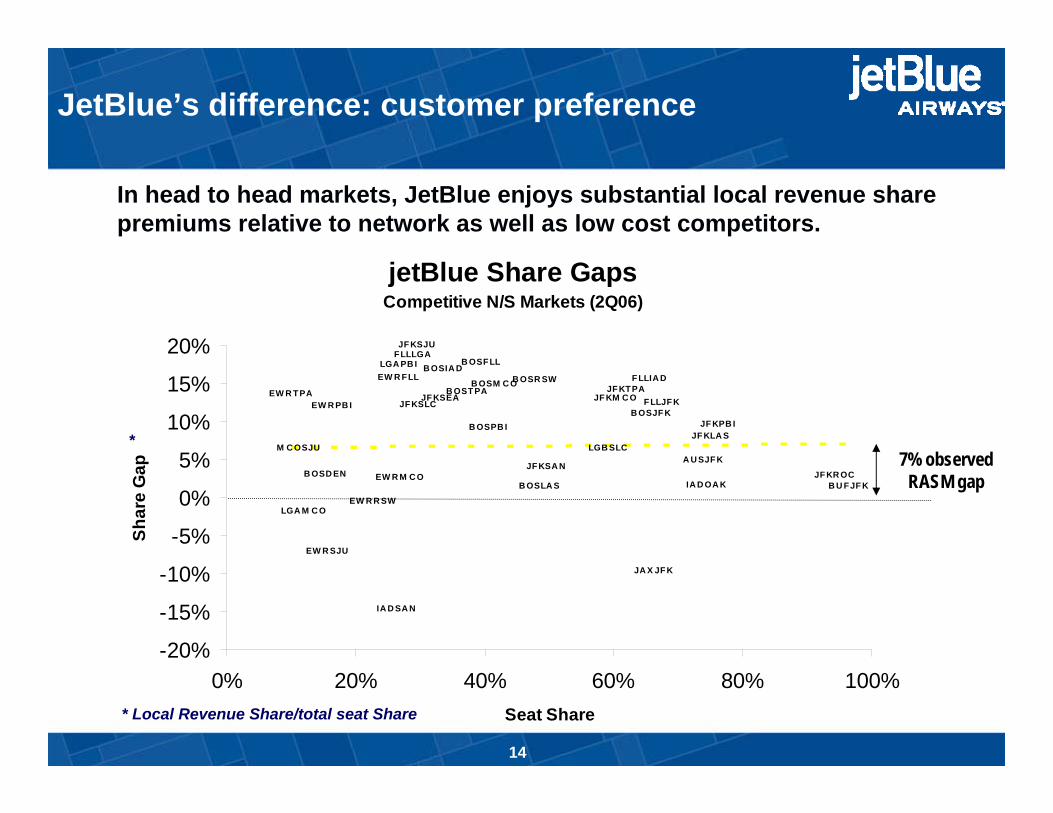

JetBlue’s difference: customer preference

• In head to head markets, JetBlue enjoys substantial local revenue share premiums relative to network as well as low cost competitors.

•

•

jetBlue Share GapsCompetitive N/S Markets (2Q06)

JA X JF K

EW R TPA

B OSD EN

IA D SA N

JFKSLC

EW R R SW

B OSLA S

EW R PB I

LGB SLC

B OSPB I

B OSR SW F LLIA DB OST PA

IA D OA K

A U SJFK

EW R FLL

EW R M C O JF KR OC

JF KLA S

B OSIA D

JF KTPA

JF KPB I

B U FJF K

F LLJF KJF KM C O

EW R SJU

JF KSEA

LGA PB I

JF KSA N

B OSFLL

B OSM C O

JF KSJU

B OSJF K

M C OSJU

LGA M C O

FLLLGA

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

0% 20% 40% 60% 80% 100%Seat Share

Shar

e G

ap 7% observed RASM gap

• * Local Revenue Share/total seat Share

• *

•

14

Arial 14 bold –dark blue font

Revenue growth strategies:

• JetBlue has substantial opportunity to drive revenue improvement:

• - Route structure:− - Network connectivity

− - Largest low cost carrier in the world’s largest market

− - Growing presence in focus cities: (BOS,IAD,FLL,LGB)

• - Revenue Management− - Shift from load factor to a RASM focus

− - Better demand segmentation

− - Optimize connect traffic opportunities

• - Marketing− - New distribution channels

− - Interline opportunities at JFK

− - Monetize a loyal customer base

15

Marty St. George

VP Route Planning

16

Planning philosophy

- Sustainable business models require at least one of two structural advantages:

- Network advantage- Cost advantage

- JetBlue is well positioned on both fronts:- Largest low-fare carrier in the largest air travel market in the world- Low cost structure

- Moreover, we enjoy this competitive positioning while delivering outstanding customer service

17

Planning’s 2007 roadmap

- Continue to grow JFK, both through new destinations (both A320 and Embraer 190) and by increasing connectivity

- Add selected frequency and destinations in our focus cities (Boston, Ft. Lauderdale, Long Beach, Washington D.C./Dulles)

- Achieve first two goals while reducing controllable costs per ASM

18

Network update

19

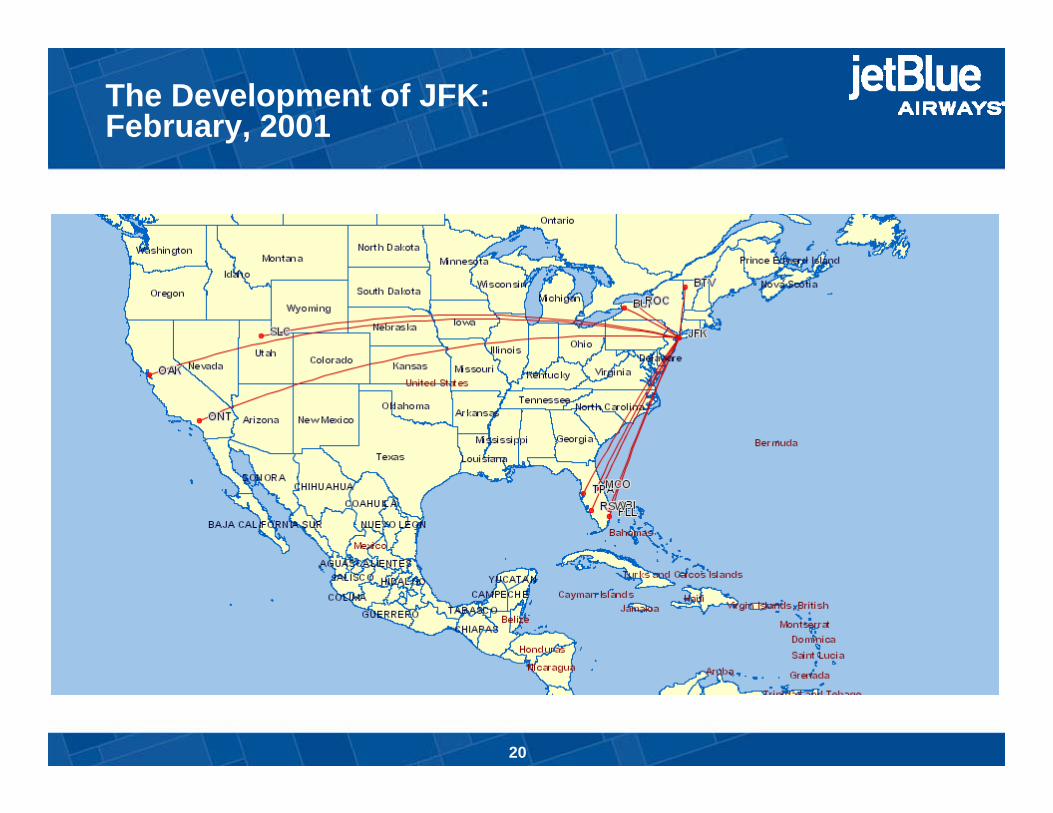

The Development of JFK:February, 2001

20

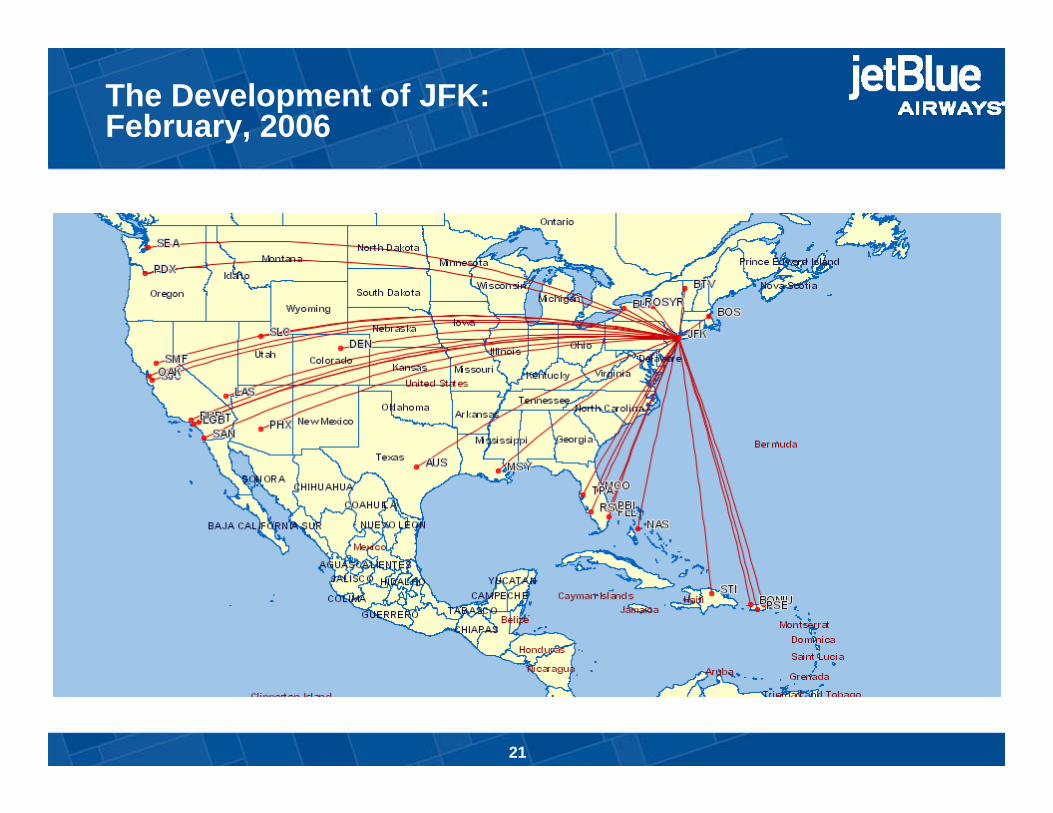

The Development of JFK:February, 2006

21

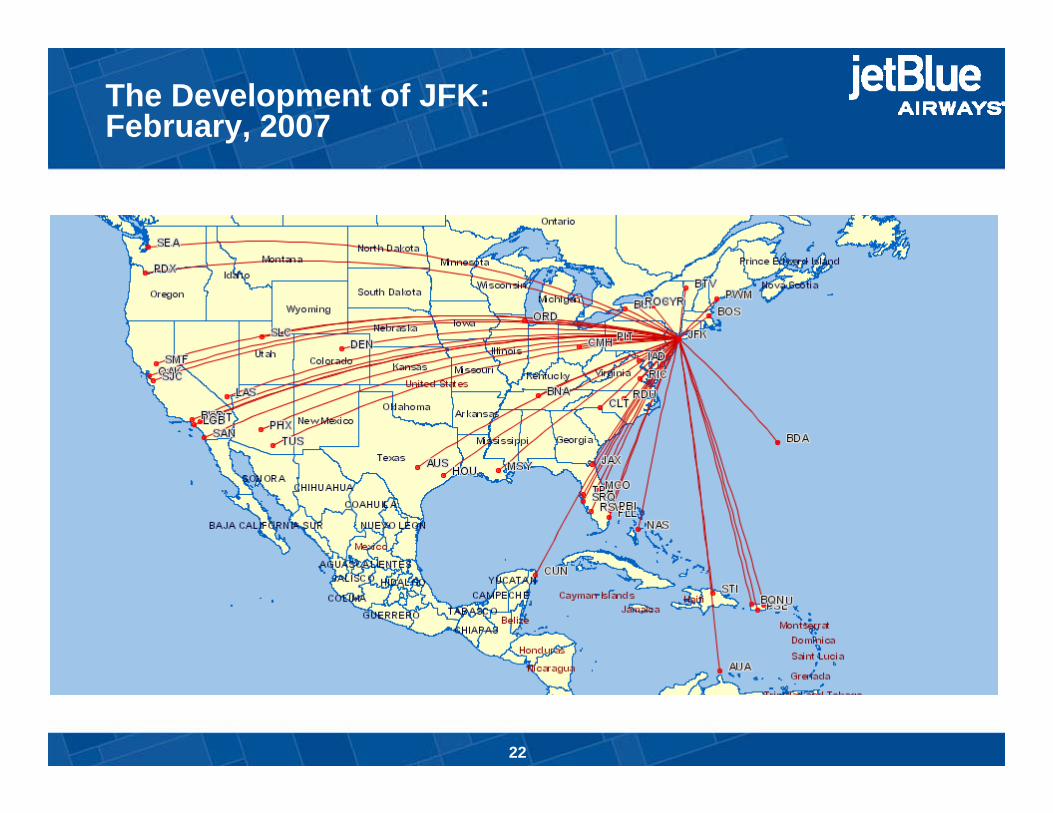

The Development of JFK: February, 2007

22

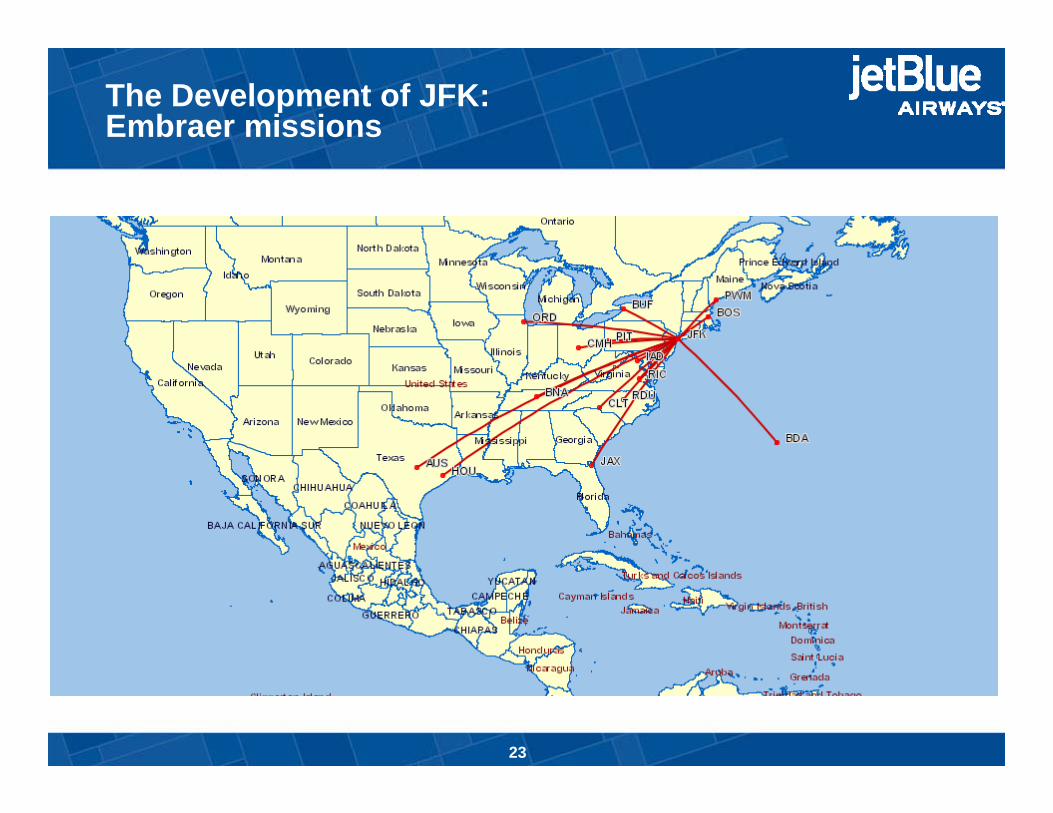

The Development of JFK: Embraer missions

23

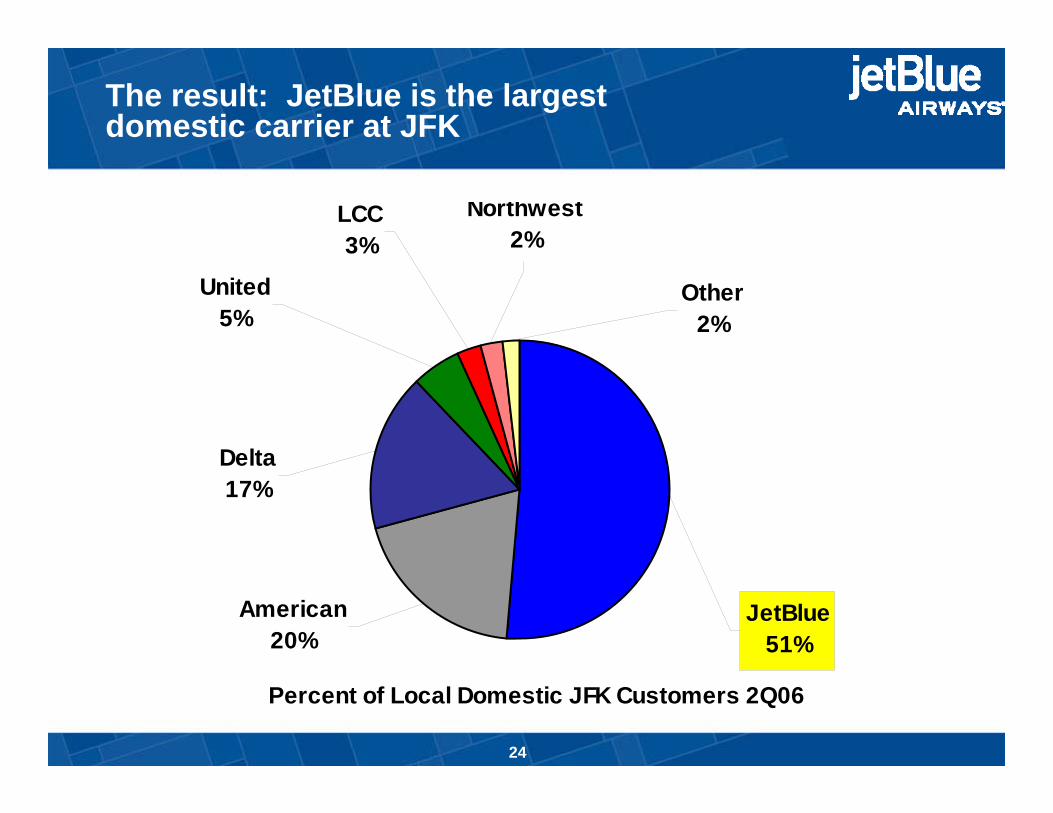

The result: JetBlue is the largest domestic carrier at JFK

Percent of Local Domestic JFK Customers 2Q06

Other2%

Delta17%

LCC3%

United5%

Northwest2%

JetBlue51%

American20%

24

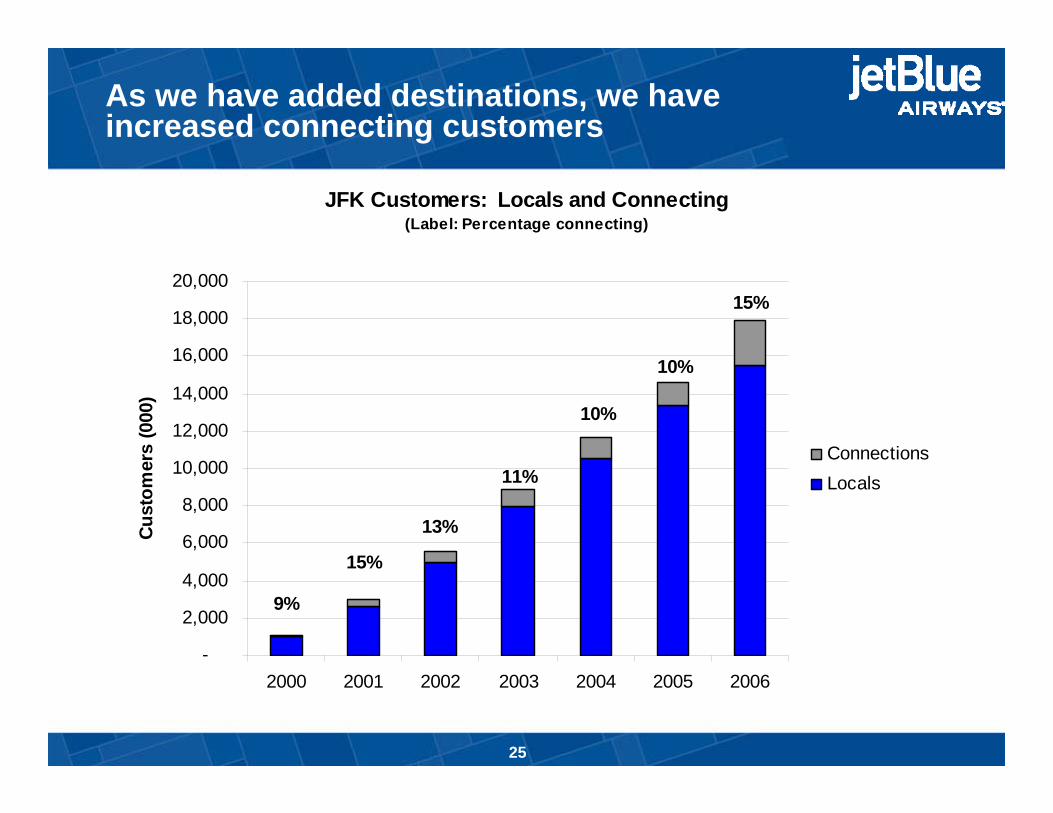

As we have added destinations, we have increased connecting customers

JFK Customers: Locals and Connecting(Label: Percentage connecting)

15%

10%

10%

11%

13%

15%

9%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2000 2001 2002 2003 2004 2005 2006

Cust

omer

s (0

00)

ConnectionsLocals

25

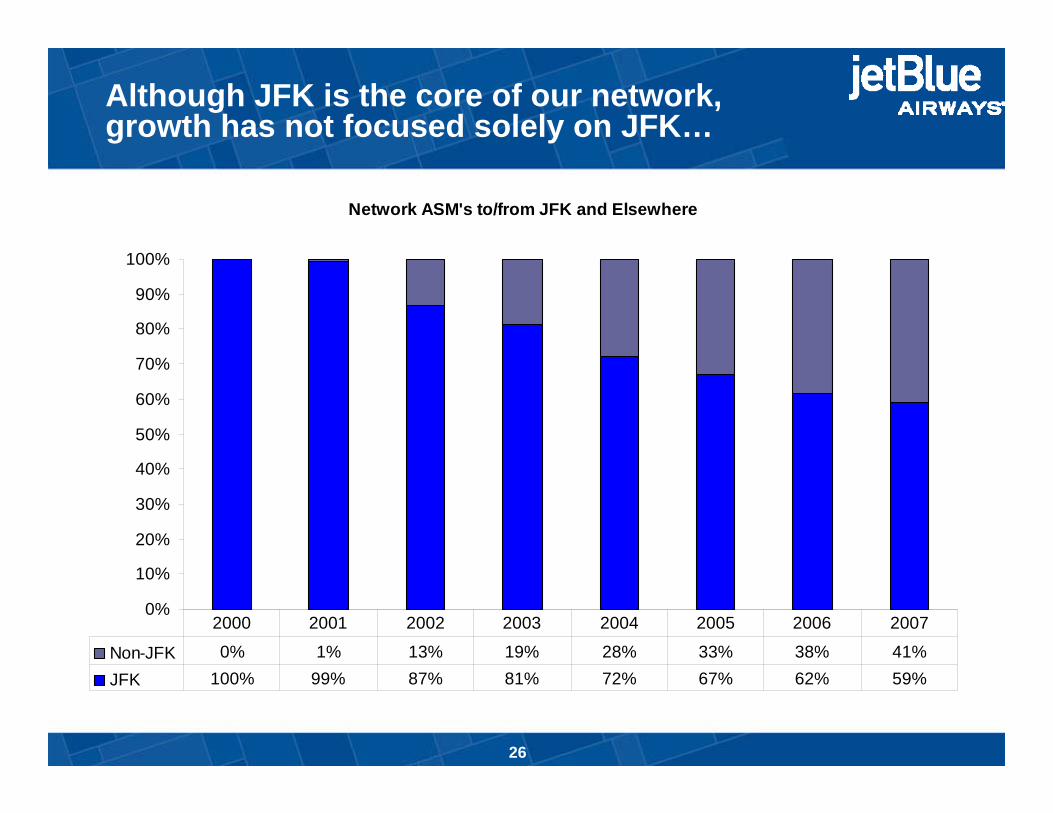

Although JFK is the core of our network, growth has not focused solely on JFK…

Network ASM's to/from JFK and Elsewhere

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Non-JFK 0% 1% 13% 19% 28% 33% 38% 41%JFK 100% 99% 87% 81% 72% 67% 62% 59%

2000 2001 2002 2003 2004 2005 2006 2007

26

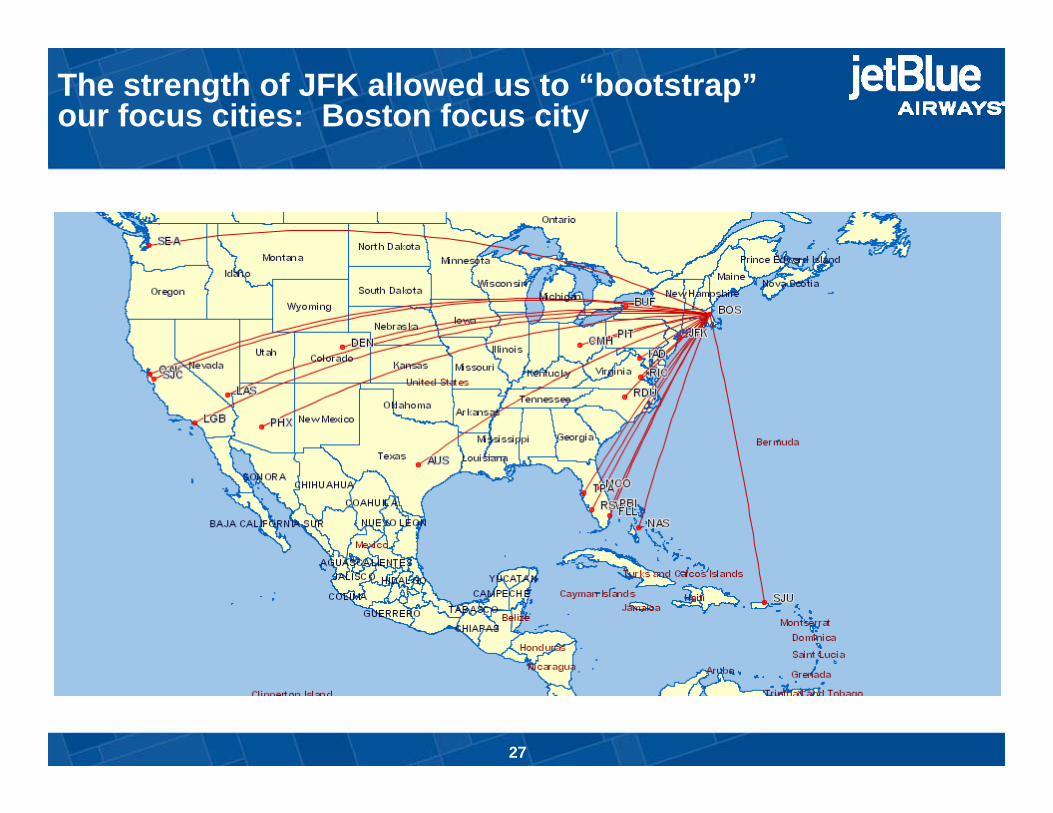

The strength of JFK allowed us to “bootstrap”our focus cities: Boston focus city

27

Boston plus Long Beach

28

Boston, Long Beach and Fort Lauderdale…

29

Boston, Long Beach, Fort Lauderdaleand Washington

30

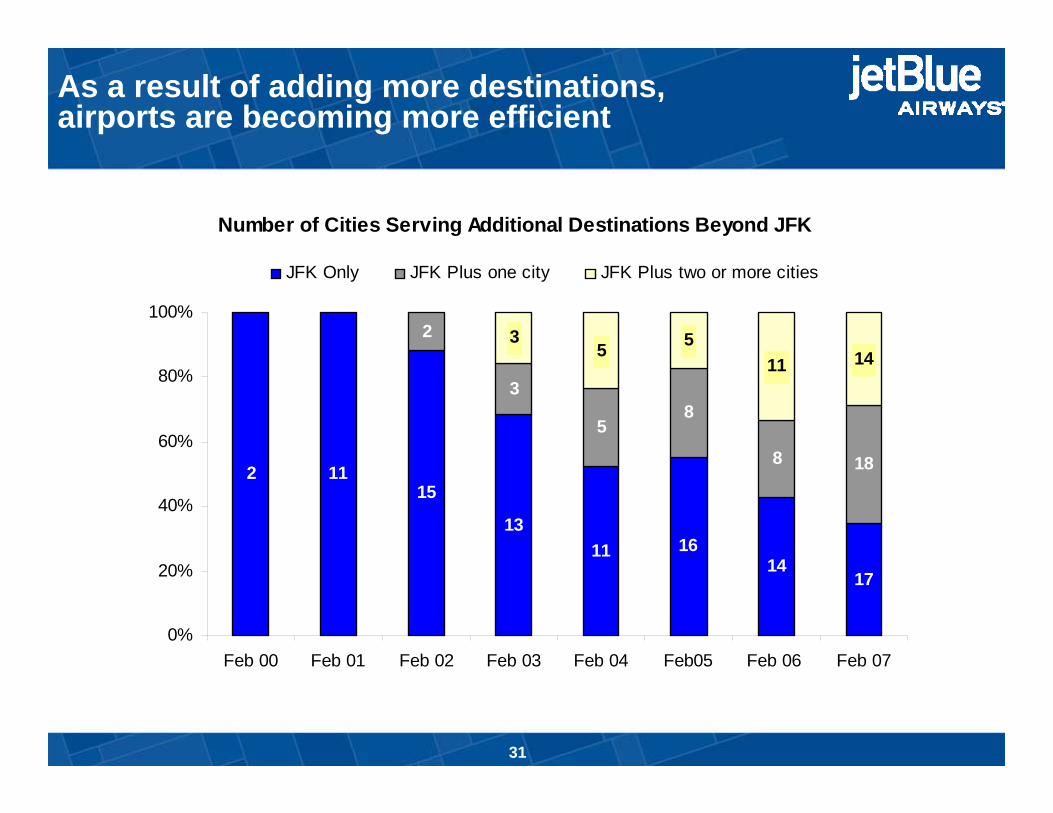

As a result of adding more destinations, airports are becoming more efficient

Number of Cities Serving Additional Destinations Beyond JFK

2 1115

1311 16

1417

2

3

58

8 18

35 5

11 14

0%

20%

40%

60%

80%

100%

Feb 00 Feb 01 Feb 02 Feb 03 Feb 04 Feb05 Feb 06 Feb 07

JFK Only JFK Plus one city JFK Plus two or more cities

31

System Map: February, 2007

32

2007 goals: planning

- Execute to the core plan− Continue to add new destinations to JFK, building presence and connectivity− Grow frequency and destinations from existing focus cities− Maintain focus on operational efficiency

- Build on our strength as unsustainable capacity is cancelled

- Stay nimble

33

Roadmap to success

- JetBlue has all the elements of a winning strategic position:− Low cost structure− Largest low-cost carrier in the biggest air travel market in the world− Beloved by customers, and able to achieve revenue premiums

34

Rick Zeni

VP Revenue Management

35

• - Revenue Management Philosophy• - Fare Structure• - New Market Pricing• - Fare Increases• - Data and Analytics

Revenue management at JetBlue

36

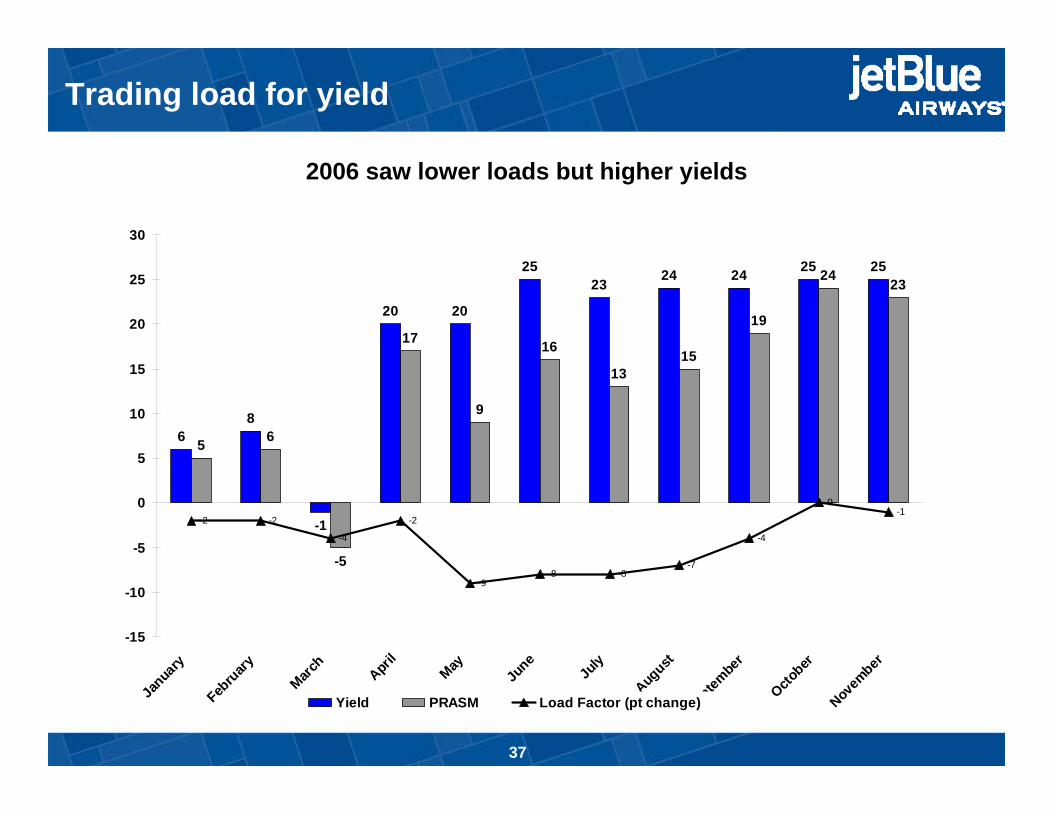

68

-1

20 20

2523 24 24 25 25

5 6

-5

17

9

16

1315

19

24 23

-2 -2

-4

-2

-9-8 -8

-7

-4

0-1

-15

-10

-5

0

5

10

15

20

25

30

Janua

ry

Febru

ary

March

April

May

June

July

August

Septem

ber

October

Novem

ber

Yield PRASM Load Factor (pt change)

2006 saw lower loads but higher yields

Trading load for yield

37

Arial 14 bold –dark blue font

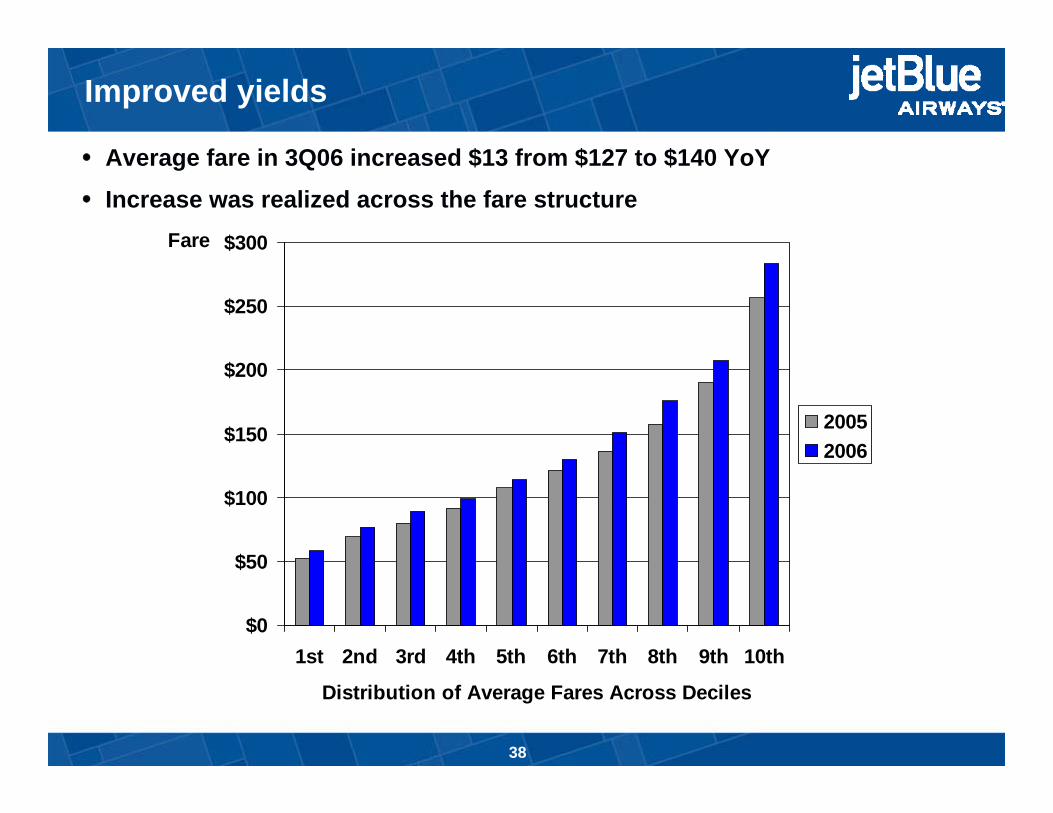

Improved yields

Average fare in 3Q06 increased $13 from $127 to $140 YoY

Increase was realized across the fare structure

$0

$50

$100

$150

$200

$250

$300

1st 2nd 3rd 4th 5th 6th 7th 8th 9th 10th

Distribution of Average Fares Across Deciles

Fare

20052006

38

Arial 14 bold –dark blue font

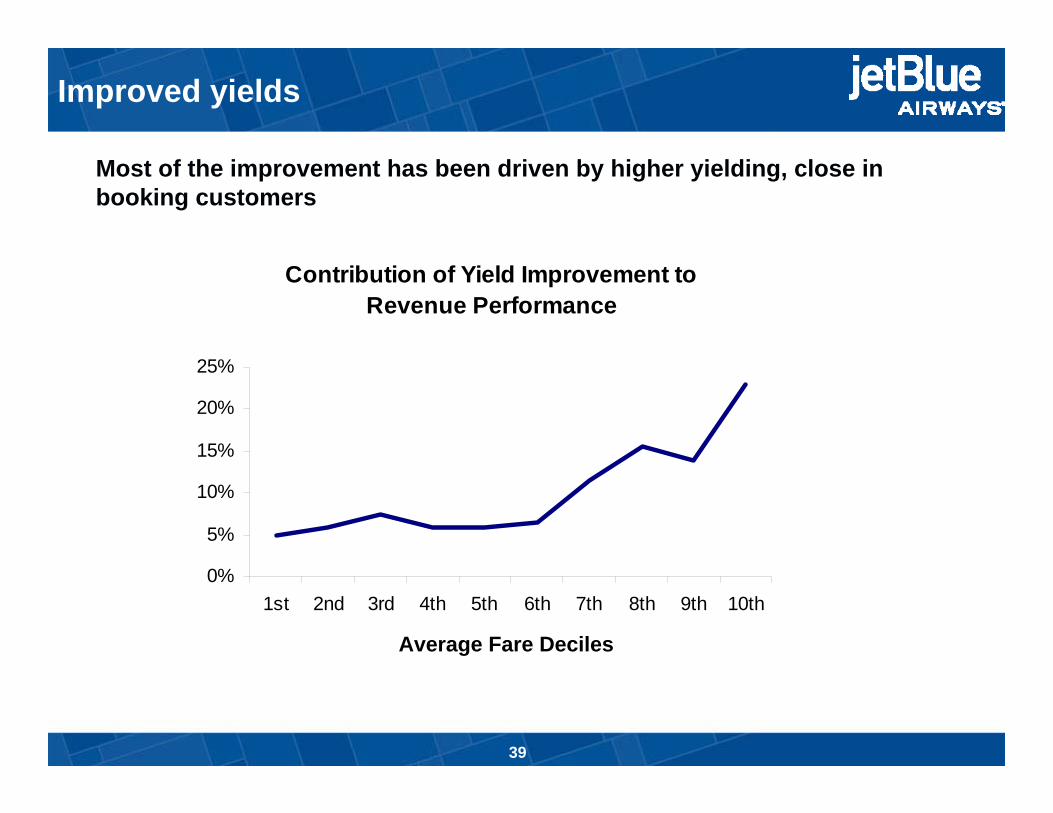

Improved yields

• Most of the improvement has been driven by higher yielding, close in booking customers

Contribution of Yield Improvement to Revenue Performance

0%

5%

10%

15%

20%

25%

1st 2nd 3rd 4th 5th 6th 7th 8th 9th 10th

Average Fare Deciles

39

Arial 14 bold –dark blue font

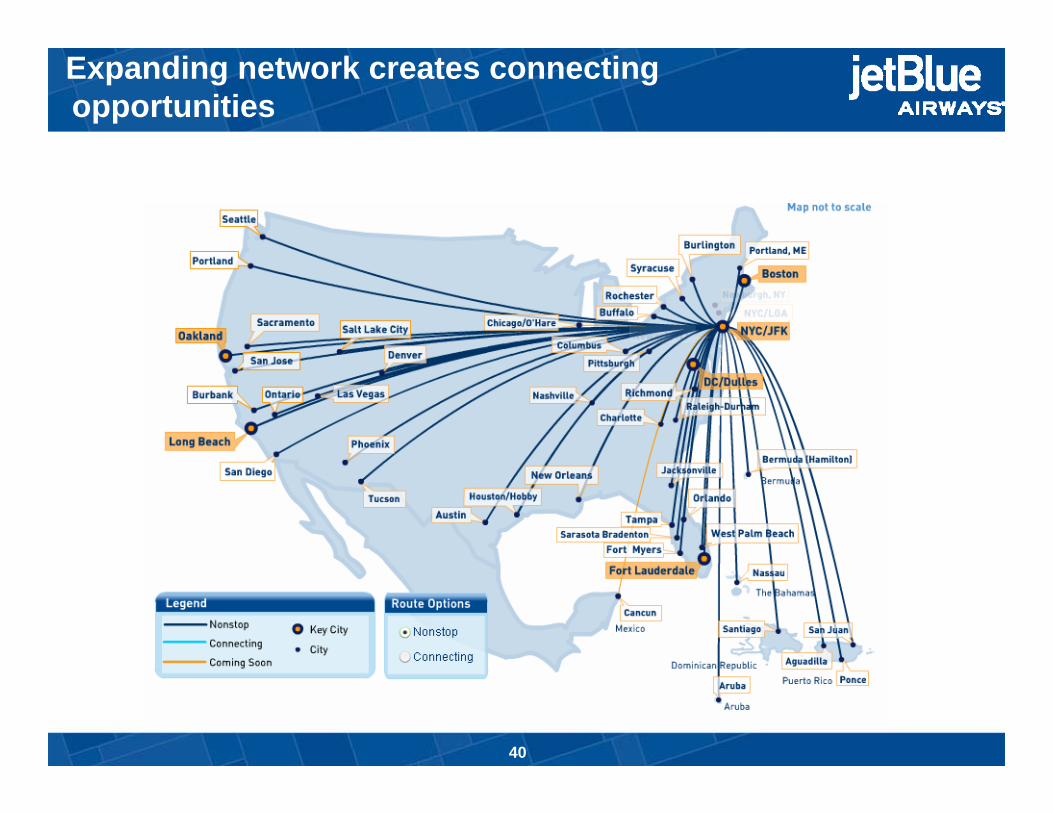

Expanding network creates connecting opportunities

40

Arial 14 bold –dark blue font

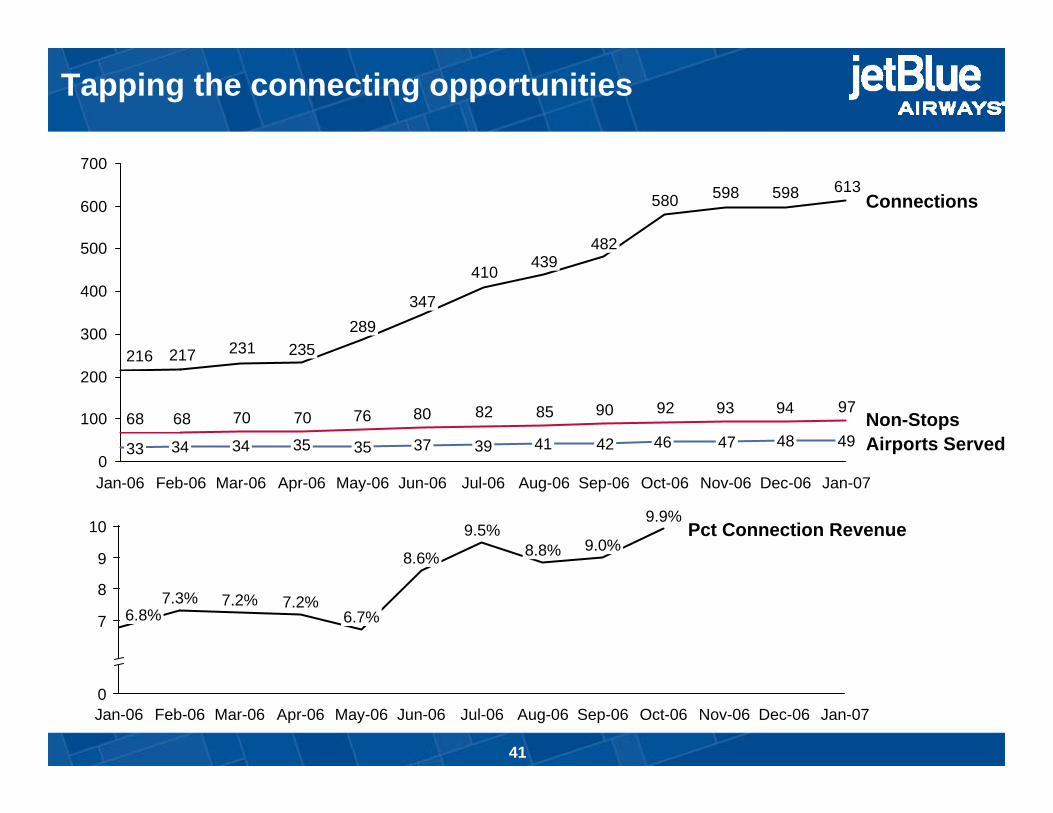

613598598580

410

231217216

97949392908582807670706868

0

100

200

300

400

500

600

700

Jan-06

34

Feb-06

34

Mar-06

35

235

Apr-06

35

289

May-06

37

347

Jun-06

39

Jul-06

33

439

Aug-06

42

482

Sep-06

46

Oct-06

47

Nov-06

48

Dec-06

49

Jan-07

Airports Served

Connections

Non-Stops41

Jul-06

8.8%

Aug-06

9.0%

Sep-06

9.9%

Oct-06 Nov-06 Dec-06 Jan-070

10

7

8

9

6.8%

Jan-06

7.3%

Feb-06

7.2%

Mar-06

7.2%

Apr-06

6.7%

May-06

8.6%

Jun-06

9.5% Pct Connection Revenue

Tapping the connecting opportunities

41

Tim Claydon

SVP, Sales & Marketing

42

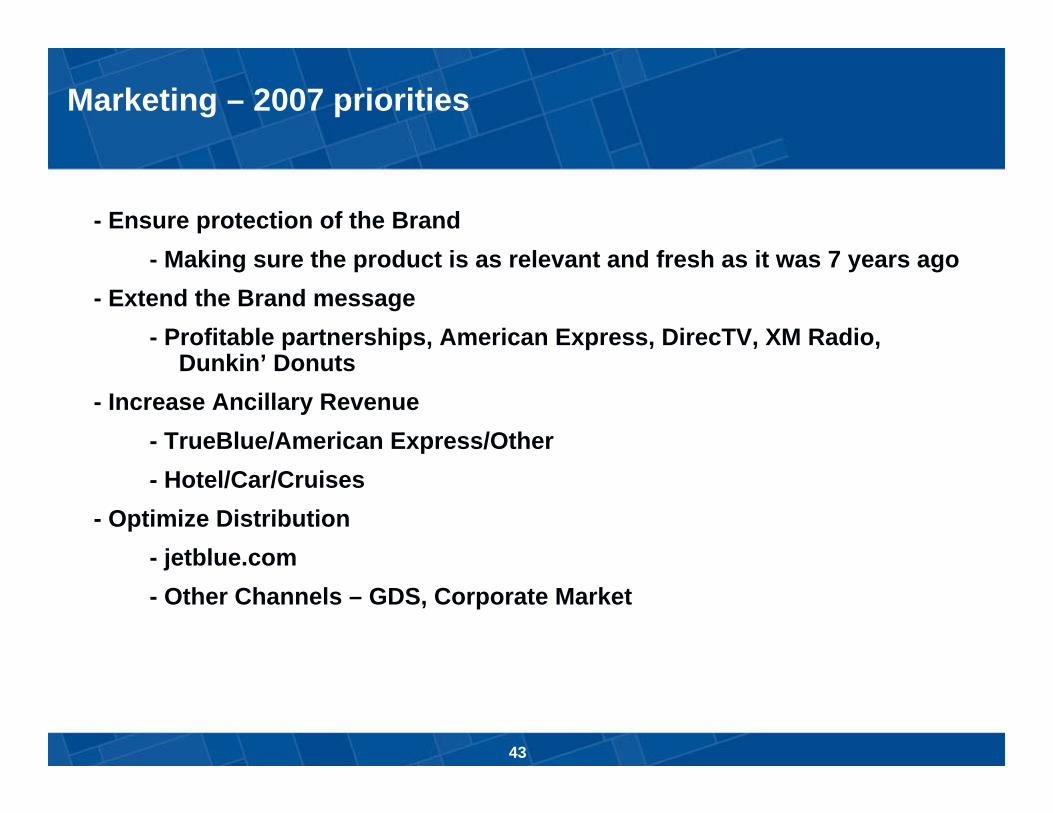

Marketing – 2007 priorities

- Ensure protection of the Brand- Making sure the product is as relevant and fresh as it was 7 years ago

- Extend the Brand message- Profitable partnerships, American Express, DirecTV, XM Radio,

Dunkin’ Donuts- Increase Ancillary Revenue

- TrueBlue/American Express/Other- Hotel/Car/Cruises

- Optimize Distribution- jetblue.com- Other Channels – GDS, Corporate Market

43

Marketing - distribution

- GDS- Now in all four major GDS’s: Sabre, Galileo, Worldspan, Amadeus

- >$100m in incremental revenue for 2007- Seeing significant premiums to average of $35 one-way- Midweek booking strength- Closer in bookings- Hitting the corporate customer

- OTA’s- Continue to have productive discussions with OTA’s- Similar profile to JetBlue.com customer

- CompanyBlue- 2006 revenue has doubled and is targeted to double again in 2007.- 740 active accounts- Little attrition due to GDS involvement - With profile similar to that of GDS bookings

44

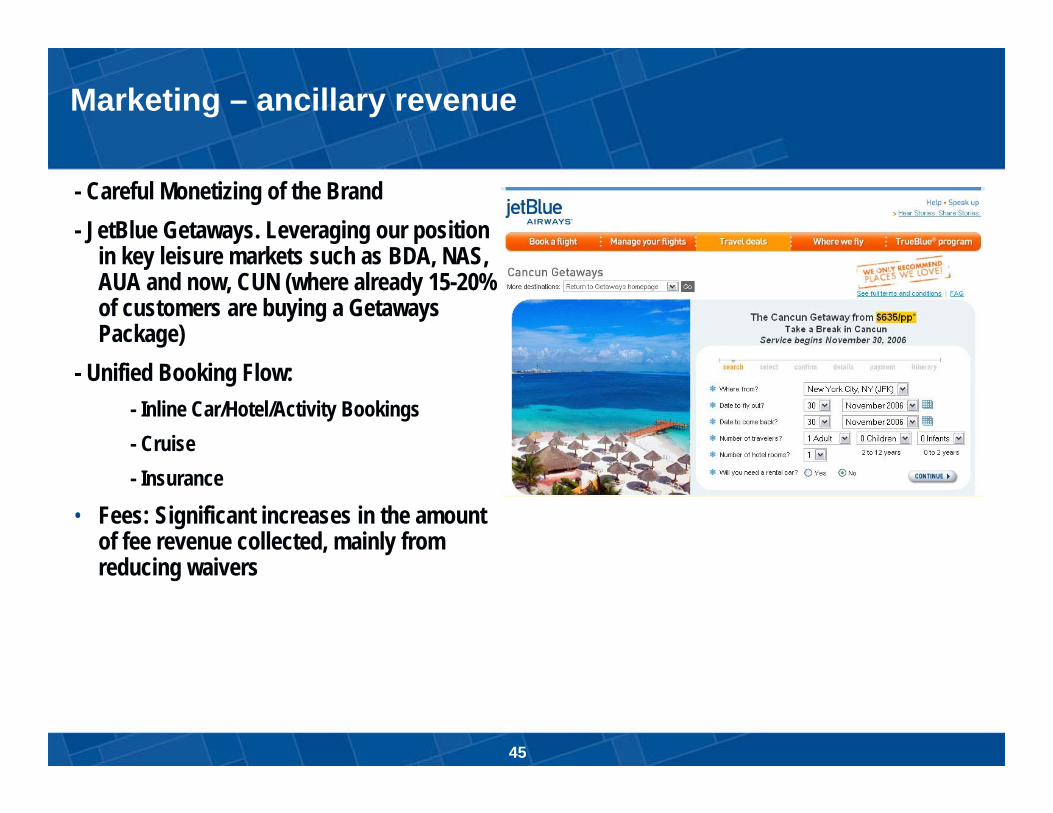

Marketing – ancillary revenue

- Careful Monetizing of the Brand- JetBlue Getaways. Leveraging our position

in key leisure markets such as BDA, NAS, AUA and now, CUN (where already 15-20% of customers are buying a Getaways Package)

- Unified Booking Flow:- Inline Car/Hotel/Activity Bookings- Cruise- Insurance

• Fees: Significant increases in the amount of fee revenue collected, mainly from reducing waivers

45

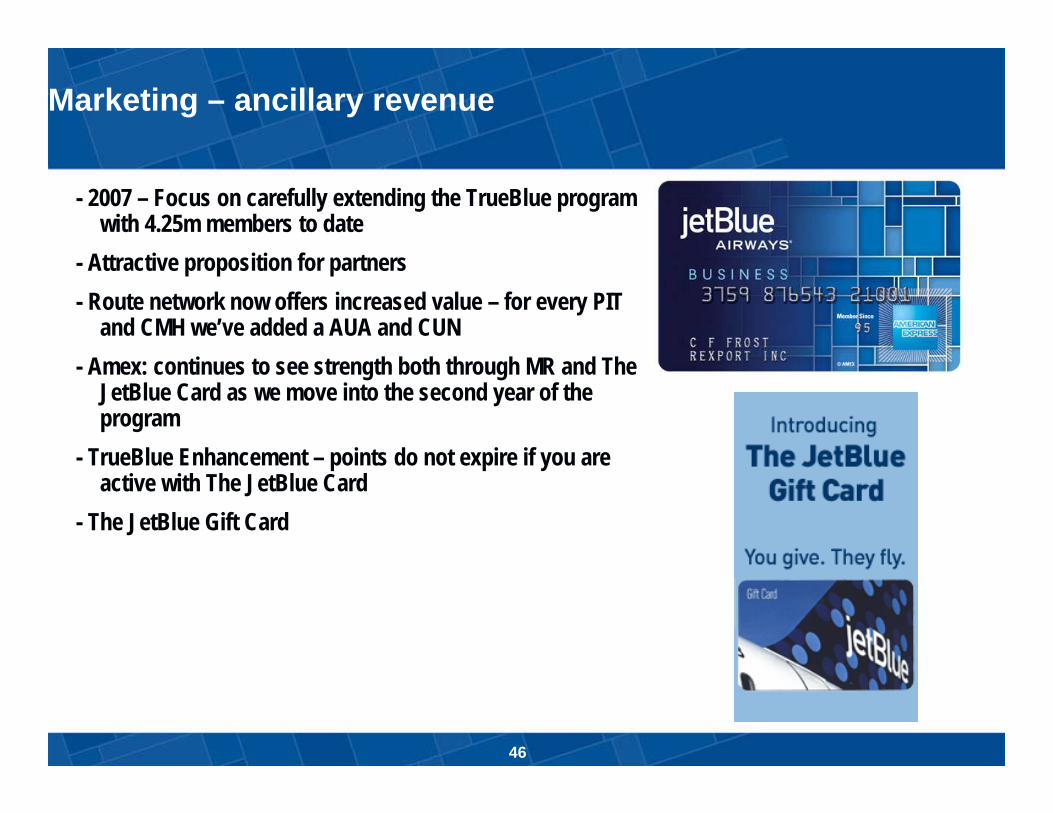

Marketing – ancillary revenue

- 2007 – Focus on carefully extending the TrueBlue program with 4.25m members to date

- Attractive proposition for partners- Route network now offers increased value – for every PIT

and CMH we’ve added a AUA and CUN- Amex: continues to see strength both through MR and The

JetBlue Card as we move into the second year of the program

- TrueBlue Enhancement – points do not expire if you are active with The JetBlue Card

- The JetBlue Gift Card

46

Marketing –other partnerships

- Partnerships with progressive Brands, joint promotion and exposure opportunities- Significant PR value

47

Inter-national

46%Domestic

54%

Other11%

Delta21%

American20%

JetBlue48%

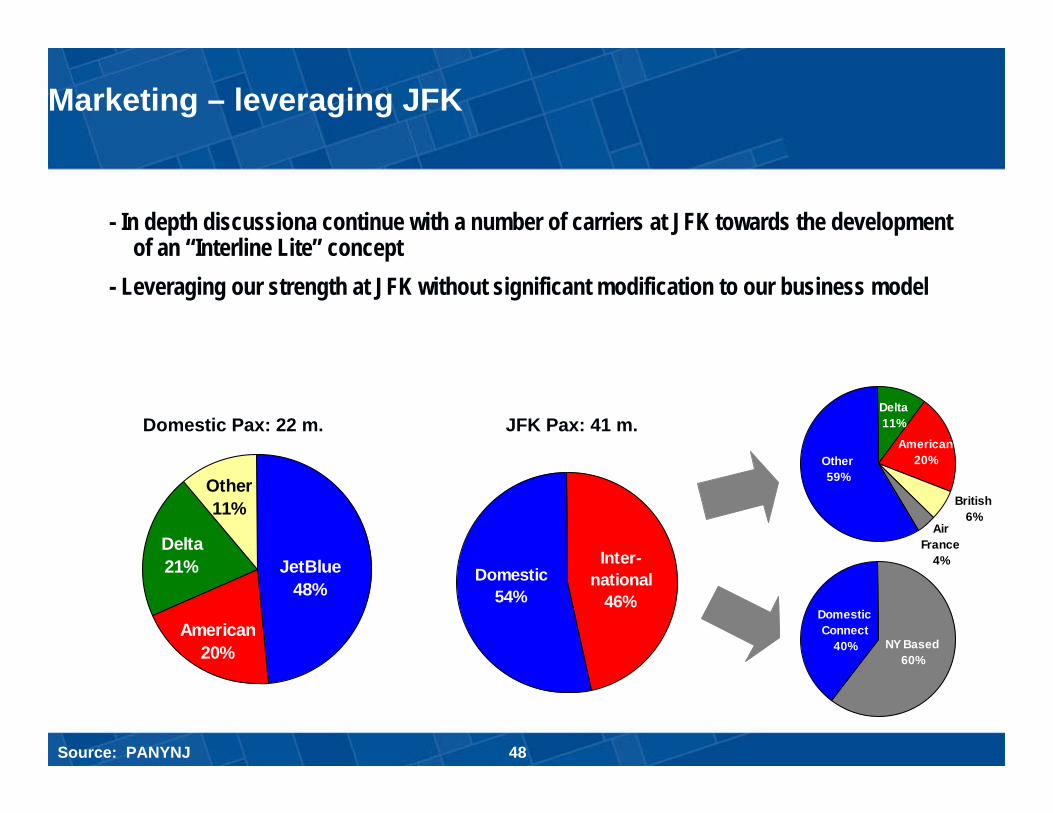

Marketing – leveraging JFK

- In depth discussiona continue with a number of carriers at JFK towards the development of an “Interline Lite” concept

- Leveraging our strength at JFK without significant modification to our business model

Domestic Pax: 22 m. JFK Pax: 41 m.

DomesticConnect

40% NY Based60%

Other59%

Delta11%

American20%

British6%

Air France

4%

Source: PANYNJ 48

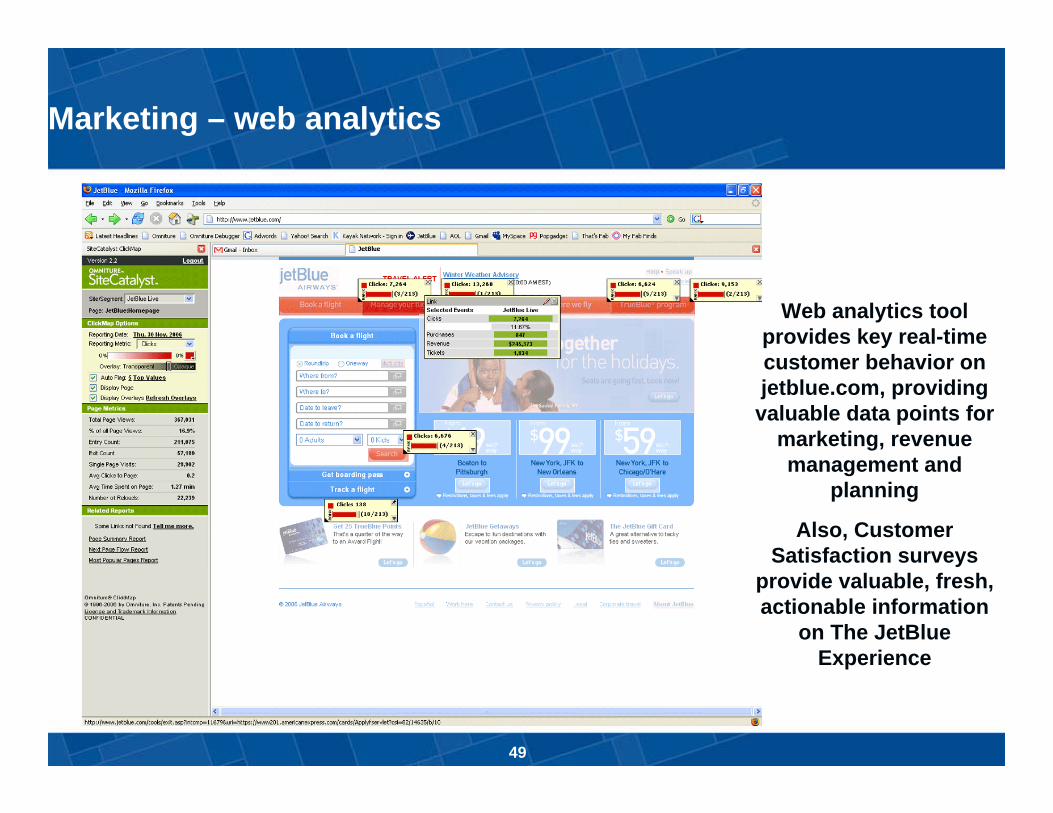

Marketing – web analytics

Web analytics tool provides key real-time customer behavior on jetblue.com, providing valuable data points for

marketing, revenue management and

planning

Also, Customer Satisfaction surveys

provide valuable, fresh, actionable information

on The JetBlue Experience

49

Marketing - brand

- Continued strength of the Brand:− 2006 Conde Nast Traveler Readers’

Choice Awards – Five Years Running!− JD Power Highest Low Cost Carrier

Customer Satisfaction− T&L Magazine 2006 World Travel Awards

– Best Domestic Airline

John Harvey, CFO

50

- Develop a sustainable low cost structure to drive bottom-line earnings

- Slow growth to improve free cash flow defecit

- Build cash ‘war chest’ to develop position of strength

Finance goals

51

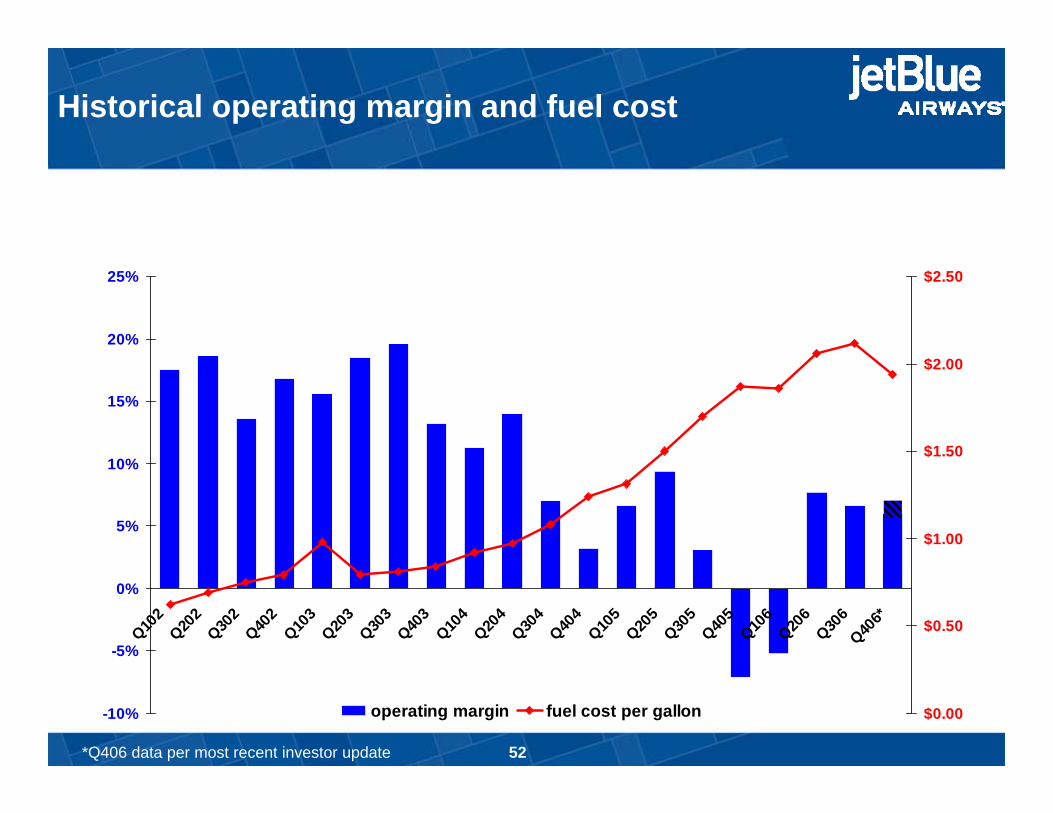

-10%

-5%

0%

5%

10%

15%

20%

25%

Q102

Q202

Q302

Q402

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406*

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

operating margin fuel cost per gallon

*Q406 data per most recent investor update

Historical operating margin and fuel cost

52

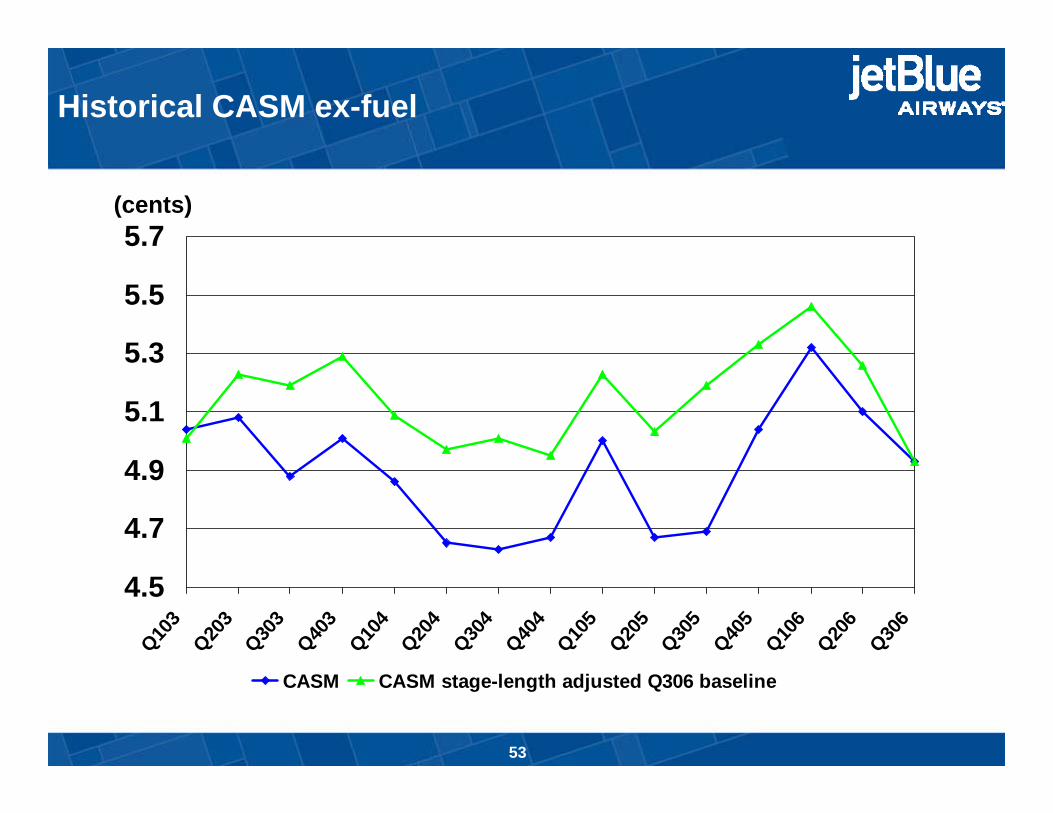

4.5

4.7

4.9

5.1

5.3

5.5

5.7

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

CASM CASM stage-length adjusted Q306 baseline

(cents)

Historical CASM ex-fuel

53

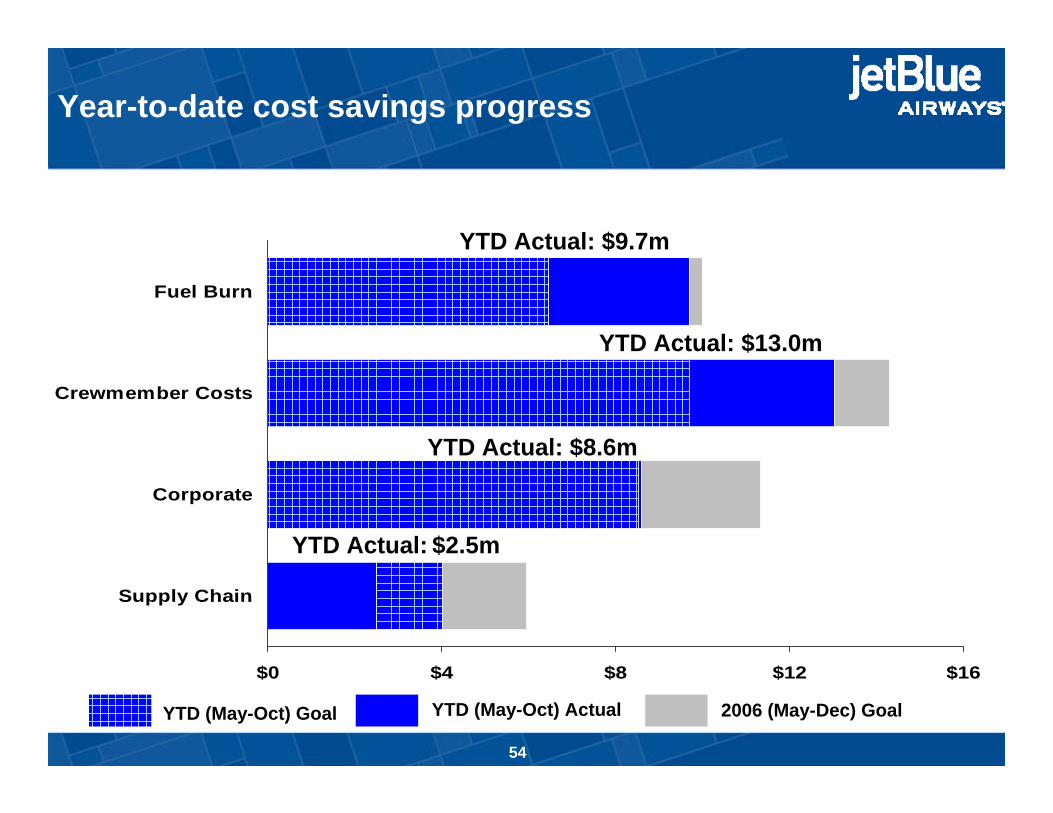

$0 $4 $8 $12 $16

Supply Chain

Corporate

Crewmember Costs

Fuel Burn

YTD Actual: $2.5m

YTD (May-Oct) Goal YTD (May-Oct) Actual 2006 (May-Dec) Goal

YTD Actual: $9.7m

YTD Actual: $13.0m

YTD Actual: $8.6m

Year-to-date cost savings progress

54

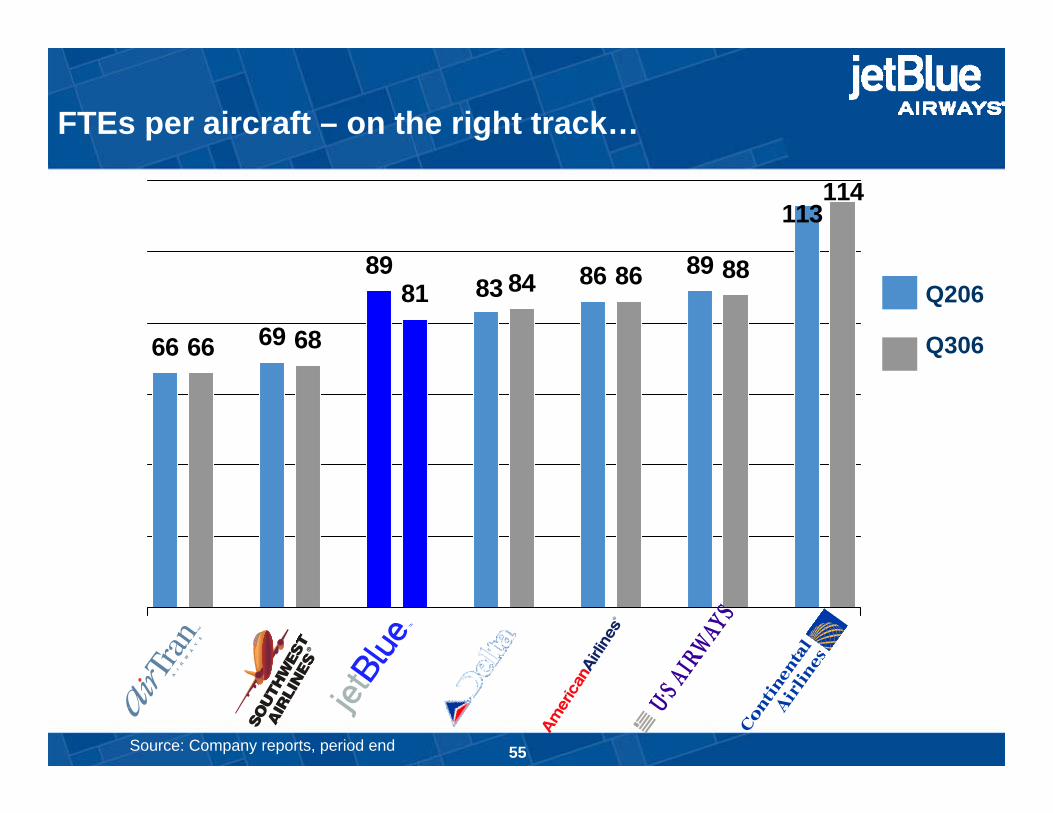

66 68

8981 84 86 88

114

66 69

83 86 89

113

FTEs per aircraft – on the right track…

Q206

Q306

Source: Company reports, period end 55

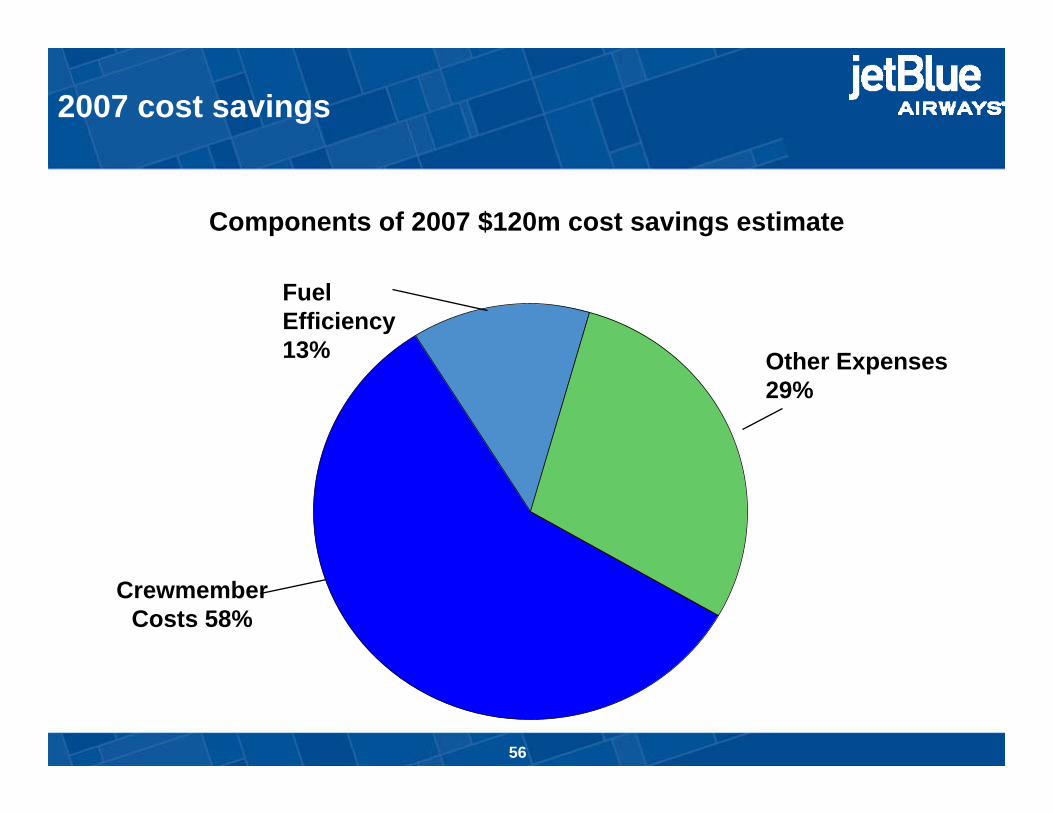

Crewmember Costs 58%

Fuel Efficiency 13% Other Expenses

29%

2007 cost savings

Components of 2007 $120m cost savings estimate

56

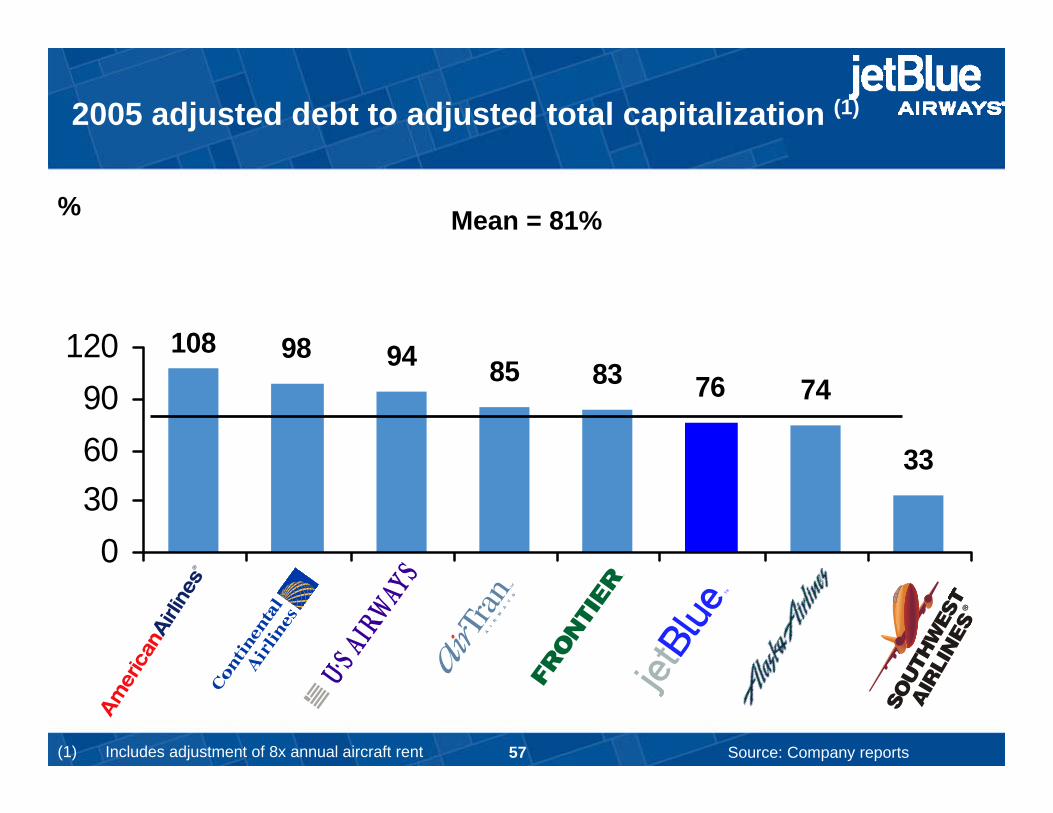

108 98 94 83 76 74

33

85

0306090

120

2005 adjusted debt to adjusted total capitalization (1)

(1) Includes adjustment of 8x annual aircraft rent

% Mean = 81%

Source: Company reports57

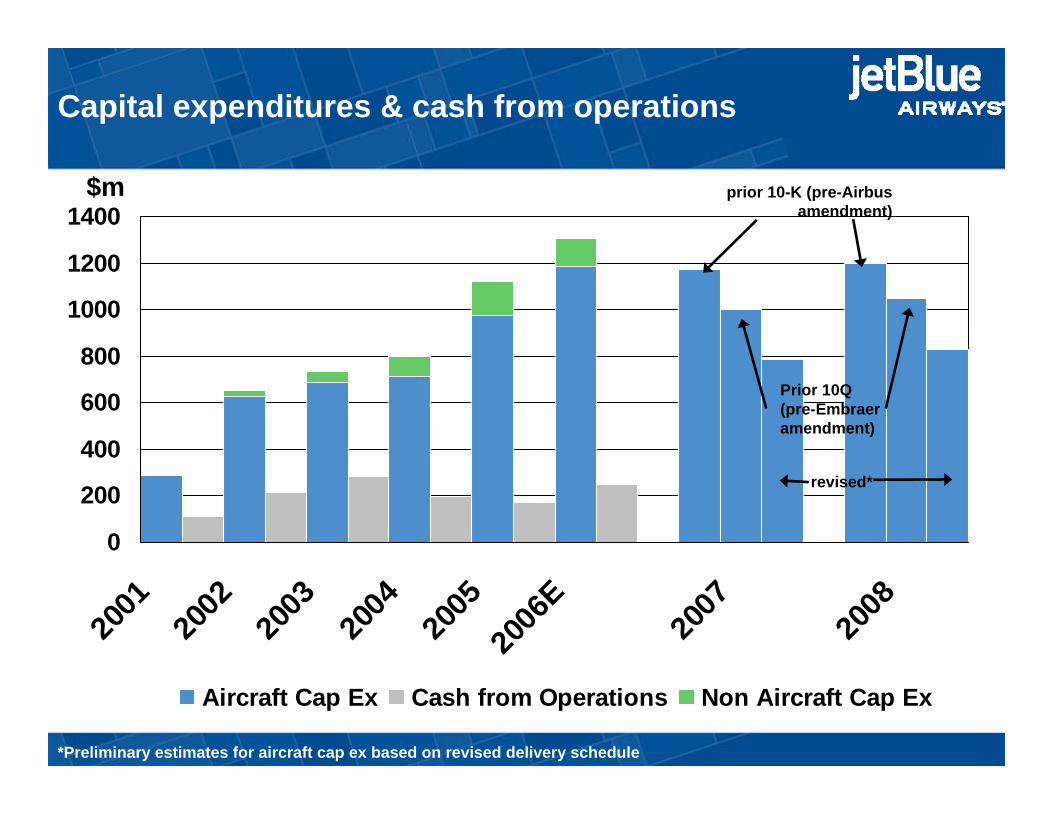

Capital expenditures & cash from operations

0

200

400

600

800

1000

1200

1400

2001

2002

2003

2004

2005

2006

E

2007

2008

Aircraft Cap Ex Cash from Operations Non Aircraft Cap Ex

$m prior 10-K (pre-Airbus amendment)

Prior 10Q (pre-Embraer amendment)

revised*

*Preliminary estimates for aircraft cap ex based on revised delivery schedule

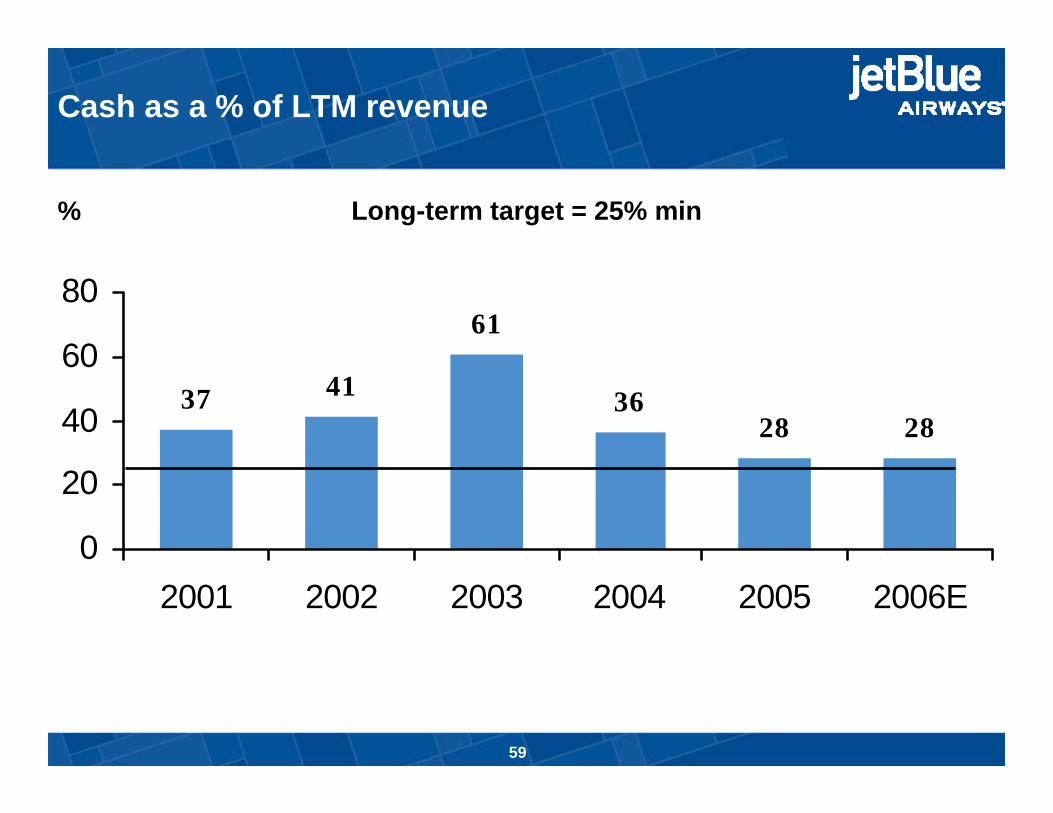

37 41

61

3628 28

0

20

40

60

80

2001 2002 2003 2004 2005 2006E

Cash as a % of LTM revenue

Long-term target = 25% min%

59

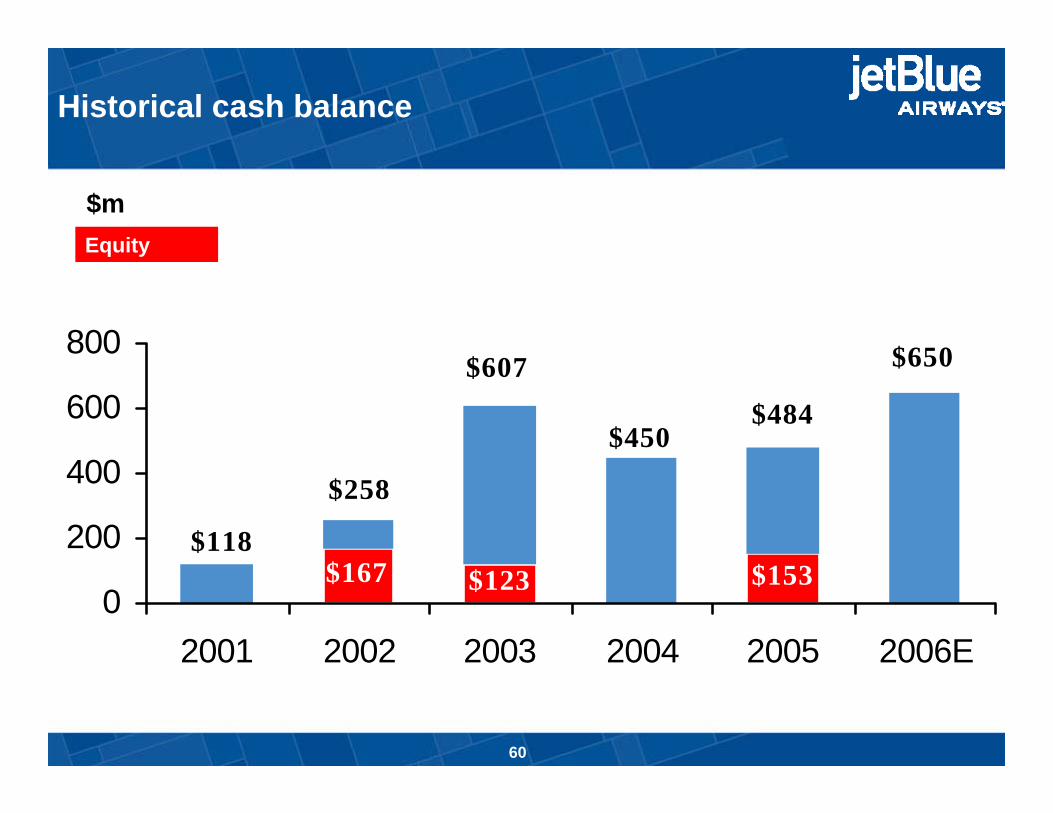

$167 $123 $153$118

$258

$607 $650

$484$450

0

200

400

600

800

2001 2002 2003 2004 2005 2006E

Historical cash balance

$mEquity

60

Dave Barger,

President & COO

61

62

RTP: On the Right Track | Scale the Culture

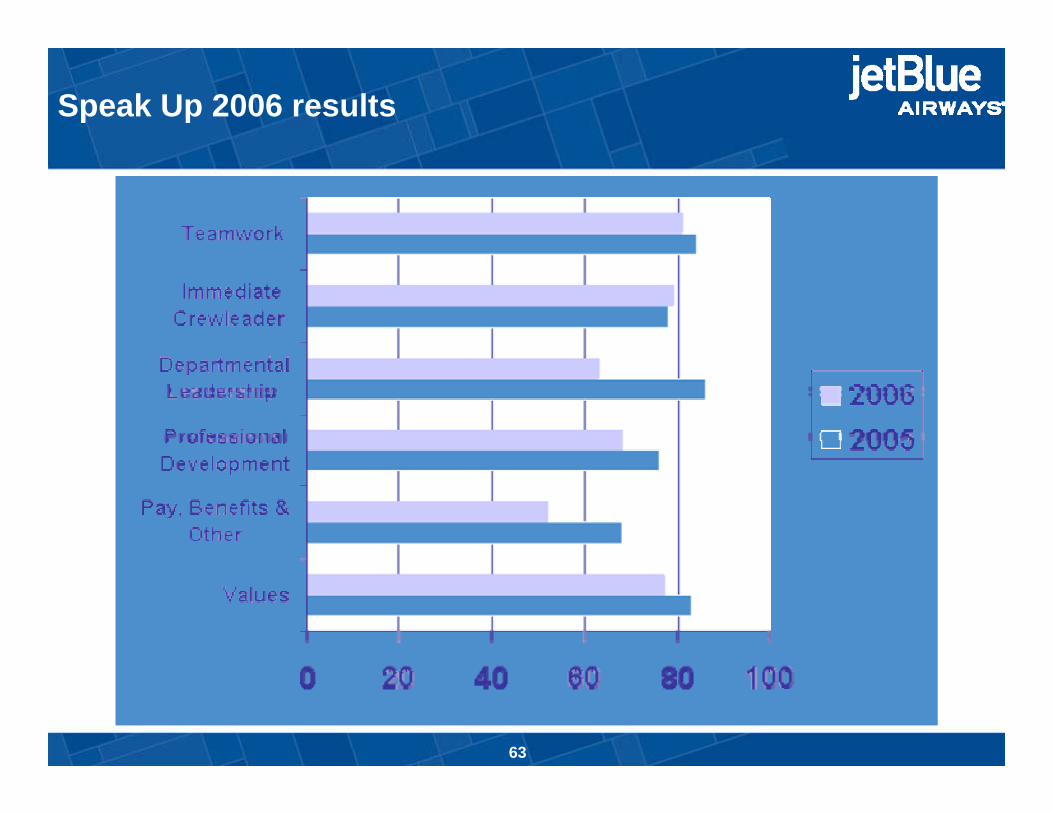

Speak Up 2006 results

63

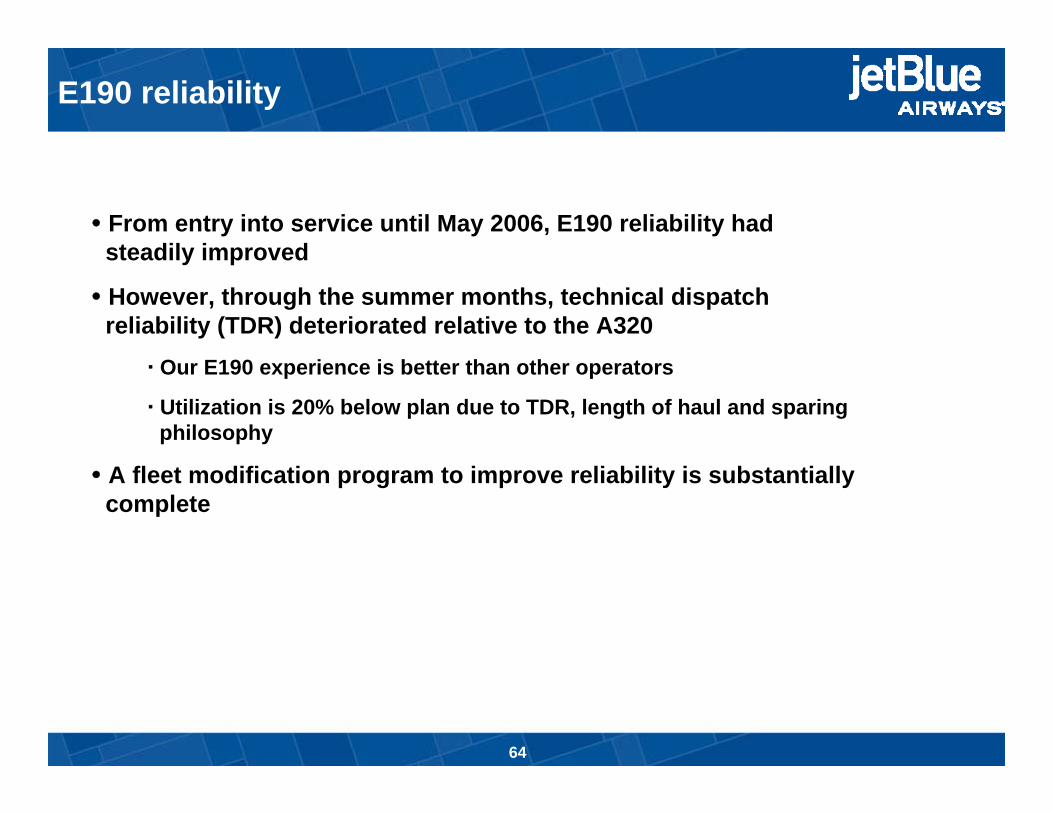

E190 reliability

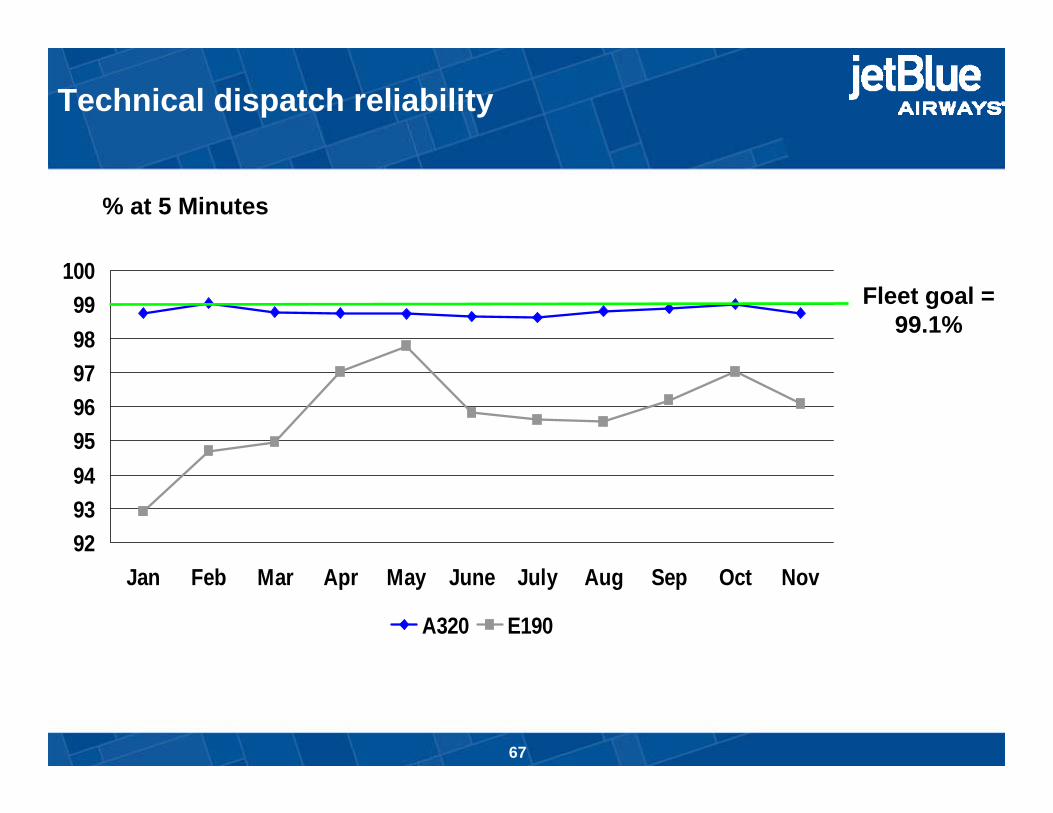

I. Committee ReportsFrom entry into service until May 2006, E190 reliability had steadily improved

However, through the summer months, technical dispatch reliability (TDR) deteriorated relative to the A320

Our E190 experience is better than other operators

Utilization is 20% below plan due to TDR, length of haul and sparing philosophy

A fleet modification program to improve reliability is substantially complete

64

95.0

96.0

97.0

98.0

99.0

100.0

Janua

ryFeb

ruary

March

April

May

June

July

August

Septem

ber

October

%

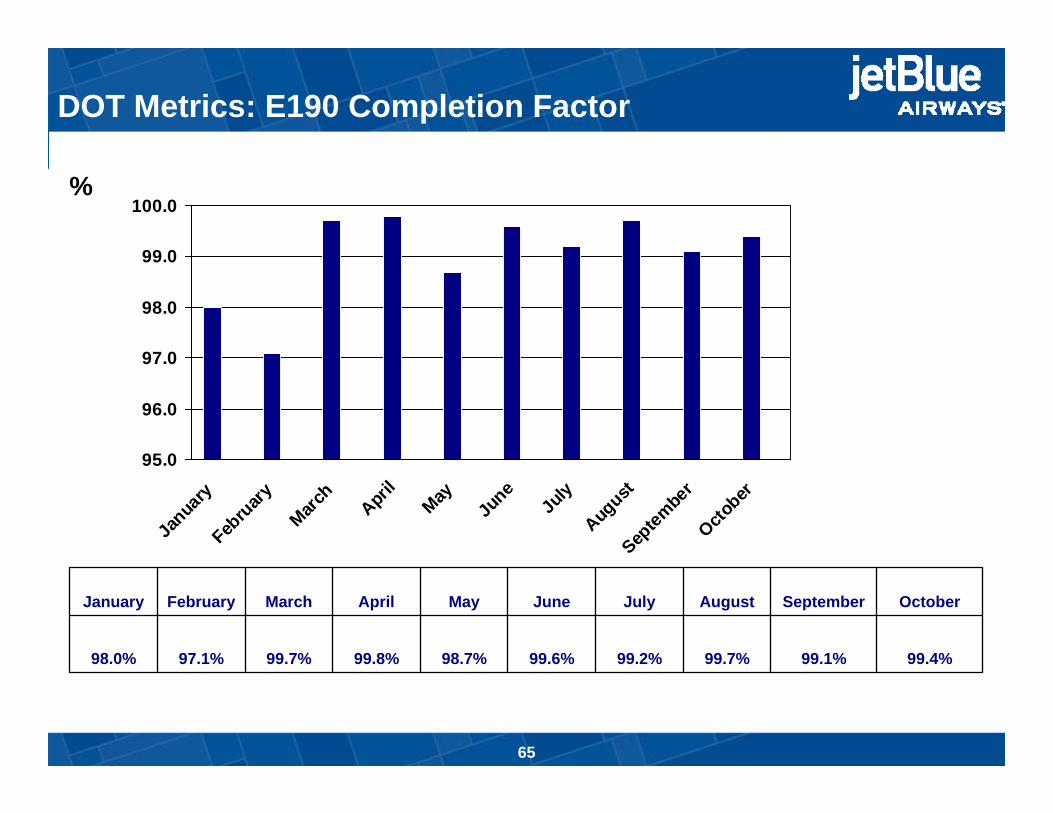

DOT Metrics: E190 Completion Factor

65

99.1%

September

99.4%99.7%99.2%99.6%98.7%99.8%99.7%97.1%98.0%

OctoberAugustJulyJuneMayAprilMarchFebruaryJanuary

40.0

50.0

60.0

70.0

80.0

90.0

Janua

ryFeb

ruary

March

April

May

June

July

August

Septem

ber

October

%

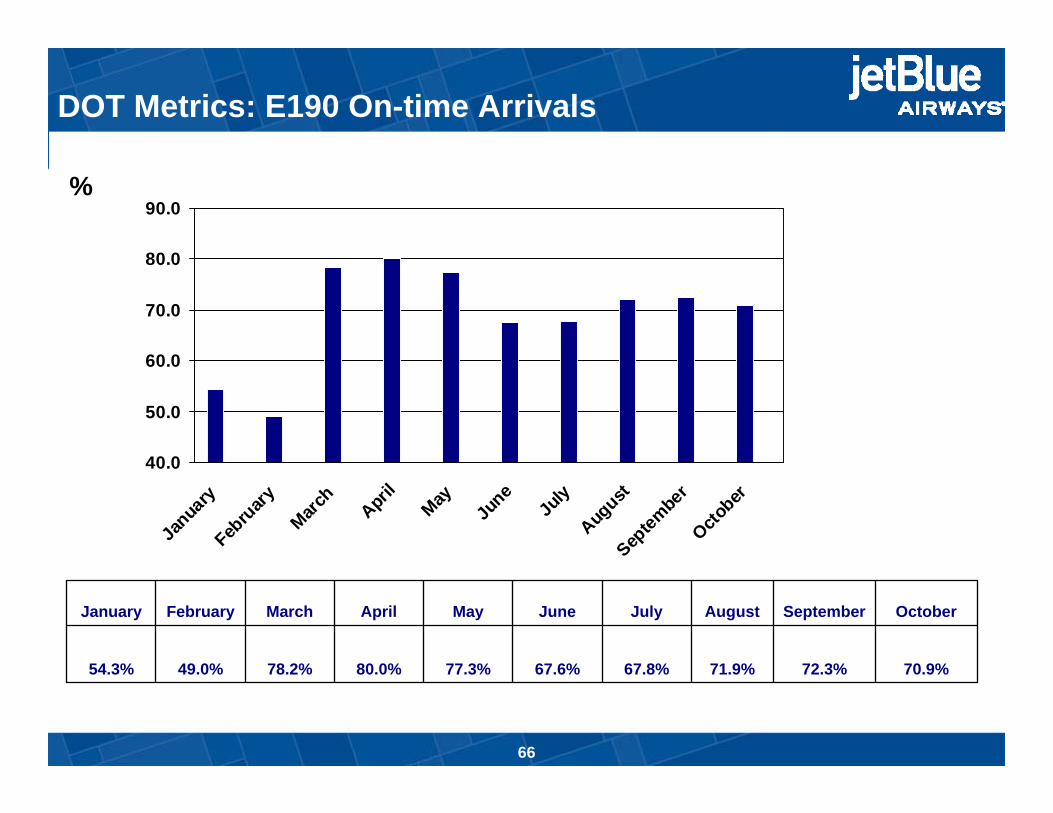

DOT Metrics: E190 On-time Arrivals

66

72.3%

September

70.9%71.9%67.8%67.6%77.3%80.0%78.2%49.0%54.3%

OctoberAugustJulyJuneMayAprilMarchFebruaryJanuary

Technical dispatch reliability

9293949596979899

100

Jan Feb Mar Apr May June July Aug Sep Oct Nov

A320 E190

Fleet goal = 99.1%

% at 5 Minutes

67

98

98.4

98.8

99.2

99.6

100

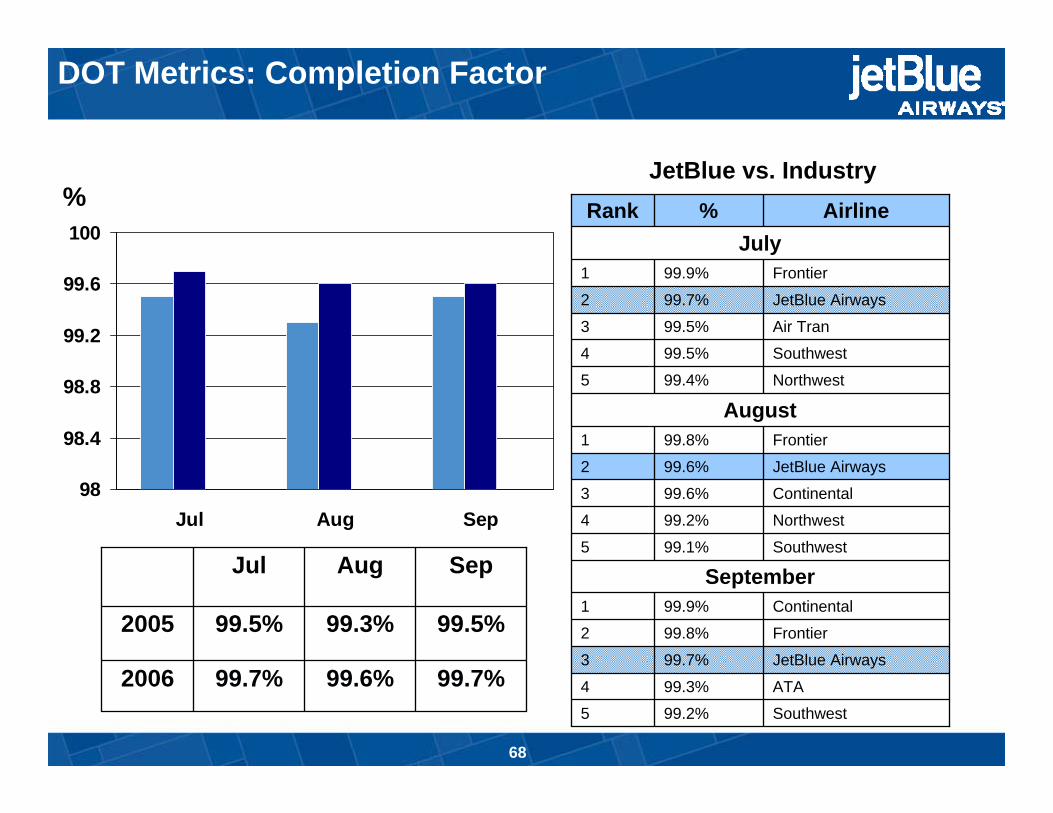

Jul Aug Sep

99.7%99.6%99.7%2006

99.5%99.3%99.5%2005

SepAugJul

%

Continental99.9%1

Frontier99.8%2

JetBlue Airways99.7%3

ATA99.3%4

Southwest99.1%5

September

Southwest99.2%5

Northwest99.2%4

Continental99.6%3

JetBlue Airways99.6%2

Frontier99.8%1

AugustNorthwest99.4%5

Southwest99.5%4

Air Tran99.5%3

JetBlue Airways99.7%2

Frontier99.9%1

JulyAirline%Rank

DOT Metrics: Completion Factor

JetBlue vs. Industry

68

0

20

40

60

80

Jul Aug Sep

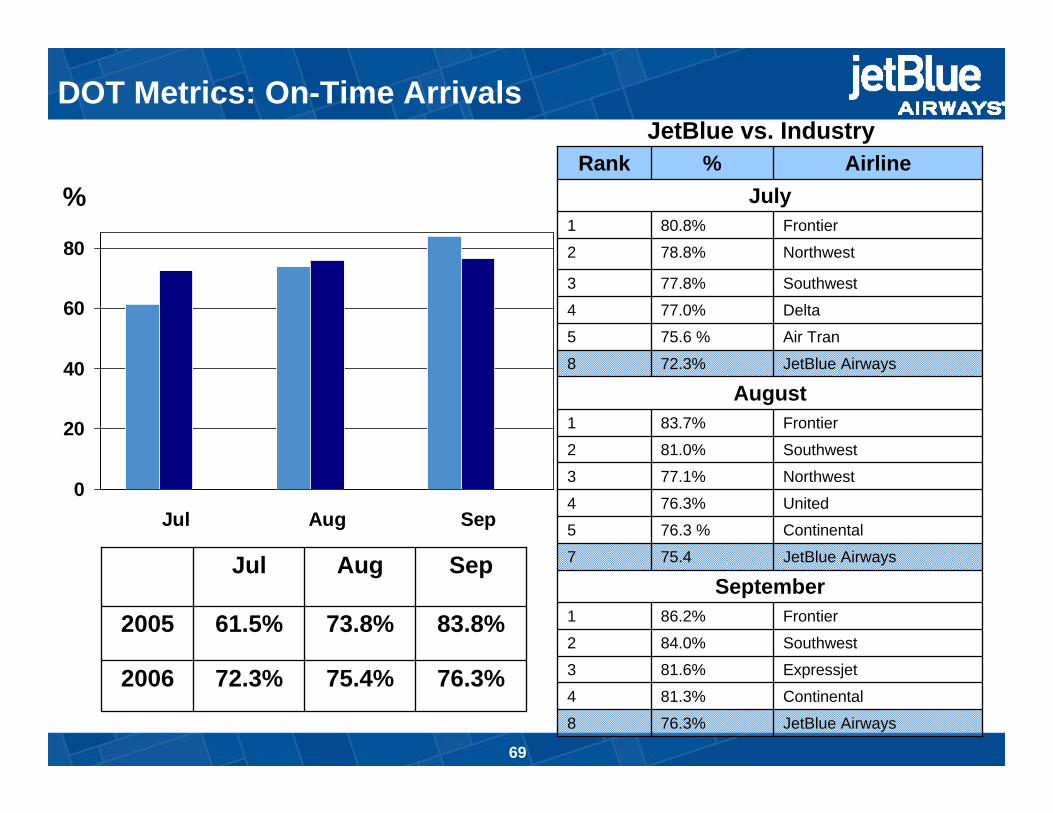

76.3%75.4%72.3%2006

83.8%73.8%61.5%2005

SepAugJul

%

Continental76.3 %5

JetBlue Airways75.47

Expressjet81.6%3

Southwest84.0%2

Frontier86.2%1

September

Continental81.3%4

Air Tran75.6 %5

JetBlue Airways76.3%8

United76.3%4

Northwest77.1%3

Southwest81.0%2

Frontier83.7%1

AugustJetBlue Airways72.3%8

Delta77.0%4

Southwest77.8%3

Northwest78.8%2

Frontier80.8%1

JulyAirline%Rank

DOT Metrics: On-Time ArrivalsJetBlue vs. Industry

69

2.40

3.20

4.00

4.80

5.60

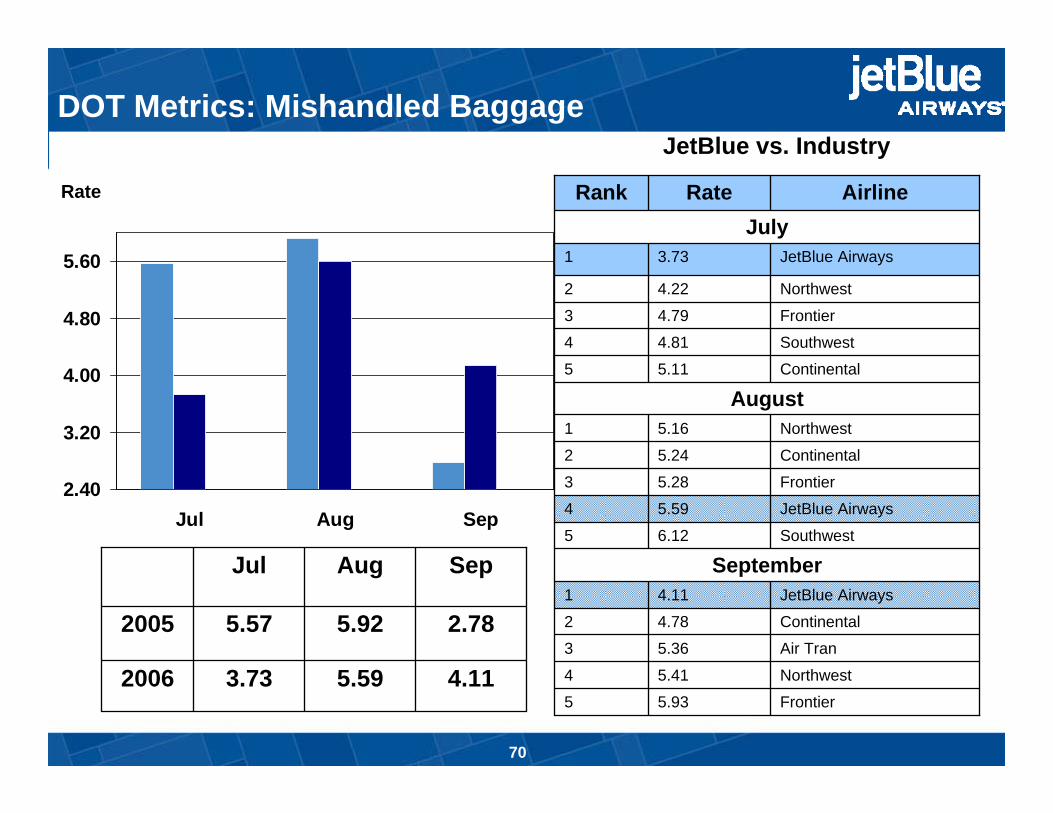

Jul Aug Sep

4.115.593.732006

2.785.925.572005

SepAugJul

Rate

Air Tran5.363

Continental4.782

JetBlue Airways4.111

SeptemberSouthwest6.125

Northwest5.414

Frontier5.935

JetBlue Airways5.594

Frontier5.283

Continental5.242

Northwest5.161

AugustContinental5.115

Southwest4.814

Frontier4.793

Northwest4.222

JetBlue Airways3.731

JulyAirlineRateRank

DOT Metrics: Mishandled BaggageJetBlue vs. Industry

70

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Jul Aug Sep

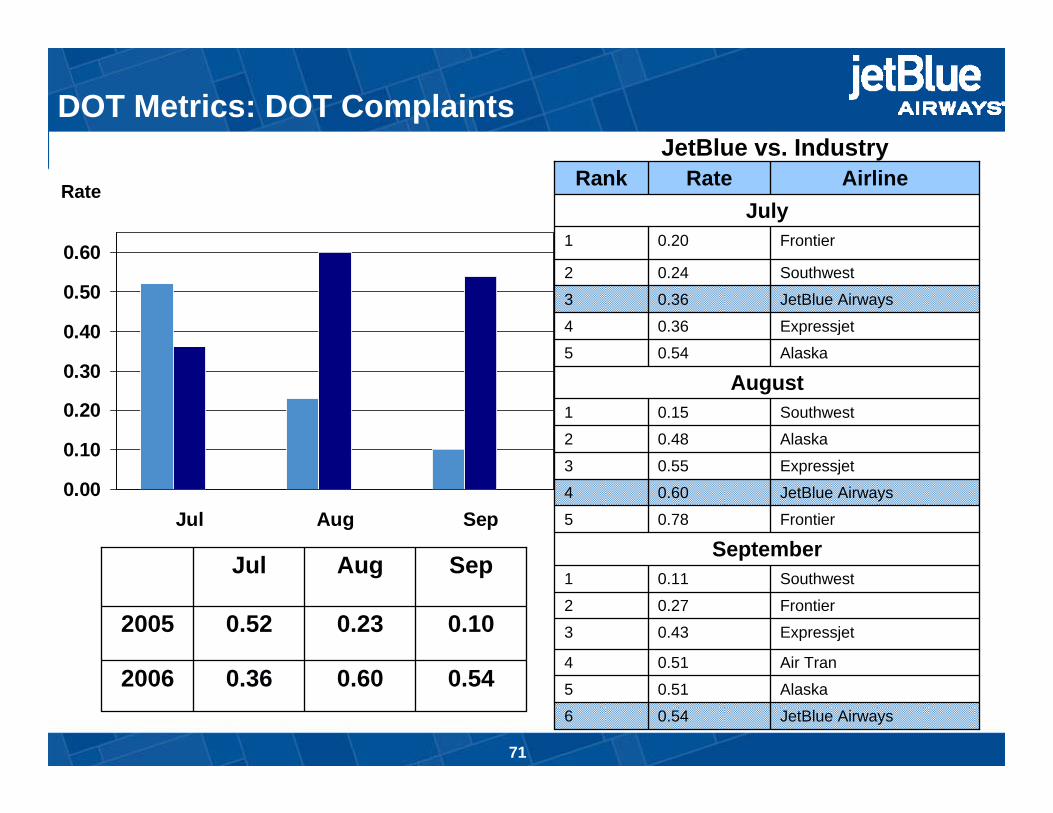

0.540.600.362006

0.100.230.522005

SepAugJul

Rate

Alaska0.515

Expressjet0.433

Frontier0.272

Southwest0.111

SeptemberFrontier0.785

Air Tran0.514

JetBlue Airways0.546

JetBlue Airways0.604

Expressjet0.553

Alaska0.482

Southwest0.151

AugustAlaska0.545

Expressjet0.364

JetBlue Airways0.363

Southwest0.242

Frontier0.201

JulyAirlineRateRank

DOT Metrics: DOT ComplaintsJetBlue vs. Industry

71

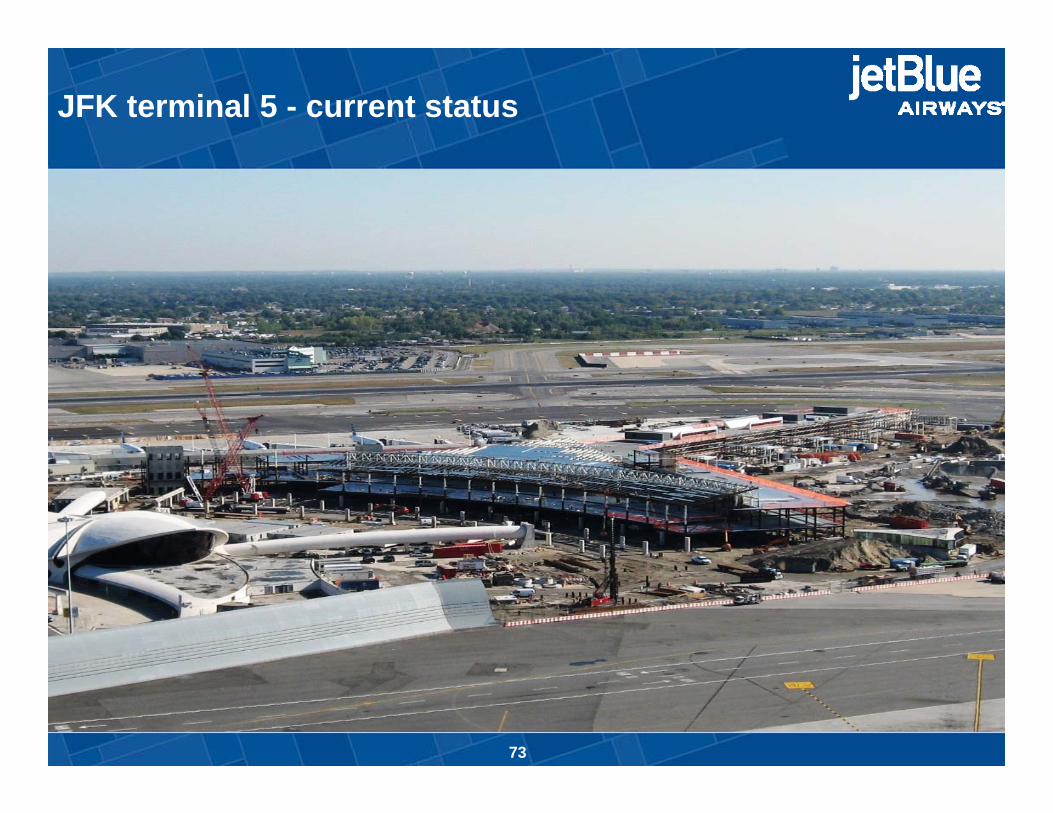

JFK terminal 5 - current status

I. Committee ReportsTerminal:

Piles and foundations are complete

- Structural steel is substantially complete

Building enclosure activities commenced

Parking Garage:

Contract awarded

T6 parking lot vacated, preliminary construction commenced

Schedule:Construction proceeding on scheduleSubstantial completion anticipated for 4Q08

72

JFK terminal 5 - current status

73

JetBlue Airways

Investor Day

Lunch